Embed Size (px)

Citation preview

FILE COP | RETURN TOReport No. 274a-TUN REPORTS DESK

The Economic Development ONE WEEK

of TunisiaVolume 11: Annex-IndustryDecember 27, 1974

EMENA RegionCountry Programs Department II

Not for Public Use

Document of the International Bank for Reconstruction and DevelopmentInternational Development Association

This report was prepared for official use only by the Bank Group. It may notbe published, quoted or cited without Bank Group authorization. The Bank Group doesnot accept responsibility for the accuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit = Dinar = 1000 millimies

With effect from 1955

US $1.00 = 0.42 DinarDinar 1.00 = US $2.381

With effect from September 28, 1964

US $1.00 - 0.52 DinarDinar 1.00 = US $1.90

With effect from December 20, 1971

US $1.00 = 0.48 DinarDinar 1.00 = US $2.08

With effect from February 1973

US $1.00 = 0.44 DinarDinar 1.00 = US $2.27

UNITS AND WEIGHTS AND MEASURES:METRIC

British/U. S. Equivalents

1 m = 3.28 ft. 1 m ton = 0.981 g. ton1.1 US sh. ton

1 m2 = 10.76 sq.ft. 1 kg = 2.2 lb.

1 km = 0.62 mi. 1 litre = 0.22 gal.1 km2 = 0.386 sq.mi. = 0.26 US liq. gallon1 hectare = 2.5 acres 1 m3 = 1.31 cubic yards

FISCAL YEARJanuary 1 - December 31

THE ECONOMIC DEVELOPMENT OF TUNISIA

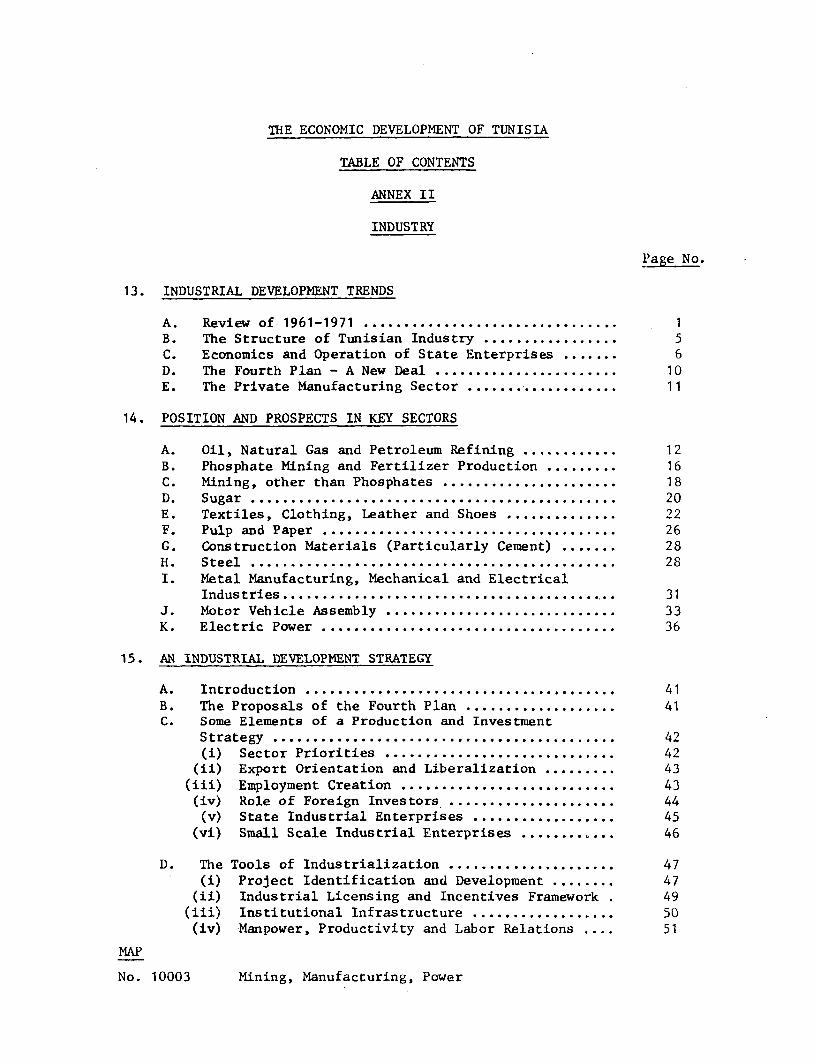

TABLE OF CONTENTS

ANNEX II

INDUSTRY

Page No.

13. INDUSTRIAL DEVELOPMENT TRENDS

A. Review of 1961-1971 ................................ 1B. The Structure of Tunisian Industry .... ............. 5C. Economics and Operation of State Enterprises 6D. The Fourth Plan - A New Deal ....................... 10E. The Private Manufacturing Sector .... ................ 11

14. POSITION AND PROSPECTS IN KEY SECTORS

A. Oil, Natural Gas and Petroleum Refining .... ........ 12B. Phosphate Mining and Fertilizer Production ... ...... 16C. Mining, other than Phosphates ...................... 18D. Sugar .......... .................................... 20E. Textiles, Clothing, Leather and Shoes .... .......... 22F. Pulp and Paper ..................................... 26G. Construction Materials (Particularly Cement) ....... 28H. Steel .......... .................................... 28I. Metal Manufacturing, Mechanical and Electrical

Industries .................................... 31J. Motor Vehicle Assembly ............................. 33K. Electric Power ..................................... 36

15. AN INDUSTRIAL DEVELOPMENT STRATEGY

A. Introduction ....................................... 41B. The Proposals of the Fourth Plan ................ ... 41C. Some Elements of a Production and Investment

Strategy ........................................... 42(i) Sector Priorities ............................. 42

(ii) Export Orientation and Liberalization .... ..... 43(iii) Employment Creation ........................... 43(iv) Role of Foreign Investors ...... ................ 44(v) State Industrial Enterprises .... .............. 45

(vi) Small Scale Industrial Enterprises ............ 46

D. The Tools of Industrialization ..................... 47(i) Project Identification and Development ........ 47

(ii) Industrial Licensing and Incentives Framework . 49(iii) Institutional Infrastructure .... .............. 50(iv) Manpower, Productivity and Labor Relations .... 51

MAP

No. 10003 Mining, Manufacturing, Power

ANNEX II: INDUSTRY

13: INDUSTRIAL DEVELOPMENT TRENDS

A. Review of 1961-1971

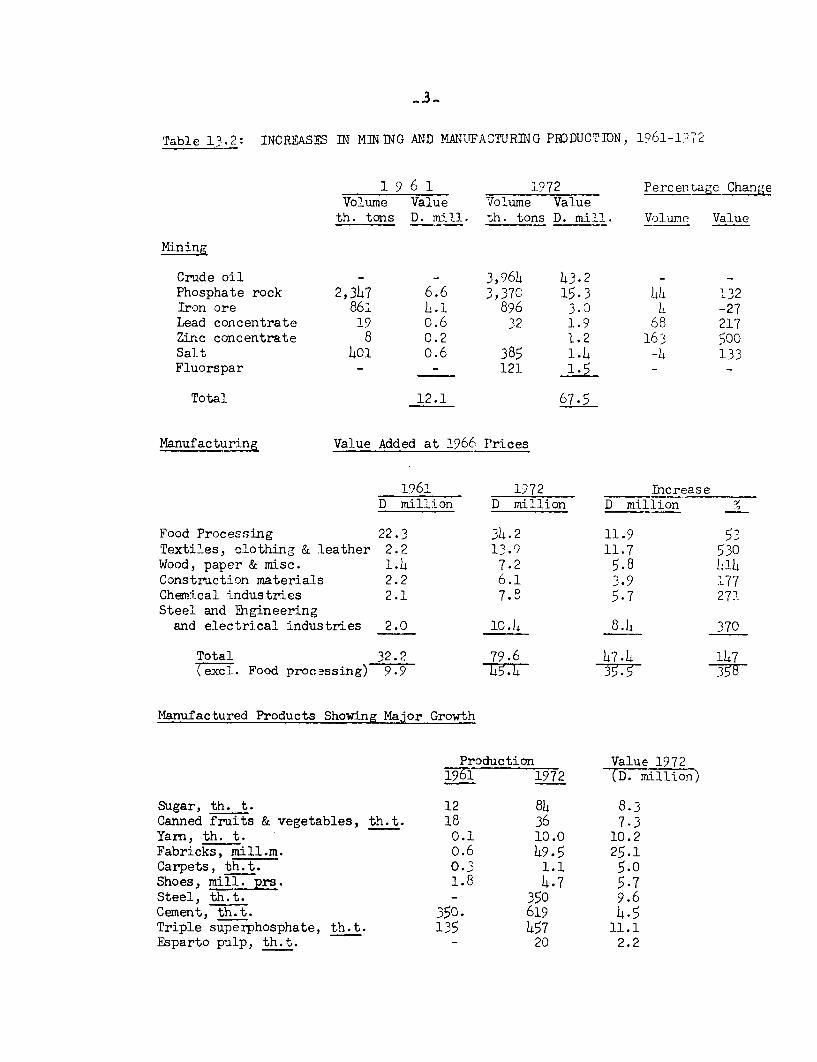

13.1 During the period 1961-1971, industrial production increased by 150percent, corresponding to an average annual growth rate of 9.9 percent. Therewas a remarkable 20 percent further increase in 1972, bringing the averageannual growth rate to 10.4 percent, due, in part, to a record year for theolive oil processing industry. A substantial part of the growth over thedecade is due to the rapidly increasing production of petroleum. The growthfor the manufacturing sector alone was about 8 percent, but apart from foodprocessing, growth has been dynamic: about 15 percent per year. The miningindustry has stagnated because of difficulties in the exploitation of rockphosphate, to be described later, as well as dwindling reserves of iron ore.Food processing, which accounted for about 50 percent of industrial output in1961, has been held back by unstable agricultural production, and by therelatively slow growth in certain subsectors where a processing potential wasthought to exist (sugar, canned fruits and vegetables, wine and essentialoils). About 240,000 people are employed in industry, of whom about 170,000are in manufacturing and 19,000 in mining; roughly one-third of these jobswere created during the 1960s, mostly in manufacturing.

Table 13.1: TRENDS IN INDUSTRIAL OUTPUT, 1961-1972(Million Dinars at 1966 Prices)

Value Added Growth Rate /11961 1971 1972 1961-71 1961-72

Power and water 4.0 13.2 14.5 13.4 13.0Petroleum -- 23.5 25.8 -- --

Mining 8.9 11.6 12.1 1.6 1.7Manufacturing 32.2 61.6 79.6 7.9 8.8

of which:Food processing (22.3) (24.9) (34.2) (1.3) (3.2)Other manufacturing (9.9) (36.7) (45.4) (15.0) (14.8)

Total 45.1 109.9 132.0 9.9 10.4

/1 Least squares method.

Source: Annex Table 2.7.

- 2 -

13.2 The thrust of industrialization during miost of this period, exceptfor the last three years,was supplied by large projects in the state sector.Tunisian industrialization has hitherto been focussed on a relatively smalldomestic market. Exports accounted for about one-quarter of manufacturinggrowth (other than food processing) in 1960-67 and for about only one-eighthof the increase in 1967-72. Industrial exports are represented mainly byphosphate fertilizers, esparto pulp, one-half of carpet production, one-thirdof canned vegetables production, and relatively minor exports of hides andessential oils with a low industrial processing component (Annex Table 8.4).

13.3 Table 13.2 reviews the progress during the past decade in greaterdetail. It shows the predominance of petroleum and phosphate rock in themineral sector. In contrast, manufacturing expanded over a wide front.Petroleum refining, textiles and clothing and pulp and paper showed thehighest rates of growth, but from a low initial production base. Furtherdetail is provided in Annex Tables 2.7, 8.1 and 8.2. Some of the abovemanufactures are based upon imported raw materials (e.g. coking coal for thesteel industry, cotton, tinplate for canning, and sulfur for the productionof superphosphate). In the main, however, the products showing rapid growthare made from domestic materials, and thus have greater developmental impact.This is clearly true for pulp (esparto grass), canned goods (vegetable andfish), cement (limestone), and carpets (wool). In other raw material process-ing industries, domestic use has simply replaced exports. This is true foriron ore and hides, for example.

13.4 In this respect, the phosphate fertilizer industry is in an inter-mediate position. Tunisia encountered considerable difficulties in exportingphosphate rock in the 1960s. While some of them are likely to continue, itis at least conceivable that the rock will have a higher value when locallyprocessed, and the Tunisian phosphoric acid plants can be specifically adaptedto the character and quality of Tunisian rock. Furthermore, the rehabilita-tion and partial mechanization of some existing mines, the development of twonew mines, one using highly mechanized methods, and the recent increasedemphasis on reducing costs and increasing competitiveness, plus the recentrise in phosphate prices, should improve the financial position of thisindustry in the Fourth Plan period (1973-1976).

13.5 Until the late 1960s, the main poles of industrial growth wereabout a dozen major state manufacturing enterprises, private investmentplaying a relatively minor role.

-3-

Table 13.2: INCREASES IN MINING AND MAiNUFACOTURING PRODUCTION, 1961-1?72

1 9 6 1 1972 Percentage ChangeVolume Value Volume Value

th. tons D. mill. th. tons D. mill. Volume Value

Mining

Crude oil - - 3,964 43.2 - -Phosphate rock 2,347 6.6 3,37c 15.3 44 1 32Iron ore 861 L.1 896 3.0 4 -27Lead concentrate 19 o.6 32 1.9 68 217Zinc concentrate 8 0.2 1.2 163 500Salt 401 o.6 385 1.4 -4 133Fluorspar - - 121 1.5 - -

Total 12.1 67.5

Manufacturing Value Added at 1966 Prices

196' 1972 IncreaseD million D million D million

Food Processing 22.3 34.2 11.9 53Textiles, clothing & leather 2.2 13.9 11.7 530Wood, paper & misc. 1.4 7.2 5.8 L14Construction materials 2.2 6.1 3.9 177Chemical industries 2.1 7.8 5.7 271Steel and Bhgineering

and electrical industries 2.0 10.4 8.4 370

Total 32.2 79.6 47.4 147Texcl. Food processing) 9.9 73 -3-57-

Manufactured Products Showing Major Growth

Production Value 197219i61 1972 (D. million)

Sugar, th. t. 12 84 8.3Canned fruits & vegetables, th.t. 18 36 7.3Yarn, th. t. 0.1 10.0 10.2Fabricks, mill.m. o.6 49.5 25.1Carpets, th.t. 0.3 1.1 5.0Shoes, mill. 1._8 4.7 5.7Steel, th.t. - 350 9.6Cement, th.t. 350. 619 4.5Triple superphosphate, th.t. 135 457 11.1Esparto pulp, th.t. - 20 2.2

- 4 -

Table 13.3: INVESTMENTS IN MANUiVACTURING(Million Dinars at current prices)

Total Private Public

1961 6.3 0.6 5.71962 5.8 0.8 5.01963 7.2 1.7 5.51964 22.3 2.9 19.41965 26.2 0.1 26.1

1966 10.1 1.6 8.51967 12.9 3.3 9.61968 10.7 2.8 7.91969 15.5 4.8 10.71970 18.2 6.3 11.9

1971 21.6 6.8 14.b1972 20.4

Source: M1inistere du Plan.

Public investment in industry started with a beet sugar factory cum sugarrefinery and an esparto cellulose plant in 961-63, followed by the ElFouladh steel mill and big new textile mills in 1964-65. Subsequent stateinvestments in manufacturing have generally been on a more modest scale, buthave included a large new fertilizer plant, a paper mill located close toth-e pulp mill and, finally, expansion of cement production, motor vehicleassembly and handicrafts, the latter organized by the Office National de 1'Artisanat. The great bulk of these investments were outside Tunis, andreflected, to a substantial extent, deliberate regional. industrializatLon.

13.6 As the capital-output and capital-income ratios slhow, the indus-trialization strategy during the last ten years was relatively expensive.The incremental capital output ratio of mianufacturing was about 4.? for theperiod 1961-71 (with 1972 added in, it falls to 3.7), while the cost per newjob created averaged D 4,000 (at constant 1?66 prices) (Statistical Ap)pendix,Table 5.9). If we exclude food processing, in which activity is governedlargely by fluctuations in agricultural production, the incremental capitaloutput ratio for 1961-71 is 3.8, which is st-ll highi. The relatively poorimmediate investment return is traceable in large part to public-sectorprojects accounting for over 80 percent of total 1961-70 investment, andabout 55 percent of 1971 value added, in manufacturing. The reason is thelow output of these projects; it must be borne in mind, however, that theGovernment focussed on projects in relativelv capital-intensive basicindustries which the private sector was not in a position to undertake.

13.7 The reasons for the relatively low investment return were theoften inadequate technical and economic analysis, and the inexperience ofmanagement. The scarcity of skilled labor meant low productivity with highoperations costs: the new industries had to train their own labor andcreate an industrial mentality. The strategy did at least create arnindustrial base and a pool of know-how as a platform for future growth.However, a disproportionate share of resources was allocated to projectswhichmnot only failed to yield-immediate economic,andlfinancial returns buthave-only doubtful prospects..of.long7-run viability.. Inz%the light.of thestrengths andcweaknesses Eof, -this _first ,phase. of industrialization, theGovernment,has2. devis,ed.a new-.str.at,egy-which 'puts:spr,imat.,yx,'emphasis on exportindustriesj; prTeferabtly.ylabAor-,i-nte-n-sl2 ye- in,-whic'hhth-eepr.ivate,sector will beassigned ?a imajpor rolecanddto ouhi¢chhf eig nprui-va bein,vest-erjs,will;be encour-aged Lto. contrib.ute -financ,ej9kno.8- ho,w,wand expvr,t-m

B. Thec-,StructureeoffTunisi'annIn:duStEstry

13..., Intil 969 p,whennitheelast tiinduatrial lcen-sus-swassta en 1i,there wereabbutt- 950 umanuf.ct-uri-ngges.tab.lishhments sinrlTulni,sia-.1 Souteo123. ofDJtheseempl,oyedvimo,recthan-,1OG0Cwor,kerssanddacco.uned.-forXrab.oitt71 lprcen7tof -thetotallvalueiadded'. AAsimilar.rnumb.er.-of! p.l1ants'emp~,oy)i'ngg5Q9-9r,workersaccounted,:fo-rranotheri155pe,r-centt,. (Annex,xTdb1ee897)37. ExerisQme'oft theselarger-.plantascondxictttheitioperations,sinnaasem i.-handt,xaftl:fashion;, thenumber oftuitr.ui.nuriaTlunits.sisstheref-ore.,qiltecsma.ll,,The,se include:

.-- ThiesE lF6uladh'hirit'egateddsteelim,ill ,prQduci:aggabout4 70,-000tonssof fconcret-eereiktf4r,ci'nggrod.sp er,rygar -;

- TWoocementtplants sw-itwhhaacQmbLilneddpflodUctionnof fabout'625,c-TQ0O0tonsL;;.,

- TheeBiAzer-tte pet-ral'umrrref-inery;with -aathrougup.,t-tof --onemiAlli.on -tonsi;;,

A-- g trowiiing(gt ext±ld ei ndlstry y ddmi a t.e ddb y y the,e St a tewoE ag ediSGOITEXRsvbuattnow,i%wi'thhpri'vat.e -textileefirmpI-offincreasingimpo,rtance -E Severilcl-,thing,faetorigssareeunier--coastruction;

- - Ariiresparto:cpta15irmir.JIlanddaapA§er~r;m ll,,eachhwit1m ajcapacity ofab out] t24?]Q0O(J30t 0to3nsi;;

- A Anoitor, ivehi cE6easvmWaXyp-twlth-Rahna an ua§lol pj4 :0of about1 ,5QO))Ccars'Eanddltht~ tttrmbc19s,

- Fifv^eror s ix cfundr-ea,san4dmeagJlma-nuagguri.nggplang tsp with lowcapqclties:;

- A food-`processing(flndustry-vineludti g.someE v-able,units, suchas a.brewery, two,or three out of-37,canneries, some flour millsand noodle factories, olive oil presses and vegetable oil re-fineries. In general, however, food processing units are smalland their equipment outmoded and/or heavily worn.

13.9 Geographically, despite the Government's regionalization efforts,Tunisian industry 1/ is heavily concentrated in Tunis and the surroundingarea (52 percent of industrial employment) and in the governorates of Sousse,Sfax, Gafsa, and Bizerte (each with 8-9 percent of the total, or altogetheranother 35 percent). The prominence of Gafsa is entirely due to its phosphaterock mines; Bizerte has steel, cement, oil refining, and shipbuilding; andSfax and Sousse have a number of food processing and other consumer goodsindustries (textiles, shoes, furniture) as well as mechanical industries(including motor vehicle assembly) in Sousse and phosphate fertilizerplants at Sfax. Sugar is manufactured at Beja and paper-pulp at Kasserine.Kairouan is a special case because its traditional carpet-making is carriedout mainly by handicraft rather than by industrial methods. Only Medeninein the South entirely lacks industry. An industrial complex is underconstruction at Gabes; the first unit, a phosphoric acid plant, was putinto service in 1972.

C. Economics and Operation of State Enterprises -/

13.10 State enterprises were established in manufacturing for thefollowing motives (in approximate order of importance):

- to start basic industries requiring investments far beyondthe capacity of the private sector (steel, major textilecomplex, pulp and paper, sugar)

- to stimulate regional development (pulp and paper, sugar)

- to administer nationalized industries (phosphate and ironore mining, phosphate fertilizers, cement)

- to launch pioneer projects (automobile assembly, canning,furniture making).

The State went somewhat beyond these objectives in a number of small venturesadditional to the major projects. In 1969 it owned or held a majority insome 50 mining and manufacturing enterprises, employing about 32,000 personsrepresenting over 80 percent of employment in "large enterprises" and 55percent of employment in all manufacturing and mining establishments em-ploying more than 5 persons. State enterprise dominated all industries ex-cept food processing.

1/ The figures shown include mining energy, and transport. This distribu-tion, however, is quite representative also for the combined mining andmanufacturing activities.

2/ The origins and objectives of state-owned enterprises in general, theinstitutional framework, financial structures, and operating resultswere studied by an IBRD Mission whose report was issued in August 1969(EMA-13a). Much of the detailed information provided by this reportis still relevant.

13.11 The establishment of state enterprises, in principle, required par-liamentary approval, as did increases in capital or advances from the statebudget. Such control, however, did not extend to financing through the state-owned Societe Tunisienne de Banque (STB) or to foreign suppliers' credits. Inprinciple, government administration and supervision ("tutelle") of statemanufacturing enterprises was to be the joint responsibility of the Ministriesof Industry and Finance, which would have imposed financial checks on state in-dustrial investments. However, during most of the 1960s, these two Ministrieswere combined. At the moment, the primary responsibility for state economicenterprises is vested in the Ministry of National Economy, subject howeverto budgeting and planning constraints exercised by the Ministries of Financeand Planning respectively. General policy and major investment decisions arematters for the whole cabinet. Within the Ministry of National Economy, sixeconomic and financial comptrollers are responsible for supervising 5-8 state-owned enterprises, and attend their Board meetings.

13.12 The financial results for the state enterprises for the years 1970,1971 and 1972 are detailed In Annex Table 8.10 and are summarized in the tol-lowing table.

Table 13.4: OPERATING PROFITS/LOSSES OF STATE ENTERPRISE, BY SECTOR(D '000)

No. of Net Operating Profit/Lossfirms 1970 1971 1972

Mining 8 -4,073 -3,004 -4,658Petroleum 3 18,632 24,800 25,561Water, electricity 2 3,472 3,764 2,729Manufacturing 47 1,294 -1,806 2,355

Food processing 7 1,543 1,280 2,177Construction materials 15 246 154 514Steel, engineering,

electrical 12 -698 -2,058 446Chemicals 6 856 1,239 1,183Textiles, clothing 2 -467 -478 -463Wood, furniture 2 12 156 102Paper, printing 3 -198 -2,099 -1,604

Total 60 19,235 23,664 25,987

Total, excl. petroleum 57 693 -1,136 426

Source: Ministere du Plan (preliminary study).

Crude oil production has been very successful and profitable, and completelydominates the earnings picture. The situation in the other sectors is muchless satisfactory, with phosphate, steel, textiles and paper, in particular,showing deficits.

- 8 -

13.13 While important as indicating the financial trend of the enterprisesof a given sector, these statements are hardly meaningful as regards economicperformance. Some enterprises enjoyed prices or processing margins twice theworld level, while others, like the Djerissa iron ore mines, had to competein the world market despite the handicap of an increasingly unfavorableresource base. Increases in world commodity prices occurred in 1973 and 1974are going now to change significantly the position and financial prospects ofseveral enterprises. Because operations of leading state enterprises domi-nate or heavily influence the sub-sectors with which they are associated, andwhich are analyzed in Section II, only a brief summary of past performanceand problems will be attempted here. The enterprises are dealt with indecreasing order of total fixed investments.

El Fouladh - Steel (1967): 1/ A fully integrated steel mill based uponan output of only 70,000 tons of bars is not viable, even at full capacity.In fact, until 1972 the domestic market absorbed only about one-half of themill's production,and prices, until the recent world boom, were about twicethose of equivalent imports. In order to make a reasonable profit in com-petition with impQrts, the company would have needed about 45 percent pro-tection in 1970. Financial reconstruction has not been completed and aviable long-term plan is needed.

Sogitex - Textiles and Clothing (1965): Operating six textile andclothing mills, this company was the first modern industrial installationin the textiles sector and, until recently, provided the bulk of the indus-try's output as well as much of the staff and skilled labor for the privatemills which have subsequently been established. Within the past four yearsthe company has started exporting (presently about one-quarter of sales), andis also entering into joint ventures for clothing exports with foreign part-ners. It operates a vocational school for the textile industry with statesupport. With original equipment of variable quality, its productivity inspinning is said to be about two-thirds of that of Western European mills.Although, by its published accounts, the company has approximately brokeneven during the last two years and has a promnising earnings potential, itsfinancial position is weak.

Gafsa Company - Phosphate Rock Mining (1896, State controlled since 1966):The Tunisian phosphate mines account for about 4 percent of world productionof crude phosphate. A substantial fertilizer industry is based on thesemines, and includes three major producers, which absorb about one-third ofthe output of the mines. The mines, however, have made losses during thelast 5 yeers. Until 1972, operations were characterized by very low produc-tivity, unsafe working conditions, high labor turnover, inadequate staffing,and a lack of reliable accounting records and planning. A promising effort

1/ Figures in parentheses show first year of operations after initialbreaking-in period.

- 9 -

at financial and technical rehabilitation and redevelopment has been initiated.Moreover, the threefold increase in phosphate prices which occurred at theend of 1973 will substantially improve the financial performance of thephiosphate industry.

Ste. Nat. de Cellulose, and Sotupalfa - respectively Pulp and Paper(1966 and 1970): After the foreign suppliers of the pulp mill had failedto solve its operating problems, the Tunisian management recently broughtthe pulp mill close to nominal operating capacity, which has also been at-tained for the paper mill. The financial and economic results have beenpoor, however, raw material costs for pulp exceeding sales proceeds in 1971,and the paper mill producing at only two-thirds of capacity because of marketconstraints. The long-term outlook is clouded by expected supply constraintsand high costs of the basic raw material (esparto grass), by the disappearanceof a market premium for esparto paper and by the impracticality of the conceptof meeting most of Tunisia's varied paper requirements from a small local mill.Nevertheless, the efforts and achievements of the staff and workers are im-pressive. Moreover, the general increase in pulp and paper prices is likelyto contribute to improve the situation of this enterprise.

Ste. Nat. de Sucre - Sugar Beet Factory and Cane and Beet Sugar Refining(1963): Commercially, this pioneering venture is a profitable operat:ion (highsugar prices to the consumer and substantial profits from the refining of im-ported sugar), but the return on the beet sugar part of the operation has beenlow because of low yields from the beet fields, the high investment cost ofthe factory (mainly related to the small scale of operations), and a very shortcampaign leading to insufficient plant utilization (only 42 days on an aver-age). The recent increase in world market prices for sugar has reduced themargin between these prices and the Tunisian price.

Ste. Tun. d'Industrie Automobile (STIA) (1961): The French Renaultcompany was originally associated with this venture, but sold out in 1968.This company assembles about 1,500 motor vehicles a year (Renault cars,Berliet trucks, trailers and buses), with a local component of 20-30 percentfor cars and 40-50 percent for trucks and buses. It is essentially a sub-contractor for other vehicle manufacturers. The plant is generally wellsuited for its operations and well run. However, the overall operation isat present an economic loss since the rate of effective protection was about133 percent of value added for cars and 80 percent for the operation as awhole in 1972. The reasons for the high costs are the low volume and greatvariety of models, insufficient capacity utilization and the high cost oflocal supplies and procurement in general. Local assembly of motor vehiclesis hardly ever economic except as a brief transitory phase leading to inte-grated production. STIA is now trying to expand the assembly and coIIstructionof a well-designed bus for domestic production as an autonomous venture, withthe proposed technical assistance of a leading bus manufacturer with success-ful experience in a similar situation.

13.14 In brief, some of major state enterprises lacked economic justifi-cation, the exceptions being textiles and phosphate mining. The finiancialweakness of several enterprises arose from excessive investment per unitof output, under-capitalization and continued losses in the past, but

- 10 -

prospects are now more favorable in several activities as a result of in-creases in world commodity prices. Only the sugar company and the automobileassembly plant have escaped this dilemma by being able to charge high prices.Ministerial supervision is often handicapped by shortage of staff with suf-ficient experience to supervise these enterprises and help to solve theirdifficult problems.

D. The Fourth Plan - A New Deal

13.15 Within the last two years, the Government has developed an industrialstrategy which puts primary emphasis on export industries, assigns a majorrole in industrialization to the private Tunisian sector and looks to foreignprivate investors for contributions of finance, know-how and export markets.These foreign investments will also serve as catalysts. Cooperation withand emulation of foreign companies is expected to lift Tunisian industry fromits present status to export competitiveness. By these means, it is hoped,production will be increased by 50 percent, with an appreciably lower capital-output ratio than during the last decade. About 40,000 new jobs would bedirectly created in manufacturing. The main growth points would be clothingand knitwear for export on the one hand and phosphate fertilizers on theother hand; these exports would reach D 39 million and D 18 million respect-ively by 1976. A summary of investments and projected growth in value addedand employment, by major industrial sectors, is given in Annex Table 8.12.

13.16 Scheduled investments total about D 160 million. They includeabout a dozen large projects (D 3 million and over), mainly in the Statesector, and another dozen fairly large projects (D 1-2 million), primarilyfor textile production (spinning mills, weaving mills, finishing plants).The bulk of the program, about D 100 million, would be for medium-sized newplants and expansion projects (below D I million), mainly in the privatesector. This represents a substantial progressicn for manufacturing invest-ment: D 20 million a year, against D 6.3 million in 1970 and somewhat overD 6.9 million in 1971. Altogether, investments in manufacturing are expectedto account for 13.4 percent of total Fourth Plan investment, compared with11.9 percent in the Third Plan. Whereas private investments were responsiblefor 20 percent of the Third Plan total for manufacturing, their share in theFourth Plan is planned to rise to over 50 percent.

13.17 Manufacturing activities provide about 12.5 percent of total employ-ment (counting all the small establishments). Yet the manufacturing sectorhas been given the task of creating 40,800 new jobs in 1973-76, i.e. more than34 percenit of all new employment and more than the total employment createdin manufacturing during the decade 1961-71.

Table 13.5: EMPLOYMENT 1972 AND NEW JOBS 1973-76(in thousands)

1972 1973-76

Organized sector 70 35Artisans and other 100 6

170 41

/1 The organized sector includes firms with 5 or more employed covered bythe Industrial Census. Another 35,000 are employed in artisan estab-lishments producing textiles, clothing and leather goods (particularlycarpet-making)) and the remainder in even smaller production units,particularly in food processing, textiles, clothing and leather.

All but a small proportion of the new jobs would be in sectors other than foodprocessing. This employment creation would be combined with a sharp increasein productivity (production rising by 17.5 percent per year, employment byabout 8.2 percent). The number of investment projects approved in 1973 andearly 1974, particularly under the law of April 1972 on incentives to exportindustries, suggests that these new industrial employment goals for the Planperiod will be appreciably exceeded.

E. The Private Manufacturing Sector

13.18 In 1970 there were about 200 large and medium-sized manufacturingcorporations supplying data on "Sources and Allocation of Funds" (AnnexTable 8.11). The 40 largest were responsible for about 55 percent of thecash flow of the private manufacturing group. Individually, the latter hadnet cash flows (depreciation plus profits minus taxes and dividends) averagingabout D 60,000; the highest single figure was D 166,000. These large firmswere mainly in textiles, food, plastics, leather and shoes, and light metalmanufactures. Though exact figures are lacking, there appears to be littleforeign participation in Tunisian manufacturing enterprise. NPK phosphatefertilizers (with a Swedish company as the leading shareholder), Bata shoesand a textile firm (Grovo-Massanel) are important exceptions.

13.19 There has been a tendency towards multiplication of firms in thesame line of business. This is attributable to the "imitation effect" andto the fact),apparently, that it was easier to obtain investment incentivesfor new firms than for the expansion of existing companies. Mergers betweenenterprises in the same branch have occurred, but they appear to be theexception. On the other hand, a few individuals and groups are emergingwith holdings in more than one industry.

13.20 Data collected in connection with a study of SNI's operationsindicate that capacity utilization is a major problem (e.g. in steel pipes,radiators, polyurethane foam, etc.), particularly when superimposed upon

- 12 -

excessive fragmentation. In several cases, domestic production has beeninitiated without adequate study of economic returns. Competing imports areoften-prohibited, permitting a small number of domestic producers to survive,in an oligopolistic and protected market, with very low economic efficiencyin converting imported raw materials into finished products. Infant industryprotection is, of course, a normal instrument for getting industry started)and the Government is now seriously concerned to streamline these industriesand take them out of the shelter of the nursery into the open arena of theEuropean market.

13.21 A characteristic of Tunisian firms is their weak financial structure,with high short-term credit, as shown by the following summary (excludingfood processing and construction materials).

Table 13.6: SOURCES AND ALLOCATION OF FUNDS, 1970(Percent)

Large Cash Flows Medium Cash Flows and/and/or Invest. or Investments

30 enterprises 120 enterprises

Sources of Funds

Internal Savings 25.3 33.3Capital Increase 11.5 7.2Long and Medium Term Loans 19.9 9.4Short-term Credit 43.1 50.1

100.0 100.0

Allocation of Funds

Fixed Investments 51.9 38.3Inventories 27.7 34.8Participations, Receivables 3.5 1.0Loan Repayment 17.4 22.0Increase in Cash (0.7) 3.6

100.0 100.0

Source: Annex Table 8.11.

Neither firms with large cash flows and/or investments, nor the group withsmaller resources and commitments, generated any substantial funds for newfixed investments after allowing for loan repayments. Moreover, most firmsappear to be over-dependent on short-term credit for their permanent workingcapital. Financial 'rehabilitation, together with restructuring, remains thefirst priority for Tunisian industrialization, and calls for a more highlydeveloped organization and greater initiative on the part of the banks.

- 13 -

14. POSITION AND PROSPECTS IN KEY SECTORS -

A. Oil, Natural Gas, and Petroleum Refining

14.1. Petroleum prospecting in Tunisia is carried out entirely by for-eign companies, and permits have been issued for an area totalling 181,604km2 . The small size of the petroleum sector, the advanced technology, thegreat risks and small expected returns on exploration are invoked by theauthorities as reasons for relying entirely on foreign firms.

14.2 In 1961, Tunisia was entirely dependent on imports to meet its demandfor liquid fuels. During the following decade, production rose to 4.8 milliontons, or three times domestic requirements. Tunisia thus became a relativelyimportant exporter of petroleum, petroleum proceeds being valued at $85 millionequivalent in 1972 and $285 million in 1974. Virtually all of the productionhas come from a single find by the Italian ENI in 1964 on the Tunisian-Algerianborder. UN intervention was necessary to settle the ownership question (70percent of the reserve was attributed to Tunisia), and a common developmentprogram was then agreed by the two Governments. The Societe Italo-Tunisienned'Exploitation Petroliere (SITEP), with 50 percent participation by theState and ENI, was created to exploit the field, which entered productionin 1966, cumulative production by the end of 1972 exceeding 21 million tons.The El Borma crude is light and of very low sulfur content, which places itat/a considerable premium in European and American markets. As a result,most of the production has been exported. A factor facilitating the trans-port of the El Borma production was the existence of the Trapsa pipeline fromthe Southern Algerian fields to the Tunisian port of La Skirra, built in1959, with a proven capacity of 15.6 million tons per year; El Borma waslinked to the Trapsa line by another 114 km pipeline. Since El Borma crudecontains large quantities of associated gas, a separate gas pipeline hasrecently been constructed. The output of El Borma, which has total recover-able reserves of 40-50 million tons, has reached its peak of 4.5 milliontons, and is now expected to decline by 8 percent per year. Renewed

1/ The industrial groupings are similar to, though not always identical with,those used in the Fourth Plan. Thus petroleum refining is included withcrude petroleum and phosphate fertilizers with phosphate rock production.Steel and motor vehicle assembly are broken out, for separate discussion,from the Plan category "Mechanical Industries", while "Chemicals","Wood, paper and sundry industries" and "Food processing" are discussedonly in terms of representative sub-industries, i.e. pulp and paper,phosphate fertilizers and sugar production. This restriction is nottoo important; it was obviously impossible to cover all industries.The most important omissions where, ideally, additional coverage wouldhave been desirable, are probably fruit and vegetable canning, theleather processing industry, and handicrafts and carpet-making.

- 14 -

intensive exploratory efforts, combined with technological advances in off-shore activities, have identified four more fields. The first three are ex-pected to peak at a combined output somewhat below 0.5 million tons. 1/. Thelatest discovery, Ashtart, located off the shore in the Gulf of Gabes, ismore important, with an expected production in the range of 1.0-1.5 metrictons. It is scheduled to enter production in 1974. The oil extracted fromthis field differs sharply from that of other Tuiiisian sources, being aheavy oil with a moderately high sulfur content (2-3 percent), and willprobably have a higher value for domestic refining than for export.

14.3 Crude oil production is likely to remain around the present levelfor a number of years. Unless new discoveries of some importance are madein the next two or three years, however, a subsequent decline in productionis inevitable. Prospects for such discoveries are essentially limited tooff-shore oil, the mainland having been intensively explored. During thedecade 1962-1971, D 94 million were invested in exploration and developmentwhereas, since the discovery of the Ashtart field in 1971, investments havejumped to D 29 million for the single year of 1972 (D 16 million for explora-tion, D 8.5 million for the development of Ashtart, and D 4.5 million for otherdevelopment).

Table 14.1: INVESTMENT IN PETROLEUM EXPLORATION AND DEVELOPMENT(millions of Dinars)

1962 1963 1964 1965 1966 1967 1968 1969 1970 1971 1972

TotalTunisia 4.3 3.7 7.1 11.1 13.4 12.3 12.0 9.2 8.6 12.7 28.9

El Borma 1.0 0.9 2.8 6.0 8.8 5.1 4.3 4.7 5.2 5.4 2.2

Other 3.3 2.8 4.3 5.1 4.6 7.2 7.7 4.5 2.6 7.3 26.7

14.4 To date, two major sources of natural gas have been located. TheSidi Abderrahmane field in the Cap Bon was discovered in 1949. Since 1959its production has been used to supply the Tunis area, where a small numberof industrial plants and 220,000 households are linked to the SERENT system,taken over by STEG in 1971. Production from this field peaked at 9.5 millioncubic meters in 1968 and has declined very rapidly since. It now providesless than 1 million cu.m. annually, necessitating additional production ofgas from light fuels. As a potential source it has now been surpassed by

1/ The Douleb-Tamesmida field entered production in 1968 and is nowreaching its peak output at 250,000 tons annually; this production isbrought by separate pipeline to La Skirra. Two other fields locatedon the coast between Sousse and Sfax entered into production in 1973;their long-range production potential is projected at about 200,000tons per year each.

- 15 -

associated gas from El Borma oil fields, the production of which reached1.2 million cu.m. in 1971. Flared in the past, this gas will now be tappedthrough a new pipeline to Gabes, with pressurization use limited to the an-nual throughput capacity of 300 million m3. 1/ There it will supply an elec-tricity generating complex as well as several other industries planned forthe area. The three other oil fields are potential sources of relativelysmall amounts of gas. A large gas field was discovered at Sidi El AgarLab,but the gas will not burn in the open air.

14.5 The STIR refinery at Bizerte was completed in 1964. This refinery,Tunisia's first, was a joint venture of the Tunisian State and Italian petro-leum interests. With a nominal capacity of one million tons, it was well belowthe optimal size for even a simple refinery. Designed essentially to supplythe domestic needs for refined products, the refinery operated below capacitythrough 1968, utilizing a mix of foreign crude oils with a yield approximatingthe consumption pattern of the domestic market. Higher oil prices resultingfrom the closure of the Suez Canal made marginal exports of refined productsattractive; these exports have subsequently shrunk because of rising domesticrequirements. Since 1968, the refinery has been operating at capacity.

Table 14.2: PRODUCTION AND CONSUMPTION OF REFINED PETROLEUM PRODUCTS 1964-1972

1964 1965 1966 1967 1968 1969 1970 1971 1972

Production (000 tons) 719 742 806 858 1037 1101 1163 1156 1093

Domestic consumptionof locally refinedproducts 569 638 723 722 769 833 936 976 941

The growth of domestic needs beyond refinery capacity and the transit of 13million tons of crude oil through La Skirra (of which 4 million tons is

Tunisian crude) have spurred plans for building a second refinery with acapacity of the order of 6-8 million tons. It should be possible to buildthis refinery with sufficient capacity to increase refined product exportsand to locate it in the South rather than to extend the Bizerte facilities,since it would be closer there to the supply of crude from the Trapsa pipelineand the Ashtart field. Moreover, this refinery could be a basis to developchemical industries in the region, which enjoy especially favorable prospectsas a result of new petroleum prices.

14.6 Petroleum world prices have been multiplied by 3.5 in 1974 in com-parison to 1973. Even with the expected decrease in production in the comingyears, the Tunisian economy will benefit substantially from the new prices.In 1973, crude oil and refined products exports came to 4.1 million tons and

1/ The size of the pipeline is determined mainly by the declining futureavailability of gas, allowing for reinjection of gas into the oil fieldsto maintain their pressure.

- 16 -

imports to 0.8 million (Statistical Appendix, Table_ 9.6.1), net exports amount-ing to 3.3 million tons and representing D 34 million. In 1974, the volumeof net exports will be only about 2.8 million tons as a result of a decreasein production and an increase in domestic consumption, but their value willbe over D 100 million.

B. Phosphate Mining and Fertilizer Production

4.17 Phosphate mining and processing is a major economic activity inTunisia. In recent years, phosphate rock production has been in the rangeof 3.0-3.4 million tons. Total exports of the phosphate sector were valuedat D 23 million in 1972, of which D 10.3 million was phosphate rock andD 12.7 million phosphate fertilizers. Phosphate mining is of crucial im-portance to the poor region around Gafsa, employing about 11,000 people andproviding the immediate livelihood for an estimated 50,000. In recent years,the industry has run into substantial difficulties. A drastic decline wasavoided by converting a growing proportion of phosphate rock into phosphatefertilizers. According to the Fourth Plan, the conversion of rock intofertilizers would roughly double by 1976 to 2.1 million tons. At the sametime, exports of phosphate rock would be maintained at the present level ofabout 2.3-2.4 million tons. The export value of pbosphate rock and phosphatefertilizers, at 1973 prices, would then attain D 38 million. The success ofthis strategy will depend upon Tunisian competitiveness in both the miningand the fertilizer ends of the business.

14.8 Up to 1973, world demand for phosphate fertilizers grew by about7 percent per year; world phosphate rock production increased at about thesame rate, from 40 million tons in 1960 to 85 million tons in 1971. Tunisia'sproduction, on the other hand, after rising from 2.0 million tons in 1960to 3.5 million tons in 1965, has since stagnated in the range of 3.0-3.4million tons; in two abnormal years, due to floods, production even fell wellbelow 3.0 million tons. Having reached a high of about 5 percent of worldproduction in the mid-1960's, Tunisia's share has now fallen to about 3.7percent.

14.9 Since the period of exceptionally high export prices in 1965 and1966, and up until 1973, the mines generally operated at a loss, with lossesaveraging about D 2 million per year since 1968. These losses were due toboth external and internal factors. The external factors include a severedrop in prices, compounded by a $3 per ton fall in world market dollar quotationsand an eight percent devaluation of the dollar in relation to the Tunisiandinar. In real terms, i.e. taking into account also the fall in the value ofmoney as measured by the Tunisian Consumer Price Index, proceeds from sales ofphosphate rock in 1972 were only about two-thirds of their 1963 level.

14.10 Depressed prices were related to the vigorous expansion of theUnited States phosphate industry, which increased its export market sharefrom 24 to 30 percent between 1965 and 1972, entering Tunisia's traditionalmarkets in Western Europe. Tunisia's problem was accentuated by the low aver-age grade of its rock. In fact, 90 percent of Tunisian rock grades 65/68percent BPL, whereas other major exporters market a significantly betteraverage grade and, as the following table indicates, obtained far higheraverage prices.

- 17 -

Table 14.3: AVERAGE GRADE OF WORLD PHOSPHATE ROCK DELIVERIES AND AVERAGESELLING PRICES, 1972

Grade BPL Share in World Production List Prices Florida Rock% US$/ton FOB

Below 68 39 8.50 (aver. 64-66 and 66-68)69-72 17 9.50 (estimate)73-77 22 11.20 (aver. 72-73, 74-75 and

75-77)Total 100

The prices shown are only indicative of grade differences. In 1970-72,Tunisia 65/68 percent ore sold at $8.63 per ton. The situation has changedconsiderably since 1973 as a result of an increase in fertilizer demand causedby the return of land to wheat growing in the United States and, more generally,by a rise in the rate of world consumption of phosphate fertilizers. Theprice of phosphate has about tripled since the end of 1973 coming up to $36per ton for the Tunisian phosphate quality.

14.11 In spite of its inferior quality, rock phosphate represents one ofTunisia's few natural resources. The infrastructure, some largely amortizedproduction facilities and available labor) constitute additional resourceswhich offer a challenge for their more efficient use in the future. Further-more, Tunisian phosphate fertilizers can be imported free of duty into theEuropean Common Market, whereas fertilizers imported from the United Statespay a six percent duty. Unfortunately, present mining operations are char-acterized by very low productivity, obsolete equipment, unsafe working con-ditions, high labor turnover, and inadequate staffing. 1/ A major effort willtherefore be needed, both in investments and management, first to raise pro-duction to the Plan target of 4.5 million tons of saleable product by 1976(including production of about 250,000 tons from the Kasserine area) and,second, to increase productivity. The program of modernization and develop-ment of the phosphate mines puts the necessarv investment at about D 60million. Its implementation and success will be facilitated by the recentrise in prices.

14.12 The output of the Tunisian fertilizer industry has risen from amodest level in 1960 until it now absorbs nearly one-third of production ofthe mines. The potential advantage of such conversion is substantial: forevery D 2.72 per ton of phosphate rock added in mining, another D 5.25 canbe added in processing (figures for 1971). Three major producers and threesmaller producers are now active in the fertilizer industry.

1/ Sfax-Gafsa employed 11,000 people to produce 3.15 million tons ofsaleable product (3.5 man-years per 1,000 tons) in 1972. OCP, Morocco,employed 13,000 people to produce about 14 million tons (0.93 man-yearsper 1,000 tons).

- 18 -

Table 14.4: DOMESTIC PRODUCTION CAPACITY AND rMPLOYMENT, 1972

1972 CapacitiesStart of (th. tons) Total Employ-

Company Ownership Operations Product Product Rock Equiv. Invest. ment$ mill.

SIAPE State (86%) 1952 TDP 260 455 14 650NPK Foreign

Private (83%) 1966 TSP 200 350 15 490ICM State (55%) 1972 Phosph. 110 420 25 213

acid

14.13 Investments in the phosphate fertilizer industry are valued todayat about D 23 million equivalent, of which about D 4 million is in SIAPE (netassets as of December 31, 1972), D 8.5 million in NPK (excluding accumulatedlosses) and D 10 million in ICM (Stage I). The first two produce triple super-phosphate (with phosphoric acid as an intermediate product). In contrast,since July 1972 ICM has been producing phosphoric acid for export. Theearnings record of SIAPE was until recently unsatisfactory while NPK has yetto yield a profit. The reasons for poor earnings are manifold: insufficientcapacity utilization (NPK), variations in the quality of phosphate received(the good qualities being reserved for export), mill maintenance problems,sensitivity to the fluctuating margin between raw phosphate prices andfertilizer prices. Present plans envisage the expansion of SIAPE and NPKproduction by about 50 percent by 1976 and a virtual doubling of ICM's capacity.

14.14 Fertilizer manufacture involves very heavy investments and has ahigh cost per job created. The planned investments are justified only if theindustry enjoys adequate comparative advantages. Since 1973, phosphate andfertilizer prices have soared. In view of the likelihood of an increase inproduction in some countries and the appearance of new manufacturers, priceswill probably decline over the next three or four years; however, they shouldstabilize at a level justifying such investments. Moreover, the advantagesderiving from savings in transportation. processing and handling costs areassured, particularly in the case of triple superphosphate. Ilowever, the costof capital will be of crucial importance in such capital-intensive investments,and the future competitiveness of an expanded fertilizer production in Tunisiawill hinge very much upon the extent to which incremental costs are lower thanaverage conversion costs in present plants.

C. Mining, Other Than Phosphate

14.15 The phosphate industry accounts for about 60 percent of the valueof mineral production. Iron ore and lead-zinc concentrates each account foranother 13-14 percent, while salt and fluorspar each account for about 5 per-cent. The total value of minerals production other than phosphates was aboutD 9 million in 1971. Production during the last five years has been declining,with prices for iron ore and lead-zinc concentrates generally unfavorable.Only in fluorspar has there been considerable expansion. Salt is recoveredfrom salines along the coast. Production would have increased were it notfor substantial damage caused by a flood in 1969. The industry overall at

- 19 -

present employs about 8,000 workers plus an estimated 2,000 artisan miners,and is important to the economy of some regions otherwise lacking in devel-opment potential (particularly true for Djerissa iron mines). G.O.T. is themain shareholder in the Djerissa company and in Sotemi which operates thenon-ferrous metals mines. The only exceptions to state operation are (a) thesalt producer, which is a subsidiary of a French company and (b) thePennaroya-Tunisia company, in which the Government and Pennaroya, France,hold equal shares. This company operates a lead smelter at Megrine whichalso processed imported ores and is developing a new zinc mine at Fedj Hassine.

14.16 The geological background is not favorable to substantial miningdevelopment; known reserves are limited and do not permit the expectationof more than 10 years additional activity in the iron, lead and zinc mines.Moreover, the grade of ore is low or, at best, medium. The economic potentialhas also been reduced by wasteful mining methods. Such methods are stillextensively used among the artisan miners. In many cases, three-quarters ormore of the ore which could have been mined by professional methods is leftin the ground.

14.17 The situation in iron ore and lead-zinc mining is critical. TheDjerissa ore, while grading only 55 percent Fe, is self-fluxing and thereforecommands a reasonable price (about 15 cents per unit FOB in 1972). Un-fortunately, the reserves of the mined hematite were only 3.8 million tonsas of January 1, 1973, corresponding to about 5-6 years of additional life.There are another 14 million tons of iron carbonate grading 40 percent Fe,which could supply 5.6 million tons of saleable concentrates grading 60 per-cent Fe if current studies demonstrate technical and economic feasibility.

14.18 About 30 lead and zinc mines are spread over Northern Tunisia.The grade of ore (about 5-11 percent combined lead and zinc) is barely eco-nomic. Equipment is obsolete, there are managerial deficiencies, an<l pro-ductivity is low. Since proven reserves are small, important new investmentcannot be undertaken apart from the new mine at Fedj Hassine, expected toproduce 25,000 tons of zinc concentrates by 1976. Nevertheless, it is con-sidered likely that present levels of production could be maintained foranother 9-10 years. Moreover, exploration in depth by the Office Nationaldes Mines may establish sufficient reserves to maintain production for an-other 1 or 2 decades.

14.19 Production of fluorspar 1/ (mainly acid-grade) started in 1965 andhas been rising rapidly. Two beneficiation plants (producing 97 percentCaF2 and up concentrates from relatively low-grade 35-75 percent ores) arein operation and another is projected. Market prospects appear to be rea-sonably good and production is expected to reach 110,000 tons by 1976, com-pared with 50,000 tons in 1972. Reserves by the end of 1972 were estimated

1/ Fluorspar is used to produce hydrofluoric acid which (in the form ofaluminum fluoride) is used in aluminum smelting and in the chemicalsindustry. CNEI has been working on a project to convert fluorsparinto hydrofluoric acid and its derivatives (aluminum fluoride).

- 20 -

at 7.5 million tons (proven, probable and inferred) which would yield notquite 2 million tons of saleable concentrate. Additional reserves are likelyto be located; major world aluminum producers have expressed interest inparticipating in exploration. A few years ago there was a world shortage ofacid-grade fluorspar which has now been overcome, prices for concentrateshaving declined from $70-80 per ton to $50-60 per ton (FOB Tunisian port) in1973. These prices were still remunerative and went up since then.

14.20 During the last decade about D 8.5 million was invested in the ex-ploration and production of ferrous and non-ferrous metals. It is expectedthat a similar sum will be spent in 1973-76. This includes exploration ex-penditure of D 3 million. Exploration is concentrated on about 60,000 sq.km. in Northern and Central Tunisia. The annual exploration expenditurerepresents about 10 percent of the value of mineral production, 1/ (mostcountries spend only 1-2 percent). This high rate is necessary to makeup for past neglect, and is justified with a view to maintaining mining pro-duction at the present level, or, hopefully, permitting a slight increase.Employment is expected to fall by about 20 percent, mainly through the dis-appearance of artisan miners.

14.21 It is an extremely difficult task to inject new life into an in-dustry whose time is apparently running out, and the problem is exacerbatedby surplus labor, since the States mines maintain people on the payroll torelieve unemployment. One cannot feel optimistic about the commercial ex-ploitation of carbonates at Djerissa (deeper 'Level mining, additional proc-essing). A feasibility study is expected by the end of 1973. By that time,the Tunisian Government will need to devise some combination of a subsidy tomaintain jobs for miners (presently numbering 1,400) and supporting personnelin their present habitat with an orderly system for transferring personnel toother mines or otherwise retraining and resettling them. 2/ A similar situa-tion exists with respect to the mining of non-ferrous metals.

D. Sugar

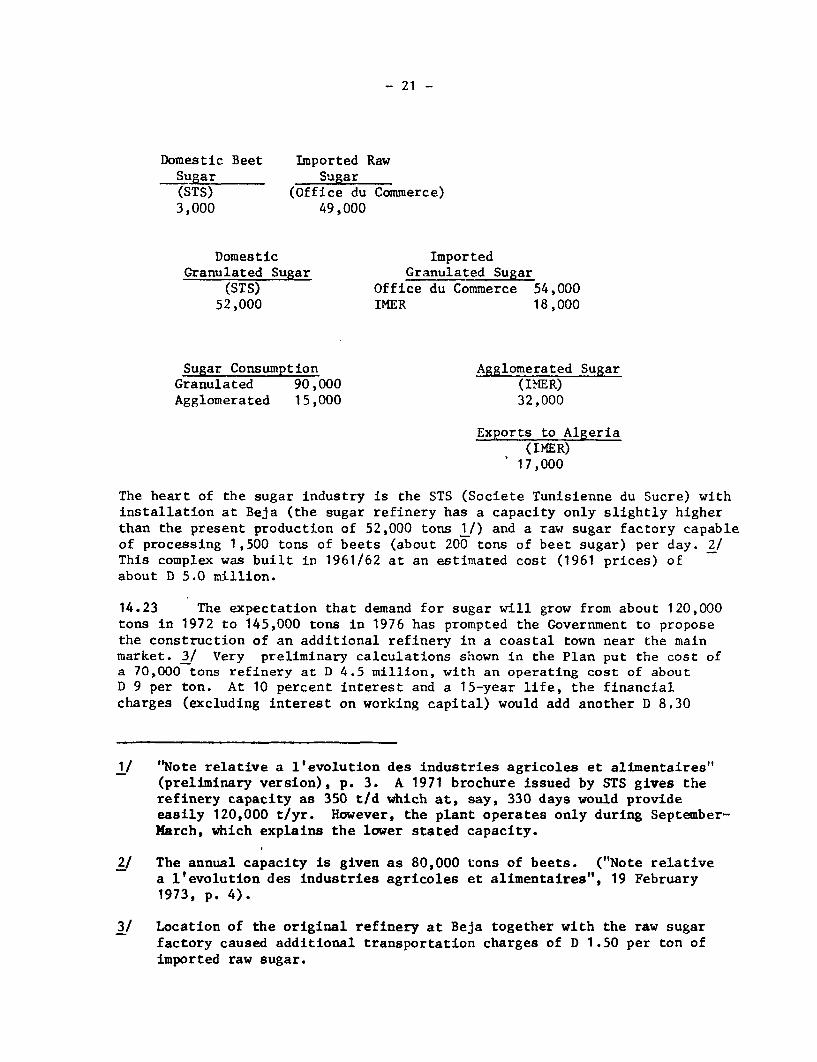

14.22 The sugar economy of Tunisia may be shown by the following diagram(figures in tons):

1/ Excluding salt and phosphate production where no exploration is done.

2/ Such a gradual demobilization is taking place (under much more favorablecircumstances) at the Tamera Mine near th'-e El Fouladh steel mill, whereemployment has been reduced from 848 in 1968 to 240 today, apparentlywith no great change in production.

- 21 -

Domestic Beet Imported RawSugar Sugar(STS) (Office du Commerce)3,000 49,000

Domestic ImportedGranulated Sugar Granulated Sugar

(STS) Office du Commerce 54,00052,000 IMER 18,000

Sugar Consumption Agglomerated SugarGranulated 90,000 (IMER)Agglomerated 15,000 32,000

Exports to Algeria(IMER)

17,000

The heart of the sugar industry is the STS (Societe Tunisienne du Sucre) withinstallation at Beja (the sugar refinery has a capacity only slightly higherthan the present production of 52,000 tons 1/) and a raw sugar factory capableof processing 1,500 tons of beets (about 200 tons of beet sugar) per day. 2/This complex was built in 1961/62 at an estimated cost (1961 prices) ofabout D 5.0 million.

14.23 The expectation that demand for sugar will grow from about 120,000tons in 1972 to 145,000 tons in 1976 has prompted the Government to proposethe construction of an additional refinery in a coastal town near the mainmarket. 3/ Very preliminary calculations shown in the Plan put the cost ofa 70,000 tons refinery at D 4.5 million, with an operating cost of aboutD 9 per ton. At 10 percent interest and a 15-year life, the financialcharges (excluding interest on working capital) would add another D 8.30

1/ "Note relative a l'evolution des industries agricoles et alimentaires"(preliminary version), p. 3. A 1971 brochure issued by STS gives therefinery capacity as 350 tld which at, say, 330 days would provideeasily 120,000 t/yr. However, the plant operates only during September-March, which explains the lower stated capacity.

2/ The annual capacity is given as 80,000 tons of beets. ("Note relativea l'evolution des industries agricoles et alimentaires", 19 February1973, p. 4).

3/ Location of the original refinery at Beja together with the raw sugarfactory caused additional transportation charges of D 1.50 per ton ofimported raw sugar.

- 22 -

per ton. The margin between imported refined sugar and imported crude sugar(D 20 in 1973) is enough to make a new refinery an attractive investment. 1/Agglomerated sugar sells at a further premium of D 20 above granulated sugar.

E. Textiles, Clothing, Leather and Shoes

14.24 The textiles (spinning, weaving and finishing) and clothing (in-cluding shoes and leather) sectors accounted for about 30 percent of theindustrial value added outside food processing in 1972, and over 50 percentof the employment. The percentage breakdown, by activities, is slhown below:

Table 14.5: TEXTILES AND CLOTHING: DISTRIBUTION OF VALUE ADDEDAND EMPLOYMENT BY SUB-SECTORS, 1972

PercentagesValue RatioAdded Employment Col. 1/Col. 2

Spinning, weaving, finishing 43.2 13.5 3.2Clothing and knitwear 23.6 16.8 1.4Carpets 19.3 64.5 0.3Leather and shoes 13.9 5.2 2.7

100.0 100.0 1.0

The output of the sector as a whole has grown by 20 percent per year overthe last decade. The production of cotton yarn and fabrics has grown fromnegligible quantities to about 10,000 tons of yarn and 38,500 tons of fabrics.The Office National de l'Artisanat invested about D 4 million in carpet produc-tion during the last decade, and production is estimated to have increased2-1/2 times. Figures in Table 14.5 Column 3 indicate the striking employmentpotential of the clothing and knitwear sector and, particularly, carpet making.The high ratio of employment to value added in the latter sector does, however,also reflect a low rate of remuneration.

14.25 Until recently the textile sector was dominated by the state enter-prise Sogitex, which operates six textile and clothing mills with a capacityof nearly 6,000 tons of cotton yarn, 27 million meters of woven goods (cotton,artificial and synthetic), Tunisia's main textiles finishing plant (with ca-pacity for treating 25 million meters of fabrics), and one factory makingjeans, shirts, and working garments entirely for export.

14.26 Nevertheless, the private sector has been expanding. Whereas, inthe beginning, Sogitex was responsible for 80 percent of the Tunisian produc-tion of woven fabrics, today the proportion is less than one-half. The next

1/ The present price difference between raw and refined beet sugar in theEuropean Common Market countries lies in a range of roughly D14-18 perton.

- 23 -

largest enterprise is the Djilani group, which operates a cotton weaving plantat Sfax, and will be constructing a spinning plant with an initial capacityof about 1,500 tons at the same location. The same group is also initiatingthe manufacture of clothing and knitwear for export, the latter on a largescale, in association with the leading French textile manufacturer. Otherleading manufacturers, for the most part, have entered certain specializedcorners of the market, where they have substituted for imports with varyingefficiency (jute cordage and sacks, knitwear, terry cloth, woolen blankets,etc.). The rest of the industry is small and fragmented. Certain imbalancesof structure are apparent: Sogitex, which used to have a surplus of cottonyarn, is now importing such yarn. There is a special scarcity of combed yarn,though such yarns will be produced increasingly by both Sogitex and theDjilani group. The Sogitex finishing mill (the largest in Tunisia) hasmodern equipment, but has certain operating problems; custom finishing forother producers represents only 10-20 percent of its total business.

14.27 The Plan sets the following targets:

Table 14.6: TEXTILES AND CLOTHING: FOURTH-PLAN TARGETS(Dinars Million)

1972 1976

ExportsClothing and knitwear 2.6 39.0 (Clothing 30.3;

knitwear 8.7)Cotton fabrics 1.2 4.5Carpets 2.3 3.5Other (e.g. shoes) 1.2 1.3

Total 7.3 48.3

Employment (Thousands) 50.2 75.8

Investments, 1973-76 39.6

Spinning, weaving, finishing 21.0Clothing and knitwear 16.8

This 'program is heavily dependent on clothing and knitwear exports. One-half of these exports are already covered by factories under constructionwith the benefit of the export promotion law of April 1972. There is avirtually unlimited market in Western Europe, particularly for clothing,and Tunisian exports would represent only 4 Dercent of the imports projectedby the Six. Moreover, in foreign or mixed Tulnisian-foreign ventures, theforeign investor will contribute a built-in market. Finally, Tunisian com-petitiveness in items like standard shirts and blue jeans is very great:because of the low wages, the manpower cost per unit produced, in spite oflow productivity, is only about 60 percent of the corresponding cost inWestern Europe, and this far outweighs higher depreciation and financialcharges. Eventually, it should also be possible to raise the output perman-hour on existing installations by 50-100 percent, thus reducing both

- 24 -

capital and labor charges. There is a shortage of foreman and maintenancemechanics, but it is planned to relieve this shortage through appropriateaction. The most serious problem is the upgrading of the mass of semi-skilled labor, mainly raw recruits from agricultural areas, unused to in-dustrial discipline, and with a high rate of turnover. Tunisian managersof both textile and clothing mills expect productivity to rise considerablyover the next few years. A realistic study of what is likely to happen toproductivity and wages, on reasonable assumptions with respect to emigration,would be of great value for industrial planning and to entrepreneurs, bothforeign and domestic.

14.28 Working within a financial constraint, leading companies clearlysee their main comparative advantage in the clothing end, which is thereforebeing pushed at the expense of spinning, weaving, and finishing. The Planitself adopts the pessimistic hypothesis that all exports of clothing andknitwear will be based on imported fabrics. Export processing firms willhave complete freedom of procurement, turning to Tunisian supplies onlywhere these would be competitive in terms of price, delivery periods, andabove all quality.

14.29 The question has been raised to what extent Tunisia is really readyto join the textile export business (as distinguished from clothing and knit-wear) and, if the answer is in the affirmative, at what rate and for whatproducts. A subsidiary question is how hard it should aim at supplying itsown export processing industries in clothing and knitwear, or whether itshould seek a more general market orientation. Investment in the spinningof cotton for export would mean competition with yarn flowing to Europeanweaving mills in a constant stream from factories in cotton-producing coun-tries (Turkey, Nigeria, Ivory Coast, Congo), and production and marketingskills in woolen and worsted weaving, not yet available in Tunisia. But ifthese fields are difficult, gradual entry into the custom spinning of arti-ficial and synthetic fibers and the weaving of cotton-type fibers should befeasible. Both in weaving and finishing, the first priority is to use exist-ing capacities more effectively. Since finishing capacity could be doubledwith only a 30 percent increase in the original investment, the main invest-ment should presumably be in weaving.

14.30 The next 3-4 years will be crucial for the private textile sector.The domestic market is extremely small, with its import substitution poten-tial largely exhausted, and it will come under increasing pressure from newfirms established in the customs-free zone which could well dump on theTunisian market (after payment of import duty) certain lots which, for qualityor other reasons, had not been deliverable abroad. It is therefore necessarythat small Tunisian mills turn increasingly towards exports (including salesto clothing and knitwear manufacturers-exporters established under the Law ofApril 1972). Regroupings and mergers will be necessary for economies in ex-port marketing, research and development, manpower training. Speed is essen-tial, since many other countries are vying for a place in the European market.

- 25 -

14.31 Sogitex's problem is different. It is an established producer ofreasonable size. It has an investment program totalling D 4.5 million, butonly one-half, covering the most urgent needs, has been sanctioned for thenext 4 years. This is because the program has been tailored to the expectedavailability of self-financing. The company's financial structure is excep-tionally weak. In 1972, the gross cash flow of D 2 million was absorbed al-most entirely by loan repayments. Nevertheless, the long-term outlook issound if good management can be maintained. Financial restructuring shouldtherefore be pushed more vigorously. A restructured Sogitex could, in theory,initiate a more ambitious investment program. At the same time (and this seemsto be the present intention), Sogitex might give off certain units which wouldthen form the nuclei of viable new firms. Sogitex and these nuclei couldthen provide a lease on life to small firms through subcontracting.

14.32 The current Tunisian production of shoes of all types is aboutseven million pairs, predominantly for the domestic market. About one-quarter are produced on an industrial scale by Bata and SICA, the restbeing furnished by some 20 medium and small establishments and by artisans.This includes a high and rising proportion of textile shoes. In contrast,plastic shoes are not allowed to be manufactured in Tunisia. While bothsole leather and leather for uppers are produced ,(there is one tannery forcattle hides and two smaller tanneries for sheep and goat skins), the sup-ply of hides and skins is a major problem, and 60 percent of the cattlehides are imported. Only about one-third of the gross supply of sheepskinsand goatskins are industrially tanned (Tanneries Modernes de la Manouba),another third are treated by small tanners and artisans (some of these arepickled and exported) and the remainder are either sold with the wool totourists (about 200,000 skins) or lost. 1/

14.33 There is a very considerable export market for shoes in WesternEurope, as may be seen e.g. from the following summary of imports by theexpanded Common Market in 1971 (million pairs):

Footwear with leather uppers 19.5Slippers and other house shoes 21.5Footwear made primarily from textiles 59.4Rubber footwear 22.6Footwear made of plastic materials 29.8

152.8

Though these imports have nearly trebled since 1973, they still representonly about 15 percent of total Western Europe consumption. In addition,there are major export opportunities for skin and leather garments, gloves,and ladies handbags. Western European manufacturers are looking for oppor-tunities to establish processing plants in the Mediterranean area, partic-ularly in countrieb which will be associated with the Common Market. The

The proportions just indicated are highly uncertain; statistics andinformation on this subject are vague and contradictory. It is possi-ble that a far higher proportion of the sheepskins are not exported

with the wool.

- 26 -

main reason is an acute labor shortage, which has led to the closing ofplants in Germany and has thwarted shoe industry expansion in Austria.The Tunisian shoe industry can enter this market initially with shoes inthe lower and medium price ranges where quality requirements are not severe.

14.34 The Plan foresees only relatively minor investments totalling D1.3 million in the shoe industry and only a 25 percent increase in produc-tion and employment, i.e. no major change in productivity. Perhaps thesegoals are realistic, but to an outsider they seem too modest. Shoes, glovesand leather goods is a sector where Tunisia could incontestably attain a com-parative advantage. Three related and carefully phased types of action maybe envisaged: a development plan for these industries to be prepared byconsultants, the active canvassing of foreign investors interested in thisparticular industry, and the support of SNI and other banks for the restruc-turing of small industries and artisan shops.

F. Pulp and Paper

14.35 The production of pulp and paper merits special attention because:(a) it is the largest industry in the suib-sector "Wood, Paper, Printing andSundry Industries", (b) it represents a pioneering effort to extend Tunisia'sindustrial potential while at the same time providing employment opportuni-ties for an under-developed region, (c) pulp and paper production has en-countered so many problems that there are serious doubts about even theshort-term viability of this industry, which directly employs about 3,500in the Kasserine region, if the harvesting of esparto grass is induced.

14.36 The SNTC (Societe Nationale de Cellulose) was created in 1963 toproduce pulp from esparto grass at Kasserine, in the center of the regionwhere this grass grows wild, and possessing river water and a large supplyof under-employed labor. The mill was to have a capacity of 80 tons perday (an estimated 24,000 tons per year). The foreign suppliers withdrewafter two years when the mill had attained a maximum output of only 45 tonsper day; with technical assistance from other sources, the rate has now beenbrought up to 76 tons per day. The total investment as of the end of 1972was D 7.5 million equivalent; the accumulated losses as of the end of 1970nearly D 3 million. An additional D 8 million has been invested in infra-structure (houses, schools, hotels, etc.).

14.37 The pulp mill was originally intended for export production. How-ever, it was decided to provide paper-making facilities at the same location.The paper making company, Sotupalfa (under joint management with SNTC) wascreated in 1964, and a mill with nominal capacity very similar to that ofthe pulp mill started operating in 1970. The paper mill has produced at,or even above rated capacity, but because of market constraints, annual pro-duction in 1972 was only 15,000 tons.

14.38 The pulp mill had a marginal economic justification (its justifica-tion conceivable only in terms of employment and other developmental bene-fits). While the technical problems have now been solved, the economic andfinancial problems are becoming critical:

- 27 -

(a) Traditionally, there was a market for esparto grass in theUnited Kingdom, France and Spain; the resulting relativelyshort-fibered pulp was used in special grades of printingand writing papers. Today, however, papermakers can obtainsimilar qualities through the beating, blending and refiningof wood pulp.

(b) Esparto grass is becoming increasingly costly. It takes 2.4tons of esparto grass (at D 12.50, say D 30 per ton, deliveredat the mill) to produce one ton of pulp. Moreover, the grasscan be harvested only during November-March, which gives riseto substantial storage costs, and operations cannot be mechanized.

The total production of esparto pulp is only 60,000 tons/year, and previouslyexisting plants in Algeria, Spain and France have either closed, or facegreat difficulties in staying alive. 1/ But the most vital threat t:o theTunisian plant is that, because of the rural exodus, the source of manpowerfor harvesting is drying up. Even though exports of esparto have been pro-hibited, the situation is expected to become critical during the 1974/75campaign. Possibilities of forest planting (e.g. eucalyptus) as a substi-tute pulping material are discussed in the chaptei on Agriculture.

14.39 One major idea behind the creation of the paper company was tofind a local market for the pulp. Another was to achieve certain economiesin investment and production costs by integrating pulp and paper production.These objectives, however, were offset by several drawbacks:

(a) The total Tunisian market for paper is less than 40,000 tons,of which about one-third is for kraft paper, and another thirdfor special grades which cannot be made by Sotupalfa, leavingonly about 12-13,000 tons as the present local market. Hence,roughly one-half of the production has to be exported. Yetexport prices barely covered raw material costs.

(b) In 1971, the company produced 40 different types of paper(without considering variations in thickness and weight),with the result that the idle time of the machines roughlyequalled their production time. In 1972, the number oftypes manufactured was cut drastically to 5, which couldhardly satisfy the needs of the market, increasing thepressure for paper imports.

(c) Even with increased product specialization, Sotupalfa usedonly about 50 percent esparto pulp. The rest was importedin the form of long-fibered pulp ane. was burdened with ad-ditional transportation from port to mill. A further im-plication was, of course, that only about one-quarter ofthe esparto pulp was absorbed domestically.

1/ Nevertheless, a new Algerian plant with a capacity of 36,000 tons/yearis scheduled to start operations in about 3 years.

- 28 -

For all these reasons, it is clear that there can be no viability based uponthe Tunisian market. Better economics can only be obtained through special-ization (utilizing whatever advantages esparto pulp may still possess forcertain uses). One way of achieving this would be to interest an interna-tional paper company in becoming a partner and assuming the responsibilityfor export marketing.

G. Construction Materials (particularly cement)

14.40 The construction materials sub-sector, with a 1972 value added ofD 7.0 million at current prices, accounted for about 8 percent of industrialproduction but less than 6 percent of industrial employment. A substantialnumber of people are employed in brick and tile making and in cement products,essentially for the home market. Value-wise, and particularly in terms oftotal investments, cement production is the most important activity. At aplanned expenditure of D 21 million, it accounts for three-quarters of theprojected investments 1973-1976. Another important activity is the produc-tion of glass containers (Sotuver). Sotuver's expansion plans are essentiallygeared to the domestic market for glass containers. The Tunisian market istoo small for the economic production of window glass.

14.41 Tunisia's two cement mills have a combined capacity of 630-730,000tons. The larger one, CAT, near Tunis, produced 430,000 tons in 1972, thesmaller, CPB, near Bizerte, produced 196,000 tons. Both mills are in thestate sector, as are most of the other enterprises in the construction ma-terials industry. Much of the cement mill equipment is old and severelyworn. Production has fallen behind the country's rapidly expanding needs,and 1973 imports are projected at 250-300,000 tons. Demand is expected torise above 1 million tons by 1976. Capacity will be increased by buildinga new cement plant at Gabes with two kilns and by adding another kiln atBizerte, each new kiln having a capacity of 1,000 tons per day, say 330,000tons a year. In addition, a regional project is currently being studiedwith Algeria.

H. Steel

14.42 Studies for a steel mill were begun in 1959, and orders for aplant to be located at Menzel Bourguiba placed in 1963. The mill was com-missioned by the end of 1965 with the following major units: blast furnace(300 t/d), two oxygen steel converters of 12 tons each, a two-strand con-tinuous caster with a capacity of 300 t/d of billets, and a combinationmerchant bar and wire rod mill with a capacity of 12 t/h. The total in-vestment was D 25.5 million. The company would use ore from Djerissa,as well as from a small deposit close to the mill, together with importedcoke.

14.43 The scheduled annual production was 100,000 tons of pig iron (ofwhich part would be exported), and 70,000 tons of finished steel. Actualproduction and sales have grown as follows:

- 29 -

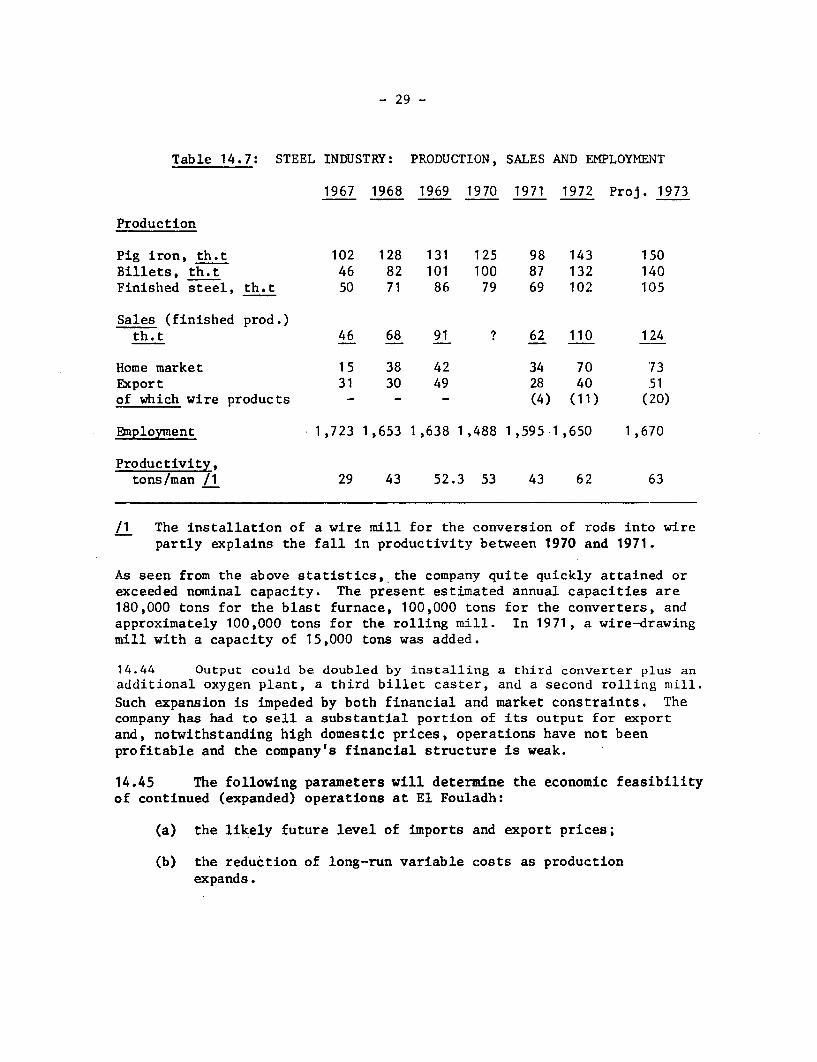

Table 14.7: STEEL INDUWSTRY: PRODUCTION, SALES AND EMPLOYMENT

1967 1968 1969 1970 1971 1972 Proj. 1973

Production

Pig iron, th.t 102 128 131 125 98 143 150Billets, th.t 46 82 101 100 87 132 140Finished steel, th.t 50 71 86 79 69 102 105

Sales (finished prod.)th.t 46 68 91 ? 62 110 124

Home market 15 38 42 34 70 73Export 31 30 49 28 40 .51of which wire products - - - (4) (11) (20)

Employment 1,723 1,653 1,638 1,488 1,595 1,650 1,670

Productivity,tons/man /1 29 43 52.3 53 43 62 63

/1 The installation of a wire mill for the conversion of rods into wirepartly explains the fall in productivity between 1970 and 1971.

As seen from the above statistics, the company quite quickly attained orexceeded nominal capacity. The present estimated annual capacities are180,000 tons for the blast furnace, 100,000 tons for the converters, andapproximately 100,000 tons for the rolling mill. In 1971, a wire-drawingmill with a capacity of 15,000 tons was added.