Embed Size (px)

Citation preview

Reforming Public Pensions in the U.S. and the U.K.

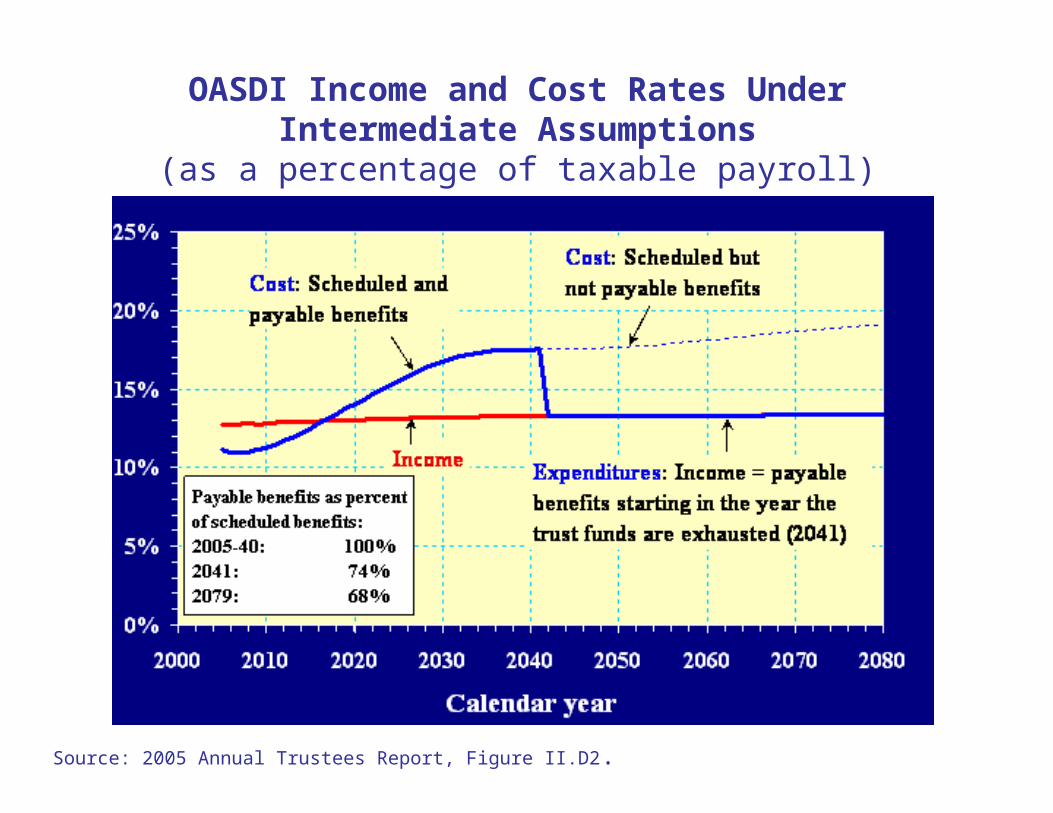

OASDI Income and Cost Rates Under Intermediate Assumptions

(as a percentage of taxable payroll)

Source: 2005 Annual Trustees Report, Figure II.D2.

Old Age, Survivors and Disability Insurance (OASDI)

Payroll tax rate ….12.4%, up to cap of $90,000 (indexed to

average earnings)

Benefit Determination

• Average the best 35 wage indexed annual earnings (AIME) • Use a progressive benefit formula (PIA = f [AIME]) • Adjust benefits from PIA if they start other than at the age for full benefits (commonly called the normal retirement age) • No benefits before age 62 • Between 62 and the age for full benefits (which is in transition from 65 to 67), benefits are only paid if earnings are low enough, referred to as an earnings or retirement test. • No further increases for a delayed start beyond age 70

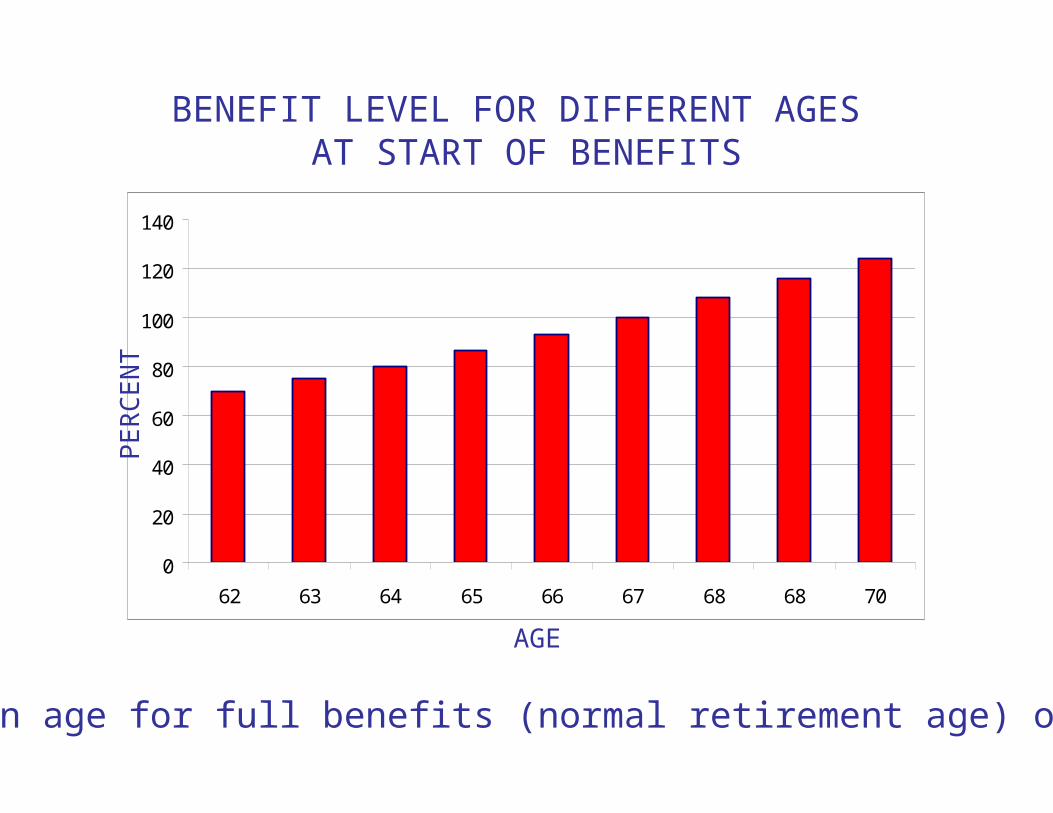

0

20

40

60

80

100

120

140

62 63 64 65 66 67 68 68 70

AGE

PE

RC

EN

TBENEFIT LEVEL FOR DIFFERENT AGES

AT START OF BENEFITS

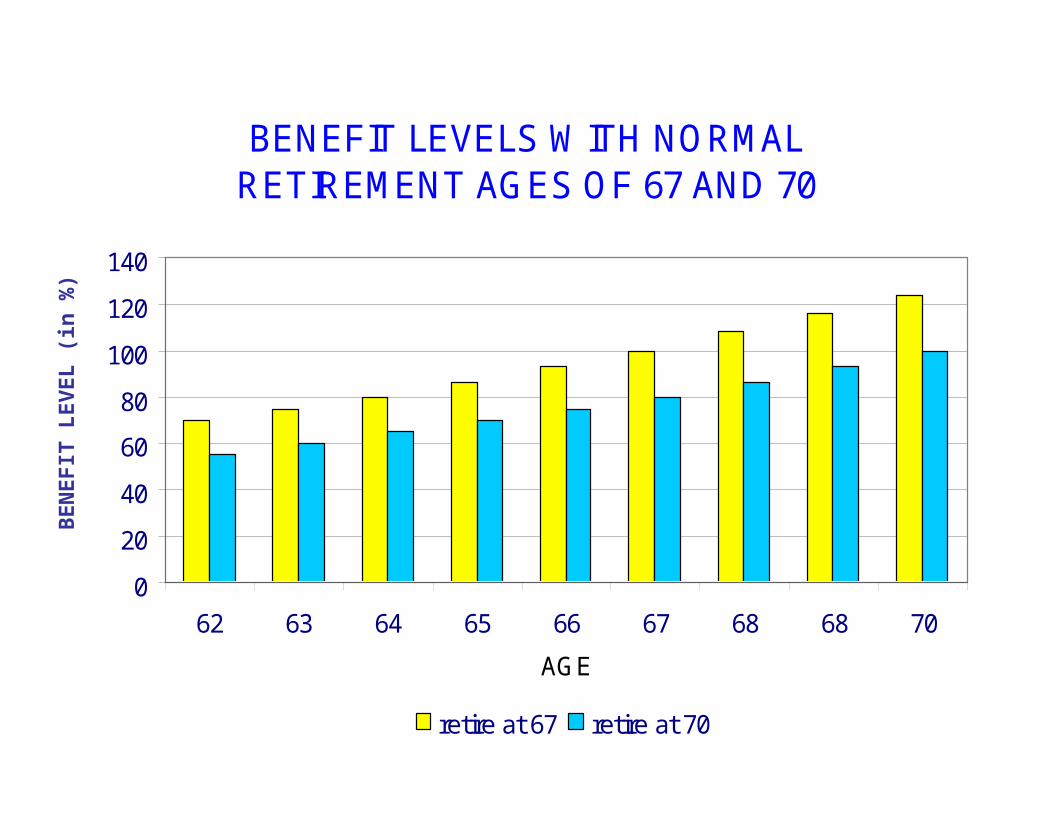

For an age for full benefits (normal retirement age) of 67.

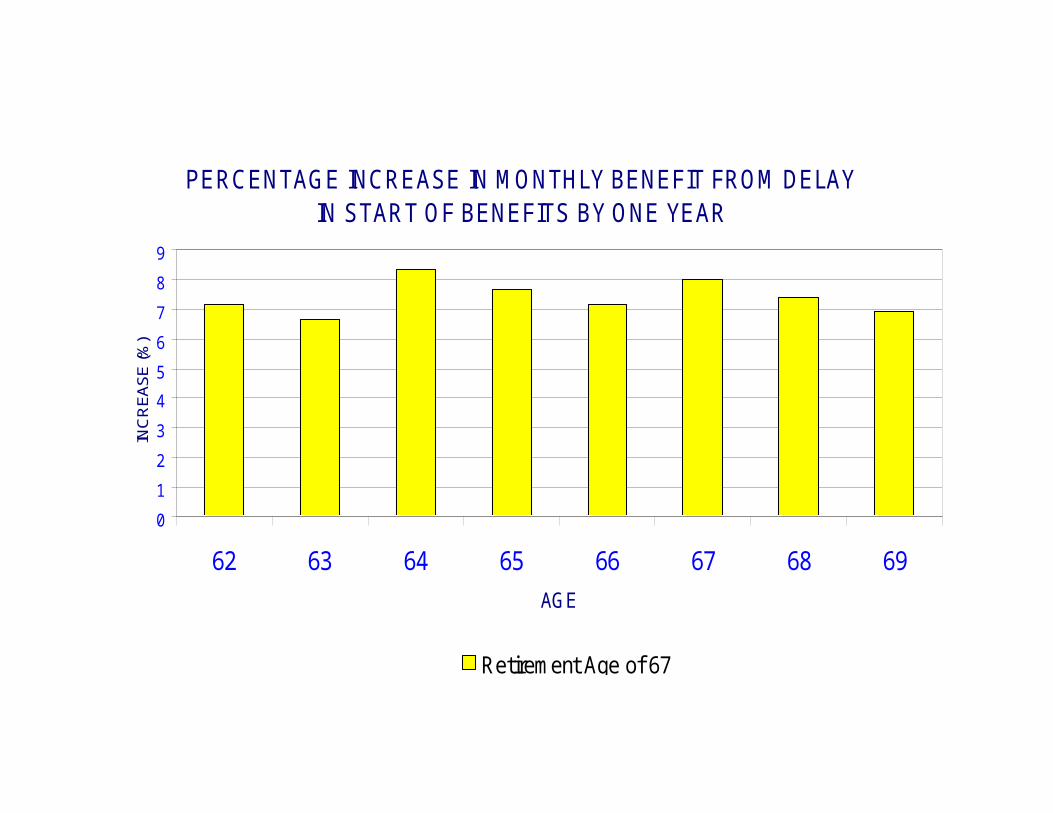

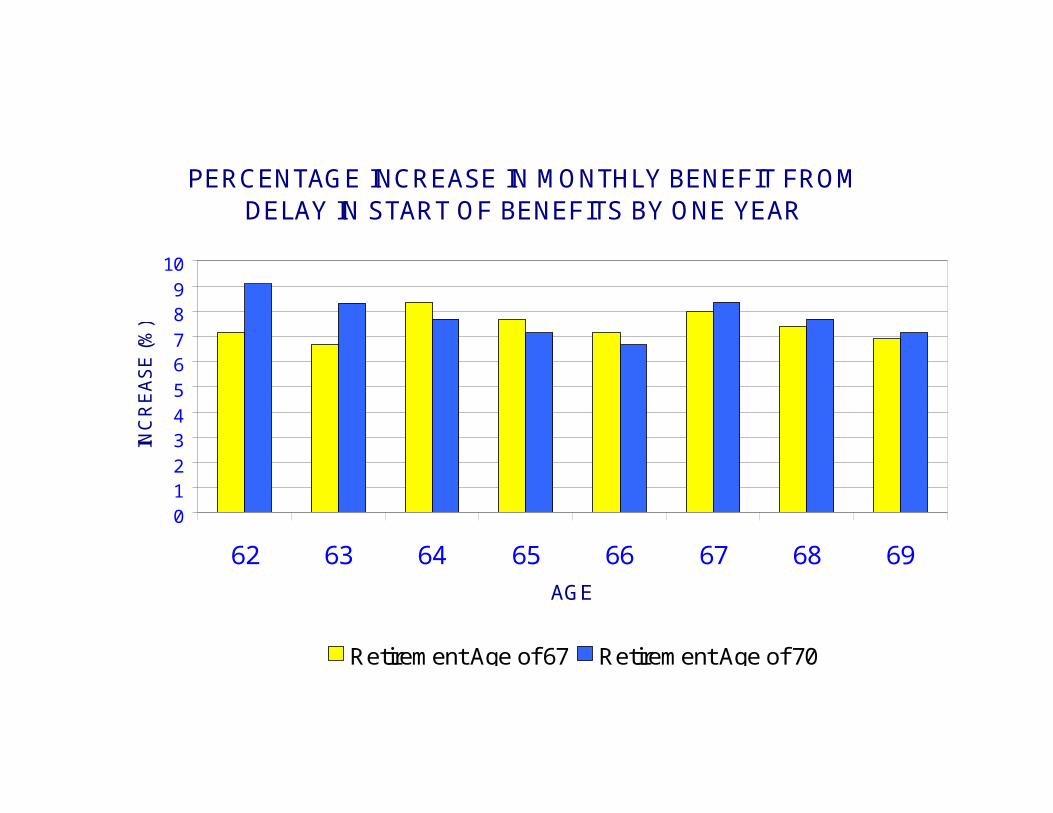

PERCENTAGE INCREASE IN MONTHLY BENEFIT FROM DELAY IN START OF BENEFITS BY ONE YEAR

0

1

2

3

4

5

6

7

8

9

62 63 64 65 66 67 68 69

AGE

INC

RE

AS

E (%

)

Retirement Age of 67

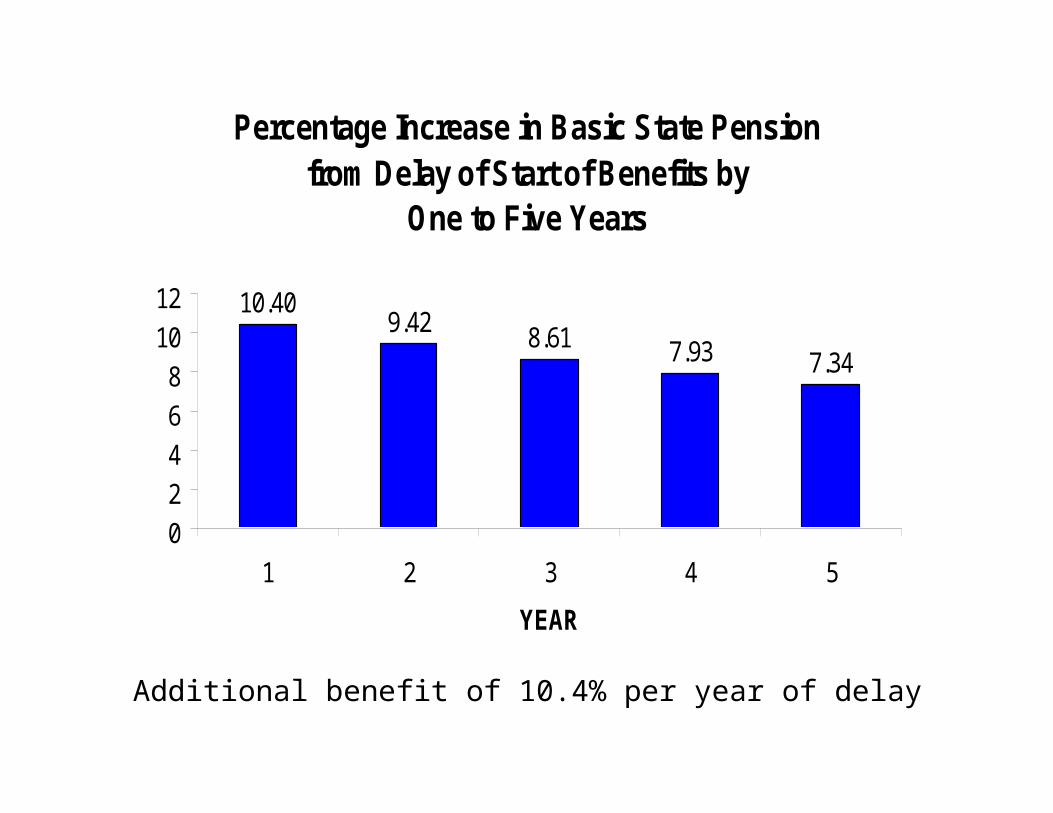

Additional benefit of 10.4% per year of delay

Percentage Increase in Basic State Pension from Delay of Start of Benefits by

One to Five Years

9.42 8.61 7.93 7.34

10.40

0

2

4

6

8

10

12

1 2 3 4 5

YEAR

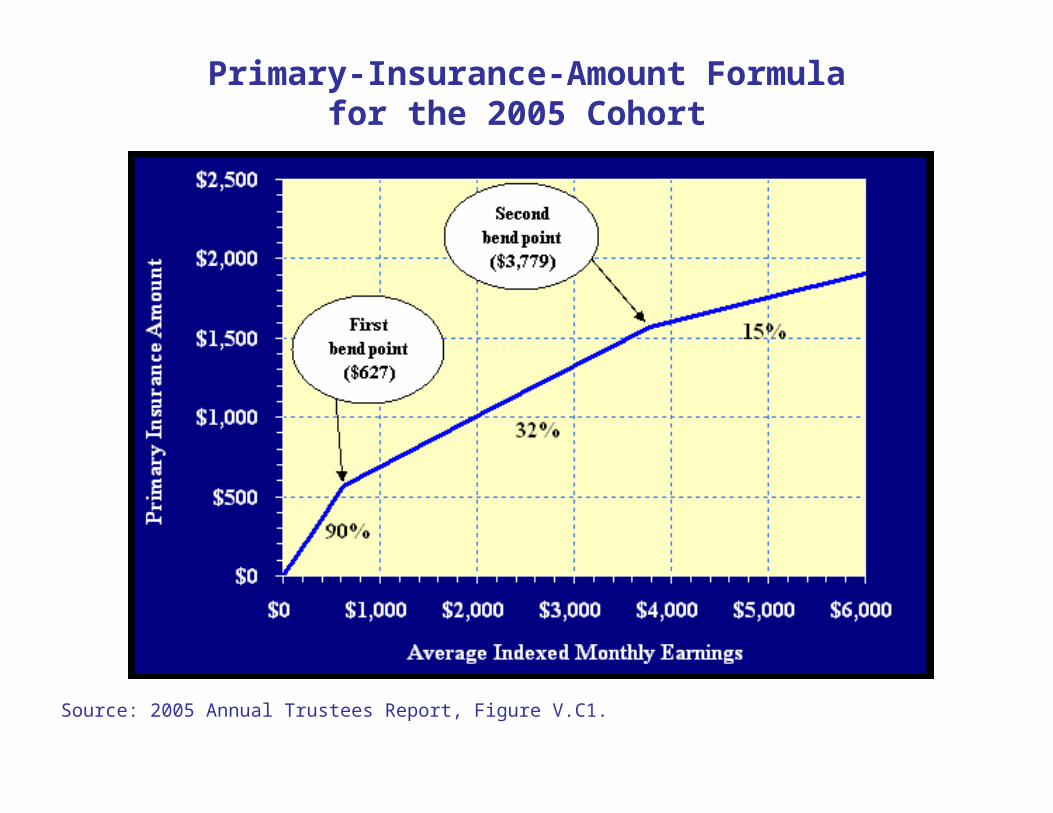

Primary-Insurance-Amount Formulafor the 2005 Cohort

Source: 2005 Annual Trustees Report, Figure V.C1.

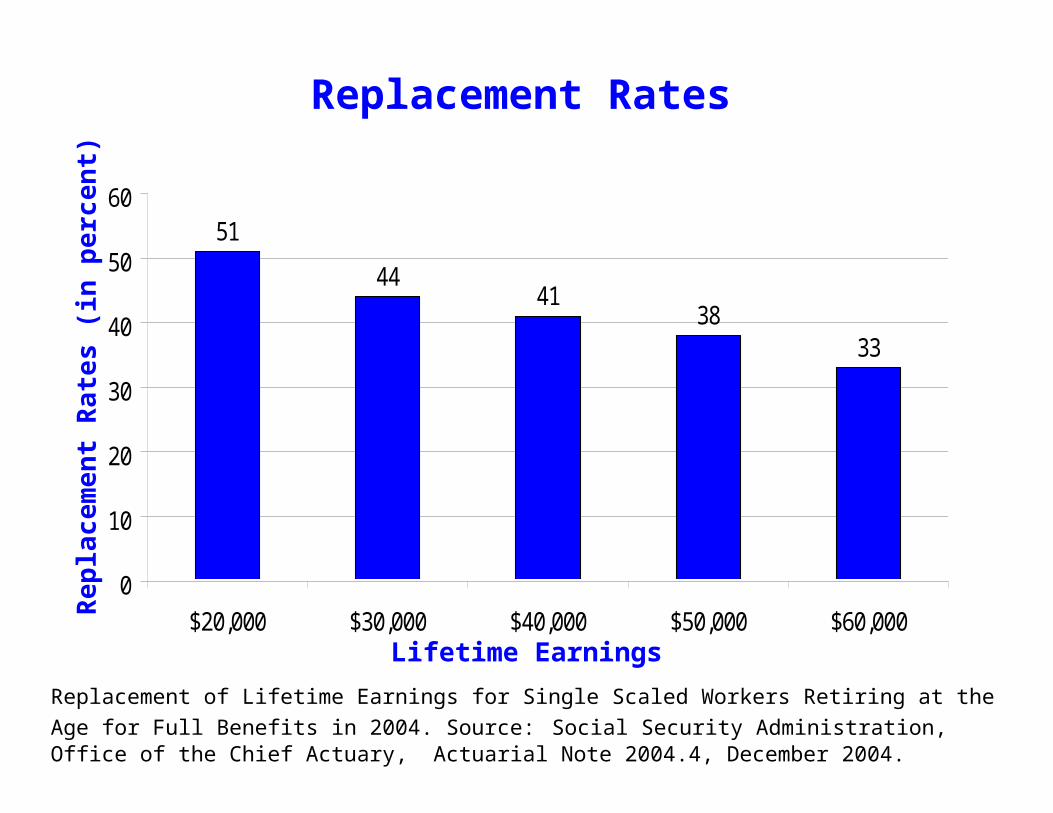

51

4441

3833

0

10

20

30

40

50

60

$20,000 $30,000 $40,000 $50,000 $60,000

Replacement RatesR

ep

lac

em

en

t R

ate

s (

in p

erce

nt)

Lifetime Earnings

Replacement of Lifetime Earnings for Single Scaled Workers Retiring at the Age for Full Benefits in

2004. Source: Social Security Administration, Office of the Chief Actuary, Actuarial Note 2004.4, December 2004.

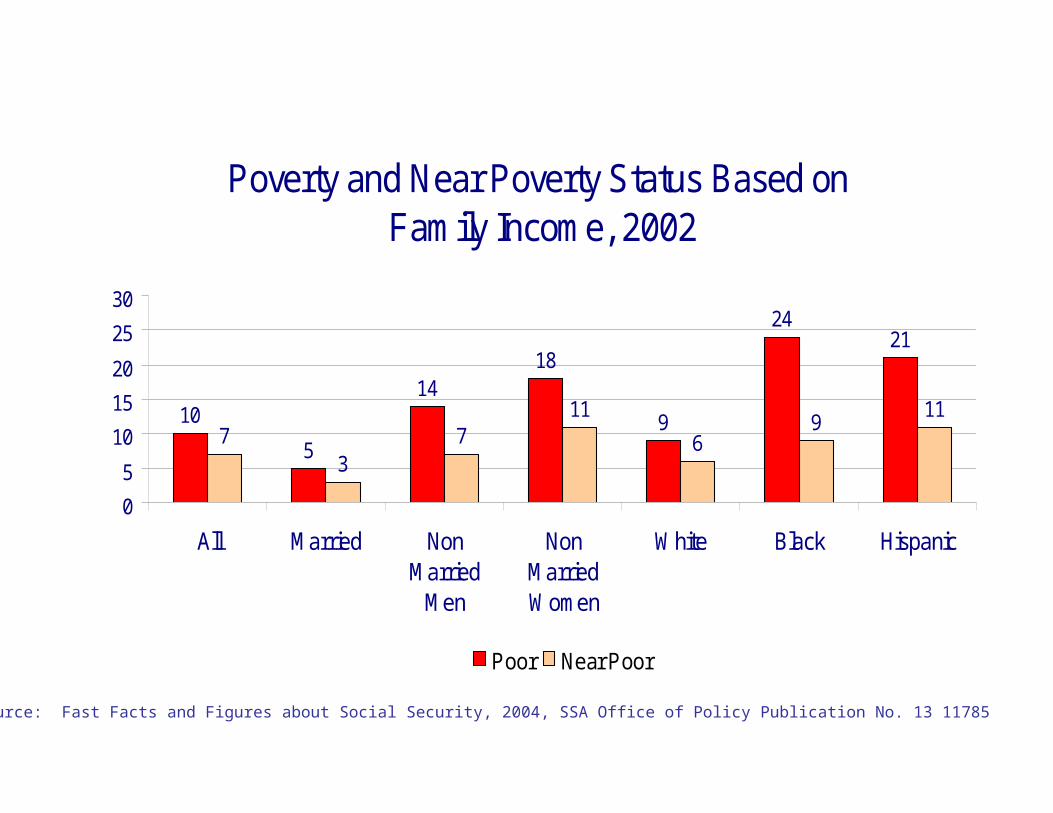

Poverty and Near Poverty Status Based on Family Income, 2002

10

5

1418

9

2421

73

711

69

11

0

5

10

15

20

25

30

All Married NonMarried

Men

NonMarriedWomen

White Black Hispanic

Poor Near Poor

Source: Fast Facts and Figures about Social Security, 2004, SSA Office of Policy Publication No. 13 11785

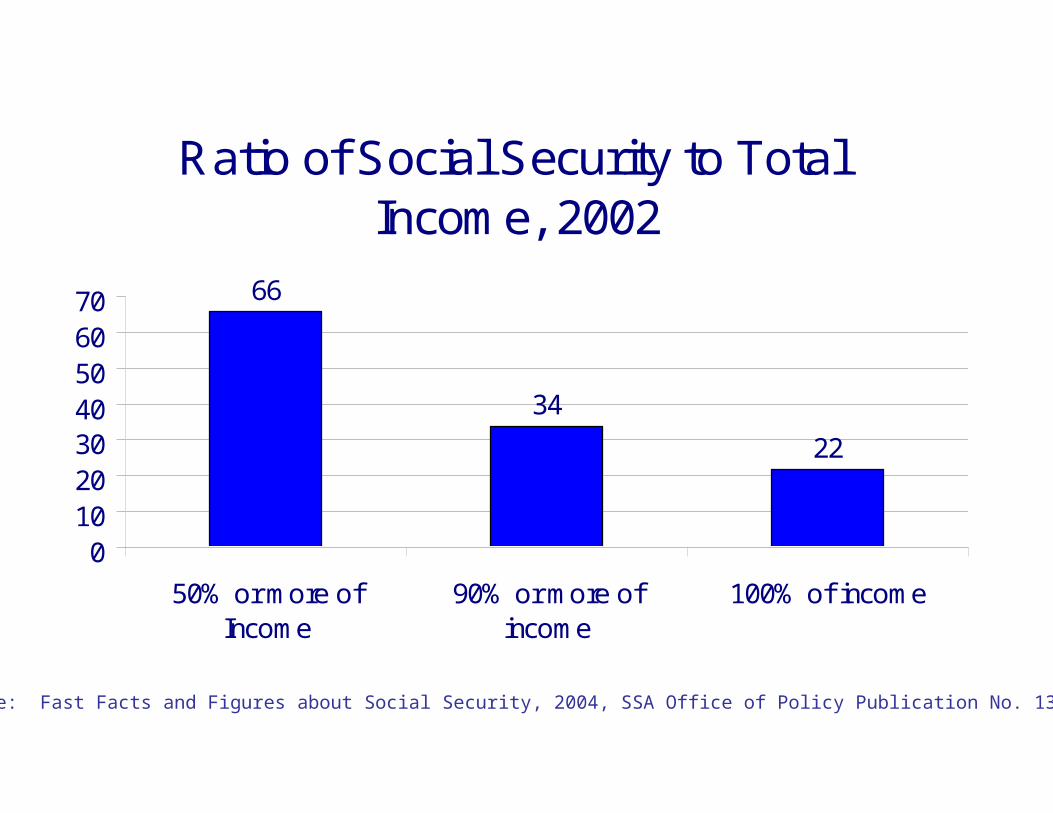

Ratio of Social Security to Total Income, 2002

66

34

22

010203040506070

50% or more ofIncome

90% or more ofincome

100% of income

Source: Fast Facts and Figures about Social Security, 2004, SSA Office of Policy Publication No. 13 11785

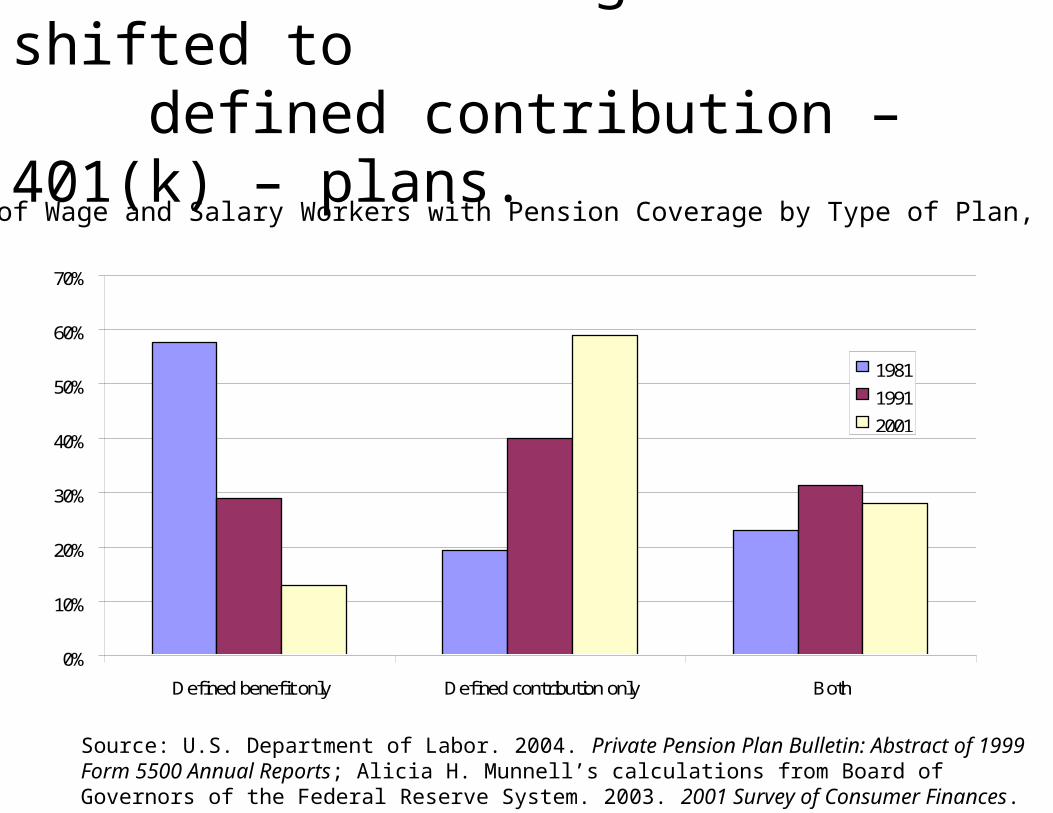

Pension coverage has shifted to defined contribution – 401(k) – plans.

Percent of Wage and Salary Workers with Pension Coverage by Type of Plan, 1981-2001

Source: U.S. Department of Labor. 2004. Private Pension Plan Bulletin: Abstract of 1999 Form 5500 Annual Reports; Alicia H. Munnell’s calculations from Board of Governors of the Federal Reserve System. 2003. 2001 Survey of Consumer Finances.

0%

10%

20%

30%

40%

50%

60%

70%

Defined benefit only Defined contribution only Both

1981

1991

2001

President BushSTATE OF THE UNION ADDRESS

February 2, 2005

“Right now, a set portion of the money you earn is taken out of your paycheck to pay for the Social Security benefits of today's retirees. If you are a younger worker, I believe you should be able to set aside part of that money in your own retirement account, so you can build a nest egg for your own future.”

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

2041

2043

2045

2047

2049

2051

2053

2055

2057

2059

2061

2063

2065

2067

2069

Per

cen

t o

f p

ayro

ll

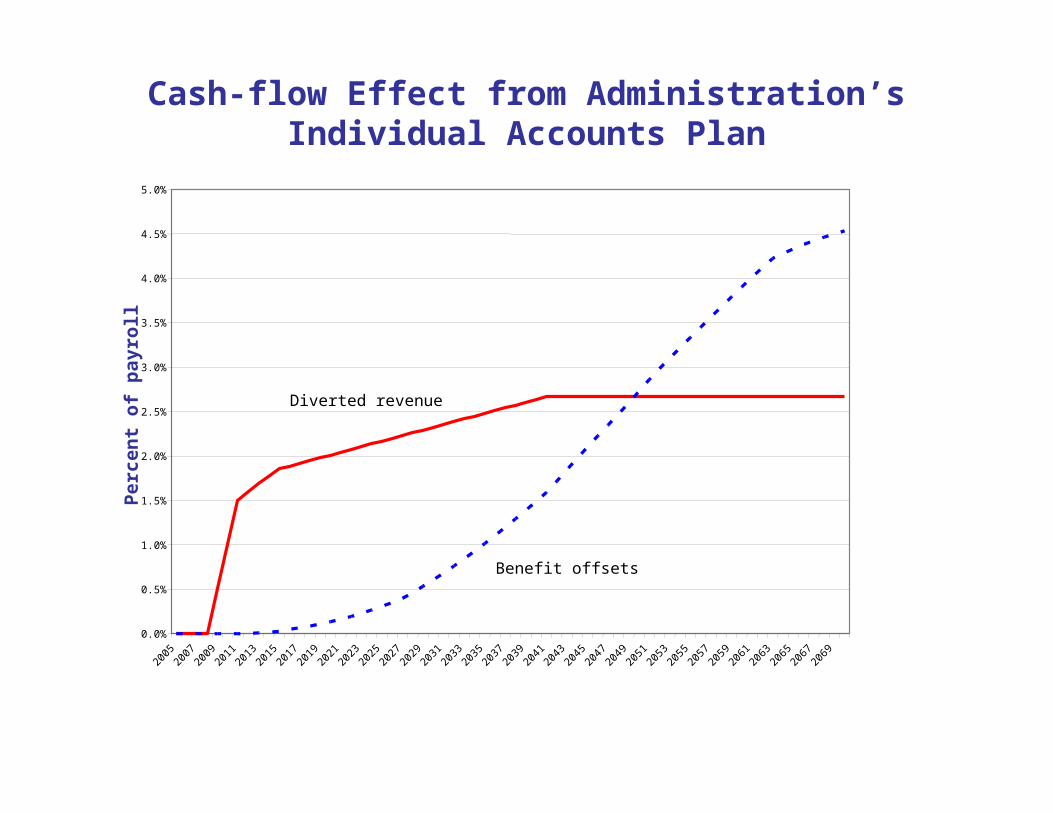

Diverted revenue

Benefit offsets

Cash-flow Effect from Administration’sIndividual Accounts Plan

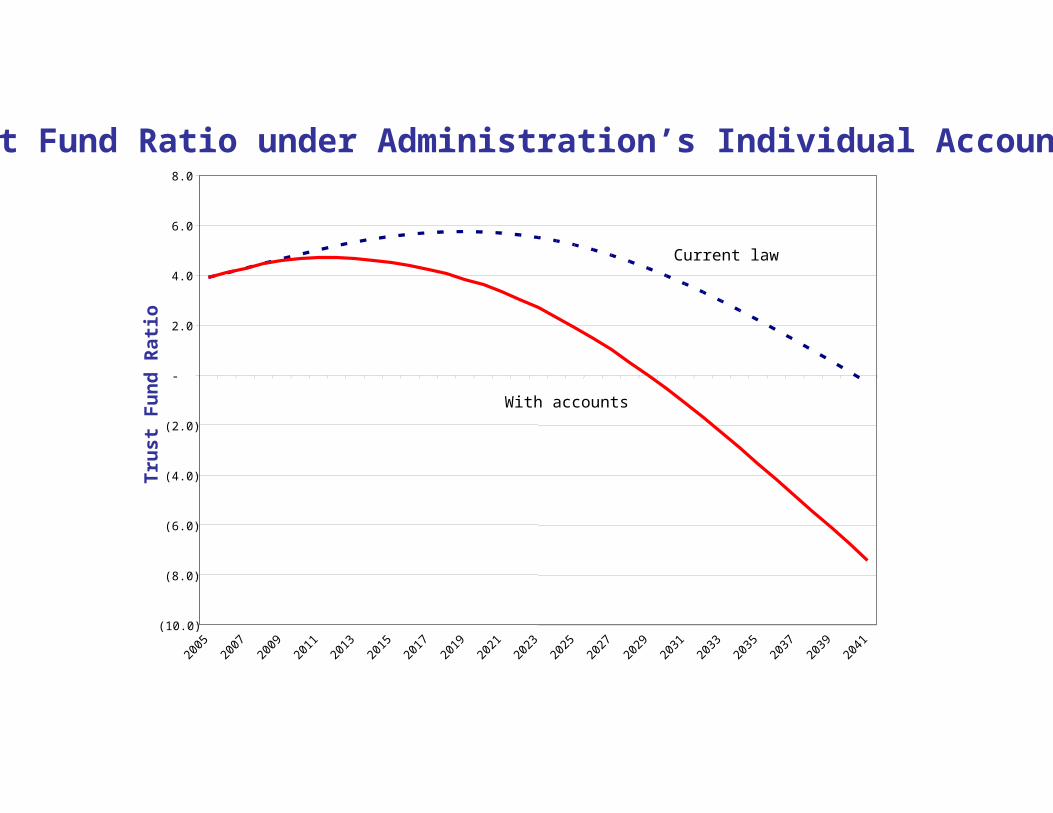

Trust Fund Ratio under Administration’s Individual Account Plan

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

8.0

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

2041

Tru

st F

un

d R

ati

o

Current law

With accounts

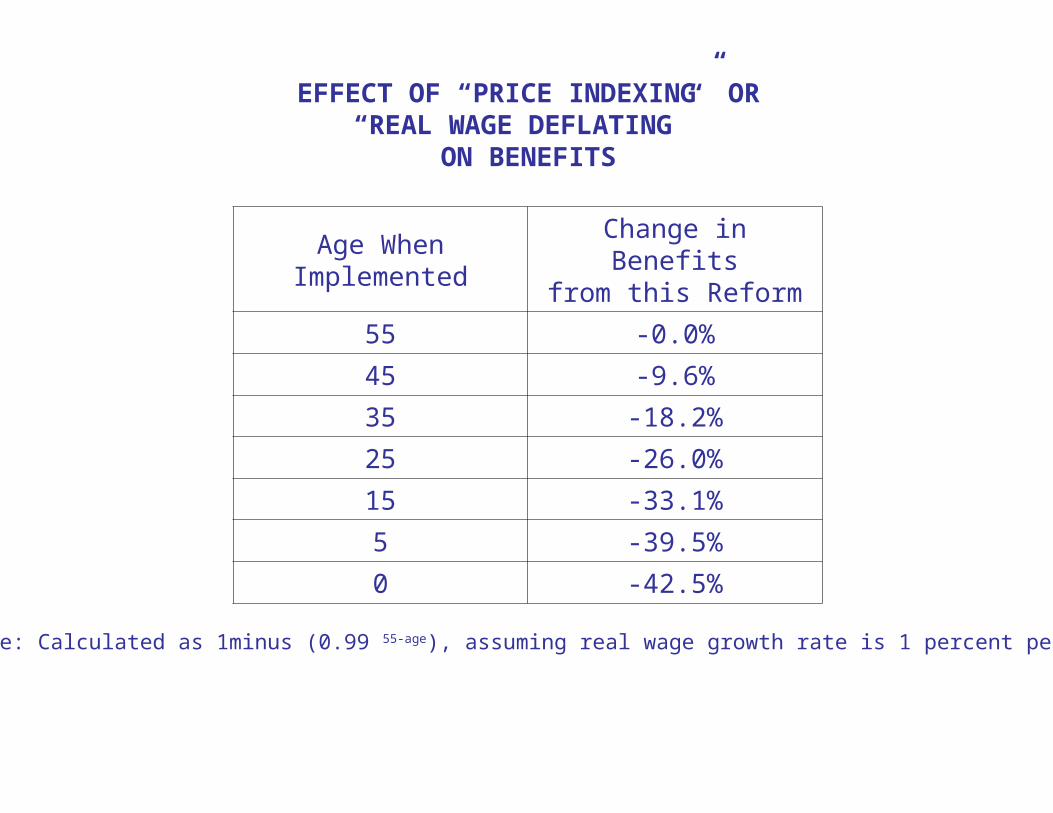

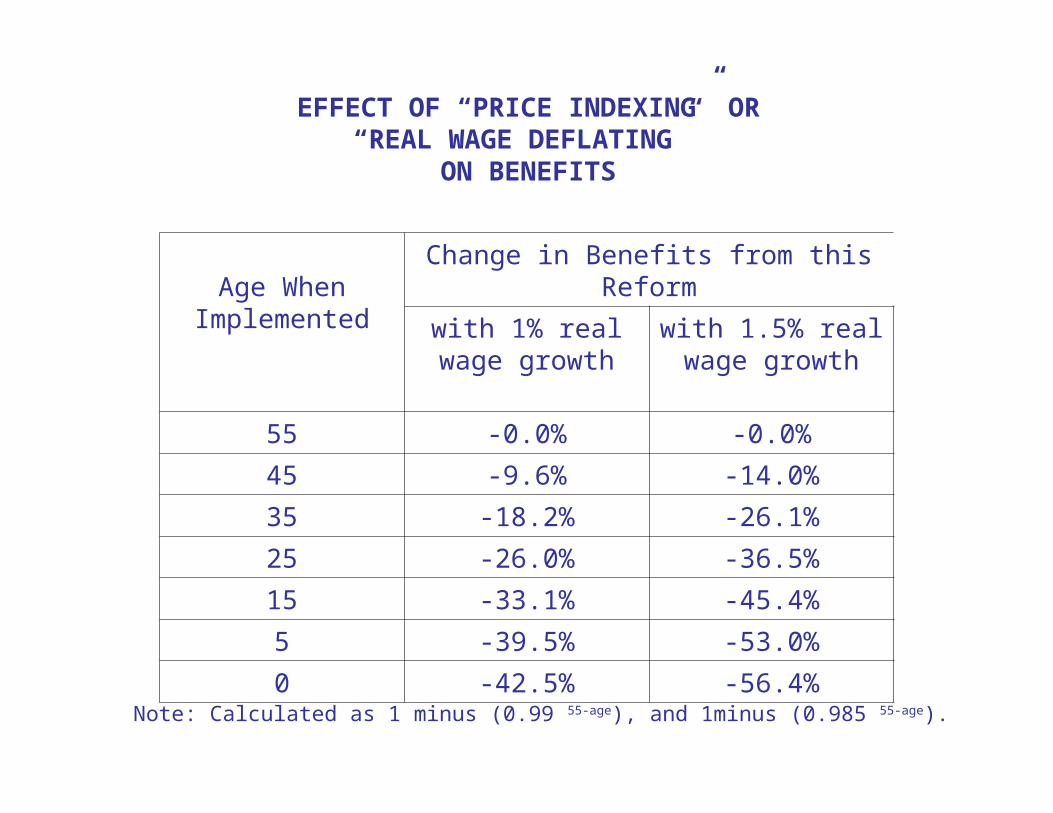

EFFECT OF “PRICE INDEXING” OR“REAL WAGE DEFLATING”

ON BENEFITS

Age WhenImplemented

Change in Benefitsfrom this Reform

55 -0.0%

45 -9.6%

35 -18.2%

25 -26.0%

15 -33.1%

5 -39.5%

0 -42.5%

Note: Calculated as 1minus (0.99 55-age), assuming real wage growth rate is 1 percent per year.

EFFECT OF “PRICE INDEXING” OR“REAL WAGE DEFLATING”

ON BENEFITS

Age WhenImplemented

Change in Benefits from this Reform

with 1% real wage growth

with 1.5% real wage growth

55 -0.0% -0.0%

45 -9.6% -14.0%

35 -18.2% -26.1%

25 -26.0% -36.5%

15 -33.1% -45.4%

5 -39.5% -53.0%

0 -42.5% -56.4%

Note: Calculated as 1 minus (0.99 55-age), and 1minus (0.985 55-age).

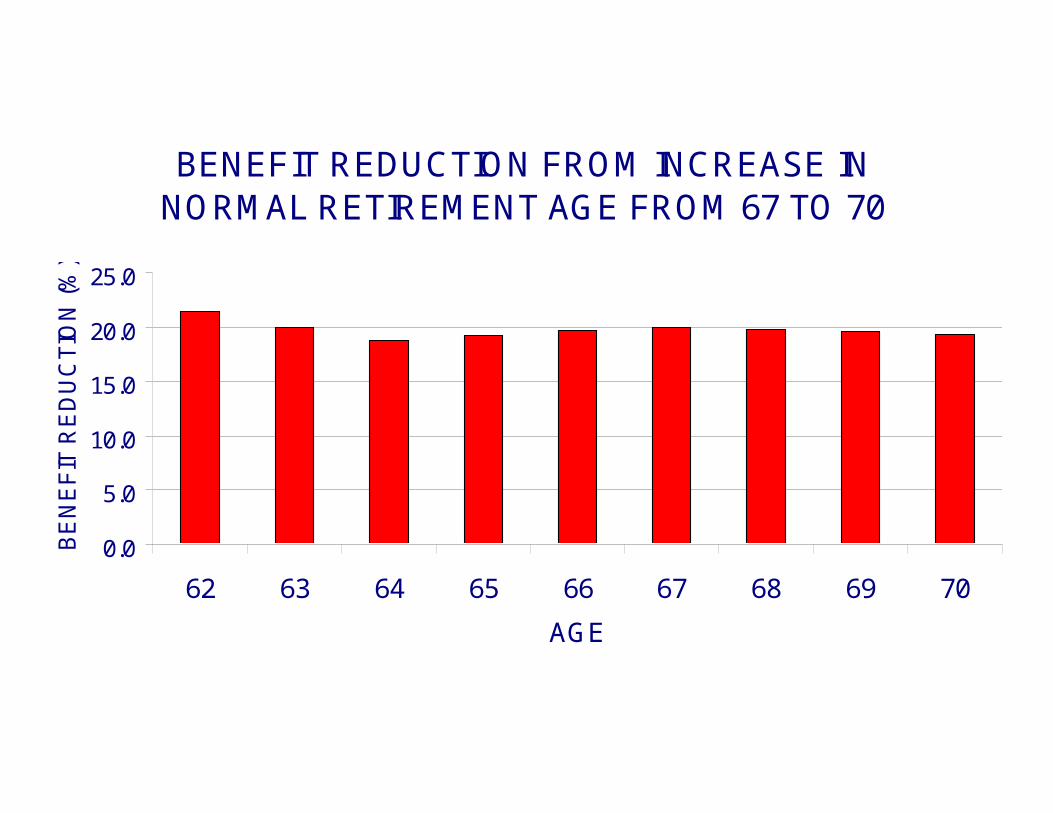

BENEFIT REDUCTION FROM INCREASE INNORMAL RETIREMENT AGE FROM 67 TO 70

0.0

5.0

10.0

15.0

20.0

25.0

62 63 64 65 66 67 68 69 70

AGE

BE

NE

FIT

RE

DU

CT

ION

(%

)

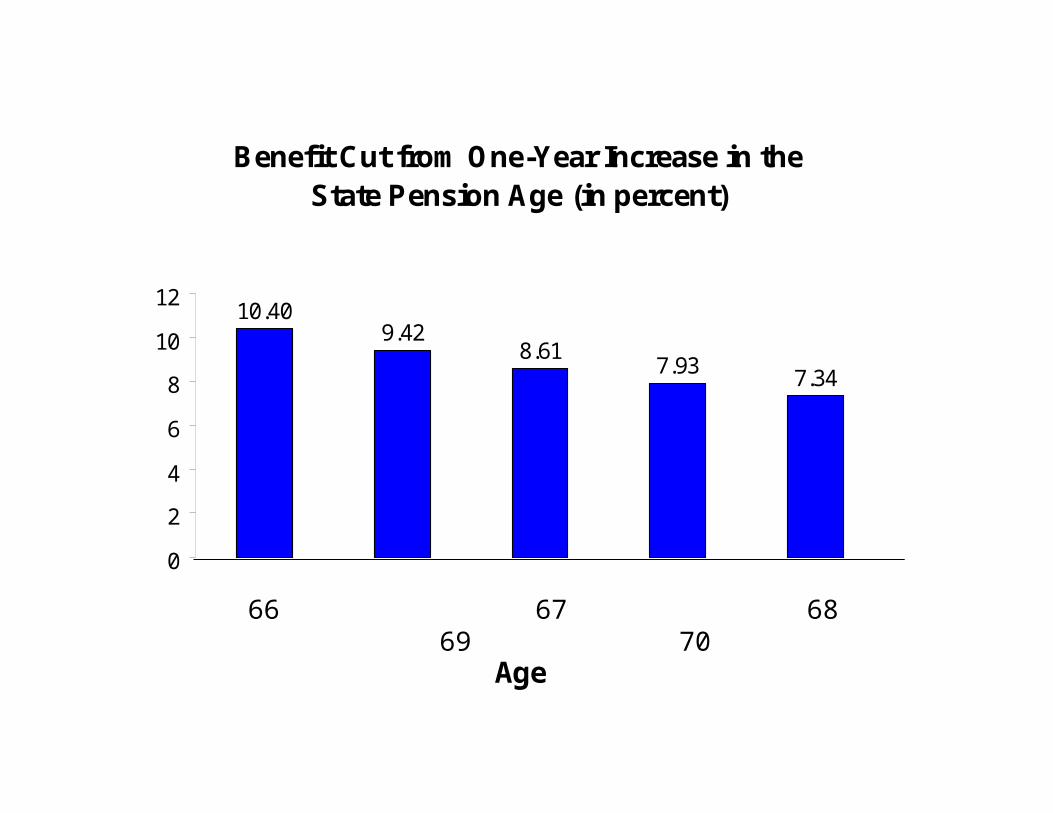

66 67 68 69 70

Age

Benefit Cut from One-Year Increase in the State Pension Age (in percent)

9.428.61

7.93 7.34

10.40

0

2

4

6

8

10

12

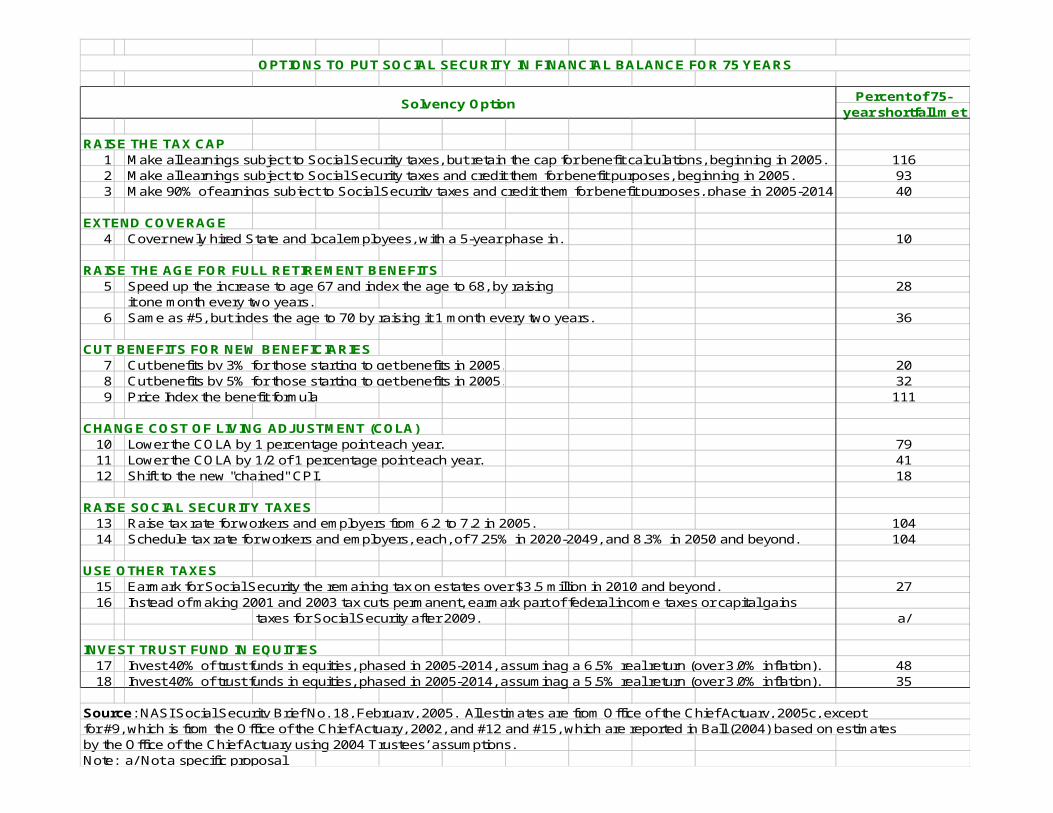

Percent of 75-year shortfall met

RAISE THE TAX CAP1 Make all earnings subject to Social Security taxes, but retain the cap for benefit calculations, beginning in 2005. 1162 Make all earnings subject to Social Security taxes and credit them for benefit purposes, beginning in 2005. 933 Make 90% of earnings subject to Social Security taxes and credit them for benefit purposes, phase in 2005-2014. 40

EXTEND COVERAGE4 Cover newly hired State and local employees, with a 5-year phase in. 10

RAISE THE AGE FOR FULL RETIREMENT BENEFITS5 Speed up the increase to age 67 and index the age to 68, by raising 28

it one month every two years.6 Same as #5, but indes the age to 70 by raising it 1 month every two years. 36

CUT BENEFITS FOR NEW BENEFICIARIES7 Cut benefits by 3% for those starting to get benefits in 2005. 208 Cut benefits by 5% for those starting to get benefits in 2005. 329 Price Index the benefit formula 111

CHANGE COST OF LIVING ADJUSTMENT (COLA)10 Lower the COLA by 1 percentage point each year. 7911 Lower the COLA by 1/2 of 1 percentage point each year. 4112 Shift to the new "chained" CPI. 18

RAISE SOCIAL SECURITY TAXES13 Raise tax rate for workers and employers from 6.2 to 7.2 in 2005. 10414 Schedule tax rate for workers and employers, each, of 7.25% in 2020-2049, and 8.3% in 2050 and beyond. 104

USE OTHER TAXES15 Earmark for Social Security the remaining tax on estates over $3.5 million in 2010 and beyond. 2716 Instead of making 2001 and 2003 tax cuts permanent, earmark part of federal income taxes or capital gains

taxes for Social Security after 2009. a/

INVEST TRUST FUND IN EQUITIES17 Invest 40% of trust funds in equities, phased in 2005-2014, assuminag a 6.5% real return (over 3.0% inflation). 4818 Invest 40% of trust funds in equities, phased in 2005-2014, assuminag a 5.5% real return (over 3.0% inflation). 35

Source: NASI Social Security Brief No. 18, February, 2005. All estimates are from Office of the Chief Actuary, 2005c, exceptfor #9, which is from the Office of the Chief Actuary, 2002, and #12 and #15, which are reported in Ball (2004) based on estimatesby the Office of the Chief Actuary using 2004 Trustees’ assumptions. Note: a/ Not a specific proposal

Solvency Option

OPTIONS TO PUT SOCIAL SECURITY IN FINANCIAL BALANCE FOR 75 YEARS

BENEFIT LEVELS WITH NORMAL RETIREMENT AGES OF 67 AND 70

0

20

40

60

80

100

120

140

62 63 64 65 66 67 68 68 70

AGE

retire at 67 retire at 70

BE

NE

FIT

LE

VE

L (

in %

)

PERCENTAGE INCREASE IN MONTHLY BENEFIT FROM DELAY IN START OF BENEFITS BY ONE YEAR

0123456789

10

62 63 64 65 66 67 68 69

AGE

INC

RE

AS

E (

%)

Retirement Age of 67 Retirement Age of 70

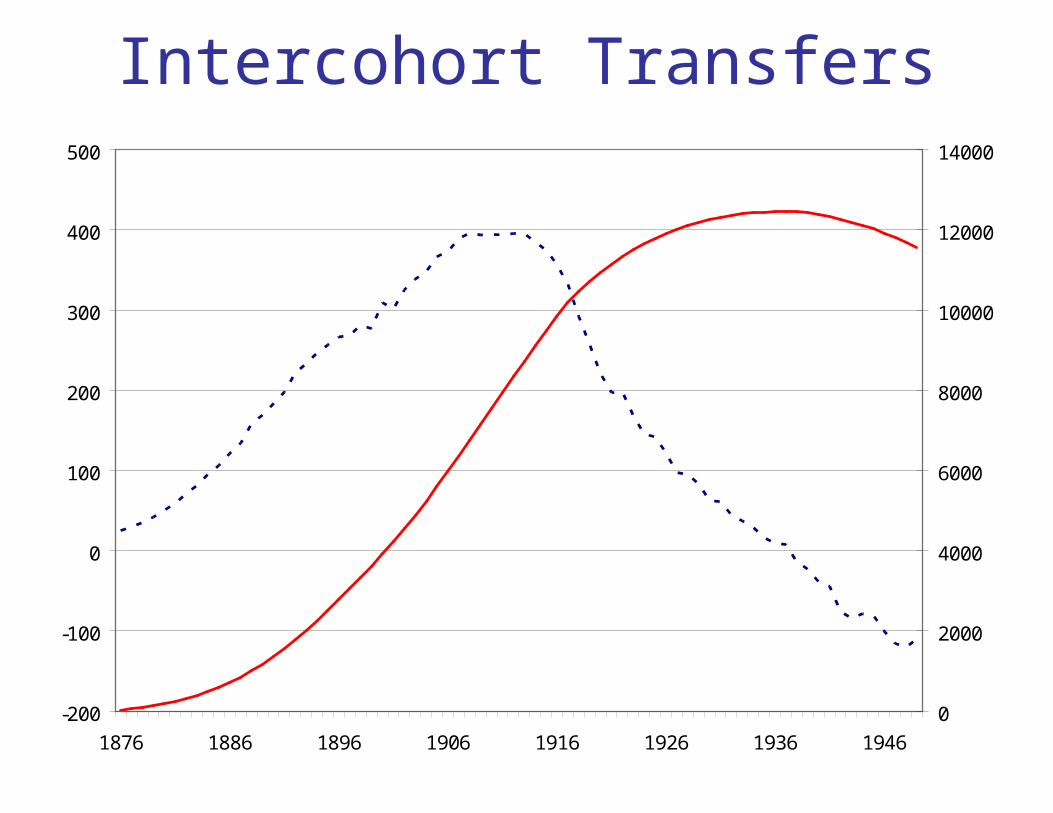

Intercohort Transfers

-200

-100

0

100

200

300

400

500

1876 1886 1896 1906 1916 1926 1936 1946

0

2000

4000

6000

8000

10000

12000

14000Annual Amount: PV $2002, billions Cumulative: PV $2002, billions

Net transfers to cohort born in

each year

Cumulative Sum: net transfers to all cohorts

born in and prior to each year

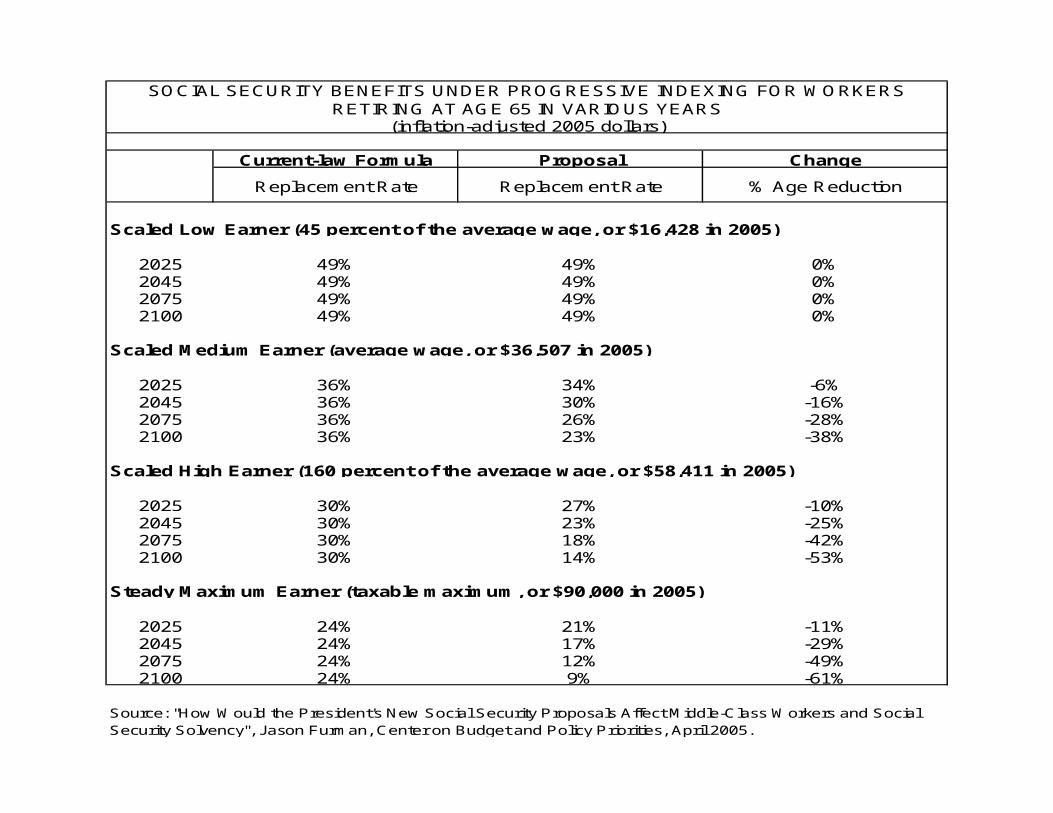

Scaled Low Earner (45 percent of the average wage, or $16,428 in 2005)

2025204520752100

Scaled Medium Earner (average wage, or $36,507 in 2005)

2025204520752100

Scaled High Earner (160 percent of the average wage, or $58,411 in 2005)

2025204520752100

Steady Maximum Earner (taxable maximum, or $90,000 in 2005)

2025204520752100

Source: "How Would the President's New Social Security Proposals Affect Middle-Class Workers and Social Security Solvency", Jason Furman, Center on Budget and Policy Priorities, April 2005.

SOCIAL SECURITY BENEFITS UNDER PROGRESSIVE INDEXING FOR WORKERS RETIRING AT AGE 65 IN VARIOUS YEARS

(inflation-adjusted 2005 dollars)

Current-law Formula Proposal Change

Replacement Rate Replacement Rate % Age Reduction

49% 0%49%49%49%49%

0%0%0%

36% -6%

49%49%49%

34%30%26%23%

-16%-28%-38%

30% -10%

36%36%36%

27%23%18%14%

-25%-42%-53%

24% -11%

30%30%30%

21%17%12%9%

-29%-49%-61%

24%24%24%