Embed Size (px)

Citation preview

Chapter 09 - Prospective Analysis

9-1

Prospective Analysis

REVIEW Prospective analysis is the final step in the financial statement analysis process. It includes forecasting of the balance sheet, income statement and statement of cash flows. Prospective analysis is central to security valuation. Both the free cash flow and residual income valuation models described in Chapter 1 require estimates of future financial statements. We provide a detailed example of the forecasting process to project the income statement, the balance sheet, and the statement of cash flows. We describe the relevance of forecasting for security valuation and provide an example utilizing forecasted financial statements to implement the residual income valuation model. We discuss the concept of value drivers and their reversion to long-run equilibrium levels. In the appendix, we provide a detailed example of short-term cash flow forecasting.

Chapter 09 - Prospective Analysis

9-2

OUTLINE • The Projection Process Projecting Financial Statements Application of Prospective Analysis in the Residual Income Valuation Model Trends in Value Drivers • Short-term Forecasting (Appendix)

Chapter 09 - Prospective Analysis

9-3

ANALYSIS OBJECTIVES • Describe the importance of prospective analysis. • Explain the process of projecting the income statement, the balance sheet and the

statement of cash flows. • Discuss and illustrate the Importance of Sensitivity Analysis. • Describe the implementation of the projection process in the valuation of equity

securities. • Discuss the concept of value drivers and their reversion to long-run equilibrium

levels.

Chapter 09 - Prospective Analysis

9-4

QUESTIONS 1. Prospective analysis is central to security valuation. All valuation models rely on

forecasts of earnings or cash flows that are, then, discounted back to the present to arrive at the estimated value of the security. Prospective analysis is also useful to examine the viability of companies’ strategic plans, that is, whether they will be able to generate sufficient cash flows from operations to finance expected growth or whether they will be required to seek external financing. In addition, prospective analysis is useful to examine whether announcing strategies will yield the benefits expected by management. Finally, prospective analysis can be used by creditors to assess companies’ ability to meet debt service requirements.

2. Prior to the forecasting process, financial statements can be recast to better portray

economic reality. Adjustments might include elimination of transitory items or reallocating them to past or future years, capitalizing (expensing) items that have been expensed (capitalized) by management, capitalizing operating leases and other forms of off-balance sheet financing, and so forth.

3. In addition to trend analysis, analysts frequently incorporate external (non-financial)

information into the prospective process. Some examples are the expected level of macroeconomic activity, the degree to which the competitive landscape is changing, any strategic initiatives that have been announced by management, and so forth.

4. The forecast horizon is the period for which specific estimates are made. It is usually 5-7

years. Forecasts beyond the forecast horizon are of dubious value since estimates are uncertain.

5. Since all valuation models are infinite horizon models, analysts frequently assume a

steady state into perpetuity after the forecast horizon. A common assumption is that the company will grow at the long-run rate of inflation, that is, remaining constant in real terms.

6. The projection process begins with an expected growth in sales. Gross profit and

operating expenses are, then, estimated as a percentage of forecasted sales using historical ratios and external information. Depreciation expense is usually estimated as a percentage of beginning gross depreciable assets under the assumption that depreciation policies will remain constant. Interest expense is usually estimated at an average borrowing rate applied to the beginning balance of interest bearing liabilities. Projections of expected interest rates are used for variable rate indebtedness and new borrowings. Finally, tax expense is estimated using the effective tax rate on pre-tax income.

7. In the first step, balance sheet items are projected using forecasted income sales

(COGS) and relevant turnover ratios. Long-term assets are projected using forecasted capital expenditures. Long-term liabilities are projected from current maturities of long-term debt disclosed in the debt footnote, and paid-in-capital is assumed to be constant in this stage. Retained earnings are projected adding (subtracting) projected profits (losses) and subtracting projected dividends. Once total liabilities and equities are forecasted, total assets is set equal to this amount and forecasted cash is computed as the plug figure.

Chapter 09 - Prospective Analysis

9-5

In the second step, long-term liabilities and equities are adjusted to yield the desired level of cash. The analyst must be careful to maintain the historical leverage ratio and adjust liabilities and equities proportionately.

8. The residual income model expresses stock price as the book value of stockholders’

equity plus the present value of expected residual income (RI). Residual income can be expressed in ratio form as,

RI = (ROEt – k) * BVt-1 Where ROE=NIt/BVt-1. This form highlights the fact that stock price is only impacted so long as ROE ≠ k. In equilibrium, competitive forces will tend to drive rates of return (ROE) to cost (k) so that abnormal profits are competed away. The estimation of stock price, then, amounts to the projection of the reversion of ROE to its long-run value for a particular company and industry. ROE is a value driver since it impacts our valuation of the stock price. Its components (asset turnover and profit margin) are also value drivers

9. We can make two observations regarding the reversion of ROE:

a. ROEs tend to revert to a long-run equilibrium. This reflects the forces of competition. Furthermore, the reversion rate for the least profitable firms is greater than that for the most profitable firms. And finally, reversion rates for the most extreme levels of ROE are greater than those for firms at more moderate levels of ROE.

b. The reversion is incomplete. That is, there remains a difference of about 12% between

the highest and lowest ROE firms even after ten years. This may be the result of two factors: differences in risk that are reflected in differences in their costs of capital (k); or, greater (lesser) degrees of conservatism in accounting policies.

The reversion of ROA and NPM are similar. While some reversion of TAT is evident, it is much less than that of the other value drivers.

10. Short-term cash forecasts are key to assessments of short-term liquidity. An asset is

called "liquid" because it will or can be converted into cash within the current period. The analysis of short-term cash forecasts will reveal whether an entity will be able to repay short-term loans as planned. This also means such analysis is extremely important for a potential short-term credit grantor. Short-term cash forecasts often are relatively realistic and accurate because of the shortness of the time span covered.

11. A cash forecast, to be most meaningful, must be for a relatively short-term period of

time. There are many unpredictable variables involved in the preparation of a reliable forecast for a highly liquid asset such as cash. Over a long period of time (that is, beyond the time span of one year), the difference in the degree of liquidity among items in the current assets group is usually insignificant. What is more important for long time spans are the projections of net income and other sources and uses of funds. The focus should be shifted to working capital (and other accrual measures), and away from cash flows, for longer forecast horizons of, say, thirty months—where the time required to convert current assets into cash is insignificant.

Chapter 09 - Prospective Analysis

9-6

12. Cash inflows and outflows are highly interrelated. These two flows are crucial to a

company’s “circulation system." A deficiency in any part of the system can affect the entire system. For example, a reduction or cessation of sales affects the vital conversion of finished goods into receivables or cash, which in turn leads to a drop in the cash reservoir. If the system is not strengthened by "transfusion" (such as additional investment by owners or creditors), production must be curtailed or discontinued. Lack of cash inflows also will reduce other expenses such as advertising, promotion, and marketing expenses, which will further adversely affect sales. This can yield a vicious cycle leading to business failure.

13. Most would agree with this assertion. Cash is the most liquid asset and when

management urgently needs to purchase assets or incur expenses, a cash exchange is the quickest and easiest means to execute a transaction. Moreover, unless management has a credit line established with a reliable outsider (such as a revolving account at a bank), lack of cash can mean a permanent loss of profitable opportunities.

14. Ratio analysis is a static measurement tool. Ratios measure relations among financial

statement items as of a given moment and time. In contrast, funds flow analysis is a dynamic measure covering a period of time. A dynamic model of funds flow analysis uses the present only as a starting point and utilizes the best available estimates of future plans and conditions to forecast the future availability and disposition of cash or working capital. Analyzing funds flow also encompasses the projected operations of a company. Since one of the fundamental assumptions of accounting is the going-concern concept, some assert that the dynamic model is more realistic and is superior to static representations. However, care should be taken in placing too much reliance on funds flow analysis as it is primarily based on estimates, and not on realized observations.

15. Except for transactions involving the raising of money from external sources (such as

through loans or additional investments) and the investments of money in long-term assets, almost all internally generated cash flows relate to and depend on sales. Accordingly, the usual first step in preparing a cash forecast is to estimate sales for the period under consideration. The reliability of any cash forecast depends on the accuracy of this forecast of sales. In arriving at the sales forecast, the analyst should consider: (1) past trends of sales volume, (2) market share, (3) industry and general economic conditions, (4) productive and financial capacity, and (5) competitive factors, among other variables.

Chapter 09 - Prospective Analysis

9-7

EXERCISES Exercise 9-1 (45 minutes) Projected Income Statement for Year 12

Quaker Oats Company Forecasted Income Statement

For Year Ended June 30, Year 12 Revenues [given] ................................................................. $6,000.0

Costs and expenses Cost of goods sold [a] ................................................... $3,186.0

Selling, general, and administrative [b] ....................... 2,439.4

Other expenses [c] ......................................................... 35.2

Interest, net [d] ............................................................... 91.4

Total costs and expenses ................................................... 5,752.0

Income from continuing operations ................................. 248.0

Income taxes [e] ................................................................... 105.9

Income before discontinued operations .......................... 142.1

(Loss) on disposal of discontinued operations [given] ... (2.0)

Net income ........................................................................... $ 140.1 Notes:

[a] Cost of sales is estimated to be at a level representing the average percentage of cost of sales to sales as prevailed in the four-year period ending June 30, Year 11, which is 53.1% (19,909.2 – 9,331.3)/19,909.2. Therefore, 6,000 x .531 = $3,186.

[b] Selling, general & administrative expenses in Year 12 are expected to increase by the same percentage as these expenses increased from Year 10 to Year 11, which is 15%. Therefore, $2,121.2 x 1.15 = $2,439.4.

[c] Other expenses are expected to be 8% higher in Year 12. Therefore, 32.6 x 1.08 = $35.2. [d] Interest expense (net of interest capitalized) and interest income will increase by 6% due

to increased financial needs. Therefore, $86.2 x 1.06 = $91.4 [e] The effective tax rate in Year 12 will equal that of Year 11, which is 42.7% ($175.7/$411.5).

Therefore, tax expense = $248 x .427 = $105.9.

Chapter 09 - Prospective Analysis

9-8

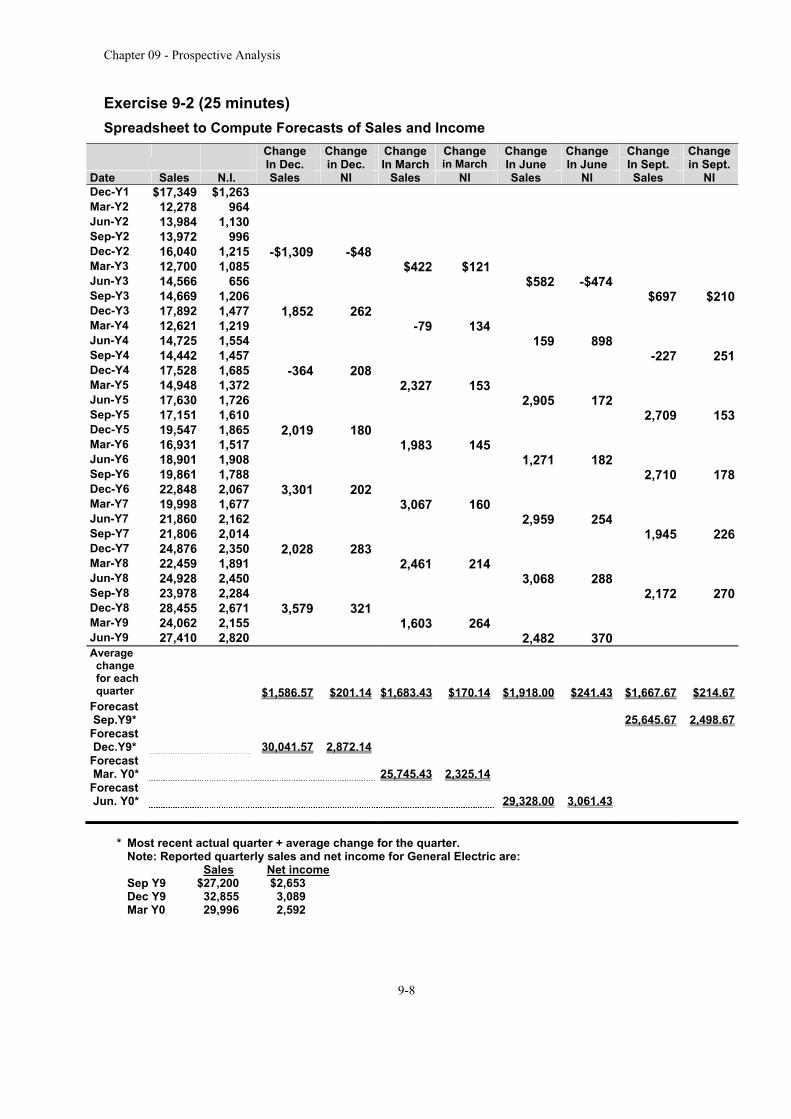

Exercise 9-2 (25 minutes) Spreadsheet to Compute Forecasts of Sales and Income

Change In Dec.

Change in Dec.

Change In March

Change in March

Change In June

Change In June

Change In Sept.

Change in Sept.

Date Sales N.I. Sales NI Sales NI Sales NI Sales NI Dec-Y1 $17,349 $1,263 Mar-Y2 12,278 964 Jun-Y2 13,984 1,130 Sep-Y2 13,972 996 Dec-Y2 16,040 1,215 -$1,309 -$48 Mar-Y3 12,700 1,085 $422 $121 Jun-Y3 14,566 656 $582 -$474 Sep-Y3 14,669 1,206 $697 $210 Dec-Y3 17,892 1,477 1,852 262 Mar-Y4 12,621 1,219 -79 134 Jun-Y4 14,725 1,554 159 898 Sep-Y4 14,442 1,457 -227 251 Dec-Y4 17,528 1,685 -364 208 Mar-Y5 14,948 1,372 2,327 153 Jun-Y5 17,630 1,726 2,905 172 Sep-Y5 17,151 1,610 2,709 153 Dec-Y5 19,547 1,865 2,019 180 Mar-Y6 16,931 1,517 1,983 145 Jun-Y6 18,901 1,908 1,271 182 Sep-Y6 19,861 1,788 2,710 178 Dec-Y6 22,848 2,067 3,301 202 Mar-Y7 19,998 1,677 3,067 160 Jun-Y7 21,860 2,162 2,959 254 Sep-Y7 21,806 2,014 1,945 226 Dec-Y7 24,876 2,350 2,028 283 Mar-Y8 22,459 1,891 2,461 214 Jun-Y8 24,928 2,450 3,068 288 Sep-Y8 23,978 2,284 2,172 270 Dec-Y8 28,455 2,671 3,579 321 Mar-Y9 24,062 2,155 1,603 264 Jun-Y9 27,410 2,820 2,482 370 Average change for each quarter

$1,586.57

$201.14

$1,683.43

$170.14

$1,918.00

$241.43

$1,667.67

$214.67 Forecast Sep.Y9*

25,645.67

2,498.67

Forecast Dec.Y9*

30,041.57

2,872.14

Forecast Mar. Y0*

25,745.43

2,325.14

Forecast Jun. Y0*

29,328.00

3,061.43

* Most recent actual quarter + average change for the quarter. Note: Reported quarterly sales and net income for General Electric are:

Sales Net income Sep Y9 $27,200 $2,653 Dec Y9 32,855 3,089 Mar Y0 29,996 2,592

Chapter 09 - Prospective Analysis

9-9

Exercise 9-3 (40 minutes) a. To illustrate how predictions of market share and total market sales can be used

in the forecasting process, consider the following example. If an analyst, for instance, predicts that (i) Cough.com will maintain its 0.08% share of the market for children's cough medicine and (ii) total Industry sales of children's cough medicine for year 2006 is $3.2 billion, then a reasonable estimate of Cough.com's year 2006 sales is $2.56 million. This is computed as 0.08% market share multiplied by the expected $3.2 billion of industry sales.

b. All relevant data should be sought out, subject to cost-benefit considerations, in

the prediction of sales. The importance of sales to predictions of financial performance and financial condition cannot be overemphasized. Accordingly, companies invest considerable research and effort in predicting sales. Regarding what types of data to seek and how to obtain them, let’s consider a retailer. To project the sales of a retailer, an analyst might consider visiting outlets that sell the retailers’ products and observe customer-buying patterns versus the patterns observed for key competing products. This activity can be done using anecdotal observation or using formal statistical sampling depending upon the analysts' perceived need for accuracy. Moreover, the analyst can seek information from insiders via interview or interpretation of formal or informal disclosures made by the company. The analyst can also review company strategies and industry trends. In sum, good predictions involve more than sophisticated models—they demand that the analyst take the perspective of a customer constrained by the economic environment predicted to exist.

c. Relying on predicted year 2006 total industry sales of $3.2 billion, the sales of

Cough.com are predicted to be as follows

2006 Market share is 5% greater 2006 Market share is 5% worse [105% x .08%] x $3.2 billion [95% x .08%] x $3.2 billion

= $2.688 million = $2.432 million d. What-If industry sales are 10% higher:

[105% x .08%] x [110% x $3.2 billion] [95% x .08%] x [110% x $3.2 billion] = $2.9568 million = $2.6752 million What-If industry sales are 10% lower:

[105% x .08%] x [90% x $3.2 billion] [95% x .08%] x [90% x $3.2 billion] = $2.4192 million = $2.1888 million

Chapter 09 - Prospective Analysis

9-10

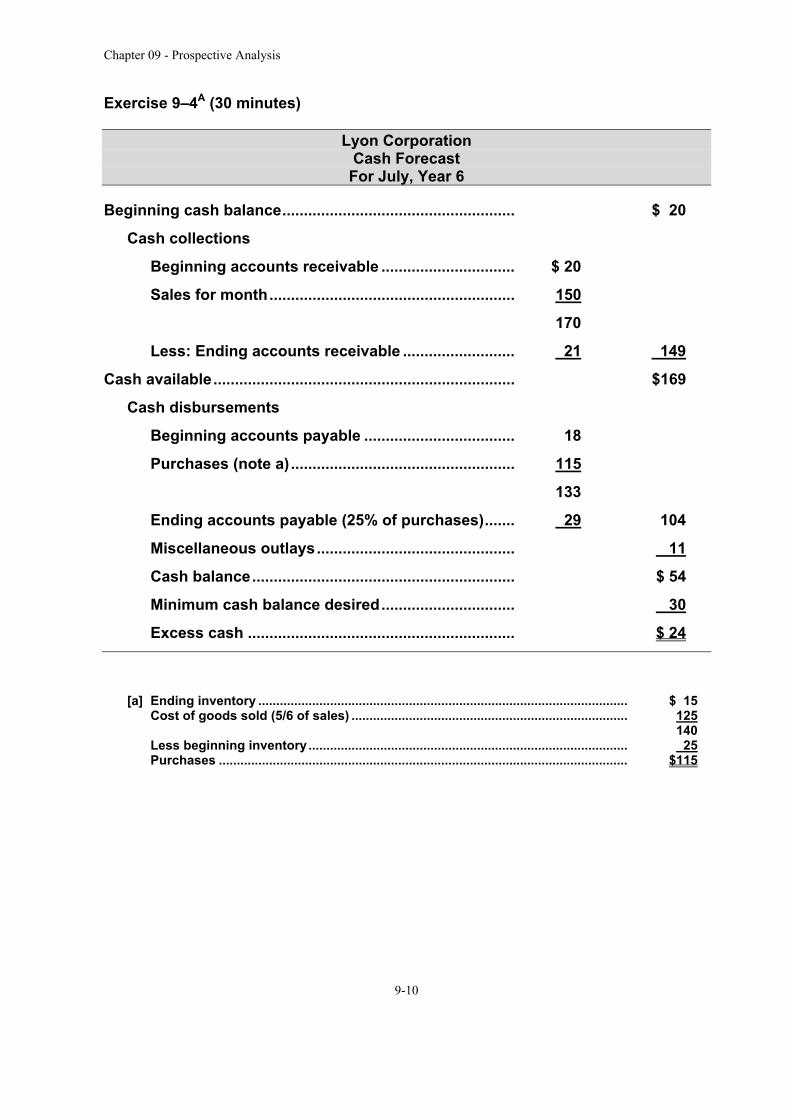

Exercise 9–4A (30 minutes)

Lyon Corporation Cash Forecast For July, Year 6

Beginning cash balance ...................................................... $ 20

Cash collections

Beginning accounts receivable ............................... $ 20

Sales for month ......................................................... 150

170

Less: Ending accounts receivable .......................... 21 149

Cash available ...................................................................... $169

Cash disbursements

Beginning accounts payable ................................... 18

Purchases (note a) .................................................... 115

133

Ending accounts payable (25% of purchases) ....... 29 104

Miscellaneous outlays .............................................. 11

Cash balance ............................................................. $ 54

Minimum cash balance desired ............................... 30

Excess cash .............................................................. $ 24

[a] Ending inventory ....................................................................................................... $ 15 Cost of goods sold (5/6 of sales) ............................................................................. 125 140 Less beginning inventory ......................................................................................... 25 Purchases .................................................................................................................. $115

Chapter 09 - Prospective Analysis

9-11

PROBLEMS Problem 9-1 (90 minutes) a. Coca-Cola

INCOME STATEMENT Year 3

Estimate Year 2 Year 1 Net sales 20,297 20,092 19,889

Cost of goods 6,106 6,044 6,204

Gross profit 14,191 14,048 13,685

Selling general & administrative expense 7,972 7,893 9,221

Depreciation & amortization expense 863 803 773

Interest expense -66 -308 292

Income before tax 5,422 5,660 3,399

Income tax expense 1,620 1,691 1,222

Net income 3,802 3,969 2,177

Outstanding shares 3,491 3,491 3,481 RATIOS

Sales growth 1.02% 1.02% Gross Profit Margin 69.92% 69.92% Selling General & Administrative Exp / Sales 39.28% 39.28% Depreciation (depn exp / pr yr PPE gross) 12.14% 12.14% INT (int / pr yr LTD) -5.45% -5.45% Tax (Inc Tax / Pre-tax inc) 29.88% 29.88%

Chapter 09 - Prospective Analysis

9-12

Problem 9-1 — continued

BALANCE SHEET Year 3

Estimate Year 2 Year 1 Cash 587 1,934 1,892 Receivables 1,901 1,882 1,757 Inventories 1,066 1,055 1,066 Other 2,300 2,300 1,905 Total current assets 5,854 7,171 6,620 Property, plant & equipment 8,305 7,105 6,614 Accumulated depreciation 3,515 2,652 2,446 Net property & equipment 4,791 4,453 4,168 Other assets 10,793 10,793 10,046 Total assets 21,438 22,417 20,834 Accounts payable & accrued liabilities 3,717 3,679 3,905 Short-term debt & cmltd 3,899 3,899 4,816 Income taxes 815 851 600 Total current liab 8,431 8,429 9,321 Deferred income, taxes & other 1,403 1,403 1,362 Long term debt 1,219 1,219 835 Total liabilities 11,053 2,622 2,197 Common stock 873 873 870 Capital surplus 3,520 3,520 3,196 Retained earnings 19,674 20,655 18,543 Treasury stock 13,682 13,682 13,293 Shareholder equity 10,385 11,366 9,316 Total liabilities & net worth 21,438 22,417 20,834 RATIOS AR turn 10.68 10.68 11.32 INV turn 5.73 5.73 5.82 AP turn 1.64 1.64 1.59 Tax Pay (Tax pay / tax exp) 50.33% 50.33% 49.10% FLEV 2.06 1.97 2.24 Div/sh $1.37 $1.37 $1.21 CAPEX 1,200 1188 1165 CAPEX/Sales 5.91% 5.91% 5.86%

Chapter 09 - Prospective Analysis

9-13

Problem 9-1 — continued

Statement of Cash Flows Year 3

Estimate

Net income 3,802

Depreciation 863

Accounts receivable -19

Inventories -11

Accounts payable 38

Income taxes -36

Net cash flow from operations 4,636

CAPEX -1,200 Net cash flow from investing activities -1,200 Long term debt 0 Additional paid in capital 0 Dividends -4,783 Net cash flow from financing activities -4,783 _____ Net change in cash -1,347 Beginning cash 1,934 Ending cash 587

b. Based on our initial projection of Coca-Cola’s balance sheet, it appears that the

company will require approximately $1.5 billion of external financing in Year 3. This amount will yield a cash balance of approximately $2 billion, consistent with prior years.

Chapter 09 - Prospective Analysis

9-14

Problem 9-2 (95 minutes) a. Best Buy

Year 3

Estimate Year 2 Year 1 Income statement Net sales 18,800 15,326 12,494

Cost of goods 15,048 12,267 10,101

Gross profit 3,752 3,059 2,393

Selling general & administrative expense 2,761 2,251 1,728

Depreciation & amortization expense 304 167 103

Income before tax 688 641 562

Income tax expense 263 245 215

Net income 425 396 347

Outstanding shares 208 208 200 RATIOS Sales growth 22.67% 22.67% Gross Profit Margin 19.96% 19.96% Selling General & Administrative Exp / Sales 14.69% 14.69% DEPRECIATION (depn exp / pr yr PPE gross) 15.28% 15.28% Tax (Inc Tax / Pre-tax inc) 38.22% 38.22%

Chapter 09 - Prospective Analysis

9-15

Problem 9-2 — continued

BALANCE SHEET Year 3

Estimate Year 2 Year 1 Cash 196 746 751 Receivables 384 313 262 Inventories 2,168 1,767 1,184 Other 102 102 41 Total current assets 2,850 2,928 2,238 Property, plant & equipment 3,249 1,987 1,093 Accumulated depreciation 847 543 395 Net property & equipment 2,403 1,444 698 Other assets 466 466 59 Total assets 5,719 4,838 2,995 Accounts payable & accrued liabilities 3,034 2,473 1,704 Short-term debt & cmltd 114 114 16 Income taxes 136 127 65 Total current liab 3,284 2,714 1,785 Long term liabilities 122 122 100 Long term debt 67 181 15 Total long-term liabilities 189 303 115 Common stock 20 20 20 Capital surplus 576 576 247 Retained earnings 1,650 1,225 828 Shareholder equity 2,246 1,821 1,095 Total liabilities & net worth 5,719 4,838 2,995 RATIOS AR turn 48.96 48.96 47.69 INV turn 6.94 6.94 8.53 AP turn 4.96 4.96 5.93 Tax Pay (Tax pay / tax exp) 51.84% 51.84% 30.23% FLEV 2.55 2.66 2.74 Div/sh $0.00 $0.00 $0.00 CAPEX 1,262 1029 416 CAPEX/Sales 6.71% 6.71% 3.33%

Chapter 09 - Prospective Analysis

9-16

Problem 9-2 — continued

Statement of Cash Flows Year 3

Estimate Net income 425 Depreciation 304 Accounts receivable -71 Inventories -401 Accounts payable 561 Income taxes 9 Net cash flow from operations 827 CAPEX -1,262 Net cash flow from investing activities -1,262 Long term debt -114 Additional paid in capital 0 Dividends 0 Net cash flow from financing activities -114 ____ Net change in cash -550 Beginning cash 746 Ending cash 196

b. Based on our projection, it appears that Best Buy will require about $550 Million

of external financing to yield a cash balance of approximately $750 million. Analysts must allocate this external financing between debt and equity so as to preserve the financial leverage level presently used by Best Buy.

Chapter 09 - Prospective Analysis

9-17

Problem 9-3 (90 minutes) a. Merck

INCOME STATEMENT Year 3

Estimate Year 2 Year 1

Net sales 56,435 47,716 40,343 Cost of goods 34,272 28,977 22,444 Gross profit 22,164 18,739 17,900 Selling general & administrative expense 7,725 6,531 6,469 Depreciation & amortization expense 1,661 1,464 1,277 Interest expense 237 342 329 Income before tax 12,541 10,403 9,824 Income tax expense 3,762 3,121 3,002 Net income 8,779 7,282 6,822 Outstanding shares 2,976 2,976 2,968 RATIOS

Sales growth 18.27% 18.27% Gross Profit Margin 39.27% 39.27% Selling General & Administrative Exp / Sales 13.69% 13.69% DEPRECIATION (depn exp / pr yr PPE gross) 8.76% 8.76% INT (int / pr yr LTD) 4.94% 4.94% Tax (Inc Tax / Pre-tax inc) 30.00% 30.00%

Chapter 09 - Prospective Analysis

9-18

Problem 9-3 — continued

BALANCE SHEET Year 3

Estimate Year 2 Year 1 Cash 5,254 3,287 4,255 Receivables 6,168 5,215 5,262 Inventories 4,233 3,579 3,022 Other 880 880 1,059 Total current assets 16,536 12,961 13,598 Property, plant & equipment 24,056 18,956 16,707 Accumulated depreciation 7,514 5,853 5,225 Net property & equipment 16,543 13,103 11,482 Other assets 17,942 17,942 15,075 Total assets 51,020 44,007 40,155 Accounts payable & accrued liabilities 6,983 5,904 5,391 Short-term debt & cmltd 4,067 4,067 3,319 Income taxes 1,897 1,573 1,244 Total current liab 12,947 11,544 9,954 Deferred income, taxes and other 11,614 11,614 11,768 Long term debt 4,787 4,799 3,601 Total liabilities 29,347 27,957 25,323 Common stock 30 30 30 Capital surplus 6,907 6,907 6,266 Retained earnings 37,123 31,500 27,395 Treasury stock 22,387 22,387 18,858 Shareholder equity 21,673 16,050 14,832 Total liabilities & net worth 51,020 44,007 40,155 RATIOS AR turn 9.15 9.15 7.67 INV turn 8.10 8.10 7.43 AP turn 4.91 4.91 4.16 Tax Pay (Tax pay / tax exp) 50.41% 50.41% 41.45% FLEV 2.35 2.74 2.71 Div/sh $1.06 $1.06 $0.98 CAPEX 5,100 4312 3641 CAPEX/Sales 9.04% 9.04% 9.03%

Chapter 09 - Prospective Analysis

9-19

Problem 9-3 — continued

Statement of Cash Flows Year 3

Estimate

Net income $ 8,779 Depreciation 1,661 Accounts receivable -953 Inventories -654 Accounts payable 1,079 Income taxes 323 Net cash flow from operations 10,235 CAPEX -5,100 Net cash flow from investing activities -5,100 Long term debt -12 Additional paid in capital 0 Dividends -3,156 Net cash flow from financing activities -3,168 _____ Net change in cash 1,967 Beginning cash 3,287 Ending cash 5,254

b. Based on our initial projections, it appears that Merck will have excess cash of

approximately $2 billion in year 3. This excess cash should be used to reduce both debt and equity so as to maintain historical financial leverage.

Chapter 09 - Prospective Analysis

9-20

Problem 9-4 (90 minutes)

Historical

figures Forecast Horizon

Terminal Year

Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 20x8 20x8 Sales growth 8.50% 10.65% 10.65% 10.65% 10.65% 10.65% 10.65% 3.50% Net profit Margin (Net income/Sales) 6.71% 8.22% 8.22% 8.22% 8.22% 8.22% 8.22% 8.22% NWC turn (Sales/avg NWC) 8.98 9.33 9.33 9.33 9.33 9.33 9.33 9.33 FA turn (Sales/avg FA) 1.67 1.64 1.64 1.64 1.64 1.64 1.64 1.64 Total operating assets/Total equity 1.96 2.01 2.01 2.01 2.01 2.01 2.01 2.01 Cost of equity 12.5% ($ Thousands) Sales 25,423 28,131 31,127 34,443 38,112 42,171 46,663 48,297 Net income ($ Mil) 1,706 2,312 2,558 2,831 3,132 3,466 3,835 3,969 Net working capital 2,832 3,015 3,336 3,692 4,085 4,520 5,001 5,176 Fixed assets 15,232 17,136 18,961 20,981 23,216 25,689 28,425 29,420 Total Operating assets 18,064 20,151 22,297 24,673 27,301 30,209 33,426 34,596 L-T Liabilities 8,832 10,132 11,211 12,405 13,727 15,189 16,807 17,395 Total Stockholder's Equity ($ Mil) 9,232 10,019 11,086 12,267 13,574 15,020 16,619 17,201 Residual Income Computation Net Income 2,558 2,831 3,132 3,466 3,835 3,969 Beginning Equity 10,019 11,086 12,267 13,574 15,020 16,619 Required Equity Return 12.5% 12.5% 12.5% 12.5% 12.5% 12.5% Expected Earnings 1,252 1,386 1,533 1,697 1,877 2,077 Residual Income 1,306 1,445 1,599 1,769 1,958 1,892 Discount factor 0.89 0.79 0.70 0.62 0.55 Present value of residual income 1,161 1,142 1,123 1,105 1,086 Cum PV residual income 1,161 2,303 3,425 4,530 5,616 Terminal value of abnormal earnings 11,665 Beg book value of equity 10,019 Value of equity - Abnormal Earnings 27,301 Common shares outstanding (mil) 1,737 per share $15.72

Chapter 09 - Prospective Analysis

9-21

Problem 9-5 (90 minutes) a. Telnet Corporation Pro Forma Income Statement ($000s) Six Months Ended June 30, Year 2

Sales revenue ($250 x 6 mos.) .................................................................... $1,500 Cost of goods sold (note [a]) ...................................................................... 1,199 Gross margin ............................................................................................... 301 Selling and administrative expenses ($47.5 x 6 mos.) ............................. 285 Expected pre-tax income ............................................................................ 16 Estimated income taxes (at 50%) ............................................................... 8 Expected net income ................................................................................... $ 8

Note [a]: We use T-accounts to compute cost of goods sold ($ thousands)

Raw Material Inventory

Beginning (given) 0 Material purchases ($125 x 6 mos.) 750

715 To W.I.P. inventory [a] (plug)

Ending (given) 35

Work in Process Inventory Beginning (given) 0 From raw materials inventory [a] 715 Labor ($30.5 x 6 mos.) 183 Variable overhead ($22.5 x 6 mos.) 135 Rent ($10 x 6 mos.) 60 Depreciation ($35 x 6 mos.) 210 Patent amortization ($.5 x 6 mos.) 3

7 Prepaid expenses (given) 1,299 To F.G. inventory [b] (plug)

Ending (given) 0

Finished Goods Inventory Beginning (given) 0 From W.I.P. inventory [b] 1,299

1,199 Cost of goods sold (plug)

Ending (given) 100

Chapter 09 - Prospective Analysis

9-22

Problem 9-5 — continued b. Telnet Corporation Pro forma Balance Sheet ($000s) June 30, Year 2 ASSETS Cash ............................................................................. $ 40 (minimum cash) Accounts receivable ................................................... 375 (45 days' sales)* Inventories ($35 + $100) ............................................. 135 (given) Prepaid expenses ........................................................ 7 (given) Total current assets .................................................. 557 (subtotal) Equipment ................................................................... 1,200 (given) Less accumulated depreciation ................................. 210 ($35 x 6 mos.) Equipment, net .......................................................... 990 (subtotal) Patents ......................................................................... 40 (given) Less amortization ........................................................ 3 ($500 x 6 mos.) Patents, net ................................................................ 37 (subtotal) Total Assets ................................................................. $1,584 LIABILITIES AND STOCKHOLDERS’ EQUITY Accounts payable ....................................................... $ 125 (30 days' purchases)** Accrued taxes.............................................................. 8 (from Inc. Stmt.) Stockholders' equity ................................................... 1,300 (given) Retained earnings ....................................................... 8 (from Inc. Stmt.) Additional funds needed ............................................ 143 "plug" Total liabilities and equity .......................................... $1,584

* ($250,000 x 6) / 180 days = $8,333 per day x 45 days = $375,000 ** ($125,000 x 6) / 180 days = $4,166 per day x 30 days = $125,000

Chapter 09 - Prospective Analysis

9-23

Problem 9-5 — continued c. Telnet Corporation Forecasted Statement of Cash Flows For Six Months Ended June 30, Year 2

Cash balance, beginning ................................................... $ 60,000 Add collection of accounts receivable * ........................... 1,125,000 $1,185,000 Less disbursements for

Material purchases ** .................................................... 625,000 Labor .............................................................................. 183,000 Rent ................................................................................ 60,000 Overhead ........................................................................ 135,000 Selling expense ............................................................. 285,000 (1,288,000)

Tentative cash balance ....................................................... $ (103,000) Minimum cash balance required ....................................... 40,000 Additional borrowing required ........................................... $ 143,000 Ending cash balance ......................................................... $ 40,000 Loan balance ....................................................................... $ 143,000

* Collection of accounts receivable Jan. Feb. Mar. Apr. May June Sales .......................................................................... 250 250 250 250 250 250 Collections ................................................................ 0 125 250 250 250 250 Accumulated Collections ........................................ 0 125 375 625 875 1,125 ** Payment of accounts payable Jan. Feb. Mar. Apr. May June Purchases ................................................................. 125 125 125 125 125 125 Payments .................................................................. 0 125 125 125 125 125 Accumulated Payments .......................................... 0 125 250 375 500 625

Chapter 09 - Prospective Analysis

9-24

Problem 9-6 (95 minutes) Quaker Oats Forecasted Statement of Cash Flows For Year Ended June 30, Year 12 Cash provided by (used for) operations Net income (a) ............................................................................................. $ 238.8 Items in income not affecting cash Depreciation & amortization (b) ............................................................... 196.6 Deferred income taxes (c) ........................................................................ 54.7 Provision for restructuring charges (given) ........................................... 0.0 Increase in receivables (d) ......................................................................... (8.9) Increase in inventories (e) .......................................................................... (45.2) Increase in other current assets (f) ........................................................... (25.6) Increase in accounts payable (g) ............................................................... 42.1 Increase in other current liabilities (h) ...................................................... 24.5 Cash provided by operating activities ...................................................... $ 477.0 Cash provided by (used for) investment activities Capital expenditures, PP&E (given) .......................................................... $ (300.0) Asset retirements (given) ........................................................................... 20.0 Other changes (given) ................................................................................ (30.0) Cash used for investing activities ............................................................. $ (310.0) Cash provided by (used for) financing activities Repayments of L-T debt (given) ................................................................ $ (45.0) Net decrease in S-T debt (given) ............................................................... (40.0) Cash dividend paid (given) ........................................................................ (135.0) Additions to L-T debt—plug (i) .................................................................. 55.8 Cash provided by financing activities ....................................................... $(164.2) Net increase in cash (j) ............................................................................... $ 2.8

Cash, beginning balance ............................................................................ 30.2 Cash, balance at end of year ...................................................................... $ 33.0

Notes: (a) Average percent of income from continuing operations to sales, Years 9-11

($235.8 +$228.9 + $148.9) / ($5,491.2 + $5,030.6 + $4,879.4) = 3.98% Net income in Year 12 = $6,000 x .0398 = $238.8

Chapter 09 - Prospective Analysis

9-25

Problem 9-6 – continued

(b) Depreciation and amortization in Year 12 = $238.8 x .8233 = $196.6 (c) Average percent of deferred income taxes (noncurrent) and other items to income from

continuing operations, Years 9-11: $140.4 / $613.6 = 22.9% Noncurrent deferred income tax in Year 12 = $238.8 x .229 = $54.7 (d) Ending accounts receivable = $6,000 x (42/360) = $700.0

For Year 12: Accounts receivable, beg $691.1 Accounts receivable, end 700.0 Increase $ 8.9

(e) Year 12 cost of sales = $6,000 x .51 = $3,060

Ending inventory = $3,060 x (55/360) = $467.5 For Year 12: Inventory, beg $422.3

Inventory, end 467.5 Increase $ 45.2

(f) ($13.7 + $14.1 + $48.9)/3 = $25.6 (g) Year 12 purchases = $2,807.2 x 1.12 = $3,144.1

Accounts payable, end = $3,144.1 x (45/360) = $393.0 For Year 12: Accounts payable, beg $350.9

Accounts payable, end 393.0 Increase $ 42.1

(h) ($43.2 + $83.4 - $53.1)/3 = $24.5 (i) Amount required to balance statement. (j) Percent of cash to revenues in Year 11 = $30.2 / $5,491.2 = 0.55%

Year-end cash in Year 12 = $6,000 x 0.55% = $33 Increase in cash for Year 12 = $33 - $30.2 = $2.8

Chapter 09 - Prospective Analysis

9-26

CASES Case 9-1 (60 minutes) Kodak INCOME STATEMENT 20x7 Est 20x6 20x5

Net sales 12,515 13,234 13,994 Cost of goods 8,199 8,670 8,375 Gross profit 4,316 4,564 5,619 Selling general & administrative expense (except depreciation) 1,761 1,862 1,776 Depreciation expense 766 765 738 Research & development costs 737 779 784 Goodwill amortization 0 154 151 Restructuring costs (credits) 0 659 -44 Earnings from operations 1,052 345 2,214 Interest expense 208 219 178 Other expense (income) 18 18 -96 Income before tax 827 108 2,132 Income tax expense 245 32 725 Net income 582 76 1,407 Outstanding shares 290 290 290 RATIOS Sales growth -5.43% -5.43% Gross Profit Margin 34.49% 34.49% Selling General & Administrative Exp / Sales 14.07% 14.07% DEPRECIATION (depn exp / pr yr PPE gross) 5.90% 5.90% R&D/sales 5.89% 5.89% INT (int / pr yr STD and LTD) 6.49% 6.49% Tax (Inc Tax / Pre-tax inc) 29.63% 29.63%

Chapter 09 - Prospective Analysis

9-27

Case 9-1 – continued BALANCE SHEET 20x7 Est 20x6 20x5 Cash $ 17 $ 448 $ 246 Receivables 2,210 2,337 2,653 Inventories 1,075 1,137 1,718 Other 761 761 874 Total current assets 4,064 4,683 5,491 Property, plant & equipment 13,972 12,982 12,963 (NOTE 4) Accumulated depreciation 8,089 7,323 7,044 Net property & equipment 5,883 5,659 5,919 Other assets 3,020 3,020 2,802 Total assets $12,967 $13,362 $14,212 Accounts payable & accrued liabilities 3,098 3,276 3,403 Short-term debt 1,378 1,378 2,058 Current maturities of l-t debt 13 156 148 (NOTE 8) Income taxes 544 544 606 Total current liab 5,033 5,354 6,215 Long term debt 1,653 1,666 1,166 Postemployment liabilities 2,728 2,728 2,722 Other long-term liabilities 720 720 681 Total liabilities 10,134 10,468 10,784 Common stock 978 978 978 Capital surplus 849 849 871 Retained earnings 6,773 6,834 7,387 Treasury stock 5,767 5,767 5,808 Shareholder equity 2,833 2,894 3,428 Total liabilities & net worth 12,967 13,362 14,212 RATIOS AR turn 5.66 5.66 5.27 INV turn 7.63 7.63 4.87 AP turn 2.65 2.65 2.46 FLEV 4.58 4.62 4.15 Div/sh $2.22 $2.22 $1.88 CAPEX 990 1047 783 CAPEX/Sales 7.91% 7.91% 5.60%

Chapter 09 - Prospective Analysis

9-28

Case 9-1 – continued Statement of Cash Flows 20x7 Estim.

Net income $ 582

Depreciation 766

Accounts receivable 127

Inventories 62

Accounts payable (178)

Net cash flow from operations 1,359 CAPEX (990) Net cash flow from investing activities (990) Long term debt (156) Dividends (643) Net cash flow from financing activities (799) _____ Net change in cash (431) Beginning cash 448 Ending cash $ 17

Chapter 09 - Prospective Analysis

9-29

Case 9-2 (120 minutes) Miller Company Cash Forecast For Years Ended December 31, Years 2 through 4 Year 2 Year 3 Year 4

Cash balance at beginning of period .................. $ 0 $1,929,000 $254,500 Cash received from stockholders ....................... 100,000 0 0 Proceeds of loan (see [a]) .................................... 1,700,000 100,000 0 Cash receipts less cash payments (see [b]) ....... 129,000 125,500 146,500 Payments for construction ................................... 0 (1,700,000) (100,000) Payments on loan (see [a]) ................................... 0 (200,000) (200,000) Cash balance at end of period ............................. $1,929,000 $ 254,500 $101,000

Supporting Schedules for the Cash Forecast

[a] Schedule of interest and commitment fees Amount of Interest Loan or Fee

Year 2: To be borrowed 1/1 .................................................................. $ 800,000 To be borrowed 4/1 .................................................................. 500,000 Commitment fee due 4/1 ($1,000,000 x 1% x 1/4) .................. $ 2,500 To be borrowed 7/1 .................................................................. 300,000 Commitment fee due 7/1 ($500,000 x 1% x 1/4) ..................... 1,250 To be borrowed 12/31 .............................................................. 100,000 Commitment fee due 12/31 ($200,000 x 1% x 1/2) ................. 1,000 Interest due on loan: On $800,000 @ 5% .............................................................. 40,000 On $500,000 @ 5% x 3/4 ..................................................... 18,750 On $300,000 @ 5% x 1/2 ..................................................... 7,500 Total at 12/31/Year 2 ................................................................. $1,700,000 $71,000 Year 3: To be borrowed 4/1 .................................................................. 100,000 Commitment fee due 4/1 ($100,000 x 1% x 1/4) ..................... 250 Repayment of loan: Due 6/30 .............................................................................. (100,000) Due 12/31 ............................................................................ (100,000) Interest due on loan: On $1,700,000 @ 5% x 1/4 .................................................. 21,250 On $1,800,000 @ 5% x 1/4 .................................................. 22,500 On $1,700,000 @ 5% x 1/2 .................................................. 42,500 Total at 12/31/Year 3 ................................................................. $1,600,000 $86,500 Year 4: Repayment of loan: Due 6/30 .............................................................................. (100,000) Due 12/31 ............................................................................ (100,000) Interest due on loan: On $1,600,000 @ 5% x 1/2 .................................................. 40,000 On $1,500,000 @ 5% x 1/2 .................................................. 37,500 Total at 12/31/Year 4 ................................................................. $1,400,000 $77,500

Chapter 09 - Prospective Analysis

9-30

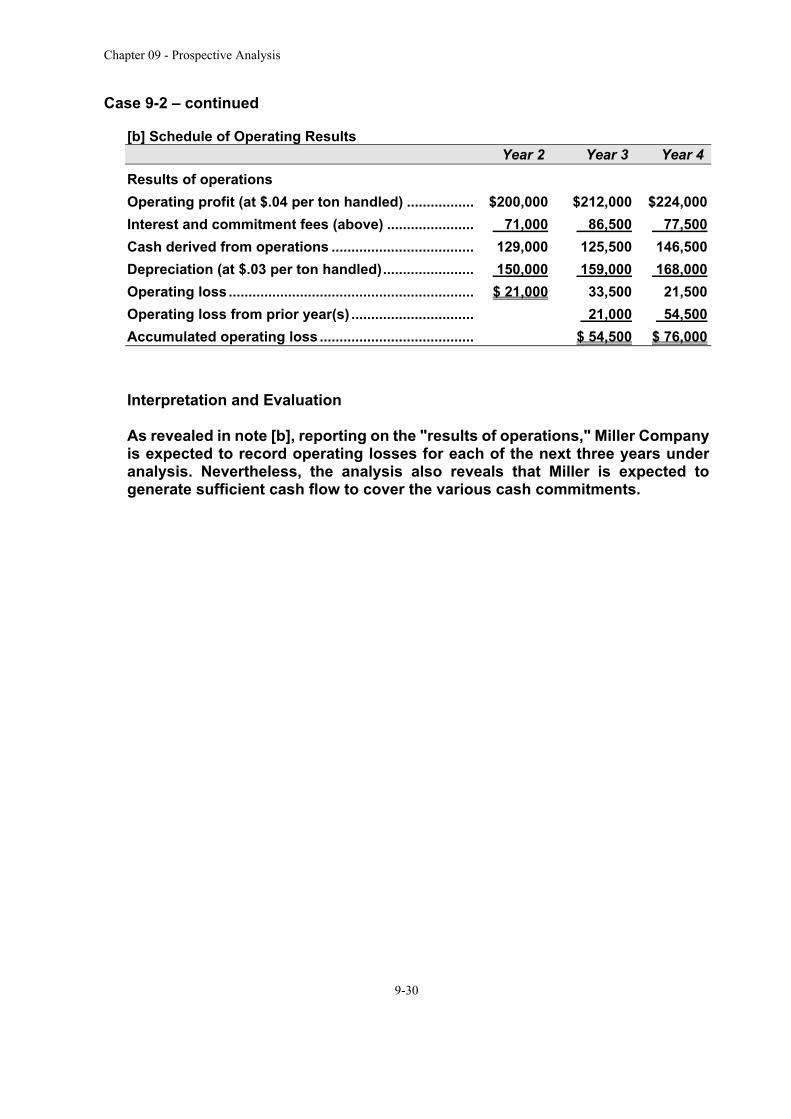

Case 9-2 – continued [b] Schedule of Operating Results

Year 2 Year 3 Year 4 Results of operations Operating profit (at $.04 per ton handled) ................. $200,000 $212,000 $224,000 Interest and commitment fees (above) ...................... 71,000 86,500 77,500 Cash derived from operations .................................... 129,000 125,500 146,500 Depreciation (at $.03 per ton handled) ....................... 150,000 159,000 168,000 Operating loss .............................................................. $ 21,000 33,500 21,500 Operating loss from prior year(s) ............................... 21,000 54,500 Accumulated operating loss ....................................... $ 54,500 $ 76,000

Interpretation and Evaluation As revealed in note [b], reporting on the "results of operations," Miller Company is expected to record operating losses for each of the next three years under analysis. Nevertheless, the analysis also reveals that Miller is expected to generate sufficient cash flow to cover the various cash commitments.

Chapter 09 - Prospective Analysis

9-31

Case 9-3 (100 minutes) Royal Company Cash Forecast For Years Ending March 31, Years 6 and 7

Year 6 Year 7 Beginning balance of cash ...................................... $ 0 $ 75,000 Cash receipt from customers (see Schedule A) .... 825,000 1,065,000 Cash disbursements Direct materials (see Schedule B) ......................... 220,000 245,000 Direct labor .............................................................. 300,000 360,000 Variable overhead ................................................... 100,000 120,000 Fixed costs ............................................................. 130,000 130,000 Total cash disbursements ..................................... 750,000 855,000 Operating cash receipts less disbursements ........ 75,000 210,000 Cash from sale of receivables and inventories ..... 90,000 0 Total cash available .................................................. $165,000 $ 285,000 Payments to general creditors ................................ 90,000 270,000 2

Ending balance of cash ............................................ $ 75,000 1 $ 15,000 1 This amount could have been used to pay general creditors or carried forward to the beginning

of the next year. 2 Computed as: ($600,000 x 60%) - ($50,000 + $40,000).

Schedule A Cash Receipts from Customers

Year 6 Year 7 Sales .......................................................................................... $900,000 $1,080,000 Beginning accounts receivable .............................................. 0 75,000 Total ......................................................................................... 900,000 1,155,000 Less: Ending accounts receivable ......................................... 75,000 90,000 Cash receipts from customers ............................................... $825,000 $1,065,000

Schedule B Cash Disbursements for Direct Materials

Year 6 Year 7 Direct materials required for production ................... $200,000 $240,000 Required ending inventory .......................................... 40,000 3 50,000 4

Total ............................................................................. 240,000 290,000 Less: Beginning inventory .......................................... 0 40,000 Purchases .................................................................. 240,000 250,000 Beginning accounts payable ...................................... 0 20,000

Total ............................................................................. 240,000 270,000 Less: Ending accounts payable ................................. 20,000 25,000 Disbursements for direct materials ............................ $220,000 $245,000 3 Computed as: 12,000 units x 2/12 = 2,000; 2,000 x $20 per unit = $40,000. 4 Computed as: 15,000 units x 2/12 = 2,500; 2,500 x $20 per unit = $50,000.

Chapter 09 - Prospective Analysis

9-32

Case 9-4 (115 minutes) a. (1) Estimated Total Cash Receipts

Sep. Oct. Nov. Dec. Total sales ............................................. $40,000 $48,000 $60,000 $80,000 Credit sales (25%) ................................. 10,000 12,000 15,000 20,000 Cash sales ................................ $30,000 36,000 $45,000 $60,000 Receipts of past month's credit sales 10,000 12,000 15,000 Total cash receipts ............................... $46,000 $57,000 $75,000

(2)

Estimated Cash Disbursements for Purchases Oct. Nov. Dec. Total

Total Sales ........................................ $48,000 $60,000 $80,000 — Purchases (70% next mo. sales) .... $42,000 $56,000 $25,200 $123,200 Less: 2% purchase discount .......... 840 1,120 504 2,464 Cash disbursements ....................... $41,160 $54,880 $24,696 $120,736

(3)

Estimated Cash Disbursements for Operating Expenses Oct. Nov. Dec. Total

Sales ................................................. $48,000 $60,000 $80,000 — Salaries and Wages (15%) .............. $ 7,200 $ 9,000 $12,000 $28,200 Rent (5%) .......................................... 2,400 3,000 4,000 9,400 Other Expenses (4%) ....................... 1,920 2,400 3,200 7,520 Cash disbursements ....................... $11,520 $14,400 $19,200 $45,120 (4)

Estimated Total Cash Disbursements Oct. Nov. Dec. Total

Purchases [part (2)] ......................... $41,160 $54,880 $24,696 $120,736 Operating expenses [part (3)] ......... 11,520 14,400 19,200 45,120 Plant and equipment (given) ........... 600 400 1,000 Total cash disbursements .............. $53,280 $69,680 $43,896 $166,856 (5)

Estimated Net Cash Receipts and Disbursements Oct. Nov. Dec. Total

Total cash receipts .......................... $46,000 $57,000 $75,000 $178,000 Total cash disbursements .............. 53,280 69,680 43,896 166,856 Net cash increase ............................ $31,104 $ 11,144 Net cash decrease ........................... $ 7,280 $12,680

Chapter 09 - Prospective Analysis

9-33

Case 9-4 — continued (6)

Estimated Financing Required Oct. Nov. Dec. Total

Beginning cash balance .................. $12,000 $ 8,720 $ 8,040 $12,000 Net cash increase ............................ 31,104 11,144 Net cash decrease ........................... 7,280 12,680 Cash position before financing ...... $ 4,720 $(3,960) $39,144 $23,144 Financing required .......................... 4,000 12,000 16,000 Interest expense 1 ............................ (180) (180) Financing retired .............................. (16,000) (16,000) Ending cash balance ....................... $ 8,720 $ 8,040 $22,964 $22,964

1 Computed as: ($4,000 x .06 x 3/12) + ($12,000 x .06 x 2/12). b. (1) Union Corporation Forecasted Income Statement For the Quarter Ended December 31, Year 6

Sales [see (1) in part a] ....................................................... $188,000 Deduct

Cost of goods sold (70% of sales) ............................... $131,600 Less: Purchase discounts taken [see (2) in part a] .... 2,464 129,136

Gross profit ......................................................................... 58,864 Selling and administrative expenses

Salaries and wages [see (3) in part a] ......................... 28,200 Rent [see (3) in part a] ................................................... 9,400 Other expenses [see (3) in part a] ................................ 7,520 Depreciation ($750 x 3 months) ................................... 2,250

Total selling and administrative expenses ....................... 47,370 Operating income ............................................................... 11,494 Interest expense ................................................................. 180 Net income ....................................................................... $ 11,314

Chapter 09 - Prospective Analysis

9-34

Case 9-4 — continued (2) Union Corporation Forecasted Balance Sheet As of December 31, Year 6

ASSETS Current Assets

Cash [see (6) in part a] .................................................. $ 22,964 Accounts receivable (25% of Dec. sales) .................... 20,000 Inventory [($30,000 + 70% of $36,000) x 98%] ............. 54,096

Total current assets ............................................................ $ 97,060 Plant and equipment .......................................................... 101,000 Less: Accumulated depreciation ...................................... 2,250 98,750 Total assets ......................................................................... $195,810 LIABILITIES AND EQUITY Liabilities ............................................................................. $ 0 Stockholders' equity ........................................................... 195,810 Total liabilities and equity .................................................. $195,810