Embed Size (px)

Citation preview

Chairman'’s Communique ……......

Respected Fraternity Members,

I feel honored to assume this distinguished position as the Chairman of Largest

Branch of CIRC of ICAI. At the outset, I pay my deepest gratitude to my father for his

continuous blessings on me even after 19 years of him and to the God for giving me the

opportunity to serve the Jaipur Branch. I would also like to express my sincere

thanks and gratitude to all the fraternity members and specially to my

colleagues in the Management Committee for reposing confidence in me and

unanimously electing me to lead the most promising and active branch.

It is like a dream coming true. I am aware of the onerous responsibility which

comes along with this designation of Chairman of Jaipur Branch of CIRC of

ICAI.

As we commemorate and look forward to celebrating this 70th year of our foundation, let us make the year a

landmark one. It's my humble request to senior members to mentor our GenNext youth, teaching them the

timeless and classical attributes to become complete professionals.

I along with my Management Committee Members assure every member and student that they will be provided

with the best platform for professional and academic development with the continuous support of our respected

Central and Region Council Members.

Our activities and events for the members and students are being continuously conducted in a systematic and

coordinated manner to ensure maximum benefit to all. Going forward, I wish to focus on ensuring that a concrete

and robust platform is created for the support and development of young members both professionally and in soft

skills as they shall be representing ICAI for a long time, and also pass their knowledge to the next generation. I

ensure that our excellent infrastructure shall be optimally utilised to carry out necessary activities for all. I also

wish to host events that are specifically designed to enrich our women members and students.

Let us all work together to lead our institution to our dreams. Winston Churchill once said,

“We make a living by what we get, but we make a life by what we give”. We believe that we must also give back

to the society.

We are quite confident that your involvement in various initiatives of branch will give us inspiration to put in more

energy and to take profession to new heights. We seek your blessings, support and suggestions to convert the

dream in to reality.

Regards,

It is undoubtedly a great honor for me to be blessed

with a unique opportunity of serving the members

and students as Secretary of Jaipur Branch of CIRC

of ICAI for third consecutive term. I thank the

Managing Committee Members for electing me

as Secretary successive 3rd time of this largest

branch of CIRC of ICAI. I accept it with a deep

sense of professional responsibility and commitment.

It is my pleasure and privilege to communicate with you all through our Branch

Newsletter, as the Secretary of our esteemed & illustrious Branch. I take the

opportunity to thank all the members of Jaipur branch for their support and best

wishes without which I could not have achieved this position.

I congratulate the new team of office bearers of the branch for taking the branch

activities to a new high by conducting various Seminars, Workshops and

Certificate Courses.

Let me conclude with the wonderful quote of Nelson Mandela,

“There is no passion to be found playing small - in settling for a life that is less

than the one you are capable of living “

So Respected members, let us set our goals high and march towards a prosperous

future….

Thanking You,

Editor in Chief CA Ankit Jain 9828049550

Editor CA Amit Gattani 9414070608

Joint Editors CA Shiv Shankar Gupta 9414389398 CA Akash Bargoti 9983332663 CA Sanjay Shah 9829470807

Deputy Editors CA Akhil Jain 8890033333 CA Manan Jain 9024164785

Members CA Aashish Jain 9828505753 CA Abhishek Maheshwari 9461594721 CA Ajay Gaur 9982426699 CA Akash Jain 9460671198 CA Amit Agarwal 9414062551 CA Amit Sharma 9828126000 CA Anil Yadav 9660917000 CA Ankit Bansal 9001355573 CA Ankit Maheshwari 8094869000 CA Ankur Gupta 9461044624 CA Ankur Jain 8955865421 CA Anoop Bhatia 9571055666 CA Anu Mittal 9571476934 CA Anuj Gupta 8233966358 CA Anuj Sharma 9828152341 CA Arvind Khandewal 9829016383 CA Ashish Sharma 9829215399 CA Atul Mansingka 9414240839 CA Ayush Gupta 7742274087 CA Ayushi Jain 9929636655 CA B L Choudhary 9351320922 CA Badri Narayan Maheshwari 9829109903 CA Deepak Garg 9314254223 CA Deepak Kalani 9829138879 CA Dharmesh Gaur 9887646004 CA Dgeeraj Borad 9829068558 CA Dilip Mohata 9314616464 CA Dinesh Bohra 9680831847 CA Dinesh Natani 9414783757 CA Diwakar Shah 9928586137 CA Gaurav Jain 9649999966 CA Hansika Jain 9001794488 CA Happy Kedawat 9829062729 CA Himanshu Goyal 9829555874 CA Mahendra Modi 9352638180 CA Mansi Baid 9509572907 CA Milan Pareek 9460153100 CA Mohit Sharma 9928822522 CA Mudit Lakhotiya 8898481888 CA Nakul Dangayach 9929157400 CA Namit Vatsa 9887251033 CA Namrata Jain 9799942233 CA Neha Goyal 9928425254 CA Parkhar Nareda 9782510101 CA Pawan Bhatia 9413620006 CA Pawas Jain 9799384878 CA Pulkit Khandelwal 9783592230 CA Puneet Jain 9950144400 CA Raghav Dangayach 8290800171 CA Rakesh Lohiya 9828032031 CA Ravi Vijayvargiya 7891819191 CA Rishabh Bumb 8003495302 CA Ritu Sanghi 9950190119 CA Rohit Bakliwal 9636478844 CA Ruchita Dhoot 9829671929

CA Sachin Baheti 9829306344

CA Sachin Jain (Lal Kothi) 9829393505 CA Sachin Kumar Jain 9829720077 CA Sanjay Rathi 9414074964

CA Shailesh Mantri 9829946484 CA Shyam Maheshwari 9079134550 CA Somya Sethi 9001873000

CA Sourabh Agarwal 9828169924 CA Sugandha Jain 9828111881 CA Sunil Kumar Kumawat 7737714979

CA Umesh Jethani 9314506944 CA Vibhor Agarwal 9799425550 CA Vinod Agarwal 9414070269

CA Vinod Rathi 9828010132 CA Vipin Garg 9314032579 CA Yashasvi Sharma 9829210717

CA Yogesh Bansal 9529466585 Advisors

CA Ajay Vijaywargia CA Rajendra Kumar Bakiwala

CA Anil Bafna CA Rakesh Totuka CA Anil Lodha CA Ram Manohar Lohiya CA B P Mundra CA Ratan Goyal

CA Brijesh Maheshwari CA Ravindra Badaya CA C L Yadav CA Ravindra Raniwala CA Chandra Shekhar Sharma CA Rohit Mahehwari

CA D R Mohnot CA S C Bafna CA Dinesh Godika CA S K Somani CA G C Jain CA S L Gangwal

CA Ganesh Bangar CA S S Bhandari CA Gopal Ghiya CA S S Dhakad CA H M Singhvi CA Sanjay Ghiya

CA J K Agarwal CA Sanjay Godha CA Jagdish Somani CA Sanjay Sharda CA K K Dhoot CA Satish Gupta

CA L D Sharma CA Shailendra Agarwal CA Mangal Maheshwari CA Sharad Kabra CA Manoj Bansali CA Sudhir Bansali

CA Natwar Sarda CA Sunil Bhargava CA Nitin Vyas CA Sunil Goyal CA O P Agarwal CA Sunil Sukhla

CA P C Modi CA Suresh Chand Gupta CA P C Parwal CA Ummed Mal Jain CA P P Pareek CA Vijay Kumar Jain

CA Pankaj Malik CA Vijendra Bangar CA Pawan Jain CA Vikas Rajvanshi CA R A Sharma CA Vimal Chopra

CA R K Gurwala CA Vinod Agarwal CA R P Vijay CA Vinod Gangwal CA Rajeev Sogani CA Vipin Gangwal

Managing Committee Chairman CA Ankit Jain Vice Chairman CA Sushil Kumar Jalan

Secretary CA Sanjay Kumar Maheshwari Treasurer, CICASA Chairman CA Shishir Agarwal Chairman, CPE Committee CA Dinesh Jain

Chairman, YMEG CA Abhishek Sharma Chairman, Direct Tax Committee CA Nikhilesh Kataria Chairman, Indirect Tax Committee CA Shiv Shanker Gupta

Central Council Member, ICAI CA Shyam Lal Agarwal Central Council Member, ICAI CA Prakash Sharma Vice Chairman, CIRC, ICAI CA Rohit Ruwatia Agarwal

Secretary, CIRC, ICAI CA Pramod Boob Regional Council Member, ICAI CA Gautam Sharma

Editorial Board

Designed by : ITT Faculties of Jaipur Branch of ICAI

Anil Kumar Sharma Sanjay Kishore Karni Singh Rathore Suraj Sharma Maneesh Pareek

Published by : Sh. S. C. Chaturvedi, Administrative Officer on behalf of The Institute of Chartered Accountant of India JAIPUR (CIRC) ICAI

Bhawan, D-1, Institutional Area, Jhalana Doonagari, Jaipur-4 Ph. 0141-3044200-21 *Fax : 0141-3044215

Email : [email protected]@icai.in *website : jaipur-icai-org

Respected Professional colleague,

It gives me immense pleasure to share the May edition of

newsletter of Jaipur Branch.

In a world where there is severe competition in all walks of life, it is

difficult to differentiate and build our own identity. One of the ways

to stand out from the crowd is to “Innovate”. Professionals need an

edge to survive and Innovation can provide that edge—boosting

your productivity, growth and profitability. Also, as professionals, let’s have a hunger for

excellence. Getting passionate about our work, learning from the best, working really hard and

believing in ourselves will definitely make us attain excellence. So this coming year, lets

innovate and excel in our professional lives! I would like to take this opportunity to sincerely

thank all the contributors for sending the updates and sparing their precious time for the cause

of the profession.

In order to make the newsletter more resourceful, we need your support by way of

contribution of updates, useful suggestions, etc. I would request you to send your contributions

on the topics of Direct Taxes, GST, Corporate Law, Information technology, FEMA, Indian &

World economy and other interesting topics. We will publish the best contribution at its own

discretion.

I extend my sincere gratitude to the Editorial team for their hard work to publish this

newsletter in time.

I would like to wish all of you “Happy CA Day 2018” and also remember:-

“Write in your heart that every day is the best day in the year”

Happy Reading!

With warm Regards,

CA AMIT GATTANI Mobile: 9414070608

E-mail: [email protected]

CA Shiv Shankar Gupta CA Akash Bargoti CA Sanjay Shah

Respected Professional Colleague,

After receiving a wonderful response to the previous editions of our Newsletter, it

gives us immense pleasure to share the latest edition.

“Change is inevitable” Ours is a profession that requires constant up-gradation in

knowledge as well as learning & unlearning of topics and techniques.

With the objective of “sharing knowledge” and installing “creativity with

commitment”, we have planned a lot many interesting additions to the

newsletter, which you will find in the coming month' issues.

We wish all our readers a very happy “CA Day”. We hope that the readers find this

issue more interesting and useful.

Looking forward to your valuable feedback and suggestions, also expecting more

contributions in form of articles for future issues of our newsletter.

With warm regards

From the desk of Joint Editors…

CA Akhil Jain CA Manan Jain

Respected Professional Colleague,

The path to professional excellence has many routes which includes being

receptive to changes, learning new processes and adapting technological

advances. Though we plan and follow these promising routes but our final goal

always remains the same – Achieve Professional Excellence. To make this goal our

mission, we must look at our current progress and accordingly chart the way

forward. We must definitely address the professional needs of the members to

create leaders who shape the future of our profession as well as inspire others to

follow their footsteps.

We will continue our momentum and along the way achieve holistic growth for

the members and students of our Branch and ICAI.

Here, we take this opportunity to appeal to all my members that we need to take

active participation in branch activities. We are taking the right steps in that

direction and I will request all to contribute in the development of our e-

Newsletter.

With warm regards

From the desk of Deputy Editors…

BRANCH ACTIVITY DURING THE MONTH OF MARCH-2018

1. Full Day Seminar for Women Members “Fly with freedom- It’s never too late” (4.3.2018)

Jaipur Branch of CIRC of ICAI hosted a Full Day seminar for Women members “Fly with freedom- It’s never too late” on 04.03.2087 at Hotel Fortune Select Metropolitan, Near Nehru Sahkar Bhawan, 22 Godam Circle, Jaipur, under the aegis of Committee for Capacity Building of Members in Practice (CCBMP) ICAI.

There were three technical sessions and one Panel session. In the Inaugural Session Ms. Kamla Podddar Chairperson NIFD & Ms. Archana Surana, Chairperson ARCH Academy were the Chief Guest. CA. Abhishek Sharma (then Chairman-Jaipur Branch), CA. Sanjay Kumar Maheshwari Secretary Jaipur Branch & other Managing Committee Members were present.

First Technical Session

In this session CA. Nivedita Sarda, Jaipur was the eminent Speaker. She delivered the lecture on Profession opportunities for Women in Current Scenario.

Second Technical Session

In this session CA. Shipra Gupta, Gurgaon was the eminent Speaker. She delivered the lecture on Strengths of Her– Motivational & Networking Session.

Third Technical Session (Panle Discussion)

In this session CA. Shalini Rajvanshi, CA. Rupal Kumbhat, Ms. Rolee Agarwal IRS and Ms. Anita Hada TV journalist were the panelist. CA. Vertika Kedia was the moderator of this session.

Fourth Technical Session

In this session Sh. Ashok Sharma, AVP Axis Bank was the eminent speaker. He delivered the lecture on Investment Opportunity & Wealth creation awareness for Women Members.

2. Orientation Programme for CAs appearing in the Campus Interview (09. 03.18)

An orientation programme was conducted on 09.03.2018

by the Branch for the young budding Chartered

Accountants. This programme aimed at imparting them

with the training for appearing in the Campus Interviews

scheduled on different dates at various places in the

country and achieving success there on.

The training was imparted keeping in mind about the

contemporary demands of the corporate sector. CA. Shyam

Lal Agarwal & CA. Prakash Sharma-Central Council

Members, ICAI were the Chief Coordinators. They

welcomed the Newly Qualified Chartered Accountants. In

this programme CA. Ankit Jain–Coordinator placement

programme & Chairman-Jaipur Branch and other Managing

Committee Members were also present to inspire and

boost up the morale of the new Chartered Accountants. In

this programme CA. Rajeev Sogani delivered the lecture on

Expectation of Corporate from CAs, CA. Paresh Gupta

delivered the lecture on Role of CA in Digital Era, CA. Vimal

Chopra delivered the lecture on Corporate Ethics and

Business Communication & CA. Vishal Agarwal delivered

the lecture on opportunities in Financial Services Sector.

CA. Mohit Sancheti & CA. Milan Pareek taken the session on

Mock Interview.

3. Campus Placement Programme (12.3.2018 & 14.3.18)

Jaipur Branch of CIRC of ICAI participated in campus placement programme for the newly qualified chartered accountants under the aegis of ICAI, New Delhi on 12.3.2018 & 14.3.2018. From Jaipur Centre 05 companies participated on 12.3.2018 & One company participated on 14.3.2018 in this campus placement programme. The names of the companies which participated in this campus are mentioned below :-

S No. Name of the company

01 Infosys

02 JSW Steel Ltd.

03 Wipro Ltd

04 Whirlpool of India Ltd

05 Maruti Suzuki India

06 Ramanand Goyal & Co.

4. Half Day Seminar on Bank Audit for Article Assistants (24.03.2018)

Jaipur Branch of CIRC of ICAI organized a Half Day Seminar on Bank Audit for Article Assistants on 24.3.2018 at ICAI Bhawan. In this Seminar CA. Akesh Vyas, New Delhi was eminent speaker. He delivered the lecture on Bank Auidt. CA. Pulkit Khandelwal was the convenor of the Seminar.

5. One Day Awareness Programme on Bank Auidt (25.03.2018 – 6CPE)

Jaipur Branch of CIRC of ICAI hosted One Day Awareness Programme on Bank Audit under the aegis AASB, ICAI on 25th March, 2018 at ICAI Bhawan, Jaipur.

There were three technical sessions and one Panel Discussion session. In the Inaugural Session CA. Prakash Sharma, CCM-ICAI, CA. Shyam Lal Agarwal, Chairman AASB, ICAI, CA. Gyan Chandra Misra, Chairman-CIRC, CA. Pramod Kumar Boob, Secretary-CIRC, CA. Ankit Jain, Chairman-Jaipur Branch, CA. Sanjay Kumar Maheshwari, Secretary-Jaipur Branch and other Managing Committee Members of Jaipur Branch were also present. On this occasion Jaipur Branch of CIRC of ICAI felicitated to CA. Gyan Chandra Misra being elected as Chairman-CIRC, CA. Rohit Ruwatia Agarwal being elected as Vice Chairman-CIRC, CA. Pramod Kumar Boob being elected as Secretary-CIRC & CA. Gautam Sharma being Regional Council Member-CIRC by presenting Memento, Safa & shawl. CA. Pulkit Khandelwal was the convenor of this inaugural session.

First Technical Session

In this session CA. Akesh Vyas, New Delhi was the eminent Speaker. CA. Akesh Vyas delivered the lecture on NPA Provisions & Prudential Norms. CA. Mudrika Natani was the convenor of the session.

Second Technical Session

In this session CA. Niranjan Joshi, Mumbai was the eminent Speaker. He delivered the lecture on Overview of Bank Branch Audit (Planning, Reporting & Certifications). CA. Rekha Maheshwari was the convenor of the session.

Third Technical Session

In this session CA. Nishith Seth, New Delhi was the eminent speaker. He delivered the lecture on Bank Audit in I.T. Environment in CBS & System Audit including Internal Control. CA. Harsha Ramnani was the convenor of the session.

Fourth Technical Session (Panel Discussion by Experts)

In this session CA. Shyam Lal Agarwal, Chairman AASB was the session Chairman. CA. S. S. Bhandari, CA. Mukesh Gupta, CA. Ajay Atolia, CA. Vikas Rajvanshi, CA. Niranjan Joshi, Mumbai, CA. Akesh Vyas, CA. Nishith Seth & CA. Shyam Lal Agarwal, Chairman AASB & Central Council Member, ICAI were the panelist.

BRANCH ACTIVITY DURING THE MONTH OF APRIL-2018

1. S C Meeting on E-Way Bill & Refund Procedure under GST (07.04.2018 - 2CPE)

Jaipur Branch of CIRC of ICAI organized a S C Meeting on E-Way Bill & Refund Procedure under GST on 07.04.2018 at ICAI Bhawan, Jaipur. CA. Ayush Gupta was the eminent speaker. CA. Ayush Gupta delivered the lecture on above subject during the programme. CA. Raghav Dangayach was the convenor of the meeting.

2. S C Meeting on Effectively Challenging Reopening u/s 148 of Income Tax Act 1961 (14.04.2018 - 2CPE)

Jaipur Branch of CIRC of ICAI organized a S C Meeting on S C

Meeting on Effectively Challenging Reopening u/s 148 of

Income Tax Act 1961 on 14.04.2018 at ICAI Bhawan, Jaipur.

CA. Rohan Sogani was the eminent speaker. CA. Rohan

Sogani delivered the lecture on above subject during the

programme. CA. Pulkit Khandelwal was the convenor of the

meeting.

3. Special Session on Growing Businesses and Overcoming Turbulence (16.04.2018 - 2CPE)

Jaipur Branch of CIRC of ICAI hosted a Special Session on

Growing Businesses and Overcoming Turbulence under the

aegis of Committee for Capacity Building of Members in

Practice (CCBMP), ICAI & International Affairs (IA), ICAI on

16.04.2018 at ICAI Bhawan, Jaipur. Mr. Abdulwahid Aboo,

Kenya was the eminent speaker. In this occasion CA. Ankit

Jain, Chairman & CA. Sanjay Kumar Maheshwari, Secretary

Jaipur Branch felicitated to Mr. Abdulwahid Aboo by

presenting Memento & shawl. Mr. Abdulwahid Aboo

delivered the lecture on above mentioned subject during

the programme. CA. Mudrika Natani was the convenor of

the meeting.

4. Motivation Session How to Prepare & Face CA Examinations (19.04.2018)

The Jaipur Branch organized a Motivational Programme on

How to Prepare & Face CA Examinations on 19.04.2018 at

ICAI Bhawan from 4.00PM to 6.00PM. CA Pramod Kumar

Boob, Secretary, CIRC, ICAI was the eminent speaker. CA.

Pramod Kumar Boob delivered the lecture on above

subject.

5. S C Meeting on Practical aspects under RERA (21.04.2018 - 2CPE)

The Jaipur Branch organized a S C Meeting on S C Meeting

on Practical aspects under RERA on 21.04.2018 at ICAI

Bhawan, Jaipur. CA. Himanshu Goyal was the eminent

speaker. CA. Himanshu Goyal delivered the lecture on

above subject during the programme. CA. Shivangi Shukla

was the convenor of the meeting.

6. 6 Days GST Workshop (23.4.18 to 28.4.18)

Jaipur Branch of CIRC of ICAI organized GST workshop for CA members from 23.4.2018 to 28.4.2018 at ICAI Bhawan, Jaipur. On 23.4.2018 CA. Ranjan Mehta was the eminent speaker,

he delivered the lecture on Specific concept &

contemporary Issues of Supply & Time of Supply and Value

of Supply.

On 24.4.2018 CA. Rahul Lakhwani was the eminent speaker,

he delivered the lecture on Specific concept &

contemporary Issues in Place of Supply of Goods and

Services.

On 25.4.2018 CA. Jatin Harjai was the eminent speaker, he

delivered the lecture on Specific concept & contemporary

Issues in Input Tax Credit.

On 26.4.2018 CA. Varun Khandelwal was the eminent

speaker, he delivered the lecture on Specific concept &

contemporary Issues in Refunds, ISD, Job Work Procedure.

On 27.4.2018 CA. Vikas Modi was the eminent speaker, he

delivered the lecture on E-Way Bill, Maintenance of

Records and Finalization of Books of Accounts under GST

Regime.

On 28.4.2018 CA. Yash Dhadda & CA. Pulkit Khandelwal

were the eminent speakers, they delivered the lecture on

Specific Concept & contemporary issues in Advance ruling,

SCN, Inspection of Vehicles & Premises.

CA. Ashutosh Agarwal, CA. Manan Jain, CA. Mohit Patni and

CA. Deepak Jain were the convenors of this workshop.

BRANCH ACTIVITY DURING THE MONTH OF MAY-2018

1. SC Meeting on Practical issues & possible solutions on E-way bills under GST (05.05.2018-2CPE)

Jaipur Branch of CIRC of ICAI organized S C Meeting on Practical issues & possible solutions on E-way bills under GST on 05.05.2018 at ICAI Bhawan, Jaipur. CA. Ujjval Sharma was the eminent speaker. CA. Ujjval Sharma delivered the lecture on above subject during the programme. CA. Rakesh Lohiya was the convenor of the meeting.

2. 4 Days Workshop on Adv. Excel changed to Power Excel (7.5.18 to 10.5.18)

Jaipur Branch of CIRC of ICAI organized 4 Days Workshop on Adv. Excel changed to Power Excel for CA members from 7.5.2018 to 10.5.2018 at ICAI Bhawan, Jaipur. CA. Sachin Jain (Lalkothi) was the eminent trainer of this

workshop. CA. Sachin Jain taken the session on explore the

power of Power Query, Power Pivot and Power BI to

participants.

3. Full Day Programme in Memenory of S. Vaidyanath Aiyar (19.05.2018 – 6 CPE)

Jaipur Branch of CIRC of ICAI hosted Full Day programme on

S. Vaidyanath Aiyar Memorial Lecture CA Members on

Saturday 19th

May, 2018 at ICAI Bhawan, Jaipur under the

aegis of CIRC of ICAI.

There were three technical sessions and one session of

Panel Discussions. CA Prakash Sharma, Central Council

Member, ICAI, CA Ankit Jain, Chairman, Jaipur Branch, CA

Sanjay Kumar Maheshwari, Secretary-Jaipur Branch & CA

Gyan Chandra Misra, Chairman, CIRC of ICAI, CA. Rohit

Ruwatia Agarwal, Vice Chairman, CIRC of ICAI, CA Pramod

Kumar Boob, Secretary, CIRC of ICAI and others Managing

Committee Members Jaipur Branch inaugurated the

programme by lighting the lamp.

First Technical Session

In this session CA. Siddharth Ranka, Jaipur was the eminent Speaker. CA. Siddharth Ranka delivered the lecture on Family Trust & HUF Tax planning.

Second Technical Session

In this session Adv. Kapil Goel, New Delhi was the eminent Speaker. Adv. Kapil Goel delivered the lecture on Notice & Assessment under section 147/148 of Income Tax Act.

Third Technical Session

In this session CA. P C Parwal, Jaipur was the eminent speaker. CA P C Parwal delivered the lecture on Amendments by Finance Act 2018 & New Income Tax return forms.

Fourth Technical Session (Panel Discussion on Benami Law & Penny Stock)

In this session a Panel Discussion was arranged on Benami

Law & Penny Stock. CA. O P Agrawal, CA. P C Parwal, CA

Satish Kumar Gupta & Adv Kapil Goel were the panelist. CA.

Nikhilesh kataria, Chairman, Direct Tax Committee, Jaipur

Branch was the moderator of the session.

4. S C Meeting on Legal mandate, Practices, Procedures & Precautions to Protect Office Data & its Security (26.05.2018-2CPE)

Jaipur Branch of CIRC of ICAI organized S C Meeting on

Legal mandate, Practices, Procedures & Precautions to

Protect Office Data & its Security on 26.05.2018 at ICAI

Bhawan, Jaipur. Dr. C B Sharma, IPS, Retd. was the eminent

speaker. Dr. Sharma delivered the lecture on above subject

during the programme. CA. Manan Jain was the convenor

of the meeting.

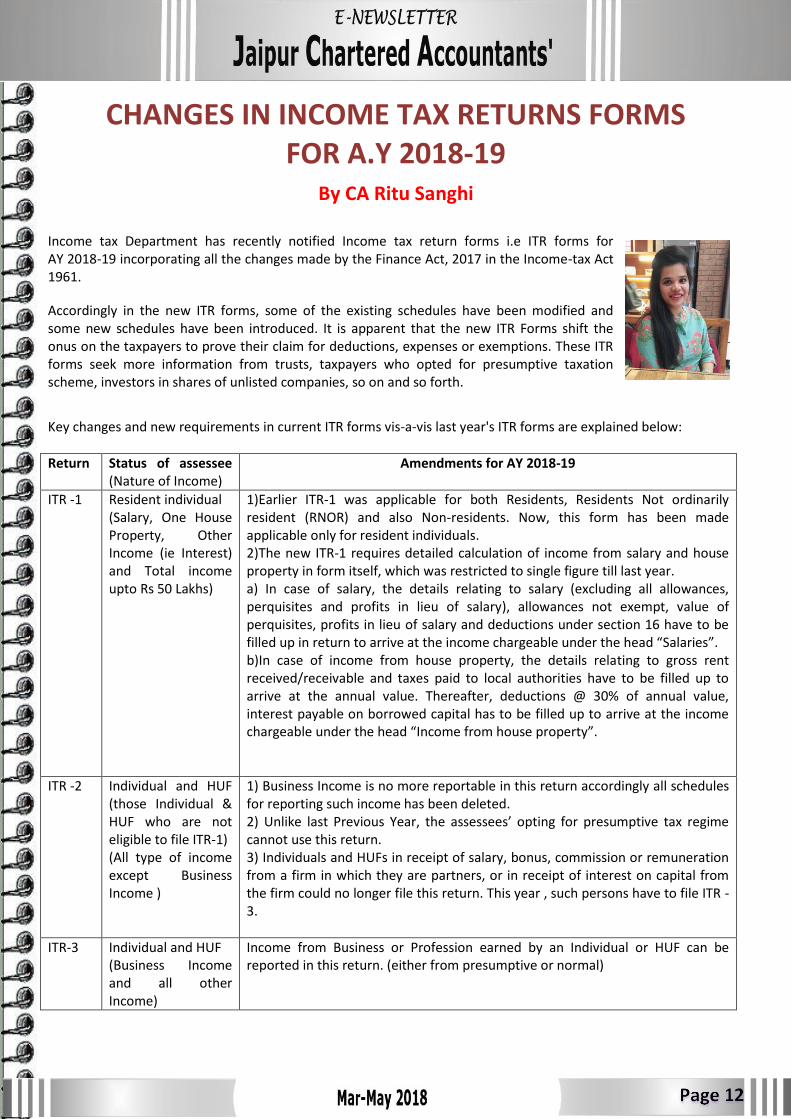

CHANGES IN INCOME TAX RETURNS FORMS FOR A.Y 2018-19

By CA Ritu Sanghi

Income tax Department has recently notified Income tax return forms i.e ITR forms for AY 2018-19 incorporating all the changes made by the Finance Act, 2017 in the Income-tax Act 1961.

Accordingly in the new ITR forms, some of the existing schedules have been modified and some new schedules have been introduced. It is apparent that the new ITR Forms shift the onus on the taxpayers to prove their claim for deductions, expenses or exemptions. These ITR forms seek more information from trusts, taxpayers who opted for presumptive taxation scheme, investors in shares of unlisted companies, so on and so forth.

Key changes and new requirements in current ITR forms vis-a-vis last year's ITR forms are explained below:

Return Status of assessee (Nature of Income)

Amendments for AY 2018-19

ITR -1 Resident individual (Salary, One House Property, Other Income (ie Interest) and Total income upto Rs 50 Lakhs)

1)Earlier ITR-1 was applicable for both Residents, Residents Not ordinarily resident (RNOR) and also Non-residents. Now, this form has been made applicable only for resident individuals. 2)The new ITR-1 requires detailed calculation of income from salary and house property in form itself, which was restricted to single figure till last year. a) In case of salary, the details relating to salary (excluding all allowances, perquisites and profits in lieu of salary), allowances not exempt, value of perquisites, profits in lieu of salary and deductions under section 16 have to be filled up in return to arrive at the income chargeable under the head “Salaries”. b)In case of income from house property, the details relating to gross rent received/receivable and taxes paid to local authorities have to be filled up to arrive at the annual value. Thereafter, deductions @ 30% of annual value, interest payable on borrowed capital has to be filled up to arrive at the income chargeable under the head “Income from house property”.

ITR -2 Individual and HUF (those Individual & HUF who are not eligible to file ITR-1) (All type of income except Business Income )

1) Business Income is no more reportable in this return accordingly all schedules for reporting such income has been deleted. 2) Unlike last Previous Year, the assessees’ opting for presumptive tax regime cannot use this return. 3) Individuals and HUFs in receipt of salary, bonus, commission or remuneration from a firm in which they are partners, or in receipt of interest on capital from the firm could no longer file this return. This year , such persons have to file ITR -3.

ITR-3 Individual and HUF (Business Income and all other Income)

Income from Business or Profession earned by an Individual or HUF can be reported in this return. (either from presumptive or normal)

ITR-4 Individual , HUF and Firms (Presumptive Taxation)

1) In case a taxpayer opts for presumptive taxation scheme under section 44AD, 44ADA or 44AE, he will have to file the return of income in form ITR 4. 2) Additional Details sought in new ITR-4 are: GSTR Number (if registered) Turnover/ Gross receipt as per GST returns The old ITR 4 sought only 4 financial particulars of the business, a) total creditors, (b) total debtors, (c) total stock-in-trade and (d) cash balance. (a to d mandatory) The new ITR 4 form seeks details of other financial particulars of business such as partners/members own capital, secured/unsecured loans, advances, other liabilities fixed assets, bank balance, other assets etc (to the extent applicable)

ITR-5 Partnership Firms There are no other changes in the ITR -5 form other than the common clauses added in the form

ITR-6 Companies other than companies claiming exemption under section 11 (All type of income)

1)Additional disclosure requirements for Ind AS-Compliant Companies A new Schedule for Ind AS Compliant companies has been introduced wherein they shall be required to disclose the balance sheet and profit & loss account in the same format as prescribed under of Schedule III to the Companies Act, 2013. . 2)Break-up of payments/receipts in foreign currency A new schedule FD has been inserted wherein breakup of payment and receipts in foreign currency are required to be reported by an assessee who is not liable to get its accounts audited under Section 44AB. 3) Reporting of CSR appropriations A new column has been inserted to provide details of apportionments made by the companies from the net profit for the CRS( Corporate Social Responsibility) activities. 4) MAT Adjustments MAT Adjustments for Ind-AS Compliant companies, adjustments for permissible deductions/allowances, have now been provided. Changes have also been made in the Schedule MAT wherein information relevant to Ind AS Compliant companies as per sub-section (2A) to (2C) to section 115JB has to be Furnished 5) Details of Beneficial Owners Every unlisted company is required to provide details of all beneficial owners who are holding 10% or more voting power (directly or indirectly) at any time during the year 2017-18.These companies are required to provide the name, address, percentage of shares held and PAN of the beneficial owners. 6) GST Transactions A new Schedule has been inserted which requires every company, who is not required to get its accounts audited under Section 44AB, to provide break up of total expenditure in two parts i.e. (i)expenditure in respect of entities registered under GST viz. a). relating to exempt goods or services b.) relating to entities falling under composition scheme c.) relating to other GST registered entities. AND (ii)expenditure relating to entities not registered under GST.

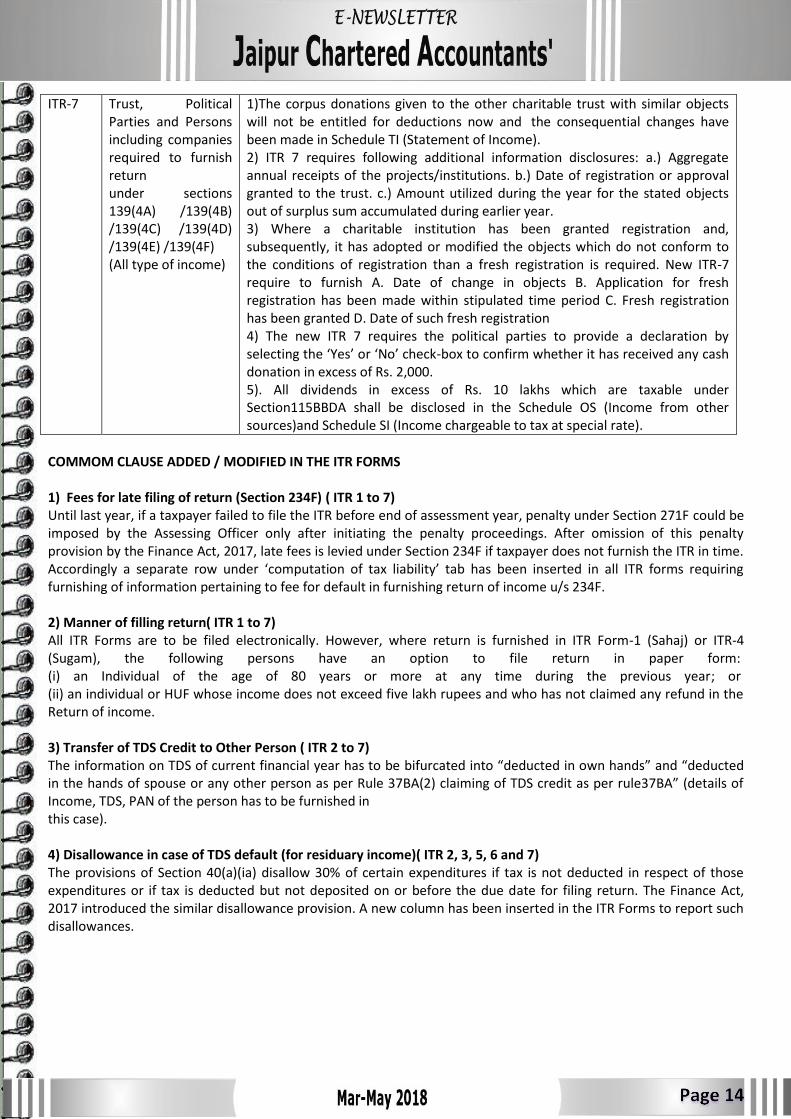

ITR-7 Trust, Political Parties and Persons including companies required to furnish return under sections 139(4A) /139(4B) /139(4C) /139(4D) /139(4E) /139(4F) (All type of income)

1)The corpus donations given to the other charitable trust with similar objects will not be entitled for deductions now and the consequential changes have been made in Schedule TI (Statement of Income). 2) ITR 7 requires following additional information disclosures: a.) Aggregate annual receipts of the projects/institutions. b.) Date of registration or approval granted to the trust. c.) Amount utilized during the year for the stated objects out of surplus sum accumulated during earlier year. 3) Where a charitable institution has been granted registration and, subsequently, it has adopted or modified the objects which do not conform to the conditions of registration than a fresh registration is required. New ITR-7 require to furnish A. Date of change in objects B. Application for fresh registration has been made within stipulated time period C. Fresh registration has been granted D. Date of such fresh registration 4) The new ITR 7 requires the political parties to provide a declaration by selecting the ‘Yes’ or ‘No’ check-box to confirm whether it has received any cash donation in excess of Rs. 2,000. 5). All dividends in excess of Rs. 10 lakhs which are taxable under Section115BBDA shall be disclosed in the Schedule OS (Income from other sources)and Schedule SI (Income chargeable to tax at special rate).

COMMOM CLAUSE ADDED / MODIFIED IN THE ITR FORMS 1) Fees for late filing of return (Section 234F) ( ITR 1 to 7) Until last year, if a taxpayer failed to file the ITR before end of assessment year, penalty under Section 271F could be imposed by the Assessing Officer only after initiating the penalty proceedings. After omission of this penalty provision by the Finance Act, 2017, late fees is levied under Section 234F if taxpayer does not furnish the ITR in time. Accordingly a separate row under ‘computation of tax liability’ tab has been inserted in all ITR forms requiring furnishing of information pertaining to fee for default in furnishing return of income u/s 234F. 2) Manner of filling return( ITR 1 to 7) All ITR Forms are to be filed electronically. However, where return is furnished in ITR Form-1 (Sahaj) or ITR-4 (Sugam), the following persons have an option to file return in paper form: (i) an Individual of the age of 80 years or more at any time during the previous year; or (ii) an individual or HUF whose income does not exceed five lakh rupees and who has not claimed any refund in the Return of income. 3) Transfer of TDS Credit to Other Person ( ITR 2 to 7) The information on TDS of current financial year has to be bifurcated into “deducted in own hands” and “deducted in the hands of spouse or any other person as per Rule 37BA(2) claiming of TDS credit as per rule37BA” (details of Income, TDS, PAN of the person has to be furnished in this case). 4) Disallowance in case of TDS default (for residuary income)( ITR 2, 3, 5, 6 and 7) The provisions of Section 40(a)(ia) disallow 30% of certain expenditures if tax is not deducted in respect of those expenditures or if tax is deducted but not deposited on or before the due date for filing return. The Finance Act, 2017 introduced the similar disallowance provision. A new column has been inserted in the ITR Forms to report such disallowances.

5) Reporting of sum taxable as Gift (ITR 2, 3, 5, 6 and 7) Erstwhile provisions of Section 56(2)(vii) were applicable only to an individual and HUF. The Finance Act, 2017 had extended, the scope of this provision by introducing a new clause, i.e. Section 56(2)(x) which covers all taxpayers within its ambit and accordingly new columns have been inserted in ITR forms under ‘Schedule OS’ to report such income. 6) Details of GST paid and refunded (ITR 3, 5, and 6) The new ITR forms have introduced new columns to report CGST, SGST, IGST and UTGST paid by, or refunded to, assessee during the Financial Year. [Applicable for ITR 3, 5, and 6] 7) Section wise capital gains exemption (ITR 2, 3, 5 and 6) The new ITR Forms introduce specific columns to report each capital gain exemption separately. Details of each capital gains exemption under Sections 54, 54B, 54EC, 54EE, 54F, 54GB and 115F shall be reported in its applicable column now. Further, a taxpayer availing of these capital gains exemptions is required to mention the date of transfer of original capital asset which was missing in earlier ITR Forms. (Applicable to ITR 2, 3, 5 and 6) 8) Capital gains on transfer of unquoted shares (ITR 2, 3, 5, 6 and 7) In the case of capital gain arising on transfer of unquoted shares, it would now be mandatory for the investors to obtain the valuation report. To ensure that investors correctly report the capital gains from unlisted shares, the new ITR Forms require the taxpayer to provide figures of actual sales consideration and FMV as determined by a Merchant Banker or CA. 9).Revised Depreciation Schedule (ITR 3, 5 and 6) CBDT has restricted the highest rate of depreciation for any block of asset to 40%. i.e. all block of assets which were eligible for depreciation at the rate of 50%, 60%, 80% or 100% would be eligible for depreciation at the rate of 40%. Accordingly Depreciation Schedule in ITR-3, ITR-5 & ITR-6 has been modified. The following additional information is also required to be disclosed in Schedule DPM: • Depreciation disallowed under section 38(2) of the Income-tax Act,1961. • Net aggregate depreciation. • Proportionate aggregate depreciation allowable in the event of succession, amalgamation, demerger etc 10) Details of foreign bank account of non-residents (ITR 2, 3, 4, 5, 6 and 7) In case of non-residents, the requirement of furnishing details of anyone foreign Bank Account has been included for the purpose of credit of refund. 11) Impact on profit or loss due to ICDS deviation (ITR 3, 5 and 6) The new ITR Forms require separate reporting of both profit and loss (and not on net basis) in Schedule-OI, Schedule BP (Computation of income from business or profession) and Schedule ICDS. [Applicable to ITR 3,5 and 6] 12) Removal of 'Gender' from personal information (ITR 2, 3 and 4) Individual taxpayers who are filing income-tax return in Form ITR 2 or ITR 3 or ITR 4 aren’t required to mention the gender, i.e., male or female or transgender, as the column of gender has been removed. Hope these keys points will help the taxpayers in providing required details in correct applicable ITR forms and proper filling of ITR for AY 2018-19 in order to avoid any deficiency pointed out by CPC.

*******

Ransomware and Auditor’s role By CA Ankita Sankhala

The adage is true that the security system has to win every time, the attacker has to win only once- Dustin Dykes In today time auditor’s responsibility is not limited to conduct audit as required in laws but as an auditor we have some more responsibilities towards our client and we have to aware them about ransomware and its impact on their whole business environment

Ransomware is a malicious software which is designed in such a way that it can block access to an individual computer system until a sum of money is paid in ransom. If an individual didn’t pay that ransom then their computer system may remain blocked and individual will not able to access anything in the system. It is a malware designed to make target’s data unusable or to prevent access to systems.

If computer system of individual of any business organization got blocked due to this malware then owner of system will not able to access any of its financial records, contracts, policies or whatever data is saved on that system is not accessible until demanded ransom is paid in hard to trace digital currency to the attacker.

Businesses are often willing to pay whatever sum is demanded of them to get back to business as soon as possible as they have to resume their business otherwise this will affect their business processes.

Once this malware has gained entry, it will identify an organization’s most sensitive or prized data, corrupt the data to make them useless, create backdoors in the system to make future infiltrations easy and encrypt the data all before sending a ransom demand. Ransomware goal is not steal data but to deny access.

Ransomware will not only affect the files at workstation, Software is smart enough to travel across your network and encrypts any files located on mapped and unmapped network drivers. It just like a Chartered Accountant office is attacked and through that they get details of all the clients and encrypt them.

To kidnap a human for ransom or rob a bank is risky task to get money but ransomware is an easy option to earn money. Attacker can do it from any part of the world.

There is no such things as 100 % security but companies should implement reasonable security as Prevention is the best defense.

There are many ways a computer system is attacked:-

Individual get an email which look alike a business email or invoice and when it’s downloaded system got infected with some malicious file or software.

When an individual download any file from internet then malicious file also downloaded from the internet.

Sometimes individual get free software options on internet and when an individual installs that software or open an infected webpage malicious code also get installs with the software and affects the system.

Businesses should have a strategy or proper incident management plan in case of a cyberattack. While scrubbing or restoring entire network or infected files make sure that attackers or any malicious code is no more.

As an auditor while conducting an audit of Information system an auditor have to consider few points and aware their clients about it.

Remove excessive permissions to access sensitive and critical data or limits each user access rights as it will limits the power of ransomware.

Prepare a software restriction policy and ask client to block the typical ransomware extensions it will prevent malware or malicious code from running.

Clients may also face litigation or scrutiny from regulators and consumers so they also hire lawyer to face that litigation and be prepared for such situations also.

Attacker mainly exploit a vulnerability running on old version of system. Auditor have to verify that system is running on current version.

Auditor have to verify that patches are being applied on timely manner as and when required and update the system.

Auditor have to check and verify that devices which are connected from internet also updated such as TV, Voice activated device and other device

Check and confirm that anti-virus is updated and effective enough to protect the system from any malware.

Check and verify that data is backed up on time and is effective and properly designed otherwise backed up system may also get affected from the virus and it will no more usable.

Auditor have to assure that employees are trained and educated about such malware, they have knowledge about what types of files may contain virus and malware and they don’t download any unnecessary software on the workstation and don’t open any unwanted email or download it to workstation.

Auditor have to check and assure that vulnerability scanning is performed on timely basis for the whole network and these reports are not ignored by the management and lessons should be learnt from the findings and proper steps are taken by senior management.

Auditor can check the vulnerability and suggest client the option of insurance to cover ransom, legal fees, consultant fees, loss of business due to operations slowdown/shutdown, data destruction, damage to reputation.

Auditor can check and help client in establishing guidelines and company’s policies and procedures for protecting sensitive data on corporate computers and mobile devices.

Auditor can take help from third party and advice client to hire them in the event of crisis as they are experts of field and can manage such situations.

Auditor have verify that early warning system is enabled and detect a ransomware attack in progress using threshold based alerts that will keep aware if any anomalous file activity on the servers. It will alert the teams that any malicious code is entered in the system and they can respond to the incidents quickly.

Auditor have to check that firewall and intrusion Detection System is working properly and effective to stop any virus or malicious code from entering the network.

Auditor should question whether senior executives have holistic approach for people, process and technology to make a defense strategy successful.

Auditor have to go through the defense strategy that help to block attacks and quickly discover any infections in progress it will limit the impacts on data and operations.

Auditor have to check that multi layered end point security, network security, encryption and strong authentication and reputation based technologies is implemented and working properly to block any spam mail and malicious code to damage the system.

This list is not full and final list but it can help auditor to prevent their client from attack of any malware. Auditor and client both should be updated with the change in technologies as these kind of attacks is always on headline of newspapers. These days payment are demanded in Bitcoin. Due to this attacker go untraceable as Bitcoin is in decentralized form and no one in the world know personal details of buyer and seller.

Recently electricity department of one state in India is also attacked by ransomware. Big Companies like Sony Pictures also attacked in past from these kinds of attacks and it impacts not only their bank balance but also affects their reputation in the market. Every time reason of attack is not to gain financial benefits but sometimes it is due to personal grudges.

Prevention is always better then cure. So try to secure system and be alert from these kind of viruses as they will result in big losses to companies.

*******

GST REFUND PROCEDURE – AN ANALYTICAL REVIEW By CA Ekta Jain

GST has been a Pandora box since its release; it has been a roller costar ride for whole of the nation. Logic to bring in such a radical change in Indirect taxation process has been to bring in a smooth flow of funds compliances till the end, and such a simplification cannot be thought of without a hassle-free REFUND mechanism. So, what is offered in the refund structure of GST law is covered mainly u/s 54 of CGST Act, 2017, some of the provisions are also discussed in Section 15 of IGST Act,2017 and u/s section 54 of RSGST Act (for Rajasthan). Under the GST regime, for availing refund of tax claimed under different circumstances separate list of Section is prescribed covered under Chapter XI . Chapter X , Rule 89 to Rule 97 encompasses the procedural requirements and various forms involved in the entire process of application, sanction and rejection of Refund under GST. Refund mechanism under GST also provide as u/s 54(4), that where the amount claimed as refund is less than two lakh rupees, it shall not be necessary for the applicant to furnish any documentary & other evidences, but he may file a declaration, certifying that the incidence of such tax and interest has not been passed on to any other person, thus trying to simplify the procedural requirement. Doctrine of unjust enrichment which was applicable on availing refund of additional customs duty, excise duty & service tax is also adopted into GST regime which is covered u/s 57 of CGST Act, 2017 The term refund is defined as under u/s 54 of CGST Act, 2017 “refund” includes refund of tax paid on zero-rated supplies of goods or services or both or on inputs or input services used in making such zero-rated supplies, or refund of tax on the supply of goods regarded as deemed exports, or refund of unutilised input tax credit as provided under sub-section 54(3).. Identification of Events where Refund arise under GST-: (1). A specialised agency of the UNO or any MFI’s and Organization notified under the United Nations (Privileges and Immunities) Act, 1947, Consulate or Embassy of foreign countries or any other person or class of persons, as notified under section 55, are entitled to a refund of tax paid by it on inward supplies of goods or services or both. (2). A registered person, supplying zero rated supplies made without payment of tax, i.e. against a bond or

LUT, may claim refund of any unutilized ITC , at the end of any tax period. (3). A registered person, supplying zero rated supplies made after payment of tax, may claim refund of tax paid by him on his outward export supplies. (4). A registered person making supplies chargeable at lower rate of tax while his inputs being charged at higher rate of tax, may also claim refund of such excess ITC paid by him. (5). In case tax is deposited under protest and where the tax becomes refundable as a consequence of judgment, decree, order or direction of the Appellate Authority, Appellate Tribunal or any court. (6). The balance in the Electronic Cash Ledger or Electronic credit ledger after payment of tax, interest, penalty, fee or any other amount payable under this act or the rules made thereunder may be refunded. (7). Supply of goods regarded as Deemed Exports, refund can be claimed either by the supplier or the recipient. (8). In case where tax is paid on advance received by the supplier and eventually supplies not made due to cancellation of contract or for any other reason, refund in such cases may also be filed by the registered person. As it is known vide notification no. 66/2017-Central Tax dated 15-11-2017 all taxpayers are now exempted from payment of tax on advances received in case of supply of goods. (9). In case of mistake on part of a registered dealer, regarding taxability of a particular supply as inter-state supply or intra-state supply as a consequence of which tax been deposited under a wrong head, such registered person shall first deposit the tax due under right head & thereafter may make an application for refund of tax deposited under the wrong head, as specified in sub rule 89(2)(j) (10). In case of mistake on part of a registered dealer, while determining nature of a particular supply, as supply of goods or supply of services, as a consequence of which tax calculation goes wrong and some excess tax been deposited by him, such registered person may also file application for claim of refund of excess tax deposited, as per sub rule 89(2)(k).

Above mentioned circumscribe the broad line of events where refund can be applied by any person for any tax and interest, if any, paid by him, before the expiry of specified time from the relevant date in FORM GST RFD-01and manner outlined by Rule 89 of CGST Act. Who can claim refund of GST through online form RFD-01 Any person, except the first two categories as mentioned below may file an application in FORM GST RFD-01:

Persons covered under notification issued

under section 55, claiming refund of any tax, interest, penalty, fees or any other amount paid by him,

Persons claiming refund of integrated tax paid on goods exported out of India,

In case the reason for filing refund claim being the excess balance in the electronic cash ledger i.e. in case of excess tax deposited by a registered person, then claim for such refund may also be filed at the time of filing return in FORM GSTR-3, FORM GSTR-4 or FORM GSTR-7, as the case may be under the GST Act and no separate application in FORM GST RFD-01 for refund is required in such cases.

In case of Supplies to a Special Economic Zone unit or a Special Economic Zone developer, the application for refund shall be filed by the –

(a) Only supplier of goods after such goods have been admitted in full in the Special Economic Zone for authorised operations, as endorsed by the specified officer of the Zone in RFD-01

(b) Only supplier of services along with such evidence regarding receipt of services for authorised operations as endorsed by the specified officer of the Zone in RFD-01

In respect of supplies regarded as deemed exports, the application may be filed by,

(a) the recipient of deemed export supplies; or

(b) the supplier of deemed export supplies in cases where the recipient does not avail of input tax credit on such supplies and furnishes an undertaking to the effect that the supplier may claim the refund

ACKNOWLEDGMENT OF REFUND APPLICATION (Rule 90)-: Where a registered person applies for refund at the time of filing return in FORM GSTR-3, FORM GSTR-4 or FORM GSTR-7, as the case may be under the GST Act, an acknowledgement shall be generated in FORM GST RFD-02, as per rule 90(1), clearly indicating the date of filing of the claim for refund. Where refund application is filed in FORM GST RFD-01, except specified above, proper officer shall, within fifteen days of filing of the said application, scrutinize the application for its completeness and where the application is found to be complete, proper officer shall issue an acknowledgement in FORM GST RFD-02, clearly indicating the date of filing of the claim for refund. Where any deficiencies are noticed in the application for refund filed by a registered person, the proper officer shall communicate the deficiencies to the applicant in FORM GST RFD-03, requiring him to file a fresh refund application after rectification of such deficiencies. Also in case such deficiencies have been communicated by proper officer, to a registered person, where the application to claim refund was filed on account of refund of input tax credit, and where the electronic credit ledger of the applicant was debited by him for an amount equal to the refund so claimed, the amount so debited shall be re-credited to the electronic credit ledger of the applicant.

GRANT OF PROVISIONAL REFUND AND ORDER SANCTIONING REFUND-:

After the proper office is satisfied, he may either: - Issue full refund to the bank account of the

Registered Person as per section 54(8) in cases pertaining to-: (a) refund of tax paid on zero-rated supplies of goods or services or both or on inputs or input services used in making such zero-rated supplies; (b) refund of unutilised input tax credit ; i.e un-utilised input tax credit where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies; i.e. credit as per section 54(3) (c) refund of tax paid on a supply which is not provided, either wholly or partially, and for which invoice has not been issued, or where a refund voucher has been issued; (d) refund of tax in pursuance of section 77i.e. tax wrongfully collected and paid to Central Government or State Government.

(e) the tax and interest, if any, or any other amount paid by the applicant, if he had not passed on the incidence of such tax and interest to any other person; or (f) the tax or interest borne by such other class of applicants as the Government may, on the recommendations of the Council, by notification, specify. In above mentioned cases CA certificate is also not required to be furnished for claim of refund as per sub-rule 89(2)(m). After making refund order in FORM GST RFD-06, where the proper officer is satisfied that the amount need to be credited to applicant bank account, he shall issue a payment advice in FORM GST RFD-05, for the amount of refund and the same shall be electronically credited to any of the bank accounts of the applicant mentioned in his registration particulars and as specified in the application for refund as per rule 92(4). FORM GST RFD-06 order shall clearly mention the amount of total refund due, refund already made to him on provisional basis, amount adjusted against any outstanding demand under the Act or under any existing law and the balance amount refundable. - Credit full refund to the account of Consumer Welfare Fund u/s 57-: In cases other than discussed above the proper officer shall credit the refund so determined to the Consumer Welfare Fund which shall be utilised by the Government for the welfare of the consumers in such manner as may be prescribed. Such order shall be issued within 60 days of receipt of application complete in all respects u/s 54(7). In case the proper officer is satisfied that the amount refundable is liable to be credited to Consumer Welfare Fund u/s 54(5), he shall make an order in FORM GST RFD-06 and shall issue a payment advice in FORM GST RFD-05, for the amount of refund to be credited to the Consumer Welfare Fund as per rule 92(5) However, in such cases refund of amount less than Rs. 1000/- shall not be made by the proper officer in accordance with Sec 54(14). - Withhold the refund on account of outstanding liabilities of the Registered Person-: Also, where the proper officer is of the opinion that the amount of refund is liable to be withheld under sub-section 10 or sub-section 11 of section 54, he shall pass an order in Part B of FORM GST RFD-07 informing him the reasons for withholding of such refund as per Rule 92(2).

- Adjust the outstanding liabilities of the Registered Person with its refund due-: In cases where the amount of refund is completely adjusted against any outstanding demand under the Act or under any existing law, an order giving details of the adjustment may be issued in Part-A of FORM GST RFD-01 as per proviso to rule 92(1). - Reject the refund application. In case the proper officer is satisfied, for reasons to be recorded in writing, that the whole or any part of the amount claimed as refund is not admissible or is not payable to the applicant, he shall issue a show cause notice in FORM GST RFD-08 to the applicant, requiring him to furnish a reply in FORM GST RFD-09 within fifteen days of the receipt of such notice and after considering the reply, make an order in FORM GST RFD-06, sanctioning the amount of refund in whole or part, or rejecting the said refund claim. However, no application for refund shall be rejected without giving the applicant a reasonable opportunity of being heard as per Sub rule (3) of Rule 92. Also in case any amount claimed as refund is rejected, either fully or partly, the amount debited, to the extent of rejection, shall be re-credited to the electronic credit ledger by an order made in FORM GST PMT-03. Identification of Events where Refund do not arise under GST-: One important point here to note is that, under the GST regime, refund of un-utilised input tax credit shall not be allowed:- 1. In cases where the goods exported out of India

are subjected to export duty as provided under proviso to sec 54(3) or

2. If the supplier avails of drawback in respect of central tax paid on such supplies as provided under proviso to sec 54(3), or

3. If the supplier claims refund of the integrated tax paid on such supplies of exports.

Thus, process of refund is thorough and detailed, and strives at reducing the long drawn refund clearance procedure. Under GST those Refund which took years to pass would take just a minimal period of 60 days. Thus aims at relieving the refund applicant, covering all genre of taxpayers at large, giving relief to manufacturer and exporters and enabling smooth flow of funds, if implemented properly.

*******

Accounting & Actuarial Fundamentals of Ind AS 19 - Employee Benefits

By CA Kartikey Kandoi

Actuarial Valuation of Employee Benefits:

As per Financial reporting framework entity has to recognise liability if the entity has a

present obligation arising from past events, the settlement of which is expected to result in

an outflow of resources embodying economic benefits from the entity.

As per AS 15/ Ind AS 19 company has to make provision in books for liability as at balance

sheet date by using Projected Unit Credit Method and considering valuation

assumptions viz Discount rate, salary escalation rate, employee turnover rate etc. as

prescribed in Accounting Standard.

Company has to disclose certain items for employee benefit in their notes to accounts, which are calculated &

provided by Actuary using methodology prescribed in AS 15/ Ind AS 19.

In some instances Insurer provide Closing liability (funding valuation) to company with a qualification that this is

not an AS 15 certificate. Company has to ensure that they give certain disclosures in notes to account based on

applicability of accounting standard. For Instance Post-Employment Benefit’s Disclosure in Notes to accounts is

mandatory for Non - SMC Company.

Valuation assumptions can be different for funding valuation based on company’s view. For example cautious

assumptions for funding, but Accounting Standard requires Best estimate assumptions for provisioning in books

of accounts.

As per Income tax rules Directors can be part of trust fund if shareholding less than 5% & whole time employee

of company, but for AS 15 provisioning liability for whole-time directors should be included in balance sheet.

So, ALL Companies (Listed/ unlisted, Private/ public company) have to ensure that Actuarial Valuation is done as

required by AS 15/ Ind AS 19.

Detailed information on applicability of Accounting Standards can be found in: Appendix II - Applicability of

Accounting Standards to Various Entities:

http://www.icaiknowledgegateway.org/littledms/folder1/appendix-ii-accounting-standar.pdf

The benefit may be funded or unfunded, both has its advantages and disadvantages (in terms of

opportunity cost),

Benefits of Funding Employee Benefits:

Provide Security to employees that benefit will be paid as they are insured and managed by professionals and

regulated by competent authority.

Provide Flexibility to employer to contribute towards accumulation of fund.

Company may not face liquidity problem when they have to pay huge amount to outgoing employees for

benefits to be paid.

As per Income Tax Act, superannuation benefits, gratuity, and other benefits are deductible from income when

benefits are paid or Contribution made in trust fund to the limits prescribed in Income tax rules 87-88 & 101-

104.

Provides Tax benefits on investment income of trust fund, so company should consider tax effective return for

considering funding decision.

Beneficial in case of employee transfers : When employee transfers form one organisation to another

may be as part of mergers & acquisition or transfer within group Company, accrued benefit liability as on date of

transfer should also be transferred to another company. In case scheme is funded, equitable transfer of assets also

needs to be made to another fund. In case if an employee transferred from one group company to another

company then the company should transfer their Gratuity, PF (in case of recognised provident fund) from one

trust fund to another, since continuation of service is pre requisite for getting tax free benefit and for that transfer

of fund is required.

Recording Liability Transfer In/Out. Effect is as follows:

For Example: - Mr. Ramesh who served 10 years in company X Ltd and transferred to Group Company, company Y

Ltd in current year with continuation of service. After 8 months service he Left organisation. Now Mr. Ramesh will

ask for Gratuity at time of Final settlement, since his total duration is 10 years 8 months, round to 11 years, he will be

eligible for 11 years Gratuity i.e. 11*15/26* last basic salary and this will be paid by Y limited at time of FNF. But

effectively out of this 11 years only 1 year belong to Y ltd, so ideally they should recover 10 years equivalent Gratuity

from X ltd. Now whether to recover or Not, is company’s call and it depends on Materiality of transaction amount. In

other company generally company provide us Amount they are recording of Liability Transfer In/ Out for Company X

to Y ltd.

Suggestion: - Entry should be recorded to ensure true and fair view of Accounts, otherwise results of BOTH

companies deviate to the extent amount is Material.

New Accounting Standard for Employee benefits and its effect

Effect of Ind AS on Actuarial Valuation requirement:

When entity prepares its first Ind AS financial statements (as at 31.03.2018), it has to comply with Ind AS

101, and need to provide comparative figures for 31.03.2017 which will need to be prepared by preparing

opening Ind AS balance sheet at 01.04.2016 and applying effect of Ind ASs and arrive at figures at

31.03.2017 to be used as comparatives for financial statements of 31.03.2018.

So, Actuarial Valuation report as at 31.03.2017 will need to be provided by both basis, existing AS 15 & Ind

AS 19.

As per roadmap, Companies to which Ind AS is not applicable should have to follow Accounting Standards

specified in Annexure to the Companies (Accounting Standards) Rules, 2006. So, actuaries will have to

provide reports to both set of companies, to whom different rules apply.

Significant changes in Ind AS 19 compared to AS 15:

Discount Rate should be used with reference to market yields at the end of reporting period on

Government bonds. However, Subsidiaries, associates, joint ventures and branches domiciled outside

India market yields on high quality corporate bonds, but if no deep market than use Government bonds.

Expected return on assets will be same as Discount rate used for valuation of obligation and Net interest

cost to be calculated on Net Liabilities/ Assets.

For Post-retirement benefit plans (example Gratuity, Pension & PRMB) Actuarial Gain/ Loss will be

taken to Other Comprehensive Income and not to be reclassified into Profit & Loss in subsequent

period whereas AS 15 required it to be recognized in Profit & Loss.

For Other long term benefits (example compensated absences & long service award) Actuarial gain/

loss continues to be recognized in Profit & Loss. Hence, recognition criteria remain same in Ind AS 19

as was in AS 15.

Past service cost to be recognized in Profit & Loss in year of occurrence. Ind AS 19 doesn’t

differentiate between vested & non-vested past service cost recognition.

Actuarial Gain or Loss due to change in assumption needs to be shown separately for due to change in

Demographic assumption & due to change in financial assumption.

As per AS 15 employee includes whole-time directors and other management personnel; whereas as

per Ind AS 19 employees include directors and other management personnel.

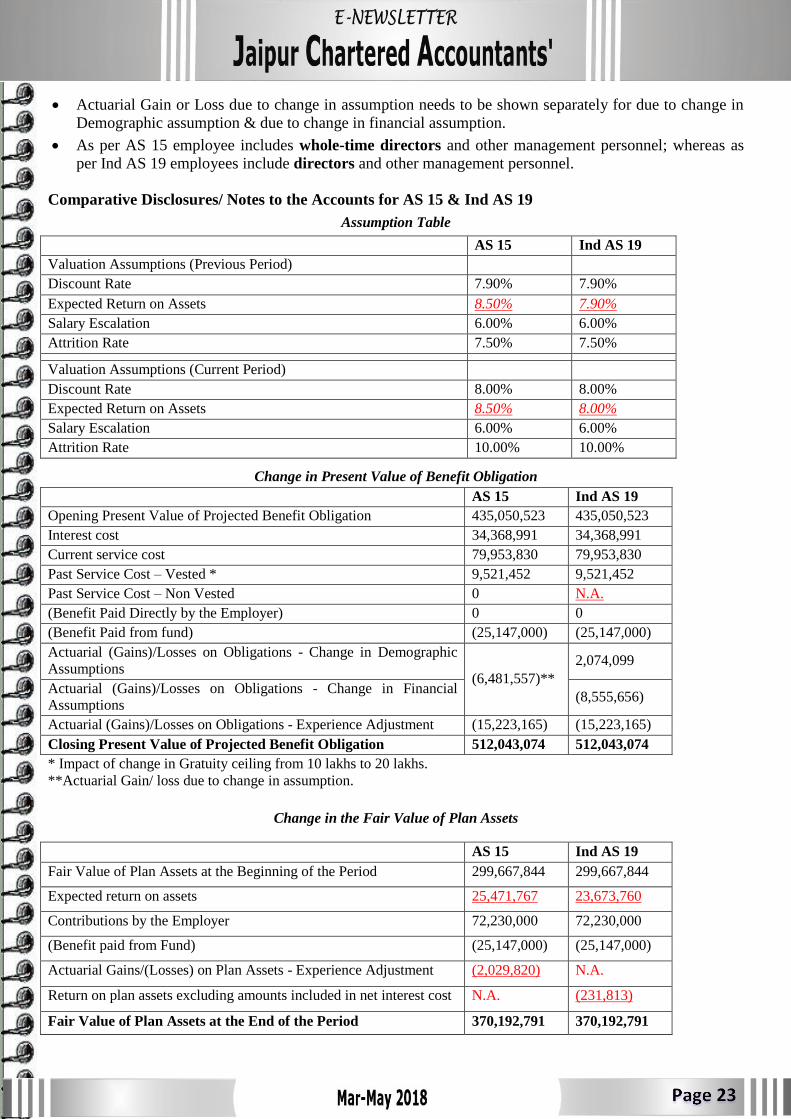

Comparative Disclosures/ Notes to the Accounts for AS 15 & Ind AS 19

Assumption Table

AS 15 Ind AS 19

Valuation Assumptions (Previous Period)

Discount Rate 7.90% 7.90%

Expected Return on Assets 8.50% 7.90%

Salary Escalation 6.00% 6.00%

Attrition Rate 7.50% 7.50%

Valuation Assumptions (Current Period)

Discount Rate 8.00% 8.00%

Expected Return on Assets 8.50% 8.00%

Salary Escalation 6.00% 6.00%

Attrition Rate 10.00% 10.00%

Change in Present Value of Benefit Obligation

AS 15 Ind AS 19

Opening Present Value of Projected Benefit Obligation 435,050,523 435,050,523

Interest cost 34,368,991 34,368,991

Current service cost 79,953,830 79,953,830

Past Service Cost – Vested * 9,521,452 9,521,452

Past Service Cost – Non Vested 0 N.A.

(Benefit Paid Directly by the Employer) 0 0

(Benefit Paid from fund) (25,147,000) (25,147,000)

Actuarial (Gains)/Losses on Obligations - Change in Demographic

Assumptions (6,481,557)**

2,074,099

Actuarial (Gains)/Losses on Obligations - Change in Financial Assumptions

(8,555,656)

Actuarial (Gains)/Losses on Obligations - Experience Adjustment (15,223,165) (15,223,165)

Closing Present Value of Projected Benefit Obligation 512,043,074 512,043,074

* Impact of change in Gratuity ceiling from 10 lakhs to 20 lakhs.

**Actuarial Gain/ loss due to change in assumption.

Change in the Fair Value of Plan Assets

AS 15 Ind AS 19

Fair Value of Plan Assets at the Beginning of the Period 299,667,844 299,667,844

Expected return on assets 25,471,767 23,673,760

Contributions by the Employer 72,230,000 72,230,000

(Benefit paid from Fund) (25,147,000) (25,147,000)

Actuarial Gains/(Losses) on Plan Assets - Experience Adjustment (2,029,820) N.A.

Return on plan assets excluding amounts included in net interest cost N.A. (231,813)

Fair Value of Plan Assets at the End of the Period 370,192,791 370,192,791

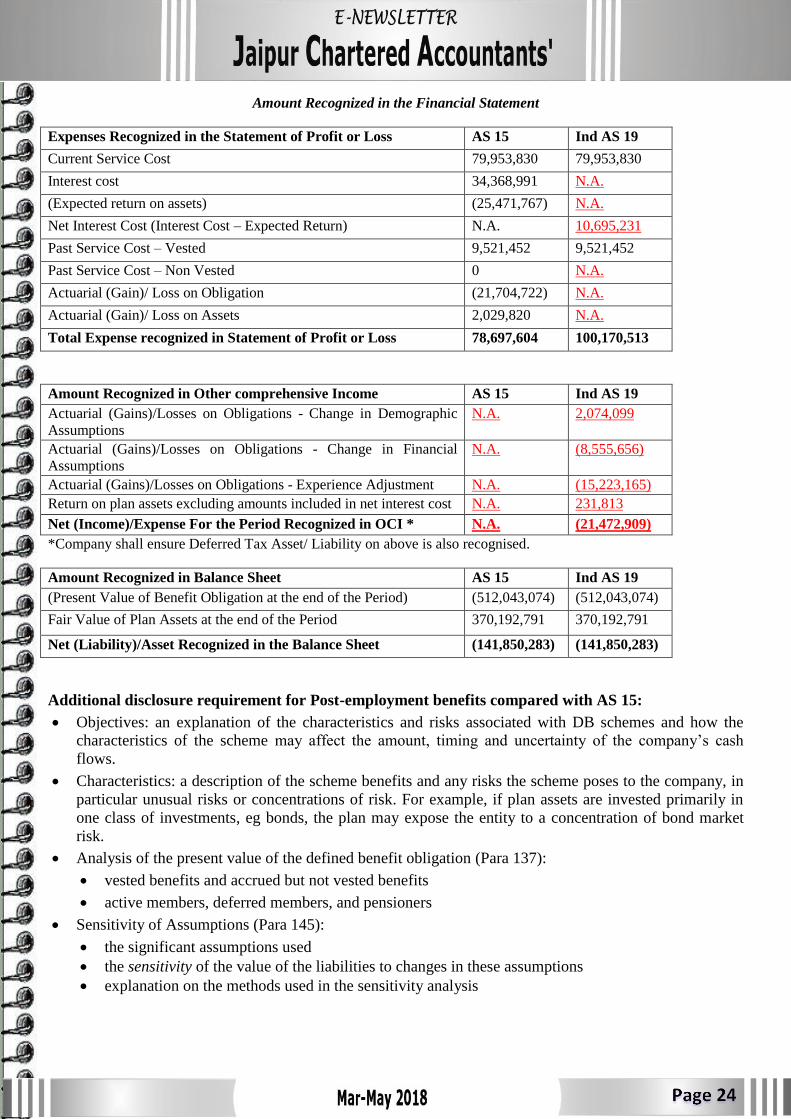

Amount Recognized in the Financial Statement

Expenses Recognized in the Statement of Profit or Loss AS 15 Ind AS 19

Current Service Cost 79,953,830 79,953,830

Interest cost 34,368,991 N.A.

(Expected return on assets) (25,471,767) N.A.

Net Interest Cost (Interest Cost – Expected Return) N.A. 10,695,231

Past Service Cost – Vested 9,521,452 9,521,452

Past Service Cost – Non Vested 0 N.A.

Actuarial (Gain)/ Loss on Obligation (21,704,722) N.A.

Actuarial (Gain)/ Loss on Assets 2,029,820 N.A.

Total Expense recognized in Statement of Profit or Loss 78,697,604 100,170,513

Amount Recognized in Other comprehensive Income AS 15 Ind AS 19

Actuarial (Gains)/Losses on Obligations - Change in Demographic

Assumptions

N.A. 2,074,099

Actuarial (Gains)/Losses on Obligations - Change in Financial

Assumptions

N.A. (8,555,656)

Actuarial (Gains)/Losses on Obligations - Experience Adjustment N.A. (15,223,165)

Return on plan assets excluding amounts included in net interest cost N.A. 231,813

Net (Income)/Expense For the Period Recognized in OCI * N.A. (21,472,909)

*Company shall ensure Deferred Tax Asset/ Liability on above is also recognised.

Amount Recognized in Balance Sheet AS 15 Ind AS 19

(Present Value of Benefit Obligation at the end of the Period) (512,043,074) (512,043,074)

Fair Value of Plan Assets at the end of the Period 370,192,791 370,192,791

Net (Liability)/Asset Recognized in the Balance Sheet (141,850,283) (141,850,283)

Additional disclosure requirement for Post-employment benefits compared with AS 15:

Objectives: an explanation of the characteristics and risks associated with DB schemes and how the

characteristics of the scheme may affect the amount, timing and uncertainty of the company’s cash

flows.

Characteristics: a description of the scheme benefits and any risks the scheme poses to the company, in

particular unusual risks or concentrations of risk. For example, if plan assets are invested primarily in

one class of investments, eg bonds, the plan may expose the entity to a concentration of bond market

risk.

Analysis of the present value of the defined benefit obligation (Para 137):

vested benefits and accrued but not vested benefits

active members, deferred members, and pensioners

Sensitivity of Assumptions (Para 145):

the significant assumptions used

the sensitivity of the value of the liabilities to changes in these assumptions

explanation on the methods used in the sensitivity analysis

An entity shall disclose a description of any asset-liability matching strategies used by the plan or the

entity, including the use of annuities and other techniques, to manage risk (Para 146).

Effect on Future Cash flows (Para 147):

expected employer contributions over the coming year

description of the funding arrangements

weighted average duration of the obligation

maturity profile of the defined benefit obligation (undiscounted expected cashflow for future years)

Five-year history of asset value, liabilities, surplus/deficit and experience gains and losses is not

required to be disclosed.

Leave Valuation under Ind AS 19:

For Other long term benefit para 153 to 158 of Ind AS 19 are relevant. Leave benefit is classified as

Other-long term benefit.

As per Para 156, Actuarial Gain/ loss is charged to P&L and no requirement of OCI unlike post -

employment benefit obligation.

As per Para 158 No specific Disclosure is required for Other-long term benefits.

Whereas in case of Post-employment benefit para 135 requires detailed disclosure that’s why company

have to make detailed disclosure in Notes to Accounts for benefit like Gratuity, Pension plans.

Audit Check Points – Actuarial Valuation

Understanding benefit scheme of company.

Whether Gratuity is paid in line with Gratuity Act or company pay without restriction.

Employee Data - appropriate, complete and cut off.

Inclusion of Directors, trainee’s data.

Include all employees for Gratuity provision even though service less than 5 years.

Ensure leave availment is valued on Gross salary and encashment on eligible salary which can be basic salary (as

per company policy).

Appropriate divisor is used in calculation of Gratuity (generally 26) and Leave (as per company policy)

respectively.

Treatment for due but not paid liability.

Treatment for liability and assets transfer In/ Out.

Validating appropriateness of valuation assumptions.

Check for average past service, discontinuance/ accrued benefit liability.

Check results of actuarial gain/ loss for year and analyse for valid reasons.

Compare charge on Profit & Loss and OCI for current year v/s previous year.

Check results of balance sheet, Profit and Loss, OCI amount match in Actuary Report, accounting books and

financials including notes to accounts.

SA 620 Using the Work of an Auditor’s Expert.

Independence confirmation from Actuary.

Conclusion:

IFRS is being used by most countries to account for Employee Benefits, this Standard has been issued with the idea

that there will be similarities in accounting with other countries. In my opinion there is lot to be done by Accounting

and Actuarial bodies, to create awareness so that the standard could be implemented smoothly.

Important Judgements: Source: Taxmann By CA Sachin Kumar Jain

GST Important JudgementsUpdates:-

Important Judgement:

1. Smt. Anuradha Agarwal, 103, Rajendra Marg, Bhilwara- (Raj)- 311001 Versus Income Tax Officer, Ward-3, Income Tax

Office, Bilwara (Raj) –

Date of Pronouncement: 25.05.2018

Merely because the loan was sanctioned for housing purpose, it cannot be said that the Assessee cannot use it for

advancing loans to others for earning interest. It may amount to the violation of terms and conditions of the agreement

so entered with the bank while sanctioning of the loan, but there is no contravention under the Income Tax Act for

advancing such funds for earning interest income.

Orders of the ld. CIT(A) Ajmer dated 05/10/2017 for the A.Y. 2013-14 in the matter of order u/s 143(3) of the Income-

tax Act, 1961 [hereinafter referred to as ‘the Act’, for short]. In all these appeals, a common issue has been taken,

therefore, all the appeals are being heard together and the Bench decided to dispose of all these appeals by a

consolidated order. At the time of hearing, none appeared on behalf of the Assessee. Even though, the Assessee filed

adjournment petition but nobody was there to prosecute the adjournment petition. Accordingly, the Bench decided to

dispose of the appeals after hearing the ld Departmental Representative.

In all these appeals, the common issue involved is against confirming the disallowance on interest payment claimed U/s

57 of the Act.

2. Shri Kallepu Sharath Chander Vs. ACIT, Hyderabad

Date of pronouncement: 30.05.2018

Where the land is shown in revenue record as agricultural land, it is immaterial whether any agricultural income is

shown in the return or not, the gains from sale are exempt from taxation. Therefore, the reason given by the AO for not

accepting the assessee’s contention is not sustainable and that the land sold by the Assessee being agricultural land, no

capital gain is taxable on the profit from sale of such land.

3. M/s A Daga Royal Arts Vs. ITO, Jaipur

Date of Pronouncement: 15.05.2018

Rule 6DD is not exhaustive. The fact that the transaction does not fall with Rule 6DD does not mean that a disallowance

has to be per force made. Further, the second proviso to section 40A(3) refers to “the nature and extent of banking

facility, consideration of business expediency and other relevant factors” which means that the object of the legislature

is not to make disallowance of cash payments which have to be compulsory made by the assessee on account of

business expediency.

4. Abicor and BinzelTechnoweld Pvt. Ltd. Versus The Union of India Lack of access to online profile on the Goods and

Service Tax Network - petitioner unable to generate e-way bills - Held that - The special sessions of Parliament or special

or extraordinary meetings of Council would mean nothing to the assessees unless they obtain easy access to the

website and portals. The regime is not tax friendly.

Abicor hearing update 6.03.2018 Bombay High Court

1) Court has taken minutes of meeting between GSTPAM and Commissioners on record and directed the Council and

Commissioners to resolve the problems pointed out by GSTPAM. This meeting was held as per directions of the Court

on27.02.2018.

2) Counsel for Petitioner pointed out that the Economic Survey of India 2017-18 shows 98 Lakhs registrations till

December 2017. However Government Affidavit shows only 38 lakh ppl have filed GSTR 1. Govt Affidavit further shows

that composition taxpayers are only 17.41 lakhs as on date. This means that around 50 lakh registered persons have not

filed the returns. It cannot be said that 50 lakh taxpayers are deliberately defaulting in filing of returns. Only reasonable

inference is that the system is preventing large swathes of taxpayers from compiling with the statute.

3) Similarly Counsel for Petitioners pointed out that Government Affidavit shows 64 lakh taxpayers are migrated

registrants as on date. But TRAN-01 was filed only by 9 lakh taxpayers. Even adjusting for composition taxpayers this

means that only 15% of the total migrated taxpayers have filed FORM TRAN-01. It cannot be said that all of the other

85% migrated taxpayers were ineligible for TRAN-01 or deliberately gave up their rights. It is clear that many ppl have

been unable to file TRAN-01 due to system errors.

4) Court has made adverse observations during hearing on the blockage of returns due to non-payment of late fees and

enquired with the Additional Solicitor General whether there is a provision for such blockage.

5) Till the issue of validity of blockage of returns for nonpayment of late fees is decided, as an interim measure

Petitioner was allowed to file returns for past many months which were stuck due to nonpayment of late fees.

Undertaking taken from Government to refund late fees within 7 days or auto direct the late fees to "tax" head within 7

days from date of payment.

6) Court has asked the Council and the Commissioners to streamline the system so that it works in accordance with the

provisions of law and not outside it.

7) Court has set a deadline of 24 April 2017 to resolve various issues pointed out by GSTPAM. Failure to do so would