Embed Size (px)

Citation preview

Published by Articulate® Storyline www.articulate.com

Revised 10/21/2016

Published by Articulate® Storyline www.articulate.com

One of our values at Discover is to communicate openly and honestly with others to create an environment of trust. Creating an environment of trust with consumers is a key component of providing exceptional customer service while becoming the most rewarding relationship consumers have with a financial institution. Your role in documenting complaints is critical to our business since it provides us with the opportunity to track, investigate, and take appropriate action when necessary.

Published by Articulate® Storyline www.articulate.com

By the end of this course you will understand the importance of identifying and documenting consumer complaints and be able to: • Identify when a consumer expresses a complaint, or a potential allegation involving discrimination or Unfair

Deceptive or Abusive Acts or Practices, known as UDAAP.

Published by Articulate® Storyline www.articulate.com

In order to fulfill our responsibility to the company, our customers, and regulatory agencies, it is a requirement that all consumer-facing employees accurately document all complaints received from our consumers. Your support creates an opportunity to drive positive change that is beneficial to both the consumer and employee experience. As a result of your adherence to feedback and complaint handling policies and procedures, the company has realized numerous benefits through the implementation of improvements to current processes and by initiating projects to address consumer concerns. Without the complaint documentation done by each one of you, these improvements, and others, may have gone unidentified or taken longer to receive the attention each deserves. Therefore, to reinforce our commitment as an organization and to ensure your understanding of complaint terminology and its documentation requirement, you will take training on this topic two times each year.

Published by Articulate® Storyline www.articulate.com

Published by Articulate® Storyline www.articulate.com

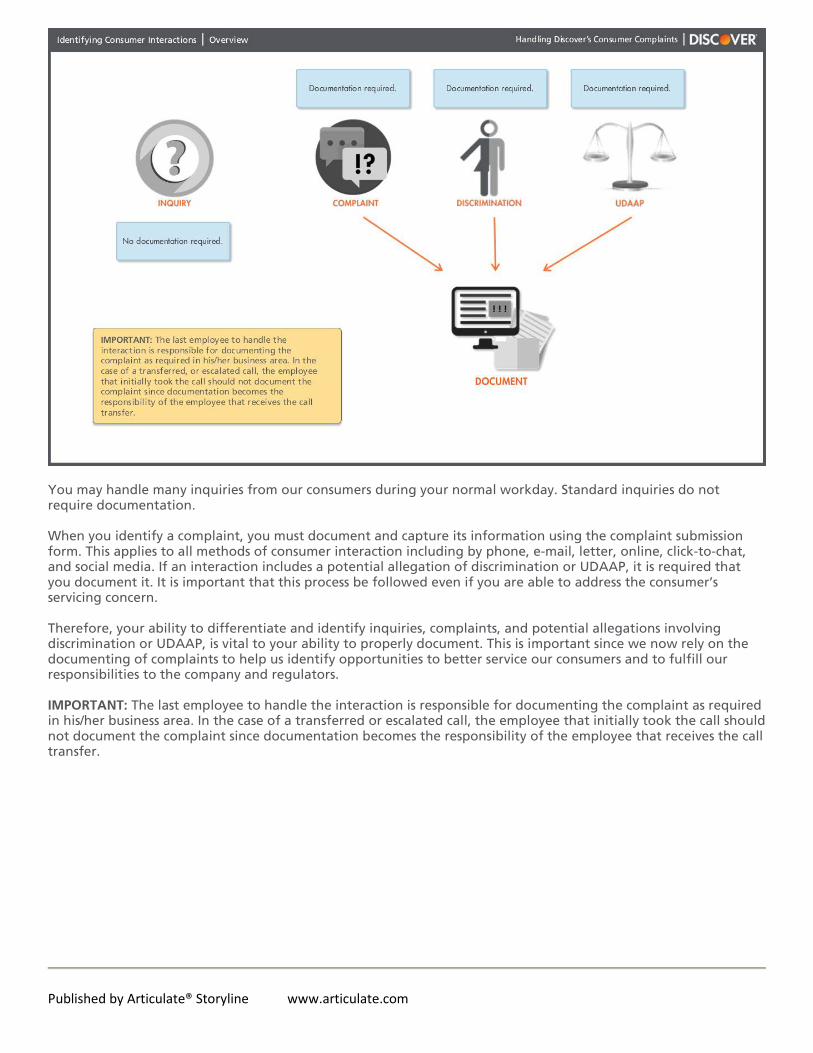

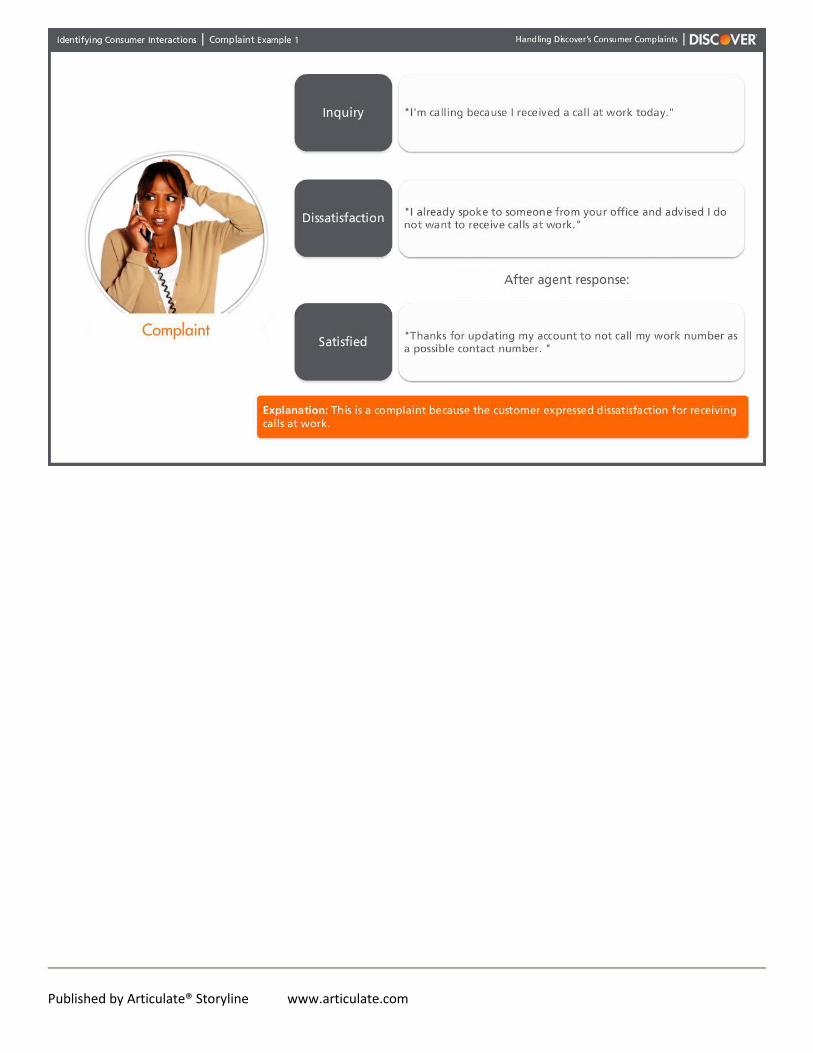

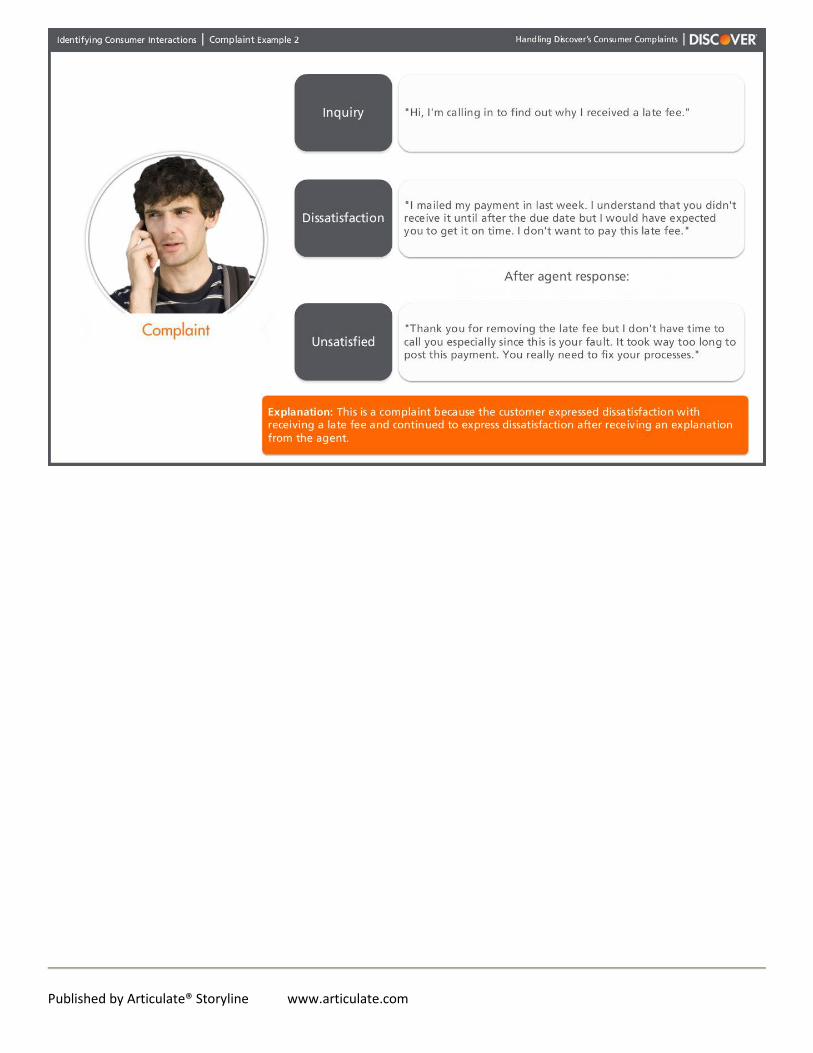

You may handle many inquiries from our consumers during your normal workday. Standard inquiries do not require documentation. When you identify a complaint, you must document and capture its information using the complaint submission form. This applies to all methods of consumer interaction including by phone, e-mail, letter, online, click-to-chat, and social media. If an interaction includes a potential allegation of discrimination or UDAAP, it is required that you document it. It is important that this process be followed even if you are able to address the consumer’s servicing concern. Therefore, your ability to differentiate and identify inquiries, complaints, and potential allegations involving discrimination or UDAAP, is vital to your ability to properly document. This is important since we now rely on the documenting of complaints to help us identify opportunities to better service our consumers and to fulfill our responsibilities to the company and regulators. IMPORTANT: The last employee to handle the interaction is responsible for documenting the complaint as required in his/her business area. In the case of a transferred or escalated call, the employee that initially took the call should not document the complaint since documentation becomes the responsibility of the employee that receives the call transfer.

Published by Articulate® Storyline www.articulate.com

If, after interacting with an employee or third party service provider, a consumer expresses dissatisfaction or demands relief regarding a Discover product, service, or practice, a consumer’s feedback is considered a complaint. You are required to submit all complaints to Discover within two business days of receipt. Complaints are then forwarded to the NRC Complaint Management team using a standard complaint template and the [email protected] email address.

Published by Articulate® Storyline www.articulate.com

Published by Articulate® Storyline www.articulate.com

Published by Articulate® Storyline www.articulate.com

Published by Articulate® Storyline www.articulate.com

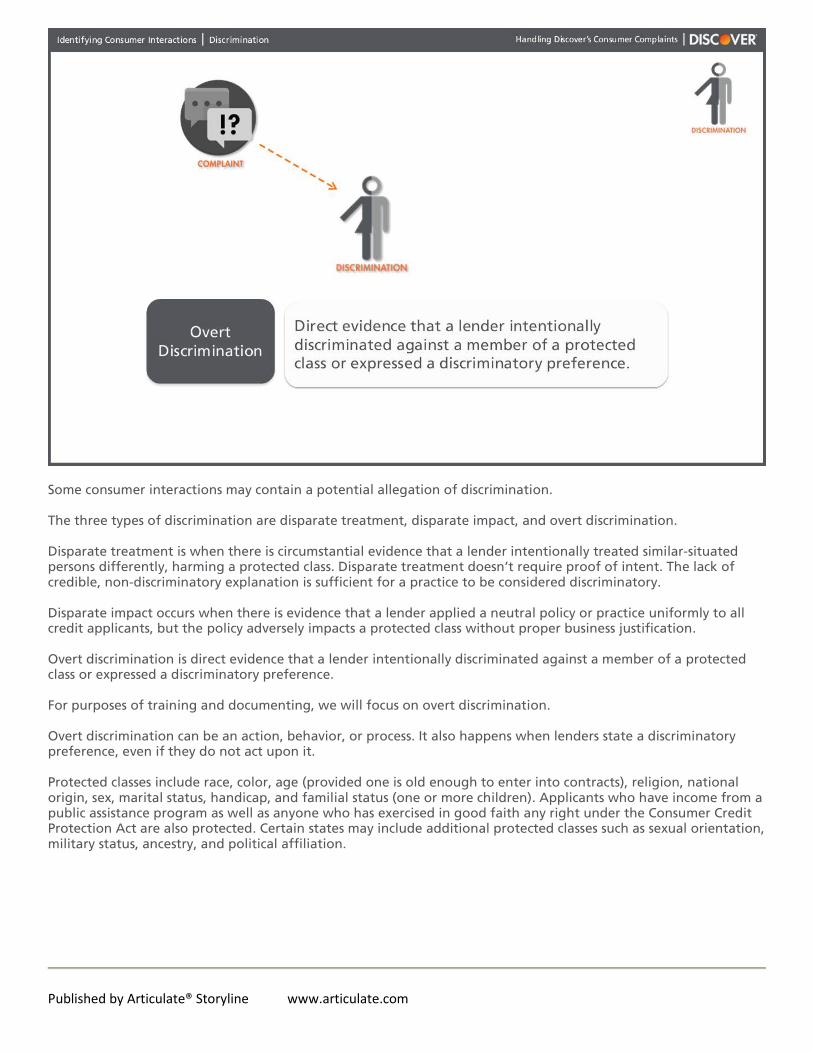

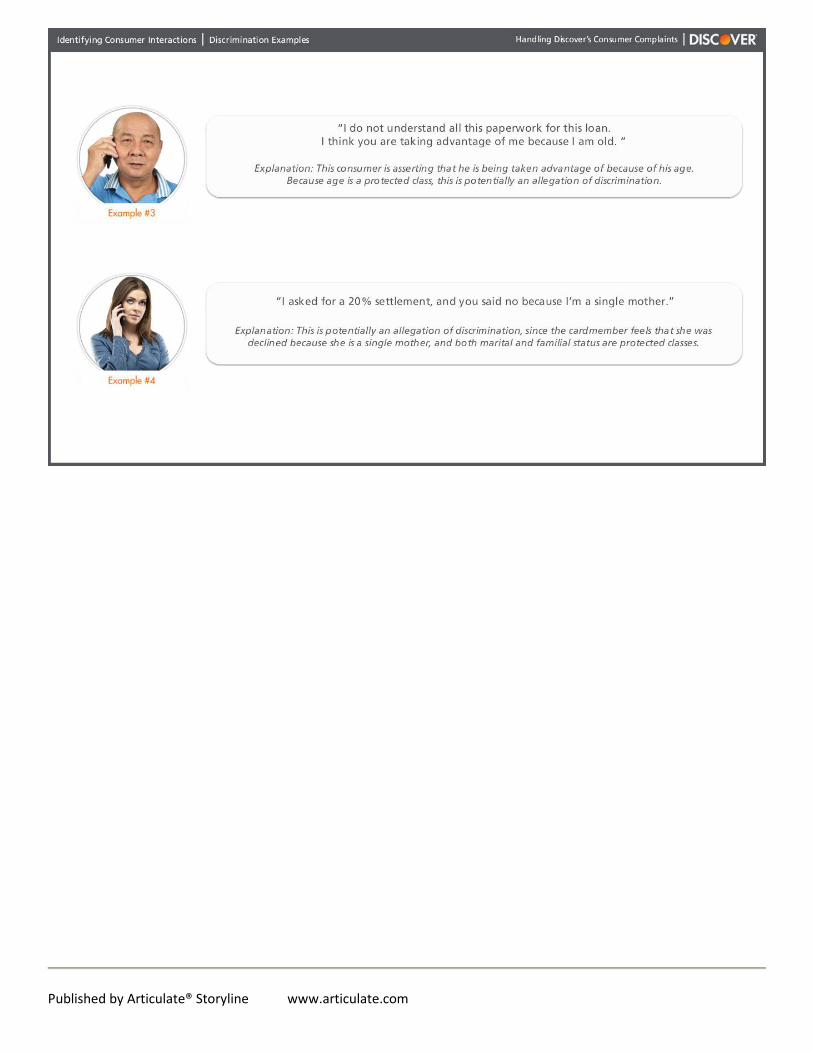

Some consumer interactions may contain a potential allegation of discrimination. The three types of discrimination are disparate treatment, disparate impact, and overt discrimination. Disparate treatment is when there is circumstantial evidence that a lender intentionally treated similar-situated persons differently, harming a protected class. Disparate treatment doesn’t require proof of intent. The lack of credible, non-discriminatory explanation is sufficient for a practice to be considered discriminatory. Disparate impact occurs when there is evidence that a lender applied a neutral policy or practice uniformly to all credit applicants, but the policy adversely impacts a protected class without proper business justification. Overt discrimination is direct evidence that a lender intentionally discriminated against a member of a protected class or expressed a discriminatory preference. For purposes of training and documenting, we will focus on overt discrimination. Overt discrimination can be an action, behavior, or process. It also happens when lenders state a discriminatory preference, even if they do not act upon it. Protected classes include race, color, age (provided one is old enough to enter into contracts), religion, national origin, sex, marital status, handicap, and familial status (one or more children). Applicants who have income from a public assistance program as well as anyone who has exercised in good faith any right under the Consumer Credit Protection Act are also protected. Certain states may include additional protected classes such as sexual orientation, military status, ancestry, and political affiliation.

Published by Articulate® Storyline www.articulate.com

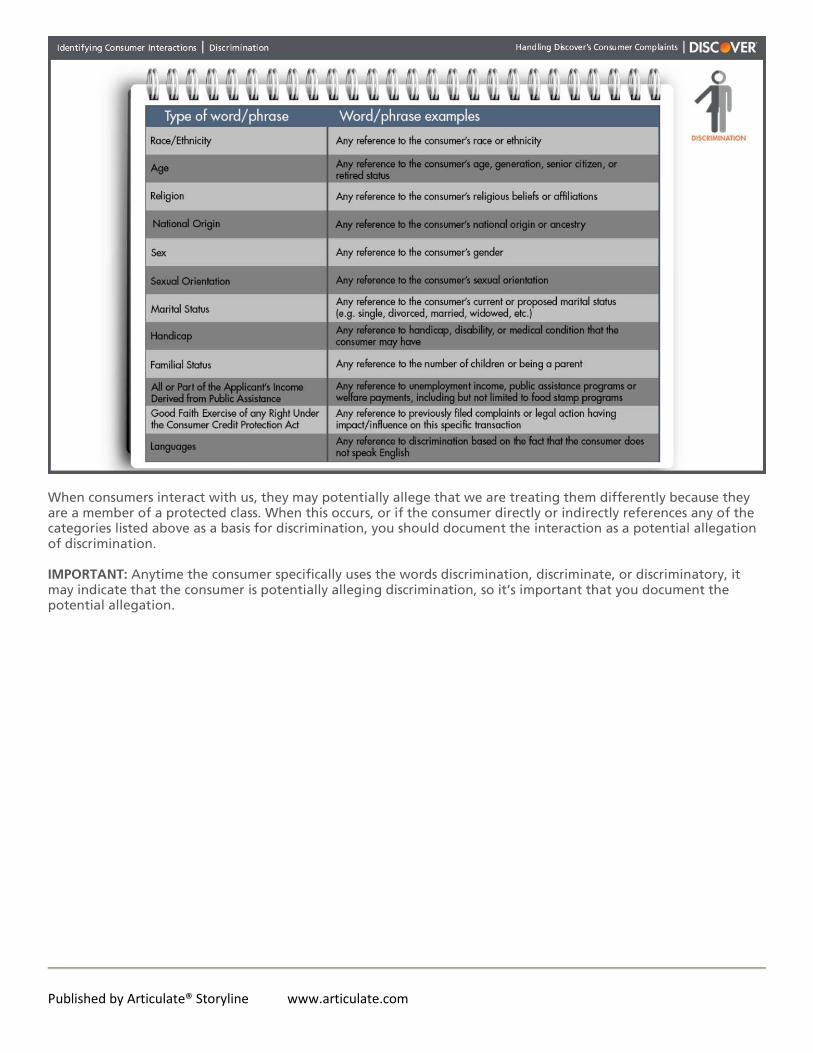

When consumers interact with us, they may potentially allege that we are treating them differently because they are a member of a protected class. When this occurs, or if the consumer directly or indirectly references any of the categories listed above as a basis for discrimination, you should document the interaction as a potential allegation of discrimination. IMPORTANT: Anytime the consumer specifically uses the words discrimination, discriminate, or discriminatory, it may indicate that the consumer is potentially alleging discrimination, so it’s important that you document the potential allegation.

Published by Articulate® Storyline www.articulate.com

Published by Articulate® Storyline www.articulate.com

Published by Articulate® Storyline www.articulate.com

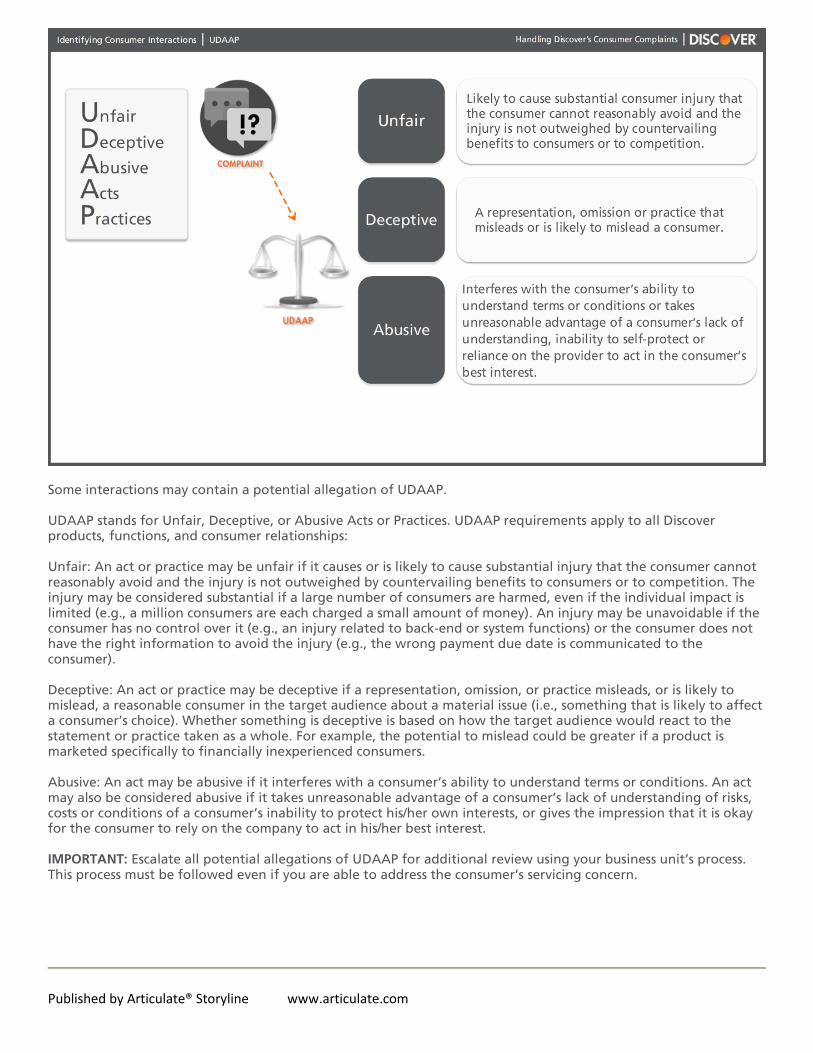

Some interactions may contain a potential allegation of UDAAP. UDAAP stands for Unfair, Deceptive, or Abusive Acts or Practices. UDAAP requirements apply to all Discover products, functions, and consumer relationships: Unfair: An act or practice may be unfair if it causes or is likely to cause substantial injury that the consumer cannot reasonably avoid and the injury is not outweighed by countervailing benefits to consumers or to competition. The injury may be considered substantial if a large number of consumers are harmed, even if the individual impact is limited (e.g., a million consumers are each charged a small amount of money). An injury may be unavoidable if the consumer has no control over it (e.g., an injury related to back-end or system functions) or the consumer does not have the right information to avoid the injury (e.g., the wrong payment due date is communicated to the consumer). Deceptive: An act or practice may be deceptive if a representation, omission, or practice misleads, or is likely to mislead, a reasonable consumer in the target audience about a material issue (i.e., something that is likely to affect a consumer’s choice). Whether something is deceptive is based on how the target audience would react to the statement or practice taken as a whole. For example, the potential to mislead could be greater if a product is marketed specifically to financially inexperienced consumers. Abusive: An act may be abusive if it interferes with a consumer’s ability to understand terms or conditions. An act may also be considered abusive if it takes unreasonable advantage of a consumer’s lack of understanding of risks, costs or conditions of a consumer’s inability to protect his/her own interests, or gives the impression that it is okay for the consumer to rely on the company to act in his/her best interest. IMPORTANT: Escalate all potential allegations of UDAAP for additional review using your business unit’s process. This process must be followed even if you are able to address the consumer’s servicing concern.

Published by Articulate® Storyline www.articulate.com

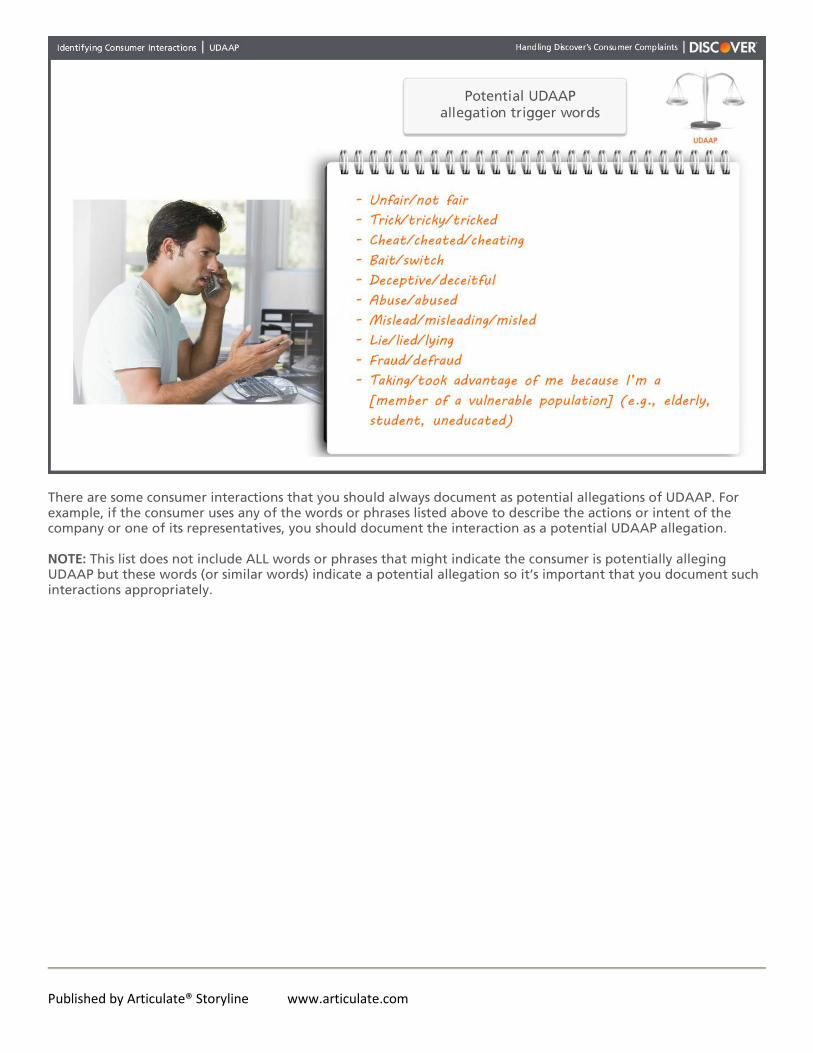

There are some consumer interactions that you should always document as potential allegations of UDAAP. For example, if the consumer uses any of the words or phrases listed above to describe the actions or intent of the company or one of its representatives, you should document the interaction as a potential UDAAP allegation. NOTE: This list does not include ALL words or phrases that might indicate the consumer is potentially alleging UDAAP but these words (or similar words) indicate a potential allegation so it’s important that you document such interactions appropriately.

Published by Articulate® Storyline www.articulate.com

Published by Articulate® Storyline www.articulate.com

Published by Articulate® Storyline www.articulate.com

By completing this course, you now have the knowledge and skills necessary to: • Identify when a consumer expresses a complaint or a potential allegation involving discrimination or Unfair

Deceptive Abusive Acts or Practices knows as UDAAP.

Published by Articulate® Storyline www.articulate.com