Embed Size (px)

Citation preview

4/19/2017

1

Real Estate Checklist -

Things Every Elder Law

Attorney Needs to

Understand4th Annual Elder Law Bootcamp: Basics and Beyond

April 27 & 28, 2017

Paul Peterson, Miles L. Jacobs and Erica Crohn Minchella

Sole Owner or Tenant in Common

Property of deceased sole owner or tenant in common passes

to his devisees assuming will is probated, retroactive to date of death

No time limit on probating will

to his heirs at law if no will per Article 2 of Probate Act (755 ILCS 5/1-1

et.seq.)

See Affidavit of Heirship and Heirship Chart attached as exhibits to

Rights of Heirs and Devisees in Illinois Real Estate booklet

Subject to

claims against the estate of deceased

6 months from publication of notice or 3 months from mailing per

Sec. 18-3

2 years from date of death if no estate opened

rights of the personal representative

state and federal tax liens

4/19/2017

2

Passage of Title - Probated Estate

Independent representative unless prohibited in will or supervised

estate requested

Independent Administration set forth at Article 28 of Probate Act

Power to sell, lease, mortgage without court order per Sec. 28-8

Good faith purchasers for value protected in dealing with independent

representative per Sec. 28-9

If real estate distributed to heir or devisee, independent

representative required to record instrument of release and

distribution prior to closing estate

NOT a deed

Sample form CCP 0421 at Cook County Clerk of Court website

Is Probate Necessary or Desired?

Probate applies to assets not otherwise disposed of

Probate necessary to

Determine heirship

Admit will to probate to vest title in devisees

Will contest period is 6 months per Sec. 8-1

Shorten claims period and pay and/or resolve claims

Sell without guardian proceeding

Minor or disabled heir or devisee

Hold assets for missing heir or devisee

4/19/2017

3

Is Title Insurance Necessary? The deceased probably had a title insurance policy insuring them as of the date that they took

title for the purchase price years ago

Owner’s policy includes heirs and devisees who take by operation of law as of the date of the

deceased’s title acquisition

If they sell, they will need a title commitment anyway

Possible items since the acquisition of title:

Deed into revocable trust

Joint tenancy deeds

Transfer on Death Instruments

Line of credit mortgage or reverse mortgage

Judgements

Unpaid taxes

Deed in Lieu of Probate

If all heirs and devisees, if any, are competent adults willing to convey, title company will consider insuring purchaser without probate

Deed can recite grantees as “a, b and c, being the sole heirs at law and devisees of d, who died ______, ______,

CTIC requirements listed at www.ntiweb.com, sample forms as exhibit in probate booklet

Get forms from title officer

Affidavit of heirship

Death certificate

Copy of will (if decedent died testate)

State and Federal tax releases, if applicable

Notarized Statement of Information re final expenses paid and no claims

Personal Undertaking as to claims against the estate of the deceased

Risk premium

See exhibits re Statement of Information and Personal Undertaking

4/19/2017

4

Small Estates Affidavit

755 ILCS 5/25-1 et seq.

Applies to transfer of personal property where total value of personal

property in estate is less than $100,000

Purpose is to allow a holder of personal property to transfer assets to

disclosed heirs or devisees without liability to third parties like

undisclosed heirs or creditors for that distribution

Affiant obligated to pay disclosed unpaid debts and valid claims prior to

distribution to heirs or devisees

Affiant indemnifies all relying on affidavit up to amount lost due to acts

of affiant plus attorneys fees

Surviving Joint Tenant

765 ILCS 1005/1 et seq.

Four unities

Time – created at the same time

Title – acquired by same conveyance

Interest – equal shares

Possession – all have an undivided right to possession

Title passes to the surviving joint tenant(s) on death

Judgement solely against deceased joint tenant ceases to be lien on land

Exceptions of tax liens and liens in favor of governmental bodies (Public Aid Code)

Deceased joint tenancy affidavit – See exhibit

Certified copy of death certificate

Certified copy of will, if any

Information re no state or federal estate tax due

4/19/2017

5

Tenancy by the Entirety 735 ILCS 5/12-112; 750 ILCS 65/22; 765 ILCS 1005/1c

Requires marital residence owned as tenants by the entirety

If valid homestead but later different homestead, title is in joint tenancy unless

If divorce where order silent as to estate, tenancy in common

If Tenancy by Entirety deed where property not homestead, unknown estate

New judgement against one not enforceable against residence as long as parties stay alive,

married to each other and both live in the residence

Statute unclear as to whether judgement should be paid at sale of marital residence

Judgement prior to purchase can be insured as subordinate to purchase money mortgage but

raised as exception on owner’s policy

Judgement not enforceable against owner until tenancy broken

Judgement enforceable against mortgage if not purchase money mortgage

On death of one spouse, treat like joint tenancy property

Title in Trust

Illinois Trusts and Trustees Act 760 ILCS 5/

Powers and authorities of trust per Sec 4.1 et seq.

Certification of trust to third parties per Sec 8.5

Revocable Living Trust

Deed in trust should have full power and authority, third parties protected language. See exhibit.

Trustee can certify validity of trust per

Trustee or successor trustee can act for benefit of settlor during settlor’s life if properly drafted incompetency provisions

Pass beneficial interest or trustee conveys on settlor’s death without probate

Where settlor is trustee and beneficiary of trust, trust assets may be subject to claims of creditors upon settlor’s death per Rush University Medical Center v. Sessions, 2012 IL 112906

Illinois land trust

Separates beneficial interest from power of direction

Trustee merely holds title, acts at direction of designated party

Beneficial interest can be held as tenants by the entirety

Contingent on death beneficiary can disclaim per 755 ILCS 5/2-7

4/19/2017

6

Transfer on Death Instrument (TODI) 755 ILCS 27/1 et seq.

Transfers title to defined property on death of the individual executing Transfer on Death Instrument (TODI)

Revocable per Sec 45

Transferor can still convey, sell or mortgage TODI property per Sec 60

Applies to residential real estate only, per Sec 5 being

1 to 4 units,

a condo or

agricultural land of 40 acres or less with a single family residence

Sec 40 and 45 requirements for valid TODI

essential elements and formalities of deed

Be executed by owner and two witnesses and all attested by notary

If beneficiary is witness, legacy to beneficiary in excess of intestacy share is void unless two other

witnesses

State the transfer is to take place at transferor’s death

Be recorded prior to transferor’s death

Transfer on Death Instrument (contd.)

Transfer effective on death of transferor

Contestable within two years of death of transferor or 6 months from issuance of letters of office

Purchaser or mortgagee prior to lis pendens of contest takes free of contest

Subject to terms of TODI

Subject to liens and encumbrances of record at time of death

Subject to claims of creditors of transferor per Rush Medical case?

Beneficiary may disclaim

If predeceased beneficiary,

TODI instrument can contain alternate contingent beneficiaries

If predeceased beneficiary was descendant of transferor, to beneficiary’s descendants per stirpies

If to a class, to the remaining members of the class

To the transferor’s estate if none of above

4/19/2017

7

Transfer on Death Instrument –

Notice of Death Affidavit

Notice of death affidavit to confirm title per Section 75 to include

(1) the names and addresses of all beneficiaries,

(2) the legal description of the land,

(3) the street address and PIN for the land,

(4) the date and recording number of the TODI,

(5) the name of the deceased owner,

(6) the date and place of death, and

(7) the name and address to which future tax bills should be sent.

The notice of death affidavit should be acknowledged before a notary public.

The recording of a notice of death affidavit, however, is not a condition to the transfer of title under the TODI.

Income Tax Basis of Transferred Assets

Income tax basis is beyond the scope of this presentation

Presenters are not qualified to give tax information

This is a warning to refer client to qualified tax counsel or

accountant

Review IRS Publication 551: Basis of Assets at www.irs.gov

If it is not clear, get the Fair Market Value of the asset on transfer and

the transferor’s basis at transfer and send them to their tax accountant

Basis on transfer can be subsequently be adjusted by things like

recognized gains, capital improvements and depreciation

4/19/2017

8

Basis of Transfer from Spouse

Basis of asset transferred from a Spouse is

the basis of the transferring Spouse

plus any gain recognized for transfer into

trust where liabilities assumed are

greater than basis of the property

transferred

Basis of Gift

Gift – Per Pub. 551, basis at transfer can be either Fair Market Value (FMV) or donor’s

basis

If the FMV is equal to or greater than the donor’s basis at transfer, then the basis is

the donor’s basis

If the FMV is less than donor’s basis at transfer and

you have a capital gain on sale, your basis is donor’s adjusted basis plus or

minus your basis adjustments

You have a capital loss on sale, your basis is FMV at the time of transfer plus or

minus your basis adjustments

No gain or loss if you use above to figure a gain and get a loss or to figure a loss

and get a gain

4/19/2017

9

Basis of Inherited Property

Per Pub. 551, “Generally”

FMV on date of death

FMV at time of alternate valuation if elected by estate

Valuation for special use valuation if farm or closely held business if estate elects those valuation methods

Decedent’s adjusted basis if property donated for conservation easement

Basis of Surviving Joint Tenant

If sole survivor did not contribute to purchase price and had no income

from property, then FMV on date of death of deceased joint tenant

If sole survivor did not contribute to purchase price and had income

from property, then FMV on date of death less survivor’s share of prior

allowed depreciation

If sole survivor contributed to purchase price and shared income, then

survivor’s purchase price plus deceased percentage times FMV on date

of death less survivor’s share of depreciation

Remember: This is not tax advice. It is a warning to refer your client to

qualified tax counsel or accountants.

4/19/2017

10

Statutory Attacks on Transfers

US Bankruptcy Code Sections 547, 548 & 544

Uniform Fraudulent Transfer Act 740 ILCS 160/1

Probate Act

755 ILCS 5/2-6 Person who “intentionally and unjustifiably

causes the death of another”

Treat as having predeceased person killed

If joint tenancy interest, treat as if joint tenancy

severed

Financial Exploitation

AARP, in an October 2016 bulletin, noted “…there are

40 million family caregivers in the U.S. who are

providing $470 billion in uncompensated care every

year.”

That figure does not include the amounts paid to

compensated caregivers

A 2009 study in which the National Committee for the

Prevention of Elder Abuse participated in estimated

an annual $2.6 billion in financial elder abuse per

year

4/19/2017

11

Statutory Penalties for Financial

Exploitation of Elderly or Disabled 755 ILCS 5/2-6.2 Financial exploitation, abuse or neglect

Misappropriation includes undue influence, breach of a fiduciary relationship, fraud,

deception, extortion and conversion

Convicted under Section 16-1.3 or 17-56 of Criminal Code of 2012 or found by a

preponderance of evidence to be civilly liable

Treat guilty party as having predeceased decedent, but sever joint tenancy estate

If deceased knew of conviction or finding of civil liability and thereafter ratified transfer,

convicted party can keep transfer

Holder of property not liable for transfer prior to conviction or holding or transfer thereafter

if no knowledge of conviction or holding

Court may allow convicted to get a reduction in benefits instead of no benefit

Statutory Penalties for Financial

Exploitation of Elderly or Disabled 755 ILCS 5/2-6.6 Person convicted of violation of Section 12-19, 12-21,

16-1.3 or 17-56 or 23-4.4a of Criminal Code of 2012 or person found by

preponderance of evidence to be civilly liable for financial exploitation

Treat convicted as having predeceased deceased or sever joint tenancy

If deceased knew of conviction or finding of civil liability and thereafter

ratified transfer, convicted party can keep transfer

Holder of property not liable for transfer prior to written notice of

conviction or holding or transfer unless knowledge of conviction or

holding

Court may allow a reduction in benefits instead of no benefit

4/19/2017

12

Presumptively Void Transfers to Caregivers

755 ILCS 5/4.1 et seq. Rebuttable presumption that TRANSFER

INSTRUMENT executed after 1/1/15 is void if the transferee is a non-

family member caregiver and the fair market value of the transfer

exceeds $20,000

Action against transfer instrument must be brought within 2 years of

death

Caregiver is person or their spouse, cohabitant, child or employee who

has “assumed responsibility for all or a portion of the care of another

person who needs assistance with activities of daily living.”

Family member caregiver is spouse, child, grandchild, sibling, aunt,

uncle, niece, nephew, first cousin, or parent of person receiving care

but does not appear to include their spouses

Presumptively Void Transfers to

Caregivers (contd)

Caregiver pays all attorneys fees if he contests presumption and loses

Presumption rebutted by

1) preponderance of evidence that transferee’s share under

transfer instrument is not greater than the share that transferee

was entitled to under the transferor’s transfer instrument in effect

prior to the transferee becoming a caregiver or

2) by clear and convincing evidence that the transfer was not the

product of fraud, duress or undue influence

4/19/2017

13

Presumptively Void Transfers to

Caregivers (contd)

Assume a new trust written after 1/1/15 leaves $50,000 to daughter-

in-law who was taking father-in-law to doctors, preparing his meals

and making sure father-in-law took his medications and $5 million to

State University.

Is daughter-in-law a non-family member caregiver?

The entire trust agreement is presumed void if daughter-in-law is

a caregiver. Can university attempt to rebut presumption if

daughter-in-law does not try to? (Her husband probably gets all or

part of the $5 million if she does not.)

Is drafter of trust liable to university for frustration of settlor’s

intention?

Seniors and Foreclosure

4/19/2017

14

Reverse Mortgages

Seniors can wind up in foreclosure on

Reverse Mortgages in the following

situations:

1. Non-payment of taxes

2. Non-payment of insurance

3. Failure to occupy the property

4. Death of obligated party

5. Death of second to die of couple

Solutions to Foreclosure of Reverse

Mortgage

Pay outstanding obligations (sometimes, the homeowner

just forgets to make payment or misses an installment)

(Investigate a chapter 13 as a possibility if catching up

debt is necessary)

Sell the property – can obtain any equity in the property

for the homeowner.

The Estate or Heirs of the homeowner have the right to

purchase the property for 95% of the appraised value.

Secretary of Housing and Urban Development Rules,

Chapter 13,4330.1 Rev-5, 279.94(A)(!).

4/19/2017

15

Appointment of Guardian

If the Homeowner is known to be incompetent, the

Foreclosure Court can be asked to appoint a Guardian to

watch out for the interests of the Homeowner.

Timing is critical, since the Guardian would need to be

appointed before the sheriff’s sale. That presumes that

someone is aware of the fact that a foreclosure is pending

and a Guardian needs to be appointed.

Appointment of a Guardian can assure that family

members can protect the property and equity in the

property.

Appointing a Special Representative for

a Deceased Homeowner

Circuit court lacks subject matter jurisdiction when a lawsuit is filed against a

deceased person because such a suit is a nullity. To avoid this rule and confer

jurisdiction, a plaintiff may substitute the deceased party’s personal

representative. 735 ILCS5/2-1008. See ABN Amro v. McGahan, 237 Ill 2d 526

(2010)

Foreclosure cases are deemed quasi-in rem proceedings, so, even though the

mortgagee is foreclosing against property, and may be the only remedy they

may seek, the mortgagor is a necessary party.

The appointment of a Special Representative may help in identifying heirs to

provide defenses, but may not be under an obligation to do so.

4/19/2017

16

Probate Court Can Force Short Sale of

Property

If the sale real property of descendant is

mortgaged for more than its value and selling is a

prerequisite to closing the estate, probate courts

can force the lender to accept a short sale. 755

ILCS 5/20-6(b) See IL App (2d) 130945

CIDCAGO TITLE INSURANCE COMPANY DECEASED JOINT TENANCY AFFIDAVIT

STATE OF ILLINOIS COUNTY OF

ss. ORDER NO.:

being duly sworn states that _______ resides at __________________ _

in the City

That ____ was acquainted - .... ______________ deceased who, at the

time of death, was one of the owners of the land in _____________ County,

Illinois, described as:

That the deceased died -::-:--:----:--:--:-:-----copy of death certificate of the deceased attached hereto.

That the deceased died:

Leaving no Last Will & Testament.

, as evidenced by a certified

Leaving a Last Will & Testament a copy of which is attached hereto. The original of the W!proven will should be filed with the Clerk of Probate Division of the Circuit Court of __________ COW!ty, Illinois.

Leaving a Last Will & Testament which was filed in the Unproven Will Box of the Probate Division of the Circuit Court of ___________ CoW!ty, Illinois about---------·

That the total value of the estate of the deceased, including both real and personal property owned by the deceased either individually or in joint tenancy at the time of the death of the deceased, does not exceed the sum of dollars.

Affiant makes this affidavit for the purpose of inducing Cbicago Title Insurance Company to issue its Title Insurance Policy, describing the above mentioned property.

Subscribed and sworn to before me by the said

this ___ day ______ ,A.D. 20 __ _

DJTAf'f

Excerpts From IRS Publication 551: Basis of Assets

Property Transferred From a Spouse

The basis of property transferred to you or transferred in trust for your benefit by your spouse (or former spouse if the transfer is incident to divorce) is the same as your spouse's adjusted basis. However, adjust your basis for any gain recognized by your spouse or former spouse on property transferred in trust. This rule applies only to a transfer of property in trust in which the liabilities assumed, plus the liabilities to which the property is subject, are more than the adjusted basis of the property transferred.

At the time of the transfer, the transferor must give you the records necessary to determine the adjusted basis and holding period of the property as of the date of transfer. For more information, see Pub. 504, Divorced or Separated Individuals.

Property Received as a Gift

To figure the basis of property you receive as a gift, you must know its adjusted basis (defined earlier) to the donor just before it was given to you, its Fair Market Value ("FMV") at the time it was given to you, and any gift tax paid on it.

FMV Less Than Donor's Adjusted Basis

If the FMVofthe property at the time of the gift is less than the donor's adjusted basis, your basis depends on whether you have a gain or a loss when you dispose of the property. Your basis for figuring gain is the same as the donor's adjusted basis plus or minus any required adjustment to basis while you held the property. Your basis for figuring loss is its FMV when you received the gift plus or minus any required adjustment to basis while you held the property (see Adjusted Basis earlier). If you use the donor's adjusted basis for figuring a gain and get a loss, and then use the FMV for figuring a loss and have a gain, you have neither gain nor loss on the sale or disposition of the property. Example. You received an acre of land as a gift. At the time of the gift, the land had an FMV of $8,000. The donor's adjusted basis was $10,000. After you received the land, no events occurred to increase or decrease your basis. If you sell the land for $12,000, you will have a $2,000 gain because you must use the donor's adjusted basis ($10,000) at the time of the gift as your basis to figure gain. If you sell the land for $7,000, you will have a $1,000 loss because you must use the FMV ($8,000) at the time of the gift as your basis to figure a loss. If the sales price is between $8,000 and $10,000, you have neither gain nor loss. For instance, if the sales price was $9,000 and you tried to figure a gain using the donor's adjusted basis ($10,000), you would get a $1,000 loss. If you then tried to figure a loss using the FMV ($8,000), you would get a $1,000 gain. Business property. If you hold the gift as business property, your basis for figuring any depreciation, depletion, or amortization deduction is the same as the donor's adjusted basis plus or minus any required adjustments to basis while you hold the property.

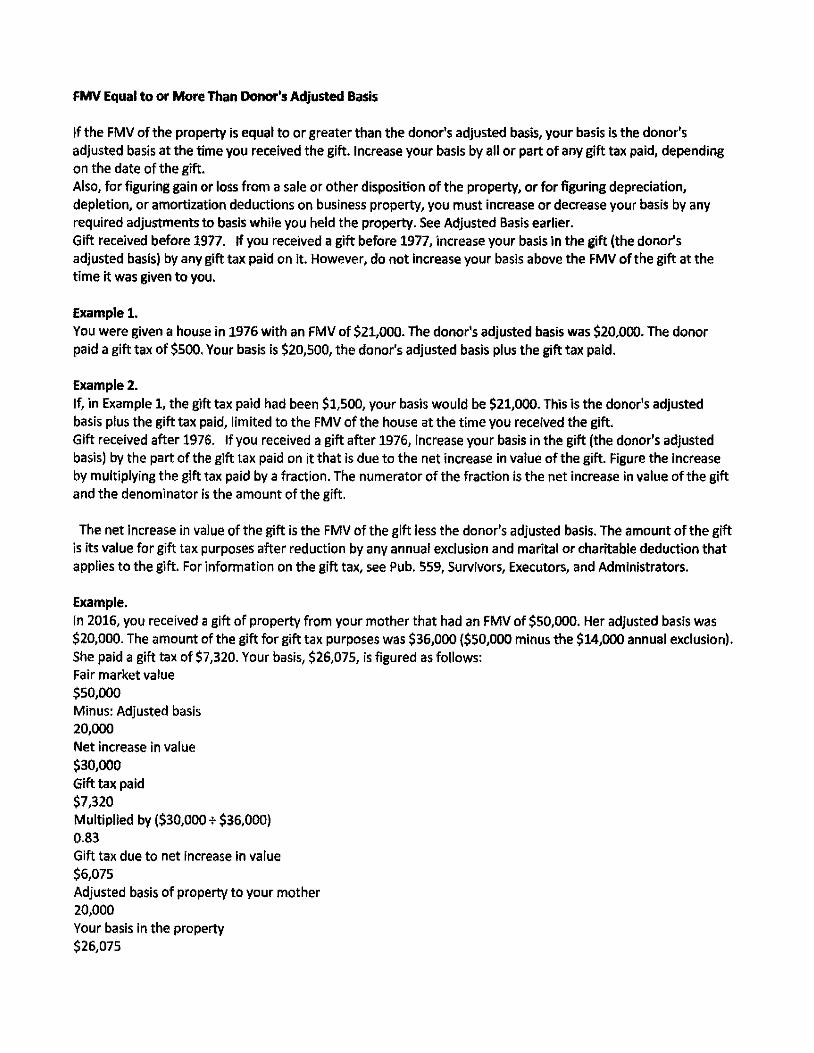

FMV Equal to or More Than Donor's Adjusted Basis

If the FMV of the property is equal to or greater than the donor's adjusted basis, your basis is the donor's adjusted basis at the time you received the gift. Increase your basis by all or part of any gift tax paid, depending on the date of the gift. Also, for figuring gain or loss from a sale or other disposition of the property, or for figuring depreciation, depletion, or amortization deductions on business property, you must increase or decrease your basis by any required adjustments to basis while you held the property. See Adjusted Basis earlier. Gift received before 1977. If you received a gift before 1977, increase your basis in the gift (the donor's adjusted basis) by any gift tax paid on it. However, do not increase your basis above the FMV of the gift at the time it was given to you.

Example 1. You were given a house in 1976 with an FMV of $21,000. The donor's adjusted basis was $20,000. The donor paid a gift tax of $500. Your basis is $20,500, the donor's adjusted basis plus the gift tax paid.

Example2. If, in Example 1, the gift tax paid had been $1,500, your basis would be $21,000. This is the donor's adjusted basis plus the gift tax paid, limited to the FMV of the house at the time you received the gift. Gift received after 1976. If you received a gift after 1976, increase your basis in the gift (the donor's adjusted basis) by the part of the gift tax paid on it that is due to the net increase in value of the gift. Figure the increase by multiplying the gift tax paid by a fraction. The numerator of the fraction is the net increase in value of the gift and the denominator is the amount of the gift.

The net increase in value of the gift is the FMV of the gift less the donor's adjusted basis. The amount of the gift is its value for gift tax purposes after reduction by any annual exclusion and marital or charitable deduction that applies to the gift. For information on the gift tax, see Pub. 559, Survivors, Executors, and Administrators.

Example. In 2016, you received a gift of property from your mother that had an FMV of $50,000. Her adjusted basis was $20,000. The amount of the gift for gift tax purposes was $36,000 ($50,000 minus the $14,000 annual exclusion). She paid a gift tax of $7,320. Your basis, $26,075, is figured as follows: Fair market value $50,000 Minus: Adjusted basis 20,000 Net increase in value $30,000 Gift tax paid $7,320 Multiplied by ($30,000 + $36,000) 0.83 Gift tax due to net increase in value $6,075 Adjusted basis of property to your mother 20,000 Your basis in the property $26,075

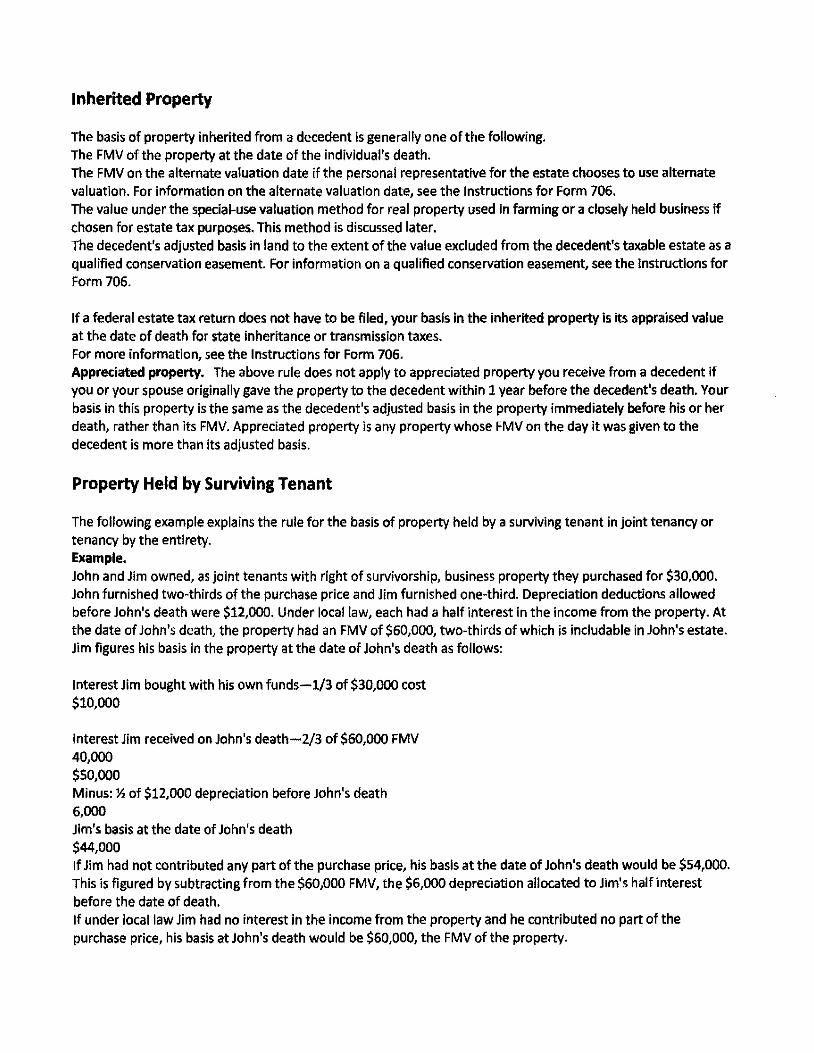

Inherited Property

The basis of property inherited from a decedent is generally one of the following. The FMV ofthe property at the date of the individual's death. The FMV on the alternate valuation date if the personal representative for the estate chooses to use alternate valuation. For information on the alternate valuation date, see the Instructions for Form 706. The value under the special-use valuation method for real property used in farming or a closely held business if chosen for estate tax purposes. This method is discussed later. The decedent's adjusted basis in land to the extent of the value excluded from the decedent's taxable estate as a qualified conservation easement. For information on a qualified conservation easement, see the Instructions for Form 706.

If a federal estate tax return does not have to be filed, your basis in the inherited property is its appraised value at the date of death for state inheritance or transmission taxes. For more information, see the Instructions for Form 706. Appreciated property. The above rule does not apply to appreciated property you receive from a decedent if you or your spouse originally gave the property to the decedent within 1 year before the decedent's death. Your basis in this property is the same as the decedent's adjusted basis in the property immediately before his or her death, rather than its FMV. Appreciated property is any property whose FMV on the day it was given to the decedent is more than its adjusted basis.

Property Held by Surviving Tenant

The following example explains the rule for the basis of property held by a surviving tenant in joint tenancy or tenancy by the entirety. Example. John and Jim owned, as joint tenants with right of survivorship, business property they purchased for $30,000. John furnished two-thirds of the purchase price and Jim furnished one-third. Depreciation deductions allowed before John's death were $12,000. Under local law, each had a half interest in the income from the property. At the date of John's death, the property had an FMV of $60,000, two-thirds of which is includable in John's estate. Jim figures his basis in the property at the date of John's death as follows:

lnterestJim bought with his own funds-1/3 of$30,000 cost $10,000

Interest Jim received on John's death-2/3 of $60,000 FMV 40,000 $50,000 Minus: Y, of $12,000 depreciation before John's death 6,000 Jim's basis at the date of John's death $44,000 If Jim had not contributed any part of the purchase price, his basis at the date of John's death would be $54,000. This is figured by subtracting from the $60,000 FMV, the $6,000 depreciation allocated to Jim's half interest before the date of death. If under local law Jim had no interest in the income from the property and he contributed no part of the purchase price, his basis at John's death would be $60,000, the FMV of the property.

Qualified Joint Interest

Include one-half of the value of a qualified joint interest in the decedent's gross estate. It does not matter how much each spouse contributed to the purchase price. Also, it does not matter which spouse dies first. A qualified joint interest is any interest in property held by married individuals as either of the following. Tenants by the entirety, or Joint tenants with right of survivorship if the married couple are the only joint tenants.

Basis. As the surviving spouse, your basis in property you owned with your spouse as a qualified joint interest is the cost of your half of the property with certain adjustments. Decrease the cost by any deductions allowed to you for depreciation and depletion. Increase the reduced cost by your basis in the half you inherited.

Farm or Closely Held Business

Under certain conditions, when a person dies the executor or personal representative of that person's estate can choose to value the qualified real property on other than its FMV. If so, the executor or personal representative values the qualified real property based on its use as a farm or its use in a closely held business. If the executor or personal representative chooses this method of valuation for estate tax purposes, that value is the basis of the property for the heirs. Qualified heirs should be able to get the necessary value from the executor or personal representative of the estate. Special-use valuation. If you are a qualified heir who received special-use valuation property, your basis in the property is the estate's or trust's basis in that property immediately before the distribution. Increase your basis by any gain recognized by the estate or trust because of post-death appreciation. Post-death appreciation is the property's FMVon the date of distribution minus the property's FMV either on the date of the individual's death or the alternate valuation date. Figure all FMVs without regard to the special-use valuation.

You can elect to increase your basis in special-use valuation property if it becomes subject to the additional estate tax. This tax is assessed if, within 10 years after the death of the decedent, you transfer the property to a person who is not a member of your family or the property stops being used as a farm or in a closely held business.

To increase your basis in the property, you must make an irrevocable election and pay interest on the additional estate tax figured from the date 9 months after the decedent's death until the date of the payment of the additional estate tax. If you meet these requirements, increase your basis in the property to its FMV on the date of the decedent's death or the alternate valuation date. The increase In your basis is considered to have occurred immediately before the event that results in the additional estate tax.

You make the election by filing with Form 706-A a statement that does all of the following. Contains your name, address, and taxpayer identification number and those of the estate; Identifies the election as an election under section 1016(c) ofthe Internal Revenue Code; Specifies the property for which the election is made; and Provides any additional information required by the Instructions for Form 706-A.

For more information, see the instructions for Form 706 and the Instructions for Form 706-A.

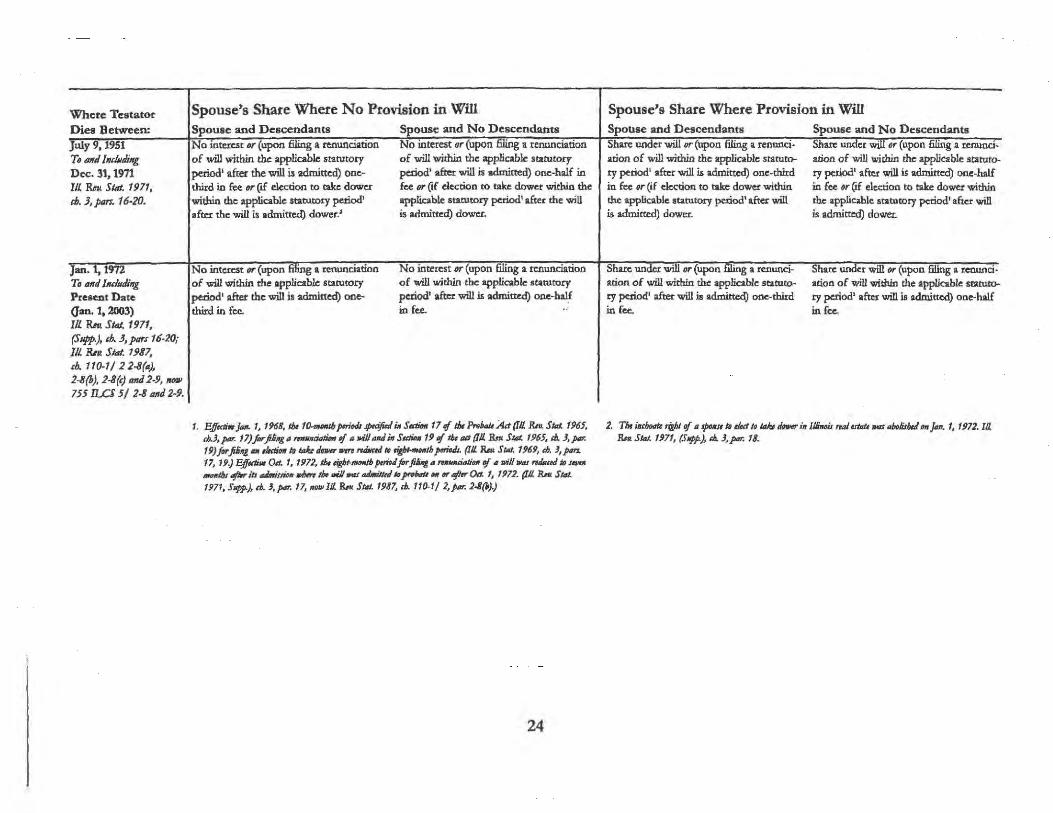

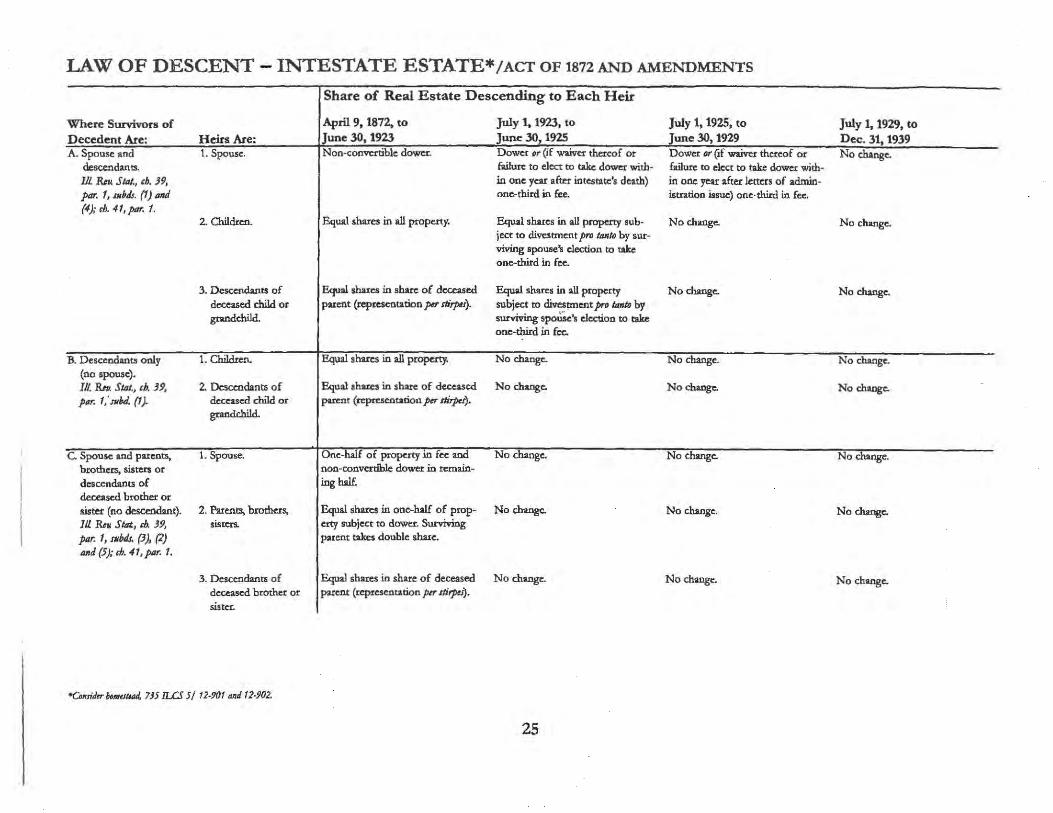

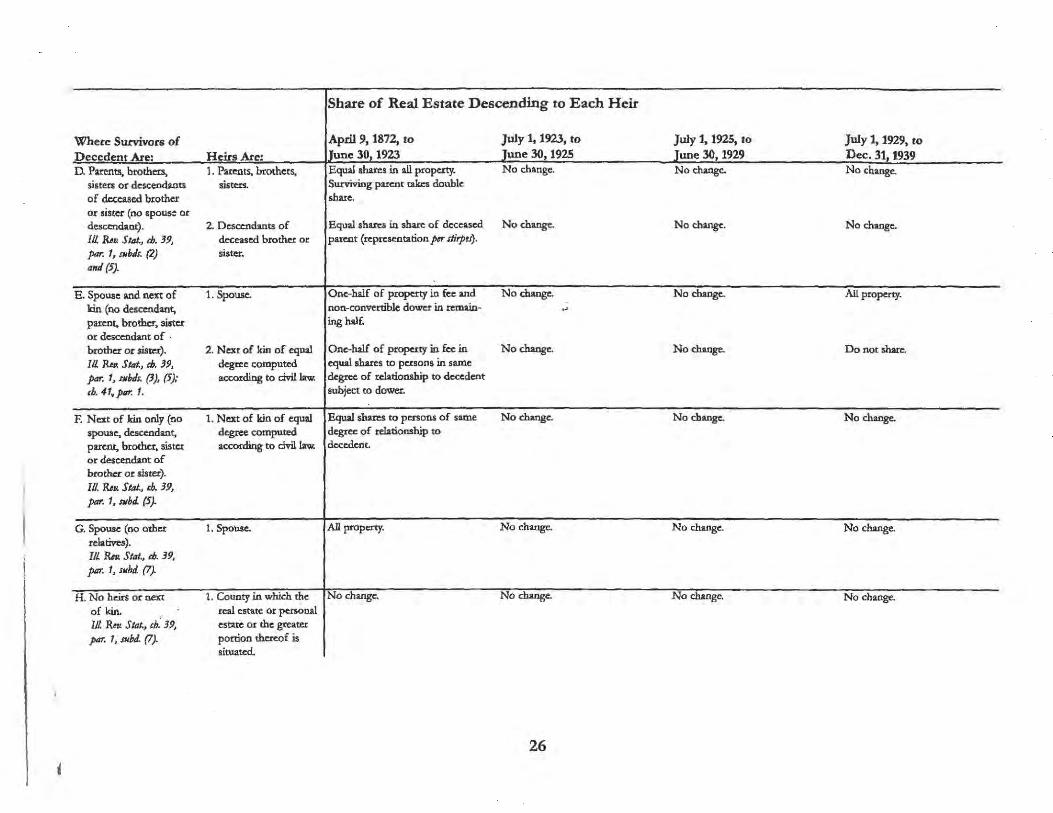

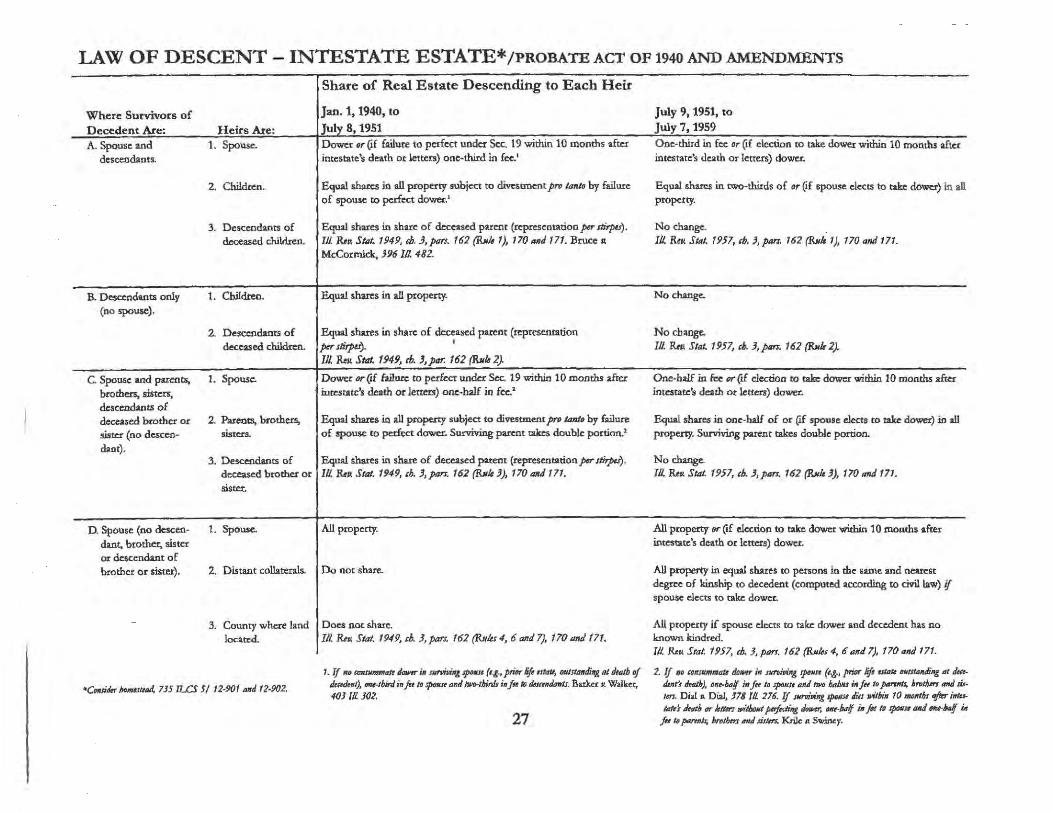

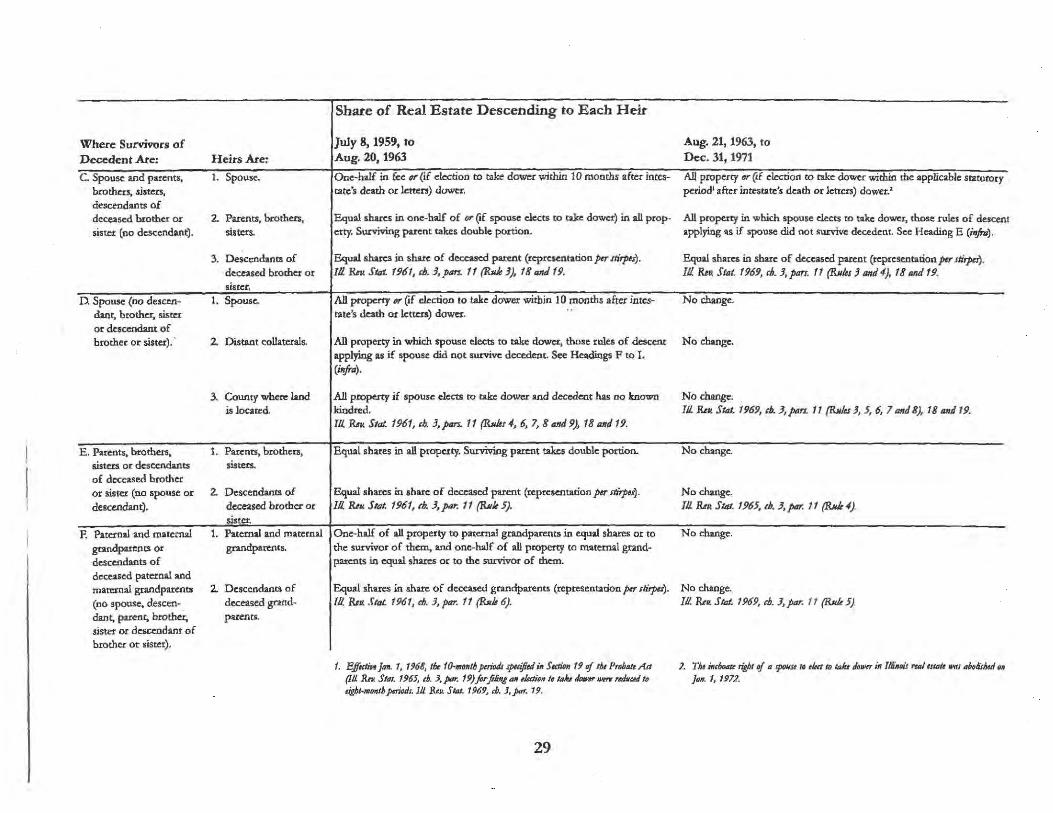

RIGHTS OF HEIRS AND LEGATEES AND THEIR PURCHASERS IN ILLINOIS REAL

ESTATE With Chart on Intestate Descent

The appended chart is an update of the previously published and widely used chart “Rights of

Surviving Spouse and Law of Descent in Illinois” by John D. Lagorio, Jr. former Vice President of Chicago Title Insurance Company. Paul Peterson V.P. & Senior Underwriter Chicago Title Insurance Company Fidelity National Title Insurance Company Commonwealth Title Insurance Company

INTRODUCTION The lawyer dealing with real estate previously owned by a deceased sole owner or tenant in common must often resolve the conflicting rights of heirs, legatees,1 claimants, and purchasers and decide whether to institute time consuming and expensive probate proceedings. How a lawyer proceeds will vary from case to case depending on whether the heirs, the legatees, or a third party purchaser will be the ultimate title holder, whether there are unpaid claims against the estate, and whether a foreign decedent is involved. This publication is intended to assist the lawyer in understanding these conflicting rights and to aid in deciding whether probate proceedings are desirable in a particular case. It will discuss how title insurance can be used to insure against risks when probate proceedings are not contemplated. Prohibited, Decreased or Void Transfers Complicating this process are the provisions of the Probate Act which may affect the passage of title by any vehicle, whether through intestacy, will, trust, joint tenancy, tenancy by the entirety or transfer on death. Sanctions are imposed where an heir murdered an ancestor2, where a party taking was convicted of financial exploitation, abuse or neglect of an elderly or disabled person3, where a parent neglected a deceased child4, or where a person is convicted or found civilly liable for certain abuses against the deceased elderly or disabled person5. Further complicating passage of title is the new presumption that the entire transfer instrument and not just the specific transfer is void if it includes a transfer on death to a non-family caregiver in excess of $20,0006. Deceased Joint Tenants / Tenants by the Entirety Passage of title to real estate formerly owned by a deceased joint tenant7 or tenant by the entirety8 ordinarily provides few problems and should not require probate proceedings. As a general rule, on the death of a joint tenant the interest of the deceased joint tenant passes by operation of the joint tenancy to the surviving joint tenants. The title is subject to the lien for any state estate tax or federal estate tax due against the estate of the deceased joint tenant. Generally, judgments solely against the interest of the deceased joint tenant perfected after the creation of the joint tenancy but not levied upon do not affect the interest of the surviving joint tenant.9 Once the attorney has ascertained that the decedent held title in joint tenancy and the joint

1 Legatee, as defined in 755 ILCS 5/1 – 2.12, includes devisee. 2 755 ILCS 5/2-6 3 755 ILCS 5/2-6.2 4 755 ILCS 5/2-6.5 5 755 ILCS 5/2-6.6 6 755 ILCS 5/4a-5 et seq. 7 765 ILCS 1005/1 8 765 ILCS 1005/1c 9 See Gayton v. Kovanda, 368 Ill.App.3d 363, 857 N.E.2d 929 (1st. Dist. 2006). See, however, 305 ILCS 5/5-13.5 and 305 ILCS 5/3-10 providing for the survival against the share of the deceased joint tenant of the lien for Medicaid payments and for payments for Aid to the Aged, Blind or Disabled provided for the benefit of the deceased joint tenant and United States v. Craft, 535 US 274 (S.Ct. 2002) holding a federal revenue lien against the deceased tenant by the entirety remained against half of the homestead of the surviving tenant by the entirety

tenancy was not severed,10 he should obtain a certified death certificate, a copy of the last will and testament, if any, a state estate tax release and a federal estate tax release11 or a certification that no taxes were due. Considerations for the deceased joint tenant should also relate to the deceased tenant by the entirety. Additionally, an ordinary judgment creditor whose lien was perfected after the creation of the estate cannot enforce its lien solely against the interest of a tenant by the entirety until the estate is terminated except if the estate was created for the sole intent of avoiding payment of existing debts beyond the transferor’s ability to pay those debts as they become due.12 The death certificate must be examined for the date of death, the identity of the decedent, and the cause of death. The cause of death must be reviewed since a party who intentionally and unjustifiably causes the death shall not receive any property, benefit or interest by reason of the death.13 This test appears to be a codification of existing case law which applied to lesser crimes than murder.14 A person convicted of certain crimes against the elderly or disabled may not receive any benefit from the joint tenancy or tenancy by the entirety but would retain what interest in the property they had prior to the crime.15 The will of the deceased joint tenant or tenant by the entirety should be examined to ascertain that the case law dealing with joint and mutual wills or the doctrine of election is not applicable. A joint and mutual will, executed by both the deceased joint tenant and the surviving joint tenant, can create a contract to devise the property to the devisees set forth in the joint and mutual will.16 While title still passes through the joint tenancy to the surviving joint tenant, the title is subject to the survivor’s contract which may be enforced by the devisees against the survivor, his estate, or in some cases, his purchaser. The doctrine of election, on the other hand, arises where the deceased joint tenant’s will devises the specifically described joint tenancy property to someone other than the surviving joint tenant and devises other property to the surviving joint tenant. The surviving joint tenant must decide whether to take as a surviving joint tenant or as a legatee under the will.17 The final items to be considered, the lien for state estate tax and federal estate tax, will be discussed at length in a later section. 10 Lawwe v. Byrne, 252 Ill. 194; Szymczak v. Sszymczak, 306 Ill. 542; Duncan v. Suby, 378 Ill. 194. 11 A bona fide purchaser for an adequate and full consideration from a surviving joint tenant has the protections afforded by 26 U.S.C. 6324 (a)(2) and Revenue Ruling 56-144, 24 U.S.L.W. 2506 with respect to the lien for federal estate taxes, but some title insurers are hesitant to rely on this revenue ruling, especially where a large estate tax is due. 12 735 ILCS 5/12-112 13 755 ILCS 5/2 – 6. 14 State Farm Life Insurance Co. v. Davidson, 144 Ill. App. 3d 1049. 15 755 ILCS 5/2-6.6 16 Tontz v. Heath, 20 Ill.2d 286. 17 Carper v. Crowl, 149 Ill. 465. See, however, Williamson v. Williamson, 657 N.E.2d 651, 257 Ill.App.3d 999 (1st Dist. 1995) holding the doctrine of election inapplicable to joint tenancy property unless the will shows a clear intent to put the beneficiary to the election.

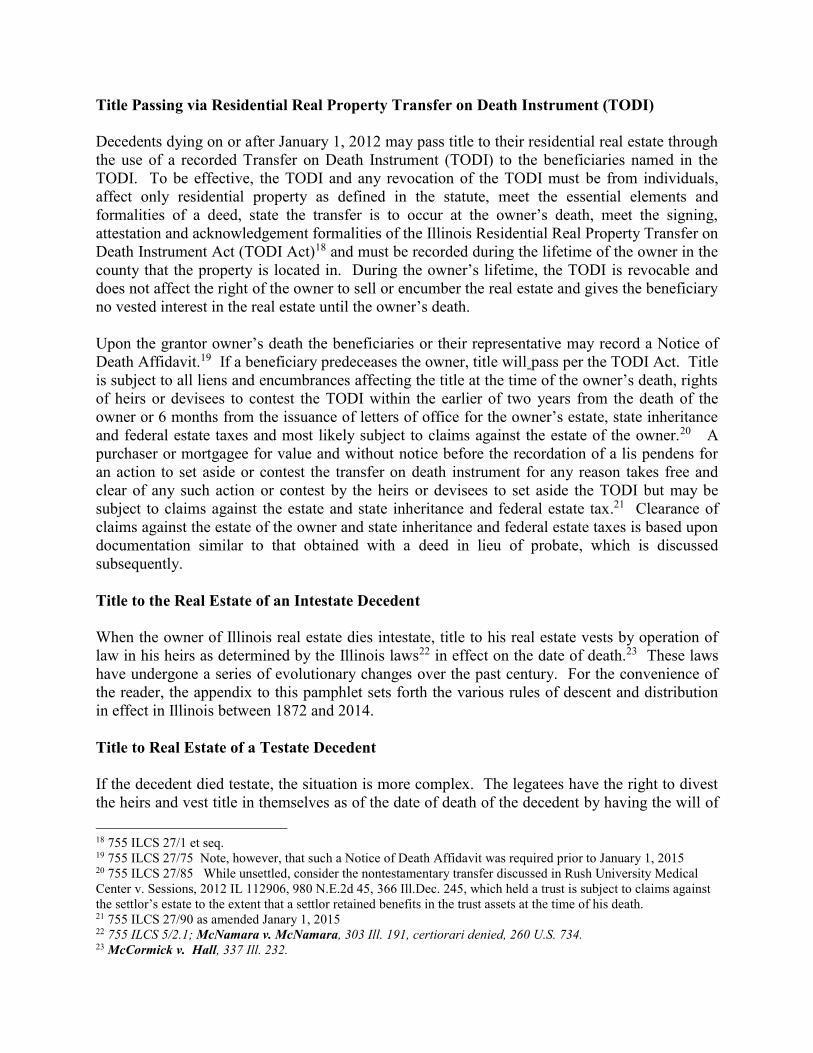

Title Passing via Residential Real Property Transfer on Death Instrument (TODI) Decedents dying on or after January 1, 2012 may pass title to their residential real estate through the use of a recorded Transfer on Death Instrument (TODI) to the beneficiaries named in the TODI. To be effective, the TODI and any revocation of the TODI must be from individuals, affect only residential property as defined in the statute, meet the essential elements and formalities of a deed, state the transfer is to occur at the owner’s death, meet the signing, attestation and acknowledgement formalities of the Illinois Residential Real Property Transfer on Death Instrument Act (TODI Act)18 and must be recorded during the lifetime of the owner in the county that the property is located in. During the owner’s lifetime, the TODI is revocable and does not affect the right of the owner to sell or encumber the real estate and gives the beneficiary no vested interest in the real estate until the owner’s death. Upon the grantor owner’s death the beneficiaries or their representative may record a Notice of Death Affidavit.19 If a beneficiary predeceases the owner, title will pass per the TODI Act. Title is subject to all liens and encumbrances affecting the title at the time of the owner’s death, rights of heirs or devisees to contest the TODI within the earlier of two years from the death of the owner or 6 months from the issuance of letters of office for the owner’s estate, state inheritance and federal estate taxes and most likely subject to claims against the estate of the owner.20 A purchaser or mortgagee for value and without notice before the recordation of a lis pendens for an action to set aside or contest the transfer on death instrument for any reason takes free and clear of any such action or contest by the heirs or devisees to set aside the TODI but may be subject to claims against the estate and state inheritance and federal estate tax.21 Clearance of claims against the estate of the owner and state inheritance and federal estate taxes is based upon documentation similar to that obtained with a deed in lieu of probate, which is discussed subsequently. Title to the Real Estate of an Intestate Decedent When the owner of Illinois real estate dies intestate, title to his real estate vests by operation of law in his heirs as determined by the Illinois laws22 in effect on the date of death.23 These laws have undergone a series of evolutionary changes over the past century. For the convenience of the reader, the appendix to this pamphlet sets forth the various rules of descent and distribution in effect in Illinois between 1872 and 2014. Title to Real Estate of a Testate Decedent If the decedent died testate, the situation is more complex. The legatees have the right to divest the heirs and vest title in themselves as of the date of death of the decedent by having the will of 18 755 ILCS 27/1 et seq. 19 755 ILCS 27/75 Note, however, that such a Notice of Death Affidavit was required prior to January 1, 2015 20 755 ILCS 27/85 While unsettled, consider the nontestamentary transfer discussed in Rush University Medical Center v. Sessions, 2012 IL 112906, 980 N.E.2d 45, 366 Ill.Dec. 245, which held a trust is subject to claims against the settlor’s estate to the extent that a settlor retained benefits in the trust assets at the time of his death. 21 755 ILCS 27/90 as amended Janary 1, 2015 22 755 ILCS 5/2.1; McNamara v. McNamara, 303 Ill. 191, certiorari denied, 260 U.S. 734. 23 McCormick v. Hall, 337 Ill. 232.

the decedent admitted to probate in a court of competent jurisdiction in Illinois.24 An unadmitted will does not vest title to Illinois real estate in the legatees. Even a will which has been admitted to probate in a foreign state is insufficient to vest title to Illinois real estate.25 Probate of the will gives the heirs an opportunity to examine the will and, if they desire, to contest the validity of the will in court or submit a different will for admission to probate. The order admitting the will to probate has the effect of a conveyance from the decedent to the legatees. It divests the heirs and renders conveyances by the heirs, or liens affecting the real estate by reason of title in the heirs, ineffective against the decedent’s land.26 There is no statutory time limit for the filing of a petition to admit the will to probate. The will may need to be interpreted. The most innocuous clause in a will can lead to a will construction suit that may not be filed for years after the probate proceedings have closed. 27 Determining Heirship Problems may arise in determining heirship due to children born out of wedlock,28 a posthumous child,29 adopted heirs or parties inheriting from adopted decedents,30 persons intentionally and unjustifiably causing the death of the decedent,31 persons convicted of the financial exploitation, abuse or neglect of the decedent,32 parents neglecting a deceased child,33 parties convicted of certain offenses against the elderly or disabled,34 disclaimers,35 simultaneous deaths36 and missing or unknown heirs. Additionally, with the recognition of civil unions37 in Illinois in 2011, a party to a civil union has the same rights and responsibilities as a spouse, including the right of inheritance, the right to a surviving spouse’s award and the right to renounce a will, and the affidavit of heirship must affirmatively deal with civil unions. Same sex marriages are also authorized in Illinois.38 In those cases in which the heirship is uncertain or contested, a probate proceeding may he necessary to obtain an order declaring heirship.

24 755 ILCS5/4–13; Barnett v. Barnett, 284 Ill. 580. 25 755 ILCS 5/7-5, Sternberg v. St. Louis Union Trust Co., 394 Ill. 462; Plenderleith v. Edwards, 328 Ill. 431. 26 See, however, Eckland v. Jankowski, 407 Ill. 263, holding an innocent purchaser from the heirs, relying on a

probate proceedings adjudicating the deceased died intestate, was protected from the devisees claiming under a subsequently discovered will by his reliance on the public record.

27 A classic example of a will construction suit is O’Connell v. Gaffney, 23 Ill. 2d 611, wherein the Illinois Supreme Court reversed the Appellate Court and held that the share of a predeceased brother under the legacy “… to be paid in equal shares to my two brothers, James Gaffney and Edward Gaffney … lapsed as the clause did not create a class gift and was to be distributed to the parties taking under the residuary clause of the will. 28 755 ILCS 5/2–2, which defines those parents eligible to inherit and provides for an unpaid child support offset.

See Estate of Hicks, 174 Ill.2d 433 holding section 2(d), which then permitted only the maternal side to inherit from an intestate illegitimate without spouse or descendants, unconstitutional. The heirs of illegitimates have changed over time.

29 755 ILCS 5/2-3. 30 755 ILCS 5/2-4. The law as to adopted children has changed over time. 31 755 ILCS 5/2-6.2 and 2-6.6. 32 755 ILCS 5/2-6.2 33 755 ILCS 5/2-6.5 34 755 ILCS 5-2-6.6 35 755 ILCS 5/2-7. 36 755 ILCS 5/3-1 37 750 ILCS 75/1 et. seq 38 750 ILCS 80/1 et seq., effective 6/1/14, authorizing same sex marriages, may make civil unions rare

Avoidance of Probate in Vesting Title Where the Decedent Left a Will If the decedent dies testate, probate proceedings may be necessary to vest the legatees with title. Until there is an order admitting the will to probate, title remains in the heirs subject to the rights of the legatees to perfect their title by having the will admitted. This does not necessarily mean that the will must be admitted to probate in every instance. Often, the heirs and legatees are the same parties and take the same share of the decedent’s real estate under the laws of intestacy or the terms of the will. In such a case, probate proceedings will not change the title. Alternatively, if the heirs and legatees are different parties or take different shares, and the heirs are all competent adults, title can be confirmed in the legatees by conveyances of record from all the heirs. If all the heirs and legatees deed to a third party by warranty deed, the deeds should be effective to convey after acquired title in case the will is subsequently admitted to probate.39 Even in those cases where it is necessary to have the will admitted to probate in Illinois, full probate proceedings may be avoided by simply having the will admitted to probate without having a personal representative appointed40 or by the use of Summary Administration.41 Summary Administration provides for the admission of the will to probate, the entry of an order declaring heirship, and the transfer of personal (but not real) property to the legatees without liability on the part of the transferor. Under both procedures the will is subject to the customary will contest items discussed later. Neither procedure shortens the period in which a claimant against the estate may enforce his lien against the real estate since a personal representative is not appointed.42 The petition of Summary Administration does, however, make representations regarding possible state estate and federal estate tax. An order admitting the will to probate in any county in Illinois vests title in the legatees in all counties in Illinois. However, if the will has been probated in a county other than where the property is located, the legatees are advised to place third parties on constructive notice of their rights under the will by recording an authenticated copy of the will and the order admitting it to probate in the county where the real estate is located.43 This recording procedure can also be utilized to place third parties on constructive notice of legatees’ rights to have the will admitted in Illinois where a will already has been admitted in a state other than Illinois. Conditions of Title Affecting All Estates In addition to establishing title in the heirs or legatees, the lawyer must concern himself in any estate with claims against the estate of the decedent, possible federal estate tax and possible state estate tax, as well as the rights of any personal representative that may be appointed. In addition, where a parent takes from a child as an heir, legatee, beneficiary, survivor, appointee or in any other capacity (other than joint tenancy), if the parent did not support the decedent child or 39 A warranty deed per 765 ILCS 5/9 conveys after acquired title. An unmodified quit claim deed, per 765 ILCS 5/10 does not convey after acquired title. 40 755 ILCS 5/6-8. 41 755 ILCS 5/9-8 and 9-9. 42 755 ILCS 5/18-12. 43 765 ILCS 5/33; See Lewis v. Barnhart, 145 U.S. 56, holding no constructive notice was imparted by a recorded

will that failed to comply with the statute.

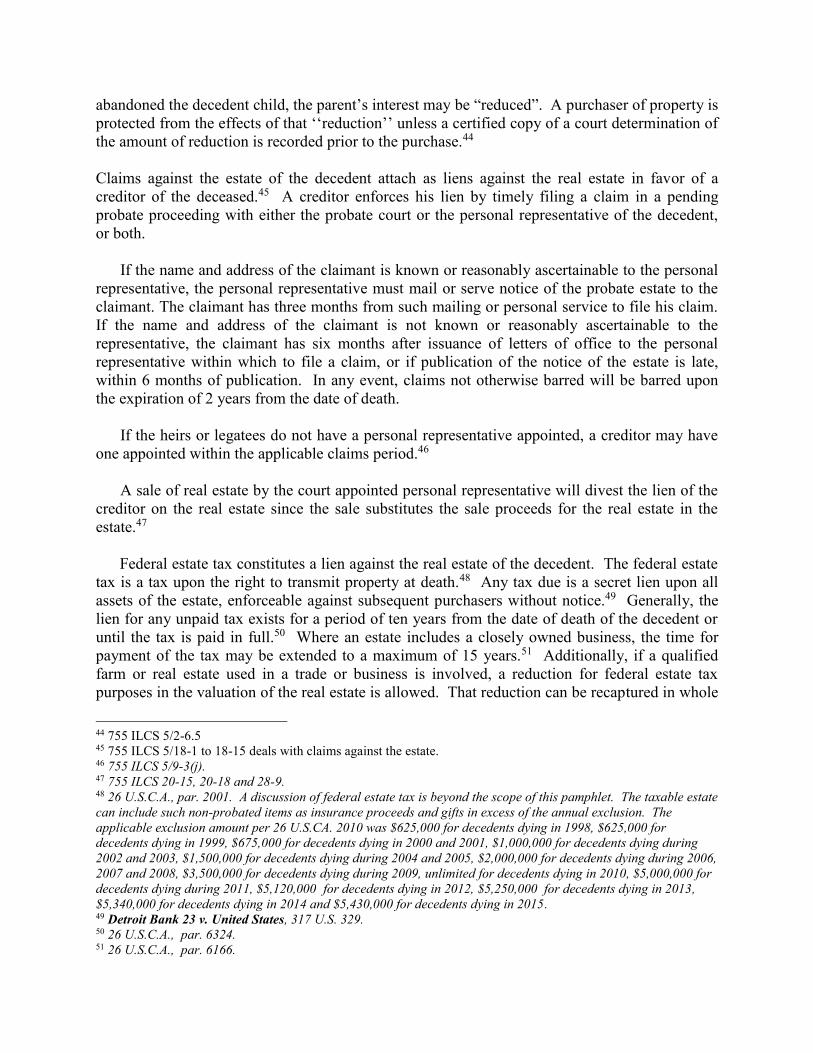

abandoned the decedent child, the parent’s interest may be “reduced”. A purchaser of property is protected from the effects of that ‘‘reduction’’ unless a certified copy of a court determination of the amount of reduction is recorded prior to the purchase.44 Claims against the estate of the decedent attach as liens against the real estate in favor of a creditor of the deceased.45 A creditor enforces his lien by timely filing a claim in a pending probate proceeding with either the probate court or the personal representative of the decedent, or both.

If the name and address of the claimant is known or reasonably ascertainable to the personal representative, the personal representative must mail or serve notice of the probate estate to the claimant. The claimant has three months from such mailing or personal service to file his claim. If the name and address of the claimant is not known or reasonably ascertainable to the representative, the claimant has six months after issuance of letters of office to the personal representative within which to file a claim, or if publication of the notice of the estate is late, within 6 months of publication. In any event, claims not otherwise barred will be barred upon the expiration of 2 years from the date of death.

If the heirs or legatees do not have a personal representative appointed, a creditor may have one appointed within the applicable claims period.46

A sale of real estate by the court appointed personal representative will divest the lien of the creditor on the real estate since the sale substitutes the sale proceeds for the real estate in the estate.47

Federal estate tax constitutes a lien against the real estate of the decedent. The federal estate tax is a tax upon the right to transmit property at death.48 Any tax due is a secret lien upon all assets of the estate, enforceable against subsequent purchasers without notice.49 Generally, the lien for any unpaid tax exists for a period of ten years from the date of death of the decedent or until the tax is paid in full.50 Where an estate includes a closely owned business, the time for payment of the tax may be extended to a maximum of 15 years.51 Additionally, if a qualified farm or real estate used in a trade or business is involved, a reduction for federal estate tax purposes in the valuation of the real estate is allowed. That reduction can be recaptured in whole

44 755 ILCS 5/2-6.5 45 755 ILCS 5/18-1 to 18-15 deals with claims against the estate. 46 755 ILCS 5/9-3(j). 47 755 ILCS 20-15, 20-18 and 28-9. 48 26 U.S.C.A., par. 2001. A discussion of federal estate tax is beyond the scope of this pamphlet. The taxable estate can include such non-probated items as insurance proceeds and gifts in excess of the annual exclusion. The applicable exclusion amount per 26 U.S.CA. 2010 was $625,000 for decedents dying in 1998, $625,000 for decedents dying in 1999, $675,000 for decedents dying in 2000 and 2001, $1,000,000 for decedents dying during 2002 and 2003, $1,500,000 for decedents dying during 2004 and 2005, $2,000,000 for decedents dying during 2006, 2007 and 2008, $3,500,000 for decedents dying during 2009, unlimited for decedents dying in 2010, $5,000,000 for decedents dying during 2011, $5,120,000 for decedents dying in 2012, $5,250,000 for decedents dying in 2013, $5,340,000 for decedents dying in 2014 and $5,430,000 for decedents dying in 2015. 49 Detroit Bank 23 v. United States, 317 U.S. 329. 50 26 U.S.C.A., par. 6324. 51 26 U.S.C.A., par. 6166.

or in part if the real estate is sold or the trade or business discontinued within a 10 year period.52 While the liens imposed under these two special sections are extended, a purchaser is not affected under either section unless a notice of such a lien is filed in the county in which the real estate is located.53

The lien imposed by the State of Illinois on account of the decedent’s death is a lien on the decedent’s real property. The amount of that lien is determined by the statute in effect as of the date of death of the decedent.54 The state lien is not valid as against any purchaser, mortgagee, pledgee or other holder of a security interest for a full and adequate consideration in money or money’s worth, as the lien attaches to the proceeds of the sale. No release from the Attorney General shall be required with respect to such sales or mortgages.55 A purchaser or mortgagee will, however, take subject to a prior recorded notice of lien for taxes due the State of Illinois in excess of the federal estate tax exemption on account of Section 2032A election by the estate.56 For property in the hands of an heir or legatee, the state lien lasts until the latter of 10 years from the date of death or one year after the last deferred payment if the payments are deferred or payable in installments.57 Finally, the title is subject to the rights of the personal representative of the decedent, if and when appointed. Included in these rights are the right to possess the real estate58 and the right to sell, lease or mortgage the real estate, either pursuant to court order for the payment of claims or for the proper administration of the estate,59 all under supervised administration or pursuant to a power of sale in the will60 or pursuant to the representative’s powers under independent administration.61 The rights of the personal representative are not terminated until the closing of a probate proceeding or until an order is entered divesting the representative of his rights in the real estate. There is no limitation as to when an estate may be opened and accordingly, if no estate has been opened, there is no limitation as to when the rights of a personal representative may be exercised. Practically, however, if no probate proceeding has been opened within 2 years of the date of death of the decedent, the time within which unknown creditors could commence a hostile proceedings has passed and the likelihood of an heir or legatee filing a proceeding after that point is minimal. 52 26 U.S.C.A., par. 2032A. 53 26 U.S.C.A., pars. 6324A and 6324B. 54 35 ILCS 405/1 et. Seq. See http://illinoisattorneygeneral.gov/publications/estatetax.htm for the Illinois Attorney General’s summary of the exemption amount for recent specific years. Generally, an Illinois Estate and Generation Skipping Transfer Tax will be due for estates in excess of a federal taxable estate of $1,000,000 for decedents dying in 2003, $1,500,000 for decedents dying in 2004 and 2005 and $2,000,000 for decedents dying between 2006 and 2009. There was no estate tax in 2010. The exemption was $2,000,000 for decedents dying in 2011, $3,500,000 for decedents dying in 2012 and $4,000,000 for decedents dying in 2013, 2014 and 2015. 55 35 ILCS 405/10 56 35 ILCS 405/6 and 405/10. 57 35 ILCS 405/10. 58 755 ILCS 5/20-1. 59 755 ILCS 5/20-2 and 20-4. 60 755 ILCS 5/2-15. 61 755 ILCS 5/28-8(i).

Conditions of Title When the Will is Admitted to Probate In addition to the items discussed in the foregoing section, the legatees’ title under a will admitted to probate is subject to the right of the heirs to have the will formally proved, the right of the heirs or alternative legatees to contest the will, and the rights of other legatees under the will. A will may be admitted to probate without prior notification of the heirs and legatees, based upon a petition filed by the representative62 and affidavits by the witness to the will of the proper execution of the will.63 The petitioner must then give notice of his petition and the order admitting or denying admission of the will to all heirs and legatees of the decedent who have not appeared in the proceeding and/or waived notice within 14 days of the entry of the order.64 The notice must include the prescribed explanation of the rights of the heirs or legatees.65 The order entered is ineffective as to any omitted or improperly notified heir or legatee who had not appeared or waived notice. Lack of notice may be cured by a subsequent appearance, waiver of notice, and consent to entry of the order on behalf of the omitted or improperly notified heir or legatee. If this is not obtained, an amended petition to admit the will to probate must be filed. The periods within which an omitted or improperly notified heir can petition for formal proof of, contest, or renounce the will commence on the date of entry of the amended petition.66 An heir or legatee has the right to petition the court to have the will formally proved using stricter evidence standards.67 The petition must be filed within 42 days of the entry of the order admitting the will. The heirs or legatees also have the right to contest the validity of the will within six months of the order admitting the will to probate.68 The petition to contest the will may be filed either with, or instead of, a demand for formal proof of the will. Within seven months after entry of the order admitting the will, a spouse or party to a civil union has the right to renounce the will and to take a statutory one-third share of the estate (one-half of the estate if there are no children).69 The legatees obviously take their title subject to the provisions of the will. Depending on the terms of the will and the value of the estate, the legatees may be subject to the rights of other legatees under the will to abatement or contribution.70 There is no priority of distribution between real and personal assets of the estate.

62 755 ILCS 5/6-2. 63 755 ILCS 5/6-4. 64 755 ILCS 5/6-10. 65 Supreme Court Rule. 66 755 ILCS 5/6-11. 67 755 ILCS 5/6-21. 68 755 ILCS 5/8-1. 69 755 ILCS 5/2-8. 70 755 ILCS 5/24-3.

Sales by Heirs and Legatees if a Personal Representative has not been Appointed

As a general rule, if a personal representative of the decedent’s estate has not been appointed, a purchaser from the heirs and legatees of the decedent acquires his title subject to the same defects in title that affected the title of the heirs and legatees. This is in stark contrast to the protections against all parties claiming through the decedent’s estate given by statute to a purchaser from the personal representative of the decedent. When there has been no court determination, the purchaser must ascertain who the heirs are, whether the decedent died testate, whether a will is valid and is, in fact, the last will, and who the legatees are. If the decedent died testate, the purchaser must obtain deeds from all heirs and all legatees to cover the possibilities that the will may or may not ever be admitted to probate or may be contested. In addition to determining ownership, the purchaser must concern himself with possible claims against the estate of the decedent, state estate tax, federal estate tax, and the rights and powers of the personal representative if and when appointed. The first three items, discussed earlier, have statutes of limitations protecting a purchaser. While there is no statute of limitations for the rights of the personal representative, if the above items have been resolved, the possibility of the personal representative dealing with the property contrary to the wishes of the heirs and devisees is very minimal. A purchaser can often obtain title insurance to protect himself over these four items before statutes of limitation have run. Effect of the Appointment of a Personal Representative on the Heirs, Legatees, and Purchaser

The issuance of letters of office to a personal representative of a decedent’s estate in Illinois invests the representative with broad powers to deal with real estate. An independent representative acting pursuant to the provisions of Article XXVIII of the Probate Act has the power to take possession of, lease, sell or mortgage real estate without notice to interested parties.71 A good faith purchaser or lender from the independent representative takes title free of the rights of all persons having an interest in the estate, including the heirs, legatees, and claimants.72 A will may grant similar powers to the personal representative and have the same effect.73 Even if the decedent died intestate and independent administration is not elected or is unavailable, the personal representative still has the powers under Article XX of the Probate Act to possess, lease, sell or mortgage the real estate which is not the residence of an heir or devisee after petitioning the court and giving appropriate notice to interested parties.74 Each time real estate is sold by a personal representative, the proceeds of the sale must be

71 755 ILCS 5/28-8(i). 72 755 ILCS 5/28-9. 73 755 ILCS 5/20-15. 74 755 ILCS 5/20.1, 20-2, and 20-18.

covered by a bond.75 If the testator waived surety for his representative, the bond filed at the beginning of the estate automatically increases and a separate bond for the sale of real estate need not be filed. In all other estates, a separate bond must be filed in conjunction with the sale of real estate. This bond is required by Statute before the purchaser becomes a protected party when the sale is had pursuant to court order or the sale is had pursuant to a power of sale in the will.76 The purchaser from an independent representative appears to be protected without a bond, however.77 The remedies for the failure of the independent representative to file this bond if it was required appear to be limited to actions against the personal representative or the attorney for the estate. The sale by a personal representative does not affect the lien for federal estate tax. Accordingly, evidence that no tax is due or releases of the tax should be obtained. It may be desirable to have the personal representative sell real estate if there are unpaid claims, if the heirs or legatees do not want the property, if there are numerous heirs or legatees, if there are minors involved, or if there is conflict among the heirs or the legatees. In addition to adjudicating who the heirs and legatees are and providing a vehicle for conveniently selling, leasing or mortgaging real estate, probate proceedings also shorten the period within which claims may be filed, thereby permitting a faster distribution of estate assets. During the pendency of the estate the title of the heirs or legatees is subject to the rights of the personal representative, claims against the estate, state estate tax, and the rights to contest the will, all of which have been previously discussed. Title is also subject to expenses of administration and to possible surviving spouse’s or civil union partner’s and children’s awards. Expenses of administration include such items as attorney’s fees and the personal representative’s fees. Surviving spouses’ and children’s award are allowances “… free from execution, garnishment or attachment in the hands of the representative … (in) such a sum of money as the court deems reasonable for proper support … for the period of nine months after the death of the decedent …”78 The priority of the distribution of the assets of the estate is governed by statute. All claims including expenses of administration and surviving spouses’ and children’s awards must be paid prior to any distribution to the heirs or legatees.79 The priority of distribution among the legatees is also set forth.80 In a supervised administration, unless the final account is waived based upon consents of all interested parties, the final account of the personal representative should show proof of payment and indicate the proper distribution of assets.81 The order discharging the personal representative and closing the estate confirms the distributions indicated on the final account. In estates governed by the provisions of Independent Administration, while the heirs or 75 755 ILCS 5/12-9 and 28-1; Major Revisions of Probate Act Simplifies Settlement of Decedent’s Estates by Morton Jon Barnard, John C. Williams, and James N. Zartman, Ill. Bar Journal 68:248, pp. 253 and 254. 76 755 ILCS 5/20-15 and 20-18 referring to 20-5(e). 77 755 ILCS 5/28-9. 78 755 ILCS 5/15-1, 15-2 and 20-18. 79 755 ILCS 5/18-10 and 18-13. 80 755 ILCS 5/24-3. 81 755 ILCS 5/24-1

legatees receive a final account, no final account need be filed with the court unless an interested party requests an accounting as in supervised administration.82 If the real estate is being retained by the heirs or legatees, the independent representative is required to confirm title in the heirs or legatees by recording an instrument of release and distribution with the recorder of deeds in the county where the real estate is located.83 The instrument of release and distribution must set forth the parties entitled to the real estate and the legal description of the real estate. Courts in different counties have approved their own form of instrument of release and distribution. An independent representative may demand the return of the real estate in the hands of the heirs or devisees if the need so arises during the pendency of the estate, even after recording the instrument of release and distribution. A purchaser from the heirs or legatees relying on the instrument of release and distribution, however, is protected against all parties claiming through the estate.84 If the heirs or legatees retain an interest in real estate at the end of the probate estate, a Notice of Probate must also be recorded in the county in which the property is located prior to the termination of the probate proceeding. If independent administration is involved, the Notice of Probate may be combined with the Instrument of Release and Distribution.85 Attached as Exhibit A is the combined Notice of Probate and Instrument of Release and Distribution used in Cook County. Foreign Decedents As set forth previously, whenever Illinois real estate is involved, Illinois law will apply.86 The heirs and their shares are determined by Illinois law as of the date of death. If the decedent died testate, it may be necessary to have the will admitted to probate in Illinois to vest title to Illinois real estate in the legatees. A foreign probate proceeding, including an order admitting the will to probate in a foreign state, does not vest title to Illinois real estate. The recording of an exemplified copy of the will of a foreign decedent admitted in a foreign state only constitutes constructive notice of the rights of the legatees to have the will admitted to probate in Illinois. A foreign will may be admitted to probate in Illinois if it was executed in conformity with the laws of the State of Illinois, with the state where it was executed, or with the testator’s domicile at the time of execution and must be proved pursuant to statute.87 Such conveyances by the foreign representative are subject to claims against the estate of the decedent, federal estate taxes, and if the sale is held pursuant to a power of sale under a will which has been admitted to probate in Illinois, to the right to have the will formally proved, the right to contest the will and the right of the surviving spouse to renounce the will. If the executor or trustee under a foreign will is a foreign corporate trustee, it must be 82 755 ILCS 5/28-11(a) 83 755 ILCS 5/28-10(a) 84 755 ILCS 5/28-10(d). 85 755 ILCS 5/20-24. 86 See Sternberg v. St. Louis Union Trust Co., 394 Ill. 452, wherein a will which was valid in Missouri, was construed to have been revoked under then existing Illinois Law. 87 755 ILCS 5/7-1.

qualified to accept and execute trusts in Illinois.88 An unqualified corporate trustee could not act as trustee or executor in Illinois or validly exercise a power of sale relating to Illinois real estate either as executor or as trustee, even though ancillary proceedings to probate the will are had in Illinois.89 Foreign trust companies can qualify to do a trust business in Illinois and act as executor or trustee if the laws of the state in which they are incorporated authorize Illinois trust companies to qualify under the Illinois law. If a foreign trust company does not qualify under Illinois law, an administrator with the will annexed must be appointed in Illinois in order to exercise a power of sale in a will. In the case of a foreign trustee in title, it would be necessary to have a qualified successor trustee appointed. The Role of Title Insurance The role of title insurance in any real estate transaction is first to provide an assurance as to who owns the real estate and what liens or restrictions the real estate is subject to; secondly, to provide a legal defense and compensation if that assurance is wrong; and finally, to provide a party capable of assuming risks over matters that are uncertain, unknown, or unacceptable to the insured. A primary reason for the growth of title insurance is the expertise in this specialized field of the title insurers and their willingness to assume risks not only over known matters but over matters not ascertainable from the public records, such as unknown heirs, subsequently discovered wills, fraud or forgery, an unadjudicated incompetency or inchoate liens. The expertise of the title insurer comes into play when an examination of a formal probate proceeding is made. The proceeding must be checked for compliance with the statutory provisions. The will, if any, must be interpreted. The most innocuous clause in a will can lead to a will construction suit that may not be filed for years after the probate proceedings have closed.90 Finally, a conclusion must be drawn as to the effect of the probate proceeding. The vesting of title without full probate proceedings being had and the items that the title is subject to have been discussed earlier. Determining heirship and the validity of a last will and insuring over the rights of creditors are the big issues. The willingness of a title insurer to insure title when no probate proceedings are had often provides a faster, easier, and less expensive alternative to probate proceedings. A list of the requirements and fees of a title insurer to insure over the items that title is subject to when no probate proceedings are had is attached as Exhibit B-1. Relative to the items at Exhibit B-1, a title insurer will require state estate tax clearance if no purchaser is involved, federal estate tax releases or evidence that no such taxes were due, and, unless the decedent died more than two years earlier, satisfactory information, indemnities, and premiums to permit the title insurer to guarantee over claims against the estate and possible rights of the personal representative. The affidavit of heirship provides the most difficulty. It should recite facts concerning the

88 205 ILCS 620/4-1. 89 755 ILCS 5/22-4. The Pennsylvania Co. for Insurance on Lives v. Bauerle, 143 Ill. 459 90 755 ILCS 5/22-6.

decedent’s heirship sufficient to determine who the heirs are, state there are no other heirs, and conclude with a statement that the affidavit is made to induce the title insurer to show specified parties as the sole heirs of the decedent. The preparer should keep in mind that Illinois statutes provide for representation per stirpes. It also should be remembered that heirs dying after the deceased owner of the land are themselves deceased owners whose heirs (including spouse) and legatees must also be considered. An affidavit checklist is attached as Exhibit B-2. If the heirship is more remote than the spouse and children, the appended chart should be consulted. In such cases the existence of any surviving heirs in each closer class must affirmatively be denied until the class that contains the decedent’s closest surviving heir is reached. The form of the statement of information and undertakings required by the title insurer before it will guarantee over claims against the estate of the decedent vary from company to company and county to county. Attached as Exhibit B-3 is the Statement of Information, and as Exhibits B-4 and B-5, the undertakings for intestate and testate decedents, respectively, which are acceptable to Chicago Title Insurance Company in Cook County, Illinois. The amount of the premium that will be charged for insuring over claims against the estate of the decedent once the statement and undertaking are obtained depends upon the amount of the policy issued and the amount of time remaining in the two years from date of death in which a proceeding to enforce a claim may be commenced. If that period has elapsed and no proceeding has been filed, claims against the estate will be deleted without documentation or a premium being required. If the decedent died testate, the rights or the heirs to contest the will and the rights of the legatees to admit the will are customarily dealt with by proper deeds from all heirs and legatees. The rights of the heirs to contest the will can also be deleted if the will has been properly admitted to probate, the period in which a will contest could have been filed has elapsed and no such contest has in fact been filed. Title insurance can be utilized to avoid some of the court time, paperwork, and expense involved in a formal probate proceeding. Additionally, it can often prove to be faster and less expensive. When the claims period has elapsed, title insurance is preferable unless probate becomes necessary to vest title. Additionally, a title insurer has the expertise to aid and assist the attorney in providing the best resolution for his client. CONCLUSION Vesting title to real estate owned by a decedent can be accomplished without resort to a probate proceeding if the heirs and legatees are competent, cooperative adults. Title can also be vested in the legatees by having the will admitted to probate without appointing a personal representative of the decedent’s estate. Title insurance can be utilized to guarantee the effectiveness of these procedures and to provide protection over the various liens affecting the title to a decedent’s real estate. Use of these methods in lieu of full probate proceedings permits an attorney to provide his clients with prompt, efficient results at minimal cost.

EXHIBIT A NOTICE OF PROBATE AND RELEASE OF ESTATE’S INTEREST IN REAL ESTATE (Rev. 8/1/00) CCP 0421 NOTICE OF PROBATE UNDER SUPERVISED OR INDEPENDENT ADMINISTRATION The undersigned, who was appointed representative of the estate of _________________, deceased, on ______, 20__, by the Circuit Court of Cook County Department, Probate division (Case No. _______________, Docket _______________, Page _________, ) and is currently acting as representative, gives notice pursuant to Section 5/20-24(a) of the Probate Act that: Decedent of __________________ (address) died on __________________, ____ owning the following described real estate (INSERT OR ATTACH LEGAL DESCRIPTION. If decedent had a partial interest, state the extent of the interest.) Permanent Real Estate Index No:_______________________________. The street address of the real estate is ____________________________.

RELEASE OF ESTATE’S INTEREST IN REAL ESTATE

UNDER INDEPENDENT ADMINISTRATION Pursuant to Sections 5/28-8(i) and 5/28-10(a) of the Probate Act, the undersigned independent representative releases the estate’s interest in the above real estate and confirms that title passed at decedent’s death to the following heirs or legatees: (INSERT OR ATTACH LIST.) Name Address Share

Dated: _____________________________ ____________________________________ Representative(s) ____________________________________ Print or type name(s) of Representative(s) Address(es):_________________________ State of ____________________ County of ___________________ Acknowledged before me this _______ day of ___________, 20_____, by ____________________, *a duly

authorized officer of _____________________, a ___________corporation, on behalf of the corporation.

___________________________________

(Notary Public) This instrument was prepared by and should be mailed to: Send subsequent tax bills to: *Use only for a corporate acknowledgment.

EXHIBIT B-1 CHICAGO TITLE INSURANCE COMPANY REQUIREMENTS FOR ACCEPTANCE OF PERSONAL UNDERTAKING AND ADDITIONAL PREMIUM PAYMENT IN LIEU OF PROBATE I. The following documentation is required for presentation to the Examiner of Title

Underwriter for review.

Affidavit of Heirship (See attached checklist) A Certified or Uncertified Copy of the Death Certificate Joint Tenancy Affidavit (if applicable) A Copy of Will (if decedent died testate) Illinois Estate Tax and Illinois Generation-Skipping Transfer Tax release or final

receipt (if applicable) Federal Estate Tax release or estate closing letter (if applicable) Notarized Statement of Information (See attached copy) Personal Undertaking form (See attached copy) Paid funeral bill(s) Paid hospital bill(s) Paid personal physician bill(s)

II. Upon review and acceptance of the above documentation the Examiner or Title

Underwriter will arrange for the billing of the appropriate premium. The premium charged is based on the date of death, as follows: