Embed Size (px)

Citation preview

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 1/40

Chapter 10

Auditing

Revenue and

Related Accounts

Copyright © 2010 South-Western/Cengage Learning

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 2/40

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 3/40

LO 1 The Cycle Approach

• Revenue cycle transactions include all the processes

ranging from the sale to shipping a product, billing

the customer, and collecting cash

• A company's revenue cycle transactions reflects itsoperations

• A cycle approach is one way to help the auditor focus

on the important account balances surrounding a

transaction to ensure that sufficient audit evidence is

gathered and evaluated

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 4/40

Overview of the Revenue Cycle

(Sales made on Account)

• Receive customer purchase order

• Check inventory stock status

– Generate back order if item not in stock

• Obtain credit approval• Prepare shipping and packing documents

• Ship and verify shipment of goods

• Prepare the invoice

• Send monthly statements to customers

• Receive payment

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 5/40

LO 2 Audit Steps for an Integrated

Audit• Update information on business risk

• Analyze potential motivations to misstate sales

• Perform analytical procedures to look for unexpectedrelationships

• Develop understanding of internal controls

• Determine the important controls that need to be tested

• Develop a plan for testing internal controls and perform thetests of key controls

• Analyze the results of the tests of controls

• Perform planned substantive procedures

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 6/40

Example: An Integrated Audit of

Sales and Receivables• Consider the Risk of Misstatement in the Revenue Cycle

(Steps 1 and 2)

• While sales transactions are routine for most organizations and

do not represent an abnormally high risk, for other

organizations, revenue recognition may be complicated

Difficult audit issues include:

• When to recognize revenues

– Auditor must understand client's operations and related GAAPissues

– Example: point of sale revenue recognition vs. percentage of

completion

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 7/40

Example: An Integrated Audit of

Sales and Receivables (continued)

• Impact of any unusual sales terms and whether title passed to

customer

– Example: related party transactions

• Goods recorded as sales have been shipped• Sales made with recourse or that have significant returns

– Example: irrevocable right to return goods

The presence of these issues increase inherent risk and the

probability of material misstatement

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 8/40

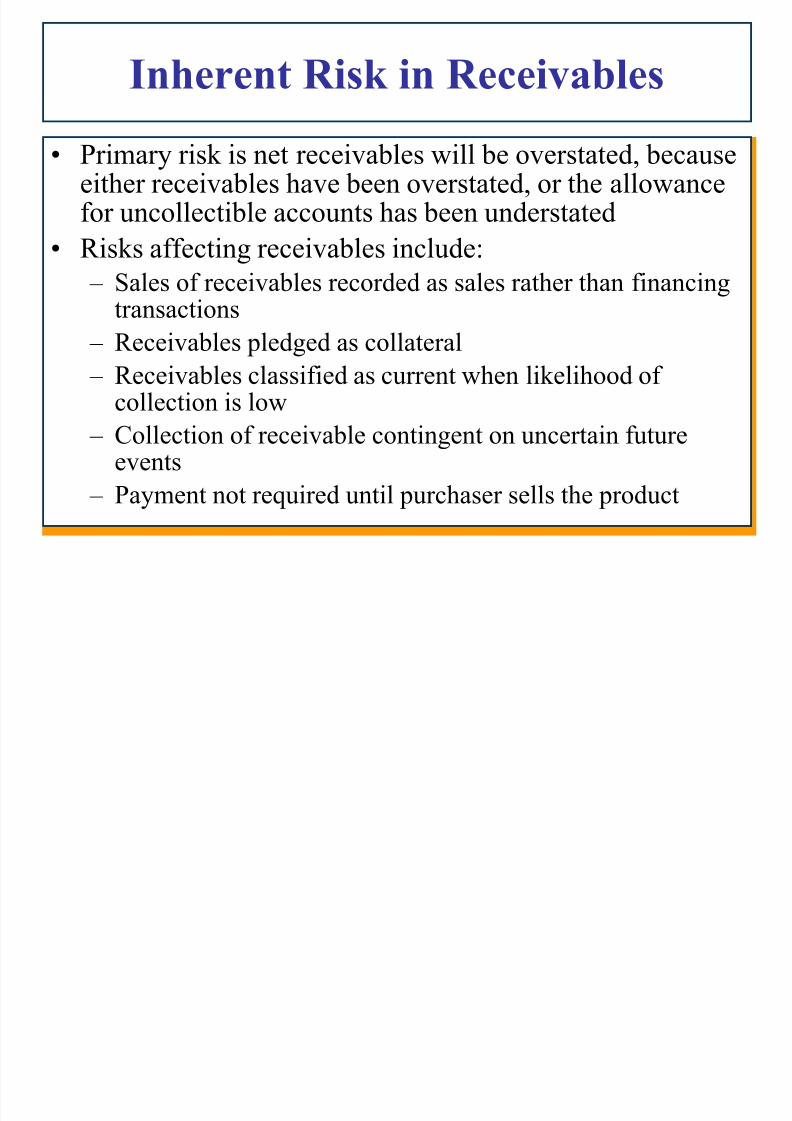

Inherent Risk in Receivables

• Primary risk is net receivables will be overstated, becauseeither receivables have been overstated, or the allowancefor uncollectible accounts has been understated

• Risks affecting receivables include:

– Sales of receivables recorded as sales rather than financingtransactions

– Receivables pledged as collateral

– Receivables classified as current when likelihood of

collection is low – Collection of receivable contingent on uncertain futureevents

– Payment not required until purchaser sells the product

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 9/40

Perform Preliminary Analytical

Procedures (Step 3)

The auditor then performs a preliminary review

and notes that:

•There is no unusual year-end sales activity

• Accounts receivable growth is consistent with

revenue growth

• Revenue growth, receivables growth, and gross

margin are consistent

• There is no unusual concentration of sales made to

customers

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 10/40

Develop an Understanding of

Internal Controls (Step 4)

• Although the auditor must understand all componentsof internal controls, particular attention is paid tosignificant control procedures and monitoringcontrols

• The auditor obtains an understanding of the controls by – Walk-through of the processing of transactions

– Inquiry

– Observation – Review of client documentation

• It is critical this understanding be documented in thework papers

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 11/40

Identify Important Controls (Step 5)

• The auditor understands the risks of the

revenue cycle

• The following key controls are identified for

testing:

– Credit authorization and consistency of credit policies

– Access to the computerized price list for goods sold

– Accuracy of quantities and prices for items shippedand billed

– Daily reconciliation of items shipped and items billed

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 12/40

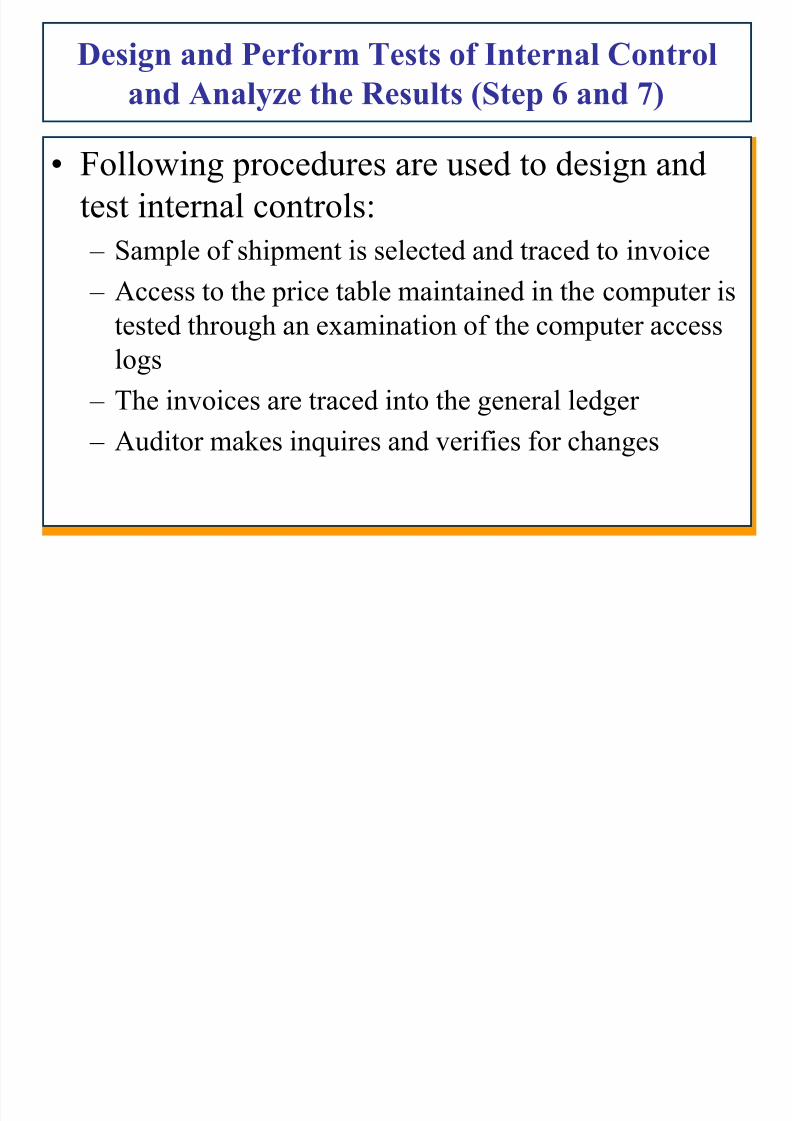

Design and Perform Tests of Internal Control

and Analyze the Results (Step 6 and 7)

• Following procedures are used to design and

test internal controls:

– Sample of shipment is selected and traced to invoice

– Access to the price table maintained in the computer is

tested through an examination of the computer access

logs

– The invoices are traced into the general ledger

– Auditor makes inquires and verifies for changes

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 13/40

Perform Substantive Tests (Step 8)

• Since revenue is always considered high risk, theauditor performs the following substantive test ofdetails as year-end procedures: – Examines shipments made during the last 15 days of the year

and the first 15 days of the next year to determine that they are(a) appropriate (normal terms, etc.) and (b) are recorded in thecorrect time period

– Sends a sample of accounts receivable confirmations tocustomers selected using MUS sampling

– Examines the client‘s allowance for uncollectible accounts for:• consistency with past years,

• subsequent collections and

• consistency with industry trends.

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 14/40

LO 3 Risk Related to Revenue

Recognition

SAS # 99 states that the auditor should ordinarily

presume there is a risk of material misstatement due

to fraud relating to revenue recognition.

Methods Used to Inflate Revenue• Recognition of revenue on shipments that never occurred.

• Hidden ―side letters‖ giving customers an irrevocable right to return

the product.

• Recording consignment sales as final sales.• Early recognition of sales that occurred after the end of the fiscal

period.

• Shipment of unfinished product.

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 15/40

Risk Related to Revenue Recognition

(cont.)

Methods Used to Inflate Revenue (continue)

• Shipment of product before customers wanted or agreed to delivery.

• Creation of fictitious invoices.

• Shipment to customers that did not place an order.

• Shipment of more product than the customer ordered.

• Recording shipments to the company‘s own warehouse as sales.

• Shipping goods that have been returned and recording the

reshipment as a sale of new goods before issuing credit for the

returned sale.

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 16/40

Criteria for Revenue Recognition

• Revenue should not be recognized until it is

realized

• As per SEC following criteria should be met in

applying the concept – Persuasive evidence of an arrangement exists

– Delivery has occurred or services have been rendered

– The seller‘s price to the buyer is fixed or determinable – Collectibility is reasonably assured

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 17/40

Fraud Risk Factors-Revenue

Recognition

• There are a number of ‗red flags‘ to which the auditorshould be alert when determining the potential forfraud

• Identifying and adjusting the audit to address theserisk factors involves the following:

– Examining motivation to enhance revenue due to eitherinternal or external pressures.

– Examining the financial statements through preliminaryanalytical procedures

– Recognizing that not all of the fraud will be instigated bymanagement

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 18/40

External and Internal Risk Factors

• External

– Analyst Expectations

– Industry Trends

– Investigations

• Internal

– Management compensation schemes

– Expiration of stock options

– Accounting is not centralized – Weak controls

– CFO does not have an accounting background

– Use of stock option to increase stock‘s market value

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 19/40

LO 4 Perform Preliminary

Analytical Procedures

• Compare client revenue trend with economic

conditions and industry trends

• Compare cash flow from operations with net

income

• Perform analytical procedures

– Ratio analysis

– Trend analysis

– Reasonableness tests

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 20/40

LO 5 Linking Internal Controls and

Financial Statement Assertions

Internal control procedures should be sufficient toensure the management assertions are achieved:

• Existence/Occurrence: sales are recorded only when shipmenthas occurred and the primary revenue producing activity has

been performed• Completeness: all valid sales transactions are recorded

• Rights/obligations

• Valuation

• Internal controls related to Returns, Allowances, andWarranties

• Documenting Controls

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 21/40

Design and Perform Tests of

Internal Control

• The approaches to testing the reconciliation controlcould involve one or more of the following:

– Inquiry: Talk with the personnel who perform the controlabout the procedures and processes involved in the

reconciliation. – Observation: Observe the entity personnel performing the

reconciliation.

– Examination: Review the documentation supporting

completion of the reconciliation. – Reperformance: Perform the reconciliation and agree to the

reconciliation completed by the entity personnel.

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 22/40

Other Testing Procedures in Sales

Cycle

• Manual reviewing evidence of control operation — Take a

sample of recorded transactions and determine that the prices

agree with authorized prices.

• Computerized testing of computer controls — Test controls

used to limit access to the computer files, select a number of

prices in the system and reconcile to pre-authorized price

changes.• Testing of monitoring controls — Management should have

controls in place to assist them in monitoring proper prices.

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 23/40

LO 6 Substantive Tests of Revenue

for Existence/Occurrence and Valuation

• Vouch recorded sales transaction back to

customer order and shipping document

– Compare quantities billed and shipped withcustomer order

– Special care should be given to sales recorded at

the end of the year – Scan sales journal for duplicate entries

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 24/40

Substantive Tests of Revenue

Cutoff Issues

• Can be performed for sales, sales returns, cash

receipts

– Provides evidence whether transactions are

recorded in the proper period

– Cutoff period is usually several days before and

after balance sheet date

– Extent of cutoff tests depends on effectiveness ofclient controls

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 25/40

Substantive Tests of Revenue

Cutoff Issues

• Sales cutoff – Auditor selects sample of sales recorded during cutoff period and

vouches back to sales invoice and shipping documents todetermine whether sales are recorded in proper period

– Cutoff tests assertions of existence and completeness – Auditor may also examine terms of sales contracts

• Sales return cutoff – Client should document return of goods using receiving reports

– Reports should date, description, condition, quantity of goods – Auditor selects sample of receiving reports issued during cutoff

period and determines whether credit was recorded in the correct period

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 26/40

Substantive Tests of Revenue

for Completeness

• Use of pre-numbered documents is important

• Analytical procedures

• Cutoff tests• Auditor selects sample of shipping documents

and traces them into the sales journal to test

completeness of recording of sales

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 27/40

LO 7 Substantive Tests of Accounts

Receivable Existence

• Valuation

– Are sales and receivables initially recorded at their correctamount?

– Will client collect full amount of recorded receivables?

• Rights and Obligations

– Contingent liabilities associated with factor or salesarrangements

– Discounted receivables

• Presentation and Disclosure

– Pledged, discounted, assigned, or related party receivables

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 28/40

Standard Accounts Receivable Audit

Procedures

• Obtain and evaluate aging of accounts

receivable

• Confirm receivables with customers

• Perform cutoff tests

• Review subsequent collections of receivables

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 29/40

Aging Accounts Receivable

Because receivables are reported at net realizablevalue, auditors must evaluate management estimatesof uncollectible accounts

• Auditor will obtain or prepare schedule of aged accountsreceivable

• If schedule is prepared by client, it is tested formathematical and aging accuracy – Aging schedule can be used to

• Agree detail to control account balance• Select customer balances for confirmation

• Identify amounts due from related parties for disclosure• Identify past-due balances

– Auditor evaluates percentages of uncollectibility – Auditor then recalculates balance in the Allowance account

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 30/40

Confirming Receivables with

Customers

• Confirmations provide reliable external evidenceabout the – Existence of recorded accounts receivable and

– Completeness of cash collections, sales discounts, and sales

returns and allowances

• Confirmations are required by GAAS unless one ofthe following is present: – Receivables are not material

– Use of confirmations would be ineffective – Environment risk is assessed as low and sufficient evidence is

available from using other substantive tests

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 31/40

Types of Confirmations

Positive confirmations

• Customers are asked to agree the amount on the

confirmation with their accounting records and torespond directly to the auditor whether they agree

with the amount or not

• Positive confirmation requires a response• If customer does not respond, auditor must use

alternative procedures

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 32/40

Types of Confirmations (continued)

Negative confirmations• Customers are asked to respond only if they disagree

with the balance (non-response is assumed to meanagreement)

• Less expensive since there are no additional procedures if customer does not respond

• May be used when all of the following are present – Confirming a large number of small customer balances

– Environment risk for receivables is assessed as low – Auditor believes customers will give proper attention to

confirmations

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 33/40

Follow-up procedures for non-

responses• If customer does not respond to positive confirmation,

auditor may send a second, or even third, request• If customer still does not respond, auditor will use

alternative procedures• Examine the cash receipts journal for cash collected after

year-end – Care is taken to ensure receipt is year-end receivable, not

subsequent sale

• Examine documents supporting receivable (purchaseorder, sales invoice, shipping documents) to determine if

sale occurred prior to year-end – Evidence gathered from internal documents is not considered asreliable

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 34/40

Follow-up procedures for exceptions

noted

• Customers are asked to agree the amount on theconfirmation to their accounting records; differencesare called exceptions

• Reasons for exceptions:

– Timing differences

– Disputed items

– Customer errors

– Client misstatement

• Because misstatements are projected to the population of receivables, the auditor must determinethe reason for the exception

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 35/40

Related-Party Receivables

• Amounts due from related parties should beseparately disclosed

• Audit procedures to identify related-partytransactions include:

– Review SEC filings

– Review the accounts receivable subsidiary ledger and trial balance

– Management inquiry

– Communicate names of related parties so all audit teammembers can be alert for related-party transactions

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 36/40

Sold, Discounted, and Pledged

Receivables

• Receivables sold with recourse, discounted, or pledged as collateral should be disclosed

• Audit procedures to identify these items include:

– Management inquiry – Scan cash receipts journal for large cash inflows fromunusual sources

– Bank confirmations, which include information onobligations and terms

– Review board of director minutes, which contain approvalfor these items

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 37/40

LO 8 Fraud Indicators and

Audit Procedures

Potential fraud indicators:• Excessive credit memo or other adjustments to accounts receivable

just after year-end

• Customer complaints and discrepancies in receivable confirmations

• Unusual entries to the receivable subsidiary ledger or sales journal

• Missing or altered source documents

• Lack of operating cash flow when operating income has beenreported

• Unusual reconciling differences between receivable subsidiaryledger and control account

• Sales in the last month with unusual terms

• Pre- or post-dated transactions

• Unusual adjustments to sales accounts just before or after year-end

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 38/40

Fraud Indicators and

Audit Procedures (continued)

Substantive procedures that may highlight potentialfraud indicators:

• Review of source documents including invoices, shippingdocuments, customer purchase orders, etc

• Review and analyze credit memos and other adjustments to

receivables• Confirm sales terms with customers• Analyze large or unusual sales made near year-end• Scan the general ledger, receivables subsidiary ledger, and

sales journal for unusual activity

• Perform analytical review of credit memo and write-offactivity• Analyze recoveries of written-off accounts

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 39/40

Explain Auditing of Allowance for

Doubtful Accounts

• Accounts receivable should be reported at theirnet realizable value

• The balance of the allowance for doubtfulaccounts is estimated and depends on a number of

factors• Understating the allowance overstates net

accounts receivable and net income

• Where accounts receivable are material, theauditor should obtain an understanding of howmanagement developed the estimate by using oneor more of these approaches:

8/13/2019 REV Copy

http://slidepdf.com/reader/full/rev-copy 40/40

Explain Auditing of Allowance for

Doubtful Accounts (continued)

– Review and test the process used by management todevelop the estimate

• Test aging schedule

• Evaluate estimated percentages of uncollectibility used

– Develop an independent model to estimate theaccounts

– Review subsequent events such as subsequentcollections on account

![ISO 9001 Clauses Simply Explained Rev.1[1] Copy](https://img.pdfslide.net/doc/110x75/55cf94f9550346f57ba5af3c/iso-9001-clauses-simply-explained-rev11-copy.jpg)