Embed Size (px)

Citation preview

Financial Statements

2010

Contents

Report to partners 1

Report of the independent auditor to the partners of Deloitte LLP 7

Consolidated income statement 8

Consolidated statement of comprehensive income 9

Consolidated balance sheet 10

Consolidated statement of changes in equity 12

Consolidated cash flow statement 13

Notes to the financial statements 14

Financial Statements 1

The Board presents its report to the members and theaudited financial statements of Deloitte LLP for the yearended 31 May 2010. The financial statementsincorporate the financial statements of Deloitte LLP andentities controlled by Deloitte LLP. The financialstatements that will be filed at Companies House willcomprise the consolidated financial statements togetherwith the separate financial statements of Deloitte LLP.

The members of Deloitte LLP are known and referred toby both clients and staff as partners. Throughout thefinancial statements references to partners should betaken as referring to members, as defined by theLimited Liability Partnerships Regulations.

Executive GroupDeloitte’s activities are managed by the Senior Partnerand Chief Executive and the Executive Group, which isappointed by the Senior Partner and Chief Executive.In keeping with our client service focus, members of theExecutive Group are also actively engaged with ourclients.

The members of the Executive Group are:John Connolly, Senior Partner and Chief Executive,Steve Almond, Global, Sabri Challah, CorporateDevelopment, Stuart Counsell, Finance and Legal,Cahal Dowds, Regions and Quality, Martin Eadon,Clients & Industries, Margaret Ewing, Vice Chairman,Heather Hancock, Innovation and Brand, John Kerr,Talent, Vince Niblett, Audit, David Owen, Consulting,Gerry Paisley, Practice Protection, David Sproul, Tax,Richard Buck, Technology, Panos Kakoullis, SuperScale Relationships, Ian McNeil, Partner EdgeProgramme, Tim Mahapatra, Corporate Finance,Richard Punt, Growth and Nick Shepherd, DriversJonas Deloitte.

Senior Partner and Chief ExecutiveJohn Connolly, the Senior Partner and Chief Executive ofDeloitte LLP has full executive authority for themanagement of the firm. The Senior Partner and ChiefExecutive is nominated by the Board of Partners andelected by the partners for a four-year term of office.John Connolly began his third term as Senior Partnerand Chief Executive on 1 June 2007.

The responsibilities of the Senior Partner and ChiefExecutive fall under five principal headings:

• the business of Deloitte, including the developmentand management of services at the highest level ofquality, and compliance with all regulations;

• the development of policies and strategic direction;

• financial performance;

• partners, including the development andmanagement of our talent goals; and

• international, representing the UK firm’s associationwith Deloitte Touche Tohmatsu Limited.

John Connolly is also the Chairman of the Board ofDirectors of Deloitte Touche Tohmatsu Limited (DTTL),the international organisation of which Deloitte LLP isa member. In this separate role, he is able to helpenhance quality throughout the network of memberfirms and, to share within the network the collectiveexpertise and experience of client service, talentdevelopment and quality and risk management.The international network has a separate ChiefExecutive Officer, Jim Quigley.

Board of PartnersThe Board of Partners is responsible for the promotionand protection of partner interests and for the oversightof the Executive Group. It approves Deloitte’s long-termstrategies and has specific oversight of risk.

As with the Senior Partner and Chief Executive, theChairman is nominated by the Board and elected bythe partners and serves for a four-year term of office.David Cruickshank commenced his first term of officeas Chairman on 1 June 2007. The separation of theroles of the Chairman and the Senior Partner and ChiefExecutive provides a strong measure of accountabilityfor the Executive team.

The current Board comprises:David Cruickshank, Chairman, John Connolly, SeniorPartner and Chief Executive, Steve Almond, MartinEadon, Vince Niblett, David Owen, David Sproul, DavidBarnes, John Cullinane, Richard Edwards, JohnFotheringham, Humphry Hatton, Ellie Patsalos, ChrisPowell, Ian Steele, Geoff Taylor and Denis Woulfe.

Report to partners

2

Principal activityThe principal activity of Deloitte is the provision ofAudit, Tax, Consulting and Corporate Finance services inthe United Kingdom. In addition, professional servicesare provided in Switzerland and the Middle East bysubsidiary entities.

StrategyDeloitte’s strategy is to be the pre-eminent professionalservices firm for clients and talent, reflected in superiorgrowth and performance compared to market. Otherelements of our strategy include:

• a broader and deeper range of capability than ourcompetitors; delivered to clients through integratedand innovative solutions;

• a focus on exceptional quality and a passion for clientservice;

• an environment where our people can develop andexcel; and

• a global mindset and culture that emphasises teamingand high performance.

StructureDeloitte LLP is incorporated as a Limited LiabilityPartnership under the Limited Liability Partnerships Act2000 and is wholly owned by its partners. The principalsubsidiary undertakings of Deloitte LLP are set out innote 23.

These financial statements are the accounts of DeloitteLLP and reflect the results for the year ended 31 May2010. The financial statements consolidate the accountsof Deloitte LLP and all its subsidiary undertakings (the‘group’), drawn up to 31 May each year.

Designated membersThe designated members (as defined in the LimitedLiability Partnerships Act 2000) during the year were:John Connolly, Steve Almond, Martin Eadon, GerryPaisley, David Sproul and Bob Warburton. Aidan Birkett,Stuart Counsell, David Cruickshank, Vince Niblett andDavid Owen were appointed on 1 August 2009.Bob Warburton retired on 30 September 2009 andAidan Birkett retired on 31 March 2010. All thedesignated members, except David Cruickshank, servedas members of the Deloitte LLP Executive Group, themost senior management committee.

Business performance and outlookWe have achieved a strong performance in a toughenvironment. Our revenues were £1,953 million, just£16 million below prior year. The profit for the financialyear distributable to partners was £590 million against£601 million in the prior year. The average profit earnedby each partner in the year, after providing for annuitiespayable to retired partners, was £873,000 comparedwith £883,000 in the prior year.

Each of our business divisions performed strongly intheir markets.

AuditRevenue in Audit was 2.9% below the prior year.We continued to build our market share and significantaudit wins in the year included FTSE100 companiesKingfisher plc and Essar plc. The Financial Servicespractice delivered strong growth driven by our AdvisoryPractice and Risk and Regulation Services.

Whilst the economic environment will remain fragile,we anticipate a return to revenue growth in 2011 inpart fuelled by our strongly positioned Financial Servicespractice, a return to growth in core audit and strongprospects in Switzerland and our Information andTechnology Risk Services business.

TaxTax achieved a market leading performancenotwithstanding a decline of 2.3% in revenue. We areseeing a pickup in transaction volumes across theCorporate, Private Equity and Real Estate areas and thiscontributed to a markedly stronger performance in thesecond half of the year. We had particularly goodperformances in Financial Services, UK Corporates andour Switzerland practice. The continued focus by bothtax payers and revenue authorities on tax risk andgovernance also led to a growth in activity across allareas.

In 2011 we expect a return to growth with a number ofbusinesses seeing significant growth opportunities asthe economy recovers. Deloitte Tax was recognised atthe LexisNexis Taxation Awards 2010, bolstering ourmarket standing and underpinning our confidence ingrowing the business in the year ahead.

Report to partners

Financial Statements 3

ConsultingRevenue in Consulting declined by 4% but in thecontext of the curtailment of discretionary spend inboth the public and private sectors, this was a veryrobust performance. The impact of the recession wasfelt most keenly in the first half of the financial year.In the second half, business activity showed a significantupturn, especially in Financial Services. There was goodgrowth in the Manufacturing sector and we hadsignificant new engagements with clients in theTechnology and Media industries. Enterprise CostReduction was again one of the most sought afterservice offerings across all market sectors. Of greateremphasis this year was supporting clients with risk andregulation, particularly in relation to Solvency IIlegislation.

In the year ahead, we anticipate growth opportunitiesacross most market sectors but with a very challengingmarket in our Government and Public Sector practice,although we will continue to present innovative ideasand opportunities to government departmentsconsistent with their agendas.

Corporate FinanceRevenue in Corporate Finance grew by 10.6% in theyear, despite the continuing sluggishness in somemarkets. The Reorganisation Services business hadanother very strong year building upon the prior yearsuccesses. We recorded good growth in our AdvisoryGroup, in our Swiss practice and also in our Middle EastJoint Venture. The newly created Drivers Jonas Deloittecommenced in March and added a new stream ofrevenues in Real Estate Advisory. We continued toacquire a series of high profile assignments in ourForensic and Dispute Services business.

Our role supporting the restructuring of Dubai Worldwas a landmark engagement. Other majorengagements in the year included our TransactionServices Group acting on the first major acquisition of aglobal consumer brand by a Chinese corporation; ourrole supporting the Landsbanki Winding Up Board andResolution Committee in Iceland and our SpecialistFinance Group advising on four of the five major NHSPFI projects.

Revenue (£m)

0

500

1,000

1,500

2,000

2,500

20062007200820092010

Service line revenue

32%

26%

24%

18%

Audit

Tax

Consulting

Corporate Finance

We are approaching 2011 with confidence. Theforthcoming changes in the regulatory environment andlarge scale transformations in the Financial Services andPublic Sectors will offer opportunities for our business.Whilst spending cuts will mean a significant curb onnew projects, there will be opportunities as the PublicSector seeks to restructure how public services aredelivered. We also anticipate an improvement in thedebt market will lead to more deal activity in thesecond half of the year.

4

PeopleStaff costs at £750m were 4% lower, reflecting thedecline in average headcount during the year.

Assets and liabilitiesTotal assets are £874m. The negative partners’ interestsof £20m arises as a result of partners’ distributable profitbeing determined by reference to the firm’s equityaccounts which are based on different accountingpolicies to the group accounts, which are prepared underInternational Financial Reporting Standards (IFRS).The most significant difference is the provision of retiredpartner annuities of £373m. The liability is conditional onthe future generation of profits and is payable over anumber of years with £62m payable between 10 and15 years and £133m payable after 15 years.

Provisions include the net present value of annuitiespayable to current partners of £320m. Payment ofthese annuities is also conditional on the futuregeneration of profits within the group.

Cash flowProfit after tax and working capital movementsgenerated a positive operating cash flow for the year of£601m.

The main treasury risks relate to interest, liquidity andcurrency. The primary currency is sterling but certainexpenses and charges from overseas offices aredenominated in other currencies. Some fees arerendered in other currencies and the foreign subsidiaryundertakings have functional currencies different fromthat of the group. The volume and timing of currencyinflows and outflows provide a natural hedge andDeloitte does not undertake formal hedgingtransactions. Complex financial instruments are notused and speculative activity is not undertaken.

Finance and capital structureAt the balance sheet date fixed capital amounted to£127m or £188,000 per partner. Profit distributable topartners is determined by the firm’s equity accountswhich are based on accounting policies which differfrom IFRS. The principal differences relate to theaccounting treatment of annuities and defined benefitpension schemes. The distributable profit for the yearbased on the equity accounts was £590m, the balanceof which will, in accordance with the currentdistribution policy, be released to partners in the 12-month period following the year end.The balance of Deloitte’s funding is provided by bankfacilities. We continue to maintain a significant level of

committed undrawn facilities to enable us to respondrapidly to opportunities and to fund initiatives withoutthe need for specific financing.

Partners’ drawings and capitalAll partners are equity partners and share in the profitsand subscribe the entire capital of Deloitte LLP. Eachpartner’s capital subscription is linked to his or her shareof profit and is repaid in full on ceasing to be a partner.The rate of capital subscription is determined from timeto time depending upon the financing requirements ofthe business.

Partners draw a proportion of their profit share in12 monthly on account instalments during the year inwhich the profit is made, with the balance of theirprofits, net of tax retention, paid in instalments in thesubsequent year. All payments are made subject to thecash requirements of the business. Tax retentions arepaid to HM Revenue & Customs on behalf of partnerswith any excess being released to partners asappropriate.

Partners’ profit sharingPartners share profits based upon a comprehensiveevaluation of their individual contribution to theachievement of the group’s strategic objectives.

Partners are assigned to an equity group, which isreviewed annually and which describes the attributes,skills and broad performance expected of them. Eachequity group carries a wide band of profit sharing unitsso that relative contributions can be recognised.

Seven key criteria are used for assessing theperformance and contribution of each partner to thesuccess of Deloitte. These are:

• QualityEach partner must be a role model for quality in theirprofessional work.

• TalentContribution to mentoring, leading, recruitment,engagement, development and training our people.

• ClientsClient portfolio managed and roles carried out.

Report to partners

Financial Statements 5

• Brand and EminenceMarket-related activity including regulatory relations,thought leadership, innovation and brand protectionroles.

• Revenue Generation, Growth, Business BuildingContribution to business development building andrelationship building.

• Financial SuccessOverall contribution to the financial success ofDeloitte.

• Leadership and ManagementContribution to the group’s broad success throughleadership and management roles.

Partners within all equity groups are expected to beambassadors for Deloitte LLP externally and leaders byexample to all of our employees in everything they do.Certain attributes transcend all equity groups. Theseare:

• unassailable integrity;

• quality service to our clients;

• the highest levels of technical excellence;

• development of people;

• compliance with the group’s policies and standardsand external regulatory requirements; and

• high quality management of risk.

Partners who provide audit services are expected to beresponsive to their clients’ service needs, but they arenot evaluated or remunerated on the selling of otherservices to their audit clients.

Partner performance is evaluated in all designatedcompetencies, beginning with the Board’s approval ofthe profit sharing strategy proposed by the SeniorPartner and Chief Executive and concluding with theBoard’s review of the recommended profit allocationand equity group going forward for each individualpartner, the conclusions of which are disclosed in full toall partners. A committee of partners is tasked withoverseeing the management process to ensureconsistent and equitable treatment.

Creditor payment policyDeloitte’s policy is to settle terms of payment withsuppliers when agreeing the terms of each transaction,ensure suppliers are made aware of the terms ofpayment and abide by the terms of payment.

Trade creditors of the group at 31 May 2010 wereequivalent to 18 days’ (2009: 16 days’) purchases,based on the average daily amount invoiced bysuppliers during the year.

Political donationsIt is Deloitte’s policy not to give cash contributions toany political party or other groups with a politicalagenda. However, we do seek to develop and maintainconstructive and balanced relationships with politicalparties and may make available partner, staff andadvisor resources, and technical and factual informationon occasion.

Disclosures on such matters for companies are coveredby the Political Parties, Elections and Referendums Act.Although the scope of this Act does not cover LimitedLiability Partnerships, we regard it as appropriate todisclose equivalent details. For the period ended31 May 2010 Deloitte donated £399,057 to theConservative Party and £13,500 to the Labour Partythrough the provision of staff and advisor resources.

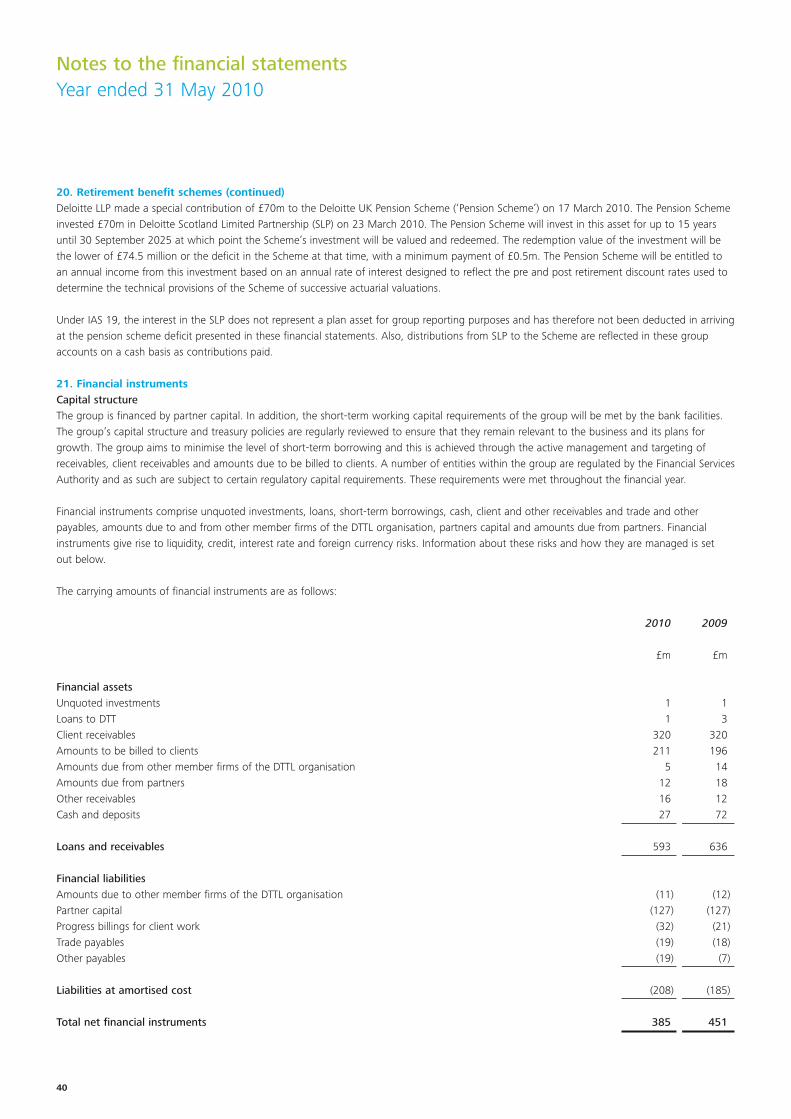

Going concernThe financial position of the group, its cash flows andliquidity position are described above. In addition note21 of the financial statements provides details of theborrowing facilities and includes the group’s objectives,policies and processes for managing its capital; itsfinancial risk management objectives; details of itsfinancial instruments; and its exposures to credit riskand liquidity risk.

The group has considerable financial resources,including net cash of £27m and £400m of undrawncommitted facilities. £100m is a 3 year facility whichexpires in August 2013. £300m is due to expirebetween 30 September 2010 and 31 July 2011.The group has a strong focus on working capitalmanagement and forecasts indicate that it is notdependent upon the renewal of facilities which are duefor renewal within the next 12 months. In addition, wehave a broad client base across each of our service linesand industry offerings. The Board believes that thegroup is well placed to manage its business riskssuccessfully.

6

The Board, following a review of its profit and cashflow plans, has concluded, at the time of approving thefinancial statements, that the parent partnership andthe group have adequate resources to continue inoperational existence for the foreseeable future.Accordingly, they continue to adopt the going concernbasis in preparing the financial statements.

Statement of partners’ responsibilities in respectof the financial statementsThe partners are responsible for preparing the financialstatements in accordance with applicable law andregulations.

The Limited Liability Partnerships (Accounts and Audit)(Application of Companies Act 2006) Regulations 2008,made under the Limited Liability Partnerships Act 2000require the partners to prepare financial statements foreach year. Under that law the partners have elected toprepare the financial statements in accordance withIFRS as adopted by the European Union. The financialstatements are also required by law to be properlyprepared in accordance with the Companies Act 2006,as applicable to limited liability partnerships.

International Accounting Standard 1 requires thatfinancial statements present fairly for each financial yearthe firm’s financial position, financial performance andcash flows. This requires the fair presentation of theeffects of transactions and other events and conditions,in accordance with the definitions and recognitionscriteria for assets, liabilities, income and expenses setout in the International Accounting Standards Board’s‘Framework for the preparation and presentation offinancial statements’. In virtually all circumstances, a fairpresentation will be achieved by compliance with allapplicable IFRS. However, partners are also required to:

• properly select and apply accounting policies;

• present information, including accounting policies, ina manner that provides relevant, reliable, comparableand understandable information; and

• provide additional disclosures when compliance withthe specific requirements in IFRS are insufficient toenable users to understand the impact of particulartransactions, other events and conditions on theentity’s financial position and financial performance.

The partners are responsible for keeping adequateaccounting records that disclose with reasonableaccuracy at any time the financial position of the firmand enable them to ensure that the financial statementscomply with the Companies Act 2006, as applicable tolimited liability partnerships. They are also responsiblefor safeguarding the assets of the firm and hence fortaking reasonable steps for the prevention anddetection of fraud and other irregularities.

The partners are responsible for the maintenance andintegrity of the corporate and financial informationincluded on the firm’s website. Legislation in the UnitedKingdom governing the preparation and disseminationof financial statements may differ from legislation inother jurisdictions.

AuditorGrant Thornton UK LLP will be proposed forreappointment.

Approved by the Board andsigned on behalf of the Board

John ConnollySenior Partner and Chief Executive23 August 2010

Report to partners

Financial Statements 7

We have audited the group financial statements ofDeloitte LLP for the year ended 31 May 2010 whichcomprise the consolidated income statement, theconsolidated statement of comprehensive income, theconsolidated balance sheet, the consolidated statementof changes in equity, the consolidated cash flowstatement, the principal accounting policies and notes1 to 23. These financial statements have been preparedunder the accounting policies set out therein.

We have reported separately on the parent partnershipfinancial statements of Deloitte LLP for the year ended31 May 2010.

This report is made solely to the partners, as a body, inaccordance with Chapter 3 of Part 16 of the CompaniesAct 2006 as applied by the Limited Liability Partnerships(Accounts and Audit ) (Application of Companies Act2006) Regulations 2008. Our audit work has beenundertaken so that we might state to the partnersthose matters we are required to state to them in anauditor's report and for no other purpose. To the fullestextent permitted by law, we do not accept or assumeresponsibility to anyone other than the partnership andthe partners as a body, for our audit work, for thisreport, or for the opinions we have formed.

Respective responsibilities of partners andauditorThe partners' responsibilities for preparing the Report toPartners and the financial statements in accordancewith International Financial Reporting Standards (IFRS)as adopted by the European Union are set out in theStatement of partners' responsibilities.

Our responsibility is to audit the financial statements inaccordance with relevant legal and regulatoryrequirements and International Standards on Auditing(UK and Ireland). It is our responsibility to form anindependent opinion based on our examination, and toreport our opinion to you.

In addition, we report to you if, in our opinion, DeloitteLLP has not kept proper accounting records; or returnsadequate for our audit have not been received frombranches not visited by us; or the financial statementsare not in agreement with the accounting records andreturns; or if we have not received all the informationand explanations we require for our audit.

We read other information contained in the Report toPartners and consider whether it is consistent with theaudited financial statements.

This other information comprises only the Report toPartners. We consider the implications for our report ifwe become aware of any apparent misstatements ormaterial inconsistencies with the group financialstatements.

Basis of audit opinionWe conducted our audit in accordance with InternationalStandards on Auditing (UK and Ireland) issued by theAuditing Practices Board. An audit includes examination,on a test basis, of evidence relevant to the amounts anddisclosures in the group financial statements. It alsoincludes an assessment of the significant estimates andjudgements made by the partners in the preparation ofthe group financial statements, and of whether theaccounting policies are appropriate to the group'scircumstances, consistently applied and adequatelydisclosed.

We planned and performed our audit so as to obtain allthe information and explanations which we considerednecessary in order to provide us with sufficient evidenceto give reasonable assurance that the financial statementsare free from material misstatement, whether caused byfraud or other irregularity or error. In forming our opinionwe also evaluated the overall adequacy of thepresentation of information in the group financialstatements.

OpinionIn our opinion the group financial statements:

• give a true and fair view of the group’s affairs as at31 May 2010 and of its profit for the year thenended;

• have been properly prepared in accordance with IFRSas adopted by the European Union; and

• have been prepared in accordance with the CompaniesAct 2006 as applied by the Limited Liability Partnerships(Accounts and Audit) (Application of Companies Act2006) Regulations 2008.

Stephen MaslinSenior Statutory Auditor for and on behalf ofGrant Thornton UK LLPStatutory AuditorChartered Accountants

London23 August 2010

Report of the independent auditor to the partners of Deloitte LLP

Consolidated income statementYear ended 31 May 2010

Note £m £m

Revenue 3 1,953 1,969

Operating expensesExpenses and disbursements on client assignments (277) (254)Staff costs 4 (750) (781)Depreciation and amortisation (41) (41)Other operating expenses (292) (312)

Profit from operations 5 593 581

Other income 17 23 –Finance income 6 30 41Finance cost 6 (103) (58)

Profit before tax 543 564

Tax 7 1 (2)

Profit for the year before provision for annuities and remuneration for current partners 544 562

Provision for annuities and remuneration for current partners 8 (128) (36)

Profit for the financial year 16 416 526

Reconciliation with the firm’s equity accounts

Profit for the financial year based on the firm’s equity accounts 615 631

Retired partner annuities and other adjustments (25) (30)

Profit for the financial year distributable to partners 590 601

Adjustments for IFRS not adopted in the firm’s equity accounts (174) (75)

Profit for the financial year 416 526

The profit distributable to partners is determined in accordance with accounting policies which differ from IFRS. The principal differences relate tothe accounting treatment of annuities and defined benefit pension schemes.

8

2010 2009

Consolidated statement of comprehensive incomeYear ended 31 May 2010

£m £m

Profit for the financial year 416 526

Other comprehensive income and expenseActuarial losses on defined benefit pension schemes (14) (183)Exchange differences on translation of foreign operations – 1

Other comprehensive expense for the year, net of tax (14) (182)

Total comprehensive income for the year, attributable to partners as owners of the parent entity 402 344

Financial Statements 9

2010 2009

Consolidated balance sheetAs at 31 May 2010

Note £m £m

Assets

Non-current assetsProperty, plant and equipment 9 206 221Intangible assets 10 43 10Financial assets 11 2 4

251 235

Current assetsClient and other receivables 12 596 587Cash and cash equivalents 27 72

623 659

Total assets 874 894

Liabilities

Current liabilities Trade and other payables 13 225 185Provisions 14 30 29Partner capital 16 3 10

258 224

Non-current liabilitiesRetirement benefit obligation 20 249 234Deferred tax 15 1 2Provisions 14 697 558Partner capital 16 124 117

1,071 911

EquityPartners’ other reserves 16 (455) (241)

Total liabilities and equity 874 894

10

2010 2009

Consolidated balance sheetAs at 31 May 2010

Partners’ interests Note £m £m

The following balances relating to partners are included in the consolidated balance sheet:Partners’ capital 16 127 127Amounts due from partners 16 (12) (18)Provision for current partner annuities 16 320 239Partners’ other reserves – current partners (82) 73

Partners’ interests for current partners 353 421

Provision for partner annuities for retired partners 14 (373) (314)

Total partners’ interests including provision for retired partners which is dependent on future generation of profits (20) 107

The financial statements on pages 8 to 44 were approved by the Board on 23 August 2010.Signed on behalf of the Board,

John Connolly Stuart Counsell

Financial Statements 11

2010 2009

Consolidated statement of changes in equityYear ended 31 May 2010

£m £m

Partners’ other reserves at the start of the year (241) 60

Profit for the year 416 526Actuarial losses on defined benefit pension schemes (14) (183)Exchange differences on translation of foreign operations – 1

Total comprehensive income 402 344

Profits allocated to partners during the year (601) (641)Other transactions with partners (15) (4)

Partners’ other reserves at the end of the year (455) (241)

12

2010 2009

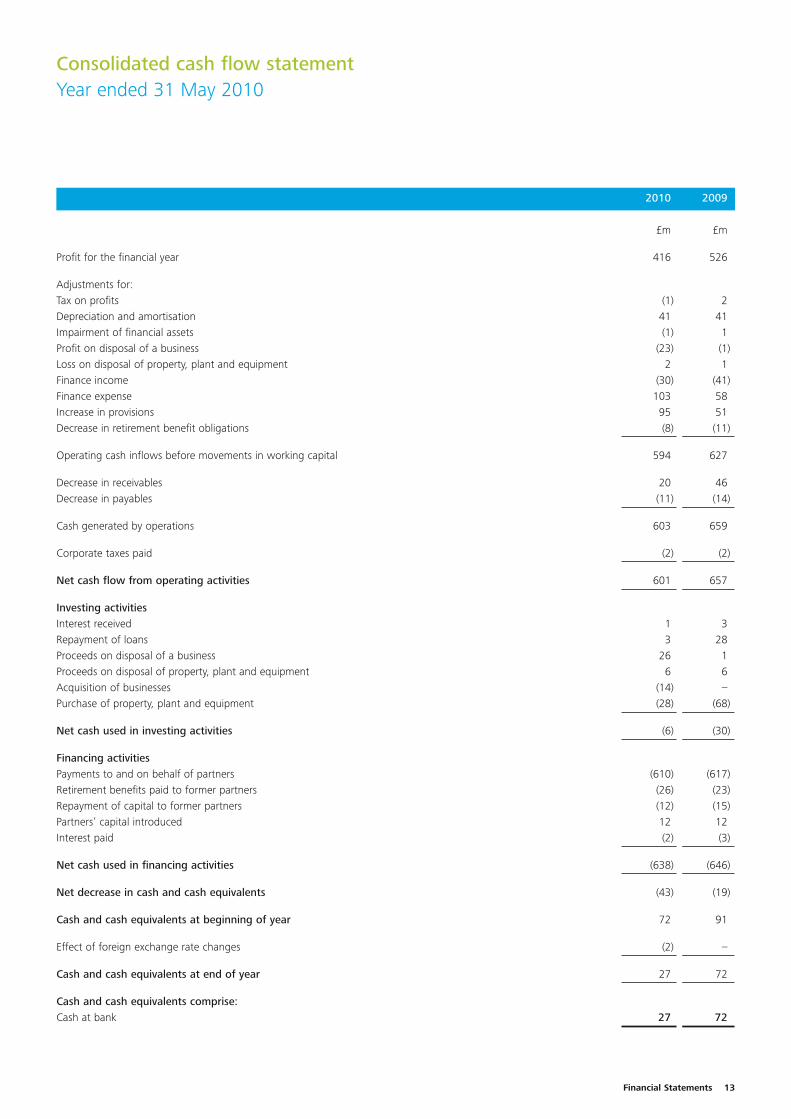

Consolidated cash flow statementYear ended 31 May 2010

£m £m

Profit for the financial year 416 526

Adjustments for:Tax on profits (1) 2Depreciation and amortisation 41 41Impairment of financial assets (1) 1Profit on disposal of a business (23) (1)Loss on disposal of property, plant and equipment 2 1Finance income (30) (41)Finance expense 103 58Increase in provisions 95 51Decrease in retirement benefit obligations (8) (11)

Operating cash inflows before movements in working capital 594 627

Decrease in receivables 20 46Decrease in payables (11) (14)

Cash generated by operations 603 659

Corporate taxes paid (2) (2)

Net cash flow from operating activities 601 657

Investing activitiesInterest received 1 3Repayment of loans 3 28Proceeds on disposal of a business 26 1Proceeds on disposal of property, plant and equipment 6 6Acquisition of businesses (14) –Purchase of property, plant and equipment (28) (68)

Net cash used in investing activities (6) (30)

Financing activitiesPayments to and on behalf of partners (610) (617)Retirement benefits paid to former partners (26) (23)Repayment of capital to former partners (12) (15)Partners’ capital introduced 12 12Interest paid (2) (3)

Net cash used in financing activities (638) (646)

Net decrease in cash and cash equivalents (43) (19)

Cash and cash equivalents at beginning of year 72 91

Effect of foreign exchange rate changes (2) –

Cash and cash equivalents at end of year 27 72

Cash and cash equivalents comprise:Cash at bank 27 72

Financial Statements 13

2010 2009

14

1. Accounting policiesThe principal accounting policies adopted in thepreparation of these financial statements are set outbelow. These policies, except as noted below, havebeen consistently applied throughout the year and thepreceding year.

Basis of accountingThe financial statements have been prepared inaccordance with International Financial ReportingStandards (IFRS) as adopted by the European Union (EU).

In these financial statements the following Standardsand related amendments and Interpretations topublished Standards are reflected for the first time:

IFRS 8 ‘Operating Segments’ requires the use of a‘management approach’ to segment reporting, underwhich information is presented on the same basis asthat used for internal reporting purposes.

Revision to IAS 1 ‘Presentation of Financial Statements:Revised 2007’ which has had an impact on thepresentation of the group’s primary financial statementsbut has had no other impact.

IAS 1 requires a third comparative to be included withinthe Consolidated Balance Sheet (along withsupplementary notes) in the instance that any previouslyreported financial information is restated orrepresented. In the current year the adoption of IFRS 8triggers this requirement. However, the Board concludedthat the additional information provided would not bematerial to the users of the consolidated financialstatements and would not enhance the overall clarity ofthe consolidated financial statements as thecomparative numbers have not changed, except forwithin Note 3.

Revision to IFRS 3 ‘Business Combinations’ whichcontinues to apply the acquisition method to businesscombinations but with some significant changes to theaccounting treatment of the consideration and therelated costs in respect of acquisitions. The group hasvoluntarily adopted IFRS 3 (2008) Revised, which ismandatory for financial years beginning on or after1 July 2009.

The changes to the revised Standard require that allpayments to purchase a subsidiary are recorded at fairvalue at the acquisition date and that all acquisition-related costs are expensed.

Revision to IAS 27 ‘Consolidated and Separate Financialstatements’ which requires the effects of all transactionswith non-controlling interests to be recorded in equitywhere there is no change in control.

A number of new amendments and interpretationshave been endorsed by the EU as part of adopted IFRS,but are not yet effective. None of these amendments isexpected to have a significant impact on the group’sfinancial statements.

The financial statements have been prepared on thehistorical cost basis, except for the revaluation ofcertain financial assets.

ConsolidationThe consolidated financial statements incorporate thefinancial statements of Deloitte LLP and entitiescontrolled by Deloitte LLP (its subsidiaries) made up to31 May each year.

Control is achieved where Deloitte LLP has the power togovern the financial and operating policies of aninvestee entity so as to obtain benefits from itsactivities.

The results of subsidiaries acquired or disposed ofduring the year are included in the consolidated incomestatement from the effective date of acquisition or upto the effective date of disposal, as appropriate.

Where necessary, adjustments are made to the financialstatements of subsidiaries to bring the accountingpolicies used into line with those used by the group.

All intra-group transactions, balances, income andexpenses are eliminated on consolidation.

Going ConcernThe Board has, at the time of approving the financialstatements, a reasonable expectation that Deloitte LLPhas adequate resources to continue in operationalexistence for the foreseeable future. Thus it continuesto adopt the going concern basis of accounting inpreparing the financial statements. Further detail iscontained in the Report to partners on page 5.

Notes to the financial statementsYear ended 31 May 2010

Financial Statements 15

1. Accounting policies (continued)Business CombinationsThe acquisition of subsidiaries is accounted for using theacquisition method. The cost of the acquisition ismeasured as the aggregate of the fair values, at the dateof exchange, of assets given and liabilities incurred orassumed by the group in exchange for control of theacquiree. The acquiree’s identifiable assets, liabilitiesand contingent liabilities that meet the conditions forrecognition under IFRS 3 are recognised at their fairvalue at the acquisition date. Goodwill is recognisedwhere the cost of the business combination exceeds thetotal of these fair values. Where the excess is positive, itis treated as an intangible asset, subject to an annualimpairment review. Where the excess is negative it isrecognised immediately in the income statement.

RevenueRevenue represents amounts chargeable to clients forprofessional services provided during the year includingrecoverable expenses on client assignments butexcluding Value Added Tax.

Services provided to clients, which at the balance sheetdate have not been billed to clients, are recognised asrevenue.

Revenue recognised in this manner is based on anassessment of the fair value of the services provided atthe balance sheet date as a proportion of the totalvalue of the engagement. Revenue is only recognisedwhere the group has a contractual right to receiveconsideration for work undertaken and no revenue isrecognised on contingent engagements until thecontingent event crystallises.

Provision is made against unbilled amounts on thoseengagements where the right to receive payment iscontingent on factors outside the control of the group.Unbilled revenue is included in client and otherreceivables.

LeasesLeases are classified as finance leases whenever theterms of the lease transfer substantially all the risks andrewards of ownership to the lessee. All other leases areclassified as operating leases.

Rentals payable under operating leases are charged toincome on a straight-line basis over the term of therelevant lease.

Benefits received and receivable as an incentive to enterinto an operating lease are also spread on a straight-linebasis over the lease term or to the first break clausewhere applicable.

Foreign currenciesTransactions denominated in foreign currencies arerecorded at the rate of exchange ruling at the date ofthe transaction. Monetary assets and liabilitiesdenominated in foreign currencies at the balance sheetdate are retranslated to the relevant functional currencyat the rates ruling at that date. These translationdifferences are dealt with in the income statement.

The individual financial statements of each groupcompany are presented in the currency of the primaryeconomic environment in which it operates (itsfunctional currency). For the purpose of theconsolidated financial statements, the results andfinancial position of each group company are expressedin pounds sterling, which is the functional currency ofDeloitte LLP, and the presentational currency for theconsolidated financial statements.

The assets and liabilities of the group’s foreignoperations are translated at exchange rates prevailingon the balance sheet date. Income and expense itemsare translated at the average exchange rates for theperiod, unless exchange rates fluctuate significantlyduring that period, in which case the exchange rates atthe date of transactions are used. Exchange differencesarising on the retranslation of the foreign operations, ifany, are classified as equity and transferred to thegroup’s other reserves.

TaxationThe taxation payable on profits of the Limited LiabilityPartnership is the personal liability of the partners and isnot dealt with in these financial statements. A retentionfrom profit distributions is made to fund the taxationpayments on behalf of partners. The tax expenserepresents the sum of the current and deferred taxrelating to the corporate subsidiaries. The current taxexpense is based on taxable profits of these companies.Taxable profit excludes items of income or expense thatare taxable or deductible in other years and it furtherexcludes items that are never taxable or deductible.The group’s liability for current tax is calculated usingtax rates that have been enacted or substantivelyenacted by the balance sheet date.

16

1. Accounting policies (continued)Deferred tax in the subsidiaries is generally recognised,using the liability method, in respect of temporarydifferences at the balance sheet date between thecarrying amounts of assets and liabilities for financialreporting purposes and the corresponding tax bases.Deferred tax is measured at the tax rates enacted orsubstantively enacted at the balance sheet date andwhich are expected to apply in the periods in which thetemporary differences reverse. Deferred tax assets arerecognised to the extent that it is probable that taxableprofits will be available against which deductibletemporary differences can be utilised.

Property, plant and equipmentProperty, plant and equipment is stated at cost lessaccumulated depreciation and any impairment loss.The gain or loss arising on the disposal of an asset isdetermined as the difference between the sale proceedsand the carrying amount of the asset and is recognisedin income.

Depreciation is provided to write off the cost less theestimated residual value of property, plant andequipment by equal instalments over the estimateduseful economic lives as follows:

Leasehold improvements: Period of leaseFixtures and fittings: 5-10 yearsComputer equipment: 3-5 yearsMotor vehicles: 4 years

The residual value, if not insignificant, is reassessedannually in addition to useful lives.

Intangible assetsIntangible assets are recognised only if all of thefollowing conditions are met:

• an asset is created that can be identified;

• it is probable that the asset created will generatefuture economic benefits; and

• the development cost of the asset can be measuredreliably.

The direct cost of staff in the development of computersystems for the group has been capitalised as anintangible asset and is being amortised on a straight-line basis over a period of 10 years. Where no internallygenerated intangible asset can be recognised,development expenditure is recognised as an expense inthe period in which it is incurred.

Intangible assets have been recognised as part of thefair value determination arising from businesscombinations referred to above. Customer relationships,brands and order books are stated at cost lessaccumulated amortisation. The intangible assets arebeing amortised over a period of between 5 and10 years, being the estimated economic life.

Impairment of tangible and intangible assetsAt each balance sheet date, the group reviews thecarrying amounts of its tangible and intangible assets todetermine whether there is any indication that thoseassets have suffered an impairment loss. If any suchindication exists, the recoverable amount of the asset isestimated in order to determine the extent of theimpairment loss (if any).

If the recoverable amount of an asset is estimated to beless than its carrying amount, the carrying amount ofthe asset is reduced to its recoverable amount.

An impairment loss is recognised as an expenseimmediately.

Any impairment loss in respect of goodwill is notreversed. In the case of other assets an impairment lossis reversed where there are changes in the estimatedrecoverable amount.

Financial assetsFinancial assets are classified as loans and receivables.Loans and receivables have fixed or determinablepayments that are not quoted in an active market.

Financial assets include cash and cash equivalents,investments, client receivables, amounts due from othermember firms of the DTTL organisation, including long-term loans and amounts due from partners.The group determines the classification of its financialassets at initial recognition and they are initiallyrecorded at fair value.

Loans and receivables are subsequently measured atamortised cost using the effective interest rate method,less any impairment. Interest income is recognised byapplying the effective interest rate, except for short-term receivables when the recognition of interest wouldbe immaterial.

Cash and cash equivalents comprise cash in hand, ondemand deposits and other short-term highly liquidinvestments.

Notes to the financial statementsYear ended 31 May 2010

Financial Statements 17

1. Accounting policies (continued)Financial liabilitiesFinancial liabilities, including borrowings, are initiallymeasured at fair value, net of transaction costs and aresubsequently measured at amortised cost using theeffective interest rate method. Interest cost is recognisedby applying the effective interest rate, except for short-term payables when the recognition of interest would beimmaterial. The group determines the classification of itsfinancial liabilities at initial recognition. Financial liabilitiesinclude trade payables, amounts due to other memberfirms of the DTTL organisation and partner capital.

Financial guaranteesFinancial guarantees are recorded as liabilities if it isanticipated that they will crystallise as liabilities. In thesecircumstances financial guarantees are measured initiallyat their fair values and are subsequently measured atthe higher of:

• the amount of the obligation under the contract, asdetermined in accordance with IAS 37 ‘Provisions,Contingent Liabilities and Contingent Assets’; or

• the amount initially recognised less, whereappropriate, accumulated amortisation.

ProvisionsProvisions are recognised when the group has a presentlegal or constructive obligation as a result of a pastevent, and it is probable that the group will be requiredto settle that obligation. Provisions are measured at thebest estimate of the expenditure required to settle theobligation at the balance sheet date and are discountedto present value where the effect is material. The increaseduring the period in the discounted amount, arisingfrom the passage of time and the effect of any changein the discount rate, is charged to the incomestatement as a finance cost.

Retirement benefit obligationsThe group operates both defined benefit and definedcontribution pension schemes. The net deficit or surplusfor the defined benefit schemes is calculated inaccordance with IAS 19 ‘Employee Benefits’, based onthe present value of the defined benefit obligations atthe balance sheet date less the fair value of theschemes’ assets. The cost of providing benefits isdetermined using the projected unit credit method,with actuarial valuations being carried out at eachbalance sheet date. Actuarial gains and losses arerecognised in full in the period in which they occur.

They are recognised outside the income statement andpresented in the statement of comprehensive income.

Where the actuarial valuation of the schemedemonstrates that the scheme is in surplus, therecognisable asset is limited to that which the groupcan benefit from in the future.

Past service cost is recognised immediately in theincome statement to the extent that the benefits arealready vested.

The group’s payments to the defined contributionpension schemes are charged to the income statementas they fall due.

Partners’ remunerationRemuneration to certain partners which arises from acontractual obligation has been charged to the incomestatement in the year. These contractual obligationscomprise salaries paid in overseas subsidiaries and fixednon-discretionary profit share arrangements.

Partners’ interestsPartners subscribe capital in proportion to their equityinterest in Deloitte LLP. Partners’ capital may only bewithdrawn when a partner retires from the LLP. Partnercapital has been classified as a liability.

Partners’ non-current liabilities represent provisions forthe pension annuities of current partners and partnercapital. The provision relates to annuities payable, underthe Partner Pension Plan, which commence when thepartner reaches the age of 60. The annuities areunfunded and are dependent upon the futuregeneration of profits.

Drawings by partners on account of profits have beenclassified as amounts due from partners within currentassets.

18

2. Critical accounting judgements and keysources of estimationThe preparation of financial statements requires theBoard to make estimates and assumptions that affectthe reported amount of revenue, expenses, assets andliabilities and the disclosure of contingent assets andliabilities. Estimates and judgements are continuallyevaluated and are based on historical experience andexpectations of future events that are consideredreasonable in the circumstances. Actual results maydiffer from those estimated.

The Board considers that the following estimates andjudgements are likely to have the most significanteffects on the amounts recognised in the financialstatements.

Retirement benefit obligationThe pension liability in respect of the defined benefitschemes has been independently valued based oninformation provided by the group in terms of thepensionable pay and contributions to the schemes.The liabilities disclosed for the defined benefit schemesare sensitive to movements in the related actuarialassumptions, in particular those relating to discount rateand mortality. The group will continue to review theseassumptions against the group’s experience and marketdata, and adjustments will be made in future periodswhere appropriate.

Provision for partner annuitiesThe provision for annuities for both retired and currentpartners has been independently valued based oninformation provided by the group in terms of futurelevels of pension annuity, current partner retirementrates and mortality. This data is based on the experiencewithin the group over the last five years. The liabilitiesdisclosed for the partner annuities are sensitive tomovements in the related actuarial assumptions, inparticular those relating to discount rate and mortality.The group will continue to review these assumptionsagainst the group’s experience and market data, andadjustments will be made in future periods whereappropriate.

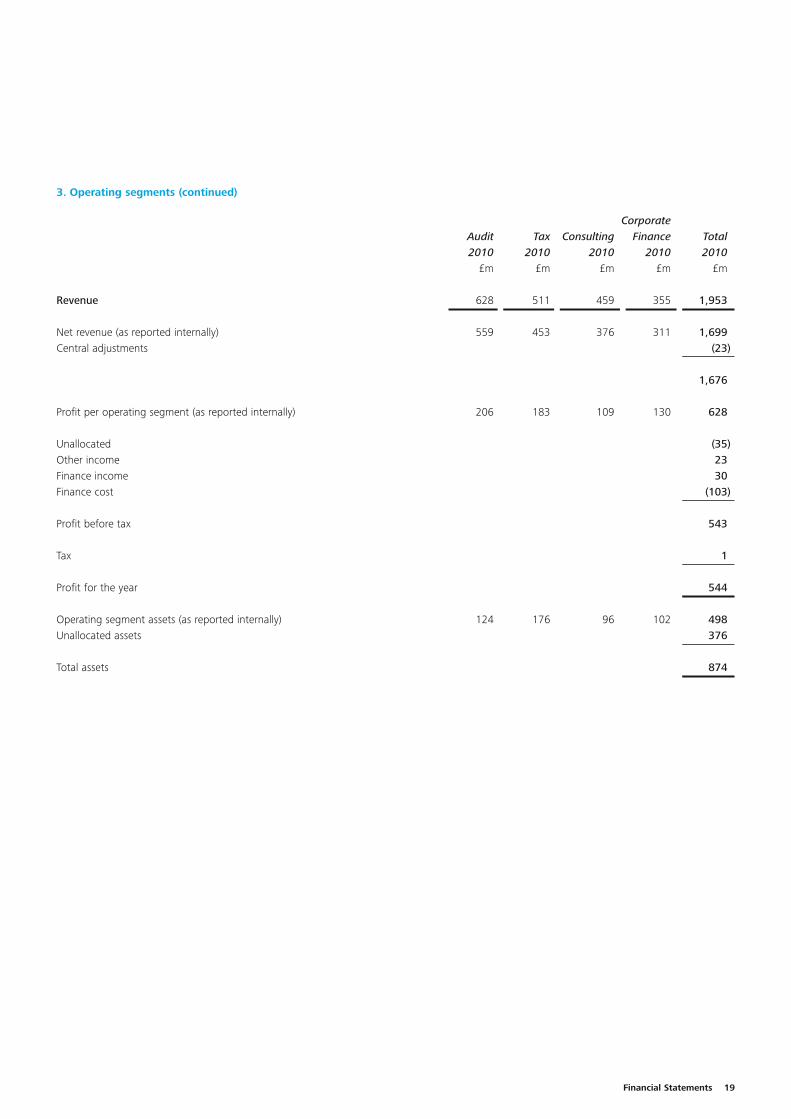

3. Operating segmentsThe group has four reportable operating segments;Audit, Tax, Consulting and Corporate Finance. The Auditsegment provides audit, internal audit, regulatory, riskand control and accounting and financial reportingservices. The Tax segment provides business tax,employer and personal tax services. The Consultingsegment provides strategy, operations, human capital,enterprise application and technology integrationservices as well as actuarial and insurance solutions.The Corporate Finance segment provides transactionsupport, reorganisation services, forensic and disputeservices and advisory services.

The reportable segments reflect the group’s principalmanagement and internal reporting structures and arestrategic business units that offer different services.

The group evaluates the performance of the segmentson the basis of net revenue and profit or loss fromoperations before unallocated costs, finance income,finance cost and tax expense. Net revenue is revenueless expenses and disbursements incurred on clientassignments. The adoption of IFRS 8 has not changedthe nature or number of the reported segments.The reported revenue and profit of each segment haschanged as it reflects the results reported internally.The comparative numbers have been restated so thatthese are in line with those reported internally.

Central adjustments largely represents time spent oninternal projects by Deloitte members of staff.Unallocated items include any costs which cannot beallocated to an operating segment on a meaningfulbasis. Net revenue and profit reported internally differsto that reported in the financial statements due todifferences in accounting policies adopted.

Performance assessment of the segments includes areview of certain assets such as client receivables net ofpayments on account and deferred income andamounts to be billed to clients and prepayments.All other assets, including non-current assets, balanceswith partners, cash, provisions and retirement benefitbalances are controlled centrally and are not allocatedacross service lines. There is no internal reporting ofliabilities by operating segment and thus no segmentaldisclosures are provided.

Inter-segment revenue is not material as revenue isshared proportionately by those service lines deliveringservices to clients.

Notes to the financial statementsYear ended 31 May 2010

CorporateAudit Tax Consulting Finance Total2010 2010 2010 2010 2010

£m £m £m £m £m

Revenue 628 511 459 355 1,953

Net revenue (as reported internally) 559 453 376 311 1,699Central adjustments (23)

1,676

Profit per operating segment (as reported internally) 206 183 109 130 628

Unallocated (35)Other income 23Finance income 30Finance cost (103)

Profit before tax 543

Tax 1

Profit for the year 544

Operating segment assets (as reported internally) 124 176 96 102 498Unallocated assets 376

Total assets 874

Financial Statements 19

3. Operating segments (continued)

Notes to the financial statementsYear ended 31 May 2010

CorporateAudit Tax Consulting Finance Total2009 2009 2009 2009 2009

£m £m £m £m £m

Revenue 647 523 478 321 1,969

Net revenue (as reported internally) 568 460 408 283 1,719Central adjustments (4)

1,715

Profit per operating segment (as reported internally) 200 171 135 117 623

Unallocated (42)Finance income 41Finance cost (58)

Profit before tax 564

Tax (2)

Profit for the year 562

Operating segment assets (as reported internally) 144 190 97 95 526Unallocated assets 368

Total assets 894

2010 2009£m £m

Revenue per income statement 1,953 1,969Expenses and disbursements on client assignments (277) (254)

Net revenue 1,676 1,715

The accounting policies of the reportable segments are the same as the group’s accounting policies as described in note 1. Segment net revenueand profit without the allocation of central costs, other income, finance income and costs and tax expense are the measures that are reported tothe Senior Partner and Chief Executive for the purposes of assessment of segment performance and resource allocation.

Included in group revenue is net revenue of approximately £46m (2009: £50m) which arose from supplying professional services to the group’slargest client, which is a non-audit client.

The group’s revenue and information about its segment assets (non-current assets excluding financial instruments) by geographical location isdetailed below. Both revenue and non-current assets are based on those arising in the legal entities situated in each country.

20

3. Operating segments (continued)

Revenue Net revenue Non-current assets2010 2009 2010 2009 2010 2009

£m £m £m £m £m £m

UK 1,786 1,823 1,552 1,594 236 220Other Countries 167 146 147 125 13 11

1,953 1,969 1,699 1,719 249 231

To manage and drive the business, the group is managed using a matrix structure which incorporates both service lines and the nature of theindustry to which the services are supplied. Revenue by industry is:

Net NetRevenue Revenue revenue revenue

2010 2009 2010 2009£m £m £m £m

Financial Services 546 554 475 482Consumer Business 217 213 189 185Government & Public Sector 215 227 187 198Telecoms, Media & Technology 206 248 179 216Real Estate, Hospitality & Leisure 169 157 147 137Manufacturing 161 179 140 155Energy, Infrastructure & Utilities 153 143 133 125Private Equity 65 53 57 46Life Science 63 70 54 61Professional Partnerships 34 39 30 34Other 124 86 108 80

1,953 1,969 1,699 1,719

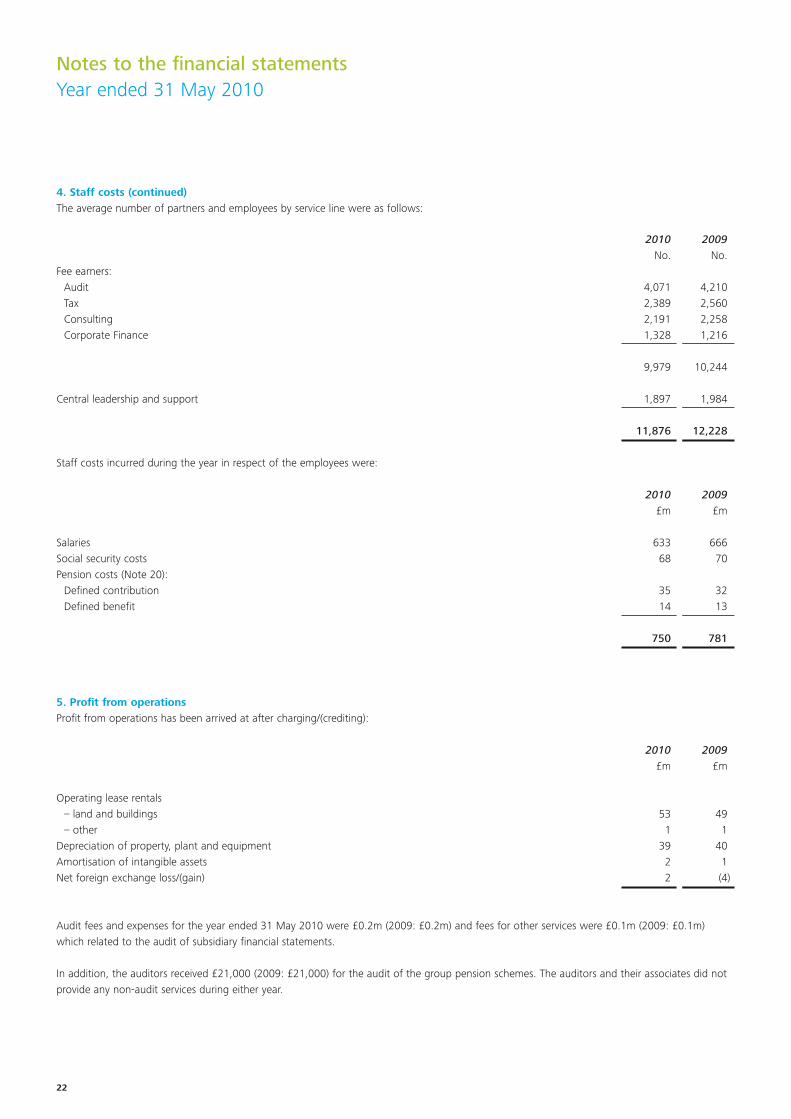

4. Staff costsThe average number of partners and employees during the year were:

2010 2009No. No.

Partners 676 681

Other personnel 11,200 11,547

11,876 12,228

Financial Statements 21

3. Operating segments (continued)

Notes to the financial statementsYear ended 31 May 2010

2010 2009No. No.

Fee earners:Audit 4,071 4,210Tax 2,389 2,560Consulting 2,191 2,258Corporate Finance 1,328 1,216

9,979 10,244

Central leadership and support 1,897 1,984

11,876 12,228

Staff costs incurred during the year in respect of the employees were:

2010 2009£m £m

Salaries 633 666Social security costs 68 70Pension costs (Note 20):

Defined contribution 35 32Defined benefit 14 13

750 781

5. Profit from operationsProfit from operations has been arrived at after charging/(crediting):

2010 2009£m £m

Operating lease rentals – land and buildings 53 49– other 1 1

Depreciation of property, plant and equipment 39 40Amortisation of intangible assets 2 1Net foreign exchange loss/(gain) 2 (4)

Audit fees and expenses for the year ended 31 May 2010 were £0.2m (2009: £0.2m) and fees for other services were £0.1m (2009: £0.1m)which related to the audit of subsidiary financial statements.

In addition, the auditors received £21,000 (2009: £21,000) for the audit of the group pension schemes. The auditors and their associates did notprovide any non-audit services during either year.

22

4. Staff costs (continued)The average number of partners and employees by service line were as follows:

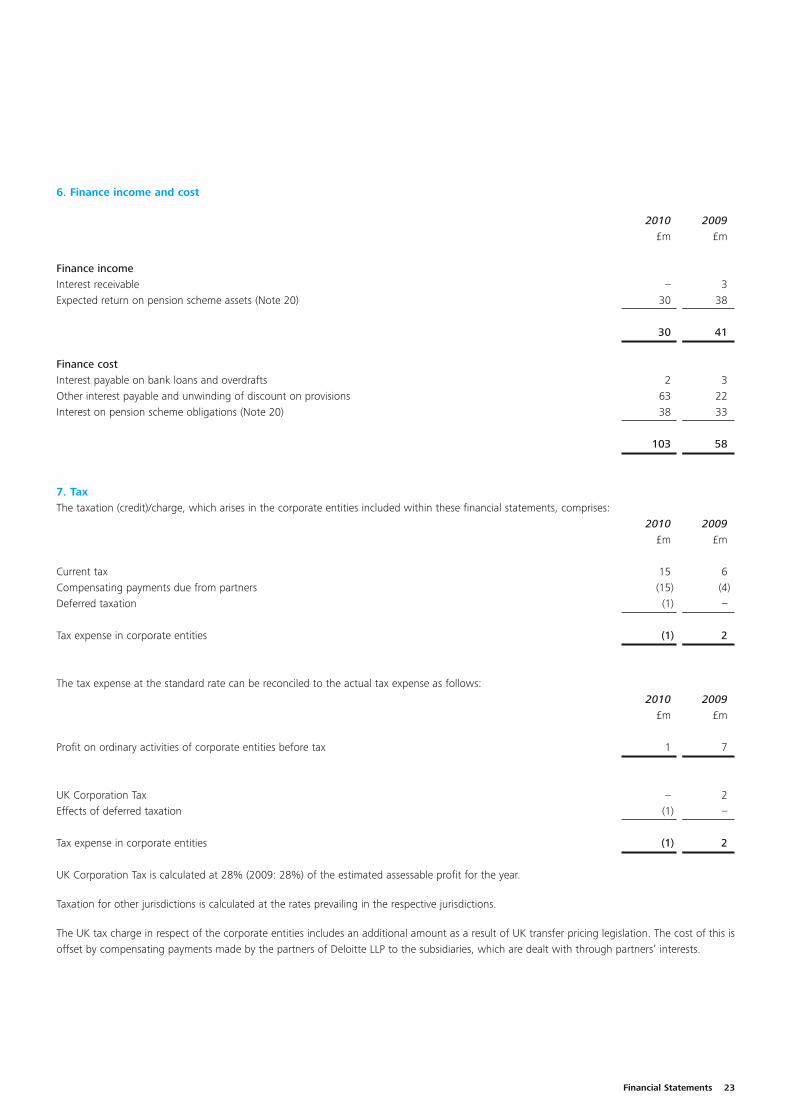

2010 2009£m £m

Finance incomeInterest receivable – 3Expected return on pension scheme assets (Note 20) 30 38

30 41

Finance costInterest payable on bank loans and overdrafts 2 3Other interest payable and unwinding of discount on provisions 63 22Interest on pension scheme obligations (Note 20) 38 33

103 58

7. TaxThe taxation (credit)/charge, which arises in the corporate entities included within these financial statements, comprises:

2010 2009£m £m

Current tax 15 6Compensating payments due from partners (15) (4)Deferred taxation (1) –

Tax expense in corporate entities (1) 2

The tax expense at the standard rate can be reconciled to the actual tax expense as follows:2010 2009

£m £m

Profit on ordinary activities of corporate entities before tax 1 7

UK Corporation Tax – 2Effects of deferred taxation (1) –

Tax expense in corporate entities (1) 2

UK Corporation Tax is calculated at 28% (2009: 28%) of the estimated assessable profit for the year.

Taxation for other jurisdictions is calculated at the rates prevailing in the respective jurisdictions.

The UK tax charge in respect of the corporate entities includes an additional amount as a result of UK transfer pricing legislation. The cost of this isoffset by compensating payments made by the partners of Deloitte LLP to the subsidiaries, which are dealt with through partners’ interests.

Financial Statements 23

6. Finance income and cost

Notes to the financial statementsYear ended 31 May 2010

2010 2009£m £m

Annuity provision for current partners 101 36Remuneration for current partners paid under a contractual arrangement 27 –

128 36

9. Property, plant and equipmentFixtures

Leasehold Computer and Motor improvements equipment fittings vehicles Total

£m £m £m £m £mCostAt 1 June 2008 163 74 38 37 312Additions 29 16 12 11 68Disposals – (4) – (13) (17)

At 1 June 2009 192 86 50 35 363Additions 8 13 2 5 28Acquisitions 3 – – – 3Disposals (4) (14) (1) (10) (29)

At 31 May 2010 199 85 51 30 365

DepreciationAt 1 June 2008 41 37 22 12 112Charge for the year 13 17 5 5 40Disposals – (4) – (6) (10)

At 1 June 2009 54 50 27 11 142Charge for the year 15 16 4 4 39Disposals (2) (14) (1) (5) (22)

At 31 May 2010 67 52 30 10 159

Net book amountAt 31 May 2010 132 33 21 20 206

At 31 May 2009 138 36 23 24 221

Capital commitments contracted but not provided for as at 31 May 2010 amounted to £9m (2009: £5m).

24

8. Provision for annuities and remuneration for current partners

Customerrelationships,order books,

brand andIT software Goodwill contracts Total

£m £m £m £mCostAt 1 June 2008 and 1 June 2009 17 – – 17Acquisitions 2 20 13 35

At 31 May 2010 19 20 13 52

AmortisationAt 1 June 2008 6 – – 6Charge for the year 1 – – 1

At 1 June 2009 7 – – 7Charge for the year 2 – – 2

At 31 May 2010 9 – – 9

Net book amountAt 31 May 2010 10 20 13 43

At 31 May 2009 10 – – 10

Intangible assets recognised on acquisition represent the following; order books £5m, brand £1m, customer relationships £4m, favourablecontracts £3m and IT software £2m. Details of goodwill arising on acquisitions are provided in note 17.

Financial Statements 25

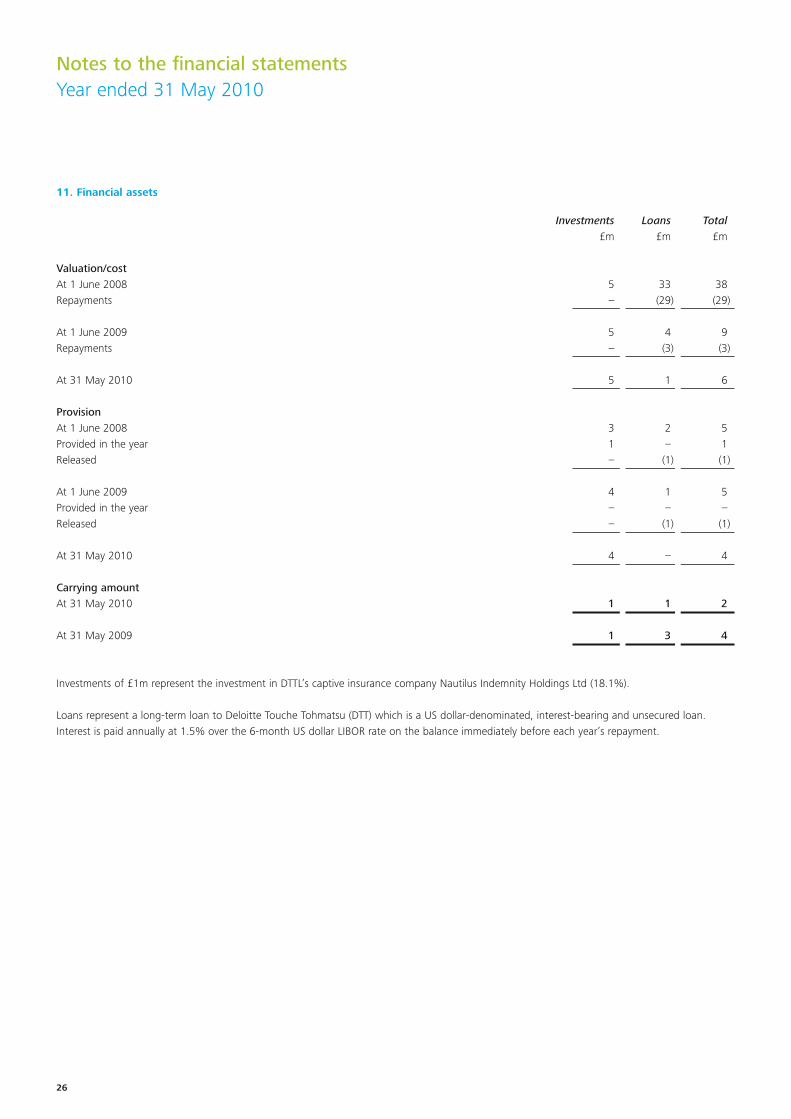

10. Intangible assets

Notes to the financial statementsYear ended 31 May 2010

Investments Loans Total£m £m £m

Valuation/costAt 1 June 2008 5 33 38Repayments – (29) (29)

At 1 June 2009 5 4 9Repayments – (3) (3)

At 31 May 2010 5 1 6

ProvisionAt 1 June 2008 3 2 5Provided in the year 1 – 1Released – (1) (1)

At 1 June 2009 4 1 5Provided in the year – – –Released – (1) (1)

At 31 May 2010 4 – 4

Carrying amountAt 31 May 2010 1 1 2

At 31 May 2009 1 3 4

Investments of £1m represent the investment in DTTL’s captive insurance company Nautilus Indemnity Holdings Ltd (18.1%).

Loans represent a long-term loan to Deloitte Touche Tohmatsu (DTT) which is a US dollar-denominated, interest-bearing and unsecured loan.Interest is paid annually at 1.5% over the 6-month US dollar LIBOR rate on the balance immediately before each year’s repayment.

26

11. Financial assets

2010 2009£m £m

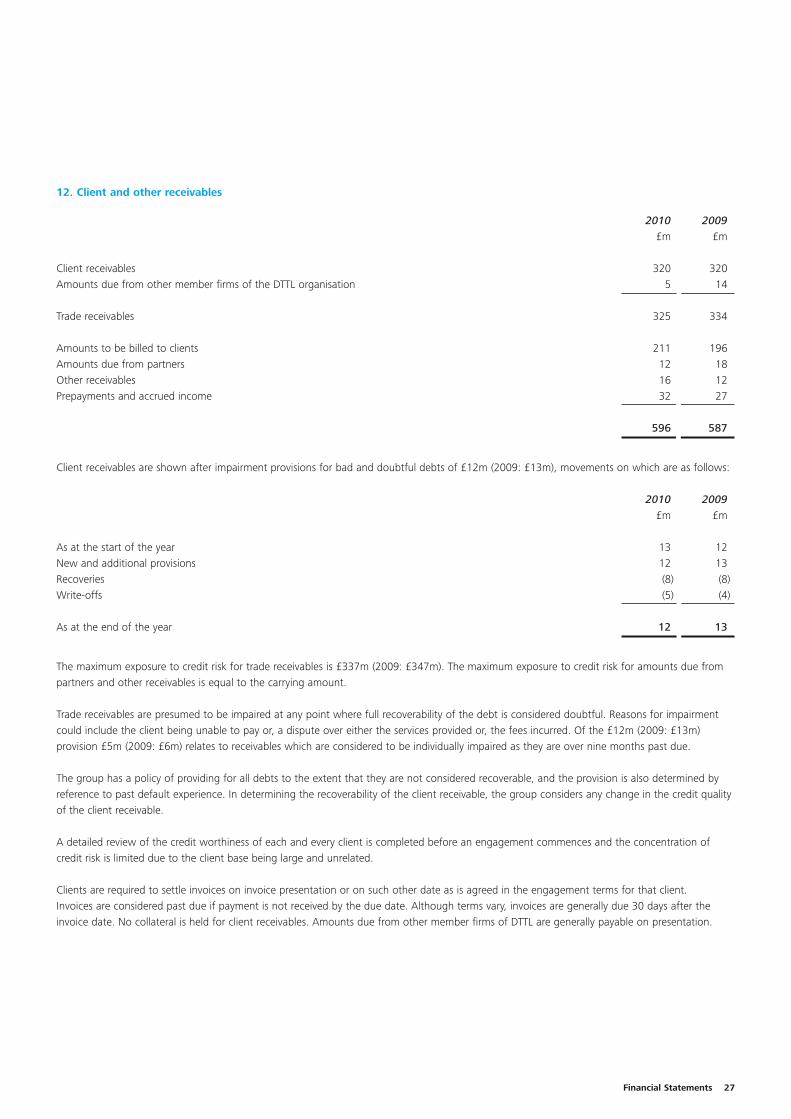

Client receivables 320 320Amounts due from other member firms of the DTTL organisation 5 14

Trade receivables 325 334

Amounts to be billed to clients 211 196Amounts due from partners 12 18Other receivables 16 12Prepayments and accrued income 32 27

596 587

Client receivables are shown after impairment provisions for bad and doubtful debts of £12m (2009: £13m), movements on which are as follows:

2010 2009£m £m

As at the start of the year 13 12New and additional provisions 12 13Recoveries (8) (8)Write-offs (5) (4)

As at the end of the year 12 13

The maximum exposure to credit risk for trade receivables is £337m (2009: £347m). The maximum exposure to credit risk for amounts due frompartners and other receivables is equal to the carrying amount.

Trade receivables are presumed to be impaired at any point where full recoverability of the debt is considered doubtful. Reasons for impairmentcould include the client being unable to pay or, a dispute over either the services provided or, the fees incurred. Of the £12m (2009: £13m)provision £5m (2009: £6m) relates to receivables which are considered to be individually impaired as they are over nine months past due.

The group has a policy of providing for all debts to the extent that they are not considered recoverable, and the provision is also determined byreference to past default experience. In determining the recoverability of the client receivable, the group considers any change in the credit qualityof the client receivable.

A detailed review of the credit worthiness of each and every client is completed before an engagement commences and the concentration ofcredit risk is limited due to the client base being large and unrelated.

Clients are required to settle invoices on invoice presentation or on such other date as is agreed in the engagement terms for that client.Invoices are considered past due if payment is not received by the due date. Although terms vary, invoices are generally due 30 days after theinvoice date. No collateral is held for client receivables. Amounts due from other member firms of DTTL are generally payable on presentation.

Financial Statements 27

12. Client and other receivables

Notes to the financial statementsYear ended 31 May 2010

An analysis of the age of trade receivables that are not impaired but are past due at the year end is presented below:

2010 2009£m £m

1 – 3 months 89 883 – 6 months 17 306 – 9 months 1 7

At 31 May 107 125

Non-impaired trade receivables that are not past due:

Less than 1 month 218 209

325 334

13. Trade and other payables2010 2009

£m £m

Progress billings for client work 32 21Trade payables 19 18Amounts due to other member firms of the DTTL organisation 11 12Corporation tax 5 2Social security and other taxes 47 49Other payables 19 7Accruals and deferred income 92 76

225 185

28

12. Client and other receivables (continued)

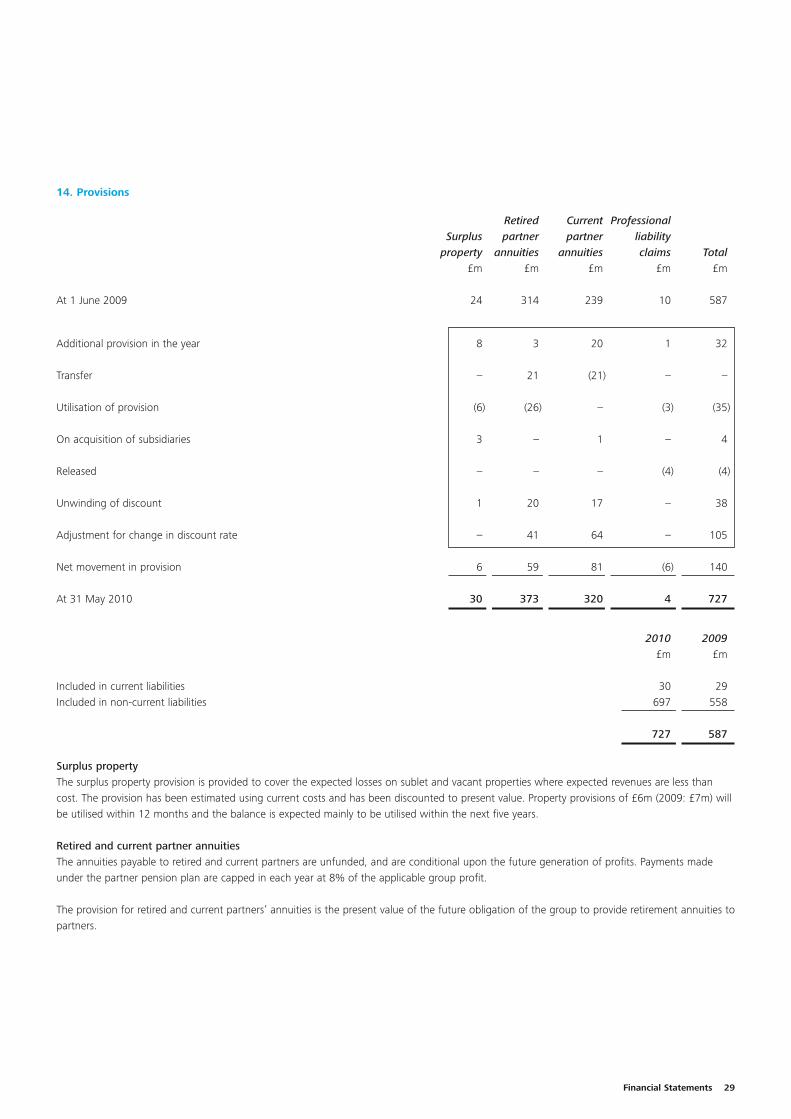

Retired Current ProfessionalSurplus partner partner liability

property annuities annuities claims Total£m £m £m £m £m

At 1 June 2009 24 314 239 10 587

Additional provision in the year 8 3 20 1 32

Transfer – 21 (21) – –

Utilisation of provision (6) (26) – (3) (35)

On acquisition of subsidiaries 3 – 1 – 4

Released – – – (4) (4)

Unwinding of discount 1 20 17 – 38

Adjustment for change in discount rate – 41 64 – 105

Net movement in provision 6 59 81 (6) 140

At 31 May 2010 30 373 320 4 727

2010 2009£m £m

Included in current liabilities 30 29Included in non-current liabilities 697 558

727 587

Surplus propertyThe surplus property provision is provided to cover the expected losses on sublet and vacant properties where expected revenues are less thancost. The provision has been estimated using current costs and has been discounted to present value. Property provisions of £6m (2009: £7m) willbe utilised within 12 months and the balance is expected mainly to be utilised within the next five years.

Retired and current partner annuitiesThe annuities payable to retired and current partners are unfunded, and are conditional upon the future generation of profits. Payments madeunder the partner pension plan are capped in each year at 8% of the applicable group profit.

The provision for retired and current partners’ annuities is the present value of the future obligation of the group to provide retirement annuities topartners.

Financial Statements 29

14. Provisions

Notes to the financial statementsYear ended 31 May 2010

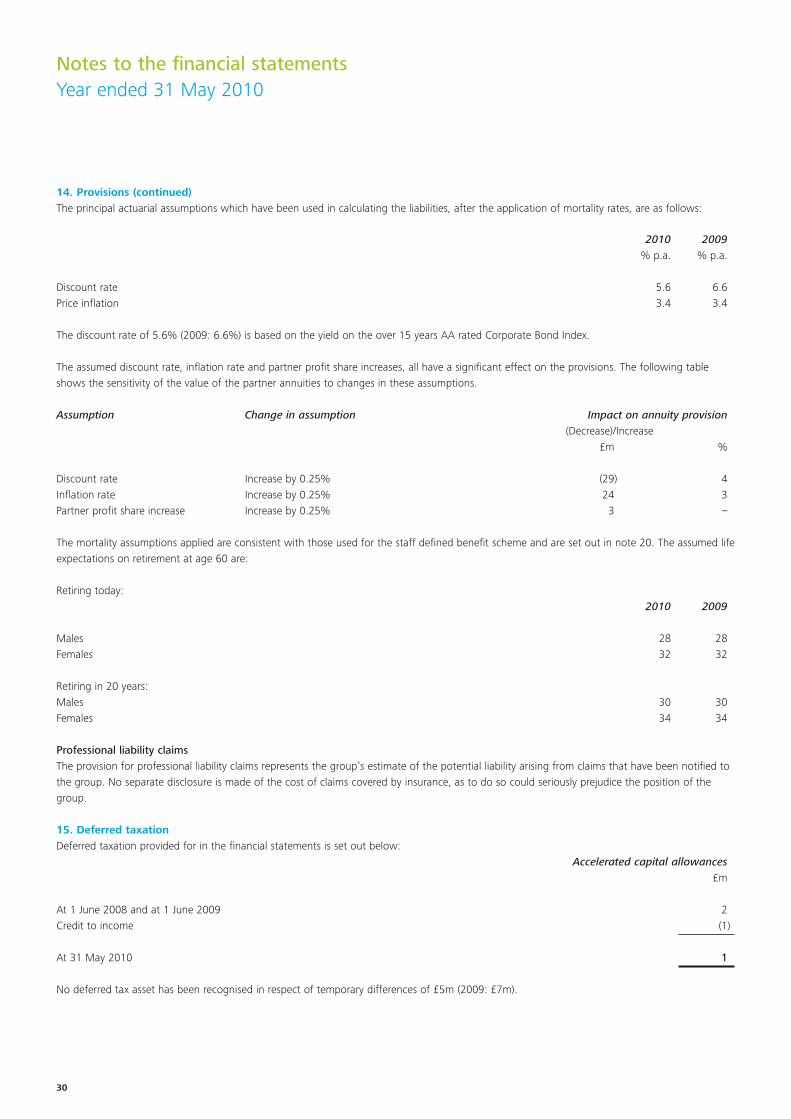

2010 2009% p.a. % p.a.

Discount rate 5.6 6.6Price inflation 3.4 3.4

The discount rate of 5.6% (2009: 6.6%) is based on the yield on the over 15 years AA rated Corporate Bond Index.

The assumed discount rate, inflation rate and partner profit share increases, all have a significant effect on the provisions. The following tableshows the sensitivity of the value of the partner annuities to changes in these assumptions.

Assumption Change in assumption Impact on annuity provision(Decrease)/Increase

£m %

Discount rate Increase by 0.25% (29) 4Inflation rate Increase by 0.25% 24 3Partner profit share increase Increase by 0.25% 3 –

The mortality assumptions applied are consistent with those used for the staff defined benefit scheme and are set out in note 20. The assumed lifeexpectations on retirement at age 60 are:

Retiring today:2010 2009

Males 28 28Females 32 32

Retiring in 20 years:Males 30 30Females 34 34

Professional liability claimsThe provision for professional liability claims represents the group’s estimate of the potential liability arising from claims that have been notified tothe group. No separate disclosure is made of the cost of claims covered by insurance, as to do so could seriously prejudice the position of thegroup.

15. Deferred taxationDeferred taxation provided for in the financial statements is set out below:

Accelerated capital allowances£m

At 1 June 2008 and at 1 June 2009 2Credit to income (1)

At 31 May 2010 1

No deferred tax asset has been recognised in respect of temporary differences of £5m (2009: £7m).

30

14. Provisions (continued)The principal actuarial assumptions which have been used in calculating the liabilities, after the application of mortality rates, are as follows:

Provision Partners’Amounts for current equity –

Partners’ due from partner othercapital partners annuities reserves Total

£m £m £m £m £m

Partners’ interests at 1 June 2008 130 (46) 238 60 382Profit for the financial year – – – 526 526Allocated profits – 641 – (641) –Pension scheme actuarial loss – – – (183) (183)Translation reserve – – – 1 1Movement in provision – – 1 – 1Drawings and distributions – (613) – – (613)Compensating payment due to subsidiary undertakings – – – (4) (4)Capital:

Introduced 12 – – – 12Repaid (15) – – – (15)

Partners’ interests at 1 June 2009 127 (18) 239 (241) 107Profit for the financial year – – – 416 416Allocated profits – 601 – (601) –Pension scheme actuarial loss – – – (14) (14)Translation reserve – – – – –Movement in provision – – 81 – 81Drawings and distributions – (595) – – (595)Compensating payment due to subsidiary undertakings – – – (15) (15)Capital:

Introduced 12 – – – 12Repaid (12) – – – (12)

Partners’ interests at 31 May 2010 127 (12) 320 (455) (20)

The negative partners’ interests of £20m arises as a result of partners’ distributable profit being determined by reference to the firm’s equityaccounts which are based on different accounting policies to the group accounts, which are prepared under IFRS. The most significant differenceis the provision for retired partner annuities of £373m. The liability is conditional on the future generation of profits and is payable over a periodof years with £62m payable between 10 and 15 years and £133m payable after 15 years.

Deloitte LLP’s profits are divided based on units allocated to partners. The unit allocation is completed after the year end and accordingly therewas no automatic division of profits among the partners at 31 May 2010. As a result, the balance of profit available for division among thepartners as at 31 May 2010 is included in other reserves.

Partners’ other reserves rank after unsecured creditors and loans, and other debts due to partners rank pari passu with unsecured creditors in theevent of a winding up.

Partner capital of £3m (2009: £10m) has been included as a current liability and £124m (2009: £117m) has been included as a non currentliability. Partner capital in total is £127m (2009: £127m).

Financial Statements 31

16. Partners’ interests

Notes to the financial statementsYear ended 31 May 2010

17. Acquisitions and disposalsAcquisitionsA summary of the assets and liabilities acquired as part of the ReportSource, Drivers Jonas and the MC Schweiz transactions is set out below.IFRS 3 does not permit the possibility of mergers or of accounting for a business combination as a pooling of interests. Instead, all cases meetingthe definition of a business combination must be accounted for as an acquisition and consequently, the purchase method of accounting hasbeen applied.

ReportSourceBook and Fair value

£m

Net assets acquired

Client receivables 3Trade and other payables (3)

–

Goodwill 3

Total cash consideration 3

Net cash (outflow)/inflow arising on acquisition:

Cash consideration (3)Cash and cash equivalent acquired –

(3)

On 1 February 2010 the group acquired the assets and liabilities of ReportSource for cash consideration of £2.7m. ReportSource is the largest UK-based Hyperion consultancy. Its integration into Consulting now makes Deloitte a leading provider of Enterprise Practice Management advisoryservices in the UK.

No fair value adjustments were identified as part of the acquisition. The primary reason for the transaction was to enable Deloitte to extend anddeepen its enterprise performance management service offering to clients.

ReportSource contributed £1.6m to revenue and £0.1m to profit before tax for the period between the date of acquisition and the balance sheetdate.

32

Book Fair value Fairvalue adjustment value

£m £m £m

Net assets acquired:

Property, plant and equipment 2 – 2Intangible assets – 4 4Client receivables 17 – 17Prepayments and accrued income 7 – 7Cash and cash equivalents 3 – 3Trade and other payables (28) (1) (29)Provisions (1) (3) (4)

– – –

Goodwill –

Total cash consideration –

Net cash (outflow)/inflow arising on acquisition:

Cash consideration –Cash and cash equivalent acquired 3

3

On 1 March 2010 the group entered into a transaction with Drivers Jonas LLP and its subsidiaries which has been accounted for as an acquisition.The business has been merged with the existing Deloitte business and is trading as Drivers Jonas Deloitte. The primary reason for the transactionwas to maximise the opportunities in the real estate advisory market through combining the experience and expertise of both businesses and tobe able to offer clients solutions in tax, corporate finance and business consultancy from one firm.

Drivers Jonas Deloitte contributed £14m to revenue and £3m to profit before tax for the period between the date of acquisition and the balancesheet date. Trade and other payables include £12m in respect of the balance of the current account payable to the former partners of DriversJonas following completion.

The following fair value adjustments arose:

• intangible assets of £4m have been recognised for the current value of anticipated income streams resulting from customer relationships, orderbook and brand relating to the Drivers Jonas business;

• a provision of £1m has been created which relates to a provision of an annuity payable to former Drivers Jonas partners; and

• a provision of £3m has been recognised relating to existing properties of the Drivers Jonas business to align to current market value of theleases.

Financial Statements 33

17. Acquisitions and disposals (continued)Drivers Jonas

Notes to the financial statementsYear ended 31 May 2010

Book Fair value Fairvalue adjustment value

£m £m £m

Net assets acquired:

Property, plant and equipment 1 – 1Intangible assets 2 9 11Client receivables 5 – 5Amounts to be billed to clients 1 – 1Prepayments and accrued income 1 – 1Cash and cash equivalents 1 – 1Trade and other payables (8) – (8)Loans (11) – (11)Provisions – (3) (3)

(8) 6 (2)

Goodwill 17

Total cash consideration 15

Net cash (outflow)/inflow arising on acquisition:

Cash consideration (15)Cash and cash equivalent acquired 1

(14)

On the 30 April 2010 the group acquired the Swiss management consultancy group of MC Schweiz for cash consideration of £15m (CHF25m).The principal asset of the MC Schweiz group is the public sector consultancy, Exsigno, which now trades as Exsigno Deloitte and is part of DeloitteConsulting in Switzerland. The primary reason for the transaction was to take advantage of Exsigno’s presence in the public sector and healthcareconsultancy market in Switzerland. The goodwill arising on acquisition represents the significant value attributable to the experience and expertiseof the staff within Exsigno and the non-contractual relationships.

The acquired group contributed £2m to revenue and broke even in the period between the date of acquisition and the balance sheet date.

The following fair value adjustments arose:

• intangible assets of £9m have been recognised for the current value of anticipated income streams resulting from customer relationships, orderbook and favourable contracts relating to the Exsigno business; and

• a provision of £3m has been recognised in relation to the pension liability which arises under IAS 19. There is no pension liability under SwissGAAP.

34

17. Acquisitions and disposals (continued)MC Schweiz

17. Acquisitions and disposals (continued)

Other transactionsOn the 1 March 2010 the group also acquired the assets and liabilities of dcarbon8 for cash consideration of £10,000. Goodwill of £10,000 aroseon this transaction. There is no material impact on revenue or profit for the year ended 31 May 2010.

On 31 May 2010 Deloitte LLP acquired the business assets of IM Global for a cash consideration of £0.5m. No goodwill arose as a result of thetransaction. There is no impact on revenue or profit for the year ended 31 May 2010.

Summary of financial impact of transactionsIf these transactions had taken place at the beginning of the year, consolidated revenue would have been £2,029m and group profit for thefinancial year would have been £427m. Costs incurred of £15m in relation to the acquisitions have been charged to the income statement.

DisposalsOn 1 October 2009 the group completed a sale agreement to dispose of the Abacus Enterprise Software business, which operated in the group’stax division, for a cash consideration of £26m and a profit of £23m. The business contributed £2m (2009: £7m) to revenue and £0.6m (2009:£2m) to profit before tax for the period 1 June 2009 to 30 September 2009, which has been incorporated in the group‘s results.

18. Operating lease commitmentsAt 31 May 2010, the group had outstanding commitments for future minimum lease payments under non-cancellable operating leases, which falldue as follows:

Land and Land andbuildings Other buildings Other

2010 2010 2009 2009£m £m £m £m

Operating payments which fall due:Within one year 63 4 59 2Within two to five years 223 4 215 3In more than five years 478 – 517 –

764 8 791 5

19. Contingent liabilitiesThe group has entered into a several guarantee to guarantee a proportion of certain liabilities of DTT. At 31 May 2010 the contingent liabilityunder this guarantee amounted to £65m (2009: £68m).

20. Retirement benefit schemesDefined contribution schemesThe group operates defined contribution schemes and stakeholder pension arrangements for employees, as well as a number of closed schemes.

In all cases, the schemes’ assets are held separately from those of the group in trustee administered or, in the case of stakeholder, contract-basedarrangements.

The total cost charged to the income statement of £35m (2009: £32m) represents contributions payable to these schemes by the group.

Financial Statements 35

Notes to the financial statementsYear ended 31 May 2010

20. Retirement benefit schemes (continued)Defined benefit schemesIn the UK the group provides retirement benefits through a defined benefit scheme. The defined benefit sections of the scheme are closed to newmembers. Under the scheme, employees are entitled to retirement benefits of up to two-thirds of their final salary, subject to HMRC limits,on attainment of retirement ages between 60 and 65. No other post-retirement benefits are provided. The scheme is a funded scheme.

The pension scheme assets are held in a separate Corporate Trustee administered fund to meet the long-term pension liabilities for past andpresent employees.