Embed Size (px)

Citation preview

BMO Government Finance Conference| Spring 2016 1

Region of Peel

BMO Government Finance

Conference

May 2016

BMO Government Finance Conference| Spring 2016 2

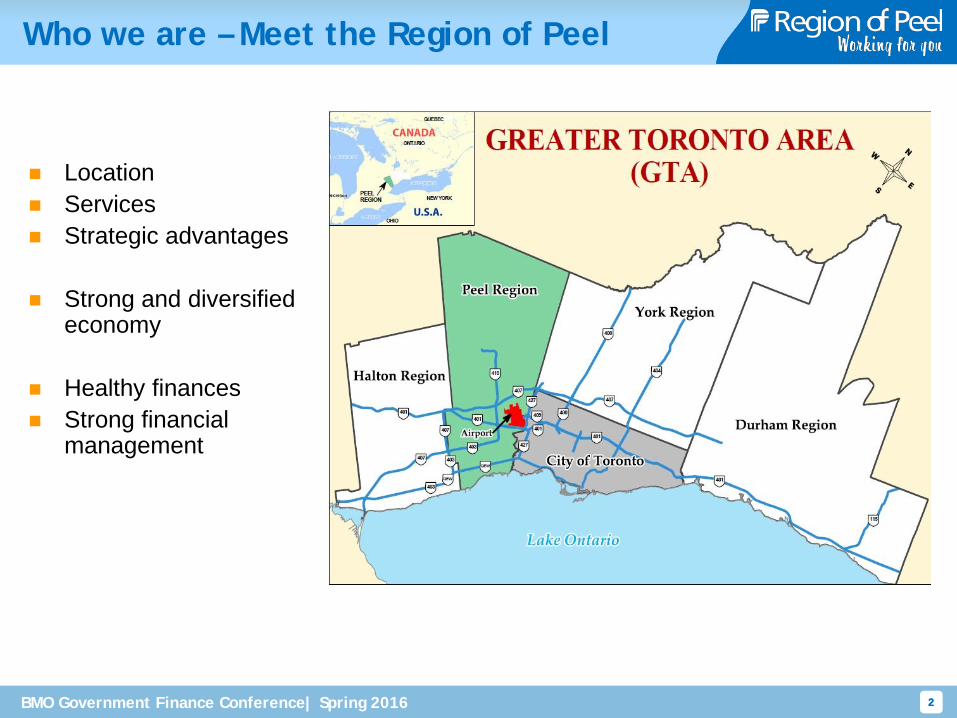

Who we are – Meet the Region of Peel

2

Location Services Strategic advantages

Strong and diversified

economy

Healthy finances Strong financial

management

BMO Government Finance Conference| Spring 2016 3

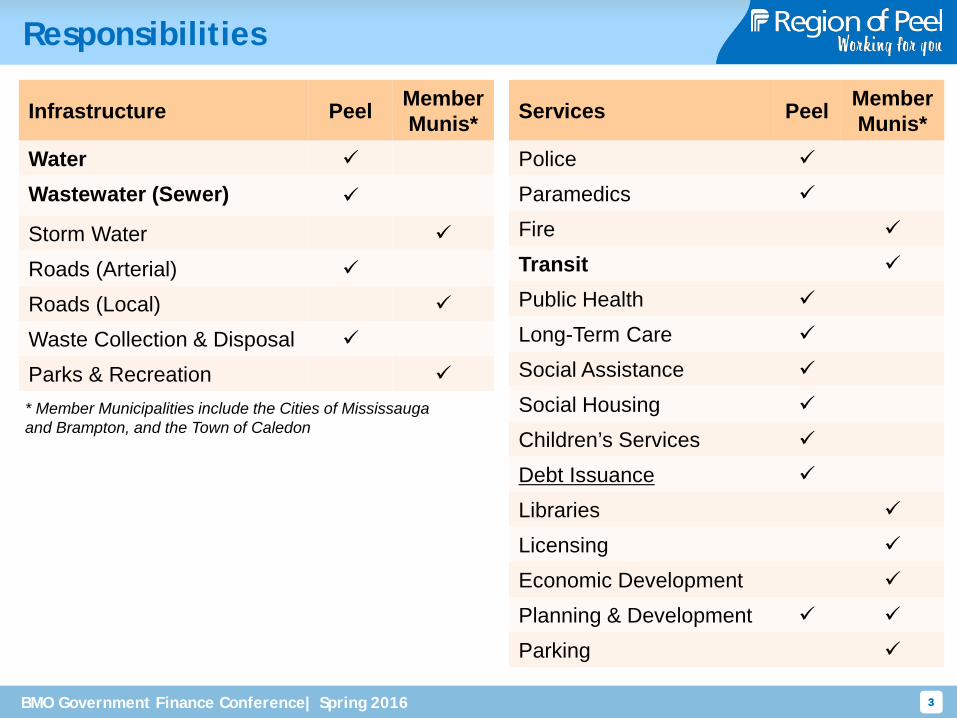

Responsibilities

3

Infrastructure Peel Member Munis*

Water Wastewater (Sewer)

Storm Water Roads (Arterial) Roads (Local) Waste Collection & Disposal Parks & Recreation * Member Municipalities include the Cities of Mississauga and Brampton, and the Town of Caledon

Services Peel Member Munis*

Police Paramedics Fire Transit Public Health Long-Term Care Social Assistance Social Housing Children’s Services Debt Issuance Libraries Licensing Economic Development Planning & Development Parking

BMO Government Finance Conference| Spring 2016 4

Governance

4

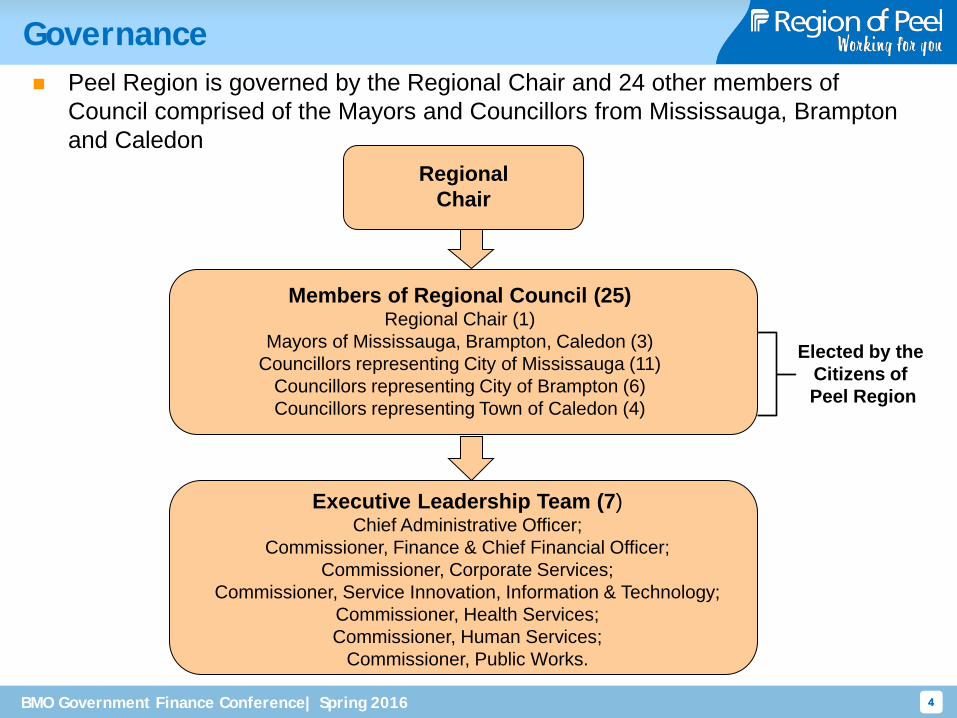

Peel Region is governed by the Regional Chair and 24 other members of Council comprised of the Mayors and Councillors from Mississauga, Brampton and Caledon

Regional Chair

Members of Regional Council (25) Regional Chair (1)

Mayors of Mississauga, Brampton, Caledon (3) Councillors representing City of Mississauga (11)

Councillors representing City of Brampton (6) Councillors representing Town of Caledon (4)

Executive Leadership Team (7) Chief Administrative Officer;

Commissioner, Finance & Chief Financial Officer; Commissioner, Corporate Services;

Commissioner, Service Innovation, Information & Technology; Commissioner, Health Services; Commissioner, Human Services;

Commissioner, Public Works.

Elected by the Citizens of Peel Region

BMO Government Finance Conference| Spring 2016 5

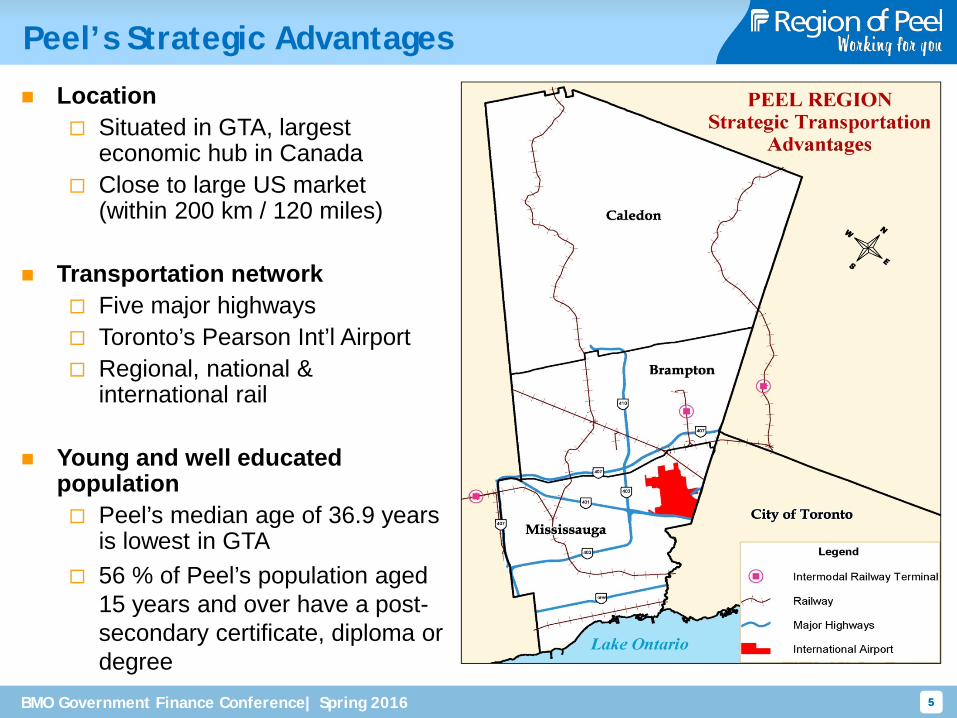

Peel’s Strategic Advantages

5

Location Situated in GTA, largest

economic hub in Canada Close to large US market

(within 200 km / 120 miles)

Transportation network Five major highways Toronto’s Pearson Int’l Airport Regional, national &

international rail

Young and well educated population Peel’s median age of 36.9 years

is lowest in GTA 56 % of Peel’s population aged

15 years and over have a post-secondary certificate, diploma or degree

BMO Government Finance Conference| Spring 2016 6

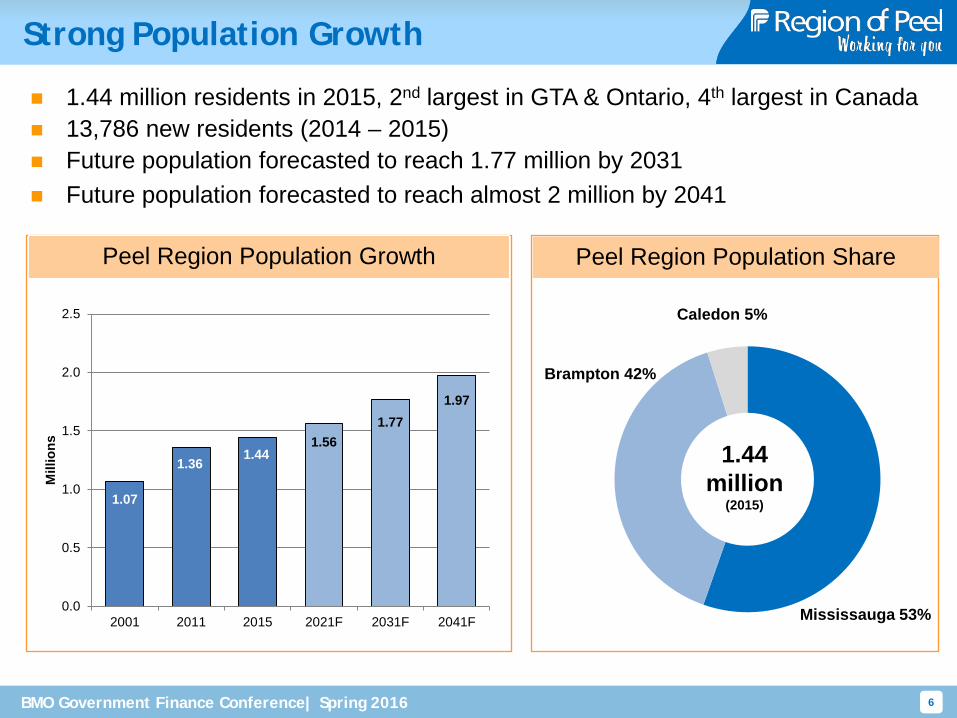

1.44 million residents in 2015, 2nd largest in GTA & Ontario, 4th largest in Canada 13,786 new residents (2014 – 2015) Future population forecasted to reach 1.77 million by 2031 Future population forecasted to reach almost 2 million by 2041

Peel Region Population Growth

1.07

1.36 1.44

1.56 1.77

1.97

0.0

0.5

1.0

1.5

2.0

2.5

2001 2011 2015 2021F 2031F 2041F

Mill

ions

Brampton 42%

1.44 million

(2015)

Peel Region Population Share

Caledon 5%

Mississauga 53%

Strong Population Growth

BMO Government Finance Conference| Spring 2016 7

Diversified Labour Market

7

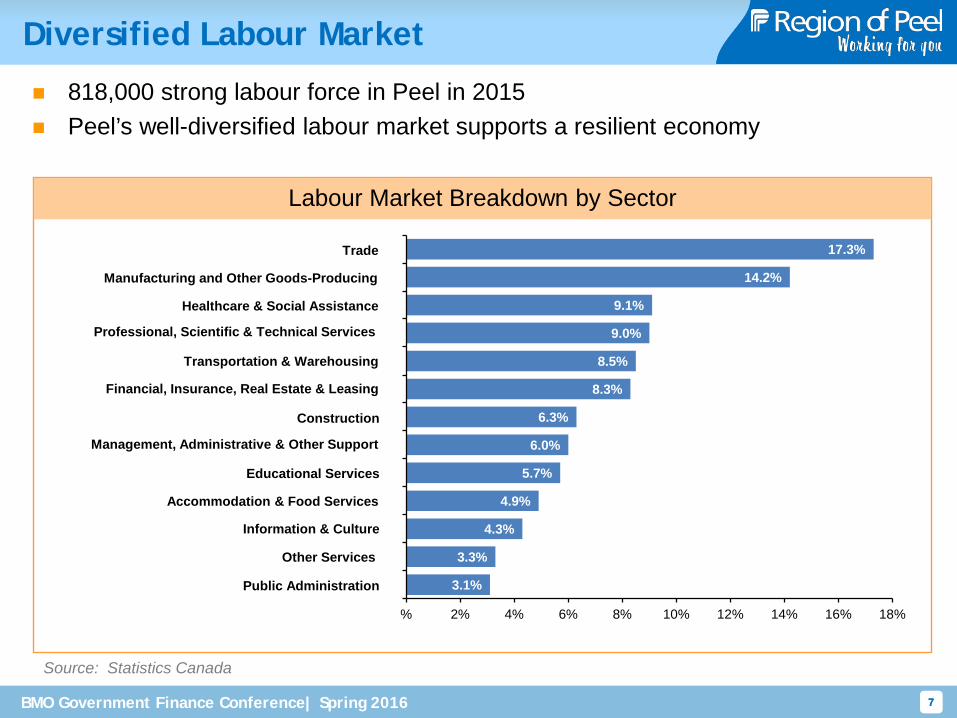

818,000 strong labour force in Peel in 2015 Peel’s well-diversified labour market supports a resilient economy

Source: Statistics Canada

Trade

Transportation & Warehousing

Financial, Insurance, Real Estate & Leasing

Healthcare & Social Assistance

Construction

Professional, Scientific & Technical Services

Information & Culture

Accommodation & Food Services

Public Administration

Other Services

3.1%

3.3%

4.3%

4.9%

5.7%

6.0%

6.3%

8.3%

8.5%

9.0%

9.1%

14.2%

17.3%

% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Labour Market Breakdown by Sector

Educational Services

Manufacturing and Other Goods-Producing

Management, Administrative & Other Support

BMO Government Finance Conference| Spring 2016 8

Labour Market Conditions

8

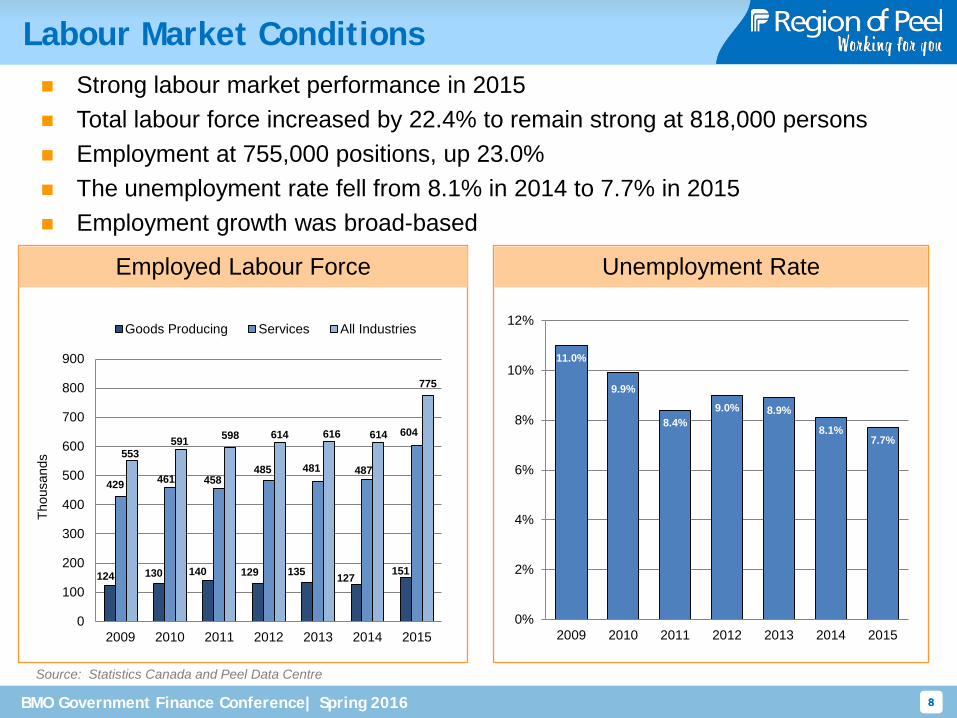

Strong labour market performance in 2015 Total labour force increased by 22.4% to remain strong at 818,000 persons Employment at 755,000 positions, up 23.0% The unemployment rate fell from 8.1% in 2014 to 7.7% in 2015 Employment growth was broad-based

Source: Statistics Canada and Peel Data Centre

Employed Labour Force Unemployment Rate

11.0%

9.9%

8.4% 9.0% 8.9%

8.1% 7.7%

0%

2%

4%

6%

8%

10%

12%

2009 2010 2011 2012 2013 2014 2015

124 130 140 129 135 127 151

429 461 458 485 481 487

604

553 591 598 614 616 614

775

0

100

200

300

400

500

600

700

800

900

2009 2010 2011 2012 2013 2014 2015

Thou

sand

s

Goods Producing Services All Industries

BMO Government Finance Conference| Spring 2016 9

Household Income

9

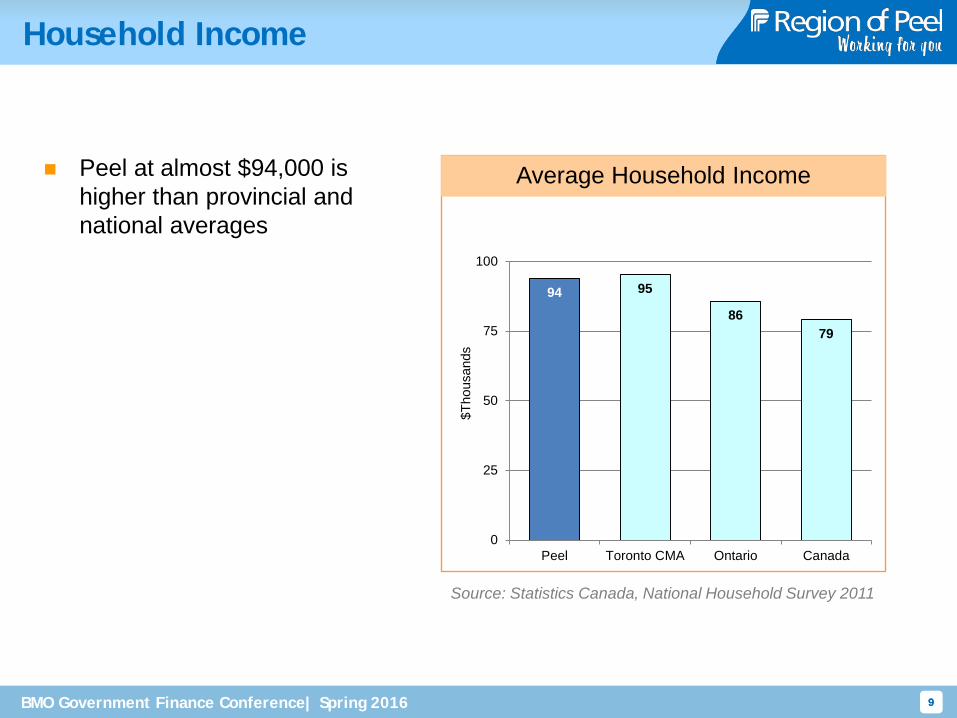

Source: Statistics Canada, National Household Survey 2011

Peel at almost $94,000 is higher than provincial and national averages

Average Household Income

94 95

86 79

0

25

50

75

100

Peel Toronto CMA Ontario Canada

$Tho

usan

ds

BMO Government Finance Conference| Spring 2016 10

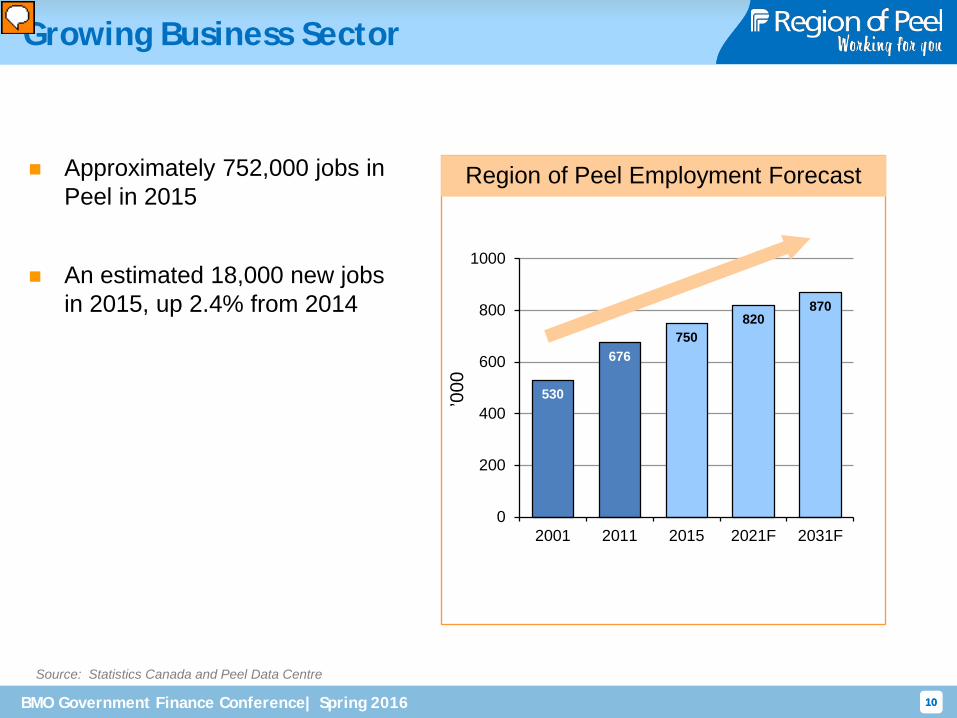

Growing Business Sector

10

Source: Statistics Canada and Peel Data Centre

Region of Peel Employment Forecast

530

676 750

820 870

0

200

400

600

800

1000

2001 2011 2015 2021F 2031F

’000

Approximately 752,000 jobs in Peel in 2015

An estimated 18,000 new jobs in 2015, up 2.4% from 2014

BMO Government Finance Conference| Spring 2016 11 11

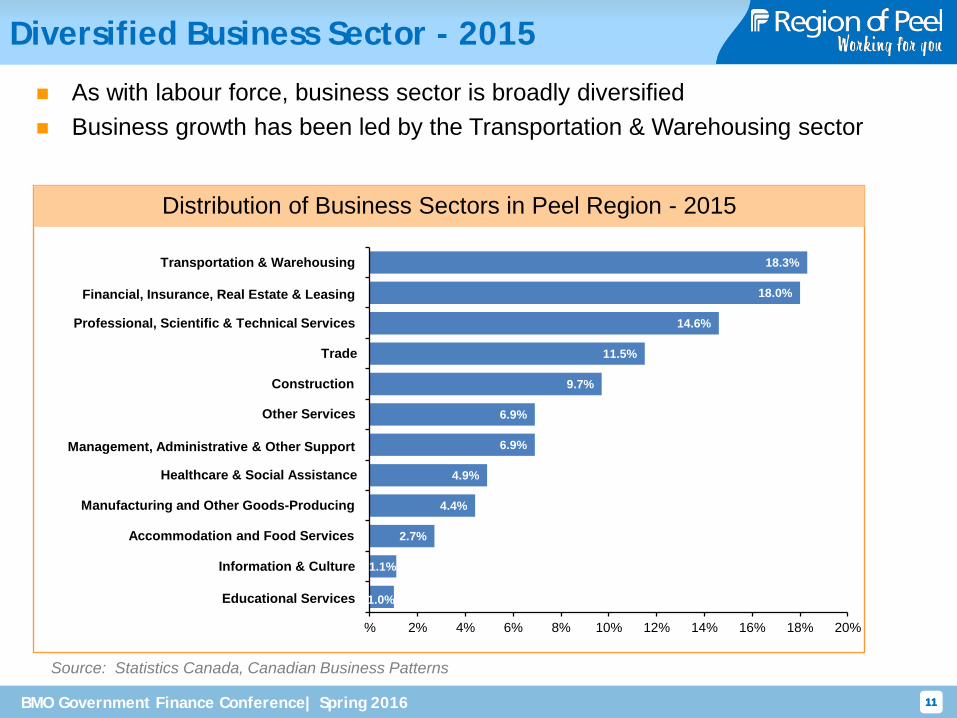

Diversified Business Sector - 2015

11

Source: Statistics Canada, Canadian Business Patterns

Distribution of Business Sectors in Peel Region - 2015

1.0%

1.1%

2.7%

4.4%

4.9%

6.9%

6.9%

9.7%

11.5%

14.6%

18.0%

18.3%

% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Trade

Manufacturing and Other Goods-Producing

Transportation & Warehousing

Professional, Scientific & Technical Services

Financial, Insurance, Real Estate & Leasing

Construction

Management, Administrative & Other Support

Educational Services

Healthcare & Social Assistance

Accommodation and Food Services

Information & Culture

As with labour force, business sector is broadly diversified Business growth has been led by the Transportation & Warehousing sector

Other Services

BMO Government Finance Conference| Spring 2016 12

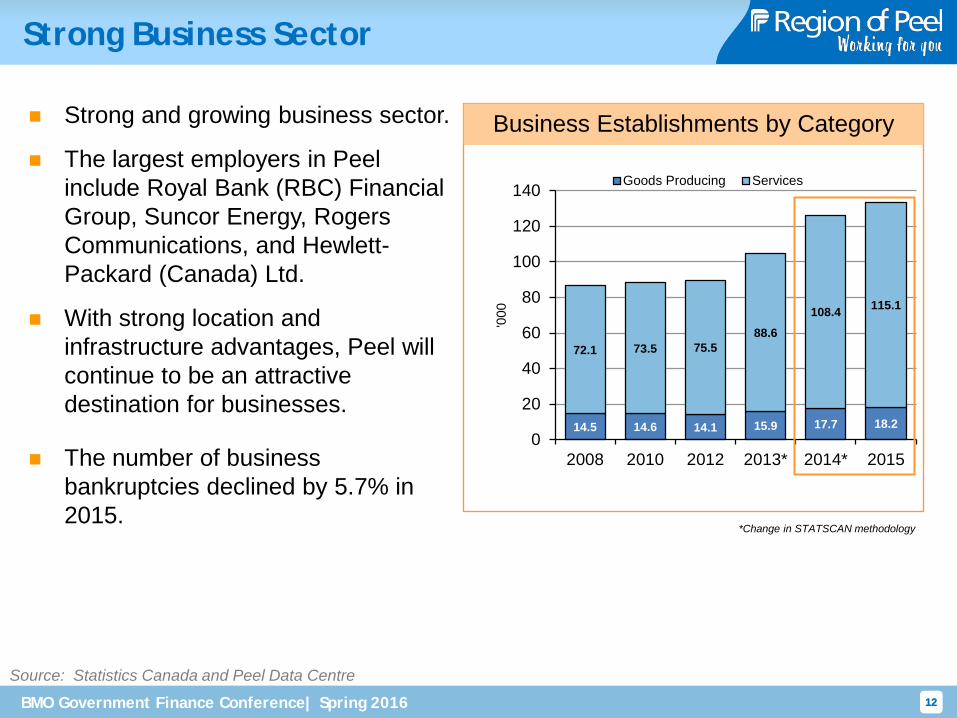

Strong Business Sector

12

Strong and growing business sector.

The largest employers in Peel include Royal Bank (RBC) Financial Group, Suncor Energy, Rogers Communications, and Hewlett-Packard (Canada) Ltd.

With strong location and infrastructure advantages, Peel will continue to be an attractive destination for businesses.

The number of business bankruptcies declined by 5.7% in 2015.

Source: Statistics Canada and Peel Data Centre

Business Establishments by Category

14.5 14.6 14.1 15.9 17.7 18.2

72.1 73.5 75.5 88.6

108.4 115.1

0

20

40

60

80

100

120

140

2008 2010 2012 2013* 2014* 2015

'000

Goods Producing Services

*Change in STATSCAN methodology

BMO Government Finance Conference| Spring 2016 13

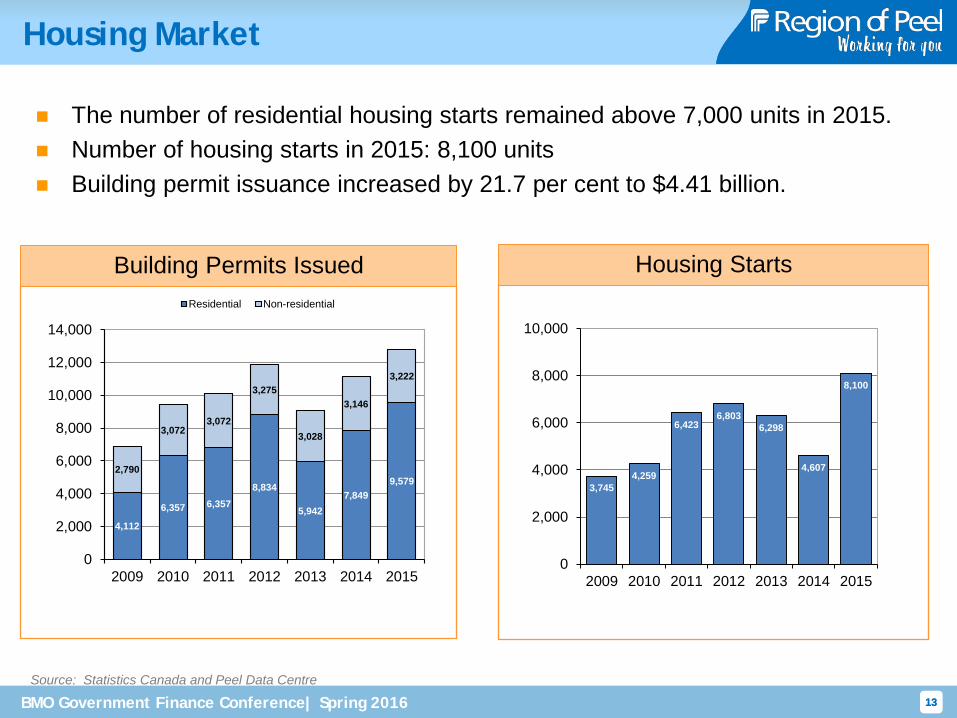

Housing Market

13

Source: Statistics Canada and Peel Data Centre

Building Permits Issued

The number of residential housing starts remained above 7,000 units in 2015. Number of housing starts in 2015: 8,100 units Building permit issuance increased by 21.7 per cent to $4.41 billion.

4,112

6,357 6,357 8,834

5,942 7,849

9,579 2,790

3,072 3,072

3,275

3,028

3,146

3,222

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2009 2010 2011 2012 2013 2014 2015

Residential Non-residential

Housing Starts

3,745 4,259

6,423 6,803

6,298

4,607

8,100

0

2,000

4,000

6,000

8,000

10,000

2009 2010 2011 2012 2013 2014 2015

BMO Government Finance Conference| Spring 2016 14

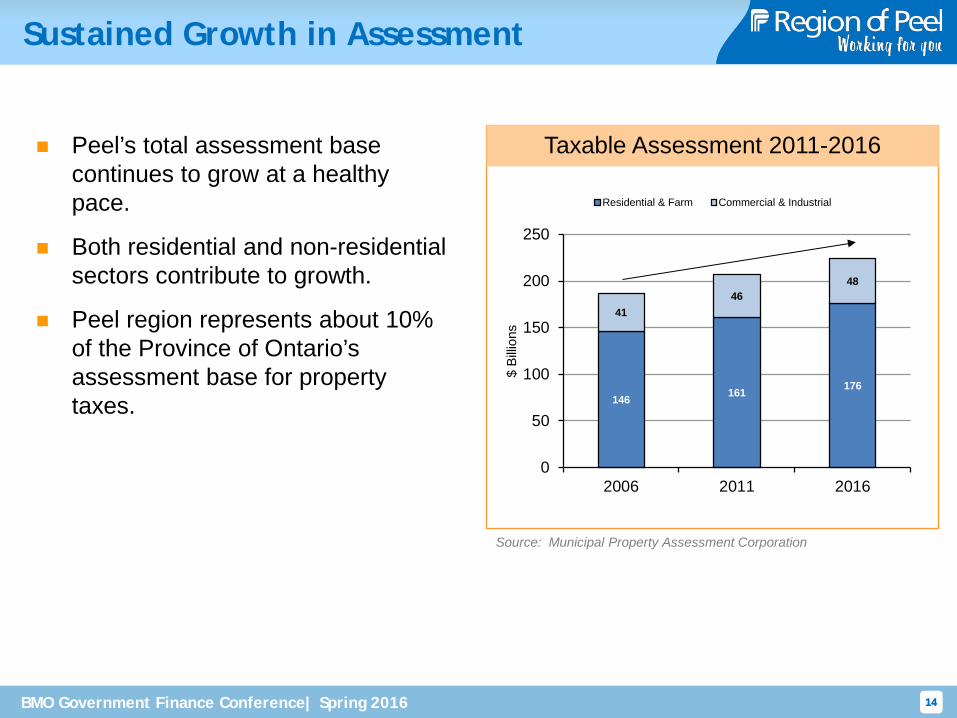

Sustained Growth in Assessment

14

Peel’s total assessment base continues to grow at a healthy pace.

Both residential and non-residential sectors contribute to growth.

Peel region represents about 10% of the Province of Ontario’s assessment base for property taxes.

Taxable Assessment 2011-2016

146 161 176

41 46

48

0

50

100

150

200

250

2006 2011 2016$

Billio

ns

Residential & Farm Commercial & Industrial

Source: Municipal Property Assessment Corporation

BMO Government Finance Conference| Spring 2016 15

Planning Financial Sustainability

Council and Management Actions

Long-term Financial Planning Strategy Term of Council Priority Includes 10 year operating budget model

Commitment to funding infrastructure replacement from reserves Water/wastewater: 3.5% rate increase for reserves in 2015

Phasing out of directly operated childcare centres More contracted out / private sector servicing Eliminated backlog / waitlist

Development Charges By-law Update 2015 Council directed update in 2014 as the 20% threshold was approached Average 13.8% rate increase adopted effective October 5, 2015 Collection of residential DCs for hard services (97% of DC rate) at subdivision

approval expected to offset $100 million in borrowing Changes to process for next update (2018) to include early consultation with area

municipalities and developers in part to minimize debt

BMO Government Finance Conference| Spring 2016

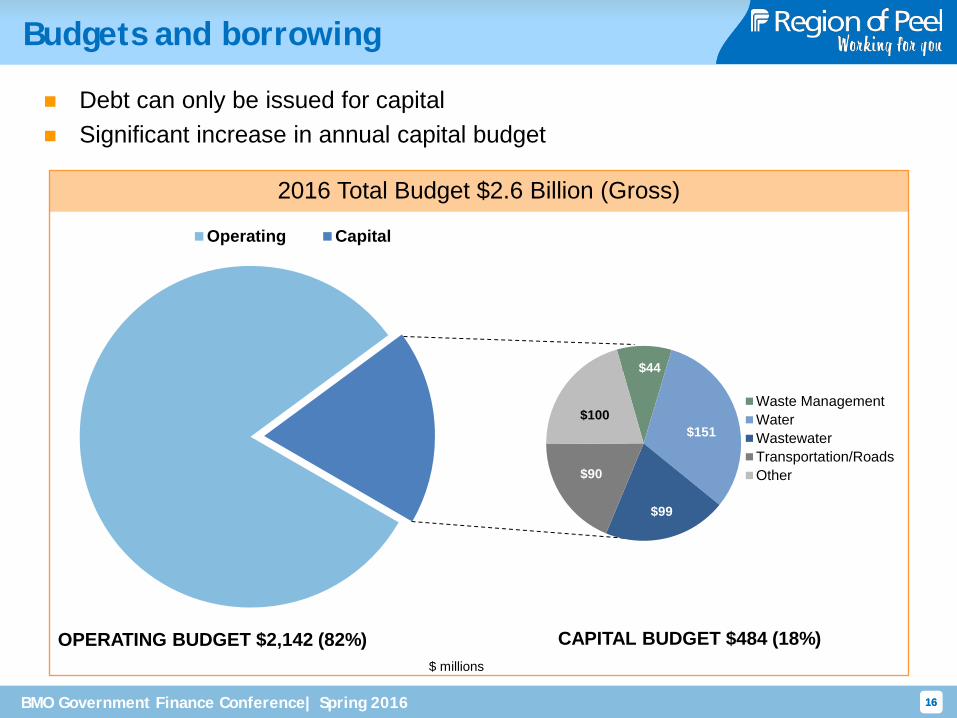

$ millions

CAPITAL BUDGET $484 (18%) OPERATING BUDGET $2,142 (82%)

Operating Capital

$44

$151

$99

$90

$100 Waste ManagementWaterWastewaterTransportation/RoadsOther

16

Budgets and borrowing

16

2016 Total Budget $2.6 Billion (Gross)

Debt can only be issued for capital Significant increase in annual capital budget

BMO Government Finance Conference| Spring 2016 17

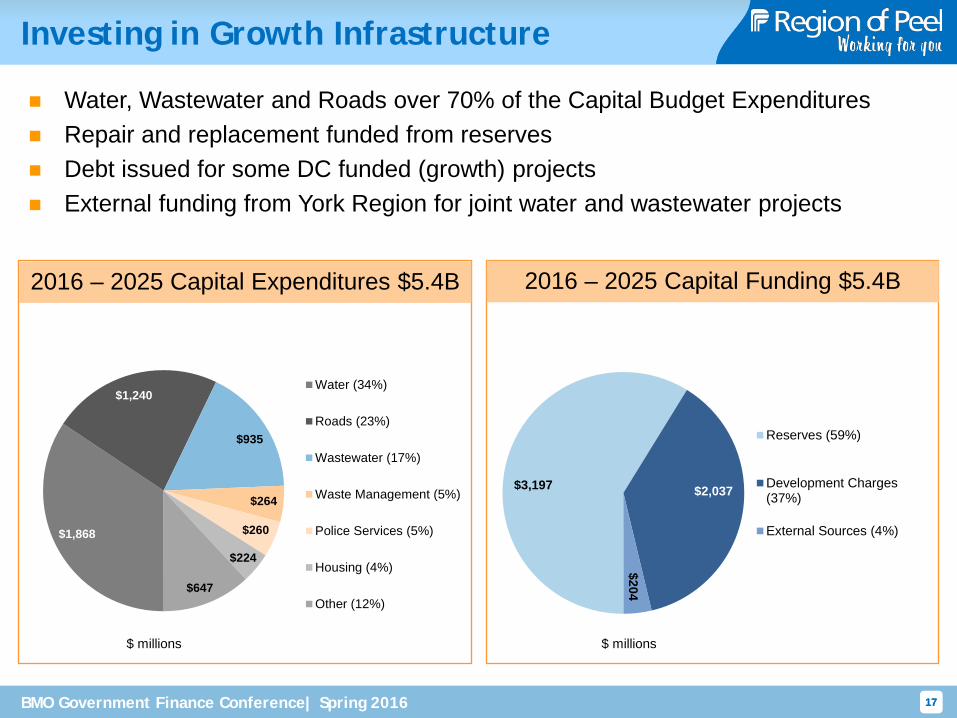

Investing in Growth Infrastructure

17

$1,868

$1,240

$935

$264

$260

$224

$647

Water (34%)

Roads (23%)

Wastewater (17%)

Waste Management (5%)

Police Services (5%)

Housing (4%)

Other (12%)

$3,197 $2,037

$204

Reserves (59%)

Development Charges(37%)

External Sources (4%)

$ millions $ millions

Water, Wastewater and Roads over 70% of the Capital Budget Expenditures Repair and replacement funded from reserves Debt issued for some DC funded (growth) projects External funding from York Region for joint water and wastewater projects

2016 – 2025 Capital Funding $5.4B 2016 – 2025 Capital Expenditures $5.4B

BMO Government Finance Conference| Spring 2016 18 18

Levy DCs against new development to fund growth-related infrastructure (Provincial legislation)

Peel Council: “growth pays for

growth” philosophy to ensure existing tax base not impacted by cost of development

DC rates must be updated at least every 5 years Peel DC by-law updated Sept. 2015

with a new DC by-law review scheduled for early 2018

20% trigger for update approved by Council

Borrowing needs are for long life projects

Water, wastewater, roads funded from DCs

Development Charges (DCs) (a.k.a. System Impact Fees)

BMO Government Finance Conference| Spring 2016 19

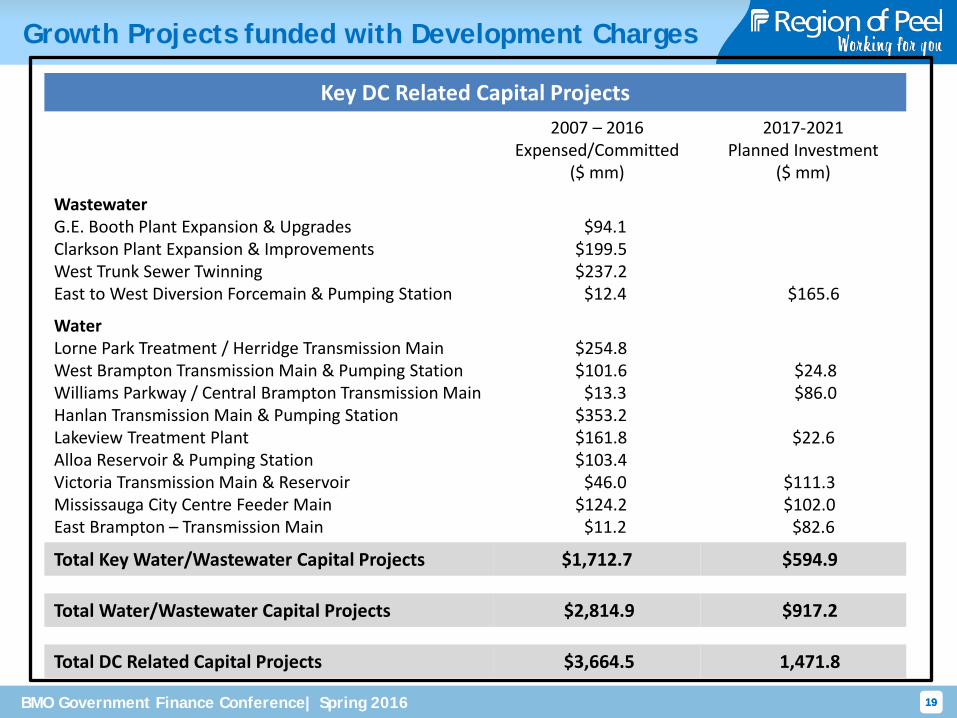

Growth Projects funded with Development Charges

19

Key DC Related Capital Projects 2007 – 2016

Expensed/Committed ($ mm)

2017-2021 Planned Investment

($ mm)

Wastewater G.E. Booth Plant Expansion & Upgrades Clarkson Plant Expansion & Improvements West Trunk Sewer Twinning East to West Diversion Forcemain & Pumping Station

$94.1 $199.5 $237.2 $12.4

$165.6

Water Lorne Park Treatment / Herridge Transmission Main West Brampton Transmission Main & Pumping Station Williams Parkway / Central Brampton Transmission Main Hanlan Transmission Main & Pumping Station Lakeview Treatment Plant Alloa Reservoir & Pumping Station Victoria Transmission Main & Reservoir Mississauga City Centre Feeder Main East Brampton – Transmission Main

$254.8 $101.6 $13.3 $353.2 $161.8 $103.4 $46.0 $124.2 $11.2

$24.8 $86.0

$22.6

$111.3 $102.0 $82.6

Total Key Water/Wastewater Capital Projects $1,712.7 $594.9

Total Water/Wastewater Capital Projects $2,814.9 $917.2

Total DC Related Capital Projects $3,664.5 1,471.8

BMO Government Finance Conference| Spring 2016 20

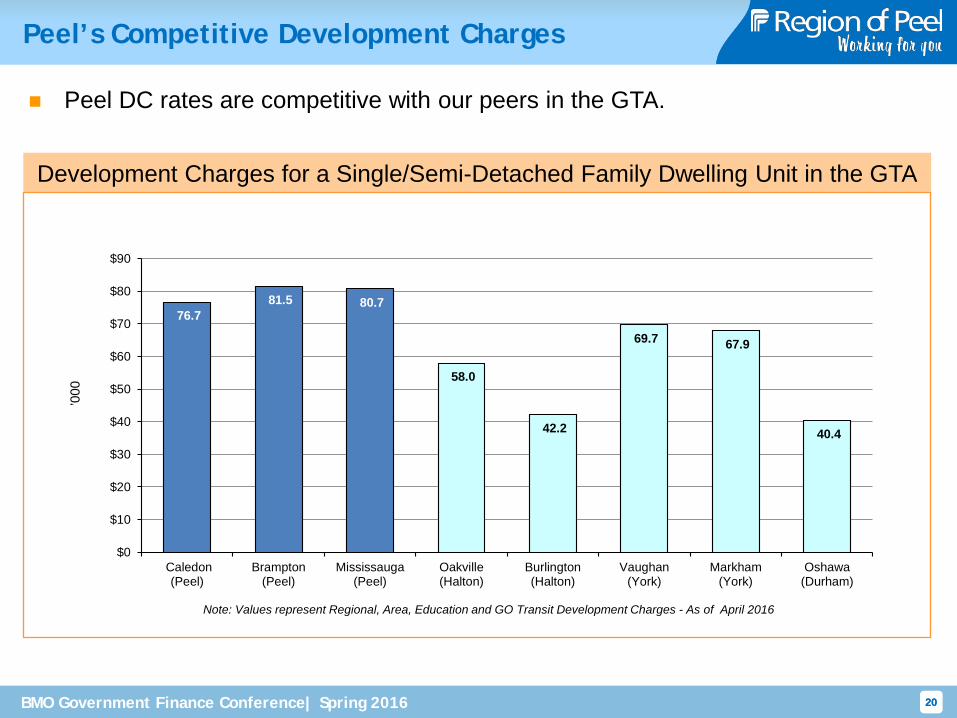

Peel’s Competitive Development Charges

20

Development Charges for a Single/Semi-Detached Family Dwelling Unit in the GTA

76.7 81.5 80.7

58.0

42.2

69.7 67.9

40.4

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

Caledon(Peel)

Brampton(Peel)

Mississauga(Peel)

Oakville(Halton)

Burlington(Halton)

Vaughan(York)

Markham(York)

Oshawa(Durham)

Note: Values represent Regional, Area, Education and GO Transit Development Charges - As of April 2016

Peel DC rates are competitive with our peers in the GTA. ’0

00

BMO Government Finance Conference| Spring 2016 21

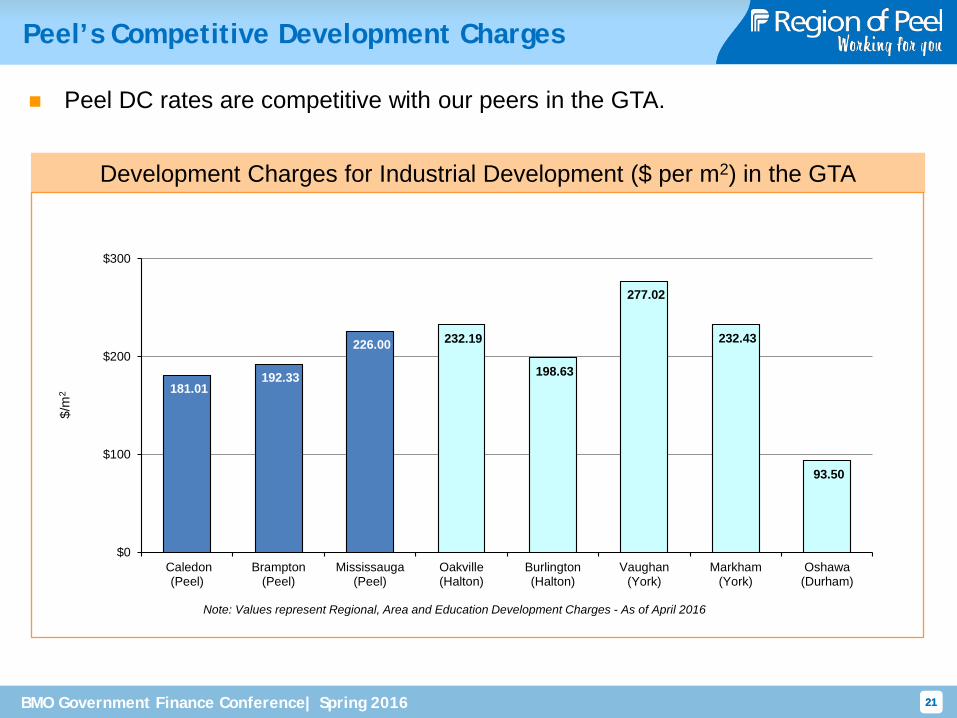

Peel’s Competitive Development Charges

21

Development Charges for Industrial Development ($ per m2) in the GTA

181.01 192.33

226.00 232.19

198.63

277.02

232.43

93.50

$0

$100

$200

$300

Caledon(Peel)

Brampton(Peel)

Mississauga(Peel)

Oakville(Halton)

Burlington(Halton)

Vaughan(York)

Markham(York)

Oshawa(Durham)

Note: Values represent Regional, Area and Education Development Charges - As of April 2016

Peel DC rates are competitive with our peers in the GTA. $/

m2

BMO Government Finance Conference| Spring 2016 22

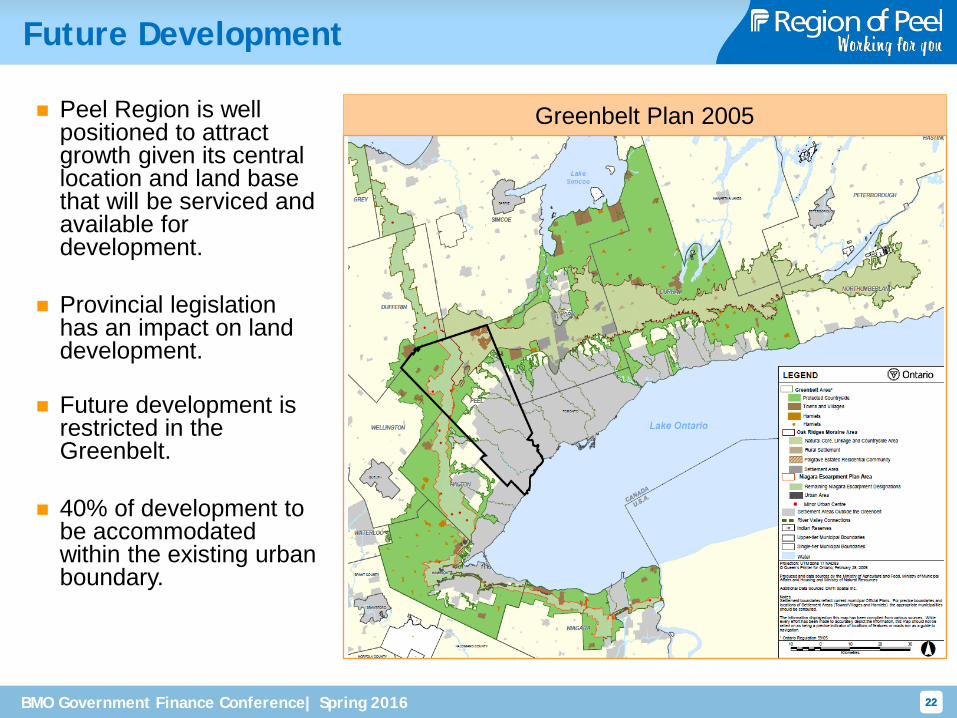

Future Development

22

Peel Region is well positioned to attract growth given its central location and land base that will be serviced and available for development.

Provincial legislation has an impact on land development.

Future development is restricted in the Greenbelt.

40% of development to be accommodated within the existing urban boundary.

Greenbelt Plan 2005

BMO Government Finance Conference| Spring 2016 23

$973

$589

$1,001 $1,059 $1,079

$1,020 $1,054

0

200

400

600

800

1,000

1,200

Halton Peel Toronto Vaughan(York)

Richmond Hill(York)

Markham(York)

Durham

$/Ye

ar

23

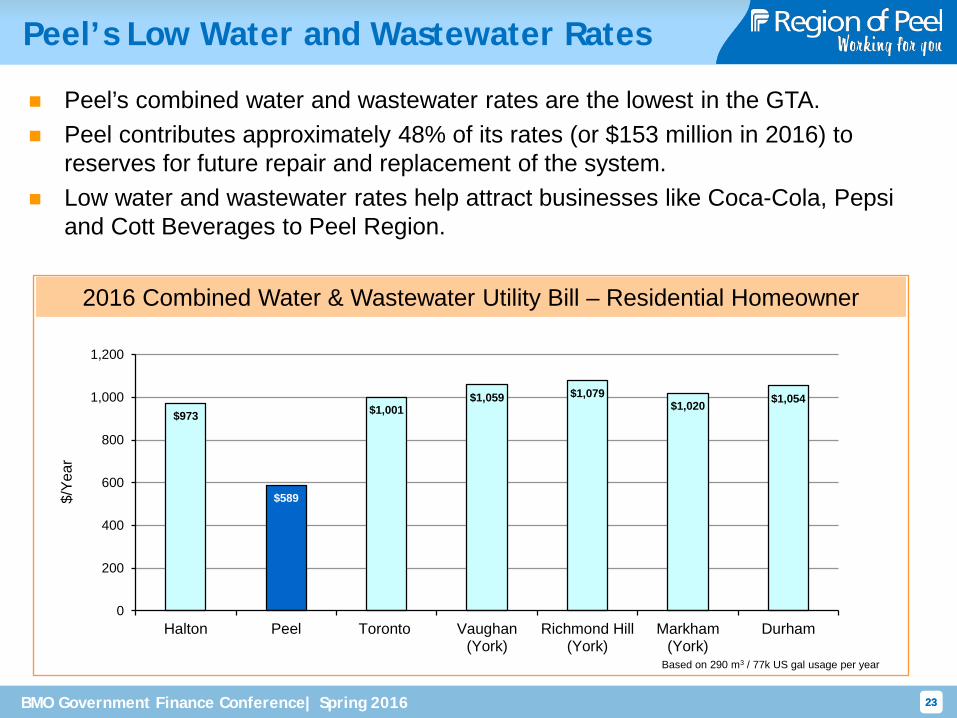

Peel’s Low Water and Wastewater Rates

2016 Combined Water & Wastewater Utility Bill – Residential Homeowner

Peel’s combined water and wastewater rates are the lowest in the GTA. Peel contributes approximately 48% of its rates (or $153 million in 2016) to

reserves for future repair and replacement of the system. Low water and wastewater rates help attract businesses like Coca-Cola, Pepsi

and Cott Beverages to Peel Region.

Based on 290 m3 / 77k US gal usage per year

BMO Government Finance Conference| Spring 2016 24 24

Ontario Municipal Act, 2001 Safeguards

Municipal debentures rank pari passu s.408(7)

Annual budget provisions Debt provision: municipality shall in each year prepare and adopt a

budget including estimates of all sums required during the year including amounts sufficient to pay all debts falling due within the year and amounts required to be raised annually for sinking funds and retirement funds

Balanced budget: budget shall provide that estimated revenues are equal to the estimated expenditures and the municipality will levy taxes sufficient to ensure that this is the case s.289 and 290

Proceeds from the sale of a debenture issue cannot be applied towards the payment of current expenditures s.413(1)

BMO Government Finance Conference| Spring 2016 25 25

Municipal Act, 2001 Safeguards (cont’d)

Debenture by-law cannot be repealed until the debt and interest have been paid s.414(1)

Doctrine of ultra vires Municipalities only have borrowing powers which are expressly set out in

legislation s.s. 9 and 17

Municipal officer guilty of an offense Any municipal officer who refuses to perform his or her duty to ensure that

all the obligations of their municipality’s debenture by-law are fulfilled is guilty of an offence s.422

Liability of members of council for diversion of funds Any member of Council who votes to divert funds to pay current

expenditures – funds that were originally raised to retire debt is personally liable for the misapplied funds and is disqualified from holding any municipal office for two years s.s. 424

BMO Government Finance Conference| Spring 2016 26 26

Strong Credit Rating

Long Range Financial Planning Strategy endorsed by Council commits to maintaining a strong credit rating S&P “AAA” since 2001

Moody’s “Aaa” since 2011

Large, highly liquid investments of $2.1B (as of April 30, 2016)

BMO Government Finance Conference| Spring 2016 27 27

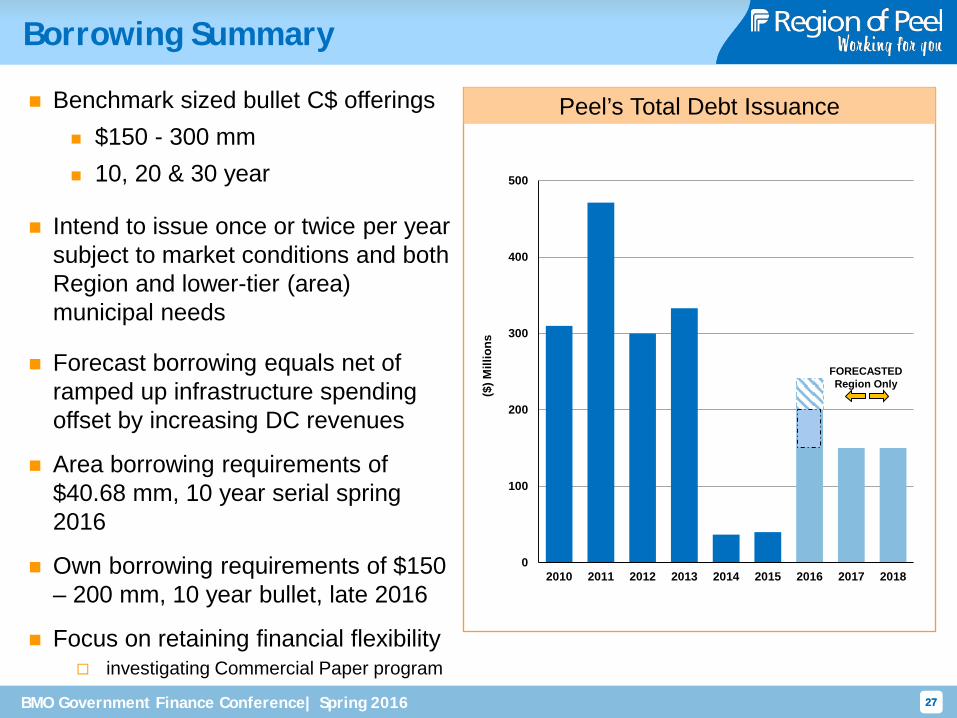

Borrowing Summary

Benchmark sized bullet C$ offerings $150 - 300 mm 10, 20 & 30 year

Intend to issue once or twice per year subject to market conditions and both Region and lower-tier (area) municipal needs

Forecast borrowing equals net of ramped up infrastructure spending offset by increasing DC revenues

Area borrowing requirements of $40.68 mm, 10 year serial spring 2016

Own borrowing requirements of $150 – 200 mm, 10 year bullet, late 2016

Focus on retaining financial flexibility investigating Commercial Paper program

Peel’s Total Debt Issuance

0

100

200

300

400

500

2010 2011 2012 2013 2014 2015 2016 2017 2018

($) M

illio

ns

FORECASTED Region Only

BMO Government Finance Conference| Spring 2016 28 28

Summary

Additional $1.1 billion forecasted to 2031 in Region’s 2015 DC background study primarily for long term expansion of water, wastewater and roads systems

DC’s collected to fund these system investments as development built

Water and Wastewater rates lowest in GTA Peel also issuing for Area municipalities

All Peel debt is general obligation

Strong liquidity ($2.1B) and high credit ratings (S&P AAA, Moodys Aaa)

Strong and diversified Peel economy

peelregion.ca/investors

BMO Government Finance Conference| Spring 2016 29 29

More Information

Paul Pohl, BComm.

Senior Treasury and Portfolio Manager

Finance 10 Peel Centre Drive, Suite A, 2nd Floor Brampton, ON L6T 4B9 Tel: 905-791-7800 ext. 4599 Fax:905-791-0564 [email protected] peelregion.ca/investors

Dave Bingham, MBA, CPA, CMA

Treasurer & Director Corporate Finance

Finance 10 Peel Centre Drive, Suite A, 2nd Floor Brampton, ON L6T 4B9 Tel: 905-791-7800 ext. 4292 Fax:905-791-0564 [email protected] peelregion.ca/investors

Updated information including:

credit rating reports financial statements budget tax and water/wastewater rates development charges peelregion.ca/investors

Peel Investor website