Embed Size (px)

Citation preview

Report No. 7478-GU

GuatemalaPublic Sector Expenditure Review

May 23, 1989

Country Department IILatin America and Caribbean Regional Office

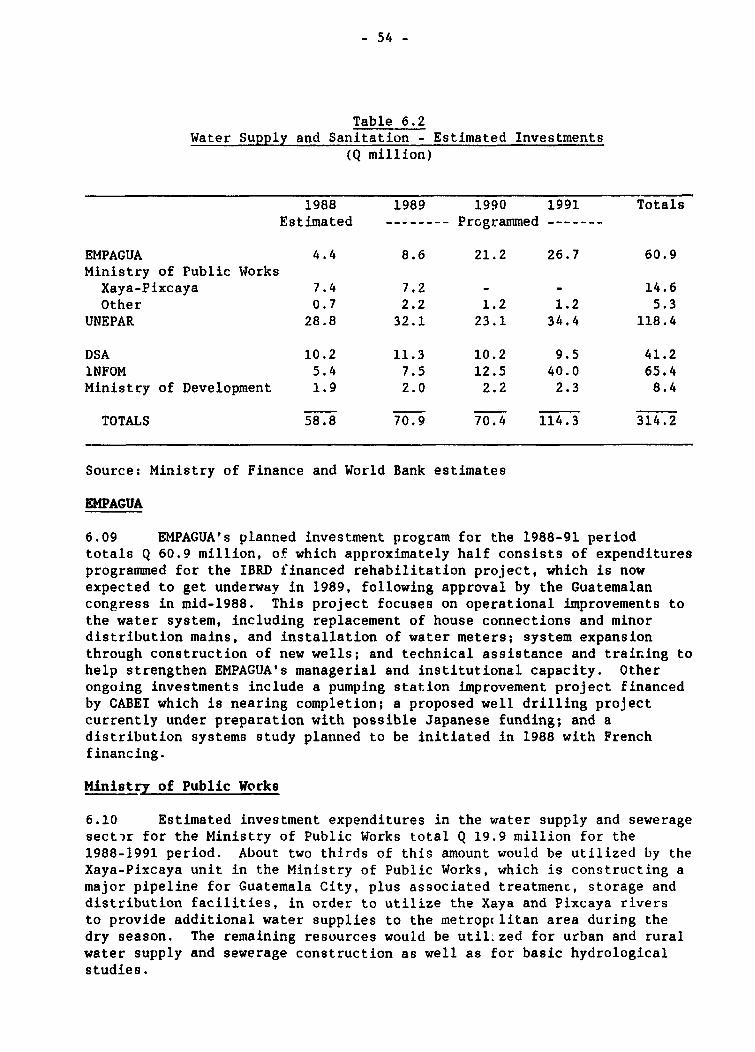

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

US$1 = 2.70 Quetzales (Q)

ABBREVIATIONS AND ACRONYMS

AVIATECA - Empresa Guatemalteca de Aviacion (Guatemalan Aviation Company)BANDESA - Banco Nacional de Desarrollo Agricola (National Bank for

Agriculture Development)BANVI - Banco Nacional de la Vivienda (National Housing Bank)CABEI - Central American Bank for Economic IntegrationEEGSA - Empresa Electrica de Guatemala (Guatemalan Electric Company)EMPAGUA Empresa Municipal de Agua Potable (Municipal Water Supply Co.)EPNSTC - Empresa Portuaria Nicional Santo Tomas de Castilla (Santo Tomas

de Castilla National Port Company)PrGUA - Ferrocarriles de Guatemala (Guatemalan Railway Company)GUATEL - Empresa Guatemalteca de Telecomunicaciones (Guatemala

Telecommunications Company)IDB - Inter-American Development BankICTA - Instituto de Ciencia y Technologia Agricolas (Institute of

Science and Agricultural Technology)IGSS - Instituto Guatemalteco de Seguridad Social (Guatemalan Social

Security Institute)INDE - Instituto Nacional de Electrificacion (National Electricity

Company)INDECA - Instituto Nacional de Comercializacion Agricola (National

Agricultural Marketing Institute)INFOM - Instituto de Pomento Municipal (Municipal Development

Institute)INTA - Instituto Nacional de Trarsformacion Agraria (National

Institute for Agrarian Reform)MCTOP - Ministry of Communications, Transport and Public WorksMSP - Ministry of Public HealthNGOs - Non-Governmental OrganizationsSEGEPLAN - Secretaria General de Planificacion (General Planning Office)UNDP - United Nations Development ProgramUNEPAR - Executing Unit for Rural Water SupplyUSAID - United States Agency for International Development

FISCAL YEAR

January 1 to December 31

FOR OFFCIAL USE ONLY

Page 1 of 2COUNATRY DATA - CUATOKALA

AREA POPULATION D8D&ITY (1986)

108 9 thcus. sq he. In sIllion 8.438 (1q87) 77.5 per sq. kme.Rate of 0rowth: 2.92 (1980-8S) 269.5 per sq. km. of agricultural land

POPUJLATION CH4ARACTERISTICS 1965 1973 1966 IeALTH (1986)

Crude B3irth R&.t* (per 1000) 46 45 40 Populetion per physician 8.600Crude Death Roet (per 1000) 17 1a 10 Populati~ o, e hosputel bed 800Infant Mortality (per 1000 line births) 112 92 65

INCOME OISTRIOUION (Pri-. Ir.con,. Recoi.*d by) 1973 1986 ACCESS T0 ELEACTRICITY (1966)

Highest 20 percent 601 889 1 of d.ellina* - total 37.2

Lo.ast. 20 percent 88 61L.eeot 40 percent 131 148 ESUCATION 1965 1973 1986

ACCESS TO SAFE WATER 1965 1973 198$ Enrolleent Rates:

------ ----- ----- ------ ----- ----- ------ -- -- - --- ---- PrissryF Total 508 616 761Percent of population:

Total 11 39 51 Malo 655 6716 801

Urban 30 as 9 Female 451 883l 721Rurel 2 14 26 Secondary: Total as 121 171

Kael 101 121 171MfEIRITION 1968 1973 1988 Feeale 71 111 161

nenFood Produccion Por Capita (1979.100) 54 78 108 (INP PER CAPITA 1985 1973 1956rer Capita Supply of Calories/day 2.028 2.1.50 2.345----------------- -- --- -P., Capita Supply of Proteins grass/day 57 57 61 (Current US Dollars) 300 430 930

1980 1966 1967 AAB6UAL GROWTH RATES (N, conset, prices)

CROSS NATIONAL PRODUCT oilI. QI ODP oil. Q 8 CDP sil. Q I CDP 1968-73 1973-60 1980-65 196 1966 1987

MOP at earkat prices 7.679 100.0 15.8363 100.0 17.595 100.0 6.1 F.S -0.5 -0.6 0.1 3.1Groom Do...stic In-esteent 1.252 16 1.637 10.3 2,431 13.8 5.2 7.0 -8.1 -19.1 0.2 31.4Cros National Sacings 1.075 13.6 1.481 9.4 1.037 5.9 7.9 3.2 -14.5 -22.6 34.1 -4.8

Curre nt Account Balance (176) -2.2 (93) -0.6 (1,394) -7.9 nt.&. n.a. n... n.e. n.a. n.a.Eaports of Goode A NPS 1.748 22.2 2,542 16.1 2,807 16.0 7.0 5.2 -4.6 3.1 -14.0 6.0Ia.p.rt. of Goo~ds A NFS 1,96 24.9 2.311 14.6 3.948 22.4 3.3 5.6 -9.9 -12.6 -14.7 47.1

Value Added Labor Porce V.A. per Worber

OUTPUT, LABOR FORCE AND PROODUCTIVITY 1960 1967 1980 1987 1960 1967

(Constant 1980 Prices) oil. Q (1) oil. Q (1) EsplO00 (1) Emol.000 (I) Quatnal (1) Quetonl (1)

Aqriculture 1.958 24.8 1.978 25.7 1.034 49.4 838 36.2 1,894 44.6 2.360 69.2Industry 1.733 22.0 1,54S 20.1 384 16.9 378 16.3 4.890 115.1 4.084 119.7se-i~ces 4.189 83.2 4.166 54.2 703 33.6 1,089 47.8 8,958 140.3 3.792 111.1

TotalI/A,-ra,o 7.879 100.0 7,689 100.0 2.091 100.0 2,318 100.0 4.247 100.0 3.412 10000

N,llion Quetoslee As percent of current CDP

CONSOLIDATED NONFINANCIAL PUBoLIC SECTOR 1981 1962 1983 1964 1988 1986 1987 1981 1982 1983 1964 1988 1988 1987

A. TVotal Curre.nt Renenun 974 1012 964 983 1162 1i81 2144 11.3 11.8 10.9 10 4 10 8 it 1 12 8.

Total Curr,nt E.penditure b,77 878 678 952 1038 1605 1974 10.2 10.1 9.7 10 1 9 - 10.1 II 2

C Current. 8Balec. 97 134 107 33 146 147 170 1.1 1.8 1.2 0.3 1 3 0. 1 o

0. C.P,tal R-on..uea 9 16 10 6 5 64 90 0.1 0.2 0.1 0.1 00 0 4 0 SE Capital E.penditurne 724 546 413 380 301 314 467 6 4 6.3 4.6 3.8 2 7 2 0 92 8

1 Fi..d Capital Forestion 682 810 366 306 259 297 428 7.9 8.9 4.3 3.2 2 3 1 2 42 Other Cap,tal Expenditures 42 38 26 54 42 17 89 0.5 0.4 0.3 0.6 0.4 0 1 0 3

C O,erall Bele-co -618 -396 .297 -322 -150 -103 -227 -7.2 -A.5 -3.3 -3.4 -1.3 -O 6 -1 31 off,cial Capital Grentt 1 1I 1 2 1 0 198 0.0 0.0 0.0 0.0 0 0 0 0 1 12. Net Fore.gn F..Pnc.ng 109 108 124 21 26 68 68 1.3 1.2 1.4 0 2 0 2 0 4 0 43 Net Donent.c F.na-nq. 808 283 172 299 123 35 64 5.9 3.3 1.9 3.1' 1 1 0 2 0 44 Other 0 0 0 0 0 0 -101 0.0 0.0 0.0 0 0 0 0 0 0 -06

This document has a testricted distribution and may be 'ised by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bar.k authorization.

Page 2 of 2COUNJTRY DATA - IRJATEOIALA

MONEY, CREDIT AND PRICES

(Million Q-atualas) 1980 1Q81 1982 1983 1984 1985 1986 1987

floe3 aid Quasi Money 1.692 1.907 2,191 2 155 2,399 3,193 3,875 4,166CIa; as on Governmenet (Net) as9 780 1.081 1i2n 1,54) ',703 1.244 981Claias on Private Sector 1,222 1,388 1,518 1,710 1,907 2,078 2,281 2.751Claima on Other Financial 29 72 21 44 38 24 18 37

Money and Quasi Money as I of 001' 21.5 22.2 25.1 23.8 25.8 28.8 24 5 23 7Co.u..e, Price Inden (1980n100) 100.0 111.4 111.8 118.8 120.8 143.4 198 4 220.9

Annus' percentage changes in:C.onsume Price 1nden 10.71 11.41 0 41 4.61 3.41 18 71 37.01 12.51Claims on Govermeant (Net) 240.01 124 51 39.81 15 21 28.81 9 91 -27 01 -21.11Clie;s on Private Sector 95.31 147.41 -70.91 113.01 414.21 -23 71 -45.51 138.71

8ALAPCE OP PAYNDITS

(USS M;illone) 1980 fl81 1982 1Q33 1984 1985 1988 1Q87 MERCrIANDISE EX(PORTS

- ----- ------ ------ ------ -- --- ---- - -- --- ---- --- -- - ---- (Average 1980-87) mi. USI (1)Eaports of Goode and NFS 1,748 1,471 1,288 1.178 1,231 1,182 1,161 1,138 ---------------- ---

Marchandica (FOB) 1,520 1,291 1,170 1,092 1.132 1.060 1,044 978 Coffee 393 0 33 9

Non-Factor Services 228 180 118 84 99 102 117 159 Cotton 78 2 6.8

Sugar 85 7 5.7Imports of Goode and NFS 1,983 2.031 1.829 1,317 1,435 1,282 1,053 1,599 Banana 74.2 8 4

Morchendica (FOB) 1,472 :5b40 1.284 1.058 1,182 1,077 878 1.333 Meat 18 5 1.4

Non-Factor Services 491 491 345 281 253 185 17Q 285 Other 533.2 48.1

Reaource Balance (215) (581) (341) (141) (204) (101) 108 (482) Total FOB 1,180.8 100 0Net Factor Income (711 (103) (121) (113) (1-03) (188) (199) (172)

Factor Rec,.ipts 77 55 24 29 so so 33 31Factor Paysents 147 158 145 143 262 215 232 203 EXTERNAL DEBT (end period)(MLT interest paymen.ts) 80 83 77 89 95 114 208 178 (U.14Milos 1980 1988 1987

Net Current Transfers 110 91 83 31 29 20 51 70---------------- -- --- ..MALT Public & Pub. Guara. 551 2,151 2,084

Currant Account Balance (178) (573) (399) (224) (378) (287) (42) (584) Short Term Debt A IMF 335 323 508

Non-Guaran.teed Private Debt 282 119 118Long-Term Capital Inflos 244 407 350 298 147 101 184 2Q1------- ---

Direct Investmen.t a5 110 78 45 38 81 89 91 Total Outstanding & DisIurad 1,188 2.593 2,6888Official Cepitsl Grants 0 0 0 0 0 0 48 128

Net LT Loans (OAS data) 92 280 279 214 85 29 5 (147)Disbursements 170 344 337 317 254 285 184 171 DEBT SERVICE RATIORepayments 78 65 59 103 170 235 17Q 318 (percent) 1980 1Q88 1987

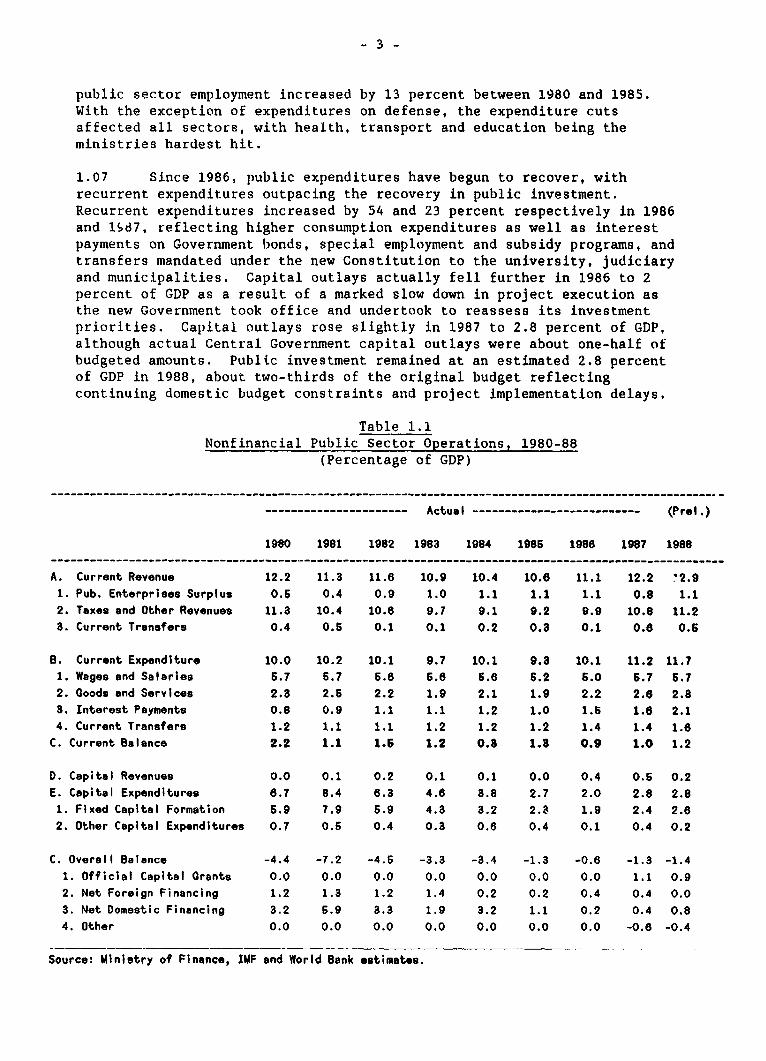

Other LT infloos (Net) 58 17 (7) 34 24 11 82 221---------------- -- --- --

MALT Public A Pub. Cuaro. 2.5 31.4 41.5Total Oth,er Iteas (Net) (387) (182) 22 (40) 249 71 (142) 233 Short Term Debt A IMP 1 7 8.8 2 8

Non-Guarantaad Private Debt 8 1 1.0 0 9

Changes in Net Resarva.(nn 319 348 28 (29) (18) 95 0 40 Total Outstanding A Diobureed 9.2 3Q 2 45.1Net cre.dit fron IMF 0 113 0 41 20 (49) (58) (20)

EXCHIANGE RATES 19630 1981 1982 1983 1984 1985 1988 1987 IBRD LENDOING (nl. USUI 1Q84 1985 1988 1987

Of.vical Rats: Commitments 50 0 44 8 0.0 0.0

Byett. par UISS (and period) 1 000 1.000 1.000 1.000 1.000 1.000 1.000 1 000Bust:, per USII (peri,d mug I 000 1 000 1.000 1.000 1.000 1 000 1.000 1.000 Gross Diebures-ent 7.9 48 6 17 0 11.7

Principal Repayment 13 8 14 2 17 0 22 0Banbing Rate: Net Disbureenant (5.7) 34 4 0.0 (10.3)Bust: par US15 (end period) - - - - - - 2.500 2 500 Interest Charges 12 4 It 4 21 0 23 0Bust:, Par US; (per,od sav) -- - - - - - 2 500 2.500 Net Transfers (18 1) 23 0 (21 0) (33 3)

Marbet Rats: Debt Outstanding A D'sb 188 8 '221 2 278 7 330 0Bust:. per USS (and period) - - - - - 2.850 2 570 2 510 Debt Outstanding A Ucd, 284 0 299 0 282 4 282 4Bust:. per liSt (Period avg) -- - - - - 2.850 2 700

GUATEMALA

PUBLIC SECTOR EXPENDITURE REVIEW

TABLE OF CONTENTS

EXECUTIVE SUMMARY

CHAPTER I: PUBLIC SECTOR EXPENDITURES AND RESOURCEMOBILIZATION ............................................. 1

A. Public Expenditure Fram,iework and Recent Trends ........ 2

Trends in Government Expenditure ..... ......... ....... 2Public Sector Revenues ............. ................... 4

B. Future Expenditure Options and Financing Requirements. 6

Level of Public Expenditures (1988-1991) .............. 7Composition of Public Expenditures (1988-1991) ........ 8Improving the Allocation of Public Expenditures in

the 1990s ........... ............................... 11Financing Requirements and Sources ..................... 13Public Savings, Investment and Growth (A Macro-economic

Scenario) ............................. 16Growth, Domestic Savings, and External Debt ........... 19Private Funding for Development ...... . ................ 20Concl' ions and Principal Recommendations .............. 20

CHAPTER II: AGRICULTURE SECTOR . ............................. 22

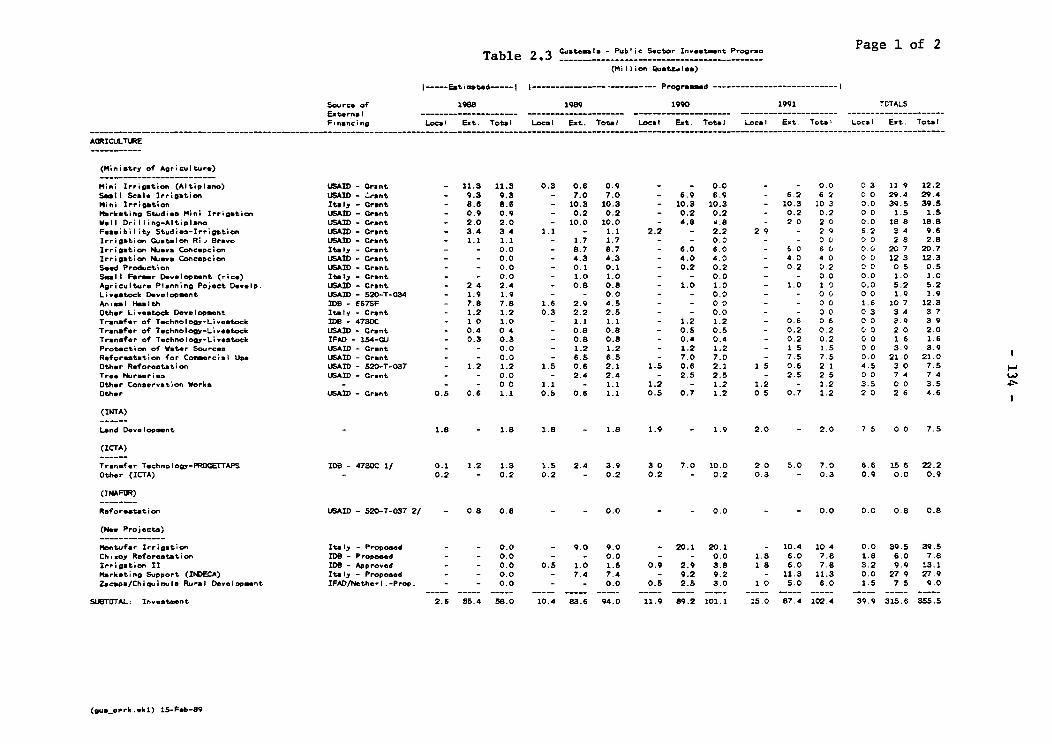

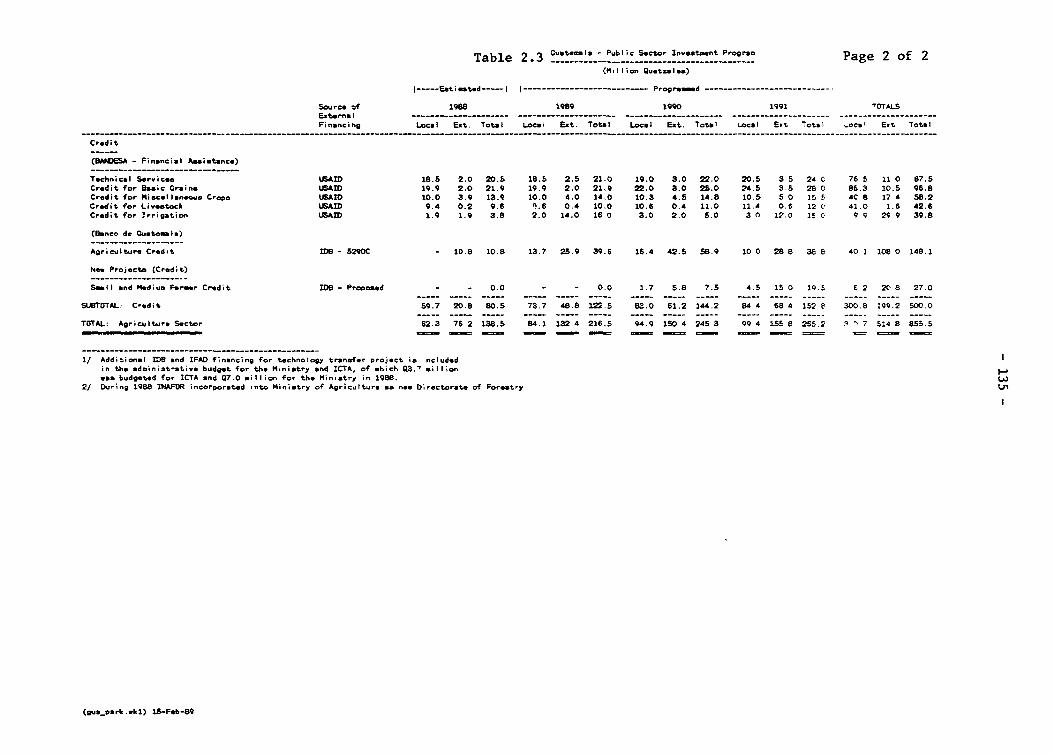

Sectoral Organization ....... .......................... 22Principal Sector Issues and Development Priorities .... 23Public Expenditures in Agriculture ..... ............... 25Planned Investment Program in Agriculture (1988-1991).. 26Ongoing Investment Projects ...... ..................... 26New Investment Projects in Agriculture .... ............ 27Agriculture Credit ..................................... 28Conclusions and Principal Recommendations ............. 29

This report is based on the findings of an economic mission that visitedGuatemala in April/May 1988. The mission was composed of George Park(Mission Chief), Tarsicio Castaneda (Health Sector), Chris Hennin (Non-Governmental Organizations), Pablo Jordan (Consultant, Housing andMunicipal Development), Jose Marques (Macroeconomic Framework), Abel Mateus(Agriculture Sector), Thomas McCarthy (Consultant, Agriculture Sector),Cesar Vallejo (Consultant, Planning and Project Execution), and AndrewVandendriessche (Public Expenditure Programming). In addition, RicardoKlockner and Luis Luzuriaga helped prepare the chapter on power, RicardoKlockner and Adan Cajina (consultant) the chapter on water supply, andShanta Pai the chapter on telecommunications. The report has been revisedand updated following discussions with the Government in December 1988 andJanuary 1989, including a revision of the public sector investment programto incorporate preliminary estimates on expenditures in 1988 to the extentdata was available.

- 2 -

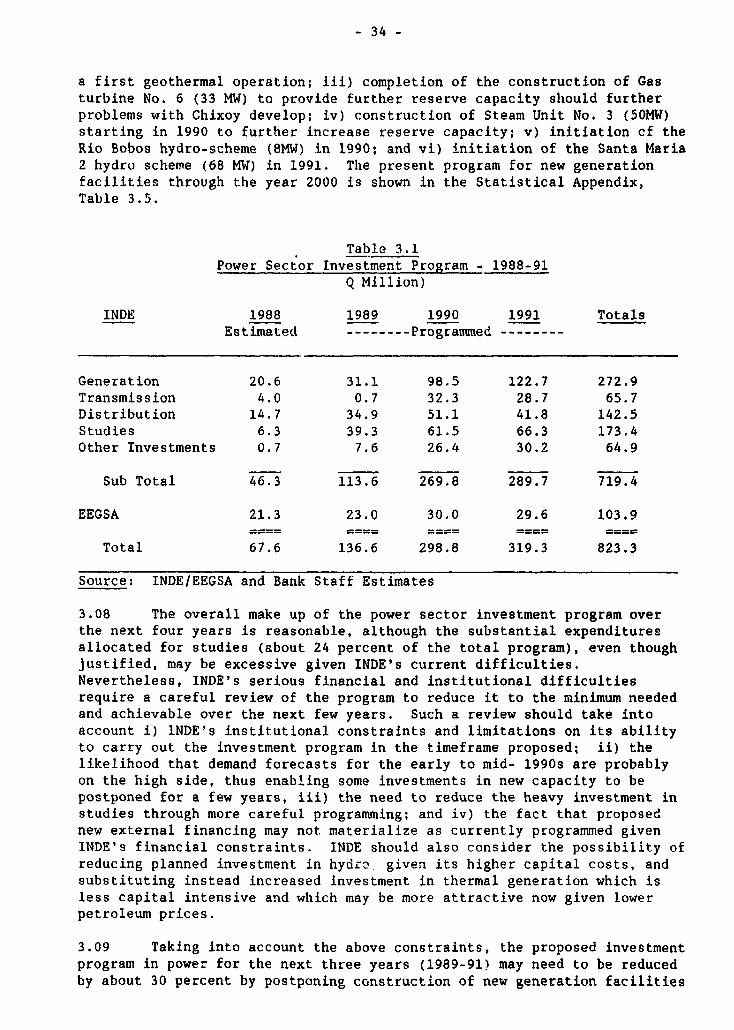

CHAPTER III: POWER SECTOR ............. ..................... 32

Key Sector Issues .. 32Sector Investment Program, 1988-1991 .. 33Financing Needs . .35

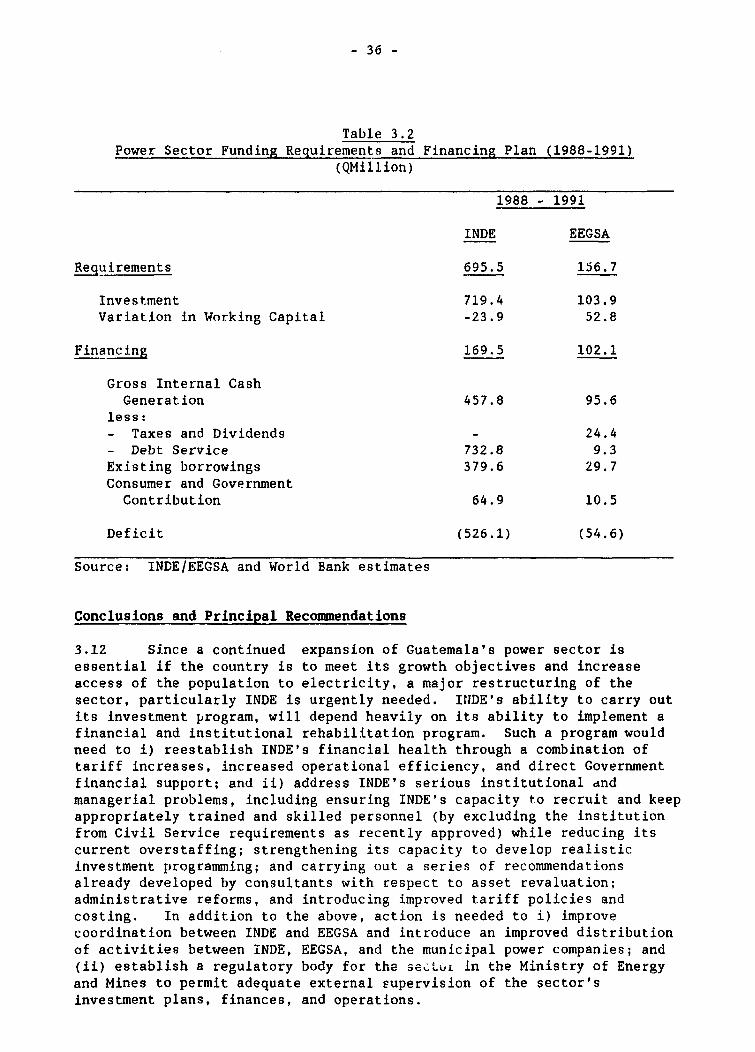

Conclusions and Principal Recommendations ............. 36

CHAPTER IV: THE TRANSPORT SECTOR .... 38

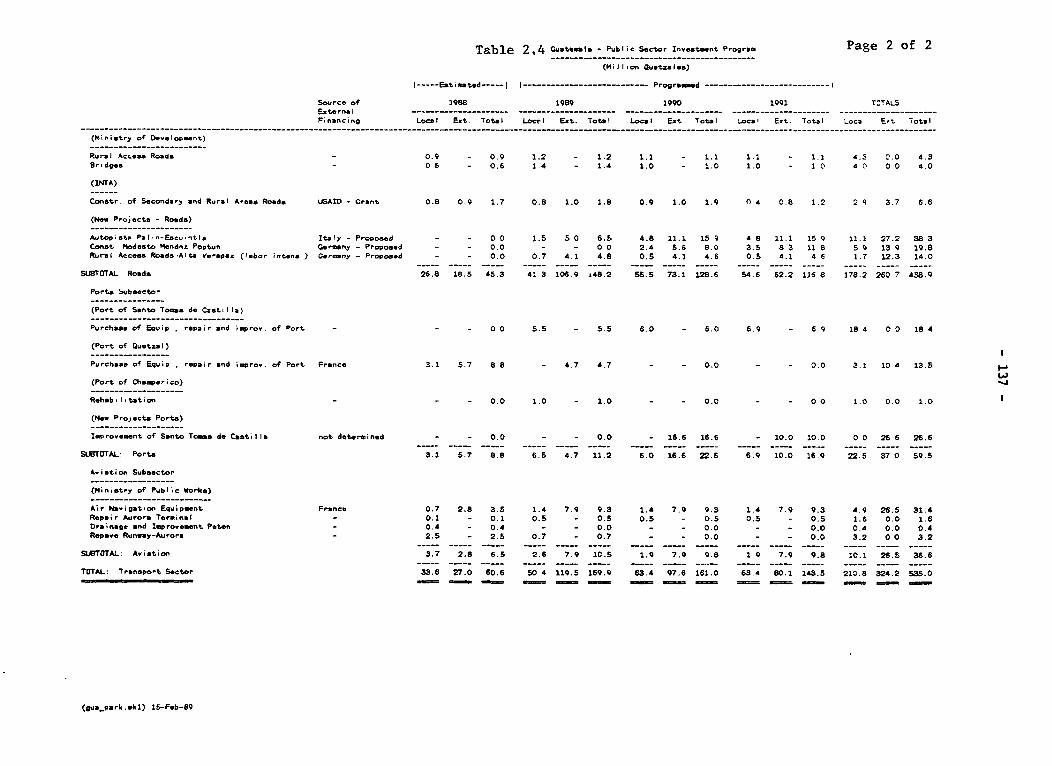

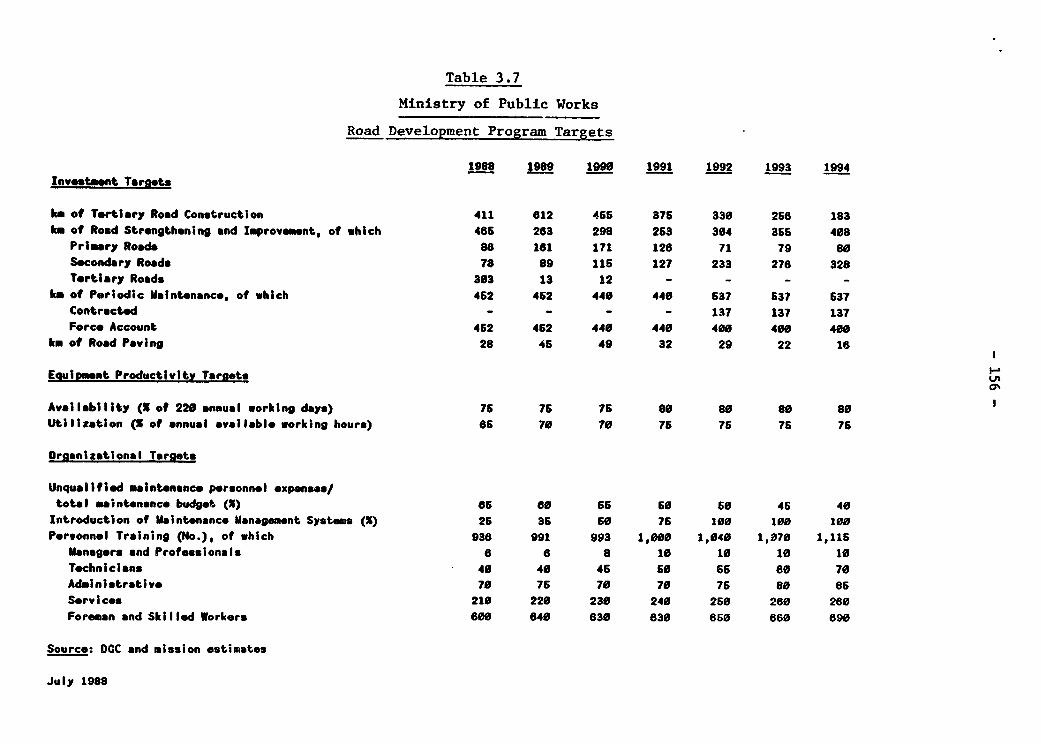

Institutional Framework .. 38Planned Investment in Transportation . .39Roads Subsector .. 40Ports Subsector .. 42Railway Subsector .. 42Aviation Subsector .. 43Conclusions and Principal Recommendations 43

CHAPTER V: TELECOHMUNICATIONS SECTOR .. 44

Institutional Framework. 44Current Service Levels and Sector Development

Objectives .. 44Sector Constraints .. 45Sector Financing .............. ........................ 46Investment Program (19&S-91) and Financing Plar. 47Conclusions and Principal Recommendations 50

CHAPTER VI: WATER SUPPLY SECTOR ... 31

Key Sector Issues ................. 52Programmed Investments (1988-1991) .. 53Conclusions and Principal Recommendations 56

CHAPTER VII. THE SOCIAL SECTORS (Health and Education) .59

A. Health Sector Needs, Investment Program, andFinancing ............................................ 60

Key Sector Issues and Expenditure Priorities 61Government's Program .. 63Proposed Investment Program, 1988-91 .. 63

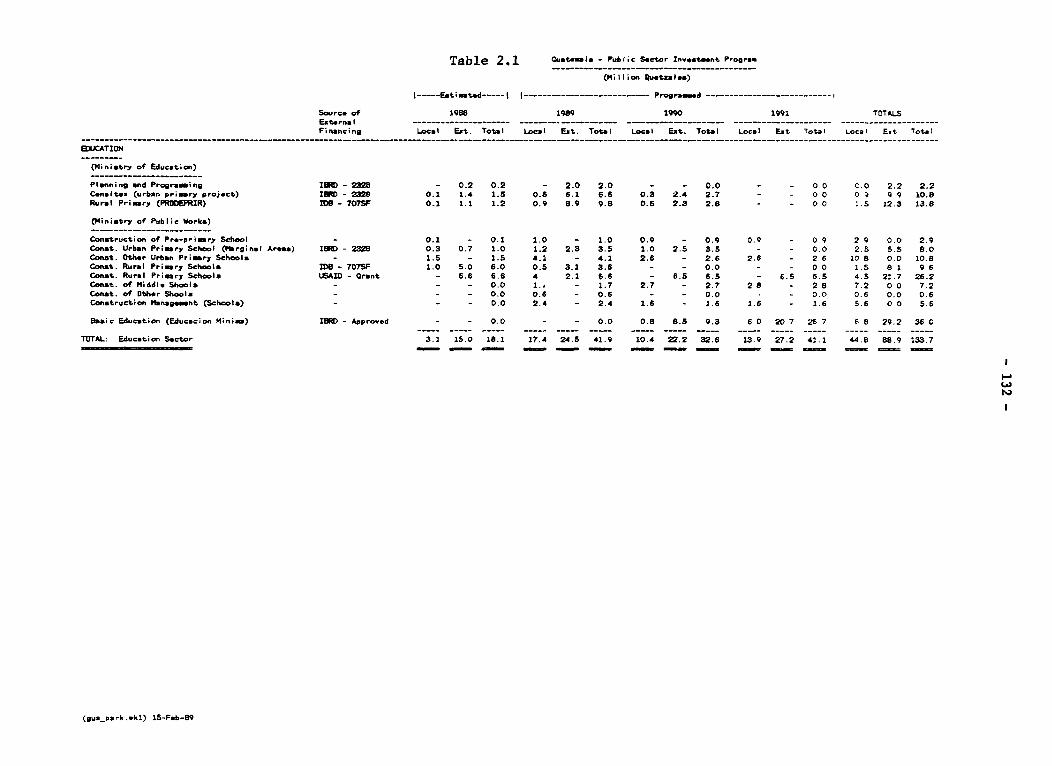

B. Education Sector Needs, Investment Program andFinancing ........................................... 66

Key Sector Issues ............ .... 67Government's Program .. 68Proposed Investment/Expenditure Program .. 70

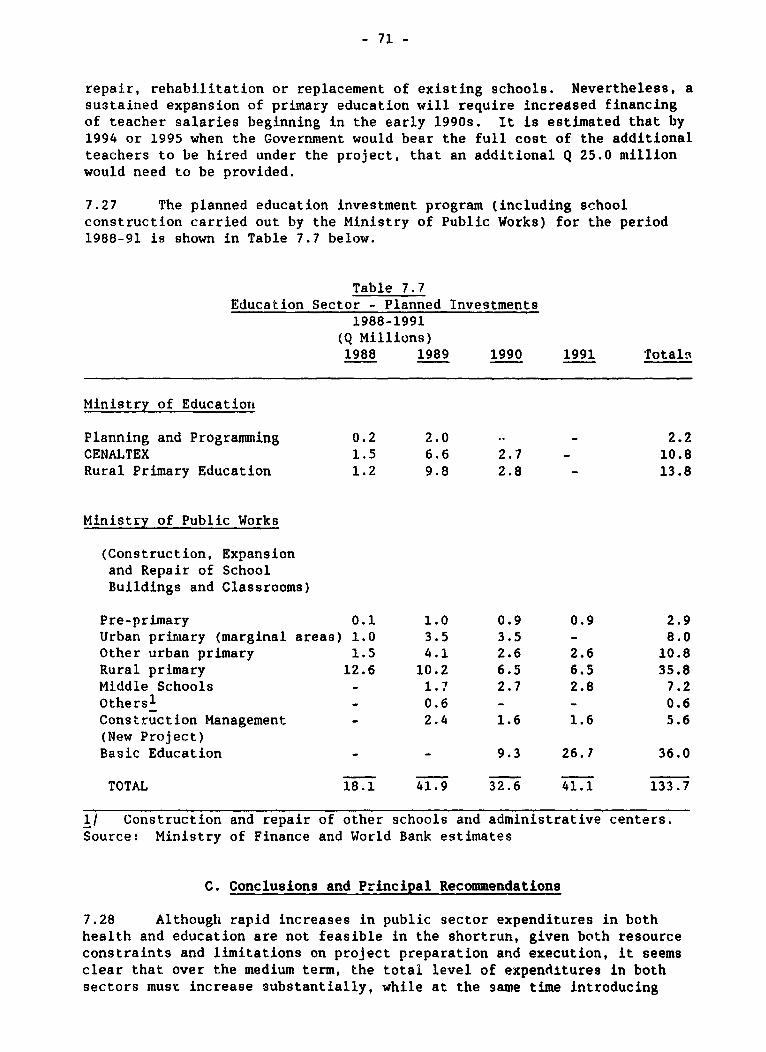

C. Conclusions and Principal Recommendations 71

- 3 -

CHAPTER VIII: HOUSING AND URBAN DEVELOPMENT .... ............. 74

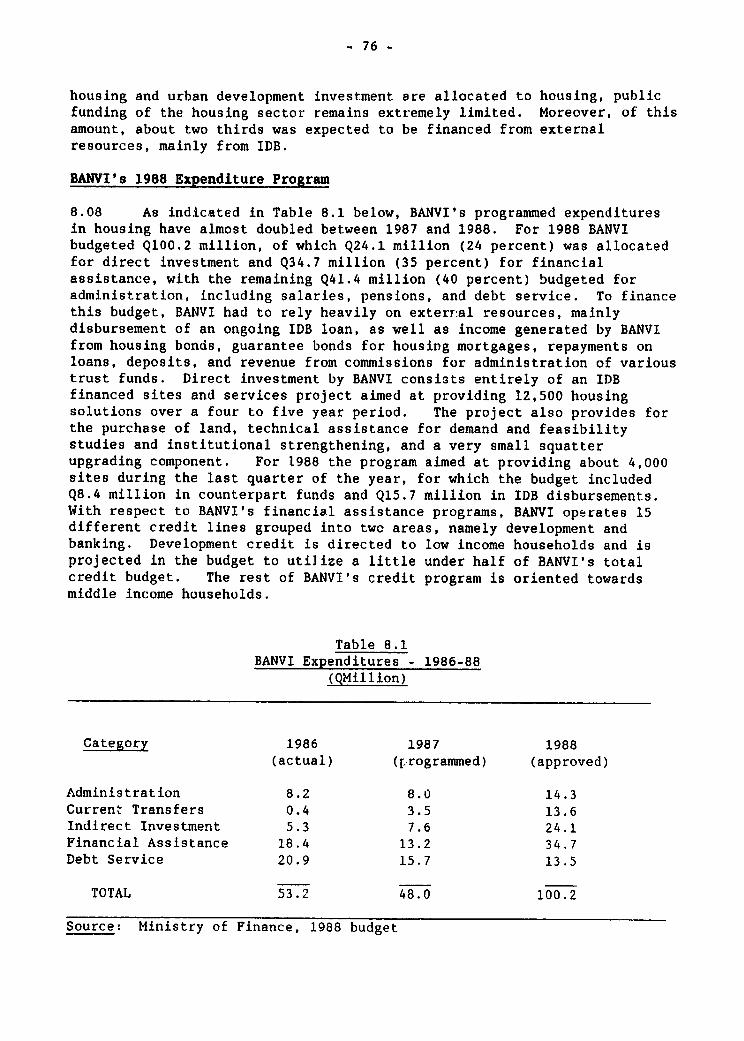

A. Housing Sector Needs, Investment Program andFinancing ........... ................................ ,4

Institutional F.7amework and Key Sector Issues ......... 74Public Expenditures in Housing and Urban Development .. 75lHousing Sector Needs and Revised Policy Framework ..... 77

B. Urban Development ..................................... 77

Sector Organization .................................... 7eMunicipal Finance Issues .............................. 78INFOM's Investment and Expenditure Program ............ 78Municipal Investments in Guatemala City .... ........... 81Combined Investment Program for Housing and UrbanDevelopment ......................................... 81

C. Conclusions and Principal Recommendations ............. 82

CHAPTER IX: STRENGTHENING PLANNING, PROJECT PREPARATION,AND PROJECT EXECUTION ..................... 85

Planning and Programming of Investments .... ........... 85Project Preparation ................................... 87Project Execution ..................................... 88

CHAPTER X. OVERA1,L CONCLUSIONS AND RECOMMENDATIONS ........ 92

ANNEX I: The Tax Regime ...................................... 100

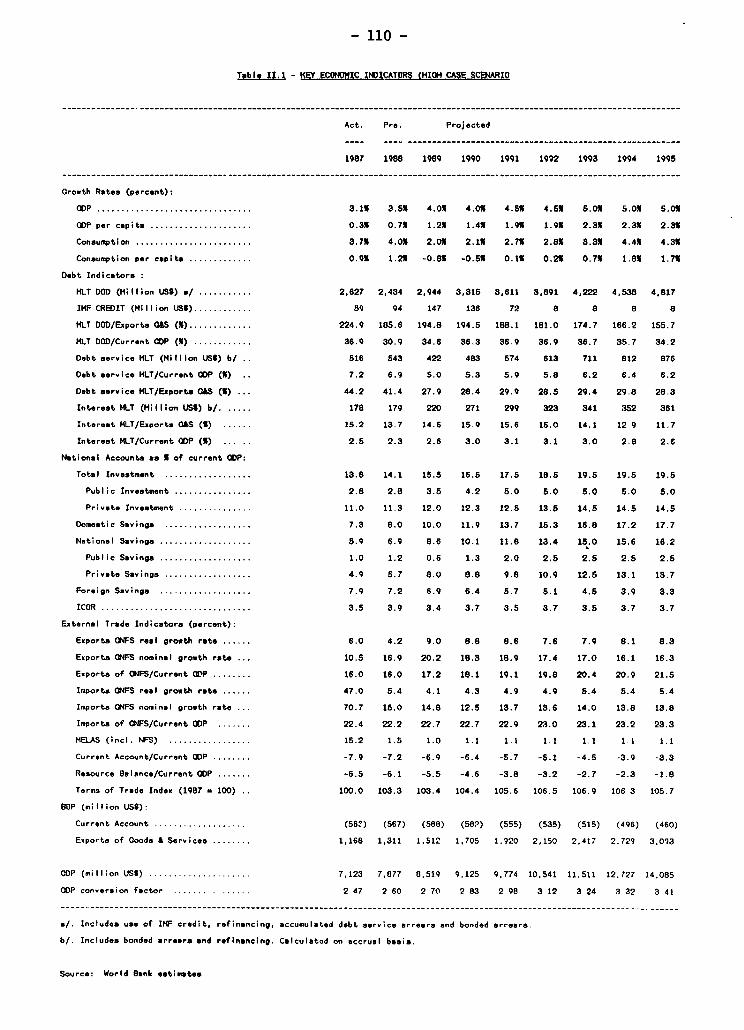

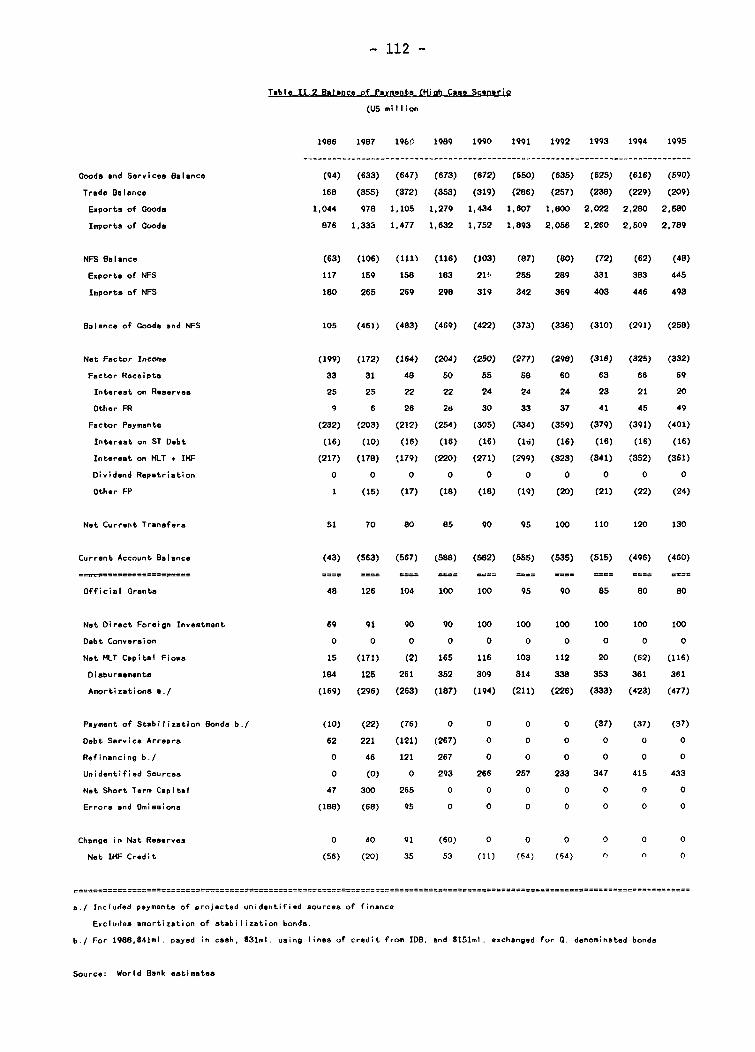

ANNEX II: Macroeconomic Projections .......................... 109

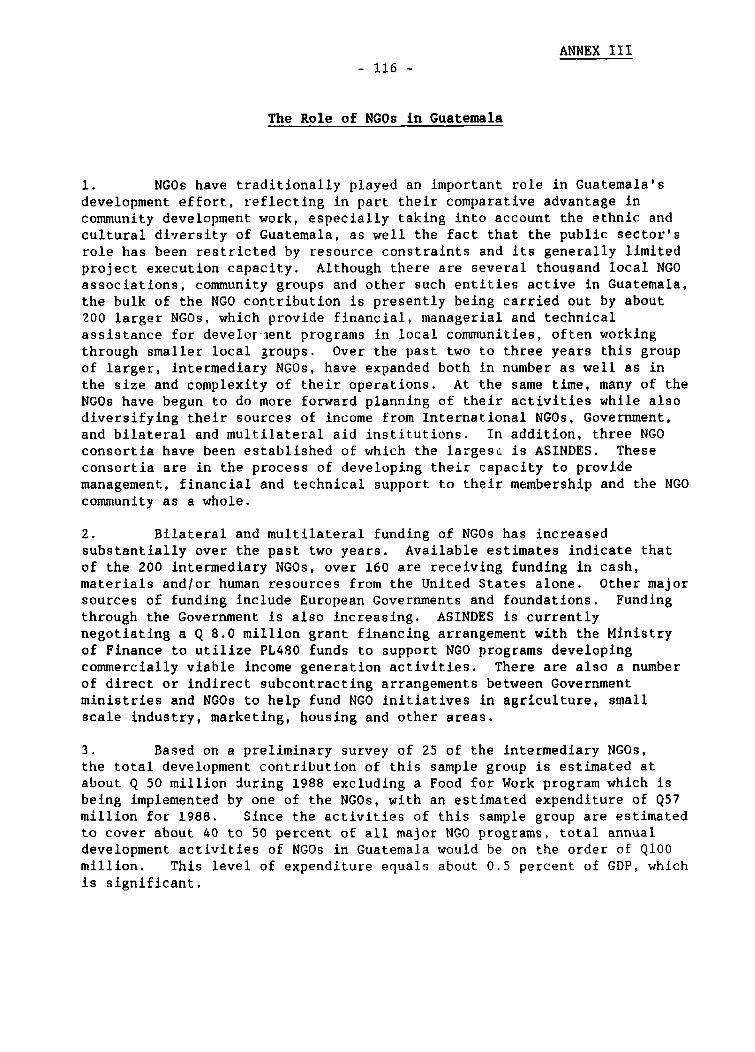

ANNEX III: The Role of NGOs in Guatemala ..................... 116

STATISTIC-AL APPENDIX .................... 318

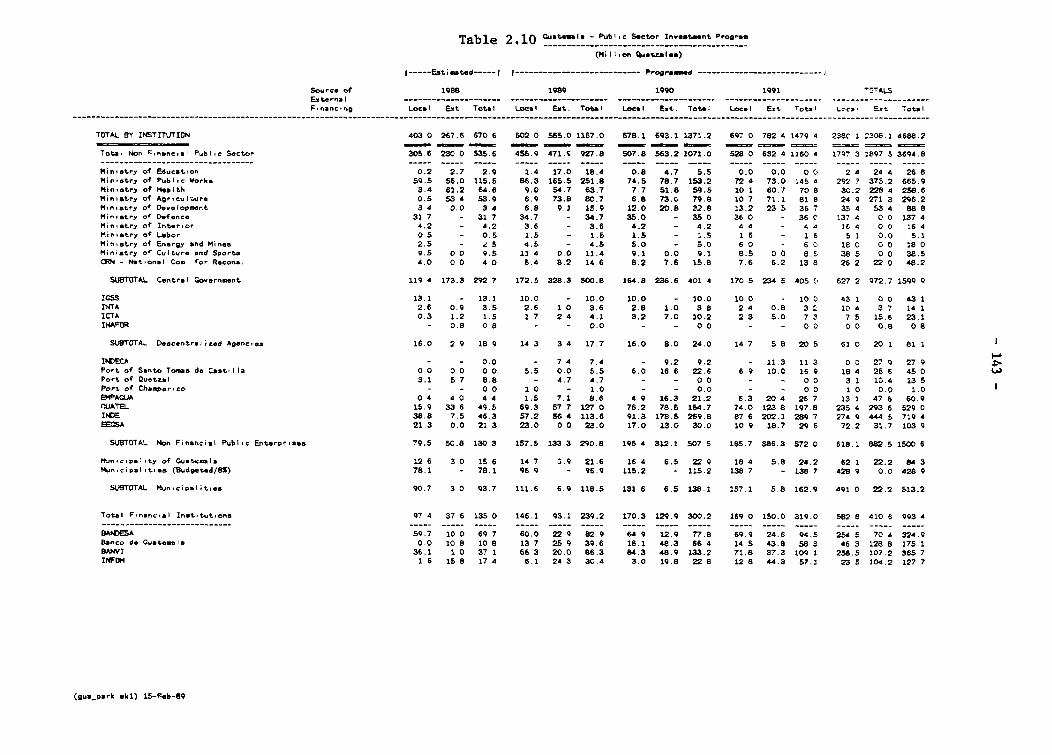

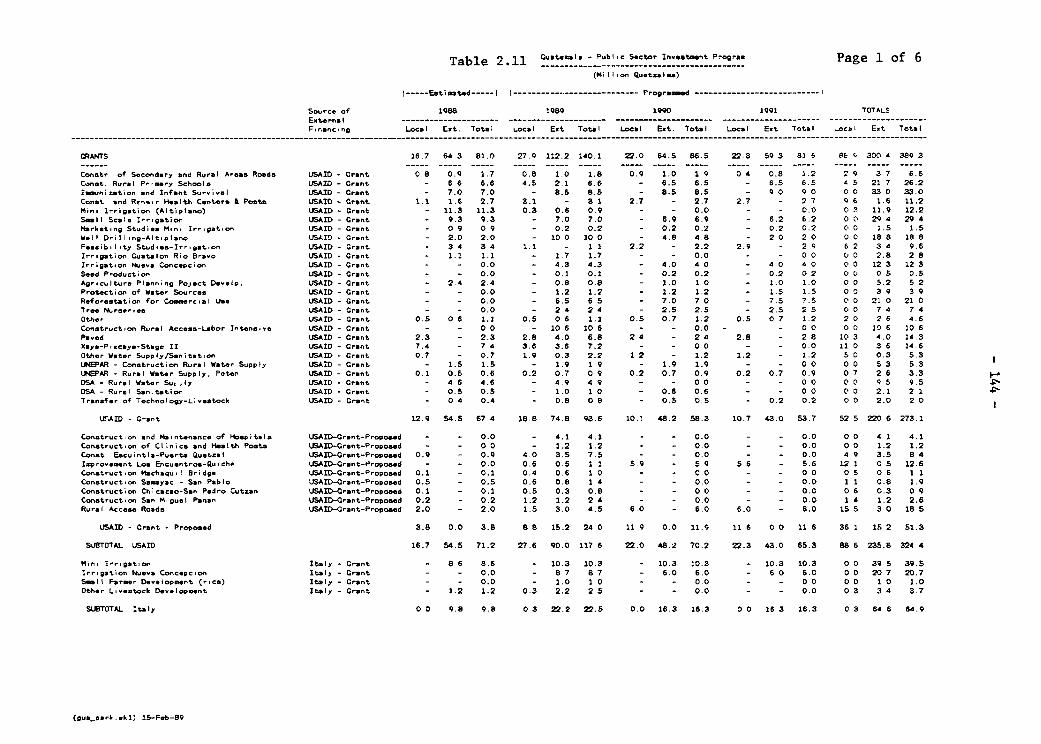

Section I: Standard Tables ................................. 119Section II: Public Sector Investment Program ............... 132Section III: Other Sector Tables ........................... 150

EXECUTIVE SUMMARY

Introduction

i. Guatemala confronts major social, political and economicchallenges as it strives to consolidate its newly established democraticframework; improve the well being of some 60 to 70 percent of thepopulation living in poverty; and reestablish a sound macroeconomicframework for sustained economic growth. These challenges are compoundedby the limited and uneven provision of basic social services, rapidpopulation growth, and the country's fragmented social structure. Almosthalf of Guatemala's 8.4 million people are indigenous descendants of theMaya civilization, with only limited assimilation into the socio-economicmainstream.

ii. Following many years of military rule, a democratically electedcivilian Government took office in early 1986. This Government hasundertaken the difficult task of stabilizing the economy and developing themedium term policies required to restore sustained economic growth, tacklethe country's major social issues, and strengthen the fledgling democraticsystem. At the heart of the Government's challenge is the need to mobilizeand utilize public resources more efficiently, while at the same timeensuring a macro-economic framework conducive to private sector investmentand renewed growth. This report is part of an ongoing World Bank effort tosupport the Government's efforts to reorganize and strengthen management ofthe public sector. It analyzes the overall allocation and use of publicsector resources, the content and focus of the public sector investmentprogram, and projected financing requirements through 1991.

Macroeconomic Background

iii. After several decades of substantial growth averaging close to 6percent of GDP during the 1960s and 1970s, Guatemala's economic performancedeclined sharply in the early 1980s as the country's external terms oftrade deteriorated, internal political difficulties mounted, andmacroeconomic adjustment efforts were untimely or insufficient. Theuncertain political and economic climate in Guatemala and the rest ofCentral America exacerbated capital flight, and sharply reduced privatedomestic and foreign investment, as well as external financing. By themiddle of the 198Cs Guatemala faced serious economic and financialproblems: foreign trade was virtually at a standstill owing in large partto an unmanageable multiple exchange rate regime; inflation was runningover 30 percent; investment and national savings were nearly half the levelof the 1970s; arrears on external payments had reached about $600 miliion;

- ii -

and GDP was 6 percent below its 1980 level. The sharp decline in GDP andmuch lower fiscal revenues also prompted a rapid increase in externalborrowing, with medium and long term debt more than tripling to US$2.5billion by 1987.

iv. Upoin taking office in early 1986, Guatemala's democraticallyelected Government moved quickly to stabilize the economy, taking measuresto impr3ve exchange rate management, reduce the fiscal deficit and increaseinterest rates. These measures, combined with favorable coffee prices,resulted in a substantial improvement in economic performance, with GDPgrowing by 3 percent in 1987, the first real growth in several years.Faced with renewed balance of payment pressures in late 1987 and 1988, theGovernment took additional stabilization measures in 1987 and mid-1988.Despite its success in stabilizing the economy, however, the Government'sefforts to improve resource mobilization and accelerate public sectorinvestment have been less successful.

Public Expenditure Trends and Key Issues

v. Faced with a major decline in tax revenues in the first half ofthe 1980s, the Government drastically cut public investment and constrainedother public expenditures, especially in the social sectors. Total publicexpenditures fell from 16 percent of GDP in 1980 to 12 percent in 1985,while capital outlays were cut by more than half, falling from over 6percent to 2.7 percent during the same period. Since 1986, publicexpenditures have begun to recover, with recurrent expenditures growingfaster than public investment, owing mainly to efforts to make up forprevious declines in real wages. At the same time, as a result ofcontinued problems in project management and budget constraints, capitaloutlays fell further to only 2 percent of GDP in 1986. Public investmentincreased moderately to 2.8 percent of GDP in 1987 and preliminaryestimates indicate the same level for 1988. Total public expenditures in1988 reached about 14.5 percent of GDP, still below the 1980 level.

vi. These trends highlight three underlying expenditure issues.First, Guatemala's overall level of public expenditures is low, especiallywhen compared with the range of unmet needs of its population. In fact,Central Government expenditures are only about one-half of the level inother countries with a similar level of per capita income. Second,the share of current expenditures, particularly wages, appears to be highin comparison with the relatively limited coverage of basic services andthe small size of the public sector investment effort. This reflects bothlow public sector productivity as well as overstaffing, especially in anumber of public enterprises. Third, the level of public sector investmentactually executed remains very low, again in comparison with the country'spriorities for expanding basic services and ensuring an adequate and wellmaintained infrastructure to support growth objectives and the exportdrive.

- iii -

Resource Mcbilization Issues and Basic Expenditure Options

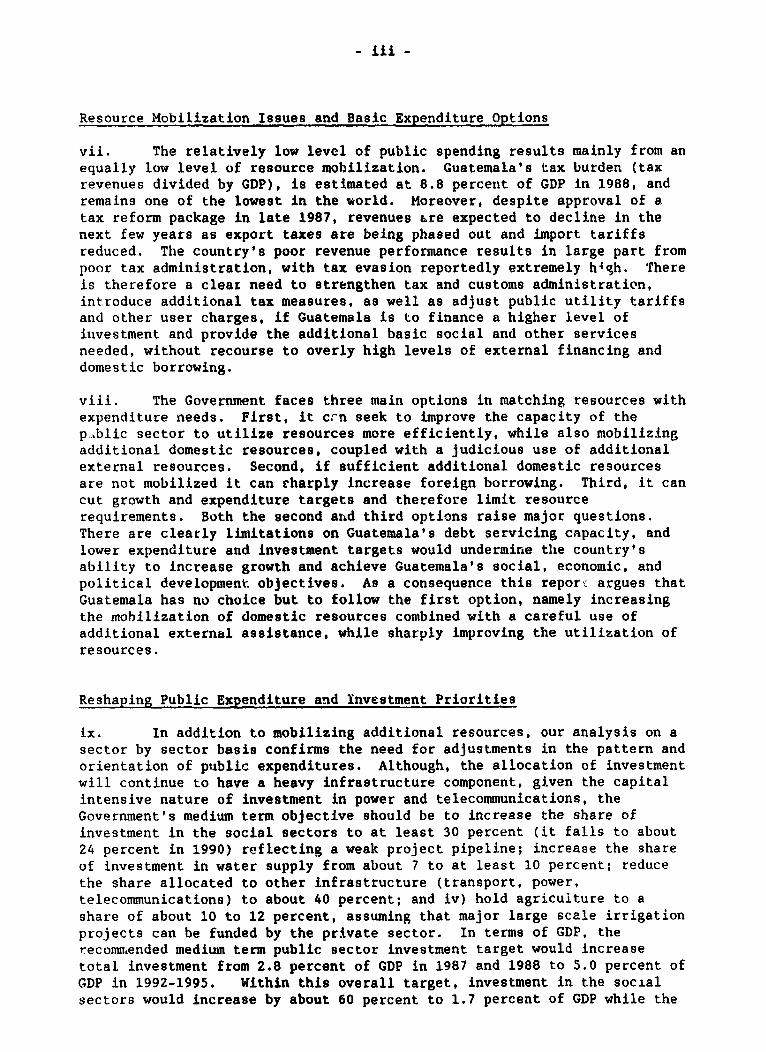

vii. The relatively low level of public spending results mainly from anequally low level of resource mobilization. Guatemala's tax burden (taxrevenues divided by GDP), is estimated at 8.8 percent of GDP in 1988, andremains one of the lowest in the world. Moreover, despite approval of atax reform package in late 1987, revenues are expected to decline in thenext few years as export taxes are being phased out and import tariffsreduced. The country's poor revenue performance results in large part frompoor tax administration, with tax evasion reportedly extremely high. Thereis therefore a clear need to strengthen tax and customs administration,introduce additional tax measures, as well as adjust public utility tariffsand other user charges, if Guatemala is to finance a higher level ofinvestment and provide the additional basic social and other servicesneeded, without recourse to overly high levels of external financing anddomestic borrowing.

viii. The Government faces three main options in matching resources withexpenditure needs. First, it cmn seek to improve the capacity of thep..blic sector to utilize resources more efficiently, while also mobilizingadditional domestic resources, coupled with a judicious use of additionalexternal resources. Second, if sufficient additional domestic resourcesare not mobilized it can sharply increase foreign borrowing. Third, it cancut growth and expenditure targets and therefore limit resourcerequirements. Both the second and third options raise major questions.There are clearly limitations on Guatemala's debt servicing capacity, andlower expenditure and investment targets would undermine the country'sability to increase growth and achieve Guatemala's social, economic, andpolitical development objectives. As a consequence this repor:. argues thatGuatemala has no choice but to follow the first option, namely increasingthe mobilization of domestic resources combined with a careful use ofadditional external assistance, while sharply improving the utilization ofresources.

Reshaping Public Expenditure and Investment Priorities

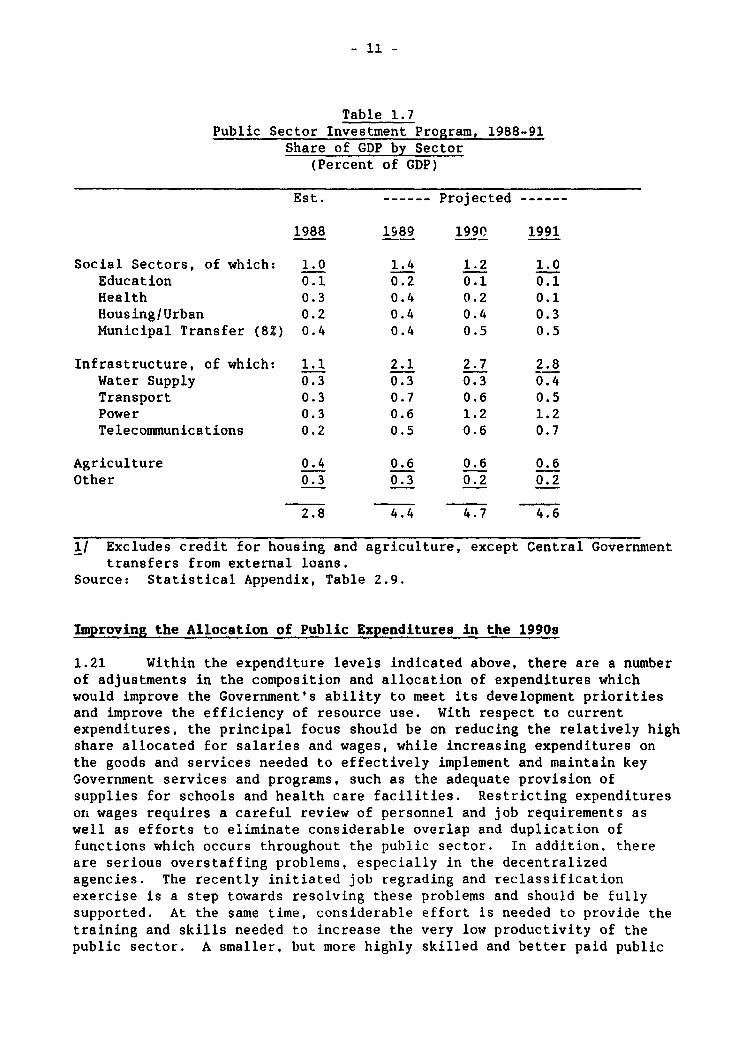

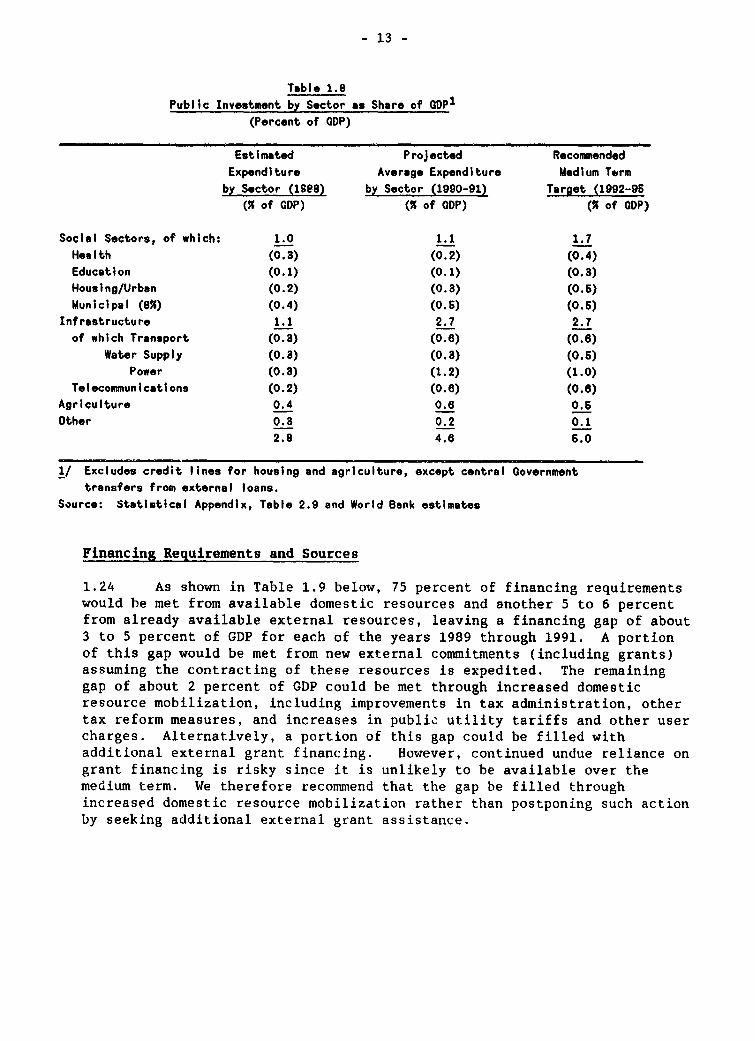

ix. In addition to mobilizing additional resources, our analysis on asector by sector basis confirms the need for adjustments in the pattern andorientation of public expenditures. Although, the allocation of investmentwill continue to have a heavy infrastructure component, given the capitalintensive nature of investment in power and telecommunications, theGovernment's medium term objective should be to increase the share ofinvestment in the social sectors to at least 30 percent (it falls to about24 percent in 1990) reflecting a weak project pipeline; increase the shareof investment in water supply from about 7 to at least 10 percent; reducethe share allocated to other infrastructure (transport, power,telecommunications) to about 40 percent; and iv) hold agriculture to ashare of about 10 to 12 percent, assuming that major large scale irrigationprojects can be funded by the private sector. In terms of GDP, thereconmiended medium term public sector investment target would increasetotal investment from 2.8 percent of GDP in 1987 and 1988 to 5.0 percent ofGDP in 1992-1995. Within this overall target, investment in the socialsectors would increase by about 60 percent to 1.7 percent of GDP while the

- iv -

share allocated to infrastructure would remain at 2.7 percent of GDP, aboutthe same level estimated for 1990 and 1991. Nevertheless, the compositionof investment in infrastructure should be shifted to permit increasedinvestment in water supply (from 0.? lo between 0.5 and 0.6 percent ofGDP), while investment in power and telecommunications is reduced slightlyfrom 1.8 to 1.6 percent of GDP. The share allocated to agriculture woulddecrease slightly from the 0.6 percent of GDP estimated for 1990 to 0.5percent, but remain higher than the 0.4 percent estimated for 1988. Majorsector experditure issues are highlighted below.

Agriculture Sector

x. Agriculture remains Guatemala's most important sector, accountingfor one-fourth of GDP and two-thirds of export income, while employing overone-half of the work force. Nevertheless, despite its importance andpotential as the principal source for renewed growth and export income,Central Government expenditures on agriculture have fallen substantially inrecent years from about 1 percent GDP in 1980 to about 0.3 percent in 1985.Although the share of expenditures has increased since then to an estimated0.7 percent of GDP in 1988, the amount of funding for the sector remainsinadequate. Indeed public expenditures per person employed in agriculturehave been substantially lower than other countries in Latin America--forexample, about one-half of what Bolivia, Costa Rica and Peru spent in 1980.

x. Nevertheless, although public spending on agriculture may need tobe increased over the medium-term, the first priority should be to improvethe utilization and allocation of already available resources, including anaccelerated effort to resolve institutional bottlenecks. There are fourbasic areas where changes are recommended. First, expenditure prioritiesneed to be adjusted to increase the share of resources budgeted foragriculture extension, while better focusing agriculture investmentexpenditures on small farmer and poverty alleviation objectives and puttingincreased resources into natural resource protection, especiallyreforestation. With respect to future investment in agriculture, thiswould imply: i) expanding on-going programs in the Highlands aimed atdiversifying production of smallholders, including further emphasis onmini-irrigation; ii) expanding soil conservation efforts, includingsubstantially increasing investment and programs aimed at reforestation;and iii) reducing substantially plans for sharp increases in public sectorinvestment in larger scale irrigation projects which, given their high costper hectare and focus on commercial farming, could be financed in largepart by the private sector.

xii. The second major institutional and expenditure priority isstrengthening agriculture extension, which is critical for growth of smallfarmer income and productivity. This will require an indepth evaluation ofexisting extension efforts to identify principal constraints, coupled withthe identification of alternative approaches to providing enhancedtechnical assistance to small farmers, taking into account Guatemala'ssocial and geographical diversity. One possible approach would be to buildon the system of local agriculture representatives now being establishedthrough an expanded training effort, with the objective of maximizing theimpact of the Agriculture Ministry's small extension staff. Otherapproaches might consider the use of model farmers and the introduction of

supFporting audio-visual materials, complemented by private sector and NGOsponsored extension development efforts. Simply allocating more resourcesto extension without first developing an extension improvement programwould be counterproductive. However, once such a program is developedadditional resources woold likely be needed.

xiii. The third priority is improving access to agricultural credit,which requires both the modernization and reorganizat'.on of BANDESA (theagriculture bank), as well as consideration of other mechanisms forproviding credit to small farmers and ensuring sufficient capital forprivate investment in input supply, marketing and export ventures. On-going technical assistance efforts to strengthen BANDESA, with support fromUSAID and the Federal Republic of Germany should be expedited.

xix. A fourth area requiring attention is the Government's approach tofood security and the limited cost effectiveness and impact of ongoingprograms. An indepth review of existing programs and policies is needed,including an assessment of the effectiveness of INDECA's operations.Further investment in INDECA marketing facilities should be halted pendingthe outcome of such a study. In fact, if resources currently allocated toINDECA were invested in improved extension and rural infrastructure, theywould probably result in more food productioa and export crops, as well ashigher farmer incomes and lower prices for food, than if these resourcescontinue to be spent on INDECA's limited marketing efforts.

Infrastructure Sectors

xv. Investments in infrastructure account for about 55 percent oftotal public sector investment programmed for 1989 through 1991, with about21 percent on average programmed for power, 14 percent fortelecommunications, 14 percent for transport, and 7 percent for watersupply. As a percent of GDP about 1.6 on average is programmed for powerand telecommunications, 0.3 percent for water supply and 0.6 percent fortransport during the three year period. Although the share of investmentallocated to water supply appears on the low side, the o-erall content ofthe investment program in infrastructure is satisfactory and no majo.changes are recommended or feasible in the shortatwerm. Indeed, theprincipal challenge in the next few years will be to ensure that even thisrelatively low level of investment is achieved. This will require a majoreffort to address serious institutional and financial issues in the powersector, as well as a substantial improvement in implementation capacity inall of the other institutions involved in carrying out investments ininfrastructure. By the early 1990s, a major effort is needed to double theshare of GDP allocated to investments in water supply, while maintainingthe share allocated to transport, and reducing slightly the share of GDPallocated to power and telecommunications. Although additional heavyinvestment in the power sector in the middle 1990s may require anincreasing share of GDP, this should be accommodated by increasing theoverall level of public investment rather than penalizing investment in thesocial sectors.

- vi -

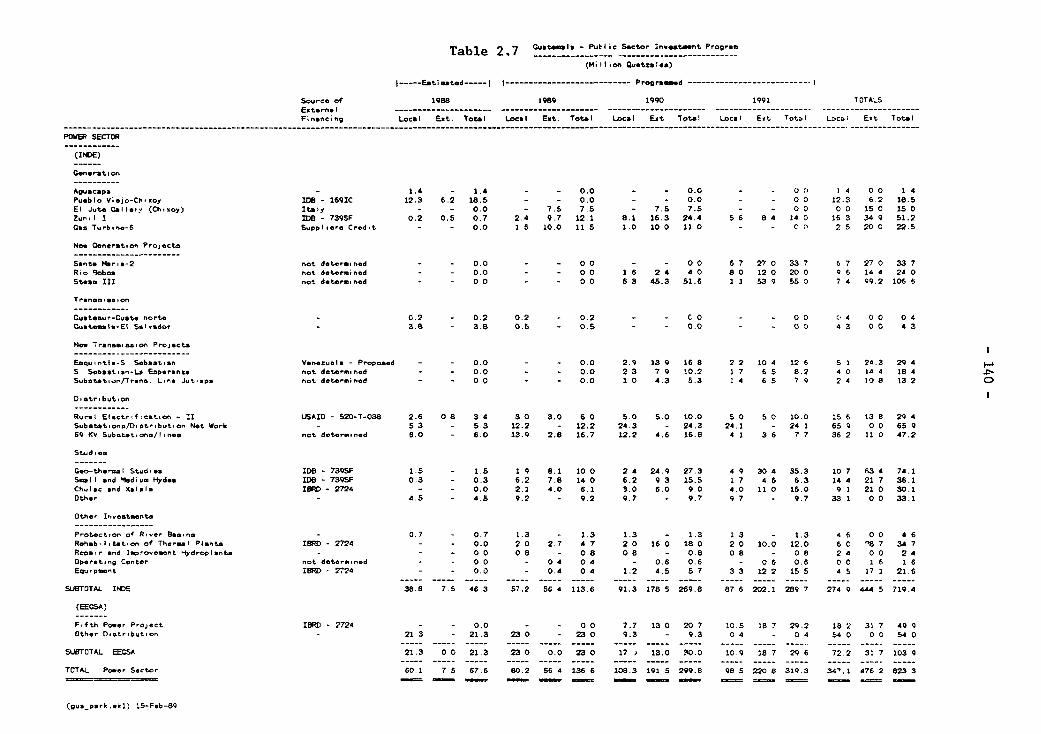

Power Sector

xvi. Maintaining an adequate level of investment in power, both toincrease the current low level of public access to electricity and ensuresufficient capacity in the sector to meet the country's growth objectives,will require a major financial and institutional restructuring of thesector. INDE (the power company) faces an extremely serious financialcrisis, wtth an expected deficit of QS00 to 600 million over the four yearperiod (1988-1991). As a consequence, INDE's ability to carry out itsinvestment program will depend on Government agreement to, and timelyimplementation of, a program tos i) reestablish INDE's financial healththrough a combination of tariff increases, increased operationalefficiency, and direct Government financial support; ii) improvecoordination between INDE and EEGSA (the principal distribution company),while also improving the distribution of activities between INDE, EEGSA,and the municipal power companies; iii) establish a regulatory body for thesector in the Ministry of Energy and Mines to permit adequate externalsupervision of the sector's investment plans, finances and operations; andiv) address INDE's serious institutional problems, including reducing itsserious overstaffing, strengthening its investment programming capacity,and carrying out existing recommendations regarding administrative reformsand asset revaluation.

xvii. INDE's problems should be addressed within the framework of adetailed adjustment program to be agreed between INDE and the Government.Such a program could take the form of a legal contract spelling out thespecific actions to be taken by INDE to strengthen its operations, while atthe same time indicating the level and nature of Government financial andpolicy support. The Government would also need to ensure that INDE wouldhave the autonomy in personnel matters needed to make the staffingadjustments required.

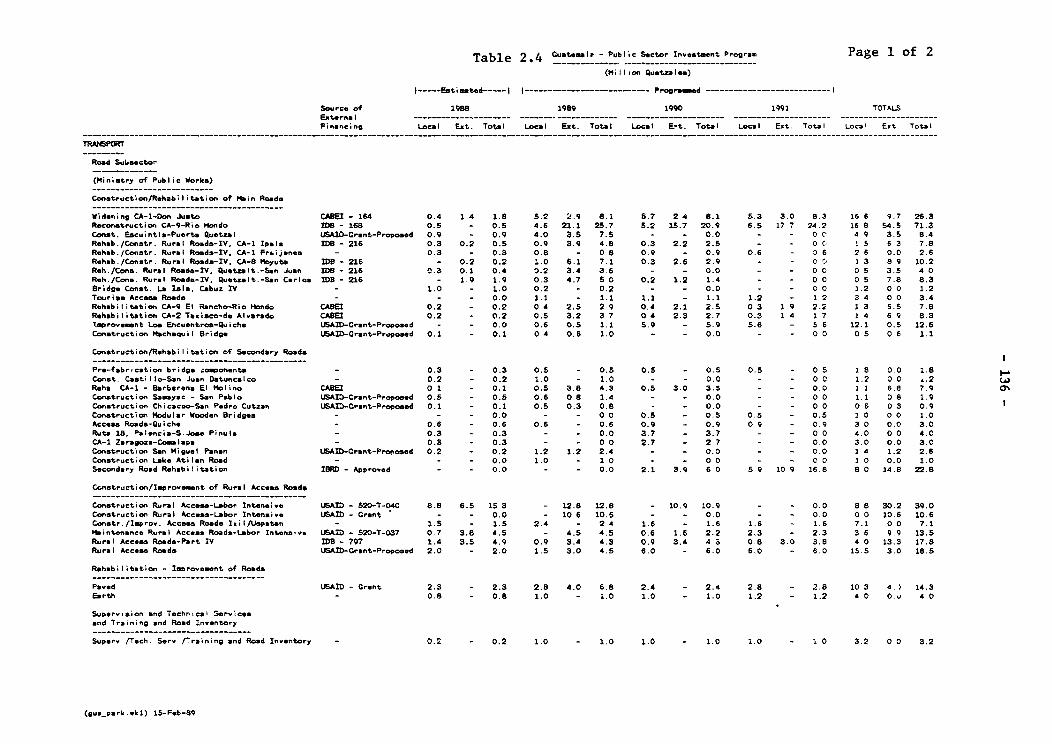

Transport Sector

xviii. The current focus of the Government's investment program intransport, with its emphasis on road rehabilitation and rural roadconstruction, is consistent with sector priorities. Nevertheless, theGovernment faces three basic expenditure issues which affect futureinvestment in the sector1, First, with respect to the road subsector, theprincipal challenge will be ensuring adequate financing for the program andaccelerating project execution by the Ministry of Public Works. Estimatedinvestment in the road subsector for the period 1988-91 already shows alower rate of execution than that proposed in the Ministry's medium term(1988-94) program. Road rehabilitation and maintenance must continue toreceive high priority given the deteriorated state of the road network andits importance in facilitating agriculture development and exports.Second, the Government needs to carefully review the feasibility of newinvestment in the railways which is tentatively planned over the mediumterm, given the questionable economic role of the railways in competitionwith road transport. No new investment in railways should be consideredpending completion of the National Transport Study. Third, with respect to

- vii -

ports, the Government should carefully assess the timing and magnitude ofproposed new investments in Puerto Santo Tomas de Castilla. Although thecountry's export development efforts clearly require an efficient portsystem, new investment ought to be accompanied by, if not preceded by, aprogram to improve the very low level of port productivity.

Telecommunications Sector

vx. Guatemala currently faces major bottlenecks in telecommunicationswhich seriously undermine public and private sector productivity. Thisresults from many years of limited investment given serious delays in theimplementation of major telecommunications projects. If the very ambitiousinvestment levels programmed for the next few years are to be achieved andservice levels sharply improved, overall management of the sector will needto be strengthened, including i) increasing the participation of theprivate sector in the provision of specialized services, such as datatransmisaion, while encouraging the use of private contractors to speednetwork construction; ii) revising low domestic tariffs, since these reducethe efficiency of service; and iii) improving the project implementationcapacity of GUATEL (the state-owned telecommunications enterprise) andaccelerating efforts to obtain the additional external financing requiredfor GUATEL's investment program.

Water Supply Sector

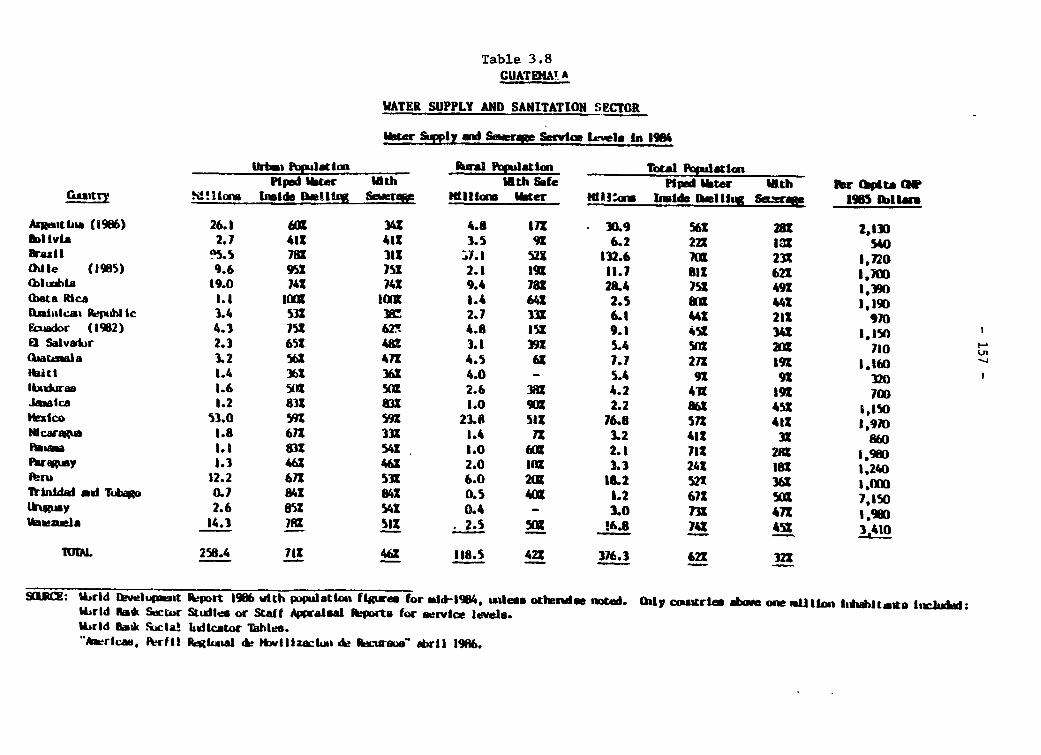

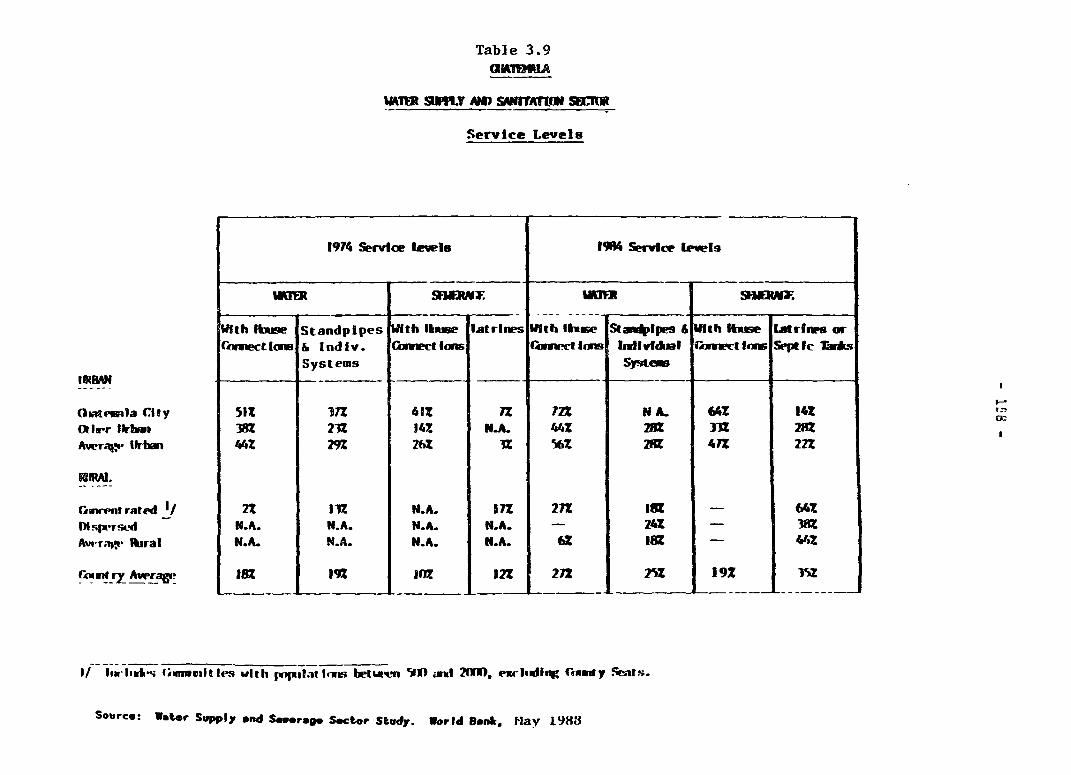

xx. Programmed investments in water supply and sanitation are fullyjustified, however the level of investment remains low in comparison withsector needs and the Government's emphasis on improving the availability ofbasic services. With current spending levels only about 0.3 percent ofGDP, there is substantial room for improvement. A possible medium termobjective would be to increase investment levels to between 0.5 and 0.6percent of GDP by 1992-1995, thus almost doubling the current level ofinvestment. This would require extensive restructuring of the sector,including: i) financial reforms to ensure adequate cost recovery, includingreform of the antiquated water title system and increasing tariff levels;ii) revising the organization of the sector to improve planning,operations, and project implementation, while eliminating the existingfragmentation in sector institutions; iii) early approval of legislation tobetter allocate and protect water sources; and Wit expanding projectpreparation activities in local communities, while also focusing onincreasingly serious contamination problems stemming from the inadequatemanagement of toxic wastes.

The Social Sectors

xxi. Guatemala's provision of public social services and efforts tomeet the basic needs of its rapidly growing population have beeninadequate. As a consequence, health indices are worse than many countriesin Latin America, literacy rates remain among the lowest in the continent,and the country confronts a serious shortage of housing meeting minimalstandards. Given these serious constraints, the Government's developmentprogram rightly stresses the importance of allocating more resources toprimary health care and primary education, while also facilitating theavailability of basic housing. At the same time, the Government has

- viii -

substantially increased the amount of resources available for municipaldevelopment through the transfer of 8 percent of ordinary revenues directlyto the municipalities for purposes of capital investment in infrastructureand public services. Achievement of these broad goals in the social sectorwill require first, a majol improvement in the utilization of existingresources, and second, a substantial increase in the level of funding forthe sector. This increase in resources should include not only increasedpublic funding, but additional efforts to facilitate the use of privatesector resources, including NGOs, and further mobilization of localcommunity resources. As a medium-term target, public sector investment inthe social sectors (health, education, housing/urban development) should beincreased from the estimated level of 1.2 percent of GDP in 1990, includingthe 8 percent transfer to the municipalities, to about 1.7 percent of GDPby 1992-1995. At the same time, part of the additional resources needed tomeet basic social needs could be provided under the proposed SocialInvestment Fund, which would open up additional funding channels formunicipalities, NGOs and other community organizations.

The Health Sector

xxii. The difficulty which the Government has in not being able toprovide adequate health care reflects not only inadequate funding, but alsoinefficient utilization of existing resources, combined with continuedoveremphasis in practice on more expensive curative care as opposed tobasic primary health care and preventive medicine. Primary health care hasreceived only about one-fourth of current expenditures and less than one-fifth of capital expenditures in the last few years. At the same time,poor hospital administration has led to an explosive increase in currentexpenditures for curative medicine, which almost doubled since 1986, whilestill leaving the hospitals without adequate resources for maintenance andsupplies. Expenditure adjustments in health should focus initially onincreasing the share of resources allocated for primary and preventivehealth care; increasing the share of resources allocated to rural areas,thus beginning to correct the current bias towards Guatemala City; andensuring adequate funding for materials, supplies, and maintenance.Increasing resources for preventive medicine and primary health care isfar the most cost effective way to improve the overall health ofGuatemala's population.

xxiii. These adjustments do not necessarily require major increases intotal resources available to the sector in the short-term, but better andmore cost effective use of existing staff, while adjusting the mix of staffand physical resources. As such, the Health Ministry should focus ontraining and recruiting primary health care personnel while redeployingmore staff to rural areas. At the same time, a major effort is needed toimprove the targeting, coordination, and cost effectiveness of on-goingpreventive and primary health care programs managed by the Ministry ofHealth. As a second priority, the Government should begin preparation ofan expanded investment program, with emphasis on primary health care, sincethe level of investment in the sector will fall sharply in the next fewyears unless a very weak project pipeline is strengthened. As a minimumthe goal should be to increase the level of investment from 0.2 percent ofGDP as projected for 1990 to at least 0.4 percent of GDP in 1992-1995.Finally, in addition to increasing investment expenditures in the sector,the overall level of resources allocated to the sector must be increased

- ix -

over the medium-term if health indicators are to improve. As a medium termgoal the Government should aim at increasing the total share ofexpenditures on health (including investment) from less than 1.5 percent ofGDP at present to at least 3.0 percent by 1995.

The Education Sector

xxiv. Although Guatemala's education system has grown rapidly over thepast 20 years, the current educational profile remains similar to the leastdeveloped countries in Latin America. The overall literacy rate is low,52 percent on average and less than 15 percent in some rural areas. Overtwo-fifths of the labor force has no formal schooling and another quarteronly 1 to 3 years of schooling. This poor level of educationalachievement reflects a long history of under investment and misdirectedinvestment in the sector. Until recently, less than 2 percent of GDP wasbeing spent on education compared to about 4.5 percent in other developingcountries. At the same time, the allocation of expenditures has beenskewed, with an unduly high share devoted to higher education, and withinsufficient resources programmed for teaching materials and support ofprimary education, particularly in rural areas. In addition to improvingthe quality and coverage of the system, the country faces the additionalchallenge of coping with the country's ethnic and linguistic diversity.

xxv. Although the Government has moved to increase spending in thesector, further efforts are needed. The principal expenditure adjustmentsrecomuen?ed include: i) making better use of available resources throughimproved utilization of existing facilities and improved management andsupervision of teachers; ii) increasing the share ef resources allocated toprimary education as well as to supplies and materials, while decreasingthe share allocated to higher education; iii) developing new educationalinvestment initiatives for the 1990s to strengthen a weak project pipeline;and iv) increasing the overall share of public resources allocated toeducation over the medium term. This will require not only increasedCentral Government participation, but also increased use of local communityresources. The overall goal should be to increase the share of resourcesallocated to education from the current low level of about 2 percent toabout 4 percent of GDP by 1995, with the share of investment in the sectorincreasing from an estimated 0.1 percent of GDP in 1990 to at least ('.3percent of GDP in 1992-1995.

Housing Sector

xIVi. Guatemala's housing deficit, which is substantial, is currentlyestimated at over 700,000 units, with public and private housing outputmeeting only a very small portion of needs. Since most families have aroof over their heads of one form or another, this deficit indicates mainlythe very high level of very poor quality or substandard housing. Effortsto resolve the country's housing shortage, require adjustments in sectorfinancing as well as policies. The challenge is to: i) introduce financialsector reforms which will encourage increased private sector involvement inhousing finance; ii) rationalize BANVI's operations and complete ongoinginitiatives to remedy serious organizational and financial constraints; andiii) develop new approaches to meeting the housing needs of the urban poor,focusing more on self-help and housing rehabilitation, while also tacklingland tenure issues.

Municipal Development

xxvii. Prospects for accelerating municipal development in Guatemala'ssecondary and smaller cities have improved considerably in the past fewyears as a result of the Government's decentralization effort and theallocation of 8 percent of general revenues for fixed capital investment.Nevertheless, most secondary municipalities have little or no capacity toeffectively program and manage development projects. Additional technicalassistance is urgently needed, particularly now that the easy and moreobvious investment needs are being taken care of. This will requireenhancing the capacity of INFOM to provide technical support, as well asfacilitating the efforts of NGOs and other community groups to providedirect support to municipalities.

Level of Public Expenditures (1988-1991)

xxviii. During the 1988-1991 period total spending for the consolidatedpublic sector is projected to increase slightly from about 14.5 percent ofGDP in 1988 to 17 percent in 1989 through 1991, with expenditures on publicsector investment increasing from an estimated 2.8 percent of GDP in 1988to an average of 4.5 percent of GDP for the remainder of the period.Higher spending levels are not feasible in the short-term, sinceachievement of even the projected levels already assumes substantialadditional resource mobilization as well as major improvements in theexecution of the public sector investment program. The proposedinvestment levels for 1989-1991 are adequate provided the expendituretargets are achieved. Guatemala cannot continue to maintain public sectorinvestment levels of less than 3.0 percent of GDP, if it is to meet itssocial and basic infrastructure needs. Urgent efforts are therefore neededto ensure that the minimum 4.5 percent of GDP target is indeed reached.

Financing Requirements and Sources (1989-1991)

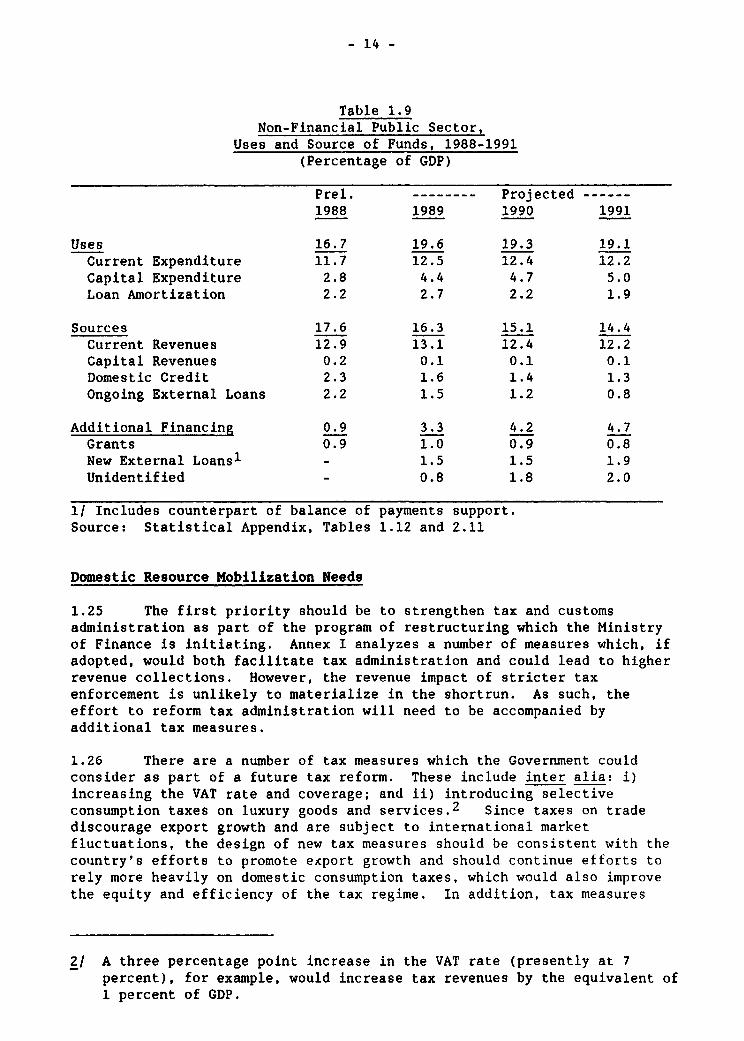

xxix. Total public sector financing requirements for the period 1989 to1991 would average about 19 percent of GDP per jear, including loanamortizatior. needs as well as current and capital expenditures. Of thistotal, about 80 percent (15 percent of GDP) is expected to be financed fromdomestic resources and already available external funds. The remaining gapof about 4 percent of GDP would be met in part from new external financing,leaving about 2 percent of GDP to be financed through increased domesticresource mobilization, including improvements in tax administration, othertax reform measures, and increases in public utility tariffs and otherusers charges. Alternatively, a portion of the gap could be filled withadditional external grant financing. However, continued undue reliance ongrant financing is risky since its is unlikely to be available over themedium term.

- xi -

Public Savings, Investment and Growth

xxx. The macroeconomic projection scenario prepared as background forthe analysis of public expenditures confirms the importance of a stepped uppublic and private sector investment effort if Guatemala is to achieve GDPgrowth averaging between 4 and 5 percent per annum, which is the minimumconsidered necessary to begin making up for the sharp economicdeterioration experienced in the early 1980s. In fact, even with GDPgrowth at the 4 to 5 percent level, Guatemala would still require about tenyears to return to its 1980 level of per capita GDP, assuming thatpopulation growth averages about 2.7 percent per year.

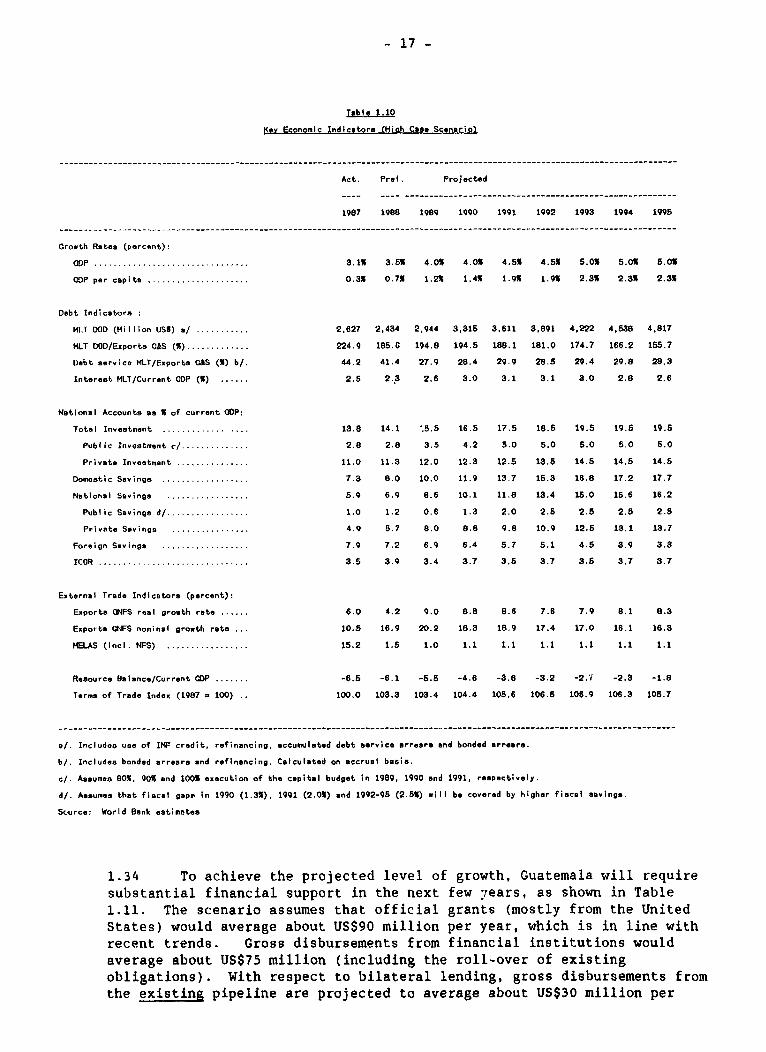

xxxi. The high case scenario assumes that gross fixed investment wouldneed to grow gradually from about 14 percent of GDP in 1988 to 19.5 percentin 1995, reflecting both a recovery in private fixed investment as well asthe increase in public sector investmenL to 5 percent in 1992 andthereafter. At the same time, domestic savings would have to increase from8 percent of GDP in 1988 to 18 percent in 1995. This savings effort wouldrequire continued austerity in public expenditure policies as well as asignificant effort to increase public savings from 1 percent of GDP in 1988to 2.5 -ercent in the 1990s. To achieve the projected level of growthGuatemala would also require substantial external financial support. Theprojections assume: i) official grants averaging US$90 million per year;ii) gross disbursements from bilateral sources averaging US$30 million peryear; iii) a sharp increase in gross disbursements from multilateralinstitutions from US$100 million in 1988 to close to US$200 million peryear; iv) gross disbursements from financial institutions averaging aboutUS$75.0 million per year (including the roll-over of existing obligations);and v) additional assistance to cover the large unfinanced gap of aboutUS$280 million per year, with about one-third being filled by suppliers'credit and the remaining US$180 million from bilateral or other sources.

Strengthening Planning, Project Preparation and Project Execution

xxxii. Resource mobilization and improved targeting and allocation ofpublic resources are major issues on Guatemala's development agenda. Otherimportant issues include the need to improve planning, proiect preparationand project execution. Inadequate planning and project preparation reducesthe Government's flexibility in programming investments to meet itsdevelopment objectives, increases the risk of introducing low priorityprojects with poor returns into the investment program, and limits theGovernment's ability to channel external assistance into well definedpriority areas. At the same time, the public sector's poor projectexecution performance restricts the Govenrnment's ability to attractadditional external support, increases the cost of major projects both interms of higher commitment and other loan charges as well as higher prices,and delays the initiation of project benefits with obvious costs to theeconomy as a whole.

xxxiii. Investment programming has become largely an ad hoc process inrecent years, determined mainly by individual agencies, depending in parton their political clout, and allocations made by the budget office, oftenwithout sufficient information or guidance on priorities. Recognizing theimportance of a stronger planning and investment coordinating function, the

- xii -

Government has recently moved to strengthen the planning agency's capacityto program investments by introducing a number of organizational changes.Nevertheless, although the new arrangement provides a stronger functionalbasis for planning, SEGEPLAN (the planning agency) will requireconsiderable strengthening in the areas of investment programming, projectevaluation and monitoring. In the meantime, it would be helpful toestablish a small working group of economists and sectoral experts fromSEGEPLAN and other entities to: i) establish the principal policyadjustments and spending needs for each key sector; ii) review existingprograms and budgets to determine how well these priorities are being met;iii) identify the specific programs and/or projects which either need to berestructured or prepared to achieve the Government's objectives; and iv)help prepare expenditure guidelines for preparation of the 1990 budget.This should be combined with preparation of a public sector investmentprogram and overall spending guidelines for the next three years consistentwith the expected availability of resources and the macroeconomicframework.

xxxiv. Deficient project preparation is one of the most importantbottlenecks slowing Government development efforts. First, there aresimply not enough projects being prepared. In fact the only substantivepreparation work is being carried out largely by external donors, thusgiving them a major role in determining investment priorities. Second,many of the projects have been only partially prepared, particularly inrespect to implementation and procedural arrangements, thus opening the wayfor serious delays during execution. To help resolve this problem, theGovernment should take the necessary steps to make the proposed NationalSystem for Financing Pre-investment (SINAFIP) operational, while ensuringthat procedures for the system are as simple and straightforward aspossible. In addition, without waiting for SINAFIP, SEGEPLAN should reviewexisting project preparation efforts and identify which preparation workshould be stopped, accelerated, or started in accordance with theGovernment's current priorities. Without a major project preparationeffort, public sector investment will most likely decline during the 1990s.

xxxv. Poor or slow project execution remains one of the most seriousconstraints on public sector investment. More than anything else,improving execution requires the appointment of experienced projectmanagers, while ensuring that they have the high level support and adequatefinancing needed. At the same time, to better ensure that the projectmanager can operate effectively, it is important that: i) theadministrative framework and operational requirements for projectimplementation are fully worked out during project preparation; ii) projectconditionality is realistically defined; and iii) adequate mechanisms formonitoring project execution and rapidly resolving implementation problemsare established. Recent Ministry of Finance initiatives to improve themanagement of external financial resources have begun to improvecoordination and monitoring of priority investment projects. These effortsneed to be continued and further strengthened.

- xiii -

Conc lus ion

xxxvi. Guatemala is fortunate in that it has no major "white elephants"in its public sector investment program. At the same time, it does notface the need to make major cuts in investment as has been the case in manyother countries. Nevertheless, Guatemala faces the difficult challenge ofimproving the mobilization and utilization of limited public resources ifthe country is to pay its "social debt" and achieve its growth objectives.The additional public sector resource mobilization and savings effort of 2percent of GDP recommended in the short-term constitutes the minimal effortneeded if Guatemala is to begin to tac ̂ e its basic developmnent challenges.Given the country's current low tax ra,.o, this effort sho'uld not representa major sacrifice. Indeed, a much greater effort will be needed over themedium term if Guatemala is to overccme the serious backlog in socialinvestment, meet growing recurrent financing requirements for maintenanceand operational costs, and provide the basic infrastructure and servicesneeded to support its export diversification strategy.

xxxvii. The additional resource mobilization effort must also beaccompanied by substantial improvements in the efficiency of resource useand a concerted effort to prepare new programs and projects, especially inthe social sectors where the project pipeline is the weakest. In fact,this is the greater challenge. Increasing the availability of resourcesfor investment and needed service; may face political obstacles, but can beachieved through a combination of easily identifiable actions to tapdomestic and external resources. Improving the design of projects and theefficiency of project execution is much more difficult since it requiresnot only legal and institutional changes, but also changes in the waypublic sector personnel are trained, motivated, and deployed.

CHAPTER It PUBLIC SECTOR EXPENDITURES AND RESOURCE MOBILIZATION

Introduction

1.01 Guatemala, the largest of the Central American countries in termsof population and economic activity, faces major social, political andeconomic challenges as it strives to consolidate a newly establisheddemocratic political framework; improve the well being of some 60 to 70percent of its population living in poverty; and reestablish a sound macroeconomic framework for restoring sustained economic growth, following thesharp decline in growth experienced during the first part of the 1980s.These challenges are compounded by serious inequalities in the distributionof income, by the limited and uneven provision of basic social services,and by the country's fragmented social structure. Almost one-half ofGuatemala's 8.4 million people are indigenous descendants of the Mayacivilization with limited assimilation into the socio-economic mainstream.Economic and social integration has been made more difficult by thecountry's rugged topography, the scattered settlement of the Indianpopulation in the Western Highlands, and the fact that only one-fifth ofthe Indian population speak Spanish, the rest communicating in 23 differentIndian languages.

1.02 Guatemala's policy makers face major expenditure allocation andresource mobilization issues in their efforts to more effectively meet thebasic development needs of the country's rapidly growing population.Although there is general agreement that more resources need to begenerated and utilized more efficiently if the backlog of social and otherbasic development needs are to be fulfilled (what the Government refers toas the "Social Debt"), there are serious questions concerning the amount ofadditional resources needed, the priorities for public expenditure, and themeans to more effectively use public sector resources. This reportidentifies major expenditure issues and recommends changes in how resourcesare generated, allocated, and utilized. It is part of an ongoing WorldBank effort to support the Government's efforts to reorganize andstrengthen management of the public sector.

1.03 Chapter I reviews the role and impact of public expenditures inmeeting the country's development objectives, including patterns and trendsin public expenditures, together with an analysis of the principal publicsector expenditure issues and projected financing requirements for theperiod through 1991. Specific sector expenditure and investment issues forthe Central Government and major decentralized agencies are covered inChapters II through VIII. The report concludes with a discussion ofplanning, project preparation, and project execution issues (Chapter IX).

- 2 -

A. Public Expenditure Framework and Recent Trends

Background

1.04 Guatemala's recent public expenditure and investment performance,must be viewed within the context of economic developments during the firstpart of the 1980s, which saw a sharp decline in GDP as the country'sexternal terms of trade deteriorated, internal politicai difficultiesmounted, and macroeconomic adjustment efforts were untimely orinsufficient. During this period, the uncertain political and economicclimate in Guatemala and the rest of Central America resulted in a sharpreduction in private domestic and foretgn investment as well as externalfinancing, while capital flight was exacerbated. As a consequence, by themiddle of the 1980s Guatemala faced serious economic and financialproblems: foreign trade was virtually at a standstill owing in large partto an unmanageable multiple exchange rate regime; inflation was runningover 30 percent; investment and national savings were nearly half the levelof the 1970s; arrears on external payments had reached about US$600million; and GDP was 6 percent below its 1980 level. The sharp decline inGDP and much lower fiscal revenues also prompted a rapid increase inexternal borrowing, with medium and long-term debt more than tripling toUS$2.5 billion by 1987.

1.05 After taking office in early 1986, the new civilian Governmentmoved to stabilize the economy, taking measures to improve exchange ratemanagement, increase interest rates, and reduce the fiscal deficit. Thesemeasures, combined with favorable coffee prices, resulted in a substantia'limprovement in economic performance in 1987, with GDP growing by 3 percent,the first real growth in several years. Faced with renewed balance ofpayment pressures in late 1987 and 1988, the Government took additionalstabilization measures in 1987 and mid-1988. Nevertheless, despite itssuccess in stabilizing the economy, the Government's efforts to improvedomestic resource mobilization and accelerate public sector investment havebeen less successful, as discussed in greater detail below.

Trends in Government Expenditure

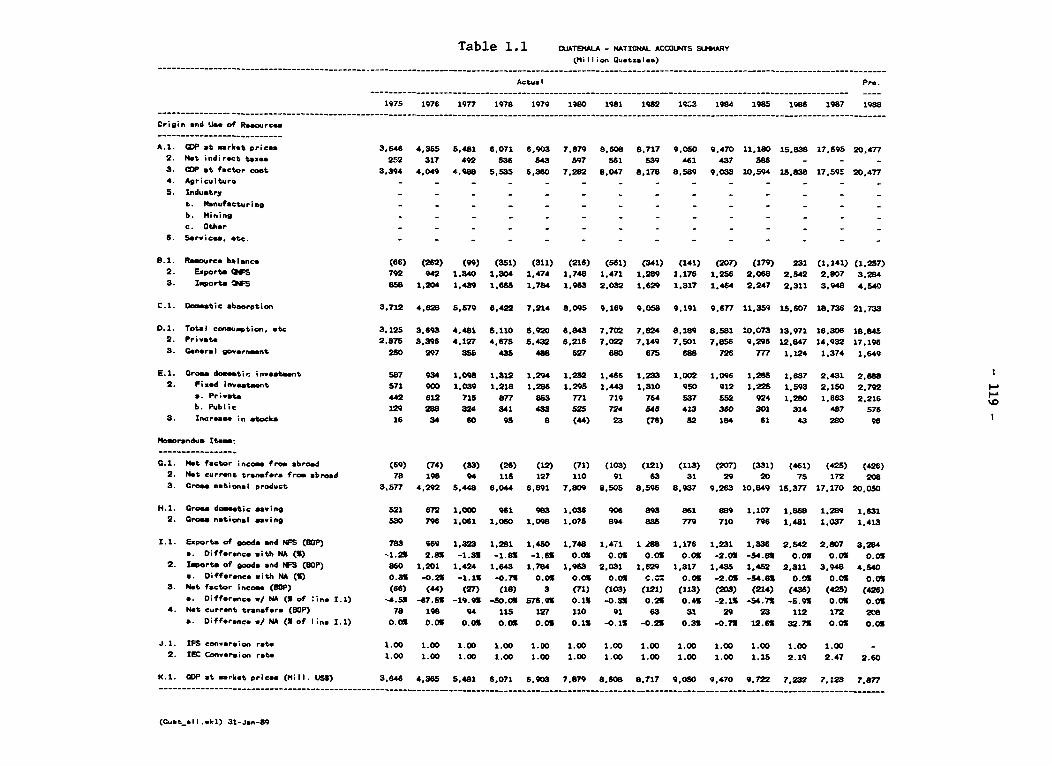

1.06 Faced with a major decline in tax revenues in the first half ofthe 1980s, Guatemala drastically cut public investment and constrainedother public expenditures, especially in the social sectors. As aconsequence, total public expenditures fell from 17 percent of GDP in 1980to about 12 percent in 1985. Real per capita Central Governmentexpenditures on health and education, for example, were cut by 60 and 16percent respectively; public outlays for education averaged only 2.3percent of GDP in 1980-85 compared with an average of 4.5 percent for alldeveloping countries. Capital outlays were also cut by more than halfduring the same period, falling from 6.7 to 2.7 percent of GDP, owing inpart to the completion of two major hydroelectric projects and a majorport. Central Government recurrent expenditures declined by over 1 percentof GDP, reflecting mainly a fall in the wage bill, even though overall

public sector employment increased by 13 percent between 1980 and 1985.With the exception of expenditures on defense, the expenditure cutsaffected all sectors, with health, transport and education being theministries hardest hit.

1.07 Since 1986, public expenditures have begun to recover, withrecurrent expenditures outpacing the recovery in public investment.Recurrent expenditures increased by 54 and 23 percent respectively in 1986and lSd7, reflecting higher consumption expenditures as well as interestpayments on Government bonds, special employment and subsidy programs, andtransfers mandated under the new Constitution to the university, judiciaryand municipalities. Capital outlays actually fell further in 1986 to 2percent of GDP as a result of a marked slow down in project execution asthe new Government took office and undertook to reassess its investmentpriorities. Capital outlays rose slightly in 1987 to 2.8 percent of GDP,although actual Central Government capital outlays were about one-half ofbudgeted amounts. Public investment remained at an estimated 2.8 percentof GDP in 1988, about two-thirds of the original budget reflectingcontinuing domestic budget constraints and project implementation delays.

Table 1.1Nonfinancial Public Sector Operations, 1980-88

(Percentage of GDP)

--------------------------------------------------------------------- __------__-----------------------.-

---------------------- Actual -------------------------- (Prel.)

1980 1981 1982 1983 1984 198S 1988 1987 1988

A. Current Revenue 12.2 11.3 11.8 10.9 10.4 10.6 11.1 12.2 *2.9

1. Pub. Enterprises Surplus 0.5 0.4 0.9 1.0 1.1 1.1 1.1 0.8 1.1

2. Taxes and Other Revenues 11.3 10.4 10.6 9.7 9.1 9.2 9.9 10.8 11.2

B. Current Transfers 0.4 0.6 0.1 0.1 0.2 0.3 0.1 0.8 0.6

B. Current Expenditure 10.0 10.2 10.1 9.7 10.1 9.3 10.1 11.2 11.71. Wages and Salaries 6.7 6.7 6.6 6.6 6.8 6.2 6.0 6.7 6.7

2. Goods and Services 2.3 2.5 2.2 1.9 2.1 1.9 2.2 2.6 2.8

3. Interest Payments 0.8 0.9 1.1 1.1 1.2 1.0 1.S 1.8 2.14. Current Transfers 1.2 1.1 1.1 1.2 1.2 1.2 1.4 1.4 1.6C. Current Balance 2.2 1.1 1.6 1.2 0.8 1.3 0.9 1.0 1.2

D. Capital Revenues 0.0 0.1 0.2 0.1 0.1 0.0 0.4 0.5 0.2

E. Capital Expenditures 8.7 8.4 8.3 4.8 3.8 2.7 2.0 2.8 2.8

1. Fixed Capital Formation 6.9 7.9 5.9 4.3 3.2 2.8 1.9 2.4 2.6

2. Other Capital Expenditures 0.7 0.6 0.4 0.3 0.6 0.4 0.1 0.4 0.2

C. Overall Balance -4.4 -7.2 -4.5 -3.3 -3.4 -1.3 -0.6 -1.3 -1.4

1. Official Capital Grants 0.0 0.0 0.0 0.0 0.0 0.0 0.0 1.1 0.9

2. Net Foreign Financing 1.2 1.3 1.2 1.4 0.2 0.2 0.4 0.4 0.0

3. Net Domestic Financing 3.2 6.9 3.3 1.9 3.2 1.1 0.2 0.4 0.8

4. Other 0.0 0.0 0.0 0.0 0.0 0.0 0.0 -0.6 -0.4

Source: Ministry of Finance, IMF and World Bank estimates.

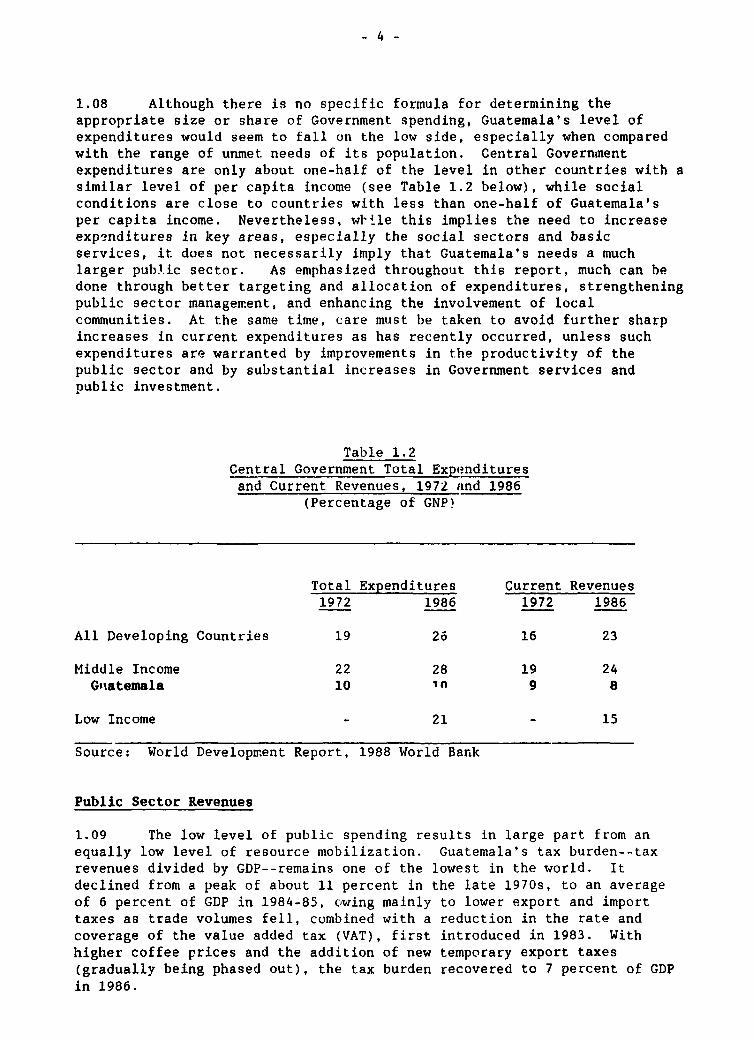

- 4 -

1.08 Although there is no specific formula for determining theappropriate size or share of Government spending, Guatemala's level ofexpenditures would seem to fall on the low side, especially when comparedwith the range of unmet needs of its population. Central Governmentexpenditures are only about one-half of the level in other countries with asimilar level of per capita income (see Table 1.2 below), while socialconditions are close to countries with less than one-half of Guatemala'sper capita income. Nevertheless, wI'le this implies the need to increaseexpe3nditures in key areas, especially the social sectors and basicservices, it does not necessarily imply that Guatemala's needs a muchlarger public sector. As emphasized throughout this report, much can bedone through better targeting and allocation of expenditures, strengtheningpublic sector management, and enhancing the involvement of localcommunities. At the same time, care must be taken to avoid further sharpincreases in current expenditures as has recently occurred, unless suchexpenditures are warranted by improvements in the productivity of thepublic sector and by substantial increases in Government services andpublic investment.

Table 1.2Central Government Total Expe.ndituresand Current Revenues, 1972 and 1986

(Percentage of GNP)

Total Expenditures Current Revenues1972 1986 1972 1986

All Developing Countries 19 26 16 23

Middle Income 22 28 19 24G'iatemala 10 in 9 8

Low Income - 21 - 15

Source: World Development Report, 1988 World Bank

Public Sector Revenues

1.09 The low level of public spending results in large part from anequally low level of resource mobilization. Guatemala's tax burden--taxrevenues divided by GDP--remains one of the lowest in the world. Itdeclined from a peak of about 11 percent in the late 1970s, to an averageof 6 percent of GDP in 1984-85, owing mainly to lower export and importtaxes as trade volumes fell, combined with a reduction in the rate andcoverage of the value added tax (VAT), first introduced in 1983. Withhigher coffee prices and the addition of new temporary export taxes(gradually being phased out), the tax burden recovered to 7 percent of GDPin 1986.

- 5 -

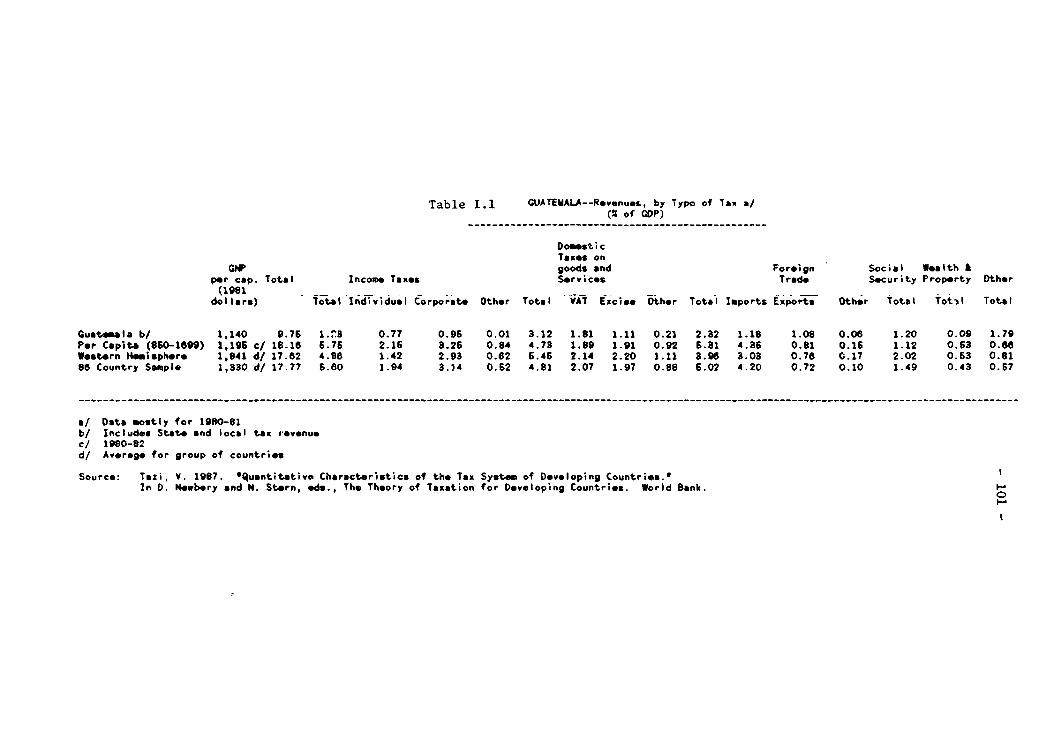

1.10 Since 1986, the Government has undertaken a number of initiativesto improve revenue performance. These have included the introduction ofnew temporary export taxes in mid-1986 to absorb part of the windfallprofit associated with the gradual unification of the exchange rate,followed by a major tax reform package in late 1987.1 As a result of theseadjustments, the tax burden increased to 8.2 percent in 1987 and to 8.8percent in 1988, with trade taxes growing to about 30 percent of revenuesin 1988. Despite this improvement, however, the tax burden is expected todecline gradually to ire-reform levels of 7.8 percent of GDP in 1991, asshown in Table 1.3, unless additional measures are taken, including furtherstrengthening of tax administration. The projected decline in revenuesresults largely from the Government's export promotion policies, as aconsequence of whic:. both temporary export and import taxes are beinggradually phased out. Additional details of the 1987 tax reform areprovided in Annex I.

Table 1.3Central Government Revenue, 1987-91

(Percentage GDP)

Est. Prel. ------ Projected ------1987 1988 1989 1990 1991

Tax Revenues 8.2 8.8 8.5 8.0 7.8Direct taxes 1.6 2.2 2.4 2.4 2.4

(income tax) (1.4) (1.9) (2.1) (2.1) (2.1)Indirect taxes 6.6 6.6 6.1 5.6 5.4

VAT 2.3 2.4 2.4 2.4 2.3Export 0.9 0.7 0.3 0.0 0.0Import 1.6 1.9 1.8 1.6 1.5Other 1.8 1.6 1.6 1.6 1.6

Source: Ministry of Finance and World Bank estimates

1.11 A major cause of Guatemala's poor revenue performance, is taxevasion, which is reportedly extremely high owing mainly to lax taxadministration. Although there is no hard evidence to indicate the degreeof tax evasion, it is interesting to note that Guatemala's income tax ratesare similar to or even higher than in other countries. Nevertheless, itsincome tax yields only a small fraction of the revenues obtained elsewhere(see Annex I). Income tax actually paid in 1986 represented only 1.4percent of corporate gross income and 3.4 percent of personal gross income.Administration of the VAT is equally poor, with many firms failing to turnin VAT receipts to the treasury and the treasury unable to provide VATrefunds to eligible taxpayers. The situation with other taxes is alsogloomy: property taxes collected reflect only a small portion of marketvalues, despite recent efforts to improve the register and valuation of

1/ The 1987 tax reform: (i) reduced top marginal income tax rates and thenumber of tax brackets; (ii) closed some talx loopholes; (iii) limitedtax deductions; (iv) introduced advance tax payments (pagos a cuenta)for corporate income tax; and iv) increased import tariffs by 4percent. The latter tariff increase will be gradually reduced to 1percent by 1992.

- 6 -

properties, including a self-valuation system (autovaluo); gift andinheritance taxes are widely avoided via trusts; taxes on idle land areseldom enforced; and selective consumption taxes introduced in 1985 are notbeing applied as a result of privaEe sector complaints that theyconstituted double taxation with the VAT and were thereforeunconstitutional.

B. Future Expenditure Options and Financing Requirements

1.12 Since Guatemala's present level of resource mobilization andpublic expenditure is too low to satisfy the population's basic needs andmeet the country's requirements ̀or improving and expanding basicinfrastructure to support growth objectives, the Government faces threebasic options.

First, improve the capacity of the public sector to utilizeresources more efficiently, ircluding reallocating resources tobetter meet investment and :-ecurrent expenditure requirements inkey areas, while accelerating efforts to mobilize additionaldomestic resources coupled with a judicious use of additionalexternal assistance.

Second, sharply increase external borrowing to make up forshortfalls in internal resource mobilization.

Third, pursue more limited growth1 and expenditure objectives.

Both the second and third options raise serious questions. There areclearly limitations on Guatemala's external debt servicing capacity, whileundue dependence on external resources is risky and not advisable. At thesame time, further limiting the low level of investment and expenditure onbasic services would undermine the country's ability to increase growth andaddress underlying social constraints which are critical for maintainingsocial and economic stability. As a consequence, this report argues thatGuatemala's only real choice is to follnw option number one, namely toincrease domestic resource mobilization, while making judicious use ofadditional external assistance, and at the same time addressing the seriousinstitutional and managerial bottlenecks which limit the capacity of theGovernment to use and allocate resources more efficiently.

1.13 Increasing expenditures on public services and essent!alinfrastructure does not mean that the size of the public sector must heexpanded. Indeed, the first priority should be to use available resourcesmore effectively. What it does mean is that a larger share of resourcesshould be allocated for investment and basic services in health andeducation, for example, while reducing overstaffing and minimizingunnecessary expenditures on general administration. At the same time, theGovernment should explore ways to minimize demands on the CentralGovernment purse. This implies continued efforts to increase localcommunity participation in the planning and financing of local developmentneeds, while also facilitating the expansion of on-going NGO sponsoreddevelopment efforts. In addition, productive investments which directly

benefit large scale private commercial interests, such as major irrigationschemes for large-scale farmers, could be financed directly by the privatesector.

1.14 The overall goal should be to adequately finance public servicesand investment in those sectors and areas where private investment cannoteffectively operate or where public interest clearly outweighs privateconcerns. It seems clear that in such areas as health, education, lowincome housing, water supply and sanitation, road irfrastructure, andagriculture services, especially for the small and medium sized farmers,that strong public sector involvement is essential. It is much less clearin such areas as telecommunications and power, for example, where privatesector financing of investment is more feasible. Although issues ofprivatization go well beyond this report, the Government may need toconsider whether certain services could not be more cheaply and effectivelysupplied by the private sector, with Government participation restricted tothe important role of maintaining an adequate regulatory environment.

1.15 The following paragraphs analyze the projected level andcomposition of public sector expenditures over the short-term (1989-1991)and recommend adjustments in the expenditure pattern and level of publicexpenditures to be achieved over the medium-term, perhaps by 1995. This isfollowed by an analysis of financing requirements for the period through1991, within the context of a medium-term economic projection scenario forachieving renewed growth.

Level of Public Expenditures (1989-1991)

1.16 Projections of total spending for the consolidated public sectorfor the period 1989-91 (Table 1.4 below) show a slight increase over theperiod, with expenditures increasing from 14 percent of GDP in 1987 toabout 14.5 percent in 1988 and to about 17 percent in 1989 through 1991.This increase in total expenditures assumes a further resource mobilizationeffort and improvements in execution of the investment program. Withinthis overall total, current expenditures reached 11.2 percent of GDP in1987, increased to 11.7 percent in 1988, and are projected to average 12.3percent through 1991. Investment expenditures ::eachee. only 2.8 percent ofGDP in 1987, and preliminary estimates indicate a similar level for 1988.However public investment levels are projected to increase to an average4.5 percent of GDP through 1991, assuming substantial additional domesticrevenue mobili7ation as well as major improvements in execution of thepublic sector investment program.

- 8 -

Table 1.4Public Sector Expenditures by Category (1980-1991)

(Percentage of GDP)

------- Actual ------- Prel. *.-- Projected ---1980 1984 1986 1987 1988 1989 1990 1991

Current Expenditures 10.0 10.1 10.1 11.2 11.7 12.5 12.4 12.2of which wages andsalaries 5.7 5.6 5.0 5.7 5.7 5.8 5.7 5.6goods and services 2.3 2.1 2.2 2.6 2.3 2.3 2.3 2.3interest payments 0.8 1.2 1.5 1.6 2.1 2.3 2.2 2.2current transfers 1.2 1.2 1.4 1.4 1.6 2.2 2.2 2.2

Capital Expenditures 6.7 3.8 2.0 2.8 2.8 4.4 4.7 5.01

Total Expenditures 16.7 13.9 12.1 14.0 14.5 16.9 17.1 17.2

1/ Includes additional unidentified investment of 0.4% of GDPSource: Statistical Appendix, Table 1.12

1.17 The proposed overall levels of spending are adequate provided thecapital expenditure target is achieved. If Guatemala is to adequatelymeet its social and basic infrastructure requirements, it cannot continueto maintain public sector investment levels of less than 3.0 percent ofGDP. Urgent efforts are therefore needed to ensure that the minimum 4.5percent of GDP target is indeed achieved in the next few years, increasingto 5.0 percent in the early 1990s. In fact, the level of 5.0 percent ofGDP still falls below average investment levels in other middle incomecountries in which public investment is in most cases over 6 percent ofGDP.

Composition of Public Expenditures (1989-1991)

1.18 As indicated in Table 1.5 below, the share of current and capitalexpenditures for the consolidated public sector is projected to be about 73and 27 percent respectively for the 1989-91 period, assuming that projectedlevels of investment are actually achieved. The share of wages andsalaries for the same period is expected to average about 33 percent oftotal expenditures, with about 14 percent on average allocated for othergoods and services, 13 percent for interest payments and 13 percent fortransfers. Although cross country comparisons must be treated withcaution as data is not strictly comparable, this spending pattern showsthat Guatemala allocates a higher share to wages than other middle incomecountries, while current transfers are considerably lower. Since thequantity and coverage of public services provided does not appear veryextensive, the very high share accorded to wages (even higher in earlieryears) would seem to reflect low productivity in the public sector togetherwith an inappropriate mix of skills, while also indicating that theGovernment is acting as an employer of last resort.

Table 1.5Public Sector Expenditures by Category

(1980-1991)(Percent of Total)

Otheractual ------- Prel. --- Projected --- Middle

1980 1984 1986 1987 1988 1989 1990 1991 Incomel/

Current Expenditures 60 73 8'. 80 81 74 73 73 77of which:Wages and Salaries 34 40 41 40 40 34 33 33 23Goods and Services 14 15 18 18 16 14 14 14 13Interest Payments 5 8 13 11 14 13 13 13 7Current Transfers 7 9 12 10 11 13 13 13 34

Capital Expenditures 40 27 16 20 19 26 27 27 23

1/ World Development Report, 1988, World Bank. Based on 1980 data for MiddleIncome Countries.Source: Ministry of Finance and World Bank estimates

Composition of Public Sector Investment (1988-91)

1.19 As summarized in Table 1.6 below, infrastructure investments,given their large capital requirements, are expected to continue to accountfor the largest share of public sector investment expenditure. The shareof infrastructure out of total capital investments increases from about 40percent in 1988 to close to 60 percent in 1990 and 1991, owing mainly toprojected higher investments in power and telecommunications. Investmentsin the social sectors (health, education, housing and urban development--including the 8 percent transfer to the municipalities) accounted for anestimated 36 percent of investment in 1988 and are projected to account forabout 30 percent of investment in 1989, but fall to about 24 percent oftotal investment in 1990 and 1991, reflecting in part a weak projectpipeline in health and education, as well as the completion of heavyinvestments in hospital equipment planned during 1988 and 1989.Agriculture investment is projected to average about 13.5 percent of totalpublic sector investment over the period.

- 10 -