Embed Size (px)

Citation preview

25th April 2018

Q1 2018 PRESENTATION

Leif Gustafsson, CEO

Aku Rumpunen, CFO

Q1 2018 Highlights

• Organic sales growth of 10.4% was supported

by both business divisions

• Comparable EBITA improved by 17.3% to EUR

23.1 million (19.7) with margin of 13.2%

(12.1%) supported by both business divisions

• Modular Space organic rental sales growth

14.2% and EBITA improvement by 35.2%

• Acquisition of KBS Infra supporting ER Central

Europe

2

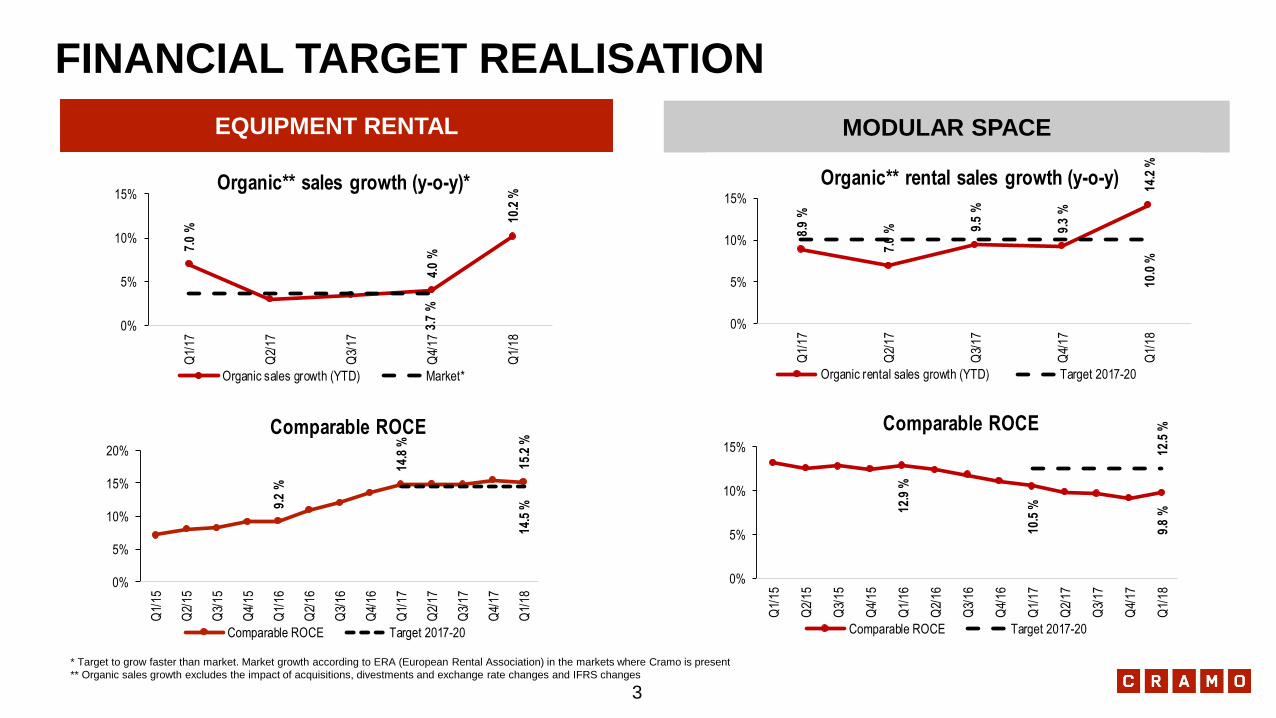

FINANCIAL TARGET REALISATION

EQUIPMENT RENTAL MODULAR SPACE

* Target to grow faster than market. Market growth according to ERA (European Rental Association) in the markets where Cramo is present

** Organic sales growth excludes the impact of acquisitions, divestments and exchange rate changes and IFRS changes

3

9.2

%

14.8

%

15.2

%14

.5 %

0%

5%

10%

15%

20%

Q1/

15

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Comparable ROCE

Comparable ROCE Target 2017-20

12.9

%

10.5

%

9.8

%12

.5 %

0%

5%

10%

15%

Q1/

15

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Comparable ROCE

Comparable ROCE Target 2017-20

7.0

%

4.0

%

10.2

%

3.7

%

0%

5%

10%

15%Q

1/17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Organic** sales growth (y-o-y)*

Organic sales growth (YTD) Market*

8.9

%

7.0

% 9.5

%

9.3

%

14.2

%10

.0 %

0%

5%

10%

15%

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Organic** rental sales growth (y-o-y)

Organic rental sales growth (YTD) Target 2017-20

4

BUSINESS

SEGMENTS

4

85.792.2 92.2

0

20

40

60

80

100

120

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Sal

es (

EU

R m

illio

n)

Sales

10.8

15.716.7

12.0

%

17.7

% 19.3

%

10%

12%

14%

16%

18%

20%

22%

24%

0

5

10

15

20

25

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

RO

CE

EB

ITA

(EU

R m

illio

n)

EBITA and ROCE

EBITA ROCE

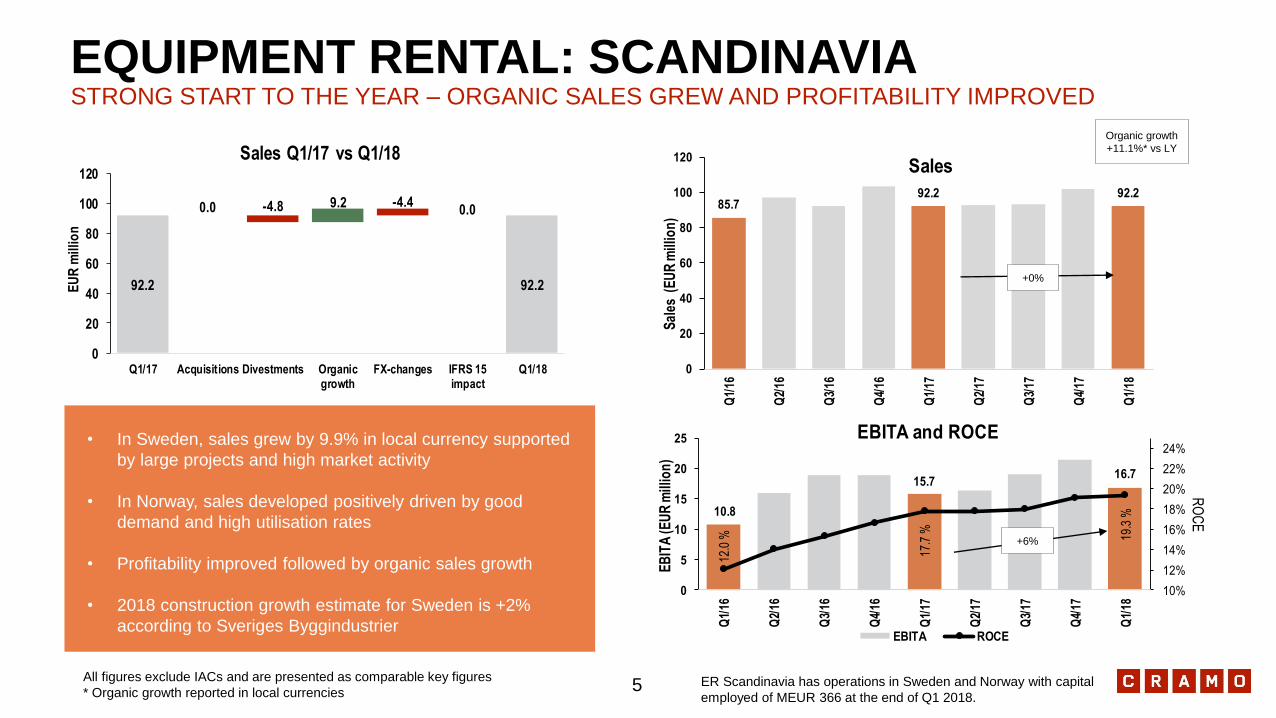

• In Sweden, sales grew by 9.9% in local currency supported

by large projects and high market activity

• In Norway, sales developed positively driven by good

demand and high utilisation rates

• Profitability improved followed by organic sales growth

• 2018 construction growth estimate for Sweden is +2%

according to Sveriges Byggindustrier

EQUIPMENT RENTAL: SCANDINAVIASTRONG START TO THE YEAR – ORGANIC SALES GREW AND PROFITABILITY IMPROVED

+6%

Organic growth

+11.1%* vs LY

ER Scandinavia has operations in Sweden and Norway with capital

employed of MEUR 366 at the end of Q1 2018.

+0%

All figures exclude IACs and are presented as comparable key figures

* Organic growth reported in local currencies

92.2 92.2

0.0 -4.8 9.2 -4.40.0

0

20

40

60

80

100

120

Q1/17 Acquisitions Divestments Organicgrowth

FX-changes IFRS 15impact

Q1/18

EU

R m

illio

n

Sales Q1/17 vs Q1/18

5

28.130.7

32.3

0

5

10

15

20

25

30

35

40

45

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Sal

es (

EU

R m

illio

n)

Sales

-0.5

2.2 2.4

8.2

%

13.4

%

13.4

%

0%

5%

10%

15%

20%

-2

0

2

4

6

8

10

12

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

RO

CE

EB

ITA

(EU

R m

illio

n)

EBITA and ROCE

EBITA ROCE

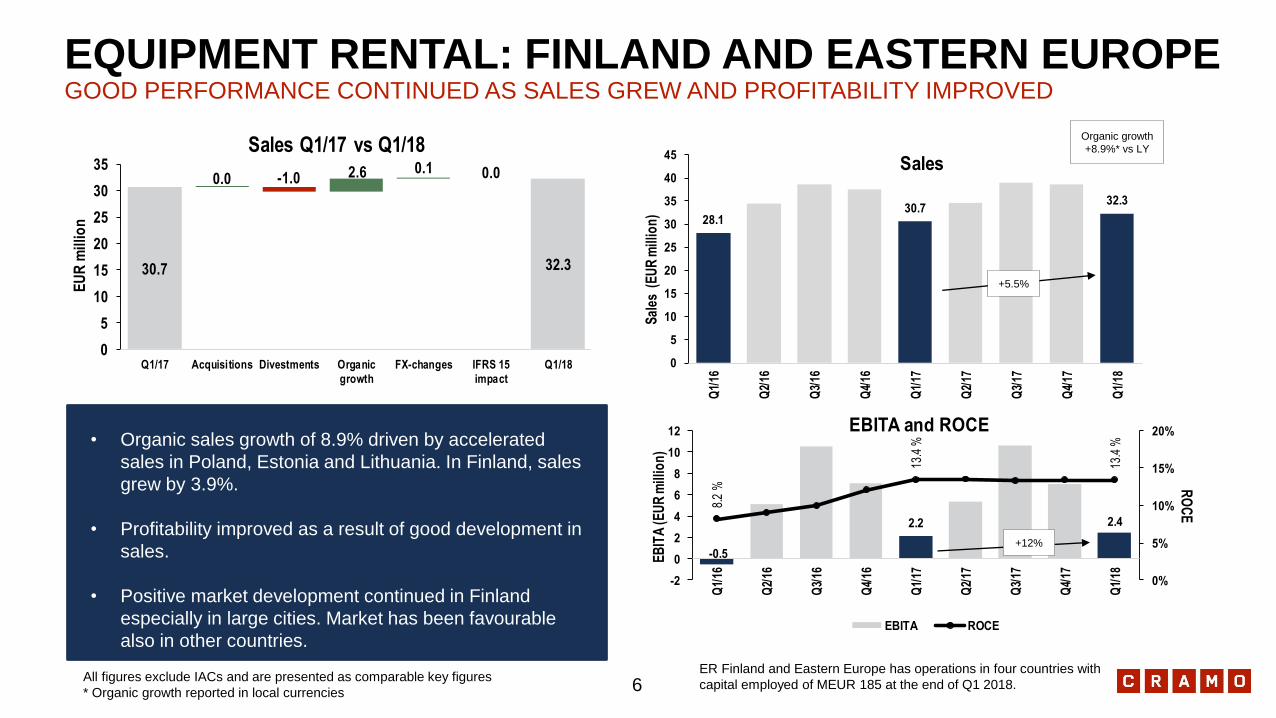

EQUIPMENT RENTAL: FINLAND AND EASTERN EUROPEGOOD PERFORMANCE CONTINUED AS SALES GREW AND PROFITABILITY IMPROVED

+12%

Organic growth

+8.9%* vs LY

+5.5%

• Organic sales growth of 8.9% driven by accelerated

sales in Poland, Estonia and Lithuania. In Finland, sales

grew by 3.9%.

• Profitability improved as a result of good development in

sales.

• Positive market development continued in Finland

especially in large cities. Market has been favourable

also in other countries.

ER Finland and Eastern Europe has operations in four countries with

capital employed of MEUR 185 at the end of Q1 2018.All figures exclude IACs and are presented as comparable key figures

* Organic growth reported in local currencies

30.7 32.3

0.0 -1.0 2.6 0.1 0.0

0

5

10

15

20

25

30

35

Q1/17 Acquisitions Divestments Organic

growth

FX-changes IFRS 15

impact

Q1/18

EU

R m

illio

n

Sales Q1/17 vs Q1/18

6

13.814.5

18.7

0

5

10

15

20

25

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Sa

les

(E

UR

mil

lio

n)

Sales

-3.4-2.5

-1.8

-1.5

%

5.1

%

4.4

%

-3%

-1%

1%

3%

5%

7%

-4

-3

-2

-1

0

1

2

3

4

5

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

RO

CE

EB

ITA

(E

UR

mil

lio

n)

EBITA and ROCE

EBITA ROCE

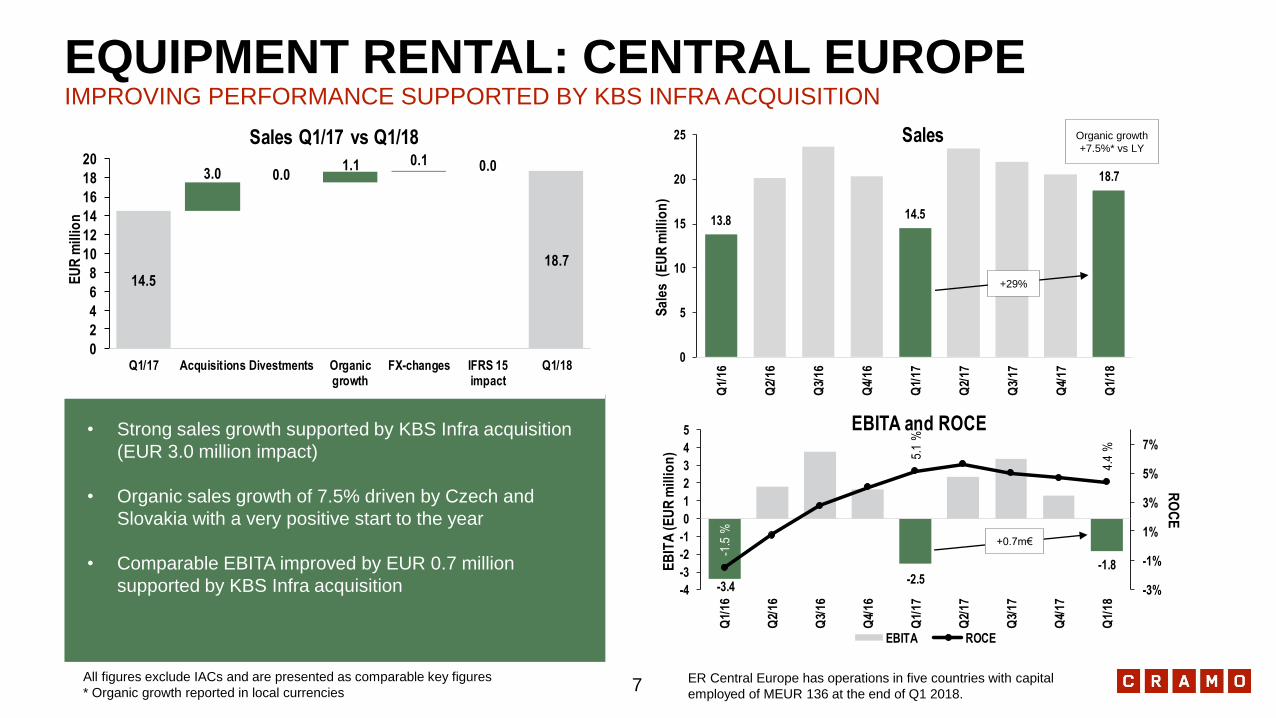

EQUIPMENT RENTAL: CENTRAL EUROPEIMPROVING PERFORMANCE SUPPORTED BY KBS INFRA ACQUISITION

Organic growth

+7.5%* vs LY

ER Central Europe has operations in five countries with capital

employed of MEUR 136 at the end of Q1 2018.

• Strong sales growth supported by KBS Infra acquisition

(EUR 3.0 million impact)

• Organic sales growth of 7.5% driven by Czech and

Slovakia with a very positive start to the year

• Comparable EBITA improved by EUR 0.7 million

supported by KBS Infra acquisition

All figures exclude IACs and are presented as comparable key figures

* Organic growth reported in local currencies

14.5

18.7

3.0 0.01.1 0.1 0.0

0

2

4

6

8

10

12

14

16

18

20

Q1/17 Acquisitions Divestments Organicgrowth

FX-changes IFRS 15impact

Q1/18

EU

R m

illio

n

Sales Q1/17 vs Q1/18

+0.7m€

+29%

7

7.9

6.3

8.5

12.9

%

10.5

%

9.8

%

5%

7%

9%

11%

13%

15%

17%

19%

0

1

2

3

4

5

6

7

8

9

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

RO

CE

EB

ITA

(EU

R m

illio

n)

EBITA and ROCE

EBITA ROCE

18.4 20.022.6

9.6 5.7

9.5

28.025.7

32.1

0

5

10

15

20

25

30

35

40

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Sal

es (

EU

R m

illio

n)

Sales

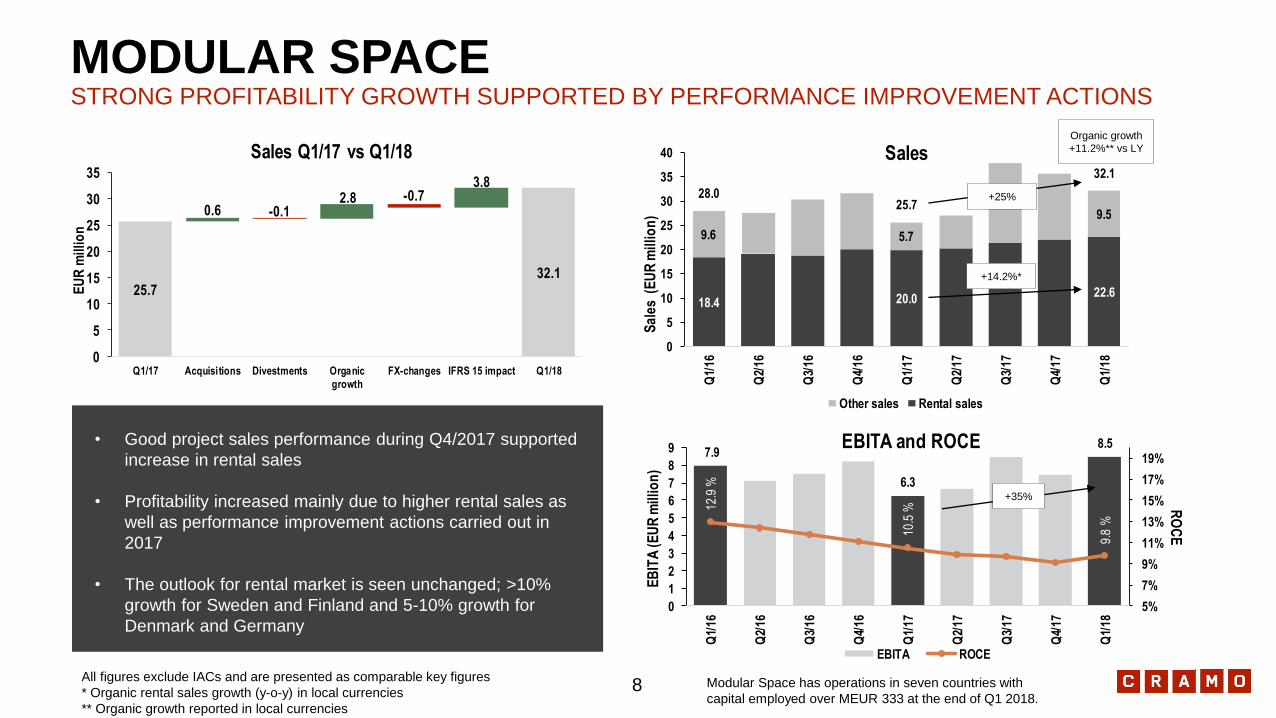

Other sales Rental sales Sales

• Good project sales performance during Q4/2017 supported

increase in rental sales

• Profitability increased mainly due to higher rental sales as

well as performance improvement actions carried out in

2017

• The outlook for rental market is seen unchanged; >10%

growth for Sweden and Finland and 5-10% growth for

Denmark and Germany

MODULAR SPACESTRONG PROFITABILITY GROWTH SUPPORTED BY PERFORMANCE IMPROVEMENT ACTIONS

Modular Space has operations in seven countries with

capital employed over MEUR 333 at the end of Q1 2018.

+35%

Organic growth

+11.2%** vs LY

+14.2%*+25%

All figures exclude IACs and are presented as comparable key figures

* Organic rental sales growth (y-o-y) in local currencies

** Organic growth reported in local currencies

+25%

25.732.1

0.6 -0.12.8 -0.7

3.8

0

5

10

15

20

25

30

35

Q1/17 Acquisitions Divestments Organic

growth

FX-changes IFRS 15 impact Q1/18

EU

R m

illi

on

Sales Q1/17 vs Q1/18

8

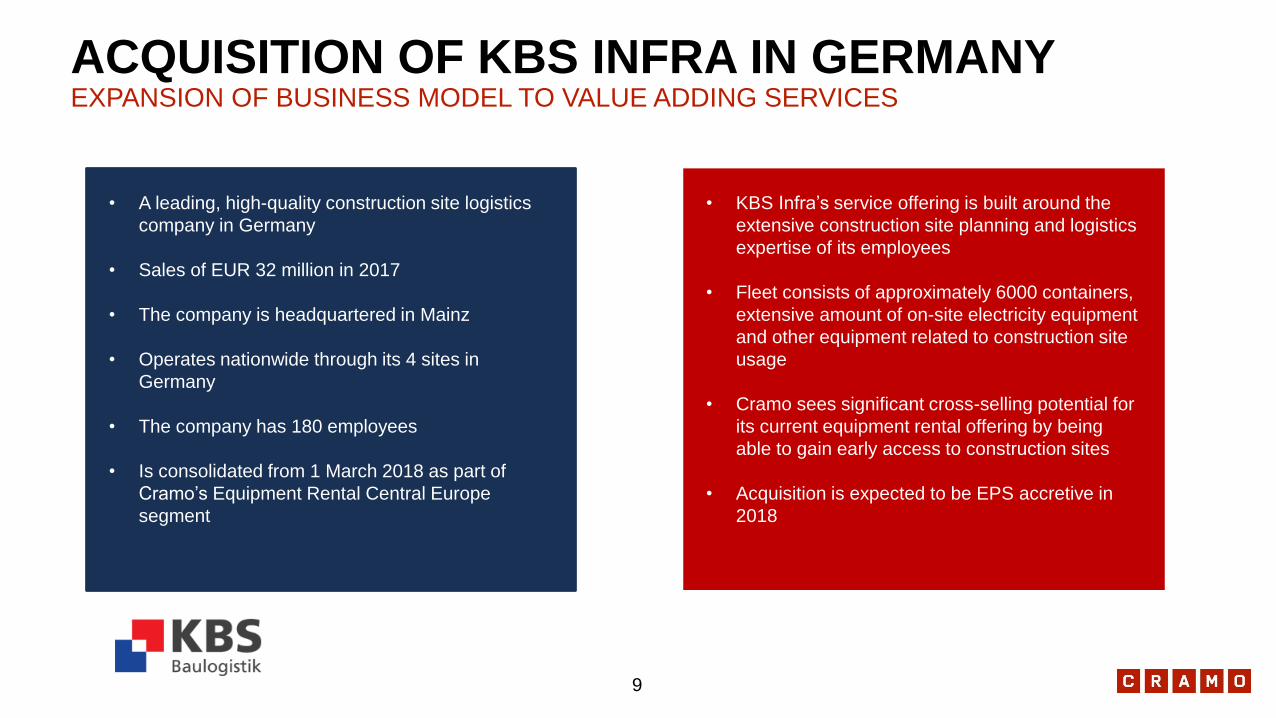

ACQUISITION OF KBS INFRA IN GERMANYEXPANSION OF BUSINESS MODEL TO VALUE ADDING SERVICES

• A leading, high-quality construction site logistics

company in Germany

• Sales of EUR 32 million in 2017

• The company is headquartered in Mainz

• Operates nationwide through its 4 sites in

Germany

• The company has 180 employees

• Is consolidated from 1 March 2018 as part of

Cramo’s Equipment Rental Central Europe

segment

• KBS Infra’s service offering is built around the

extensive construction site planning and logistics

expertise of its employees

• Fleet consists of approximately 6000 containers,

extensive amount of on-site electricity equipment

and other equipment related to construction site

usage

• Cramo sees significant cross-selling potential for

its current equipment rental offering by being

able to gain early access to construction sites

• Acquisition is expected to be EPS accretive in

2018

9

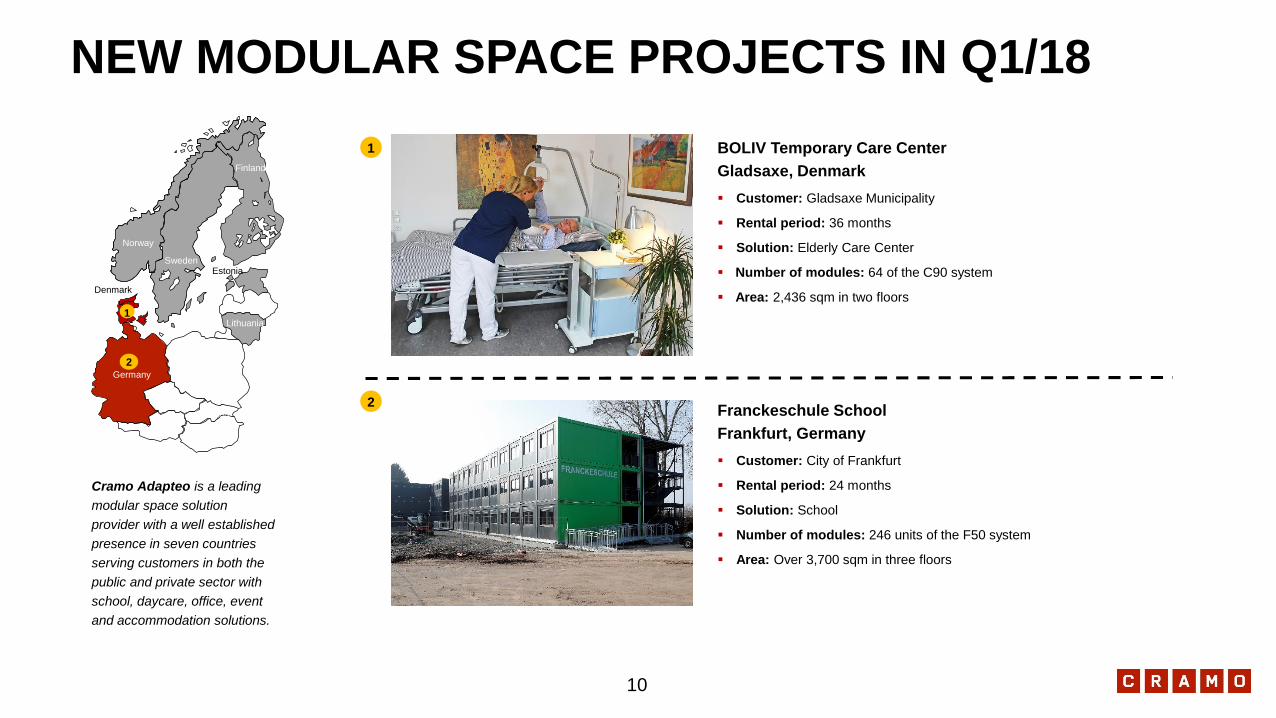

NEW MODULAR SPACE PROJECTS IN Q1/18

BOLIV Temporary Care Center

Gladsaxe, Denmark

▪ Customer: Gladsaxe Municipality

▪ Rental period: 36 months

▪ Solution: Elderly Care Center

▪ Number of modules: 64 of the C90 system

▪ Area: 2,436 sqm in two floors

Franckeschule School

Frankfurt, Germany

▪ Customer: City of Frankfurt

▪ Rental period: 24 months

▪ Solution: School

▪ Number of modules: 246 units of the F50 system

▪ Area: Over 3,700 sqm in three floors

Denmark

Germany

Slovakia

Lithuania

Estonia

Norway

Sweden

Finland

1

1

2

2

Cramo Adapteo is a leading

modular space solution

provider with a well established

presence in seven countries

serving customers in both the

public and private sector with

school, daycare, office, event

and accommodation solutions.

10

GROUP

PERFORMANCE

Q1 2018

11

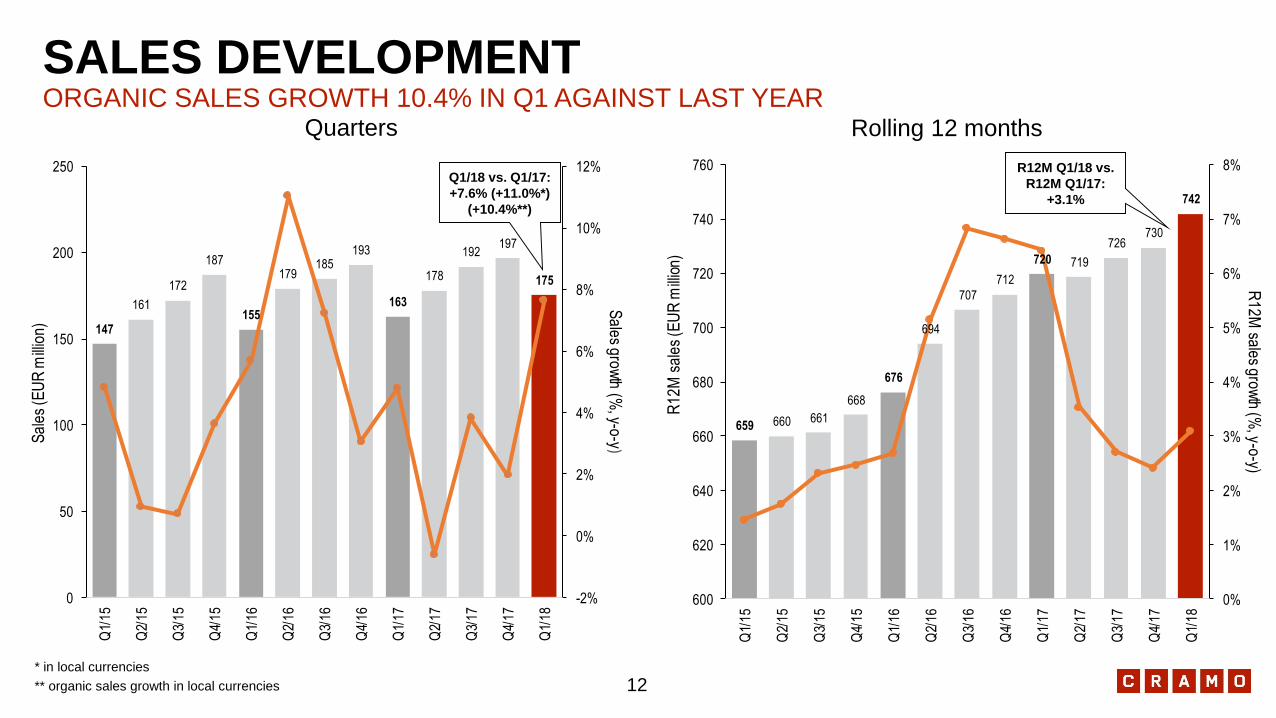

147

161

172

187

155

179185

193

163

178

192197

175

-2%

0%

2%

4%

6%

8%

10%

12%

0

50

100

150

200

250

Q1/

15

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Sa

les g

row

th (%

, y-o-y)S

ales

(EU

R m

illio

n)

659 660 661

668

676

694

707

712

720 719

726730

742

0%

1%

2%

3%

4%

5%

6%

7%

8%

600

620

640

660

680

700

720

740

760

Q1/

15

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

R1

2M

sale

s gro

wth

(%, y-o

-y)

R1

2M

sa

les

(EU

R m

illio

n)

SALES DEVELOPMENTORGANIC SALES GROWTH 10.4% IN Q1 AGAINST LAST YEAR

* in local currencies

** organic sales growth in local currencies

Quarters Rolling 12 months

R12M Q1/18 vs.

R12M Q1/17:

+3.1%

Q1/18 vs. Q1/17:

+7.6% (+11.0%*)

(+10.4%**)

12

162.9175.3

3.7 -5.915.8 -4.9 3.8

0

20

40

60

80

100

120

140

160

180

200

Q1/17 Acquisitions Divestments Organic

growth

FX-changes IFRS 15

impact

Q1/18

EU

R m

illio

n

Sales Q1/17 vs Q1/18

GROUP Q1 ORGANIC SALES GROWTH VS LY

Organic sales growth

+10.4% vs LY

▪ Equipment Rental +10.2%

▪ Scandinavia +11.1%

▪ Finland and Eastern Europe

+8.9%

▪ Central Europe +7.5%

▪ Modular Space +11.2%

13

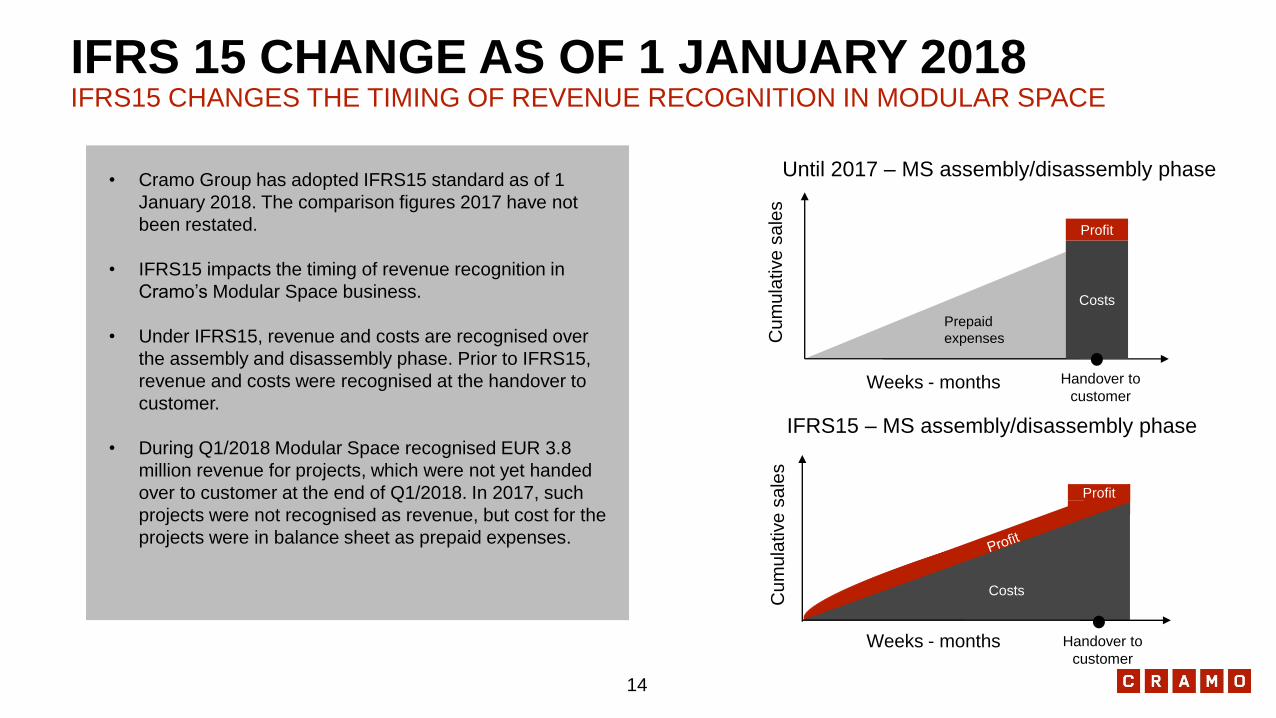

IFRS 15 CHANGE AS OF 1 JANUARY 2018IFRS15 CHANGES THE TIMING OF REVENUE RECOGNITION IN MODULAR SPACE

• Cramo Group has adopted IFRS15 standard as of 1

January 2018. The comparison figures 2017 have not

been restated.

• IFRS15 impacts the timing of revenue recognition in

Cramo’s Modular Space business.

• Under IFRS15, revenue and costs are recognised over

the assembly and disassembly phase. Prior to IFRS15,

revenue and costs were recognised at the handover to

customer.

• During Q1/2018 Modular Space recognised EUR 3.8

million revenue for projects, which were not yet handed

over to customer at the end of Q1/2018. In 2017, such

projects were not recognised as revenue, but cost for the

projects were in balance sheet as prepaid expenses.

Cu

mu

lative

sa

les

Costs

Profit

Prepaid

expenses

Until 2017 – MS assembly/disassembly phase

Handover to

customer

Cu

mu

lative

sa

les

Costs

IFRS15 – MS assembly/disassembly phase

Handover to

customer

Weeks - months

Weeks - months

Profit

14

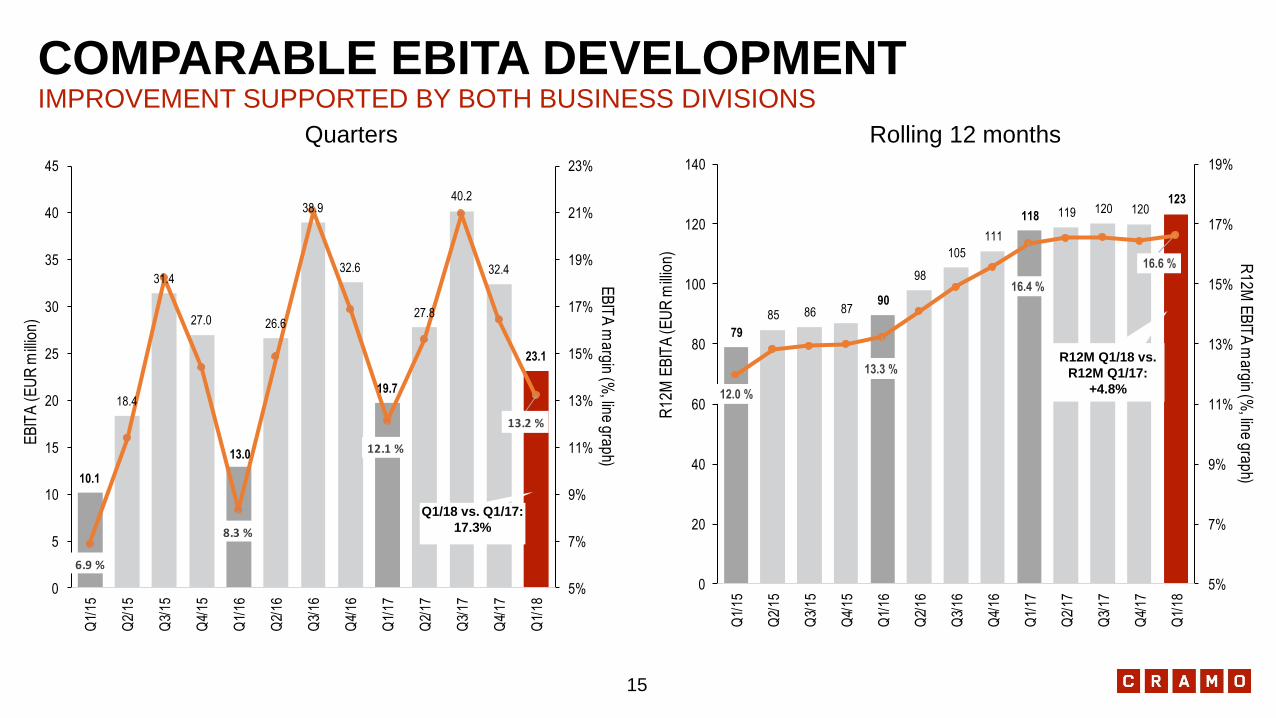

10.1

18.4

31.4

27.0

13.0

26.6

38.9

32.6

19.7

27.8

40.2

32.4

23.1

6.9 %

8.3 %

12.1 %

13.2 %

5%

7%

9%

11%

13%

15%

17%

19%

21%

23%

0

5

10

15

20

25

30

35

40

45

Q1/

15

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

EB

ITA

ma

rgin

(%, lin

e g

rap

h)

EB

ITA

(E

UR

mill

ion

)

79

85 86 8790

98

105

111

118 119 120 120123

12.0 %

13.3 %

16.4 %

16.6 %

5%

7%

9%

11%

13%

15%

17%

19%

0

20

40

60

80

100

120

140

Q1/

15

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

R1

2M

EB

ITA

ma

rgin (%

, line

gra

ph)

R1

2M

EB

ITA

(E

UR

mill

ion

)

COMPARABLE EBITA DEVELOPMENTIMPROVEMENT SUPPORTED BY BOTH BUSINESS DIVISIONS

Quarters Rolling 12 months

Q1/18 vs. Q1/17:

17.3%

R12M Q1/18 vs.

R12M Q1/17:

+4.8%

15

23

9.4

24

0.4

65

.5

67

.9

59

.8 64

.2

59

.3

56

.9

54

.8

51

.4 59

.1

33

.6 %

33

.0 %

34

.0 %

34

.5 %

32

.3 %

33

.5 %

33

.1 %

31

.9 %

35

.3 %

31

.5 % 3

3.7

%

0

50

100

150

200

250

300

0.0 %

5.0 %

10.0 %

15.0 %

20.0 %

25.0 %

30.0 %

35.0 %

40.0 %

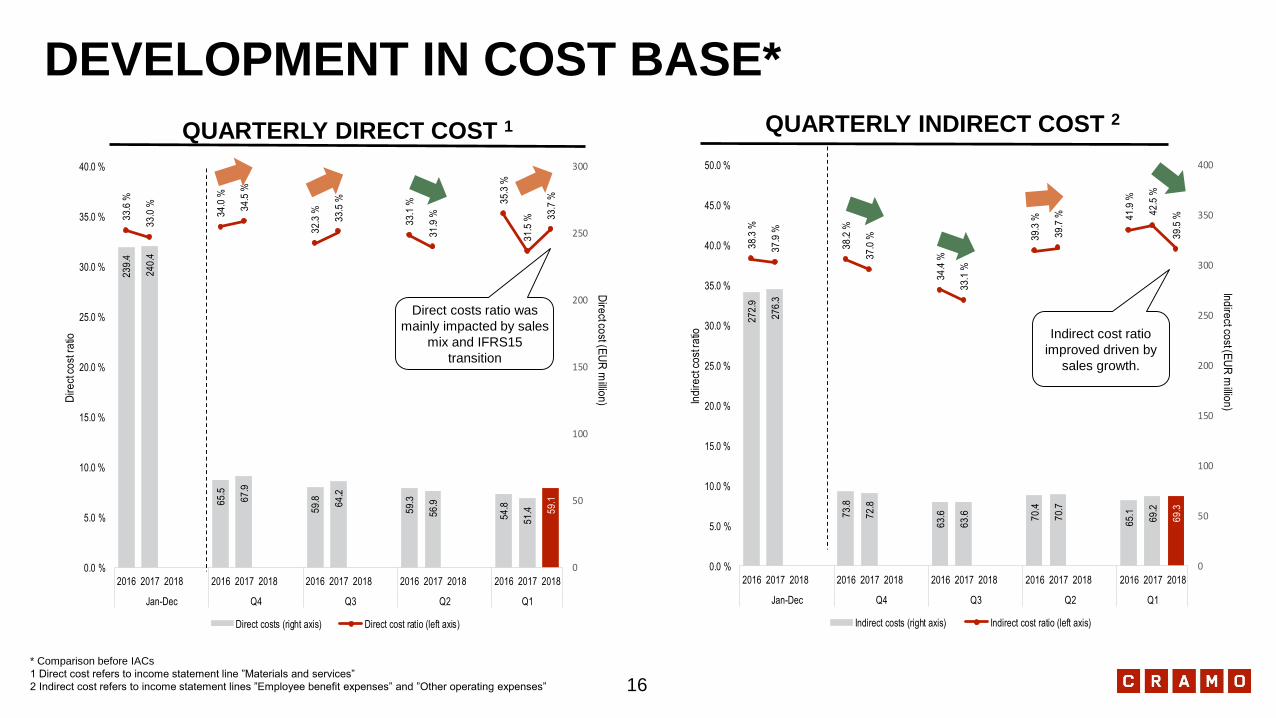

2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018

Jan-Dec Q4 Q3 Q2 Q1

Dire

ct cost (E

UR

millio

n)D

ire

ct c

ost

ra

tio

Direct costs (right axis) Direct cost ratio (left axis)

27

2.9

27

6.3

73

.8

72

.8

63

.6

63

.6 70

.4

70

.7

65

.1

69

.2

69

.3

38

.3 %

37

.9 %

38

.2 %

37

.0 %

34

.4 %

33

.1 %

39

.3 %

39

.7 % 4

1.9

%

42

.5 %

39

.5 %

0

50

100

150

200

250

300

350

400

0.0 %

5.0 %

10.0 %

15.0 %

20.0 %

25.0 %

30.0 %

35.0 %

40.0 %

45.0 %

50.0 %

2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018 2016 2017 2018

Jan-Dec Q4 Q3 Q2 Q1

Ind

irect co

st (EU

R m

illion

)Ind

ire

ct c

ost

ra

tio

Indirect costs (right axis) Indirect cost ratio (left axis)

* Comparison before IACs

1 Direct cost refers to income statement line ”Materials and services”

2 Indirect cost refers to income statement lines ”Employee benefit expenses” and ”Other operating expenses”

QUARTERLY INDIRECT COST 2QUARTERLY DIRECT COST 1

DEVELOPMENT IN COST BASE*

16

Direct costs ratio was

mainly impacted by sales

mix and IFRS15

transition

Indirect cost ratio

improved driven by

sales growth.

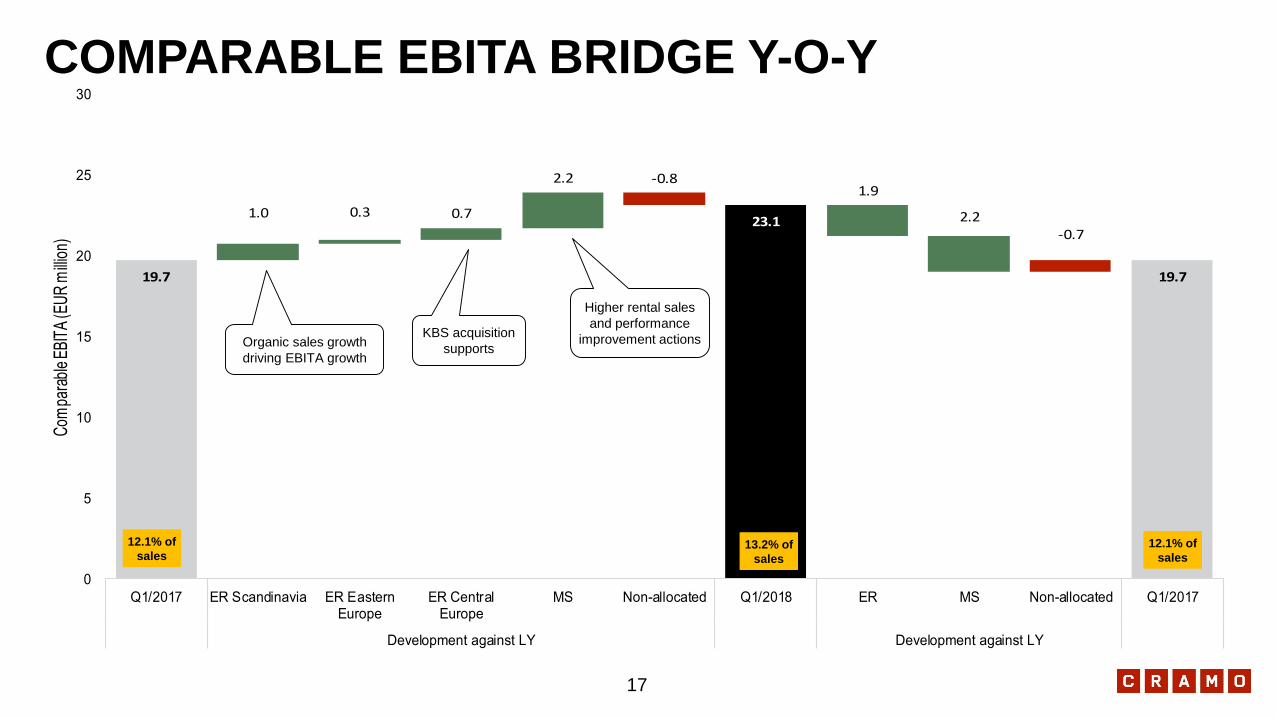

19.7

23.1

19.7

1.0 0.3 0.7

2.2 -0.81.9

2.2-0.7

0

5

10

15

20

25

30

Q1/2017 ER Scandinavia ER EasternEurope

ER CentralEurope

MS Non-allocated Q1/2018 ER MS Non-allocated Q1/2017

Development against LY Development against LY

Com

para

ble

EBIT

A (E

UR

milli

on)

COMPARABLE EBITA BRIDGE Y-O-Y

12.1% of

sales13.2% of

sales

12.1% of

sales

17

Organic sales growth

driving EBITA growth

KBS acquisition

supports

Higher rental sales

and performance

improvement actions

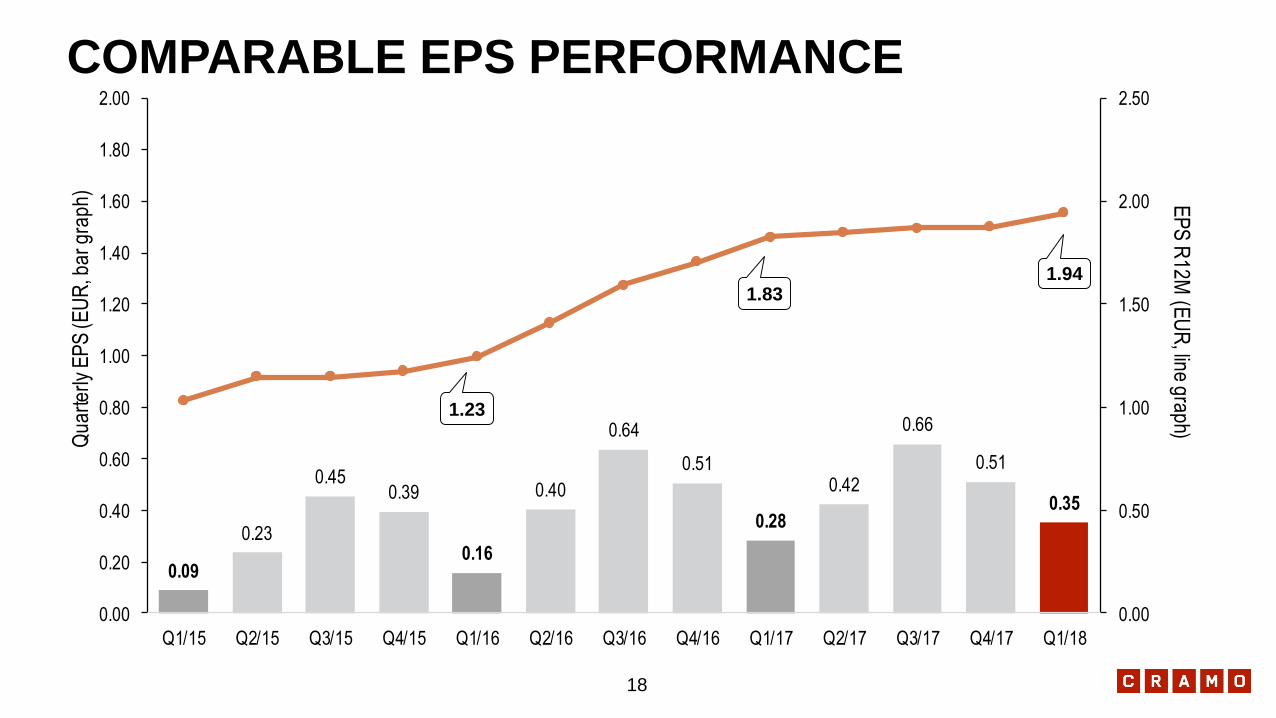

0.09

0.23

0.450.39

0.16

0.40

0.64

0.51

0.28

0.42

0.66

0.51

0.35

0.00

0.50

1.00

1.50

2.00

2.50

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17 Q3/17 Q4/17 Q1/18

EP

S R

12M (E

UR

, line graph)Q

ua

rte

rly

EP

S (

EU

R, b

ar

gra

ph

)COMPARABLE EPS PERFORMANCE

1.831.94

1.23

18

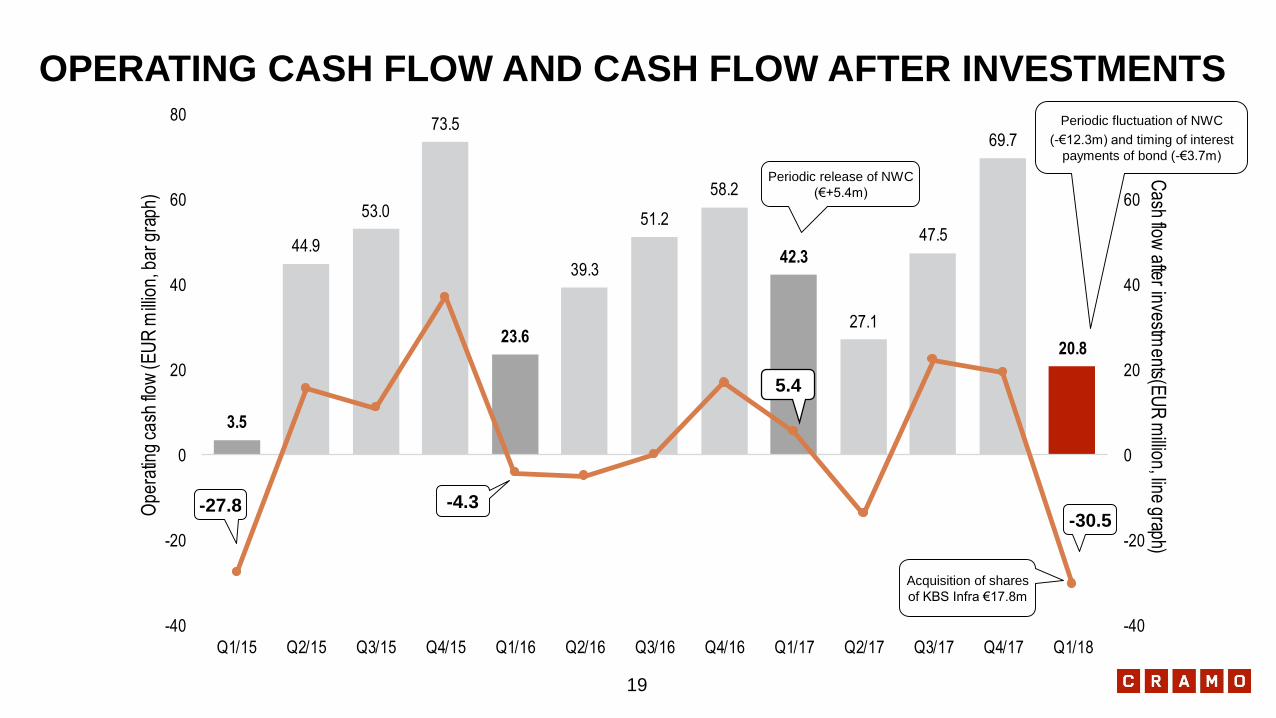

3.5

44.9

53.0

73.5

23.6

39.3

51.2

58.2

42.3

27.1

47.5

69.7

20.8

-40

-20

0

20

40

60

80

-40

-20

0

20

40

60

80

Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 Q1/17 Q2/17 Q3/17 Q4/17 Q1/18

Cash flow

after investments(E

UR

million, line graph)

Ope

ratin

g ca

sh fl

ow (

EU

R m

illio

n, b

ar g

raph

)

OPERATING CASH FLOW AND CASH FLOW AFTER INVESTMENTS

5.4

-4.3-30.5

Acquisition of shares

of KBS Infra €17.8m

19

Periodic fluctuation of NWC

(-€12.3m) and timing of interest

payments of bond (-€3.7m)

Periodic release of NWC

(€+5.4m)

-27.8

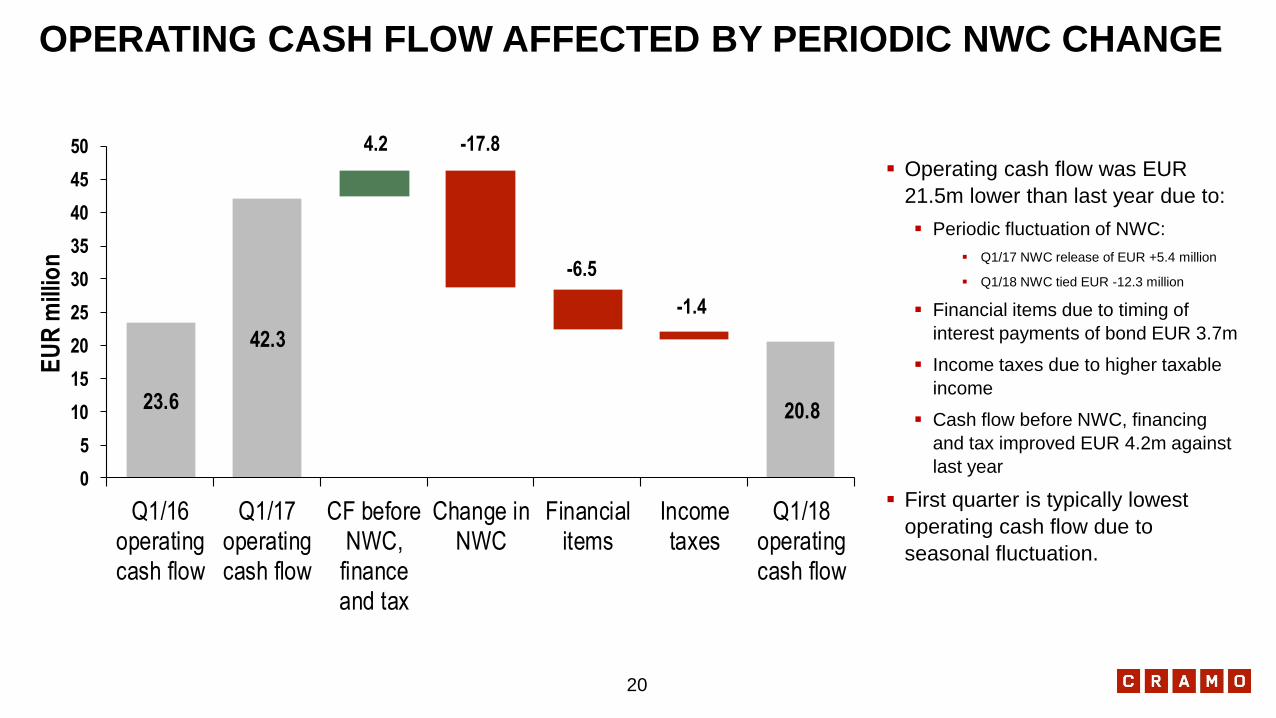

23.6

42.3

20.8

0

5

10

15

20

25

30

35

40

45

50

Q1/16operatingcash flow

Q1/17operatingcash flow

CF beforeNWC,

financeand tax

Change inNWC

Financialitems

Incometaxes

Q1/18operatingcash flow

EU

R m

illio

nOPERATING CASH FLOW AFFECTED BY PERIODIC NWC CHANGE

20

4.2 -17.8

-6.5

-1.4

▪ Operating cash flow was EUR

21.5m lower than last year due to:

▪ Periodic fluctuation of NWC:

▪ Q1/17 NWC release of EUR +5.4 million

▪ Q1/18 NWC tied EUR -12.3 million

▪ Financial items due to timing of

interest payments of bond EUR 3.7m

▪ Income taxes due to higher taxable

income

▪ Cash flow before NWC, financing

and tax improved EUR 4.2m against

last year

▪ First quarter is typically lowest

operating cash flow due to

seasonal fluctuation.

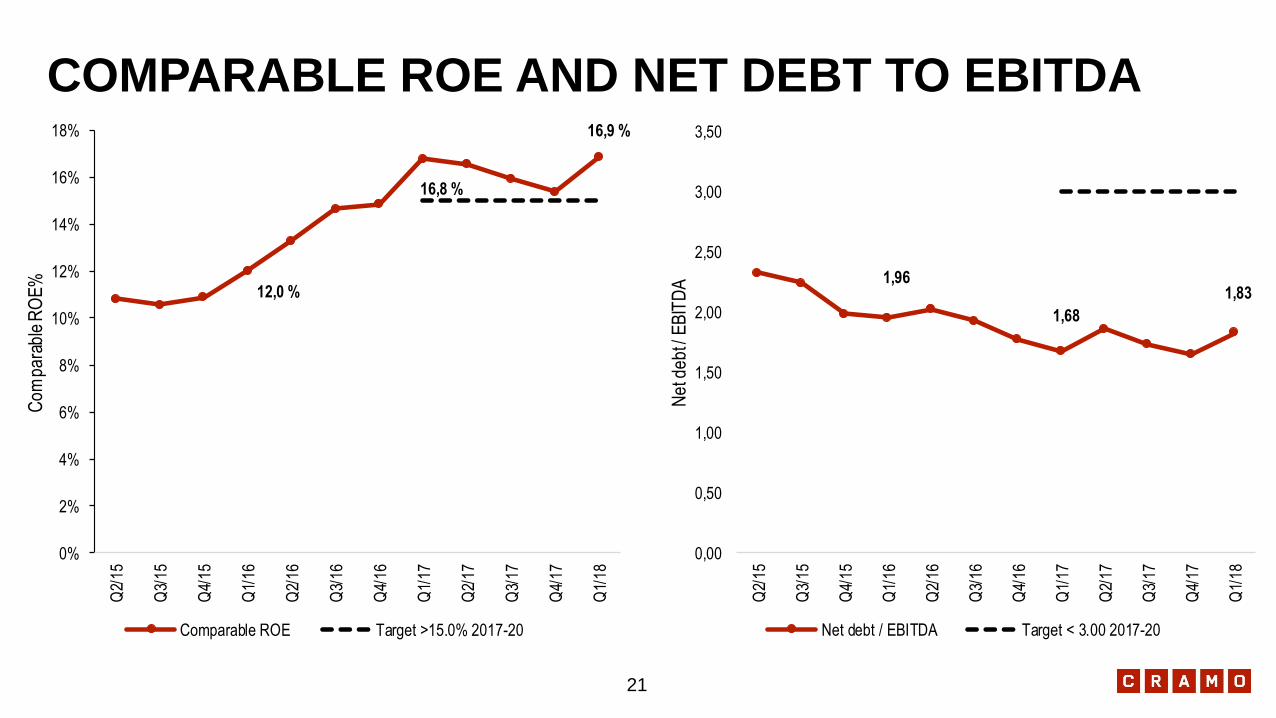

COMPARABLE ROE AND NET DEBT TO EBITDA

12,0 %

16,8 %

16,9 %

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%Q

2/15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Co

mp

ara

ble

RO

E%

Comparable ROE Target >15.0% 2017-20

1,96

1,68

1,83

0,00

0,50

1,00

1,50

2,00

2,50

3,00

3,50

Q2/

15

Q3/

15

Q4/

15

Q1/

16

Q2/

16

Q3/

16

Q4/

16

Q1/

17

Q2/

17

Q3/

17

Q4/

17

Q1/

18

Ne

t de

bt /

EB

ITD

A

Net debt / EBITDA Target < 3.00 2017-20

21

CONCLUSION

AND OUTLOOK

2018

22

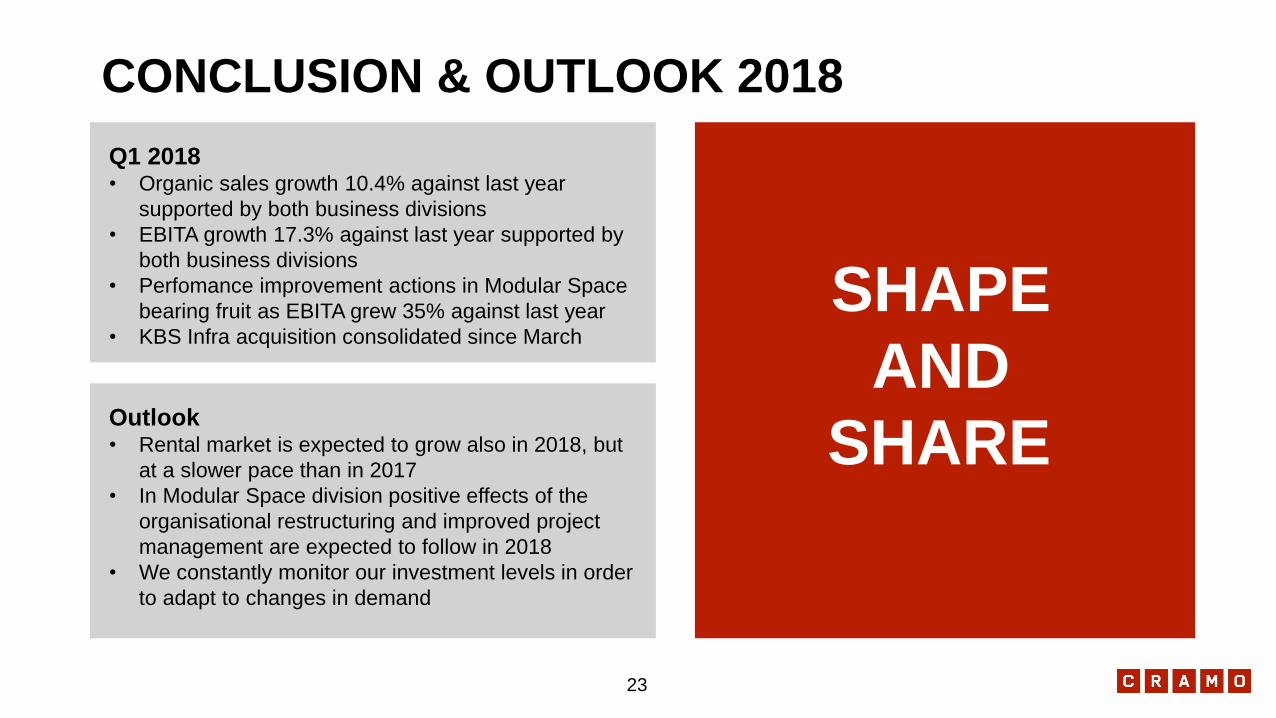

CONCLUSION & OUTLOOK 2018

SHAPE

AND

SHARE

Q1 2018• Organic sales growth 10.4% against last year

supported by both business divisions

• EBITA growth 17.3% against last year supported by

both business divisions

• Perfomance improvement actions in Modular Space

bearing fruit as EBITA grew 35% against last year

• KBS Infra acquisition consolidated since March

Outlook• Rental market is expected to grow also in 2018, but

at a slower pace than in 2017

• In Modular Space division positive effects of the

organisational restructuring and improved project

management are expected to follow in 2018

• We constantly monitor our investment levels in order

to adapt to changes in demand

23

![stream.kkr.mlit.go.jp[131] [1381 [138] [13.8] [lag] [18.7] Iga] [11 n 159] 029 009 [19.6] [195] [ [158] [16.1] [16.3] [162] [16.6] a. 49 [162 t1à,91 [13 [la 3] [13](https://img.pdfslide.net/doc/110x75/5e6d7c3cbb75887523501471/131-1381-138-138-lag-187-iga-11-n-159-029-009-196-195-158.jpg)