Embed Size (px)

Citation preview

RECENT DEVELOPMENTSCURRENT TAX CONTROVERSIESIN BRAZIL

Leonardo Homsy, Partner, Campos Mello Advogados, Rio de Janeiro, Brazil

*This presentation is offered for informational purposes only, and the content should not be construed as legal advice on any matter.

Agenda

Payroll tax on certain indemnity payments

Equity-based compensation plans

Application of Article 7 of the Double Taxation Treaties(Business Profits)

Taxation of software

Payroll tax on certain indemnity payments

Payroll tax: 20% applied on total payroll (INSS), plus certain charges toa total of 27-30%

Temporary methodology: 1-2% of gross revenues (for selectedeconomic sectors only)

Mandatory indemnity payments for employees: non-exhaustive list

“Christmas bonus” or “13th salary” granted to employeesproportional to number of months worked during the year

Remunerated 30-day vacations per 12 months of work plus a bonusequivalent of 1/3 monthly wage

Maternity/paternity leave

15-day sickness leave

Prior notice of dismissal

Compensation for extra hours of work

3

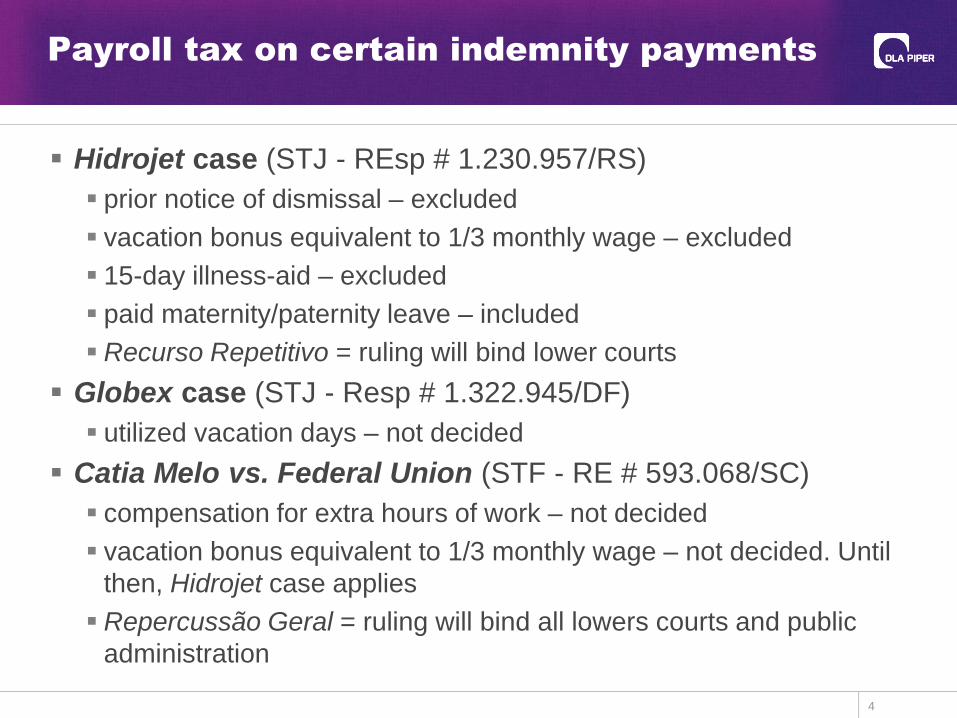

Payroll tax on certain indemnity payments

Hidrojet case (STJ - REsp # 1.230.957/RS)

prior notice of dismissal – excluded

vacation bonus equivalent to 1/3 monthly wage – excluded

15-day illness-aid – excluded

paid maternity/paternity leave – included

Recurso Repetitivo = ruling will bind lower courts

Globex case (STJ - Resp # 1.322.945/DF)

utilized vacation days – not decided

Catia Melo vs. Federal Union (STF - RE # 593.068/SC)

compensation for extra hours of work – not decided

vacation bonus equivalent to 1/3 monthly wage – not decided. Untilthen, Hidrojet case applies

Repercussão Geral = ruling will bind all lowers courts and publicadministration

4

Equity-based compensation plans

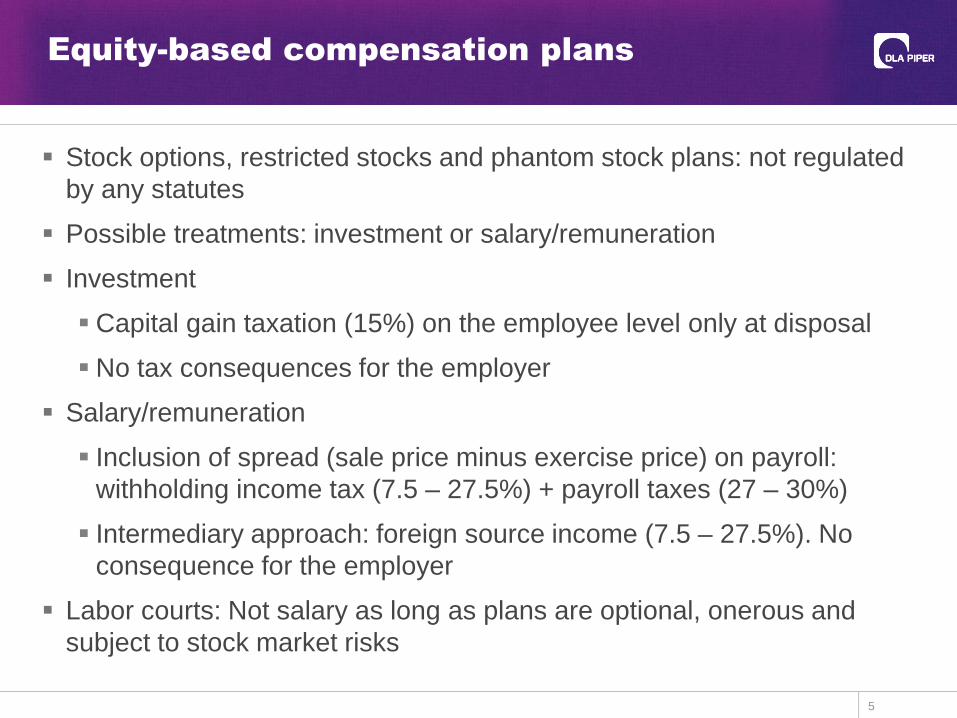

Stock options, restricted stocks and phantom stock plans: not regulatedby any statutes

Possible treatments: investment or salary/remuneration

Investment

Capital gain taxation (15%) on the employee level only at disposal

No tax consequences for the employer

Salary/remuneration

Inclusion of spread (sale price minus exercise price) on payroll:withholding income tax (7.5 – 27.5%) + payroll taxes (27 – 30%)

Intermediary approach: foreign source income (7.5 – 27.5%). Noconsequence for the employer

Labor courts: Not salary as long as plans are optional, onerous andsubject to stock market risks

5

Equity-based compensation plans

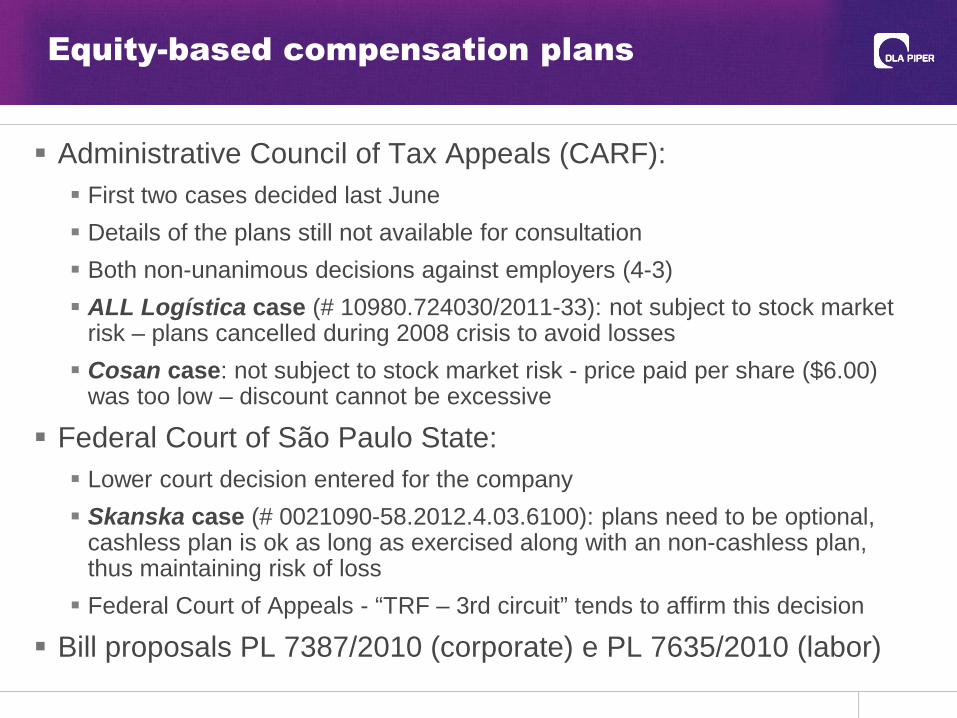

Administrative Council of Tax Appeals (CARF):

First two cases decided last June

Details of the plans still not available for consultation

Both non-unanimous decisions against employers (4-3)

ALL Logística case (# 10980.724030/2011-33): not subject to stock marketrisk – plans cancelled during 2008 crisis to avoid losses

Cosan case: not subject to stock market risk - price paid per share ($6.00)was too low – discount cannot be excessive

Federal Court of São Paulo State:

Lower court decision entered for the company

Skanska case (# 0021090-58.2012.4.03.6100): plans need to be optional,cashless plan is ok as long as exercised along with an non-cashless plan,thus maintaining risk of loss

Federal Court of Appeals - “TRF – 3rd circuit” tends to affirm this decision

Bill proposals PL 7387/2010 (corporate) e PL 7635/2010 (labor)

Taxation of software licensing and services

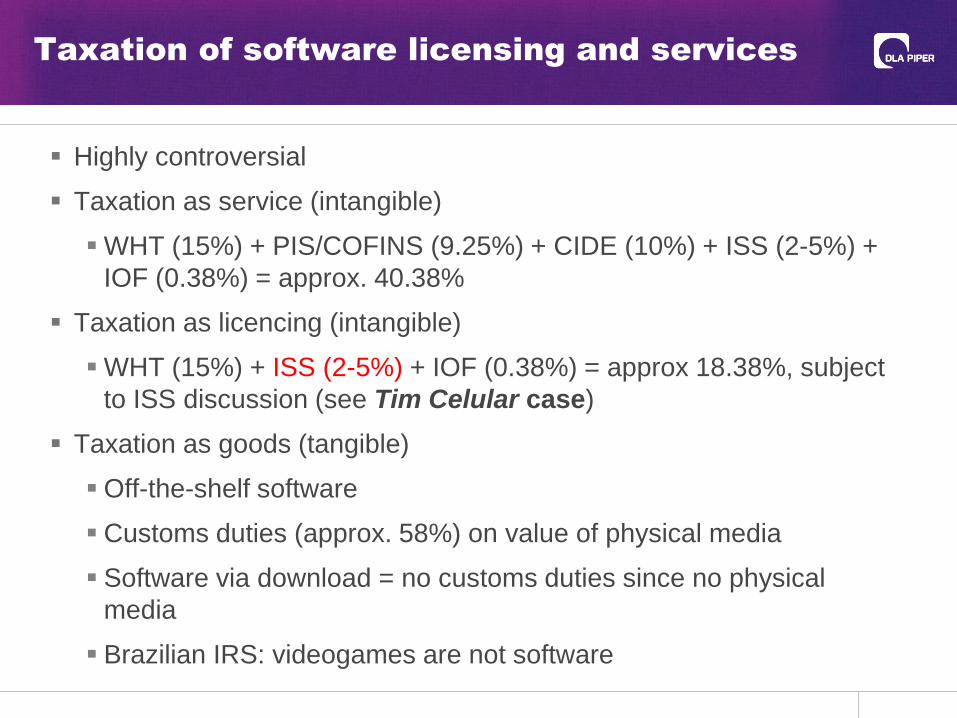

Highly controversial

Taxation as service (intangible)

WHT (15%) + PIS/COFINS (9.25%) + CIDE (10%) + ISS (2-5%) +IOF (0.38%) = approx. 40.38%

Taxation as licencing (intangible)

WHT (15%) + ISS (2-5%) + IOF (0.38%) = approx 18.38%, subjectto ISS discussion (see Tim Celular case)

Taxation as goods (tangible)

Off-the-shelf software

Customs duties (approx. 58%) on value of physical media

Software via download = no customs duties since no physicalmedia

Brazilian IRS: videogames are not software

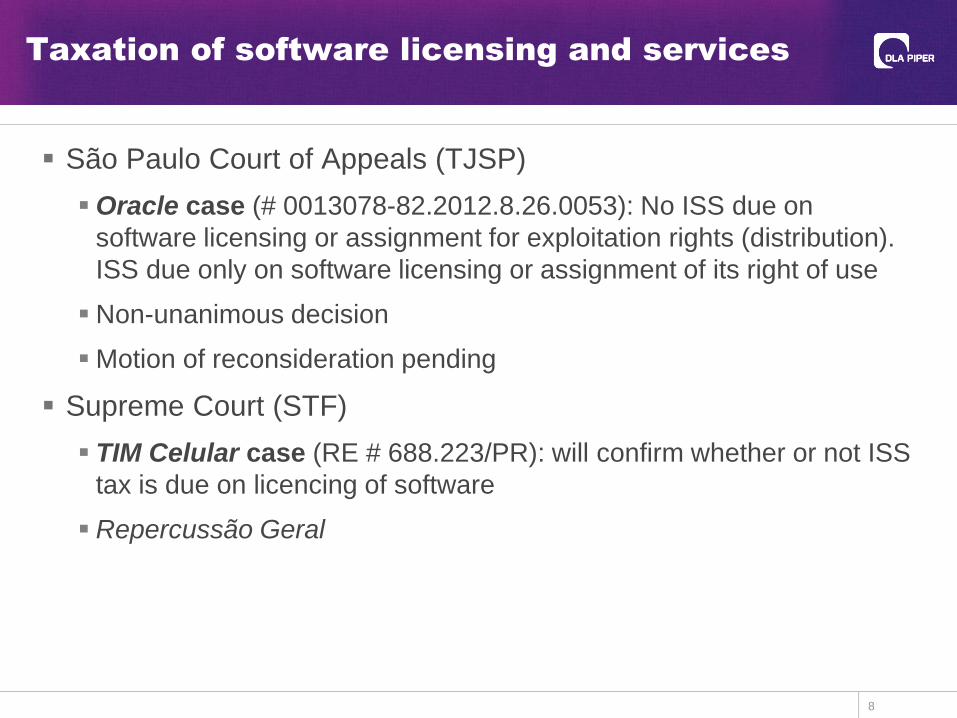

Taxation of software licensing and services

São Paulo Court of Appeals (TJSP)

Oracle case (# 0013078-82.2012.8.26.0053): No ISS due onsoftware licensing or assignment for exploitation rights (distribution).ISS due only on software licensing or assignment of its right of use

Non-unanimous decision

Motion of reconsideration pending

Supreme Court (STF)

TIM Celular case (RE # 688.223/PR): will confirm whether or not ISStax is due on licencing of software

Repercussão Geral

8

9

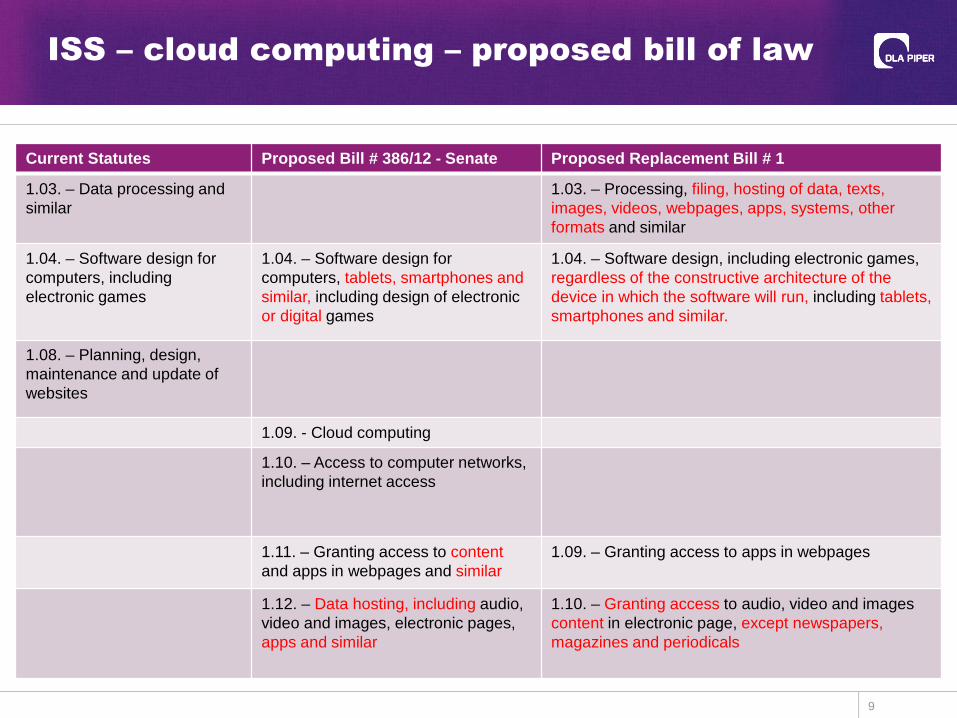

ISS – cloud computing – proposed bill of law

Current Statutes Proposed Bill # 386/12 - Senate Proposed Replacement Bill # 1

1.03. – Data processing andsimilar

1.03. – Processing, filing, hosting of data, texts,images, videos, webpages, apps, systems, otherformats and similar

1.04. – Software design forcomputers, includingelectronic games

1.04. – Software design forcomputers, tablets, smartphones andsimilar, including design of electronicor digital games

1.04. – Software design, including electronic games,regardless of the constructive architecture of thedevice in which the software will run, including tablets,smartphones and similar.

1.08. – Planning, design,maintenance and update ofwebsites

1.09. - Cloud computing

1.10. – Access to computer networks,including internet access

1.11. – Granting access to contentand apps in webpages and similar

1.09. – Granting access to apps in webpages

1.12. – Data hosting, including audio,video and images, electronic pages,apps and similar

1.10. – Granting access to audio, video and imagescontent in electronic page, except newspapers,magazines and periodicals

Payments for services to foreign companies

in treaty jurisdictions

Article 7 (Business profits) follows OECD model: Exclusive residencetaxation, unless PE

Brazilian IRS in practice overrules Article 7

Different arguments have been used by IRS since 2000.

Declaratory Interpretative Act # 1/2000 (ADI 1/2000): Application of“Other Income” Article

Private Rulings # 147/2004 and 35/2005: Same treatment as royalties,according to many protocols

Private Rulings # 136/2004 and 56/2009: Domestic legislationdifferentiates “profit” from “income”

Private Ruling # 85/2006, Application of “Independent professionalServices” Article

March 2013 10

Payments for services to foreign companies

in treaty jurisdictions

11

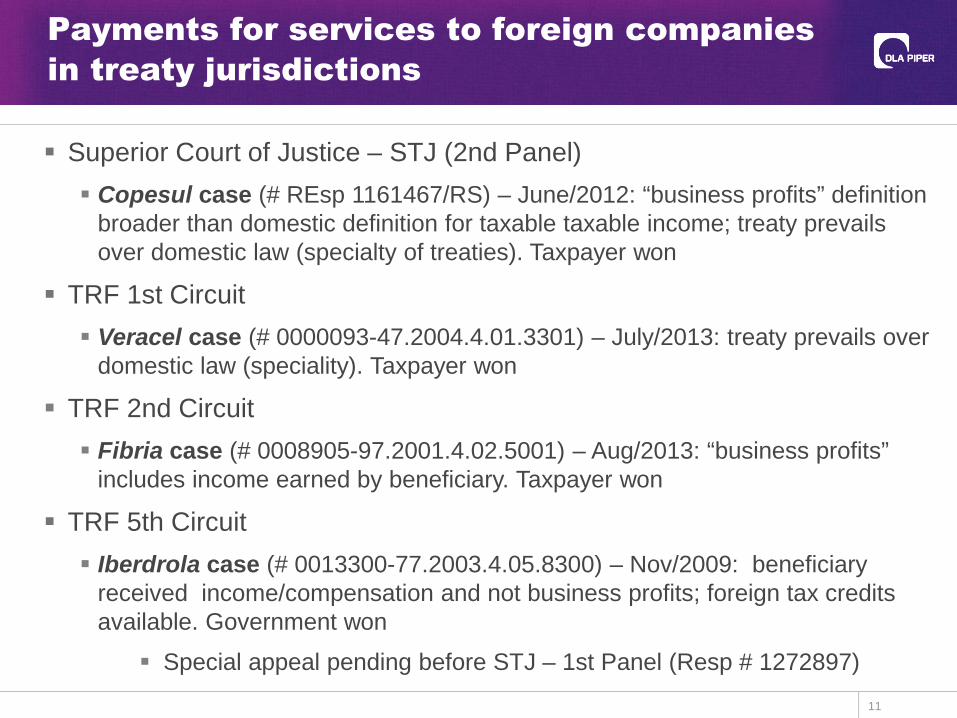

Superior Court of Justice – STJ (2nd Panel)

Copesul case (# REsp 1161467/RS) – June/2012: “business profits” definitionbroader than domestic definition for taxable taxable income; treaty prevailsover domestic law (specialty of treaties). Taxpayer won

TRF 1st Circuit

Veracel case (# 0000093-47.2004.4.01.3301) – July/2013: treaty prevails overdomestic law (speciality). Taxpayer won

TRF 2nd Circuit

Fibria case (# 0008905-97.2001.4.02.5001) – Aug/2013: “business profits”includes income earned by beneficiary. Taxpayer won

TRF 5th Circuit

Iberdrola case (# 0013300-77.2003.4.05.8300) – Nov/2009: beneficiaryreceived income/compensation and not business profits; foreign tax creditsavailable. Government won

Special appeal pending before STJ – 1st Panel (Resp # 1272897)

Payments for services performed by

foreign companies

12

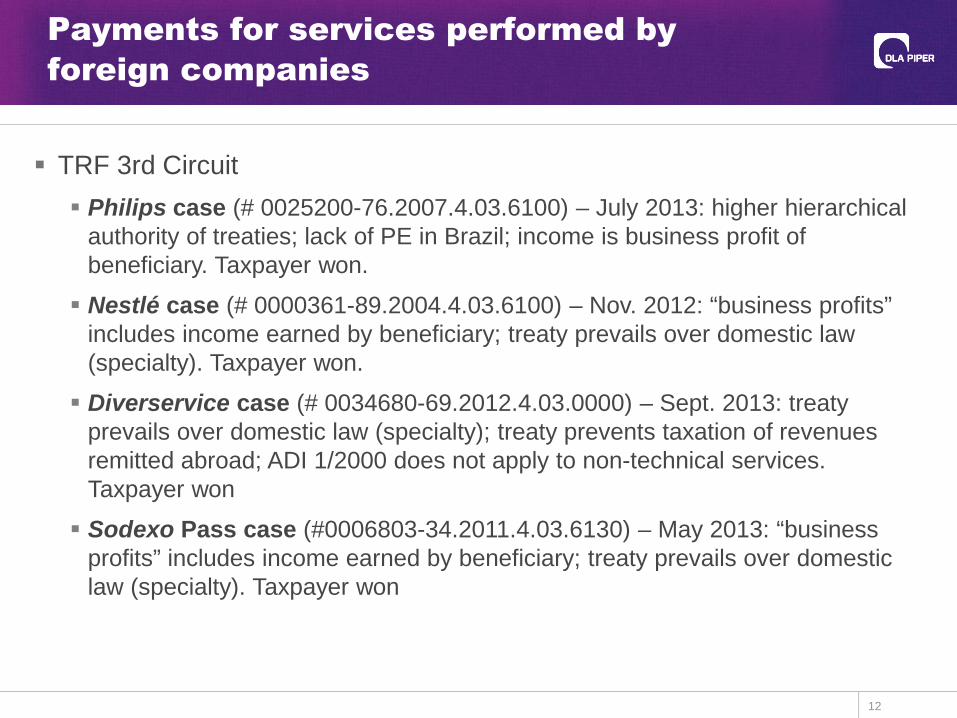

TRF 3rd Circuit

Philips case (# 0025200-76.2007.4.03.6100) – July 2013: higher hierarchicalauthority of treaties; lack of PE in Brazil; income is business profit ofbeneficiary. Taxpayer won.

Nestlé case (# 0000361-89.2004.4.03.6100) – Nov. 2012: “business profits”includes income earned by beneficiary; treaty prevails over domestic law(specialty). Taxpayer won.

Diverservice case (# 0034680-69.2012.4.03.0000) – Sept. 2013: treatyprevails over domestic law (specialty); treaty prevents taxation of revenuesremitted abroad; ADI 1/2000 does not apply to non-technical services.Taxpayer won

Sodexo Pass case (#0006803-34.2011.4.03.6130) – May 2013: “businessprofits” includes income earned by beneficiary; treaty prevails over domesticlaw (specialty). Taxpayer won

13

Leonardo HomsyCampos Mello AdvogadosAv. Almirante Barroso, 52-1202

Centro – Rio de Janiero, RJ-4578, Brazil 20031-000T +55 21 3262 3016

M +55 21 9 8240 [email protected]

www.camposmello.adv.br

Circular 230 Notice: In compliance with U.S. Treasury Regulations, please be advised that any taxadvice given herein (or in any attachment) was not intended or written to be used, and cannot

be used, for the purpose of (i) avoiding tax penalties or (ii) promoting, marketing orrecommending to another person any transaction or matter addressed herein.

RECENT DEVELOPMENTSCURRENT TAX CONTROVERSIESIN RUSSIA

Elena Zaitseva, Partner, DLA Piper – Moscow, St Petersburg

*This presentation is offered for informational purposes only; the content should not be construed as legal advice on any matter.

Contents

General Russian tax trends

Anti-tax-avoidance measures: tax dispute trends and expectedtax law amendments

Landmark tax disputes

Tax court dispute statistics

March 2013 15

General Russian tax trends

Changeable tax legislation. A number of federal laws introducingamendments to the Tax Code

Adoption of certain OECD concepts, including new transfer pricingrules effective from 2012

Previously a "form over substance" country, Russia is now a "formand substance" country

Enhancing the system of tax administration

Increasing amount of tax cases resolved in the course of theobligatory pre-trial procedures

Extensive application of domestic anti-tax-avoidance measures

Substantial developments in cross-border anti-tax-avoidancemeasures are expected soon

March 2013 16

Anti-tax-avoidance measures (1)

Both domestic and cross-border anti-tax-avoidance measures havebeen declared by the Russian government as one of the keyelements of the Russian tax strategy

The domestic anti-avoidance rules have already been developed bythe court and formalized in some major rulings of the Russian HigherArbitrazh Court

The rulings are extensively applied by tax authorities:

largely focus on the identification of fictitious/sham transactions

application of the "substance over form" and "businesspurposes" doctrines to reassess the tax consequences of thetransactions

court practice is controversial; each case requires close attentionto detail

March 2013 17

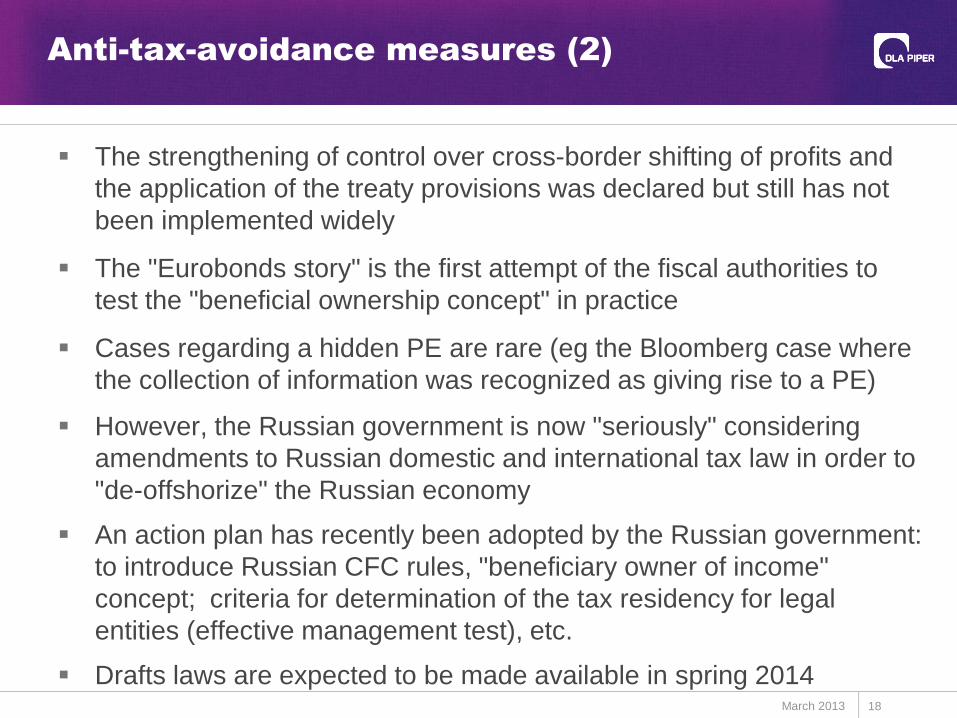

Anti-tax-avoidance measures (2)

The strengthening of control over cross-border shifting of profits andthe application of the treaty provisions was declared but still has notbeen implemented widely

The "Eurobonds story" is the first attempt of the fiscal authorities totest the "beneficial ownership concept" in practice

Cases regarding a hidden PE are rare (eg the Bloomberg case wherethe collection of information was recognized as giving rise to a PE)

However, the Russian government is now "seriously" consideringamendments to Russian domestic and international tax law in order to"de-offshorize" the Russian economy

An action plan has recently been adopted by the Russian government:to introduce Russian CFC rules, "beneficiary owner of income"concept; criteria for determination of the tax residency for legalentities (effective management test), etc.

Drafts laws are expected to be made available in spring 2014March 2013 18

Landmark disputes.

Deductibility of intra-group charges (1)

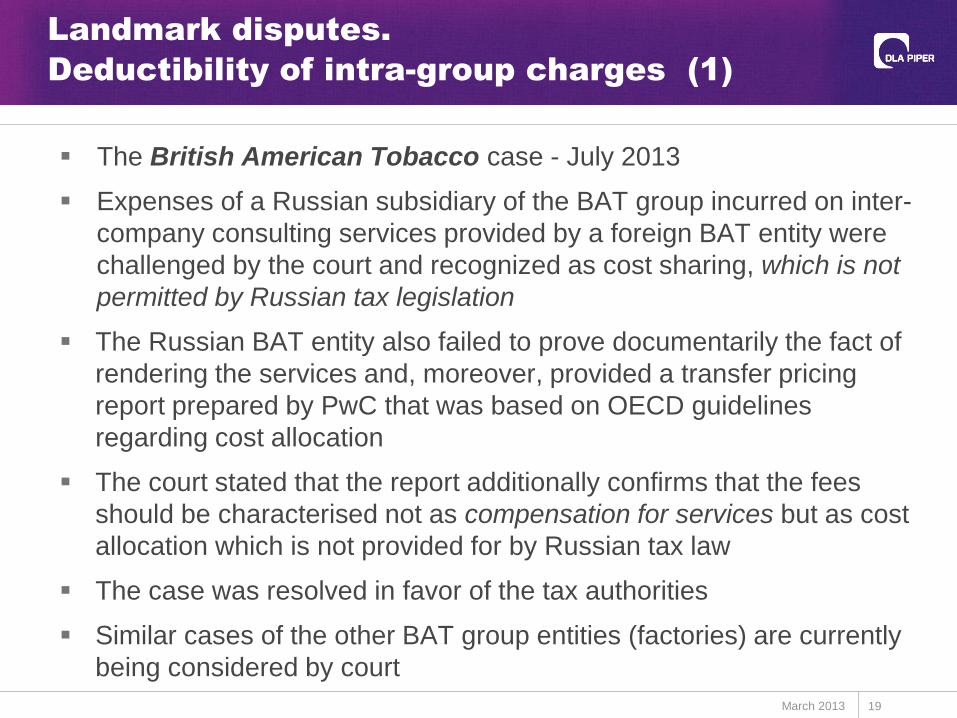

The British American Tobacco case - July 2013

Expenses of a Russian subsidiary of the BAT group incurred on inter-company consulting services provided by a foreign BAT entity werechallenged by the court and recognized as cost sharing, which is notpermitted by Russian tax legislation

The Russian BAT entity also failed to prove documentarily the fact ofrendering the services and, moreover, provided a transfer pricingreport prepared by PwC that was based on OECD guidelinesregarding cost allocation

The court stated that the report additionally confirms that the feesshould be characterised not as compensation for services but as costallocation which is not provided for by Russian tax law

The case was resolved in favor of the tax authorities

Similar cases of the other BAT group entities (factories) are currentlybeing considered by court

March 2013 19

Landmark disputes.

Deductibility of intra-group charges (2)

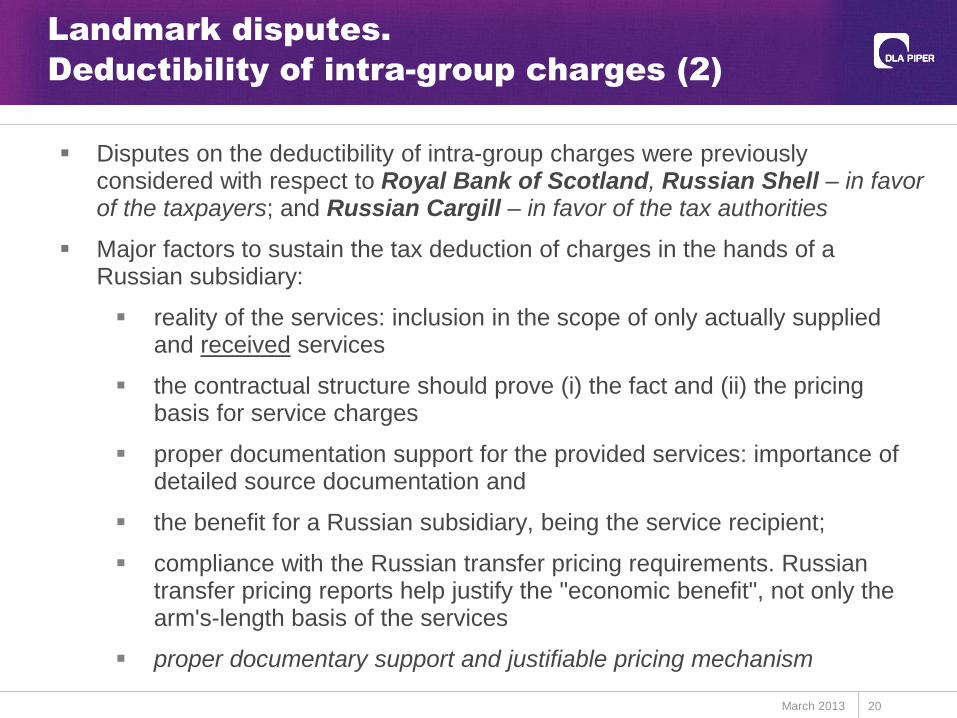

Disputes on the deductibility of intra-group charges were previouslyconsidered with respect to Royal Bank of Scotland, Russian Shell – in favorof the taxpayers; and Russian Cargill – in favor of the tax authorities

Major factors to sustain the tax deduction of charges in the hands of aRussian subsidiary:

reality of the services: inclusion in the scope of only actually suppliedand received services

the contractual structure should prove (i) the fact and (ii) the pricingbasis for service charges

proper documentation support for the provided services: importance ofdetailed source documentation and

the benefit for a Russian subsidiary, being the service recipient;

compliance with the Russian transfer pricing requirements. Russiantransfer pricing reports help justify the "economic benefit", not only thearm's-length basis of the services

proper documentary support and justifiable pricing mechanism

March 2013 20

Landmark disputes. Intra-group loans

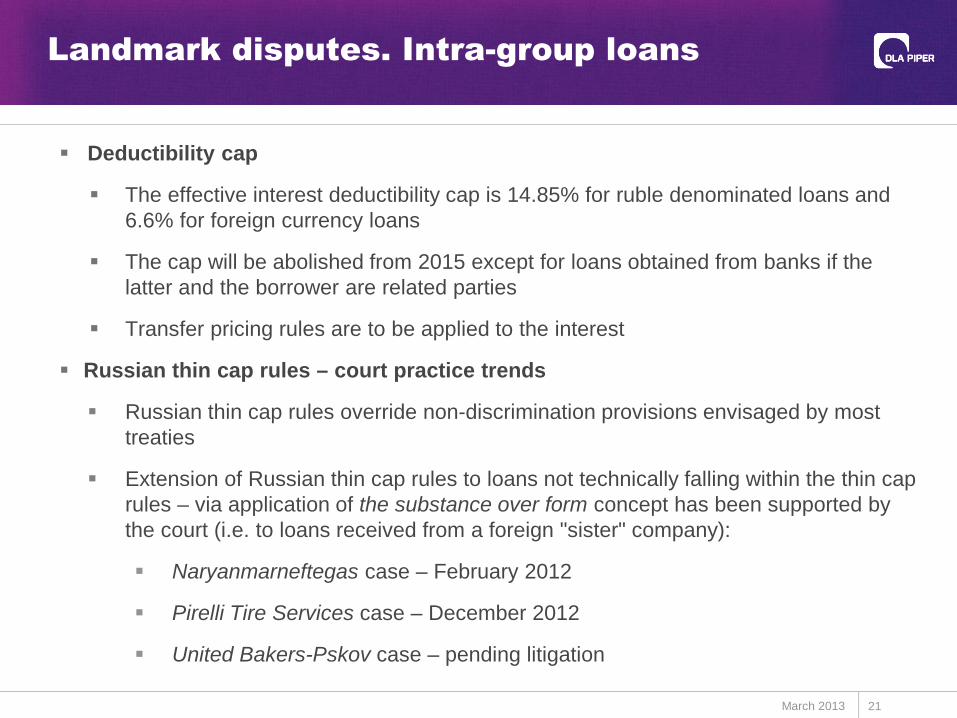

Deductibility cap

The effective interest deductibility cap is 14.85% for ruble denominated loans and6.6% for foreign currency loans

The cap will be abolished from 2015 except for loans obtained from banks if thelatter and the borrower are related parties

Transfer pricing rules are to be applied to the interest

Russian thin cap rules – court practice trends

Russian thin cap rules override non-discrimination provisions envisaged by mosttreaties

Extension of Russian thin cap rules to loans not technically falling within the thin caprules – via application of the substance over form concept has been supported bythe court (i.e. to loans received from a foreign "sister" company):

Naryanmarneftegas case – February 2012

Pirelli Tire Services case – December 2012

United Bakers-Pskov case – pending litigation

March 2013 21

Transfer pricing – expected tax disputes

for 2014 and going forward

New Russian transfer pricing rules are in force staring year 2012

Transfer pricing audits are being appointed starting December 2013

The new transfer pricing law contains a number of gray areascreating room for disputes

Numerous rulings (although not generally binding under Russian law)are being issued by the Ministry of Finance on the application of thetransfer pricing law

An extensive court practice under the new transfer pricing law isexpected for the period starting 2014

March 2013 22

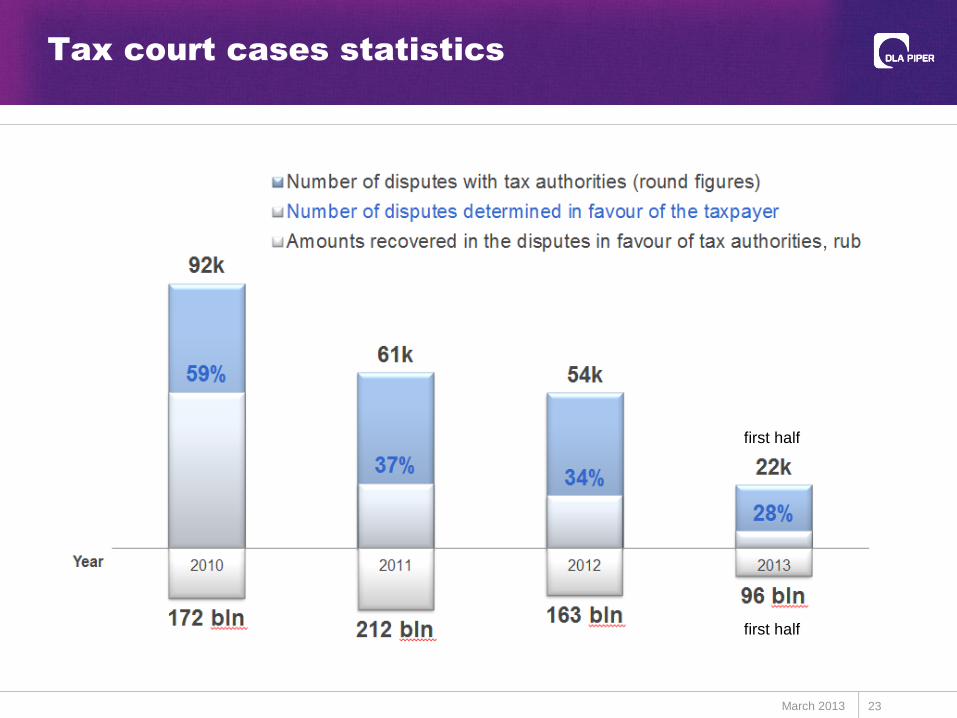

Tax court cases statistics

March 2013 23

first half

first half

March 2013 24

Elena Zaitseva, PartnerDLA Piper

25, Leontievsky per 28A Nevsky pr.Moscow St Petersburg125009 Russia 191186 RussiaOffice Phone: Office Phone:+7 495 221 44 41 +7 812 448 72 00

telephone: +7 921 951 08 [email protected]

Circular 230 Notice: In compliance with U.S. Treasury Regulations, please be advised that any taxadvice given herein (or in any attachment) was not intended or written to be used, and cannot

be used, for the purpose of (i) avoiding tax penalties or (ii) promoting, marketing orrecommending to another person any transaction or matter addressed herein.

RECENT DEVELOPMENTSCURRENT TAX CONTROVERSIESIN INDIA

Dharmesh Pandya, Partner, DLA Piper – New York

*This presentation is offered for informational purposes only; the content should not be construed as legal advice on any matter.

26

Dharmesh PandyaDLA Piper

1251 Avenue of the Americas27th Floor

New York, NY 10020T +1 650 833 2086

Circular 230 Notice: In compliance with U.S. Treasury Regulations, please be advised that any taxadvice given herein (or in any attachment) was not intended or written to be used, and cannot

be used, for the purpose of (i) avoiding tax penalties or (ii) promoting, marketing orrecommending to another person any transaction or matter addressed herein.

RECENT DEVELOPMENTSCURRENT TAX CONTROVERSIESIN CHINA

Todd Wang, Of Counsel, DLA Piper – Hong Kong

*This presentation is offered for informational purposes only, and the content should not be construed as legal advice on any matter.

Dealing with an increasingly

tough tax environment

PART I Tax Controversy

March 2013 28

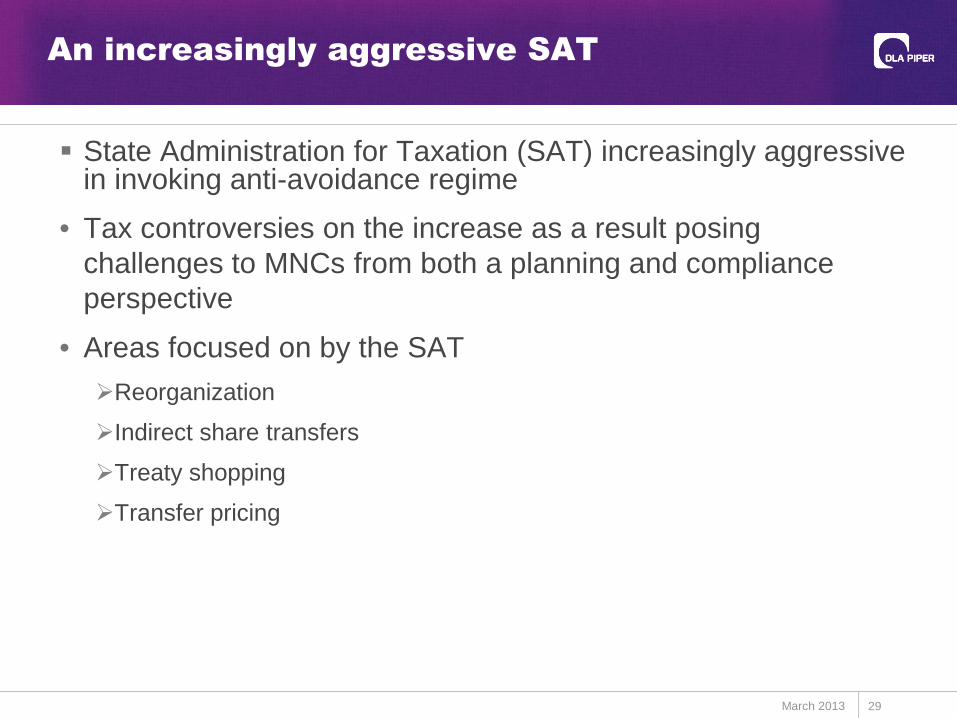

An increasingly aggressive SAT

State Administration for Taxation (SAT) increasingly aggressivein invoking anti-avoidance regime

• Tax controversies on the increase as a result posingchallenges to MNCs from both a planning and complianceperspective

• Areas focused on by the SAT

Reorganization

Indirect share transfers

Treaty shopping

Transfer pricing

March 2013 29

Anti-avoidance regime

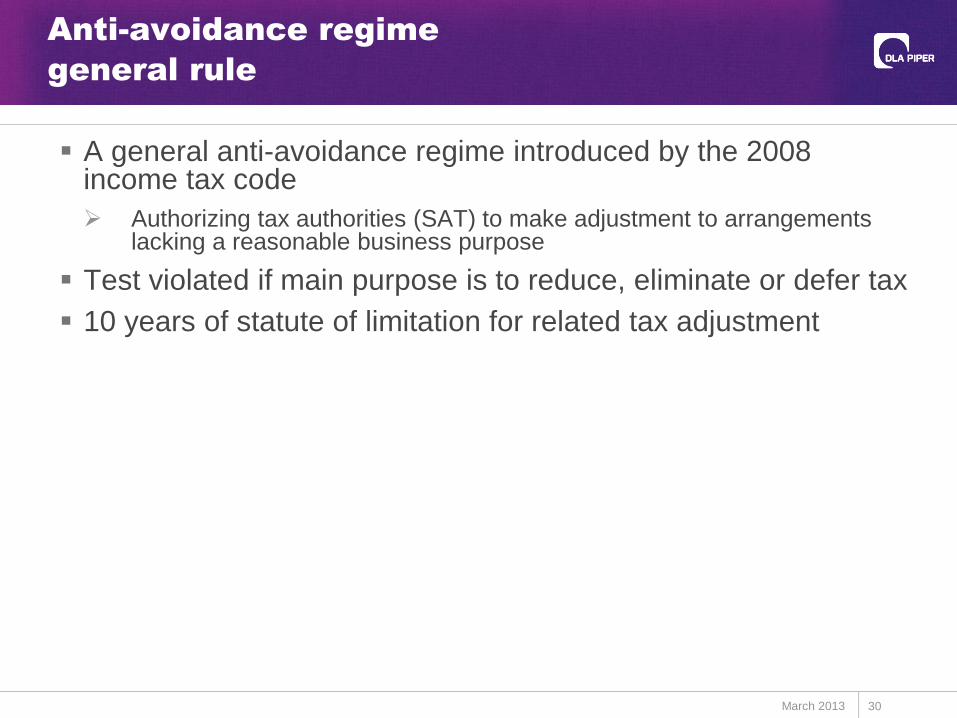

general rule

A general anti-avoidance regime introduced by the 2008income tax code

Authorizing tax authorities (SAT) to make adjustment to arrangementslacking a reasonable business purpose

Test violated if main purpose is to reduce, eliminate or defer tax

10 years of statute of limitation for related tax adjustment

March 2013 30

Anti-avoidance regime

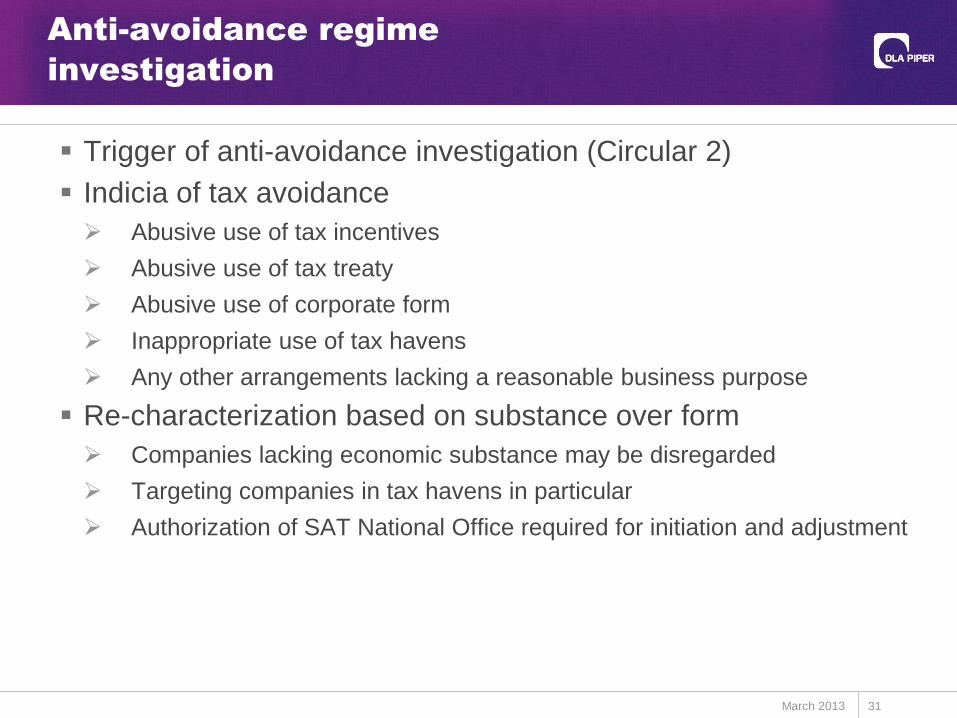

investigation

Trigger of anti-avoidance investigation (Circular 2)

Indicia of tax avoidance

Abusive use of tax incentives

Abusive use of tax treaty

Abusive use of corporate form

Inappropriate use of tax havens

Any other arrangements lacking a reasonable business purpose

Re-characterization based on substance over form

Companies lacking economic substance may be disregarded

Targeting companies in tax havens in particular

Authorization of SAT National Office required for initiation and adjustment

March 2013 31

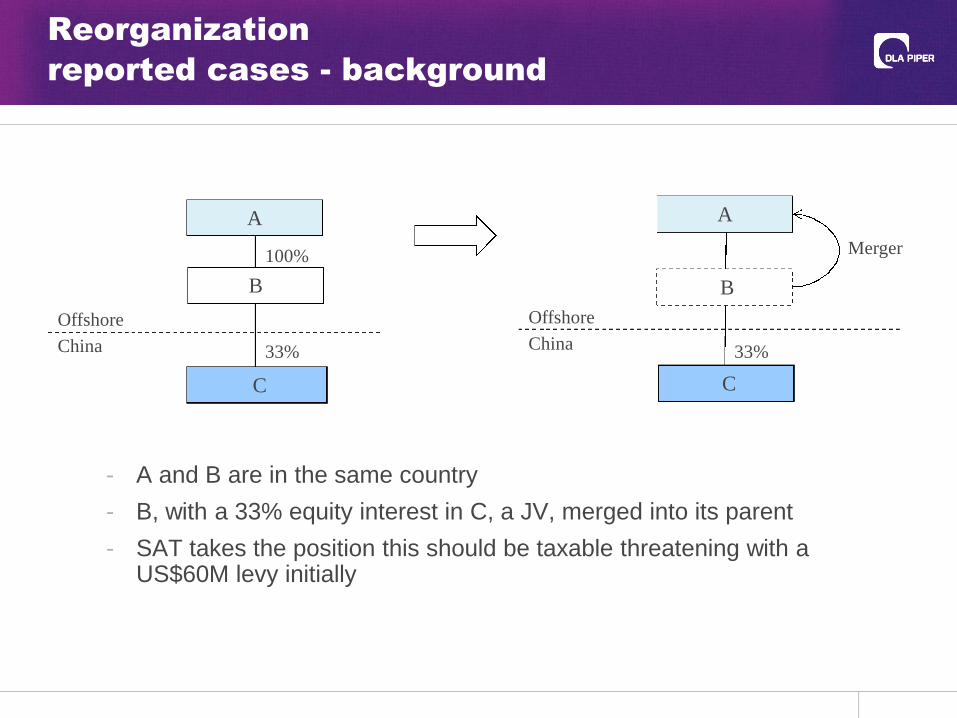

- A and B are in the same country

- B, with a 33% equity interest in C, a JV, merged into its parent

- SAT takes the position this should be taxable threatening with aUS$60M levy initially

Reorganization

reported cases - background

A

C

China

Offshore

B

China

Offshore

100%

A

C

Merger

33%

B

33%

Reorganization

reported cases – SAT's position

Circular 59 inapplicable because both parties to the mergerare foreign companies with no operations in China

Sub deemed to have disposed of its equity interest in JV toparent

Taxable value imputed based on arm's length principle

Reorganization

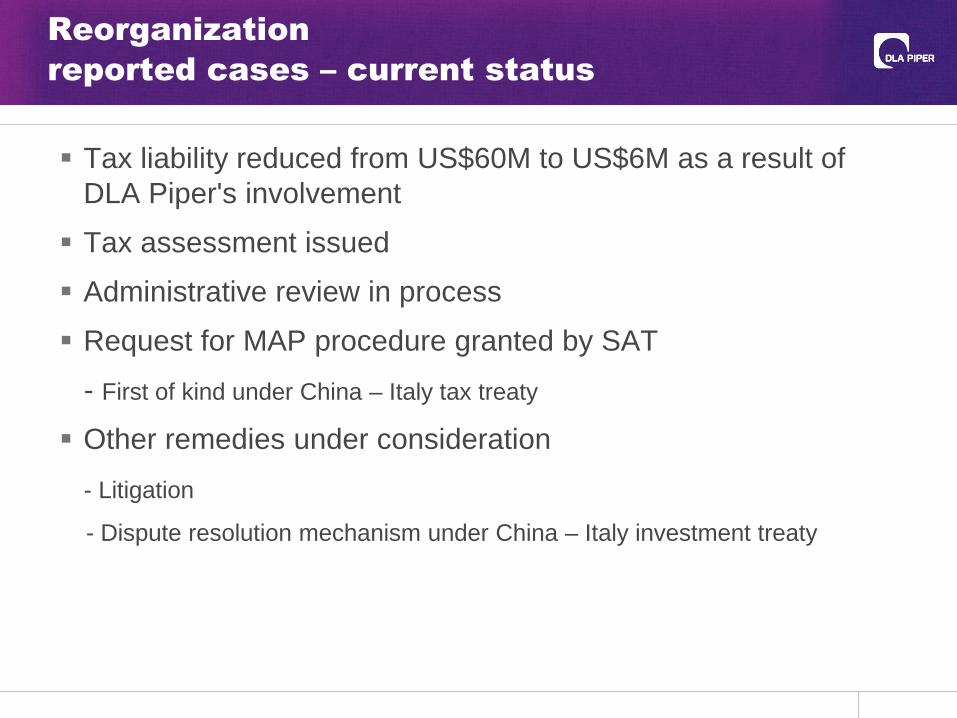

reported cases – current status

Tax liability reduced from US$60M to US$6M as a result ofDLA Piper's involvement

Tax assessment issued

Administrative review in process

Request for MAP procedure granted by SAT

- First of kind under China – Italy tax treaty

Other remedies under consideration

- Litigation

- Dispute resolution mechanism under China – Italy investment treaty

Reorganization

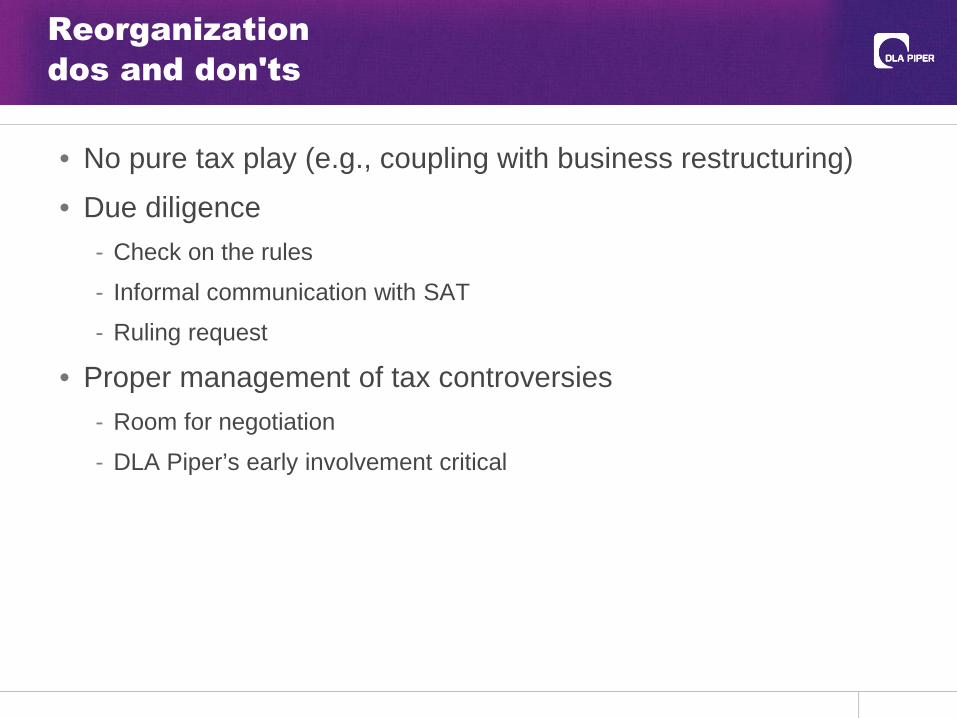

dos and don'ts

• No pure tax play (e.g., coupling with business restructuring)

• Due diligence

- Check on the rules

- Informal communication with SAT

- Ruling request

• Proper management of tax controversies

- Room for negotiation

- DLA Piper’s early involvement critical

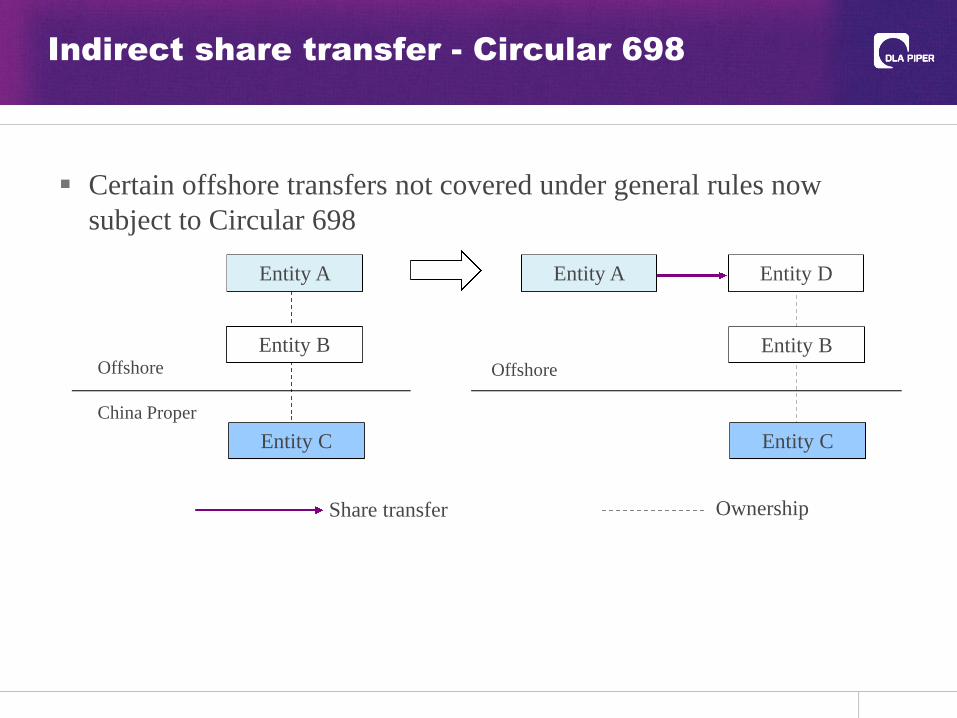

Indirect share transfer - Circular 698

Certain offshore transfers not covered under general rules nowsubject to Circular 698

Entity A Entity D

Entity C

China Proper

Offshore Offshore

Entity B

Share transfer

Entity B

Entity A

Entity C

Ownership

Indirect share transfer - Circular 698

• Reporting triggered if the transferred foreign holding companylocated in a tax jurisdiction which:

does not tax capital gains so realized or

has an effective tax rate of less than 12.5 percent

• Extensive disclosures required within 30 days:

Transfer agreement

Info on relationship between transferor and transferred holding companyre financing, business operations, and purchase/sales

Info on holding company, e.g., business operations, personnel, finance,assets

Info on relationship between holding company and Chinese sub

Business purpose for setting up holding company initially

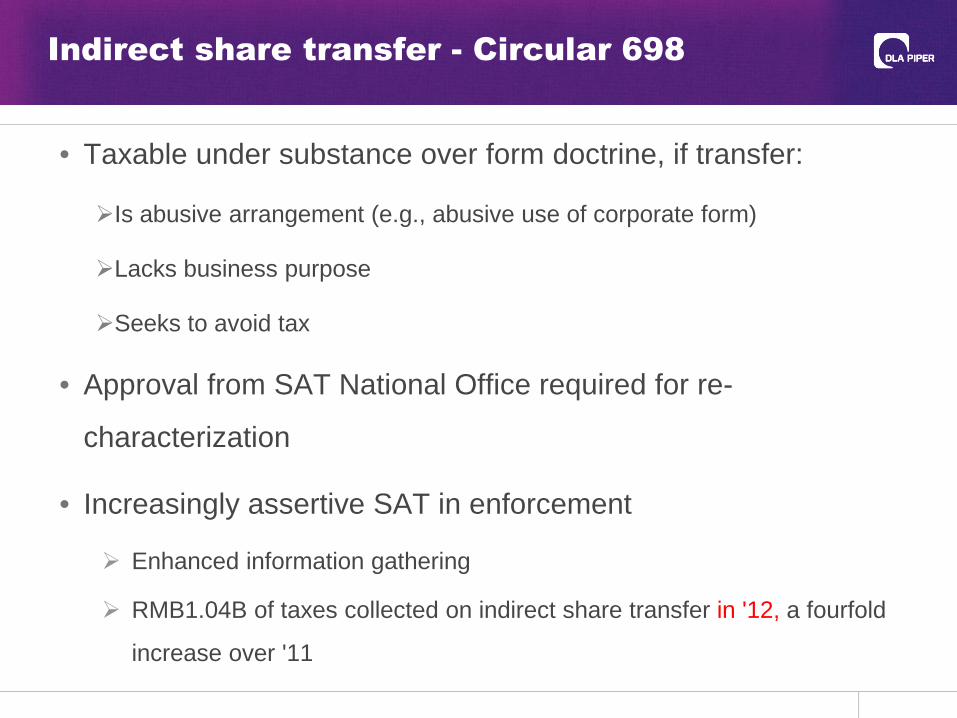

Indirect share transfer - Circular 698

• Taxable under substance over form doctrine, if transfer:

Is abusive arrangement (e.g., abusive use of corporate form)

Lacks business purpose

Seeks to avoid tax

• Approval from SAT National Office required for re-

characterization

• Increasingly assertive SAT in enforcement

Enhanced information gathering

RMB1.04B of taxes collected on indirect share transfer in '12, a fourfold

increase over '11

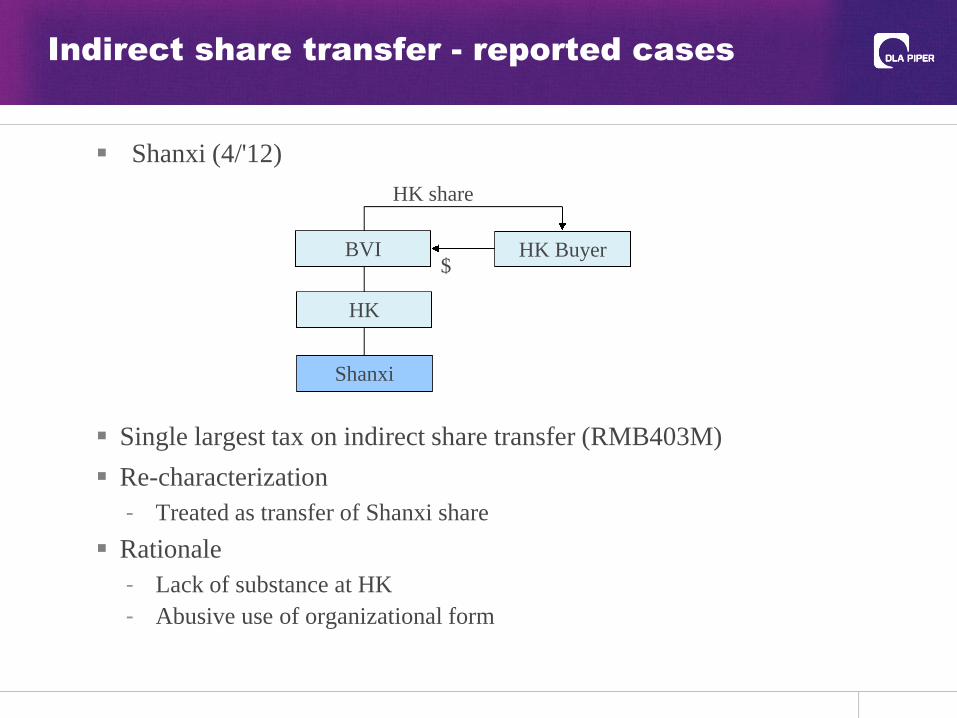

Indirect share transfer - reported cases

Shanxi (4/'12)

Single largest tax on indirect share transfer (RMB403M)

Re-characterization

- Treated as transfer of Shanxi share

Rationale

- Lack of substance at HK

- Abusive use of organizational form

HK share

$

Shanxi

HK

BVI HK Buyer

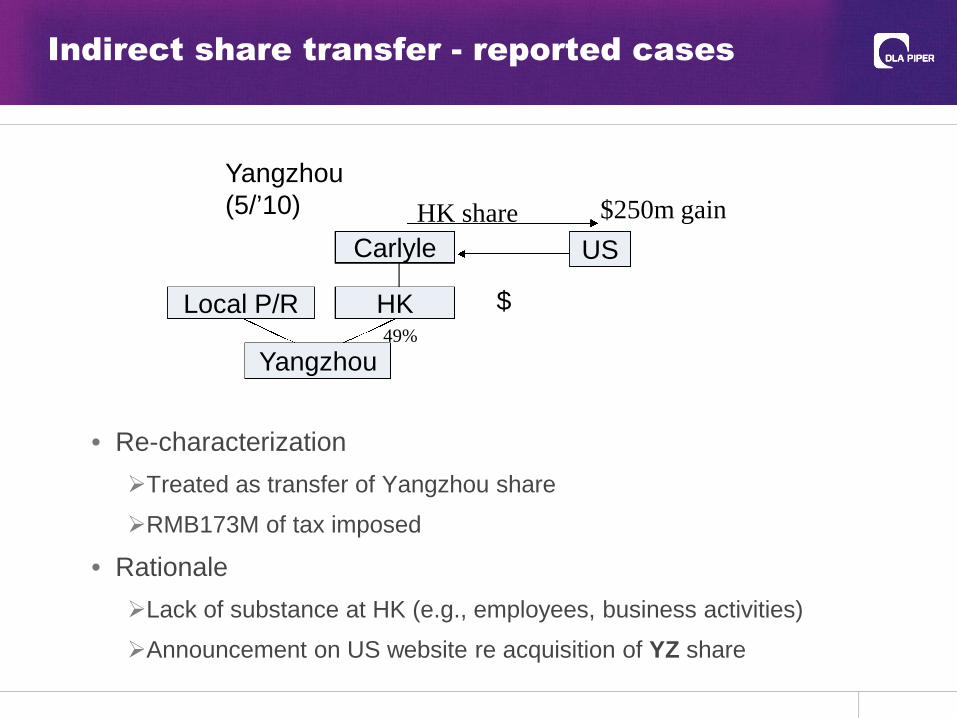

Indirect share transfer - reported cases

• Re-characterization

Treated as transfer of Yangzhou share

RMB173M of tax imposed

• Rationale

Lack of substance at HK (e.g., employees, business activities)

Announcement on US website re acquisition of YZ share

Carlyle

HK

HK share

US

$

$250m gain

Yangzhou(5/’10)

Local P/R

Yangzhou49%

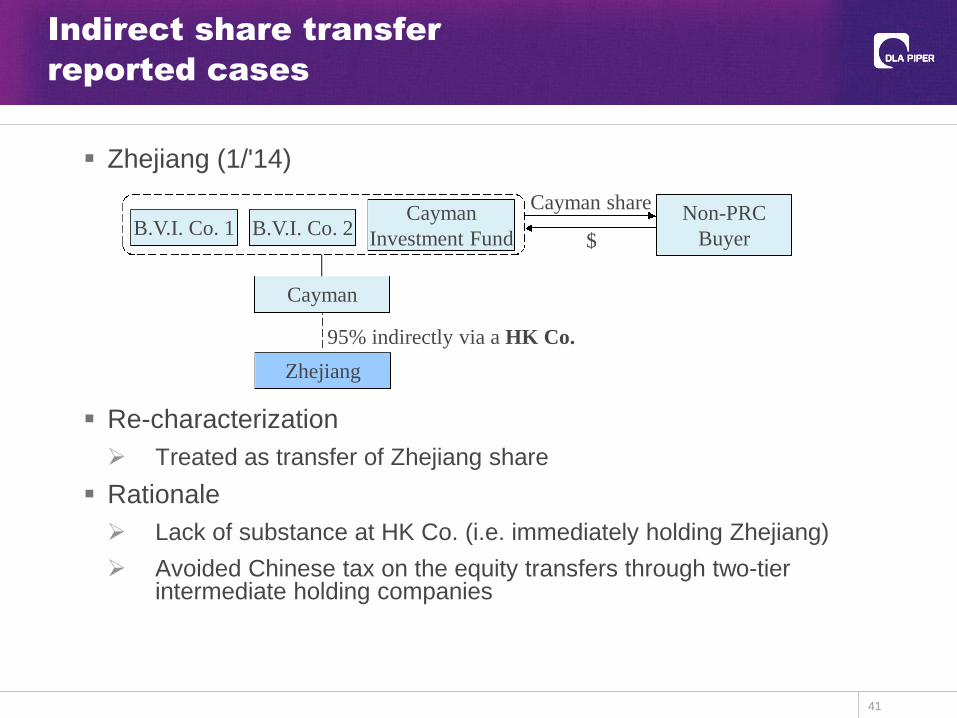

Zhejiang (1/'14)

Re-characterization

Treated as transfer of Zhejiang share

Rationale

Lack of substance at HK Co. (i.e. immediately holding Zhejiang)

Avoided Chinese tax on the equity transfers through two-tierintermediate holding companies

41

Cayman share

$

Zhejiang

Non-PRCBuyer

Indirect share transfer

reported cases

B.V.I. Co. 1Cayman

Investment FundB.V.I. Co. 2

95% indirectly via a HK Co.

Cayman

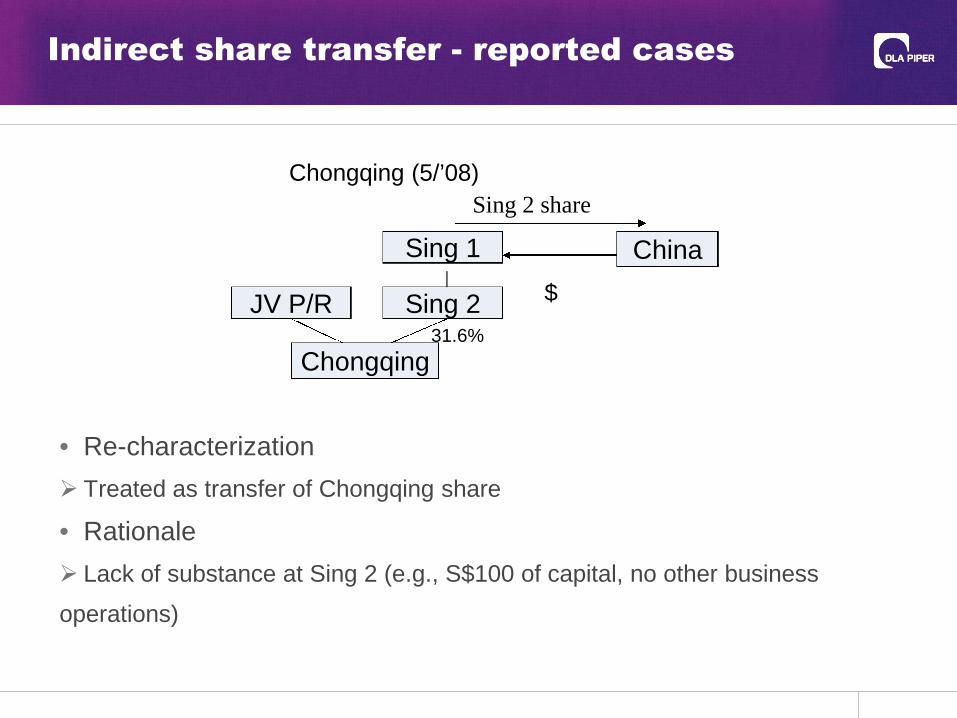

Indirect share transfer - reported cases

• Re-characterization

Treated as transfer of Chongqing share

• Rationale

Lack of substance at Sing 2 (e.g., S$100 of capital, no other business

operations)

Sing 1

Sing 2

Sing 2 share

China

$

Chongqing (5/’08)

JV P/R

Chongqing31.6%

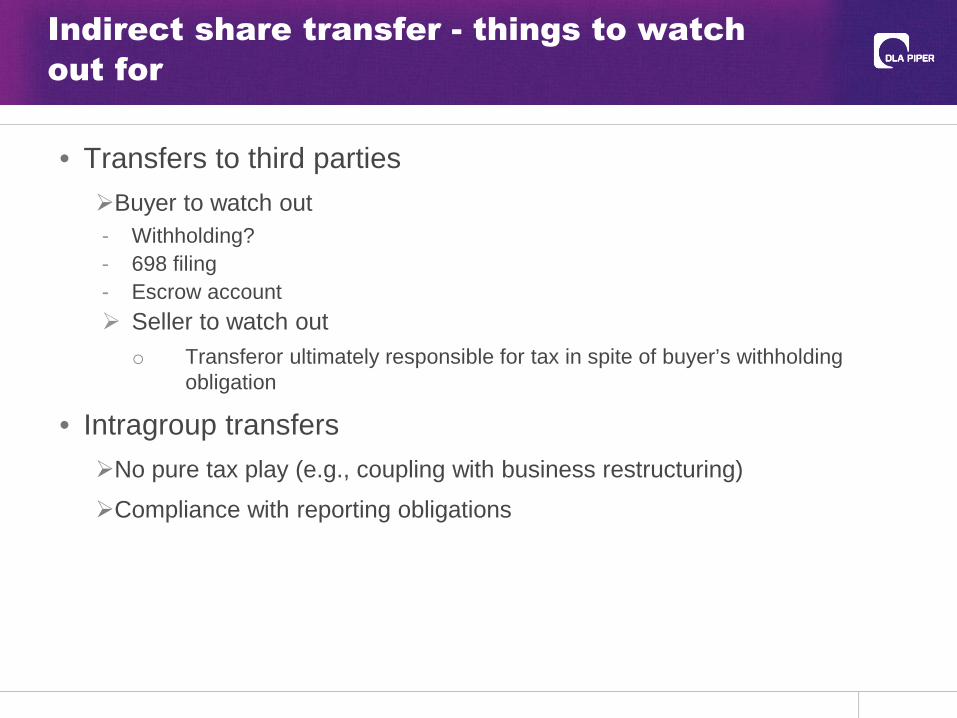

Indirect share transfer - things to watch

out for

• Transfers to third parties

Buyer to watch out

- Withholding?

- 698 filing

- Escrow account

Seller to watch out

o Transferor ultimately responsible for tax in spite of buyer’s withholdingobligation

• Intragroup transfers

No pure tax play (e.g., coupling with business restructuring)

Compliance with reporting obligations

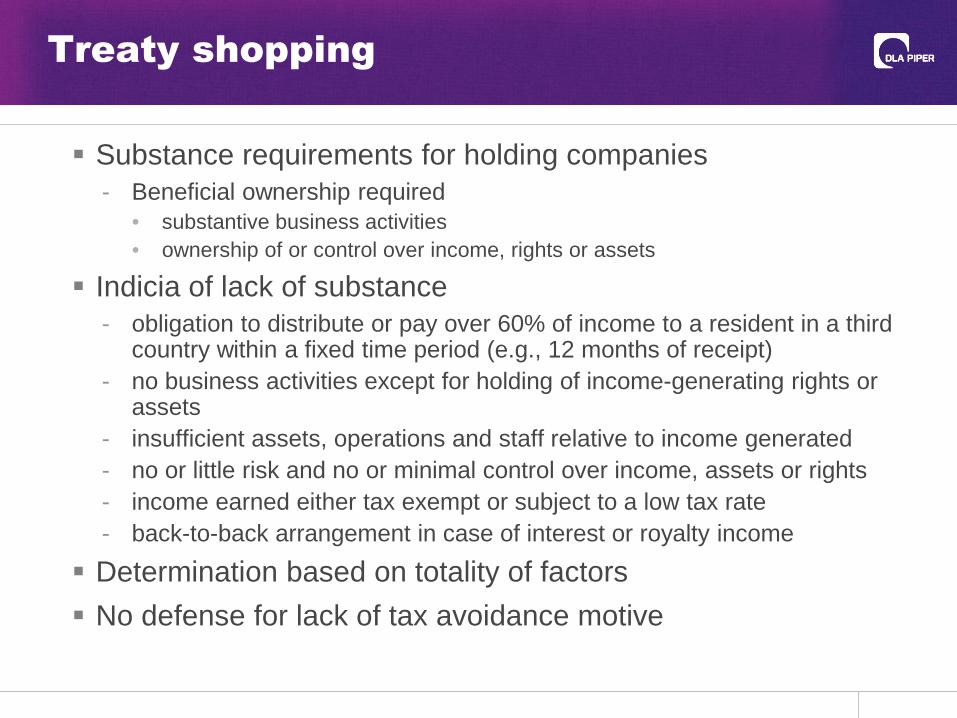

Treaty shopping

Substance requirements for holding companies- Beneficial ownership required

• substantive business activities

• ownership of or control over income, rights or assets

Indicia of lack of substance- obligation to distribute or pay over 60% of income to a resident in a third

country within a fixed time period (e.g., 12 months of receipt)

- no business activities except for holding of income-generating rights orassets

- insufficient assets, operations and staff relative to income generated

- no or little risk and no or minimal control over income, assets or rights

- income earned either tax exempt or subject to a low tax rate

- back-to-back arrangement in case of interest or royalty income

Determination based on totality of factors

No defense for lack of tax avoidance motive

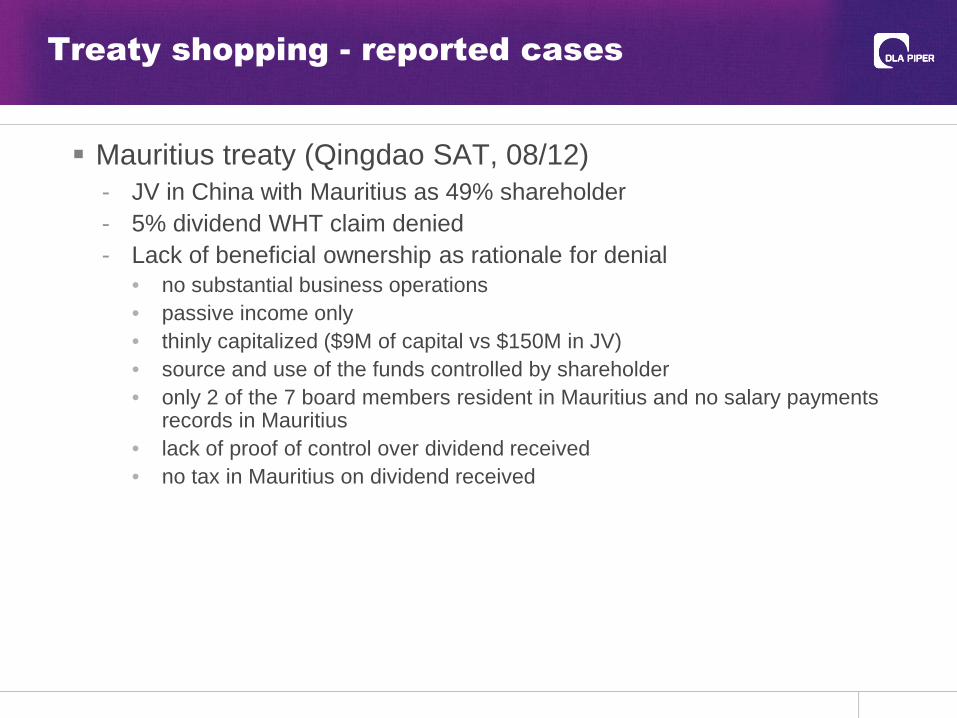

Treaty shopping - reported cases

Mauritius treaty (Qingdao SAT, 08/12)- JV in China with Mauritius as 49% shareholder

- 5% dividend WHT claim denied

- Lack of beneficial ownership as rationale for denial• no substantial business operations

• passive income only

• thinly capitalized ($9M of capital vs $150M in JV)

• source and use of the funds controlled by shareholder

• only 2 of the 7 board members resident in Mauritius and no salary paymentsrecords in Mauritius

• lack of proof of control over dividend received

• no tax in Mauritius on dividend received

Dealing with an increasingly

tough tax environment

PART II Transfer Pricing

March 2013 46

Transfer pricing – documentation

Annual documentation now a regular practice around the nation

Local tax authority now expect and emphasize on:

"record of the transfer pricing decision making process and underlyingreasoning," rather than "justification of inter-company transaction result"

better details of global and China business operation, especially thebusiness connection between China and overseas principal

higher quality of functional and risk analysis

substance over form principle, and reasonable business purpose

election of most appropriate transfer pricing valuation method

balance of functions, risk and profit

inclusion of internal comparable analysis and historical analysis

analysis of contribution to the group's revenue and profit

"Simultaneous" vs. “annual" practice

March 2013 47

Transfer pricing – audit

Continuous increase of audit cases and adjustment amount

Focus on big MNC in East Coast and first-layer cities

Picking up of audit cases and practice in western China, and second-layercities

Growing attention to intangible transactions, services and financing

"Pilot TP audit cases" in southern China

o Chapter 10 of the United Nations' Practical Manual on Transfer Pricing forDeveloping Countries (the Paper), 2012. Making a difference from the OECDdoctrine

o Under-evaluation of Local Special Advantages (especially regional cost saving effectand market premium)

o Under-evaluation of local intangibles

o Alternatives to traditional transaction net margin method

o Challenges against traditional TP arrangement for contract R&D, and tollmanufacturing

First audit case with "Specialist Panel," precedence for high value and highlycontroversial TP audit cases

March 2013 48

Transfer pricing - audit

First TP audit against Representative Office of Foreign Enterprises

First overseas on-site investigation in the name of "authorized visitingrepresentative"

Development of inter-company transaction database at local level

The last G20 country that sign on the Convention on Mutual AdministrationAssistance in Tax Matters

o Tax information exchange

o Offshore collection of short paid taxes

o Assistance in provision of relevant legal documents

Transfer pricing – 2013 audit cases

The first TP audit case with adjustment based on "RegionalCost Saving"

Taxpayer: evolved from a single function manufacturer to a multi-functionenterprises with R&D, manufacturing and other operation functions

Tax authority: Guangzhou SAT, Guangdong Province

The case

o SAT - Regional Cost Saving identified based on comparison of different cost factors(salary, facilities, energy, working hours) associated with the relocation of R&Dfunctions

o Taxpayer – Regional Cost Saving is offset by relocation cost, fixed assetinvestment, training and support expenses

o Tax adjustment imposed based on [Cost Saving x arm's length return rate xEnterprise Income Tax rate]

o Additional tax paid, RMB 50 million over 3 years

March 2013 50

Transfer pricing – 2013 audit cases

TP audit cases against traditional toll manufacturing arrangement

Taxpayers: Electronic manufacturers changes their business model fromcontract manufacturing to toll manufacturing, with service fee calculated basedon [labor cost + operating expenses] x (1 + 3% ~ 10%), which reduces theprofit left in China

Tax authority: Suzhou, Wuxi and Guangdong SAT

The case:

Taxpayer –

o The toll factory does not bear inventory or risk, and the mark up range (3~ 10%) isdirectly supported by benchmarking based on comparable contract manufacturers

SAT –

o There is no substantial difference between toll manufacturing and contractmanufacturing, in term of business operation and function

o The difference is limited to funding needs for inventory

o Toll manufacturers should earn a profit close to [(COGs + operation expenses) xarm's length return for contract manufacturers] – Interest for inventory funding]

Tax adjustment imposed, and COGs determined with reference to customs records

March 2013 51

Transfer pricing – 2013 audit cases

The "biggest" TP audit adjustment

Taxpayer: Subsidiaries of Fortune 500, with increasing revenue butdecreasing profit from 2004 to 2013, and significant service fee payment tooverseas service center

Tax authority: Xiamen SAT, Fujian Province

The case

Global shared service cost pooled in Singapore service center based on number ofemployees, but then further allocated to China subsidiaries based on revenue

Some of the service costs are related to overseas parent company's managementrole and with no benefit to the China subsidiaries

China subsidiaries are not entitled to the IP created through the shared services

Additional tax payment about $72 million, and late payment interest about $12.9million

March 2013 52

Transfer pricing – 2013 audit cases

TP adjustment based on profit split method

Taxpayer: Clothing distributor, dealing with wholesale and retail of clothesimported from overseas affiliates

Tax authority: Shenzhen SAT, Guangdong Province

The case

o Taxpayer - apply for huge service fee payment to overseas parent / service center

o SAT

• conduct detailed survey over the taxpayer's business operation and value train

• service fee payment short of business substance and inconsistent with theidentified business operation

• overseas affiliates' involvement and investment in China market is limited

• local marketing intangibles are created but not properly compensated

o Profit split method used for tax adjustment, additional income tax and late paymentinterest totaled $2.3 million

March 2013 53

Transfer pricing - APA

SAT continues to encourage APA in 2012 and 2013

More bilateral APA than unilateral APA (9 vs. 3 concluded in 2012)

Average time cost at about 2 years

Over 50% APA in manufacturing industry, while expansion to IT,software and information technologies

Continuous increase of APA application in the pipeline (140+reported)

Increase in APA over intangible, service and financial inter-companytransactions

SAT criteria for APA application

o Timing of application

o Quality of application documents

o Special industrial and regional features

o Importance and attention of competent authority

March 2013 55

Todd WangDLA Piper

17th Floor, Edinburgh TowerThe Landmark

15 Queensroad, CentralHong Kong

Office Phone +852 2103 [email protected]

Circular 230 Notice: In compliance with U.S. Treasury Regulations, please be advised that any taxadvice given herein (or in any attachment) was not intended or written to be used, and cannot

be used, for the purpose of (i) avoiding tax penalties or (ii) promoting, marketing orrecommending to another person any transaction or matter addressed herein.