Embed Size (px)

Citation preview

Research and Analytics Division, Value Ideas Investment Services Pvt. Ltd., Mumbai

October 2016

INITIATING COVERAGE 10/25/2016

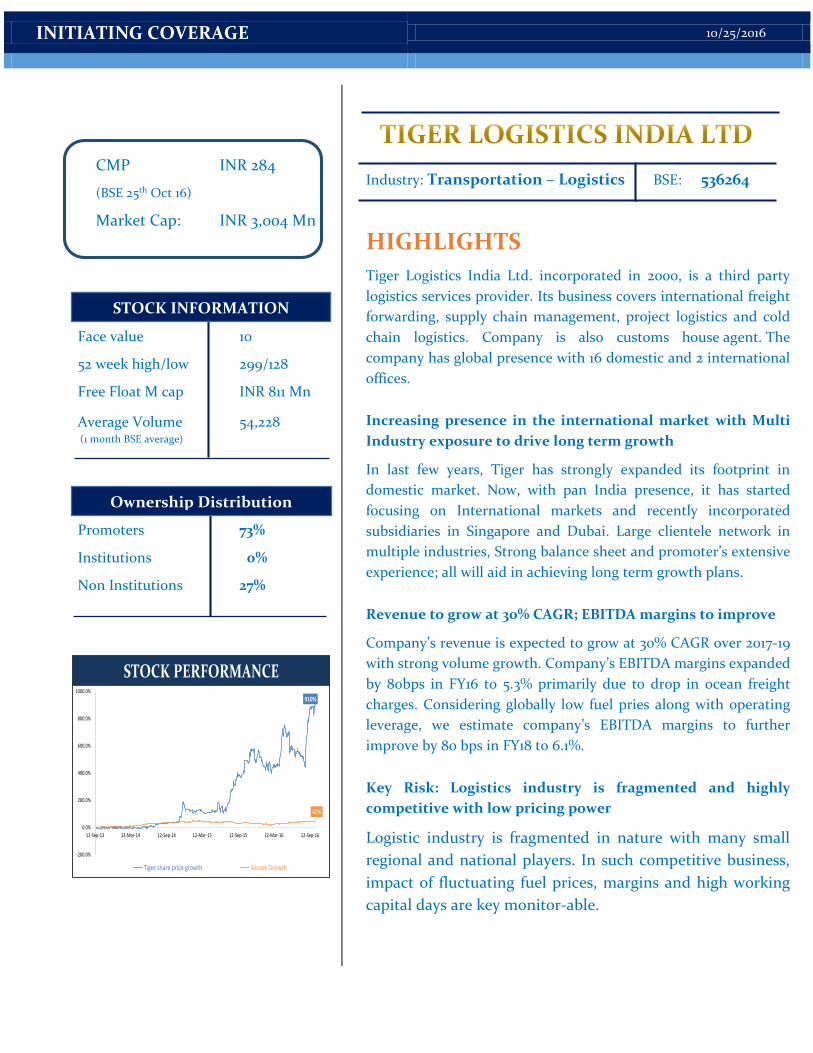

CMP INR 284

(BSE 25th Oct 16)

Market Cap: INR 3,004 Mn

Face value 10

52 week high/low 299/128

Free Float M cap INR 811 Mn

Average Volume 54,228 (1 month BSE average)

Promoters 73%

Institutions 0%

Non Institutions 27%

Industry: Transportation – Logistics BSE: 536264

HIGHLIGHTS

Tiger Logistics India Ltd. incorporated in 2000, is a third party

logistics services provider. Its business covers international freight

forwarding, supply chain management, project logistics and cold

chain logistics. Company is also customs house agent. The

company has global presence with 16 domestic and 2 international

offices.

Increasing presence in the international market with Multi

Industry exposure to drive long term growth

In last few years, Tiger has strongly expanded its footprint in

domestic market. Now, with pan India presence, it has started

focusing on International markets and recently incorporated

subsidiaries in Singapore and Dubai. Large clientele network in

multiple industries, Strong balance sheet and promoter’s extensive

experience; all will aid in achieving long term growth plans.

Revenue to grow at 30% CAGR; EBITDA margins to improve

Company’s revenue is expected to grow at 30% CAGR over 2017-19

with strong volume growth. Company’s EBITDA margins expanded

by 80bps in FY16 to 5.3% primarily due to drop in ocean freight

charges. Considering globally low fuel pries along with operating

leverage, we estimate company’s EBITDA margins to further

improve by 80 bps in FY18 to 6.1%.

Key Risk: Logistics industry is fragmented and highly

competitive with low pricing power

Logistic industry is fragmented in nature with many small

regional and national players. In such competitive business,

impact of fluctuating fuel prices, margins and high working

capital days are key monitor-able.

910%

42%

-200.0%

0.0%

200.0%

400.0%

600.0%

800.0%

1000.0%

12-Sep-13 12-Mar-14 12-Sep-14 12-Mar-15 12-Sep-15 12-Mar-16 12-Sep-16

Tiger share price growth Sensex Growth

STOCK PERFORMANCE

STOCK INFORMATION STOCK INFORMATION

Ownership Distribution

INITIATING COVERAGE 10/25/2016

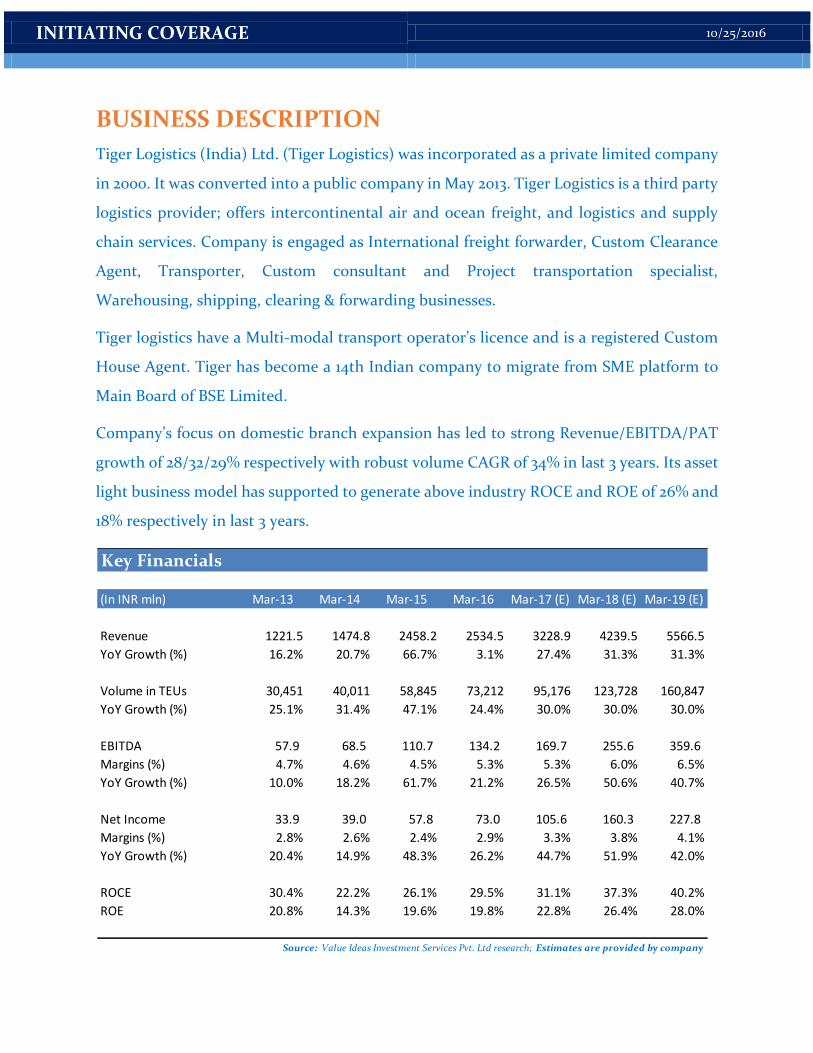

BUSINESS DESCRIPTION

Tiger Logistics (India) Ltd. (Tiger Logistics) was incorporated as a private limited company

in 2000. It was converted into a public company in May 2013. Tiger Logistics is a third party

logistics provider; offers intercontinental air and ocean freight, and logistics and supply

chain services. Company is engaged as International freight forwarder, Custom Clearance

Agent, Transporter, Custom consultant and Project transportation specialist,

Warehousing, shipping, clearing & forwarding businesses.

Tiger logistics have a Multi-modal transport operator’s licence and is a registered Custom

House Agent. Tiger has become a 14th Indian company to migrate from SME platform to

Main Board of BSE Limited.

Company’s focus on domestic branch expansion has led to strong Revenue/EBITDA/PAT

growth of 28/32/29% respectively with robust volume CAGR of 34% in last 3 years. Its asset

light business model has supported to generate above industry ROCE and ROE of 26% and

18% respectively in last 3 years.

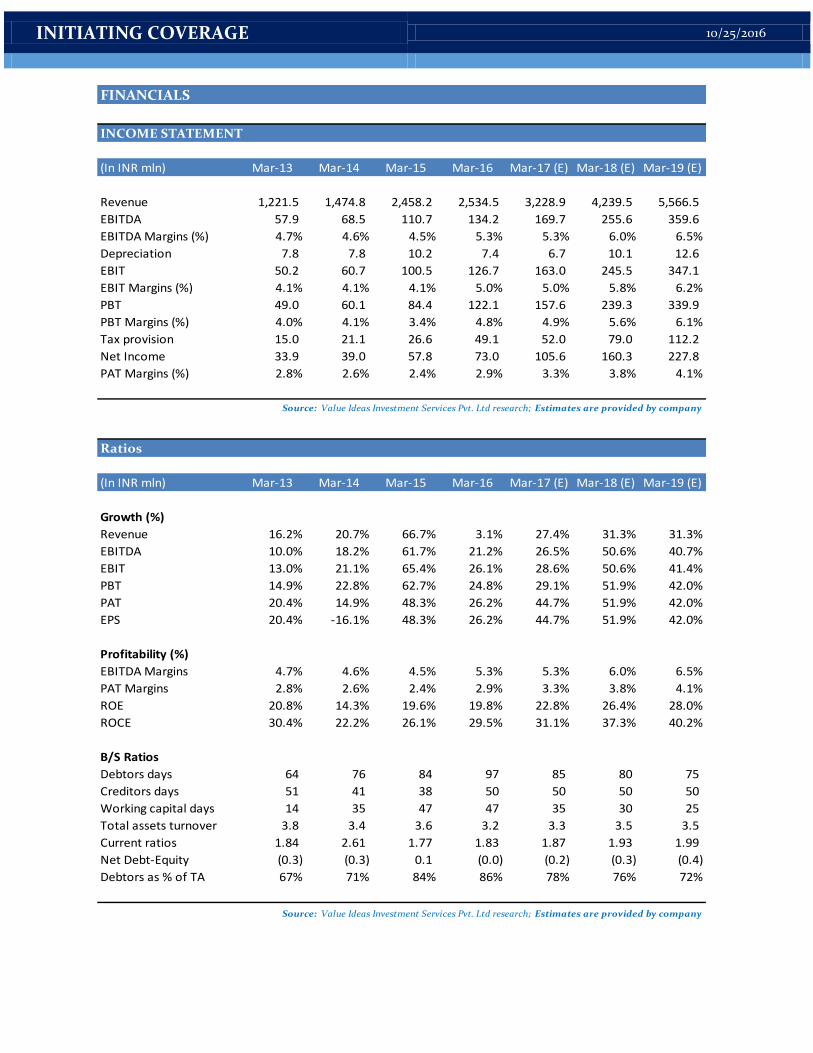

Key Financials

(In INR mln) Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 (E) Mar-18 (E) Mar-19 (E)

Revenue 1221.5 1474.8 2458.2 2534.5 3228.9 4239.5 5566.5

YoY Growth (%) 16.2% 20.7% 66.7% 3.1% 27.4% 31.3% 31.3%

Volume in TEUs 30,451 40,011 58,845 73,212 95,176 123,728 160,847

YoY Growth (%) 25.1% 31.4% 47.1% 24.4% 30.0% 30.0% 30.0%

EBITDA 57.9 68.5 110.7 134.2 169.7 255.6 359.6

Margins (%) 4.7% 4.6% 4.5% 5.3% 5.3% 6.0% 6.5%

YoY Growth (%) 10.0% 18.2% 61.7% 21.2% 26.5% 50.6% 40.7%

Net Income 33.9 39.0 57.8 73.0 105.6 160.3 227.8

Margins (%) 2.8% 2.6% 2.4% 2.9% 3.3% 3.8% 4.1%

YoY Growth (%) 20.4% 14.9% 48.3% 26.2% 44.7% 51.9% 42.0%

ROCE 30.4% 22.2% 26.1% 29.5% 31.1% 37.3% 40.2%

ROE 20.8% 14.3% 19.6% 19.8% 22.8% 26.4% 28.0%

Source: Value Ideas Investment Services Pvt. Ltd research; Estimates are provided by company

INITIATING COVERAGE 10/25/2016

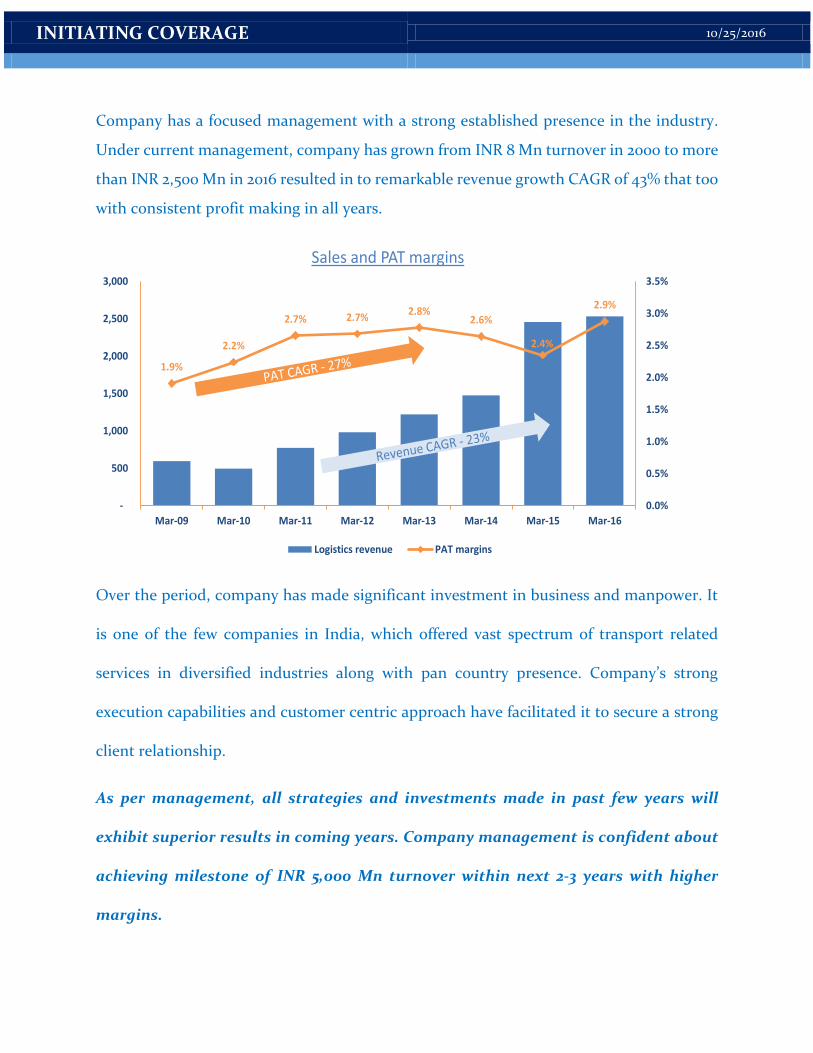

Company has a focused management with a strong established presence in the industry.

Under current management, company has grown from INR 8 Mn turnover in 2000 to more

than INR 2,500 Mn in 2016 resulted in to remarkable revenue growth CAGR of 43% that too

with consistent profit making in all years.

Over the period, company has made significant investment in business and manpower. It

is one of the few companies in India, which offered vast spectrum of transport related

services in diversified industries along with pan country presence. Company’s strong

execution capabilities and customer centric approach have facilitated it to secure a strong

client relationship.

As per management, all strategies and investments made in past few years will

exhibit superior results in coming years. Company management is confident about

achieving milestone of INR 5,000 Mn turnover within next 2-3 years with higher

margins.

1.9%

2.2%

2.7% 2.7%2.8%

2.6%

2.4%

2.9%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

-

500

1,000

1,500

2,000

2,500

3,000

Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16

Sales and PAT margins

Logistics revenue PAT margins

INITIATING COVERAGE 10/25/2016

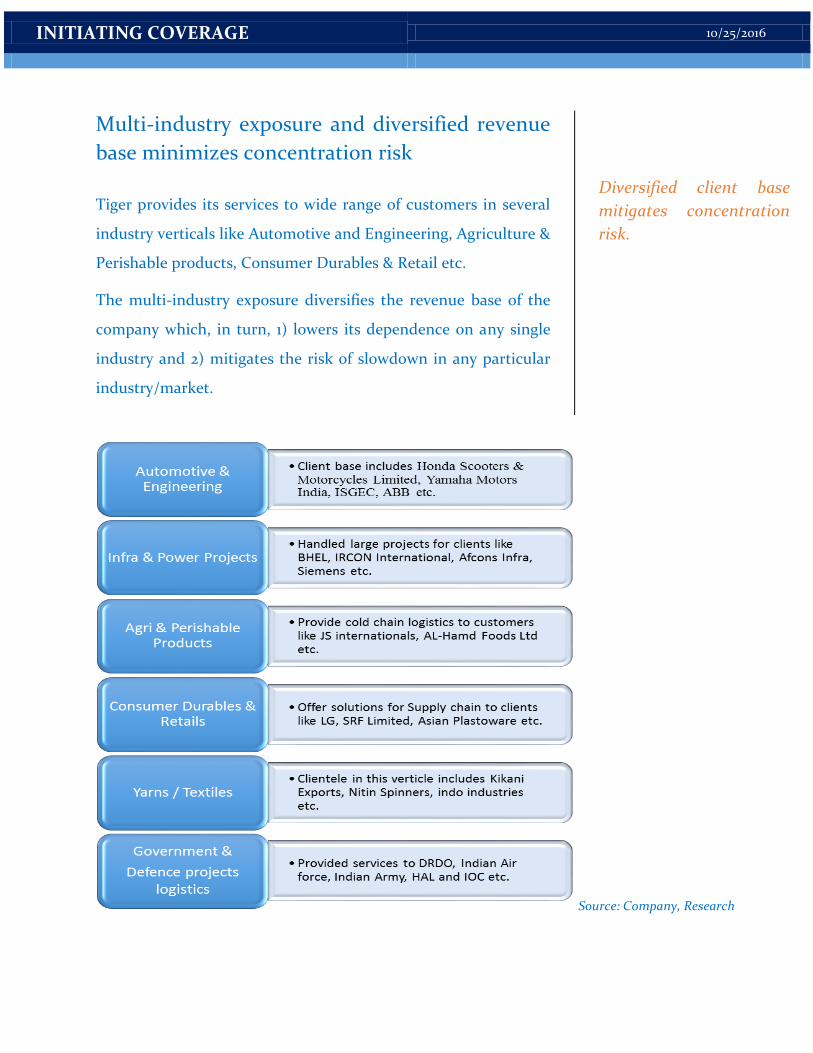

Multi-industry exposure and diversified revenue

base minimizes concentration risk

Tiger provides its services to wide range of customers in several

industry verticals like Automotive and Engineering, Agriculture &

Perishable products, Consumer Durables & Retail etc.

The multi-industry exposure diversifies the revenue base of the

company which, in turn, 1) lowers its dependence on any single

industry and 2) mitigates the risk of slowdown in any particular

industry/market.

Diversified client base

mitigates concentration

risk.

Source: Company, Research

INITIATING COVERAGE 10/25/2016

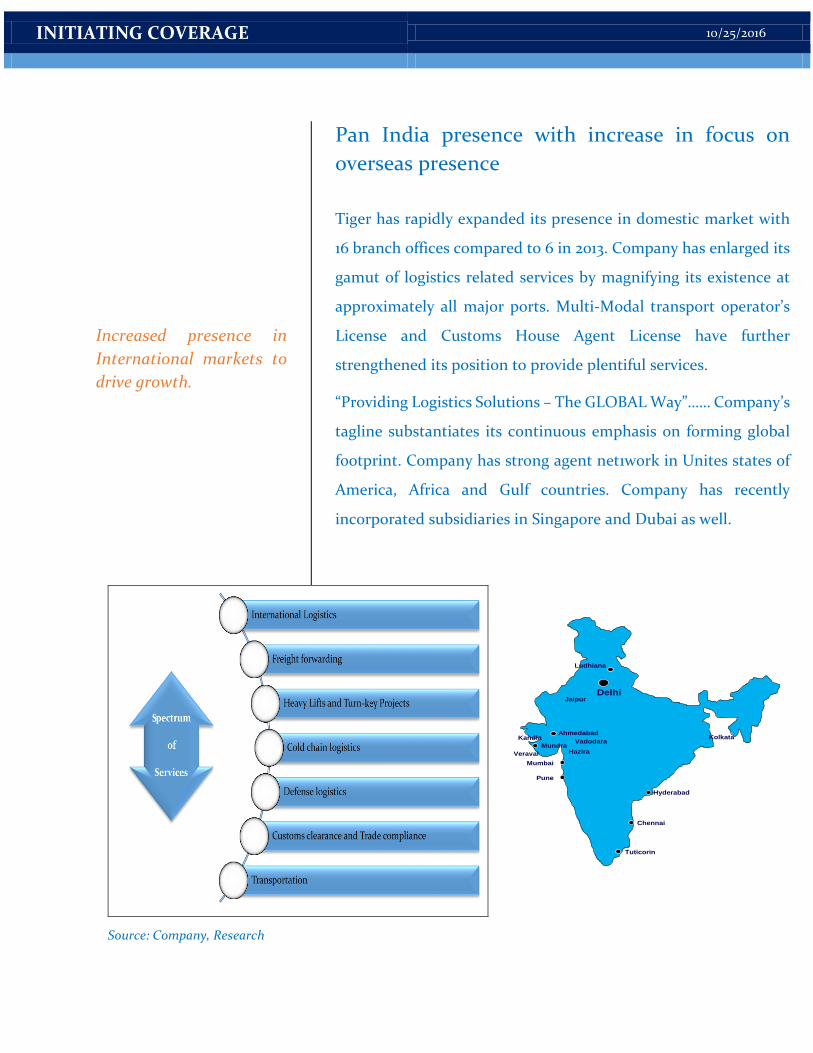

Increased presence in

International markets to

drive growth.

Pan India presence with increase in focus on

overseas presence

Tiger has rapidly expanded its presence in domestic market with

16 branch offices compared to 6 in 2013. Company has enlarged its

gamut of logistics related services by magnifying its existence at

approximately all major ports. Multi-Modal transport operator’s

License and Customs House Agent License have further

strengthened its position to provide plentiful services.

“Providing Logistics Solutions – The GLOBAL Way”…… Company’s

tagline substantiates its continuous emphasis on forming global

footprint. Company has strong agent net1work in Unites states of

America, Africa and Gulf countries. Company has recently

incorporated subsidiaries in Singapore and Dubai as well.

Source: Company, Research

Kolkata

Ludhiana

Delhi

Mumbai

Pune

Chennai

Hyderabad

Mundra

Jaipur

Ahmedabad

Veraval

Vadodara

Hazira

Tuticorin

Kandla

INITIATING COVERAGE 10/25/2016

Strong execution capabilities and established relationship with

clients to drive growth:

Tiger has a strong clientele including prominent Government Institutions (Indian

Army, BHEL, DRDO, HAL etc.), and private organizations (Maruti Suzuki, Honda,

Yamaha, LG etc.). By successfully expanding its client base, the company has been

able to lower its client concentration. The contribution from the top 5 clients of the

business has decreased to ~20% of total revenues in FY16 compared to 50% in FY13.

Geographic expansion in to the international business hubs is further likely to

expand the revenue and client base.

Clientele

INITIATING COVERAGE 10/25/2016

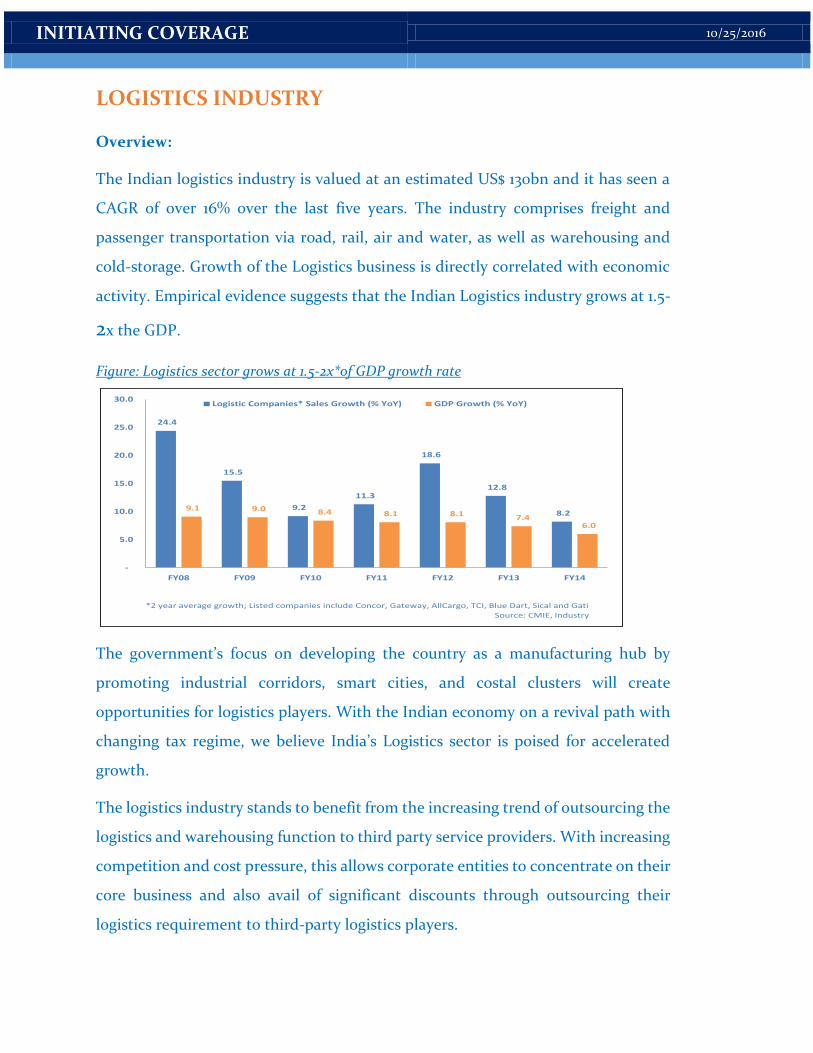

LOGISTICS INDUSTRY

Overview:

The Indian logistics industry is valued at an estimated US$ 130bn and it has seen a

CAGR of over 16% over the last five years. The industry comprises freight and

passenger transportation via road, rail, air and water, as well as warehousing and

cold-storage. Growth of the Logistics business is directly correlated with economic

activity. Empirical evidence suggests that the Indian Logistics industry grows at 1.5-

2x the GDP.

Figure: Logistics sector grows at 1.5-2x*of GDP growth rate

The government’s focus on developing the country as a manufacturing hub by

promoting industrial corridors, smart cities, and costal clusters will create

opportunities for logistics players. With the Indian economy on a revival path with

changing tax regime, we believe India’s Logistics sector is poised for accelerated

growth.

The logistics industry stands to benefit from the increasing trend of outsourcing the

logistics and warehousing function to third party service providers. With increasing

competition and cost pressure, this allows corporate entities to concentrate on their

core business and also avail of significant discounts through outsourcing their

logistics requirement to third‐party logistics players.

24.4

15.5

9.2

11.3

18.6

12.8

8.2 9.1 9.0 8.4 8.1 8.1 7.4

6.0

-

5.0

10.0

15.0

20.0

25.0

30.0

FY08 FY09 FY10 FY11 FY12 FY13 FY14

Logistic Companies* Sales Growth (% YoY) GDP Growth (% YoY)

*2 year average growth; Listed companies include Concor, Gateway, AllCargo, TCI, Blue Dart, Sical and Gati

Source: CMIE, Industry

INITIATING COVERAGE 10/25/2016

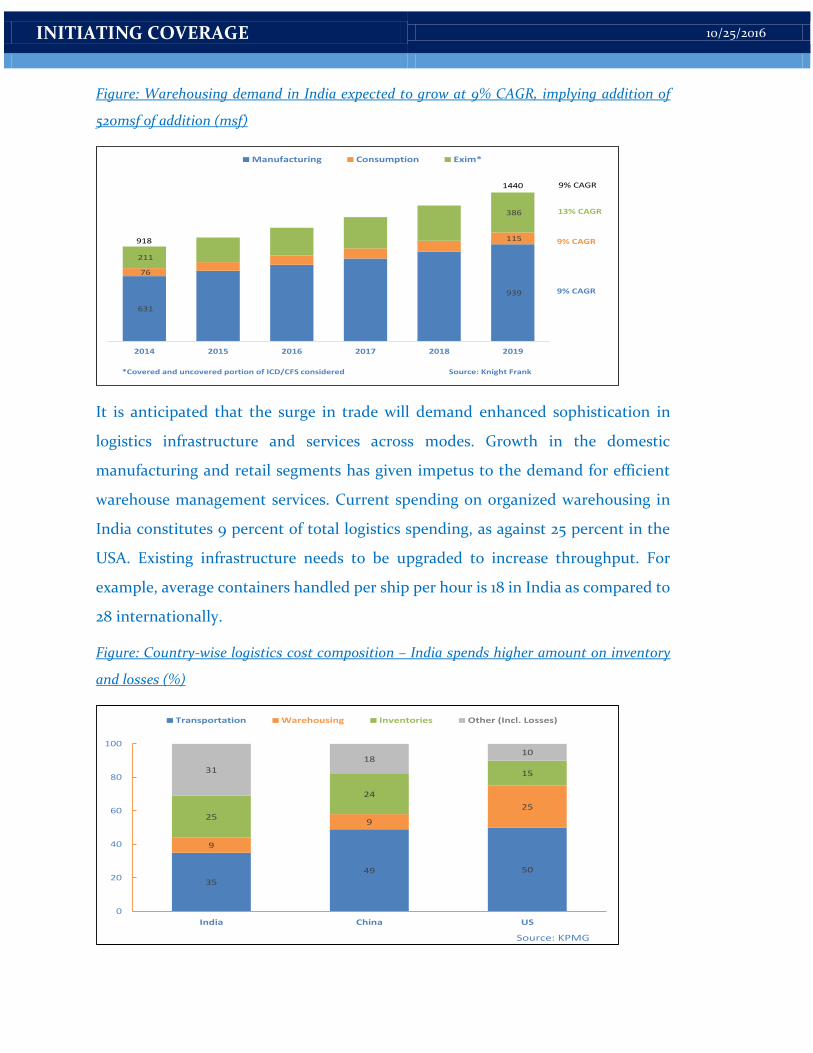

Figure: Warehousing demand in India expected to grow at 9% CAGR, implying addition of

520msf of addition (msf)

It is anticipated that the surge in trade will demand enhanced sophistication in

logistics infrastructure and services across modes. Growth in the domestic

manufacturing and retail segments has given impetus to the demand for efficient

warehouse management services. Current spending on organized warehousing in

India constitutes 9 percent of total logistics spending, as against 25 percent in the

USA. Existing infrastructure needs to be upgraded to increase throughput. For

example, average containers handled per ship per hour is 18 in India as compared to

28 internationally.

Figure: Country-wise logistics cost composition – India spends higher amount on inventory

and losses (%)

631

939

76

115

211

386

2014 2015 2016 2017 2018 2019

Manufacturing Consumption Exim*

13% CAGR

9% CAGR

9% CAGR

*Covered and uncovered portion of ICD/CFS considered Source: Knight Frank

918

1440 9% CAGR

35

49 50

9

9

2525

24

1531

1810

0

20

40

60

80

100

India China US

Transportation Warehousing Inventories Other (Incl. Losses)

Source: KPMG

INITIATING COVERAGE 10/25/2016

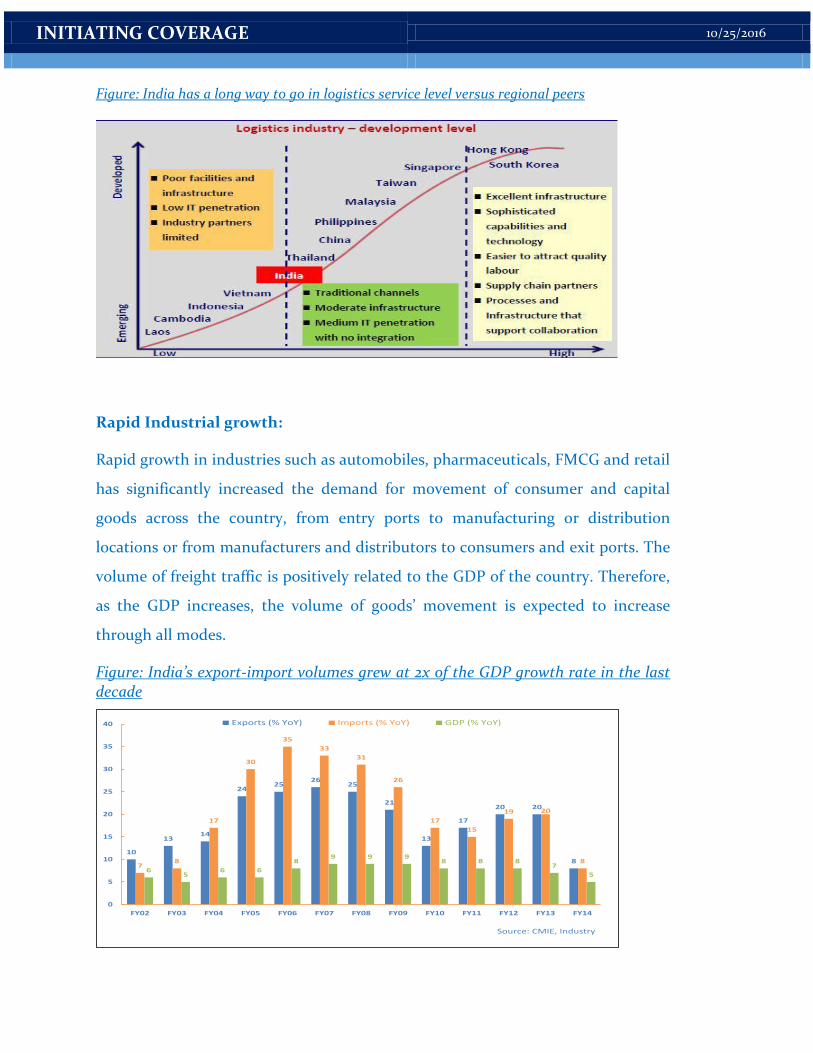

Figure: India has a long way to go in logistics service level versus regional peers

Rapid Industrial growth:

Rapid growth in industries such as automobiles, pharmaceuticals, FMCG and retail

has significantly increased the demand for movement of consumer and capital

goods across the country, from entry ports to manufacturing or distribution

locations or from manufacturers and distributors to consumers and exit ports. The

volume of freight traffic is positively related to the GDP of the country. Therefore,

as the GDP increases, the volume of goods’ movement is expected to increase

through all modes.

Figure: India’s export-import volumes grew at 2x of the GDP growth rate in the last decade

10

1314

2425

2625

21

13

17

20 20

87

8

17

30

35

33

31

26

17

15

19 20

8

65

6 6

89 9 9

8 8 87

5

0

5

10

15

20

25

30

35

40

FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Exports (% YoY) Imports (% YoY) GDP (% YoY)

Source: CMIE, Industry

INITIATING COVERAGE 10/25/2016

Streamlining indirect tax structure with the introduction of GST:

According to the CBEC, Goods and Services Tax (GST) would (i) amalgamate a large

number of Central and State taxes into a single tax, (ii) mitigate cascading or double

taxation in a major way, and (iii) pave the way for a common national market. From

the consumer point of view, the biggest advantage would be in terms of reduction

in the overall tax burden on goods, which is currently estimated at 25%-30%.

Implementation of a common nation-wide GST will be a game-changing event for

businesses in general. Taxation at a national level, rather than by each state, will

result in more efficient cross-state transportation, streamlining paperwork for road

transporters and bringing down logistics costs. Currently, each of India’s 29 states

taxes goods that move across their borders at different rates. As a result, freight that

moves across the country is taxed multiple times. Worse, there are long delays at

interstate checkpoints, as state authorities review and examine freight and apply the

relevant taxes and other levies. Truck delays average five-to-seven hours at inter-

state checkpoints. This, combined with other delays, keep trucks from moving

during 60% of the entire transit time. As much as 65% of India’s freight moves by

road, a fact which leads us to say that GST is critical for India.

Simply halving the delays due to roadblocks, tolls and other stoppages could cut

freight times by some 20-30% and logistics costs by an even higher 30-40%,

according to World Bank estimates. This alone can go a long way in boosting the

competitiveness of India’s key manufacturing sectors by 3-4% of net sales.

Outsourcing of Logistics:

The logistics industry stands to benefit from the increasing trend of outsourcing the

logistics and warehousing function to third party service providers. This function

was traditionally performed by the organizations themselves. However, corporate

entities recognize the benefits associated in engaging a third-party logistics provider

for integration of information flow, material handling, production, packaging,

inventory, transportation, warehousing and often security. This allows corporate

INITIATING COVERAGE 10/25/2016

entities to concentrate on their core business and also avail of significant discounts

through outsourcing.

According to ASSOCHAM, around 55 per cent of Indian companies outsourced

logistics services such as supply chain management and warehousing in 2009, as

compared to about 10-15 per cent in 1999. As per the industry estimates, the

increasing trend of outsourcing resulted in the growth of third-party logistics

market at a CAGR of about 22 per cent, during 2012-15.

MANAGEMENT AND CORPORATE GOVERNANCE

Strong and professional management driven by highly experienced

promoters:

Mr. Harpreet Singh Malhotra founded Tiger logistics in 2000 as private limited

company. Mr. Malhotra brings with him rich industry experience/competence,

which has helped Tiger to continuously deliver profitable growth over the years. He

had spearheaded the company from INR 8 Mn turnover in 2000 to more than INR

2500 Mn in 2016 (43% CAGR) that too with consistent profit making in all years. He

is supported by his capable and competent team, especially business heads of each

function/vertical.

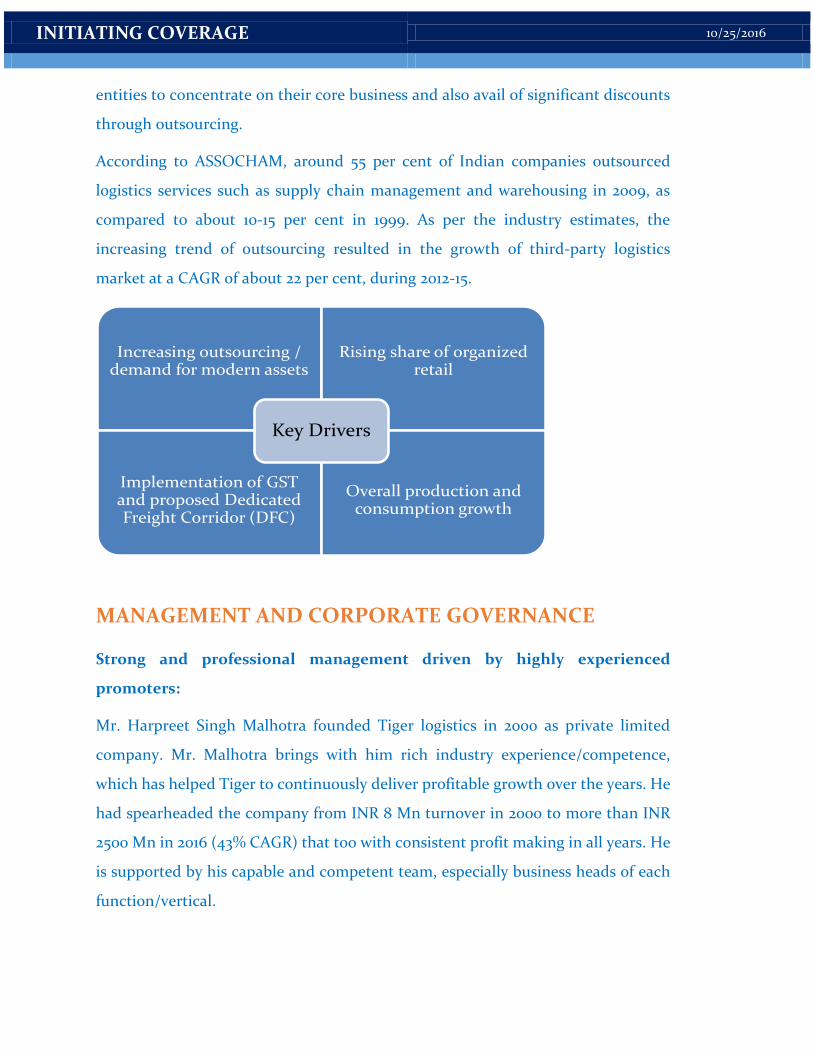

Increasing outsourcing / demand for modern assets

Rising share of organized retail

Implementation of GST and proposed Dedicated Freight Corridor (DFC)

Overall production and consumption growth

Key Drivers

INITIATING COVERAGE 10/25/2016

Tiger’s board consists of six directors, of whom three are independent. We believe

that the competence set and size of the board are appropriate in relation to the

current size of the company and its planned progress.

As Tiger is structured on asset light business model with service centric approach,

promoters and key managerial personnel are essential pillars of the business. Out of

total 300 employees currently, 70% employees have been working with company for

more than 10 years, which exhibits its committed and capable manpower.

ACCOLADES:

Company has won several awards at both national and international level. Some of

them are-

India’s Greatest Brand in the LOGISTICS arena for the year 2015-16.

World’s Greatest Brand, 2015—Asia & GCC in the service category - Logistics

sector

All India Maritime and Logistics Awards (MALA) In 2014

Best Logistics Service Provider of the year 2014

List of awards goes on and on. Indeed, company looks at each of these awards as

higher level of responsibility to create value for its stakeholders.

Group structure raises potential conflict of interest:

Some of the Group Entities i.e. Tiger Softech (India) Pvt. Ltd., Sun Warehousing &

Distribution Pvt. Ltd., Prithvi Shipping Pvt. Ltd. and Raina Transcontinental

Limited have similar business objects. Also, Company does not have any non-

compete agreement /arrangement with any of its group entities. Management is

aware of this situation and trying to address the issue in appropriate manner.

INITIATING COVERAGE 10/25/2016

RISKS/CONCERNS

Competition Risk:

Entry barriers are relatively low in domestic logistics space. Consequently,

industry is fragmented with several small and regional players. Since Tiger is

small player in highly competitive industry, it needs to offer ancillary aids

like longer credit period leading to higher working capital requirements.

Competition is further intensifying with emergence of start-ups in transport

industry with differentiated business models.

Negligible Pricing Power:

High level of competitive intensity in the business means negligible pricing

power of the company. Whatever little pricing power company enjoys, it is

because of its credibility in the eyes of its customers in terms of quality and

timely delivery/services.

Economic Risk:

The volume of freight traffic is positively related to the GDP of the country.

Slowdown in company’s key service sectors may adversely affect demand for

company’s services and consequently the revenue growth. However,

company’s multi industry exposure reduces this risk quite significantly.

INITIATING COVERAGE 10/25/2016

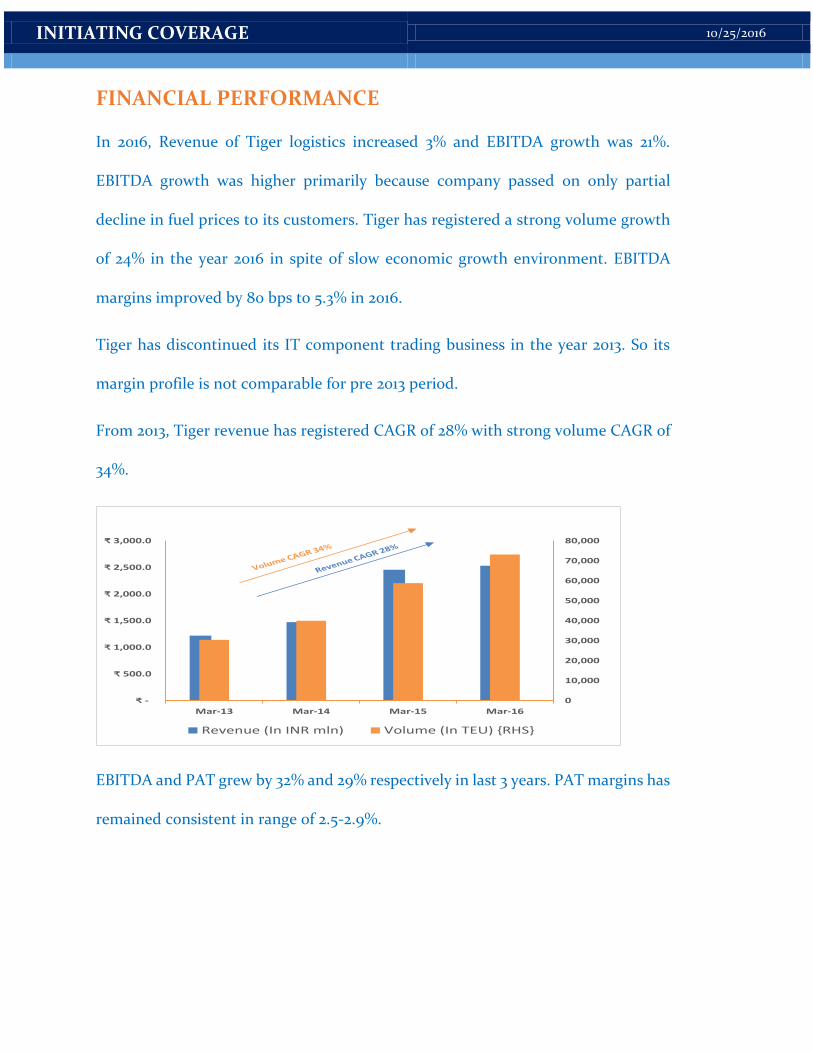

FINANCIAL PERFORMANCE

In 2016, Revenue of Tiger logistics increased 3% and EBITDA growth was 21%.

EBITDA growth was higher primarily because company passed on only partial

decline in fuel prices to its customers. Tiger has registered a strong volume growth

of 24% in the year 2016 in spite of slow economic growth environment. EBITDA

margins improved by 80 bps to 5.3% in 2016.

Tiger has discontinued its IT component trading business in the year 2013. So its

margin profile is not comparable for pre 2013 period.

From 2013, Tiger revenue has registered CAGR of 28% with strong volume CAGR of

34%.

EBITDA and PAT grew by 32% and 29% respectively in last 3 years. PAT margins has

remained consistent in range of 2.5-2.9%.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

₹ -

₹ 500.0

₹ 1,000.0

₹ 1,500.0

₹ 2,000.0

₹ 2,500.0

₹ 3,000.0

Mar-13 Mar-14 Mar-15 Mar-16

Revenue (In INR mln) Volume (In TEU) {RHS}

INITIATING COVERAGE 10/25/2016

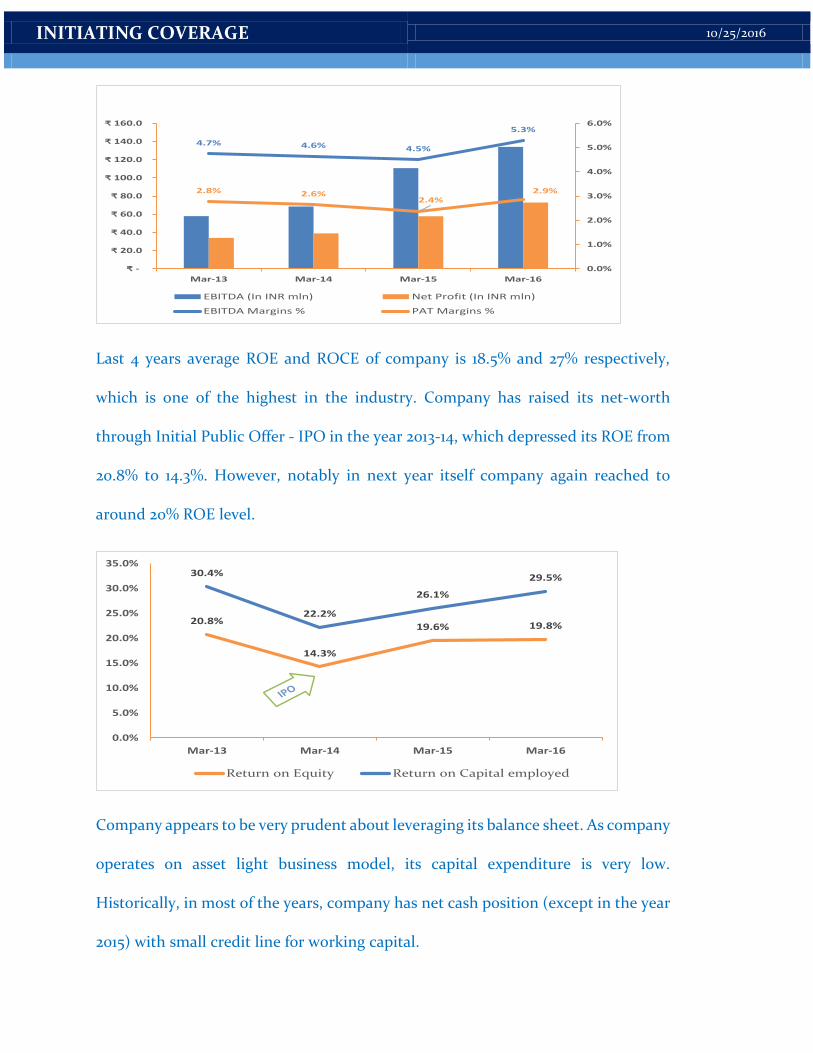

Last 4 years average ROE and ROCE of company is 18.5% and 27% respectively,

which is one of the highest in the industry. Company has raised its net-worth

through Initial Public Offer - IPO in the year 2013-14, which depressed its ROE from

20.8% to 14.3%. However, notably in next year itself company again reached to

around 20% ROE level.

Company appears to be very prudent about leveraging its balance sheet. As company

operates on asset light business model, its capital expenditure is very low.

Historically, in most of the years, company has net cash position (except in the year

2015) with small credit line for working capital.

4.7% 4.6% 4.5%

5.3%

2.8% 2.6%2.4%

2.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

₹ -

₹ 20.0

₹ 40.0

₹ 60.0

₹ 80.0

₹ 100.0

₹ 120.0

₹ 140.0

₹ 160.0

Mar-13 Mar-14 Mar-15 Mar-16

EBITDA (In INR mln) Net Profit (In INR mln)

EBITDA Margins % PAT Margins %

20.8%

14.3%

19.6% 19.8%

30.4%

22.2%

26.1%

29.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Mar-13 Mar-14 Mar-15 Mar-16

Return on Equity Return on Capital employed

INITIATING COVERAGE 10/25/2016

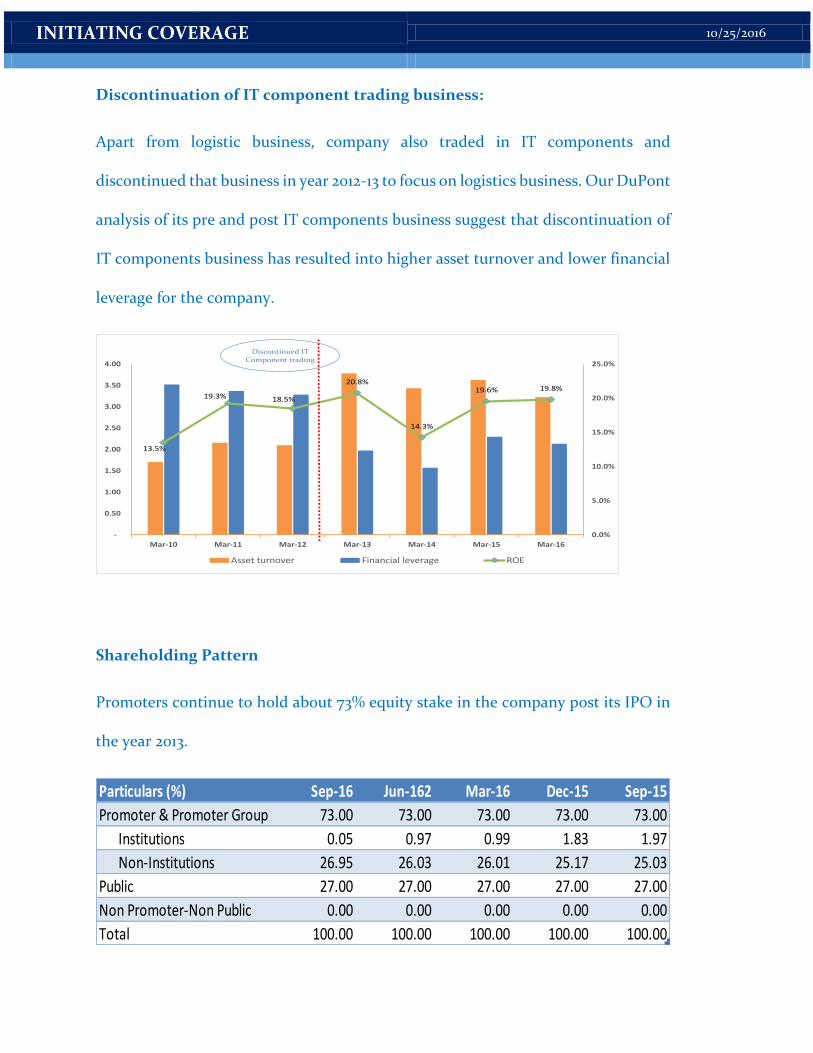

Discontinuation of IT component trading business:

Apart from logistic business, company also traded in IT components and

discontinued that business in year 2012-13 to focus on logistics business. Our DuPont

analysis of its pre and post IT components business suggest that discontinuation of

IT components business has resulted into higher asset turnover and lower financial

leverage for the company.

Shareholding Pattern

Promoters continue to hold about 73% equity stake in the company post its IPO in

the year 2013.

13.5%

19.3% 18.5%

20.8%

14.3%

19.6% 19.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16

Asset turnover Financial leverage ROE

Discontinued IT Component trading

Particulars (%) Sep-16 Jun-162 Mar-16 Dec-15 Sep-15

Promoter & Promoter Group 73.00 73.00 73.00 73.00 73.00

Institutions 0.05 0.97 0.99 1.83 1.97

Non-Institutions 26.95 26.03 26.01 25.17 25.03

Public 27.00 27.00 27.00 27.00 27.00

Non Promoter-Non Public 0.00 0.00 0.00 0.00 0.00

Total 100.00 100.00 100.00 100.00 100.00

INITIATING COVERAGE 10/25/2016

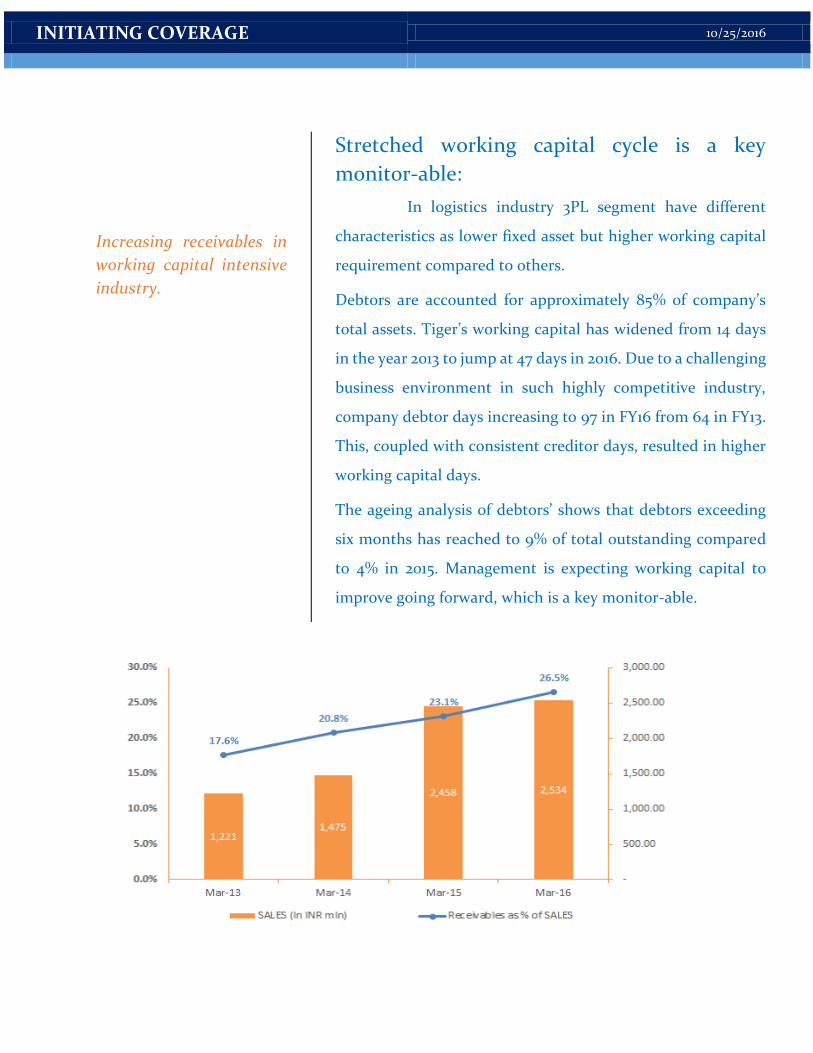

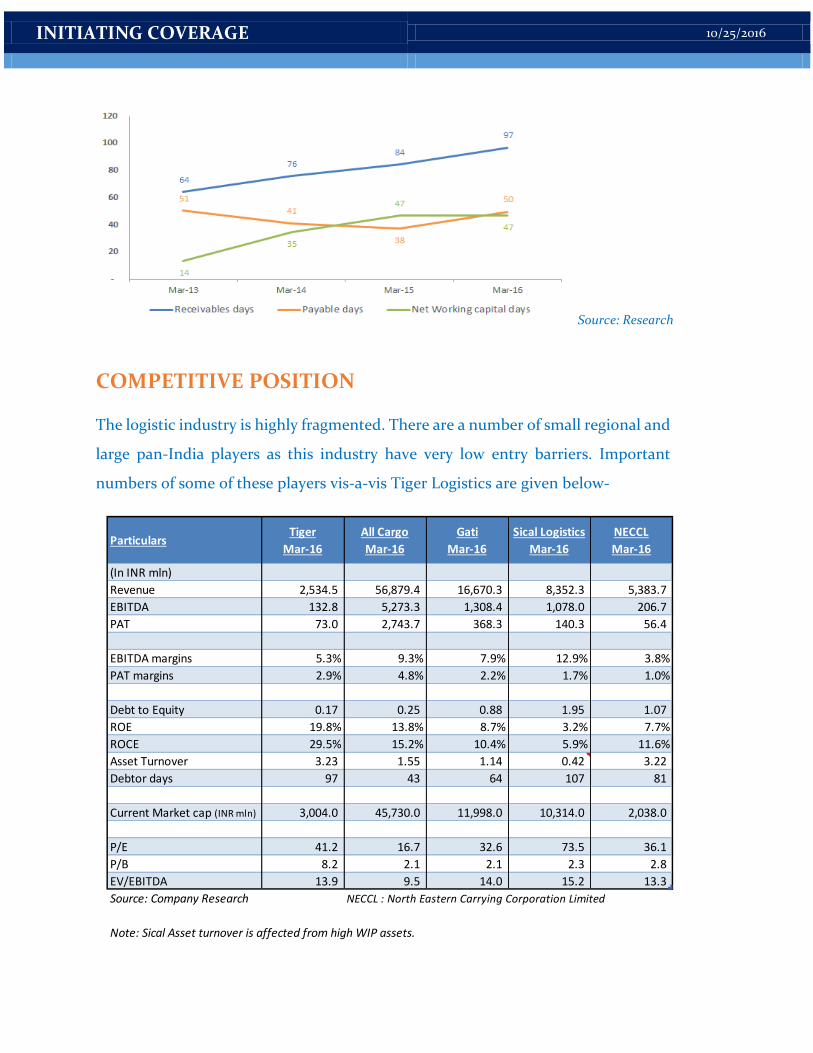

Increasing receivables in

working capital intensive

industry.

Stretched working capital cycle is a key

monitor-able:

In logistics industry 3PL segment have different

characteristics as lower fixed asset but higher working capital

requirement compared to others.

Debtors are accounted for approximately 85% of company’s

total assets. Tiger’s working capital has widened from 14 days

in the year 2013 to jump at 47 days in 2016. Due to a challenging

business environment in such highly competitive industry,

company debtor days increasing to 97 in FY16 from 64 in FY13.

This, coupled with consistent creditor days, resulted in higher

working capital days.

The ageing analysis of debtors’ shows that debtors exceeding

six months has reached to 9% of total outstanding compared

to 4% in 2015. Management is expecting working capital to

improve going forward, which is a key monitor-able.

INITIATING COVERAGE 10/25/2016

Source: Research

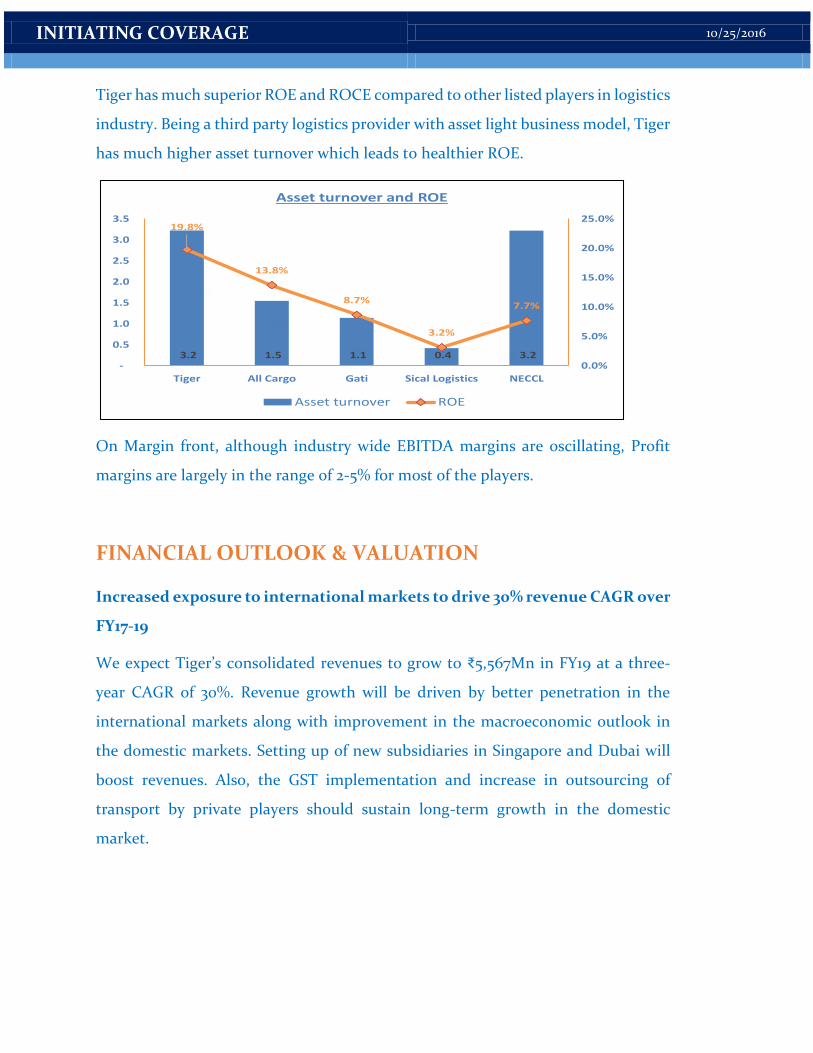

COMPETITIVE POSITION

The logistic industry is highly fragmented. There are a number of small regional and

large pan-India players as this industry have very low entry barriers. Important

numbers of some of these players vis-a-vis Tiger Logistics are given below-

ParticularsTiger

Mar-16

All Cargo

Mar-16

Gati

Mar-16

Sical Logistics

Mar-16

NECCL

Mar-16

(In INR mln)

Revenue 2,534.5 56,879.4 16,670.3 8,352.3 5,383.7

EBITDA 132.8 5,273.3 1,308.4 1,078.0 206.7

PAT 73.0 2,743.7 368.3 140.3 56.4

EBITDA margins 5.3% 9.3% 7.9% 12.9% 3.8%

PAT margins 2.9% 4.8% 2.2% 1.7% 1.0%

Debt to Equity 0.17 0.25 0.88 1.95 1.07

ROE 19.8% 13.8% 8.7% 3.2% 7.7%

ROCE 29.5% 15.2% 10.4% 5.9% 11.6%

Asset Turnover 3.23 1.55 1.14 0.42 3.22

Debtor days 97 43 64 107 81

Current Market cap (INR mln) 3,004.0 45,730.0 11,998.0 10,314.0 2,038.0

P/E 41.2 16.7 32.6 73.5 36.1

P/B 8.2 2.1 2.1 2.3 2.8

EV/EBITDA 13.9 9.5 14.0 15.2 13.3

Source: Company Research NECCL : North Eastern Carrying Corporation Limited

Note: Sical Asset turnover is affected from high WIP assets.

INITIATING COVERAGE 10/25/2016

Tiger has much superior ROE and ROCE compared to other listed players in logistics

industry. Being a third party logistics provider with asset light business model, Tiger

has much higher asset turnover which leads to healthier ROE.

On Margin front, although industry wide EBITDA margins are oscillating, Profit

margins are largely in the range of 2-5% for most of the players.

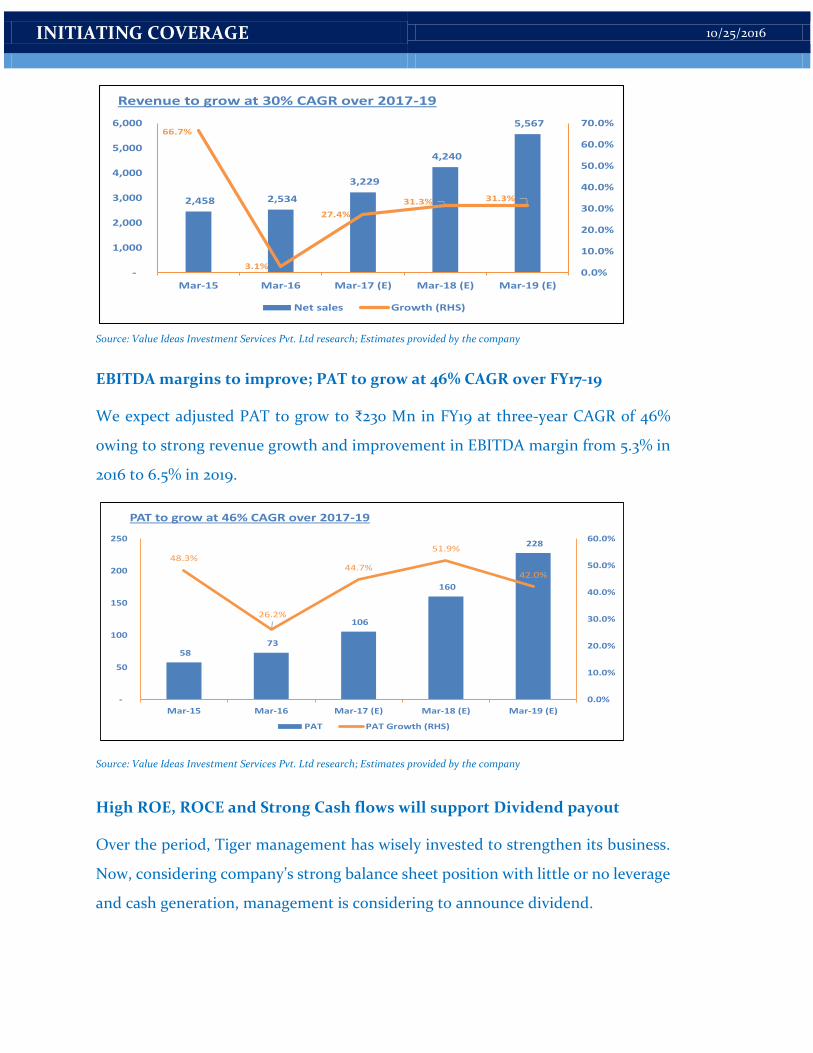

FINANCIAL OUTLOOK & VALUATION

Increased exposure to international markets to drive 30% revenue CAGR over

FY17-19

We expect Tiger’s consolidated revenues to grow to ₹5,567Mn in FY19 at a three-

year CAGR of 30%. Revenue growth will be driven by better penetration in the

international markets along with improvement in the macroeconomic outlook in

the domestic markets. Setting up of new subsidiaries in Singapore and Dubai will

boost revenues. Also, the GST implementation and increase in outsourcing of

transport by private players should sustain long-term growth in the domestic

market.

3.2 1.5 1.1 0.4 3.2

19.8%

13.8%

8.7%

3.2%

7.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Tiger All Cargo Gati Sical Logistics NECCL

Asset turnover and ROE

Asset turnover ROE

INITIATING COVERAGE 10/25/2016

Source: Value Ideas Investment Services Pvt. Ltd research; Estimates provided by the company

EBITDA margins to improve; PAT to grow at 46% CAGR over FY17-19

We expect adjusted PAT to grow to ₹230 Mn in FY19 at three-year CAGR of 46%

owing to strong revenue growth and improvement in EBITDA margin from 5.3% in

2016 to 6.5% in 2019.

Source: Value Ideas Investment Services Pvt. Ltd research; Estimates provided by the company

High ROE, ROCE and Strong Cash flows will support Dividend payout

Over the period, Tiger management has wisely invested to strengthen its business.

Now, considering company’s strong balance sheet position with little or no leverage

and cash generation, management is considering to announce dividend.

2,458 2,534

3,229

4,240

5,567

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

-

1,000

2,000

3,000

4,000

5,000

6,000

Mar-15 Mar-16 Mar-17 (E) Mar-18 (E) Mar-19 (E)

Revenue to grow at 30% CAGR over 2017-19

Net sales Growth (RHS)

58 73

106

160

228

48.3%

26.2%

44.7%

51.9%

42.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

-

50

100

150

200

250

Mar-15 Mar-16 Mar-17 (E) Mar-18 (E) Mar-19 (E)

PAT to grow at 46% CAGR over 2017-19

PAT PAT Growth (RHS)

INITIATING COVERAGE 10/25/2016

We believe that, while dividend payout can be increased going forward, Tiger’s

shareholders could benefit more by investing in new businesses given the

management's investment track record. Management has also signaled about

Capital expenditure for expansion and capacity addition in domestic business, but

that will be only after achieving its INR 5,000 Mn revenue milestone.

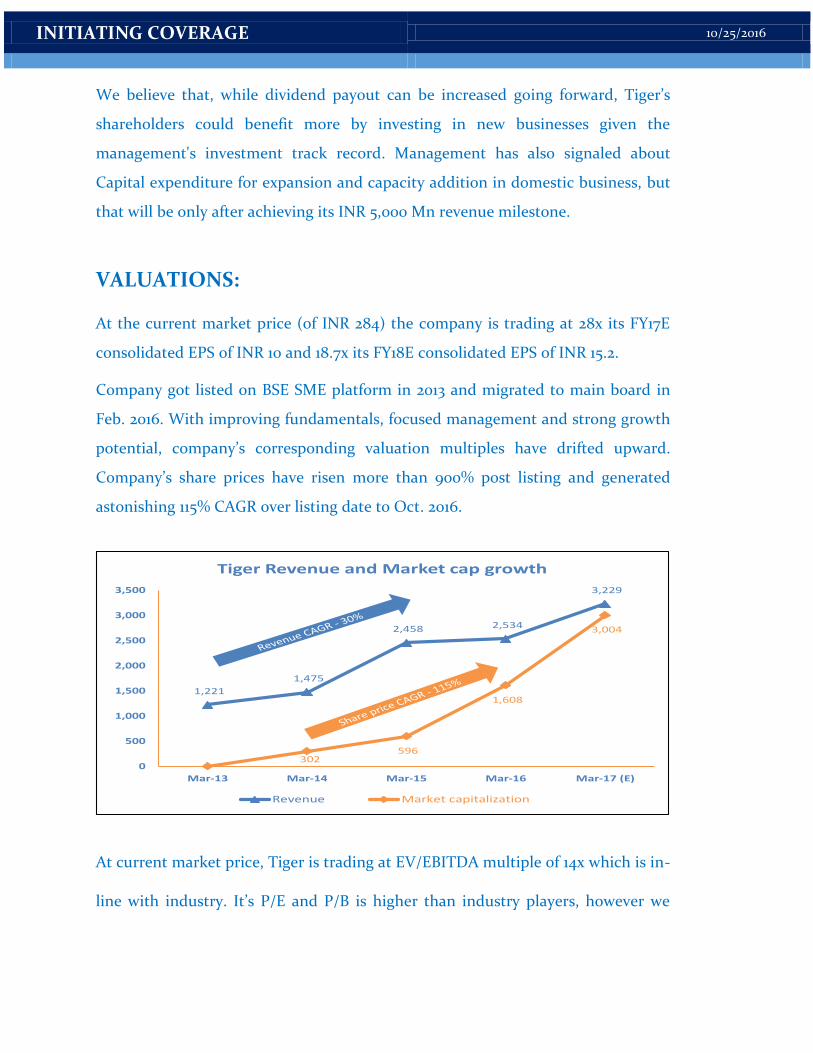

VALUATIONS:

At the current market price (of INR 284) the company is trading at 28x its FY17E

consolidated EPS of INR 10 and 18.7x its FY18E consolidated EPS of INR 15.2.

Company got listed on BSE SME platform in 2013 and migrated to main board in

Feb. 2016. With improving fundamentals, focused management and strong growth

potential, company’s corresponding valuation multiples have drifted upward.

Company’s share prices have risen more than 900% post listing and generated

astonishing 115% CAGR over listing date to Oct. 2016.

At current market price, Tiger is trading at EV/EBITDA multiple of 14x which is in-

line with industry. It’s P/E and P/B is higher than industry players, however we

1,221

1,475

2,458 2,534

3,229

302 596

1,608

3,004

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 (E)

Tiger Revenue and Market cap growth

Revenue Market capitalization

INITIATING COVERAGE 10/25/2016

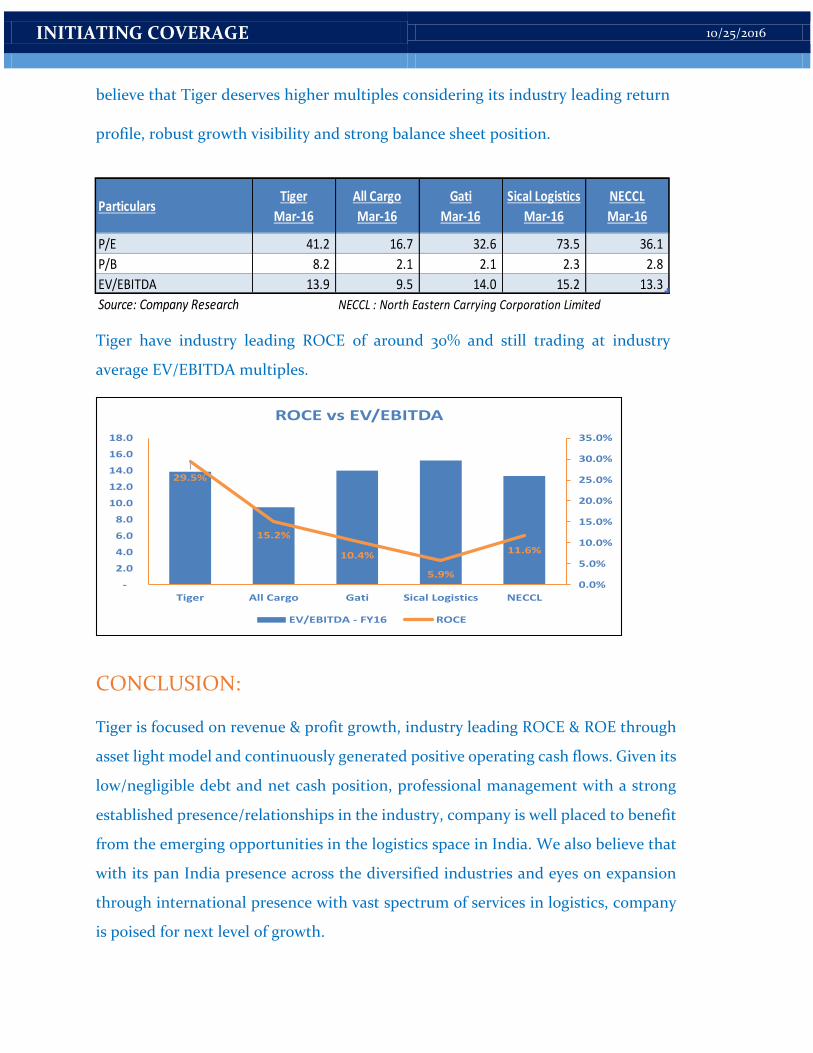

believe that Tiger deserves higher multiples considering its industry leading return

profile, robust growth visibility and strong balance sheet position.

Tiger have industry leading ROCE of around 30% and still trading at industry

average EV/EBITDA multiples.

CONCLUSION:

Tiger is focused on revenue & profit growth, industry leading ROCE & ROE through

asset light model and continuously generated positive operating cash flows. Given its

low/negligible debt and net cash position, professional management with a strong

established presence/relationships in the industry, company is well placed to benefit

from the emerging opportunities in the logistics space in India. We also believe that

with its pan India presence across the diversified industries and eyes on expansion

through international presence with vast spectrum of services in logistics, company

is poised for next level of growth.

ParticularsTiger

Mar-16

All Cargo

Mar-16

Gati

Mar-16

Sical Logistics

Mar-16

NECCL

Mar-16

P/E 41.2 16.7 32.6 73.5 36.1

P/B 8.2 2.1 2.1 2.3 2.8

EV/EBITDA 13.9 9.5 14.0 15.2 13.3

Source: Company Research NECCL : North Eastern Carrying Corporation Limited

29.5%

15.2%

10.4%

5.9%

11.6%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Tiger All Cargo Gati Sical Logistics NECCL

ROCE vs EV/EBITDA

EV/EBITDA - FY16 ROCE

INITIATING COVERAGE 10/25/2016

FINANCIALS

INCOME STATEMENT

(In INR mln) Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 (E) Mar-18 (E) Mar-19 (E)

Revenue 1,221.5 1,474.8 2,458.2 2,534.5 3,228.9 4,239.5 5,566.5

EBITDA 57.9 68.5 110.7 134.2 169.7 255.6 359.6

EBITDA Margins (%) 4.7% 4.6% 4.5% 5.3% 5.3% 6.0% 6.5%

Depreciation 7.8 7.8 10.2 7.4 6.7 10.1 12.6

EBIT 50.2 60.7 100.5 126.7 163.0 245.5 347.1

EBIT Margins (%) 4.1% 4.1% 4.1% 5.0% 5.0% 5.8% 6.2%

PBT 49.0 60.1 84.4 122.1 157.6 239.3 339.9

PBT Margins (%) 4.0% 4.1% 3.4% 4.8% 4.9% 5.6% 6.1%

Tax provision 15.0 21.1 26.6 49.1 52.0 79.0 112.2

Net Income 33.9 39.0 57.8 73.0 105.6 160.3 227.8

PAT Margins (%) 2.8% 2.6% 2.4% 2.9% 3.3% 3.8% 4.1%

Source: Value Ideas Investment Services Pvt. Ltd research; Estimates are provided by company

Ratios

(In INR mln) Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 (E) Mar-18 (E) Mar-19 (E)

Growth (%)

Revenue 16.2% 20.7% 66.7% 3.1% 27.4% 31.3% 31.3%

EBITDA 10.0% 18.2% 61.7% 21.2% 26.5% 50.6% 40.7%

EBIT 13.0% 21.1% 65.4% 26.1% 28.6% 50.6% 41.4%

PBT 14.9% 22.8% 62.7% 24.8% 29.1% 51.9% 42.0%

PAT 20.4% 14.9% 48.3% 26.2% 44.7% 51.9% 42.0%

EPS 20.4% -16.1% 48.3% 26.2% 44.7% 51.9% 42.0%

Profitability (%)

EBITDA Margins 4.7% 4.6% 4.5% 5.3% 5.3% 6.0% 6.5%

PAT Margins 2.8% 2.6% 2.4% 2.9% 3.3% 3.8% 4.1%

ROE 20.8% 14.3% 19.6% 19.8% 22.8% 26.4% 28.0%

ROCE 30.4% 22.2% 26.1% 29.5% 31.1% 37.3% 40.2%

B/S Ratios

Debtors days 64 76 84 97 85 80 75

Creditors days 51 41 38 50 50 50 50

Working capital days 14 35 47 47 35 30 25

Total assets turnover 3.8 3.4 3.6 3.2 3.3 3.5 3.5

Current ratios 1.84 2.61 1.77 1.83 1.87 1.93 1.99

Net Debt-Equity (0.3) (0.3) 0.1 (0.0) (0.2) (0.3) (0.4)

Debtors as % of TA 67% 71% 84% 86% 78% 76% 72%

Source: Value Ideas Investment Services Pvt. Ltd research; Estimates are provided by company

INITIATING COVERAGE 10/25/2016

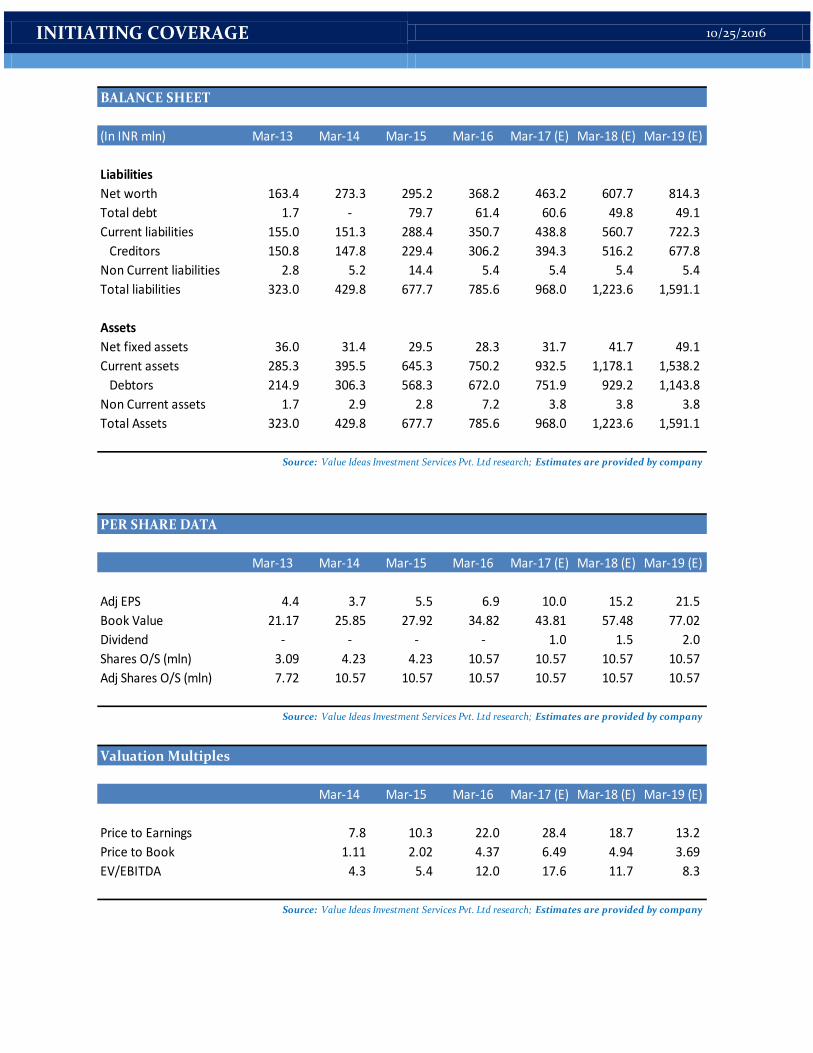

BALANCE SHEET

(In INR mln) Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 (E) Mar-18 (E) Mar-19 (E)

Liabilities

Net worth 163.4 273.3 295.2 368.2 463.2 607.7 814.3

Total debt 1.7 - 79.7 61.4 60.6 49.8 49.1

Current liabilities 155.0 151.3 288.4 350.7 438.8 560.7 722.3

Creditors 150.8 147.8 229.4 306.2 394.3 516.2 677.8

Non Current liabilities 2.8 5.2 14.4 5.4 5.4 5.4 5.4

Total liabilities 323.0 429.8 677.7 785.6 968.0 1,223.6 1,591.1

Assets

Net fixed assets 36.0 31.4 29.5 28.3 31.7 41.7 49.1

Current assets 285.3 395.5 645.3 750.2 932.5 1,178.1 1,538.2

Debtors 214.9 306.3 568.3 672.0 751.9 929.2 1,143.8

Non Current assets 1.7 2.9 2.8 7.2 3.8 3.8 3.8

Total Assets 323.0 429.8 677.7 785.6 968.0 1,223.6 1,591.1

Source: Value Ideas Investment Services Pvt. Ltd research; Estimates are provided by company

PER SHARE DATA

Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 (E) Mar-18 (E) Mar-19 (E)

Adj EPS 4.4 3.7 5.5 6.9 10.0 15.2 21.5

Book Value 21.17 25.85 27.92 34.82 43.81 57.48 77.02

Dividend - - - - 1.0 1.5 2.0

Shares O/S (mln) 3.09 4.23 4.23 10.57 10.57 10.57 10.57

Adj Shares O/S (mln) 7.72 10.57 10.57 10.57 10.57 10.57 10.57

Source: Value Ideas Investment Services Pvt. Ltd research; Estimates are provided by company

Valuation Multiples

Mar-14 Mar-15 Mar-16 Mar-17 (E) Mar-18 (E) Mar-19 (E)

Price to Earnings 7.8 10.3 22.0 28.4 18.7 13.2

Price to Book 1.11 2.02 4.37 6.49 4.94 3.69

EV/EBITDA 4.3 5.4 12.0 17.6 11.7 8.3

Source: Value Ideas Investment Services Pvt. Ltd research; Estimates are provided by company

INITIATING COVERAGE 10/25/2016

Abbreviations :

CAGR Compound Annual Growth Rate

CHA Custom House Agent

EBITDA Earnings Before Interest, Tax, Depreciation And Amortization

EPS Earnings Per Share

EV Enterprise Value

IPO Initial Public Offer

P/B Price To Book

P/E Price To Earnings

PAT Profit After Tax

ROCE Return On Capital Employed

ROE Return On Equity

3PL Third Party Logistics

INITIATING COVERAGE 10/25/2016

About us

SME Value Advisors (An offshoot of Value Ideas Investment Services Pvt. Ltd.) is a firm focused on partnering

with Emerging Corporates/SMEs helping them become better and more valuable by connecting right dots. Our research arm “Research and Analytics” is an independent research house with strong domain

knowledge on Indian economy, companies, industries and capital markets. With dedicated experienced team

of Research Analysts, we have been supporting Investment Bankers, Funds and Corporates on their research

requirements – Company Research, Industry Research, Valuations etc. Independent Equity Research (IER)

reports on SME companies is our initiative to help SMEs leverage their Stock Exchange listing to create value

for their stake holders. Analyst Disclosure

Team at Value Ideas Investment Services hereby affirms that there exists no conflict of interest that can bias the analysis in this report. As on date of this report, our team members involved in preparation of this report don’t possess any shares of this company (Tiger Logistics Ltd.). However, they reserve the right to buy/sell shares of this company in the secondary market. Disclaimer

This Independent Equity Research Report (SME IER Report) has been prepared by ‘Research and Analytics’ Division of Value Ideas Investment Services Pvt. Ltd. and is paid for by the Company itself (Tiger Logistics Ltd.). This Report is based on data publicly available, from sources considered reliable and also inputs from company management (together Data). We have relied upon and assumed, without any independent verification, the accuracy and completeness of all information provided by the company and third party database. This document also contains certain assumptions and forecasts, which the company considers reasonable at this time and which are subject to change. Value Ideas Investment Services Pvt. Ltd. does not guarantee the accuracy, adequacy or completeness of this Report and is not responsible for any errors or omissions or for the results obtained from the use of this Report.

Recipients should not construe any of the contents within this document as advice relating to business, financial, legal, taxation and/or investment matters and are advised to consult their own business, financial, legal, taxation and other advisors. This document is for information purpose only and does not constitute an invitation to subscribe for and/or purchase equity shares or other assets or securities of the Company and the information contained herein shall not form the basis of any contract. Value Ideas Investment Services Pvt. Ltd. especially states that, it has no financial liability whatsoever, to the subscribers / users of this Report.

This document is meant for the benefit and internal use of the recipient and does not carry any right of reproduction. Neither this document nor any of its contents maybe used for any purpose without the prior written approval of the company itself (Tiger Logistics Ltd.). Contact Details

Analytical contact Pramod Dangi, Vice President and Head Research - [email protected]

INITIATING COVERAGE 10/25/2016

Jinesh Mutha, Research Analyst - [email protected] Investor contact Garima Seth, Vice President [email protected] Business Development contact Manish Bansal, Director [email protected]

A glimpse of our capabilities

Value Ideas Investment Services Pvt. Ltd. Bajaj Bhavan, 111, 11th Floor Nariman Point Mumbai - 400 021, INDIA Contact persons – General Queries: Ms. Sheetal Shah; +91 9821464604 [email protected]