Embed Size (px)

Citation preview

REPORT of the AUDITOR GENERAL on the

PUBLIC ACCOUNTS OF GHANA -PUBLIC BOARDS, CORPORATIONS

AND OTHER STATUTORY INSTITUTIONS

FOR THE YEAR ENDED

31 DECEMBER 2012

To be one of the leadingSupreme Audit Institutions

in the world, deliveringprofessional, excellent, and

cost effective auditing

Our Vision

REPUBLIC OF GHANA

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations

and Other Statutory Institutions for the year ended 31 December 2012

REPORT OF THE AUDITOR-GENERAL ON THE

PUBLIC ACCOUNTS OF GHANA –

PUBLIC BOARDS, CORPORATIONS AND OTHER

STATUTORY INSTITUTIONS FOR THE YEAR ENDED

31 DECEMBER 2012

TABLE OF CONTENTS Para Page(s)

Para Page(s)

Introduction 1-4 1

PART I

Summary of significant findings and 5-21 2-6

recommendations

Audit opinion 22-28 6-8

PART II

Summary of findings and

recommendations by Ministries 29-138 9-35

PART III

Details of findings & Recommendations

No. Department Para Page(s)

Ministry of Health

1. Ghana College of Physicians & Surgeons 139-179 36-42

2. Nurses & Midwives Council 180-210 42-48

3. National Health Insurance Authority (NHIA) 211-272 48-60

4. Ghana Aids Commission 273-302 60-69

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations

and Other Statutory Institutions for the year ended 31 December 2012

Ministry of Chieftaincy & Culture

5. Kwame Nkrumah Memorial Park 303-333 69-74

6. National Theatre of Ghana 334-355 74-78

7. Ghana Dance Ensemble 356-368 78-81

8. W.E. Dubois Centre 369-409 81-87

9. Abibigromma Theatre Company 410-421 87-90

10. National Commission on Culture 422-437 90-93

Ministry of Education

11. University of Ghana 438-461 93-99

12. UoG – School of Pharmacy 462-473 99-101

13. UoG – School of Public Health 474-481 101-103

14. UoG – Medical School 482-494 103-106

15. UoG – Central Administration 495-503 106-108

16. UoG – School of Allied Health Sciences 504-512 108-110

17. UoG – School of Nursing 513-521 110-112

18. UoG – Dental School 522-530 112-114

19. Noguchi Memoral Inst. for Med. Research 531-539 114-116

20. Kwame Nkrumah Univ. of Sc. & Techno. 540-567 116-121

21. GIMPA 568-581 121-124

22. GIMPA Executive Conf. Centre (GECC) 582-584 124

23. Accra Polytechnic 585-602 125-128

24. National Service Secretariat 603-668 128-140

25. National Accreditation Board 669-683 141-144

26. University of Education – Winneba 684-702 144-148

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations

and Other Statutory Institutions for the year ended 31 December 2012

Ministry of Lands, Forestry & Mines

27. Office of the Administrator of Stool Lands 703-728 148-153

28. Land Registration Div. of the Lands Comm. 729-756 153-158

29. Public & Vested Lands Mgt. Div. of Lands

Commission 757-768 158-160

Ministry of Justice

30. Law Reform Commission 769-785 160-163

31. CHRAJ 786-822 163-169

Ministry of Interior

32. National Disaster Management Orgn. 823-831 169-171

Ministry of Communication

33. Postal & Courier Services Reg. Comm. 832-849 172-174

Ministry of Energy & Petroleum

34. Ghana National Petroleum Corporation 850-864 175-177

35. Energy Commission 865-887 177-181

36. National Petroleum Authority 888-903 181-184

37. Ghana Grid Company Ltd. 904-914 184-186

38. Takoradi Area Office 915-926 187-189

39. Kumasi Area Office 927-930 189-190

40. Bulk Oil Storage Transp. Co. Ltd (BOST) 931-939 190-192

41. Unified Petroleum Prime Fund 940-948 192-194

42. Energy Commission – Energy Fund 949-957 194-195

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations

and Other Statutory Institutions for the year ended 31 December 2012

Ministry of Finance & Economic Planning

43. Rural & Agricultural Finance Programme 958-976 196-200

44. Venture Capital Trust Fund 977-988 200-202

45. Ghana Cocoa Board 989-1004 202-206

46. Students Loan Trust Fund 1005-1014 206-208

47. Public Procurement Authority 1015-1023 208-210

48. National Insurance Commission 1024-1032 210-212

49. Bank of Ghana 1033-1071 212-219

Ministry of Information

50. Graphic Packaging Limited 1072-1087 220-223

51. Ghana Broadcasting Corporation 1088-1108 223-227

52. Graphic Communication Group Ltd. 1109-1124 228-230

53. National Film & Television Inst. 1125-1133 231-232

54. New Times Corporation 1134-1154 233-236

Ministry of Water Resources Works & Housing

55. Tema Development Corporation 1155-1168 236-239

56. Water Resources Commission 1169-1178 239-241

57. State Housing Company Limited 1179-1193 241-244

Ministry of Trade & Industries

58. Ghana Standards Board 1194-1205 244-246

59. Ghana Heavy Equipment Limited 1206-1221 246-249

60. Ghana Supply Company Limited 1222-1231 249-251

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations

and Other Statutory Institutions for the year ended 31 December 2012

Ministry of Roads & Highways

61. Ghana Highway Authority 1232-1245 251-254

Ministry of Local Govt. & Rural Devt.

62. Northern Regional Poverty Reduc. Prog. 1246-1261 254-257

63. Inst. of Local Govt. Studies 1262-1270 257-259

Ministry of Transport

64. Ghana Airports Company Limited 1271-1283 260-263

65. Ghana Maritime Authority 1284-1294 263-265

Ministry of Food & Agriculture

66. Small Farms Irrigation Project 1295-1311 265-268

Ministry of Environment, Sc. & Technology

67. Soil Research Inst. (CSIR) 1312-1321 269-271

68. Science & Tech. Policy Res. Inst. (CSIR) 1322-1330 271-273

69. Environmental Protection Agency 1331-1341 273-275

70. Inst. of Industrial Research (IIR)-

Council for Science & Indus. Research 1342-1350 276-277

71. Environmental Protection Agency

- National Environmental Fund (NEP) 1351-1363 278-280

72. Forestry Research Inst. of Ghana 1364-1375 280-283

73. Animal Research Institute 1376-1388 283-286

74. Crops Research Institute 1389-1405 286-289

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations

and Other Statutory Institutions for the year ended 31 December 2012

Other Agencies

75. National Pensions Regulatory Auth. 1406-1430 289-294

76. National Devt. Planning Commission 1431-1442 294-296

77. Internal Audit Agency 1443-1453 297-298

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations

and Other Statutory Institutions for the year ended 31 December 2012

Contributors

Ernst & Young

Kwame Asante & Associates

Osei Kwabena & Associates

Asamoah Bonsu & Co.

State Enterprises Audit Corporation

Kuffour & Associates

Egala, Atitso & Associates

Deloitte & Touche

Opoku Andoh & Co.

James Quagraine & Co.

Pannel Kerr Forster

MGI Labban Hyde

ADDS Consult

John Kay & Co.

Johnson Arkaah & Co

Sammy Tsahey & Associates

Morrison & Associates

Baker Tilly Andah & Andah

VT Consult

Odoro, Nyarko & Associates

Benning, Anang & Partners

Akus Consult

Baah & Associates

Boating Offei & Co

Robert Azu & Partners

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations

and Other Statutory Institutions for the year ended 31 December 2012

Ref. No. AG.01/109/Vol.2/62

Office of the Auditor-General

Ministries Block ‘O’

P. O. Box MB 96

Accra

Tel.: (0302) 662493

Fax: (0302) 662493/

(0302) 675496

10 September 2013

Dear Mr. Speaker,

REPORT OF THE AUDITOR-GENERAL ON THE

PUBLIC ACCOUNTS OF GHANA –

PUBLIC BOARDS, CORPORATIONS AND OTHER

STATUTORY INSTITUTIONS FOR THE PERIOD ENDED

31 DECEMBER 2012

In accordance with Article 187(5) of the 1992 Constitution of

the Republic of Ghana, I have the privilege to submit my annual

report on the Public Accounts of Ghana- Public Boards and

Corporations to you, to be tabled in the House.

2. The report is in three parts: Part I provides overall summary of

significant findings and recommendations. Part II gives summary of

findings and recommendations according to each Sector Ministry,

while Part III provides details of my findings.

3. Mr. Speaker, as part of the structures in place to promote good

governance, encouraging proper and prudent stewardship of the public

purse by Public Boards, Corporations and other statutory institutions

continues to be my priority. Promoting accountability, efficient and

effective use of the tax payers money remain my objective and it is

my hope that a time will soon come when all public servants will

spend resources with the same care exhibited in spending their own

TRANSMITTAL LETTER

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations

and Other Statutory Agencies for the year ended 31 December 2012

income. In this regard, the greatest professional satisfaction for me is

not only the disclosure of errors, waste and losses, but also the

willingness to correct unsatisfactory situations.

4. Mr. Speaker, I look forward to serving Parliament by

conducting independent and high quality audits on all the statutory

accounts. If my office is to play this vital role effectively as expected,

it must be provided with resources to do the job at the right time. To

this end, I once again wish to renew my appeal for the support of

Parliament in creating an enabling environment for the Audit Service

to achieve its mission and vision.

Acknowledgement

5. I am grateful to the contracted audit firms and my staff for the

execution of the annual audit programme.

6. I also acknowledge the co-operation and support of Chief

Executives and Chief Finan2ce Officers in the course of the audits.

7. Finally, I would like to thank the Public Accounts Committee

for their contributions to good governance and prudent stewardship by

reviewing my reports and reinforcing recommendations to the Public

Boards and Corporations for better financial management.

Yours faithfully,

AUDITOR-GENERAL

THE RT. HON. SPEAKER

OFFICE OF PARLIAMENT

PARLIAMENT HOUSE

ACCRA

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 1

Other Statutory Institutions for the period ended 31 December 2012

REPORT OF THE AUDITOR-GENERAL ON THE

PUBLIC ACCOUNTS OF GHANA –

PUBLIC BOARDS, CORPORATIONS AND OTHER

STATUTORY INSTITUTIONS FOR THE YEAR ENDED

31 DECEMBER 2012

Introduction

The audit of the accounts of Public Boards, Corporations and

other statutory Institutions for the period ended 31 December 2012

has been conducted in accordance with Article 187(2) of the 1992

Constitution of the Republic of Ghana.

2. The objective of the audit is to express an opinion on the

accounts submitted to me by each Public Board, Corporation and

other statutory Institutions after examination.

3. I also evaluated the adequacy of the system of internal controls,

compliance with relevant legislations, stated accounting policies and

applicable financial rules and regulations of these organizations.

4. Matters raised in this report are among those which came to my

notice during the period ended 31 December 2012. The observations

and recommendations arising out of the audits were discussed with

managements of the affected Institutions and comments received,

where appropriate, have been incorporated in this report. The report is

in three parts:

Part I provides a summary of the significant audit findings and

recommendations;

Part II provides the significant findings and recommendations

according to Sector Ministries; and

Part III deals with the details of findings and recommendations

2 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

PART I

SUMMARY OF SIGNIFICANT FINDINGS AND

RECOMMENDATIONS

5. Presented in Table 1 is the financial impact of the irregularities

with Table 2 showing the irregularities according to Sector Ministries.

Table 1: Summary of financial irregularities for the period ended 31

December 2012.

N

o

Type of

Irregularities

% Amount

GH¢

Amount

US$

Total Amount

GH¢

1 Outstanding

Debtors/ Loans/

Recoverable

charges

84.0 1,696,447,138.54 3,325.00 1,696,453,352.63

2 Cash Irregularities 5.8 114,953,516.99 745,455.00 116,346,697.84

3 Payroll

Irregularities

- 251,805.19 - 251,805.19

4 Procurement

Irregularities

2.5 50,492,451.95 - 50,492,451.95

5 Tax Irregularities 0.1 1,072,001.80 - 1,072,001.80

6 Stores

Irregularities

- 629,683.13 - 629,683.13

7 Contract

Irregularities

7.6 60,497,496.22 50,000,000.00 153,942,496.22

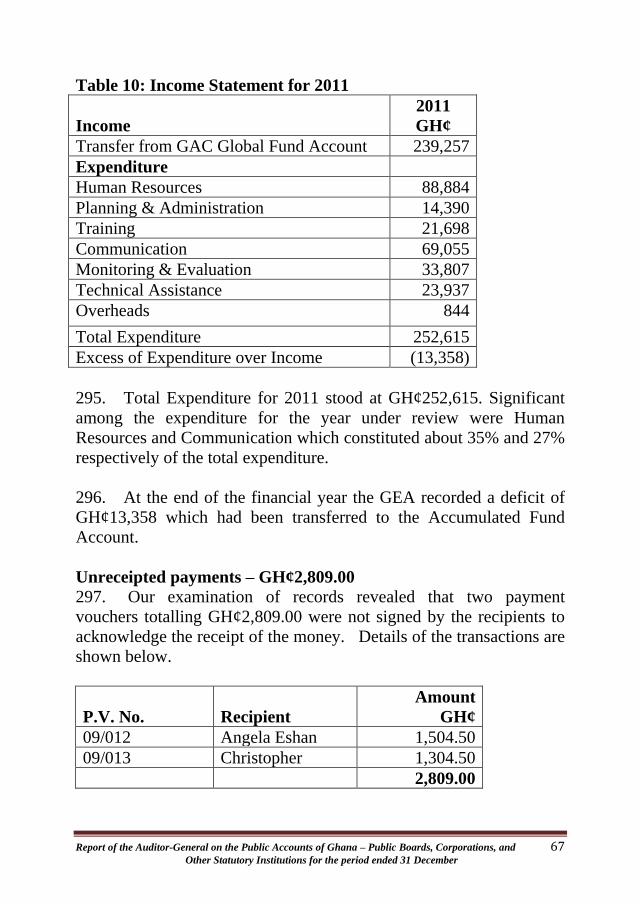

Total 100 1,924,344,093.82 50,748,780.00 2,019,188,488.76

6. Table 1 shows that the irregularities in monetary terms totaled

GH¢2,019,188,488.76 which include US$50,748,780.00 that was

converted into cedi at the prevailing exchange rate of GH¢1.8689 to

the US$1 as at 31 December 2012. My comments on the irregularities

are provided in the succeeding paragraphs.

Rep

ort

of

the A

udit

or-

Gen

era

l o

n t

he

Pu

bli

c A

cco

un

ts o

f G

ha

na –

Pu

bli

c B

oa

rds,

Corp

ora

tio

ns,

an

d

3

Oth

er

Sta

tuto

ry I

nst

itu

tio

ns

for

the p

eri

od

en

ded 3

1 D

ecem

ber

Tab

le 2

: S

um

mary

of

Fin

an

cial

Irre

gu

lari

ties

acc

ord

ing t

o S

ecto

r M

inis

trie

s

Ou

tsta

nd

ing D

eb

tors/

Loa

n

Reco

ver

ab

le c

ha

rges

Ca

sh

Irreg

ula

riti

es

Pay

roll

Irreg

ula

rit

ies

Procu

rem

en

t

Irreg

ula

riti

es

Ta

x

Irreg

ula

riti

es

Sto

res

Irreg

ula

riti

es

Co

ntr

act

Irreg

ula

riti

es

Secto

r M

inis

trie

s G

H¢

US

$

GH

¢

US

$

GH

¢

GH

¢

GH

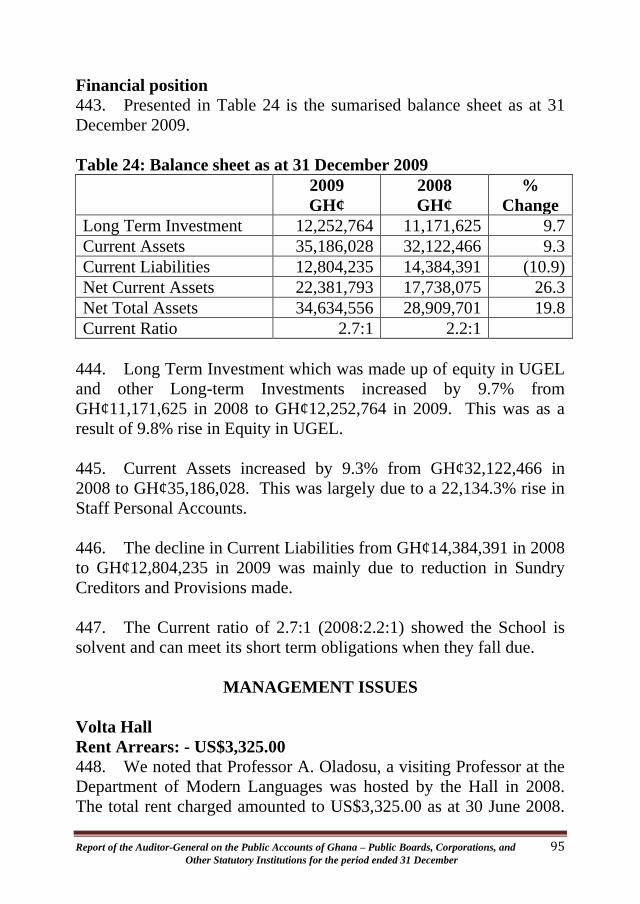

¢

U S$

GH

¢

GH

¢

US

$

Min

of

Hea

lth

298

,61

6,3

16

.77

- 1

1,8

94

,951

.44

- 6

,639

.63

31,2

22

.80

27,4

61

.33

- 2

0,3

12

.13

- -

Min

of

Chie

ftai

ncy

&

Cu

ltu

re

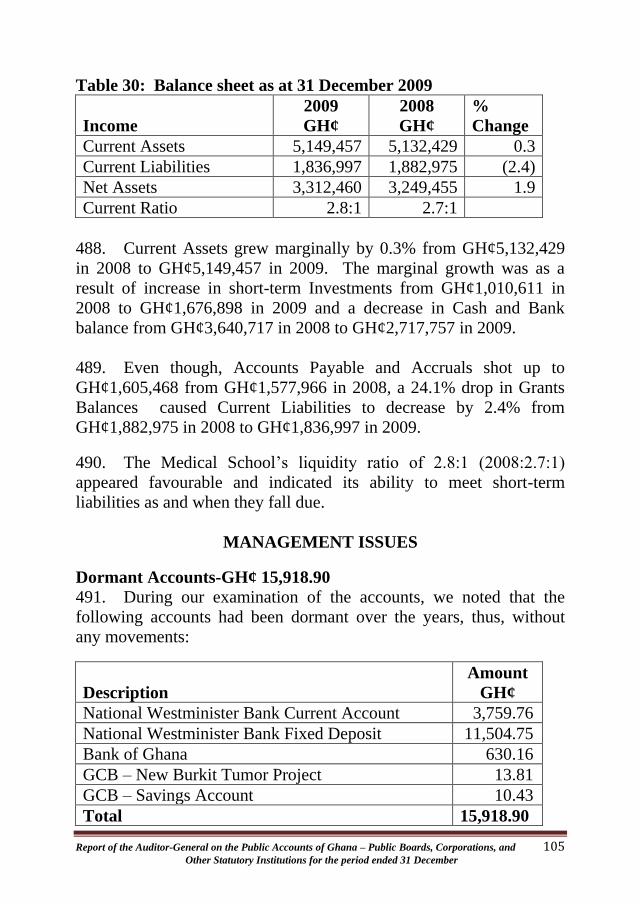

- -

83,8

28

.92

455

.00

3,4

87

.20

146

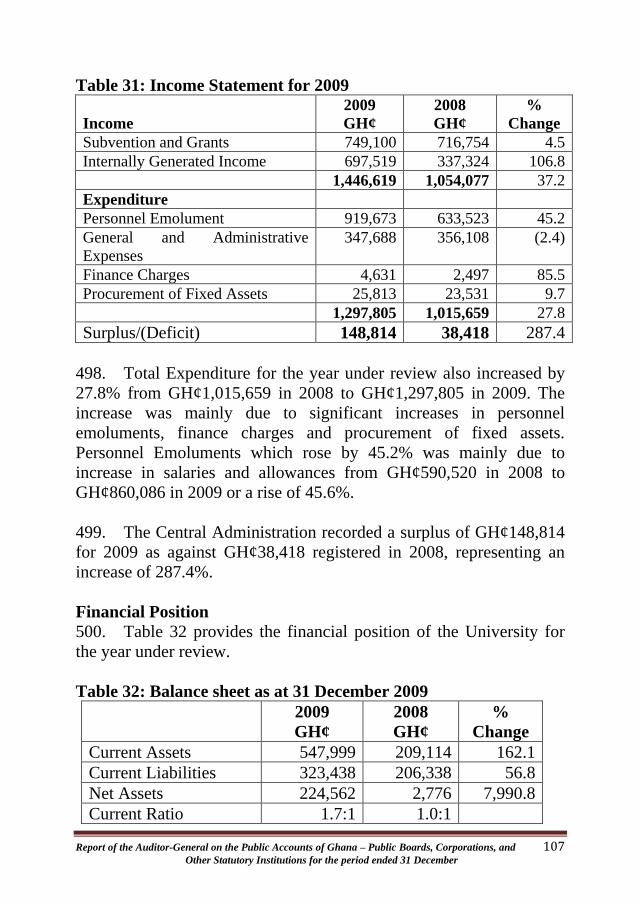

,49

9.6

6

51,8

76

.21

- 1

0,6

60

.00

- -

Min

of

Edu

cati

on

5

29

,12

9.7

6

3,3

25

.00

2,4

68

,46

1.4

2

- 1

12

,59

4.7

6

49,7

76

,354

.05

12,8

29

.92

- 4

0,4

00

.00

497

,49

6.2

2

-

Min

of

Lan

d,

Fo

rest

ry &

Min

es

- -

296

,75

8.7

5

- 3

9,5

31

.81

89,2

90

.59

798

.30

- -

- -

Min

of

Just

ice

- -

101

,61

8.0

0

- 8

9,5

51

.79

- 5

3,1

68

.20

- 3

50

,60

1.0

0

- -

Min

of

Inte

rior

- -

- -

- -

- -

- -

-

Min

of

Com

mun

icat

ion

s

- -

- -

- -

11,1

44

.21

- -

- -

Min

of

En

erg

y

2,1

56

,62

0.0

0

- 3

10

,49

4.9

6

- -

- -

- -

- -

Min

of

Fin

ance

&

Eco

n. P

lann

ing

1,3

92

,10

2,7

20

.36

- 8

3,0

22

,553

.00

745

,00

0.0

0

- -

625

,87

5.9

5

- -

60,0

00

,000

.00

50,0

00,0

00.0

0

Min

of

Info

rmat

ion

1

,820

,46

7.2

4

- 3

0,0

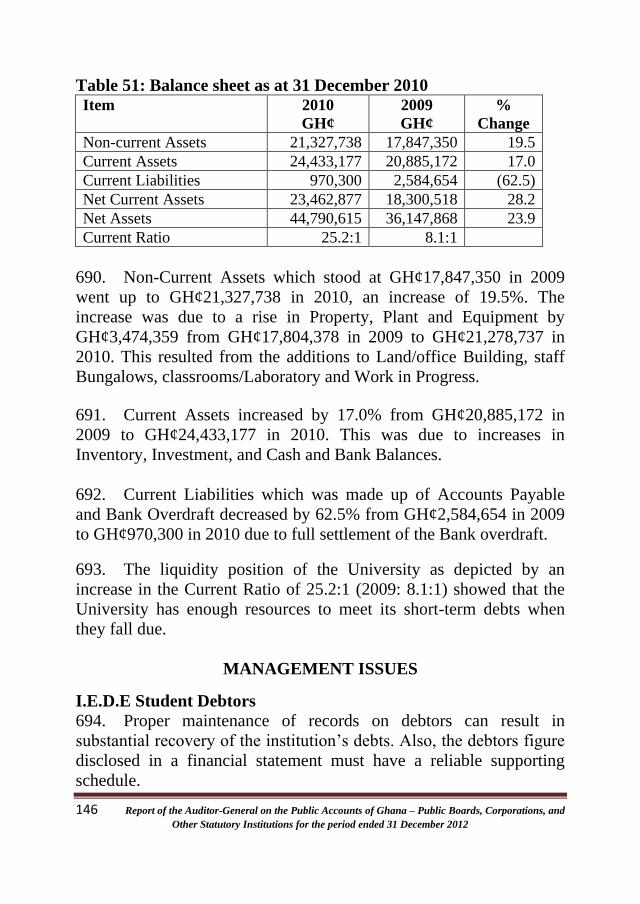

68

.00

- -

449

,08

4.8

5

- -

171

,71

0.0

0

-

Min

of

Wat

er

Res

ou

rces

Work

s &

H

ou

sin

g

- -

16,5

74

,567

.00

- -

- -

- -

- -

Min

of

Tra

de

&

Ind

ust

ries

1,2

13

,64

3.2

2

- 2

6,3

00

.00

- -

- -

- -

- -

Min

of

Road

s &

Hig

hw

ays

5,8

91

.19

- -

- -

- -

- -

- -

Min

of

Loca

l G

ovt

&

Ru

ral

Dev

.

- -

- -

- -

285

,46

5.1

8

- -

- -

Min

of

Food

&

Ag

ricu

ltu

re

- -

2,8

45

.00

- -

- -

- -

- -

Min

of

En

v.

Sci

ence

&

Tec

hn

olo

gy

2,3

50

.00

- 3

45

.00

- -

- -

-

- -

Oth

er A

gen

cies

-

- 1

40

,72

5.5

0

- -

- 3

,382

.50

- 3

6,0

00

- -

To

tal

1,6

96

,44

7,1

38

.54

3,3

25

.00

114

,95

3,5

16

.99

745

,45

5.0

0

251

,80

5.1

9

50,4

92

,451

.95

1,0

72

,00

1.8

0

- 6

29

,68

3.1

3

60,4

97

,496

.22

50,0

00,0

00.0

0

4 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

Outstanding debts/loans/recoverable charges –

GH¢1,696,453,352.63

7. These irregularities represent trade debtors, staff debtors and

outstanding loans. Absence of debt collection policy or credit

controller to retrieve the debt and managements apathy towards loan

recovery contributed significantly to the anomalies. Also improper

maintenance of records on debtors, absence of debtors aging analysis,

no documentation on loan agreements stipulating the terms and

conditions, failure to ensure that loans are repaid and managements

non compliance with rules and regulations accounted for these

irregularities.

8. I recommend that management of Public Boards, Corporations

and other statutory Institutions should strictly adhere to rules and

regulations pertaining to debts. They should put in place proper

policy on granting of loans and should ensure that adequate measures

are put in place to ensure repayment of loans on due dates to avoid or

mitigate the occurrence of bad debts.

Cash irregularities – GH¢116,346,697.84

9. Cash irregularities comprise misapplication of funds, over

estimation of funds needed, outstanding imprest, payments not

authenticated and cash shortages. These occurred as a result of poor

supervision, lack of control, management’s failure to review approved

budgets and failure of paying officers to demand receipts for

payments made. They also arose as a result of accountants’ failure to

properly file and keep records, management’s failure to ensure the

security and safety of vital documents, non monitoring of customers

payment schedules non maintenance of returned cheques register and

the lax of management in ensuring that accountants adhere to the

stipulation of the Financial Administration Act and other relevant

regulations coupled with poor accounting system.

10. I therefore urge management of Public Boards, Corporations

and other statutory Institutions to strengthen supervisory controls over

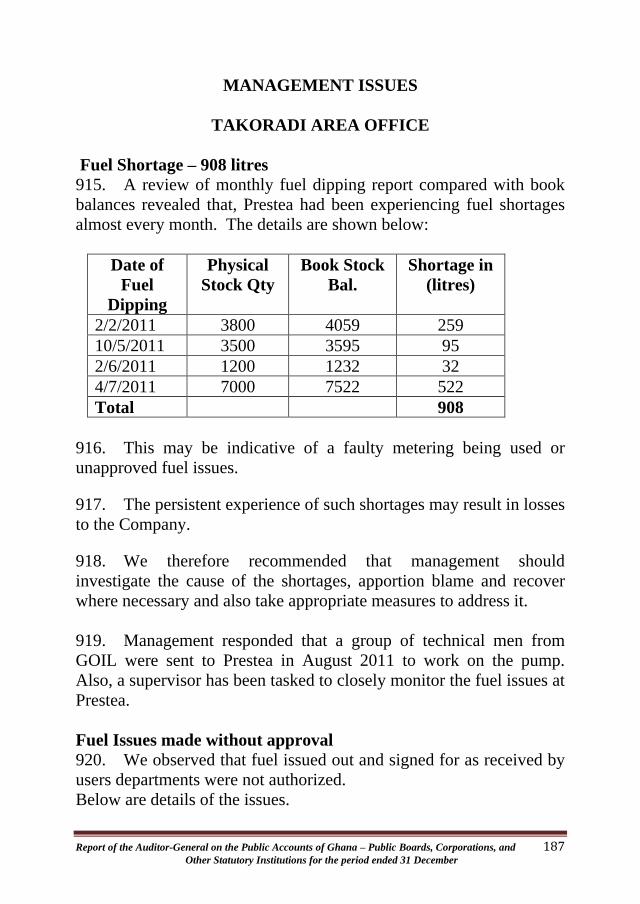

Accountants and ensure they adhere to the stipulations of the

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 5 Other Statutory Institutions for the period ended 31 December

Financial Administration Act and other relevant regulations. I also

recommend authentication of all payment vouchers, review of

approved budgets and prompt retirements of imprest.

Payroll irregularities – GH¢251,805.19

11. These lapses were caused by failure of management to exercise

due diligence and failure of officers in charge of payroll to review

payment vouchers to ensure that salaries were paid to only those who

were entitled.

12. They were also caused by management’s failure to notify

bankers to stop payments of unearned salaries. They mostly comprise

payments of unearned salaries to separated staff, non-payment to chest

of unearned salaries and payment to staff members who were not

entitled to receive those salaries.

13. I advise management of the affected institutions to promptly

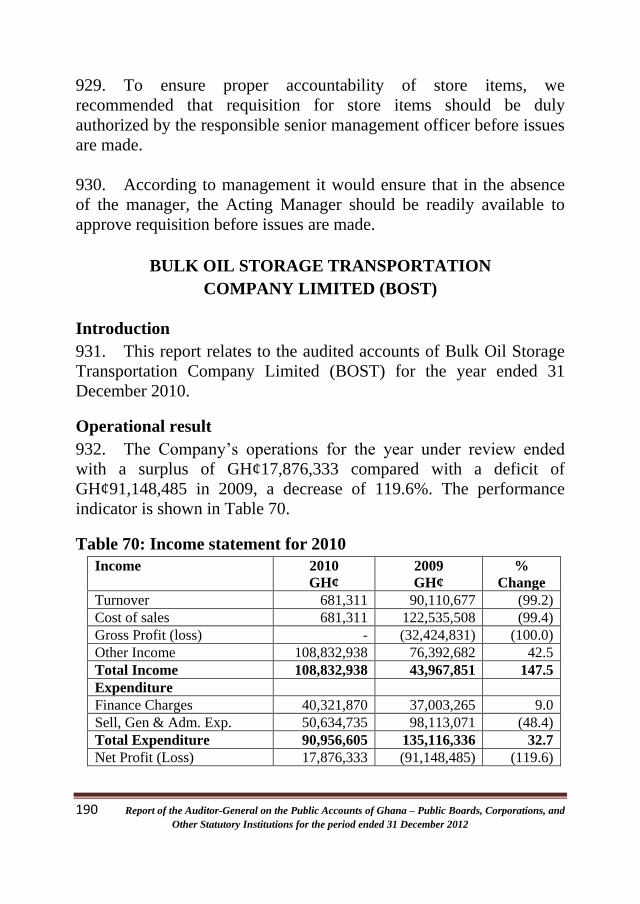

notify bankers of separated staff to withhold and pay to chest all

unearned salaries. I also recommend that officers in charge of payroll

should exercise due care in the discharge of their duties.

Procurement irregularities – GH¢50,492,451.95

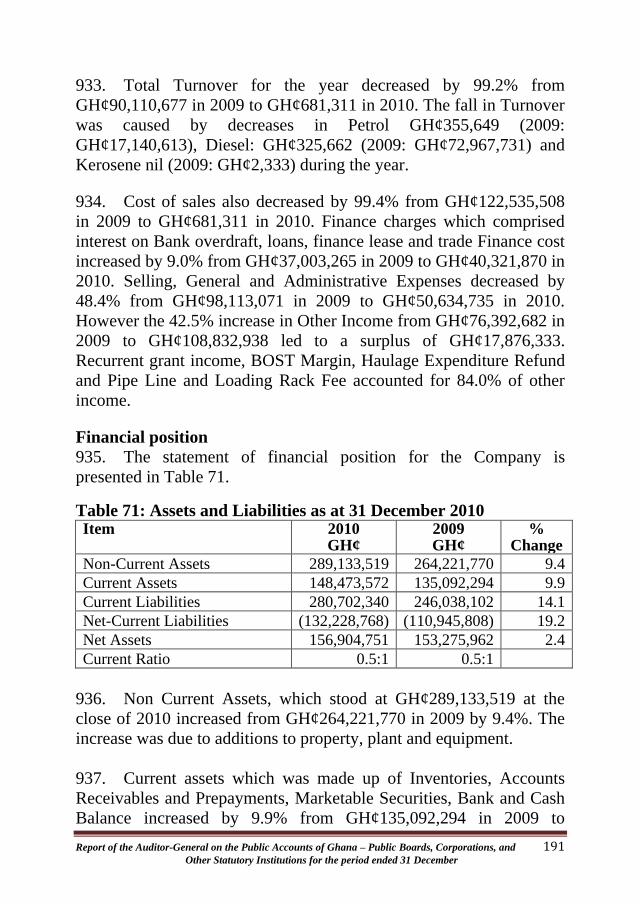

14. These irregularities occurred as a result of management

procuring goods and services without recourse to procurement

committees of the various institutions and going contrary to the

provision of the procurement Act.

15. I once again recommend that management of the respective

institutions should transact procurement dealings strictly in

accordance with the provisions of the Public Procurement Act, 2003

(Act 663).

Tax irregularities – GH¢1,072,001.80

16. Tax irregularities relates to misapplication of tax revenue,

failure to pay statutory deductions on due dates as required by law and

non- adherence to provisions in the tax laws. They also relate to

transacting of business with non VAT registered persons.

6 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

17. I recommend that Finance Officers should strictly adhere to the

tax laws to ensure that all tax revenue are promptly collected and paid

to the responsible revenue agencies.

Stores irregularities – GH¢629,683.13

18. These irregularities include, non documentation of store items

and fuel not accounted for, resulting from absence of store ledgers,

lack of awareness of officers assigned to store duties, inadequate

supervision, deficient and improvised log books and managements

failure to procure records.

19. I recommend the strengthening of controls over store items,

improved supervision and procurement of store ledgers. I also

recommend the training of officers assigned to store duties and the

strict adherence to the store regulations and Financial Administration

Regulations.

Contract irregularities - GH¢153,942,496.22

20. These mainly relate to non-performance of contract, variations

of conditions of contract without following procedures, non-

specification of mode of payments and the failure to deliver in

contract agreements and ineffective control over contracts.

21. I therefore urge management to strengthen controls over

contracts and comply with tendering procedures. I also recommend

that responsible officials for the overpayment of contract sum be

surcharged with the difference.

AUDIT OPINION

22. Most of the financial statements submitted for validation were

prepared under generally accepted accounting principles and my

office was satisfied in all material respects that the 96 audited

financial statements complied with the Ghana Accounting standards

and relevant legislation. In my opinion they presented a true and fair

view of the financial position and performance of the organizations.

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 7 Other Statutory Institutions for the period ended 31 December

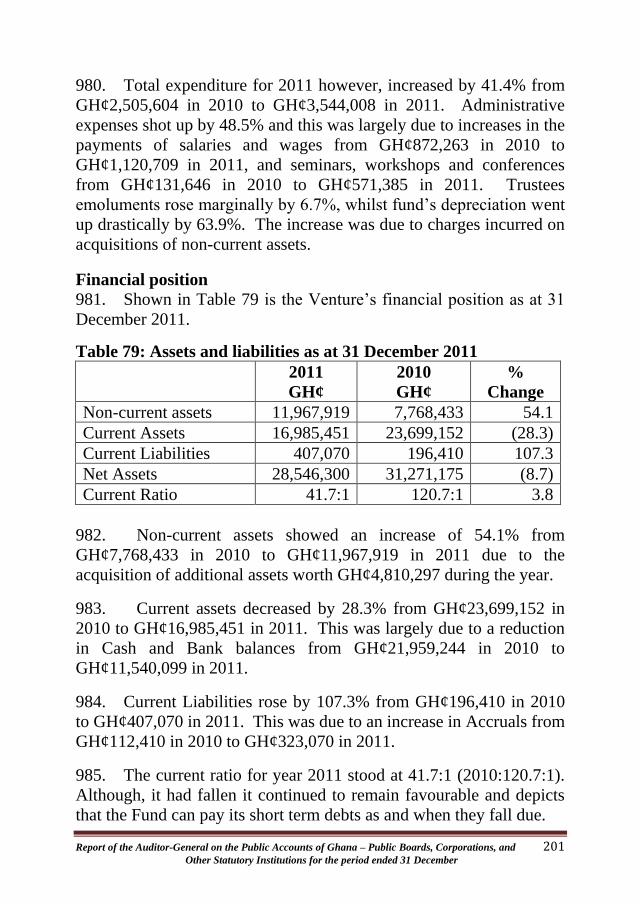

Accounts submission

23. In the year 2012, two out of a total of 74 Public Boards and

Corporations audited, failed to submit their financial statements at the

time of writing this report. As such I am unable to report on the

current status of the two defaulting organizations to provide

accountability assurance to Parliament.

24. The failure by organizations to prepare financial statements

stifles effective planning and decision making by stakeholders.

25. Once again, we noted that, the lack of accounting knowledge

by some accounting officers, staff constrains, apathy of some Chief

Executives and the failure of some governing Boards of these

organisations to ensure the preparation of the accounts caused delays

in the submission of financial statements or their non-submission.

26. There is still the need for organizations to improve upon their

processes for preparing their financial statements and annual reports

and pay more attention to compliance with the submission deadline of

31 March each year.

27. As stated in my previous reports, to enhance accountability and

timely stewardship of public funds, I recommend that Sector Ministers

as a matter of urgency should take remedial measures to ensure that

Public Boards, Corporations and Statutory Institutions:

Fill the position of Heads of Accounts Units, with personnel

with the requisite skill and experience;

Install computerized accounting software to accelerate the

production of financial statements for audit;

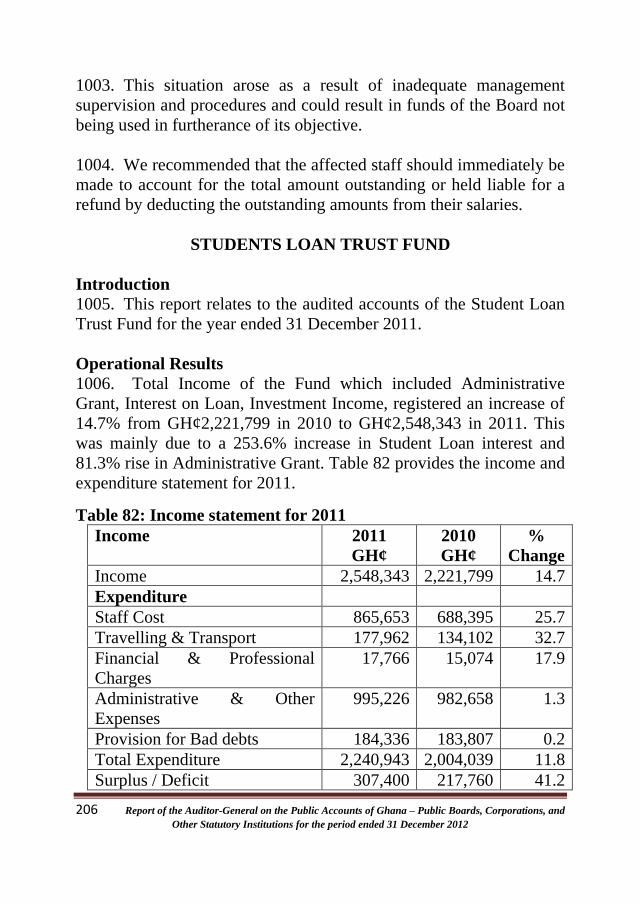

resource their accounts departments to enable them clear

the back log of outstanding accounts and submit them for

audit by 31 December 2012;

Ensure that governing Boards are responsive to their role;

8 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

Sanction any Chief Executive who fails to prepare and

submit for audit the organization’s financial statements by

the 31 March deadline; and

Sanction any official whose inaction resulted in these and

future irregularities to serve as a deterrent to others.

Conclusion

28. The operational result and financial positions of the Public

Boards, Corporations and other Statutory Institutions during the year

under review, could have been healthier if there had been effective

supervision of schedule officers. I reiterate my advice to management

to strengthen their Internal Audit Units to support and ensure sound

financial practice in accordance with the Internal Audit Agency Act

2003, (Act 658). I also recommend that management should institute

or strengthen the Audit Report Implementations Committees within

the organizations in accordance with Section 30 of the Audit Service

Act 2000 (Act 584) to ensure that recommendations made in this

report are duly implemented.

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 9 Other Statutory Institutions for the period ended 31 December

PART II

SUMMARY OF FINDINGS AND

RECOMMENDATIONS BY MINISTRIES

MINISTRY OF HEALTH

GHANA COLLEGE OF PHYSICIANS AND SURGEONS

29. We noted differences between figures in the draft financial

statements and the underlying records of the College. Expenditure

figures in the financial statement did not match actual expenditure

recorded in the cash book, hence making the statements misleading.

We referred the financial statements to the Accounts Officer to effect

the necessary corrections and re-submit them for validation, which has

not been done.

30. Eleven payment vouchers amounting to GH¢10,533.91 were

not presented for audit. We recommended that, the head of accounts

produces the payment vouchers for our examination or consider the

payments disallowed and the total amount refunded to the College’s

account. Management should also improve upon the filing and

custody of records.

31. Payments valued at GH¢4,508.78 were without official receipts

from suppliers of goods and services for authentication. We

recommended that the Accountant should obtain the official receipts

from the organizations involved and our office notified for

verification. Failure of which the Accountant should be surcharged

with the amount involved.

32. The Hospitality Section of the College made payments outside

Ghana amounting to GH¢141,885.12 without approval of the

Controller and Accountant General and prior approval of the Minister.

We recommended that management comply with the tenets of the

regulation and should in future seek the approval of the Controller and

Accountant General and the Minister before foreign payments are

made.

10 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

33. Management withheld taxes totalling GH¢16,507.00 in

contravention of Section 87(1) Part X of the Internal Revenue Act

2000. We recommended to management to remit the amount involved

without further delay.

34. Various items worth GH¢20,321.13 purchased during the

period under review did not pass through store records. To avert

diversion and other stores irregularities, we recommended that all

future purchases should be routed through stores to provide an

effective audit trail thereby ensuring accountability.

35. An unearned salary and allowance of GH¢5,891.80 was paid to

Freda Ocansey for the period of July and August 2011, after she had

resigned on 20 June 2011 due to management’s failure to ensure the

stoppage of her salary. We recommended that the amount of

GH¢5,891.80 be retrieved from Freda Ocansey and the Administrative

Manager sanctioned for his inaction.

36. An amount of GH¢57,613.23 was paid as salary arrears to

Benjamin O. Andoh who was dismissed and later re-instated from the

non tax revenue without approval from the Ministry of Finance. We

recommended that the amount of GH¢57,613.23 should be recovered

into the College’s account through the Controller and Account

General’s Department since the expenditure was salary related.

37. No environmental permit was obtained before operating the

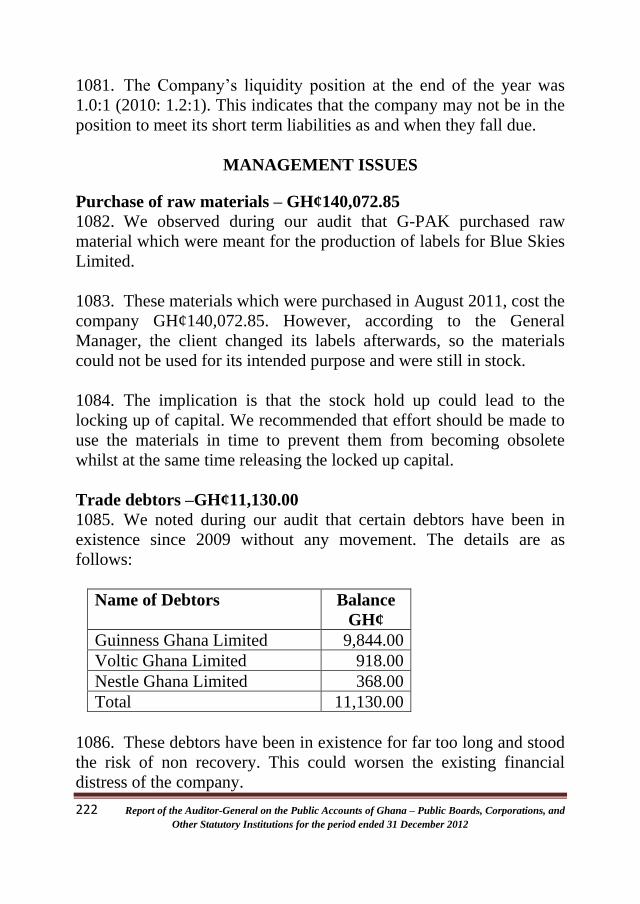

hospitality section which led to the payment of an unbudgeted penalty

fees of GH¢1,000.00 to the Environmental Protection Agency. We

recommended that in future the appropriate authorities should be

consulted before setting up any business.

38. Though the College had an Audit Report Implementation

Committee (ARIC) as required by Section 30 of the Audit Service Act

2000 (Act 584), most of the recommendations made in the previous

audit report were not implemented because the committee was not

responsive to its role. We recommended that management should

ensure that the ARIC performs its function as required by law.

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 11 Other Statutory Institutions for the period ended 31 December

NURSES AND MIDWIVES COUNCIL

39. An amount of GH¢2,000,000 released in July 2011 for the

completion of the suspended Office complex has been invested in

Treasury Bills instead of continuing with the project. We

recommended that management should apply laid down procedures

and abrogate the contract for non-performance and re-package the

remaining works for tendering and award to a competent contractor.

40. The Council paid an amount of GH¢31,222.80 to M/S Western

Automobile Center Ltd. in August 2009 for the supply of one Nissan

Urvan bus. As at the time of writing, the Company was yet to supply

the vehicle. The Council risks losing this money if not pursued. We

recommended that strenuous effort should be made to recover the

amount from the company.

41. The Council failed to remit Pay-As-You-Earn (PAYE) and

Social Security deductions of GH¢9,196.96 made from contract

(temporal) employees’ salaries for the period under review to the

appropriate authorities. Additionally, an amount of GH¢17,677.15 of

the statutory deductions which had accumulated over the years were

yet to be paid. The practice deprived the state of accrued tax revenue

and the employees were also denied the right of saving towards their

pension. We recommended that the accumulated statutory deductions

totalling GH¢26,874.11 should be remitted to the appropriate

authorities immediately to avoid penalties and employees’ losses.

NATIONAL HEALTH INSURANCE AUTHORITY

42. Levies collected by the Value Added Tax (VAT) service and

Social Security and National Insurance Trust (SSNIT) on behalf of

NHIA Scheme were not ceded to the Authority on time. As a result

CAGD owed a total amount of GH¢113,065,642 and

GH¢185,543,194.77 for 2008 and 2009 respectively and could

adversely impact on the smooth running of the Authority’s operations.

We recommended that management should consistently monitor the

remittances from the Revenue Agencies as well as the CAGD to

12 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

ensure that revenue accruing to the Health Insurance Fund are

remitted to the NHIA as and when they are due in accordance with the

provisions of Act 650.

43. Management failed to withhold the required 5% tax on

payments made for works and services totalling GH¢146,503 resulting

in a loss of tax revenue of GH¢7,325 accruing to the state. We

recommended that management should adhere to Section 88(1) of

Act 592 which requires withholding tax agencies to be held liable and

pay to the Commissioner any withheld tax and advised future

compliance with Section 84(2) of Act 592 for the avoidance of

penalties.

44. Some receipts obtained totalling GH¢131,409 in 2008 and

2009 from Samatra Hospital, a service provider for claim payment to

them had a different name as Samatra Hospital staff Welfare

Association rather than Samatra Hospital. We recommended that

internal control in cash management be strengthened. Also,

management is advised to take the appropriate legal actions against

the officials involved in this act to retrieve the misappropriated funds.

45. A total amount of GH¢56,418 was disbursed to various

facilities without the approval of the Board or District Co-ordinator.

We recommended that management should ensure that appropriate

levels of authorization and approval are sought before payments are

effected.

46. We observed a difference of GH¢1,166,183 between revenue

reported by the Denu Scheme as transfer from Head office and the

amount reported by the Head office as transfers to the scheme. We

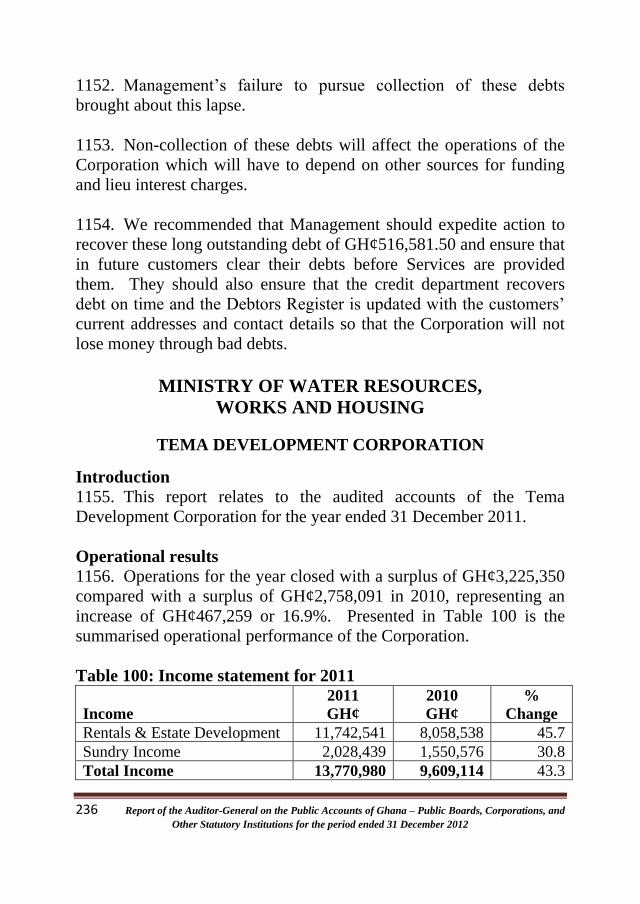

recommended that these differences should be investigated and the

required remedial action taken.

47. We did not sight Gambaga Mutual Health Insurance Scheme

receipts of an amount totalling GH¢70,295 being payment made to

some service providers in 2008. To prevent disputes which might

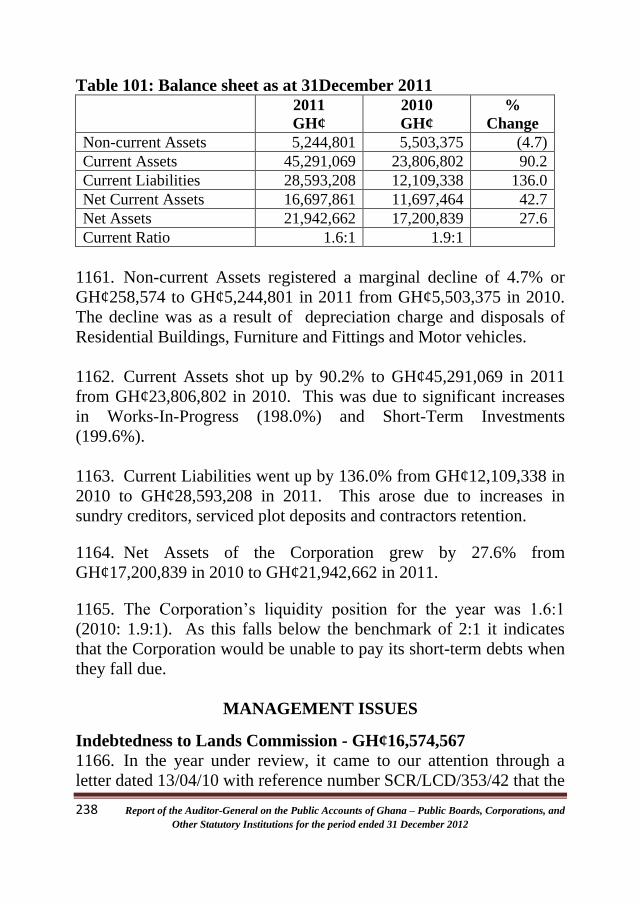

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 13 Other Statutory Institutions for the period ended 31 December

result in double payment, we recommended that management should

ensure that receipts are obtained after every payment. All supporting

documents should also be attached to payment vouchers raised.

48. An amount of GH¢158,526 purported to have been transferred

by the NHIA to the Nanomba North Mutual Health Scheme could not

be traced to the bank statement of the scheme. We recommended that

head office liaises with the scheme to have this difference investigated

and reconciled. Also, the officer in charge of the transfer of the funds

must be held liable if the loss of funds is established.

49. GH¢900,000 was withdrawn from the claims account of the

Oguaaman Mutual Health Insurance Scheme and deposited into a

purported investment account. However, no evidence of the

investment of this amount was made available for our review. We

recommended that management should ensure that these transfers are

followed up to where ever they have been invested. All investments

and interest accrued must be retrieved and paid into the scheme

account. We also recommended that in the event of any losses the

responsible officials should be held liable.

50. An amount of GH¢617,393 purported to have been transferred

from the NHIA to Wa Municipal Mutual Health Insurance Scheme

could not be traced in the scheme’s cash book and bank statements.

We recommended that regular reconciliation should be done between

the Authority and the Scheme to rectify such differences and the

officer in charge of the transfers must be held liable for any losses.

51. The Authority had made a total payment of GH¢3,598,750 on

behalf of some Mutual Health Scheme providers for some claims over

the period under review. However, these amounts were not accounted

for by the schemes. We recommended that the NHIA should always

advice the schemes of any payments made to any service provider on

behalf of the schemes. The procedure for direct payment of claims to

service providers should be streamlined such that the process is

initiated from the schemes.

14 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

52. We noted during our review a difference of GH¢2,482,130

between transfers recorded by Bantama Mutual Health Insurance

Scheme and the NHIA. The amount reported by the NHIA as

transferred to the scheme did not agree with the receipts verified at the

scheme. We recommended that the NHIA and the management of the

Bantama NHIS liaise to investigate this difference and have them

reconciled. Any losses should be accounted for by the responsible

officials.

53. Claims paid to some service providers amounting to

GH¢246,418 were made prior to vetting of the claims. We

recommended that measures be put in place to ensure claims are fully

vetted before funds are paid out so as to promptly identify and correct

any anomalies. The NHIA should also put in place measures to ensure

there are no undue delays in the payment of claims that would

necessitate the payment of claims in advance pending the vetting

process.

GHANA AIDS COMMISSION

German International Cooperation (GIZ)

54. Management of the Project failed to withhold taxes totalling

GH¢1,072 from payments made to suppliers of goods and services. To

improve inflows into the Consolidated Fund, we recommended that

management should comply with the relevant provisions of the tax

law; otherwise responsible officers would be surcharged accordingly

for any future losses.

Ghana Employers Association (GEA), Accra

55. Payment vouchers totalling GH¢2,809 were not signed by the

recipients to acknowledge the receipt of the payment. We therefore

advised management to ensure that these and subsequent payments are

receipted by beneficiaries otherwise the paying officer should be held

liable for a refund.

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 15 Other Statutory Institutions for the period ended 31 December

MINISTRY OF CHIEFTAINCY AND CULTURE

KWAME NKRUMAH MEMORIAL PARK

56. Cash payments ranging between GH¢1,050.00 and

GH¢3,519.58, amounting to GH¢195,981.50 was made to suppliers of

goods and services during the two years under review resulting in the

loss of GH¢9,799.08 in withholding tax revenue. We recommended

that management should desist from the practice, failing which

culpable officers would be surcharged with any future loss of tax

revenue.

57. The Accountant failed to produce the bank statements for

Internally Generated Funds (IGF) amounting to U$455.00 allegedly

lodged at Bank of Ghana (BoG) between May and July 2010 and

reported as revenue in the 2010 financial statement for confirmation.

We recommended to management to communicate with BoG and

confirm the existence of the account and our office informed for

verification.

58. Special imprest amounting to GH¢5,700.00 advanced in

November 2010 and September 2011 to Officers for NAFAC 2010

and 2011 Founder’s day celebration respectively have not been retired

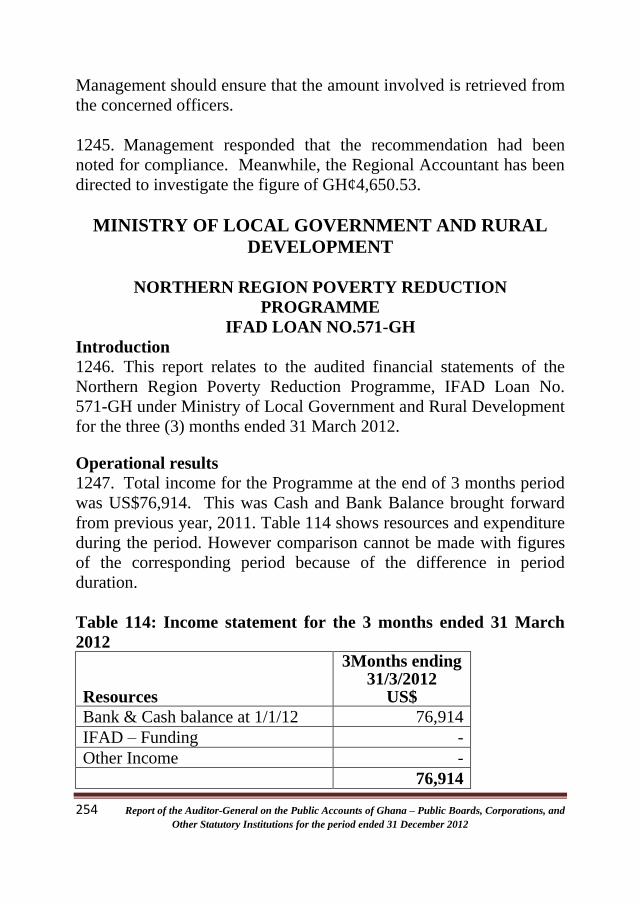

as at the time of reporting. We advised the Accountant to ensure full

retirement of the imprest or the Officers be made to refund the various

amounts given to them.

59. Purchases totalling GH¢146,499.66 were made without

obtaining at least three quotations from suppliers. We advised that in

future, management should either seek prior approval from the Public

Procurement Board before engaging in single source procurement or

obtain at least three different quotations for the selection of the most

responsive quote to obtain transparency and fair pricing.

60. Management transacted businesses totalling GH¢146,497.66

with non-VAT registered suppliers. The act deprived government of

GH¢21,974.64 in VAT revenue. We advised management to strictly

adhere to the provisions of Act 654.

16 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

NATIONAL THEATRE OF GHANA (NTG)

61. Withholding taxes amounting to GH¢2,720.43 have not been

paid to the Commissioner, Domestic Tax Revenue Division (DTRD)

of the Ghana Revenue Authority (GRA). We also noted under

deduction of withholding tax of GH¢742.50 on sitting allowances paid

to Board members. To improve inflow of funds into the Consolidated

Fund, we advised management to ensure that the total tax of

GH¢3,462.50 is paid to the DTRD without delay and also put in place

arrangements to recover the amount of GH¢742.50 from the Board

members.

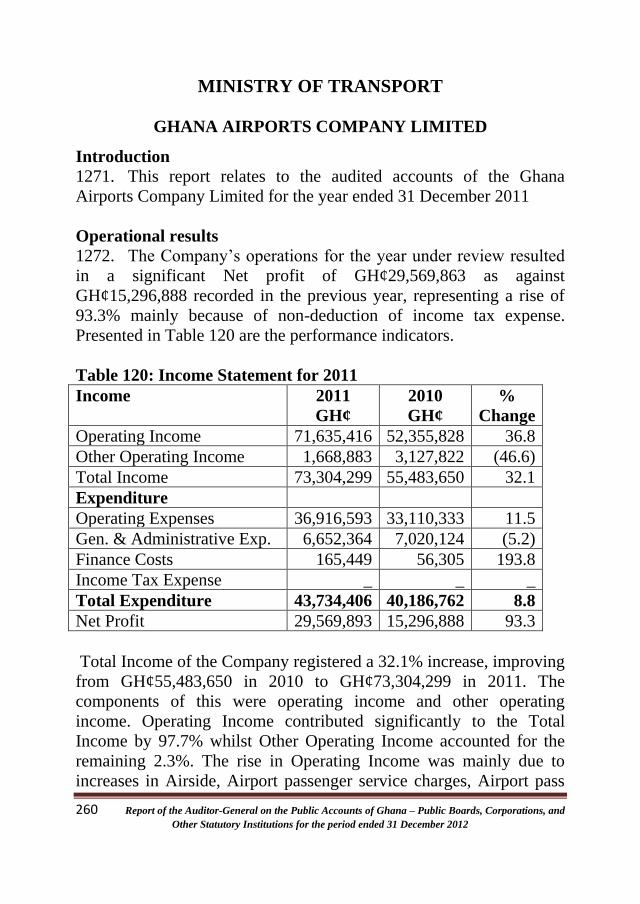

62. Payment vouchers valued at GH¢21,753.85 supposedly raised

for activities within the period under review were not presented for

authentication. Management was advised to ensure that the payment

vouchers are provided together with the supporting documents for our

verification or the amount treated as unjustified expenditure and

recovery made accordingly.

63. Fuel worth GH¢3,800.00 allegedly issued to the driver of

vehicle No. GR 2019 T for official use could not be accounted for as a

result of non-maintenance of a log book. We recommended that

management should procure a vehicle log book for the above

mentioned vehicle and ensure that details of fuel issued are duly

recorded by the driver and officers using the vehicle to certify

journeys undertaken to ensure accountability and efficient use of fuel.

Meanwhile, management should ensure that the fuel amounting to

GH¢3,800.00 is accounted for, failing which the amount should be

recovered to NTG’s bank account.

GHANA DANCE ENSEMBLE

64. Fuel coupons amounting to GH¢2,260.00 issued to vehicle

number GT1862 Y for official use, were not fully accounted for in the

drivers log book. We recommended that, adequate control measure

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 17 Other Statutory Institutions for the period ended 31 December

should be instituted to ensure that fuel usage is properly managed for

the benefit of the Ensemble.

W. E. DUBOIS CENTRE

65. Management made cash instead of cheques payments

amounting to GH¢152,827.35 in settlement of its obligations. This

practice resulted in the loss of GH¢7,641.37 in withholding tax

revenue. We recommended to management to desist from the practice

and adhere to the provision of the FAR.

66. The Accountant made payments amounting to GH¢52,529.57

to various suppliers and service providers without obtaining official

receipts. We could therefore not determine whether the intended

beneficiaries received the amount involved. For proper accountability

and transparency in the utilisation of public funds, we advised

management to ensure that the paying officer obtains the receipts for

these and subsequent payments, failing which the amount should be

recovered.

67. The Cashier could not account for non tax revenue of

GH¢404.00 and $687.38 collected during the period reviewed,

depriving the Centre of the use of the money. We advised

management to recover the amounts from the Cashier and improve on

internal controls and managerial reviews to prevent a recurrence of the

anomaly.

68. Management failed to remit to the Domestic Tax Revenue

Division (DTRD) of the Ghana Revenue Authority (GRA) taxes

amounting to GH¢566.63 withheld from payments totalling

GH¢11,332.60 made to suppliers of items purchased. In another

development, two companies were paid a sum of GH¢50,070.00 for

which the withholding tax of GH¢2,503.50 was not deducted. We

recommended to management to ensure prompt recovery of the tax

and payment of all withheld taxes in order to contribute to the revenue

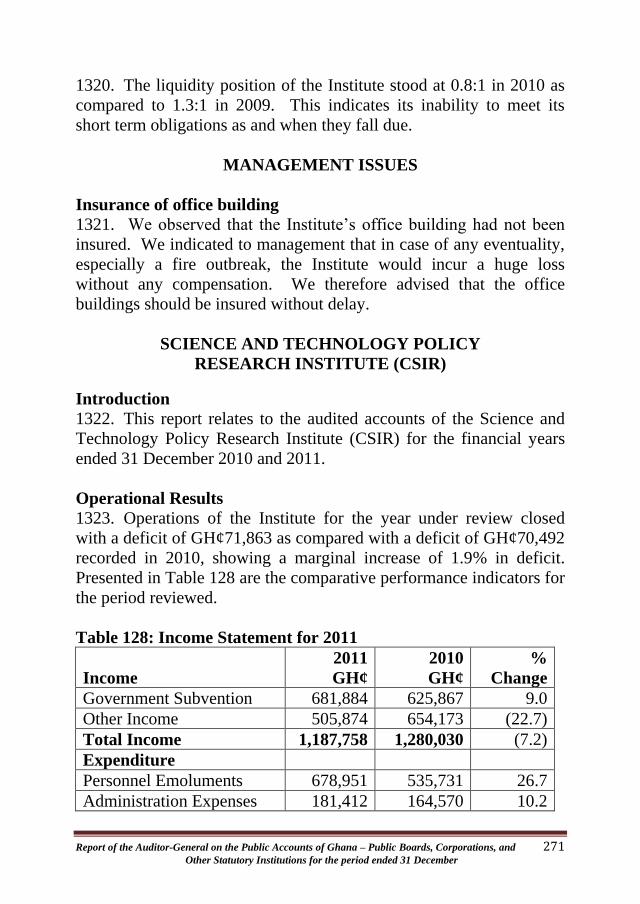

generation drive of the state and to avoid sanctions.

18 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

69. Management transacted business totalling GH¢22,668.49 with

non-VAT registered suppliers, depriving the state of VAT revenue

amounting to GH¢3,400.27 as a result. We advised management to

adhere to the provision of Act 654.

70. Management’s failure to promptly inform the Controller and

Accountant General’s Department for the stoppage of the salary of

Mr. Ayang Oliver who retired on 4 May 2011 resulted in the payment

of unearned salary of GH¢358.26. We advised prompt recovery of the

amount from the ex-employee or his bankers to government chest.

71. The Centre’s official drivers failed to record fuel worth

GH¢1,181.00 purchased in their respective vehicle log books. We

recommended strict supervision over drivers and the prompt logging

of fuel purchased for the official cars.

ABIBIGROMMA THEATRE COMPANY

72. Due to management’s failure to immediately notify the

Controller and Accountant General’s Department (C&AGD) to delete

the names of separated staff from the payroll, two former employees

were paid a total of GH¢3,128.94 as unearned salaries contrary to

Regulation 298 of L.I. 1802. We recommended that management

recover the amount from the affected officers and lodge same into the

consolidated fund, failing which the amount involved should be

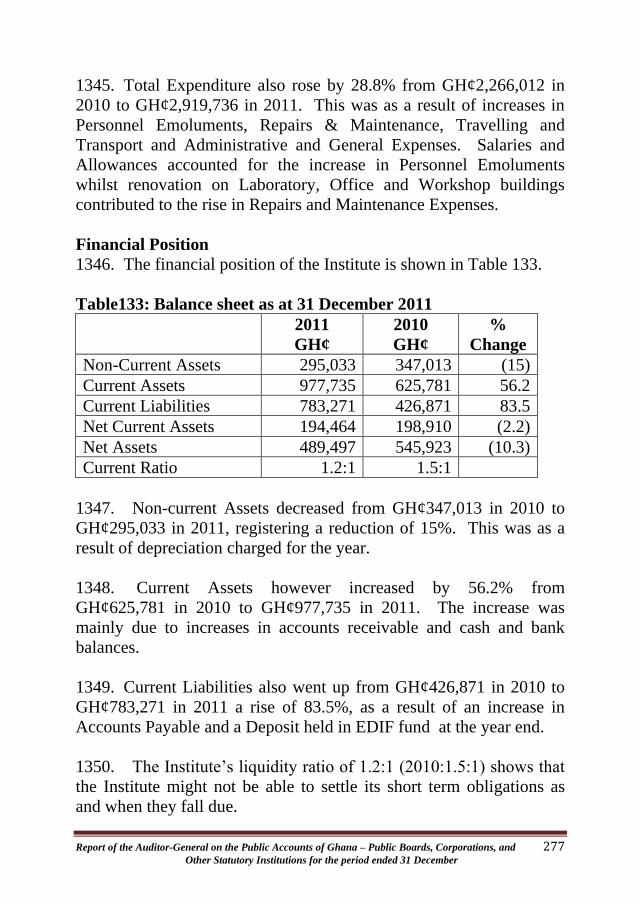

surcharged to the spending officer.

NATIONAL COMMISSION ON CULTURE

73. Goods and services worth GH¢20,496.00 were purchased from

non VAT registered persons which resulted in the loss of

GH¢3,074.40 in VAT/NHIL revenue accruing to the state. We

advised management to comply with the dictates of the above cited

regulation; otherwise defaulting officers would be surcharged with

any loss of government revenue in future.

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 19 Other Statutory Institutions for the period ended 31 December

74. Though vehicle log books were allocated to pool vehicles,

drivers failed to record fuel coupons worth GH¢1,250.00 issued for

official use as a result of lax supervision. To ensure judicious use of

fuel, we recommended that the Transport Officer should step up

supervision and the drivers made to account for the fuel coupons

failing which the amount should be recovered into the Commission’s

bank account.

MINISTRY OF EDUCATION

UNIVERSITY OF GHANA

VOLTA HALL

75. Visiting Professor at the Department of Modern Languages

was hosted by the Hall in 2008. The total rent charged amounted to

US$3,352 as at 30 June 2008. However, the rent due had still not

been settled as at 31 December 2009. We recommended that

management of the Hall should follow up to the Department of

Modern Languages and ensure that the rent due is settled.

Institute of Statistical Social and Economic Research

76. The Institute failed to withhold taxes amounting to GH¢3,303

on allowances paid to research assistants, members of staff and other

personnel engaged by the Institute to work on their projects. We

recommended that withholding taxes should be deducted from all

payments made to officers and the deducted taxes paid to the Internal

Revenue Service.

Basic School

77. Pupils indebtedness to the school amounted to GH¢53,202 as at

31 December 2009. We recommended that management of the school

should ensure that arrears of fees are collected promptly from fee

defaulters before final examinations are written. Also, overdue and

doubtful debts should be written off.

20 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

Guest Centre

78. A total amount of GH¢169,922 was owed the Centre as at 31

December 2009. Out of this amount three (3) Units of the University

constituted about 50% of the total debts owed the Centre. We

recommended that management should expedite action on the

recovery of the debts to enhance the Centre’s liquidity position.

KWAME NKRUMAH UNIVERSITY OF SCIENCE

AND TECHNOLOGY

College of Art and Social Science

79. A total of GH¢41,724 advanced to staff members of the various

faculties to organize specific programs had not been accounted for.

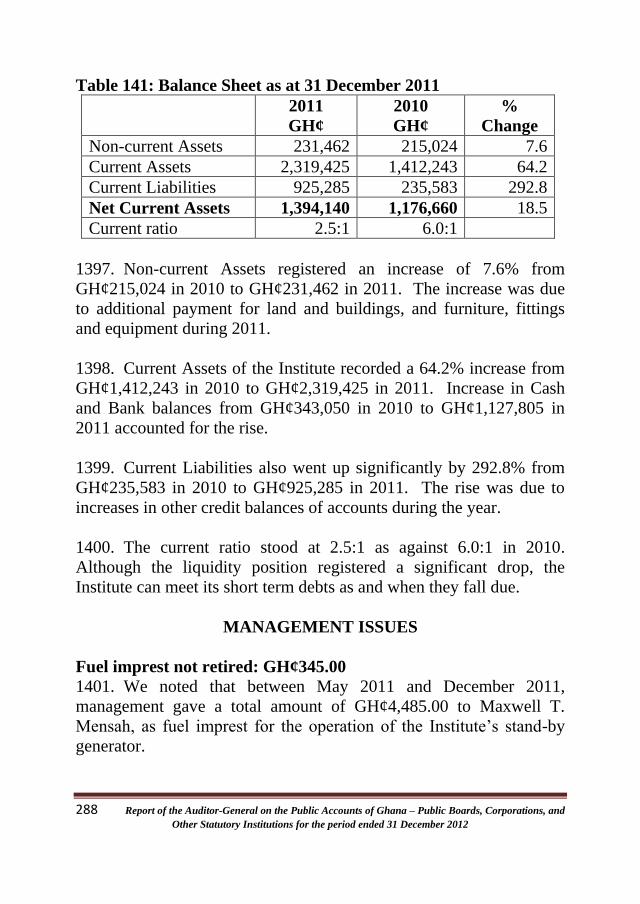

We advised management to ensure that efforts are made to get the

officers concerned to account for the advances and/or refund them

through their monthly salary deduction.

Basic School

80. An amount of GH¢40,400 was used to buy assorted exercise

books from the University Printing Press to be distributed to the basic

schools. However, we were unable to confirm whether the said

amount had been used for their intended purpose because our request

for the list showing how the distribution was made proved futile. We

recommended that management as a matter of urgency, investigate

this issue and establish procedures to avert future occurrence.

81. Additionally, loans totalling GH¢1,885 have been given to the

Students’ Representative Council (SRC) at the Provost’s office and no

effort was made for the repayment of the loan. We therefore advised

management to retrieve the amount from the SRC.

ACCRA POLYTECHNIC

82. An officer who resigned on 1 August 2011 had his name

deleted from the payroll on 1 January 2012, a delay of five months

which resulted in the payment of unearned salaries of GH¢3,035.44.

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 21 Other Statutory Institutions for the period ended 31 December

We recommended that efforts be made by management to recover the

total amount of GH¢3,035.44 from the ex-employee, pay same to

Government chest and obtain a Treasury Receipt for our verification.

83. Two officers who were granted three years study leave each

with pay failed to serve the required five-year bond term before

leaving the School. The officers also failed to refund a total of

GH¢109,559.32 being salaries and allowances paid them while

studying in contravention of the bond requirements. We recommended

to management to take the necessary steps to recover the amount with

interest at the prevailing bank rate from the officers or their guarantors

and pay same to government chest without further delay.

NATIONAL SERVICE SECRETARIAT

84. Management failed to refund to chest a total amount of

GH¢49,679,748.05 representing excess funds released for payment

of personnel allowances and overpayment of allowances recovered

contrary to Regulation 45 of the Financial Administration Regulations

( FAR) 2004 (L.I 1802). We recommended that the above stated

amount and future overpayment recoveries should be paid to chest

without any further delay. At the instance of the audit a request was

made to the Controller and Accountant General for an account number

for payment of the excess funds.

85. We did not sight the payment vouchers for 122 payments

totalling GH¢1,314,173.01. Such act undermines controls provided

for in disbursement of funds. We recommended that management

produce the payment vouchers or the responsible officials should

refund the amount involved into the Secretariat’s account.

86. Forty-one payment vouchers totalling GH¢218,074.78 were not

properly acquitted with adequate and appropriate documentations. The

occurrence was due to the Accountant’s failure to ensure that payment

vouchers were supported with the relevant documents for

authentication. We recommended that the Accountant produces the

necessary documents or refund the amount involved into the

Secretariat’s account.

22 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

87. Imprest totalling GH¢409,292.35 granted to members of staff

to run various programmes was not accounted for even though the

programmes had been completed. This was made possible because no

measures had been put in place to enforce the prompt retirement of

imprest. We recommended that the officers involved should be made

to account for the moneys received without any further delay or the

amount should be adjusted to the personal accounts of the imprest

holders in accordance with Section 288 (1) of FAR.

88. Management failed to promptly remit withholding taxes of

GH¢9,527.12 to the Domestic Tax Revenue Division (DTRD) of the

Ghana Revenue Authority (GRA). We recommended that

management adhered strictly to the above stated regulation and remit

the amount and any future tax withheld without delay to the

Commissioner of the DTRD for the avoidance of penalties.

89. Goods worth GH¢66,206.00 were procured by single sourcing.

We also noted instances where purchases were not supported with

relevant documents among other irregularities. We recommended that

management complies strictly to the laid down procedures as the non-

compliance with relevant provisions of Act 663 blurs transparency

and could compromise value for money.

90. A contract awarded for the printing of ‘T’-shirts worth

GH¢30,400.00 was fragmented into nine lots and awarded to one

contractor thus circumventing the procurement procedures. We

recommended that management comply strictly with the Procurement

Act in order to obtain value for money in its procurement dealings.

91. Procedures for variation of contract were not fully complied

with as a water bottle project awarded at an initial cost of

GH¢472,672.80 was irregularly varied to GH¢856,597.67. The

variation which represented 81% of the original contract amount was

attributed to additional works. We recommended that the additional

works should be repackaged separately and awarded in accordance

with the existing laws.

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 23 Other Statutory Institutions for the period ended 31 December

92. Incomplete records were maintained for the Farm Projects.

Consequently, out of a total amount of GH¢593,744.23 invested in the

farms, management produced records to account for an amount of

GH¢82,741.86 leaving a balance of GH¢511,002.37 unaccounted for.

We also noted that management failed to carry out feasibility studies

to inform the investments in the farms. We recommended that in

future, management should ensure the viability of projects before

sinking funds into them. We also advised management to comply with

FAR 1, prepare and present the consolidated farm account for audit.

We further advised management to in future maintain proper records

and books of accounts on the farm to avert such recurrences.

NATIONAL ACCREDITATION BOARD

93. A contract signed with Somuah Information Systems Company

Limited on 24 December 2010 for the design, development and

implementation of a comprehensive Accreditation Management

Information System (AMIS) which was to be completed by 13 June

2012 was 40% complete as at 31 June 2012. To forestall any

consequential cost overrun, we recommended that management

should urge the consultant to come out with a stringent time table for

the early completion of the work, failing which cost fluctuations

should be borne by the company.

UNIVERSITY OF EDUCATION WINNEBA

94. Student debtors from Kumasi and Accra Centers totaled

GH¢108,458 for the period reviewed. We recommended that

management should write to all student debtors to pay their debts or

withhold their certificates till their debts are paid.

MINISTRY OF LANDS, FORESTRY AND MINES

OFFICE OF THE ADMINSTRATOR OF STOOL LANDS

95. A revenue collector, Mr. Richard Anin Mensah was interdicted

and surcharged with GH¢2,500.00 in 2010 for printing and using fake

24 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

receipt books in the collection of revenue resigned in September 2011

without paying the amount. We recommended that management

should conduct a thorough investigation into the case, institute

measures to forestall a recurrence and recover the amount of

GH¢2,500.00 from the defaulting revenue collector.

96. Seven revenue collectors delayed for periods ranging between

12 and 199 days in paying revenue of between GH¢108.50 and

GH¢160,670.72 collected to the Chief Collector in contravention of

FAR 15(1). To forestall revenue leakage, we recommended that

management should step up supervision over revenue collection and

ensure that the Revenue Collectors comply with the provision of the

financial regulation stated. We also recommended that interest at the

prevailing bank rate be charged against defaulting officers as

disciplinary action to prevent any future delays and to serve as a

deterrent to others.

97. Due to delayed deletion of names from the payroll, 16

separated staffs were paid unearned salaries totalling GH¢41,431.81

during the period under review. We recommended that efforts be

made by management to recover the unearned salaries to Government

chest and produce evidence to confirm the refund.

LAND REGISTRATION DIVISION OF THE

LANDS COMMISSION

98. Management extended the service period of 14 national service

personnel to December of the two years reviewed without approval

from the Commission thereby incurring an unbudgeted cost of

GH¢11,703.72 being allowances paid them. In order not to throw the

budget of the Division into disarray, we recommended that in future,

management should budget for and seek approval from the

Commission for the engagement of temporary staff.

99. Management engaged in single source procurement of goods

and services amounting to GH¢13,738.81. We advised management to

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 25 Other Statutory Institutions for the period ended 31 December

comply with the dictates of the PPA to ensure fairness, transparency

and value for money in its procurement dealings.

100. Our audit revealed that management procured goods worth

GH¢5,322.00 from non-VAT registered entities. This resulted in the

loss of GH¢798.30 in VAT/NHIL revenue. We recommended to

management to comply with the provision of the above stated

regulation.

101. The storage facility for land documents was not spacious,

leaking and had neither fire extinguishers nor emergency exit. We also

noted that due to lack of shelves or cabinets, some of the documents

were kept on the bare floor making retrieval for referencing very

difficult and exposing them to fast deterioration. To ensure efficiency

as well as safeguard the documents, we urged management to make

provision in future budgets for funds to acquire a bigger

accommodation with the necessary facilities for the records room.

Meanwhile, management should provide shelves or pallets for the

documents on the bare floor to be arranged.

PUBLIC AND VESTED LANDS MANAGEMENT DIVISION

OF LANDS COMMISSION (PVLMD)

102. Disbursements totalling GH¢282,555.00 were made without

the necessary supporting documents for authentication. As the

anomaly could lead to illegitimate payments, we urged management

to desist from the practice and ensure that the payments are supported

with relevant documents, failure which the authorizing and paying

officers should be surcharged with the amount involved.

103. Management contracted East Legon Lodge to provide hotel

accommodation services to the Commission without competitive

tendering. We advised management to desist from the practice and act

in accordance with the dictates of Act 663 in order that value for

money would be obtained in its future procurement dealings.

104. Contrary to the provisions of the Audit Service Act , 2000 (Act

584), the Commission had not established an Audit Reports

26 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

Implementation Committee (ARIC) to implement recommendations

of audit and other monitoring reports. We advised that an ARIC

should be constituted immediately.

MINISTRY OF JUSTICE

LAW REFORM COMMISSION

105. Purchases amounting to GH¢5,228.00 were made from a non-

VAT registered person. Consequently, VAT/NHIL revenue of

GH¢784.20 was lost to the state. We recommended that in future, all

purchases should be made from VAT registered persons; otherwise

officers responsible for the loss of revenue would be surcharged with

the amount involved.

106. Drivers failed to record fuel amounting to GH¢986.00 in

respective vehicle log books in contravention of Store Regulation

1604 as a result of laxity in supervision. We recommended effective

supervision over drivers and strict compliance with the store

regulation cited. We also advised management to ensure that the

drivers account for the unlogged fuel; failing which the amount should

be recovered from them.

COMMISSION ON HUMAN RIGHTS AND

ADMINISTRATIVE JUSTICE (CHRAJ)

107. Imprest totalling GH¢22,512.00 granted to five officers of the

Commission to run various programmes were neither retired nor

adjusted to their personal account even though the programmes had

long been executed. To forestall unspent imprest being held up by

imprest holders to the detriment of the Commission, we recommended

that the officers involved be made to account for the imprest taken or

the amounts be adjusted to a personal advance account in their names

as stipulated by Regulation 288 of the FAR,2004 (L.I. 1802).

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 27 Other Statutory Institutions for the period ended 31 December

108. Notwithstanding our previous audit recommendation coupled

with the Controller and Accountant General’s directives, the

Commission failed to refund to government chest an amount of

GH¢89,551.79 resulting from overstatement made in request for funds

for the payment of personnel emolument. Management was advised to

refund the amount without any further delay. We also recommended

to management to ensure that henceforth, accurate data is submitted

for the release of funds to prevent a recurrence, otherwise the

responsible officers would be held liable for a refund of the excess

funding.

109. Management circumvented provisions of the PPA, 2003 (Act

663) in the procurement of the accommodation for its Commissioner.

We recommended that management should be circumspect and adhere

to the dictates of the PPA in such future transactions to avoid waste

and for programme objectives to be achieved.

110. Out of the total 5% withholding tax of GH¢88,529.00 for the

three year period reviewed, management remitted only GH¢36,145.00

to the Domestic Tax Revenue Division (DTRD) leaving a balance of

GH¢52,384.00. We urged management to pay the outstanding tax and

ensure prompt and regular payments in future.

111. Various purchases amounting to GH¢34,994.89 were not

routed through stores before use in violation of Store Regulation

0502. For accountability of stores, we recommended that supervision

must be strengthened and the store- keeper should keep proper records

on the Commission’s receipts and issue of items purchased.

112. Though management had constituted an Audit Reports

Implementation Committee (ARIC) in accordance with Section 30 of

the Audit Service Act 2000 (Act 584), the Committee was apparently

inactivate as we could not obtain minutes of its meetings for our

review. For prompt implementation of recommendations in audit and

other monitoring reports, we recommended that the ARIC should be

made more responsive to its functions.

28 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

MINISTRY OF COMMUNICATIONS

POSTAL AND COURIER SERVICES REGULATORY

COMMISSION

113. The Accountant withheld a total amount of GH¢6,924.64 from

payments made to suppliers of goods and services which was yet to be

remitted to the Domestic Tax Revenue Division (DTRD) of the Ghana

Revenue Authority (GRA). We also noted that tax amounting to

GH¢3,147.21 were not withheld on allowances paid to

Commissioners and staff of the Commission. These lapses deprived

the state of tax revenue for its programmes. We recommended that the

tax revenue should be paid to the DTRD GRA without delay.

MINISTRY OF ENERGY

GHANA NATIONAL PETROLEUM CORPORATION

114. Our review of trade debtors revealed that there is a dispute over

an amount of GH¢2,125,347 owed by Sage Petroleum Limited to

GNPC. We advised management of GNPC to follow up on an appeal

made to the National Petroleum Authority (NPA) for arbitration and

take the necessary action to recover the debt in order to save the

Company from any financial distress.

ENERGY COMMISSION

115. An amount of GH¢135,000 was paid to a Landlord in respect

of Land for office building at Tesano by the Commission. However,

the deal to acquire the land did not go through and the amount is yet to

be refunded. We recommended that effort should be made to recover

the amount from the land owners so that it could be used to meet other

operational activities of the Commission.

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 29 Other Statutory Institutions for the period ended 31 December

116. An amount of GH¢5,121 owed by former staff of the

Commission had seen no movement for several years. We

recommended that efforts should be made to recover the debts from

the affected persons and in future measures should be put in place to

avert such recurrences of losing public funds.

117. An amount of GH¢150,000 was released by the Ministry of

Energy to the Commission to meet its budgetary requirements

following a request by the Commission. This amount has been in the

books since 2009 and no effort has been made to pay back. We

recommended that a follow-up should be made to the Ministry to

confirm the status of the amount to enable appropriate action to be

taken for fair reporting so as to enhance decision making.

NATIONAL PETROLEUM AUTHORITY

118. An amount of GH¢26,152 owed by Energy Commission in

2010 was still outstanding as at the time of reporting. We

recommended that management should recover the amount owed by

the Energy Commission.

119. As a result of an overpayment of GH¢6,379.69 on each of the 4

Toyota Corolla vehicles purchased by the Authority from Western

Automobile Ghana Ltd, a total amount of GH¢25,494.96 was

overpaid to the latter. We recommended that NPA should make

strenuous efforts to recover the overpaid amount from Western

Automobile Ghana Ltd.

GHANA GRID COMPANY LIMITED

120. A review of monthly fuel dipping report compared with book

balance at Prestea revealed a shortage of 908 litres over a period of 4

months. The persistent experience of such shortage may result in

losses to the Company, therefore we recommended that management

should investigate the cause of the shortages, apportion blame, recover

where necessary and take appropriate measures to address it.

30 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

MINISTRY OF FINANCE AND ECONOMIC PLANNING

RURAL AND AGRICULTURAL FINANCE

PROGRAMME

121. IFAD funds amounting US$745,000 was invested into a fixed

deposit account with Ecobank. Besides, we could not obtain the

investment certificate for the fixed deposit made. Again, there was no

agreement on file nor correspondence showing duration or rate of

interest on the investment. We advised that where funds are used for

purposes other than that provided in the financing agreement prior

approval should be sought from the funding agency to prevent any

displeasure which might negatively affect the furtherance of the

Project. Management should also obtain the necessary certificate for

the investment to ensure that the right amount of interest is paid and

on time.

VENTURE CAPITAL TRUST FUND

122. Amount due from loan defaulters amounted to GH¢333,344 as

at the end of December 2012. The Trust Fund introduced a

Development Assisting Fund which a lot of people took advantage of

and had the loan but woefully failed to adhere to the repayment terms

resulting in the outstanding debt. We recommended that management

should make the necessary efforts, even including legal action to

recover the loan from defaulters.

GHANA COCOA BOARD

123. Members of staff who were given imprest to the tune of

GH¢22,553 in 2010/2011 had since not accounted for the imprest

amounts even after completion of the programme. We recommended

that the affected staff should immediately be made to account for the

total outstanding amount or be held liable for a refund by deductions

from their salaries.

Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and 31 Other Statutory Institutions for the period ended 31 December

BANK OF GHANA

124. Bank of Ghana (BoG) has a controlling interest in the Central

Securities Depository, International Bank PLC and Ghana

International Bank payment and settlement systems. However none

of these subsidiaries prepare financial returns to Bank of Ghana, the

holding company, so as to properly track and monitor their financial

performance. This situation also results in significant delays in

getting consolidated financial statements readily for review. We

advised BoG to put in place measures which would ensure proper

monitoring of financial performance of its subsidiaries and for early

presentation of trial balance for preparation of its Consolidated

Accounts.

125. A short term loan facility granted by BoG to the National

Investment Bank (NIB) of GH¢60,000,000 due on 20 September 2009

and further extension to 31 March 2010 remained unpaid as at the

time of reporting. We also did not sight any security backing the loan.

Similarly BoG granted a Bridging Facility to GCB under an MOU

made up of a cedi equivalent of US$25,000,000 and US$50,000,000

.However the bridging facility of US$ 50,000,000 remained unsettled

as at the time of reporting. We recommended that management

should take necessary steps to ensure that all loans are governed by

valid loan agreement.

126. Withholding taxes deducted on payments for goods and

services in excess of GH¢50 had not been paid to the Commissioner

of DTRD promptly within the stipulated period. Consequently

withholding tax payable to the tune of GH¢625,875.95 had

accumulated as at 31 December 2011. We advised management to

comply with the requirements of Section 87(1) of Act 594 by

remitting these immediately and subsequent withheld taxes should be

remitted by the 15 of the month following the month of deduction for

the avoidance of penalties.

32 Report of the Auditor-General on the Public Accounts of Ghana – Public Boards, Corporations, and

Other Statutory Institutions for the period ended 31 December 2012

MINISTRY OF INFORMATION

GRAPHIC PACKAGING LIMITED

127. Raw materials purchased worth GH¢140,073 since August

2011 for the production of labels for Blue Skies Limited were still in

stock. This was because Blue Skies Ltd changed its label. We