Embed Size (px)

Citation preview

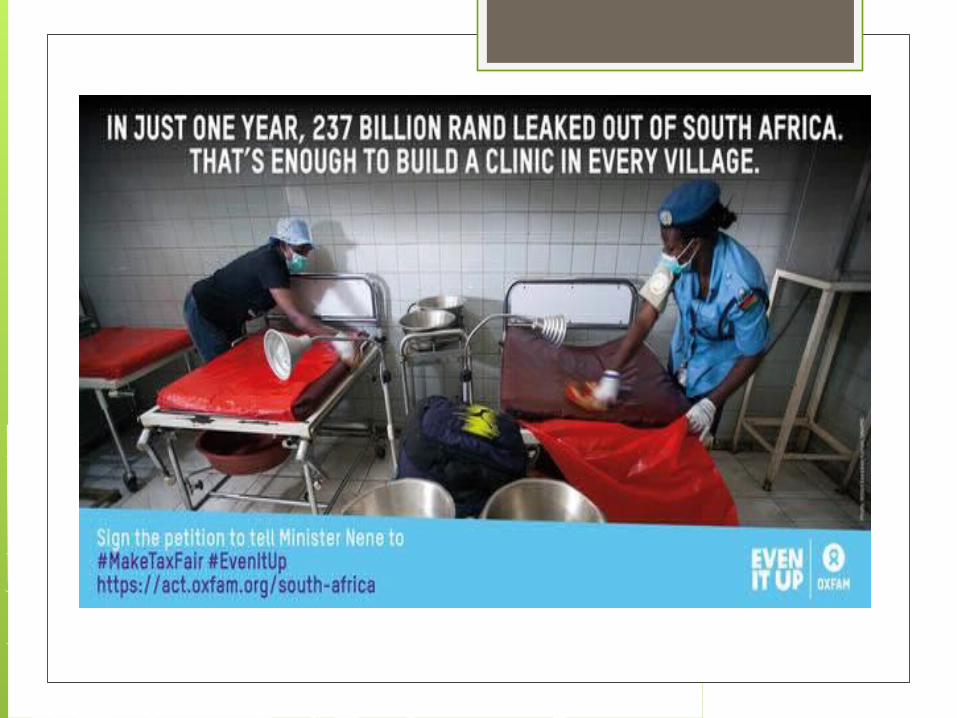

REBRIP TAX JUSTICE SEMINAR:Brazil – Sao Paulo25 June 2015

Sibulele PoswayoSANI Secretariat

Content of Presentation Discussing Tax in SA Mining Sector

Introduce SANI Generous Taxes, Tax Evasion & other

definitions South African/African Statistics in Mining

Sector South African Experience of Tax Injustice

in Extractives Recommendations on Tax –

SANI/EJN/ECSN Position

“Slower economic growth will place pressure on the projected revenue collection. Global trends of tax base erosion and profit shifting through aggressive avoidance and evasion schemes are a threat to be dealt with” - Acting SARS Commissioner

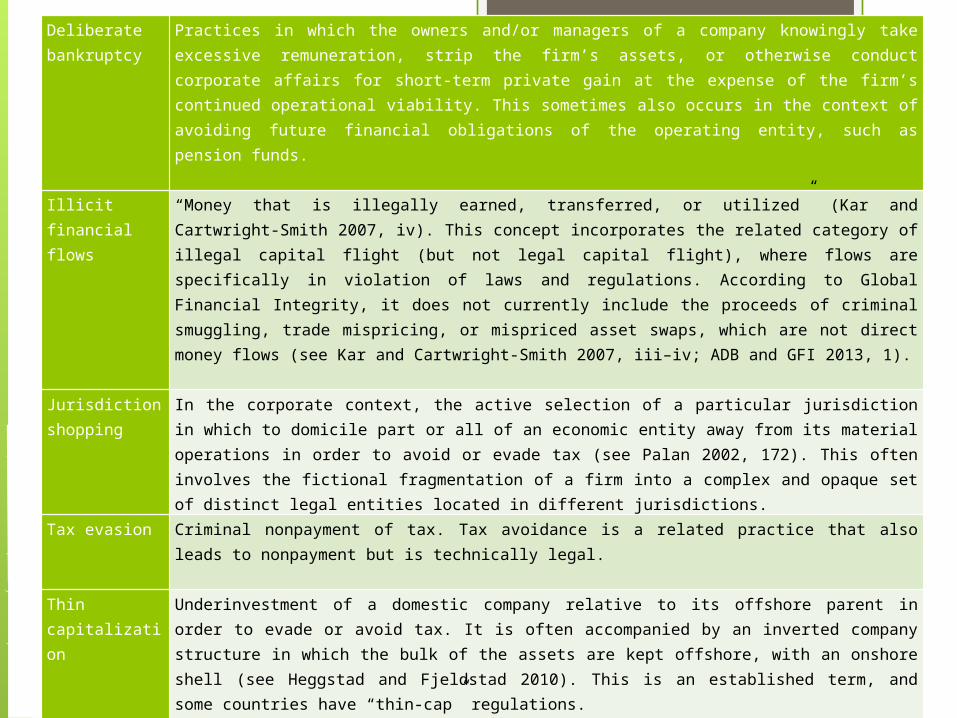

6Deliberate bankruptcy

Practices in which the owners and/or managers of a company knowingly take excessive remuneration, strip the firm’s assets, or otherwise conduct corporate affairs for short-term private gain at the expense of the firm’s continued operational viability. This sometimes also occurs in the context of avoiding future financial obligations of the operating entity, such as pension funds.

Illicit financial flows

“Money that is illegally earned, transferred, or utilized” (Kar and Cartwright-Smith 2007, iv). This concept incorporates the related category of illegal capital flight (but not legal capital flight), where flows are specifically in violation of laws and regulations. According to Global Financial Integrity, it does not currently include the proceeds of criminal smuggling, trade mispricing, or mispriced asset swaps, which are not direct money flows (see Kar and Cartwright-Smith 2007, iii–iv; ADB and GFI 2013, 1).

Jurisdiction shopping

In the corporate context, the active selection of a particular jurisdiction in which to domicile part or all of an economic entity away from its material operations in order to avoid or evade tax (see Palan 2002, 172). This often involves the fictional fragmentation of a firm into a complex and opaque set of distinct legal entities located in different jurisdictions.

Tax evasion Criminal nonpayment of tax. Tax avoidance is a related practice that also leads to nonpayment but is technically legal.

Thin capitalization

Underinvestment of a domestic company relative to its offshore parent in order to evade or avoid tax. It is often accompanied by an inverted company structure in which the bulk of the assets are kept offshore, with an onshore shell (see Heggstad and Fjeldstad 2010). This is an established term, and some countries have “thin-cap” regulations.

Trade mispricing

Abuse of pricing in trade between apparently unrelated parties, such as through the deliberate overinvoicing of imports or underinvoicing of exports, usually for the purpose of tax evasion.

Transfer pricing

“A transfer price is a price, adopted for book-keeping purposes, which is used to value transactions between affiliated enterprises integrated under the same management at artificially high or low levels in order to effect an unspecified income payment or capital transfer between those enterprises” (OECD 2001). Transfer pricing is “not, in itself, illegal or necessarily abusive” in all definitions (Tax Justice Network 2013), but here we will assume a mispricing element.

Background on Africa A decade of highly impressive growth has not

brought comparable improvements in health, education and nutrition BASIC SERVICES; in many countries, the gap between rich and poor has only widened INEQUALITY; and Africa must create jobs fast enough to keep pace with the growth of its young and growing workforce.

By some estimates, illicit flows from Africa could be as much as US $50 billion per

annum between 2000 & 2008.

Exclusion of African countries from THE BEPS project

Representation

• None in OECD• Minimal in G-20

Consultation

• Asia-Pacific and Latin American-Caribbean Regional consultation meetings

• Minimal in Africa as there was no consultation with Africa civil society

Content

• BEPS = tax evasion in Africa not covered by BEPS

• Harmful competition prevalent in Africa not covered by BEPS

• The BEPS project have largely excluded African countries in process and substance

• The African civil society have also been excluded from the BEPS project.

Exclusivity

• South Africa must use its position in the OECD and G-20 committees to promote and articulate the interests of all African countries in the BEPS project.

• South Africa must also work closely with AU and NEPAD to promote and articulate the interests of all African countries in the BEPS project.

SA as the African

champion

Corporate income tax rates, 2006–2014 (%)

SA Mining Background - 1 Taxes are the most important, sustainable

and predictable source of finance for government and taxes from the mining sector – in 2012 = R21,4 billion in 2012.

Africa is world’s largest producer of platinum group metals, chrome ore, manganese and vanadium as and a major supplier of coal, iron ore, nickel and uranium

However, the SA mining sector is insufficiently transparent with high illegal tax evasion & tax avoidance

SA Mining Background – 2Generous Taxes SA mines (&MNC’s cooperating in SA) are allowed

to write off against tax all their capital expenditures in the year of acquisition and can forward any losses indefinitely, also offsetting them against tax liability – common practice in most mining regimes

Mining MNC’s pay no VAT on their exports and are entitled to a refund for all the input taxes paid by them. This is a major gain for gold and diamond which export virtually all their produce.

SA Mining Background – 3Generous Taxes Gold mining companies’ taxable income is

derived from a formula which takes account of the ratio of profits to revenue. If companies makes no profits (or low profits at around 5% of revenue) the sate receives no ta – while still shareholders still receive dividends in the same scenario. –

This is fertile ground for cross-ownership.

SA Mining Background – 4Generous Taxes

Royalty rates are lower that originally proposed.

SA has the introduced the Royalty Bill in 2010 which was able to be implemented and find out that US$359 – US$499m a year in revenues with the current royalty rates compared to those rejected in the previous draft the Bill

SANI @ EJN’s Response Submissions on the Base erosion and

profit shifting (BEPS)even though excluded in the process.

Mining taxation to the Davies Tax Committee.

Call for National Minimum Wage in the Mining Sector to address inequality

Recommendations1. Government to promote transparency in

the Mining Sector2. The formula used to calculate income tax

for gold mines should be reviewed to ensure that companies are not able to reduce their taxable profits by cross-ownership of companies

3. Mining companies should not be allowed to completely write off their capital expenditure in the year of acquisition.

Recommendations cont

4. SA, as the only African country member of the G20 grouping, take a lead in introducing mandatory reporting for mining companies of all payments to all governments. – All companies JSE must provide this information.

5. Companies should be required to publish their beneficial owners and those of subsidies and provide a detailed organogram of the company structure as a part of normal reporting.

Recommendations cont

6, THE PRINCIPLE OF FREE, PRIOR & INFORMED CONSENT SHOULD BE INTRODUCED IN SOUTH AFRICA

In order to improve transparency at project level and community participation in mining projects, officials should be trained and deployed to ensure consultations between companies and communities proceed without coercion or corruption.

Recommendations cont

7, Use the funds from effective taxation to address social inequalities in SA

- Gini-coeffient on 0.7; Wealth inequalities which are much higher with limited ownership of shares by majority & 12% of the pop own 80% of the land.

Health

Education

Child mortality

Years of schooling

School attendance

The four dimensions of poverty

Living standar

ds

Lighting

Heating

Cooking

Water

Sanitation

Economic

activity Unemployment

Dwelling

Assets

(death of child under 5)

)

Multidimensional Poverty-SAMPI

Conclusion Tax me if you Can – Tax Campaign Community mobilisation by sharing the

truth on MNCS’s @ Tax Evasion SA Government must follow

recommendations Define clearly what Tax injustice is in

National Policies (Not just IFF’s) Use Progressive Tax to address income,

Wealth and Social Inequalities

www.sainequality.com

#SANImember

South African Network on Inequality:SANI