Embed Size (px)

Citation preview

Retirement PlansRetirement Plans

Long Term SavingLong Term Saving

Two main reasons to save Two main reasons to save money for the long term: to money for the long term: to build a retirement fund and to build a retirement fund and to afford your child’s educationafford your child’s education

Current status of Social Current status of Social Security shows that you should Security shows that you should be saving for your own be saving for your own retirementretirement

Even people with modest incomes Even people with modest incomes can retire with enormous wealth- can retire with enormous wealth- the secret is disciplinethe secret is discipline

Also- compounding interest (you Also- compounding interest (you earn interest on an investment earn interest on an investment for one year, the borrower will for one year, the borrower will pay you interest based upon the pay you interest based upon the higher second year amount)higher second year amount)

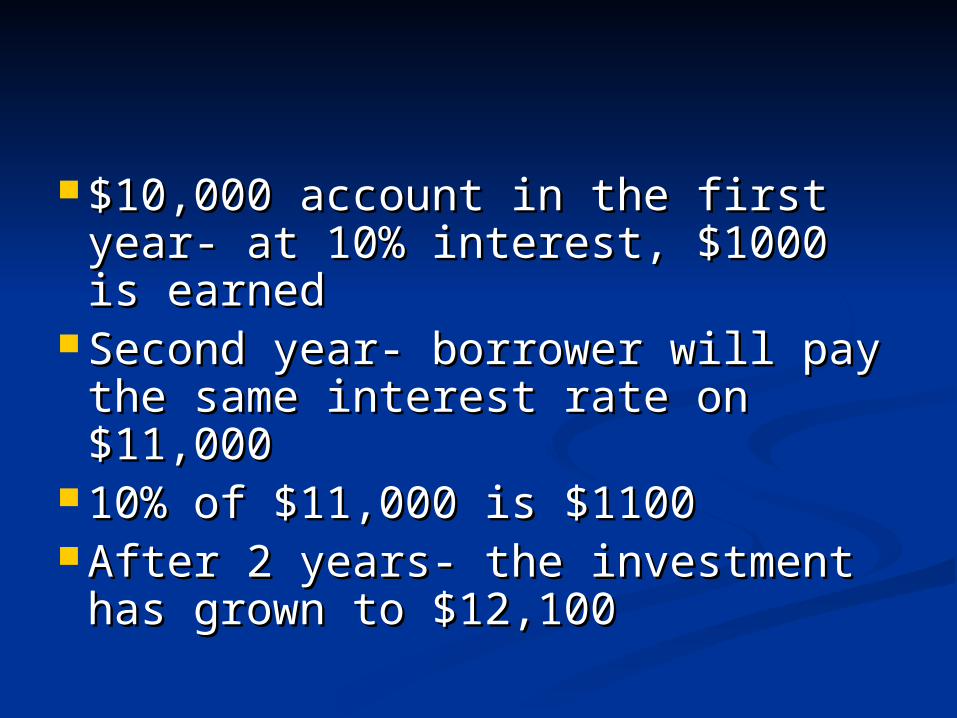

$10,000 account in the first year- $10,000 account in the first year- at 10% interest, $1000 is earnedat 10% interest, $1000 is earned

Second year- borrower will pay Second year- borrower will pay the same interest rate on the same interest rate on $11,000$11,000

10% of $11,000 is $110010% of $11,000 is $1100 After 2 years- the investment has After 2 years- the investment has

grown to $12,100grown to $12,100

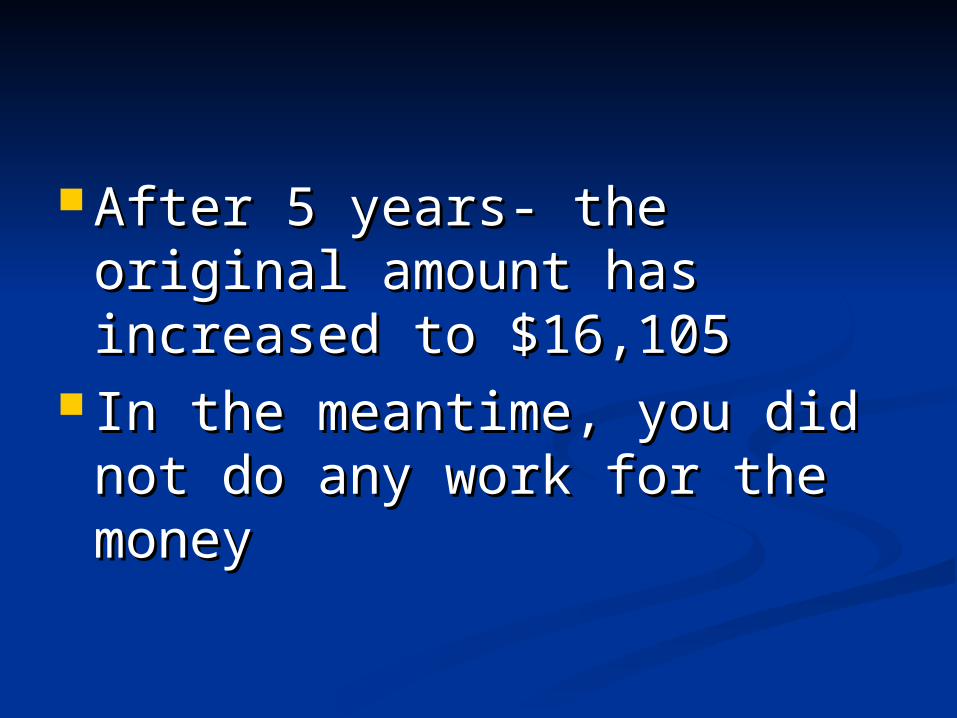

After 5 years- the original After 5 years- the original amount has increased to amount has increased to $16,105$16,105

In the meantime, you did not In the meantime, you did not do any work for the moneydo any work for the money

The money deposited in the The money deposited in the first few years will be the first few years will be the hardest working money in hardest working money in your whole portfolioyour whole portfolio

How much do you need to How much do you need to retire? Answer to that relies retire? Answer to that relies upon the lifestyle you wish to upon the lifestyle you wish to enjoy when you get olderenjoy when you get older

Could you live on $20,000 Could you live on $20,000 per year, or perhaps you per year, or perhaps you need $50,000?need $50,000?

Basically, $100,000 will give Basically, $100,000 will give you $7000 to 10,000 per year you $7000 to 10,000 per year when you retire. You’ll need when you retire. You’ll need more than that.more than that.

What are some of the What are some of the opportunity costs involved in opportunity costs involved in saving for a retirement? saving for a retirement?

Many people who are nearing Many people who are nearing retirement are finding out retirement are finding out they have not saved enough they have not saved enough money for a comfortable money for a comfortable retirementretirement

Also, the US is getting olderAlso, the US is getting older

Baby boomers (born between Baby boomers (born between 1945 and 1960) will be 1945 and 1960) will be retiringretiring

They will place an They will place an unbelievable strain on our unbelievable strain on our Social Security and Medicare Social Security and Medicare programsprograms

RetirementRetirement

First job out of collegeFirst job out of college 401 (k) most likely to be 401 (k) most likely to be

offeredoffered If no option for 401 (k), you If no option for 401 (k), you

could start a 403 (b) on your could start a 403 (b) on your ownown

Retirement PlansRetirement Plans

Two types of plans:Two types of plans:Defined BenefitDefined BenefitDefined ContributionDefined Contribution

Defined BenefitDefined Benefit

Old GM employee pensionsOld GM employee pensions Traditional pension planTraditional pension plan Most likely you will not get Most likely you will not get

thisthis

Pensions are a perk offered Pensions are a perk offered by some companiesby some companies

The organization involved The organization involved will contribute money to a will contribute money to a pension fund in the name of pension fund in the name of the employeethe employee

Upon retirement, the worker Upon retirement, the worker will receive a predetermined will receive a predetermined amount of money each month.amount of money each month.

Pension plans are not offered Pension plans are not offered as much as they were 20 or 30 as much as they were 20 or 30 years agoyears ago

The real growth is in defined The real growth is in defined contribution planscontribution plans

Defined ContributionDefined Contribution

Employer commits to Employer commits to contributing to your contributing to your retirementretirement

401 (k) most frequent type401 (k) most frequent type

401(k)401(k)

Employers will match your Employers will match your contributions up to a certain contributions up to a certain % (usually 3-5 %)% (usually 3-5 %)

Money is not taxed until you Money is not taxed until you withdraw it at retirement, withdraw it at retirement, then it is taxedthen it is taxed

401 (k)401 (k)

Government mandated Government mandated maximum that you can maximum that you can contribute increases every contribute increases every year 2006 - $15,000year 2006 - $15,000

Contribute at least as much Contribute at least as much as what your employer will as what your employer will matchmatch

401 (k)401 (k)

If your company says it will If your company says it will match 50% of your first 6% match 50% of your first 6% you contribute (means they you contribute (means they will contribute 3% of total will contribute 3% of total salary)- you must be willing salary)- you must be willing to contribute a minimum of to contribute a minimum of 6% of your salary to get that6% of your salary to get that

If you decide to put $200 a If you decide to put $200 a month into your retirement month into your retirement fund, you are actually saving fund, you are actually saving maybe $400 per month maybe $400 per month because of the additional because of the additional contribution of your contribution of your company. company.

401 (k)401 (k)

You are 100% vested in your You are 100% vested in your own contribution from Day 1own contribution from Day 1

It is your money, and it It is your money, and it cannot be taken away from cannot be taken away from you at that pointyou at that point

VestingVesting

Step: Example: After first Step: Example: After first year of working, you are year of working, you are entitled to 20% of what entitled to 20% of what company has put in. After company has put in. After second year, you are entitled second year, you are entitled to 40% of what company has to 40% of what company has put in, and so on. (5 Yr step put in, and so on. (5 Yr step vesting schedule)vesting schedule)

VestingVesting

Cliff: 0% until you get 100%Cliff: 0% until you get 100%Example is that you must Example is that you must stay five years before you stay five years before you are entitled to the are entitled to the company’s matchcompany’s match

WithdrawalsWithdrawals

If you withdraw from 401 (k) If you withdraw from 401 (k) before age 59 1/2, subject to before age 59 1/2, subject to regular tax on amount of regular tax on amount of withdrawal plus a 10% withdrawal plus a 10% penalty tax as well on penalty tax as well on anything you withdrawanything you withdraw

Hardship withdrawal Hardship withdrawal exceptionsexceptions

to buy a primary residence to buy a primary residence to prevent foreclosure or to prevent foreclosure or

eviction from your home eviction from your home to pay college tuition for to pay college tuition for

yourself or a dependent, yourself or a dependent, provided the tuition is due provided the tuition is due within the next 12 months within the next 12 months

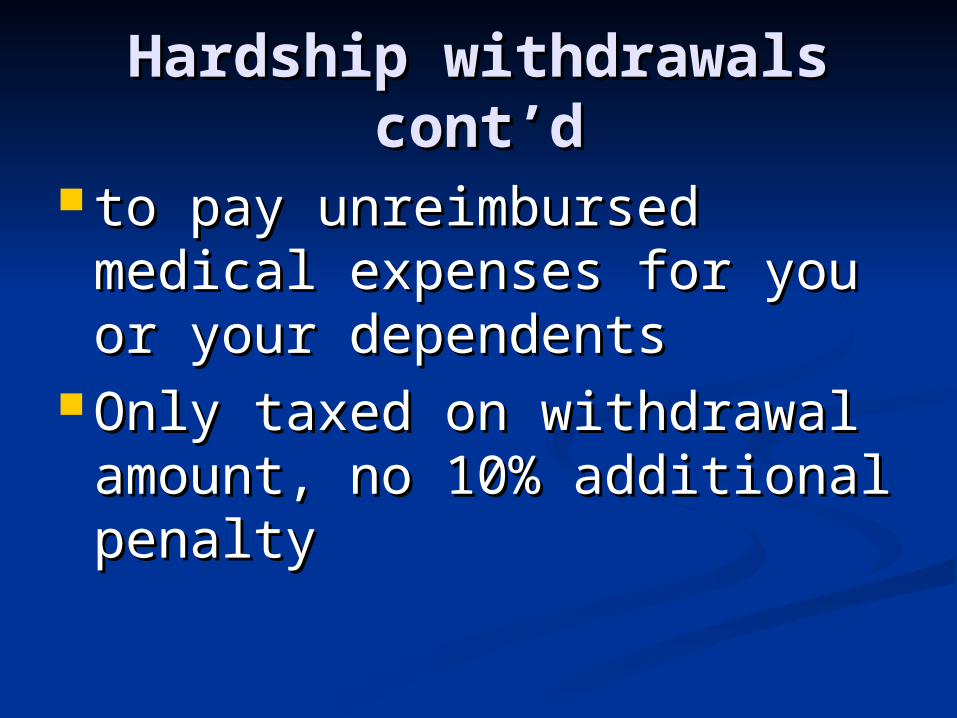

Hardship withdrawals Hardship withdrawals cont’dcont’d

to pay unreimbursed medical to pay unreimbursed medical expenses for you or your expenses for you or your dependents dependents

Only taxed on withdrawal Only taxed on withdrawal amount, no 10% additional amount, no 10% additional penaltypenalty

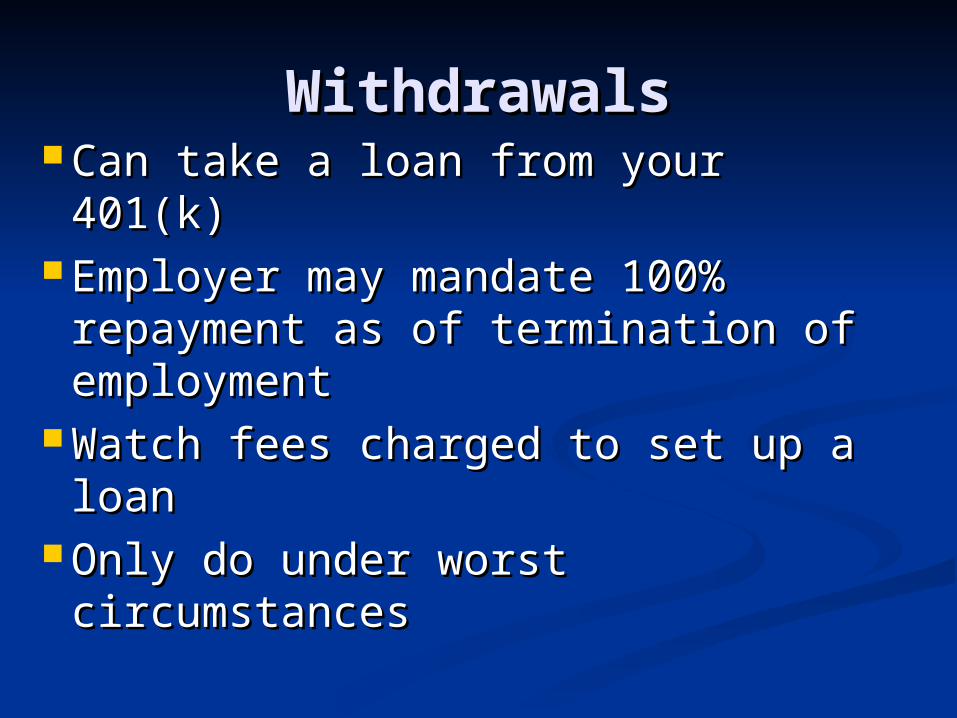

WithdrawalsWithdrawals Can take a loan from your 401(k)Can take a loan from your 401(k) Employer may mandate 100% Employer may mandate 100%

repayment as of termination of repayment as of termination of employmentemployment

Watch fees charged to set up a Watch fees charged to set up a loanloan

Only do under worst Only do under worst circumstancescircumstances

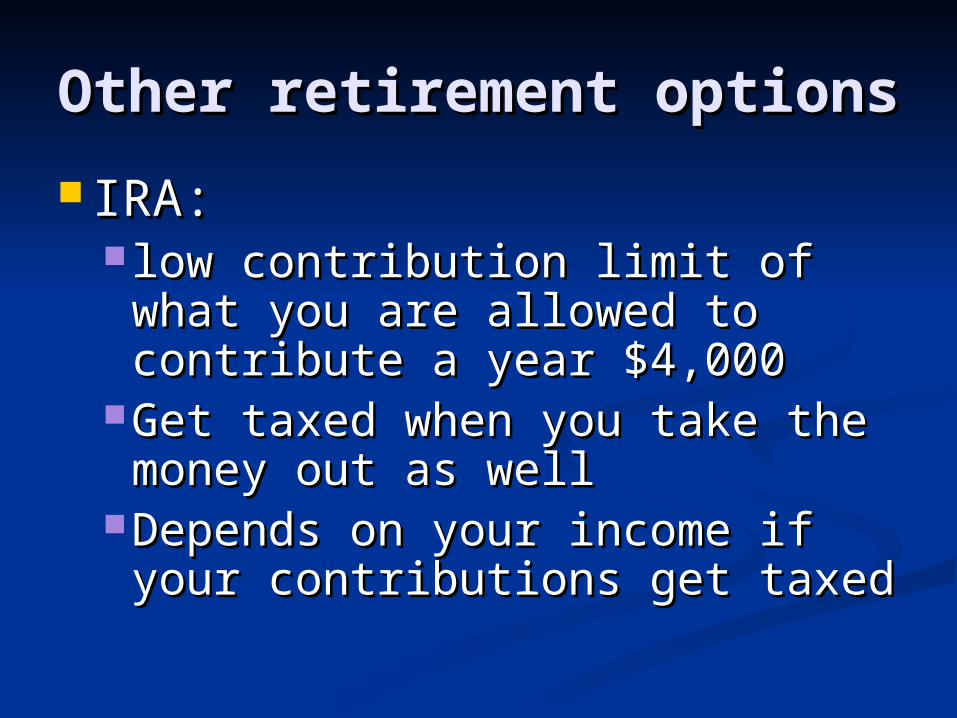

Other retirement optionsOther retirement options

IRA: IRA: low contribution limit of what low contribution limit of what

you are allowed to contribute a you are allowed to contribute a year $4,000year $4,000

Get taxed when you take the Get taxed when you take the money out as wellmoney out as well

Depends on your income if Depends on your income if your contributions get taxed your contributions get taxed

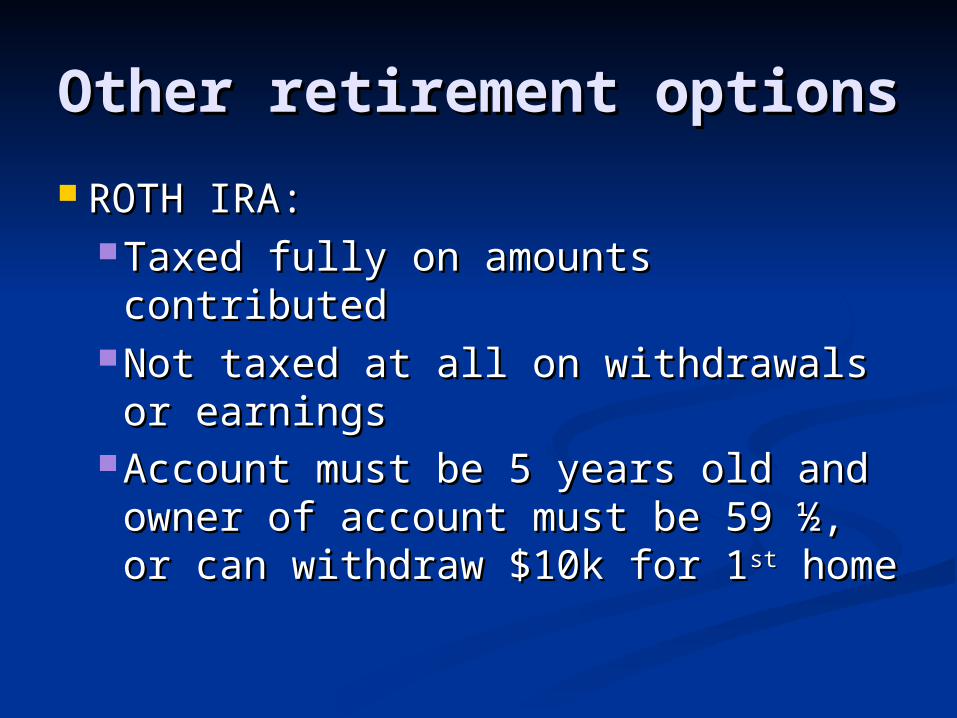

Other retirement optionsOther retirement options

ROTH IRA:ROTH IRA: Taxed fully on amounts Taxed fully on amounts

contributed contributed Not taxed at all on withdrawals or Not taxed at all on withdrawals or

earningsearnings Account must be 5 years old and Account must be 5 years old and

owner of account must be 59 ½, owner of account must be 59 ½, or can withdraw $10k for 1or can withdraw $10k for 1stst home home

Savings For Education Savings For Education ExpensesExpenses

529 college savings plans529 college savings plans Coverdell (Education) IRA’sCoverdell (Education) IRA’s

Mutual FundsMutual Funds

Pool of money invested in Pool of money invested in various investment vehiclesvarious investment vehicles

Primary investment option in Primary investment option in 401(k)’s, IRA’s, 529’s401(k)’s, IRA’s, 529’s

Offer diversification Offer diversification (decreased risk) at an (decreased risk) at an affordable priceaffordable price

![LTC Planning [Episode 76]€¦ · term care, long-term care planning, long-term care insurance, everything around that arena as it relates to clients and their risks in retirement](https://img.pdfslide.net/doc/110x75/5f1e61e79c662f37116d1671/ltc-planning-episode-76-term-care-long-term-care-planning-long-term-care-insurance.jpg)