Embed Size (px)

Citation preview

Rickmers Holding GmbH & Cie. KG

Company Presentation

November 13th, 2013

2

Disclaimer

This document and its contents are confidential and not meant for forwarding, transmission, publication, duplication, or disclosure (in wholly or partly) to other persons. Outside of

Germany the distribution of this document may be restricted by applicable laws.

This document does not constitute an offer to sell or an invitation to make an offer to buy or subscribe for securities of Rickmers Holding GmbH & Cie. KG.

This document includes 'forward-looking statements'. Forward-looking statements are all statements, which do not describe facts of the past, but containing the words "believe",

"estimate", "expect", "anticipate", "assume", "plan", "intend", "could", and words of similar meaning. These forward-looking statements are subject to inherent risks and

uncertainties since they relate to future events and are based on current assumptions and estimates of Rickmers Holding GmbH & Cie. KG, which might not occur at all or occur

not as assumed. They therefore do not constitute a guarantee for the occurrence of future results or performances of Rickmers Holding GmbH & Cie. KG. The actual financial

position and the actual results of Rickmers Holding GmbH & Cie. KG, as well as the overall economic development and the regulatory environment may differ materially from the

expectations, which are assumed explicitly or implicitly in the forward-looking statements and do not comply to them. Therefore, investors are warned to base their investment

decisions with respect to Rickmers Holding GmbH & Cie. KG on the forward-looking statements mentioned in this document.

3

Table of Contents

A. Executive Summary

B. Company profile

I. Tradition

II. Management

III. Business Model

IV. Market and Competition

V. Strategy

VI. Bond and Use of Proceeds

VII. Half-Year Financials

C. Appendix

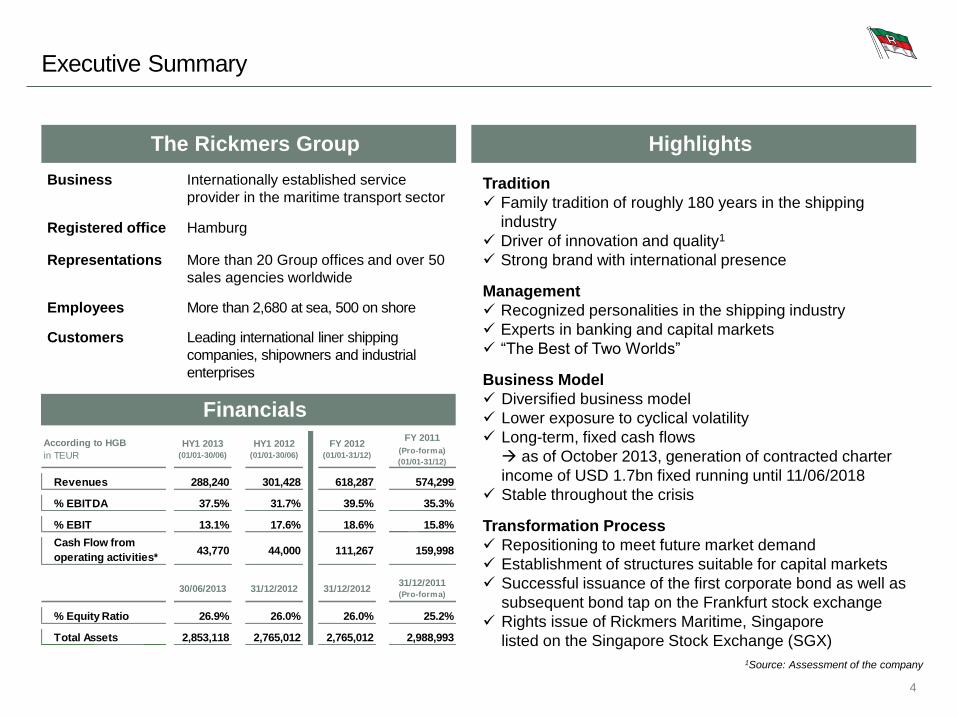

Executive Summary

4

The Rickmers Group

Business Internationally established service

provider in the maritime transport sector

Registered office Hamburg

Representations More than 20 Group offices and over 50

sales agencies worldwide

Employees More than 2,680 at sea, 500 on shore

Customers Leading international liner shipping

companies, shipowners and industrial

enterprises

Highlights

Financials

Tradition

Family tradition of roughly 180 years in the shipping

industry

Driver of innovation and quality1

Strong brand with international presence

Management

Recognized personalities in the shipping industry

Experts in banking and capital markets

“The Best of Two Worlds”

Business Model

Diversified business model

Lower exposure to cyclical volatility

Long-term, fixed cash flows

as of October 2013, generation of contracted charter

income of USD 1.7bn fixed running until 11/06/2018

Stable throughout the crisis

Transformation Process

Repositioning to meet future market demand

Establishment of structures suitable for capital markets

Successful issuance of the first corporate bond as well as

subsequent bond tap on the Frankfurt stock exchange

Rights issue of Rickmers Maritime, Singapore

listed on the Singapore Stock Exchange (SGX)

1Source: Assessment of the company

Cash Flow from

operating activities*

Total Assets 2,853,118 2,765,012 2,765,012 2,988,993

% Equity Ratio 26.9% 26.0% 26.0% 25.2%

15.8%

43,770 44,000 111,267 159,998

% EBIT 13.1% 17.6% 18.6%

Revenues 288,240 301,428 618,287

31/12/2011(Pro-forma)

According to HGB

in TEUR

HY1 2013(01/01-30/06)

HY1 2012(01/01-30/06)

FY 2012(01/01-31/12)

FY 2011

(Pro-forma)

(01/01-31/12)

574,299

% EBITDA 37.5% 31.7% 39.5% 35.3%

30/06/2013 31/12/2012 31/12/2012

5

Table of Contents

A. Executive Summary

B. Company profile

I. Tradition

II. Management

III. Business Model

IV. Market and Competition

V. Strategy

VI. Bond and Use of Proceeds

VII. Half-Year Financials

C. Appendix

6

I. Tradition

Almost 180 years under the Rickmers flag

The Rickmers Group today: “Future meets tradition“ – The combination of long family

tradition and strong market positioning creates the basis for successful corporate growth.

1834 R.C. Rickmers establishes the Rickmers shipyard in Bremerhaven

1836 R.C. Rickmers receives 1st vessel newbuild order

1842 Shipping business launched

1912 Establishment of two liner services: “Rickmers Siberian Line“ and “Rickmers East Asia Line”

1970s The shipyard receives important mandates for the newbuild of special ferries

1988 Hapag-Lloyd acquires the Rickmers-Linie – vessels in the Rickmers-Linie retain traditional colors and its name

1982 Bertram R.C. Rickmers establishes MCC Marine Consulting & Contracting, the nucleus of today‘s Rickmers Group

2000

Repurchase of the Rickmers-Linie from Hapag Lloyd

2007

Public listing of the trust Rickmers Maritime on Singapore stock exchange

2011

Strategic repositioning of Rickmers Group;

Rickmers joint venture with the Maersk Line, Limited, involving US freight,

Rickmers completes series of eight 13.100 TEU vessels; chartered out on

a long-term base to Maersk

2012

First publication of Group consolidated financial statements as part of an

open capital market communication

2013

First corporate bond issuance by Rickmers Holding GmbH & Cie. KG with

a volume of EUR 175 million and subsequent bond tap (EUR 50 million);

Rights issue of subgroup Rickmers Maritime, Singapore amounting to

EUR 62.4 million (SGD 101.7 million)

… 5th generation of the Rickmers family 1st – 4th generation of the Rickmers family…

7

Table of Contents

A. Executive Summary

B. Company profile

I. Tradition

II. Management

III. Business Model

IV. Market and Competition

V. Strategy

VI. Bond and Use of Proceeds

VII. Half-Year Financials

C. Appendix

8

II. Management

The Best of Two Worlds - High expertise level at all management levels

Shipping know-how and capital market expertise with an international background are

combined under one roof.

Chairman

Bertram R.C. Rickmers

Board of

Executive

Directors:

Ronald D. Widdows

CEO

Dr. Ignace Van Meenen

Deputy CEO and CFO

The Deputy CFO, the Chief Treasury & Risk Officer, the Global Heads of the three business segments and the COO of Rickmers-Linie

make up the Extended Board of the Rickmers Group.

Corporate

Center: Corporate

Communi-

cations

Prof. Dr. Mark-Ken Erdmann

Deputy CFO

Frank Bünte CRO and Head of Capital Markets

Controlling &

Accounting Tax M&A IT

Human

Resources

Legal

Affairs Risk & Treasury Capital Markets

Business

Segments:

Maritime Assets

Holger Strack

Global Head

Maritime Assets

Maritime Services

Björn Sprotte

Global Head

Maritime Services

Rickmers-Linie

Rüdiger Gerhardt

Global Head

Rickmers-Linie

Organisation

Advisory Board

Bertram R.C. Rickmers Claus-G. Budelman

Jost Hellmann Flemming R. Jacobs

Rickmers-Linie

Ulrich Ulrichs

COO

Rickmers-Linie

9

Table of Contents

A. Executive Summary

B. Company profile

I. Tradition

II. Management

III. Business Model

IV. Market and Competition

V. Strategy

VI. Bond and Use of Proceeds

VII. Half-Year Financials

C. Appendix

10

III. Business Model

Maritime Assets: Developing value throughout the entire vessel lifecycle

Long-term partnerships with renowned customers like Maersk ensure sustained, stable

cash flows.

Strong customer base of leading liner shipping

companies, thereof Maersk, MOL, MSC, OOCL,

Evergreen, CMA CGM, and HMM

Over 90% of revenues in this business segment

are earned with the company’s own fleet

As of October 2013, the majority of potential

charter days of the company’s own fleet were

already contracted: 98% for 2013, 76% for 2014

and 57% for 2015

Long-term contracts (of up to 10 years); charter

income from the Group’s own fleet totaling

USD 1.7bn* contracted until 11/06/2018

Book value of own vessels as of 30/06/2013:

approx. EUR 2.5bn, avg. age: 6 years

Maritime Assets

Management of 101* vessels (82 container

vessels, 15 MPC as well as conbulkers and car

carriers), thereof 58 own vessels

26 KG vessels and 3 additional non-KG third party

vessels

Coverage of the maritime value chain: from project

planning and financing arrangement to chartering

and sales

Highlights

* As of October 2013

11

III. Business Model

Maritime Services: Professional fleet management

Customers: own fleet (Maritime Assets and

Rickmers-Linie) as well as several third parties

(total of 98 vessels*)

Technical and operational ship management

Newbuilding consultancy and supervision

Maritime insurance

Crewing

Energy efficiency management

Docking and maintenance

“360°- service concept” for vessel

Long-standing internal experience represents an excellent basis for further growth as

service provider to third parties.

First foreign company with a license for recruiting

Chinese seafarers who will be employed on

international vessels

Energy efficiency initiatives: e.g. introduction of the

energy management system EMMATM in 2012

First German shipping company to be certified in

2013 in line with the ISO 50001 energy

management system standard

Maritime Services Highlights

* As of October 2013

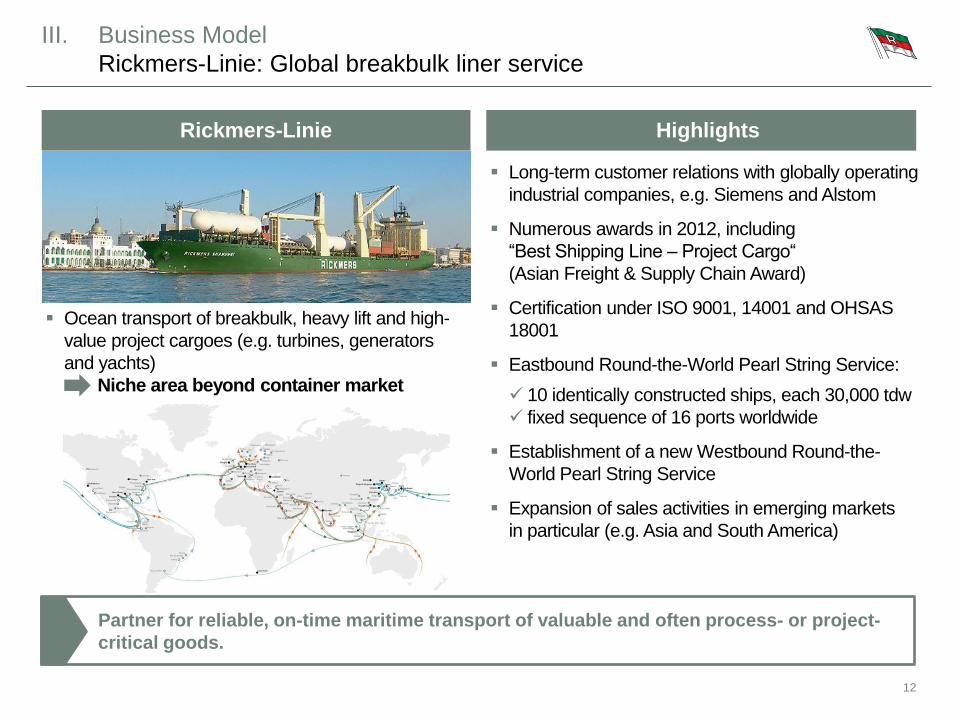

Long-term customer relations with globally operating

industrial companies, e.g. Siemens and Alstom

Numerous awards in 2012, including

“Best Shipping Line – Project Cargo“

(Asian Freight & Supply Chain Award)

Certification under ISO 9001, 14001 and OHSAS

18001

Eastbound Round-the-World Pearl String Service:

10 identically constructed ships, each 30,000 tdw

fixed sequence of 16 ports worldwide

Establishment of a new Westbound Round-the-

World Pearl String Service

Expansion of sales activities in emerging markets

in particular (e.g. Asia and South America)

Ocean transport of breakbulk, heavy lift and high-

value project cargoes (e.g. turbines, generators

and yachts)

Niche area beyond container market

12

Partner for reliable, on-time maritime transport of valuable and often process- or project-

critical goods.

III. Business Model

Rickmers-Linie: Global breakbulk liner service

Rickmers-Linie Highlights

13

The integrated, diversified range of services provides a competitive advantage.

III. Business Model

Diversified structure with synergy advantages

Maritime Assets Maritime Services Rickmers-Linie

Concurrent charter and

owner perspective

Energy efficiency programs with

direct result impact

Internal chartering within Group of multi-purpose carriers

(MPC) “In-house customer” / Know-how transfer

Common market

appearance to third

parties

Internal customer

relationship

within Group

Know-how transfer “In-house customer”

14

Table of Contents

A. Executive Summary

B. Company profile

I. Tradition

II. Management

III. Business Model

IV. Market and Competition

V. Strategy

VI. Bond and Use of Proceeds

VII. Half-Year Financials

C. Appendix

15

The container trade historically grows significantly stronger than world trade and GDP, an

additional increase is expected for the future.

IV. Market and Competition – Key Facts and Trends

Long-term growth of international maritime trade

Engine of growth for maritime trade:

Opening of emerging and developing economies

Change in the global flow of commodities due to

population development

Production trends and technological innovations

Close correlation between maritime trade and

economic development:

90% of the global cargo volume is transported over

the world’s oceans*

Complex heavy lift and project cargo can often only

be transported over the ocean

Based on the cost and energy efficiency advantages over other means of transportation,

maritime trade is an irreplaceable element in the international movement in goods.

*Source: BMWi Source: IMF (World Economic Outlook Database 07/2013) Clarkson (Container Intelligence Monthly 09/2013)

100

150

200

250

300

350

400

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013e 2014e

Ind

ex

ati

on

(1

99

5 =

10

0)

World GDP development World Trade development Container Trade development

5.7%

6.9% 7.0%6.4%

4.8%

7.7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2013 2014 2015

Demand Growth Fleet Growth

16

Currently difficult market situation: consolidation and timely adaptation to upcoming

challenges provide opportunities, especially with regard to “smaller vessels”.

IV. Market and Competition ‒ Key Facts and Trends

Growing demand is being challenged by fleet growth

Currently, maritime trade is characterized by excess supply

and low capacity utilization as well as low charter/freight

rates

This leads to increased competition and market

consolidation

Market demand and supply growth are expected to balance;

however, the trend cannot be predicted with absolute

certainty (e.g. see Howe Robinson Research estimation of

demand and fleet growth development on the right hand

side)

Howe Robinson Research 07/2013

9692 88

105 107 107

100

126

148

174

80

100

120

140

160

180

31/12/2012 31/12/2013 31/12/2014 31/12/2015

Ind

ex

<3,999 TEU 4,000 - 7,799 TEU 8,000+ TEU

Development of container vessel capacity by vessel size

Development of demand and fleet growth

In this context expected market trends might differ

significantly based on vessel size

Currently “smaller vessels” are expected to show a fortified

under-supply which may lead to a faster recovery of vessel

values and charter rates than in other size categories (e.g.

see Howe Robinson Research estimation of container

vessel capacity development by vessel size on the left

hand side)

17

Rickmers offers integrated services, from commercial and technical vessel management to

liner services for breakbulk, heavy lift and project cargo.

IV. Market and Competition - Competition

Rickmers as diversified supplier among its competitors*

Maritime

Assets

Maritime

Services

Rickmers-

Linie

* Source: Assessment

of the company

RICKMERS GROUP

Bernhard Schulte Shipmanagement Ltd.

Reederei Claus-Peter Offen (GmbH &Co.) KG

NSB Niederelbe Schifffahrtsgesellschaft mbH & Co. KG CHIPOLBROK Intermarine LLC

V. Ships Ltd.

Wilh. Wilhelmsen Holding ASA

Wallem Group Ltd.

Univan Ship Management Ltd.

Blue Star Holding GmbH & Cie. KG

Peter Döhle Schiffahrts-KG

Briese Schiffahrts GmbH & Co. KG Briese Schiffahrts GmbH & Co. KG (BBC Chartering)

Seaspan Marine Corporation

Hyundai Merchant Marine Co., Ltd.

COSCO Group

SAL Heavy Lift GmbH

Schoeller Holdings Ltd. Schoeller Holdings Ltd. (Columbia) Schoeller Holdings Ltd. (Austras Asia Line (AAL))

NYK-Hinode Line Ltd.

Danaos Shipping Co. Ltd.

Global Ship Lease, Inc.

Zodiac Maritime Agencies Ltd.

Norddeutsche Reederei H. Schuldt GmbH & Co. KG

Fleet Management Limited

Anglo Eastern Group Ltd.

Hansa Heavy Lift GmbH

stx Pan Ocean

Tramp Breakbulk-Liner

18

Table of Contents

A. Executive Summary

B. Company profile

I. Tradition

II. Management

III. Business Model

IV. Market and Competition

V. Strategy

VI. Bond and Use of Proceeds

VII. Half-Year Financials

C. Appendix

19

V. Strategy

Transformation measures overview since 2010

Transformation Measures 2010 – 2012

Realignment and greater focus on synergies between group segments

New management with respect to shipping know-how and capital market expertise

Development of a new corporate strategy

Initiation of efficiency enhancement programs, particularly for energy efficiency

Establishment of structures suitable for capital market (transparent reporting, corporate

governance structures, ongoing risk management procedures)

Successful establishment of the infrastructure for future growth

Transformation Measures 2013

Exploiting new sources of financing (see p. 20)

Taking advantage of the current market consolidation (see p. 20)

Initiation of strategical financing and investing activities

The initiated transformation process paves the way towards the capital market and builds

the basis for financing future growth.

1

2

20

V. Strategy

Transformation measures 2013 onwards …

Kick-Start of Refinancing Process

Bond proceeds used partly towards early repayment of

loans

Restructuring of debt financing is envisaged to be

executed by end of 2013

Major banks indicated to offer more favorable terms

Bond Issuance on Prime Standard of the Frankfurt

stock exchange in June 2013

Volume: EUR 175 mn, coupon: 8.875%, term: 5 years

(bullet repayment)

Bond Tap in November 2013

Increase by EUR 50 mn to EUR 225 mn, existing

terms and conditions continue to apply for new tranche

Raise of Equity, on Singapore Stock Exchange (SGX)

by Subgroup Rickmers Maritime in May 2013

Volume: EUR 62.4 mn; Rickmers Group participated in

proportion to its 33.1% stake

Refinancing Process

Successful Access to Capital Markets

With its recent successful capital market transactions, Rickmers Group is able to realize

opportunities from the current market consolidation!

Exploiting New Sources of Financing Taking Advantage of Market Consolidation

Extension of Strategically Important Trade Lanes

Restructuring of Vessel Portfolio

Sale of KG-fund vessels: “Disposal” of 23 KG-vessels in Maritime

Assets segment in 2013

Decrease in risk of valuation allowances from KG-funds

Acquisition of selected vessel types:

e.g. purchase agreement regarding five 2,200 TEU container

vessels with a total investment >USD 30 mn

Additionally JV with Apollo Global Management, LLC focusing on

acquisition of secondary market vessels (joint investment volume

up to USD 500mn over a period of several years)

Growth of 3rd party business with 11 incoming vessels in 2013 until

October into technical shipmanagement

Anti-cyclical investments of Rickmers-Linie

Initiation of the Westbound RTW service

Expansion of Europe-India and Eastbound RTW service

Expansion of sales activities in Asia as well as South and North

America

Exploration of potential M&A targets

1 2

21

Table of Contents

A. Executive Summary

B. Company profile

I. Tradition

II. Management

III. Business Model

IV. Market and Competition

V. Strategy

VI. Bond and Use of Proceeds

VII. Half-Year Financials

C. Appendix

0 €

5.000.000 €

10.000.000 €

15.000.000 €

20.000.000 €

25.000.000 €

98,00

98,50

99,00

99,50

100,00

100,50

101,00

101,50

102,00

102,50

103,00Trad

e Vo

lum

eP

rice

22

VI. Bond and Use of Proceeds

Historical Bond Performance

After some initial volatility the bond price has settled at a stable level around par with an

average trade volume of approx. EUR 828,000 per day.

* As of 5/11/2013 (source: Bloomberg)

The Rickmers bond is currently priced at 100.00*. Taking into account the accrued interest

since its issuance in June 2013, the bond shows a performance of +3.87%.

Remaining:78,5

Remaining:77.6

225.0

Invested:29,5

Invested:39.4

0

25

50

75

100

125

150

175

200

225

In m

€

23

VI. Bond and Use of Proceeds

Platform and growth investments as well as refinancing

Utilization of growth options along with the optimization of the financing structure.

* incl. issue costs

Issuance proceeds Platform (ongoing business)

and growth investments * Refinancing bank loans

24

Table of Contents

A. Executive Summary

B. Company profile

I. Tradition

II. Management

III. Business Model

IV. Market and Competition

V. Strategy

VI. Bond and Use of Proceeds

VII. Half-Year Financials

C. Appendix

2,3 2,3

0

1

2

3

30/06/2013 30/06/2012

Interest Coverage Ratio (EBITDA)

25

VII. Half-Year Financials ‒ Key Figures

Overview

26.9% 26.0%

0%

5%

10%

15%

20%

25%

30%

30/06/2013 31/12/2012

Equity ratio

1.451.37

0.0

0.5

1.0

1.5

2.0

30/06/2013 31/12/2012

Vessels' Value to Loan

288,240 301,428

108,200 95,700

37.5%

31.7%

0%

10%

20%

30%

40%

0

100,000

200,000

300,000

400,000

500,000

30/06/2013 30/06/2012

EB

ITD

A M

arg

in in

%

in T

EU

R

Revenues & EBITDA

Revenues EBITDA EBITDA Margin

26

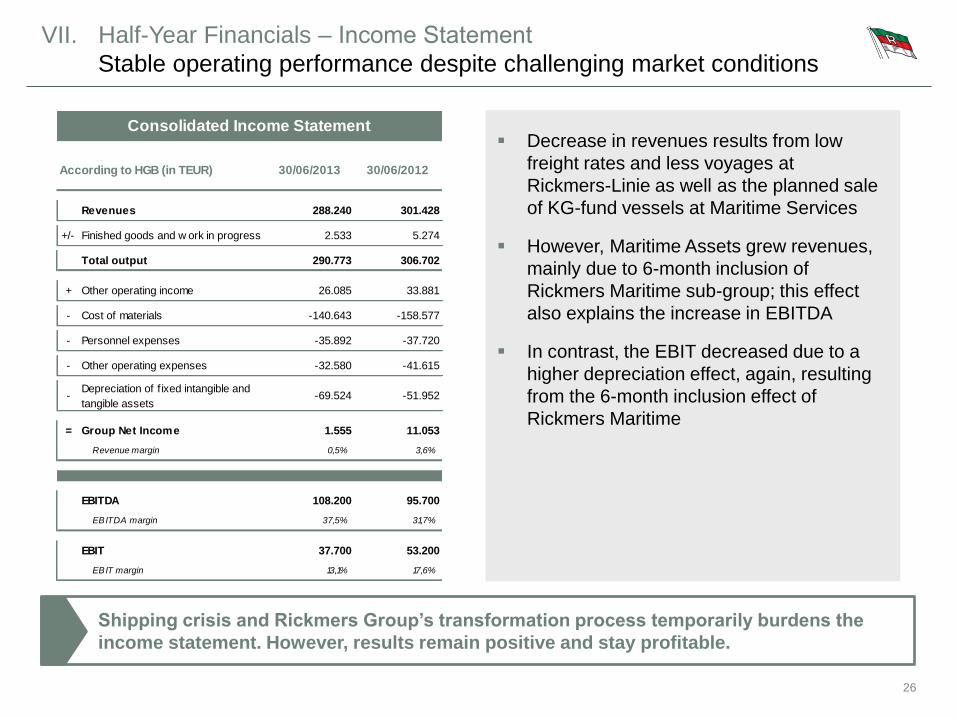

Shipping crisis and Rickmers Group’s transformation process temporarily burdens the

income statement. However, results remain positive and stay profitable.

VII. Half-Year Financials ‒ Income Statement

Stable operating performance despite challenging market conditions

Decrease in revenues results from low

freight rates and less voyages at

Rickmers-Linie as well as the planned sale

of KG-fund vessels at Maritime Services

However, Maritime Assets grew revenues,

mainly due to 6-month inclusion of

Rickmers Maritime sub-group; this effect

also explains the increase in EBITDA

In contrast, the EBIT decreased due to a

higher depreciation effect, again, resulting

from the 6-month inclusion effect of

Rickmers Maritime

Revenue margin

= Group Net Income

-Depreciation of f ixed intangible and

tangible assets-69.524

-140.643

-35.892

-32.580

-

-

According to HGB (in TEUR)

Total output

Other operating income

Personnel expenses

Other operating expenses

- Cost of materials

Consolidated Income Statement

+

+/-

30/06/2013

288.240

2.533

290.773

26.085

30/06/2012

301.428

5.274

306.702

33.881

Revenues

Finished goods and w ork in progress

-158.577

-37.720

EBIT margin

EBITDA margin

EBIT

13,1%

EBITDA

1.555

0,5%

108.200

37,5%

37.700

-41.615

-51.952

53.200

17,6%

11.053

3,6%

95.700

31,7%

27

The approach to capital markets fosters the cash situation of Rickmers Group.

VII. Half-Year Financials ‒ Balance Sheet

Increased equity ratio and strengthened cash position

Increase in equity due to rights issue of

Rickmers Maritime sub-group, Singapore

amounting to EUR 62.4 mn, in May 2013

(equity ratio: 26.9%)

Successful bond placement of

EUR 175 mn led to a cash increase

Thus liabilities increased slightly; while net

debt were reduced as well as liabilities to

banks went down by EUR 120.3 mn due to

repayments

Total assets are mainly influenced by the

value of the fleet, which decreased slightly

by -1.3% due to planned depreciation and

currency effects

2,011,524

175,808

1,721,635

Equity

III. Cash and cash equivalents

Total assets

719,512

Deferred expensesC.

73,124

12,681

2,765,012

D. Deferred tax assets 2,660

A.

208,570

15,911

1,786

2,853,118

766,452

8,063

1,841,897

8,063B. Difference from capital consolidation

Trade payables 20,068

Total equity and liabilities

5,544

F. Deferred tax liabilities 2,529

E. Deferred income

Other liabilities

2,765,012

89,438

thereof: Liabilities relating to social security 101

thereof: Tax liabilities 792

16,105

II. Receivables and other assets 105,480

194,709

III. Financial Assets

17,603

2,914

I. Inventories

Consolidated Balance Sheet

31/12/2012

A.

According to HGB (in TEUR)

I. Intangible assets

2,554,962Fixed Assets

2,526,045thereof: Vessels

B.

22,504

Current Assets

19,693

316,675

thereof: Prepayments and assets under construction 0

2,529,544II. Tangible assets

0

73,259

1,956,105D.

Provisions

Liabilities

C.

Liabilities to banks

Corporate Bonds 0

61,158

30/06/2013

2,518,746

2,598

2,496,455

2,493,023

20,741

89,716

842

137

3,464

2,457

2,853,118

90,502

0

0

1,756

51,470

80,689

3,113

0

-8,444

0

-50,809

-59,253

-12,140

41,993

-634

114

2,948

-1,312

-393

30/06/2012

107

1,540

-714

-1

0

30/06/2013

+/- Effect on cash and cash equivalents due to exchange rate movements

Cash flow from financing activities

= Cash and cash equivalents at end of period

+ Cash and cash equivalents at beginning of period

+ Increase in cash and cash equivalents due to changes in scope of

= Net change in cash and cash equivalents

376

73,124

208,570

66,940

135,070

0

- Payments to ow ners and minority shareholders

- Payments made for the repayment of borrow ings

+ Payments received from the raising of borrow ings

-5,787

195,865

-164,859

= Cash flow from investing activities

-Payments made for the purchase of consolidated companies and other

business units

+ Changes in f inancial receivables

+Payments received from equity increases and advances of

shareholders

0

23,428

24,360

41,721

Payments received from disposal of f inancial assets and repayments

- Payments made for investments in tangible and intangible assets

+Payments received from the sale of consolidated companies and other

business units

- Payments made for investments in f inancial assets

=

+ Payments received from disposal of tangible and intangible assets

+

Cash flow statement

-4,029

9,579

3,961

-11,409

44,000

30/06/2012

11,053

55,576

-12,814

-55

3,690

-11,301

-248

-3

-10,369

-12,572

-3,974

43,770

30/06/2013

1,555

68,065

-65

0

5,837

-3,273

-6

5

Increase (+) / decrease (-) in long-term provisions (> 1 year)

+ Other non-cash expenses

+ Depreciation, amortisation and impairment of f ixed assets

- Write-up of f ixed assets

+ Loss from disposal of f ixed assets

Increase (-) / decrease (+) in inventories (incl. prepayments)

- Other non-cash income

- Gain from disposal of f ixed assets

-1,433

Net income

= Cash flow from operating activities

Increase (+) / decrease (-) in liabilities and deferred income (w ithout

f inancial liabilities)

Cash flow statement

Increase (-) / decrease (+) in receivables, other assets and deferred

expenses

Increase (+) / decrease (-) in current provisions (< 1 year)

28

Despite a decrease in net income, operating cash flow - mainly driven by the asset

segment - remains stable compared to previous year’s period.

VII. Half-Year Financials ‒ Cash Flow Statement

Sustainable operating cash flow

29

Thank you for your attention.

Contact

Bertram R. C. Rickmers Chairman

Ronald D. Widdows CEO

Dr. Ignace Van Meenen Deputy CEO and CFO

Prof. Dr. Mark-Ken Erdmann Deputy CFO

Frank Bünte Chief Risk & Treasury Officer and Head of Capital Markets

Tobias Radloff Senior Manager | Tax

Rickmers Holding GmbH & Cie. KG

Neumühlen 19

22763 Hamburg, Germany

Tel. +49 (0)40.38 91 77-0

Fax +49 (0)40.38 91 77-500

www.rickmers.com

30

Table of Contents

A. Executive Summary

B. Company profile

I. Tradition

II. Management

III. Business Model

IV. Market and Competition

V. Strategy

VI. Bond and Use of Proceeds

VII. Half-Year Financials

C. Appendix

31

Appendix

Definitions

Term Explanations

TEU Twenty-foot Equivalent Unit: Unit for determining the cargo capacity of a ship; internationally standardized unit for payment of

containers of various sizes; corresponds to a 20-foot ISO container

tdw / dwt tons dead weight / dead weight tons: Unit for determining load capacity; gives the total load capacity of a merchant ship

Charter rates The price for chartering a vessel as agreed between the ship owner and the charterer.

Freight rates The price for transporting goods; pricing depends on distance, weight, form, volume and means of transport (truck, ship, aircraft)

and on the availability of resources required for the transport

Vessel type Use

Breakbulk freighter Vessels used to transport boxes, sacks, bales, cardboard boxes, crates, unpacked goods, heavy cargo

Container vessel Container transporter

Conbulker Combination of a container vessel and a bulk carrier for the simultaneous transport of containers and loose bulk cargo

Tanker Specially fitted ships for transporting liquid and gaseous materials (including crude oil, oil as a finished product, fuel,

liquid gas, water, juice)

Bulk Carrier Vessels which are used to transport loose bulk cargo such as ore, coal, cement, grain, etc.

Multi-purpose carrier Multi-purpose freighters, or heavy cargo vessels for transporting extremely heavy freight

RoRo ships So-called “roll on roll off” vessels in which the ship’s cargo is driven onboard, such as car transporter

32

Appendix

The Issuer as a group with three business segments

Rickmers-Linie Revenues represent 31.8% of the Group*

Rickmers Holding GmbH & Cie. KG (Issuer)

The three business segments form an integrated business model.

Maritime Assets Revenues represent 60.2% of the Group*

Maritime Services Revenues represent 7.9% of the Group*

* Consolidated revenues from segment information as of 30/06/2013

** ESSE Expert Shipping Service GmbH & Co. KG part of Maritime Assets since 01/01/2013;

Rickmers-Linie (Singapore) Pte. Ltd. incorporated in 2013

***In financial year 2012, the group of consolidated companies within Rickmers Holding was essentially extended

to include Rickmers Maritime, Singapore. Despite the minority holding, Rickmers Holding has secured the long

term majority of the voting rights and accordingly de facto control since the AGM on April 23th, 2012.

Rickmers Reederei

GmbH & Cie. KG,

Hamburg, Germany

(100%)

Harper Petersen & Co.

(GmbH & Cie. KG),

Hamburg, Germany

(50%)

Polaris Shipmanagement

Company Ltd.,

Douglas, Isle of Man

(100%)

Rickmers Trust Management

Pte. Ltd.,

Singapore, Singapore

(100%)

Elbe Vermögens Treuhand

GmbH (EVT), Hamburg,

Germany

(80%)

Rickmers Maritime

Singapore, Singapore

(33,1%)***

Single ship companies

Rickmers Shipmanagement

GmbH & Cie. KG,

Hamburg, Germany

(100%)

Global Management Ltd.,

Limassol, Cyprus

(100%)

Rickmers Shipmanagement

(Singapore) Pte. Ltd.,

Singapore, Singapore

(100%)

Rickmers Marine Agency

Romania S.R.L,

Constanta, Romania

(100%)

Rickmers Crewing GmbH,

Hamburg, Germany

(100%)

ESSE Expert Shipping

Service GmbH & Co. KG,

Hamburg, Germany

(100%)**

Global Marine Insurance

Brokerage Services Ltd.,

Limassol, Cyprus

(50%)

Rickmers-Linie GmbH & Cie.

KG,

Hamburg, Germany

(100%)

Rickmers (Korea) Inc.,

Seoul, South Korea

(100%)

MCC Marine Consulting &

Contracting GmbH & Cie.

KG, Hamburg, Germany

(100%)

Rickmers-Linie Belgium N.V.,

Antwerp, Belgium

(100%)

Rickmers Terminal Holding

GmbH,

Hamburg, Germany

(100%)

Rickmers (Japan) Inc.,

Tokio, Japan

(100%)

Rickmers-Linie (America)

Inc., Houston, USA

(100%)

Rickmers Shipping

(Shanghai) Co. Ltd.,

Shanghai, China

(80%)

Rickmers-Linie (Singapore)

Pte. Ltd.,

Singapore, Singapore

(100%)

Maersk-Rickmers U.S. Flag

Project Carrier

Delaware, USA

(50%)

Rickmers-Linie (Singapore)

Pte. Ltd.,

Singapore, Singapore

(100%)**

33

Appendix

Board of Executive Directors

Board of Executive Directors – Expertise in the shipping industry and capital markets.

More than 40 years experience in leading enterprises in the international shipping industry

(31 years at APL and NOL)

Chairman of the World Shipping Council (Washington D.C.)

Member of the Advisory Board of the International Transport Forum (Paris)

Industry experience and awareness of tradition stemming from almost 180 years of family history in the

shipping industry (5th generation)

Successful entrepreneur: Founder and owner of today‘s Rickmers Group

More than 35 years of management experience in the maritime value chain

Bertram R.C. Rickmers - Chairman and sole owner of Rickmers Holding

Ronald D. Widdows - CEO of Rickmers Holding as well as Rickmers-Linie

Dr. Ignace Van Meenen - Deputy CEO and CFO

More than 20 years of international management experience in capital markets and corporate finance

Various top-ranking positions in banks and major corporations

Member of the Supervisory Board of the trust Rickmers Maritime in Singapore

Joined the Rickmers Group in 2000 as nautical officer

Various management positions in technical and

commercial departments

Since 2012 Managing Director of Rickmers

Shipmanagement (Singapore)

Since January 2013 Global Head of the business

segment Maritime Services as well as Rickmers

Shipmanagement in Hamburg

Joined the Rickmers Group in 1997

Various management positions in Accounting and

Treasury

Since 2010 Managing Director of Rickmers Reederei

Since 2011 Global Head of the business segment

Maritime Assets

34

Appendix

Extended Board Committee

Extended Board Committee – broad management competencies in accounting, banking

and operational management activities of the shipping industry.

Long-term experience in “transformation” of capital

market-oriented family companies; direct reporting line to

the Group Deputy CFO/CFO and formerly Group CEO of

Bertelsmann

Overall more than 15 years of (management) experience

in financial management

Professor at the HHL

Prof. Dr. Mark-Ken Erdmann - Deputy CFO

More than 30 years of financing experience

More than 10 years of management experience

Management of the domestic ship financing

department of a German ship financing bank

Expert in ship financing and risk management

Frank Bünte - Chief Risk & Treasury Officer and

Head of Capital Markets

Holger Strack - Global Head Maritime Assets

Björn Sprotte - Global Head Maritime Services

Joined the Rickmers-Linie in 1978

Various management positions in the areas of finance,

controlling and personnel.

Since 2011 Global Head of Rickmers-Linie and

Managing Director of Rickmers-Linie GmbH & Cie. KG

Rüdiger Gerhardt - Global Head Rickmers-Linie

Joined the Rickmers Group in 2005 as General

Manager Line Management of the Rickmers-Linie

GmbH & Cie. KG, becoming Director of this division in

2008

Since July 2011 Deputy Managing Director of

Rickmers-Linie

Since July 2012 COO and Managing Director of

Rickmers-Linie

Ulrich Ulrichs - COO Rickmers-Linie

35

New energy-efficient ship generation offers diversification potential – modern forms of

financing and access to financing sources crucial for the future.

Appendix

The maritime transport sector and its demands are changing

Capacities

Financing

Efficiency

Ship

newbuildings

Competition

Excessive demand Excessive supply Tendency towards equilibrium with

excess demand

High financing willingness

(Banks / LP models) Slump in financing market

Lower bunker prices /

Low pressure to act

High number of

market participants

Over-utilisation of the shipyards/

Standardised ship specifications

Under-utilization of the shipyards /

Individualized ship specifications

High bunker prices /

High pressure to act to modernize

existing fleets

Search for alternative financing sources

and partners

Uncertainty over bunker prices / strategic

focus on energy efficiency

Potentially more stable shipyard capacity

utilization / New generation of energy-

efficient ship specifications

Completed

market consolidation Market consolidation

Vessel Prices Vessel prices at a high level Tendency towards increasing vessel

prices

Declining vessel prices with current

historical low points

Charter and

Freight Rates High price level

Significantly deceasing prices,

stabilization on low level Tendency towards increasing prices

Before 2008 Today Future expectation *

* Assessment of the company

36

Appendix

Full-Year Financials ‒ Key Figures

EBITDA

RevenuesEBITDA margin =

EBITDA

Financial resultICR (EBITDA basis) =

618,287574,299

517,897

244,360203,051

152,619

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2012 2011 (proforma) 2011 (as reported)

in T

EU

R

Revenues & EBITDA

Revenues EBITDA

2.6 2.6 2.7

00

01

02

03

2012 2011 (proforma) 2011 (as reported)

Interest Coverage Ratio (ICR)

39.5%

35.4%

29.5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2012 2011 (proforma) 2011 (as reported)

EBITDA Margin

37

Appendix

Full-Year Financials ‒ Key Figures

Equity

Balance sheet total=Equity ratio

Vessels

Liabilities to banksVessels' Value to Loan =

Liabilities to banks

EBITDASenior Debt/EBITDA =

26.0% 25.2%

15.2%

0%

5%

10%

15%

20%

25%

30%

2012 2011 (proforma) 2011 (as reported)

Equity Ratio

7.5

9.9 10.1

0

2

4

6

8

10

12

2012 2011 (proforma) 2011 (as reported)

Senior Debt / EBITDA

1.4 1.3

1.1

0.0

0.5

1.0

1.5

2.0

2012 2011 (proforma) 2011 (as reported)

Vessels' Value to Loan

38

Rising operating and after-tax profits for the past fiscal year of 2012.

Appendix

Full-Year Financials ‒ Income Statement

After repeated obtaining of a voting rights

majority at the annual shareholder meeting of

Rickmers Maritime, Singapore the trust was

fully consolidated for the first time in the annual

report of 2012.

To ensure better comparability, prior year

financial data (2011) is illustrated as pro forma.

The Rickmers Group shows profitability despite

a difficult environment:

In 2012 the Rickmers Group was able to

achieve a growth in revenues of 7.7%

compared to 2011 (pro forma).

Similarly, the operating profitability was

significantly increased by 20.3% (EBITDA

basis) and 26.7% (EBIT basis) compared to

2011 (pro forma).

Consolidated income statement

According to HGB (in TEUR) 20122011

(proforma)

2011

(as reported)

Revenues 618,287 574,299 517,897

+/- Finished goods and w ork in progress 2,863 -2,764 -2,764

Total output 621,150 571,535 515,133

+ Other operate income 86,435 29,258 26,757

- Cost of materials -308,114 -270,352 -267,734

- Personnel expenses -74,453 -67,788 -67,788

- Other operating expenses -72,042 -64,070 -63,837

-Depreciation of f ixed intangible and

tangible assets-135,576 -106,247 -76,415

= Group net income 22,459 13,805 14,370

Revenue margin 3.6% 2.4% 2.8%

EBITDA 244,360 203,051 152,619

EBITDA margin 39.5% 35.4% 29.6%

EBIT 114,664 90,508 70,531

EBIT margin 18.5% 15.8% 13.6%

39

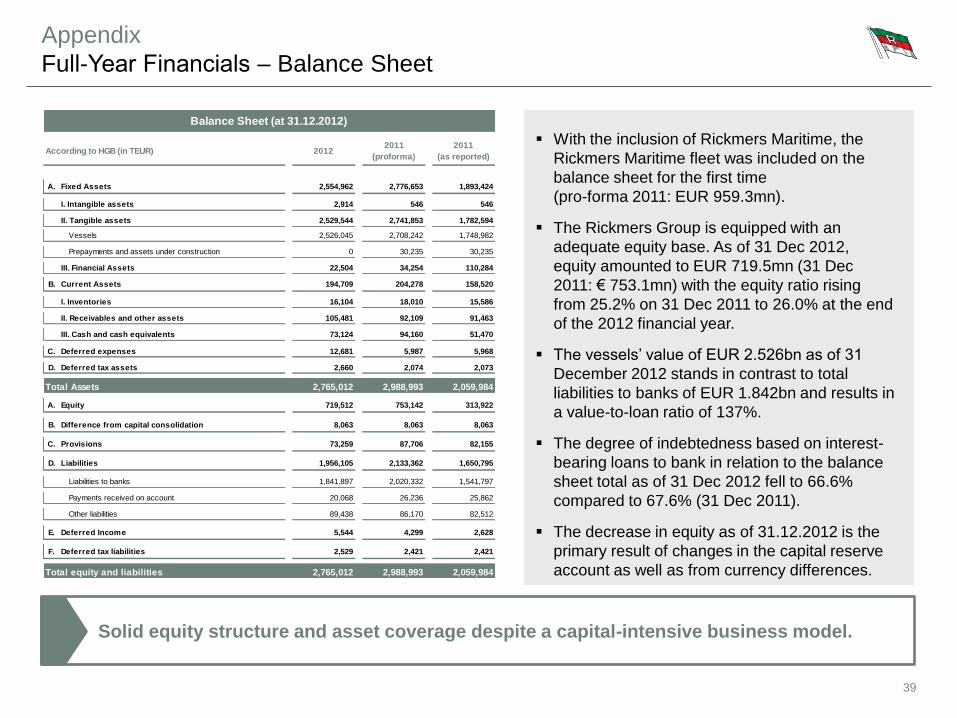

Solid equity structure and asset coverage despite a capital-intensive business model.

Appendix

Full-Year Financials ‒ Balance Sheet

With the inclusion of Rickmers Maritime, the

Rickmers Maritime fleet was included on the

balance sheet for the first time

(pro-forma 2011: EUR 959.3mn).

The Rickmers Group is equipped with an

adequate equity base. As of 31 Dec 2012,

equity amounted to EUR 719.5mn (31 Dec

2011: € 753.1mn) with the equity ratio rising

from 25.2% on 31 Dec 2011 to 26.0% at the end

of the 2012 financial year.

The vessels’ value of EUR 2.526bn as of 31

December 2012 stands in contrast to total

liabilities to banks of EUR 1.842bn and results in

a value-to-loan ratio of 137%.

The degree of indebtedness based on interest-

bearing loans to bank in relation to the balance

sheet total as of 31 Dec 2012 fell to 66.6%

compared to 67.6% (31 Dec 2011).

The decrease in equity as of 31.12.2012 is the

primary result of changes in the capital reserve

account as well as from currency differences.

Payments received on account 20,068 26,236 25,862

8,063

82,512

2,059,984

82,155

1,650,795

2,628

2,421

2,073

51,470

5,968

1,541,797

2,059,984

313,922

8,063

2,020,332

158,520

15,586

91,463

Total equity and liabilities

4,299

F. Deferred tax liabilities 2,529 2,421

E. Deferred Income 5,544

Other liabilities

2,988,9932,765,012

89,438 86,170

1,841,897

8,063B. Difference from capital consolidation

1,956,105Liabilities

C. 73,259

Liabilities to banks

Equity

546

I. Inventories

Balance Sheet (at 31.12.2012)

20122011

(proforma)

A.

110,284

2011

(as reported)

1,893,424

546

1,782,594

30,235

1,748,982

According to HGB (in TEUR)

I. Intangible assets 2,914

2,708,242Vessels

2,529,544

B.

18,010

2,776,6532,554,962Fixed Assets

2,988,993

92,109

2,765,012

73,124 94,160

12,681 5,987

22,504 34,254

Current Assets 194,709 204,278

III. Financial Assets

105,481II. Receivables and other assets

16,104

Prepayments and assets under construction 0 30,235

2,741,853

2,526,045

II. Tangible assets

719,512

D. Deferred tax assets 2,660 2,074

A.

III. Cash and cash equivalents

Total Assets

753,142

Deferred expensesC.

87,706

2,133,362D.

Provisions

40

Generation of a positive operating cash flow in excess of EUR 100mn for 2011 and 2012.

Appendix

Full-Year Financials ‒ Cash Flow Statement

Consolidated Cash Flow Statement

+/- Effect on cash and cash equivalents due to exchange rate movements -3,976 3,791 513

Cash Flow from financing activities

= Cash and cash equivalents at end of period 73,124 94,160 51,470

+ Cash and cash equivalents at beginning of period 51,470 65,982 65,982

+Increase in cash and cash equivalents due to changes in scope of

consolidation 41,736

= Net change in cash and cash equivalents -16,106 -55,810 -60,465

80,197 45,441

- Payments to ow ners and minority shareholders -14,009 -10,709 -8,141

- Payments made for the repayment of borrow ings -143,898 -493,725 -475,789

+ Payments received from raising borrow ings 8,978 592,277 592,277

0 170 170

= Cash Flow from investing activities 21,556 -303,821 -303,821

-Payments made for the purchase of consolidated companies and other

business units -77 -4,237 -4,237

+ Payments received from the change in f inancial receivables 2,400 0 0

+Payments received from equity increases and advances of

shareholders

+Payments received from the sale of consolidated companies and other

business units 0 -502 -502

- Payments made for investments in f inancial assets -666 -1,442 -1,442

Payments received from disposal of f inancial assets and repayments 8,951 11,065 11,065

- Payments made for investments in tangible and intangible assets -4,015 -308,742 -308,742

Cash Flow Statement 2012 2011( p ro f o rma)

2011( as

report ed )

108,517= -148,929 88,013

+ Payments received from disposal of tangible and intangible assets 14,963 37 37

+

*Deviation mainly due to reclassification

+ Depreciation, amortization and impairment of f ixed assets 128,883 111,919 82,088

- Write-up of f ixed assets -13,452 0 0

Incresase (+)/Decrease (-) in long-term provisions (> 1 Year) -1,872 -29 -29

+ Other non-cash expenses 8,408 13,820 13,134

-9,210 -9,176

- Other non-cash Income -21,631 -23,368 -20,511

- Gain from disposal of f ixed assets -1,062 -108 -108

2,083 1,934

Cash Flow Statement 2012 2011( p ro f orma)

2011( as

report ed )

Increase (-)/Decrease (+) in receivables, other assets and deferred

expenses-7,232 41,327 41,716

Increase (+)/Decrease (-) in current provisions (< 1 Year) -10,448 9,745 11,408

+ Loss from disposal of f ixed assets 21 14 14

Increase (-)/Decrease (+) in inventories (incl. prepayments) 1,575

Net Income 22,459 13,805 14,370

= Cash Flow from operating activities* 111,267 159,998 134,839

Increase (+)/Decrease (-) in liabilities and deferred income (w ithout

f inancial liabilities) 5,618

41

Appendix

Rickmers’ fleet of vessels

The container vessels of the Rickmers Group make up the main part of the entire fleet of vessels.

Vessel sizes under management are between 900 TEU and 13.100 TEU.

The Rickmers Group possesses 15 MPC ships for the transport of heavy lift or project cargo.

Bulk carriers are used to transport loose bulk cargo.

The Rickmers fleet of vessels comprises 3 car carriers with a capacity of 4,900 cars each.

Container ship – 13,100 TEU 8 Vessels

Container ship – 5,100 TEU Panamax 6 Vessels

Container ship – 4,700 TEU 5 Vessels

Container ship – 4,444 TEU 2 Vessels

Container ship – 4,250 TEU 17 Vessels

Container ship – 3,450 TEU 3 Vessels

Container ship – 2,800 TEU 1 Vessel

Container ship – 2,262 TEU 2 Vessels

Container ship – 2,200 TEU 11 Vessels

Container ship – 2,007 TEU 1 Vessel

Container ship – 2,000 TEU 1 Vessel

Container ship – 1,850 TEU 6 Vessels

Container ship – 1,700 TEU 9 Vessels

Container ship – 1,350 TEU 1 Vessel

Container ship – 1,200 TEU 1 Vessel

Container ship – 1,100 TEU 4 Vessels

Container ship – 1,100 TEU 1 Vessel

Container ship – 900 TEU 1 Vessel

Container ship – 822 TEU 1 Vessel

Conbulker – 1,650 TEU/35K 2 Vessels

Superflex Heavy MPC/30K 13 Vessels

Superflex Heavy MPC/17K 2 Vessels

Car Carrier 3 Vessels

42

Appendix

Employment of Rickmers fleet vessels

As of October 2013

![Acrich MJT 5050 Series - seoulsemicon.comSpecification]SAW0L60A_R3.0_1712.pdf · 0.3373 0.3534 0.3293 0.3384 0.3369 0.3451 C0 C1 C2 CIE x CIE y CIE x CIE y CIE x CIE y 0.3376 0.3616](https://img.pdfslide.net/doc/110x75/5bf955f609d3f2ab7d8cc0ef/acrich-mjt-5050-series-specificationsaw0l60ar301712pdf-03373-03534.jpg)

![Rickmers Lines - Project Cargo Stowage & Securing[1]](https://img.pdfslide.net/doc/110x75/55cf94b4550346f57ba3dd4b/rickmers-lines-project-cargo-stowage-securing1.jpg)