Embed Size (px)

Citation preview

RDC Trailblazers Leveraging new technologies while minimizing

risk and maximizing results.

Bob Hedges Managing Director, AlixPartners

Chris Chaten

Vice President, Product Management JPMorgan Chase & Co.

September 29, 2011

MOBILE RDC Changing How Consumers Bank

and How Banks Compete

Bob Hedges Managing Director, AlixPartners

September 29, 2011

Four Key Themes

• Aggressive Smartphone Adoption by Consumers Is Driving the ‘Mobilizing’ of Financial Services

• Mobile RDC Is Becoming Critical to Consumer Choice

• Significant Growth Is Forecast

• Mobile RDC Is an Important Strategic and Economic Opportunity

3 The 2011 RDC Simmit - RDC Trailblazers

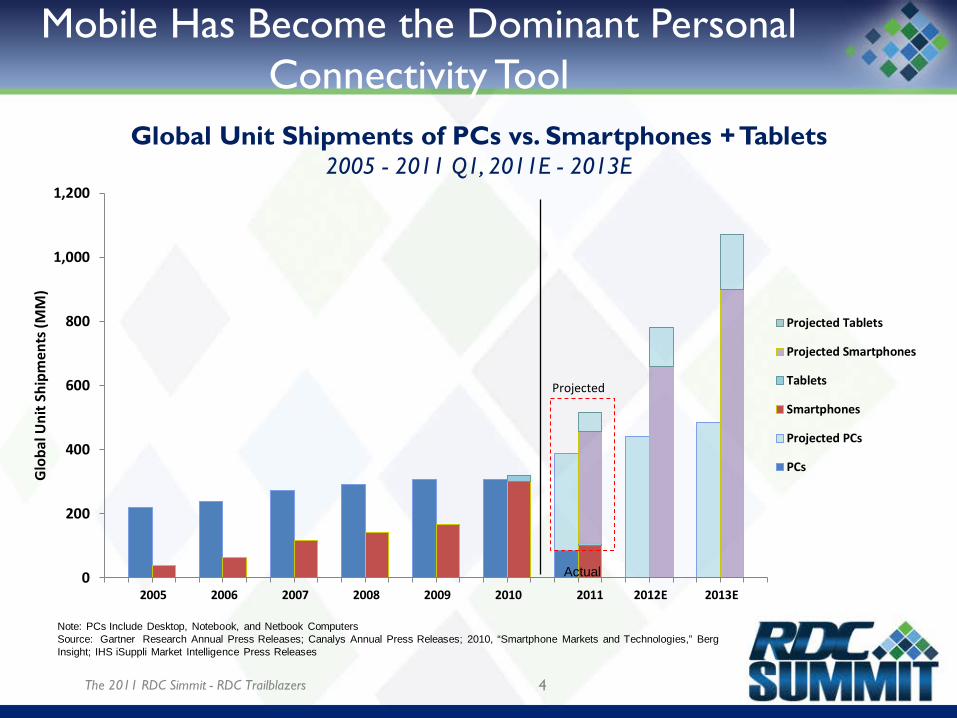

Mobile Has Become the Dominant Personal Connectivity Tool

4 The 2011 RDC Simmit - RDC Trailblazers

Global Unit Shipments of PCs vs. Smartphones + Tablets 2005 - 2011 Q1, 2011E - 2013E

Note: PCs Include Desktop, Notebook, and Netbook Computers Source: Gartner Research Annual Press Releases; Canalys Annual Press Releases; 2010, “Smartphone Markets and Technologies,” Berg Insight; IHS iSuppli Market Intelligence Press Releases

0

200

400

600

800

1,000

1,200

2005 2006 2007 2008 2009 2010 2011 2012E 2013E

Glo

bal U

nit S

hipm

ents

(MM

)

Projected Tablets

Projected Smartphones

Tablets

Smartphones

Projected PCs

PCs

Projected

Actual

5

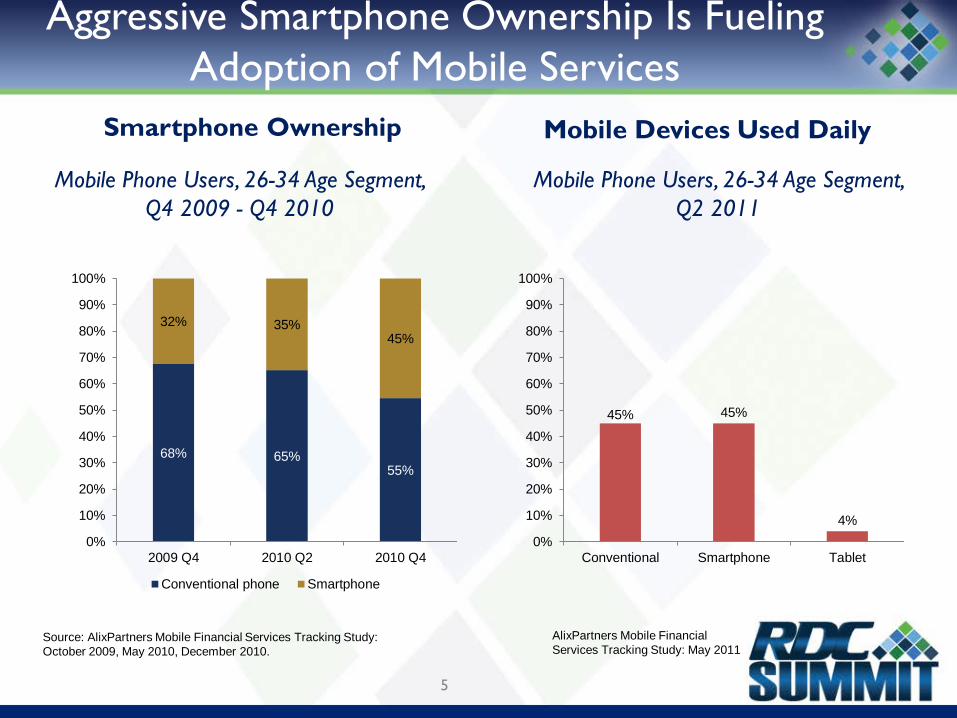

Smartphone Ownership

Source: AlixPartners Mobile Financial Services Tracking Study: October 2009, May 2010, December 2010.

68% 65% 55%

32% 35% 45%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 Q4 2010 Q2 2010 Q4

Conventional phone Smartphone

AlixPartners Mobile Financial Services Tracking Study: May 2011

Mobile Phone Users, 26-34 Age Segment, Q2 2011

45% 45%

4% 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Conventional Smartphone Tablet

Mobile Phone Users, 26-34 Age Segment, Q4 2009 - Q4 2010

Mobile Devices Used Daily

Aggressive Smartphone Ownership Is Fueling Adoption of Mobile Services

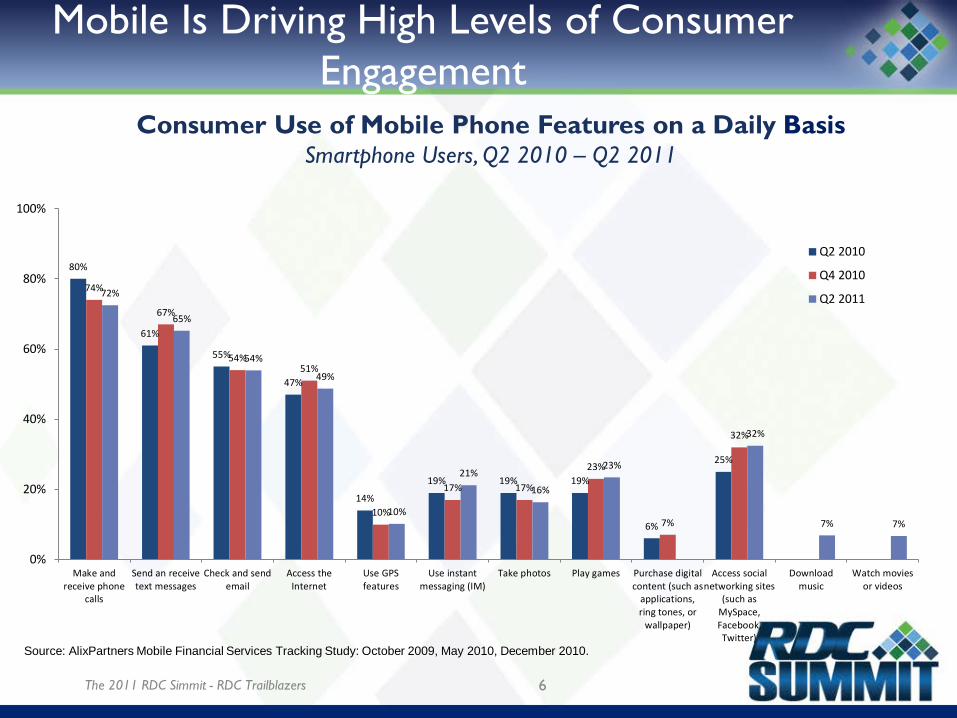

Mobile Is Driving High Levels of Consumer Engagement

6 The 2011 RDC Simmit - RDC Trailblazers

80%

61%

55%

47%

14%

19% 19% 19%

6%

25%

74%

67%

54% 51%

10%

17% 17%

23%

7%

32%

72%

65%

54%

49%

10%

21%

16%

23%

32%

7% 7%

0%

20%

40%

60%

80%

100%

Make andreceive phone

calls

Send an receivetext messages

Check and sendemail

Access theInternet

Use GPSfeatures

Use instantmessaging (IM)

Take photos Play games Purchase digitalcontent (such as

applications,ring tones, or

wallpaper)

Access socialnetworking sites

(such asMySpace,Facebook,Twitter)

Downloadmusic

Watch moviesor videos

Q2 2010

Q4 2010

Q2 2011

Source: AlixPartners Mobile Financial Services Tracking Study: October 2009, May 2010, December 2010.

Consumer Use of Mobile Phone Features on a Daily Basis Smartphone Users, Q2 2010 – Q2 2011

7

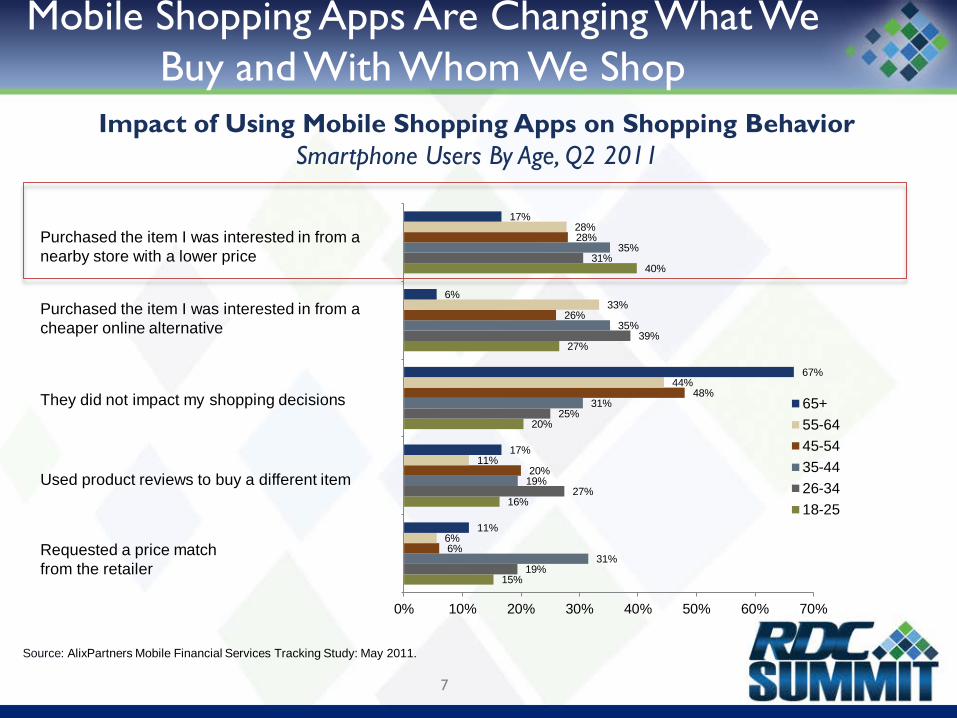

Purchased the item I was interested in from a nearby store with a lower price

Purchased the item I was interested in from a cheaper online alternative

They did not impact my shopping decisions

Impact of Using Mobile Shopping Apps on Shopping Behavior Smartphone Users By Age, Q2 2011

Used product reviews to buy a different item

Requested a price match from the retailer

15%

16%

20%

27%

40%

19%

27%

25%

39%

31%

31%

19%

31%

35%

35%

6%

20%

48%

26%

28%

6%

11%

44%

33%

28%

11%

17%

67%

6%

17%

0% 10% 20% 30% 40% 50% 60% 70%

65+55-6445-5435-4426-3418-25

Source: AlixPartners Mobile Financial Services Tracking Study: May 2011.

Mobile Shopping Apps Are Changing What We Buy and With Whom We Shop

8

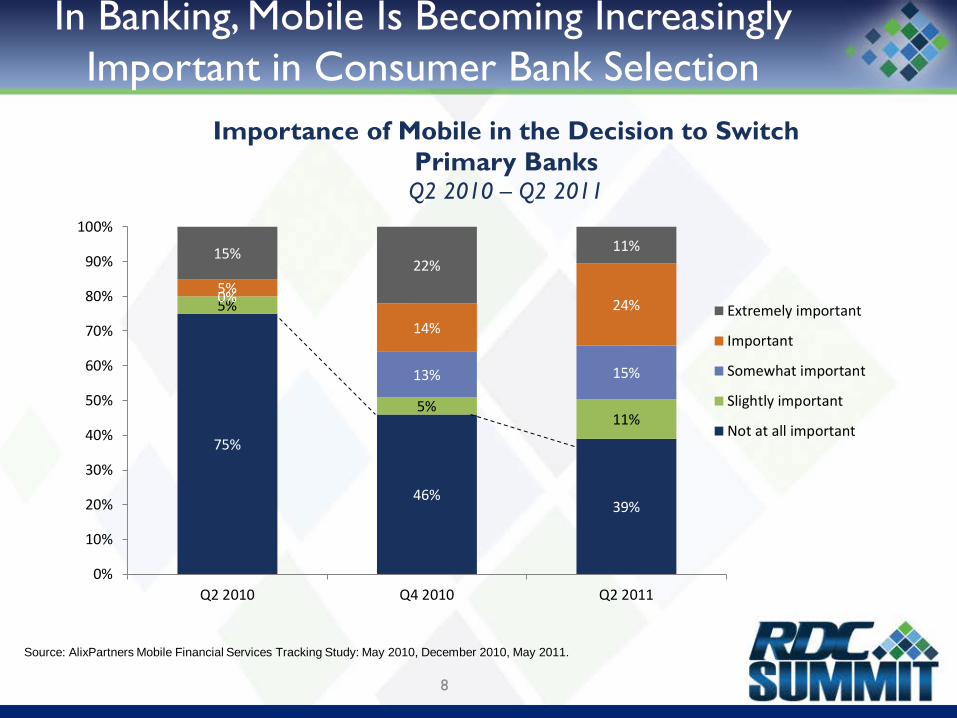

75%

46% 39%

5%

5% 11%

0%

13% 15%

5%

14% 24%

15% 22%

11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q2 2010 Q4 2010 Q2 2011

Importance of Mobile in the Decision to Switch Primary Banks Q2 2010 – Q2 2011

Extremely important

Important

Somewhat important

Slightly important

Not at all important

Source: AlixPartners Mobile Financial Services Tracking Study: May 2010, December 2010, May 2011.

In Banking, Mobile Is Becoming Increasingly Important in Consumer Bank Selection

9

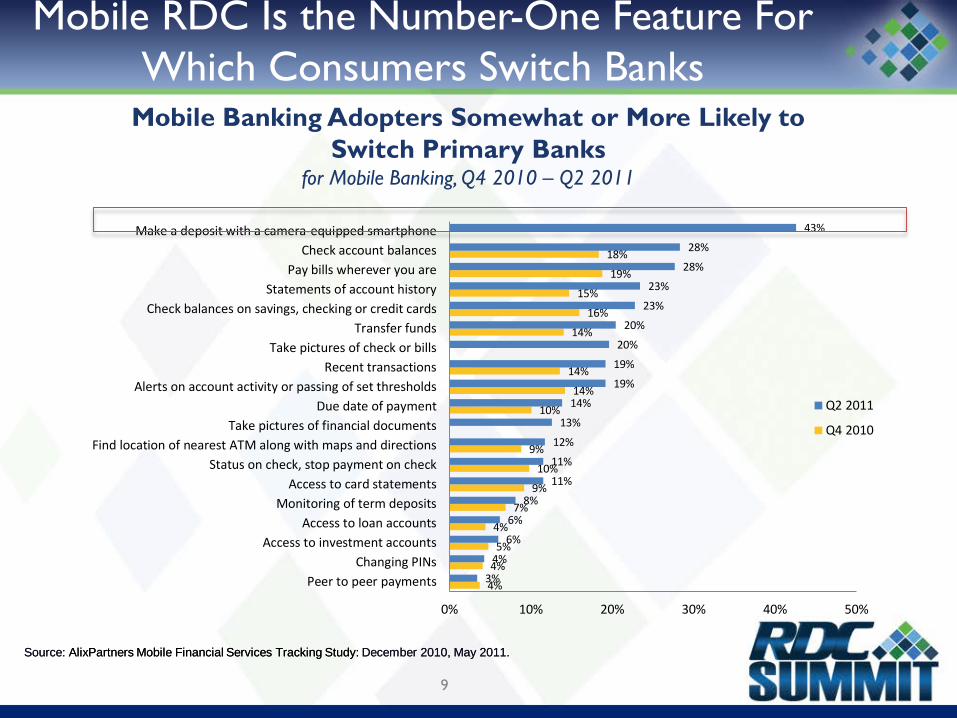

Mobile RDC Is the Number-One Feature For Which Consumers Switch Banks

Source: AlixPartners Mobile Financial Services Tracking Study: December 2010, May 2011.

Mobile Banking Adopters Somewhat or More Likely to Switch Primary Banks

for Mobile Banking, Q4 2010 – Q2 2011

4%

4%

5%

4%

7%

9%

10%

9%

10%

14%

14%

14%

16%

15%

19%

18%

3%

4%

6%

6%

8%

11%

11%

12%

13%

14%

19%

19%

20%

20%

23%

23%

28%

28%

43%

0% 10% 20% 30% 40% 50%

Peer to peer paymentsChanging PINs

Access to investment accountsAccess to loan accounts

Monitoring of term depositsAccess to card statements

Status on check, stop payment on checkFind location of nearest ATM along with maps and directions

Take pictures of financial documentsDue date of payment

Alerts on account activity or passing of set thresholdsRecent transactions

Take pictures of check or billsTransfer funds

Check balances on savings, checking or credit cardsStatements of account history

Pay bills wherever you areCheck account balances

Make a deposit with a camera-equipped smartphone

Q2 2011

Q4 2010

Source: AlixPartners Mobile Financial Services Tracking Study: December 2010, May 2011.

10

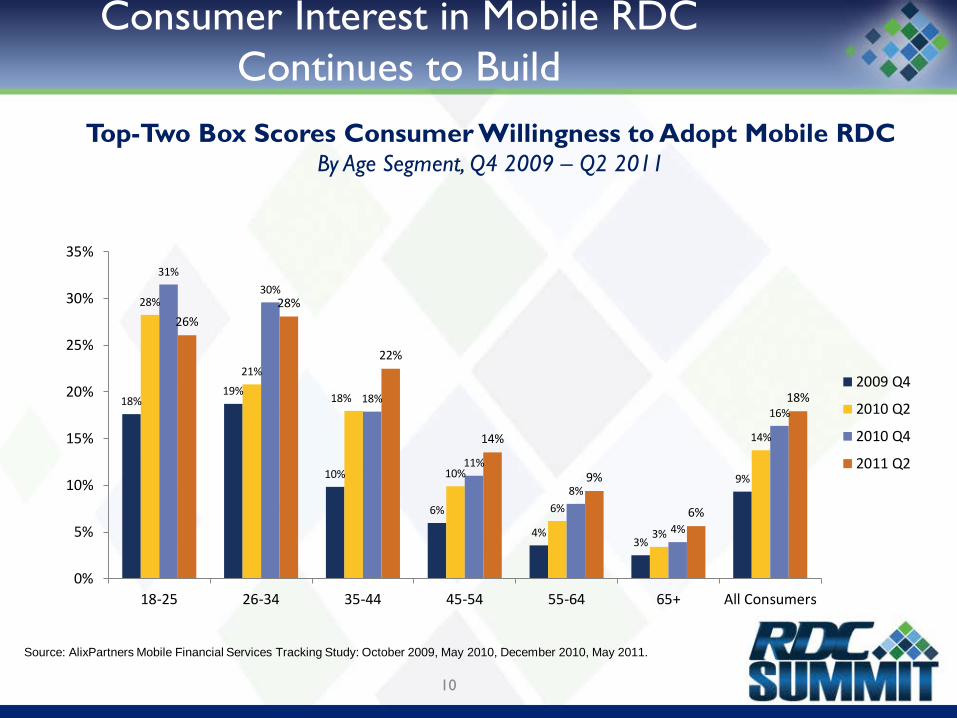

Consumer Interest in Mobile RDC Continues to Build

18% 19%

10%

6%

4% 3%

9%

28%

21%

18%

10%

6%

3%

14%

31% 30%

18%

11%

8%

4%

16%

26% 28%

22%

14%

9%

6%

18%

0%

5%

10%

15%

20%

25%

30%

35%

18-25 26-34 35-44 45-54 55-64 65+ All Consumers

2009 Q4

2010 Q2

2010 Q4

2011 Q2

Top-Two Box Scores Consumer Willingness to Adopt Mobile RDC By Age Segment, Q4 2009 – Q2 2011

Source: AlixPartners Mobile Financial Services Tracking Study: October 2009, May 2010, December 2010, May 2011.

11

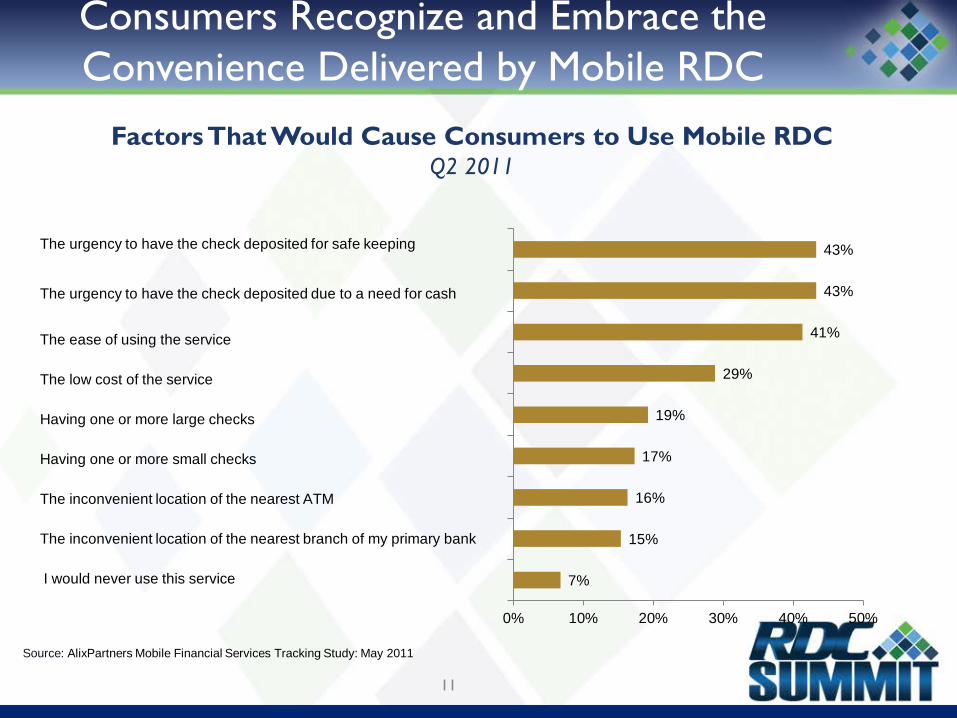

Consumers Recognize and Embrace the Convenience Delivered by Mobile RDC

Source: AlixPartners Mobile Financial Services Tracking Study: May 2011

Factors That Would Cause Consumers to Use Mobile RDC Q2 2011

7%

15%

16%

17%

19%

29%

41%

43%

43%

0% 10% 20% 30% 40% 50%

The urgency to have the check deposited for safe keeping

The urgency to have the check deposited due to a need for cash

The ease of using the service

The low cost of the service

Having one or more large checks

Having one or more small checks

The inconvenient location of the nearest ATM

The inconvenient location of the nearest branch of my primary bank

I would never use this service

12

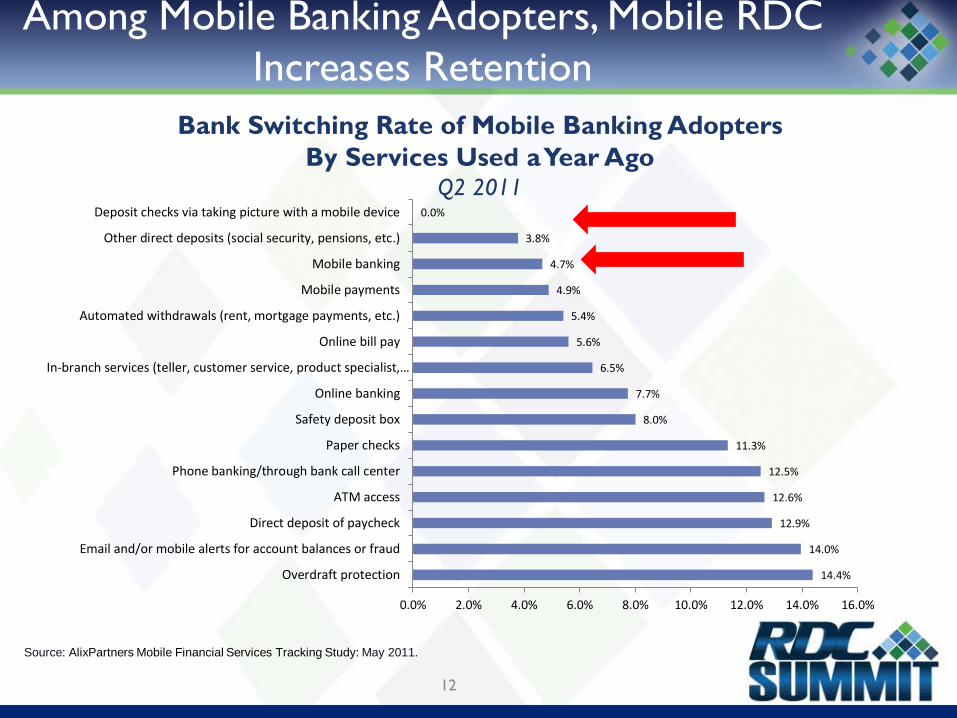

Among Mobile Banking Adopters, Mobile RDC Increases Retention

14.4%

14.0%

12.9%

12.6%

12.5%

11.3%

8.0%

7.7%

6.5%

5.6%

5.4%

4.9%

4.7%

3.8%

0.0%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0%

Overdraft protection

Email and/or mobile alerts for account balances or fraud

Direct deposit of paycheck

ATM access

Phone banking/through bank call center

Paper checks

Safety deposit box

Online banking

In-branch services (teller, customer service, product specialist,…

Online bill pay

Automated withdrawals (rent, mortgage payments, etc.)

Mobile payments

Mobile banking

Other direct deposits (social security, pensions, etc.)

Deposit checks via taking picture with a mobile device

Source: AlixPartners Mobile Financial Services Tracking Study: May 2011.

Bank Switching Rate of Mobile Banking Adopters By Services Used a Year Ago

Q2 2011

13

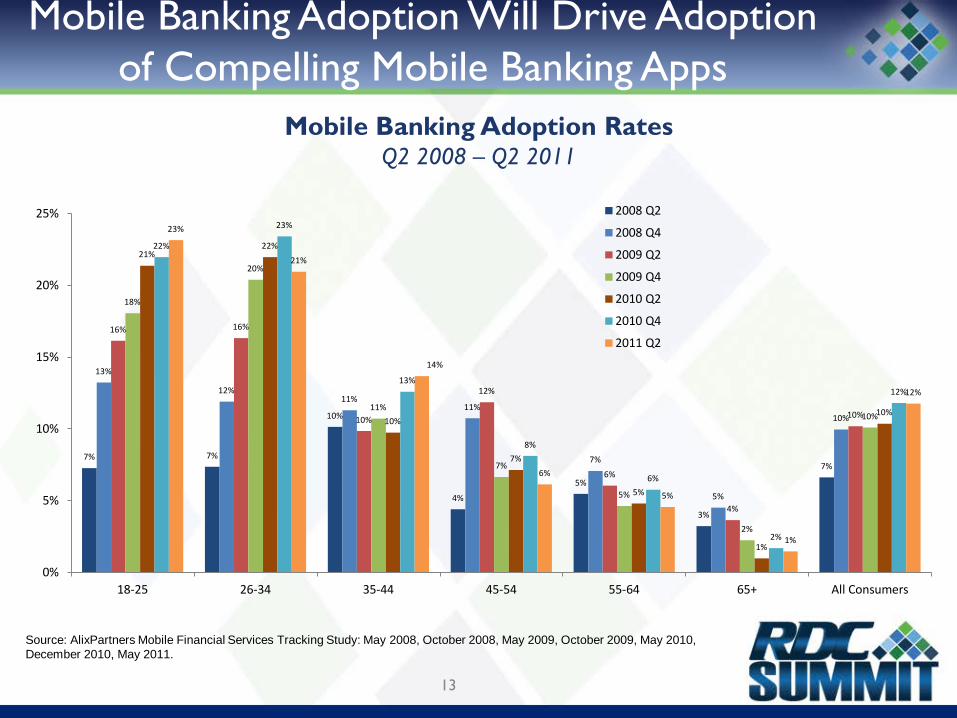

Mobile Banking Adoption Rates Q2 2008 – Q2 2011

Source: AlixPartners Mobile Financial Services Tracking Study: May 2008, October 2008, May 2009, October 2009, May 2010, December 2010, May 2011.

7% 7%

10%

4%

5%

3%

7%

13%

12% 11%

11%

7%

5%

10%

16% 16%

10%

12%

6%

4%

10%

18%

20%

11%

7%

5%

2%

10%

21% 22%

10%

7%

5%

1%

10%

22%

23%

13%

8%

6%

2%

12%

23%

21%

14%

6%

5%

1%

12%

0%

5%

10%

15%

20%

25%

18-25 26-34 35-44 45-54 55-64 65+ All Consumers

2008 Q2

2008 Q4

2009 Q2

2009 Q4

2010 Q2

2010 Q4

2011 Q2

Mobile Banking Adoption Will Drive Adoption of Compelling Mobile Banking Apps

14

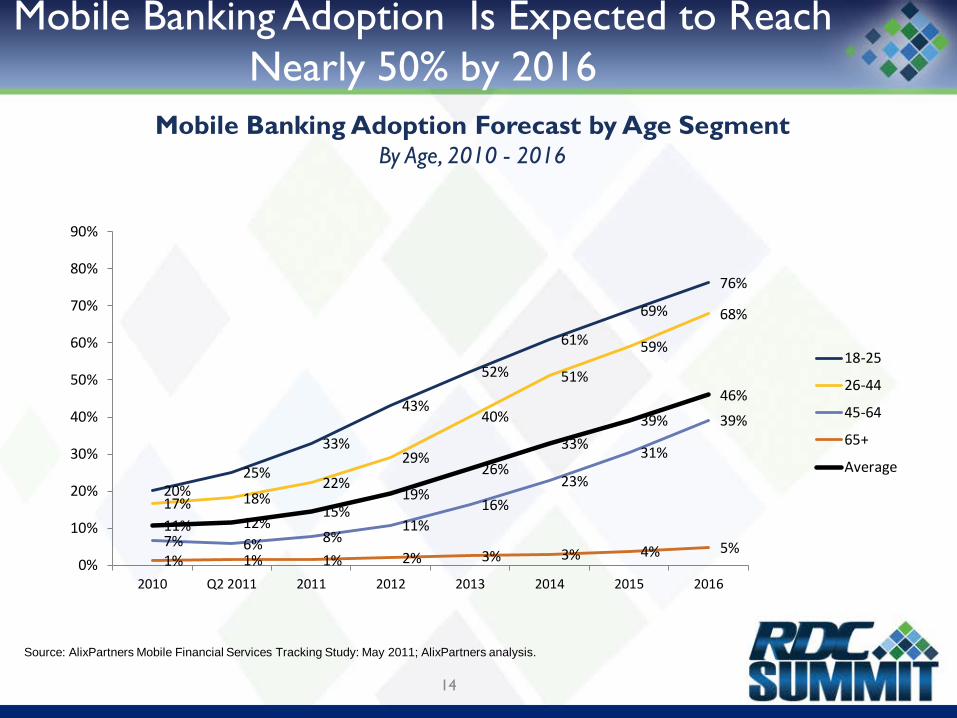

Mobile Banking Adoption Is Expected to Reach Nearly 50% by 2016

20% 25%

33%

43%

52%

61%

69%

76%

17% 18% 22%

29%

40%

51%

59%

68%

7% 6% 8% 11%

16% 23%

31%

39%

1% 1% 1% 2% 3% 3% 4% 5% 11% 12%

15% 19%

26%

33% 39%

46%

2010 Q2 2011 2011 2012 2013 2014 2015 20160%

10%

20%

30%

40%

50%

60%

70%

80%

90%

18-25

26-44

45-64

65+

Average

Mobile Banking Adoption Forecast by Age Segment By Age, 2010 - 2016

Source: AlixPartners Mobile Financial Services Tracking Study: May 2011; AlixPartners analysis.

15

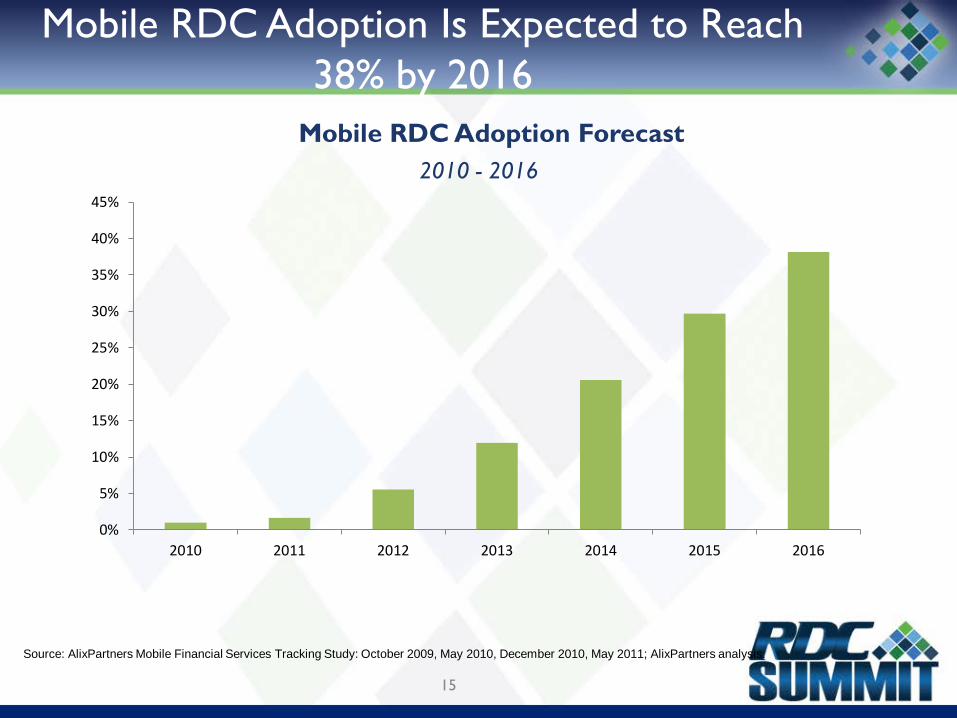

Mobile RDC Adoption Is Expected to Reach 38% by 2016

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2010 2011 2012 2013 2014 2015 2016

2010 - 2016

Source: AlixPartners Mobile Financial Services Tracking Study: October 2009, May 2010, December 2010, May 2011; AlixPartners analysis.

Mobile RDC Adoption Forecast

16

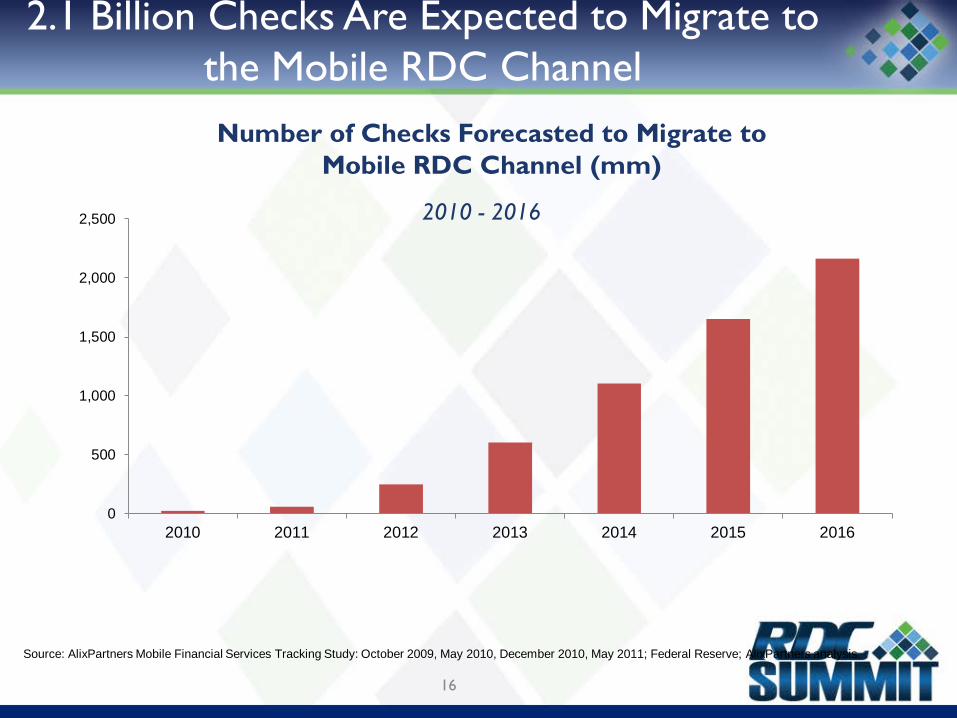

2.1 Billion Checks Are Expected to Migrate to the Mobile RDC Channel

0

500

1,000

1,500

2,000

2,500

2010 2011 2012 2013 2014 2015 2016

2010 - 2016

Source: AlixPartners Mobile Financial Services Tracking Study: October 2009, May 2010, December 2010, May 2011; Federal Reserve; AlixPartners analysis.

Number of Checks Forecasted to Migrate to Mobile RDC Channel (mm)

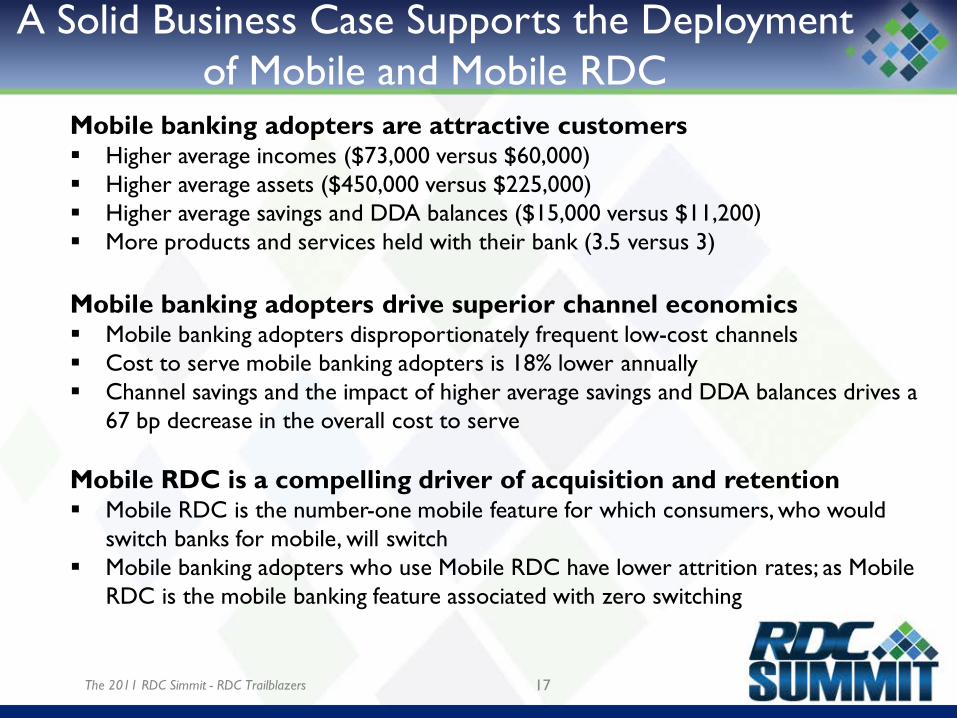

A Solid Business Case Supports the Deployment of Mobile and Mobile RDC

17 The 2011 RDC Simmit - RDC Trailblazers

Mobile banking adopters are attractive customers Higher average incomes ($73,000 versus $60,000) Higher average assets ($450,000 versus $225,000) Higher average savings and DDA balances ($15,000 versus $11,200) More products and services held with their bank (3.5 versus 3)

Mobile banking adopters drive superior channel economics Mobile banking adopters disproportionately frequent low-cost channels Cost to serve mobile banking adopters is 18% lower annually Channel savings and the impact of higher average savings and DDA balances drives a

67 bp decrease in the overall cost to serve

Mobile RDC is a compelling driver of acquisition and retention Mobile RDC is the number-one mobile feature for which consumers, who would

switch banks for mobile, will switch Mobile banking adopters who use Mobile RDC have lower attrition rates; as Mobile

RDC is the mobile banking feature associated with zero switching

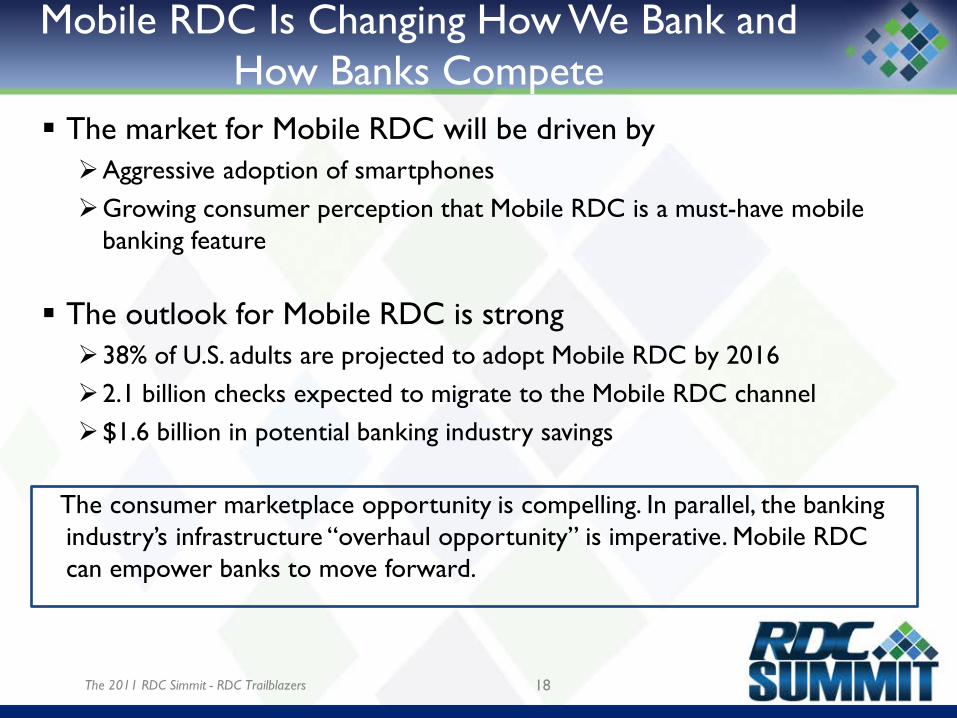

Mobile RDC Is Changing How We Bank and How Banks Compete

The market for Mobile RDC will be driven by Aggressive adoption of smartphones Growing consumer perception that Mobile RDC is a must-have mobile

banking feature

The outlook for Mobile RDC is strong 38% of U.S. adults are projected to adopt Mobile RDC by 2016 2.1 billion checks expected to migrate to the Mobile RDC channel $1.6 billion in potential banking industry savings

The consumer marketplace opportunity is compelling. In parallel, the banking industry’s infrastructure “overhaul opportunity” is imperative. Mobile RDC can empower banks to move forward.

18 The 2011 RDC Simmit - RDC Trailblazers

Remote Deposit Capture:

Getting to Mobile

Chris Chaten Vice President, Product Management

JPMorgan Chase & Co.

September 29, 2011

Agenda

• Topics – The Evolution of RDC at JPMorgan Chase – Common Questions and Concerns – What’s Next?

• Themes – Evolved Technology is Simple – Consumer mRDC is a primary deposit channel – Corporate mRDC is on the way

20 The 2011 RDC Simmit - RDC Trailblazers

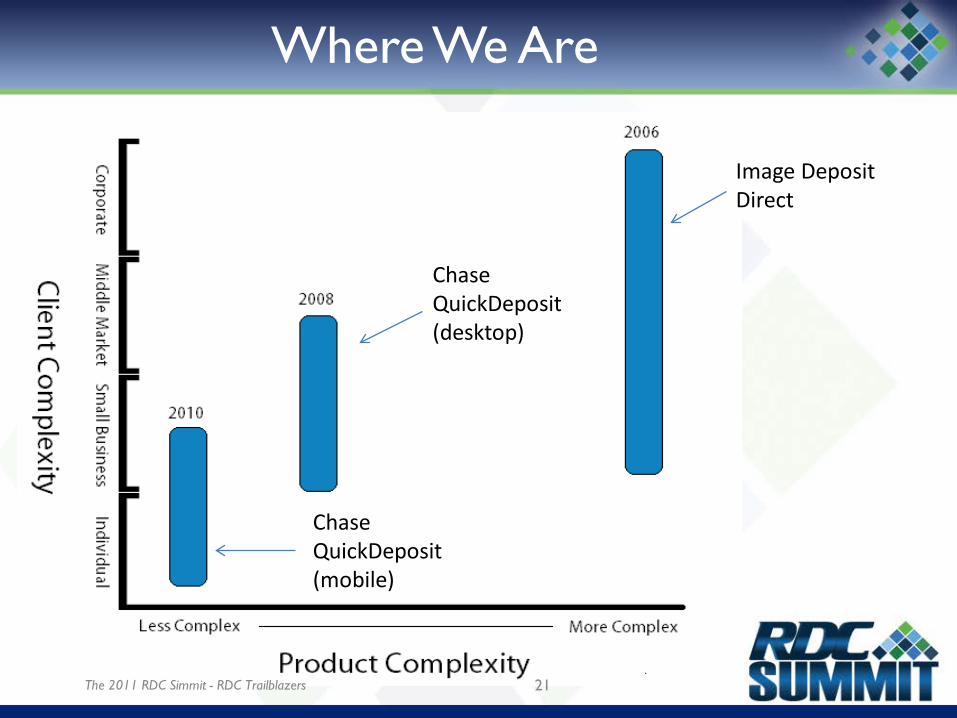

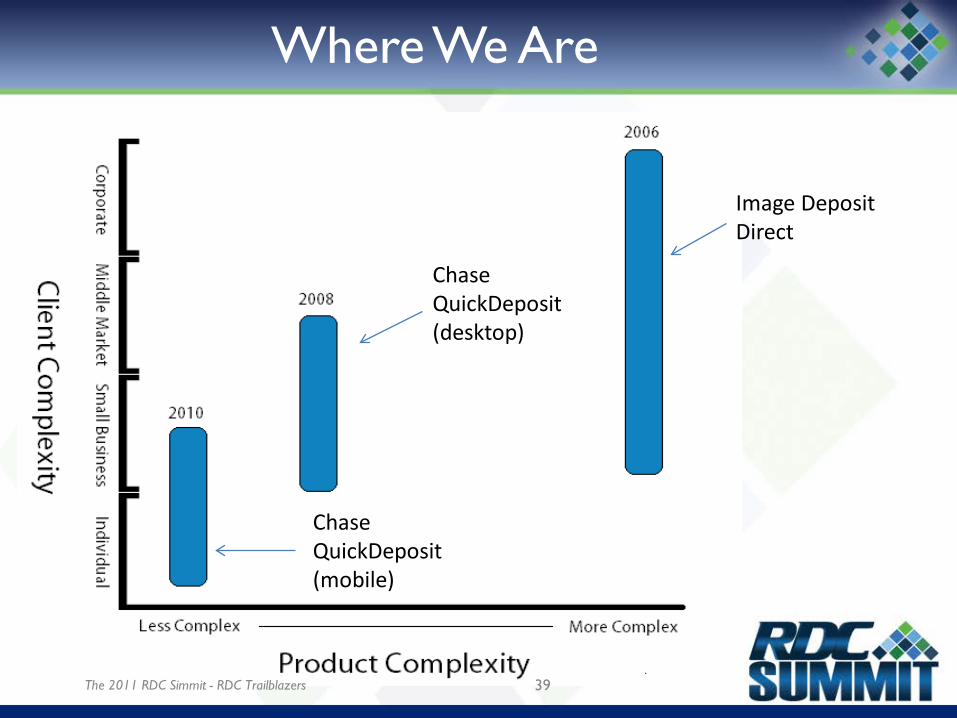

Where We Are

Image Deposit Direct

Chase QuickDeposit (desktop)

Chase QuickDeposit (mobile)

The 2011 RDC Simmit - RDC Trailblazers 21

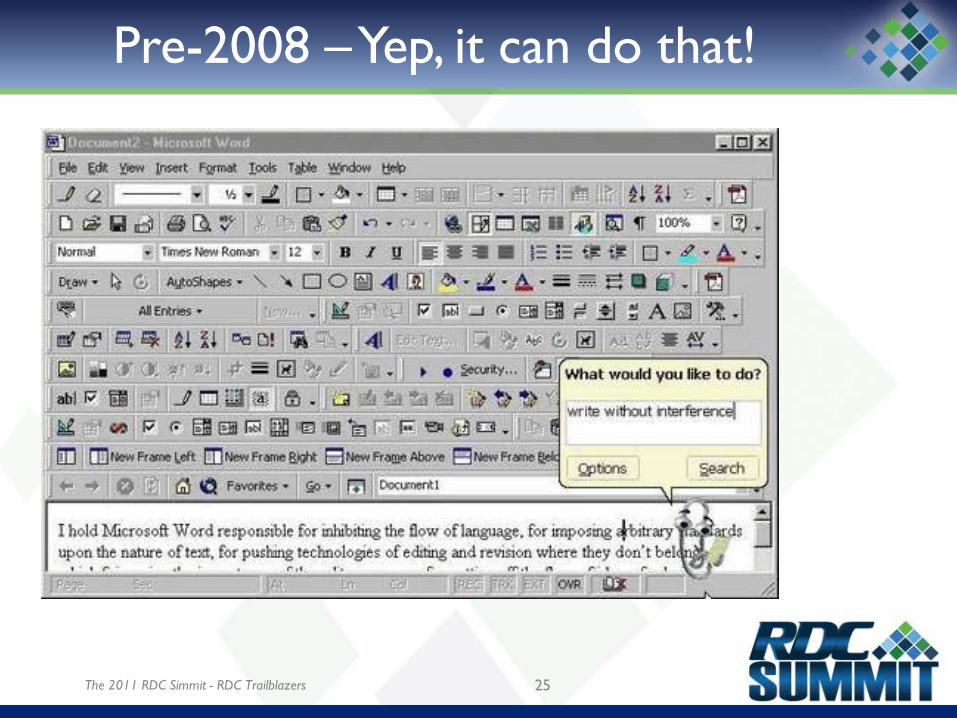

Pre-2008 – Setting the Stage

• Introduced Image Deposit Direct in 2006 • “One Size Fits All” Solution • Features / Functions:

– Coupon Scanning – Franking – Endorsement / Virtual Endorsement – Remittance Fields – Standard Forms – Custom Forms – Standard Reports – Custom Reports

The 2011 RDC Simmit - RDC Trailblazers 22

Pre-2008 – Challenges

• Manual Implementation Process – After the sale, each “feature” required implementations to

ask clients how to set it up – Manual Process Invited Setup Errors – Clients didn’t typically know what we were talking about

• Cluttered User Interface • Vendor Driven

– Little Opportunity for Differentiation – “Pace-of-Play” – Commoditization

• No Integration with Online Banking

The 2011 RDC Simmit - RDC Trailblazers 23

Pre-2008 - Who We Served

• Served the Needs of Large, Complex Clients – Clients with treasury expertise – Substitute for lockbox – Integration on AR systems – Large scale deployments to multiple sites – High-volume with many accounts

• “The RFP requires XYZ feature!” – Sales loved it. – Kind of.

The 2011 RDC Simmit - RDC Trailblazers 24

Pre-2008 – Yep, it can do that!

The 2011 RDC Simmit - RDC Trailblazers 25

2007 – Simplify, Integrate

• 75% of our clients didn’t need to be “sold” • Smaller clients had no one speaking for them • Mission – build an easy to use, no-frills solution for

the 75% – Integrate with Chase.com – Automate enrollment process

The 2011 RDC Simmit - RDC Trailblazers 26

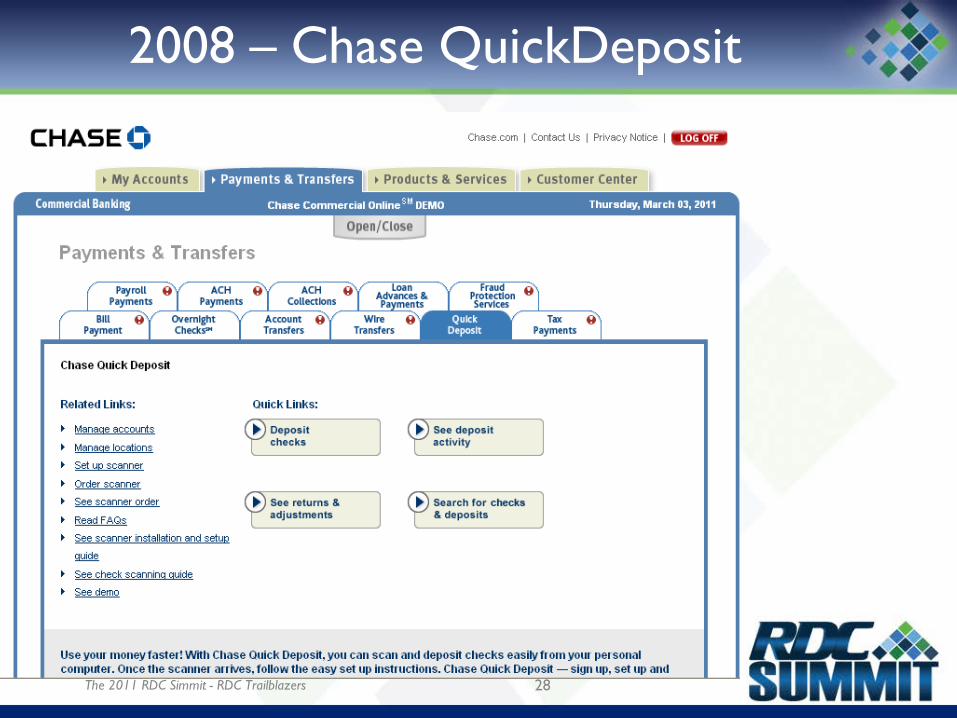

2008 – Chase QuickDeposit

• Released to our Business Banking and Commercial Banking online platform (chase.com)

• Targeted clients <$25 MM in annual revenue • Typical profile:

– 1 or 2 scanners – 1 - 3 accounts – 200 checks per month

• Clients scan up to 3,000 checks per month from 20+ locations

The 2011 RDC Simmit - RDC Trailblazers 27

2008 – Chase QuickDeposit

The 2011 RDC Simmit - RDC Trailblazers 28

2010 – Chase QuickDeposit Mobile

• Smartphones take over the world • Built a dedicated mobile development team following

WaMu deal • Opportunity to offer an innovative product to

consumers • Led to Development of Chase QuickDeposit Mobile

– Consumers, High-Net Worth, Small Business • Launched in July of 2010

The 2011 RDC Simmit - RDC Trailblazers 29

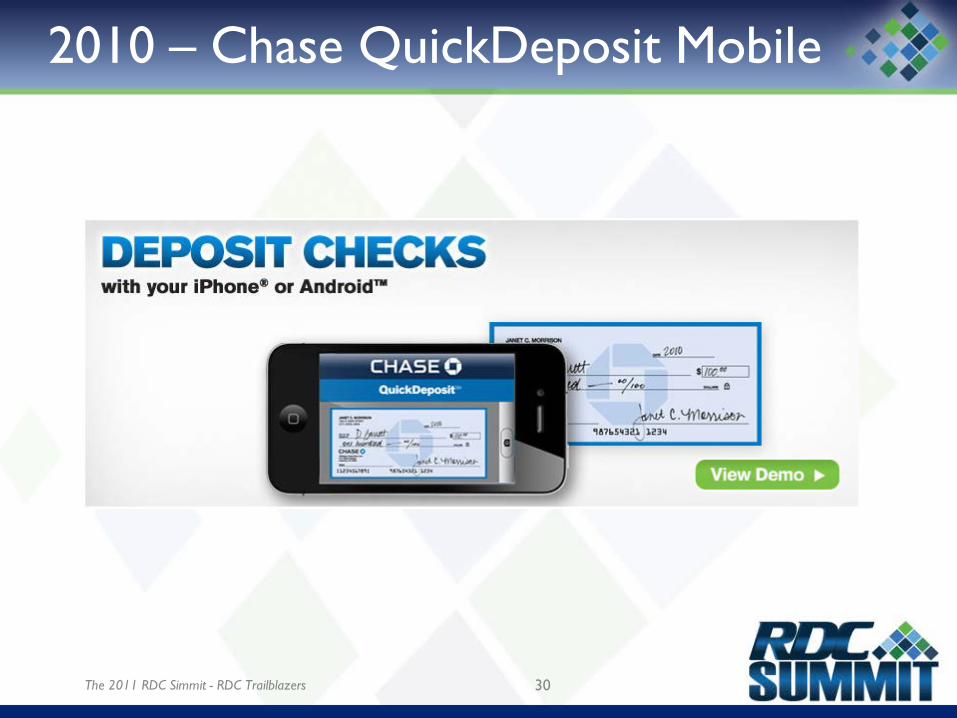

2010 – Chase QuickDeposit Mobile

30 The 2011 RDC Simmit - RDC Trailblazers

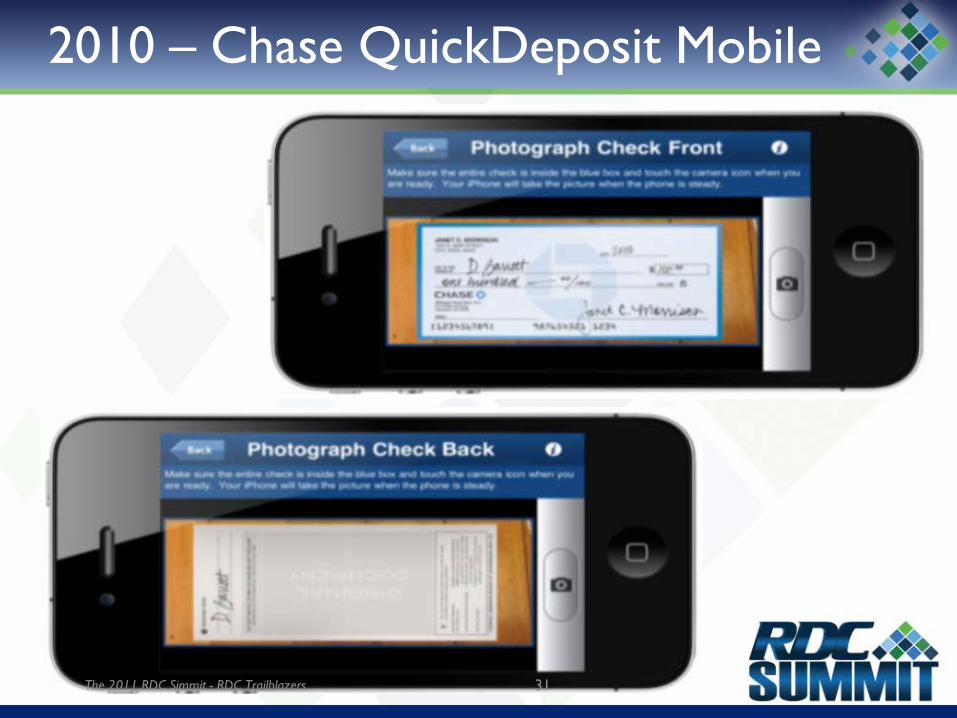

2010 – Chase QuickDeposit Mobile

The 2011 RDC Simmit - RDC Trailblazers 31

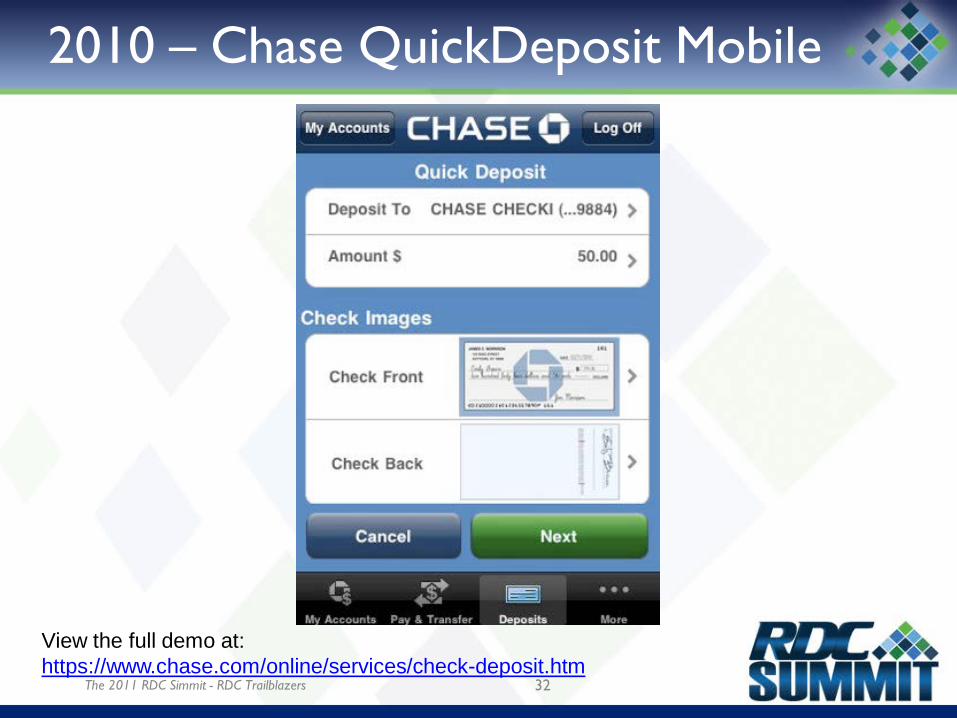

2010 – Chase QuickDeposit Mobile

View the full demo at: https://www.chase.com/online/services/check-deposit.htm

The 2011 RDC Simmit - RDC Trailblazers 32

2010 – Chase QuickDeposit Mobile

• Key Features – Supports iOS and Android – Fully-integrated component of the Chase Mobile

applications – Various deposit limits help mitigate bank-side risk – It‘s really simple

The 2011 RDC Simmit - RDC Trailblazers 33

2010 – Chase QuickDeposit Mobile

• Challenges – Image Quality – Which Operating Systems?

• iOS • Android • Blackberry • webOS • Windows Phone 7

– Fraud • Deposit Limits

The 2011 RDC Simmit - RDC Trailblazers 34

2010 – Chase QuickDeposit Mobile

• Highlights • New York Times writer David Pogue named Chase QuickDeposit as

the “best technology idea” of 2010 • Winner of 2 Webby Awards in 2011 • Super Bowl Ad

The 2011 RDC Simmit - RDC Trailblazers 35

2011 – Going Corporate

• Extended knowledge from retail space • White-label integration ties into the desktop RDC

used at brick-and-mortar branches • JPMorgan Chase now powers large bank and

brokerage mRDC applications

The 2011 RDC Simmit - RDC Trailblazers 36

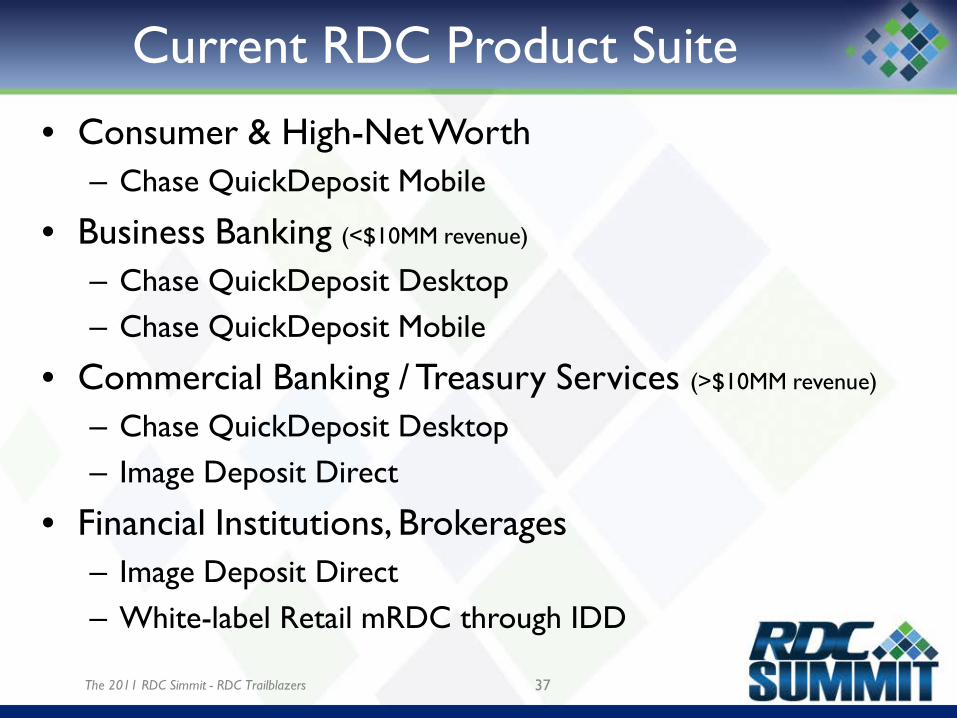

Current RDC Product Suite

• Consumer & High-Net Worth – Chase QuickDeposit Mobile

• Business Banking (<$10MM revenue)

– Chase QuickDeposit Desktop – Chase QuickDeposit Mobile

• Commercial Banking / Treasury Services (>$10MM revenue)

– Chase QuickDeposit Desktop – Image Deposit Direct

• Financial Institutions, Brokerages – Image Deposit Direct – White-label Retail mRDC through IDD

37 The 2011 RDC Simmit - RDC Trailblazers

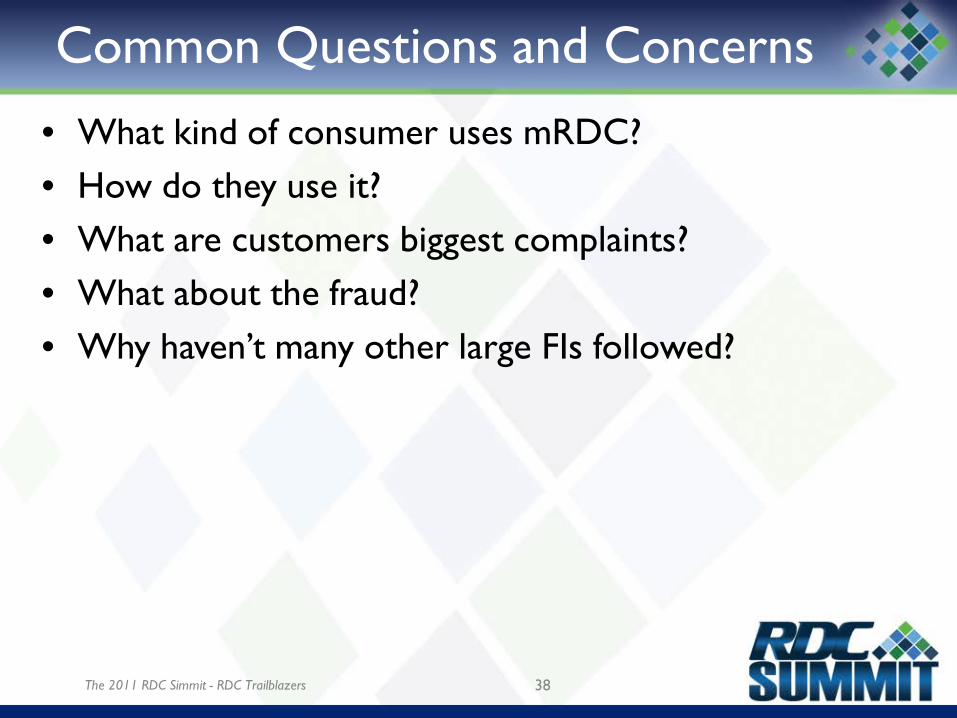

Common Questions and Concerns

• What kind of consumer uses mRDC? • How do they use it? • What are customers biggest complaints? • What about the fraud? • Why haven’t many other large FIs followed?

38 The 2011 RDC Simmit - RDC Trailblazers

Where We Are

Image Deposit Direct

Chase QuickDeposit (desktop)

Chase QuickDeposit (mobile)

The 2011 RDC Simmit - RDC Trailblazers 39

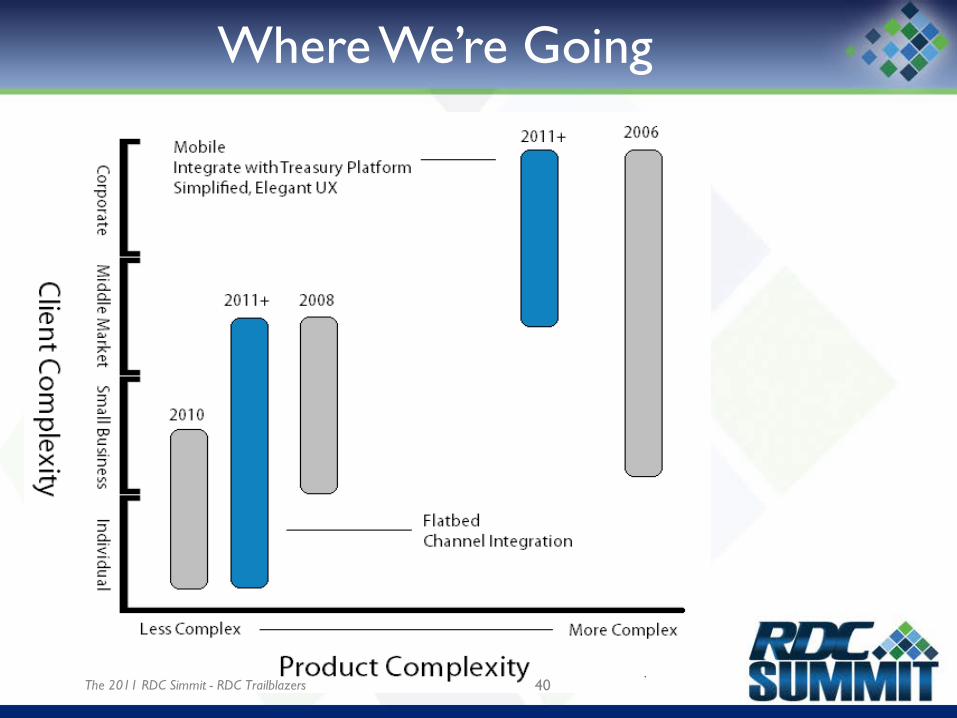

Where We’re Going

The 2011 RDC Simmit - RDC Trailblazers 40

What’s next?

• Integration with Complex Treasury Workstations • Non-FI Custom Application Development • New Hardware Optimized for Mobile Experience • Corporate mRDC via Smartphone

– Targeted at insurance agents, non-profits, and distribution companies

– An extension of the desktop solution – Coming in October 2011…

41 The 2011 RDC Simmit - RDC Trailblazers

“Main Event” Reception 6-8PM

Live Jazz, Great Food, Cool Drinks… and Prizes!

42