Embed Size (px)

Citation preview

InternationalTelecommunicationUnion

Regulatory trends & challenges

OECD experts meeting

““Towards a Services Trade Restrictiveness Index (STRI)Towards a Services Trade Restrictiveness Index (STRI)””Paris, 10 December 2008

The views expressed in this presentation are those of the author and do not necessarily reflect the opinions of the ITU or its Membership.

Youlia Lozanova Regulatory and Market Environment DivisionBDT, International Telecommunication Union

2

Agenda

1st wave of regulatory reformTowards a 2nd wave of regulatory reform Regulatory challenges todayNew strategies to stimulate growth in ICTs: infrastructure sharing

3

0

1

2

3

4

5

6

7

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

in b

illio

ns

0

20

40

60

80

100

120

140

160

nb c

ount

ries

Mobile broadbandInternet usersMobile cellular subscribersFixed lines

1st wave of regulatory reform

Creation of separate regulatory authority

Opening markets to competition

Licensing multiple operators (service-specific licences)

Lowering entry barriers

Promoting new business models

Privatization of incumbent operators

Flexible, accurate, transparent and non-discriminatory interconnection models

Subsidies to universal access providers for fixed-line services

Creating a level-playing field for investment (minimizing regulatory risk, tax incentives, etc.)

Source: ITU World Telecommunication/ICT Indicators Database and ITU Telecommunication Regulatory Database

Growth in ICTs, in billions, 1995-2007

4

It’s all about convergencefrom static market environments to dynamic fast-paced innovationfrom heavy-handed regulation to light-touch regulationfrom narrowband to broadbandfrom fixed to mobile (mobile pervasiveness) + fixed-mobile convergencefrom wired to wirelessfrom distinct to convergedfrom sometimes-on to always-on from PSTN to IP (NGN)

5

6 710 11 11 11

13

2022 23

27 28 29

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Effective regulation

14

43

86

106

124137

148 152

1990 1995 1998 2000 2002 2004 2006 2008

Growth in the number of regulators worldwide

Source: ITU Telecommunication Regulatory Database

Regulatory reform has been key to ICT development and enabled the move towards convergenceImportance of independent and effective regulatorExtending powers of regulatorsConverged regulators

Separate regulator, OECD countries

6

0%10%20%30%40%50%60%70%80%90%

100%

Basicservices

Mobilecellular (2G)

Internetservices

Wirelesslocal loop

DSL 3G FixedWireless

Broadband

Monopoly Competition

CompetitionA competitive market environment is key to promote investment, spur growth and extend connectivity

Removing market entry barriers & open access policies may speed up market development and provide a win-win scenario for investors, service providers & consumers

Additional reforms could ensure a level-playing field for all market players

Competition in selected services, 2007

Source: ITU Telecommunication Regulatory Database

7

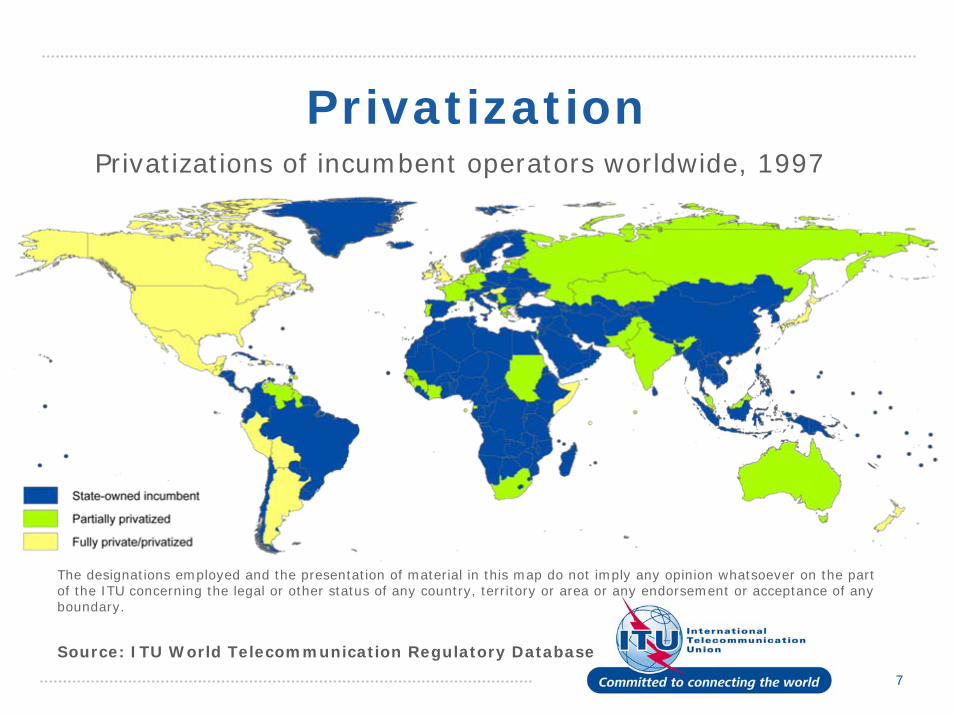

PrivatizationPrivatizations of incumbent operators worldwide, 1997

Source: ITU World Telecommunication Regulatory Database

The designations employed and the presentation of material in this map do not imply any opinion whatsoever on the part of the ITU concerning the legal or other status of any country, territory or area or any endorsement or acceptance of any boundary.

8

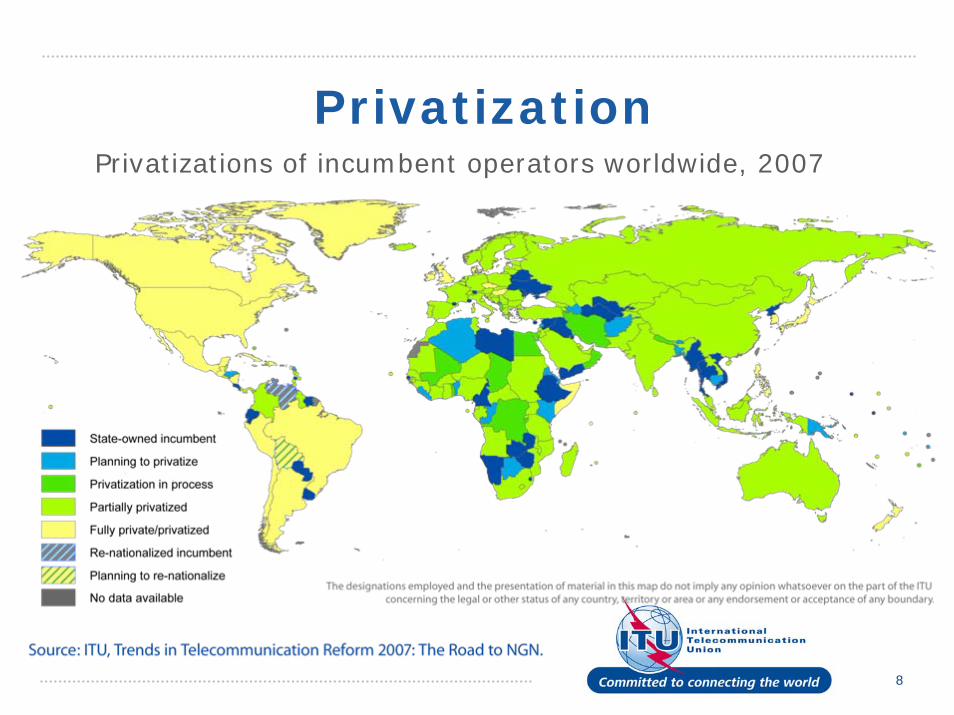

PrivatizationPrivatizations of incumbent operators worldwide, 2007

9

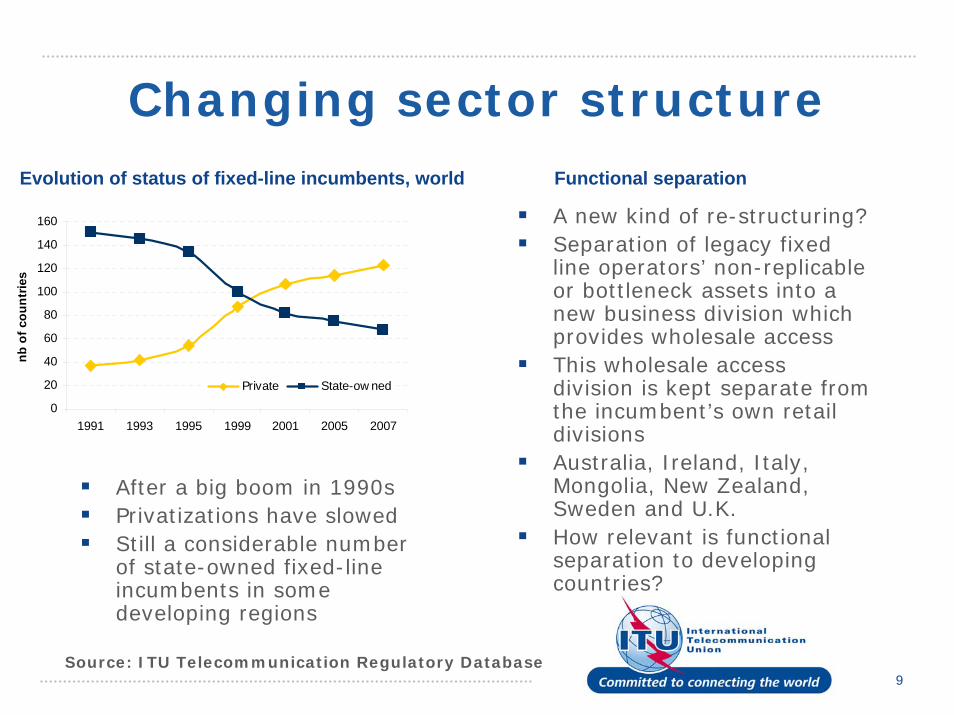

Changing sector structure

After a big boom in 1990sPrivatizations have slowed Still a considerable number of state-owned fixed-line incumbents in some developing regions

0

20

40

60

80

100

120

140

160

1991 1993 1995 1999 2001 2005 2007

nb o

f cou

ntrie

s

Private State-ow ned

Evolution of status of fixed-line incumbents, world

Source: ITU Telecommunication Regulatory Database

A new kind of re-structuring?Separation of legacy fixed line operators’ non-replicable or bottleneck assets into a new business division which provides wholesale accessThis wholesale access division is kept separate from the incumbent’s own retail divisionsAustralia, Ireland, Italy, Mongolia, New Zealand, Sweden and U.K. How relevant is functional separation to developing countries?

Functional separation

10

Enabling the move towards IP General regulatory framework:

Ensuring a level playing field Creating incentives for investmentTechnology and service neutrality in licensing & development of converged licensing frameworks Developing the enforcement capacity to resolve disputes, revoke licenses and impose sanctionsOpen & non-discriminatory accessTransparency Simplifying processes (licensing, etc.)Removing regulatory/licensing barriers to facilitate the transition from 2G to 3G and beyondSpectrum sharing & spectrum tradingSpecific incentives (tax policies, etc.)Subsidies: grants for community planning efforts, subsidized or low-interest loans

11

2nd wave of regulatory reform

Efficient and independent regulator with extended powersFrom separate telecom & broadcasting regulators towards converged regulators

LicensingFrom service-specific licenses towards general authorizations, unified & class licencesFrom technology-specific towards technology-neutral licences

SpectrumFrom administrative approach towards flexible spectrum allocation practices (sharing, trading, etc.) to create new access networks that deliver both voice and broadband cost-effectively

Network & bottleneck facilitiesFrom exclusive ownership towards passive & active infrastructure sharingOpen access to network and bottleneck facilities (fiber backbones, LLU) International gateway liberalization

Universal access & servicesFrom fixed-line voice towards broadband universal access

Flexible, transparent & simplified proceduresFacilitate market entryStimulate innovation

Spurring competition

12

VOIP

Most successful converged service to-date

Key factor for its success: low cost(both for MVNOs & users)

Strong growth is expected to continue

Fixed-line/VOIP substitution

VOIP over mobile

Estimates of international VoIP traffic

Source: ITU Background Paper on the status of VOIP worldwide, 2006

0

5

10

15

20

25

30

35

40

45

50

1996 1999 2002 2005 2008

% o

f tot

al in

t'al m

inut

es

Yankee Gp.

Telegeography /PriMetrica

Tarifica

Delta Three WP

Delta Three White Paper

Analysys

Yankee Gp.

ITU

13

VOIP: regulatory treatment

Regulatory responses vary:

VoIP has been made illegalVoIP is unregulatedThe absence or lack of regulationVoIP may be subject to similar/same regulation as PSTN, or some forms of VoIP are subject to some/all of the same regulation as PSTN, depending on the technology used VoIP may be subject to its own set of regulations,with its own specific licenses.

Source: ITU Telecommunication Regulatory Database

Number of countries allowing some type of VoIP

14

Regulatory challenges todayCompetition policy

Significant market power will not go away in an NGN environmentOpen access is key to growth in the sector

InvestmentUnbundle or share: what impact on investment in ICTs?

PricingWill NGN offer prices that are significantly lower than those available today?Spectrum pricing, MTR

Bundling and billing:How to distinguish real price of bundled services?

Interconnection Will current interconnection models work in an NGN?To regulate or not IP interconnection? IP & VoIP interconnection: towards cost-based pricing and flat rates?

Net neutralityHow to deal with traffic prioritization?

New converged servicesWhat level of universal service obligation to impose?To regulate or not content, and how?

SecurityCybersecurity threats, privacy and identity management issues

15

Aim to connect all the world to broadbandCost single biggest reason to shareDeveloping countries seek to leverage mobile infrastructure boom into mobile broadband boomDeveloping countries also seek to build IP-based backbone and backhaul networksDeveloped countries seek to leverage fixed line investments and upgrade to Fibre to home, building or curbBoth share the same goal: to expand network deployment and development by cutting costs Sharing can only take place in a competitive, transparent and non-discriminatory market & regulatory environment

New business models: sharing

74%

56%

44%

Infra

stru

ctur

esh

arin

g fo

rm

obile

oper

ator

s is

perm

itted

Infra

stru

ctur

esh

arin

g is

man

date

d

Col

ocat

ion

ism

anda

ted

ITU World Telecommunication Regulatory Database

16

Sharing: myth & reality

What it is:Using infrastructure sharing together with Universal Access strategies within a competitive frameworkReducing costsAllowing new players to provide broadbandRelying on time-tested competition principlesAbout allowing markets to workConsumers getting service

What it’s not:An attempt to put infrastructure back in the hands of monopoly providers or to stifle competition A strategy to lessen competition or to sell less equipment About markets not workingLimiting consumer choicesA limit on facilities-based competition

17

Trends in Telecommunication reform 2008:

Six Degrees of Sharing

Chapter 1: Market and regulatory trends in the ICT sectorChapter 2: Six degrees of SharingChapter 3: Extending open access to national fibre backbones in developing countriesChapter 4: Mobile network sharingChapter 5: Spectrum sharingChapter 6: International sharing: International gateway liberalizationChapter 7: The emergence of functional separationChapter 8: International mobile roamingChapter 9: IPTV and mobile TV: New regulatory challenges for regulatorsChapter 10: End-user sharingChapter 11: Conclusion:

Looking to the futurewww.itu.int/publ/D-REG-TTR.10-2008/en

18

www.itu.int/treg

19

www.itu.int/icteye

![OECD Services Trade Restrictiveness Index · 2018. 7. 28. · Trade on travel and transport services collapsed, while ICT services contributed toeconomic resilience (OECD, 2021 [8])](https://img.pdfslide.net/doc/110x75/61467a507599b83a5f003f4d/oecd-services-trade-restrictiveness-index-2018-7-28-trade-on-travel-and-transport.jpg)