Embed Size (px)

Citation preview

Ready to IPO or IPO Ready

13 May 2014

Strictly Private & Confidential

2

IPO – not an end in itself…..

Is an IPO the right strategy to pursue? Staff / business / customers / exit

What are the key drivers? Capital / liquidity / new investors / profile / other

Is my business plan robust? Achievable / Level of

predictability / Competitive positioning

What steps do I need to take to prepare? Systems / governance / structure / diligence

3

IPO scorecard

-’s

Capital

Acquisition currency

Liquidity

Incentivisation (…act like owners)

Profile

Impact for customers / partners

Maintain control of direction

New markets

Credibility with Banks etc

Attract / retain talent

+’s

Volatility of share price

Lock-ins

Regulatory obligations

Valuation only known at end of process

Management commitment

Increased disclosure / scrutiny

Control?

By the way…..all external stakeholders require a time commitment

Strong Growth

Recovery

Structural / disruptive

Old school delivery

4

IPOable - Which box do you fit in?

Long term demand characteristics (food /

resources)

Technology driven

Operate outside general GDP dynamics

Clear competitive positioning

Strong differentiators

Size / time to maturity

Track record

Solid / seasoned management

Steady progress with profits

Dividend potential

Potentially old economy

Pure play on Irish recovery

Property, recruitment, retail, hotels…

…of course, Facebook, pharma can break the rules…

Scale / origin of revenues (at least €15m+)

Strong growth trajectory

Business model – predictability of earnings

Track record of deliverability (in terms of growth and profits)

Strong management team (with bandwidth to grow and no over-reliance on one individual)

Good market position (the moat)

Dividend potential (and growing at that..!!)

Clean history

Good corporate governance (Board, remuneration, incentivisation etc)

Defensible / acceptable / market friendly IPO structure – free-float, liquidity, sell down vs new equity, pricing

Stable market conditions

Robust internal financial reporting systems

5

You don’t have to be a €100m revenue company to float!

Ticking the IPO boxes

6

What drives a successful IPO?

2%

7%

9%

29%

35%

57%

65%

91%

Listing venue selection

Reputation of the banking syndicate

Size of transaction

Good corporate governance

Right timing

Confidence in management

Compelling equity story

Attractive pricing

Source: Ernst & Young, Institutional Investor Survey. Note: % represents the number of respondents that chose the particular factor as one of their top three choices.

Source: Bloomberg 7

IPO activity

IPO activity has recovered from 2009 lows

IPO activity in Europe

IPO activity on AIM

60.0 67.9

81.2

19.5 7.7

29.0

41.8

12.9 18.3

13.1

0

100

200

300

400

500

600

€0bn

€25bn

€50bn

€75bn

€100bn

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

Value Deal Count

70.6

89.7 94.7

20.2 8.4

39.0 45.7

17.1

30.0

21.9

0

100

200

300

400

500

600

700

€0bn

€25bn

€50bn

€75bn

€100bn

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014YTD

Value Deal Count

Strong investor appetite for European IPOs in the first four months of 2014

Year-to-date, 119 European IPOs have raised €22bn. €30bn was raised by 265 companies throughout 2013

Recent Irish entrants to ESM and AIM include Mincon and Game Account

Commentary

Demand has been similarly strong for AIM listed IPOs

Year-to-date, 28 companies have raised €1.3bn on AIM. €1.1bn was raised by 52 companies throughout 2013

0.50

0.60

0.70

0.80

0.90

1.00

Price IPO price

1.50

1.60

1.70

1.80

1.90

2.00

Price IPO price

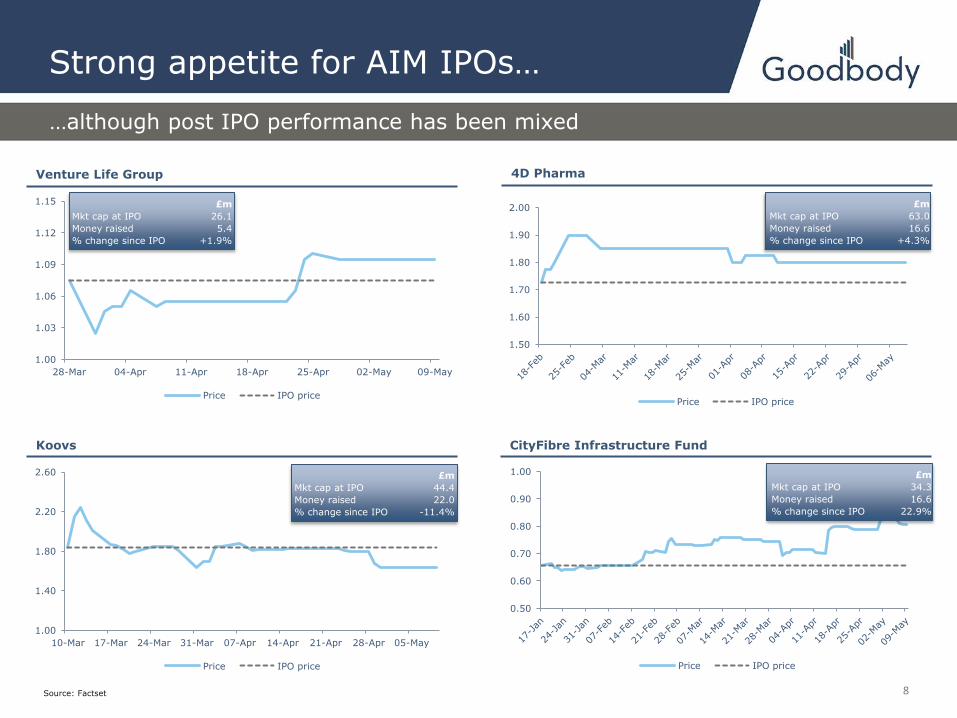

Source: Factset 8

Strong appetite for AIM IPOs…

…although post IPO performance has been mixed

Venture Life Group 4D Pharma

Koovs CityFibre Infrastructure Fund

1.00

1.03

1.06

1.09

1.12

1.15

28-Mar 04-Apr 11-Apr 18-Apr 25-Apr 02-May 09-May

Price IPO price

£m

Mkt cap at IPO 26.1

Money raised 5.4

% change since IPO +1.9%

£m

Mkt cap at IPO 63.0

Money raised 16.6

% change since IPO +4.3%

1.00

1.40

1.80

2.20

2.60

10-Mar 17-Mar 24-Mar 31-Mar 07-Apr 14-Apr 21-Apr 28-Apr 05-May

Price IPO price

£m

Mkt cap at IPO 44.4

Money raised 22.0

% change since IPO -11.4%

£m

Mkt cap at IPO 34.3

Money raised 16.6

% change since IPO 22.9%

9

IPO ready ?

Prep Phase

Finance / Operations Management

Governance Structure

Management Execution of Strategy Communication Ability to juggle competing

priorities (results vs. corporate transactions)

Alignment of interests with shareholders (incentivisation)

Business Plan Robust Deliverable Defensible

Financials Rigorous management

information systems Timely Accurate

Board Experience Perspective Composition Independence Willingness to challenge the status quo

Related Party Must pass the sniff test

Organisation Optimal group structure Location Domicile Tax Memo & Arts Shareholder register

10

Building credibility…..avoiding pitfalls

Restatements – Health check accounting policies

“We made an error in how we accounted for unbilled receivables”

Over promising and under-delivering

“One large contract has slipped into Q1 – just a timing issue”

Taxation holes

“Revenue are questioning

our treatment of…”

Related Party Transactions

“I own the building and my contracting business looks

after the FM”

Late disclosure

“We were not aware that you had been notified by the Regulator in relation to…”

Aggressive accounting

“We booked a portion of revenue prior to commencing service delivery”

Pension

“The scheme is in deficit but we have a plan to fix it…”

Management - CVs

“We weren’t aware that your CFO had done a spell with X…”

Litigation

“We were sued in 2010 and are advised that

we have a very strong case…”

Over-reliance on key suppliers/customers

“Our largest customer represents 40% of revenues…”

2 m

on

ths

pre I

PO

3

-4 m

on

ths

pre I

PO

Flexibility to adapt to changing market conditions

The process itself…from kick off to trading A

s s

oo

n a

s

po

ssib

le

Business plan IPO objectives Identify key issues Evaluate executive management

Po

st

IP

O

1 m

on

th

pre I

PO

1

-2 m

on

ths

pre I

PO

Advisers Legal DD Financial IPO venue Share option schemes Prospectus / admission doc

Audit DD Develop sales pitch Finalise Board Analyst research Verification of prosp/admission doc

Publish analyst research Pre-marketing Address stockex issues Prepare roadshow pres

Research blackout Finalise prosp/admission doc Finalise roadshow pres Begin institutional meetings Build order book

Investor relations Market making Research

Preparation Marketing

11

12

IPO costs

Capital Raise €7.5m

€000s

€15m €000s

€50m €000s

Lawyers 125 175 325

Accountants 75 150 225

Tax 15 20 50

PR 10 25 50

Listing Fees 5 10 20

Listing Documentation 125 200 300

Capital Raising (3-5%) 375 600 1500

Registrars 5 7 10

Total cost 570 1,192 2,455

% of Capital Raise 9.8% 7.9% 4.9%

Average costs of listing on AIM have increased from 6% to 11% (as a % of funds

raised) since 2007 – primarily due to the lower average size of funds raised

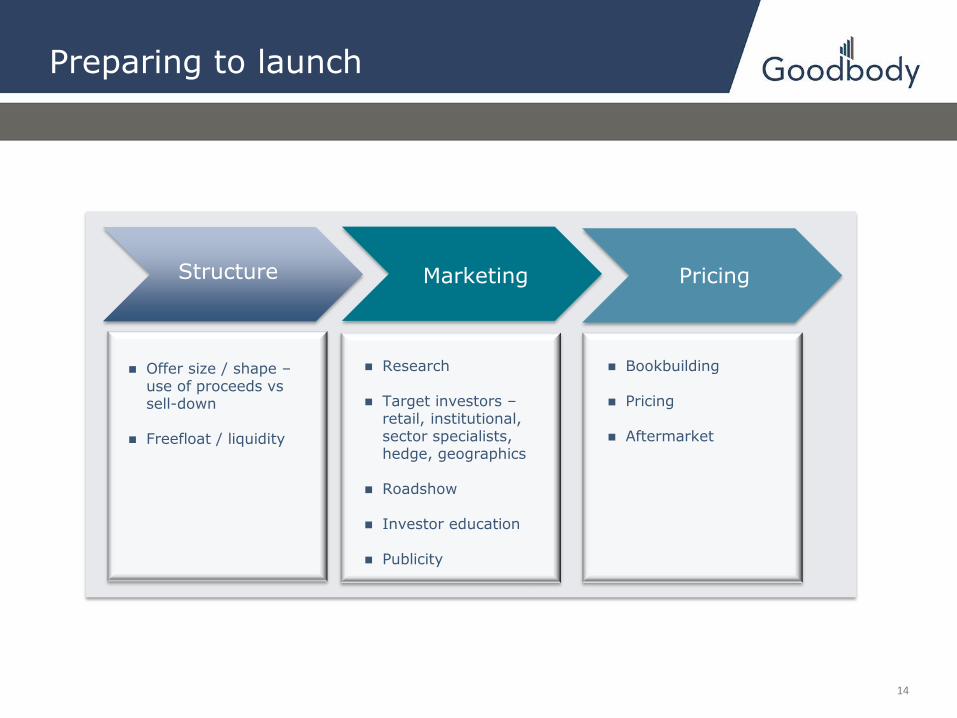

Preparing to Launch

14

Preparing to launch

Offer size / shape – use of proceeds vs sell-down

Freefloat / liquidity

Structure Marketing Pricing

Research

Target investors – retail, institutional, sector specialists, hedge, geographics

Roadshow

Investor education

Publicity

Bookbuilding

Pricing

Aftermarket

14

15

Building the investment case

Pillars

Business Proposition (Creating the

Investment Strapline)

Size of addressable market (third party verification is best)

Growth characteristics of Market (third party again!)

Competitive advantage

History of Delivery (Credibility factor)

Predictability of financial performance

Institutional investors

Our clients and your future shareholders will most likely be international institutions

Institutional Investors (Goodbody Clients)

Union Investment Mgt Irish small companies listed

on the ISE have the most internationalised share registers within Europe

Typical Share Register

Irish Institutions: 5-10% Founders, Management & private shareholders: 30-40% Overseas Institutional Inv.: 50-60%

16

17

Importance of ongoing Investor Relations Programme

After-market

Why? Continuity of communication with investors is key to strong share price

- Maximising public valuation gives ready access to ‘tap’ fresh capital - Strong share price protects against unwanted approaches

How? Two major periods of communication - Full Year and Half Year results

- Two meetings a year sufficient for majority of institutional shareholders - Well prepared presentations have long shelf life

Year round contact with sell- side analysts will keep market updated

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec

Closed period

Results Preparation

Closed period

Closed period

Closed period

AGM & Interim

Mgt Statement

Interim Mgt

Statement

Results and

Roadshow

Results and

Roadshow

18

IR diary

February

1

Talk to Goodbody about road show planning

2 3 4 5 6 7

8 9 10 11 12 13 14

15

First draft of results announcement

16 17 18

First draft of presentation

19 20

Second draft of results announcement

21

22

Second draft of presentation

23 24 25 26 27

Board meeting to sign off on results

28

Announce results Press briefing Conference call for analysts and investors Present to Goodbody sale team

March

1

Dublin IR

2

London IR

3

London IR

4

Edinburgh IR

5

Paris IR

6 7

8

Boston IR

9

NR IR

10 11 12 13 14

15 16 17 18

19 20 21

22 23 24 25 26 27 28

29 30 31

Goodbody Small Cap Conference

Equity markets are always open for companies that are “market ready”

Advantages and disadvantages need to be weighed against alternatives

Preparation is a long term investment in your business

Life as a public company imposes value enhancing discipline

19

To sum up…..

20

THE SOLE PURPOSE OF THIS PRESENTATION IS TO ASSIST THE RECIPIENT IN DECIDING WHETHER IT WISHES TO PROCEED WITH A FURTHER INVESTIGATION OF THE IDEAS AND CONCEPTS PRESENTED HEREIN. THIS PRESENTATION IS NOT INTENDED TO FORM THE BASIS OF A DECISION TO PURCHASE OR SELL SECURITIES OR ANY OTHER INVESTMENT DECISION AND DOES NOT CONSTITUTE AN OFFER, INVITATION OR RECOMMENDATION FOR THE SALE OR PURCHASE OF SECURITIES. NEITHER THE INFORMATION CONTAINED IN THIS PRESENTATION NOR ANY FURTHER INFORMATION MADE AVAILABLE IN CONNECTION WITH THE SUBJECT MATTER CONTAINED HEREIN WILL FORM THE BASIS OF ANY CONTRACT. THE INFORMATION CONTAINED HEREIN IS BASED ON PUBLICLY AVAILABLE INFORMATION AND SOURCES, WHICH WE BELIEVE TO BE RELIABLE, BUT WE DO NOT REPRESENT TO BE ACCURATE OR COMPLETE. THE RECIPIENT OF THIS PRESENTATION MUST MAKE ITS OWN INVESTIGATION AND ASSESSMENT OF THE IDEAS AND CONCEPTS PRESENTED HEREIN. NO REPRESENTATION, WARRANTY OR UNDERTAKING, EXPRESS OR IMPLIED, IS OR WILL BE MADE OR GIVEN AND NO RESPONSIBILITY OR LIABILITY IS OR WILL BE ACCEPTED BY GOODBODY STOCKBROKERS OR GOODBODY CORPORATE FINANCE (“GOODBODY”) OR BY ANY OF ITS DIRECTORS, OFFICERS, EMPLOYEES, AGENTS OR ADVISORS, IN RELATION TO THE ACCURACY OR COMPLETENESS OF THIS PRESENTATION OR ANY OTHER WRITTEN OR ORAL INFORMATION MADE AVAILABLE IN CONNECTION WITH THE IDEAS AND CONCEPTS PRESENTED HEREIN. ANY RESPONSIBILITY OR LIABILITY FOR ANY SUCH INFORMATION IS EXPRESSLY DISCLAIMED. THIS PRESENTATION IS PRIVATE AND CONFIDENTIAL AND IS BEING MADE AVAILABLE TO THE RECIPIENT ON THE EXPRESS UNDERSTANDING THAT IT WILL BE KEPT CONFIDENTIAL AND THAT THE RECIPIENT SHALL NOT COPY, REPRODUCE, DISTRIBUTE OR PASS TO THIRD PARTIES THIS PRESENTATION IN WHOLE OR IN PART AT ANY TIME. THIS PRESENTATION IS THE PROPERTY OF GOODBODY AND THE RECIPIENT AGREES THAT IT WILL, ON REQUEST, PROMPTLY RETURN THIS PRESENTATION AND ALL OTHER INFORMATION SUPPLIED IN CONNECTION WITH THE IDEAS AND CONCEPTS PRESENTED HEREIN, WITHOUT RETAINING ANY COPIES. GOODBODY STOCKBROKERS, TRADING AS GOODBODY, IS REGULATED BY THE CENTRAL BANK OF IRELAND. GOODBODY IS A MEMBER OF THE IRISH STOCK EXCHANGE AND THE LONDON STOCK EXCHANGE. GOODBODY CORPORATE FINANCE IS REGULATED BY THE CENTRAL BANK OF IRELAND. GOODBODY IS A MEMBER OF THE FEXCO GROUP OF COMPANIES.