Embed Size (px)

Citation preview

REPORT ON AN AUDIT

OF THE DISBURSEMENTS PROCESS

AUDIT PROJECT #9802

Roberta McManus, CPA, CIA, CGFO Interim City Auditor

Joanne Becknell, CIA, CGFO

Acting Senior Auditor

Gordon R. Klein, CISA, CGFO Auditor II

Auditor-In-Charge

AUDITING DEPARTMENT

M a r c h 1 9 9 9

Table of Contents

TABLE OF CONTENTS

I. SCOPE AND OBJECTIVES............................................................................................1

II. METHODOLOGY ..........................................................................................................2

III. BACKGROUND............................................................................................................5

IV. CONDITION STATEMENTS AND MANAGEMENT ACTION PLANS ...............10

A. The City should strengthen controls to prevent duplicate payments ............10

1. Valid receiving reports.............................................................................13 2. Documentation authorizing payments......................................................14 3. Cancellation of paid invoices...................................................................15 4. Detailed requisitions/POs.........................................................................16 5. Invoice routing .........................................................................................17

B. The City should strengthen internal controls to ensure the integrity of financial reporting........................................................................................20

1. Proper account coding..............................................................................20 2. Retention of support for payments...........................................................21

C. Payments for the receipt of services pursuant to a contract should be requested and made using the contract payment forms and process............22

V. EXIT CONFERENCE ..................................................................................................24

Audit of the Disbursements Process i

Scope and Objectives & Methodology

I. SCOPE AND OBJECTIVES

Our 1998 audit work plan included a review of the City’s disbursements

process. Our primary objectives were to determine whether 1) disbursements

made by the City were appropriately authorized; 2) goods/services paid for were

actually received; and 3) an adequate system of internal controls is in place to

minimize the risk of loss due to waste, fraud and abuse. The audit period was May

1997 to March 1998. In order to perform certain tests, we also examined

transactions spanning a longer period of time (Section II. Methodology).

We focused our review on those disbursements processed by the Accounts

Payable section of the Department of Management and Administration (DMA).

Payroll transactions, refunds of deposits to utility customers, and investment

transactions were not included in this review.

It is important to note that the City’s internal controls over the

procurement/disbursement cycle are highly dependent upon proper system security

within the FMS and Purchasing systems. In our Report on Financial Controls

Review in the Police Department (#9846) we evaluated system security and

authorizations of the Purchasing System as it related to Tallahassee Police

Department (TPD) cost centers only. We identified several significant security

weaknesses and resultant risks which were reported to DMA management for

corrective action. We did not evaluate system security in this audit.

Audit of the Disbursements Process 1

Scope and Objectives & Methodology

II. METHODOLOGY

Our review was conducted in accordance with generally accepted

government accounting standards and accordingly included such tests of the

records and such other auditing procedures as we considered necessary under the

circumstances.

We completed a profile of the disbursement process by interviewing key

staff, documenting the process, reviewing operating/procedures manuals,

reviewing prior audit findings, and confirming all results with the audit liaisons.

The overall analysis provided us with the basis for selecting the areas warranting

more detailed testing and/or analysis. Periodic progress meetings were held with

the audit liaisons. These meetings serve to inform the program administrators of

the audit progress and as a discussion forum which enhances the effectiveness of

the audit.

We randomly selected 113 disbursements (checks and wire transfers,

generically referred to as Checks) made between May of 1997 and March of 1998.

Twenty (20) of these were selected from TPD cost centers as part of the Financial

Controls Review in the Police Department (#9846). We have chosen to

incorporate and report the results of those tests within this audit report.

We reviewed the Checks and supporting documentation for compliance

with City policies and procedures. This review included, but was not limited to,

tests (Attribute Tests) to ensure that:

�� funds for the check were appropriated by the City Commission,

2 Audit of the Disbursements Process

Scope and Objectives & Methodology

�� release of the funds was authorized by the appropriate level of

management,

�� the invoice was properly delivered,

�� the check was for the correct amount and to the correct recipient,

�� the invoice was properly canceled, and

�� the disbursement was accounted for properly.

Our samples comprised 4.4% of the dollar amount and 0.3% of the volume

of checks issued during the audit period and consisted of:

Number of Checks

Disbursed pursuant to Total dollar amount

58 Purchase orders $ 249,499.99 32 Check requests $ 11,777,139.59 14 Travel advance/Reimbursement request $ 4,845.25 2 Contract payment request $ 113,112.88 5 Interface with Fleet Management’s FASTER

system $ 5,401.57

2 Payments directly from invoices $ 1,571.00 Total - 113 $12,151,570.28

We chose not to test transactions from the City’s payroll system, investment

or debt management activities, or those resulting from the interface with the City’s

Customer Information System (CIS).

We applied additional audit procedures to test for duplicate payments. We

downloaded all paid disbursement vouchers for the 19-month period from October

1996 through April 1998 (Total Population) in order to perform the tests

(Duplicate Payment Tests). We aggregated the total number of checks issued by

vendor and selected the top 25 vendors for the Duplicate Payments Test. We

designed our procedures to detect whether duplicate payments were made to these

vendors. The current systems used to process disbursements do not contain the

Audit of the Disbursements Process 3

Scope and Objectives & Methodology

functionality to compare the vendor invoice number against previous payments.

Based on the results of that review of the top 25, we expanded our tests to include

the total population of paid vouchers.

4 Audit of the Disbursements Process

Background

III. BACKGROUND

This audit was conducted under the authority of Section 33 of the

Tallahassee City Charter and in accordance with our audit work plan. Our review

was limited to those disbursements made by check or wire transfer from the City’s

general checking account (Operating Account) through the accounts payable

process.

In planning our procedures for this audit, we examined the volume and

dollar amounts disbursed by the City for the 14-month period from January 1,

1997, through February 28, 1998. During this period, $328 million was disbursed

by the City from its Operating Account. This was accomplished through 53,396

separate checks, wires, or electronic fund transfer (EFT) transactions.

As seen in Exhibit 1, a significant percentage of the volume of these

transactions (40%) represent individual disbursements under $100, while the

majority of the disbursements (55%) were between $100 and $10,000. Only 5% of

the disbursements were for amounts in excess of $10,000 and only 2% for amounts

in excess of $50,000.

Audit of the Disbursements Process 5

Background

Exhibit 1 - Percentage of Checks Disbursed by Volume

Less Than $10040%

Between $100 and $10K55%

Over $50K2%

Between $10K and $50K3%

All checks distributed from the City’s operating account from January 1997 through February 1998.

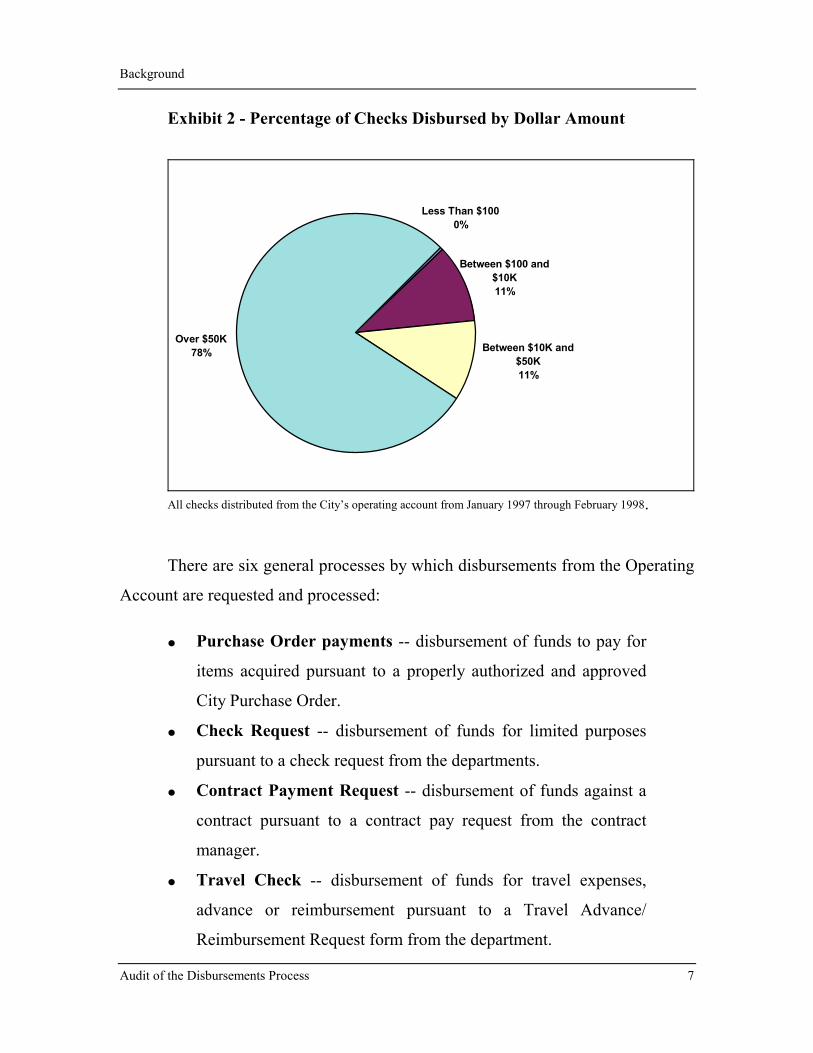

As shown in Exhibit 2, those checks over $50,000 (2% of the volume)

represent 78% of the dollar amount of monies disbursed. Those disbursements

between $100 and $10,000 and those between $10,000 and $50,000 each represent

11% of the dollar amounts disbursed.

6 Audit of the Disbursements Process

Background

Exhibit 2 - Percentage of Checks Disbursed by Dollar Amount

Between $10K and $50K11%

Over $50K78%

Between $100 and $10K11%

Less Than $1000%

All checks distributed from the City’s operating account from January 1997 through February 1998.

There are six general processes by which disbursements from the Operating

Account are requested and processed:

�� Purchase Order payments -- disbursement of funds to pay for

items acquired pursuant to a properly authorized and approved

City Purchase Order.

�� Check Request -- disbursement of funds for limited purposes

pursuant to a check request from the departments.

�� Contract Payment Request -- disbursement of funds against a

contract pursuant to a contract pay request from the contract

manager.

�� Travel Check -- disbursement of funds for travel expenses,

advance or reimbursement pursuant to a Travel Advance/

Reimbursement Request form from the department.

Audit of the Disbursements Process 7

Background

�� Fleet payment -- disbursement of funds to a vendor as a result

of an interface with Fleet Management’s computerized

management program (FASTER).

�� CIS Check -- disbursement of funds to a utility customer as a

return of deposit or final bill settlement as a result of an interface

with the City’s computerized Customer Information System

(CIS).

We did not review disbursements made pursuant to the CIS interface. All

of the other processes outlined above include Accounts Payable (AP) creating

system vouchers after ensuring that all supporting documentation (invoice, PO,

receiving report, check request, etc.) is proper. Vouchers are then converted to an

electronic check file in FMS containing all checks ready for payment. The

electronic check file, a check file listing, and supporting paperwork are then

forwarded to the City Treasurer-Clerk’s Office (TC), Disbursements Section

(Disbursements). Disbursements then:

�� prints checks and remittance advice copies from the check file,

�� matches each check and remittance advice with the appropriate

paperwork, verifies the pertinent information on the check

against the supporting documentation, reviews appropriate

approval authority on all supporting documents, and ensures the

check is made payable to the appropriate party,

�� routes contract payment requests and associated checks and

supporting documentation through TC Contracts Section

(Contracts) for review and approval,

�� cancels (marks paid) the invoices and supporting documents, and

�� disburses the payments to the vendors.

8 Audit of the Disbursements Process

Background

The remittance advices and all supporting documents are then forwarded to

the Treasurer-Clerk’s Office, Records Management Section (Records), which

scans the remittance advice and supporting documents into the City’s electronic

document management system (EDMS).

Audit of the Disbursements Process 9

Condition Statements and Management Action Plans

IV. CONDITION STATEMENTS AND MANAGEMENT ACTION PLANS

The City of Tallahassee has established procedures (internal controls) for

authorizing, processing and disbursing funds to vendors. These internal controls

are designed to ensure that purchases are:

�� budgeted,

�� authorized,

�� received, and

�� correctly billed.

These internal controls also serve to minimize the risk of waste, fraud or

abuse of City resources. Our review indicated that there are opportunities to

improve adherence to established procedures by the support sections involved

(Procurement Services, Accounts Payable and Disbursements) and by the

individual departments that initiate purchases and request payments to the vendors.

In general, we found that internal controls need to be strengthened to

prevent duplicate payments to vendors, to ensure the accuracy and integrity of the

City’s financial records, and to ensure that contracts are properly authorized,

approved, and executed.

A. The City should strengthen controls to prevent duplicate payments.

Our review revealed that the disbursement process allows duplicate

payments to vendors for the same invoice. The risk of making a duplicate payment

appears to increase based on the number of separate disbursements made to the

same vendor.

10 Audit of the Disbursements Process

Condition Statements and Management Action Plans

Therefore, we performed tests to identify transactions that met the

following criteria:

�� more than one payment to the same vendor,

�� for the same invoice number, and

�� for the same dollar amount.

Our tests included all paid voucher transactions from October 1996 through

April 1998 which totaled 140,512 transactions. These tests resulted in 2,365

transactions meeting the conditions, representing payments to 335 separate

vendors totaling over $1.6 million. All of these transactions were processed either

by Accounts Payable or Fleet Management. These tests did not directly detect

transactions that were duplicate payments but those which, based on the criteria

above, might be duplicate payments. We reported our detailed results to Accounts

Payable and Fleet Management, and staff from these areas individually researched

each suspect transaction to determine if it represented an overpayment by the City.

While our tests included all of the paid vouchers, they may not have

detected 100% of the potential duplicate payments. Departments have entered

multiple invoice numbers in one receiving report invoice number field, making it

difficult to detect duplicate invoice numbers in these instances. The receiving

process should require departments and AP to receive on each invoice separately

so that invoice number is a unique searchable field. AP and Departments need to

use that field to research whether the invoice has already been received on in the

system.

As a result of their review, Accounts Payable reported that 53 payments

made to 20 separate vendors represented duplicate payments by the City totaling

$21,744. Accounts Payable has contacted each vendor to reclaim the

Audit of the Disbursements Process 11

Condition Statements and Management Action Plans

overpayments in the form of a refund or credit. To date, $21,684 or 99.7% of the

monies have been recovered.

Fleet Management reported that 67 payments made to 22 separate vendors

represented duplicate payments totaling $5,602. Fleet Management is in the

process of contacting each vendor identified to reclaim the overpayments.

However, none of the monies have been recovered.

Accounts Payable has developed and implemented a process of testing

disbursements on a monthly basis, based on the same test procedures used in this

audit. This process identifies those transactions made during the previous month

that may have represented a duplicate payment made by the City. This process

should allow the City to detect and recover overpayments in a timely manner.

Additionally, staff is able to determine the cause of, and implement procedures to

prevent these types of errors in the future.

The overpayments that have been made are the result of not fully complying

with the internal control processes prescribed by the City of Tallahassee in its

purchasing/disbursement cycle. Internal control functions are shared by both the

support sections (Procurement Services, AP, Disbursements) and operating

departments. Based on our attribute tests, we found areas where compliance with

the process should be improved in both support and operating departments.

Specific improvement areas are discussed below according to area of

responsibility.

12 Audit of the Disbursements Process

Condition Statements and Management Action Plans

Support Departments

1. Valid receiving reports

Our review revealed that 14 of the 58 checks that were issued as PO

payments were issued without an accompanying receiving report providing

evidence that the goods/services had been received. AP staff has been using data

from the FPAY screen in FMS to determine receipts. If the FPAY screen

indicated the items had been received, the screen was printed as evidence that the

goods/services were received rather than matching the invoice to a receiving

report. Since multiple copies of the FPAY screen may be printed, multiple copies

of the invoice may be processed for payment.

Upon delivery of goods/services to the department, the vendor should send

the invoice for the payment of those goods/services to AP. The department is

responsible for receiving the goods and reporting to AP using one of the following

processes:

�� electronically through the Purchasing System, or

�� by submitting a signed hard copy receiving report.

When AP receives the invoice from the vendor, they verify that the prices

charged agree to the PO and that there is a valid receiving report from the

department. AP also verifies the mathematical extension of price and quantity

received, applies any discount applicable, and vouchers the invoice for payment.

This process ensures that the City only pays for goods and services actually

received due to the fact the computerized receiving system allows only one

receiving report to print in AP each time items are received. The manual system

Audit of the Disbursements Process 13

Condition Statements and Management Action Plans

requires one original receiving report with an appropriate signature. Since only

one receiving report is generated, should a duplicate invoice be submitted it would

not be paid because there would be no matching receiving report.

The Treasurer-Clerk, Disbursements Section (Disbursements), prints the

checks, reviews the supporting documentation for payment, and if appropriate

marks the invoice and receiving report as paid, and mails the check to the vendor.

A part of their review includes checking for a valid receiving report. We found

that Disbursements was unaware that a printout of the FPAY screen was not an

appropriate substitute for a valid receiving report and that these payments were not

caught as part of their review process.

We have reported our findings to both AP and Disbursements, and they

have discontinued accepting FPAY screen prints without additional supporting

details as evidence of receipt for vendor payments, effective December 31, 1998.

To ensure AP and Disbursements staff continue to adhere to this decision, the

basis for the decision should be documented in the appropriate operations manuals

and communicated in writing to the affected staff.

2. Documentation authorizing payments

Two of the 113 checks reviewed, totaling $1,571, were paid from an

invoice without any supporting documentation and authorized signature. There

was no evidence (i.e., neither a PO, Check Request, Travel Advance/

Reimbursement Request, Contract Pay Request, Receiving Report) that the

payments were verified for appropriateness and authorization. This lack of

documentation was not detected by Disbursements in their review. We were able

to determine that the two payments detected were appropriate. However, the

14 Audit of the Disbursements Process

Condition Statements and Management Action Plans

practice of vouchering and disbursing funds based only on an invoice bypasses all

of the City’s established control processes and exposes the City to financial loss.

3. Cancellation of paid invoices

One of the most common internal control practices used by both private and

public sector business is to cancel, or stamp “paid,” on invoices prior to mailing

the check to the vendor. This prevents the invoice from accidentally being paid

twice. The City’s process includes a step where Disbursements cancels invoices,

check requests and other similar documents prior to releasing the checks. We

found that 19 of the 113 checks reviewed were not marked paid by Disbursements

upon payment of the invoices. This creates the potential for invoices that have

already been paid to be re-submitted to AP without being detected.

We reported this problem to Disbursements management, and they have

agreed to immediately implement on a monthly basis a process of randomly spot

checking the supporting paperwork after payments have been processed. Should

any exceptions be identified, the spot checking will be increased to a weekly basis

until no further problems are noted.

Individual Departments

The internal control process starts at the department level when departments

input either a requisition or PO. For purchases under $10,000, the department

performs the steps to create a PO internally. For purchases that exceed $10,000,

the department creates a requisition in the system, and it is then converted to a PO

by Procurement Services staff. The department establishes the quantity of goods

ordered and the accounts charged at the time the requisition/PO is created. It is

Audit of the Disbursements Process 15

Condition Statements and Management Action Plans

also the department’s responsibility to inform the vendor of the City’s

requirements regarding delivery of the goods or services and delivery of the

invoice for such goods or services. We identified the following improvement

areas that need to be addressed to prevent/minimize the occurrence of duplicate

payments.

4. Detailed requisitions/POs

Our review revealed that departments regularly set up requisitions or POs as

blanket purchases. When creating a requisition or PO, departments should include

the quantity of items to be purchased and the purchase price per item. We found

that departments input a quantity of one (i.e., one office supplies) and the total

dollar amount. As a result, departments record the receipt as a percentage of the

order rather than the number of items received. Detailed requisitions/POs should

be used when practical for the purchases of services as well as goods. For

example, a PO for alarm monitoring service for one year at $10 per month should

be entered as 12 months of monitoring at $10 each and not as one unit of

monitoring service at $120.00. Blanket POs should be used on an exception basis

(i.e., for Dry Cleaning Services) and not for goods or routine services. Criteria for

the use of blanket POs should be established, documented and communicated to

departmental staff responsible for the input of requisitions.

Requisition or PO items should be created and received in detail to ensure

that:

�� AP is able to accurately match receiving reports with invoices to

ensure that the goods/services billed were actually received.

�� The City collects valuable management information regarding

the quantities of various commodities purchased and the price

16 Audit of the Disbursements Process

Condition Statements and Management Action Plans

per item. Such information is critical to determine whether

annual price agreements should be negotiated or items should be

stocked by the City warehouse. It also facilitates budget

preparation as well as project planning and review.

5. Invoice routing

Thirty-five (35) of the 113 disbursements reviewed were for payment of

invoices sent to the departments rather than to AP. The City’s prompt pay policy

requires that invoices be sent directly to AP whenever possible, and that

departments inform vendors of this requirement. When invoices are not sent

directly to AP:

�� the amount of processing time to make a vendor payment

increases, and

�� the internal control practice of segregating the person receiving

the goods/services from the person receiving the bill may be

violated.

AP, Disbursements and Fleet Management have submitted the following

action plans to ensure that duplicate payments are detected and corrected on a

timely basis.

Objective: To increase compliance with the City’s disbursement cycle internal control processes to prevent duplicate payments to vendors.

Audit of the Disbursements Process 17

Condition Statements and Management Action Plans

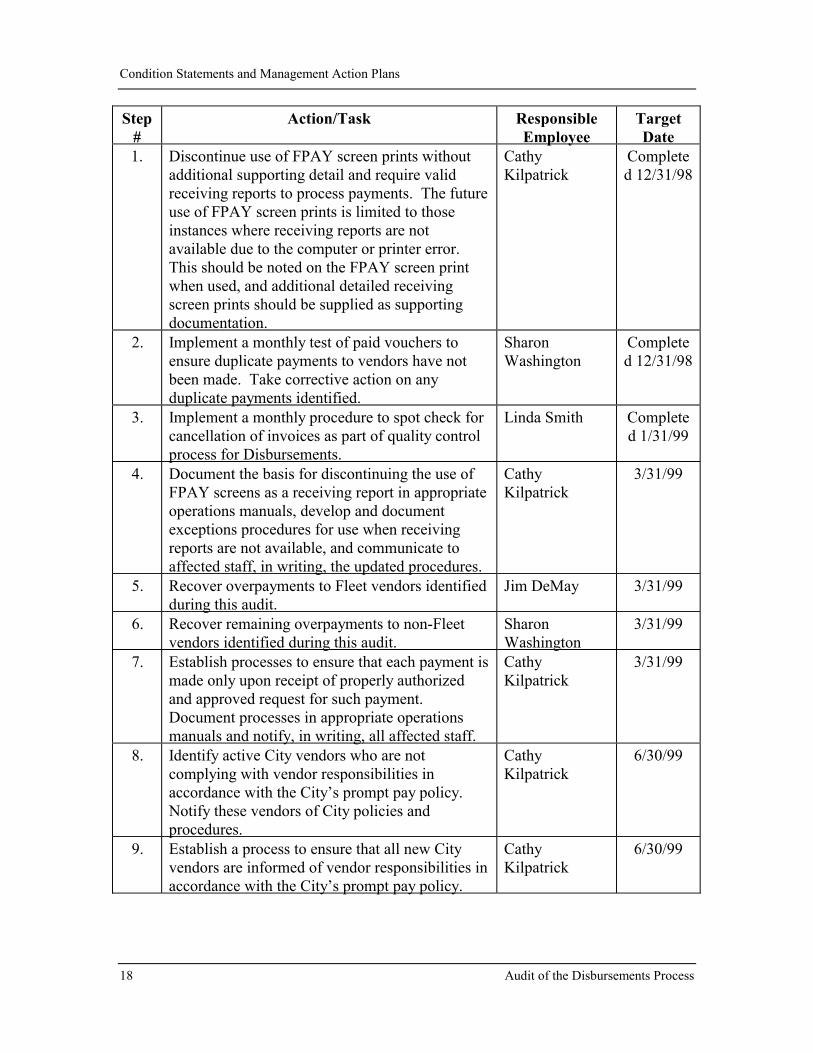

Step #

Action/Task Responsible Employee

Target Date

1. Discontinue use of FPAY screen prints without additional supporting detail and require valid receiving reports to process payments. The future use of FPAY screen prints is limited to those instances where receiving reports are not available due to the computer or printer error. This should be noted on the FPAY screen print when used, and additional detailed receiving screen prints should be supplied as supporting documentation.

Cathy Kilpatrick

Completed 12/31/98

2. Implement a monthly test of paid vouchers to ensure duplicate payments to vendors have not been made. Take corrective action on any duplicate payments identified.

Sharon Washington

Completed 12/31/98

3. Implement a monthly procedure to spot check for cancellation of invoices as part of quality control process for Disbursements.

Linda Smith Completed 1/31/99

4. Document the basis for discontinuing the use of FPAY screens as a receiving report in appropriate operations manuals, develop and document exceptions procedures for use when receiving reports are not available, and communicate to affected staff, in writing, the updated procedures.

Cathy Kilpatrick

3/31/99

5. Recover overpayments to Fleet vendors identified during this audit.

Jim DeMay 3/31/99

6. Recover remaining overpayments to non-Fleet vendors identified during this audit.

Sharon Washington

3/31/99

7. Establish processes to ensure that each payment is made only upon receipt of properly authorized and approved request for such payment. Document processes in appropriate operations manuals and notify, in writing, all affected staff.

Cathy Kilpatrick

3/31/99

8. Identify active City vendors who are not complying with vendor responsibilities in accordance with the City’s prompt pay policy. Notify these vendors of City policies and procedures.

Cathy Kilpatrick

6/30/99

9. Establish a process to ensure that all new City vendors are informed of vendor responsibilities in accordance with the City’s prompt pay policy.

Cathy Kilpatrick

6/30/99

18 Audit of the Disbursements Process

Condition Statements and Management Action Plans

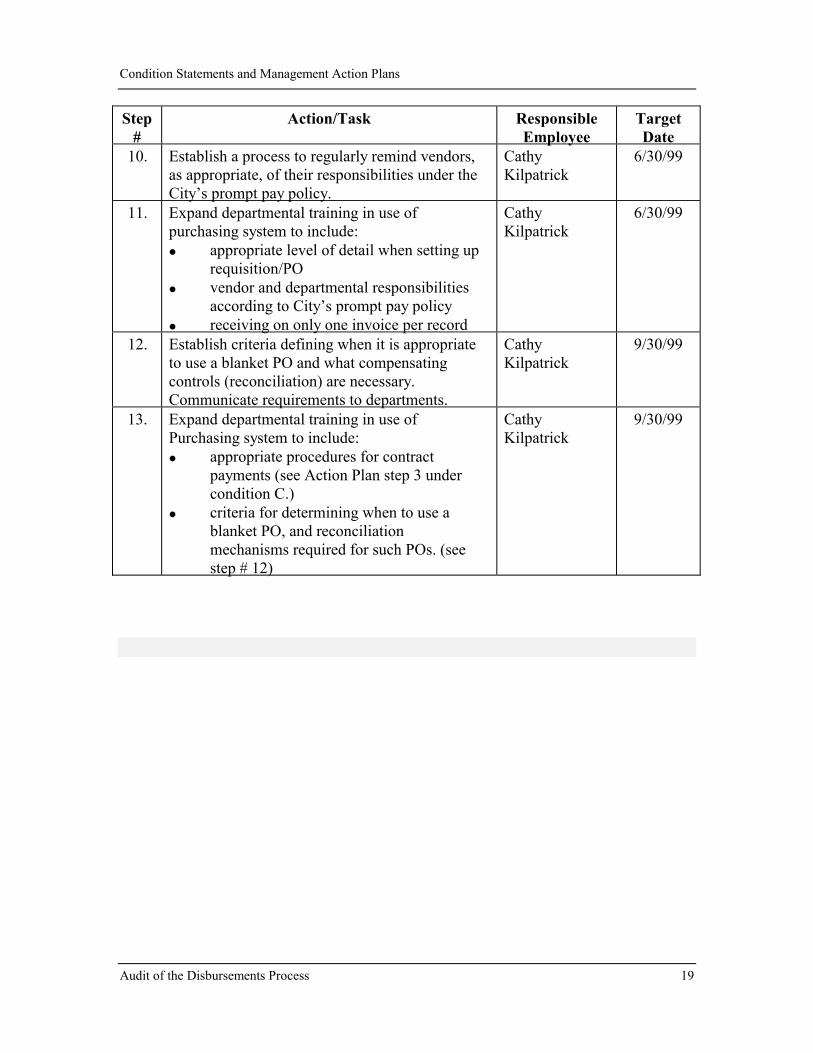

Step Action/Task Responsible Target # Employee Date

10. Establish a process to regularly remind vendors, as appropriate, of their responsibilities under the City’s prompt pay policy.

Cathy Kilpatrick

6/30/99

11. Expand departmental training in use of purchasing system to include: �� appropriate level of detail when setting up

requisition/PO �� vendor and departmental responsibilities

according to City’s prompt pay policy �� receiving on only one invoice per record

Cathy Kilpatrick

6/30/99

12. Establish criteria defining when it is appropriate to use a blanket PO and what compensating controls (reconciliation) are necessary. Communicate requirements to departments.

Cathy Kilpatrick

9/30/99

13. Expand departmental training in use of Purchasing system to include: �� appropriate procedures for contract

payments (see Action Plan step 3 under condition C.)

�� criteria for determining when to use a blanket PO, and reconciliation mechanisms required for such POs. (see step # 12)

Cathy Kilpatrick

9/30/99

Audit of the Disbursements Process 19

Condition Statements and Management Action Plans

B. The City should strengthen internal controls to ensure the integrity of financial reporting.

In addition to the internal controls already discussed, we discovered other

areas that warrant attention. These controls do not prevent duplicate payments but

do benefit the City by improving:

�� the accuracy of financial statements,

�� the accuracy of program area costs, and

�� documentation of the use of City funds.

Accurate and documented financial and program area costs allow

management to better evaluate the effectiveness of programs and to better plan

future programs and expenditures.

1. Proper account coding

Account coding identifies the appropriate fund, cost center, object code and

project against which to record an expenditure. Of the 92 disbursements reviewed,

16 of the purchases were coded incorrectly. The coding on the requisitions/POs

did not properly identify the type of purchase being made. Examples of incorrect

coding include charging:

�� monthly monitoring fees for the security system to unclassified

supplies rather than unclassified contractual services,

�� the purchase of notebooks (binders) and a modem to unclassified

contractual services rather than office supplies,

�� utility bills for water and sewer services to unclassified supplies

rather than utilities, and

20 Audit of the Disbursements Process

Condition Statements and Management Action Plans

�� the purchase of police uniform jackets to unclassified supplies

rather than uniforms and clothing.

Proper account coding (fund, cost center, object code and account) for

transactions allows departments to 1) comply with budgetary controls over the

expenditure of City funds, and 2) ensure the accuracy of financial and management

reports produced from the FMS system.

2. Retention of support for payments

Two of the 32 check requests, totaling $31,652, did not have supporting

documentation in the disbursements file for the expenditure. These included a

check to the Clerk of the Court for child support payments and a check to

Connecticut General Life for life insurance deductions which are both withheld

from employee checks. In each case, the supporting documentation was mailed to

the payee in order for the payee to appropriately apply the payment, and no copy of

this documentation was made because of the bulk (number of pages) of the

documentation. As a result, there is no supporting documentation for the details of

these disbursements in the City’s official disbursement file, and the clerical

accuracy of these checks was not verified.

In those cases where supporting documentation must be sent to the vendor

with the payment, a copy of such documentation should be made or electronically

imaged and kept in the City’s official records to support the disbursement.

DMA and Disbursements have submitted the following action plans to

ensure that expenditures are properly accounted for and that appropriate records

are retained.

Audit of the Disbursements Process 21

Condition Statements and Management Action Plans

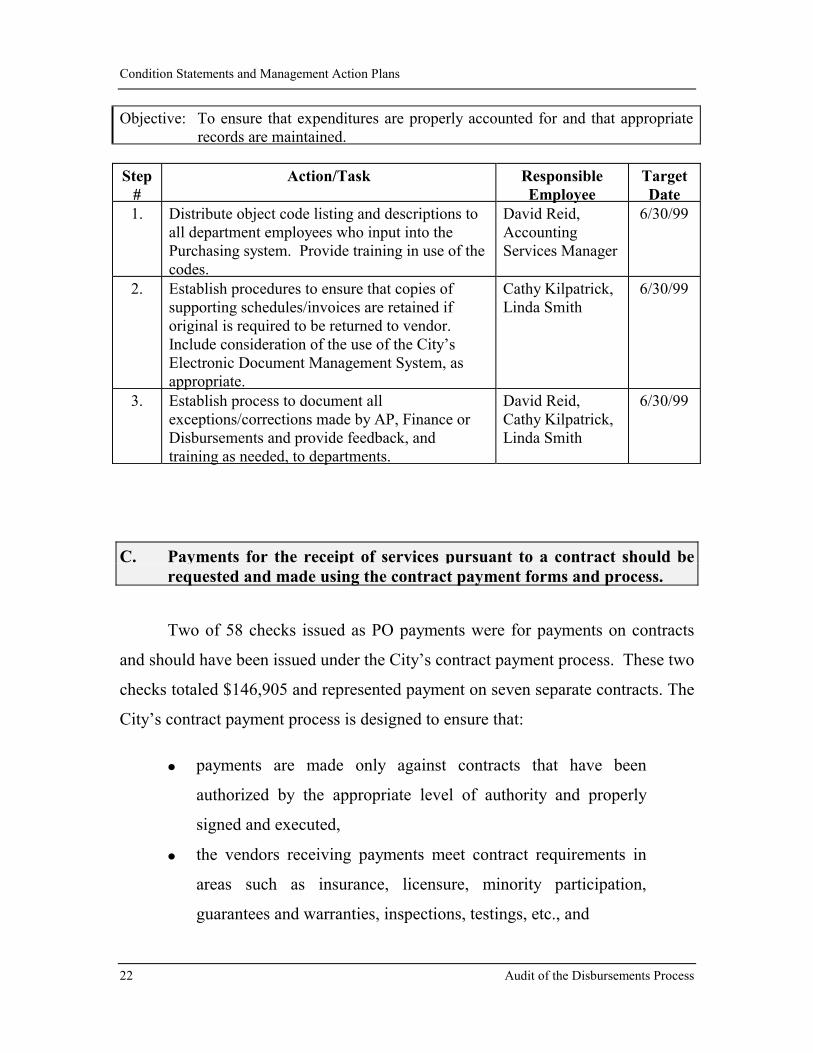

Objective: To ensure that expenditures are properly accounted for and that appropriate records are maintained.

Step

# Action/Task Responsible

Employee Target Date

1. Distribute object code listing and descriptions to all department employees who input into the Purchasing system. Provide training in use of the codes.

David Reid, Accounting Services Manager

6/30/99

2. Establish procedures to ensure that copies of supporting schedules/invoices are retained if original is required to be returned to vendor. Include consideration of the use of the City’s Electronic Document Management System, as appropriate.

Cathy Kilpatrick, Linda Smith

6/30/99

3. Establish process to document all exceptions/corrections made by AP, Finance or Disbursements and provide feedback, and training as needed, to departments.

David Reid, Cathy Kilpatrick, Linda Smith

6/30/99

C. Payments for the receipt of services pursuant to a contract should be requested and made using the contract payment forms and process.

Two of 58 checks issued as PO payments were for payments on contracts

and should have been issued under the City’s contract payment process. These two

checks totaled $146,905 and represented payment on seven separate contracts. The

City’s contract payment process is designed to ensure that:

�� payments are made only against contracts that have been

authorized by the appropriate level of authority and properly

signed and executed,

�� the vendors receiving payments meet contract requirements in

areas such as insurance, licensure, minority participation,

guarantees and warranties, inspections, testings, etc., and

22 Audit of the Disbursements Process

Condition Statements and Management Action Plans

�� payments are made in accordance with contract terms, including

retainage where appropriate.

The contract process also includes controls over contract modifications to

ensure that the scope and nature of the contract will not be changed without

approval of the appropriate authority. This deviation from the contract process

should have been identified and corrected at several steps within the disbursement

cycle by: 1) department management when the services were requested, 2)

Procurement Services when the PO was issued, 3) AP when the invoices were

processed for payment, and 4) Disbursements when the documentation was

reviewed prior to the release of checks.

AP, DMA and Disbursements have submitted the following action plans to

ensure that contract payments are appropriately processed and reviewed.

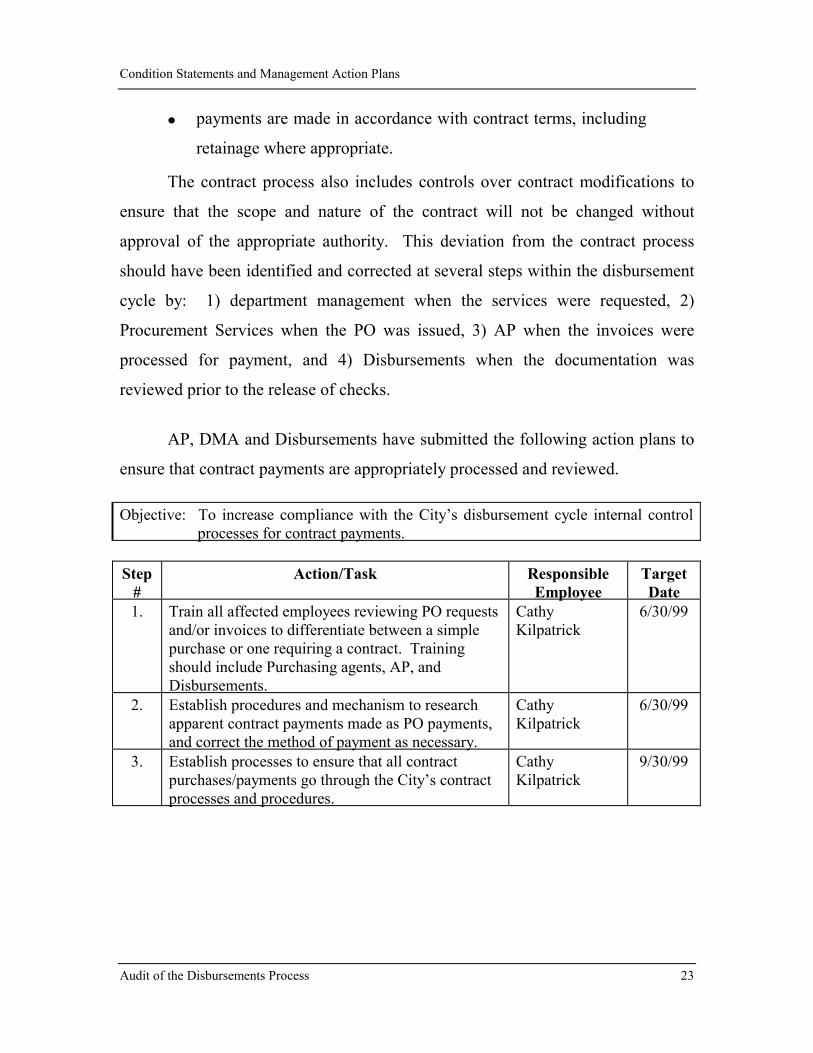

Objective: To increase compliance with the City’s disbursement cycle internal control processes for contract payments.

Step

# Action/Task Responsible

Employee Target Date

1. Train all affected employees reviewing PO requests and/or invoices to differentiate between a simple purchase or one requiring a contract. Training should include Purchasing agents, AP, and Disbursements.

Cathy Kilpatrick

6/30/99

2. Establish procedures and mechanism to research apparent contract payments made as PO payments, and correct the method of payment as necessary.

Cathy Kilpatrick

6/30/99

3. Establish processes to ensure that all contract purchases/payments go through the City’s contract processes and procedures.

Cathy Kilpatrick

9/30/99

Audit of the Disbursements Process 23

Exit Conference

V. EXIT CONFERENCE

An exit conference was held on February 15, 1999. Those attending were:

Department of Management & Administration David C. Reid, Director Dinah R. Hart, Administrative Services Administrator Cathy R. Kilpatrick, Manager for Procurement Services City Treasurer-Clerk’s Office Robert B. Inzer, City Treasurer-Clerk Linda B. Smith, Asset/Liability Administrator City Auditor’s Office Joanne G. Becknell, Acting Senior Auditor Gordon R. Klein, Auditor II

24 Audit of the Disbursements Process