Embed Size (px)

Citation preview

Risk Management in the Marine Fuel Industry Adam Nye

European Energy Derivatives - Transportation

24th May 2013

THIS IS SALES AND TRADING COMMENTARY PREPARED FOR INSTITUTIONAL INVESTORS; it is NOT a research report; tax, legal, financial, or accounting advice; or an official confirm. The views of

the author may differ from others at MS (including MS Research). MS may engage in conflicting activities -- including principal trading before or after sending these views -- market making, lending, and the

provision of investment banking or other services related to instruments/issuers mentioned. No investment decision should be made in reliance on this material, which is condensed and incomplete; does not

include all risk factors or other matters that may be material; does not take into account your investment objectives, financial conditions, or needs; and IS NOT A PERSONAL RECOMMENDATION OR

INVESTMENT ADVICE or a basis to consider MS to be a fiduciary or municipal or other type of advisor. It constitutes an invitation to consider entering into derivatives transactions under CFTC Rules 1.71

and 23.605 (where applicable) but is not a binding offer to buy or sell any financial instrument or enter into any transaction. It is based upon sources believed to be reliable (but no representation of accuracy

or completeness is made) and is likely to change without notice. Any price levels are indicative only and not intended for use by third parties. Subject to additional terms at

http://www.morganstanley.com/disclaimers.

The typical structure of an investment bank

Morgan Stanley Commodities

Investment Banking Sales & Trading

Morgan Stanley

Institutional Securities Global Wealth

Management

Commodities

Equities Fixed Income & Commodities

Interest Rates & Currency

Products

Credit Products

2 Please see additional important information and qualifications at the end of this material.

• The Sales & Trading business

is a wholesale processor of

market risk

• We manage the external

market risks which corporations

would prefer to live without

The Commodities Group

Morgan Stanley Commodities

• Morgan Stanley is an active

trader of both physical

commodities and their financial

derivatives

• Our ability to manage market

risk is the essence of the

service we provide to our clients

Morgan Stanley Commodities

Trading Sales & Marketing

• Crude oil

• Refined products

• Natural gas

• Power

• Coal

• Emissions

• LNG

• Dry bulk & tanker

chartering

Energy

• Precious

• Base

• Ferrous

Metals

• Soybeans

• Wheat

• Cocoa

• Coffee

• Live cattle

Agriculture

3 Please see additional important information and qualifications at the end of this material.

Who are our clients ? The clientbase

Morgan Stanley Commodities

4

• We aim to maintain a broad

and diverse client base such

that our derivative business

reflects the underlying physical

reality

• Our shipping clients form part

of this broader market

coverage

• Risk management is a scale

business: the more flows you

have, the greater your ability to

manage risk effectively

Commodities Marketing Structure of our clientbase

CLIENTS

CORPORATES INVESTORS

PRODUCERS REFINERS CONSUMERS

• Airlines

• Shipping

• Bus & Rail

• Industrials

• Utilities

• Active (hedge funds)

• Passive (pension funds)

Please see additional important information and qualifications at the end of this material.

END USERS INTERMEDIARIES

0

20

40

60

80

100

120

140

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

Gulf

war

Increased Iraq production,

Asian economic crisis

OPEC production

cutbacks, strong

world demand

9/11 terrorist attack

Iraq

war

Hurricane

Katrina

Militant attacks

in Nigeria

Credit crisis

OPEC

cuts

output

Global Downturn

European

Sovereign

Debt Crisis

Unrest in

the Middle

East and

North

Africa

IEA /

SPR oil

release

Middle East

production

disruption

fears

Macro

economic

concerns

over Europe

Airlines & fuel risk management Some history

Morgan Stanley Commodities

Brent crude oil $/bbl

• Airlines’ adoption of active

risk management practices

has been driven by changes

in both the oil market and the

airline sector

• Key factors

– Airline ownership

– Development of derivative

markets

– Increased volatility and

inflation in commodity

prices

– Investors

5

Source Morgan Stanley Commodities Sales & Trading, Bloomberg

Please see additional important information and qualifications at the end of this material.

0%

10%

20%

30%

40%

50%

60%

70%

Q1-12 Q2-12 Q3-12 Q4-12 Q1-13 Q2-13 Q3-13 Q4-13 2014 2015 +

EMEA

0%

10%

20%

30%

40%

50%

60%

70%

Q1-13 Q2-13 Q3-13 Q4-13 Q1-14 Q2-14 Q3-14 Q4-14 2015 2016 +

EMEA

6

Morgan Stanley Commodities

EMEA Airlines Percentage of Consumption Hedged (2012 Survey) Average % of Consumption Hedged (1, 2)

Source Morgan Stanley 2013 Airline Survey

Source Morgan Stanley 2012 Airline Survey

EMEA Airlines Percentage of Consumption Hedged (2013 Survey) Average % of Consumption Hedged (1, 2)

Notes: 1. Responses to this question were provided as a range (0-10%, 11-20%, 21-30%, etc.) To plot this graph, responses were taken to be at the midpoint of each range, and averaged. Due to this methodology, total use across all instruments may not sum to 100%.

2. The responses are not weighted by airline consumption.

Please see additional important information and qualifications at the end of this material.

A snapshot of airlines’ fuel risk management activity

• Fuel risk management is now a

routine part of almost all

airlines’ corporate treasury

function

0% 10% 20% 30% 40% 50% 60%

Extendibles

Capped Swaps

Range Swaps

Ratio Collars

Puts

Call Spreads

3-ways

4-ways

Calls

Collars

Swaps

2011 Airline Survey 2012 Airline Survey 2013 Airline Survey

Consumer hedging instruments

7

Morgan Stanley Commodities

Choice of Instruments Used in Hedging Programme (1)

% Composition of Total Hedging Programme, Averaged Across Respondents (2)

Notes: 1. Responses to this question were provided as a range (0-10%, 11-20%, 21-30%, etc.) To plot this graph, responses were taken to be at the midpoint of each range, and averaged. Due to this methodology, total use across all instruments may not sum to 100%.

2. The responses are not weighted by airline consumption.

• Airlines use a broad variety of

instruments to hedge their risk

Source Morgan Stanley 2011 Airline Survey, Morgan Stanley 2012 Airline Survey, Morgan Stanley 2013 Airline Survey

Please see additional important information and qualifications at the end of this material.

How shipping companies compare A more complex picture

Morgan Stanley Commodities

8

• Certain sectors of the shipping

industry have very similar risk

profiles to airlines

• Only specific sectors have outright exposure to fuel prices:

– Container lines, chemical tankers, ferry operators, cruise operators, car carriers, some

charterers

– Often bunker costs will be managed via contractual terms

– Otherwise these sectors follow a similar pattern to airlines with some differences

– Activity is market price driven

• How shipping companies differ

– Risk management activity is more sporadic, less disciplined and less widely adopted

– Ownership important

– Risk culture

– Risk management as a “source of profit” vs “tool to reduce volatility”

How shipping companies compare II A more complex picture

Morgan Stanley Commodities

9

• Many sectors in shipping do not

have outright fuel risk but

―gross margin risk‖

• Some sectors of the freight market only have exposure to fuel associated with a particular

freight contract:

– Tankers, dry bulk

– Contracts of Affreightment

– Time charter equivalent paper trading

• Instruments generally very simple (just lock in the bunker price)

• Not market price driven – the driver is the fixing of freight contracts and COAs

• Also fixed price bunker contracts

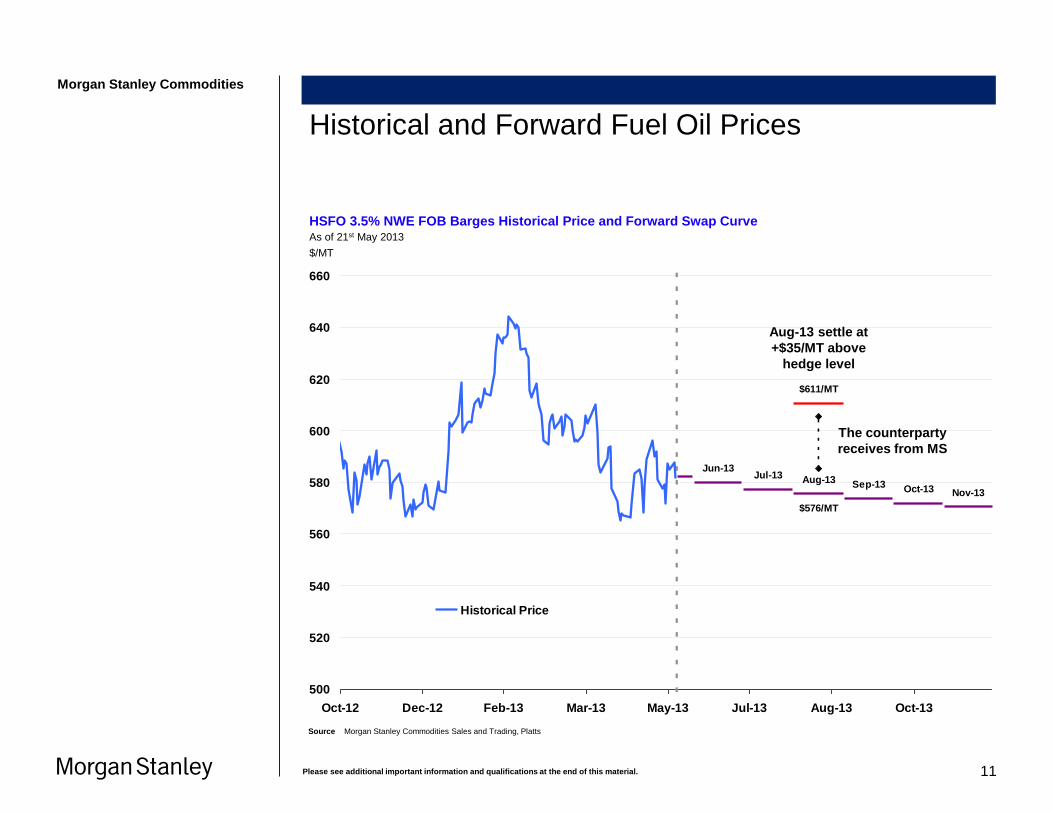

Historical and Forward Fuel Oil Prices

Morgan Stanley Commodities

10

HSFO 3.5% NWE FOB Barges Historical Price and Forward Swap Curve As of 21st May 2013

$/MT

Source Morgan Stanley Commodities Sales and Trading, Platts

Please see additional important information and qualifications at the end of this material.

Jun-13Jul-13 Aug-13 Sep-13 Oct-13 Nov-13

$576/MT

500

520

540

560

580

600

620

640

660

Oct-12 Dec-12 Feb-13 Mar-13 May-13 Jul-13 Aug-13 Oct-13

Historical Price

Jun-13Jul-13 Aug-13 Sep-13 Oct-13 Nov-13

$576/MT

$611/MT

500

520

540

560

580

600

620

640

660

Oct-12 Dec-12 Feb-13 Mar-13 May-13 Jul-13 Aug-13 Oct-13

Historical Price

Historical and Forward Fuel Oil Prices

Morgan Stanley Commodities

11

HSFO 3.5% NWE FOB Barges Historical Price and Forward Swap Curve As of 21st May 2013

$/MT

Source Morgan Stanley Commodities Sales and Trading, Platts

Please see additional important information and qualifications at the end of this material.

The counterparty

receives from MS

Aug-13 settle at

+$35/MT above

hedge level

Jun-13Jul-13 Aug-13 Sep-13 Oct-13 Nov-13

$576/MT

$551/MT

500

520

540

560

580

600

620

640

660

Oct-12 Dec-12 Feb-13 Mar-13 May-13 Jul-13 Aug-13 Oct-13

Historical Price

Historical and Forward Fuel Oil Prices

Morgan Stanley Commodities

12

HSFO 3.5% NWE FOB Barges Historical Price and Forward Swap Curve As of 21st May 2013

$/MT

Source Morgan Stanley Commodities Sales and Trading, Platts

Please see additional important information and qualifications at the end of this material.

MS receives from

the counterparty

Aug-13 settle at

-$25/MT below

hedge level

Morgan Stanley Commodities

13

Appendix A

Appendix

ICE Brent Historical Price

Morgan Stanley Commodities APPENDIX

14

ICE Brent Historical Price As of 21st May 2013

$/BBL

Source Morgan Stanley Commodities Sales and Trading, ICE

Please see additional important information and qualifications at the end of this material.

20

40

60

80

100

120

140

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13

ICE Brent

Fuel Oil & Gasoil Historical Price

Morgan Stanley Commodities APPENDIX

15

HSFO 3.5% NWE FOB Barges & ICE Gasoil Historical Price As of 21st May 2013

$/MT

Source Morgan Stanley Commodities Sales and Trading, ICE, Platts

Please see additional important information and qualifications at the end of this material.

0

200

400

600

800

1000

1200

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13

ICE Gasoil HSFO 3.5% NWE FOB Barges

Fuel Oil & Gasoil Cracks Historical Price

Morgan Stanley Commodities APPENDIX

16

HSFO 3.5% NWE FOB Barges & ICE Gasoil Cracks Historical Price As of 21st May 2013

$/BBL

Source Morgan Stanley Commodities Sales and Trading, ICE, Platts

Please see additional important information and qualifications at the end of this material.

-45

-35

-25

-15

-5

5

15

25

35

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13

ICE Gasoil Crack HSFO 3.5% NWE FOB Barges Crack

How is the market structured ? An example : oil derivatives flow

Morgan Stanley Commodities

EXCHANGES

• Highly liquid markets

• Liquidity concentrated

among a few products &

instruments

Crude Oil & Refined Products Sales & Trading Market Structure

TRADING

MARKETING

CORPORATES INVESTORS

• Producers

• Refiners

• Consumers

• Active

• Passive

• Retail

EXCHANGE TRADED

MARKET

Crude oil – Gasoil/ Heating Oil – Gasoline

Futures & Options

NYMEX / ICE

OTC MARKET

VOICE BROKERS

Banks / Traders / Majors OTC

• Large total size

• Liquidity fragmented into

many products &

instruments

10

15

Morgan Stanley Commodities

Swap for a Consumer

• Strategy

– A consumer buys a swap to

protect against escalating

prices

• A swap (or fixed for floating

contract) is the simplest

strategy for consumers to lock

in forward market prices

• Unlike an option, a swap does

not have an up-front premium

cost. A swap is a purely

financial transaction that

establishes a fixed price

• When market prices are higher

than the swap price, Morgan

Stanley pays the consumer the

difference (market price less

swap price)

• When market prices are lower

than the swap price, the

consumer pays Morgan Stanley

the difference (swap price less

market price)

6

Source Morgan Stanley Commodities

All units in $/bbl

Settlement for the swap:

Average price = 115, consumer’s P&L = 0

Average price < 115, consumer pays money

e.g. pays 2 at the price of 113

Average price > 115, consumer receives money

e.g. receives 2 at the price of 117

Consumer Buys a Swap

115

Price

Source Morgan Stanley Commodities

115

0

-2

2

113 117

P&L

$/bbl

Price

Morgan Stanley pays Consumer

Effective Price: Physical + Hedge

Market

Consumer pays Morgan Stanley

The information contained herein is not intended to be, and does not constitute, advice from Morgan Stanley. Morgan Stanley is not your advisor (municipal, financial or any other kind of

advisor) and is not acting in a fiduciary capacity. This information was prepared by Morgan Stanley sales, trading, banking or other non-research personnel. This is not a research report and

the views or information contained herein should not be viewed as independent of the interests of Morgan Stanley trading desks. To the extent any prices or price levels are noted, they are

for informational purposes only and are not intended for use by third parties, and are indicative as of the date shown and are not a commitment by Morgan Stanley to trade at any price.

Please see additional important information and qualifications at the end of this material.

Call for a Consumer

• Strategy

– A consumer buys a call to

guard against a rising market

price and to be able to

continue to take advantage

of stable or lower prices

• A call option gives the holder

the right (but not obligation) to

buy the underlying commodity

at a predetermined price by a

specified date

• The premium (price of the

option) is paid up front by

the option holder (consumer)

to the option grantor

(Morgan Stanley)

• With a call option, a consumer

protects himself against rising

prices by establishing a

maximum purchase price

• Unlike a swap, a call option

does not lock the consumer

into a fixed purchase price so

the consumer will participate in

falling prices

Morgan Stanley Commodities

11

All units in $/bbl

Settlement for the call:

Premium = 3.00

Average price ≤ 115, consumer receives 0

Consumer’s P&L = -3.00

Average price > 115, consumer receives money

e.g. consumer receives 7 for price of 122

but consumer’s P&L = 4.00

(7 less 3.00 premium)

115

Price

Effective Price: Physical + Hedge

Market

Morgan Stanley pays Consumer

Strike

Consumer Buys a Call

115 122

0

-3.00

4.00

P&L

$/bbl

Price

Source Morgan Stanley Commodities Source Morgan Stanley Commodities

The information contained herein is not intended to be, and does not constitute, advice from Morgan Stanley. Morgan Stanley is not your advisor (municipal, financial or any other kind of

advisor) and is not acting in a fiduciary capacity. This information was prepared by Morgan Stanley sales, trading, banking or other non-research personnel. This is not a research report and

the views or information contained herein should not be viewed as independent of the interests of Morgan Stanley trading desks. To the extent any prices or price levels are noted, they are

for informational purposes only and are not intended for use by third parties, and are indicative as of the date shown and are not a commitment by Morgan Stanley to trade at any price.

Please see additional important information and qualifications at the end of this material.

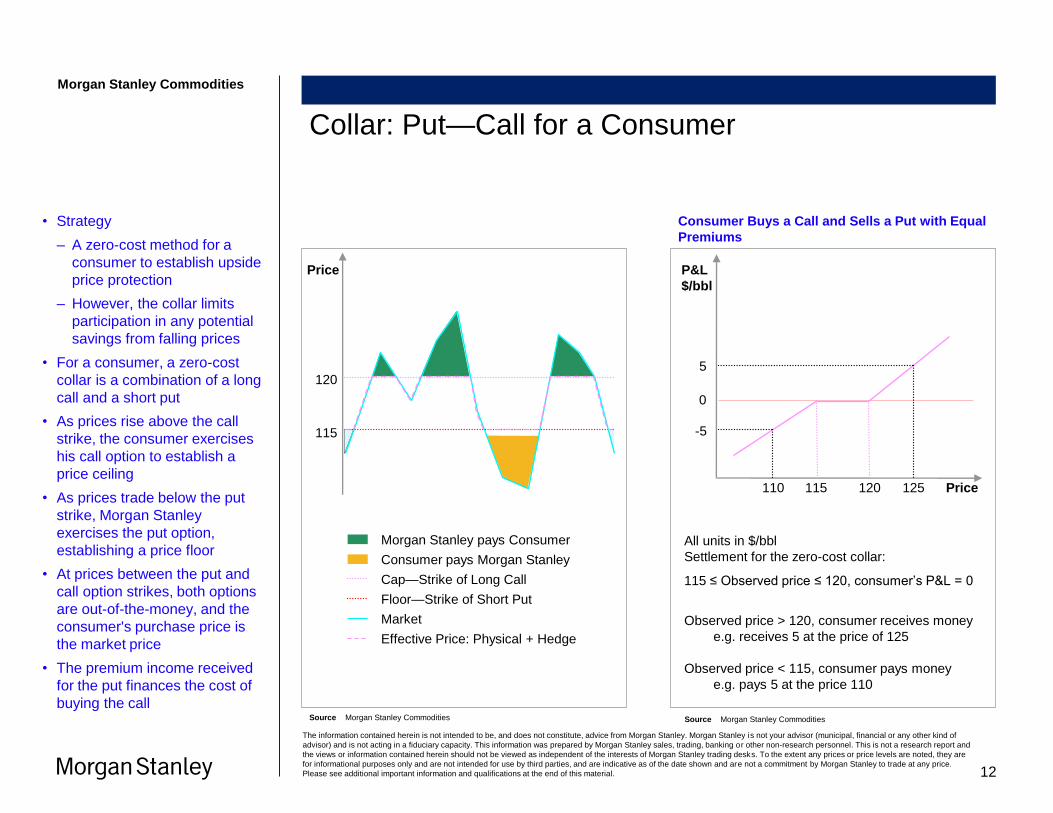

Collar: Put—Call for a Consumer

• Strategy

– A zero-cost method for a

consumer to establish upside

price protection

– However, the collar limits

participation in any potential

savings from falling prices

• For a consumer, a zero-cost

collar is a combination of a long

call and a short put

• As prices rise above the call

strike, the consumer exercises

his call option to establish a

price ceiling

• As prices trade below the put

strike, Morgan Stanley

exercises the put option,

establishing a price floor

• At prices between the put and

call option strikes, both options

are out-of-the-money, and the

consumer's purchase price is

the market price

• The premium income received

for the put finances the cost of

buying the call

Morgan Stanley Commodities

12

All units in $/bbl

Settlement for the zero-cost collar:

115 ≤ Observed price ≤ 120, consumer’s P&L = 0

Observed price > 120, consumer receives money

e.g. receives 5 at the price of 125

Observed price < 115, consumer pays money

e.g. pays 5 at the price 110

Source Morgan Stanley Commodities Source Morgan Stanley Commodities

Consumer Buys a Call and Sells a Put with Equal

Premiums

Price

115

120

Effective Price: Physical + Hedge

Market

Consumer pays Morgan Stanley

Morgan Stanley pays Consumer

Cap—Strike of Long Call

Floor—Strike of Short Put

115 120 Price 110 125

0

-5

5

P&L

$/bbl

The information contained herein is not intended to be, and does not constitute, advice from Morgan Stanley. Morgan Stanley is not your advisor (municipal, financial or any other kind of

advisor) and is not acting in a fiduciary capacity. This information was prepared by Morgan Stanley sales, trading, banking or other non-research personnel. This is not a research report and

the views or information contained herein should not be viewed as independent of the interests of Morgan Stanley trading desks. To the extent any prices or price levels are noted, they are

for informational purposes only and are not intended for use by third parties, and are indicative as of the date shown and are not a commitment by Morgan Stanley to trade at any price.

Please see additional important information and qualifications at the end of this material.

3-Way Collar: Put—Calls for a Consumer

• Strategy

– For a moderately bullish

consumer who does not

believe the price will rise

above a certain level

• A 3-way collar is a zero-cost

strategy in which a consumer

gives up some upside

protection to achieve a better

strike for the put the consumer

sold when compared to a

normal collar

• For a consumer, a zero-cost 3-

way collar includes a long call,

a short put, and a short call

Morgan Stanley Commodities

Put-call-call

Source Morgan Stanley Commodities Source Morgan Stanley Commodities

Consumer Buys a Call, Sells a Put, and Sells a

Call with Offsetting Premiums

All units in $/bbl Settlement for the 3-way collar: 115≤ Observed price ≤120, consumer’s P&L = 0 120 < Observed price ≤ 125, consumer receives money e.g. receives 5 at the price 125 Observed price < 115, consumer pays money e.g. pays 5 at the price of 110 Observed price > 125, consumer receives maximum 5; consumer is exposed to any further price increase

0

-5

115 120 Price

5

110 125

P&L

$/bbl

130

Price

115

120

125

Effective Price: Physical + Hedge

Market

Strike of Long Call

Floor—Strike of Short Put

Strike of Short Call

Morgan Stanley pays Consumer

Consumer pays Morgan Stanley

13

The information contained herein is not intended to be, and does not constitute, advice from Morgan Stanley. Morgan Stanley is not your advisor (municipal, financial or any other kind of

advisor) and is not acting in a fiduciary capacity. This information was prepared by Morgan Stanley sales, trading, banking or other non-research personnel. This is not a research report and

the views or information contained herein should not be viewed as independent of the interests of Morgan Stanley trading desks. To the extent any prices or price levels are noted, they are

for informational purposes only and are not intended for use by third parties, and are indicative as of the date shown and are not a commitment by Morgan Stanley to trade at any price.

Please see additional important information and qualifications at the end of this material.

APPENDIX

Disclaimer

Morgan Stanley Commodities

The information in this material was prepared by sales, trading, or other non-research personnel of Morgan Stanley for institutional investors. This is not a research report, and unless otherwise

indicated, the views herein (if any) are the author’s and may differ from those of our Research Department or others in the F irm. This material is not independent of the interests of our trading

and other activities, which may conflict with your interests. We may deal in any of the markets, issuers, or instruments mentioned herein before or after providing this information, as principal,

market maker, or liquidity provider and may also seek to advise issuers or other market participants.

Where you provide us with information relating to an order, inquiry, or potential transaction, we may use that information to facilitate execution and in managing our market making and hedging

activities.

This material does not provide investment advice or offer tax, regulatory, accounting, or legal advice. By submitting this document to you, Morgan Stanley is not your fiduciary, municipal, or any

other type of advisor.

This material is not based on a consideration of any individual client circumstances and thus should not be considered a recommendation to any recipient or group of recipients. This material is

an invitation to consider entering into derivatives transactions under CFTC Rules 1.71 and 23.605 (where applicable) but is not a binding offer to buy or sell any instrument or enter into any

transaction.

Unless otherwise specifically indicated, all information in these materials with respect to any third party entity not affiliated with Morgan Stanley has been provided by, and is the sole

responsibility of, such third party and has not been independently verified by Morgan Stanley, our affiliates or any other independent third party. We make no express or implied representation

or warranty with respect to the accuracy or completeness of this material, nor will we undertake to provide updated information or notify recipients when information contained herein becomes

stale.

Any prices contained herein are indicative only and should not be relied upon for valuation or for any use with third parties.

All financial information is taken from company disclosures and presentations (including 10Q, 10K and 8K filings and other public announcements), unless otherwise noted. Any securities

referred to in this material may not have been registered under the U.S. Securities Act of 1933, as amended and, if not, may not be offered or sold absent an exemption therefrom. In relation to

any member state of the European Economic Area, a prospectus may not have been published pursuant to measures implementing the Prospectus Directive (2003/71/EC) and any securities

referred to herein may not be offered in circumstances that would require such publication. Recipients are required to comply with any legal or contractual restrictions on their purchase, holding,

sale, exercise of rights, or performance of obligations under any instrument or otherwise applicable to any transaction. In addition, a secondary market may not exist for certain of the

instruments referenced herein.

The value of and income from investments may vary because of, among other things, changes in interest rates, foreign exchange rates, default rates, prepayment rates, securities, prices of

instruments or securities, market indexes, operational, or financial conditions of companies or other factors. There may be t ime limitations on the exercise of options or other rights in

instruments (or related derivatives) transactions. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be

realized. Actual events may differ from those assumed, and changes to any assumptions may have a material impact on any projections or estimates. Other events not taken into account may

occur and may significantly affect any projections or estimates. Certain assumptions may have been made for modeling purposes only to simplify the presentation or calculation of any

projections or estimates, and Morgan Stanley does not represent that any such assumptions will reflect actual future events or that all assumptions have been considered or stated. Accordingly,

there can be no assurance that any hypothetical estimated returns or projections will be realized or that actual returns or performance results will not materially differ. Some of the information

contained in this document may be aggregated data of transactions executed by Morgan Stanley that has been compiled so as not to identify the underlying transactions of any particular

customer.

This information is not intended to be provided to and may not be used by any person or entity in any jurisdiction where the provision or use thereof would be contrary to applicable laws, rules,

or regulations.

This communication is directed to and meant for sophisticated investors. Specifically, institutional investors in the U.S and those persons who are eligible counterparties or professional clients in

the U.K. It must not be re-distributed to or relied upon by retail clients.

This information is being disseminated in Hong Kong by Morgan Stanley Asia Limited and is intended for professional investors (as defined in the Securities and Futures Ordinance) and is not

directed at the public of Hong Kong. This information is being disseminated in Singapore by Morgan Stanley Asia (Singapore) Pte. This information has not been registered as a prospectus with

the Monetary Authority of Singapore. Accordingly, this information and any other document or material in connection with the offer or sale, or invitation for subscription or purchase, of this

security may not be circulated or distributed, nor may this security be offered or sold, or be made the subject of an invitation for subscription or purchase, whether directly or indirectly, to

persons in Singapore other than (i) to an institutional investor under Section 274 of the Securities and Futures Act, Chapter 289 of Singapore (the ―SFA‖), (ii) to a relevant person pursuant to

Section 275(1) of the SFA, or any person pursuant to Section 275(1A) of the SFA, and in accordance with the conditions, specified in Section 275 of the SFA or (iii) otherwise pursuant to, and in

accordance with the conditions of, any other applicable provision of the SFA. Any offering of this security in Singapore would be through Morgan Stanley Asia (Singapore) Pte, an entity

regulated by the Monetary Authority of Singapore.

This information is being disseminated in Japan by Morgan Stanley MUFG Securities Co., Ltd. Any securities referred to herein may not have been and/or will not be registered under the

Financial Instruments Exchange Law of Japan (Law No. 25 of 1948, as amended, hereinafter referred to as the ―Financial Instruments Exchange Law of Japan‖). Such securities may not be

offered, sold, or transferred, directly or indirectly, to or for the benefit of any resident of Japan unless pursuant to an exemption from the registration requirements of and otherwise in compliance

with the Financial Instruments Exchange Law and other relevant laws and regulations of Japan. As used in this paragraph, ―res ident of Japan‖ means any person resident in Japan, including

any corporation or other entity organized or engaged in business under the laws of Japan. If you reside in Japan, please contact Morgan Stanley MUFG Securities for further details at +613-

5424-5000.

This information is distributed in Australia by Morgan Stanley Australia Limited A.B.N. 67 003 734 576, holder of Australian financial services license No. 233742, which accepts responsibility

for its contents, and arranges for it to be provided to potential clients. In Australia, this report, and any access to it, is intended only for "wholesale clients" within the meaning of the Australian

Corporations Act.

For additional information, research reports, and important disclosures see https://secure.ms.com/servlet/cls. The trademarks and service marks contained herein are the property of their

respective owners. Third-party data providers make no warranties or representations of any kind relating to the accuracy, completeness, or timeliness of the data they provide and shall not have

liability for any damages of any kind relating to such data.

This material may not be redistributed without the prior written consent of Morgan Stanley.

© 2013 Morgan Stanley

17

![MARINE NH3 Ammonia as Marine Fuel · 2019. 12. 11. · MARINE NH3 Renewable Fuel Options Fuel type: Energy density LHV [MJ/kg] Volumetric energy density LHV [GJ/m3] Renewable synthetic](https://img.pdfslide.net/doc/110x75/5fdbecb9167767355544431e/marine-nh3-ammonia-as-marine-fuel-2019-12-11-marine-nh3-renewable-fuel-options.jpg)