Embed Size (px)

Citation preview

BROADBAND BROADBAND

INFRASTRUINFRASTRUCTURE CTURE

PLAN FOR PLAN FOR

CHATHAM COUNTY, N.C.CHATHAM COUNTY, N.C.

submitted by submitted by

ACTION AUDITS, LLCACTION AUDITS, LLCCARY, N.C.CARY, N.C.

919-467-5392919-467-5392

AUGUST 24, 2011AUGUST 24, 2011

AUTHORS:AUTHORS:CYNTHIA M. POLSCYNTHIA M. [email protected]@aol.comCATHARINE B. RICECATHARINE B. [email protected]@yahoo.com

TABLE OF CONTENTSEXECUTIVE SUMMARY

I. INTRODUCTION AND BACKGROUND ................................................................................ 1 A. BROADBAND AVAILABILITY IN CHATHAM COUNTY ........................................................ 1

B. IMPORTANCE OF BROADBAND FOR CHATHAM COUNTY .............................................. 8

II. BROADBAND INFRASTRUCTURE OPTIONS ................................................................. 12 A. WIRELINE BROADBAND OPTIONS ........................................................................................ 14

1. Telephone Technology (DSL) ........................................................................................................................ 14 2. Cable Technology (HFC) ................................................................................................................................ 22 3. Direct Fiber Optics Technology (FTTP) ........................................................................................................ 26

B. WIRELESS BROADBAND OPTIONS ......................................................................................... 30 1. Terrestrial Wireless ......................................................................................................................................... 30

a. Mobile Terrestrial Wireless (Conventional Cellular Service) .................................................................... 30 b. Fixed Terrestrial Wireless (Fixed Wireless Access (FWA) Networks) ..................................................... 36 c. Key Spectrum for Wireless Terrestrial Service .......................................................................................... 38

2. Satellites ......................................................................................................................................................... 39

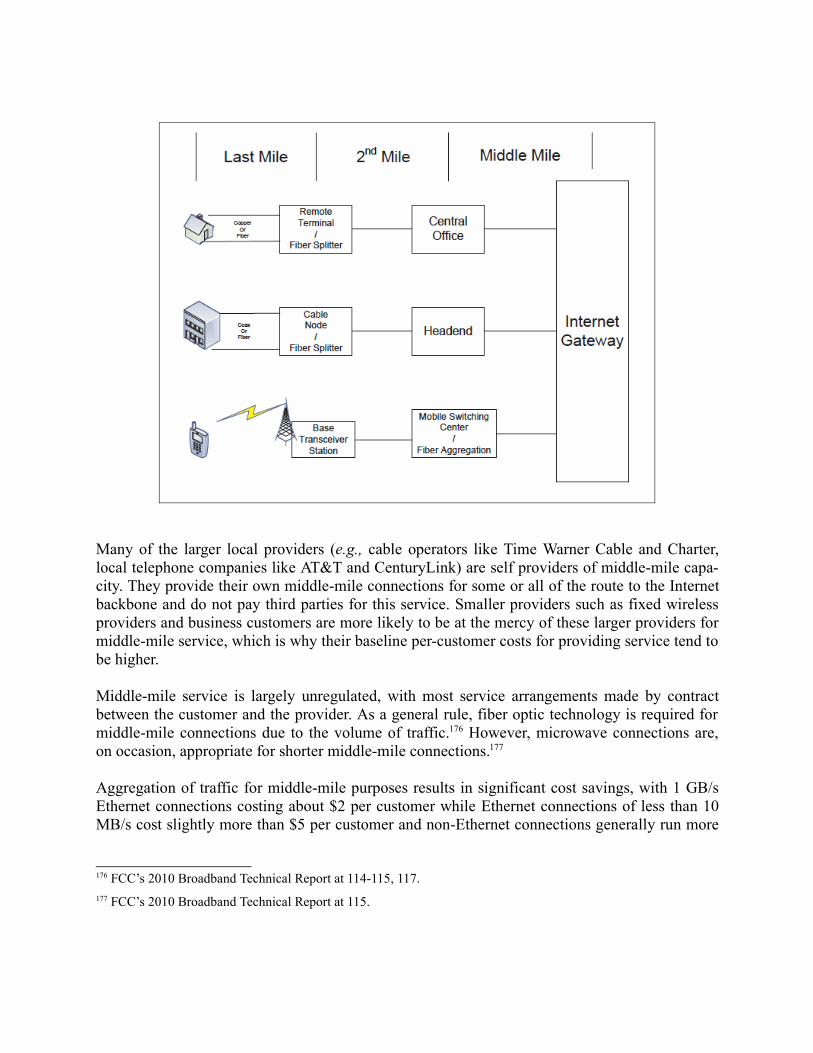

C. MIDDLE-MILE CONNECTIONS ................................................................................................ 41

D. SUMMARY OF CAPACITY AND GEOGRAPHIC LIMITS OF KEY BROADBAND OP-TIONS ........................................................................................................................................... 43

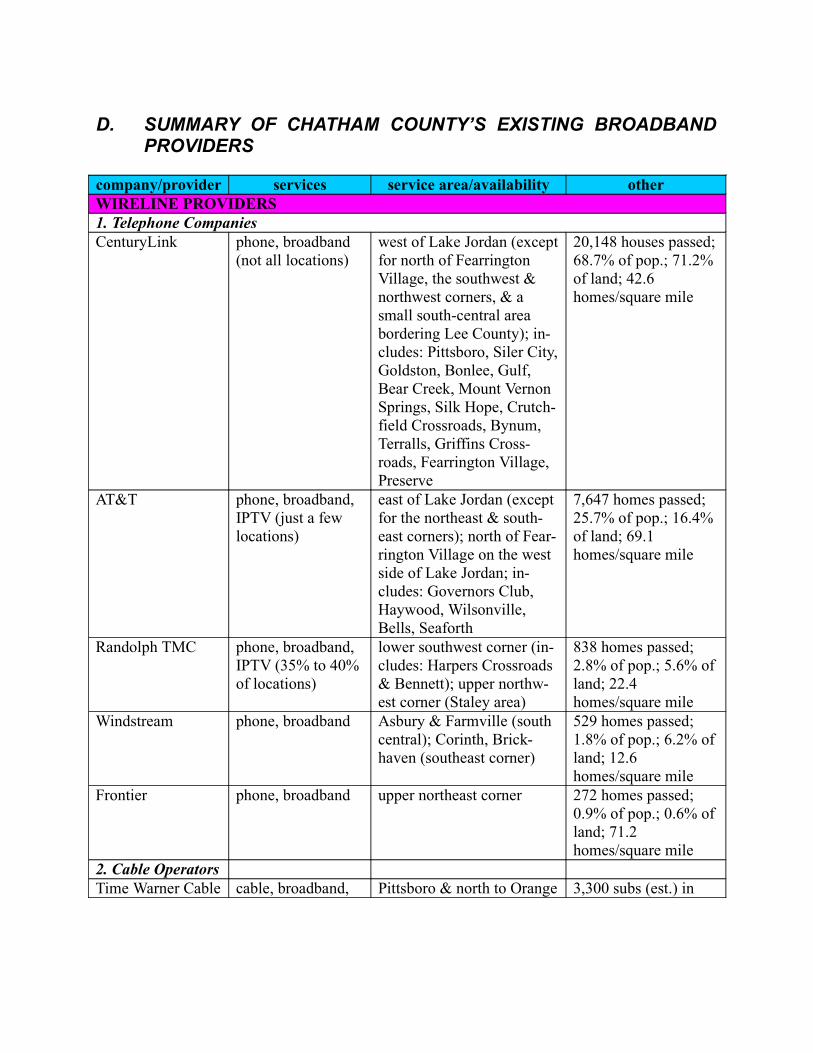

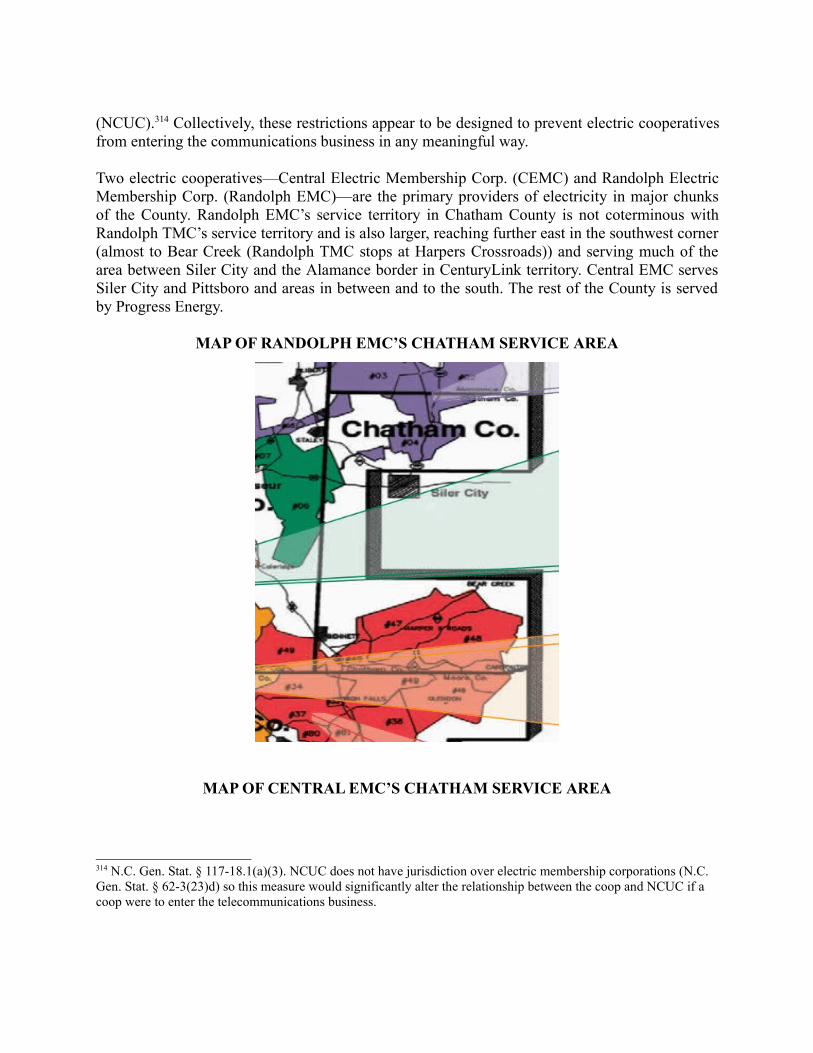

III. CHATHAM COUNTY’S EXISTING BROADBAND INFRASTUCTURE ....................... 45 A. WIRELINE PROVIDERS .............................................................................................................. 45

1. Telephone Companies ..................................................................................................................................... 46 a. CENTURYLINK (DSL) ............................................................................................................................ 47 b. AT&T (FORMERLY BELLSOUTH) ........................................................................................................ 56 c. RANDOLPH TELEPHONE MEMBERSHIP CORP. AND RANDOLPH TELEPHONE COMPANY .. 59 d. WINDSTREAM (FORMERLY HEINS TELCO) ..................................................................................... 62 e. FRONTIER (VERIZON UNTIL 2010) ..................................................................................................... 64

2. Cable Companies ........................................................................................................................................... 66 a. TIME WARNER CABLE (TWC) ............................................................................................................. 66 b. CHARTER ................................................................................................................................................. 69

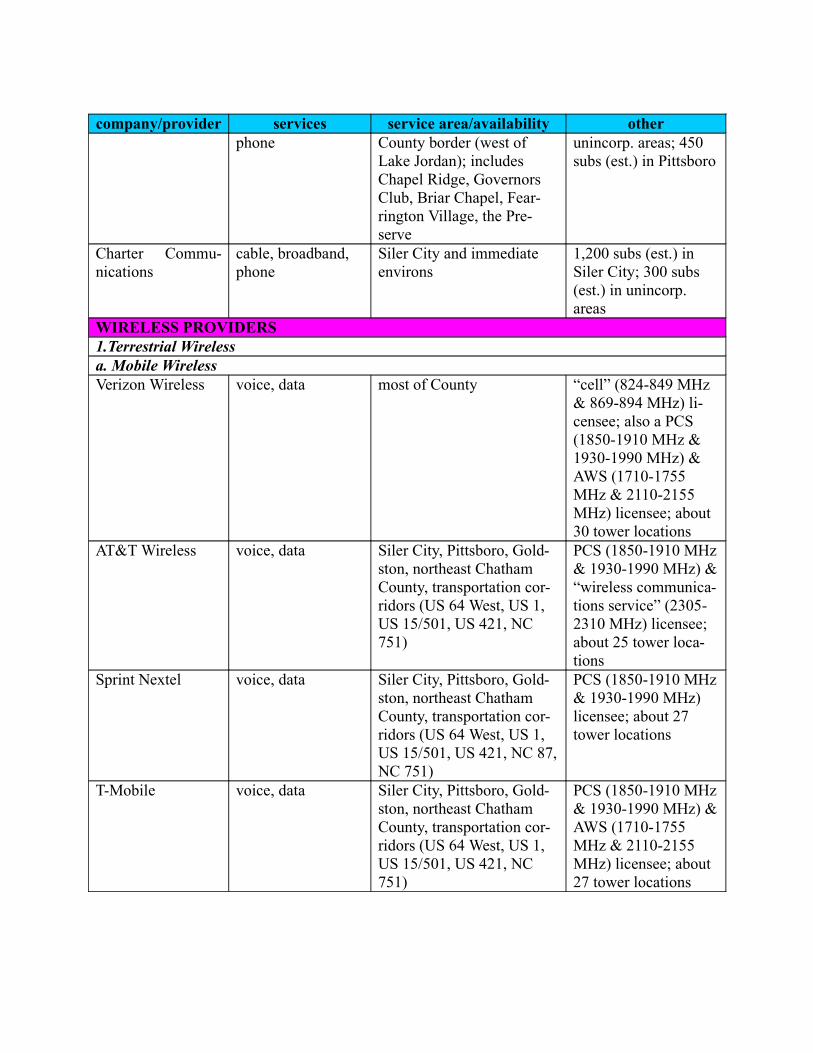

B. WIRELESS PROVIDERS .............................................................................................................. 71 1. Terrestrial Wireless Providers ......................................................................................................................... 71

a. Mobile Wireless Providers (Conventional Cell Service) ......................................................................... 72 i. Verizon Wireless .................................................................................................................................... 72 ii. AT&T Wireless ..................................................................................................................................... 74 iii. Sprint/Nextel ........................................................................................................................................ 76 iv. T-Mobile ............................................................................................................................................... 76 v. Other Wireless Carriers ......................................................................................................................... 77

b. Fixed Wireless Providers ........................................................................................................................... 79 2. Satellite ........................................................................................................................................................... 80

C. MIDDLE–MILE PROVIDERS ...................................................................................................... 80

D. SUMMARY OF CHATHAM COUNTY’S EXISTING BROADBAND PROVIDERS ............ 82

IV. BROADBAND APPLICATIONS AND USES ..................................................................... 84 A. ESTABLISHED BROADBAND USES ......................................................................................... 85

1. Education ........................................................................................................................................................ 85 2. Economic Development and Job Creation ..................................................................................................... 87 3. Personal Communications, Financial Transactions and Entertainment ......................................................... 87 4. Public Safety .................................................................................................................................................. 89 5. Government Services and Civic Engagement ................................................................................................ 91

B. EMERGING BROADBAND USES ............................................................................................... 91 1. Health Care ..................................................................................................................................................... 91

a. Electronic Health Records (her) ................................................................................................................. 92 b. Video Consultations ................................................................................................................................... 93 c. New Mobile Treatment Options ................................................................................................................ 93

2. Energy and Utility Use (Management and Control) ....................................................................................... 94 3. Transportation ................................................................................................................................................. 96 4. Smart Communities ........................................................................................................................................ 98

V. LEGAL BARRIERS TO COMPETITION AND INNOVATION .......................................... 99 A. LIMITS ON PUBLIC SECTOR ENTITIES ................................................................................ 99

1. County Authority ............................................................................................................................................ 99 2. Municipal Authority .................................................................................................................................... 100 3. Guidance for Counties .................................................................................................................................. 101 4. Authority of Telephone Cooperatives ........................................................................................................... 101 5. Authority of Electric Cooperatives ............................................................................................................... 102

B. LIMITS ON PRIVATE SECTOR PROVIDERS ........................................................................ 104 1. Service Territory Limits ................................................................................................................................ 104 2. Federal Subsidy Programs ............................................................................................................................ 104 3. Spectrum Allocations ................................................................................................................................... 105

VI. RECOMMENDATIONS ..................................................................................................... 106 A. OVERALL APPROACH .............................................................................................................. 106

B. LONG-TERM BROADBAND PLAN ......................................................................................... 106

C. SHORT-TERM PLANNING STEPS ........................................................................................... 109

APPENDIX

EXECUTIVE SUMMARYThis broadband infrastructure planning project is intended to provide Chatham County with a plan for improving broadband service, recognizing the central importance of an affordable, high-quality broadband infrastructure to the County’s future. The County’s broadband deficit is substantial and, if anything, is likely to widen in the future because of the private sector’s limited interest in investing in broadband infrastructure.

Our central recommendation is that the County develop a plan to reprogram existing County and other public resources currently devoted to broadband and telecommunications service and establish an independent fiber optic backbone network for the County through a public-private partnership. This fiber optic backbone will control and decrease the County’s communication costs over the long term. Perhaps more important, it will provide a central element of the infrastructure required for the 21st century and enable County residents to compete in the state, national, and global economy and keep up with future developments in the broadband world. Operationally, this new network will serve the County’s governmental and other public institutions while also establishing a platform for new commercial and other service providers to offer new state-of-the-art wireline and wireless service to Chatham residents.

INTRODUCTION AND BACKGROUND [§ I]

Broadband Availability in Chatham County [§ I.A]:

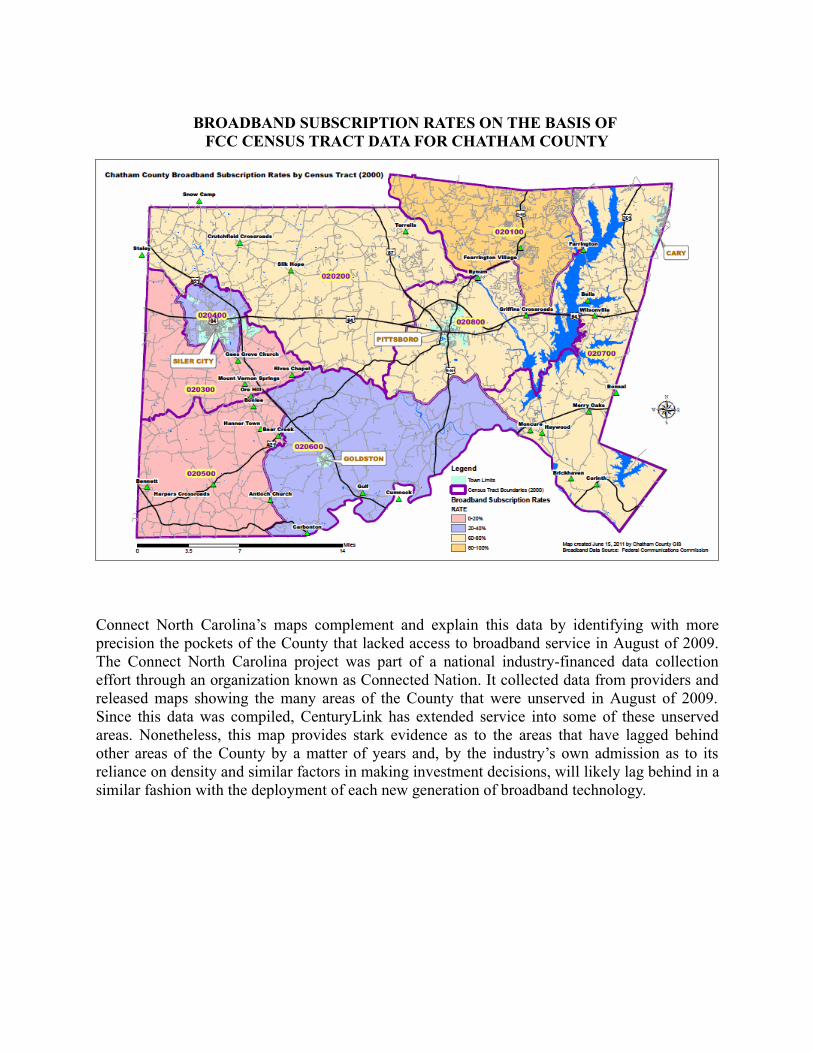

The broadband deficit in the County is the greatest in the western and southern parts of the County. The most disadvantaged areas are the two 2000 census tracts1 west and south of Siler City, with broadband subscription rates of zero to 20% (this area includes Harpers Crossroads, Bear Creek, Bonlee, and Mount Vernon Springs). Next in terms of limited access to broadband service are the 2000 census tracts for Siler City and Goldston at 20% to 40% subscription rates. The area with the highest subscription rate (and therefore the greatest access to the broadband world) is the 2000 census tract for the Chapel Hill area, with a 80% to 100% subscription rate. The other three 2000 census tracts (north of Siler City, Pittsboro, and east of Jordan Lake) fall in between the two extremes, with subscription rates of 60% to 80%.

Large swaths of the County have been left out of the broadband era for the first 10 or so years of its existence2 and are likely to continue to lag behind in the future. Problem areas go well beyond the western and southern parts of the County and include areas in the vicinity of Pittsboro, north of Siler City, and east of Lake Jordan. Service deficiencies are the most pronounced in the western and southern parts of the County, but even the more populated eastern areas are not immune to service quality problems and uneven access to service on a street-by-street basis.

1 This data was compiled by the Federal Communications Commission (FCC) in 2011 using 2000 census tracts.2 Cable modem service started to take off as a major business with serious penetration rates in 1999, with the tele-phone industry’s digital subscriber line (DSL) service following suit in 2000.

Also of concern is that even in areas characterized by government agencies as fully served, broadband service is not available or inadequate at a significant number of spots within those areas. Further, wireless broadband, as the industry is currently configured, is not much of an answer to the County’s broadband deficit due to spotty coverage and slow speeds.

The telecommunications industry, whether wireline or wireless, invests in infrastructure based primarily on population density and secondarily on economic and demographic characteristics. These investment practices make fashioning a permanent solution to the County’s broadband deficit a challenge as normal market mechanisms do not bring broadband service to the County in a timely or responsive fashion.

Importance of Broadband for Chatham County [§ I.B]:

Using 2001 as the starting date for the broadband era, parts of the County are at least 10 years off pace in terms of access to broadband technology (the more rural areas of western and southern Chatham County where there still is no broadband service). Others are 7 or 8 years off pace (Silk Hope area), some are 4 or 5 years off pace (Goldston, Bonlee), and still others are just 1 or 2 years off the pace (Pittsboro and Siler City). This pattern can be expected to repeat itself again and again in the future as new generations of broadband technologies emerge and are deployed. Each new generation of technology is unlikely to reach much of the County until the prior generation of technology is close to the end of its life cycle and the industry is in the process of moving on to the next generation of technology.

BROADBAND INFRASTRUCTURE OPTIONS [§ II]

In connection with preparing its 2010 National Broadband Plan, the Federal Communications Commission mapped out five major broadband infrastructure options. These five options consist of three wireline options (digital subscriber line telephone (DSL), hybrid fiber-coaxial cable (HFC), and fiber-to-the-premises (FTTP) systems) and two wireless options (terrestrial wireless systems (mobile and fixed) and satellites). All these options except the satellite option also re-quire middle-mile connections to the Internet to complete service delivery, making middle-mile pipelines a key part of broadband planning.

In connection with the National Broadband Plan process, the FCC also established affordable ac-cess for all American homes to broadband service at actual speeds of 4 megabits per second (MB/s) downstream and 1 MB/s upstream as national broadband availability targets. The FCC chose these speed levels as the minimum necessary to participate in contemporary society. To put these broadband speed targets in context, 1 MB/s speed in both directions is required to support a high-definition Skype video conference. The FCC also established more ambitious long-term goals for broadband access of actual speeds of 100 MB/s downstream and 50 MB/s upstream by 2020 for 100 million homes (roughly 80% to 85% of U.S. households), with interim goals of 50 Mb/s downstream and 20 MB/s upstream by 2015 for 100 million homes.

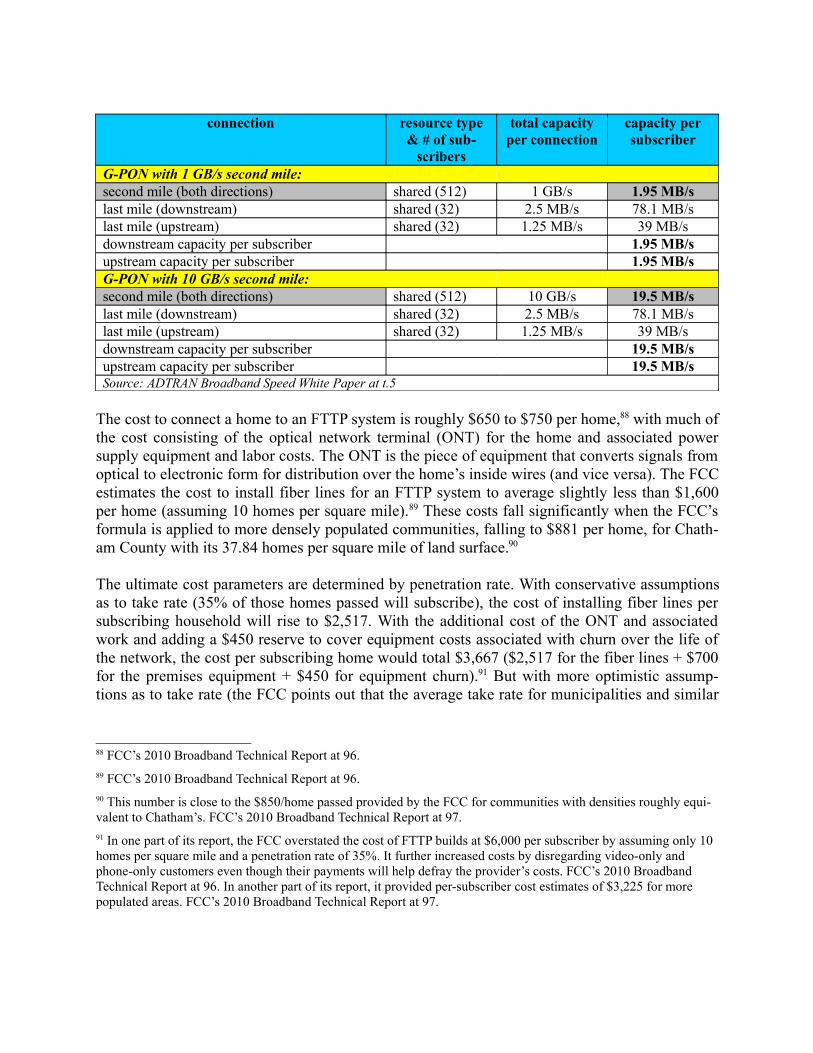

Each of the main broadband options is subject to technical limits and financial constraints but some are superior to others in performance and potential. Putting aside cost considerations, the most future-proofed and powerful technologies are advanced FTTP systems (gigabit passive op-tical network (G-PON) systems) and advanced DSL systems (VDSL2)3, with G-PON having a decided advantage over VDSL2 technology. Lagging far behind in performance characteristics and capabilities are the two technologies favored by Chatham County’s incumbent providers: the telephone industry’s ADSL24 technology and the cable industry’s HFC technology.

Wireline Broadband Options [§ II.A]:

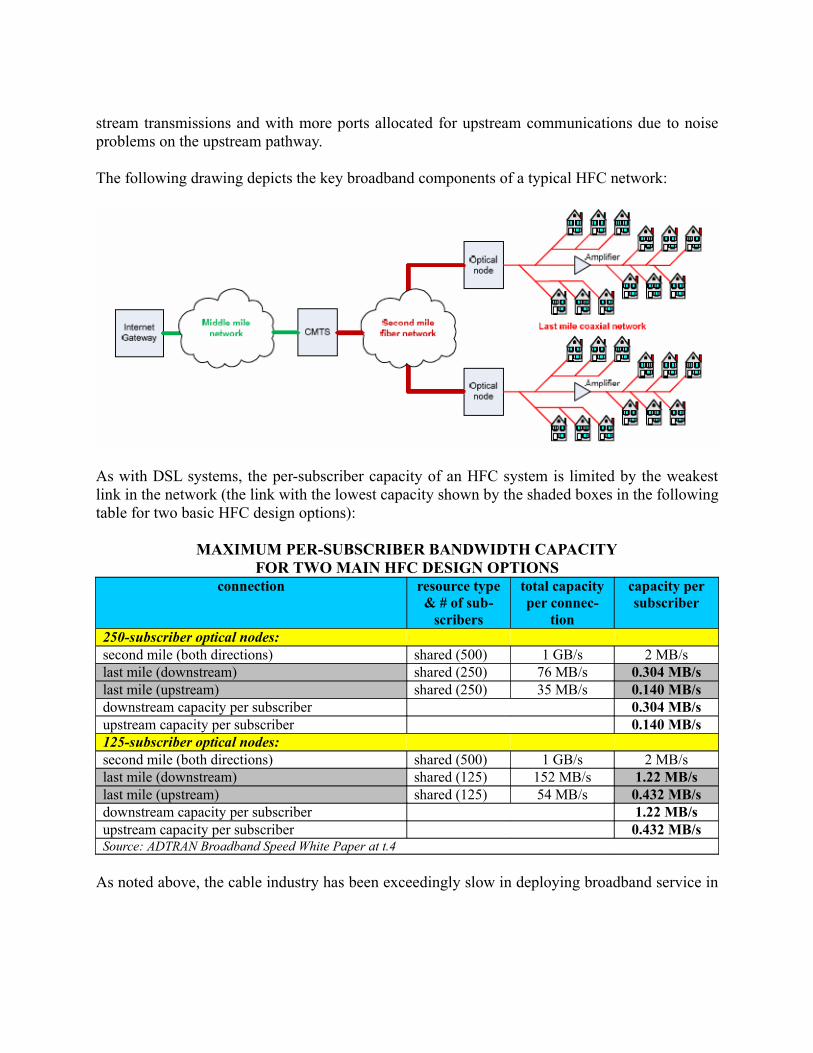

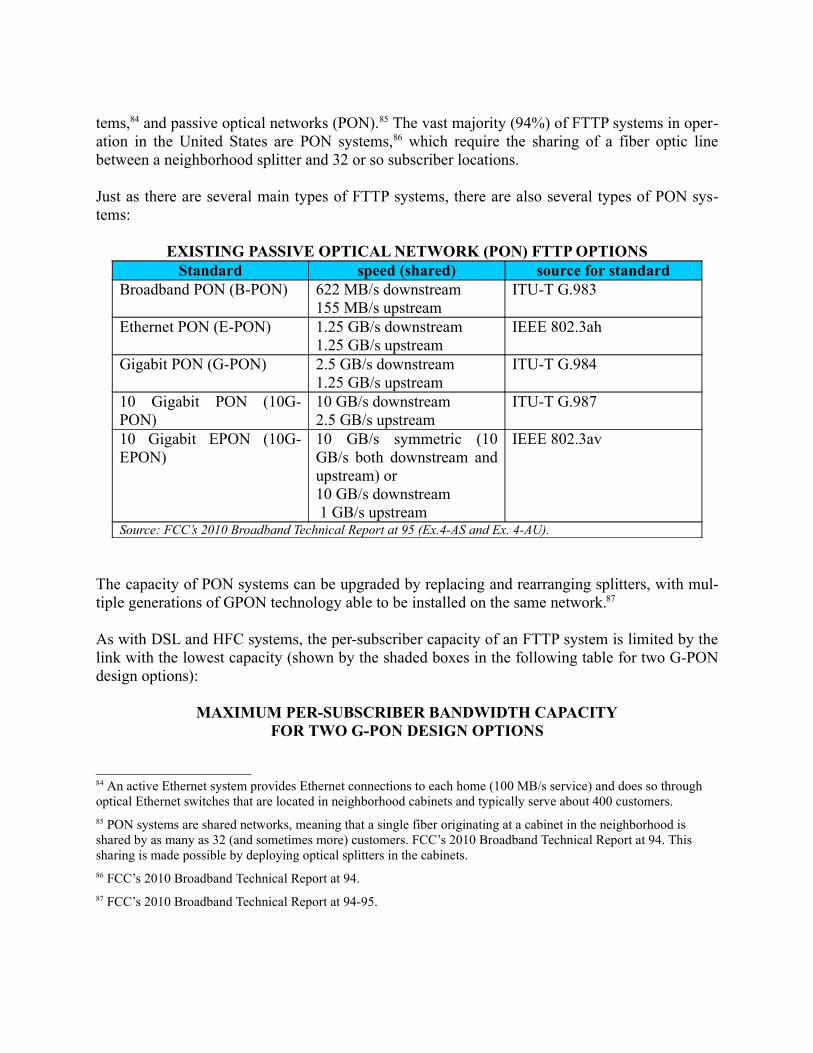

ADSL2 technology and HFC systems have built-in weaknesses due to the fact that they were grafted onto older technologies that were developed for limited purposes (voice communications in the case of ADSL2 telephone technology and one-way video programming in the case of HFC cable technology). Incumbent telephone companies are unwilling to provide telephone techno-logy (DSL) [§ II.A.1] by installing DSL access multiplexers (DSLAM) in rural areas in the num-bers necessary to limit the signal loss associated with long copper runs to subscriber locations and to ensure high-speed broadband service. Cable technology (HFC) [§ II.A.2], which requires massive bandwidth sharing between optical nodes and subscriber locations, is perhaps even more flawed in design terms because of the congestion and other problems associated with bandwidth sharing. In contrast, direct fiber optics technology (FTTP) [§ II.A.3] was designed for broad-band service and, as a result, provides the most potential capacity and is the most future proofed of the main broadband technology options.

Wireless Broadband Options [§ II.B]:

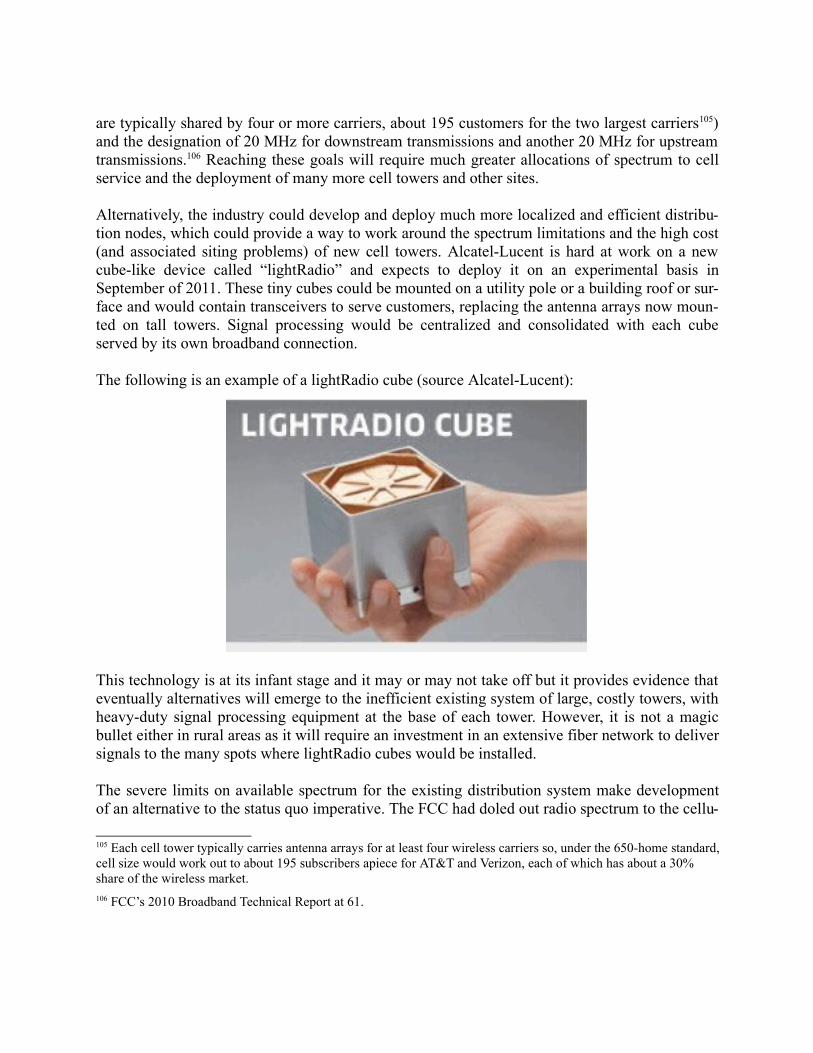

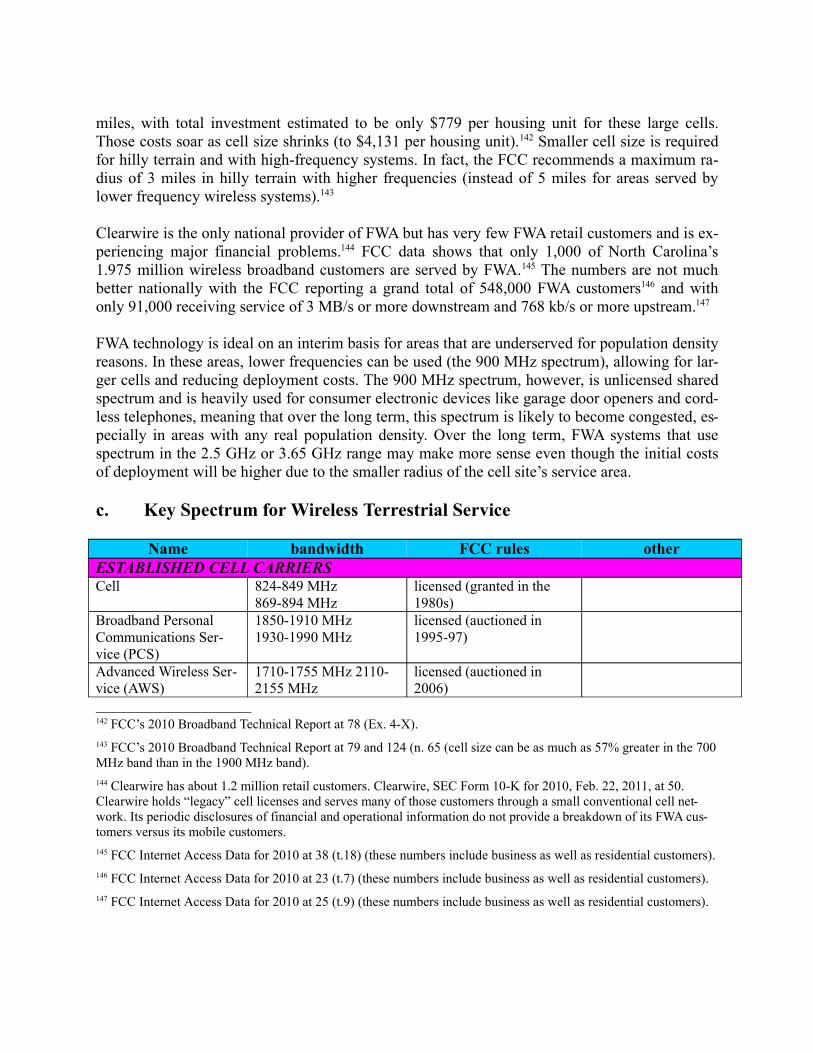

In the wireless arena, terrestrial wireless [§ II.B.1] does not currently provide much of an altern-ative to wireline technology. Mobile terrestrial wireless [§ II.B.1.a] (e.g., conventional cellular service) is limited by the high-cost of antenna towers and the limited availability of spectrum. This technology will likely need to be overhauled or augmented by new technology such as much smaller and more versatile alternatives to the large towers in relatively short order just to keep up with current demand. Fixed terrestrial wireless [§ II.B.1.b], with the possibility of much smaller service areas (and therefore less bandwidth congestion) and ease of entry for new pro-viders (due to readier availability of spectrum) is promising but largely undeveloped.

See also Key Spectrum for Wireless Terrestrial Service [§ II.B.1.c] for further detail on the spectrum currently available for wireless service.

See also Satellites [§ II.B.2] for a discussion of the technical limits and high cost of satellite ser-vice.

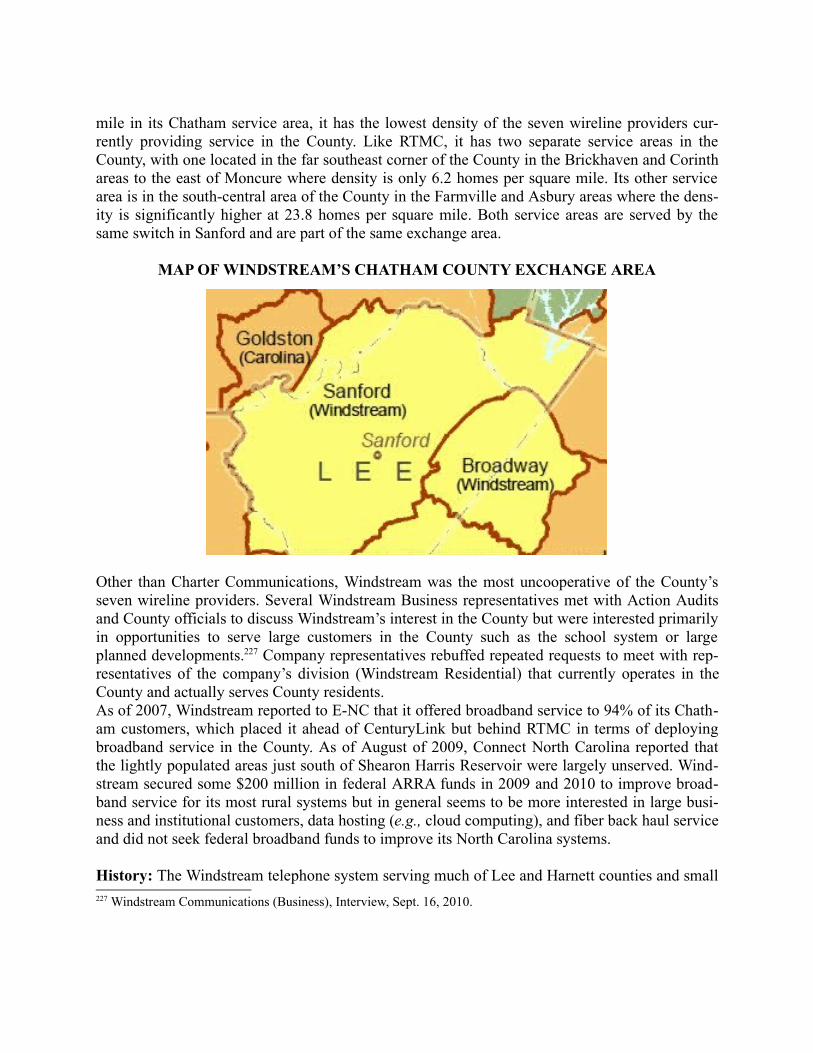

3 VDSL stands for Very High Bit Rate DSL.4 ADSL stands for Asynchronous DSL service.

Middle-mile Connections [§ II.C]:

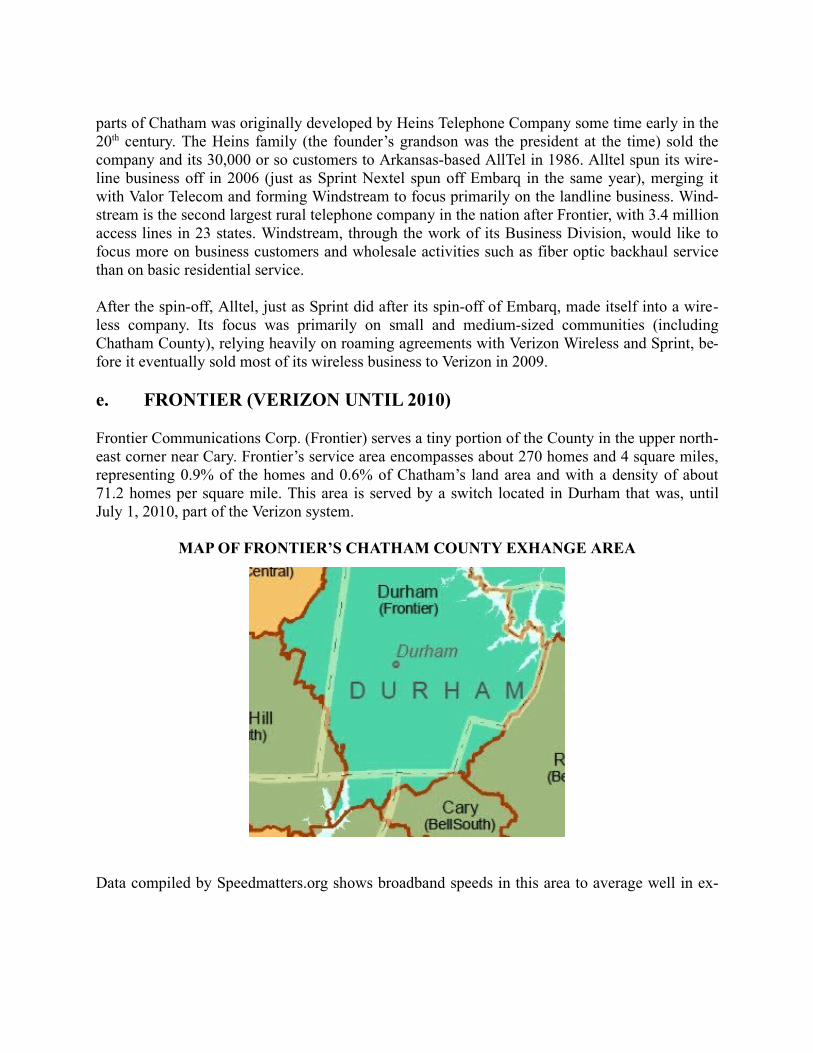

Middle-mile networks carry Internet traffic to and from local network aggregation points to In-ternet backbone connection points and are typically fiber optic networks. These middle-mile con-nections can add significantly to the cost of local broadband operations, adding anywhere from $2 to $12 per subscriber to the provider’s monthly costs. In rural and semi-rural areas, the essen-tial middle-mile market tends to be controlled by one or two incumbent providers who can and do pass along high middle-mile fees as part of broadband service fees to unknowing business and governmental customers.

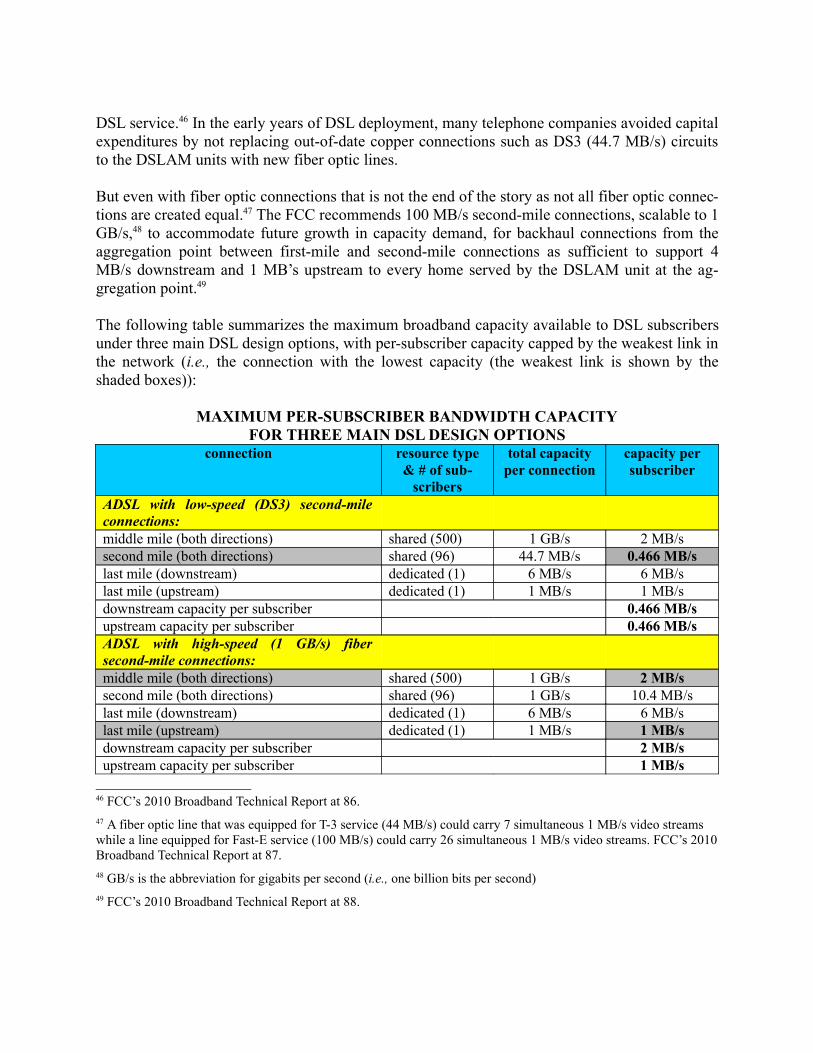

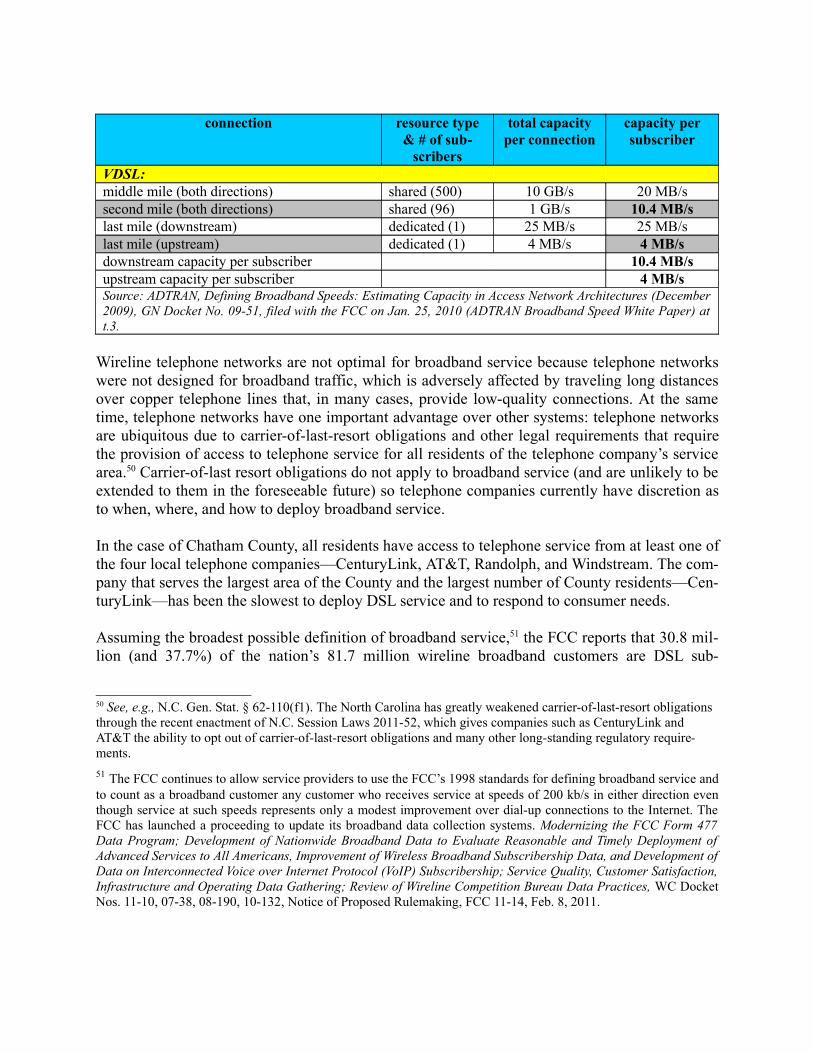

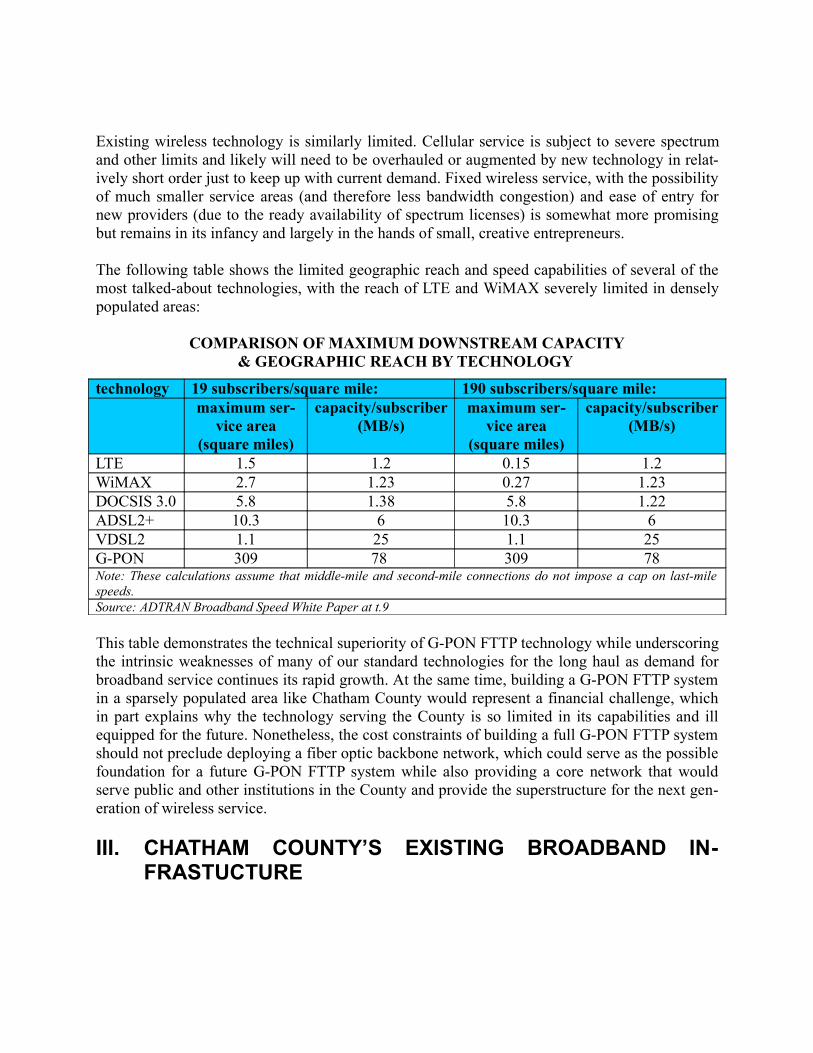

Summary of Capacity and Geographic Limits of Key Broadband Options [§ II.D]:

The most future-proofed and powerful technologies are two technologies that rely heavily on fiber optic connections: G-PON FTTP technology and VDSL2, with G-PON being more fiber rich than VDSL2 and having a decided advantage over VDSL2. A close examination of other broadband options, whether wireless or wireline, reveals the intrinsic weaknesses of most com-monly available broadband technologies and suggests that Chatham County is not equipped to respond to continued growth in broadband demand over the long haul. The cost constraints of building a full G-PON FTTP system should not preclude deploying a fiber optic backbone net-work. Such a network could serve as the possible foundation for a future G-PON FTTP system while also providing a core network that would serve public and other institutions in the County and provide the superstructure for the next generation of wireless service whether or not a com-plete G-PON FTTP system is ever deployed.

CHATHAM COUNTY’S EXISTING BROADBAND I NFRASTRUCTURE [§ III]

Chatham County’s existing array of broadband providers consist of seven wireline providers and an equal number of wireless providers.

Wireline Providers [§ III.A]:

Chatham County’s seven wireline providers include five telephone companies and two cable companies. Each of the five telephone companies has its own service area and generally does not cross its service area boundaries to provide broadband service in adjacent service areas. The two cable companies compete with the local telephone company in their service territories but have limited service areas and no plans to expand those service areas.

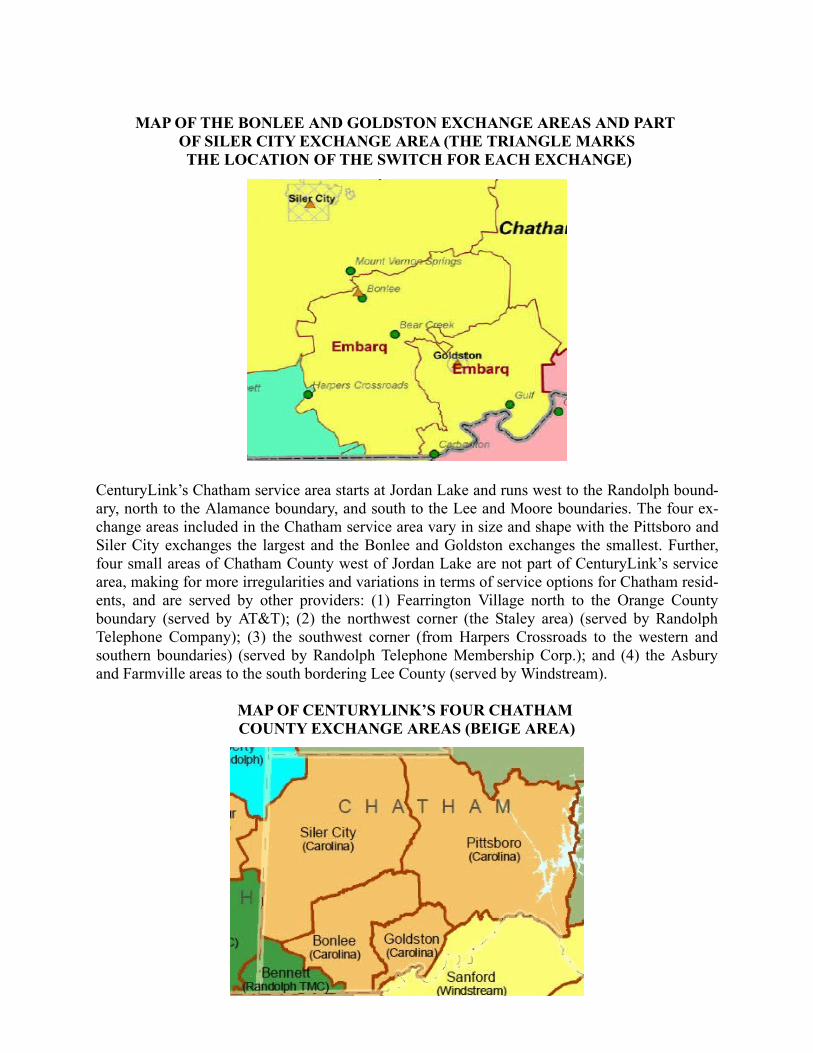

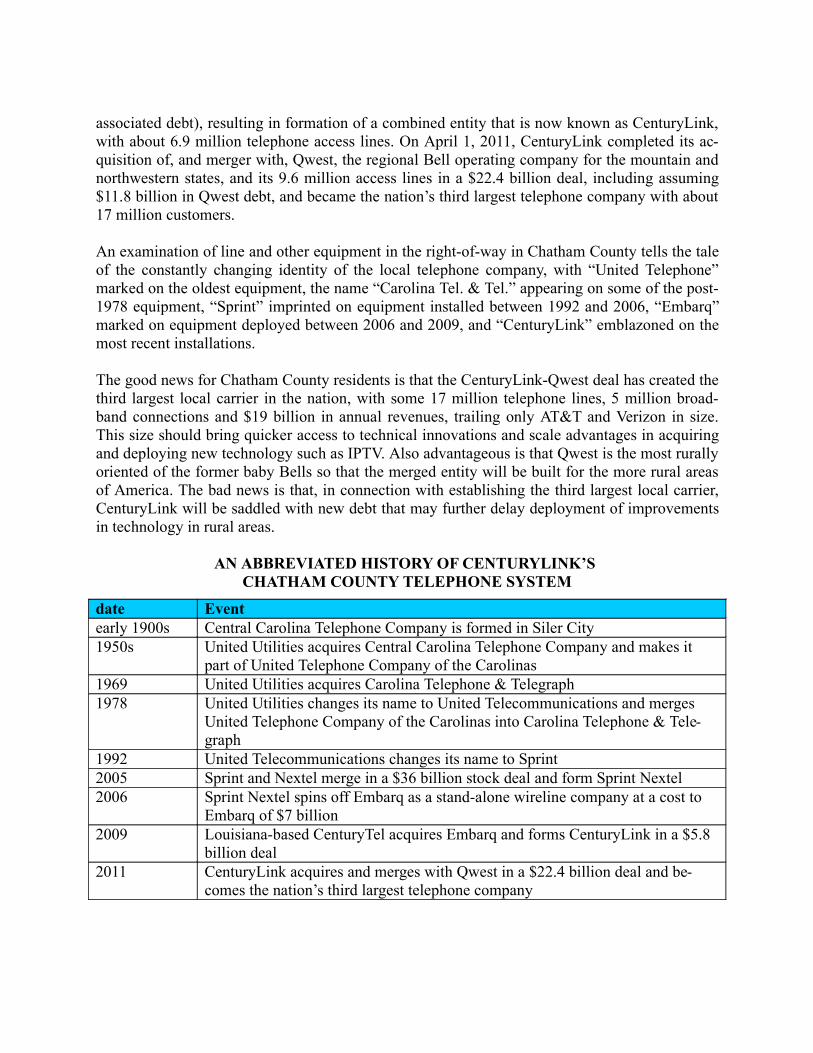

The five telephone companies [§ III.A.1] are CenturyLink, AT&T, Randolph, Windstream, and Frontier (formerly Verizon). One of these five, CenturyLink, is the County’s dominant wireline provider. In terms of size and reach it is followed by another telephone company, AT&T, and then the County’s two cable companies (Time Warner Cable and Charter). Three other telephone

companies—Randolph, Windstream, and Frontier—claim small pieces of the County at its corners and southern edge.

The County’s two cable companies [§ III.A.2]—Charter Communications and Time Warner Cable—serve roughly 5,250 subscribers in unincorporated areas of the County and in the towns of Siler City and Pittsboro or about 20% of the 25,845 occupied housing units in the County. The two cable providers have focused primarily on two incorporated areas, Pittsboro and Siler City, with Time Warner Cable also venturing into several of the major new developments in the County’s Chapel Hill area. The current service areas of both cable companies are primarily defined and limited by corporate investment practices and business preferences. Neither com-pany has any real interest in going outside their existing limited footprints (except for “green-field” developments in the case of TWC).

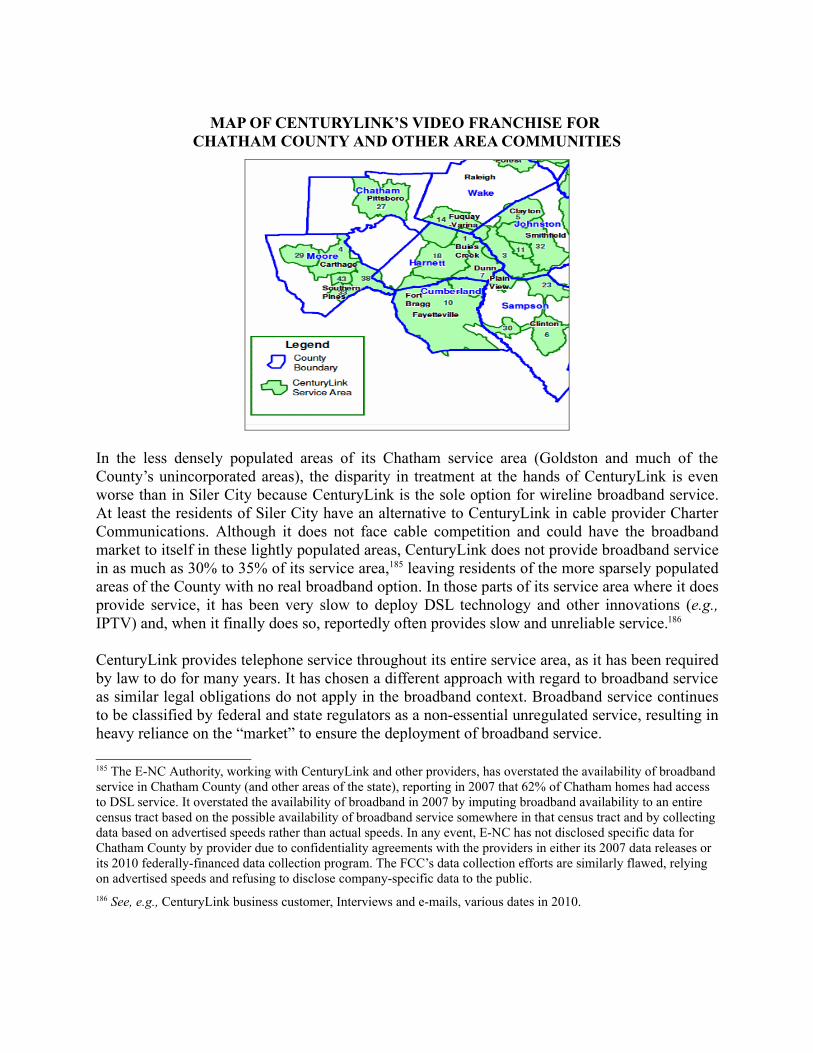

CenturyLink [§ III.A.1.a] serves about 71.1% of the Chatham County’s geographic area and 68.7% of its homes, including the County’s three municipalities (Siler City, Pittsboro, and Gold-ston) and much of central and western Chatham County. CenturyLink’s primary focus is on the more densely populated municipalities and their immediate environs, leaving broad swaths of the County with either no broadband service or low-quality broadband service.

CenturyLink acknowledges employing density-related requirements and other investment-related calculations to determine whether to invest in broadband-related network improvements in Chatham County and the rest of its service area.

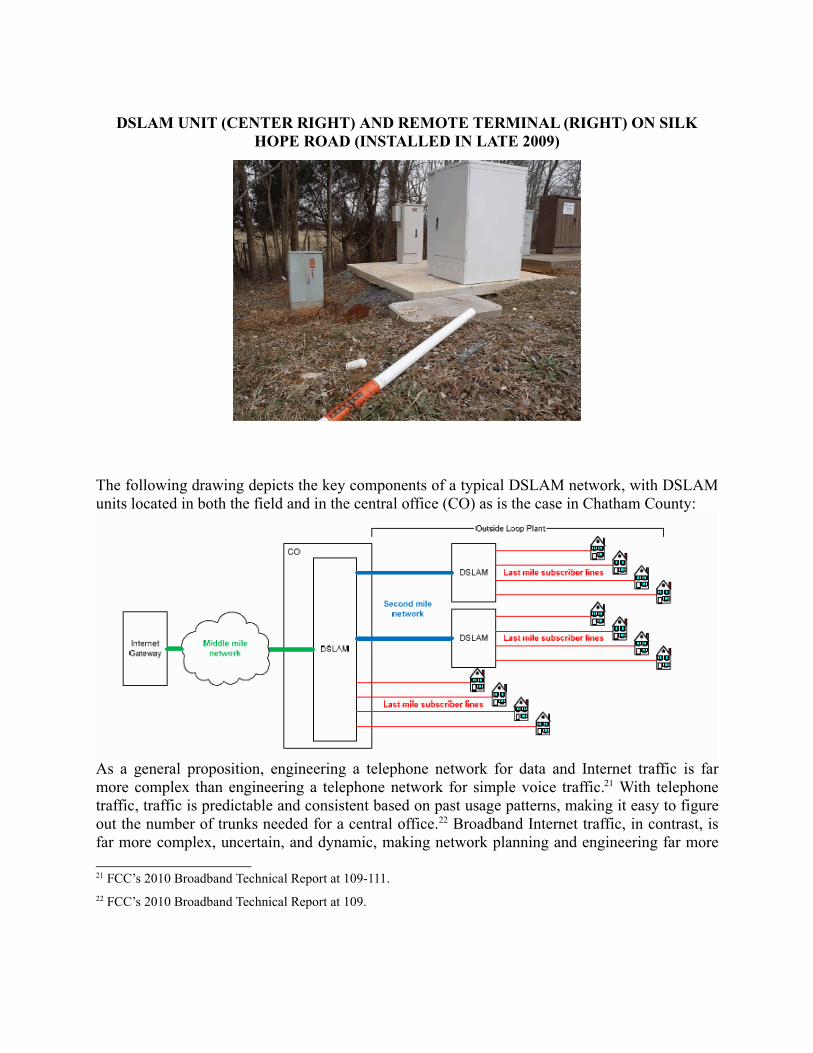

DSL was first deployed in Siler City and Pittsboro in 2002, Bonlee in 2005, Goldston in 2006, and Moncure in 2007. DSLAMs were installed even later in the Silk Hope area (2008 and 2009 time frame); Mt. Vernon Springs, south of Bonlee, and west of Pittsboro along US 64 (2010); and the Staley area (2011). These dates indicate that large parts of Chatham County lag behind the more urbanized areas of the state by six to ten years.

CenturyLink’s uneven performance has had, and will continue to have, adverse consequences for Chatham County, especially western Chatham County where CenturyLink is the only possible source of wireline broadband service for the vast majority of residents. CenturyLink provides better broadband service in the more densely populated areas of the County where it also faces cable competition (e.g., Pittsboro, Siler City).

Population density does not itself ensure high-quality broadband service as CenturyLink provides better service in Pittsboro than in Siler City although Siler City is more than twice as densely populated as Pittsboro. CenturyLink’s second-class treatment of different parts of the County is brought into sharp relief by its recent disclosure of plans to deploy new advanced broadband services (IPTV video services) in its Pittsboro exchange area but not in its Siler City, Bonlee, and Goldston exchange areas.

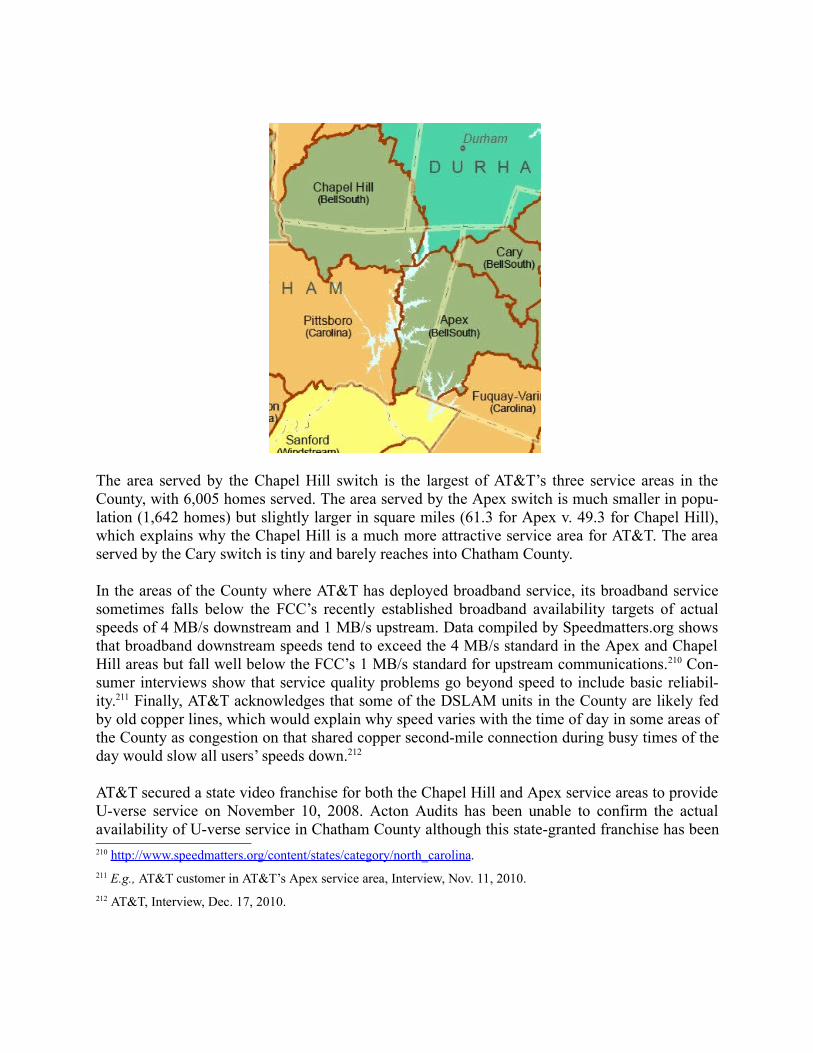

AT&T [§ III.A.1.b] (formerly BellSouth) serves about 16.4% of the Chatham County’s geo-

graphic area and 27.5% of its homes and covers about 110 square miles of the County. AT&T does not provide broadband service throughout its service area, leaving pockets of its service area, particularly low-income and minority communities, with no broadband service. In other areas, it provides low-quality broadband service due to poorly equipped DSLAM units and poorly maintained telephone lines.

AT&T states that it has begun to deploy its premier video service product (the U-verse package) in Chatham County. However, spot checks failed to turn up any evidence of U-verse availability so the number of U-verse customers in Chatham County is likely very small and limited to the Chapel Hill and Cary areas. U-verse technology requires installing a fiber-fed “Video Ready Ac-cess Device” or VRAD within no more than 3,000 feet or so of the customer’s home. AT&T’s VRAD technology is not compatible with its DSLAM technology, which means that the existing remote DSLAM units cannot be converted to U-verse use. This basic incompatibility between AT&T’s DSLAM and U-verse technology means that a substantial investment will be required to fully deploy U-verse technology throughout AT&T’s 110 square mile service area in Chatham County. Based on these underlying metrics, it is unlikely that AT&T will invest in U-verse tech-nology in the County in any area other than the most densely populated subdivisions directly within the orbit of Chapel Hill and Cary.

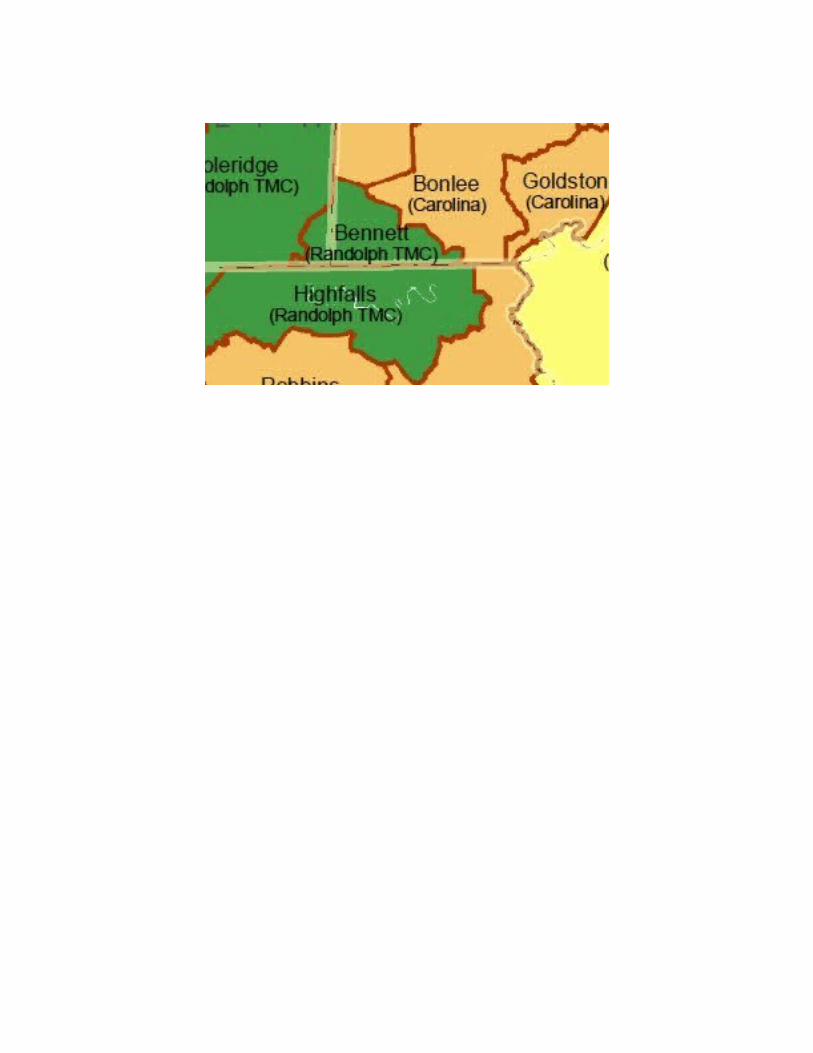

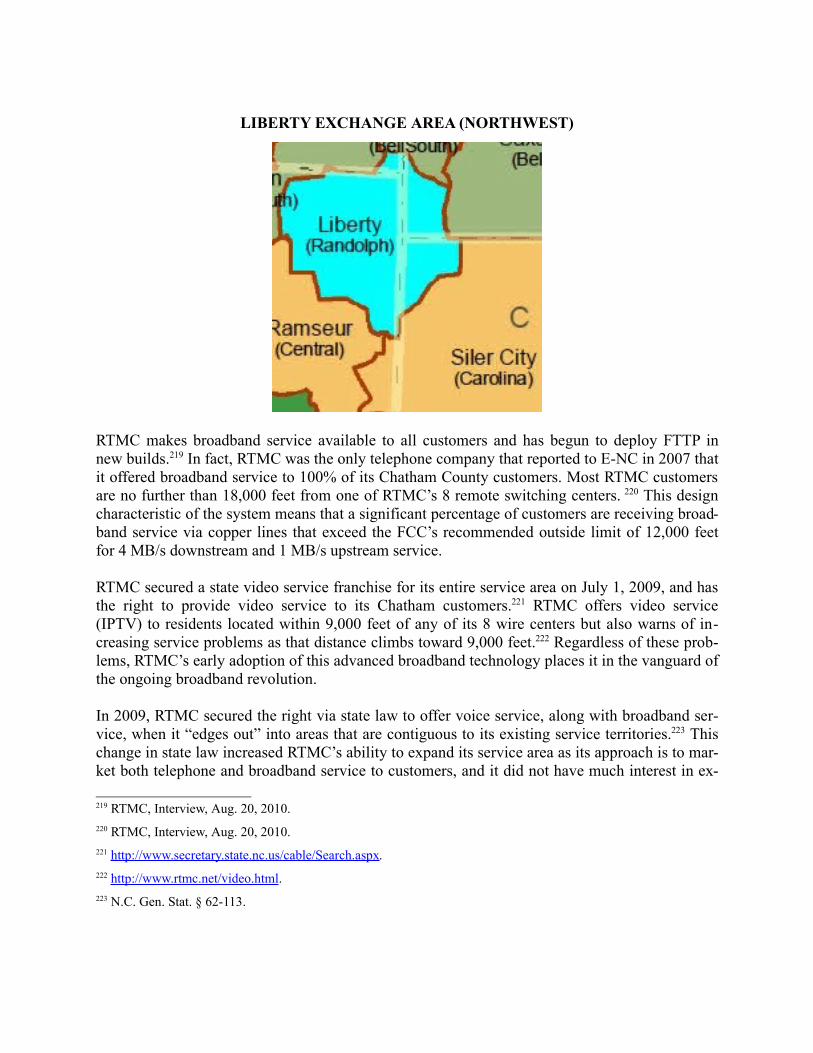

Randolph Telephone Membership Corp. [§ III.A.1.c] (RTMC) serves about 5.6% of Chatham County’s geographic area and 3.8% of its homes and covers about 38 square miles in the County. Its Bennett service area consists of the southwest corner of Chatham County while its Liberty service area occupies the County’s northwest corner.

RTMC makes broadband service available to all customers and has begun to deploy FTTP in new builds. RTMC offers video service (IPTV) to residents located within 9,000 feet of any of its 8 wire centers. RTMC is the most nimble and innovative and the most unconstrained by top-down corporate culture of Chatham County’s seven wireline providers. It is well equipped to play a role in helping to improve broadband in Chatham County but its first obligation is to serve its members (it is a non-profit organization), and it is constrained by its small size.

See also Windstream [§ III.A.1.d] and Frontier [§ III.A.1.e] for additional detail on two other telephone companies with small service areas in the County.

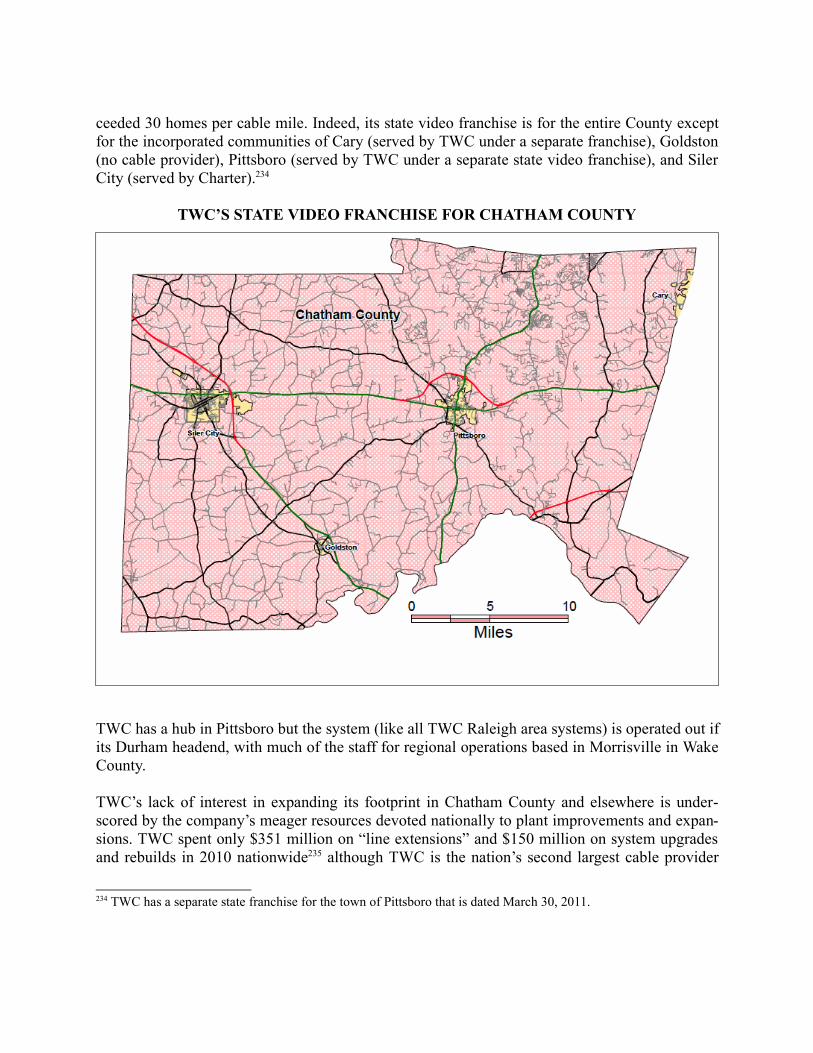

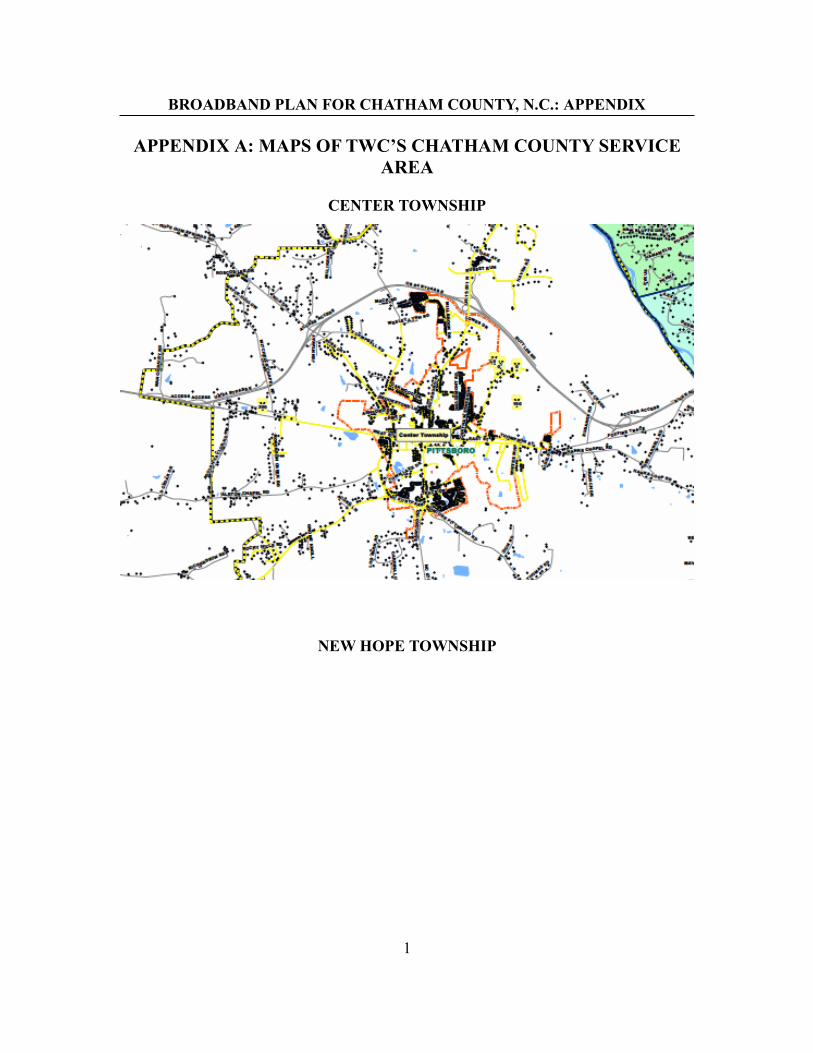

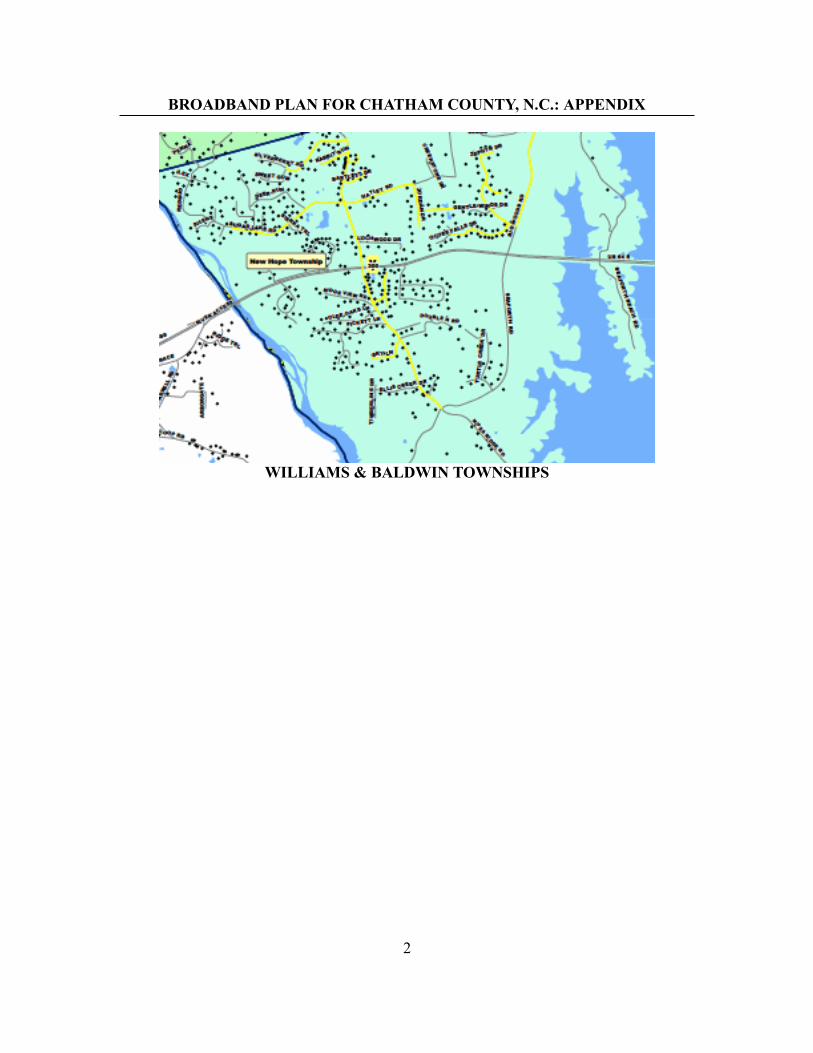

Time Warner Cable [§ III.A.2.a] is the larger of the two cable providers, with roughly 3,750 subscribers and franchises for the town of Pittsboro and unincorporated areas of the County. In venturing outside of Pittsboro, TWC has preferred greenfield developments and well-populated subdivisions, serving such developments as the Preserve, Fearrington Village, Governors Village, and Briar Chapel. TWC picks and chooses the locations to be served because TWC’s soon-to-ex-pire County franchise requires only that TWC provide service in areas with at least 30 homes per “cable mile.” TWC has relied on this provision to simply skip over entire subdivisions, streets, and roads on the way to provide service to other areas that have more attractive demographic or density characteristics. TWC provides no service in western or southern Chatham County al-

though it is entitled to operate throughout the County.

TWC is the slowest of the major cable providers to deploy state-of-the-art modem service, with DOCSIS 3.0 not reaching North Carolina (Charlotte) until 2010 and the Raleigh area until April of 2011.

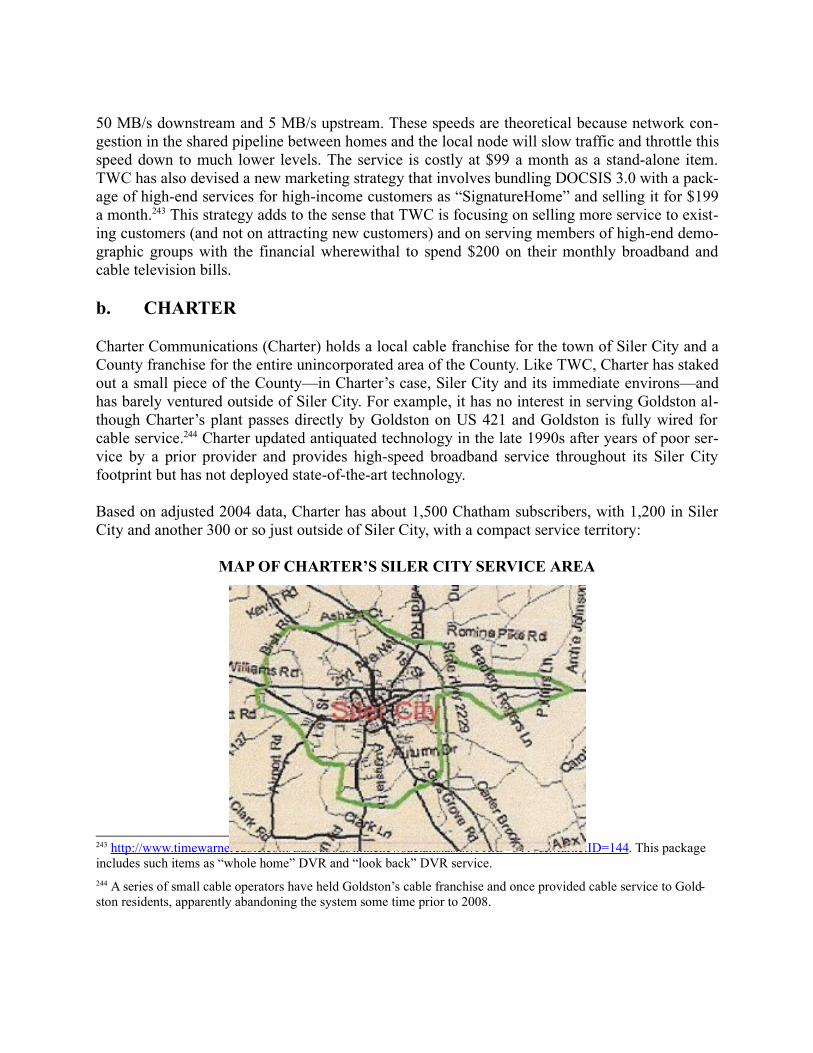

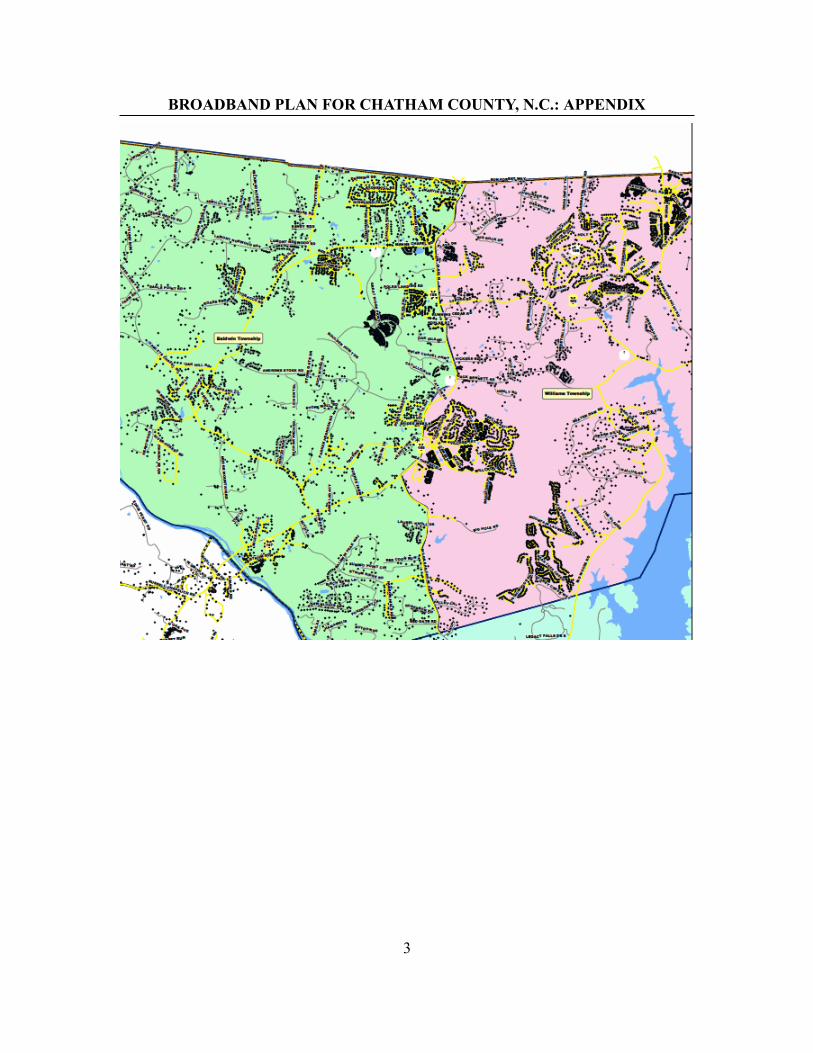

Charter [§ III.A.2.b] holds a local cable franchise for the town of Siler City and a County fran-chise for the entire unincorporated area of the County and serves about 1,500 subscribers. Like TWC, Charter has staked out a small piece of the County—Siler City and its immediate environs—and has barely ventured outside of Siler City. It has no interest in serving Goldston although Charter’s plant passes directly by Goldston on US 421 and Goldston is fully wired for cable ser-vice.

Charter updated antiquated technology in the late 1990s after years of poor service by a prior provider and provides high-speed broadband service throughout its Siler City footprint but has not deployed state-of-the-art technology. Charter’s system carries about 20 fewer analog chan-nels than TWC’s Chatham system and is likely a 550 MHz cable system. The industry standard is 750 to 860 MHz, meaning that the Siler City system is substandard and probably will not be able to carry some of the new services expected to be deployed in the future.

Wireless Providers [III.B]:

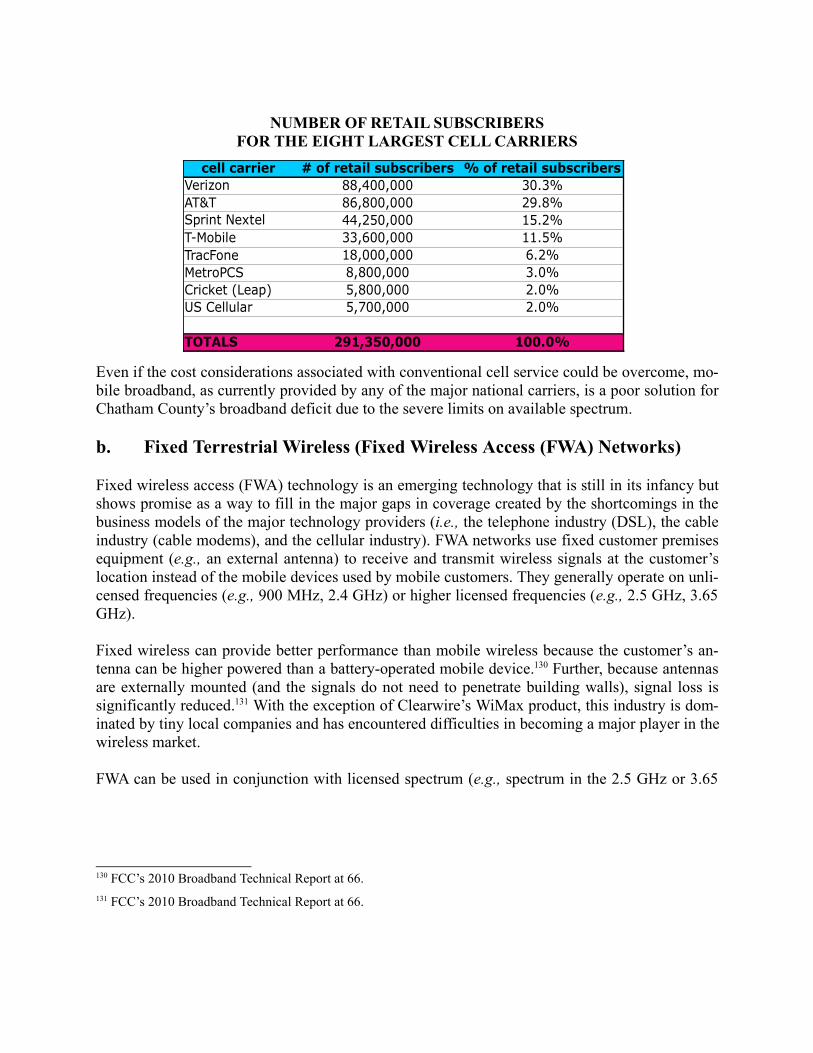

A total of seven terrestrial wireless providers [§ III.B.1], including six mobile wireless pro-viders [§ III.B.1.a] (i.e., conventional cell service providers) and one fixed wireless provider [§ III.B.1.b], operate in the County. Only one of these seven providers, Verizon Wireless, provides close to countywide service and only one, Chatham Wireless, provides high-speed service that meets the minimum Internet speeds that the FCC has determined are necessary for participating in contemporary society: 4 MB/s downstream and 1 MB/s upstream.

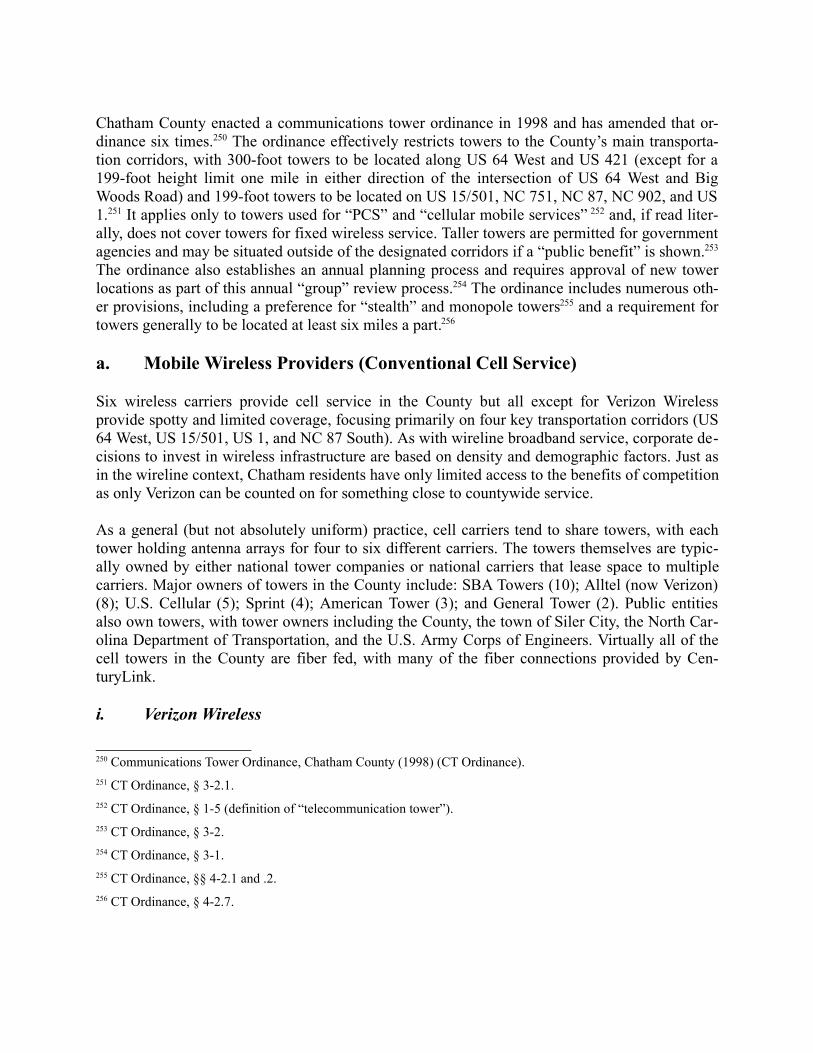

Verizon Wireless [§ III.B.1.a.i] provides the most coverage in Chatham County but wireless broadband service generally is a hit-or-miss proposition and a slow proposition in many parts of the County. All but one of the six wireless carriers (with Verizon Wireless the exception) provide spotty and limited coverage, focusing primarily on four key transportation corridors (US 64 West, US 15/501, US 1, and NC 87 South).

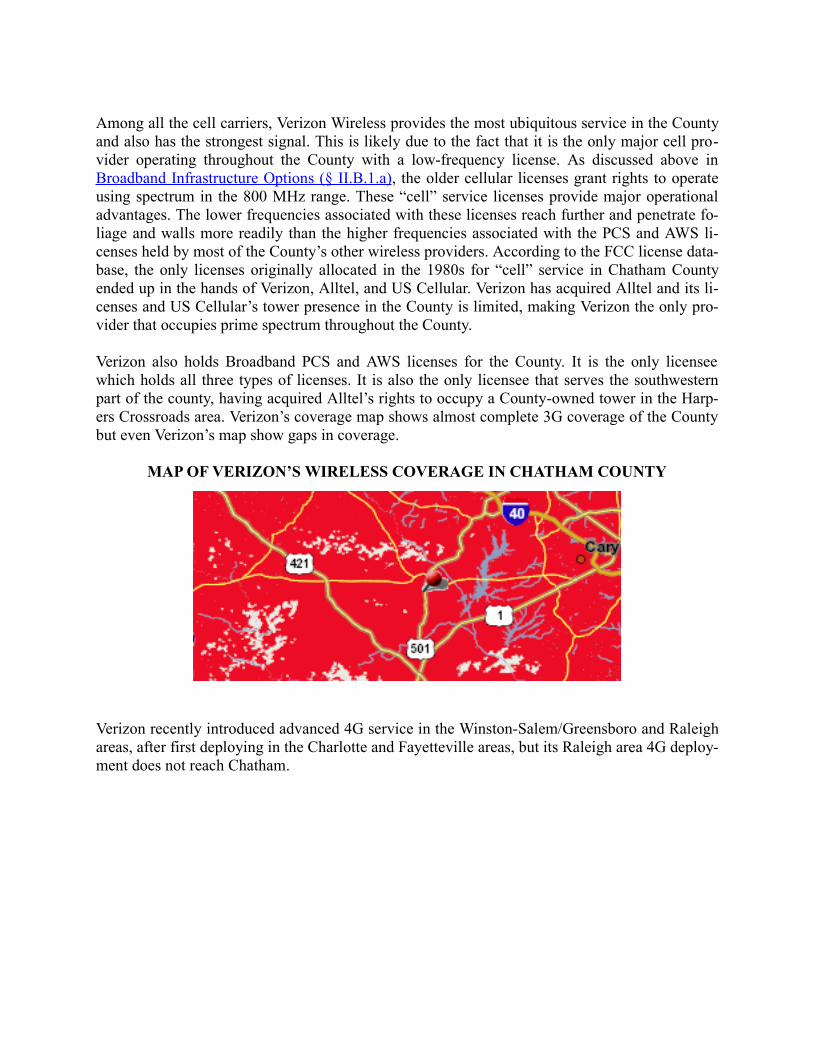

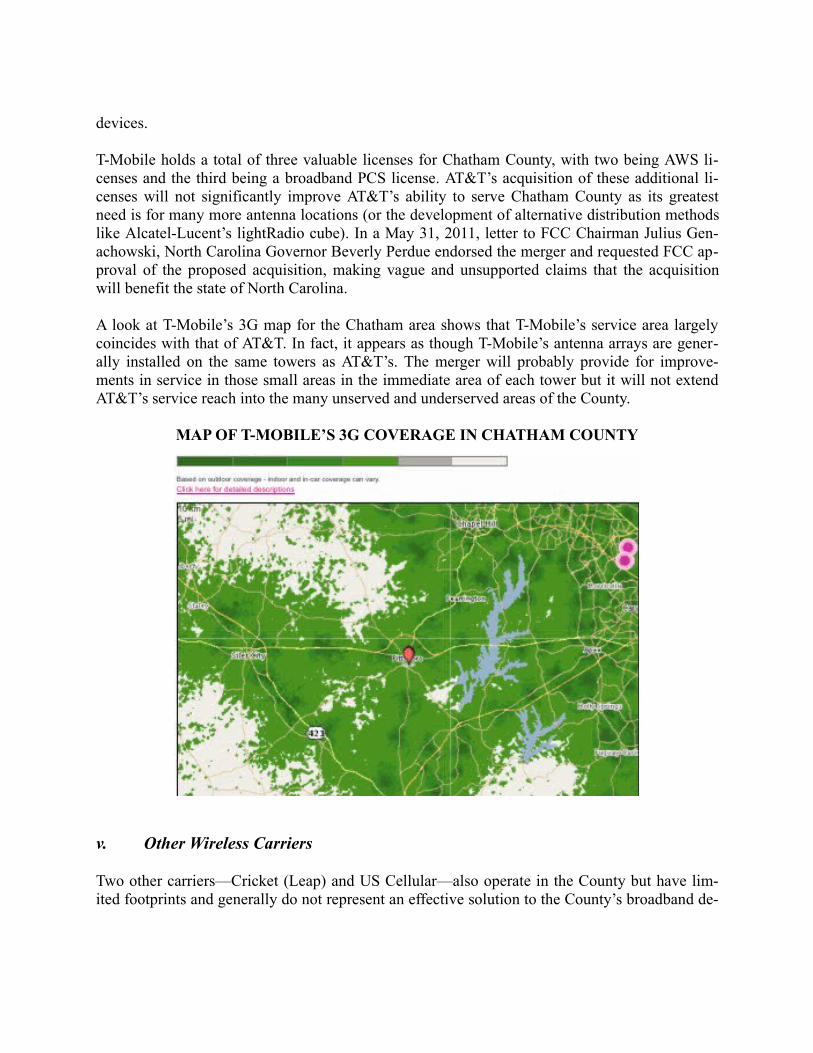

Verizon Wireless provides the most ubiquitous service in the County and also has the strongest signal. This is likely due to the fact that it is the only major cell provider operating throughout the County with an older low-frequency license. These older cellular licenses for spectrum in the 800 MHz range provide major operational advantages. The lower frequencies associated with these older cell licenses reach further and penetrate foliage and walls more readily than do the higher frequencies associated with the broadband personal communications service (PCS) and advanced wireless service (AWS) licenses held by AT&T Wireless [§ III.B.1.a.ii], Sprint/Nextel [§ III.B.1.a.iii], T-Mobile [§ III.B.1.a.iv] , and Cricket (Leap). Other wireless carriers [§

III.B.1.a.v] serving the county in addition to Cricket include US Cellular. Other than Verizon Wireless, US Cellular is the only wireless carrier operating in the County that holds an 800 MHz license but its tower presence in the County is limited, making it a poor alternative to Verizon.

As with wireline broadband service, corporate decisions to invest in wireless infrastructure are based on density and demographic factors. For example, Verizon Wireless recently activated 4G service in the Raleigh area but 4G service basically stops at Chatham’s border, limiting the abil-ity of Chatham residents to obtain access to the latest advances in wireless technology. Cell carri-ers tend to share towers, with each tower holding antenna arrays for four to six different carriers. Even so, many of the wireless carriers have chosen not to install antennas as pervasively as they could in the county, simply leaving certain portions of the county unserved. Just as in the wire-line context, Chatham residents have only limited access to the benefits of competition as only Verizon can be counted on for anything close to countywide service.

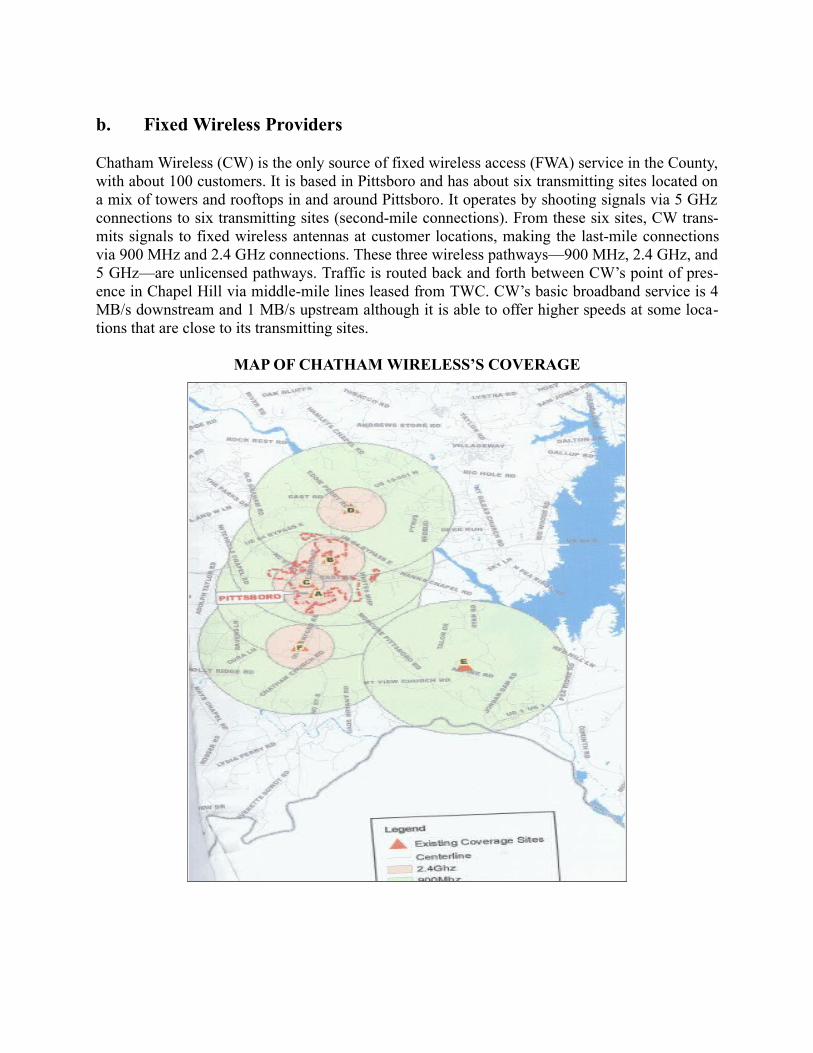

Chatham Wireless [§ III.B.1.b], the only known operational fixed wireless provider in the County, operates in the Pittsboro area where a small number of customers have access to high-speed broadband service. It has about six transmitting sites located on a mixture of towers and rooftops in and around Pittsboro. It operates by shooting signals via 5 GHz connections to the six transmitting sites. From these six sites, Chatham Wireless transmits signals to fixed wireless an-tennas at customer locations, making the last-mile connections via 900 MHz and 2.4 GHz con-nections, but the 2.4 GHz signals reach only a short distance. These three wireless pathways—900 MHz, 2.4 GHz, and 5 GHz—are unlicensed pathways. Chatham Wireless’s basic broadband service is 4 MB/s downstream and 1 MB/s upstream although it is able to offer higher speeds at some locations that are close to its transmitting sites.

Chatham Wireless’s disadvantages include the high cost of middle-mile service and effective control of the middle-mile market in Chatham County by competing broadband providers, Cen-turyLink and TWC. Another barrier to entry is the need for a large numbers of towers and other high points for transmitting sites and the cost of acquiring the necessary transmitting sites at the right locations.

Satellite [§ III.B.2] service is also available in most parts of the County from HughesNet and Vi-aSat (WildBlue) but is a flawed, limited, and expensive option due to the intrinsic limits of geo-synchronous-orbiting satellites.

Middle-mile Providers [ see § III.C]:

Small service providers such as Chatham Wireless and other possible new entrants are captive customers of their competitors for middle-mile connections to the Internet (e.g., CenturyLink and Time Warner Cable). Alternative pathways to the Internet via independent middle-mile connec-tions such as the MCNC network will open new possibilities for the development of alternative wireless and wireline networks.

The federal government (with a hand from the Golden Leaf Foundation) is financing a publicly-controlled 1,800-mile fiber optic middle-mile network for both public and private providers. MCNC is a non-profit organization, designated by the state of North Carolina several years ago to help community colleges, local educational authorities, and other similar institutions obtain access to Internet service. When this $146 million project is complete, MCNC will go from be-ing an intermediary between public entities and the private sector (a sort of collective purchasing agent) to being an independent provider of middle-mile service.

This new network, when completed in 2013, will be a state-of-the-art high-capacity fiber optic middle-mile network with points of presence at strategic locations throughout the state. With this new middle-mile network, MCNC will, for the first time, provide open access to the Internet at affordable rates that will be accessible to not only school systems and community colleges but also municipalities, counties, and other broadband providers. The closest point of presence for connecting to this network will be in Sanford.

BROADBAND APPLICATIONS AND USES [§ IV]

Broadband has managed to become a central component of our basic infrastructure in roughly a 10-year time span and will assume an even larger and more central role over the next 10 years and beyond. Most Americans already cannot function in their daily lives without access to broadband. To fully and effectively participate in the economy and society of the future, all Chatham residents need to, at a minimum, have the option of access to an affordable, high-quality broadband infrastructure just as, for many decades, they have had access to roads, highways, and electricity.

Broadband has already assumed a central role in the daily lives of most Americans as is evident in the five areas of established broadband use [§ IV.A]:

Education [§ IV.A.1] Economic development and job creation [§ IV.A.2] Personal communications, financial transactions, and entertainment [§ IV.A.3] Public safety [§ IV.A.4] Government services and civic engagement [§ IV.A.5]

In other areas, broadband has just begun to scratch the surface, with the start of the widespread deployment of networked sensors and other devices like cameras. As more and more of these connected sensors and devices are deployed in our environment, broadband will likely contribute to radical changes in our lives in many areas, including in four areas of emerging broadband use [§ IV.B]:

Health care [§ IV.B.1] Energy and utility use (management and control) [§ IV.B.2]

Transportation [§ IV.B.3] Smart communities [§ IV.B.4]

LEGAL BARRIERS TO COMPETITION AND INNOV ATION [§ V]

North Carolina law imposes sharp limits on competition by public sector entities [§ V.A] in the broadband and telecommunications market. These strict limits, which apply to member-owned cooperatives as well as municipalities, require careful planning by public entities and tend to fa-vor collaborative arrangements with the private sector as a more pragmatic and realistic way to address community broadband deficits. North Carolina counties have largely been on the side lines in the broadband area and have not tested the limits of their authority, leaving leadership to municipalities, which had broad legal authority until the legislature intervened in May of 2011 to tear the broadband wings off cities and towns.

County Authority [§§ V.A.1 and V.A.3]

North Carolina law grants counties broad authority to own property and lease property to third parties. This authority opens the way for broadband partnerships as state law imposes no definit-ive limits on the type of property that counties may own. For example, state law does not appear to prevent a county from owning a portion of the local broadband infrastructure, using the infra-structure for governmental and related functions, and then leasing portions of the infrastructure to third parties to serve the residential market. Similarly, nothing in state law precludes a county from being the anchor tenant in a partnership with a private partner that would build and own the infrastructure to specifications designed by a county to protect its long-term needs.

North Carolina law does not grant counties authority to become direct, retail providers of broad-band service and is unlikely to do so in the foreseeable future. In view of the history of hostility in the state legislature to publicly-operated cable and broadband systems, the prudent and prac-tical course would be for the County to focus on a partnership approach.

See also Municipal Authority [§ V.A.2], Authority of Telephone Cooperatives [§ V.A.4], and Authority of Electric Cooperatives [§ V.A.5] for other limits applicable to public sector entities.

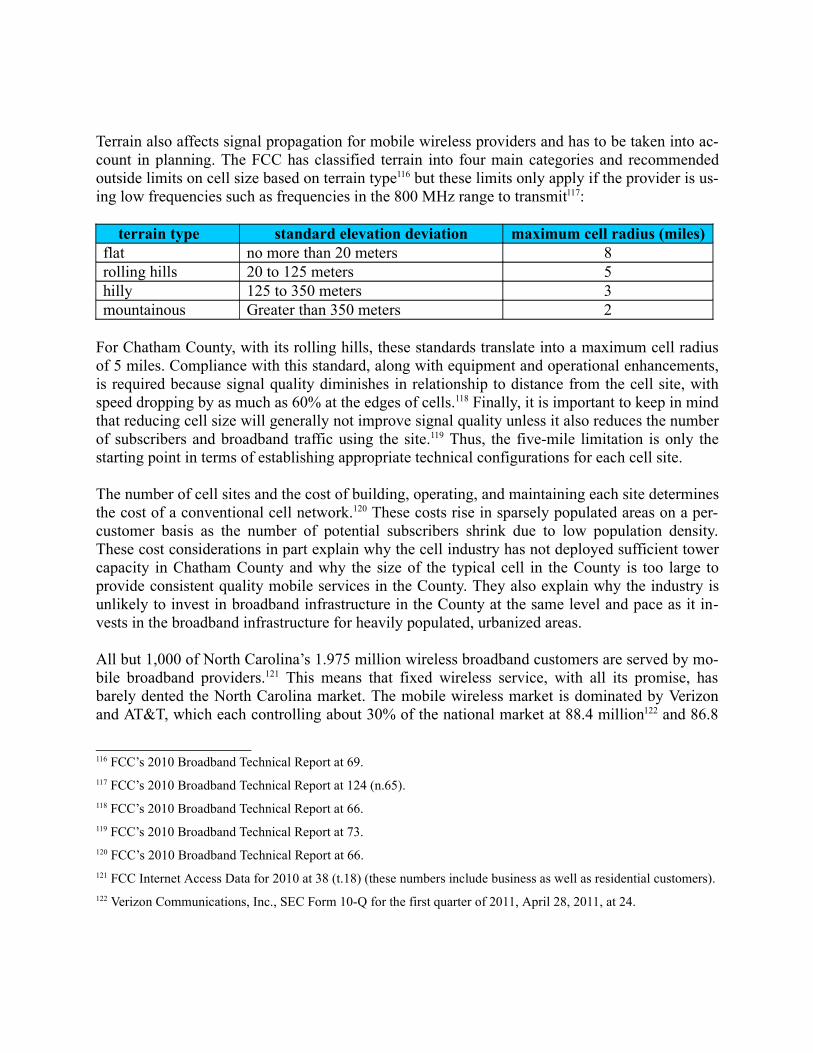

See also Limits on Private Sector Providers [§ V.B], including Service Territory Limits [§ V.B.1], Federal Subsidy Programs [§ V.B.2], and Spectrum Allocations [§ V.B.3].

RECOMMENDATIONS

Chatham County’s overall approach [§ VI.A] to addressing broadband-related needs should include: (1) improving access to service as a baseline matter (universal access to broadband service for all County residents); and (2) improving broadband speed and service quality both

now and in the future. Achieving the first goal (universal access) will have lasting value only if County residents are also able to obtain early access to advances in broadband technology on an ongoing basis in the future and are able to keep up with more urbanized areas of North Carolina and with other states.

In practical terms, meeting these needs requires that broadband service be available throughout the County and that it be updated to comply with the FCC’s new target for minimum broadband availability (4 MB/s downstream and 1 MB/s upstream). These FCC standards are interim standards and are likely to increase greatly in the future to accommodate new video intensive and other data-heavy applications as the FCC’s 2020 goal is for the vast majority of American homes to be served by broadband at speeds of 100 MB/s downstream and 50 MB/s upstream.

Long-term Broadband Plan [§ VI.B]:

Our central recommendation is to deploy a community-designed fiber optic backbone network:

The network should be ubiquitous, with as many laterals as possible into the County. Such a network would provide long-term cost controls and a future-proofed

broadband infrastructure. Fiber optics is the preferred transmission medium because of its almost unlimited

information-carrying capacity and the ease of upgrading.

The proposed network has three major goals:

It would take advantage of the collective buying power of area public institutions and more effectively deploy existing resources.

It would provide a bridge to affordable, scalable, and reliable middle-mile service (i.e., the MCNC network).

It would establish a pluggable, scalable, and expandable network that would provide a platform for development of new wireless and wireline networks.

The first step is to identify resources currently devoted to telecommunications and broadband by governmental entities and other public institutions:

These resources must be sufficient to cover the proposed network’s borrowing costs and operational costs for replacement services.

These resources should be deployed in a more targeted, planned, and effective way to develop a community-based broadband infrastructure.

The preliminary estimate of current direct expenditures (County and school district) is $625,000/year. This number is just the starting point and should be augmented by adding indirect expenditures on staff, vendors, and technical assistance to the mix.

Possible public sector partners include the towns of Siler City, Pittsboro, and

Goldston (they likely spend another $100,000 or so per year on broadband and telecommunications service).

Other possible public sector partners include: Central Carolina Community College and the new Chatham Hospital in Siler City.

The second step is to identify other project partners:

Possible partners that will need new wireless and wireline connections for smart grid include: Progress Energy, Central EMC, and Randolph EMC.

Chatham Park Investors will need an advanced broadband infrastructure for its new 30,000-person planned community in Pittsboro and south of Pittsboro (possible smart community).

Partnership opportunities should be looked at in terms of opportunities for the potential partner to become an anchor tenant for the proposed fiber backbone.

The third step is to rough out a basic technical design for the network. The network should be sufficiently versatile to support both wireless and wireline providers on a pluggable basis. The fourth step is to define cost parameters for network:

Basic assumptions about the network are that it would (1) connect key Chatham institutions and facilities together; and (2) provide the basic connections and platforms necessary to improve service in unserved and underserved areas to eventually support next-generation services throughout the County.

A feasibility study should be prepared by a third party who would develop a 10-year pro forma to establish the network’s financial viability.

The fifth step is to assess legal options as to ownership structure and identify the appropriate legal structure. The three main options are:

A public-private partnership between the County and an infrastructure provider: The County would own the infrastructure but a third party would construct and/or operate the network.

A public-private partnership between the County and an infrastructure provider: The provider would own the infrastructure, with the County centrally involved in developing the system.

A nonprofit or similar organization: This organization would develop and operate the infrastructure and would be governed by a representative cross-section of community interests and representatives.

Short-term Planning Steps [§ VI.C]:

First, the County should work with each of the seven existing wireline providers to look for

cooperative opportunities:

The major focus should be on CenturyLink as the County’s largest provider. Randolph TMC, with its advanced technology and new legal authority to “edge out”

into Chatham, and AT&T, with its big footprint in the County, should also be targeted. The two local cable providers, TWC and Charter, should also be approached but with

modest expectations due to their lack of interest in expanding their footprint in the County. But the “business group” divisions of both providers are more flexible and nimble and might be interested (Charter Business Group recently pulled together a tri-county network for Central Carolina Community College).

Second, the County should begin long-term planning discussions with possible smart grid providers, including:

The County’s three power companies (Progress Energy, Central EMC, and Randolph EMC)

Natural gas providers (PSNC Energy) Providers of water and sewer service (Chatham County, Siler City, Pittsboro); and Other pipeline providers

Third, the County should work with the Chatham Park Investors on their plans for new community to ensure a state-of-the-art broadband infrastructure such as a possible “smart community” and explore cooperative arrangements.

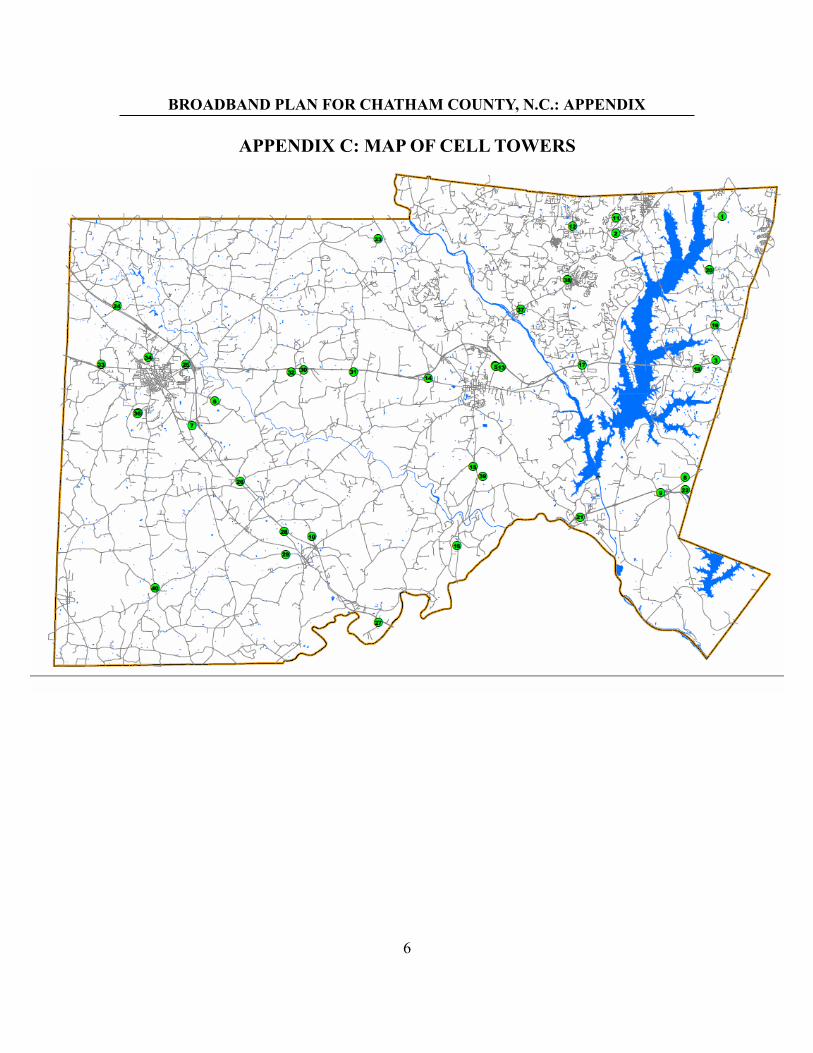

Fourth, the County should review its communications tower ordinance:

The current ordinance limits taller towers (300 feet) to US 64 West and US 421 and permits shorter towers (199 feet) on several other transportation corridors (US 1, US 15/501, NC 87, NC 751, NC 902) and may not work over the long haul.

In connection with this review, the County should develop a full inventory of other facilities and sites for transmitting sites for the next generation of wireless service.

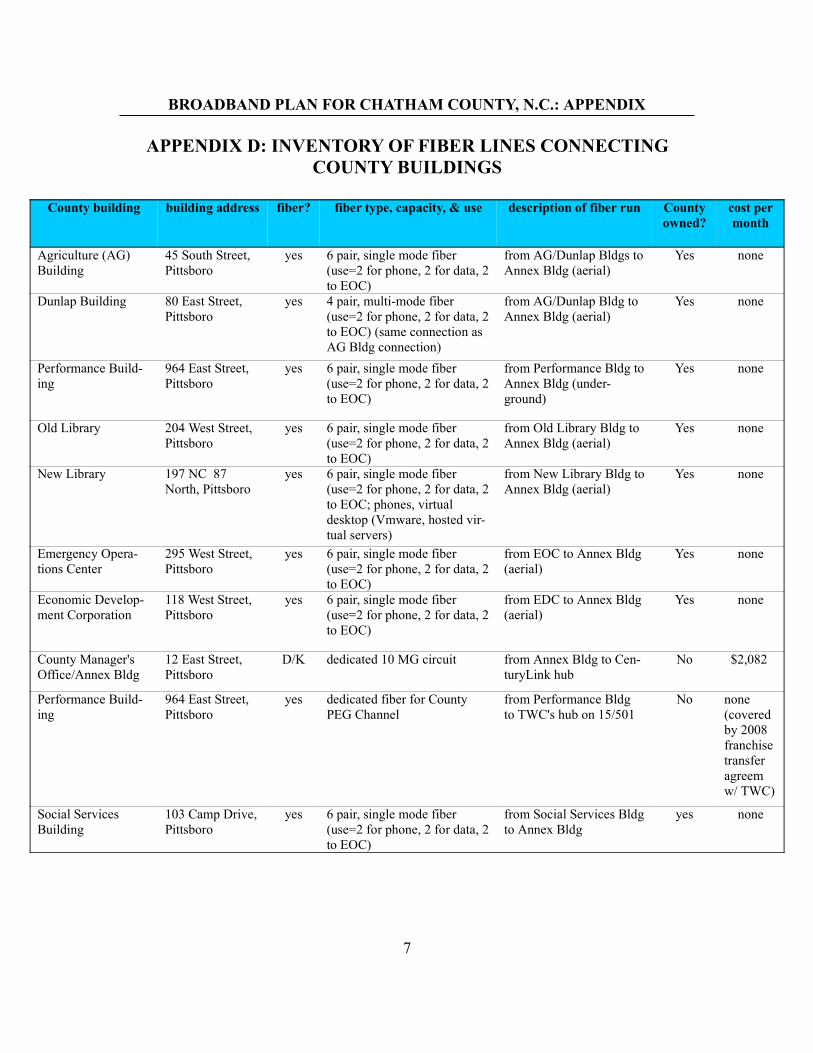

Fifth, the County should update the inventory of County-owned fiber and other communications lines (Appendix D):

All other County facilities that should be connected together by a County network should be identified.

Facilities not currently connected to the County network that are candidates for connection include: waste management facilities on Landfill Road; sheriff’s substations in Goldston, Governors Village, and Moncure; County facilities in Siler City (sheriff’s substation, Health Department, Council on Aging); a possible 911 back-up facility in Siler City; water distribution facilities scattered around the

County; EOC towers; park and recreation facilities; the Goldston and Siler City libraries; and the seven fire departments (and their sixteen fire stations).

Sixth, the County should work with the towns of Pittsboro, Siler City, and Goldston to develop a list similar to the list of County facilities for town and related facilities.

Seventh, the County should compile a detailed list of all direct and indirect expenditures by County, governmental, and other public entities on telecommunications and broadband:

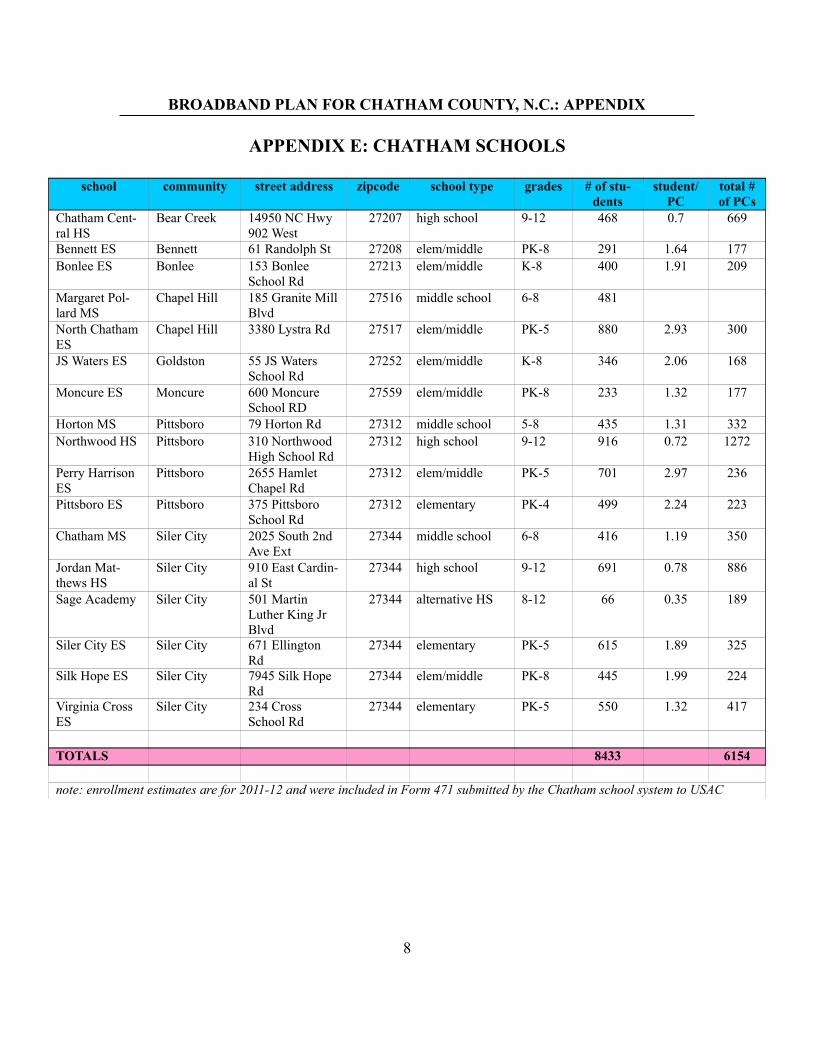

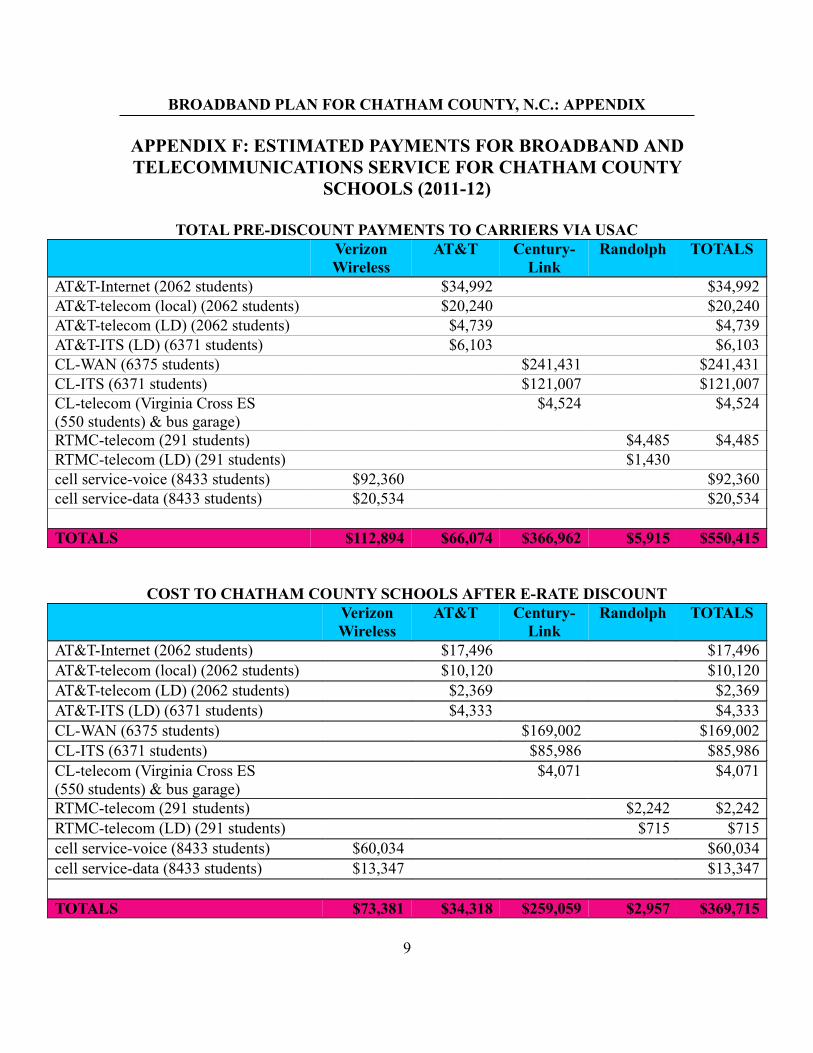

Direct expenditures by Chatham County Schools and Chatham County currently total $625,000 ($437,521 for Chatham County Schools; $187,812 or so for Chatham County).

All other direct and indirect expenditures should be identified.

Eighth, public agencies in the County should be required to coordinate to the extent possible regarding the purchase of communications services and equipment.

Ninth, the County should require all current broadband and cable providers to comply with their legal obligations, including:

Requiring Charter to comply with its existing County cable franchise (it runs until August of 2012) (requirements include connecting schools and public buildings in the Siler City area to Charter’s cable system)

Enforcing similar requirements that apply to all state cable franchisees (connect all public buildings to the cable system that are within 125 feet of the cable system)

Requiring compliance with PEG access requirements (the existing County franchises require Charter and TWC to carry the County’s channel and CCCC’s channel) (Charter and TWC recently came into partial compliance with these requirements for CCCC’s educational channel but are carrying it on the more expensive and less accessible digital tiers in violation of FCC policies)

Enforcing requirements that state cable franchisees carry PEG channels (monitor compliance by CenturyLink, AT&T, Randolph TMC, and TWC)

Tenth, the County should establish a simple complaint process for community feedback on broadband service problems and gaps in service that includes the following features:

Accessible both on-line and by telephone Simple and clear questions designed to collect information about provider name,

service availability, speed, affordability, reliability, and consistency Ability to document and map out (using the County’s GIS capabilities) service

patterns in the County and pinpoint serious service problems

Eleventh, the County should push for and seek proactive broadband advocacy programs at the

state and federal level:

These advocacy efforts should ensure recognition of broadband as a key infrastructure component of the future, especially for rural and semi-rural areas.

The County should work with the North Carolina Association of County Commissioners (NCACC) and the National Association of Counties (NACo) and through their policy processes to ensure that broadband receives priority attention on a going-forward basis.

I. INTRODUCTION AND BACKGROUND

This broadband infrastructure planning project is intended to provide a plan for improvements in broadband5 service in Chatham County, recognizing the central importance of an affordable, high-quality broadband infrastructure to the County’s future. Our research confirms that the County’s broadband deficit is substantial and also shows that it is likely to remain large and even widen in the future due to the private sector’s limited interest in investing in the County’s broadband infrastructure. Our central recommendation is that the County develop a plan to reprogram existing County and other public resources to establish an independent fiber optic backbone network for the County through a public-private partnership. This fiber optic backbone would serve the County’s governmental and other public institutions while also establishing a platform for new commercial and other providers to enter the market and offer wireline and wireless service to Chatham residents.

Getting from here to there will require additional planning by the County to flesh out the plan’s details, including its cost and the appropriate organizational structure for developing, owning, and operating the network, and to identify possible private partners for a public-private partnership.6

Core tasks in this project included securing data with regard to current broadband availability in the County, identifying broadband providers and their performance characteristics, identifying legal and other barriers affecting broadband providers, interviewing broadband providers, and identifying incentives and funding sources for broadband improvements.

A. BROADBAND AVAILABILITY IN CHATHAM COUNTY

We found existing data sources as to broadband availability in Chatham County (and elsewhere in the nation) to be flawed due to the providers’ consistent refusal to disclose most carrier-

5 In this context, broadband refers to a high-speed data connection to the Internet. Downstream or download broad-band speeds indicate how fast information can be delivered from the Internet to the customer while upstream or up-load broadband speeds refer to how fast information can be delivered from the customer to the Internet. Broadband speed is measured in “bits per second,” with a kilobit being one thousand bits and a megabit being a million bits. The Federal Communications Commission (FCC) initially defined broadband service in 1998 as any connection that delivered information at 200 kilobits per second (kb/s) in either direction or 3.5 times the speed of a standard dial-up connection of 56 kb/s. The FCC determined in 2010 that the minimum speed for adequate broadband service has ris-en to 4 megabits per second (MB/s) downstream and 1 MB/s upstream and will continue to rise in the future as new services are developed and adopted by consumers. 6 One project goal was to equip the County to apply for federal funds in the future in the event the federal govern-ment establishes a successor program to the broadband programs such as the Broadband Technologies Opportunity Program (BTOP) included in the 2009 American Recovery and Reinvestment Act (ARRA). In view of the stalemate in Congress on most spending matters and the close-to-nonexistent chance of renewal of the BTOP program in the foreseeable future, we ended up focusing on improving the County’s broadband infrastructure though a more creat-ive and aggressive use of the existing buying power of the County and other public institutions instead of seeking funds from third parties.

specific information as to numbers and locations of subscribers or solid information as to the carriers’ deployment of broadband technology in particular communities. This uncooperative attitude is aided and abetted by the alphabet soup of government agencies that have helped to wall

off basic information about network operations from the public by embracing expansive notions of what constitutes confidential information.

We started our data review by examining commercially available consumer data but found, because it was based on survey data, that it was unreliable due to consumer confusion about basic questions. For example, some survey respondents did not know the difference between broadband service delivered by a cable provider and broadband service delivered by a telephone company, resulting in data anomalies and inaccuracies. And of course, this consumer data was survey data, which is especially unreliable when the goal is to drill down to small, geographic areas and identify with precision the areas in the County where broadband coverage is non-existent or of unacceptably low quality.

Another possible data source was the E-NC-Authority, which has compiled broadband availability data for the County for both 2007 and 2010 and is the primary collector of broadband data for the state of North Carolina. Unfortunately, the E-NC Authority employed a flawed and limited methodology when it mapped out broadband availability in North Carolina on a county-by-county basis in both 2007 and its 2010 federally-funded effort7:

First, the E-NC Authority assumed that all residents of a census block have access to broadband service if a single broadband provider claims that even one household in a census block has access to broadband service.8 This technique greatly overstates the availability of broadband as, in a semi-rural county like Chatham, service is not delivered on a consistent or uniform basis throughout census blocks.

Second, the E-NC Authority did not disclose data on a provider-by-provider basis although it collected data on a provider basis. Due to confidentiality agreements it executed with the providers in both 2007 and 2010 (and permitted by the NTIA in 2010), it does not report such basic information as how many households in CenturyLink’s Chatham service territory have access to digital subscriber line (DSL) service and how many of them actually subscribe to that service.

Third, in both 2007 and 2010, the E-NC Authority allowed providers to report broadband availability based on advertised speeds even if that speed is not actually available at particular locations, greatly overstating both the availability of service and the speed with which it is delivered.

And fourth, the E-NC Authority did not report aggregate total numbers for broadband

7 Most of the flaws in the E-NC Authority’s collection methods for 2010 data are directly traceable to the adminis-tration of the federal data collection effort by the National Telecommunications and Information Administration (NTIA), which squandered about $350 million in federal funds by deeming virtually all important broadband in-formation collected through this program to be “confidential” and therefore not to be disclosed to the public (e.g., each provider’s footprint). State Broadband Data and Development Grant Program, Notice of Funds Availability and Solicitation of Applications, 74 Fed. Reg. 32,545-32,565, July 8, 2009. 8 The E-NC Authority’s 2007 methodology was slightly different but also flawed in that imputed broadband availab-ility to a wide geographic area (first to a three-mile radius circle around the wire center and then to the census tract(s) that contained any portion of the circle) regardless of whether broadband service was actually available.

customers in the County or any subset of the County in either 2007 or 2010. A user of the E-NC Authority website can obtain a list of available providers of broadband service and the advertised broadband speeds for each by County, address, and other geographical units but cannot map out the service territories of particular providers or obtain broadband subscribership numbers or penetration rate data for the County or other geographic units.

In view of the shortcomings of these data sources,9 we turned elsewhere and found data at the FCC and at an industry-financed non-profit organization (Connect North Carolina) that provides a clearer picture of the state of broadband in the County and more accurately tracks what we observed in the field and learned in consumer interviews.

FCC Data: The FCC collects extensive data twice a year from all broadband providers through FCC Form 477. In fact, the $350 million ARRA-funded NTIA data collection project more or less replicated the FCC’s existing data collection work only it did so less effectively and more clumsily by spreading data collection funds around to 51 or so state-based organizations like the E-NC Authority and by denying the public access to basic information. As with the NTIA, the FCC makes a commitment in the Form 477 process not to disclose carrier-specific data so the FCC’s publicly-released data is also far from complete. But the FCC did decide to release broadband penetration rate data on the basis of census tract for the first time in February of 2011, which provides important geographic detail as to access to broadband service in different parts of the County.

With the help of the County’s GIS Department, this FCC census tract data has been mapped out for this report. This map provides a clear picture of the areas where the broadband deficit in the County is the greatest in terms of home subscriptions, which are the western and southern parts of the County. The areas that are the most disadvantaged are the two 2000 census tracts west and south of Siler City, with broadband subscription rates of zero to 20% (this area includes Harpers Crossroads, Bear Creek, Bonlee, and Mount Vernon Springs). Next in terms of limited access to broadband service are the 2000 census tracts for Siler City and Goldston at 20% to 40% subscription rates. The area with the highest subscription rate (and therefore the greatest access to the broadband world) is the 2000 census tract for the Chapel Hill area, with a 80% to 100% subscription rate. The other three 2000 census tracts (north of Siler City, Pittsboro, and east of Jordan Lake) fall in between the two extremes, with subscription rates of 60% to 80%.

9 Through a series of statistical gimmicks and gyrations (detailed above), NTIA, working with the E-NC Authority, has generated data reporting that Chatham ranks 48th among North Carolina’s 100 counties in terms of broadband availability and that 83% of Chatham’s residents have access to DSL service, 59% have access to cable modem ser-vice, and 91% have access to wireless broadband service. See http://www.broadbandmap.gov/analyze for more de-tails. As will be documented later in this report, these numbers do not take into account service quality or speed or specify when broadband technology was deployed in the County in comparison to more urbanized areas.

BROADBAND SUBSCRIPTION RATES ON THE BASIS OF FCC CENSUS TRACT DATA FOR CHATHAM COUNTY

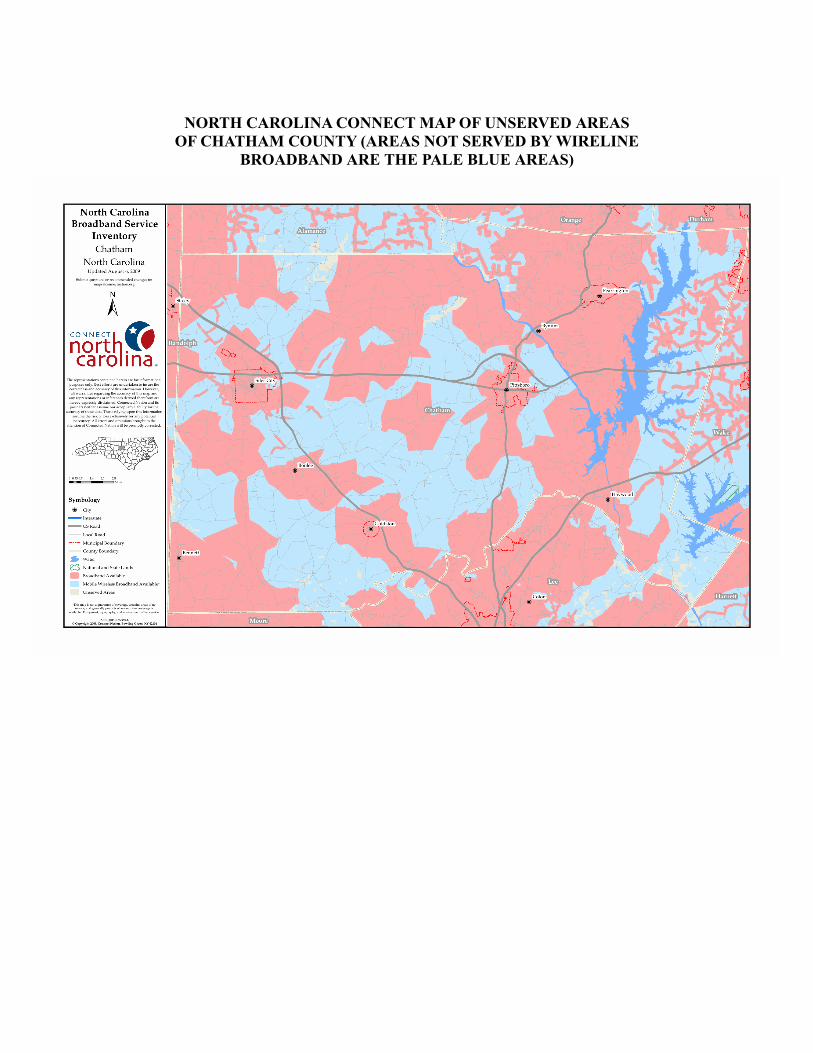

Connect North Carolina’s maps complement and explain this data by identifying with more precision the pockets of the County that lacked access to broadband service in August of 2009. The Connect North Carolina project was part of a national industry-financed data collection effort through an organization known as Connected Nation. It collected data from providers and released maps showing the many areas of the County that were unserved in August of 2009. Since this data was compiled, CenturyLink has extended service into some of these unserved areas. Nonetheless, this map provides stark evidence as to the areas that have lagged behind other areas of the County by a matter of years and, by the industry’s own admission as to its reliance on density and similar factors in making investment decisions, will likely lag behind in a similar fashion with the deployment of each new generation of broadband technology.

NORTH CAROLINA CONNECT MAP OF UNSERVED AREASOF CHATHAM COUNTY (AREAS NOT SERVED BY WIRELINE

BROADBAND ARE THE PALE BLUE AREAS)

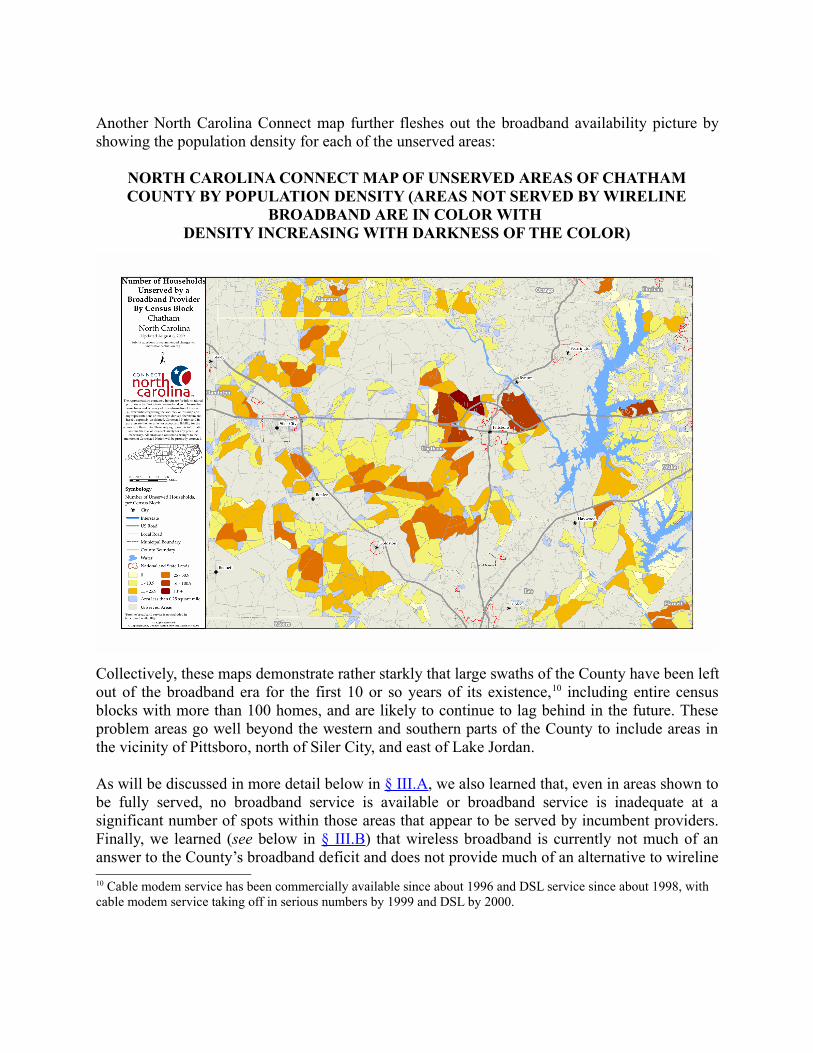

Another North Carolina Connect map further fleshes out the broadband availability picture by showing the population density for each of the unserved areas:

NORTH CAROLINA CONNECT MAP OF UNSERVED AREAS OF CHATHAM COUNTY BY POPULATION DENSITY (AREAS NOT SERVED BY WIRELINE

BROADBAND ARE IN COLOR WITH DENSITY INCREASING WITH DARKNESS OF THE COLOR)

Collectively, these maps demonstrate rather starkly that large swaths of the County have been left out of the broadband era for the first 10 or so years of its existence,10 including entire census blocks with more than 100 homes, and are likely to continue to lag behind in the future. These problem areas go well beyond the western and southern parts of the County to include areas in the vicinity of Pittsboro, north of Siler City, and east of Lake Jordan.

As will be discussed in more detail below in § III.A, we also learned that, even in areas shown to be fully served, no broadband service is available or broadband service is inadequate at a significant number of spots within those areas that appear to be served by incumbent providers. Finally, we learned (see below in § III.B) that wireless broadband is currently not much of an answer to the County’s broadband deficit and does not provide much of an alternative to wireline 10 Cable modem service has been commercially available since about 1996 and DSL service since about 1998, with cable modem service taking off in serious numbers by 1999 and DSL by 2000.

service in the County’s unwired areas due to spotty coverage and slow speeds.

We interviewed seven broadband providers (AT&T, CenturyLink, Chatham Wireless, MCNC, Randolph Telephone Membership Corp, Time Warner Cable, and Windstream Communications) to obtain a fuller sense of past broadband investment practices in the County and likely future investment patterns. We interviewed six major broadband users (Chatham County government, Central Carolina Community College, Central Electric Membership Corp., Chatham County Libraries, Chatham County Schools, and Chatham’s Emergency Operations Center) to identify possible partners and potential users. We interviewed representatives of Cambria County, Pennsylvania, a county similar in size to Chatham County (but with more rolling terrain), to obtain a sense of the lessons learned in deploying a countywide broadband network through a public-private partnership. We also spent the better part of four days in the field (November 18 and 19 and December 14, 2010; February 3, 2011), examining existing equipment and obtaining a fuller sense of the design of existing wireline and wireless networks in the County, and interviewed broadband consumers living in various areas of the County to document their broadband experiences.

Some of the providers were helpful and cooperative (MCNC, Randolph TMC, and Chatham Wireless), while others were reluctant to share hard data about their Chatham operations but did meet with us and provide us with big picture information regarding their operations (AT&T, CenturyLink, and Time Warner Cable). Still others declined to meet with us despite repeated requests for a meeting (Charter and Windstream11).

Through this process, we confirmed, clarified, and fleshed out what the data told us about Chatham County. Parts of Chatham County suffer from a major broadband deficit and, in terms of service quality and speed, most of the County lags well behind more urbanized areas and even some more rural areas where years of federal subsidies have helped to bridge the digital divide. As noted above, the service deficiencies are the most serious in the western and southern parts of the County but even the more populated eastern areas are not immune to service quality problems and uneven access to service on a street-by-street basis.

The County’s broadband deficit is due to its population density and economic and demographic characteristics. The County’s wireless deficit is as serious as its wireline deficit for similar reasons. The telecommunications industry, whether wireline or wireless, invests in infrastructure based primarily on population density and secondarily on economic and demographic characteristics. These investment practices, which are not secrets and are candidly acknowledged by industry representatives, make fashioning a permanent solution to the County’s broadband deficit a challenge as normal market mechanisms do not work in a timely or responsive fashion.

11 We met with representatives of Windstream’s business group but representatives of the part of the company that actually provides service in the County—its residential division—declined to meet with us despite repeated requests.

B. IMPORTANCE OF BROADBAND FOR CHATHAM COUNTY

Broadband services and technology are not static but rather are constantly evolving in new and unpredictable ways. For Chatham County, this means that it cannot close the broadband gap today and rest on its laurels, assuming that the gap will remain forever closed, because new broadband applications and uses will arise every day and broadband demand will continue on its sharp upward trajectory. The Board of Commissioners experiences this phenomenon on a routine basis as the County has to make decisions with frequency through the budgeting process to upgrade the County’s little piece of the broadband world to keep pace with relentless change like suddenly having to expand and modify its data storage capabilities to cover the County’s exponential growth in data generation.

The snapshot this report provides as to the current state of broadband technology in the County is less meaningful than is its assessment of the pace of implementation of broadband technology in Chatham County. An assessment of the state of broadband deployment tells us how the County stacks up against the rest of the world, starting with urbanized neighbors in North Carolina, then comparing Chatham (and North Carolina) to other areas of the country (like more densely populated states), and finally looking at other parts of the world where advanced broadband technology is king.

Using 2001 as the starting data for the broadband era, parts of the County are at least 10 years off the pace in terms of access to broadband technology (the more rural areas of western and southern Chatham where there still is no broadband service). Others are 7 or 8 years off pace (Silk Hope area), some are 4 or 5 years off pace (Goldston, Bonlee), and still others are just a year or two off the pace (Pittsboro and Siler City). This pattern can be expected to repeat itself again and again in the future as new technologies emerge and are deployed and do not reach throughout the County until each generation of technology is close to the end of its life cycle and the industry is moving on to the next great thing.

In simple terms, the data shows that rural and semi-rural North Carolina communities like Chatham County lag behind more urbanized communities in the state while the state generally lags behind much of the rest of the nation, especially the more densely populated northeastern states. And of course, the United States does not stack up well against much of the rest of the industrialized world on basic broadband availability indicators. So in terms of competitiveness in the broadband world, Chatham is just barely in the game under most comparative analyses.

Broadly speaking, census data shows that rural counties like Chatham County typically lag urbanized areas like Wake County by about 15% in terms of home-based Internet access (66% to 51% in 2009 census survey).12 In all likelihood the actual gap between Wake and Chatham counties is greater, with FCC data showing zero to 20% access in western and southern parts of the county and 20% to 40% in the Siler City and Goldston areas. This deficit is generally due to 12 Economic and Statistics Administration and NTIA, U.S. Department of Commerce, Exploring the Digital Nation: Home Broadband Internet Adoption in the United States, Nov., 2010, 37 (t.24).

the higher cost of providing service in rural areas and the resulting lack of both investment and competition in rural areas. This shortfall is especially true for in-between counties like Chatham where local telephone companies do not qualify for the generous federal subsidies that were first provided to unserved areas like much of Randolph County in the 1950s. Those large subsidies continue to this day despite the fact that many of those more rural counties long ago caught up to the in-between counties and now have better service than less rural counties like Chatham.

The national picture shows major gaps between North Carolina and much of the rest of the nation with regard to service quality. For example, 2009 census data shows North Carolina standing 38th in the nation in terms of in-home broadband use. Of perhaps even greater importance, North Carolina ranks dead last in the nation in terms of access to broadband connections that meet the new FCC targets of broadband availability of 4 MB/s downstream and 1 MB/s upstream at a mere 10%. See § II.A.1 for additional detail. To put this number in context, more densely populated and urbanized states, with more competitive broadband environments like New Jersey and Massachusetts, clock in above 60% or more than six times the North Carolina rate under this FCC measurement.

The gap in access to quality broadband service gets a little worse when we move to the international arena and compare broadband availability in the United States with broadband in other nations. According to the Organization of Economic Co-operation and Development (OECD), the United States ranked 12th among the 33 industrialized nations rated in 2009 with regard to the percentage of households with broadband access at 63.5%. South Korea leads the world at 95.9%, followed by Iceland (86.7%), Sweden (78.5%), the United Kingdom, Canada, and Germany.13 Nations lagging behind the United States include Australia, Japan, France, Switzerland, and Italy.

So whether looking at competing in the North Carolina economy, the United States economy, or the world economy, Chatham residents are at a disadvantage when it comes to broadband tools, which we know already play an important role in shaping economic and educational opportunities and will likely play an even greater role in the future.

Broadband is already a central component of our basic infrastructure and will assume an even more central role in the future. We do not need studies to confirm that most of us could not function in our daily lives without broadband, whether it is for mundane matters like applying for jobs, communicating with family members and business associates, or implementing basic financial transactions. And now we see with the younger generation that it takes on an even larger role in their lives, for good or bad, as they use broadband to watch television (Hulu) and movies (Netflix)14 and to entertain themselves (the sprawling and growing worlds of video gaming and social media). And venture into the world of elementary school where engagement

13 See http://www.oecd.org/ at Statistics for additional detail.14 Netflix is not just popular with the younger set as all ages find it an attractive service. But the younger generation has fully embraced Netflix and has already transformed “netflix” into a verb just as “google” is now a common verb.

with broadband technology is even more intense as small children grab tablets like iPads and quickly enter a digital world of information and educational processes that was unknown to those of us in the adult world.

Areas where broadband already has an established role in our lives include the following five areas:

Education Economic development and job creation Personal communications, financial transactions, and entertainment Public safety Government services and civic engagement

Areas where broadband is poised to explode and is likely to re-shape much of our daily lives in-clude the following four areas of emerging broadband use:

Health care Energy and utility use (management and control) Transportation Smart communities

We already know that broadband technology has been incorporated into curriculums at all levels of the educational process. The Chatham County Schools have embraced broadband technology and computers throughout the school system, placing a laptop computer in the hands of every high school student. But many Chatham students are losing out on much that broadband has to offer in the educational environment and are unable to take full advantage of their laptops be-cause they cannot obtain access to the Internet at home.

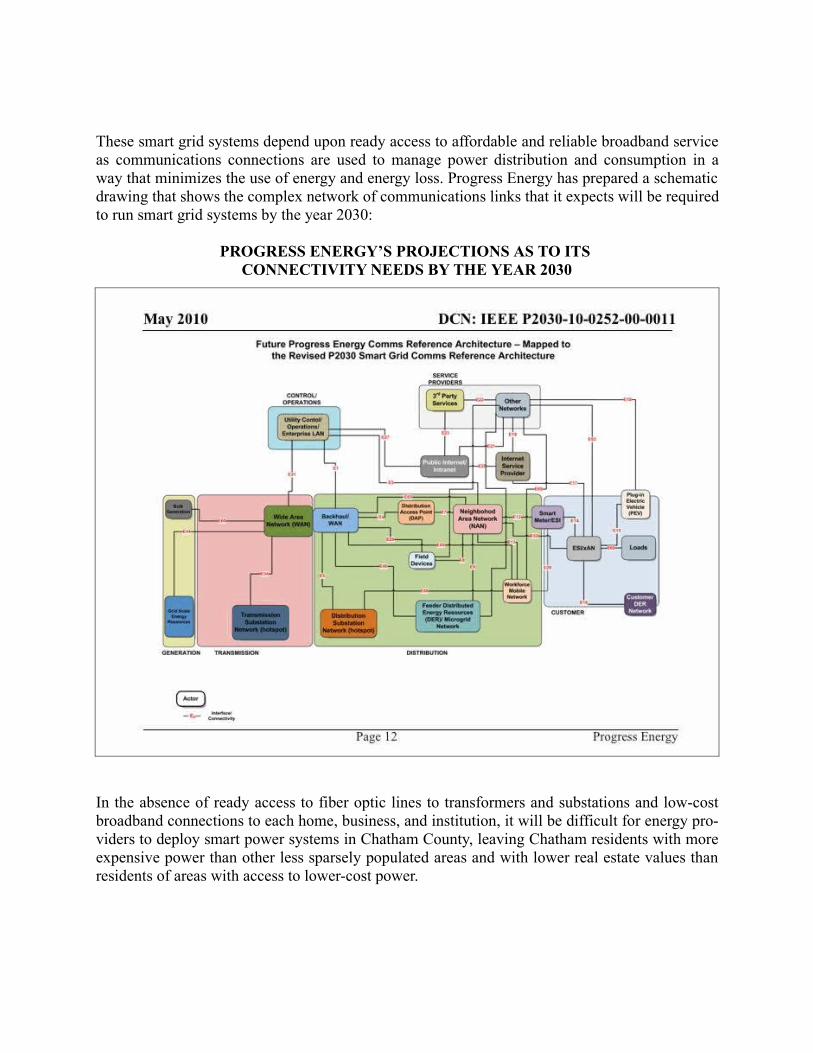

Another area where Chatham County is especially vulnerable to being left behind is the next stage of energy management and control. Ambitious plans to maximize the value of energy through smart grid services are on the drawing boards and, in many areas, in the process of being implemented by utilities, including by Progress Energy. By embedding information technology throughout the power grid and in the homes of energy users, the nation’s energy providers expect to be able to reduce the use of energy, saving consumers, businesses, and institutions significant money and starting to reduce dependence on vulnerable and polluting sources of energy such as oil wells in the Mideast and coal mines in West Virginia.

These smart grid and metering systems depend upon ready access to affordable and reliable broadband service as communications lines are used to manage power distribution and consump-tion in a way that minimizes the use of energy. In the absence of ready access to fiber optic lines to transformers and substations and low-cost broadband connections to each home, business, and institution, it will be difficult for energy providers to deploy smart power systems in Chatham County, leaving Chatham residents with more expensive power than other better equipped

counties and the side effects such as depressed real estate values.

Chatham’s broadband-related basic needs include: (1) improving access to service as a baseline matter (i.e., providing all County residents with access to broadband service); and (2) improving broadband speed and service quality both now and in the future. Achieving the first goal (universal access) will have lasting value only if County residents are also able to obtain early access to advances in broadband technology on an ongoing basis in the future and are able to keep up with more urbanized areas of North Carolina and with other states and be competitive not only in the state and the nation but also in the world.

In practical terms, meeting these needs requires that broadband service be available throughout the County and that it be updated to comply with the FCC’s new target for measuring the minimum broadband speeds required to participate in contemporary society: access to broadband at speeds of 4 MB/s downstream and 1 MB/s upstream. These FCC standards are interim standards and represent the FCC’s first step in moving the United States onto stronger footing in the broadband world. These speed targets are likely to increase greatly in the future to accommodate new video intensive and other data-heavy applications as the FCC’s 2020 goal is for the vast majority of American homes to be served by broadband at speeds of 100 MB/s downstream and 50 MB/s upstream.

Chatham County faces special problems in developing a comprehensive broadband plan because it is chopped into five separate telephone company service areas and two cable company service areas for wireline service, with overlap between the service areas of the cable companies and telephone companies but generally no overlap between the service areas of telephone companies. Chatham County is served by six mobile wireless carriers and one fixed wireless provider but, in contrast to the wireline carriers, there is overlap among the service areas of virtually all the wireless providers and some competition among the wireless carriers. In the end, each broadband provider has its own service territory (Verizon Wireless comes the closest to serving the entire county) and its own business model and approach to technology, making it difficult to secure consistent levels of broadband service throughout the County.

The difficulty of fashioning a solution in this multi-provider environment, as well as large annual public sector expenditures on telecommunications and broadband service, call for establishing a county-wide fiber optic backbone network. This network would provide all governmental and public institutions with access to uniform and scalable broadband service and would be subject to County and public control to the extent necessary to close the broadband deficit and maximize the value of the network.