Embed Size (px)

Citation preview

Quantitative Evaluation Center for Working Families

July 22, 2010

Quantitative Evaluation of Center for Working Families 2

This analysis examines services delivered to participants and their achievements in 3 AECF supported organizations (evaluation sites)• The Service Pathways analysis examines:

– Characteristics of CWF participants

– Outcomes CWF participants have achieved

– Characteristics of high achievers and services received

• The Financial Progress analysis examines:

– Changes in earned and work support income for a sample of participants

– Changes in credit scores

– Changes in spending patterns

• Cost assessments examine total cost per client of providing services and changes in costs over time

Quantitative Evaluation of Center for Working Families 3Quantitative Evaluation of Center for Working Families 3

Strengths and limitations of the evaluation

Strengths– Uses data covering a period up to five years that includes:

» receipt of services» attainment of outcomes and» changes in behaviors over time

Limitations– Lack of a control group means the analysis is descriptive– Reporting of services and outcomes at sites varies

Service Pathways Analysis– Takes time to achieve long-term outcomes; some of the key outcomes reported (receipt of

financial aid, completion of soft skills training, or financial literacy training) are intermediate outcomes

– The analysis includes a “start-up period” for each CWF site

Financial Progress Study– Data are from several different sources and are collected at different points in time– Information reported by participants may be subject to reporting error

Quantitative Evaluation of Center for Working Families 4Quantitative Evaluation of Center for Working Families 4

CWF sites are serving AECF’s target population

Characteristics at Program Enrollment (for CWF enrollees through December 2009)

CNM MET Center Bon SecoursTotal participants 910 8,221 892

Gender 62% female 73% female 51% female

Marital status 18% married or with a domestic partner

16% married or with a domestic partner

8% married or with a domestic partner

Presence of children 67% with children 77% with children 74% with children

Race Majority Hispanic, 11% Native American 90% African American 95% African American

Median age at enrollment 32 years 26 years 36 years

Education at program enrollment

75% had at least a high school diploma

62% had at least a high school diploma

61% had at least a high school diploma

Median monthly earnings* $800 $1,057 $1,200

* Based on a sample of participants

Quantitative Evaluation of Center for Working Families 5Quantitative Evaluation of Center for Working Families 5

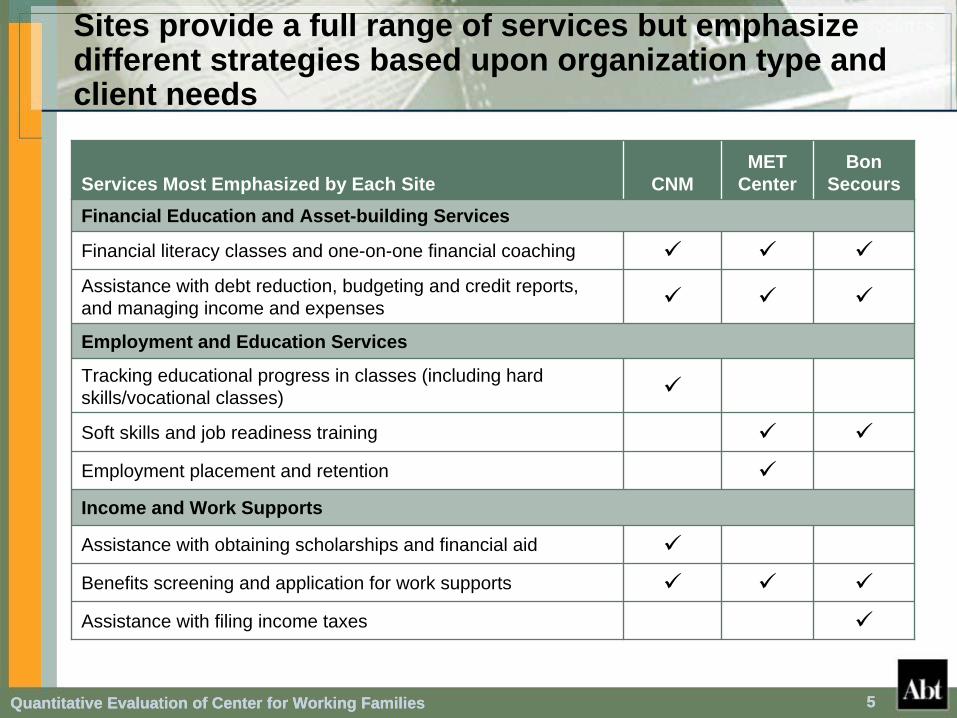

Sites provide a full range of services but emphasize different strategies based upon organization type and client needs

Services Most Emphasized by Each Site CNMMET

CenterBon

SecoursFinancial Education and Asset-building Services

Financial literacy classes and one-on-one financial coaching

Assistance with debt reduction, budgeting and credit reports, and managing income and expenses

Employment and Education Services

Tracking educational progress in classes (including hard skills/vocational classes)

Soft skills and job readiness training

Employment placement and retention

Income and Work Supports

Assistance with obtaining scholarships and financial aid

Benefits screening and application for work supports

Assistance with filing income taxes

Quantitative Evaluation of Center for Working Families 6Quantitative Evaluation of Center for Working Families 6

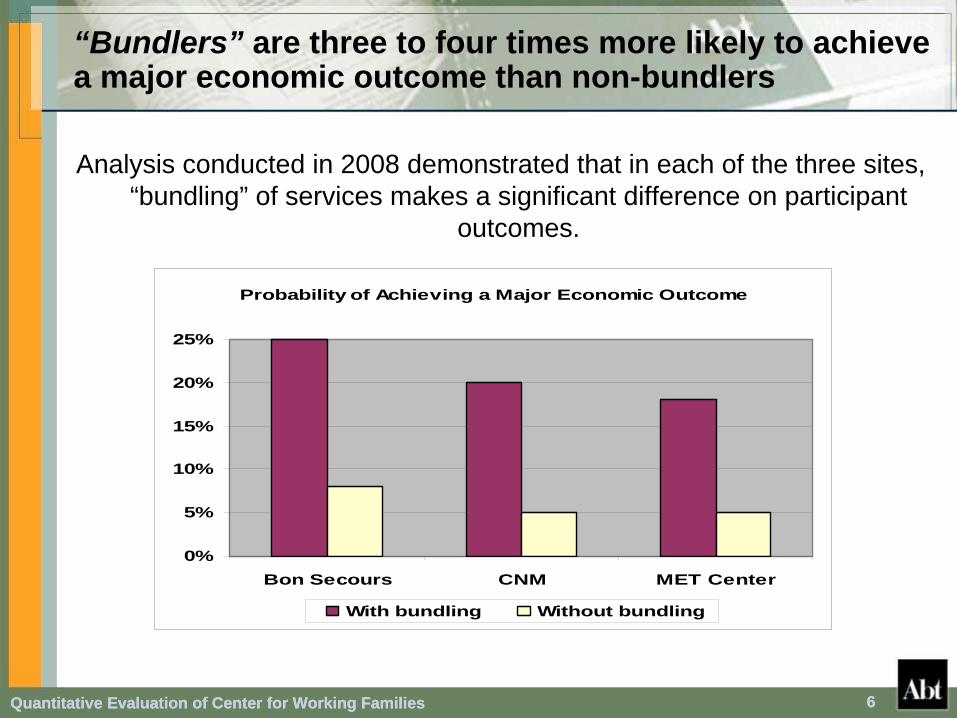

“Bundlers” are three to four times more likely to achieve a major economic outcome than non-bundlers

Analysis conducted in 2008 demonstrated that in each of the three sites, “bundling” of services makes a significant difference on participant

outcomes.

Probability of Achieving a Major Economic Outcome

0%

5%

10%

15%

20%

25%

Bon Secours CNM MET Center

With bundling Without bundling

Quantitative Evaluation of Center for Working Families 7Quantitative Evaluation of Center for Working Families 7

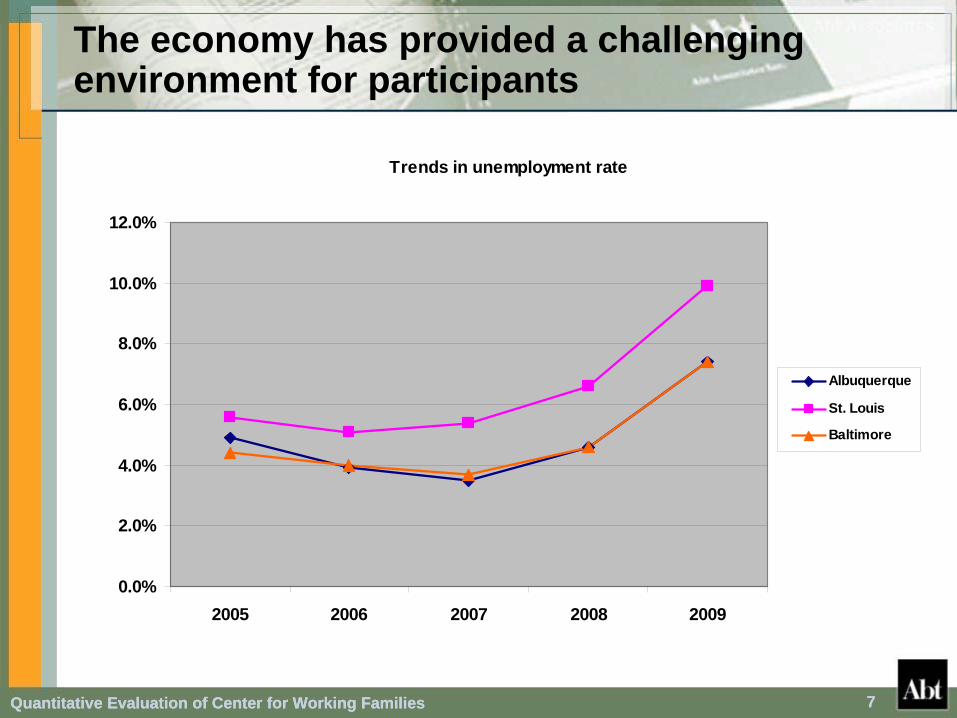

The economy has provided a challenging environment for participants

Trends in unemployment rate

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2005 2006 2007 2008 2009

Albuquerque

St. Louis

Baltimore

Quantitative Evaluation of Center for Working Families 8Quantitative Evaluation of Center for Working Families 8

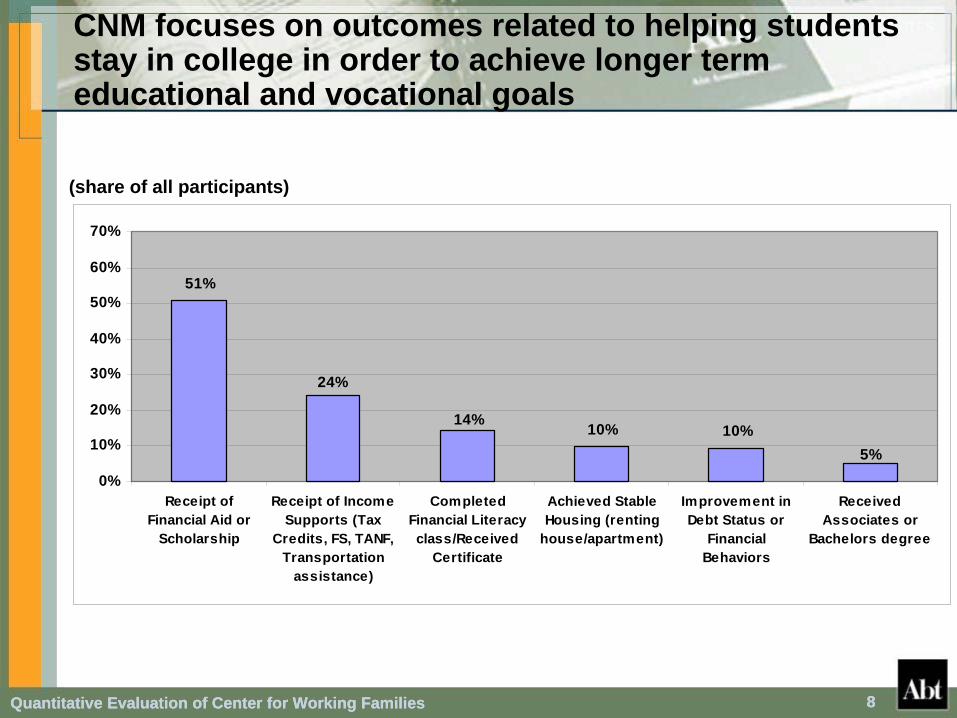

CNM focuses on outcomes related to helping students stay in college in order to achieve longer term educational and vocational goals

(share of all participants)

51%

10% 10%14%

5%

24%

0%

10%

20%

30%

40%

50%

60%

70%

Receipt ofFinancial Aid or

Scholarship

Receipt of IncomeSupports (Tax

Credits, FS, TANF,Transportation

assistance)

CompletedFinancial Literacyclass/Received

Certificate

Achieved StableHousing (renting

house/apartment)

Improvement inDebt Status or

FinancialBehaviors

ReceivedAssociates or

Bachelors degree

Quantitative Evaluation of Center for Working Families 9Quantitative Evaluation of Center for Working Families 9

MET Center key outcomes focus on job placement and retention

43%

26%

60%

77%72%

89%

0%

20%

40%

60%

80%

100%

P assed So ft Skills(share o f tho seenro lled in so ft

skills)

P assed H ard Skills (share o f tho seenro lled in hard

skills)

Jo b P lacements(share o f a llpart ic ipants)

3 M o nth R etent io n

6 M o nth R etent io n

12 M o nth R etent io n

share of eligible placements

Quantitative Evaluation of Center for Working Families 10

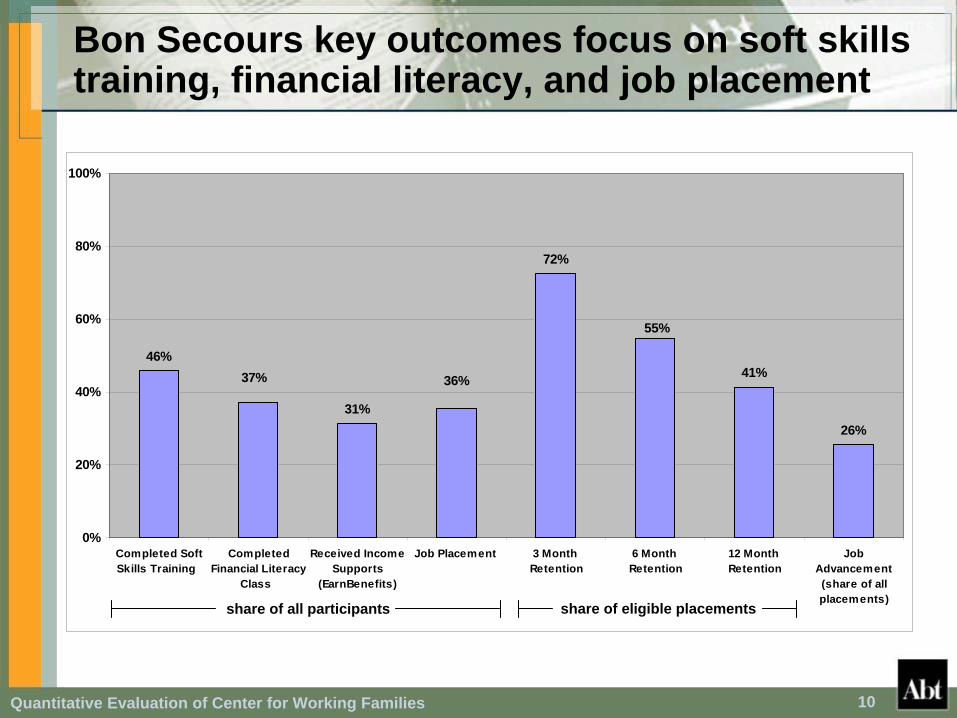

Bon Secours key outcomes focus on soft skills training, financial literacy, and job placement

46%

31%

72%

41%

26%

37% 36%

55%

0%

20%

40%

60%

80%

100%

Completed SoftSkills Training

CompletedFinancial Literacy

Class

Received IncomeSupports

(EarnBenefits)

Job Placement 3 Month Retention

6 Month Retention

12 Month Retention

JobAdvancement(share of allplacements)

share of all participants share of eligible placements

Quantitative Evaluation of Center for Working Families 11Quantitative Evaluation of Center for Working Families 11

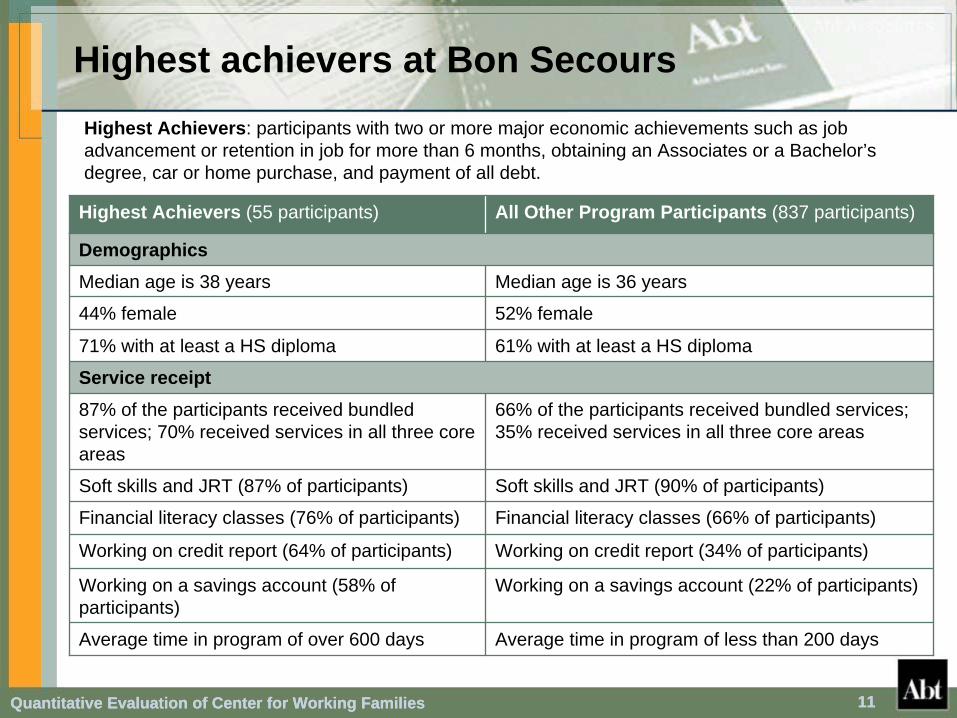

Highest achievers at Bon SecoursHighest Achievers: participants with two or more major economic achievements such as job advancement or retention in job for more than 6 months, obtaining an Associates or a Bachelor’s degree, car or home purchase, and payment of all debt.

Highest Achievers (55 participants) All Other Program Participants (837 participants)

DemographicsMedian age is 38 years Median age is 36 years

44% female 52% female

71% with at least a HS diploma 61% with at least a HS diploma

Service receipt87% of the participants received bundled services; 70% received services in all three core areas

66% of the participants received bundled services; 35% received services in all three core areas

Soft skills and JRT (87% of participants) Soft skills and JRT (90% of participants)

Financial literacy classes (76% of participants) Financial literacy classes (66% of participants)

Working on credit report (64% of participants) Working on credit report (34% of participants)

Working on a savings account (58% of participants)

Working on a savings account (22% of participants)

Average time in program of over 600 days Average time in program of less than 200 days

Quantitative Evaluation of Center for Working Families 12Quantitative Evaluation of Center for Working Families 12

Bon Secours’ participant incomes rose after enrollment

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

qp4 qp3 qp2 qp1 q0 q1 q2 q3 q4 q5 q6 q7 q8

200520062007

Average quarterly earnings (in 2009 $s) – for enrollments in 2005, 2006, and 2007

Pre-Enrollment Post-Enrollment

Quantitative Evaluation of Center for Working Families 13

Financial progress study participants have made improvements in financial behaviors

Percentage of Study Participants

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Track expenses bywriting them down

File a tax return in thelast season

Take out a refundanticipation loan

Average Score, Scale of 1-5

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Put money aside for futurepurchases

Look for ways to cutexpenses

Check credit report regularly

Scale of 1-5

Initial Survey Follow-up

Quantitative Evaluation of Center for Working Families 14

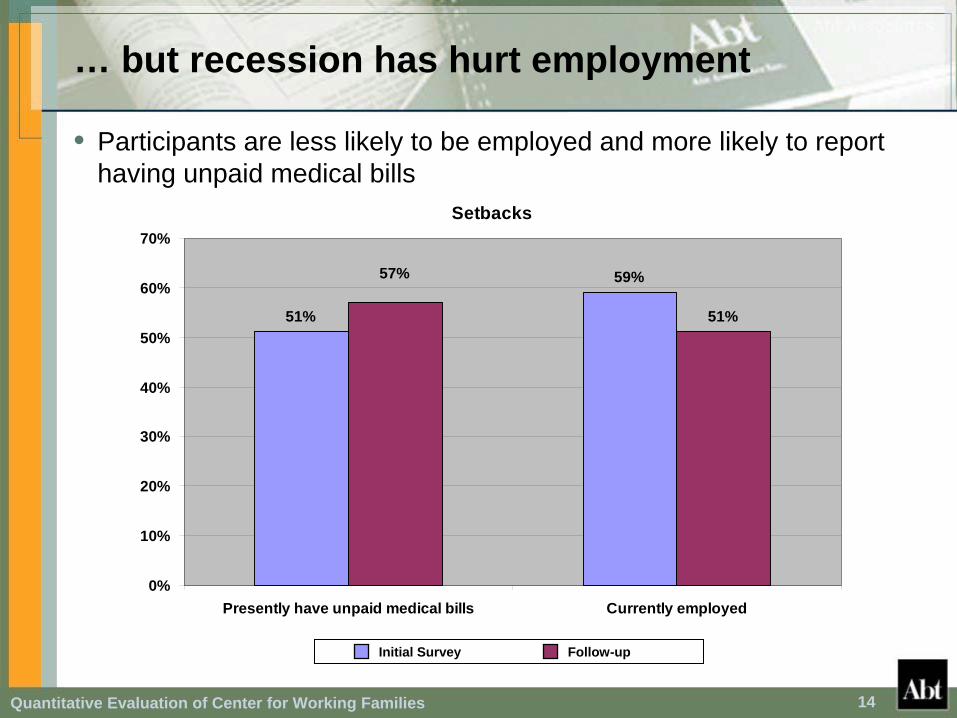

… but recession has hurt employment

• Participants are less likely to be employed and more likely to report having unpaid medical bills

Setbacks

51%

59%

51%

57%

0%

10%

20%

30%

40%

50%

60%

70%

Presently have unpaid medical bills Currently employed

Initial Survey Follow-up

Quantitative Evaluation of Center for Working Families 15

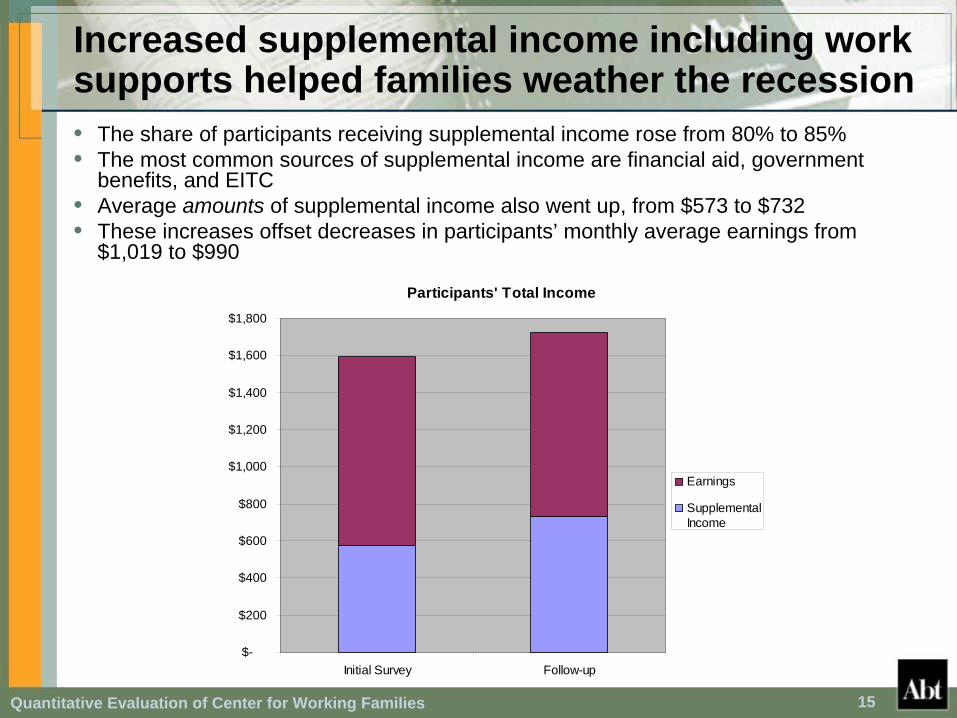

Increased supplemental income including work supports helped families weather the recession• The share of participants receiving supplemental income rose from 80% to 85% • The most common sources of supplemental income are financial aid, government

benefits, and EITC • Average amounts of supplemental income also went up, from $573 to $732• These increases offset decreases in participants’ monthly average earnings from

$1,019 to $990

Participants' Total Income

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

Initial Survey Follow-up

Earnings

SupplementalIncome

Quantitative Evaluation of Center for Working Families 16

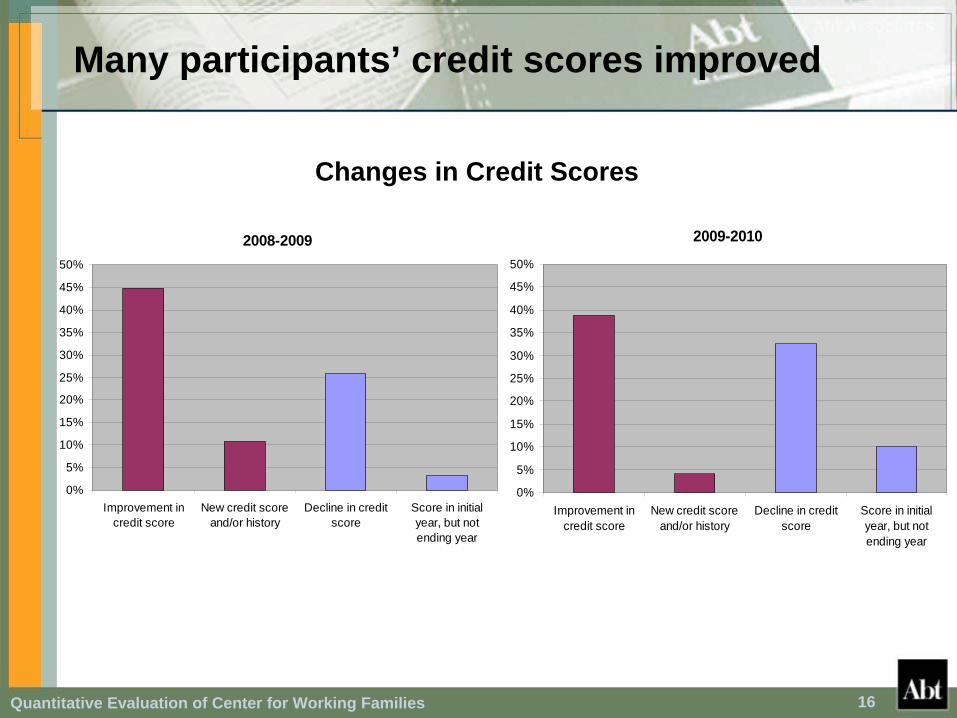

Many participants’ credit scores improved

Changes in Credit Scores

2009-2010

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Improvement incredit score

New credit scoreand/or history

Decline in creditscore

Score in initialyear, but notending year

2008-2009

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Improvement incredit score

New credit scoreand/or history

Decline in creditscore

Score in initialyear, but notending year

Quantitative Evaluation of Center for Working Families 17

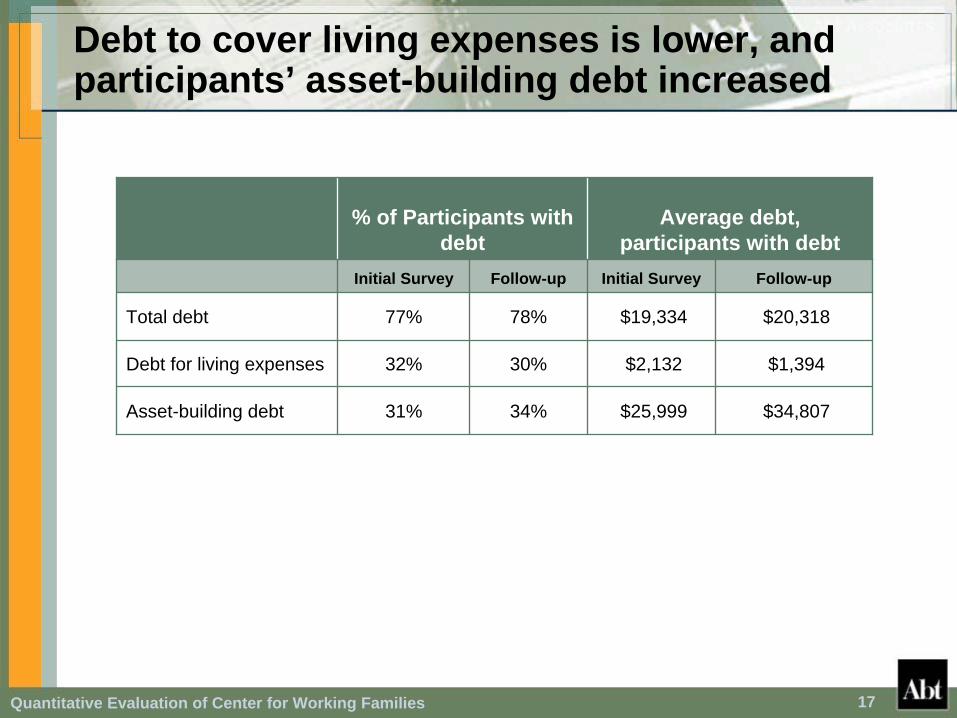

Debt to cover living expenses is lower, and participants’ asset-building debt increased

% of Participants with debt

Average debt, participants with debt

Initial Survey Follow-up Initial Survey Follow-up

Total debt 77% 78% $19,334 $20,318

Debt for living expenses 32% 30% $2,132 $1,394

Asset-building debt 31% 34% $25,999 $34,807

Quantitative Evaluation of Center for Working Families 18

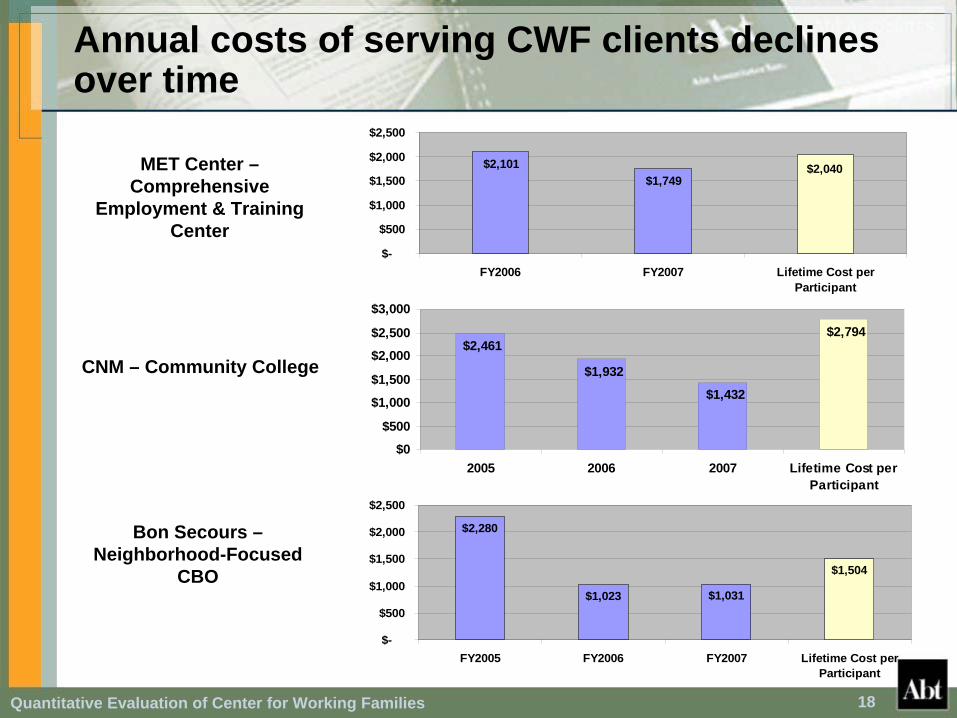

Annual costs of serving CWF clients declines over time

$2,040$1,749

$2,101

$-

$500

$1,000

$1,500

$2,000

$2,500

FY2006 FY2007 Lifetime Cost perParticipant

$2,794$2,461

$1,932

$1,432

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

2005 2006 2007 Lifetime Cost perParticipant

$2,280

$1,023 $1,031

$1,504

$-

$500

$1,000

$1,500

$2,000

$2,500

FY2005 FY2006 FY2007 Lifetime Cost perParticipant

MET Center – Comprehensive

Employment & Training Center

CNM – Community College

Bon Secours – Neighborhood-Focused

CBO

Quantitative Evaluation of Center for Working Families 19

Conclusions

• Participants showed progress toward attaining family economic success

– Improvements in financial behaviors

– Improvements in credit scores

– Better use of debt

– Educational and job achievements

• The recession has created a difficult environment for families striving to make earnings and income gains

• Increases in supplemental income helped offset earnings declines that may be related to the recession

• Major economic achievements take time

Quantitative Evaluation of Center for Working Families 20

For more information

Kimberly Burnett, Abt [email protected]

Christopher Herbert, Abt [email protected]

Anne St. George, Abt [email protected]

Bulbul Kaul, Abt [email protected]

Quantitative Evaluation of Center for Working Families 21