Embed Size (px)

Citation preview

Managing the risks of modern mobility

Rani Sakaya JohnsGlobal Mobility PartnerPwC Singapore

Jod GillGlobal Mobility Senior Manager PwC Singapore

www.pwc.com

PwC

Discussion outline

1. What is Modern Mobility?

2. What issues does this create?

3. How do you manage these issues?

4. An integrated approach

Global Tax Symposium – Asia 20152

PwC

What is modern mobility?

3Global Tax Symposium – Asia 2015

PwC

More people are moving… In new and different ways

89% of organisations plan to increase the number of internationally mobile workers in the next two years – not just formal assignments but more fluid mobility types (e.g. commuters and regional/ global roles).

Global Tax Symposium – Asia 20154

PwC

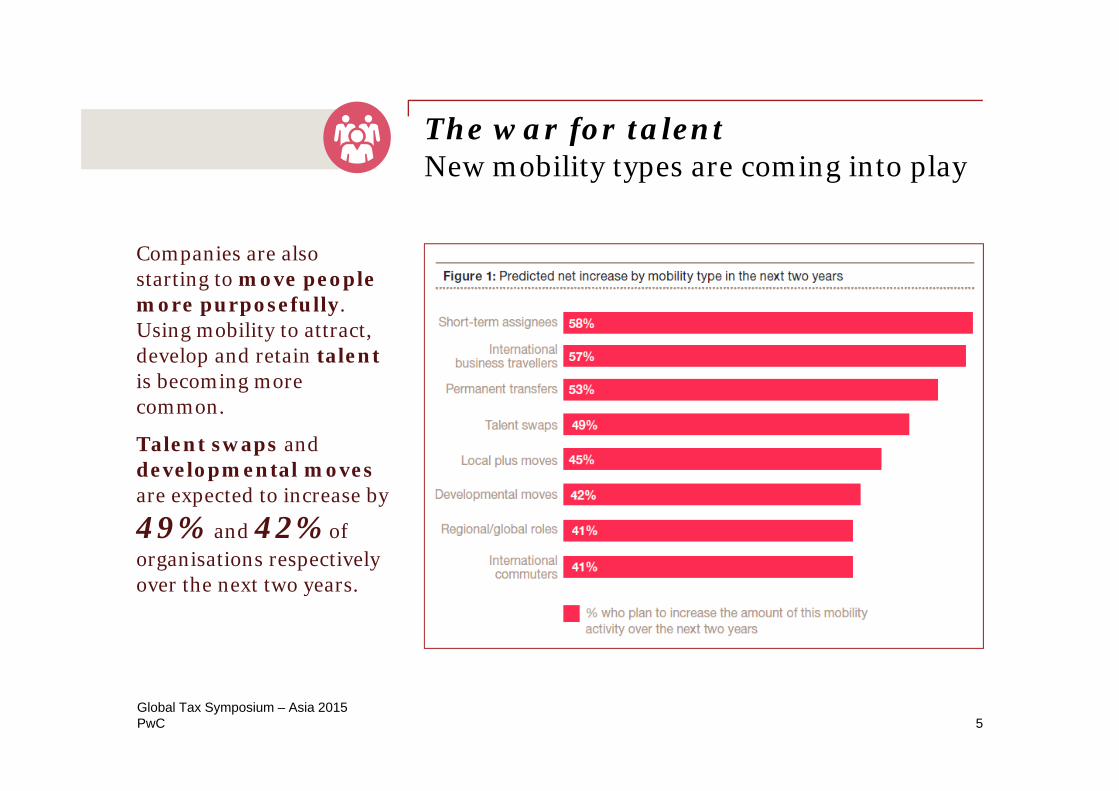

The war for talent New mobility types are coming into play

Companies are also starting to move people more purposefully. Using mobility to attract, develop and retain talent is becoming more common.

Talent swaps and developmental moves are expected to increase by

49% and 42% of organisations respectively over the next two years.

Global Tax Symposium – Asia 20155

PwC

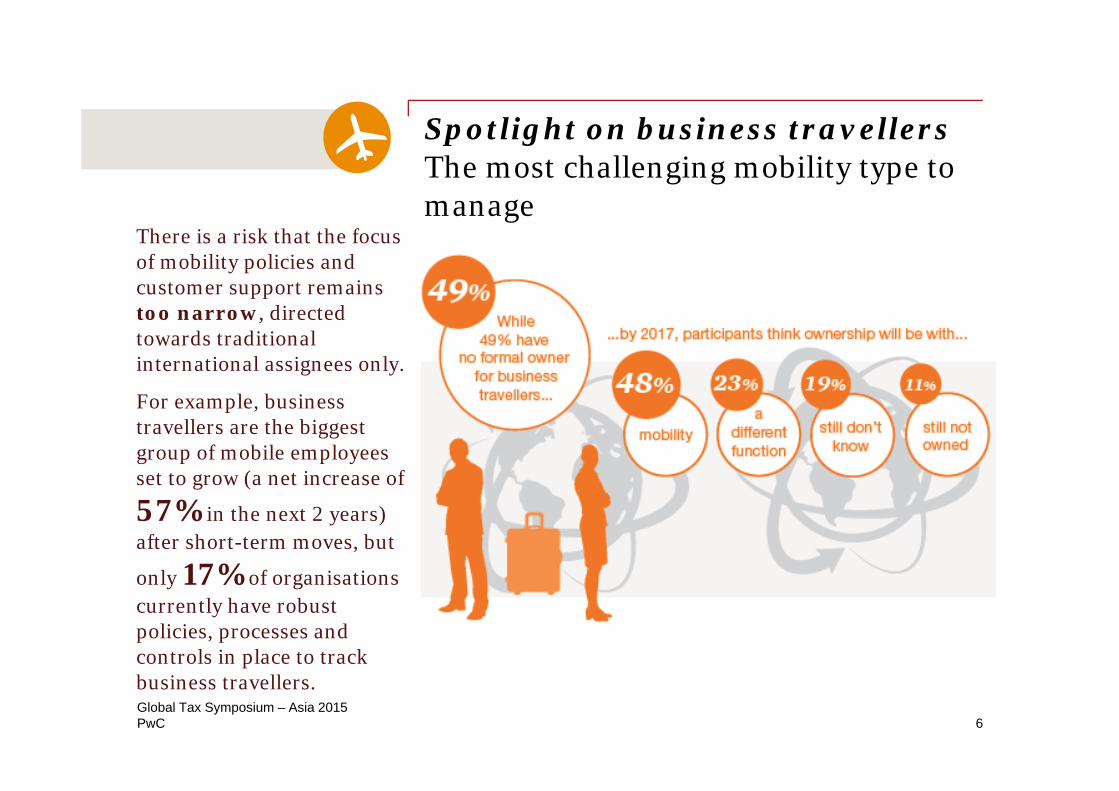

Spotlight on business travellersThe most challenging mobility type to manage

There is a risk that the focus of mobility policies and customer support remains too narrow, directed towards traditional international assignees only.

For example, business travellers are the biggest group of mobile employees set to grow (a net increase of

57% in the next 2 years) after short-term moves, but

only 17% of organisations currently have robust policies, processes and controls in place to track business travellers.Global Tax Symposium – Asia 2015

6

PwC

What is the key mobility priority for your business?

• Manage compliance effectively

• Manage costs

• Align mobility and talent

• Other

Global Tax Symposium – Asia 20157

Top mobility priorities for businesses — your views

PwC

Choose the right approach to policy – your views

Do you have specific talent based or business visitor policies?

• Only a talent based policy

• Only a business visitor policy

• Neither

• Both

Global Tax Symposium – Asia 20158

PwC

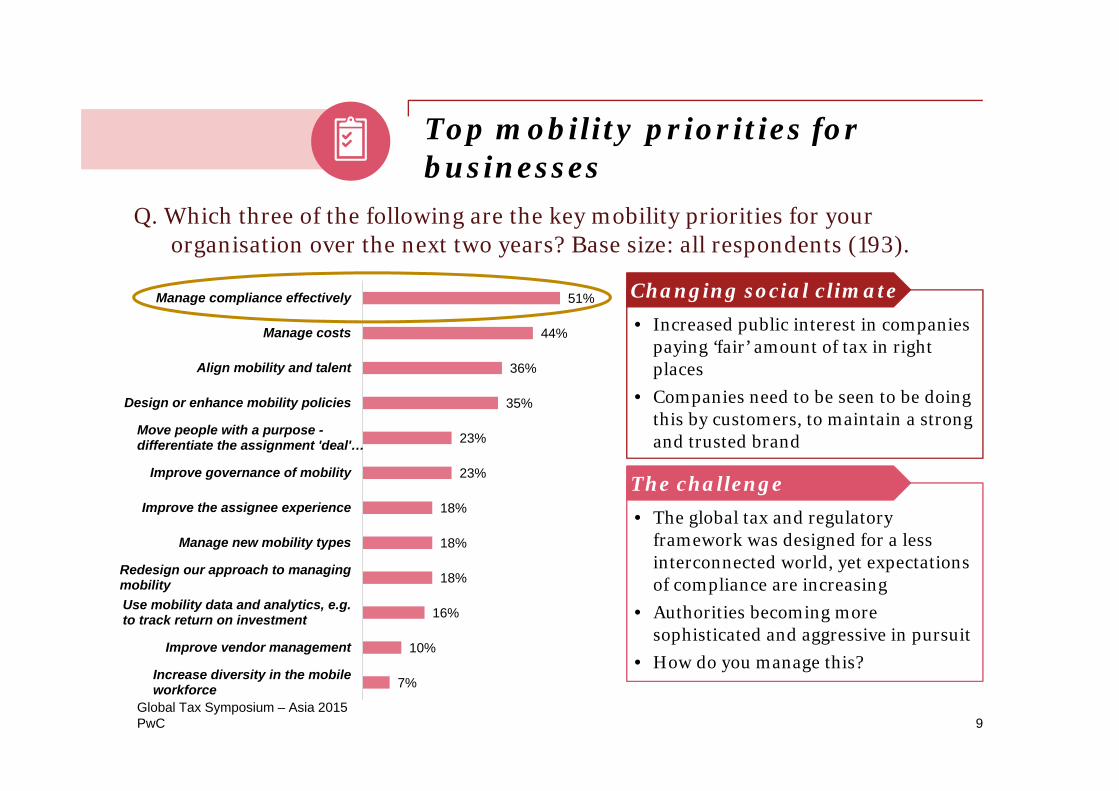

• Increased public interest in companies paying ‘fair’ amount of tax in right places

• Companies need to be seen to be doing this by customers, to maintain a strong and trusted brand

Changing social climate

Top mobility priorities for businesses

7%

10%

16%

18%

18%

18%

23%

23%

35%

36%

44%

51%

Increase diversity in the mobileworkforce

Improve vendor management

Use mobility data and analytics, e.g.to track return on investment

Redesign our approach to managingmobility

Manage new mobility types

Improve the assignee experience

Improve governance of mobility

Move people with a purpose -differentiate the assignment 'deal'…

Design or enhance mobility policies

Align mobility and talent

Manage costs

Manage compliance effectively

Q. Which three of the following are the key mobility priorities for your organisation over the next two years? Base size: all respondents (193).

• The global tax and regulatory framework was designed for a less interconnected world, yet expectations of compliance are increasing

• Authorities becoming more sophisticated and aggressive in pursuit

• How do you manage this?

The challenge

Global Tax Symposium – Asia 20159

PwC

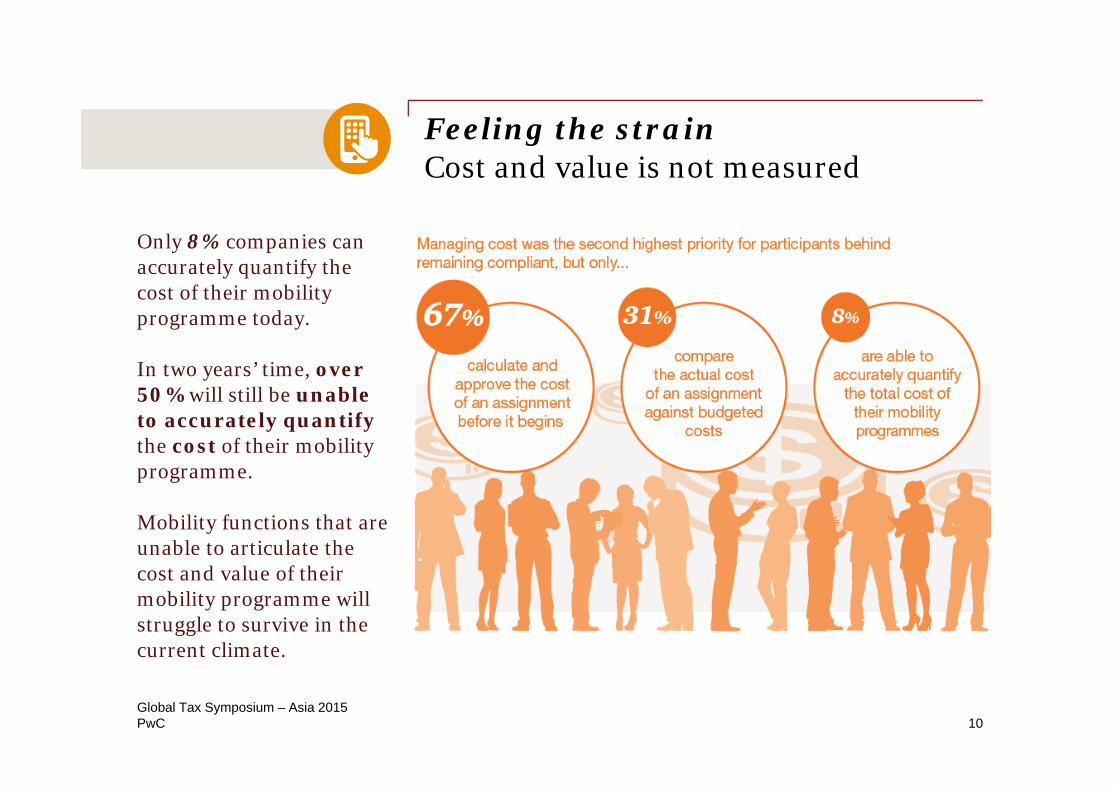

Feeling the strain Cost and value is not measured

Only 8% companies can accurately quantify the cost of their mobility programme today.

In two years’ time, over 50% will still be unable to accurately quantify the cost of their mobility programme.

Mobility functions that are unable to articulate the cost and value of their mobility programme will struggle to survive in the current climate.

Global Tax Symposium – Asia 201510

PwC

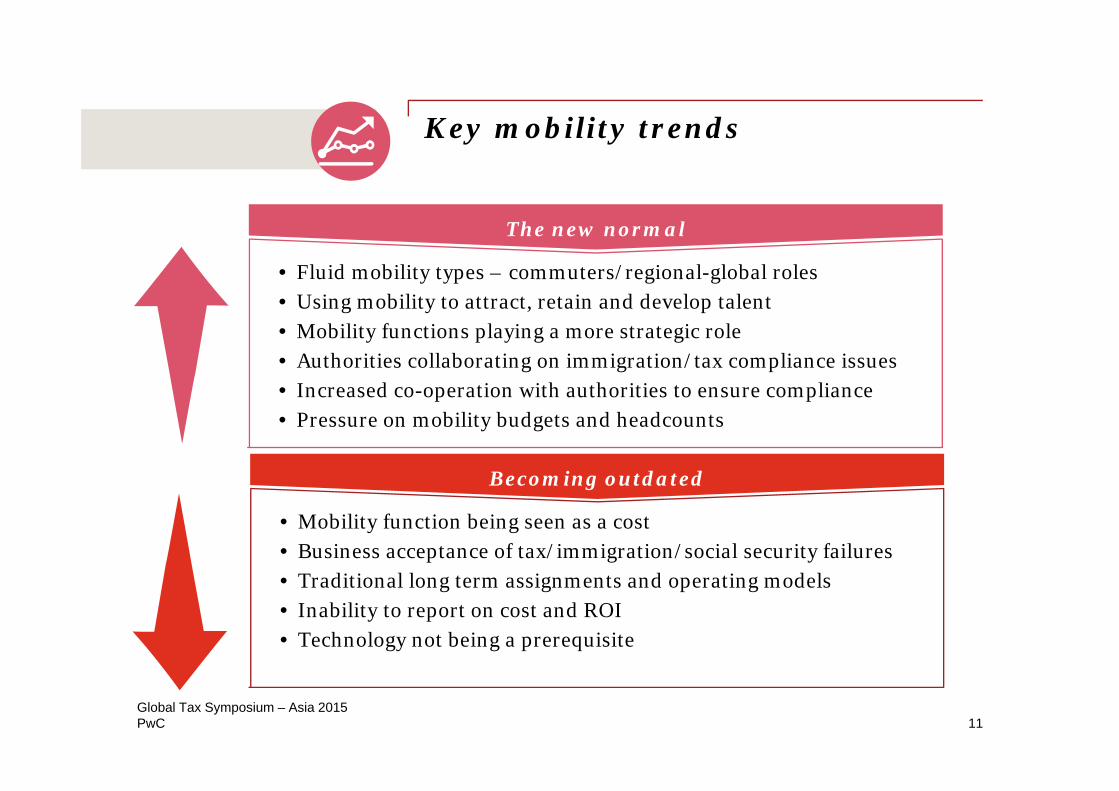

Key mobility trends

The new normal

• Fluid mobility types – commuters/regional-global roles• Using mobility to attract, retain and develop talent• Mobility functions playing a more strategic role • Authorities collaborating on immigration/tax compliance issues• Increased co-operation with authorities to ensure compliance • Pressure on mobility budgets and headcounts

Becoming outdated

• Mobility function being seen as a cost• Business acceptance of tax/immigration/social security failures• Traditional long term assignments and operating models• Inability to report on cost and ROI • Technology not being a prerequisite

Global Tax Symposium – Asia 201511

PwC

What issues does this create?

12Global Tax Symposium – Asia 2015

PwC

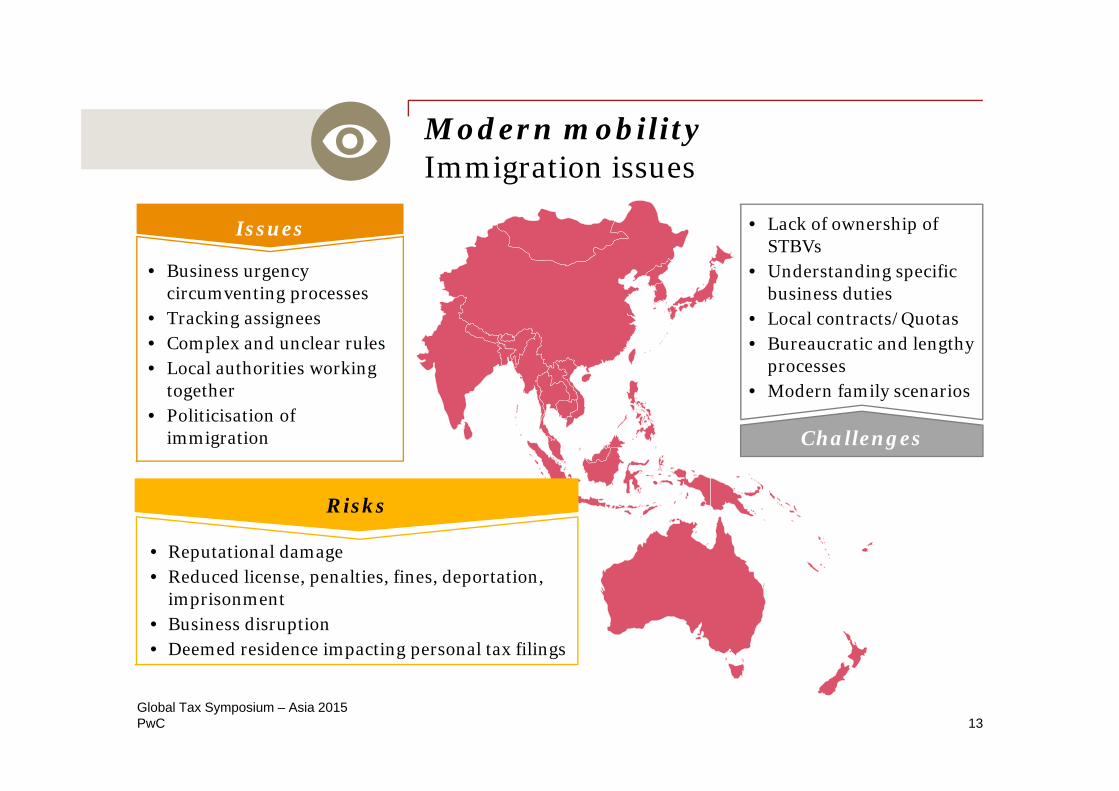

Modern mobilityImmigration issues

Issues

• Business urgency circumventing processes

• Tracking assignees• Complex and unclear rules• Local authorities working

together• Politicisation of

immigration Challenges

• Lack of ownership of STBVs

• Understanding specific business duties

• Local contracts/Quotas • Bureaucratic and lengthy

processes• Modern family scenarios

Risks

• Reputational damage • Reduced license, penalties, fines, deportation,

imprisonment• Business disruption• Deemed residence impacting personal tax filings

Global Tax Symposium – Asia 201513

PwC

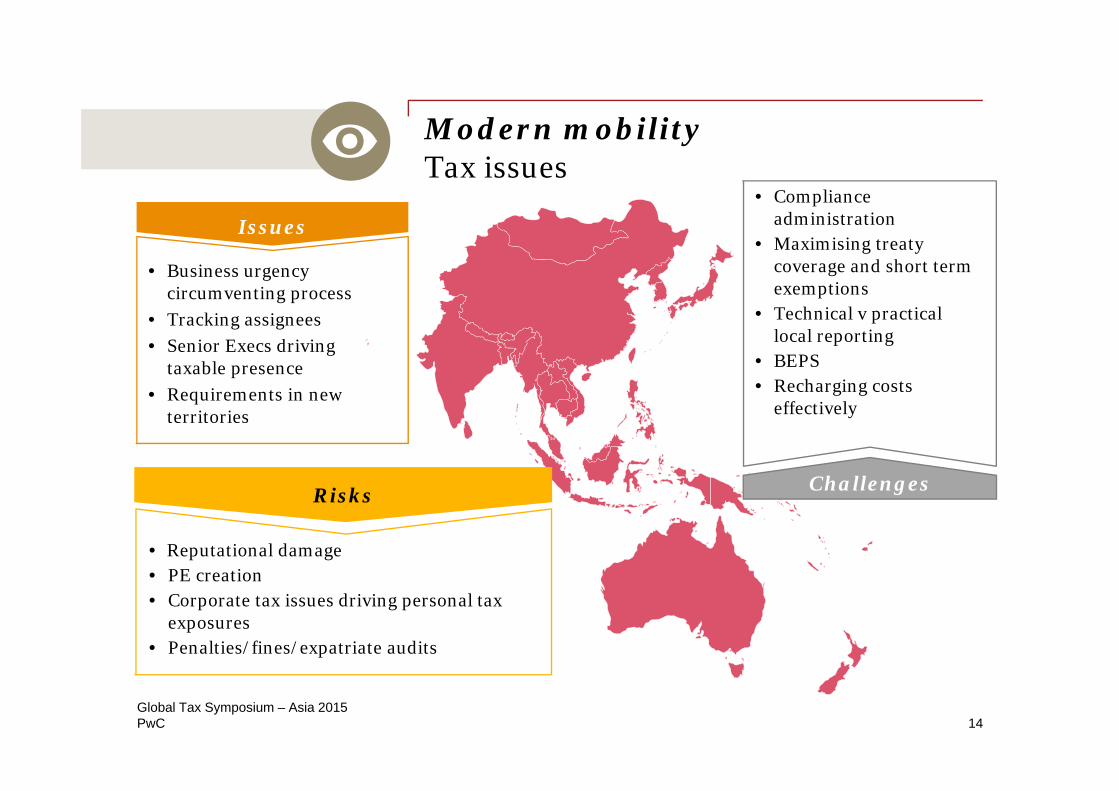

Modern mobilityTax issues

Issues

• Business urgency circumventing process

• Tracking assignees • Senior Execs driving

taxable presence• Requirements in new

territories

Risks

• Reputational damage• PE creation• Corporate tax issues driving personal tax

exposures• Penalties/fines/expatriate audits

Challenges

• Compliance administration

• Maximising treaty coverage and short term exemptions

• Technical v practical local reporting

• BEPS• Recharging costs

effectively

Global Tax Symposium – Asia 201514

PwC

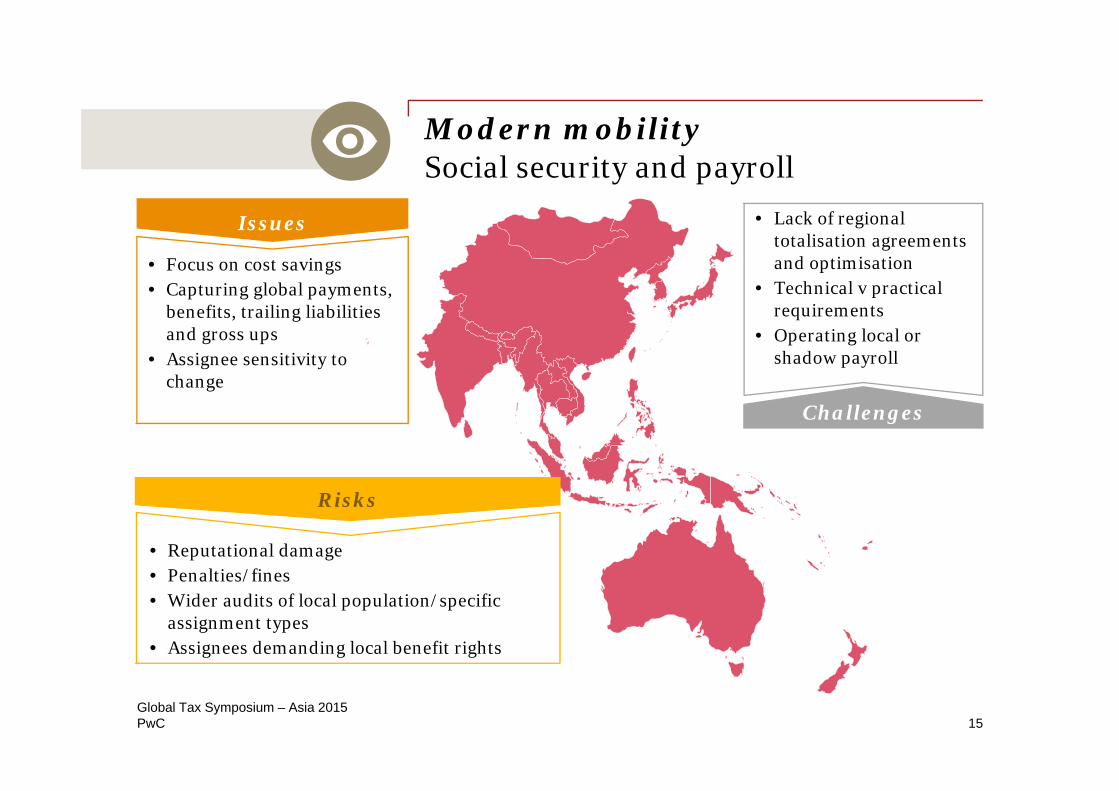

Modern mobilitySocial security and payroll

Issues

• Focus on cost savings• Capturing global payments,

benefits, trailing liabilities and gross ups

• Assignee sensitivity to change

Risks

• Reputational damage • Penalties/fines• Wider audits of local population/specific

assignment types• Assignees demanding local benefit rights

Challenges

• Lack of regional totalisation agreements and optimisation

• Technical v practical requirements

• Operating local or shadow payroll

Global Tax Symposium – Asia 201515

PwC

How do you manage these issues?

16Global Tax Symposium – Asia 2015

PwC

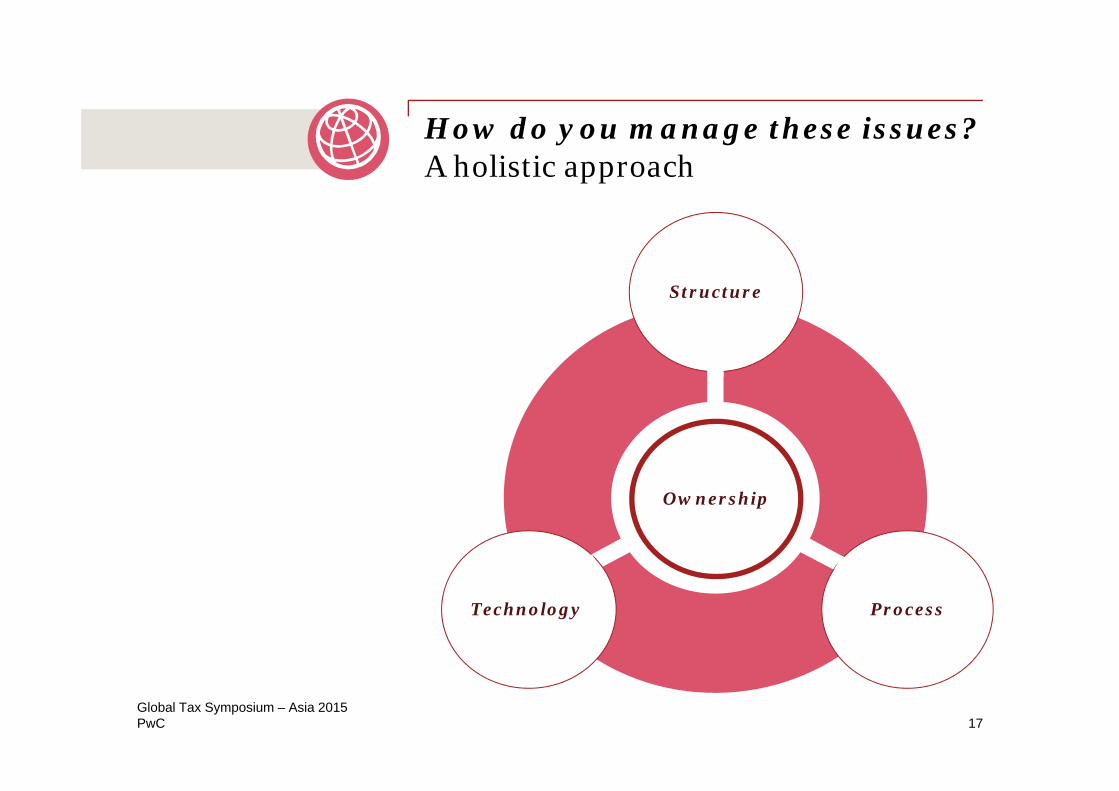

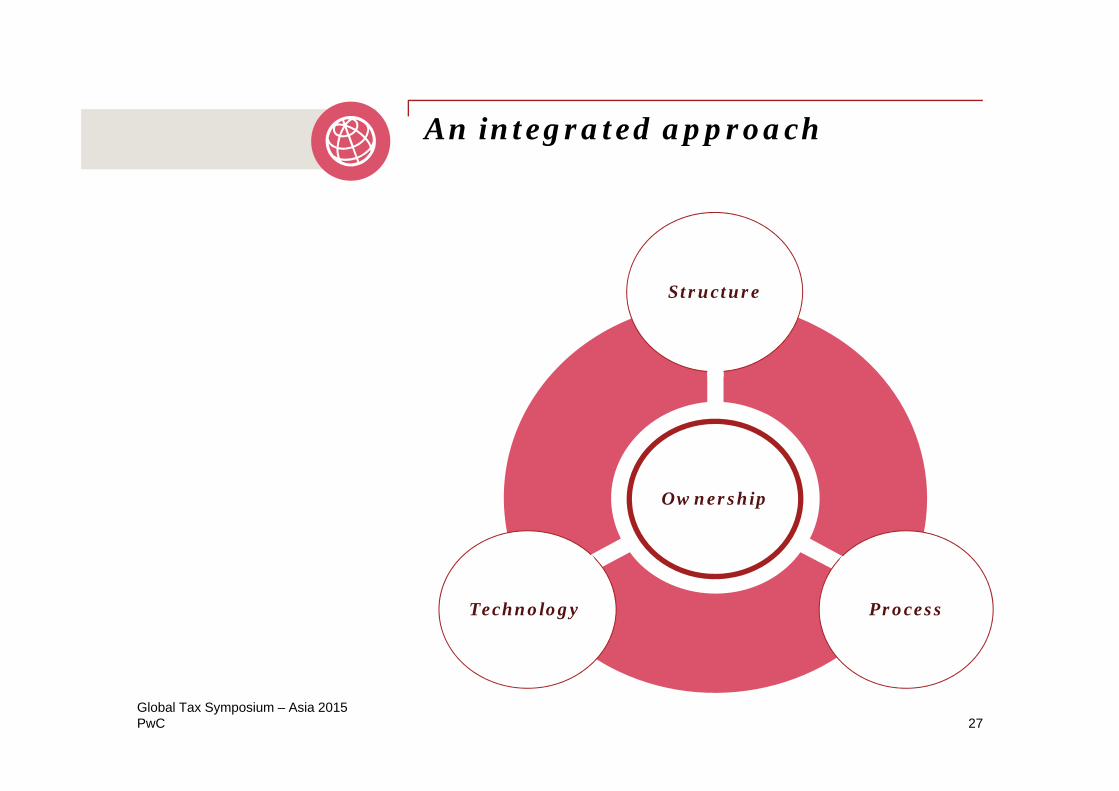

How do you manage these issues?A holistic approach

Ownership

Structure

ProcessTechnology

Global Tax Symposium – Asia 201517

PwC

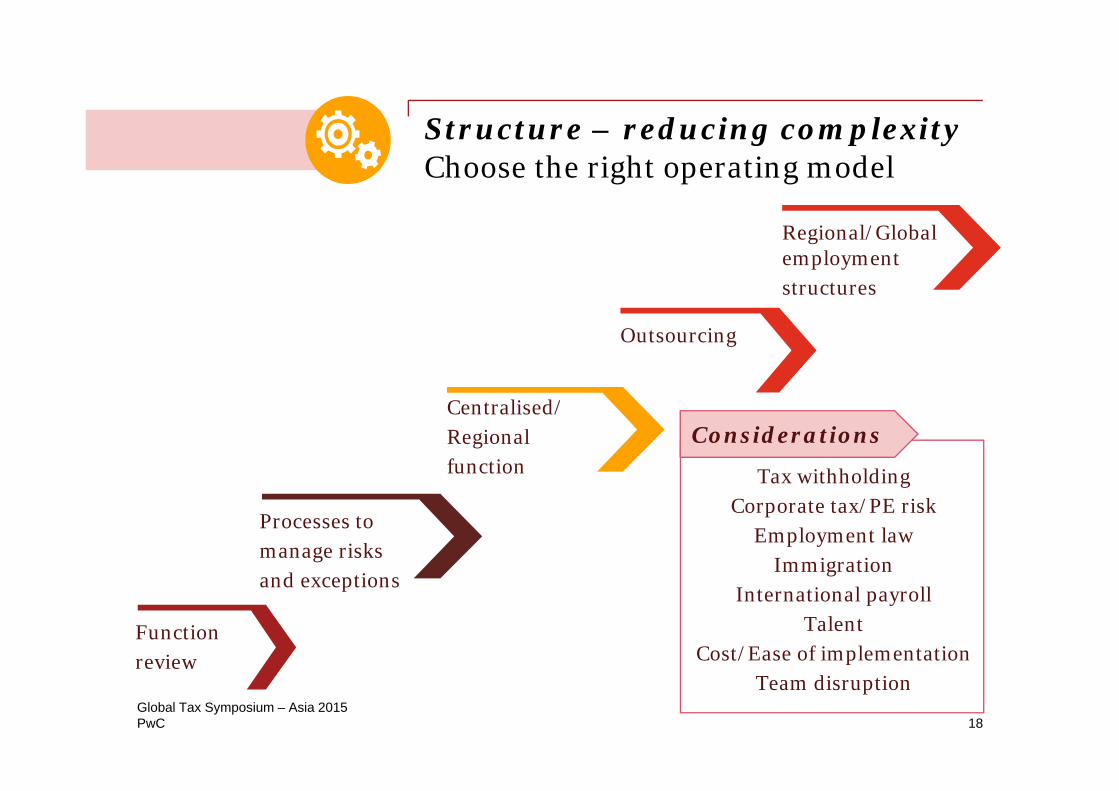

Structure – reducing complexityChoose the right operating model

Function review

Processes to manage risks and exceptions

Centralised/Regional function

Outsourcing

Regional/Global employment structures

Tax withholdingCorporate tax/PE risk

Employment lawImmigration

International payrollTalent

Cost/Ease of implementationTeam disruption

Considerations

Global Tax Symposium – Asia 201518

PwC

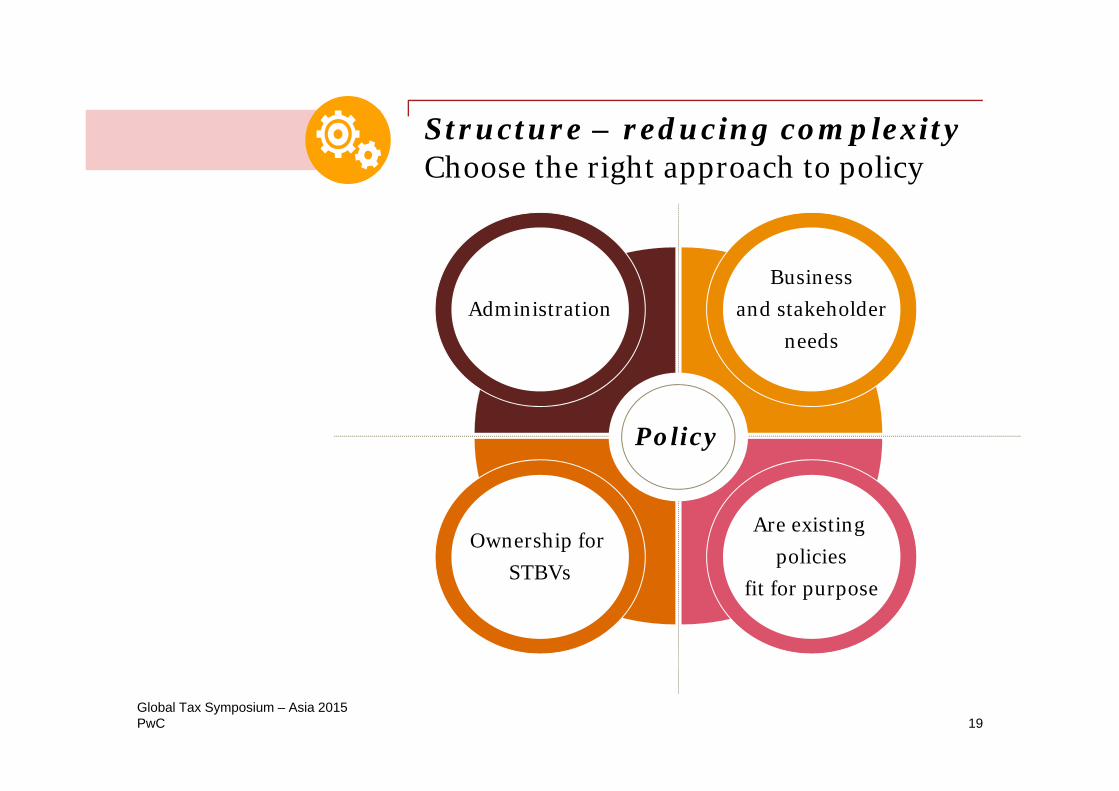

Structure – reducing complexityChoose the right approach to policy

Coverage

• Agree the process for

exceptions to be tracked and reported back to the business

Exceptions

AdministrationBusiness

and stakeholderneeds

Ownership for STBVs

Are existing policies

fit for purpose

Policy

Global Tax Symposium – Asia 201519

PwC

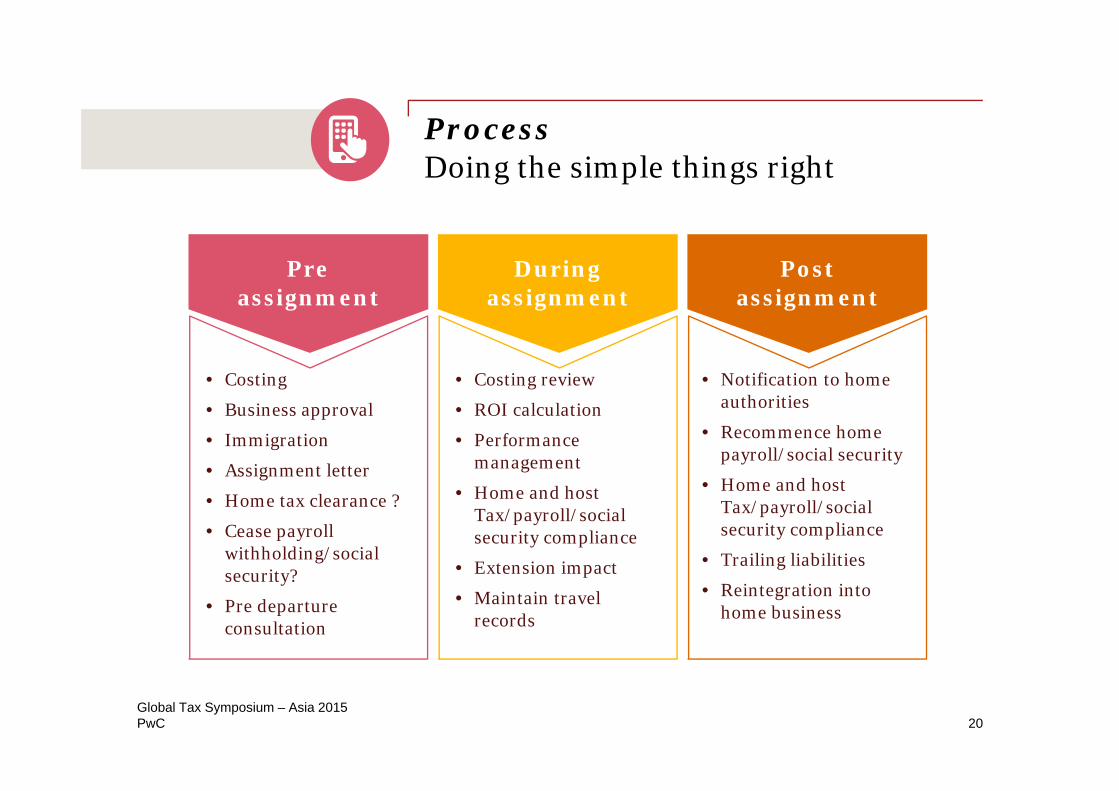

Process Doing the simple things right

Preassignment

• Costing

• Business approval

• Immigration

• Assignment letter

• Home tax clearance ?

• Cease payroll withholding/social security?

• Pre departure consultation

During assignment

• Costing review

• ROI calculation

• Performance management

• Home and host Tax/payroll/social security compliance

• Extension impact

• Maintain travel records

Post assignment

• Notification to home authorities

• Recommence home payroll/social security

• Home and host Tax/payroll/social security compliance

• Trailing liabilities

• Reintegration into home business

Global Tax Symposium – Asia 201520

PwC

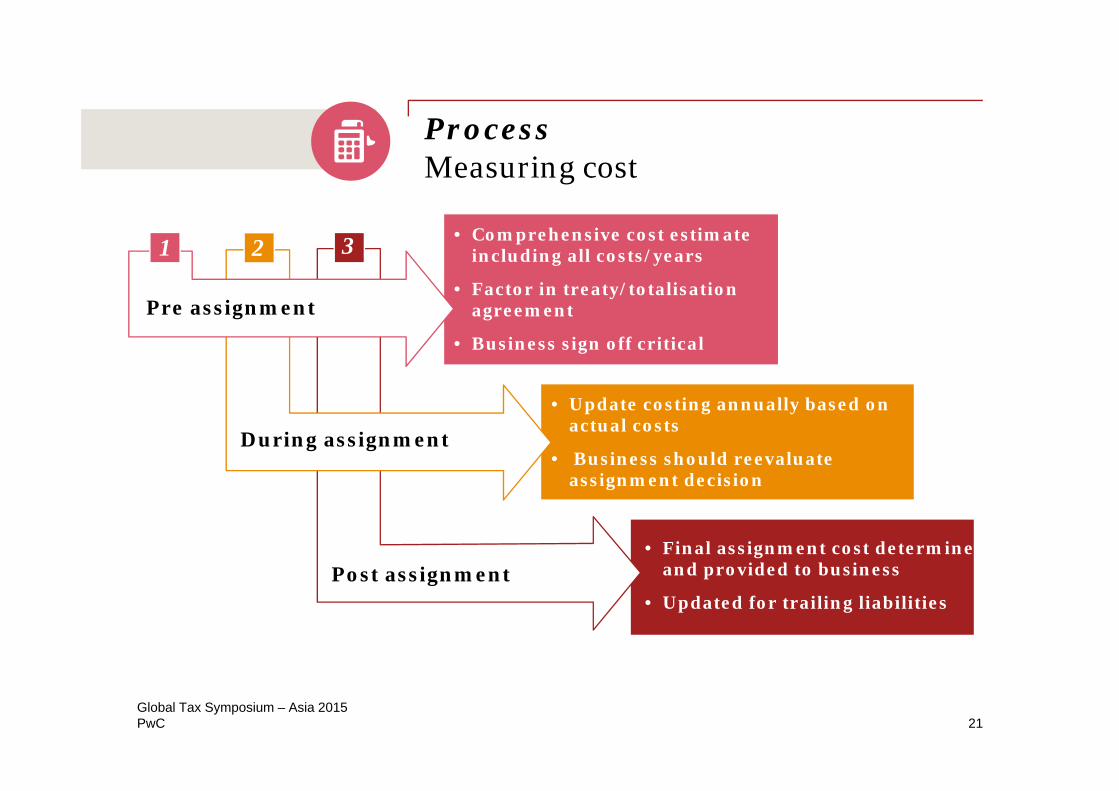

Process Measuring cost

1 2 3

• Update costing annually based on actual costs

• Business should reevaluate assignment decision

• Final assignment cost determined and provided to business

• Updated for trailing liabilities

Pre assignment

During assignment

Post assignment

• Comprehensive cost estimate including all costs/years

• Factor in treaty/totalisation agreement

• Business sign off critical

Global Tax Symposium – Asia 201521

PwC

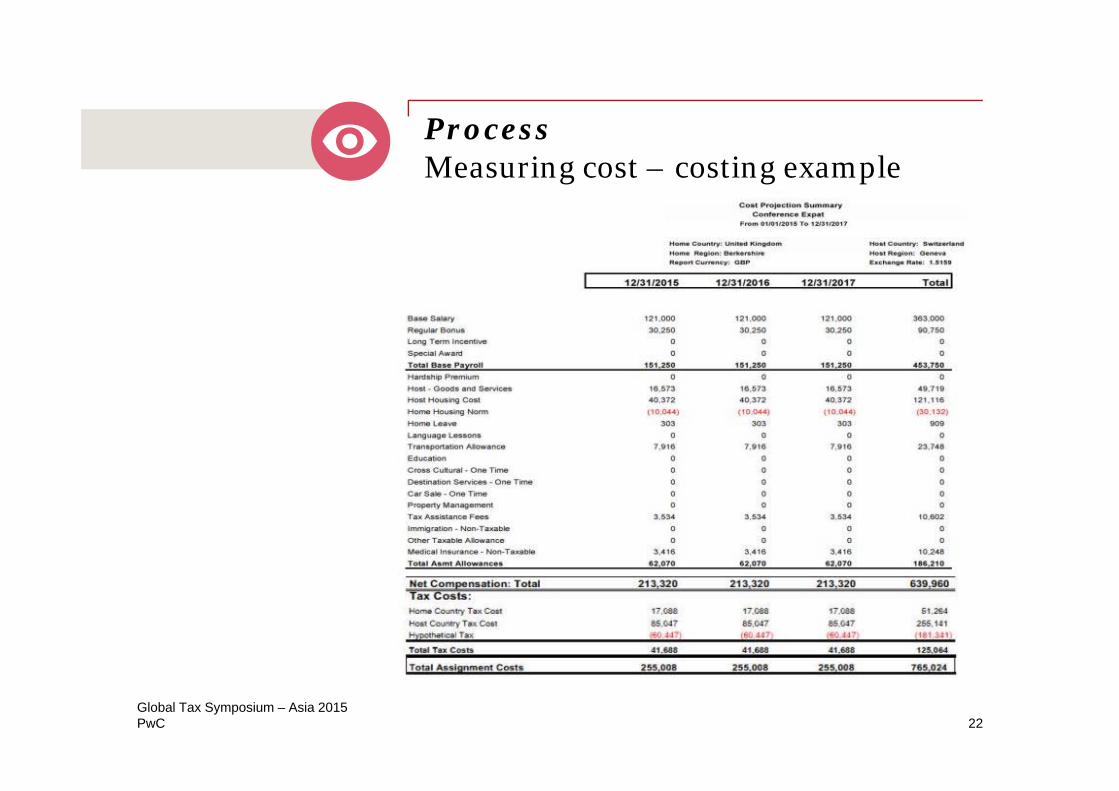

Process Measuring cost – costing example

• Update costing annually based on actual costs

• Business should reevaluate assignment decision

• Final assignment cost determined and provided to business

• Updated for trailing liabilities

• Comprehensive cost estimate including all costs/years

• Factor in treaty/totalisation agreement

• Business sign off critical

Global Tax Symposium – Asia 201522

PwC

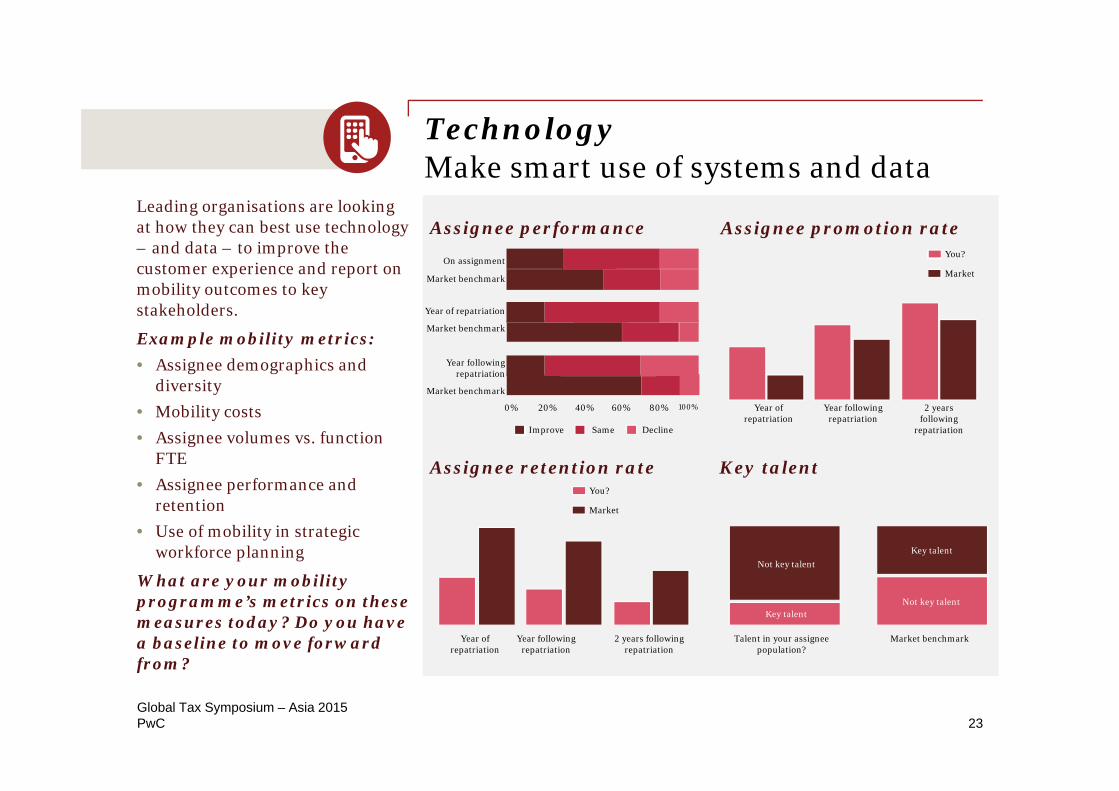

TechnologyMake smart use of systems and data

Leading organisations are looking at how they can best use technology – and data – to improve the customer experience and report on mobility outcomes to key stakeholders.

Example mobility metrics:• Assignee demographics and

diversity • Mobility costs• Assignee volumes vs. function

FTE• Assignee performance and

retention• Use of mobility in strategic

workforce planning

What are your mobility programme’s metrics on these measures today? Do you have a baseline to move forward from?

Assignee promotion rate

Talent in your assignee population?

Market benchmark

Key talent

Not key talent

Not key talent

Key talent

Assignee retention rate Key talent

100%

Market benchmark

Year following repatriation

Market benchmark

Market benchmark

0% 20% 40% 60% 80%

On assignment

Year of repatriation

Improve Same Decline

Assignee performance

Year of repatriation

Year following repatriation

2 years following repatriation

Year of repatriation

Year following repatriation

2 years following

repatriation

You?

Market

You?

Market

Global Tax Symposium – Asia 201523

PwC

TechnologyMake smart use of systems and data

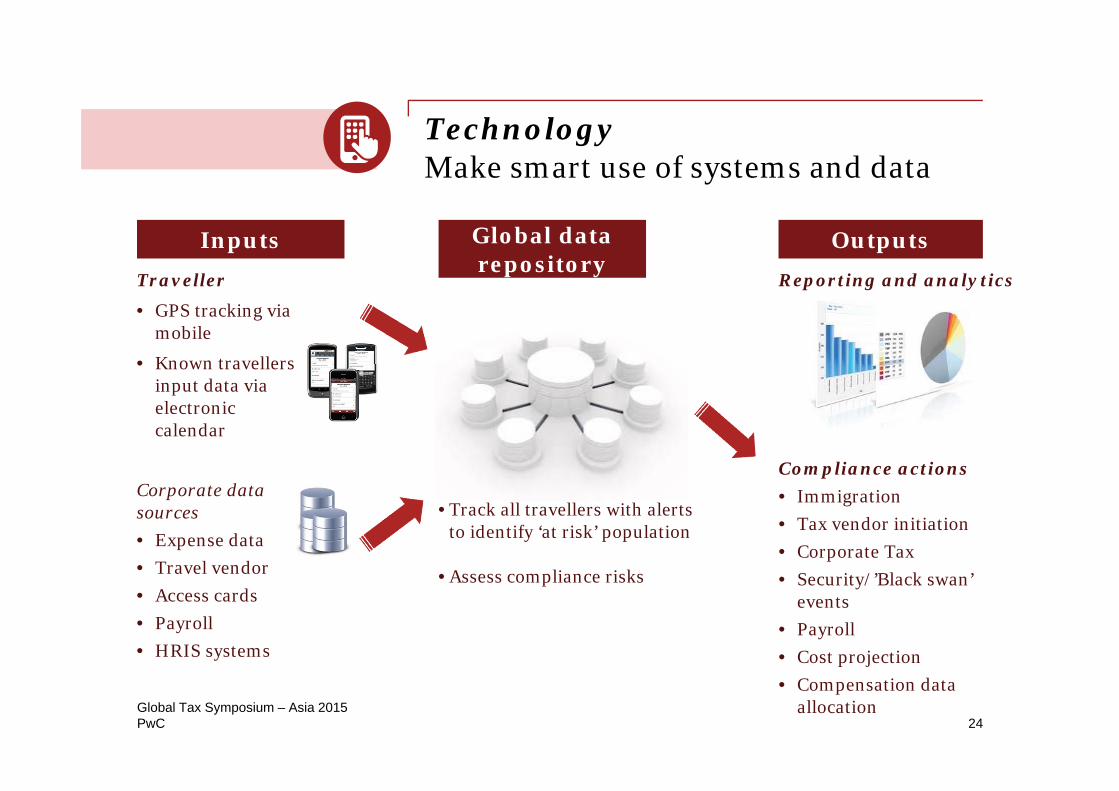

• Track all travellers with alerts to identify ‘at risk’ population

• Assess compliance risks

Reporting and analytics

Compliance actions• Immigration• Tax vendor initiation• Corporate Tax• Security/’Black swan’

events• Payroll• Cost projection• Compensation data

allocation

OutputsTraveller

• GPS tracking via mobile

• Known travellersinput data via electronic calendar

Corporate data sources• Expense data• Travel vendor• Access cards• Payroll• HRIS systems

Inputs Global data repository

Global Tax Symposium – Asia 201524

PwC

OwnershipUnderstand what stakeholders want and need

Voice of the Customer and Voice of the Assignee surveys sought the views of the users of mobility – business and mobile employees

Key mobility stakeholder interviews – To understand what is needed from the mobility programme, and HR

Business buy-in and agreed ownership allowed mobility to be viewed more as a business investment rather than simply a cost to be contained.

Defining the scope and KPIs of mobility services the business wants and needs was crucial to managing and meeting expectations.

Global Tax Symposium – Asia 201525

PwC

An integrated approach

26Global Tax Symposium – Asia 2015

PwC

An integrated approach

Global Tax Symposium – Asia 201527

Ownership

Structure

ProcessTechnology

PwC

Q&A

28Global Tax Symposium – Asia 2015

Thank you.

The information contained in this presentation is of a general nature only. It is not meant to be comprehensive and does not constitute the rendering of legal, tax or other professional advice or service by PricewaterhouseCoopers Ltd. ("PwC"). PwC has no obligation to update the information as law and practices change. The application and impact of laws can vary widely based on the specific facts involved. Before taking any action, please ensure that you obtain advice specific to your circumstances from your usual PwC client service team or your other advisers.

The materials contained in this presentation were assembled in May 2015 and were based on the law enforceable and information available at that time.

© 2015 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.