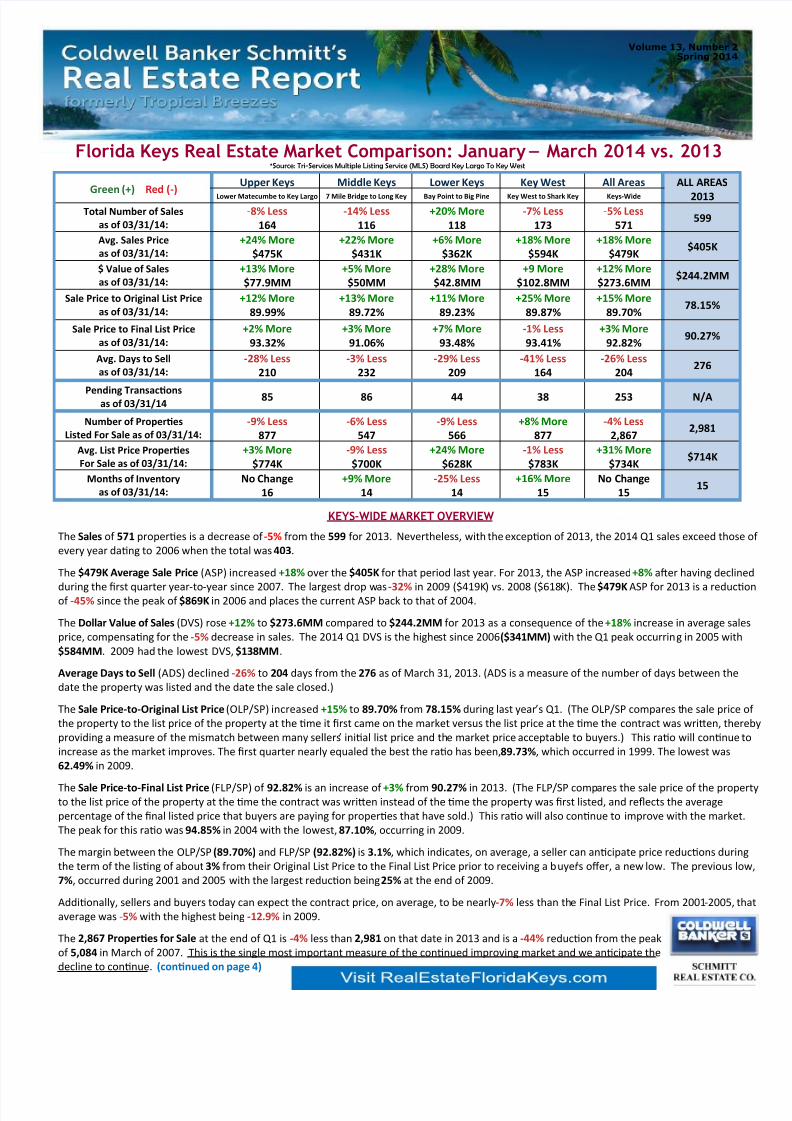

Volume 13, Number 2 Spring 2014Florida Keys Real Estate Market Comparison: January March 2014 vs. 2013 *Source: Tri-Services Multiple Listing Service (MLS) Board Key Largo To Key West Upper KeysMiddle KeysLower KeysKey WestAll AreasALL AREAS2013Green (+) Red (-)Lower Matecumbe to Key Largo7 Mile Bridge to Long KeyBay Point to Big PineKey West to Shark KeyKeys-WideTotal Number of Sales as of 03/31/14:-8% Less164-14% Less116+20% More118-7% Less173-5% Less571599Avg. Sales Priceas of 03/31/14:+24% More$475K+22% More$431K+6% More$362K+18% More$594K+18% More$479K$405K$ Value of Salesas of 03/31/14:+13% More$77.9MM+5% More$50MM+28% More$42.8MM+9 More$102.8MM+12% More$273.6MM$244.2MMSale Price to Original List Price as of 03/31/14:+12% More89.99%+13% More89.72%+11% More89.23%+25% More89.87%+15% More89.70%78.15%Sale Price to Final List Priceas of 03/31/14:+2% More93.32%+3% More91.06%+7% More93.48%-1% Less93.41%+3% More92.82%90.27%Avg. Days to Sell as of 03/31/14:-28% Less210-3% Less232-29% Less209-41% Less164-26% Less204276Pending Transaconsas of 03/31/1485864438253N/ANumber of ProperesListed For Sale as of 03/31/14: -9% Less877-6% Less547-9% Less566+8% More877-4% Less2,8672,981Avg. List Price Properes For Sale as of 03/31/14: +3% More$774K-9% Less$700K+24% More$628K-1% Less$783K+31% More$734K$714KMonths of Inventoryas of 03/31/14:No Change16+9% More14-25% Less14+16% More15No Change1515KEYS-WIDE MARKET OVERVIEWTheSalesof 571properes is a decrease of -5%fromthe 599for 2013. Nevertheless, with the excepon of 2013, the 2014 Q1 sales exceed those of every year dang to 2006 when the total was 403. The $479KAverage Sale Price(ASP) increased +18%over the $405Kfor that period last year. For 2013, the ASP increased +8%aer having declined during the rst quarter year-to-year since 2007. The largest drop w as -32% in 2009 ($419K ) vs. 2008 ($618 K). The $479KASP for 2013 is a reducon of -45%since the peak of $869Kin 2006 and places the current ASP back to that of 2004. The Dollar Value of Sales (DVS) rose +12% to $273.6MMcompared to $244.2MMfor 2013 as a consequence of the +18%increase in average sales price, compensang for the -5%decrease in sales. The 2014 Q1 DVS is the highe st since 2006($341MM)with the Q1 peak occurrin g in 2005 with $584MM. 2009 had the lowest DVS, $138MM.Average Days to Sell(ADS) declined -26%to 204 days from the 276 as of March 31, 2013. (ADS is a measure of the number of days between the date the property was listed and the date the sale closed.) The Sale Price-to-Original List Price(OLP/SP) increased +15%to 89.70% from 78.15% during last year ’s Q1. (The OLP/SP compares t he sale price of the property to the list price of the property at the me it rst came on the market versus the list price at the me the contract was wrien, thereby providing a measure of the mismatch between many sellers ’ inial list price and the market price acceptable to buyers.) This rao will connue to increase as the market improves. The rst quarter nearly equaled the best the rao has been, 89.73%, which occurred in 1999. The lowest was 62.49%in 2009. The Sale Price-to-Final List Price(FLP/SP) of 92.82% is an increase of +3%from 90.27%in 2013. (The FLP/SP comp ares the sale price of the property to the list price of the property at the me the contract was wrien instead of the me the property was rst listed, and reects the average percentage of the nal listed price that buyers are paying for properes that have sold.) This rao will also connue to improve with the market. The peak for this rao was 94.85%in 2004 with the lowest, 87.10%, occurring in 2009. The margin between the OLP/SP (89.70%) and FLP/SP (92.82%) is 3.1%, which indicates, on average, a seller can ancipate price reducons during the term of the lisng of about 3%from their Original List Price to the Final List Price prior to receiving a b uyer ’s oer, a new low. The previous low, 7%, occurred during 2001 and 2005 with the largest reducon being 25%at the end of 2009. Addionally, sellers and buyers today can expect the contract price, on average, to be nearly-7%less than the Final List Price. From 2001 -2005, that average was -5% with the highest being-12.9% in 2009.The 2,867Properes for Saleat the end of Q1 is -4% less than 2,981on that date in 2013 and is a -44%reducon from the peak of 5,084in March of 2007. This is the single most important measure of the connued improving market and we ancipate the decline to connue. (connued on page 4)