-

7/31/2019 Recruitment of Advisors in Icici

1/77

A SUMER INTERNSHIP REPORT

ON

RECRUITMENT OF ADVISORS IN ICICI

PRUDENTIAL LIFE INSURANCE

For the partial fulfillment of the requirement for theAward of

the degree of

BACHOLAR OF BUSINESS ADMINISTRATIONRoll no- 8423548

Submitted By:

JYOTI RANI

-

7/31/2019 Recruitment of Advisors in Icici

2/77

JAIPURIYA INSTITUTE OF MANAGEMENTGAZIABAD, UP

-

7/31/2019 Recruitment of Advisors in Icici

3/77

ACKNOWLEDGEMENT

This project has been prepared after lots of analysis and

efforts. I gratefully

acknowledge with due courtesy the sources consulted in the

preparation of

this project. I express my sincere gratitude to Mr. Padam Singh

(Sr. Agency

Manager) ICICI Prudential for giving me an opportunity to work

in the HR

department. I am thankful to his valuable guidance, advice,

critical reviews,

acknowledgment and association throughout the preparation of

this report.

No work is complete in itself without credits being given to the

persons who

help in achieving a desired task. I feel privileged to thank all

those people

who have directly or indirectly contributed to the completion of

this project.

JYOTI RANI

-

7/31/2019 Recruitment of Advisors in Icici

4/77

CONTENT

S.No. Topic Page No.1. Executive Summary 1

2. Meaning of Insurance 2

3. Insurance Industry 6

4. Global Insurance Industry 7

5. Insurance Market in India 12

6. Facts of Life Insurance Industry 167. Life Insurance Market

in India 19

8. Company profile - About ICICI Prudential 25

9. Nature of Job as a Trainee 43

10. Objectives of the Study 54

11. Research Methodology 55

Limitations of The Study 57

12. Analysis and Findings 58

Questionnaire Analysis 64

SWOT Analysis 68

Conclusion 69

13. Recommendations 71

Bibliography 72

14. Appendix Questionnaire 73

-

7/31/2019 Recruitment of Advisors in Icici

5/77

EXECUTIVE SUMMARY

The objective of this project was to assist ICICI Prudential

Life Insurance in expanding

their channel by recruiting Tied Agents/ Advisors for the

company. For the company tosuccessfully continue its operations, it

needs to undergo change to get new business and to

get new ideas. Moreover insurance is such a growing sector that

it has full potential to have

new customers. So it is very essential to have new people in the

system, which can add new

customers to the company.

This was achieved through a five-pronged effort. The first

objective of the study was to

look for different segments of the people. The second objective

of the project was to

analyze the person to find whether he is fit for doing

insurance. The third objective of the

project was to finally introduce some people in the system by

recruiting them as advisors of

the company.

The research methodology consisted of secondary data, which was

collected from different

colleges , Tata Press Yellow Pages etc and personal interview

with people in Delhi .

1

-

7/31/2019 Recruitment of Advisors in Icici

6/77

MEANING OF INSURANCE

Insurance or assurance i s device for indemnify ing or

guaranteeing an

individual against loss. Reimbursement is made from a fund to

which manyindividuals exposed to the same r isk have contr ibuted

certain specif ied

amounts, called premiums. Payment for an individual loss,

divided among

many, does not fa l l heavily upon the ac tual loser. The

essence of the

contract of insurance, called a policy, is mutuality.

The ent i ty that is t ransferr ing the r isk which may be an

individual or

association of any type, including a government or government

agency is

cal led the "insured". The ent ity accepting the r isk is cal

led the "insurer" .

The agreement between the two by which the r isk is t ransferred

is cal led

the "pol icy" : th is i s a lega l contract that sets out exact

ly the terms and

conditions of the coverage. The fee paid by the insured to the

insurer for

assuming the r isk is cal led the "premium". This is usual ly

determined by

the insurer to fund estimated future claims paid, administrative

costs, and

pro fit .

For example, let us assume that a couple buys a home costing

$100,000.

Knowing that the loss of their home would bring them financial

ruin, they

acqui re insurance coverage in the form of a homeowner' s

policy. That

poli cy wi ll pay th em the cost of replacing or repairing th

eir home in the

event of a catastrophe. The insurance company charges them a

premium of

$1,000 a year. Risk of loss has been transferred from the

homeowners to

the insurance company.

The major opera tions of an insurance company are underwri ting,

the

determination of which risks the insurer can take on; and rate

making, the

decisions regarding necessary prices for such r isks. The

underwriter is

r espons ib le for gua rd ing aga inst adver se sel ec tion ,

where in the re i s

2

http://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Government&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Government+agency&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Contract&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Fee&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Administration&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Profit&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Home&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Dollar&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Government&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Government+agency&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Contract&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Fee&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Administration&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Profit&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Home&gwp=8&curtab=2222_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2222&dekey=Dollar&gwp=8&curtab=2222_1&sbid=lc03a

-

7/31/2019 Recruitment of Advisors in Icici

7/77

excessive coverage of high risk candidates in proportion to the

coverage of

low risk candidates. In preventing adverse selection, the

underwriter must

conside r physi ca l, p sycholog ical , and moral hazards in r

el at ion to

applicants. Phys ica l hazards include those dangers which

surround the

individual or property, jeopardizing the well-being of the

insured. The

amoun t o f t he p remium i s det ermined by the ope ra tion o f

t he l aw o f

averages as calculated by actuaries . By invest ing premium

payments in a

wide range of revenue-producing projects, insurance companies

have

become major suppli ers of capital, an d th ey rank among th e

nation's largest

institutional investors.

COMMON TYPES OF INSURANCE

Life insurance , or iginal ly conceived to protect a man's

family when his

dea th le f t them wi thout income, has developed in to a var ie

ty of pol icy

plans.

In a whole life policy, fixed premiums are paid throughout

the

insured ' s l if et ime; t hi s accumulat ed amoun t, augmented

by

compound interest , is paid to a beneficiary in a lump sum

uponthe insured ' s dea th ; the benef i t i s pa id even i f the

insured had

terminated the policy.

Under un iver sa l l if e, t he insured can vary the amoun t

and

timing of the premiums; the funds compound to create the

death

benefit.

With va ri ab le l if e, t he f ixed p remiums a re inves ted in

a

portfolio (with earning reinvested), and the death benefit is

based

on the performance of the investment.

In term life, coverage is for a specified time period (e.g.,

510

years); such plans do not build up value during the term.

Annuity

poli cies, which pay the insu red a yearly income after a

certain

3

-

7/31/2019 Recruitment of Advisors in Icici

8/77

age , have a lso been developed . In the 1990s , l if e i

nsurance

companies began to allow early payouts to terminally ill

patients.

Fire insurance usually includes damage from lightning; other

insurance

against the elements includes hail, tornado, flood, and

drought.

Automob ile insurance includes not only insurance against fire

and theft but

a lso compensa t ion for damage to the car and for personal in

jury to the

vict im of an accident ( l iab il ity insurance) ; many car

owners , however,

c ar ry o nl y p ar ti al i ns ur an ce . In m an y s ta te s l

ia bi li ty i ns ur an ce i s

compulsory, and a number of s ta tes have inst itu ted so-ca

lled no-fault

insurance plans, whereby automobile accident victims receive

compensationwi thout having to in it ia te a l iab i li ty lawsuit

, except in spec ial cases .

Bonding, or fidelity insurance, is designed to protect an

employer against

dishonesty or default on the part of an employee.

Tit le insurance i s a imed a t p ro tect ing purchaser s o f r

ea l e st at e f rom

loss by reason of defective title.

Credit insurance safeguards businesses against loss from the fai

lure of

customers to meet their obligations.

Marine insurance protects shipping companies against the loss of

a ship or

i ts cargo , a s wel l a s many o ther i tems , and so-ca ll ed

inl and mar ine

insurance covers a vast miscel lany of i tems, including touris

t baggage,

express and parcel-post packages, truck cargoes, goods in

transit , and even

bridges and tunnels. In recent yea rs, the insu rance industry

has broadened

to guard against almost any conceivable risk; companies like

Lloyd's will

insure a dancer's legs, a pianist 's fingers, or an outdoor

event against loss

from rain on a specified day.

4

http://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2040&dekey=nofaulti&gwp=8&curtab=2040_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2040&dekey=nofaulti&gwp=8&curtab=2040_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2040&dekey=nofaulti&gwp=8&curtab=2040_1&sbid=lc03ahttp://www.answers.com/main/ntquery;jsessionid=a84rtjlumhgtd?method=4&dsid=2040&dekey=nofaulti&gwp=8&curtab=2040_1&sbid=lc03a

-

7/31/2019 Recruitment of Advisors in Icici

9/77

Insurance in brief:

Insurance is a method of spreading & transfer of risk.

Losses of unfortunate few are shared by and spread over to many

exposed to same

risk.

Assets created by the owner in expectation of future needs or

benefits have value.

Loss of assets for any reasons deprives the owner of the

expected benefits.

Insurance in this context is a mechanism that helps to reduce

the adverse

consequences due to loss of assets.

5

-

7/31/2019 Recruitment of Advisors in Icici

10/77

THE INSURANCE INDUSTRY

The insurance indus try forms an in tegra l part of the g lobal

f inancia l

market, with insurance companies being significant institutional

investors.In recent decades, the insurance sector, l ike other f

inancial services, has

grown in economic importance. This is through direct contr

ibutions to

gross domestic product (GDP) via increased levels of employment

within

the sec to r; and ind ir ec tly t hrough h ighe r l evel s o f r

isk t rans fe r and

financial intermediation.

Expanding further on this issue, it must be remembered that the

insurance

industrys primary function is to supply individuals and

businesses with

coverage against specified contingencies.

Insurance companies, therefore, engage in underwrit ing,

managing, and

financing risks. According to Sigma (2001) the largest insurance

sectors are

to be found in the U.S. and Japan, which together generates more

than fifty

percent of global premium income; followed by th e UK, Germany,

France

and Italy. Furthermore, during the last four decades the global

insurancesector has on average outpaced global economic growth.

Between 1984 and

2001, the global insurance industry grew at an overall rate of

483.6 percent

(roughly comprising of 664.8 percent from the l i fe insurance

sector, and

334.3 percent f rom the non- l ife sec tor. The l ife insurance

sector, has

continued to grow at a fast rate.

6

-

7/31/2019 Recruitment of Advisors in Icici

11/77

THE GLOBAL INSURANCE INDUSTRY

The insurance indus try forms an in tegra l part of the g lobal

f inancia l

market, with insurance companies being significant institutional

investors.In recent decades, the insurance sector, l ike other f

inancial services, has

grown in economic importance. This is through direct contr

ibutions to

gross domestic product (GDP) via increased levels of employment

within

the sec to r; and ind ir ec tly t hrough h ighe r l evel s o f r

isk t rans fe r and

financial intermediation.

Expanding further on this issue, it must be remembered that the

insurance

industrys primary function is to supply individuals and

businesses with

coverage against specified contingencies.

Insurance companies, therefore, engage in underwriting,

managing, and financing risks.

According to Sigma (2001) the largest insurance sectors are to

be found in the U.S. and

Japan, which together generates more than fifty percent of

global premium income;

followed by the UK, Germany, France and Italy. Furthermore,

during the last four decades

the global insurance sector has on average outpaced global

economic growth. Between1984 and 2001, the global insurance

industry grew at an overall rate of 483.6 percent

(roughly comprising of 664.8 percent from the life insurance

sector, and 334.3 percent

from the non-life sector. Over the last few years, growth in the

global non-life insurance

market has significantly slowed down and has only grown in line

with general economic

growth (Sigma, 2001). This is in contrast to the life insurance

sector, which has continued

to grow at a fast rate. Sigma (2002a) estimates

this to be in the region of 5.4 percent worldwide since 2000.

Measured in total premiums,

OECD countries accounted for 95.52 percent and 93.99 percent of

the life insurance

business, and 91.19 percent and 92.50 percent of non-life

insurance premium volume in

1994 and 2001, respectively.

7

-

7/31/2019 Recruitment of Advisors in Icici

12/77

Outside of the OECD, a more recent development s ince the early

nineties

has been the abi l i ty of the emerging markets to s t rengthen

the i r g lobal

marke t sha re in t he l if e i nsurance segment , w ith g rowth

r at es o ft en

reaching double-digi t f igures. Furthermore, insurance markets

within the

OECD count ries have faced fa ll ing premium income, reduced

capi tal

market yields and low interest rates , a l l of which has put

insurers under

some pressure (S igma, 2002a) . Also , the growing importance of

the

insurance industry in emerging markets is ref lected in growing

insurance

dens i ty and insurance penetra tion of the non-OECD insurance

markets

(Sigma, 1996, 2001) . Never thel es s, and despi te t hese

development s,

emerging markets s t i l l have some way to go before matching

the relat ive

s izes and importance that the insurance indus try has in indus

tr ia l izedcountries.

8

-

7/31/2019 Recruitment of Advisors in Icici

13/77

THE DETERMINANTS OF INSURANCE DEMAND

The theore tical and empirical research to da te has suggested

that , onave rage , an ove rwhe lming pos it ive r el at ionsh ip

between f inancial

development and economic growth is evident and that a

well-developed

financial sector contr ibutes to economic growth. However, on a

s ingle

country-by-country basis, Ward and Zurbruegg (2000) have shown

that

d if fe re nc es i n th e c au sa l r el at io ns hi p b et we

en i ns ur an ce m ar ke t

development and economic growth are apparent . Research efforts

have,

the re fo re , moved onto under st and ing the f ac to rs t ha t

encourage the

development of financial institutions. By identifying the

determinants that

encourage insurance demand, pol icymaker s a re able t o a id f

inancial

development, thereby posi t ive ly influencing economic growth .

These

determinants that have been empirically tested can be grouped

under three

broad subheadings; economic, political / legal, and social

factors. To

further explore exactly how these factors influence insurance

demand, they

are each considered in turn below.

Economic factors

Fir st , i t i s impor tant t o h ighl ight t ha t t he r el at

ive impor tance o f an

insurance market wi th in a count ry i s l ike ly to depend upon

economic

development, since with a greater rate of economic growth the

consumption

of insurance products should increase. Indeed, early f indings

highlighted

that the demand for life insurance is positively correlated with

income, see

Yaari (1965), Hakansson (1969), Fortune

(1973), Fisher (1973), and Lewis (1989). These results are also

confirmed

by the more recent cross- country based studies of Be enstock et

al. (1986),

Truett and Truett (1990), and Browne and Kim (1993).

9

-

7/31/2019 Recruitment of Advisors in Icici

14/77

When analyzing the impact of na tional income on non- li fe

insurance

demand, Beenstock. (1988) indicate a positive relationship

exists between

national income in indus tr ial ized count ries and spending on

property-

l iab i li ty insurance. Browne e t a l . (2000) ex tend these f

indings when

analyzing motor vehicle and liability insurance in OECD

countries, and do

not only show that a positive and statistically significant

relationship can

be found between premium density and income, but also that

income has a

more p ronounced e ff ec t on motor veh ic le i nsurance , t han

on general

liability insurance consumption. Esho et al. (2003) also test

the impact of

national income on property and casualty insurance by analyzing

data from

developed and developing nations between 1984 to 1998. Again,

they detect

a s trong pos it ive r el at ionship between nat iona l i ncome

and non-l if einsurance demand. The World Bank confirms these

findings and states that

non-l if e i nsurance can be r egarded a s a norma l good imply

ing tha t

insurance demand r ises as income increases (Les ter, September

2002) .

Despite these findings, insurance penetration in some countries

differs from

the international average.

Role of insurance in economic development

Investments are necessary for Economic development.

Life Insurance plays a major role in mobilization of public

savings.

Savings out of life insurance funds are utilized in investments

for growth.

Looking for general insurance business industry trade would be

seriously

handicap in the absence of insurance cover relating to fire and

engineering

risk.

Social factors

Insurance can also be seen as a product that is valued subject

ively by i ts

consumer. In fact Hofstede (1995) points out that the level of

insurance

within an economy depends on the national culture and the

willingness of

10

-

7/31/2019 Recruitment of Advisors in Icici

15/77

ind iv iduals to use insurance as a means of dea l ing wi th r i

sk . I t i s not

surprising that Douglas and Wildavsky (1982) show that the

demand for life

insurance in a country may be affected by the unique culture of

the country

to the extent that cul ture affects the degree of r isk

aversion. Moreover,

Schlesinger (1981) reveals that an optimal insurance decision is

direct ly

re la ted to the leve l of r i sk aversion of the insured person

and shows,

fol lowing Prat t (1964) and Szipiro (1985), that the more r isk

adverse an

individual is the higher the amount insured.This is in line with

the work by

O ut re vi ll e ( 19 96 ), wh ic h e mp ha si ze s t ha t e du

ca ti on p ro mo tes a n

understanding of risk and hence aids insurance demand.

11

-

7/31/2019 Recruitment of Advisors in Icici

16/77

INSURANCE MARKET IN INDIA

The h is tory of l i fe insurance in India da tes back to 1818

when i t was

conceived as a means to provide for English Widows.

Interestingly in thosedays a higher premium was charged for Indian

l ives than the non-Indian

lives, as Indian lives were considered more risky for coverage.

The Bombay

Mutual Life Insurance Society started its business in 1870. It

was the first

company to charge same premium for both Indian and non-Indian

lives. The

Oriental Assurance Company was establ ished in 1880. The f irs t

general

insurance company- Tital Insurance Company Limited was establ

ished in

1850. Til l the end of nineteenth century insurance business was

almost

entirely in the hands of overseas companies.

Insurance regulat ion formally began in India with the passing

of the Life

Insurance Companies Act of 1912 and the provident fund Act of

1912.

Several frauds during 20's and 30's sullied insurance business

in India. By

1938 the re were 176 insurance companies . The f ir st

comprehensive

legislat ion was introduced with the Insurance Act of 1938 that

provided

strict State Control over insurance business. The insurance

business grew ata faster pace after independence. Indian companies

strengthened their hold

on th is business but despite the growth that was wi tnessed,

insurance

remained an urban phenomenon.

The Government of India in 1956, brought together over 240

private l i fe

i ns ur er s a nd p ro vi de nt s oc ie ti es u nd er o ne n at

io na li ze d m on op ol y

corporation and LIC was born. Nationalization was justified on

the grounds

that it would create much-needed funds for rapid

industrialization. This was

in conformity with the Government's chosen path of State lead

planning and

development.

12

-

7/31/2019 Recruitment of Advisors in Icici

17/77

The (non-l ife) insurance business, however, continued to thrive

with the

pri vate sector til l 1972. Th eir operations wer e restricted

to organized trade

and industry in large ci t ies . The insurance sector in India

has come a ful l

circle from being an open competitive market to nationalization

and back to

a l iberal ized marke t aga in . Tracing the development s i n t

he Ind ian

insurance sector reveals the 360-degree turn witnessed over a

period of

almost two centuries.

By any yardst ick, India, with about 200 mil l ion middle class

households,

presents a huge untapped potential for players in the insurance

industry.

Saturat ion of markets in many developed economies has made the

Indian

market even more attractive for global insurance majors with the

per capitaincome in India expected to grow at over 6% for the next

10 years and with

improvement in awareness levels, the demand for insurance is

expected to

grow at an at t ract ive rate in India. An independent consult

ing company,

The Monitor Group has estimated that the life insurance market

will grow

from Rs.218 bi l l ion in 1998 to Rs.1003 bi l l ion by 2008 (a

compounded

annual growth of 16.5%)

WINDS OF CHANGE

Reforms have marked the entry of many of the global insurance

majors into

the Indian market in the form of jo in t ventures wi th Indian

companies .

Some of the key names are AIG, New York Li fe , All ianz,

Prudent ia l ,

Standard Life, Sun Life Canada and Old Mutual.

The entry of new players has rejuvenated the erstwhile monopoly

player

LIC, which has responded to the competi t ion in an admirable

fashion by

launching new products and improving service standards

The following are the key winds of change brought about by

privatization.

13

-

7/31/2019 Recruitment of Advisors in Icici

18/77

Marke t Expansion : The re has been an ove ra ll expans ion in

the

market. This has been possible due to improved awareness levels

thanks

to the l arge number o f adver ti sing campa igns l aunched by a

ll t he

players. Th e scope for expansion is still unlimite d as

virtually all th e

players are concentrating on large cities and towns - ex cept by

LI C to an

extent there was no significant attempt to tap the rural

markets

New Product Of ferings: Th ere has been a plethora of new

and

innovative products offered by the new players, mainly from the

stable

of their international partners. Customers have tremendous

choice from

a large variety of products from pure term (risk) insurance to

unit-linked

investment products. Customers are offered unbundled products

with a

v ar ie ty o f b en ef it s a s ri de rs f ro m wh ic h t he y c

an c ho os e. Mo re

customers are buying products and services based on their t rue

needs

and not just t radi t ional money-back policies , which is not

considered

very appropriate for long-term protection and savings. However,

there

a re s ti ll some key new p roduct s yet t o be int roduced - e

.g . hea lth

pro ducts.

C us to me r S er vi ce : No t u ne xp ec te dl y, t hi s w as o

ne a re a t ha t

witnessed the most s ignif icant change with the entry of new

players .

There is an attempt to bring in international best practices in

service and

operat ional eff iciency through use of latest technologies.

Advice and

need based selling is emerging through much better trained sales

force

and advisors. There is improvement in response and turnaround

times in

specific areas such as delivery of first policy receipt, policy

document,

premi um notice, final ma turity payment, settlement of claims

etc .

However, t he re i s a l ong way to go and var ious cus tomer

surveys

indicate that the standards are still below customer expectation

levels

14

-

7/31/2019 Recruitment of Advisors in Icici

19/77

Channels of Dis tr ibut ion: Ti ll two years back , the only

mode of

distribution of life insurance products was through Agents.

While agents

continue to be the predominant distribution channel, today a

number of

innovative alternative channels are being offered to consumers.

Some of

them are bank assurance, brokers, the internet and direct market

ing.

Though i t i s t oo ear ly to p redict , t he wide spread o f

bank b ranch

network in India could lead to bank assurance emerging as a

significant

distribution mechanism.

Why Do I Need Life Insurance?

You need life insurance in order to ensure that your loved ones

can cope financially with

your loss. That's the bottom line.

The reasoning behind life insurance is most evident when you

consider sole breadwinners,

but applies to everyone who has dependents, even stay-at-home

spouses. If you (as the

stay-at-home spouse) were to suddenly die, your family would

have to find other ways to:

ensure care of children; get the family home cleaned; handle dry

cleaning and laundry; do

grocery shopping; and many other tasks which you currently

handle. While your servicesappear to be 'low cost' because no one

is paying you directly, if your family has to replace

you with paid help you will quickly see your 'value'.

15

-

7/31/2019 Recruitment of Advisors in Icici

20/77

FACTS OF LIFE INSURANCE INDUSTRY

Life insurance premium accounts for 72% of the total premium

collection inIndia as against the global average of 59%.

About LIC

In 2001 LIC sold close to 20 million new Individual Policies

In year 2000 the turnover of LIC was worth Rs. 261 Billion

LIC has close to 2048 branches, 100 divisions and 7 zonal

offices

Market Potential

The size of the Insurance market is 31.2 Crores which makes i t

oneof the hottest destination for any company

While 5 crores people have a capaci ty to pay an annual premium

of Rs 10000 per annum, 10 crores people have a capaci ty to pay

Rs

7000 per annum , and another 15 crores people have a capacity to

pay

Rs 3500 per annum

No. Of Players

Before na tional iza tion of Insurance in 1956, there were 254 l

i feInsurers and 106 general insurers to serve the population of 36

crores

in India

UK has more than 500 insurance companies to serve a population

of

6 crores

USA has over 2200 insurance companies to serve a population of

26Crores

Even Japan has 90 Insurance Companies to serve its population of

12

Crores

16

-

7/31/2019 Recruitment of Advisors in Icici

21/77

Emerging Trends

The Non life market was the size of Rs 10000 crores last year

with a potential of growing up to at least Rs 45000 Crores provided

it

develops the way it is expected to develop.

As on date the total insured losses arising out of unfortunate

incidentof Sept 11 in WTC is on date $42-43 Billion

The Industry

The g rowth r at e o f t he insurance sec to r i s about 10%

which i sexpected to go up to 12%

Before opening up the growth rate was 14% which means there is

a

d ip o f 4 .5% which cou ld be t raced to the p reva il ing

economicrecession

The per capita insurance premium in India is just US $ 8 which

is

less then even Malaysia which is US $144

Current trends and strategies

Growth of the pension market today: groups as well as

individual.

Emerging health insurance market with third party

administrators

(TPAs) t ry ing to make a p lace for them se lves as and when

theregulations are in place

New types of pro ducts Unit linked single premium-becoming

popular.

Current trends and strategies

New distribution channels are evolving and public wi ll have

greater

choice even in the matter of point of purchase.

Distribution and servicing are becoming more technology

intensiveand closely regulated.

Insurers are t rying to dist inguish their products but only t

ime and

experience will tell.

17

-

7/31/2019 Recruitment of Advisors in Icici

22/77

Emerging trends

People are slowly moving from purely savings oriented products

to products th at offer high er degree of life cover.

The real ization that insurance is basical ly about protect ion.

So far insurance has been widely understood by the market as

another tax

saving oriented investment option

There are several products becoming available in the market that

aresuited to the life style of the people.

There is a lot of scope for tailor made products depending upon

theneed of the customer.

Bank assurance Insurance products distributed through the bank

counters all over the

country can bring vast improvement in the insurance coverage in

the

quickest possible time

Banks today are the most credible agencies (However Banks also

do

have to go for Bankers Blanket Insurance!!!)

The public has immense faith in them

Regulators keep a tight vigil over them

Mil l ions of bank s ta ff a re h ighly educated and t ra ined

Banks canaccept lower commissions, and the benefi t goes on to the

consumer

by charging a lower premium rate

Half of insurance policies sold in Europe is through

banksInsurance and IT

Key areas where differentiation is considered critical for the

future of the

insurance companies include the following:

Product Development Back Office Customer Service

Distribution

18

-

7/31/2019 Recruitment of Advisors in Icici

23/77

LIFE INSURANCE MARKET IN INDIA

Many may not be aware that the life insurance industry of India

is as old as

it is in any other part of the world. The first Indian life

insurance companywas the Oriental Life Insurance Company, which was

star ted in India in

1818 at Kolkata. A number of players (over 250 in l i fe and

about 100 in

non-life) mainly with regional focus flourished all across the

country.

However, the Government of India, concerned by the unethical s

tandards

adopted by some players against the consumers, nationalized the

industry in

two phases in 1956 (life) and in 1972 (non-life). The insurance

business of

the count ry was then brought under two publ ic sector

companies, Life

Insurance Corporation of India (LIC) and General Insurance

Corporation of

India (GIC).

In l ine wi th the economic reforms that were ushered in India

in ear ly

nineties, the Government set up a Committee on Reforms

(popularly called

the Malhotra Committee) in April 1993 to suggest reforms in the

insurance

sector. The Committee recommended throwing open the sector to

private player s to usher in comp et ition and bring more choice to

the consumer. Th e

object ive was to improve the penetrat ion of insurance as a

percentage of

GDP, which remains low in India even compared to some

developing

countries in Asia.

Reforms were in it iated with the passage of Insurance Regula

tory and

Development Authority (IRDA) Bill in 1999.

IRDA was set up as an independent regulatory authority, which

has put in

place regulations in line with global norms. So far in the pri

vate sector, 12

19

-

7/31/2019 Recruitment of Advisors in Icici

24/77

l i fe insurance companies and 9 general insurance companies

have been

registered

Insurance Regulatory and Development Authority (IRDA) ACT,

1999

Prior to 1999 the there were only two players in the market

Life insurance corporation of India (LIC)

General Insurance Corporation (GIC)

Then to protect the interests of the policyholders, to regulate,

promote and

ensure orderly growth of the insurance industry, IRDA was set

up. After

this the private players started entering the market.

This is a corporate body established for the purpose and objects

as set out

in explanation to the title.

The authority replaces Controller under insurance act 1938.

20

-

7/31/2019 Recruitment of Advisors in Icici

25/77

It states that if authority is superseded by central govt. the

insurance may

be appointed till such time as Authority is reconstituted.

Constitution of IRDA

The insurance regulatory and development authori ty consist of

the

following members.

1. Chairperson

2. Less than five whole time members

3. Less than four part time members.

Member should be person of ability, integrity &

standing.

They Should have experience in the field of :

1. Life Insurance

2. General Insurance

3. Actuarial science.

4. Finance

5. Economics

6. Law

7. Accountancy

8. Administration Chairperson, members, officers and other

employees of

authority shall be public servants.

Functions of IRDA :

To issue certificate of registration, renew, withdraw,

suspend or cancel such registration.

To protect the interest of policyholders/insured in the

matter of insurance contract with the insurance company. To

specify requisite qualification, code of conduct and

training for insurance intermediaries and agents.

To specify code of conduct for surveyors /loss assessors.

To promote efficiency in the conduct of insurance

business

21

-

7/31/2019 Recruitment of Advisors in Icici

26/77

To promote and regulate professional organizations

connected with the insurance and reinsurance business.

To undertake inspection, conduct enquiries and

investigations including audit of insurers and insurance

intermediaries.

To control and regulate the rates terms and conditions to

be offered by the insurer regarding general insurance business

not so controlled by

tariff advisory committee under section 604 of Insurance act,

1938.

To regulate investment of funds by the insurance

companies.

Life Insurance Industry in the year 2000-2001 had 16 new

entrants,

namely:

S. No Reg.Number

Date of Reg. Name of the Company

1 101 23.10.2000 HDFC Standard Life Insurance CompanyLtd.

2 104 15.11.2000 Max New York Life Insurance Co. Ltd.

3 105 24.11.2000 ICICI Prudential Life Insurance CompanyLtd.

4 107 10.01.2001 Kotak Mahindra Old Mutual LifeInsurance

Limited

5 109 31.01.2001 Birla Sun Life Insurance Company Ltd.

6 110 12.02.2001 Tata AIG Life Insurance Company Ltd.

7 111 30.03.2001 SBI Life Insurance Company Limited .

8 114 02.08.2001 ING Vy sy a Li fe In su ra nc e Comp an

yPrivate Limited

9 116 03.08.2001 Bajaj A ll ianz L if e Insurance

CompanyLimited

10 117 06.08.2001 Metlife India Insurance Company.

22

http://www.hdfcinsurance.com/http://www.hdfcinsurance.com/http://www.maxnewyorklife.com/http://www.iciciprulife.com/http://www.iciciprulife.com/http://www.omkotakmahindra.com/http://www.omkotakmahindra.com/http://www.birlasunlife.com/http://www.tata-aig.com/http://www.sbilife.co.in/http://www.ingvysyalife.com/http://www.ingvysyalife.com/http://www.allianzbajaj.co.in/http://www.allianzbajaj.co.in/http://www.metlife.co.in/http://www.hdfcinsurance.com/http://www.hdfcinsurance.com/http://www.maxnewyorklife.com/http://www.iciciprulife.com/http://www.iciciprulife.com/http://www.omkotakmahindra.com/http://www.omkotakmahindra.com/http://www.birlasunlife.com/http://www.tata-aig.com/http://www.sbilife.co.in/http://www.ingvysyalife.com/http://www.ingvysyalife.com/http://www.allianzbajaj.co.in/http://www.allianzbajaj.co.in/http://www.metlife.co.in/

-

7/31/2019 Recruitment of Advisors in Icici

27/77

Yr: 2001-2002: (From 1st Jan 2001 to Dec. 2002)

Life Insurance Industry in this year, so far has 3 new entrants;

namely

S.No. RegistrationNumber

Date of Reg. Name of the Company

1 121 03.01.2002 AMP Sanmar Life Insurance

Company Limited.

2 122 14.05.2002 Aviva Life Insurance Co. India Pvt.

Ltd.

Yr: 2003-2004: (From 1st Jan 2003 till Date)

Life Insurance Industry in this year, so far has 1 new entrants;

namely

S.No Registration

Number

Date of Reg. Name of the Company

1 127 06.02.2004 Sahara India Insurance Co. Ltd.

23

http://www.ampsanmar.com/http://www.ampsanmar.com/http://www.avivaindia.com/http://www.avivaindia.com/http://www.ampsanmar.com/http://www.ampsanmar.com/http://www.avivaindia.com/http://www.avivaindia.com/

-

7/31/2019 Recruitment of Advisors in Icici

28/77

Life Insurance Corporation of India Act, 1956

Life insurance business was nationalized in India with effect

from 19 th January 1956.

The life insurance business of 154 Indian Life offices

constituted by 16 non-Indian

insurers operation in India and 75 provident societies was taken

over by the

Government of India.

LIC of India Act was passed by the parliament on 18 th june1956

and it came into effect

from 1 st July1956.

24

-

7/31/2019 Recruitment of Advisors in Icici

29/77

COMPANY PROFILE

ABOUT ICICI PRUDENTIAL

Incorporated on July 20, 2000 i t is a 74:26, joint venture

between ICICI

and Prudent ia l p lc of U.K. In November 2000, ICICI Prudent ia

l Li fe

Insurance was granted Cert if icat ion of Registrat ion for

carrying out l i fe

insurance business by the Insurance Regulatory & Development

Authority

of India. The Company issued its first policy on December 12,

2000.

ICICI Prudential Life Insurance Company is a joint venture

between ICICIBank, a p remier f inancial powerhouse and P rudent ia

l p lc , a l eading

int erna tional f inancial s ervi ces g roup headqua rt ered in

the Uni ted

Kingdom. ICICI Prudential was amongst the first private sector

insurance

companies to begin operations in December 2000 after receiving

approval

from Insurance Regulatory Development Authority (IRDA).

ICICI Prudential 's equity base s tands at Rs. 9.25 bi l lion

with ICICI Bank

and Prudential plc holding 74% and 26% stake respectively. In

the financial

year ended March 31, 2005, the company garnered Rs 1584 crores

of new

business premium for a total sum assured of Rs 13,780 crores and

wrote

near ly 615,000 polic ies. The company has a ne twork of about

56 ,000

advisors; as well as 7-banc assurance and 150 corporate agent

tie-ups. For

the past four years, ICICI Prudential has retained its position

as the No. 1

pri vate life insurer in the country, with a wide range of

flexible products

that meet the needs of the Indian customer at every step in

life.

ICICI Prudential Life Insurance's new business has grown 77% in

'04-05 to cross Rs 1,000

crores, with annualized new business premium of Rs 1,256 crores.

The company's total

25

-

7/31/2019 Recruitment of Advisors in Icici

30/77

received premium, which includes renewal premium, has crossed Rs

2,363 crores for '04-

05.

In the year 2004-05, 80% of the premium has been generated from

unit-

linked plans, with nearly 40% of the premium collections going

into equity.

Indian policyholders have been increasingly opting for unit- l

inked plans,

which offer higher exposure to equities, ever since lower

interest rates have

forced insurers to cut bonuses on traditional policies.

In contrast, the private l i fe insurance agent force has grown

by leaps and

bounds. The need for higher geographical penetration has seen

insu rance

companies r ec ru it ing aggress ively. A t l as t count , t hey

added up to amassive 1,50,000. ICICI PruLife topped the list among

the private players,

which had close to 50,000 agents , while Bajaj Allianz had

30,000 agents .

At least s ix of the 11 private l i fe insurance players had an

agent force of

10,000 and plus.

This included Tata AIG, Max New York, HDFC Standard and Bir la

Sun

Life. All these insurance companies have allocated large amounts

of fresh

capital to build the agent network across major cities in the

past few years.

Our vision:

To make ICICI Prudential the dominant Life and Pensions player

built on trust by world-

class people and service.

This we hope to achieve by:

Understanding the needs of customers and offering them superior

products and

service Leveraging technology to service customers quickly,

efficiently and conveniently

26

-

7/31/2019 Recruitment of Advisors in Icici

31/77

Developing and implementing superior risk management and

investment

strategies to offer sustainable and stable returns to our

policyholders Providing an enabling environment to foster growth

and learning for our employees And above all, building transparency

in all our dealings.

The success of the company will be founded in its unflinching

commitment to 5 core

values -- Integrity, Customer First, Boundary less, Ownership

and Passion. Each of the

values describe what the company stands for, the qualities of

our people and the way we

work. .

We do believe that we are on the threshold of an exciting new

opportunity, where we can

play a significant role in redefining and reshaping the sector.

Given the quality of our parentage and the commitment of our team,

there are no limits to our growth.

Promoters

ICICI and Prudential came together in 1993 to form Prudential

ICICI Asset

Management Company, which has today emerged as one of the

leading

mutua l funds in Ind ia . The two companies b ring together two

o f t he

strongest financial service brands in Asia, known for their

professionalism,

excellent quality of service and long term commitment to YOU.

Riding on

the success of this relationship, the two companies joined hands

once more

in 2000, to form ICICI Prudential Life Insurance, with a

commitment to

pro vide leading-edge life insu rance solutions.

ICICI Bank has 74% stake in the company, and Prudential plc has

26%.

ICICI Bank (NYSE:IBN) is Indias second largest bank with an

asset baseof Rs. 106812 crores. ICICI Bank provides a broad

spectrum of f inancial

services to individuals and companies. This includes mortgages,

car and

personal loans, credi t and deb it cards, corporate and

agricultural finance.

The Bank servi ces a g rowing cus tomer base o f more than 7 mil

li on

27

-

7/31/2019 Recruitment of Advisors in Icici

32/77

customer accounts and 5 mil l ion bondholders accounts through a

mult i -

channel access network. This includes about 450 branches and

extension

counters, 1675 ATMs, call centres and Internet banking. ICICI

Bank posted

a net profi t of Rs.1, 206 crores for the year ended March 31,

2003. ICICI

Bank is the only Indian company to be rated above the country

rating by the

internat ional rat ing agency Moodys and the only Indian company

to be

awarded an investment grade internat ional credi t rat ing. The

Bank enjoys

the h ighest AAA (or equivalent ) ra ting f rom a l l leading

Indian ra ting

agencies.

Establ ished in 1848, Prudential plc is a leading internat ional

f inancial

serv ices company in the UK, with a round US$250 b i ll ion

funds under management and more than 16 million customers

worldwide. Prudential has

brough t to market an integrated range of financial services

products th at

now includes life assurance, pensions, mutual funds, banking,

investment

management and general insurance. In Asia, Prudential is Auks

largest life

i ns ur an ce c omp an y wi th a v as t n et wo rk o f 2 2 l if

e a nd m ut ua l f un d

operations in twelve countries - China, Hong Kong, India,

Indonesia, Japan,

Korea , Malaysi a, t he Phi li pp ines , S ingapore , Taiwan,

Tha il and and

Vietnam. Since 1923, Prudential has championed customer-centric

products

and services, supported by over 60,000 staff and agents across

the region.

Fact sheet

ICICI Prudential Life Insurance Company is a joint venture

between ICICI

Bank, a p remier f inancial powerhouse, and P rudent ia l p lc ,

a l eading

int erna tional f inancial s ervi ces g roup headqua rt ered in

the Uni ted

Kingdom. ICICI Prudential was amongst the first private sector

insurance

companies to begin operations in December 2000 after receiving

approval

from Insurance Regulatory Development Authority (IRDA).

ICICI Prudentials equity base s tands at Rs. 925 crores with

ICICI Bank

and Prudential plc holding 74% and 26% stake respectively. In

the period

28

-

7/31/2019 Recruitment of Advisors in Icici

33/77

April-December 2004, the company garnered Rs 860 crores of new

business

premi um for a total sum assured of over Rs 7,360 crores and

wrote nearly

345,000 policies. Today the company is the No.1 private life

insurer in the

country.

Distribution

ICICI Prudent ia l has one of the larges t d ist ribut ion ne

tworks amongst

pri vate life insurer s in India, having commenced operations in

69 cities and

towns in India. These are: Agra, Ahmedabad, Ajmer, Allahabad,

Amritsar,

Aurangabad, Bangalore, Barei l ly, Bhat inda, Bhopal,

Bhubhaneshwar,

Calicut, Chandigarh, Chennai, Coimbatore, Dehradun, Durgapur,

Faridabad,

Goa, Guntur, Gurgaon, Guwahat i , Gwalior, Hyderabad, Hubl i ,

Indore,Jaipur, Jalandhar, Jamnagar, Jamshedpur, Jodhpur, Kanpur,

Karnal, Kochi,

Kolka ta , Kolhapur, Kota, Kot tayam, Lucknow, Ludhiana, Madurai

,

Mangalore, Meerut , Mumbai, Mysore, Nagpur, Nasik, Noida, New

Delhi ,

Pat iala , Pune, Raipur, Rajkot , Ranchi , Rourkela, Salem, Si

liguri , Surat ,

Thane, Thrissur, Trichy, Trivandrum, Udaipur, Vadodara, Vapi,

Varanasi,

Vashi, Vijayawada and Vizag.

The company has seven bank assurance t ie-ups, having agreements

with

ICICI Bank, Federal Bank, South Indian Bank, Bank of India, Lord

Krishna

Bank and some co-operat ive banks, as well as over 160 corporate

agents

a nd b ro ke rs . I t h as a ls o t ie d u p w ith o rg an iz at

io ns l ik e Dh an f or

distribution of Salaam Zindagi, a policy for the socially and

economically

underprivileged sections of society.

29

-

7/31/2019 Recruitment of Advisors in Icici

34/77

Distribution Channels

Till date insurance agents still remain the main source through

which the insurance

products are sold. The concept is very well established in the

country like India. But still

the increasing use of other sources is imperative. It therefore

makes sense that the well-

balanced alternative channel of distribution. At present the

distribution channels that are

available in the market are:

Direct selling

Corporate agents

Group Selling

Brokers and corporative Societies

Banc assurance

ABOUT THE PROMOTERS

ICICI Bank i s India' s second- larges t bank wi th to ta l asse

ts of about

Rs .112,024 crore and a ne twork of about 450 branches and off

ices and

about 1750 ATMs. It offers a wide range of banking products and

financial

services to corporate and retai l customers through a variety of

del ivery

channels and through its specialized subsidiaries and affiliates

in the areasof investment banking, l i fe and non-l ife insurance,

venture capital , asset

management and information technology. ICICI Bank posted a net

profit of

Rs.1, 637 crores for the year ended March 31, 2004. ICICI Bank's

equity

shares are l is ted in India on stock exchanges at Chennai ,

Delhi , Kolkata

and Vadodara, t he S tock Exchange, Mumba i and the Nat ional S

tock

Exchange of India Limited and its American

Deposi tary Receipts (ADRs) are l is ted on the New York Stock

Exchange

(NYSE).

Establ ished in London in 1848, Prudential plc, through its

businesses in

the UK and Europe , the US and Asia , provides re ta i l f

inancia l serv ices

30

-

7/31/2019 Recruitment of Advisors in Icici

35/77

pro ducts and services to more th an 16 mi llion customer s,

poli cyholder and

unit holders worldwide. As of June 30, 2004, the company had

over US$300

billion in funds under management. Prudential has brough t to

market an

in tegra ted range of f inancia l serv ices products that now

includes l i fe

assurance, pensions, mutual funds, banking, investment

management and

general i nsurance . In Asia, P rudent ia l i s t he l eading

European l if e

i ns ur an ce c omp an y wi th a v as t n et wo rk o f 2 4 l if

e a nd m ut ua l f un d

operations in twelve countries - China, Hong Kong, India,

Indonesia, Japan,

Korea , Malaysi a, t he Phi li pp ines , S ingapore , Taiwan,

Tha il and and

Vietnam.

31

-

7/31/2019 Recruitment of Advisors in Icici

36/77

PRODUCTS AND SERVICES SNAPSHOT

Insurance Solutions for Individuals

ICICI Prudential Life Insurance offers a range of innovative,

customer-

centric products that meet the needs of customers at every life

stage. Its 20

pro ducts can be enhanced with up to 6 ri ders, to create a

customized

solution for each policyholder.

Savings Solutions SecurePlus i s a t ransparent and

feature-packed savings p lan that

offers 3 levels of protection. CashPlus is a transparent,

feature-packed savings plan that offers 3

levels of protection as well as liquidity options. Save n

Protect is a t radi t ional endowment savings plan that offers

life protection along with adequate returns. CashBak i s an

antic ipa ted endowment policy idea l for meeting

milestone expenses l ike a chi lds marriage, expenses for a chi

lds

higher education or purchase of an asset. LifeTime &

LifeTime II offer customers the flexibility and control

to customize the policy to meet the changing needs at different

l i festages. Each offers 4 fund options Preserver, Protector,

Balancer and

Maximiser. LifeLink II is a single premium Market Linked

Insurance Plan that

combines life insurance cover with the opportunity to stay

invested

in the stock market. Premier Life is a limited premium-paying

plan that offers customers

life insurance cover til l the age of 75. InvestShield Life i s

a Market Linked p lan that provides capi ta l

guarantee on the invested premiums and declared bonus interest.

InvestShield Cash i s a Market Linked p lan that provides capi ta

l

guarantee on the invested premiums and declared bonus in teres

t

along with flexible liquidity options.

32

-

7/31/2019 Recruitment of Advisors in Icici

37/77

InvestShield Gold i s a Market Linked p lan that provides capi

tal

guarantee on the invested premiums and declared bonus in teres

t

along with limited premium payment terms.

Protection Solutions

LifeGuard is a protection plan, which offers life cover at very

low cost. It

is avai lable in 3 options level term assurance, level term

assurance with

return of premium and single premium.

Child Plans

SmartKid education plans provide guaranteed educational benefi

ts to a

child a long with l ife insurance cover for the parent who

purchases the

poli cy. The policy is designed to provide mo ney at important

milestones inthe childs life. SmartKid plans are also available in

unit-linked form both

single premium and regular premium.

Retirement Solutions

ForeverLife is a ret i rement product targeted at individuals in

their

thirties. SecurePlus Pension i s a f lex ib le pens ion p lan

tha t a l lows one to

select between 3 levels of cover.

Market-linked retirement products

LifeTime Pension II is a regular premium market- linked

pension

plan LifeLink Pension II is a single premium market-linked

pension p lan. InvestShield Pension i s a r egular p remium pension

p lan with a

capital guarantee on the investible premium and declared

bonuses.

ICICI Prudential also launched Salaam Zindagi , a soc ia l s ec

to r g roup

insurance policy targeted at the economically underprivileged

sections of

the society.

33

-

7/31/2019 Recruitment of Advisors in Icici

38/77

Group Insurance Solutions

ICICI Prudent ia l a lso offers Group Insurance Solu t ions for

companies

seeking to enhance benefits to their employees.

ICICI Pru Group Gratuity Plan: ICICI Prus group gratui ty plan

helps

employers fund their s tatutory gratui ty obligat ion in a

scient if ic manner.

The p lan can a lso be cus tomized to s t ruc ture schemes tha t

can provide

benefits beyond th e statutory obligations.

ICICI Pru Group Superannuat ion Plan: ICICI Pru offers a f lex

ible

defined contr ibution superannuating scheme to provide a ret i

rement ki t ty

for each member of the group. Employees have the option of

choosing fromvarious annuity options or opting for a partial

commutation of the annuity

at the time of retirement.

ICICI Pru Group Term Plan: ICICI Prus f lexible group term solut

ion

helps provide affordable cover to members of a group. The cover

could be

uniform or based on designation/rank or a multiple of salary.

The benefi t

under the policy is paid to the beneficiary nominated by the

member on

his/her death.

Flexible Rider Options

ICICI Pru Life offers flexible riders, which can be added to the

basic policy

at a marginal cost, depending on the specific needs of the

customer. Accident & disabili ty benefit: I f dea th occurs as

the resu l t of an

accident during the term of the policy, the beneficiary receives

an

additional amount equal to the sum assured under the policy. If

the

death occurs while traveling in an authorized mass transport

vehicle,

the beneficiary will be entitled to twice the sum assured as

additional

benefit. Accident Benefit: This rider option pays the sum

assured under the

rider on death due to accident.

34

-

7/31/2019 Recruitment of Advisors in Icici

39/77

Critical Illness Benefit: protects the insured against financial

loss in

the event of 9 specified critical il lnesses. Benefits are

payable to the

insured for medical expenses prior to death. Major Surgical

Assistance Benefit: provides financial supports in

the event of medical emergencies, ensuring benefi ts are payable

to

t he l if e a ss ur ed f or m ed ic al e xp en se s i nc ur re d

f or s urgi ca l

procedures. Cover is offered against 43 surgical proced ures.

Income Benefit: This r ider pays the 10% of the sum assured to

the

nominee every year, t i l l maturity, in the event of the death

of the life

assured. It is available on SmarKid, SecurePlus and CashPlus

Waiver of Premium: In case of total and permanent disability due

to

an accident , the premiums are waived t i ll matur ity. This r

ider i savailable with SecurePlus and CashPlus.

SERVICE STANDARDS

Six sigma

ICICI prudent ial rea lized ear ly on that qual ity could be a s

ignif icant

differentia with respect to the competition. Hence it launched a

six-sigmainitiative as a quality measurement tool to understand and

fulfill customer

needs, set industry benchmarks and make its operations salable

with a focus

on customers and costs.

Through Six s igma there has been a cont inuous focus on the cus

tomer,

which f i ts in ideal ly with a focus on the customer, which f i

ts in ideal ly

with ICICI Prudentials customer centric approach.

35

-

7/31/2019 Recruitment of Advisors in Icici

40/77

Investment philosophy

Their investment philosophy aims to proact ively achieve

superior r isk-

adjusted returns on our funds under management. The focus is on

ensuringlong-term safety, Stability and profitability of

portfolio.

The f ramework to achieve th is objec tive i s based on sound

inves tment

pro cess and controls coupled wi th a rigorous and sophisticated

risk

management strategy. There is clearly articulated asset

allocation strategy

depending on risk characteristics of corresponding

liability.

Portfol io management is a funct ion o extensive research and is

based ondata and reasoning. Debt investments target a judicious mix

of credi t and

interest rate risk. Investments in equity target long term

appreciation and

follow a value oriented investment style.

Information technology

At ICICI Prudential, the strategic use of technology provides

the consumer

with value added services. There is a robust system, which is

employed asthe backbone o f t he company. Ini ti at ives have been

t aken to p rovide

complet e CRM solut ions so tha t t he consumer can acces s

complet e

information on the polic ies online, f rom access ing payment de

ta i ls to

sending in the premium. Channel partners can manage their entire

business

on the web through premium alerts, client diaries and premium

calculators.

36

-

7/31/2019 Recruitment of Advisors in Icici

41/77

The following companies have the following market share of the

insurance industry.

NAME OF THE PLAYER MARKET SHARE (%)

LIC 82.3

ICICI PRUDENTIAL 5.63

BIRLA SUNLIFE 2.56

BAJAJ ALLIANZ 2.03

SBI LIFE 1.80

HDFC STANDARDLIFE 1.36

TATA AIG 1.29

MAX NEW YORK 0.90

AVIVA 0.79

OM KOTAK MAHINDRA 0.51

ING VYASA 0.37

AMP SANMAR 0.26

METLIFE 0.21

37

-

7/31/2019 Recruitment of Advisors in Icici

42/77

0

10

20

30

40

50

60

70

80

90

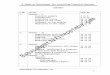

MARKET SHARE(%)

LIC

ICICIPRUDENTIAL

BIRLASUNLIFE

BAJAJALLIANZ

SBI LIFE

HDFCSTANDARDLIFE

TATA AIG

MAX NEW YORK

The market share was distributed among the private players.

Though LIC still holds 82.3%

of the insurance sector, the upcoming natures of these private

players are enough to give

more competition to LIC in the near future . LICs market share

has decreased from

95%(2002-2003) to 81%(2004-05 ).

38

-

7/31/2019 Recruitment of Advisors in Icici

43/77

ICICI PRUDENTIAL PRIORITY CIRCLE

THE PRIORITY CIRCLEPriori ty circle is an opportunity to

diversify the business and widen the

gamut of services and solutions offered to the clients. One can

now enhance

the business with capital investment and yet earn high returns.

Step into the

arena of private l i fe insurance, one of the most dynamic

industr ies today

with Priori ty Circle of ICICI prudential l i fe insurance

company l td, the

leader in todays private life insurance industry.

The vast reach

91 branches spread over 61 locations

A committed team of t ied and corporate agents , brokers ,

banks

and call centre executives

An advisor force of more than 46000 agents.

Tie ups with Indias leading banks like ICICI bank, Bank of

India, federal

bank and so uth Indian bank ICICI prudential custo mer s enjoy

the pri vilege

of approaching the company as per their convenience. Its vast

reach across

India places the company far ahead of its pears.

The pleasant experience service

The company maintains its undisputed leadership by proactively

achieving

superior risk adjusted returns on its funds. The prime focus is

on ensuring

long-term safety, profitability, stability of the portfolio.

Quality service at ICICI Pru is not an isolated function but a

practice. From

people and pro ducts to process at every stage of th e policy,

it is an

experience for the customers so everyones a customer service

associate

including you.

39

-

7/31/2019 Recruitment of Advisors in Icici

44/77

THE ADVISORS FORTE

An advisor at ICICI Prudential is one of the main strengths of

the company.

I ts a partnership that resul ts in unlimited growth opportunity

with the

company.

THE ROLE

To identify prospective customers, provide tailor-made solutions

to cater to

their individual needs, conduct regular reviews to keep

customers on track

and last but not the least, achieve targets.

THE BENEFIT

A premium product portfolio that caters to a wide range of

financial needs,excellent back-end support, attractive returns and

benefits, round the clock

customer service and extensive training for that edge over the

competition

THE ADVANTAGE

No start up capital, no supervisor, flexible working environmen

t and an

unlimited earning p otential.

40

-

7/31/2019 Recruitment of Advisors in Icici

45/77

ICICI PRUDENTIAL PRIORITY CIRCLE CONTROL

STRUCTURE

The control structure of ICICI Prudential Priority Circle goes

like this:

As a whole t i l l Zonal Head the levels are same in al l

sectors of ICICI but

after that when comes the Territory Manager, the unique levels

of Priority

Circle begins.

Under the Country Head come 2 regions:

1. Pen in su la

2 . Hi ma lay as

41

Country head

HIMALAYASAND PENINSULA

SALES HEAD

ZONAL HEAD

TERRITORYMANAGER

MANAGER priorityclients

-

7/31/2019 Recruitment of Advisors in Icici

46/77

Under those come thei r respec t ive Sales Head, Zonal Head,

Terri tory

Manager, and Manager Priority Clients.

Management Team:

Country Head (CEO) : Mrs. Shikha Sharma.

Himalayas Sales Head : Mr. Chander Chalani.

Zonal Head : Mr. Vikas Seth.

Territory Manager : Mr. Sumeet Sahni.

Manager Priority Clients : Mr. Anuj Pawra.

The MPCs are not al lowed to sel l insurance direct ly, but they

have to gothrough the advisors under them.

The advisors under the MPCs are the High Network Individuals ,

which

bring business. Th ey are selected by the MP C s by completing

certain

formalities.

The person has to pay Rs. 1500/- for becoming an Advisor. That

person is

given 9 days intensive training in which he is also given

product details.

After the t raining is over the person has to give an

examination named as

IC 33 taken by Insurance Regulatory and Development

Authority.

Once the person clears his examination a code is generated in

his name.

The person now becomes an Advisor and is ready to bring

business.

42

-

7/31/2019 Recruitment of Advisors in Icici

47/77

NATURE OF JOB AS A TRAINEE

At priority circle, the nature of the job included recruitment

of the channel

members who were further assigned to solicit insurance. The

database was

prep ared, which had the names of selected people across Delhi.

They were

invited to the off ice for the f i rs t meet with the manager-

priori ty cl ients .

The MPCs job i s to expla in the course of ac t ion fo l lowed

to jo in the

business.

Af ter the f i r s t meet i f the prospect i s sa t i s f ied he

i s g iven a document

called market 100 to explore his contacts which would help him

grow his

business. Th e pro sp ect fills the document and brings it to

the office. Th e

MPC scru t in izes the document . The next s tep i s to meet the

ter r itory

manager who would judge the prospect whether he is capable to do

the job

or not. I f the ter ri tory manager i s sa ti s fied, then the

person f i ll s o ther

formal i ties l ike form, age proof and o ther documents and i s

ready to

receive the training.

The lead t ra iner of the branch conducts the t ra in ing for

about 9 days ,following which an exam is held. After clearing the

exam the IRDA license

is given, post, which the advisor is ready to sell insurance and

do financial

consulting for his clients.

Characteristics of a good Insurance advisor

These were some of the qualities that we searched in a person

who could be an asset to thecompany and could give business .It is

not necessary to have good academic background

but a good salesman should have the following qualities:

He should be speedy, needy and greedy.

He should be presentable.

43

-

7/31/2019 Recruitment of Advisors in Icici

48/77

He should have good communication skills.

He should be ready to serve with a good smiling face.

At ICICI Priority circle, the aim is to achieve Production

Growth through

RECRUITMENT. Part of this growth is accomplished by improving

the

pro ductivity of the existing Agency memb ers. Ho wever,

bringing

s uf fi ci en t n umb ers of h igh q uali ty n ew p ro du cers

in to th e s ales

organization each year is a must. The main focus thus remains

recruitment

of HNI (High Network Individuals) Clients.

Recruitment is the prospecting, identification and training of

advisors so as

to enable him to do business, post licensing.

Broadly recruitment can be identified as a 5-step process:

1. The SEARCH for talent

2. To ENGAGE the prospective Advisor

3. The EVALUATION of potential Advisor

4. The CONFIRMATION of intent

5. The LICENSING of Advisors

SEARCH FOR TALENT

In this stage we need to identify the advisors we need to

recruit to become

a successful team. We need to clearly understand the profile we

are looking

o ut f or. T he s ea rc h m us t b e c on ti nu ou s a nd s ys

te ma ti c j us t l ik e

pro specting for sales . We must search am ong sever al so urces

on a regular

basis.

The sources were divided into different segments for a more

systematic and

focused approach. These were:

44

-

7/31/2019 Recruitment of Advisors in Icici

49/77

The first segment to be taken under study was that of students

with some commerce

background .

The segment is further sub-grouped as follows:

1. Pass out B.Com students

2. Students pursuing C.A

3. Students of M.F.C

4. Pass out students of MBA.

Our main selling point for this segment was that these students

have some financeknowledge. We gave them a career opportunity as

they could be promoted as a unit

manager as soon as they meet the required target.

The required information of such students was collected from

there respective institutions.

Those students whose response was positive were called in the

premises of ICICI

Prudential for an informal interview where they were told about

the job and the

opportunities involved.

The second segment was that of enterprising women .

The segment was further divided into sub groups, which were as

follows.

1. Hobby classes operators.

2. Beauty Saloon owners.

3. Fashion boutiques.

4. Kitty party groups.

5. Agents of direct selling products like Tupperware, Avon.

Our main Point in approaching them was that these women already

had a well-established

network in their respective fields and hence in a position to

exploit them further. If they are

45

-

7/31/2019 Recruitment of Advisors in Icici

50/77

aware of the opportunities and are ready to take risk then they

just needed to tap the market

that is already there for them.

To locate this segment of prospective financial consultant we

used our personal contacts.

The women who were positive were then told about the companys

project of locating

financial consultant.

The third segment of property dealers, commission agents,

retired members from

banking industry .

The method of research was telemarketing.

Under Telemarketing, a telephone call was made to the targeted

person wherein the

intention was to make the person aware of the objectives under

study. For this purpose we

tried to allure the target customers to become an agent.

However the call must be made keeping this in mind a few things

such as:

1. The intended person must have time to listen to us.

2. We must not offend them in any way.

3. We should be considerate enough to respect the value of their

time and must not

waste his time in unnecessary Jargons.

4. Care must b taken while introducing main subject , so that we

are able to arouse

interest .

5. The person should feel important rather than irate

customer.

The last segment was of CAs, Income Tax Consultants and

Advocates .

The data source of this segment was through Yellow Pages . We

adopted the method of

direct interview after taking appointments on phone.

46

-

7/31/2019 Recruitment of Advisors in Icici

51/77

Firstly we called up people and explained them about the work

profile .If we found them

interested, an appointment was fixed with the MPC. The Manager

clearly explains the

business opportunity and studies the prospective candidates

profile. Candidates another

round of screening was done by Unit Manager with his respective

ASM (channel

development) and they short listed the most capable candidates.

Capability doesnt mean

that the person should have some specific qualifications.

Capability meant that the chosen

candidates must have at least interpersonal skills and should be

keen enough to learn during

training process. He must also realize the importance of

marketing in the field. We

preferred people with finance background as it becomes easier

for them to understand the

insurance industry.

The second round of selection was consisted of an informal

interview with the candidate.There were main three purpose of

this:

1. To reinforce the purpose of study i.e. selecting the right

kind of people.

2. To make the candidates aware of growing opportunities in this

line of work and make