Embed Size (px)

Citation preview

I 1 I

Press Conference March 11th, 2015 Results 2014

Antoine Kohler (Chairman), Patric Schoch (CFO)

Press Conference 11.03.2015

I 2 I

Disclaimer

The information in this presentation does not constitute an offer or invitation and may not be construed as a recommendation by us to purchase, hold or sell shares of Cicor Technologies Ltd. This information or any copy thereof may not be sent or taken to or distributed in any jurisdiction in which such transmission or distribution is unlawful. This document may contain certain ‘forward-looking’ statements. By their nature, forward-looking statements involve risk and uncertainty because they relate to future events and circumstances. Actual outcomes and results may differ materially from any outcomes or results expressed or implied by such forward-looking statements.

Press Conference 11.03.2015

I 3 I

Agenda Press conference

Profile Achievements 2014 “Innovation for Success” Financials 2014 Outlook Q & A

Press Conference 11.03.2015

I 4 I

Profile Antoine Kohler

Press Conference 11.03.2015

I 5 I

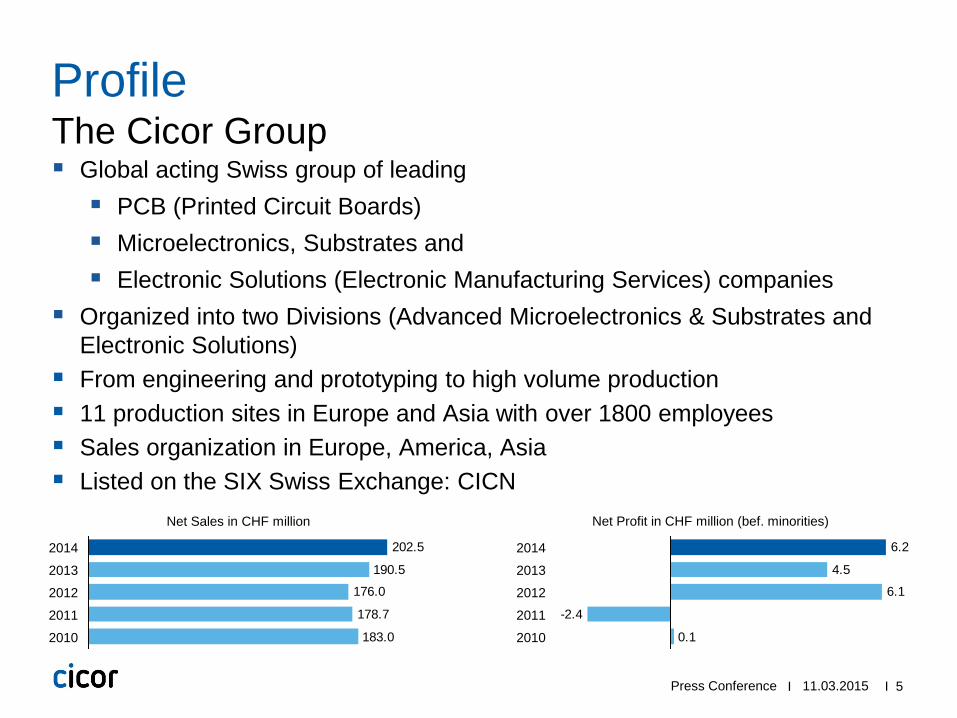

The Cicor Group Profile

Global acting Swiss group of leading PCB (Printed Circuit Boards) Microelectronics, Substrates and Electronic Solutions (Electronic Manufacturing Services) companies

Organized into two Divisions (Advanced Microelectronics & Substrates and Electronic Solutions)

From engineering and prototyping to high volume production 11 production sites in Europe and Asia with over 1800 employees Sales organization in Europe, America, Asia Listed on the SIX Swiss Exchange: CICN

183.0

178.7

176.0

190.5

202.5

2011

2012

2010

2013

2014

Net Sales in CHF million

0.1

-2.4

6.1

4.5

6.2

2010

2011

2012

2013

2014

Net Profit in CHF million (bef. minorities)

Press Conference 11.03.2015

I 6 I

Extract only Customer references

11.03.2015 Cicor respects customer confidentiality

Press Conference

I 7 I

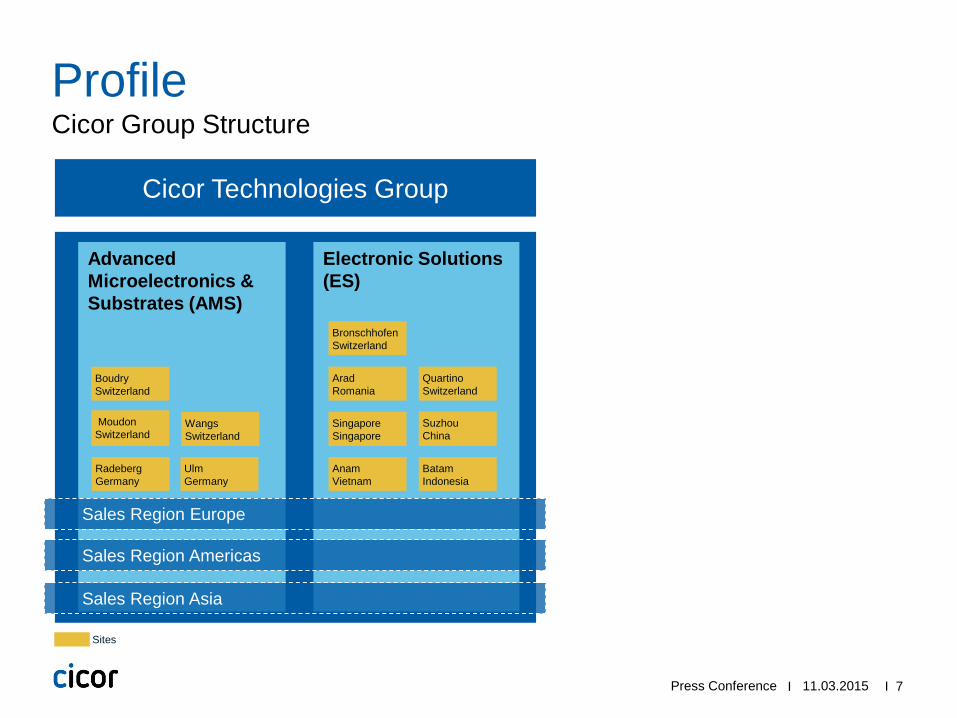

Cicor Group Structure Profile

Cicor Technologies Group

Electronic Solutions (ES)

Advanced Microelectronics & Substrates (AMS)

Boudry Switzerland

Sites

Moudon Switzerland

Wangs Switzerland

Ulm Germany

Radeberg Germany

Bronschhofen Switzerland

Arad Romania

Quartino Switzerland

Singapore Singapore

Anam Vietnam

Batam Indonesia

Suzhou China

Sales Region Europe

Sales Region Americas

Press Conference 11.03.2015

Sales Region Asia

I 8 I

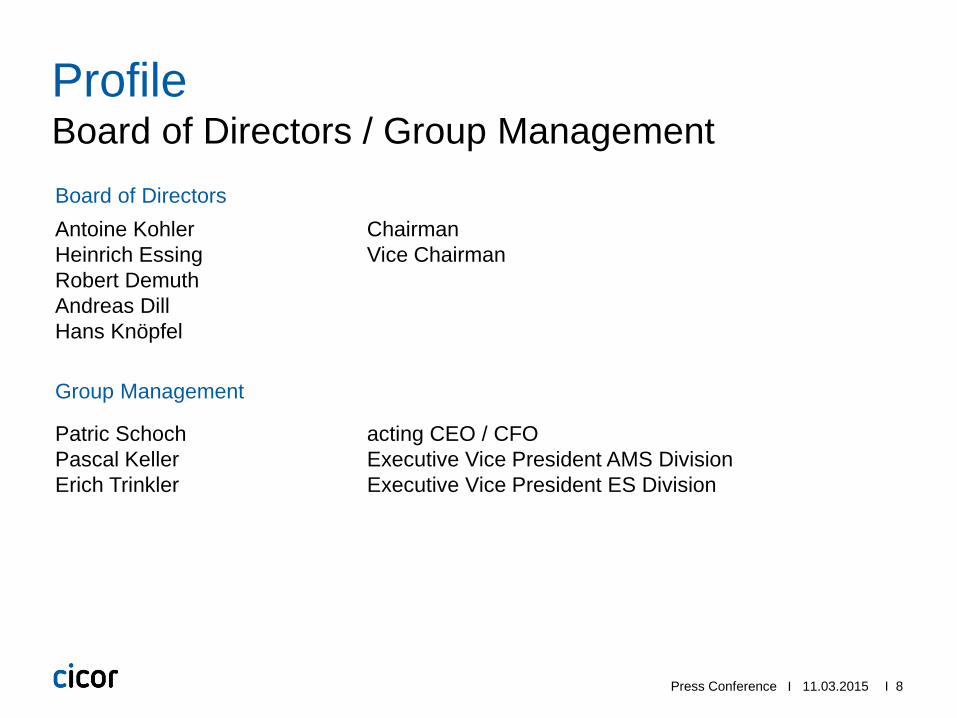

Board of Directors / Group Management Profile

Press Conference 11.03.2015

Board of Directors Antoine Kohler Chairman Heinrich Essing Vice Chairman Robert Demuth Andreas Dill Hans Knöpfel Group Management

Patric Schoch acting CEO / CFO Pascal Keller Executive Vice President AMS Division Erich Trinkler Executive Vice President ES Division

I 9 I

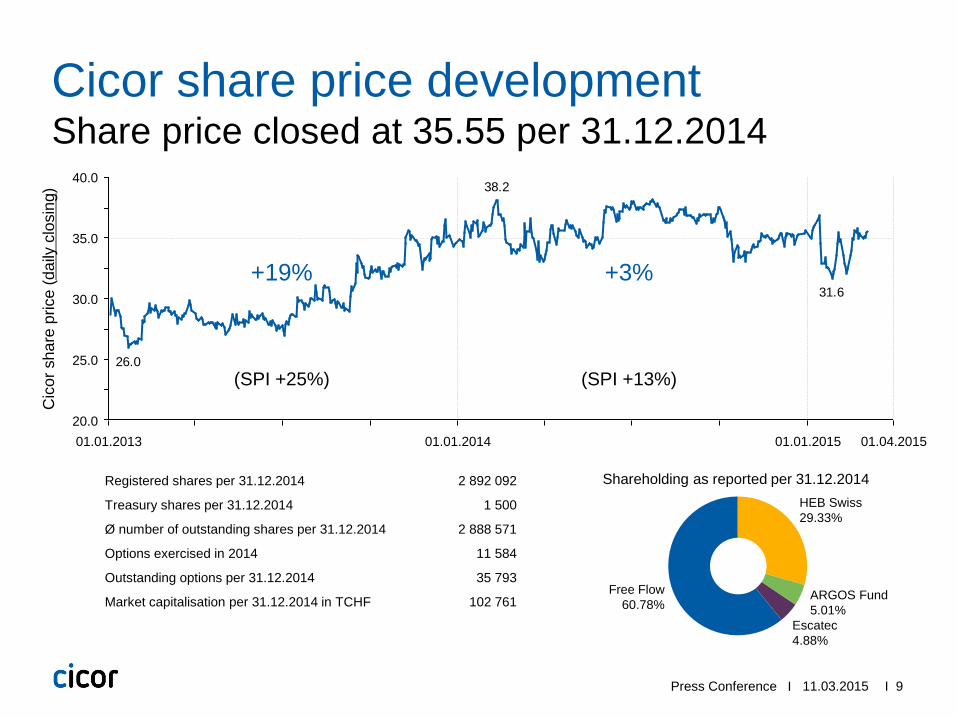

31.6

38.2

26.0

20.0 01.01.2014 01.01.2013

40.0

35.0

30.0

01.01.2015

25.0

01.04.2015

Cic

or s

hare

pric

e (d

aily

clo

sing

)

+3%

(SPI +13%)

Share price closed at 35.55 per 31.12.2014 Cicor share price development

Press Conference 11.03.2015

+19%

(SPI +25%)

Registered shares per 31.12.2014 2 892 092

Treasury shares per 31.12.2014 1 500

Ø number of outstanding shares per 31.12.2014 2 888 571

Options exercised in 2014 11 584

Outstanding options per 31.12.2014 35 793

Market capitalisation per 31.12.2014 in TCHF 102 761 Free Flow

60.78% ARGOS Fund 5.01%

HEB Swiss 29.33%

Escatec 4.88%

Shareholding as reported per 31.12.2014

I 10 I

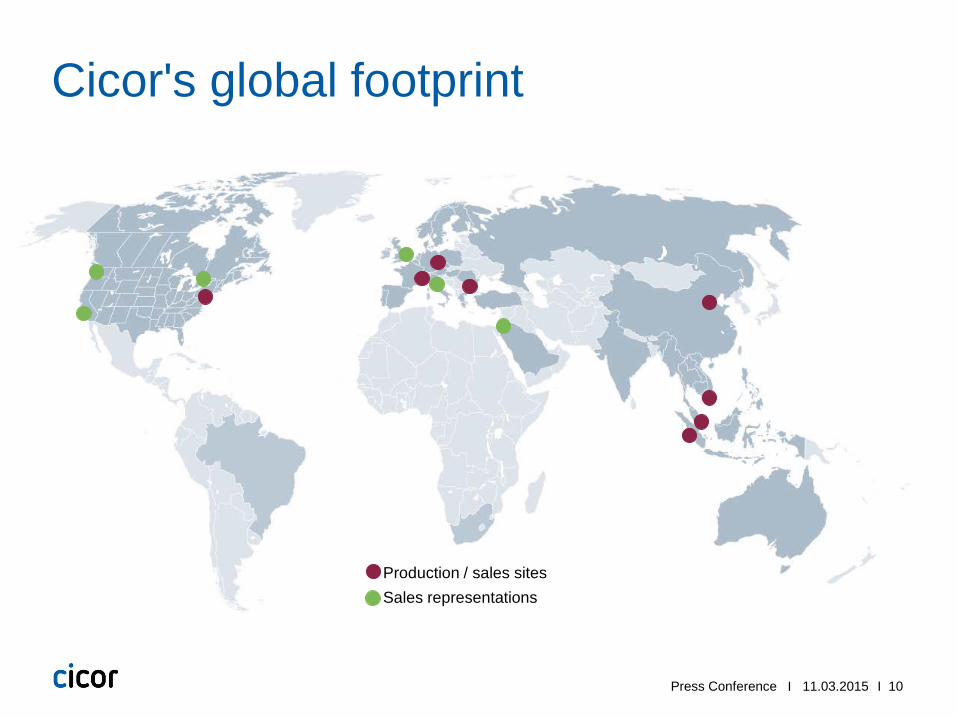

Cicor's global footprint

Global and local presence

Production / sales sites Sales representations

Press Conference 11.03.2015

I 11 I

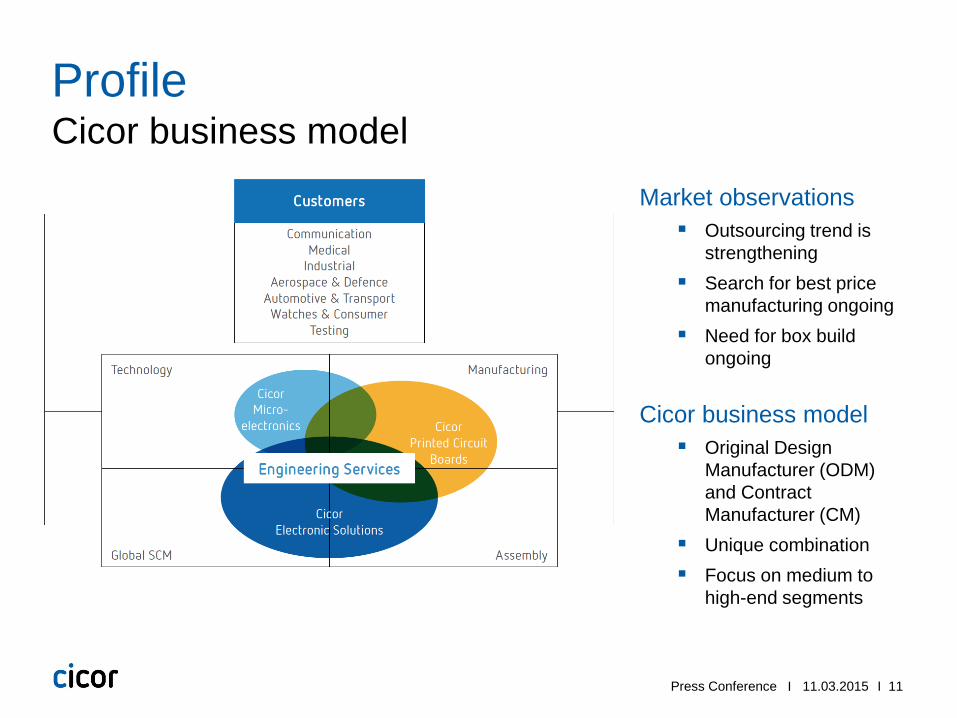

Cicor business model Profile

Market observations Outsourcing trend is

strengthening Search for best price

manufacturing ongoing Need for box build

ongoing

Cicor business model Original Design

Manufacturer (ODM) and Contract Manufacturer (CM)

Unique combination Focus on medium to

high-end segments

Press Conference 11.03.2015

I 12 I

Diversified customer portfolio Markets

Medical

Watches & Consumer

Industrial

Aerospace & Defence

Communication

Automotive & Transport

Press Conference 11.03.2015

I 13 I

Achievements 2014 Patric Schoch

Press Conference 11.03.2015

I 14 I

Highlights Achievements 2014 (1/2)

Further profitable growth in 2014 Net sales grew above the overall estimated market

growth. Continued growth in core segments medical,

industrial and automotive & transport. Higher profitability and good net profit achieved. Excellent free cash flow generated.

Expansion of technological leadership continued Significant investments into renewal and

modernization of production facilities in all regions, but below the high spending rate of 2013 and 2012.

New financing of CHF 65 million secured New financing agreement assures the Group’s long-

term financial flexibility and future growth.

Press Conference 11.03.2015

I 15 I

Highlights Achievements 2014 (2/2)

Strong balance sheet position The equity ratio as at December 31st, 2014 was

54.1% (2013: 55.6%). Net debt was reduced significantly to CHF 21.2

million. Proposed 20% increased pay-out of CHF 0.36 per

share from capital contribution reserves.

Strong management team in place Dr. Jürg Dübendorfer will join per 1 June 2015 as

the new Group CEO, completing the group management team.

Patric Schoch will resume full-time financial leadership of the Group as CFO.

Press Conference 11.03.2015

I 16 I

Return to growth in second-half of the year Advanced Microelectronis & Substrates (AMS)

Press Conference 11.03.2015

Varying market segment performance in 2014 lead to an overall reduction in sales.

The medical and industrial segments performed better, aerospace, defence and nuclear energy segments as well as watches & consumer remained low.

Rising demand in HY2 enabled the Division to outperform the first six months sales by 4.4% in the second half.

Despite the lower sales for the whole 2014, the EBIT remained stable and EBITDA improved vs 2013.

Growth in industrial applications is expected to intensify in 2015, opportunities exist in industrial automation applications and the Internet of things (IoT) or machine-to-machine communication.

The implemented strengthening of the sales organization in the second half of 2014 is expected to bear fruit starting 2015.

I 17 I

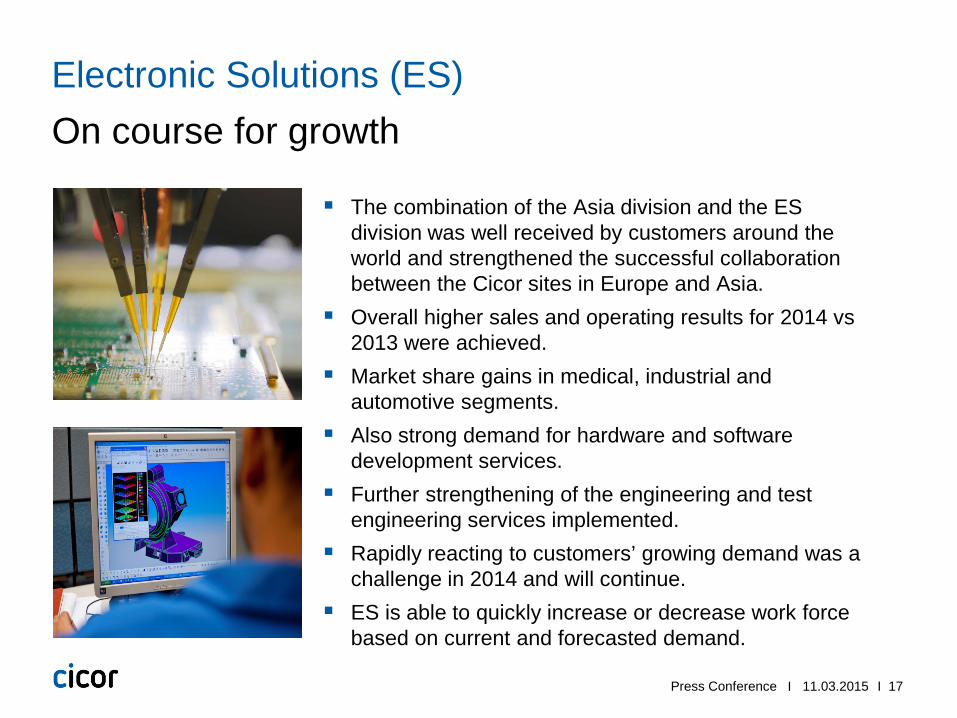

On course for growth Electronic Solutions (ES)

The combination of the Asia division and the ES division was well received by customers around the world and strengthened the successful collaboration between the Cicor sites in Europe and Asia.

Overall higher sales and operating results for 2014 vs 2013 were achieved.

Market share gains in medical, industrial and automotive segments.

Also strong demand for hardware and software development services.

Further strengthening of the engineering and test engineering services implemented.

Rapidly reacting to customers’ growing demand was a challenge in 2014 and will continue.

ES is able to quickly increase or decrease work force based on current and forecasted demand.

Press Conference 11.03.2015

I 18 I

Innovation for success Patric Schoch

Press Conference 11.03.2015

I 19 I

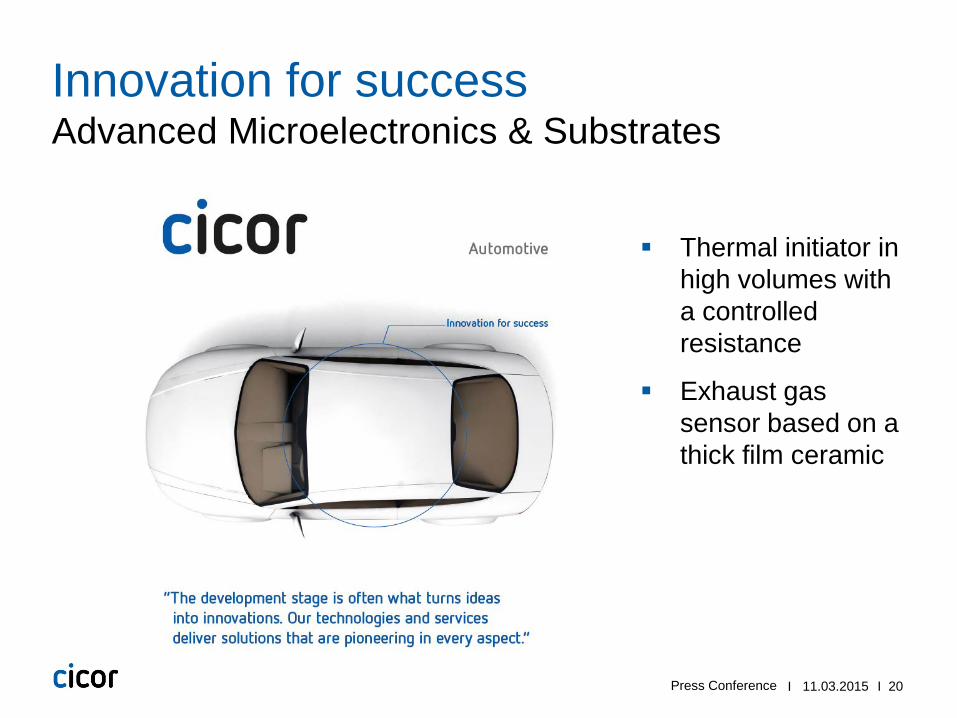

Advanced Microelectronics & Substrates Innovation for success

Thin-film-based microfluidic chip with microelectrodes for portable cell analysis

Press Conference 11.03.2015

I 20 I

Advanced Microelectronics & Substrates Innovation for success

Thermal initiator in high volumes with a controlled resistance

Exhaust gas sensor based on a thick film ceramic

Press Conference 11.03.2015

I 21 I

Innovation Insights Innovation for success

Successful first Cicor symposium

Around 70 participants from different industries

Very good press coverage and follow-up

Press Conference 11.03.2015

I 22 I

Financials 2014 Patric Schoch

Press Conference 11.03.2015

I 23 I

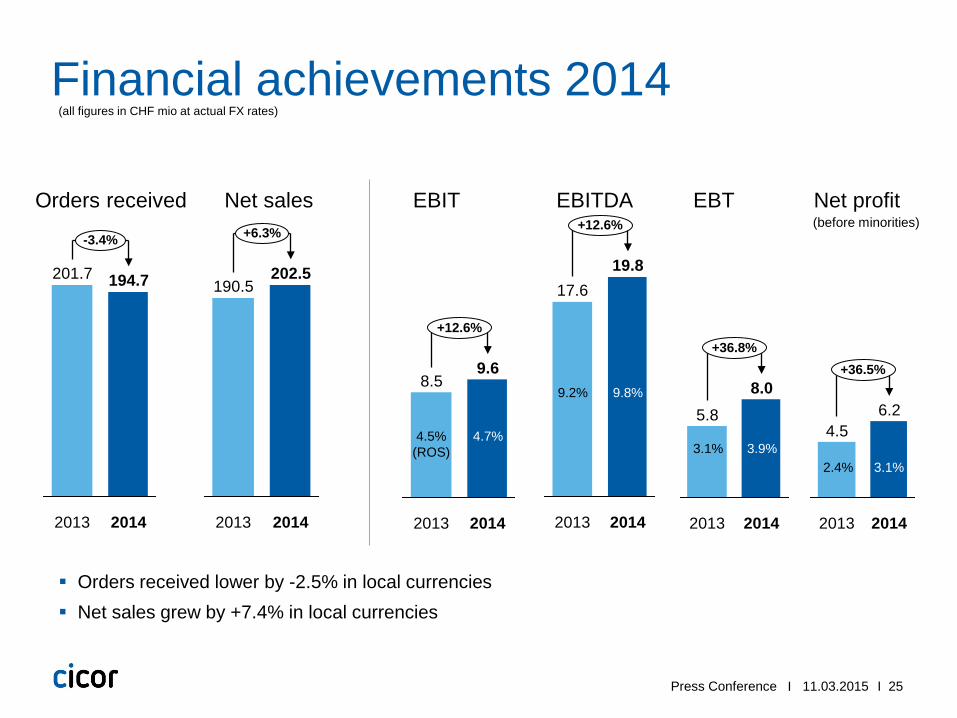

Earning power grows disproportionately to sales Financial Summary 2014

Further profitable sales growth achieved Net sales in Swiss francs rose to CHF 202 mio, a growth of 6.3% vs 2013 Simpler and more efficient organization was successfully implemented EBIT margin of 4.7% for 2014 (2013: 4.5%), EBITDA margin of 9.8% (2013:

9.2%)

Increase of EBT and net profit EBT grew by 37% to CHF 8.0 mio (2013: CHF 5.8 mio) Net profit grew in 2014 by 36% to CHF 6.2 mio (2013: CHF 4.5 mio) Earnings per share of CHF 2.11; proposed 20% increased pay-out of CHF

0.36 per share (2012 and 2013: CHF 0.30 per share)

Net working capital (NWC), free cash flow and net debt NWC kept at 2013 level, despite increase in business volume Excellent free cash flow of CHF 8.0 mio Net debt reduced from CHF 28.2 mio in 2013 to CHF 21.2 mio in 2014

Press Conference 11.03.2015

I 24 I

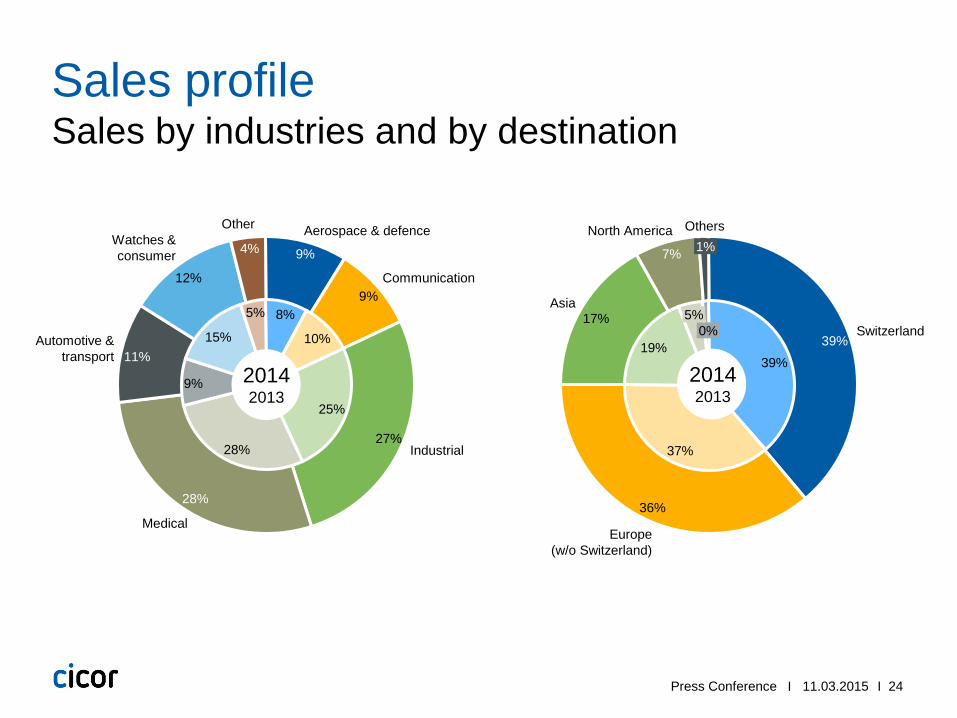

Aerospace & defence

9%

27%

9% Communication

Industrial

11%

Medical

28%

12%

Automotive & transport

Watches & consumer 4%

Other

15%

9%

28%

25%

10%

8% 5% Switzerland

39%

17%

36%

Europe (w/o Switzerland)

Asia

1% North America

7%

Others

0% 5%

19%

37%

39%

Sales by industries and by destination Sales profile

Press Conference 11.03.2015

2014 2013

2014 2013

I 25 I

+36.8%

2014

8.0

2013

5.8

Financial achievements 2014

Orders received Net sales EBIT EBITDA Net profit

-3.4%

2014

194.7

2013

201.7

+6.3%

2014

202.5

2013

190.5

+12.6%

2014

9.6

2013

8.5

+12.6%

2014

19.8

2013

17.6

6.2

2014

+36.5%

2013

4.5

9.8% 9.2%

4.5% (ROS)

4.7%

3.1% 2.4%

(before minorities) EBT

3.9% 3.1%

(all figures in CHF mio at actual FX rates)

Orders received lower by -2.5% in local currencies Net sales grew by +7.4% in local currencies

Press Conference 11.03.2015

I 26 I

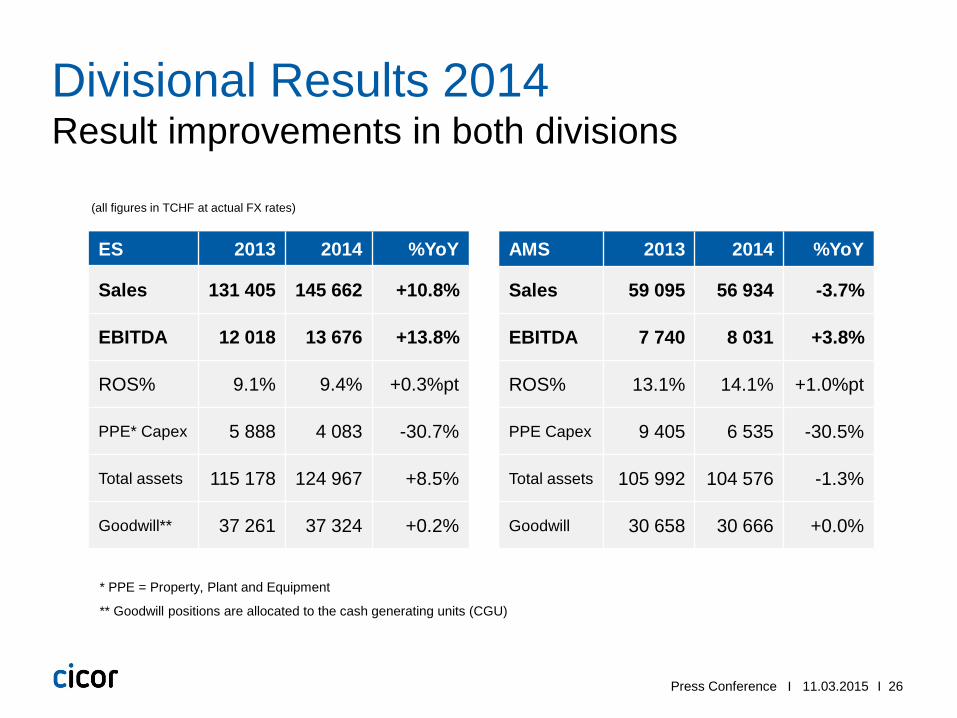

Divisional Results 2014 Result improvements in both divisions

ES 2013 2014 %YoY

Sales 131 405 145 662 +10.8%

EBITDA 12 018 13 676 +13.8%

ROS% 9.1% 9.4% +0.3%pt

PPE* Capex 5 888 4 083 -30.7%

Total assets 115 178 124 967 +8.5%

Goodwill** 37 261 37 324 +0.2%

AMS 2013 2014 %YoY

Sales 59 095 56 934 -3.7%

EBITDA 7 740 8 031 +3.8%

ROS% 13.1% 14.1% +1.0%pt

PPE Capex 9 405 6 535 -30.5%

Total assets 105 992 104 576 -1.3%

Goodwill 30 658 30 666 +0.0%

(all figures in TCHF at actual FX rates)

Press Conference 11.03.2015

* PPE = Property, Plant and Equipment

** Goodwill positions are allocated to the cash generating units (CGU)

I 27 I

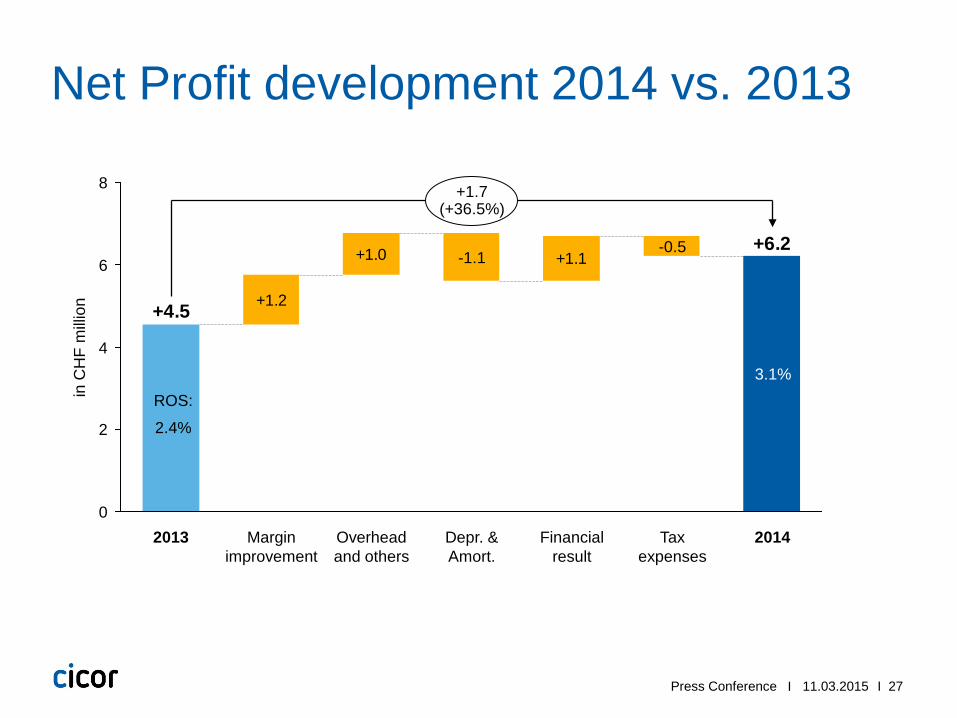

Net Profit development 2014 vs. 2013

+1.2

+1.0 +1.1+6.2

+4.5

0

2

4

6

8

in C

HF

milli

on

-1.1

+1.7 (+36.5%)

2014 Tax expenses

-0.5

Financial result

Depr. & Amort.

Overhead and others

Margin improvement

2013

3.1% ROS:

2.4%

Press Conference 11.03.2015

I 28 I

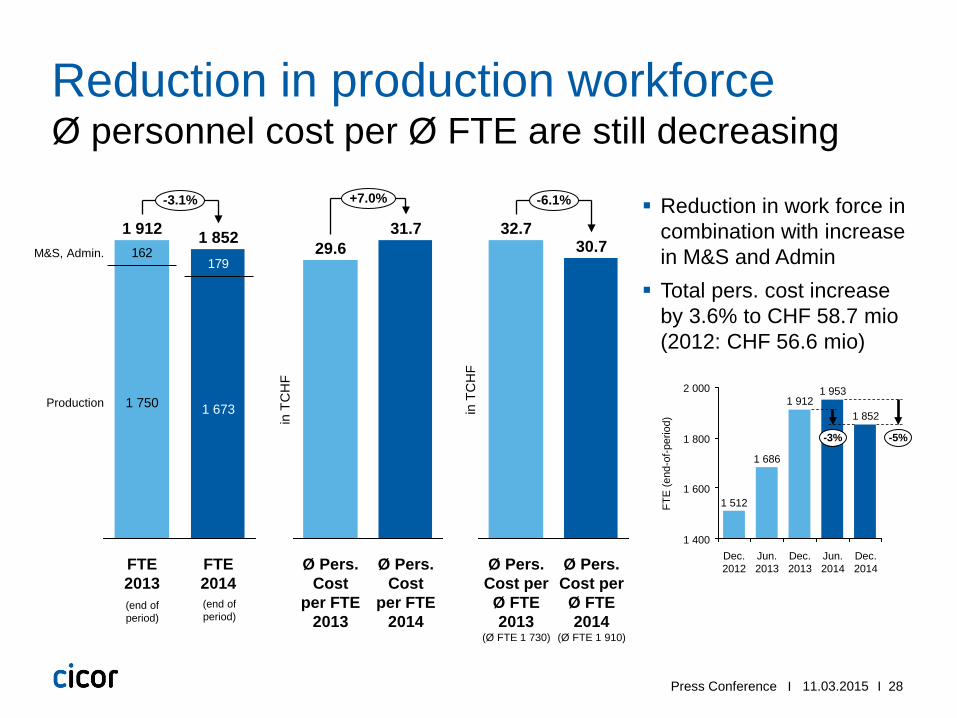

Ø Pers. Cost per

Ø FTE 2014

(Ø FTE 1 910)

-6.1%

in T

CH

F

30.7

Ø Pers. Cost per

Ø FTE 2013

(Ø FTE 1 730)

32.7

Ø personnel cost per Ø FTE are still decreasing Reduction in production workforce

179162

-3.1%

1 673

M&S, Admin.

FTE 2013

FTE 2014

Production

1 852 1 912

1 750

Reduction in work force in combination with increase in M&S and Admin Total pers. cost increase

by 3.6% to CHF 58.7 mio (2012: CHF 56.6 mio)

(end of period)

11.03.2015 Press Conference

(end of period)

2 000

1 400

1 600

1 800

1 686

Dec. 2012

1 512 FTE

(end

-of-p

erio

d)

1 953

Dec. 2014

1 852

Dec. 2013

1 912

-5%

Jun. 2013

Jun. 2014

-3%

Ø Pers. Cost

per FTE 2013

29.6

Ø Pers. Cost

per FTE 2014

+7.0%

31.7

in T

CH

F

I 29 I

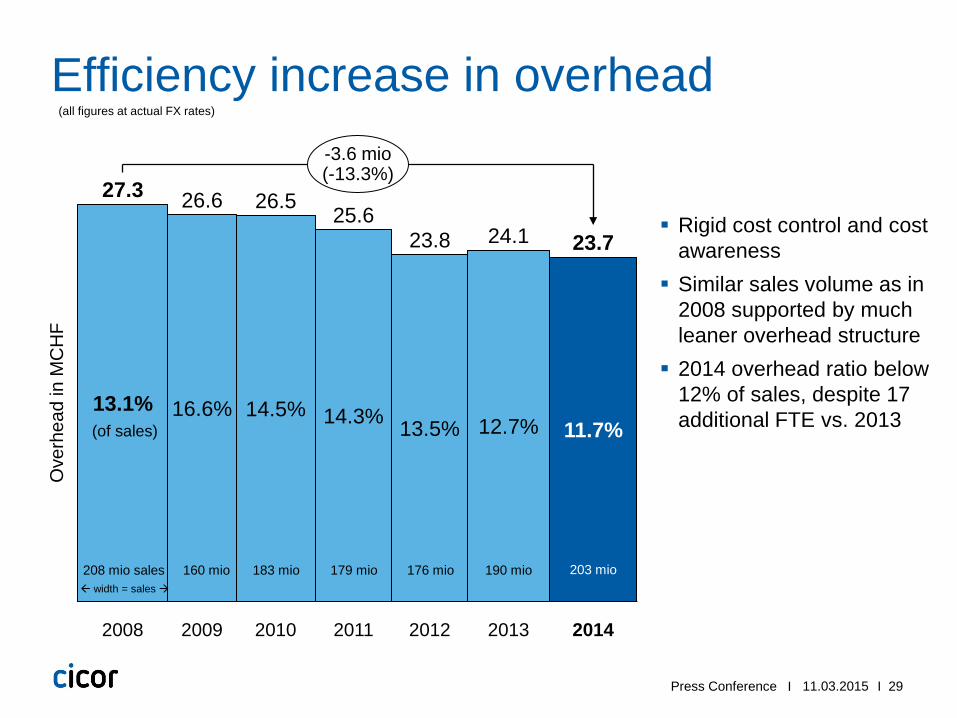

Efficiency increase in overhead

13.5%

2011

25.6

14.3%

2010

26.5

14.5%

2009

26.6

2008

11.7% 16.6%

27.3

13.1%

2014

23.7 23.8 24.1

-3.6 mio (-13.3%)

Ove

rhea

d in

MC

HF

2013

12.7%

2012

208 mio sales

Rigid cost control and cost awareness Similar sales volume as in

2008 supported by much leaner overhead structure 2014 overhead ratio below

12% of sales, despite 17 additional FTE vs. 2013 (of sales)

160 mio 183 mio 179 mio 176 mio 190 mio width = sales

(all figures at actual FX rates)

203 mio

11.03.2015 Press Conference

I 30 I

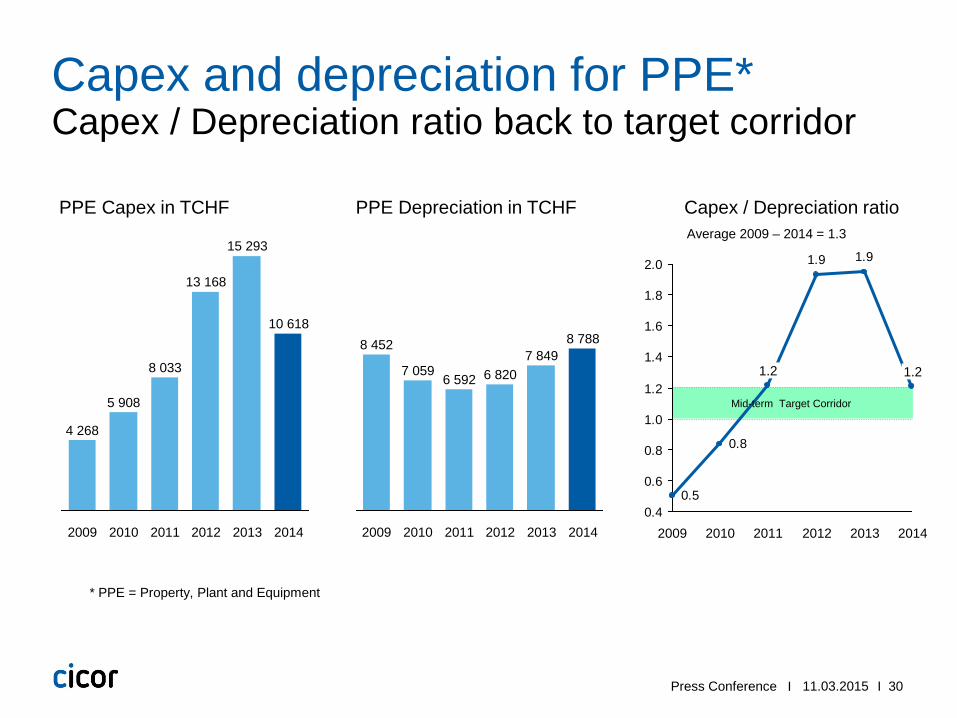

Capex / Depreciation ratio back to target corridor Capex and depreciation for PPE*

2014

8 788

2013

7 849

2012

6 820

2011

6 592

2010

7 059

2009

8 452

PPE Capex in TCHF PPE Depreciation in TCHF Capex / Depreciation ratio

* PPE = Property, Plant and Equipment

2014

10 618

2013

15 293

2012

13 168

2011

8 033

2010

5 908

2009

4 268

Average 2009 – 2014 = 1.3

1.91.9

0.8

0.50.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2009 2013

1.2

2012 2011

1.2

2010 2014

Mid-term Target Corridor

11.03.2015 Press Conference

I 31 I

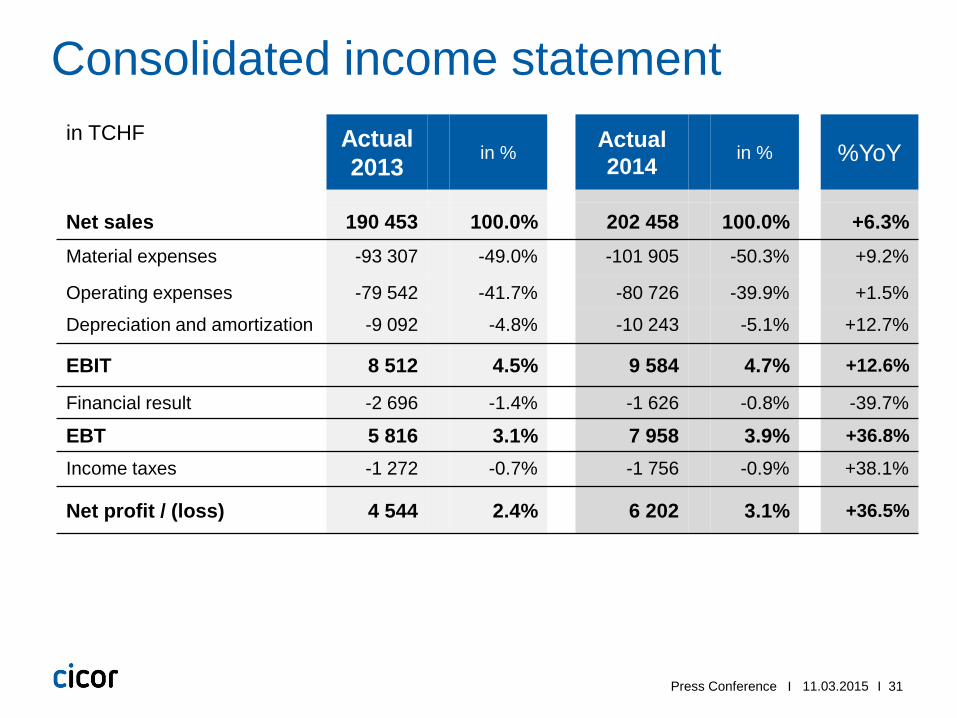

in TCHF Actual 2013 in % Actual

2014 in % %YoY

Net sales 190 453 100.0% 202 458 100.0% +6.3% Material expenses -93 307 -49.0% -101 905 -50.3% +9.2%

Operating expenses -79 542 -41.7% -80 726 -39.9% +1.5%

Depreciation and amortization -9 092 -4.8% -10 243 -5.1% +12.7%

EBIT 8 512 4.5% 9 584 4.7% +12.6%

Financial result -2 696 -1.4% -1 626 -0.8% -39.7%

EBT 5 816 3.1% 7 958 3.9% +36.8%

Income taxes -1 272 -0.7% -1 756 -0.9% +38.1%

Net profit / (loss) 4 544 2.4% 6 202 3.1% +36.5%

Consolidated income statement

11.03.2015 Press Conference

I 32 I

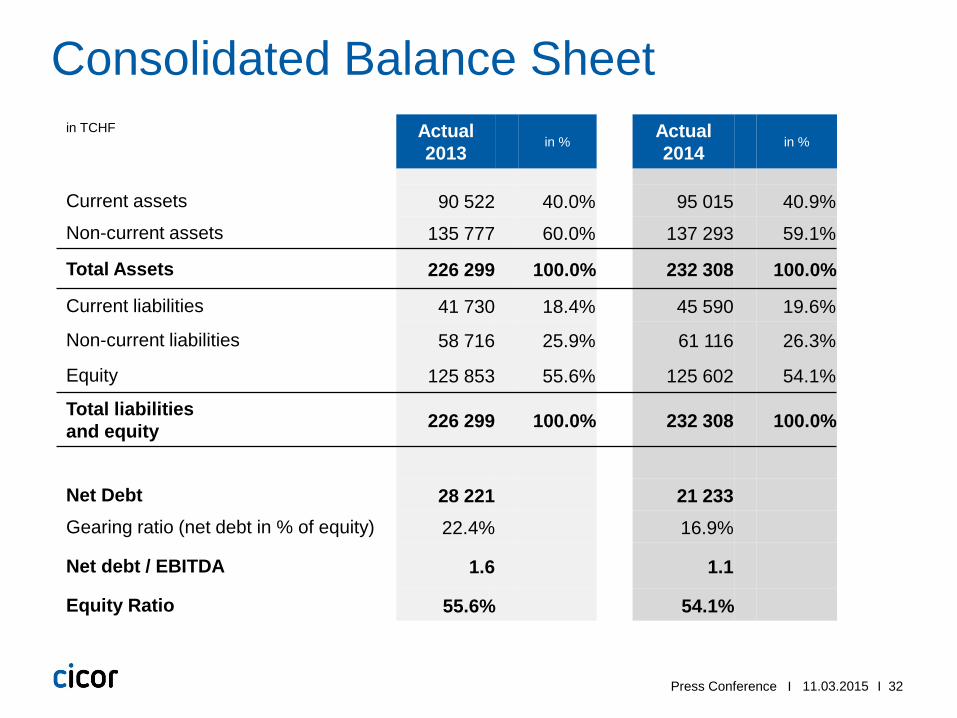

in TCHF Actual 2013

in % Actual 2014

in %

Current assets 90 522 40.0% 95 015 40.9%

Non-current assets 135 777 60.0% 137 293 59.1%

Total Assets 226 299 100.0% 232 308 100.0%

Current liabilities 41 730 18.4% 45 590 19.6%

Non-current liabilities 58 716 25.9% 61 116 26.3%

Equity 125 853 55.6% 125 602 54.1%

Total liabilities and equity 226 299 100.0% 232 308 100.0%

Net Debt 28 221 21 233 Gearing ratio (net debt in % of equity) 22.4% 16.9%

Net debt / EBITDA 1.6 1.1

Equity Ratio 55.6% 54.1%

Consolidated Balance Sheet

11.03.2015 Press Conference

I 33 I

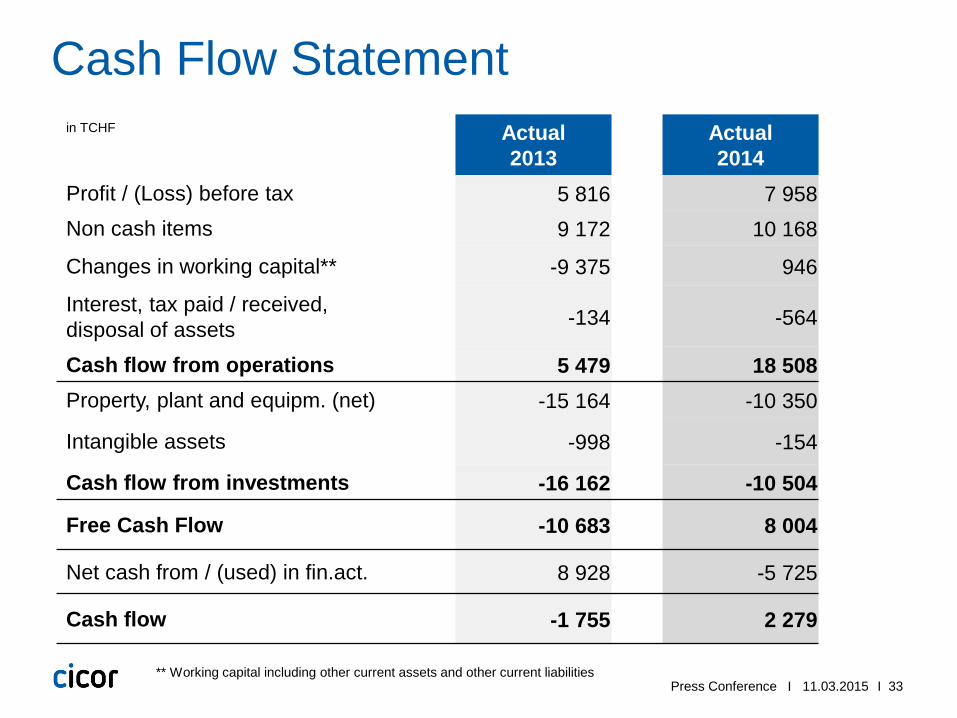

in TCHF Actual 2013

Actual 2014

Profit / (Loss) before tax 5 816 7 958 Non cash items 9 172 10 168

Changes in working capital** -9 375 946

Interest, tax paid / received, disposal of assets -134 -564

Cash flow from operations 5 479 18 508 Property, plant and equipm. (net) -15 164 -10 350

Intangible assets -998 -154

Cash flow from investments -16 162 -10 504

Free Cash Flow -10 683 8 004

Net cash from / (used) in fin.act. 8 928 -5 725

Cash flow -1 755 2 279

Cash Flow Statement

** Working capital including other current assets and other current liabilities Press Conference 11.03.2015

I 34 I

Outlook Patric Schoch

Press Conference 11.03.2015

I 35 I

Continued transparent reporting is guaranteed Switch to Swiss GAAP FER in 2015

The change to Swiss GAAP FER marks a decision by Cicor for a more pragmatic standard of comparative informational value in accordance with the principle of a true and fair view.

In application of the new reporting standard, Cicor will offset all goodwill against equity. It is expected that the equity ratio per 31 December 2014 would be around 45%.

The change would have an expected positive impact on the net profit of 2014 of around CHF 1.1 million.

The interim report for the first half of 2015 will contain reconciled financial statements.

The change in reporting standard also means that Cicor Technologies Ltd. will be transferred from Main Standard to Domestic Standard of SIX Swiss Exchange.

Press Conference 11.03.2015

I 36 I

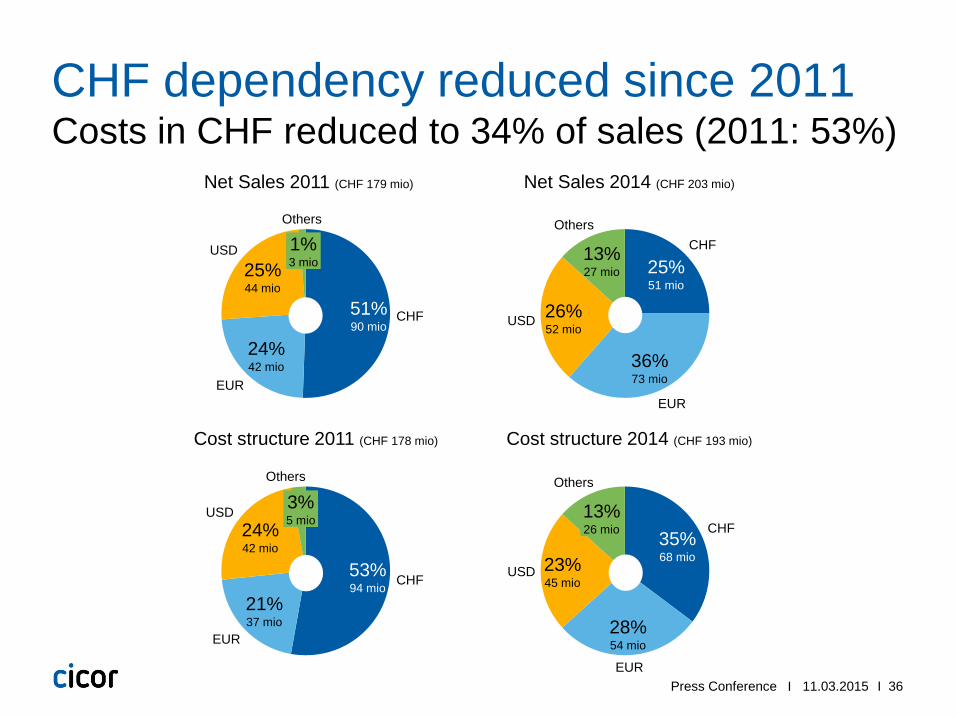

Costs in CHF reduced to 34% of sales (2011: 53%) CHF dependency reduced since 2011

51% 90 mio

CHF

24% 42 mio

EUR

25% 44 mio

USD

Others

1% 3 mio

Net Sales 2011 (CHF 179 mio)

25% 51 mio

CHF

36% 73 mio

EUR

26% 52 mio

USD

Others

13% 27 mio

Net Sales 2014 (CHF 203 mio)

53% 94 mio CHF

21% 37 mio

EUR

24% 42 mio

USD

Others

3% 5 mio

Cost structure 2011 (CHF 178 mio)

35% 68 mio

CHF

28% 54 mio

EUR

23% 45 mio

USD

Others

13% 26 mio

Cost structure 2014 (CHF 193 mio)

Press Conference 11.03.2015

I 37 I

Cicor is well prepared to face the challenges Outlook

The target for 2015 is to confirm the recent positive performance and to realize new opportunities that may arise

− The reported revenues in Swiss francs will be influenced by the recent exchange rate turbulences.

− The strong CHF could also negatively impact the competitiveness of some of Cicor’s customer groups, but...

+ …it will also push (Swiss) companies to look for outsourcing options outside Switzerland, particularly in East Europe and / or Asia.

+ Cicor has already been able to significantly reduce its dependence on the Swiss franc, but further decisive steps to mitigate the consequences of the appreciation of the Swiss franc are being evaluated by the Group Management.

+ Cicor will do everything in its power to confirm the positive performance of the last two years in spite of the strong currency-related headwinds.

Press Conference 11.03.2015

I 38 I

Questions / Answers

Press Conference 11.03.2015

I 39 I

Agenda 2015 and contacts Investor Relations

IR Agenda 2015 23 April 2015 Annual General Meeting 19 August 2015 Half-year results 2015 March 2016 Annual report 2015 Investor Relations Contacts Cicor Management AG Antoine Kohler, Chairman, and Patric Schoch, CFO WTC, Leutschenbachstrasse 95 8050 Zurich, Switzerland Phone: +41 43 811 44 05

Press Conference 11.03.2015

I 40 I

Thank you!

Press Conference 11.03.2015