Embed Size (px)

Citation preview

PT Distribusi Voucher Nusantara Tbk.

Go-to Solution for Everyday Digital Needs

27 November 2018

PT Distribusi Voucher Nusantara Tbk. (DIVA) is a digital converter and

accelerator company that connects B2B2C. DIVA introduces Intelligent

Instant Messaging (IIM) and Smart Outlet (SO). The company utilizes

phone credit distribution channel to build digital infrastructure and

ecosystem through IIM and SO where development and innovation is

limitless. Both products offer a more convenient way of doing digital

activities, while giving the solution for smartphone’s storage and

performance limitation as well as financial inclusion issue, all wrapped

in affordable yet flexible platforms and devices.

Everyday needs all catered in one app. DIVA capitalizes on the

opportunity of high social media usage in Indonesia by providing IIM

for digital product transactions and activities. DIVA makes it possible to

rely only on our must-have instant messaging apps (Whatsapp/Line/

Facebook Messenger/Telegram) to serve day-to-day digital activities.

The service is made available by adding DIVA to users’ cell phone

contact list. Users will then be able to enjoy a wide range of digital

services, which were previously provided through countless apps that

requires big chunk of storage and drains battery performance. As an

added value, DIVA builds partnership with companies to provide

customized digital transactions and services. We believe that IIM is a

very attractive tech platform since it reduces storage and

inconvenience by being a one-stop solution for many daily needs.

Financial inclusion supporter. Government is keen to encourage

financial literacy and achieve an integrated financial system in

Indonesia. DIVA comes to support that vision by providing Smart

Outlet, a unified multi-payment device that allows merchants to sell

digital products and do inventory management. This device that DIVA

produced accommodates a variety of multi-banks and multi-payment

format (debit, credit, flazz, QR code, cash). It comes in another version

equipped with identity card and fingerprint reader. We see DIVA’s

devices to be widely used given the benefits it brings to support

government’s financial inclusion and National Payment Gateway effort.

Support from Telkom Indonesia. As Indonesia’s largest telco player,

Telkom has a very large phone credit agent base. DIVA comes to

transform conventional phone credit retail distribution to a digital one.

This movement is greatly welcomed by Telkom Indonesia and is

supported by a special division made for enhancing DIVA and Telkom’s

partnership. We think that the aid given by Telkom will help to enable

DIVA’s rapid agent acquisition process, and thus drive sales higher.

Benefitting from the rising travel hype. Hand-in-hand with Smailing

Tour and telco providers, DIVA is going to launch a new form of travel

packages and promotions. Customers can purchase tours and travel

packages from DIVA agents and payment can be made in installments

in the form of bundling program with telco providers. We believe this

will grant a very attractive revenue stream for DIVA, given the

opportunity tourism industry has.

Taking into account the robust growth potential empowered by

innovative digital products that DIVA has, we value the company at

26x FY19F EV/EBITDA which implies a target price of IDR 4,950

per share. We view that DIVA has the capability to receive huge

enthusiasm from society and to build immense digital infrastructure due

to 1) Products’ mobility and ability to adopt any digital products and

services into its platform and device, 2) User-friendly IIM and Smart

Outlet, 3) Favorable relationship with banks, telco players, and

travel companies.

Paulina Equity Analyst +62 21 392 5550 ext. 610 [email protected]

BUY (TP: IDR 4,950)

Stock Information

Sector Digital

Bloomberg Ticker DIVA.IJ

Market Cap. (IDR tn) 2.1

Share Out./Float (mn) 714/214

IPO Price 2,950

FY19F Target Price (IDR) 4,950

Upside 68.1%

Relative Valuations

Target FY19F EV/EBITDA 26.0x

Target FY19F P/E 52.3x

Target FY19F P/BV 4.7x

2 DIVA | 27 November 2018

Company Background

PT Distribusi Voucher Nusantara Tbk. (DIVA) is a digital business

converter and accelerator in the form of platform and device. DIVA

aims to boost e-payment and financial inclusion in Indonesia, facilitate

digital transactions and activities, and level up Small Medium

Enterprises’ (SMEs) competitiveness. It applies B2B2C business model.

The company introduced two business initiatives: DIVA Smart Outlet

and DIVA Intelligent Instant Messaging. Both are purposed to enhance

digital products distribution and to aid enterprises and SMEs in their

business activities.

Followings are company’s breakthroughs in the digital industry,

1) DIVA Smart Outlet

Integrating payment system and PoS (Point of Sales) for digital and

non-digital products and services, DIVA Smart Outlet comes with its

simple, reliable, and secured smart device. The device enables users to

sell digital products and manage inventory system. It can also serve as

a cashier and receive e-money, debit, credit card, and QR code

payment from multiple banks. DIVA targets to distribute 24,400 units

of smart outlet for SMEs and banks. To enjoy the Smart Outlet. users

are required to pay IDR 150k (40% of the charge goes to Telkom

Indonesia) subscription fee per month to enjoy the complete service of

Smart Outlet including the internet connection. Additionally, DIVA has

KYC-featured Smart Outlet which is equipped with e-KTP and finger

print scanner. This will support companies to improve their productivity

and efficiency in customer-related process.

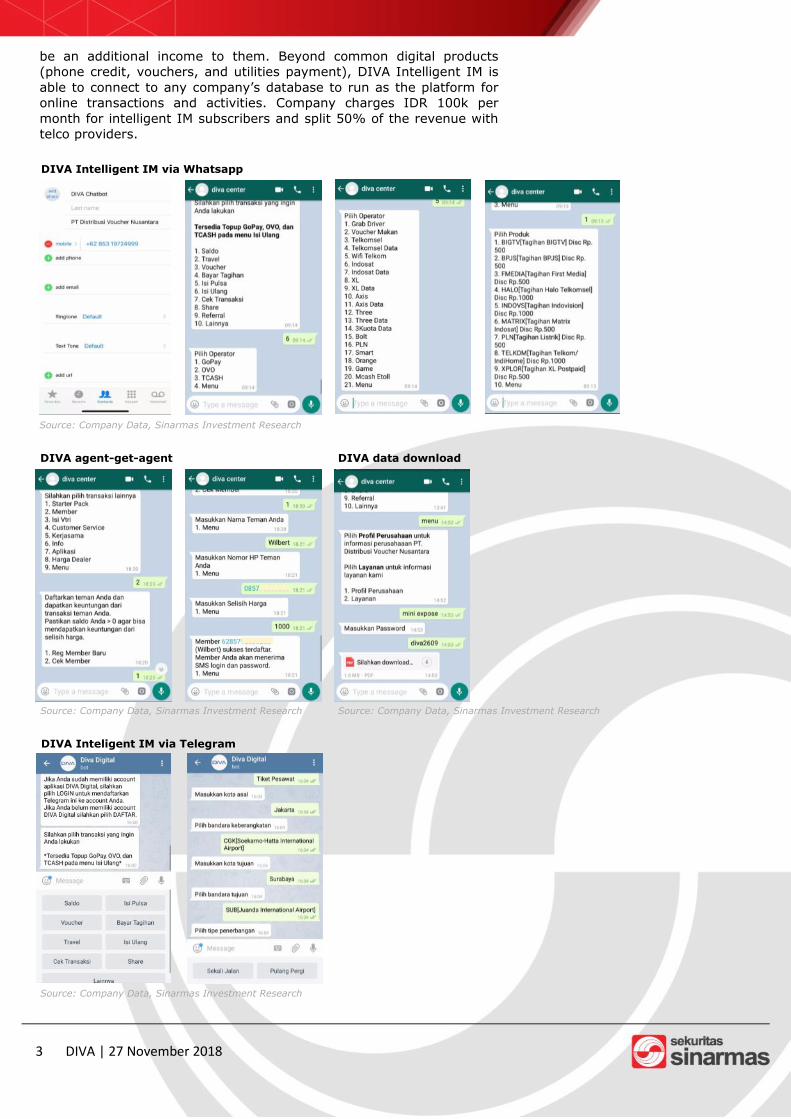

2) DIVA Intelligent Instant Messaging

DIVA tries to simplify digital sales and activities by channeling all digital

services through instant messaging. The system operates under

chatbot supported by Artificial Intelligence (AI) technology. Through

IIM, DIVA’s agents are able to sell various digital products. Users are

only required to add related contacts to their phone and do

transactions via chat instantly. Besides product marketing, agents have

the chance to acquire sub-agents where pre-determined pricing gap will

DIVA Smart Outlet

Source: Company Data, Sinarmas Investment Research

3 DIVA | 27 November 2018

be an additional income to them. Beyond common digital products

(phone credit, vouchers, and utilities payment), DIVA Intelligent IM is

able to connect to any company’s database to run as the platform for

online transactions and activities. Company charges IDR 100k per

month for intelligent IM subscribers and split 50% of the revenue with

telco providers.

DIVA Intelligent IM via Whatsapp

Source: Company Data, Sinarmas Investment Research

DIVA agent-get-agent

Source: Company Data, Sinarmas Investment Research

DIVA Inteligent IM via Telegram

DIVA data download

Source: Company Data, Sinarmas Investment Research

Source: Company Data, Sinarmas Investment Research

4 DIVA | 27 November 2018

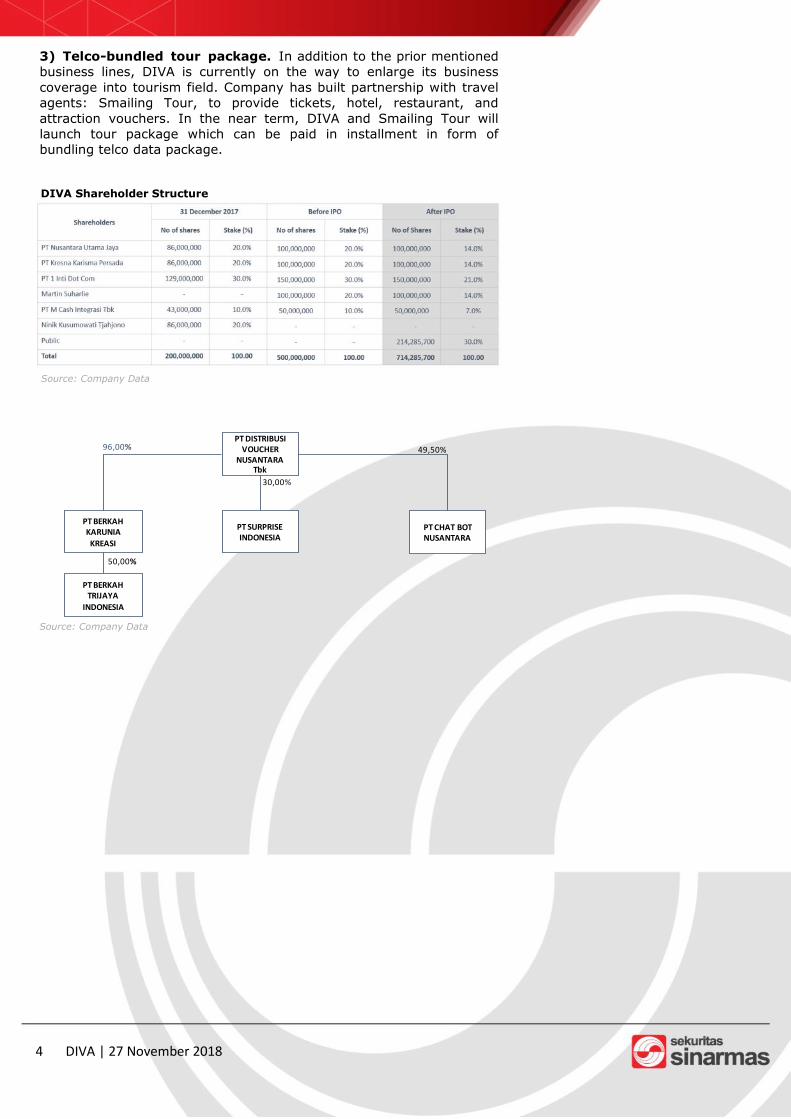

3) Telco-bundled tour package. In addition to the prior mentioned

business lines, DIVA is currently on the way to enlarge its business

coverage into tourism field. Company has built partnership with travel

agents: Smailing Tour, to provide tickets, hotel, restaurant, and

attraction vouchers. In the near term, DIVA and Smailing Tour will

launch tour package which can be paid in installment in form of

bundling telco data package.

DIVA Shareholder Structure

Source: Company Data

Source: Company Data

PT KRESNA KARISMA

PERSADA

PT M CASH INTEGRASI Tbk

PT 1 INTI DOT COM

PT NUSANTARA UTAMA JAYA

MARTIN SUHARLIE

20,00%30,00%20,00% 10,00% 20,00%

PT BERKAH KARUNIA

KREASI

PT DISTRIBUSI VOUCHER

NUSANTARA Tbk

30,00%

PT SURPRISE INDONESIA

96,00% 49,50%

PT BERKAH TRIJAYA

INDONESIA

50,00%

PT Kresna Graha

InvestamaTbk (KREN)

Ingrid

KusumodjojoRaymond

Loho

Ninik

KusumowatiTjahjono

PT Jas

KapitalPT Hero

IntiputraPublik

PT Kresna

KarismaPersada

PT Pesona

Indonesia Pertiwi

PT Kresna

Usaha Kreatif

13,20% 99,38% 0,62%15,00% 85,00%9,00% 9,00% 7,50% 1,80% 25,00%

Michael

StevenSuryandy

Jahja

50,00%50,00%21,00%

PT 1 Inti

Dot Com

PT Gratia

TujuhbelasFebruari

4,50%

Martin

Suharlie

9,00%

26,00% 60,70%6,10%

NKT

RL15%

KREN

OB

99,99%

0,01%

85%KKP

AKM

19,55%

6,00%

AMI

PMP

6,23%

4,90%

BMC

SMS

26,46%

7,21%

GTF29,65%

IMLD

YLNI

84,00%

1,00%

ISDJ15,00%

KKP

NHJT

19,55%

75,26%

IK

MK

12,37%

12,37%

MS

SJ

50,00%

50,00%

SVHK

IJ

DKL

YYH

SJ

OB

MS

KS

16,70%

16,70%

11,10%

11,10%

11,10%

11,10%

11,10%

11,10%

Michael

Steven

Suryandy

JahjaPT Kresna

Prima InvestPublik

7,20%

LVA

SJ

15,66%

14,34%

MS

IKS

33,02%

26,98%

IA10,00%

PT CHAT BOT NUSANTARA

5 DIVA | 27 November 2018

Industry Overview

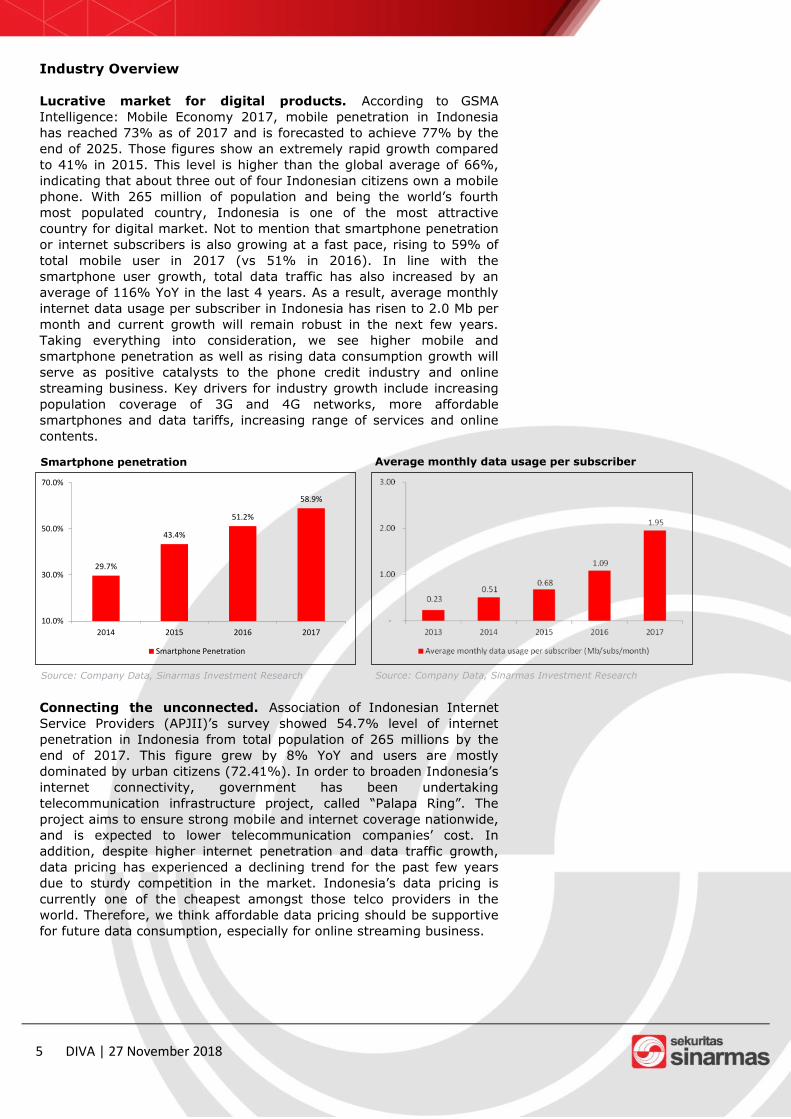

Lucrative market for digital products. According to GSMA

Intelligence: Mobile Economy 2017, mobile penetration in Indonesia

has reached 73% as of 2017 and is forecasted to achieve 77% by the

end of 2025. Those figures show an extremely rapid growth compared

to 41% in 2015. This level is higher than the global average of 66%,

indicating that about three out of four Indonesian citizens own a mobile

phone. With 265 million of population and being the world’s fourth

most populated country, Indonesia is one of the most attractive

country for digital market. Not to mention that smartphone penetration

or internet subscribers is also growing at a fast pace, rising to 59% of

total mobile user in 2017 (vs 51% in 2016). In line with the

smartphone user growth, total data traffic has also increased by an

average of 116% YoY in the last 4 years. As a result, average monthly

internet data usage per subscriber in Indonesia has risen to 2.0 Mb per

month and current growth will remain robust in the next few years.

Taking everything into consideration, we see higher mobile and

smartphone penetration as well as rising data consumption growth will

serve as positive catalysts to the phone credit industry and online

streaming business. Key drivers for industry growth include increasing

population coverage of 3G and 4G networks, more affordable

smartphones and data tariffs, increasing range of services and online

contents.

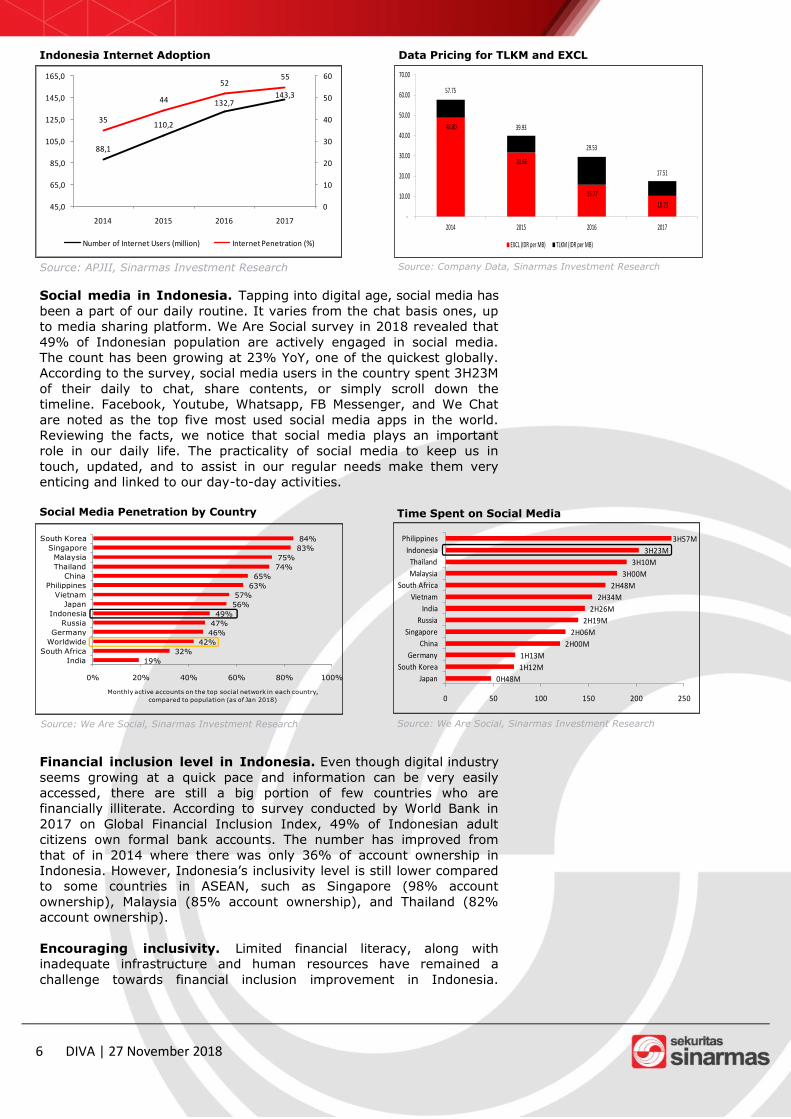

Connecting the unconnected. Association of Indonesian Internet

Service Providers (APJII)’s survey showed 54.7% level of internet

penetration in Indonesia from total population of 265 millions by the

end of 2017. This figure grew by 8% YoY and users are mostly

dominated by urban citizens (72.41%). In order to broaden Indonesia’s

internet connectivity, government has been undertaking

telecommunication infrastructure project, called “Palapa Ring”. The

project aims to ensure strong mobile and internet coverage nationwide,

and is expected to lower telecommunication companies’ cost. In

addition, despite higher internet penetration and data traffic growth,

data pricing has experienced a declining trend for the past few years

due to sturdy competition in the market. Indonesia’s data pricing is

currently one of the cheapest amongst those telco providers in the

world. Therefore, we think affordable data pricing should be supportive

for future data consumption, especially for online streaming business.

29.7%

43.4%

51.2%

58.9%

10.0%

30.0%

50.0%

70.0%

2014 2015 2016 2017

Smartphone Penetration

Smartphone penetration

Source: Company Data, Sinarmas Investment Research

Average monthly data usage per subscriber

Source: Company Data, Sinarmas Investment Research

6 DIVA | 27 November 2018

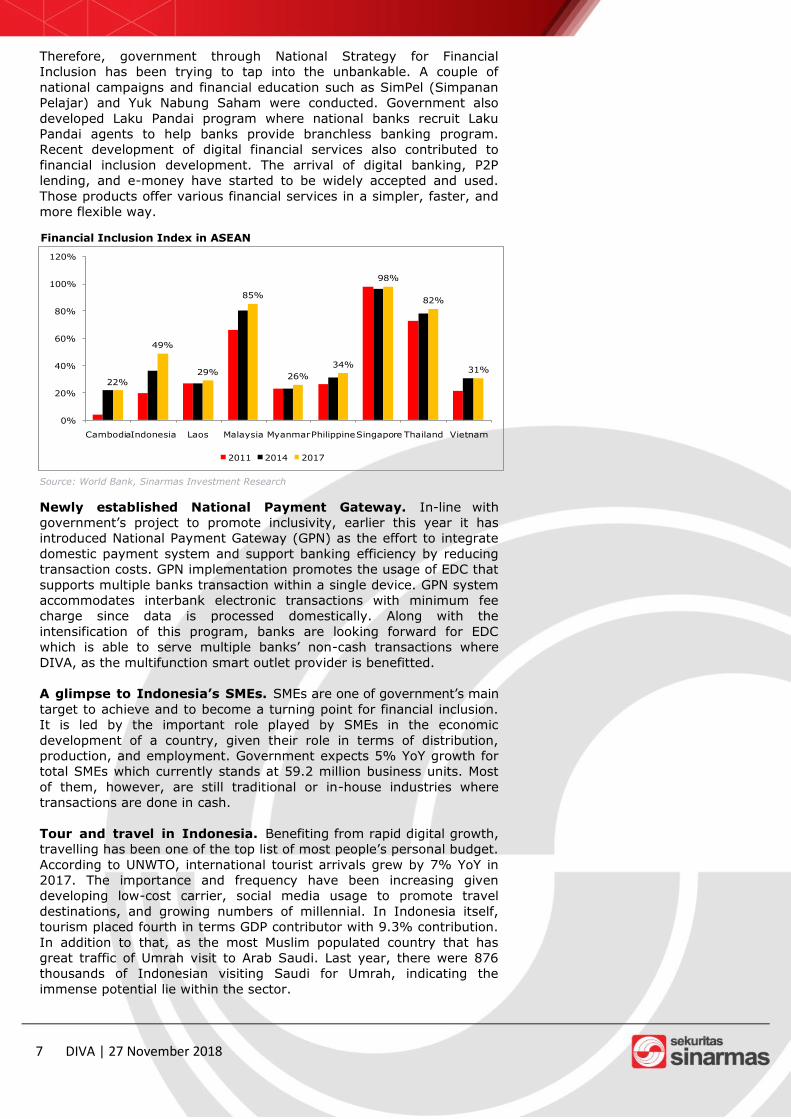

Social media in Indonesia. Tapping into digital age, social media has

been a part of our daily routine. It varies from the chat basis ones, up

to media sharing platform. We Are Social survey in 2018 revealed that

49% of Indonesian population are actively engaged in social media.

The count has been growing at 23% YoY, one of the quickest globally.

According to the survey, social media users in the country spent 3H23M

of their daily to chat, share contents, or simply scroll down the

timeline. Facebook, Youtube, Whatsapp, FB Messenger, and We Chat

are noted as the top five most used social media apps in the world.

Reviewing the facts, we notice that social media plays an important

role in our daily life. The practicality of social media to keep us in

touch, updated, and to assist in our regular needs make them very

enticing and linked to our day-to-day activities.

Financial inclusion level in Indonesia. Even though digital industry

seems growing at a quick pace and information can be very easily

accessed, there are still a big portion of few countries who are

financially illiterate. According to survey conducted by World Bank in

2017 on Global Financial Inclusion Index, 49% of Indonesian adult

citizens own formal bank accounts. The number has improved from

that of in 2014 where there was only 36% of account ownership in

Indonesia. However, Indonesia’s inclusivity level is still lower compared

to some countries in ASEAN, such as Singapore (98% account

ownership), Malaysia (85% account ownership), and Thailand (82%

account ownership).

Encouraging inclusivity. Limited financial literacy, along with

inadequate infrastructure and human resources have remained a

challenge towards financial inclusion improvement in Indonesia.

Indonesia Internet Adoption

Source: APJII, Sinarmas Investment Research

88,1

110,2

132,7143,3

35

44

5255

0

10

20

30

40

50

60

45,0

65,0

85,0

105,0

125,0

145,0

165,0

2014 2015 2016 2017

Number of Internet Users (million) Internet Penetration (%)

48.80

31.66

15.77

10.23

57.75

39.93

29.53

17.51

-

10.00

20.00

30.00

40.00

50.00

60.00

70.00

2014 2015 2016 2017

EXCL (IDR per MB) TLKM (IDR per MB)

Data Pricing for TLKM and EXCL

Source: Company Data, Sinarmas Investment Research

Social Media Penetration by Country

Source: We Are Social, Sinarmas Investment Research

Time Spent on Social Media

Source: We Are Social, Sinarmas Investment Research

19%

32%

42%

46%

47%

49%

56%

57%

63%

65%

74%

75%

83%

84%

0% 20% 40% 60% 80% 100%

India

South Africa

Worldwide

Germany

Russia

Indonesia

Japan

Vietnam

Philippines

China

Thailand

Malaysia

Singapore

South Korea

Monthly active accounts on the top social network in each country,

compared to population (as of Jan 2018)

0H48M

1H12M

1H13M

2H00M

2H06M

2H19M

2H26M

2H34M

2H48M

3H00M

3H10M

3H23M

3H57M

0 50 100 150 200 250

Japan

South Korea

Germany

China

Singapore

Russia

India

Vietnam

South Africa

Malaysia

Thailand

Indonesia

Philippines

7 DIVA | 27 November 2018

Therefore, government through National Strategy for Financial

Inclusion has been trying to tap into the unbankable. A couple of

national campaigns and financial education such as SimPel (Simpanan

Pelajar) and Yuk Nabung Saham were conducted. Government also

developed Laku Pandai program where national banks recruit Laku

Pandai agents to help banks provide branchless banking program.

Recent development of digital financial services also contributed to

financial inclusion development. The arrival of digital banking, P2P

lending, and e-money have started to be widely accepted and used.

Those products offer various financial services in a simpler, faster, and

more flexible way.

Newly established National Payment Gateway. In-line with

government’s project to promote inclusivity, earlier this year it has

introduced National Payment Gateway (GPN) as the effort to integrate

domestic payment system and support banking efficiency by reducing

transaction costs. GPN implementation promotes the usage of EDC that

supports multiple banks transaction within a single device. GPN system

accommodates interbank electronic transactions with minimum fee

charge since data is processed domestically. Along with the

intensification of this program, banks are looking forward for EDC

which is able to serve multiple banks’ non-cash transactions where

DIVA, as the multifunction smart outlet provider is benefitted.

A glimpse to Indonesia’s SMEs. SMEs are one of government’s main

target to achieve and to become a turning point for financial inclusion.

It is led by the important role played by SMEs in the economic

development of a country, given their role in terms of distribution,

production, and employment. Government expects 5% YoY growth for

total SMEs which currently stands at 59.2 million business units. Most

of them, however, are still traditional or in-house industries where

transactions are done in cash.

Tour and travel in Indonesia. Benefiting from rapid digital growth,

travelling has been one of the top list of most people’s personal budget.

According to UNWTO, international tourist arrivals grew by 7% YoY in

2017. The importance and frequency have been increasing given

developing low-cost carrier, social media usage to promote travel

destinations, and growing numbers of millennial. In Indonesia itself,

tourism placed fourth in terms GDP contributor with 9.3% contribution.

In addition to that, as the most Muslim populated country that has

great traffic of Umrah visit to Arab Saudi. Last year, there were 876

thousands of Indonesian visiting Saudi for Umrah, indicating the

immense potential lie within the sector.

Source: World Bank, Sinarmas Investment Research

Financial Inclusion Index in ASEAN

22%

49%

29%

85%

26%

34%

98%

82%

31%

0%

20%

40%

60%

80%

100%

120%

CambodiaIndonesia Laos Malaysia MyanmarPhilippineSingapore Thailand Vietnam

2011 2014 2017

8 DIVA | 27 November 2018

Investment Thesis

DIVA leverages the internet, technology, phone credit allocation, and

relationship it has to build ecosystem, and infrastructure for future

digital interest. We take a look at DIVA, its potential for growth, and

what lies ahead for the company.

Serving your everyday needs in one app. DIVA Intelligent IM

accommodates connection to no limit of platforms and companies.

Multipurpose digital activities are made feasible by only ~3 days of API

connection. Users will only need to download their favorite social media

apps, be it Whatsapp, Line, Telegram, or Facebook Messenger to do

digital transactions and enjoy plenty digital services. Digital

transactions include purchase of digital products such as prepaid phone

and food voucher, as well as settlement of utilities, postpaid and travel

bills. Digital services include online data provider and data downloads.

Features will later develop into much wider range, from e-toll top up,

movie tickets purchase, up to covering the old-fashion healthcare

appointment and insurance products. The convenience of doing basic

activities in a single platform versus different apps for different needs

makes DIVA Intelligent IM very attractive.

Promoting financial inclusion and integrated payment system.

Smart Outlet allows merchants to sell digital products, do inventory

management and transaction analysis in a handy wireless device which

receives cash and all non-cash payment. The device is very much

beneficial for KYC process of banks or any other institutions. We see

Laku Pandai program provides an excellent opportunity for DIVA to

supply branchless banking device for the agents. Smart Outlet also

comes useful for modern channel on the back of NPG’s future

integration. The business line is also supported by government’s effort

to promote branchless banking and digitalize SMEs, indicated by 1,200

devices booked by banks. We believe that DIVA Smart Outlet is the

right pick for banks and any other parties associated with the go

cashless movement.

Support from Telkom Indonesia. Through Intelligent IM, DIVA helps

to transform the conventional way of phone credit retail distribution

into a digital one. This initiative is highly welcomed by Telkom

Indonesia. In the process of digitalizing SMEs and promoting digital

transactions, Telkom Indonesia aids DIVA through its strong

distribution channel, especially in the SMEs segment. We expect robust

growth of DIVA agents in the early stage of acquisition catalyzed by

cooperation with Indonesia’s largest telco player, Telkom Indonesia.

DIVA has had 17k agents in its circle, this year, we expect DIVA to

acquire 225 thousand of agents who then will be able to create down-

line or sub-agents. The acquired agents are also encouraged to seek

other members to be DIVA agents. The so-called down-line are able to

sell DIVA digital products as well, and the pre-determined pricing gap

will be an additional income for the recruiters.

Benefitting from the rising travel hype Current development of

social media has risen the urge of travelling, especially for millennials.

Internet helps to promote must visit travel destinations and hidden

gem discoveries. The travel agencies are there to help travellers by

working their connection, experience, and knowledge to ensure

customers to get the best travel experience. DIVA, who partners with

Smailing tour and travel along with telco providers offer travel

packages where payment can be paid in installment in form of bundling

telco package. The innovation in product experience offered by DIVA

and its partners provide additional attractiveness for DIVA.

9 DIVA | 27 November 2018

Big data mining. Through the infrastructure built, DIVA will be able to

obtain valuable collection of data which pictures beneficial knowledge

to both telecommunication and media industry. The data will be

essential for not only banking, telco, and media industry, but also any

B2C related companies. The information can be employed by

businesses to analyze the supply and demand of their products,

customers preference, transactions schedule, and assist in business

development. All is beneficial for data users to optimize their selling

methods and drive profitable action. We believe that this aspect will be

one of DIVA’s most important treasure as data intelligence has become

more and more important for business to make their strategic decision.

Number of Agents

Source: Company Data, Sinarmas Investment Research

12 14 19

244

394

494

569

-

100

200

300

400

500

600

2016 2017 2018E 2019F 2020F 2021F 2022F

Number of agents (thousands)

10 DIVA | 27 November 2018

Key Risks

Risk from high-competition in the industry. Given the low-barrier for

entry of digital platform that DIVA is promoting, it creates a high

competition environment in digital market. It often forces players to involve

in subsidy game. However, we view that DIVA benefits from the full

support of Indonesia’s largest telco player, and the simplicity of platform

that it offers.

Risk from tight working capital. Phone credit distributor business nature

requires companies abundant working capital. To add, DIVA’s smart outlet

requires relatively high investment at the beginning of capex cycle for the

products. Smart outlet’s business nature also needs higher working capital

for greater number of smart outlet subscribers.

Risk from adoption process. Nowadays, people are offered with plenty

options of tech-products, including digital product providers. Therefore,

DIVA counters adoption risk as it has to attract target customers.

Risk from cyber security. Digital products are certainly open to security

risk. Hacking or virus attacks may linger along with DIVA Intelligent IM or

Smart Outlet operations which require company to figure out the best

security system to protect its activities.

Risk from execution. Tech companies are challenged to create a product

that can solve key issues in society and deliver the right output. We see

execution risk in regard to company’s unique business model, be it from

internal operation (platform, internet connectivity, contents) or issue from

other supporting parties.

11 DIVA | 27 November 2018

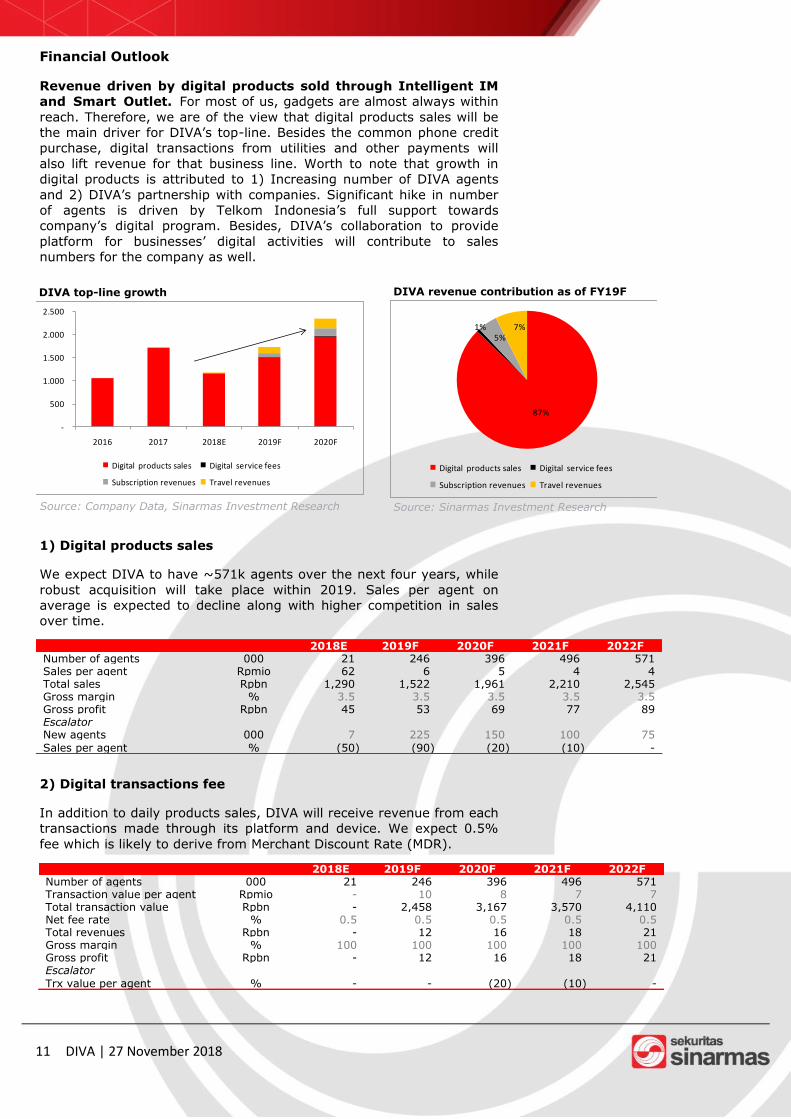

Financial Outlook

Revenue driven by digital products sold through Intelligent IM

and Smart Outlet. For most of us, gadgets are almost always within

reach. Therefore, we are of the view that digital products sales will be

the main driver for DIVA’s top-line. Besides the common phone credit

purchase, digital transactions from utilities and other payments will

also lift revenue for that business line. Worth to note that growth in

digital products is attributed to 1) Increasing number of DIVA agents

and 2) DIVA’s partnership with companies. Significant hike in number

of agents is driven by Telkom Indonesia’s full support towards

company’s digital program. Besides, DIVA’s collaboration to provide

platform for businesses’ digital activities will contribute to sales

numbers for the company as well.

1) Digital products sales

We expect DIVA to have ~571k agents over the next four years, while

robust acquisition will take place within 2019. Sales per agent on

average is expected to decline along with higher competition in sales

over time.

2) Digital transactions fee

In addition to daily products sales, DIVA will receive revenue from each

transactions made through its platform and device. We expect 0.5%

fee which is likely to derive from Merchant Discount Rate (MDR).

DIVA top-line growth

Source: Company Data, Sinarmas Investment Research

DIVA revenue contribution as of FY19F

Source: Sinarmas Investment Research

2018E 2019F 2020F 2021F 2022FNumber of agents 000 21 246 396 496 571 Sales per agent Rpmio 62 6 5 4 4 Total sales Rpbn 1,290 1,522 1,961 2,210 2,545 Gross margin % 3.5 3.5 3.5 3.5 3.5 Gross profit Rpbn 45 53 69 77 89 EscalatorNew agents 000 7 225 150 100 75

Sales per agent % (50) (90) (20) (10) -

2018E 2019F 2020F 2021F 2022FNumber of agents 000 21 246 396 496 571 Transaction value per agent Rpmio - 10 8 7 7 Total transaction value Rpbn - 2,458 3,167 3,570 4,110 Net fee rate % 0.5 0.5 0.5 0.5 0.5 Total revenues Rpbn - 12 16 18 21 Gross margin % 100 100 100 100 100 Gross profit Rpbn - 12 16 18 21 Escalator

Trx value per agent % - - (20) (10) -

-

500

1.000

1.500

2.000

2.500

2016 2017 2018E 2019F 2020F

Digital products sales Digital service fees

Subscription revenues Travel revenues

87%

1%5%

7%

Digital products sales Digital service fees

Subscription revenues Travel revenues

12 DIVA | 27 November 2018

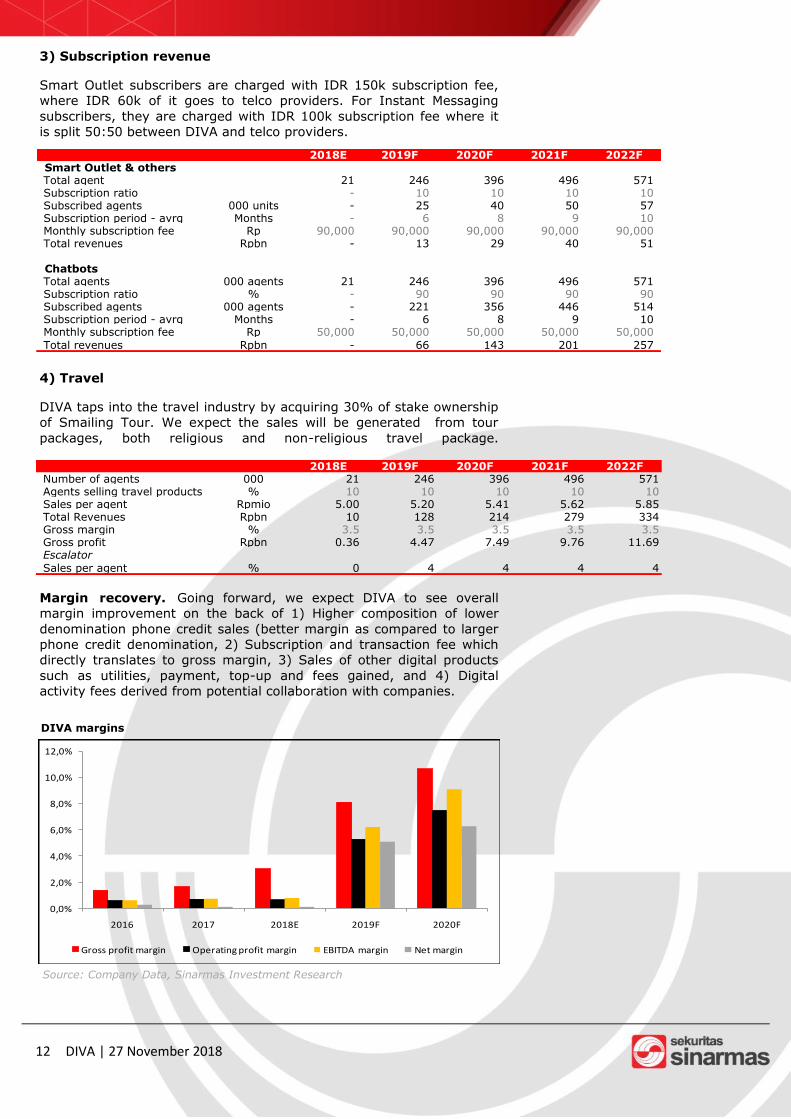

3) Subscription revenue

Smart Outlet subscribers are charged with IDR 150k subscription fee,

where IDR 60k of it goes to telco providers. For Instant Messaging

subscribers, they are charged with IDR 100k subscription fee where it

is split 50:50 between DIVA and telco providers.

4) Travel

DIVA taps into the travel industry by acquiring 30% of stake ownership

of Smailing Tour. We expect the sales will be generated from tour

packages, both religious and non-religious travel package.

Margin recovery. Going forward, we expect DIVA to see overall

margin improvement on the back of 1) Higher composition of lower

denomination phone credit sales (better margin as compared to larger

phone credit denomination, 2) Subscription and transaction fee which

directly translates to gross margin, 3) Sales of other digital products

such as utilities, payment, top-up and fees gained, and 4) Digital

activity fees derived from potential collaboration with companies.

DIVA margins

Source: Company Data, Sinarmas Investment Research

2018E 2019F 2020F 2021F 2022FSmart Outlet & othersTotal agent 21 246 396 496 571 Subscription ratio - 10 10 10 10 Subscribed agents 000 units - 25 40 50 57 Subscription period - avrg Months - 6 8 9 10 Monthly subscription fee Rp 90,000 90,000 90,000 90,000 90,000 Total revenues Rpbn - 13 29 40 51

ChatbotsTotal agents 000 agents 21 246 396 496 571 Subscription ratio % - 90 90 90 90 Subscribed agents 000 agents - 221 356 446 514 Subscription period - avrg Months - 6 8 9 10 Monthly subscription fee Rp 50,000 50,000 50,000 50,000 50,000

Total revenues Rpbn - 66 143 201 257

2018E 2019F 2020F 2021F 2022FNumber of agents 000 21 246 396 496 571Agents selling travel products % 10 10 10 10 10Sales per agent Rpmio 5.00 5.20 5.41 5.62 5.85Total Revenues Rpbn 10 128 214 279 334Gross margin % 3.5 3.5 3.5 3.5 3.5Gross profit Rpbn 0.36 4.47 7.49 9.76 11.69Escalator

Sales per agent % 0 4 4 4 4

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

2016 2017 2018E 2019F 2020F

Gross profit margin Operating profit margin EBITDA margin Net margin

13 DIVA | 27 November 2018

Relative valuation. We use 26x FY2019F EV/EBITDA, arriving at an

target price of IDR 4,950 per share. We value DIVA by using FY2019F

forecasted earnings considering primary business lines will begin

effectively starting next year. We believe that the multiple is justified

by DIVA’s business model, which innovatively transform conventional

product transactions and activities into digital ones. This is further

supported by 1) User-friendly all-in-one platform for digital transactions

and activities, 2) Synergy with government’s financial inclusion

program, 3) Support from Telkom Indonesia, 4) Valuable big data

mining.

IPO Proceeds:

PT Distribusi Voucher Nusantara Tbk. expects to achieve IDR 750bn of IPO

proceeds. The proceeds will be used as follow:

55% for working capital

40% for investments in IT and distribution infrastructures

5% for human capital investments

14 DIVA | 27 November 2018

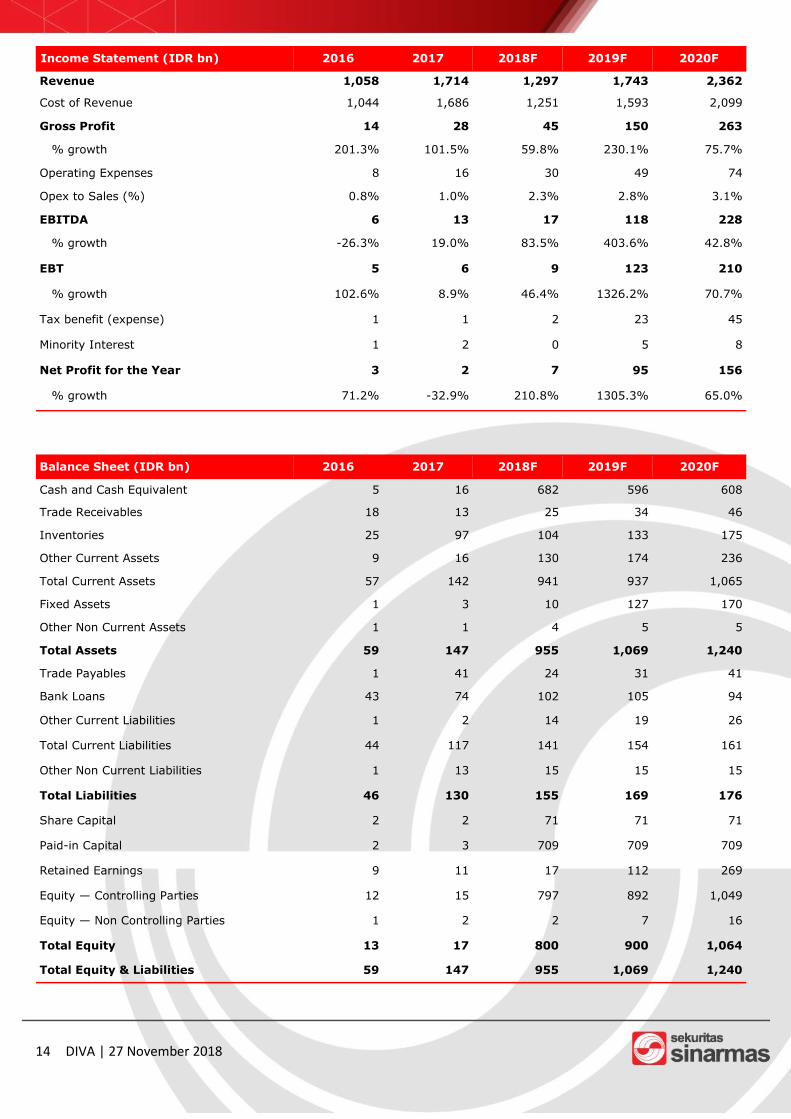

Income Statement (IDR bn) 2016 2017 2018F 2019F 2020F

Revenue 1,058 1,714 1,297 1,743 2,362

Cost of Revenue 1,044 1,686 1,251 1,593 2,099

Gross Profit 14 28 45 150 263

% growth 201.3% 101.5% 59.8% 230.1% 75.7%

Operating Expenses 8 16 30 49 74

Opex to Sales (%) 0.8% 1.0% 2.3% 2.8% 3.1%

EBITDA 6 13 17 118 228

% growth -26.3% 19.0% 83.5% 403.6% 42.8%

EBT 5 6 9 123 210

% growth 102.6% 8.9% 46.4% 1326.2% 70.7%

Tax benefit (expense) 1 1 2 23 45

Minority Interest 1 2 0 5 8

Net Profit for the Year 3 2 7 95 156

% growth 71.2% -32.9% 210.8% 1305.3% 65.0%

Balance Sheet (IDR bn) 2016 2017 2018F 2019F 2020F

Cash and Cash Equivalent 5 16 682 596 608

Trade Receivables 18 13 25 34 46

Inventories 25 97 104 133 175

Other Current Assets 9 16 130 174 236

Total Current Assets 57 142 941 937 1,065

Fixed Assets 1 3 10 127 170

Other Non Current Assets 1 1 4 5 5

Total Assets 59 147 955 1,069 1,240

Trade Payables 1 41 24 31 41

Bank Loans 43 74 102 105 94

Other Current Liabilities 1 2 14 19 26

Total Current Liabilities 44 117 141 154 161

Other Non Current Liabilities 1 13 15 15 15

Total Liabilities 46 130 155 169 176

Share Capital 2 2 71 71 71

Paid-in Capital 2 3 709 709 709

Retained Earnings 9 11 17 112 269

Equity — Controlling Parties 12 15 797 892 1,049

Equity — Non Controlling Parties 1 2 2 7 16

Total Equity 13 17 800 900 1,064

Total Equity & Liabilities 59 147 955 1,069 1,240

15 DIVA | 27 November 2018

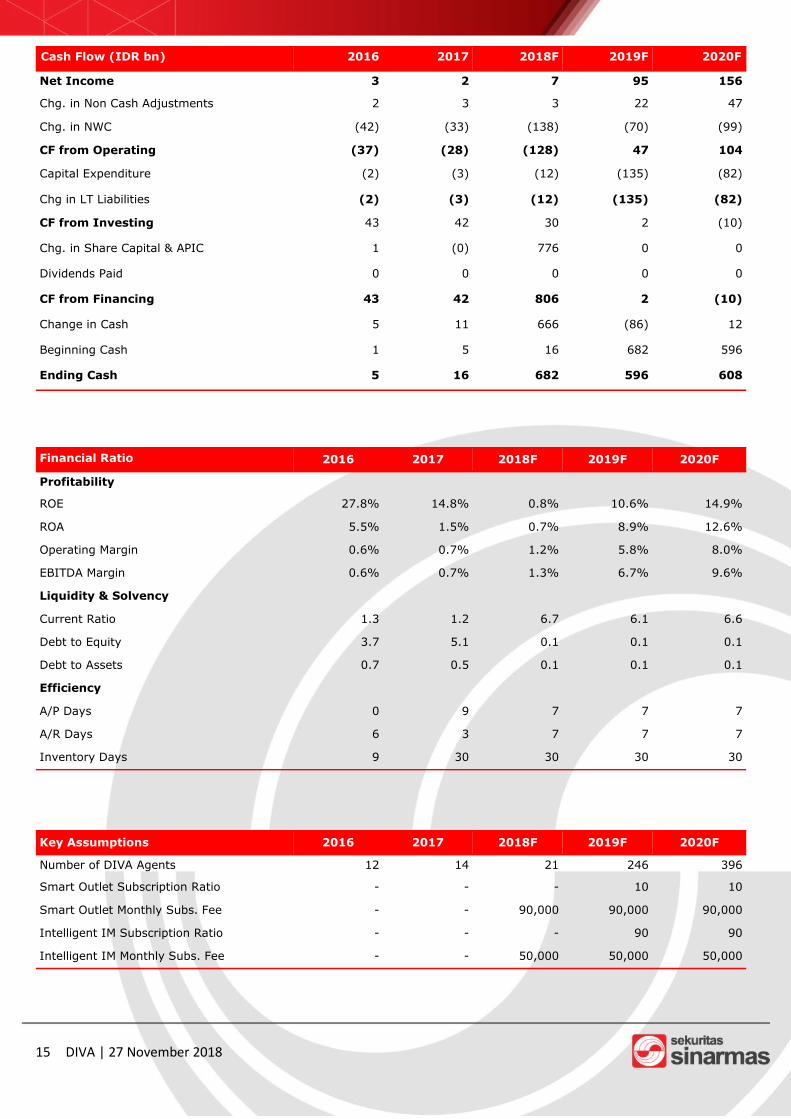

Cash Flow (IDR bn) 2016 2017 2018F 2019F 2020F

Net Income 3 2 7 95 156

Chg. in Non Cash Adjustments 2 3 3 22 47

Chg. in NWC (42) (33) (138) (70) (99)

CF from Operating (37) (28) (128) 47 104

Capital Expenditure (2) (3) (12) (135) (82)

Chg in LT Liabilities (2) (3) (12) (135) (82)

CF from Investing 43 42 30 2 (10)

Chg. in Share Capital & APIC 1 (0) 776 0 0

Dividends Paid 0 0 0 0 0

CF from Financing 43 42 806 2 (10)

Change in Cash 5 11 666 (86) 12

Beginning Cash 1 5 16 682 596

Ending Cash 5 16 682 596 608

Financial Ratio 2016 2017 2018F 2019F 2020F

Profitability

ROE 27.8% 14.8% 0.8% 10.6% 14.9%

ROA 5.5% 1.5% 0.7% 8.9% 12.6%

Operating Margin 0.6% 0.7% 1.2% 5.8% 8.0%

EBITDA Margin 0.6% 0.7% 1.3% 6.7% 9.6%

Liquidity & Solvency

Current Ratio 1.3 1.2 6.7 6.1 6.6

Debt to Equity 3.7 5.1 0.1 0.1 0.1

Debt to Assets 0.7 0.5 0.1 0.1 0.1

Efficiency

A/P Days 0 9 7 7 7

A/R Days 6 3 7 7 7

Inventory Days 9 30 30 30 30

Key Assumptions 2016 2017 2018F 2019F 2020F

Number of DIVA Agents 12 14 21 246 396

Smart Outlet Subscription Ratio - - - 10 10

Smart Outlet Monthly Subs. Fee - - 90,000 90,000 90,000

Intelligent IM Subscription Ratio - - - 90 90

Intelligent IM Monthly Subs. Fee - - 50,000 50,000 50,000

DISCLAIMER This report has been prepared by PT Sinarmas Sekuritas, an affiliate of Sinarmas Group. This material is: (i) created based on information that we consider reliable, but we do not represent that it is accu-rate or complete, and it should not be relied upon as such; (ii) for your private information, and we are not solicit-ing any action based upon it; (iii) not to be construed as an offer to sell or a solicitation of an offer to buy any secu-rity. Opinions expressed are current opinions as of original publication date appearing on this material and the infor-mation, including the opinions contained herein, is subjected to change without notice. The analysis contained here-in is based on numerous assumptions. Different assumptions could result in materially different results. The analyst(s) responsible for the preparation of this publication may interact with trading desk personnel, sales personnel and other constituencies for the purpose of gathering, integrating and interpreting market information. Research will initiate, update and cease coverage solely at the discretion of Sinarmas Research department. If and as applicable, Sinarmas Sekuritas’ investment banking relationships, investment banking and non-investment banking compensa-tion and securities ownership, if any, are specified in disclaimers and related disclosures in this report. In addition, other members of Sinarmas Group may from time to time perform investment banking or other services (including acting as advisor, manager or lender) for, or solicit investment banking or other business from companies under our research coverage. Further, the Sinarmas Group, and/or its officers, directors and employees, including persons, without limitation, involved in the preparation or issuance of this material may, to the extent permitted by law and/or regulation, have long or short positions in, and buy or sell, the securities (including ownership by Sinarmas Group), or derivatives (including options) thereof, of companies under our coverage, or related securities or deriva-tives. In addition, the Sinarmas Group, including Sinarmas Sekuritas, may act as market maker and principal, will-ing to buy and sell certain of the securities of companies under our coverage. Further, the Sinarmas Group may buy and sell certain of the securities of companies under our coverage, as agent for its clients. Investors should consider this report as only a single factor in making their investment decision and, as such, the report should not be viewed as identifying or suggesting all risks, direct or indirect, that may be associated with any investment decision. Recipients should not regard this report as substitute for exercise of their own judgment. Past performance is not necessarily a guide to future performance. The value of any investments may go down as well as up and you may not get back the full amount invested. Sinarmas Sekuritas specifically prohibits the redistribution of this material in whole or in part without the written permission of Sinarmas Sekuritas and Sinarmas Sekuritas accepts no liability whatsoever for the actions of third parties in this respect. If publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of this publication, which may arise as a result of electronic transmission. If verification is required, please request a hard-copy version. Additional information is available upon request. Images may depict objects or elements which are protected by third party copyright, trademarks and other intellec-tual properties.

©Sinarmas Sekuritas(2018). All rights reserved.