Embed Size (px)

Citation preview

Quantitative Easing and Equity Responses:

Insights from the MPC’s Framework

Georgios Chortareas*, Menelaos Karanasos**, and Emmanouil Noikokyris***

ABSTRACT

This paper explores the effects of Monetary Policy Committee's (MPC) asset purchase

announcements and communications on the UK stock market for the period 2009-2014. We

use intraday aggregate stock market data and an event study framework to assess the equities’

reaction, both their level and volatility, to survey-based measures for monetary policy stance

over a variety of time frames both preceding and following the MPC announcements. Our

results show that UK monetary policy shocks exhibit a significant impact on domestic equity

returns and volatilities. The strength of this impact hinges on the BoE’s information

dissemination through inflation reports and the MPC's voting records. Moreover, there is

evidence of news spillage prior to the announcement time.

JEL Codes: G14, E44, E52.

Keywords: Monetary Policy Committee (MPC), Intra-day data, equities response, monetary

policy shocks, equities volatility.

* Georgios Chortareas, School of Business and Management, King's College London, Franklin-Wilkins

Building, 150 Stamford Str., London SE1 9NH, UK, Email address: [email protected]

** (Corresponding author) Menelaos Karanasos Brunel University Business School, Brunel

University, Middlesex UB3 3PH, UK Email address: [email protected]

*** and Emmanouil Noikokyris Kingston Business School, Kingston University London, Kingston Hill,

Kingston upon Thames KT2 7LB, UK, Email address: [email protected]

1

1. Introduction.

The European Central Bank (ECB) initiated its quantitative easing (QE thereafter) program in

March 2015, and by the end of the same year decided to further expand the duration of the

program beyond September 2016, which was initially announced. Other central banks adopted

QE policies since late 2008 (US) and 2009 (UK) and an extensive literature analyzes their

effectiveness, with different conclusions about its effects on the real economy and financial

markets. In this paper, we examine the UK experience focusing on the reaction of stock market

returns and their volatility to asset purchases from the Bank of England’s (BoE thereafter)

Asset Purchase Facility (APF thereafter). Moreover, along with the introduction of QE by the

ECB its president has emphasized the unanimity of decisions in his introductory statement to

the press conference following the policy announcements. While the ECB's communication

framework is considered effective (Ehrmann and Fratzscher, 2007), the corresponding

framework of the BoE allows for important pieces of information to be disseminated on a

regular and systematic basis through the paraphernalia of inflation targeting. From this

perspective, the experience of UK's monetary policy implementation may constitute an

important reference point for the euro zone which takes its first steps in the implementation of

QE easing polices.

We consider the period from the onset of QE in September 2009 until March 2014,

during which the base policy rate of the BoE has been stable at the effective lower bound of

0.5%, and monetary policy is conducted through the APF's purchase of assets worth £375

billion funded by the expansion of the BoE’s balance sheet. While the impact of QE on

economic output and other macroeconomic variables can be long-lagged, the potential effect

on financial assets can be direct and more pronounced as the last respond faster to news. We

try to advance our understanding of how QE affects financial markets by considering the

impact of QE surprises not only on stock returns but on volatility as well. In addition, we

2

consider how the BoE's communication policy may affect the impact of QE policies on stock

returns.

In particular, the present paper pursues the following contributions. First, we examine

the implications of the BoE’s MPC (Monetary Policy Committee) framework for the

relationship between QE and stock returns focusing on the publication of inflation reports and

the MPC meetings minutes. To our knowledge this is the first attempt to analyze the role of

information releases (inflation forecasts and minutes) by the central bank in the context of QE

policies. Second, we examine the impact of BoE’s QE on equity returns volatility, as well as

the influence of the MPC framework on the magnitude of this relationship. To our knowledge

there is no other similar study for the UK, while scant evidence has been produced for the US.

We consider both implied and, several different types of, realized volatility. Third, we

investigate whether a significant pre-announcement drift exists in the UK as it has been

reported for the US (Lucca and Moench, 2015). Again this is the first attempt to identify the

presence of a drift in equity prices during the hours leading up to the BoE's MPC

announcements. Fourth, using survey-based measures of unexpected QE announcements and

intraday equity returns, we find that QE surprises have a minuscule impact on UK equities.

During the first hour following the MPC announcement there is no impact. When we consider

the wider sample, extending from 10 minutes before the announcements up to the end of the

announcement day, we find that smaller than expected asset purchases reduce equity prices.

A voluminous literature on the relationship between QE policies and asset prices has

evolved since the outbreak of the recent financial crisis and the subsequent adoption of QE

policies by many central banks around the globe. The bulk of evidence comes from the US and

employs event study frameworks to examine the reaction of financial assets' prices to central

bank QE announcements. This stream of literature typically gauges the efficacy of the Federal

Reserve’s QE as the cumulative change in the price of a financial asset in a short window

3

bracketing those QE related announcements (see e.g., Gagnon et al., 2011; D’Amico and King,

2013; Krishnamurthy and Vissing-Jorgensen, 2011; Meaning and Zhu, 2011; Neely, 2015;

Swanson, 2011), and its results point out to the effectiveness of QE in lowering longer-term

rates. Evidence also exists on the Fed’s QE programs impact on a wider array of financial

assets. Neely (2015), for instance, finds that Fed’s QE announcements lower global long-term

interest rates as well as the price of the dollar, while Meaning and Zhu (2011) find that large

scale asset purchases by the Fed increase equity prices and lower the level of implied volatility

in the market.

While the majority of the evidence concerns the impact of the asset purchases

conducted by the Fed, an active interest exists on the financial market implications of the BoE’s

QE program. In the UK, much of the extant literature examines the impact of QE

announcements on financial markets using event study frameworks, and the results from these

studies report significant reductions in government gilt yields in the wake of QE

announcements (e.g., Joyce et al., 2011; Breedon et al., 2012; Joyce et al., 2012; Joyce and

Tong, 2012). In terms of the equities reaction, however, the evidence produced from the early

days of the BoE’s QE program implementation is inconclusive. Breedon et al., (2012) suggest

that there is not a differential reaction of equity prices as a consequence of the bond purchase

operations during BoE’s first QE programme in 2009-2010. The results of Joyce et al. (2011),

however, who consider the same period show small and positive responses of equities which,

nevertheless are not uniform across all 6 QE announcements in the sample. While Breedon et

al., (2012) investigate the equities' reactions on the days that asset purchases were conducted,

Joyce et al. (2011) consider the days of asset purchases' announcements. In this paper we

identify the equity market implications of the BoE’s announcements about the APF asset

purchases by capturing the equities responses within a short window bracketing the QE

announcements. We assume that the forward-looking nature of the equity markets incorporates

4

the QE news on the announcement day and not on the day the asset purchases are conducted,

as is typically the case in the related literature (see e.g., Joyce et al., 2011 and Wright, 2012).

Nevertheless, our study is most closely related to those studies associating the size of equities

reaction with the amount of QE news released from each central bank announcement. The

unexpected element of QE announcements is calculated in a variety of ways using market data

(e.g., Gospodinov and Jamali, 2012; Rogers et al., 2014; Wright, 2012), economists’ surveys

(e.g., Cahill et al., 2013; Joyce et al., 2011; McLaren et al., 2014) and newspaper articles (e.g.,

Rosa, 2012).

The existing evidence for the UK shows small, if any, equity reactions to QE news from

MPC meetings. Rosa (2012) finds that until June 2011 equity returns in the first 25 minutes

following an MPC announcement are not associated with QE news from the MPC meeting.

Rogers et al. (2014) using data until 2014, find a positive reaction of equities in the first 15

minutes of the announcement to easing market-based monetary policy shocks which, however,

is smaller than that reported for the US. Both studies rely only on very short intraday windows

to gauge the equities reaction, and they do not examine how the BoE’s communication

framework might influence market expectations regarding MPC meeting announcements.

A key focus of this paper is to provide a characterization of the QE effects on asset

prices volatility, again by taking into account not only the policy announcements but also the

information content of the inflation reports and of the published MPC minutes. A considerable

amount of research on the impact of monetary policy on the intraday and daily asset prices

volatility has been produced mostly before the crisis and the implementation of QE policies.

Using daily data in an event study framework Gospodinov and Jamali (2012) find that both

historical and implied volatility of US equity returns respond significantly to monetary policy

shocks. In addition, monetary policy shocks emerge as a significant determinant of other

financial asset’s intraday realized volatility, including exchange rates and bond yields

5

(Andersson, 2010; Chuliá et al., 2010). Jubinski and Tomljanovich (2013) also find that

realized volatility is sensitive to the publication of FOMC meetings minutes. Nevertheless,

hardly one can find analyses of how stock market volatility responds to QE announcements.

The results of the present study extend the existing literature on the financial market

effects of QE by showing that the time-dimension over which reactions are measured, as well

as the communication framework of the BoE’s MPC determine the strength of the transmission.

We measure the association of the survey-based proxies for the unexpected element of BoE’s

QE announcements with intraday equity returns, both before and after the MPC meeting

announcements, as well as with reference to the publication of the inflation report and of the

voting record of the MPC members. Moreover, we offer a comprehensive study on the QE

effects on the volatility of returns using both implied volatility and a wide array of realized

volatility measures calculated over different daily and intraday periods.

In Section 2 we consider the effects of QE surprises and the implications of the MPC

framework for their transmission. Section 3 shifts focus to the analysis of stock market implied

and realized volatility in response to MPC's QE announcements, and finally Section 4

concludes.

2. Quantitative Easing and the Stock Market

2.1 Quantitative Easing and Equity returns.

In this section, we consider the effects of MPC meeting announcements on the UK equity

returns during the QE period spanning from 2009 to early 2014. Our empirical strategy relies

on an event study framework that captures the equities’ reaction to the unexpected element of

MPC announcements in a short window bracketing the announcement. This type of event study

6

methodology is the workhorse model for analyzing the impact of monetary policy on stock

returns both before the crisis and the introduction of quantitative easing (e.g., Bernanke and

Kuttner, 2005; Ehrmann and Fratzscher, 2004), and afterwards (Glick and Leduc, 2012; Joyce

et. al., 2011; Rogers et. al., 2014; Wright, 2012). Some aspects of this approach have been

particularly challenging, such as the choice of a proxy for the unexpected element of the MPC’s

announcement and the length of the window over which to measure the response (Gürkaynak

and Wright, 2013).

-Figure 1 here-

Fig. 1 shows the average cumulative stock market returns on the days of MPC

announcements in relation to equity returns when there is no MPC announcement. Since all

MPC announcements take place on Thursdays,1 when considering the non-MPC meeting days

we take stock returns on all Thursdays when there is no MPC announcement in order to avoid

any day of the week effect. Although the 5-minute average cumulative returns on the FTSE-

100 index on the 55 MPC announcements are indicative of an upward trend in stock prices on

these days (especially in the hours following the announcement), by the end of the day the

stock prices usually drop to their initial level. This pattern is in contrast to the cumulative mean

returns on all other Thursdays, excluding those coinciding with MPC announcements, which

show on average zero or slightly negative equity returns. The difference between the

cumulative mean returns on MPC and non-MPC days, however, is not statistically significant,

and all pointwise means of cumulative returns are not statistically different from zero at the

95% level of significance.

Thus, a casual inspection of the descriptive statistics is not supportive of a significant

equity response to QE news from MPC announcements. The increase in equity prices during

1 The only MPC announcement which did not take place on a Thursday is that of Monday, May 10th, 2010 because

of the general elections.

7

the hours leading up to the MPC announcement, however, points to the possibility of a pre-

announcement drift similar to that reported in the US by Lucca and Moench (2015). Moreover,

the significant variance of stock prices in the hours following the announcement is indicative

of a wider window during which the complete pass-through of the announcement materializes.

The effects of Quantitative Easing Surprises

The BoE's announcements have been subjected to intense scrutiny both during the period of

conventional monetary policy and during the recent years when unconventional practices have

been adopted. Moreover, under inflation targeting the BoE's monetary policy conduct is

characterized by increased transparency. Therefore, one would expect that the MPC's

announcements are to some extent anticipated by the market. Given that equity markets do not

react to anticipated pieces of information, disentangling stock market's reaction to MPC

meetings requires the identification of the unexpected element of MPC’s QE announcements.

To define the QE surprises, we use the difference between the actual amount of asset purchases

announced by the BoE and that expected by the market before the announcement, which is

derived as the average of the forecasts provided by economists taking part in Bloomberg’s

survey. Bloomberg surveys have also been used in previous studies to infer market expectations

about the BoE’s monetary policy decisions before the commencement of the QE period (e.g.,

Melvin et. al., 2010).

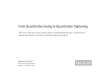

-Figure 2 here-

Although the economists’ estimates in this survey are produced about a week before

the MPC meeting, Fig. 2 shows that the size of the BoE’s APF purchases is to a great extent

anticipated by the market. Specifically, at 36 out of the 55 MPC meetings taking place during

the period under examination Bloomberg economists’ forecasts match the BoE’s

announcements, while for the rest of the announcements the divergence has been less than £10

8

billion and the market in all cases was expecting higher than realized asset purchases (the

surprises are of negative sign). The only exception is the announcement on October 6th, 2011

when asset purchases were £56.25 billion greater than that expected, resulting to a large

surprise with positive sign.

The Event Window

Another contentious aspect of the event study framework is the duration of the event window.

Recent papers examine the effects of unconventional monetary policy by capturing the equities'

response to quantitative easing announcements over a short intraday window surrounding the

announcement (e.g., Rogers et al., 201; Joyce and Tong, 2012). The idea of a narrow event

window has the appealing property that the reaction estimates are not contaminated by other

news arriving on the same day and influencing equities. A very narrow window in the context

of an event study, however, might also produce misleading results. There exists, for instance,

the possibility that markets might overreact to some announcements (Thornton, 2013).

Furthermore, the market might require some additional time to fully price unconventional

monetary policy news, because of the novelty of this method of monetary policy conduct in the

UK during a period of high turbulence and disruptions in the financial markets (Gagnon et. al.,

2011; Joyce et. al., 2011; Meaning and Zhu, 2011; Neely, 2015). In this study, we capture the

equities' reaction using two intraday windows. Both windows start at 11:50am, which is 10

minutes before the announcement, but the narrower window finishes 1-hour after the MPC

announcement at 1pm, while the wider one spans up to the closing of the trading day.

The Baseline Model

9

We measure the impact of QE news on domestic equities using the following empirical

specification:

, (1)

where rt stands for the FTSE-100 index returns calculated over the two alternative event

windows described above, and St stands for the unexpected element of the MPC’s quantitative

easing announcement on the 55 announcement days t of MPC meetings that we are considering

in our study. The coefficient estimate βMP captures equities’ reaction to unexpected asset

purchases by the Bank. We start our estimations from September 2009, when the Bloomberg

survey data have become available, and we consider the period until March 2014. We report

our results using robust regression M-estimators in order to control, for the unduly influence

of outliers on our results (see also Rogers et. al., 2014),

-Table 1 here-

The results from the estimation of Eq. (1), reported in Table 1, show that the size of

equities’ reaction to Bank’s QE news hinges on the length of the event window. While during

the first hour after the announcement QE surprises do not exert an impact on equity prices,

when the event window is up to the end of the day the reaction estimate is positive and

statistically significant. Although the reaction estimate is of minuscule size, it suggests that

smaller than expected asset purchases reduce equity prices. In particular, if the BoE’s actual

asset purchases are smaller by £1 billion from what expected by the economists participating

in Bloomberg’s survey, equities drop by 0.03%.

2.2 The MPC Framework and its Implications

tt

MP

t Sar

10

To formally assess the role of the MPC framework, and in particular of the inflation report

release and of the MPC meetings minutes publications, we employ an empirical specification

consistent with that used by Chortareas and Noikokyris (2014), and we consider the specific

effects of news about asset purchases on the first, second, and third MPC meeting following

the release of the inflation report. Moreover, we investigate the marginal impact of QE news

on those MPC meetings announcements immediately following news about unanimity in the

previous MPC meeting. Specifically, we estimate the following regression:

, (2)

where I1 , I

2 and I3 are 0-1 dummy variables taking the value of 1 on the 19 first, 18 second and

18 third MPC meetings following the release of the inflation report respectively, and zero

otherwise. IUNA is a 0-1 dummy variable taking the value of 1 on the 27 MPC meeting days

directly following MPC meetings minutes releases indicating unanimity in the decision of the

previous MPC meeting regarding the size of BoE’s APF purchases. Finally, IAP is a 0-1 dummy

variable taking the value of 1 on the 4 MPC meetings when there was a change in the size of

the program.

The results from the estimation of Eq. (2), reported in Table 1, show that during the

first hour after the MPC announcement equities react to those MPC announcements which

directly follow or precede the two elements of the MPC framework attracting most of the public

attention; the inflation report release and a unanimous MPC decision. In particular, we find that

on MPC meetings taking place a week before the inflation report release smaller than expected

asset purchases are perceived as good news by the stock market increasing stock prices. To the

extent that the announcement reveals MPC members’ private view on future economic

conditions, smaller than expected asset purchases might be perceived as a possibility of better

tt

AP

t

UNA

tttt SISISISISIar 54

3

3

2

2

1

1

11

than expected news from the forthcoming inflation report release, constituting essentially this

MPC meeting a forerunner of the inflation report.

On MPC meeting days following news of a unanimous decision in the previous

committee meeting, the positive reaction estimate suggests that stock prices drop following

news about smaller than expected asset purchases. This finding of a more pronounced

transmission on these occasions is consistent with that observed during the conventional

monetary policy conduct period from 1994 to 2008 (Chortareas and Noikokyris, 2014).

Considering the individualistic nature of the MPC’s decision-making process (Blinder and

Wyplosz, 2004), the dissenting votes and the discussions explaining them, constitute an integral

part of the information set available to investors. The absence of opposing views, can be

interpreted as a limitation to the information available to investors about future monetary

policy, which in turn can lead to overreactions. The lack of dissenting votes, however, can also

be perceived as a strong signal about MPC members’ intentions increasing the informational

content of the MPC meetings decisions. If the last is the case, we should expect investors to

uniformly adjust their pricing discovery process reducing equity returns volatility. If the lack

of dissenting votes, however, creates uncertainty over the way MPC members view current and

future economic activity, this will raise volatility.

When, however, the wider event window is considered, we find that UK equities

respond only to QE surprises from the second MPC meetings following inflation report

releases. The absence of a statistically significant relationship between QE surprises and

equities on the first and third MPC meetings following the inflation report release illustrates

the informational dominance of the inflation report on the market participants’ expectations

about the future monetary policy stance and economic output. The equity market reacts to QE

news from MPC meetings only when there has not been an inflation report during the past

month or only when it is not awaiting an inflation report within the following week. In the first

12

hour we report a reaction to news attracting media attention, such as unanimity in MPC

decisions or imminent inflation report releases, while when there is enough time to process the

announcement the market seems to respond, in a manner consistent with theory, to the

economic news deriving from the announcement. The finding that the BoE’s MPC framework

weights differently in investors’ price discovery process, depending on the event window

employed, is indicative of the difficulties that stock market participants face when pricing the

QE news.

2.3 The Pre-Announcement Drift

In this section we investigate whether equity returns exhibit systematic large values in

the hours leading up to the MPC announcement. In Fig. 1, we show that, although statistically

insignificant, equities display an upward drift in the hours before the announcement. To

formally examine the presence of a pre-announcement drift, we investigate whether returns are

systematically larger during the time leading up to the MPC announcement using the following

empirical specification of Lucca and Moench (2015):

t

MPCpre

tt Iar . (3)

In Eq. (3) rt stands for the returns on the FTSE-100 Index from the start of the trading

day until 11:55am, while MPCpreI is a dummy variable taking the value of 1 for the 55 pre-

announcement windows which are followed directly by MPC announcements and zero

otherwise. To ensure that our results are not driven by the choice of the size of the pre-

announcement window, we also employ a wider window over which we measure stock returns

which starts at 12 noon on the previous to the announcement day. We report the results from

the estimation of Eq. (3) in Table 2, and, similarly to Lucca and Moench (2015), they are not

13

indicative of significant pre-announcement effects. In particular, coefficient estimates β for the

dummy variables for both pre-announcement windows are statistically insignificant (columns

(1) and (2) in Table 2), and they remain so even after we trim our sample from the top and

bottom 1% stock returns (columns (3) and (4) in Table 2).

-Table 2 here-

To analyze the pattern of the pre-MPC stock returns more carefully, we also examine

whether they are associated with economic activity, stock market uncertainty, and ex-post QE

surprises following the original specification of Lucca and Moench (2015). To start with, we

explore the extent to which pre-MPC returns are associated with the annual growth rate of the

industrial production index and the consumer price index. We obtain the growth rate of both

variables using data from OECD’s real time and revisions database.2 The results from this

regression, presented in column (5) of Table 2, do not show strong association with the

economic activity variables. The pre-MPC equity returns, however, exhibit strong positive

association with stock market uncertainty, measured by the closing level of the FTSE IVI Index

two days before the announcement, and with the ex-post monetary policy surprises as shown

in columns (6) and (7) of Table 2 respectively. The existence of a statistically significant

relationship between pre-MPC returns and ex-post QE surprises is an indication of news

spillage, and might explain the numerically small reaction estimate of equities to QE news that

we have shown above when this relationship is considered for samples starting 10 minutes

before the announcement.

3. The MPC Announcements and Stock Market Volatility

Implied versus Realized Volatility

2 All variables enter the regressions demeaned and normalized by their standard deviation.

14

In this section we investigate the effects of the MPC announcements on the UK stock market

volatility. In order to gauge the response of the volatility to the unexpected element of the

Bank’s asset purchases announcements, we employ the event study framework from the

previous section. We consider several measures of daily and intra-day volatility, both historical

(realized) and implied, to provide a complete characterization of the impact of the 55 MPC

announcements considered in this study.

We begin by examining the association of the unexpected element of BoE’s QE

announcements with UK stock market’s realized and implied volatility. The measure of implied

volatility (IV) we use is the FTSE-100 implied volatility index. This index measures the

interpolated 30-day expected volatility, and is calculated using the prices of out-of-money

traded options. Data for the realized volatility of the FTSE-100 Index (RV) are taken from

Oxford-Man Institute’s “realized library” (Gerd et al., 2009). The measures for realized

variance are produced daily using high frequency data from that day only. We use the event

study framework employed in the previous section to obtain the reaction of these two measures

of volatility on the QE surprises from MPC meetings. In particular, we estimate the following

regression which captures the specific impact of QE surprises from the first, second, and third

MPC meeting following the release of the inflation report on equity volatilities, as well the

marginal reaction of the volatility to MPC announcements following news about a unanimous

decision and about a change in the size of BoE’s APF:

. (4)

ΔVt now stands for the first difference of implied (ΔIVt) or realized volatility (ΔRVt).

-Table 3 here-

tt

AP

t

UNA

tttt SISISISISIaV 54

3

3

2

2

1

1

15

We report the results from the M-estimation of the regression in Eq. (4) for the response

of implied volatility to QE surprises in column (1) of Table 3. As the results reveal QE surprises

do not influence the level of implied volatility in the market. The statistically insignificant

reaction of the daily changes in volatility to QE surprises suggests that expected volatility in

the UK stock market is not influenced by news regarding asset purchases emerging from MPC

meeting announcements. The statistically significant and of negative sign estimate for the

intercept, however, suggests that markets revise downwards their expectations regarding the

volatility over the next 30 days in response to the announcement. Expectations about lower

volatility could be attributed to the coordination of investors’ beliefs in the wake of the MPC

meeting announcement. For instance, Ehrmann and Sondermann (2012) find that certain

macroeconomic announcements, as well as the Banks’ inflation report release, reduce UK stock

market's conditional volatility when controlling for the news included in them.

Our results regarding the reaction of realized volatility to QE surprises on MPC meeting

days are reported in column (2) of Table 3. Contrary to implied volatility that reduces in the

wake of an MPC meeting announcement, our results show that the level of the realized variance

increases, and the difference between these two intercept estimates is statistically significant

as shown in column (3) of Table 3. Moreover, when we analyze the association between QE

news from MPC announcements and realized volatility, our results show that smaller than

expected asset purchases reduce daily realized volatility on the second MPC meeting days

following inflation report releases, unless this announcement increases the size of BoE’s APF,

when in this case realized volatility increases. These results suggest that news about smaller

than expected asset purchases on MPC meetings when no changes in the size of the amount of

asset purchases have taken place reduces not only equity prices (see Table 2), but also reduces

the realized volatility. The equity market appears not only to incorporate the news regarding

16

BoE’s asset purchases in a manner consistent with theoretical priors, but also the BoE achieves

to do so by coordinating market expectations.

Robustness Checks

To investigate further whether the reported reaction of realized volatility hinges on the measure

employed and, in particular, on whether stock market data only from the MPC meeting

announcement day are employed to gauge that day’s realized volatility, we also use two

alternative proxies for realized volatility that have been used in previous research. The first one

is the forward looking measure for (annualized) realized variance of Gospodinov et al. (2006)

which is also used in Gospodinov and Jamali (2012). Based on this specification the stock

market’s realized volatility on day t (RVG) is constructed using the 22 days-ahead squared stock

returns as follows:

, (5)

where τ stands for the days-ahead of day t and takes the value of 22. The second measure for

realized volatility is that used by Chuliá et al. (2010) and is constructed as follows:

252),

(

2

u

k

C

t ktRRV , (6)

where Rk is the 5-minute returns on the FTSE-100 Index on day t, and u measures all 5-minutes

intervals on trading day t. The first 5-minute interval following the MPC announcement is

excluded from the calculation of the realized volatility on MPC announcement days.

The results from the estimation of Eq. (4) when the dependent variable is ΔRVG and

ΔRVC are reported in columns (4) and (5) of Table 3 respectively. Our results show that the

2521

1

2

,

ti

i

G

t rRV

17

realized volatility, when measured using daily returns from 22 days ahead, does not respond to

QE surprises, as all reaction estimates are statistically insignificant. However, when the

realized volatility of stock returns on MPC announcement days is calculated from Eq. (6), using

intraday data from that day only, our results are similar to those obtained when we use the

realized volatility from Gerd et al. (2009) database. The absence of a significant response when

the measure is constructed excluding data from the MPC announcement day suggests that the

MPC announcements’ impact is traced only on the announcement day.

-Table 4 here-

Intraday Volatility

Finally, in this section we also use the same regression of Eq. (2) in order to study the impact

of MPC announcements on intraday measures of UK equity returns volatility. We use two

measures of intraday volatility in order to gauge the impact of the MPC announcement on UK

equity volatility in the hour bracketing the announcement. The first one is obtained from Eq.

(6), but now instead of calculating the daily realized volatility, we calculate equities’ realized

volatility for the period starting 10 minutes before the announcement up until 1 hour after the

announcement.

The second measure is the change in volatility ratios (ΔVolR) for equity returns used by

Andersson (2010). This measure of volatility presents the difference between the volatility ratio

in the hour following the MPC announcement and the volatility ratio for the 30 minutes before

the announcement. The volatility ratio for returns on FTSE-100 index is calculated using the

5-minute returns on the index, and is measured as the ratio of stock returns volatility on day t

of an MPC announcement for a specific period of time (either the 30 minutes before the

18

announcement or the 1 hour following the announcement) to stock returns volatility on all other

Thursdays in our sample excluding MPC announcements for the same time frames. So if t

stands for the days of monetary policy decisions, and d=1,2…,D stands for the same weekdays

but when no MPC announcement has taken place, and R is the 5-minutes log returns then the

volatility ratio is given as follows:

)(1

)(

)(1

)(

1

]0,30[

]0,30[

1

]1,0[

]1,0[

]1,30[ D

d

d

m

t

m

D

d

d

h

t

ht

hm

RabsD

Rabs

RabsD

RabsvolR . (7)

We now regress these two variables on the same independent variables as in Eq. (2),

except that now we use the absolute value of the surprise. Results from the M estimation of

these regressions are reported in Table 4. Our results show that QE surprises increase equities

volatility on MPC meetings preceding by a week the inflation report release (reaction estimate

to the interactive term I3 x abs|St| is positive and statistically significant), unless these MPC

meetings follow news about unanimity in the previous MPC meeting when we report a negative

marginal reaction (reaction estimate to the interactive term IUNA x abs|St| is negative and

statistically significant). Considering that MPC meetings directly preceding the inflation report

release might be perceived as bearing news about the forthcoming inflation report, this

speculation appears to be increasing volatility. Moreover, we find that the QE news directly

following news about unanimity in the most recent MPC meeting decreases volatility in the

equity market, as possibly investors uniformly incorporate the news in their equity pricing

models.

4. Concluding Remarks

19

This paper considers the effects of the UK’s QE program on equity prices and their volatility.

We use an event-study framework and intra-day data to characterize the equity prices reactions

to BoE’s QE announcements. The key contributions of the paper include the relatively

unexplored to date effects of QE on stock price volatility and the association of the magnitude

of the pass-through of QE news into UK equities with the MPC framework. To capture the last,

we focus on two key paraphernalia of inflation targeting, namely the publication of inflation

reports and of the MPC members voting decision.

Our results are generally indicative of a statistically significant relationship between

QE surprises and equity returns on the days of MPC meeting announcements, which, however,

is of small magnitude. Although our evidence reiterates prior findings about a statistically

significant impact of QE announcements on intraday UK equity prices (Rogers, et al. 2014),

we also provide a comprehensive analysis of the time dimension of this impact, and of the role

of BoE’s communication policy. Moreover, we find a significant pre-announcement upward

drift in UK equity prices during the period considered, which partly accounts for the less

pronounced impact of QE announcements on equities.

Our evidence suggests that equity markets react differently to QE news in the hour

following the announcement and in the hours until the end of the trading day. In particular, in

the first hour following the MPC meeting announcements, equities react significantly and in a

manner intuitively expected only to those MPC meetings announcements following news about

a unanimous decision in the previous MPC meeting. QE news from these MPC meetings

announcements also appear to reduce stock price volatility. When the impact of QE news from

MPC meeting announcements preceding by a week the inflation report release is considered,

however, the results reveal a different pattern. This QE news appears not only to increase

volatility in equity markets during the hour following the announcement, but also the equities’

reaction is confusing. Smaller than expected asset purchases are now perceived as positive

20

news leading to slightly higher equity prices, as perhaps they are perceived to be indications of

the news included in the forthcoming inflation report.

In our study, while equities during the first hour following an announcement are

sensitive to news from MPC meetings attracting media attention (e.g., unanimous decisions

and imminent inflation report releases), when the wider window is considered a different

picture emerges. Equities returns and volatility appear to respond significantly, both in

magnitude and statistically, only to QE surprises emerging from the second MPC meetings

following inflation report releases. These MPC meetings occur almost two months after the

previous inflation report release and at least a month further from the new inflation report,

reinforcing the view that the inflation report is a dominant channel of BoE’s information

dissemination process.

In general, we find evidence of a significant impact of QE surprises on UK equities.

The communication framework of the BoE is an important factor determining the pass-through

of QE announcements to the stock market. The inflation report release emerges as a reference

point for the BoE communication and news about the MPC decisions unanimity appears to

increase the magnitude of the transmission. The results from the UK experience offer the

benefit of hindsight to think about the effectiveness of similar QE programs such as that of the

ECB, which is at its early stages of implementation. The increasing emphasis on the unanimity

of decision put by the ECB president's introductory statement to the press conference and the

corresponding media interest, signifies the importance of obtaining a better understanding of

the role of central banks’ communication.

21

REFERENCES

ANDERSSON, M., 2010. Using Intraday Data to Gauge Financial Market Responses to

Federal Reserve and ECB Monetary Policy Decisions. INTERNATIONAL JOURNAL OF

CENTRAL BANKING, 6(2), pp. 117-146.

BERNANKE, B.S. and KUTTNER, K.N., 2005. What Explains the Stock Market's Reaction

to Federal Reserve Policy? The Journal of Finance, 60(3), pp. 1221-1257.

BLINDER, A. S., WYPLOSZ, C., 2005. Central bank talk: Committee structure and

communication policy. Presented at the ASSA meetings, Philadelphia, January.

BREEDON, F., CHADHA, J.S. and WATERS, A., 2012. The financial market impact of UK

quantitative easing. Oxford Review of Economic Policy, 28(4), pp. 702-728.

CAHILL, M.E., D’AMICO, S., LI, C. and SEARS, J.S., 2013. Duration Risk versus Local

Supply Channel in Treasury Yields: Evidence from the Federal Reserve's Asset Purchase

Announcements. Finance and Economics Discussion Series 2013-35. Board of Governors of

the Federal Reserve System (U.S.).

CHORTAREAS, G. and NOIKOKYRIS, E., 2014. Monetary policy and stock returns under

the MPC and inflation targeting. International Review of Financial Analysis, 31(0), pp. 109-

116.

CHULIÁ, H., MARTENS, M. and DIJK, D.V., 2010. Asymmetric effects of federal funds

target rate changes on S&P100 stock returns, volatilities and correlations. Journal of Banking

& Finance, 34(4), pp. 834-839.

D’AMICO, S. and KING, T.B., 2013. Flow and stock effects of large-scale treasury purchases:

Evidence on the importance of local supply. Journal of Financial Economics, 108(2), pp. 425-

448.

EHRMANN, M. and FRATZSCHER, M., 2004. Taking Stock: Monetary Policy Transmission

to Equity Markets. Journal of Money, Credit and Banking, 36(4), pp. 719-737.

EHRMANN, M. and FRATZSCHER, M., 2007. Communication by central bank committee

members: different strategies, same effectiveness? Journal of Money, Credit and Banking,

39(2/3), 509-541.

EHRMANN, M. and SONDERMANN, D., 2012. The News Content of Macroeconomic

Announcements: What if Central Bank Communication Becomes Stale? International Journal

of Central Banking, 8(3), pp. 1-53.

GAGNON, J., RASKIN, M., REMACHE, J. and SACK, B., 2011. The Financial Market

Effects of the Federal Reserve’s Large-Scale Asset Purchases. INTERNATIONAL JOURNAL

OF CENTRAL BANKING, 7(1), pp. 3-43.

GERD, H. LUNDE, A. SHEPHARD, N. AND SHEPPARD, K. (2009) "Oxford-Man Institute's

realized library v0.2", Oxford-Man Institute, University of Oxford.

22

GLICK, R. and LEDUC, S., 2012. Central bank announcements of asset purchases and the

impact on global financial and commodity markets. Journal of International Money and

Finance, 31(8), pp. 2078-2101.

GOSPODINOV, N., GAVALA, A. and JIANG, D., 2006. Forecasting volatility. Journal of

Forecasting, 25(6), pp. 381-400.

GOSPODINOV, N. and JAMALI, I., 2012. The effects of Federal funds rate surprises on S&P

500 volatility and volatility risk premium. Journal of Empirical Finance, 19(4), pp. 497-510.

GÜRKAYNAK, R.S. and WRIGHT, J.H., 2013. Identification and Inference Using Event

Studies. The Manchester School, 81, pp. 48-65.

JOYCE, M., LASAOSA, A., STEVENS, I. and TONG, M., 2011. The Financial Market Impact

of Quantitative Easing in the United Kingdom. INTERNATIONAL JOURNAL OF CENTRAL

BANKING, 7(3), pp. 113-161.

JOYCE, M.A.S., MCLAREN, N. and YOUNG, C., 2012. Quantitative easing in the United

Kingdom: evidence from financial markets on QE1 and QE2. Oxford Review of Economic

Policy, 28(4), pp. 671-701.

JOYCE, M.A.S. and TONG, M., 2012. QE and the Gilt Market: a Disaggregated Analysis*.

The Economic Journal, 122(564), pp. F348-F384.

JUBINSKI, D. and TOMLJANOVICH, M., 2013. Do FOMC minutes matter to markets? An

intraday analysis of FOMC minutes releases on individual equity volatility and returns. Review

of Financial Economics, 22(3), pp. 86-97.

KRISHNAMURTHY, A. and VISSING-JORGENSEN, A., 2011. The Effects of Quantitative

Easing on Interest Rates: Channels and Implications for Policy. Brookings Papers on Economic

Activity, 43(2 (Fall)), pp. 215-287.

LUCCA, D.,O and MOENCH, E., 2015. The Pre-FOMC Announcement Drift. Journal of

Finance, 70(1), pp. 329-371.

MCLAREN, N., BANERJEE, R.N. and LATTO, D., 2014. Using Changes in Auction Maturity

Sectors to Help Identify the Impact of QE on Gilt Yields. The Economic Journal, 124(576),

pp. 453-479.

MEANING, J. and ZHU, F., 2011. The impact of recent central bank asset purchase

programmes. BIS Quarterly Review, December, pp. 73-83.

MELVIN, M., SABOROWSKI, C., SAGER, M. and TAYLOR, M.P., 2010. Bank of England

Interest Rate Announcements and the Foreign Exchange Market INTERNATIONAL

JOURNAL OF CENTRAL BANKING, 6(3), pp. 211-247.

NEELY, C.J., 2015. Unconventional monetary policy had large international effects. Journal

of Banking & Finance, 52, pp. 101-111.

23

ROGERS, J.H., SCOTTI, C. and WRIGHT, J.H., 2014. Evaluating asset-market effects of

unconventional monetary policy: a multi-country review. Economic Policy, 29(80), pp. 749-

799.

ROSA, C., 2012. How "Unconventional" Are Large-Scale Asset Purchases? The Impact of

Monetary Policy on Asset Prices. Federal Reserve Bank of New York Staff Reports 560, (May).

SWANSON, E., 2011. Let's Twist Again: A High-Frequency Event-study Analysis of

Operation Twist and Its Implications for QE2. Brookings Papers on Economic Activity, 42(1

(Spring)), pp. 151-207.

THORNTON, D.L., 2013. The Identification of the Response of Interest Rates to Monetary

Policy Actions using Market-Based Measures of Monetary Policy Shocks. Oxford Economic

Papers,66(1), pp. 67-87.

WRIGHT, J.H., 2012. What does Monetary Policy do to Long-term Interest Rates at the Zero

Lower Bound?*. The Economic Journal, 122(564), pp. F447-F466.

24

TABLES AND FIGURES

TABLE 1

QE SURPRISES AND UK EQUITY RETURNS

(1) (2) (3) (4)

c .006

(0.21)

0.04

(0.48)

.008

(0.29)

-.001

(-0.01)

St -.004

(-1.05)

0.03**

(2.43)

- -

I1 St - - 0.03

(1.53)

-0.01

(-0.15)

I2 St - - 0.01

(0.43)

0.18**

(2.18)

I3 St - - -0.06**

(-2.28)

-0.07

(-0.86)

IUNA St - - 0.06**

(2.10)

0.13

(1.36)

IAP St - - -0.01

(-0.57)

-0.15*

(-1.81)

R2(%) 2.17 6.37 11.39 15.24

Notes: In columns (1) and (2), we report results from the estimation of

Eq. (1). Two different event windows for the calculation of stock

returns are employed; Both start 10 minutes before the MPC

announcement and the narrow one ends 1 hour after the announcement

(r[-10,+1h]), while the wider one extends up to the closing of the trading

day (r[-10,close]). St denotes the unexpected element of the MPC’s QE

announcement, which is calculated as the difference between the

actual asset purchases of the Bank and the mean of economists’

estimates regarding the amount of Bank’s asset purchases taken by

Bloomberg’s survey. We examine 55 MPC announcements starting

from September 2009 when the Bloomberg survey data are available

until March 2014. In columns (3) and (4) we report the results from

Eq. (2) where I1 (I2 / I3) are 0-1 dummy variables taking the value of 1

on first (second / third) MPC meeting following the release of the

inflation report and zero otherwise. IUNA is a 0-1 dummy variable

taking the value of 1 on MPC meeting days directly following MPC

meeting minutes releases indicating unanimity in the decision of the

previous MPC meeting about asset purchases.

*/**/*** denote significance at 90%, 95%, and 99% confidence levels

respectively.

hr 1,10 closer ,10 hr 1,10 closer ,10

25

TABLE 2

PRE-MPC Announcement Returns (1) (2) (3) (4) (5) (6) (7)

(excl. top/bottom 1%)

(excl. top/bottom 1%)

c -0.03*

(-1.70) 0.01

(0.33) -0.03*

(-1.70) 0.02

(0.71) 0.10

(1.13)

0.14

(1.44)

0.14

(1.36) MPCpre

tI 0.17

(1.62) 0.24

(1.54) 0.07

(0.88) 0.17

(1.18) - - -

Δ(IP)t - - - - 0.23*

(1.88)

- -

Δ(INF)t - - - - 0.14

(1.18)

- -

(FTSE-IVI) t - - - - - 0.29***

(2.79)

-

S t - - - - - - 0.15***

(9.50)

Obs. 1,150 1,150 1,128 1,128 55 55 55

MPC Ann. 55 55 54 54 55 55 55

Notes: This table reports the results from Eq. (3) in the main body of the text. MPCpreI

is a dummy variable taking the value of 1

on the 55 pre-announcement windows which are directly followed by MPC announcements and zero otherwise. Δ(IP)t denotes the

annual growth in the industrial production index and Δ(INF)t is the annual growth in Consumer Price Index. (FTSE IVI)t stands for

the level of the FTSE 100 implied volatility index on the closing two days before the MPC announcement. St is the unexpected

element of the MPC’s quantitative easing announcement. Huber-White standard errors for the estimates are reported in the

parentheses.

*/**/*** denote significance at 90%, 95%, and 99% confidence levels respectively.

]55:118[ amamr ]55:1112[ ampmr

]55:118[ amamr ]55:1112[ ampmr

]55:118[ amamr ]55:118[ amamr ]55:118[ amamr

26

TABLE 3

QE SURPRISES AND DAILY CHANGES IN EQUITY VOLATILITY

(1) (2) (3) (4) (5)

ΔIV ΔRV βIV=βRV

[Sign.]

ΔRVG ΔRVC

c -0.75***

(-2.99)

1.08***

(3.22)

[0.00] -0.07

(-1.01)

1.08***

(2.54)

I1 St 0.12

(0.63)

0.10

(0.39)

[0.93] .004

(0.07)

0.09

(0.28)

I2 St -0.15

(-0.66)

0.71**

(2.31)

[0.03] -0.06

(-0.84)

0.77**

(2.00)

I3 St 0.02

(0.08)

0.48

(1.57)

[0.24] 0.02

(0.23)

0.51

(1.30)

IUNA St -0.18

(-0.66)

-0.28

(-0.77)

[0.83] -0.02

(-0.31)

-0.33

(-0.72)

IAP St 0.10

(0.42)

-0.66**

(-2.17)

[0.05] -.002

(-0.03)

-0.76**

(-1.96)

R2(%) 8.07 6.56 - 6.52 9.16

Notes: This table displays the results from the M-estimation of Eq. (4). ΔIV is the daily

change in implied volatility taken by FTSE-100 implied volatility index. ΔRV denotes

the daily change in realized volatility taken from Oxford-Man Institute’s “realized

library” (Gerd et al., 2009). Column (3) reports the p-value of an equality test of the

estimates from regressions in columns (1) and (2). ΔRVG and ΔRVG stand for the daily

change of stock market’s realized volatility obtained from Eq. (5) and Eq. (6)

respectively.

*/**/*** denote significance at 90%, 95%, and 99% confidence levels respectively.

27

TABLE 4

QE SURPRISES AND INTRA-DAY VOLATILITY

(1) (2)

ΔRVG ΔVolR

c 3.05***

(15.16)

-0.13

(-1.06)

I1 |abs|St 0.09

(0.58)

0.07

(0.77)

I2 |abs|St 0.04

(0.23)

0.15

(1.32)

I3 |abs|St 0.38**

(2.08)

0.33***

(2.96)

IUNA |abs|St -0.46**

(-2.16)

-0.24*

(-1.85)

IAP |abs|St 0.12

(0.67)

-0.08

(-0.71)

R2(%) 13.98 18.36

Notes: This Table reports the results from the M-estimation of

Eq. (4). ΔRVG is the realized volatility of equities from 10-

minutes before the announcement until 1 hour after the

announcement calculated by Eq. (6). ΔVolR is the volatility ratio,

calculated by Eq. (7), showing the difference between the

volatility ratio for FTSE-100 index returns for the hour following

the MPC announcement and the volatility ratio for the 30 minutes

before it. |abs|St is the absolute value of the unexpected element

of an MPC announcement.

*/**/*** denote significance at 90%, 95%, and 99% confidence

levels respectively.

28

FIGURE 1

CUMULATIVE STOCK RETURNS ON FTSE 100 STOCK PRICE INDEX.

Notes: The solid line depicts the average cumulative 5-minute returns on the 55 Thursdays

of MPC announcement days from September 2009 to March 2014. The dashed line depicts

the average cumulative 5-minute returns on all Thursdays in our sample excluding those

which have an MPC announcement. 95% confidence intervals from Newey-West standard

errors for each point wise cumulative mean return includes the zero point suggesting that

statistically it is not statistically different from zero. The vertical dashed line points the

time of the MPC announcement.

-0.1

-0.05

0

0.05

0.1

0.15

0.28

:00

8:2

0

8:4

0

9:0

0

9:2

0

9:4

0

10:0

0

10:2

0

10:4

0

11:0

0

11:2

0

11:4

0

12:0

0

12:2

0

12:4

0

13:0

0

13:2

0

13:4

0

14:0

0

14:2

0

14:4

0

15:0

0

15:2

0

15:4

0

16:0

0

16:2

0

MPC Announcement

29

FIGURE 2

THE UNEXPECTED COMPONENT OF BANK’S ASSET PURCHASES ANNOUNCEMENT.

A. Actual vs. forecasted size of APP B. Monetary Surprises

Notes: The dashed line in Panel A of this figure reports the actual size of the Bank’s APF program as announced

on each of the 55 MPC meetings, while the solid line depicts the average of the estimates provided by economists

taking part in Bloomberg’s survey preceding the MPC meeting. Monetary surprises in Panel B show the difference

between the actual minus the expected size of the Bank’s APF program.

150

200

250

300

350

400

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14

actualexpected

£56.25b

45

60

Sep

-09

Mar

-10

Sep

-10

Mar

-11

Sep

-11

Mar

-12

Sep

-12

Mar

-13

Sep

-13

Mar

-14