Embed Size (px)

Citation preview

FURNMART LIMITED ANNUAL REPORT

3Furnmart Annual Report 2018 3Furnmart Annual Report 2018

IN THIS REPORT

WHO WE ARE

5 GROUP PROFILE5 MISSION STATEMENT

CONTENTS

CHAPTER 016-7 BRIEF PROFILE OF DIRECTORS

CHAPTER 028-9 MANAGEMENT REPORT

CHAPTER 03 10-11 DIRECTORS’ REPORT

CHAPTER 04 12 CORPORATE GOVERNANCE

13-18 REPORT OF THE INDEPENDENT AUDITOR

CHAPTER 05

ANNUAL FINANCIAL STATEMENTS19 CONSOLIDATED AND SEPARATE STATEMENTS OF COMPREHENSIVE INCOME

20 CONSOLIDATED AND SEPARATE STATEMENTS OF FINANCIAL POSITION

21 CONSOLIDATED AND SEPARATE STATEMENTS OF CHANGES IN EQUITY

22 CONSOLIDATED AND SEPARATE STATEMENTS OF CASH FLOWS

23-34 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

35-36 CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENTS

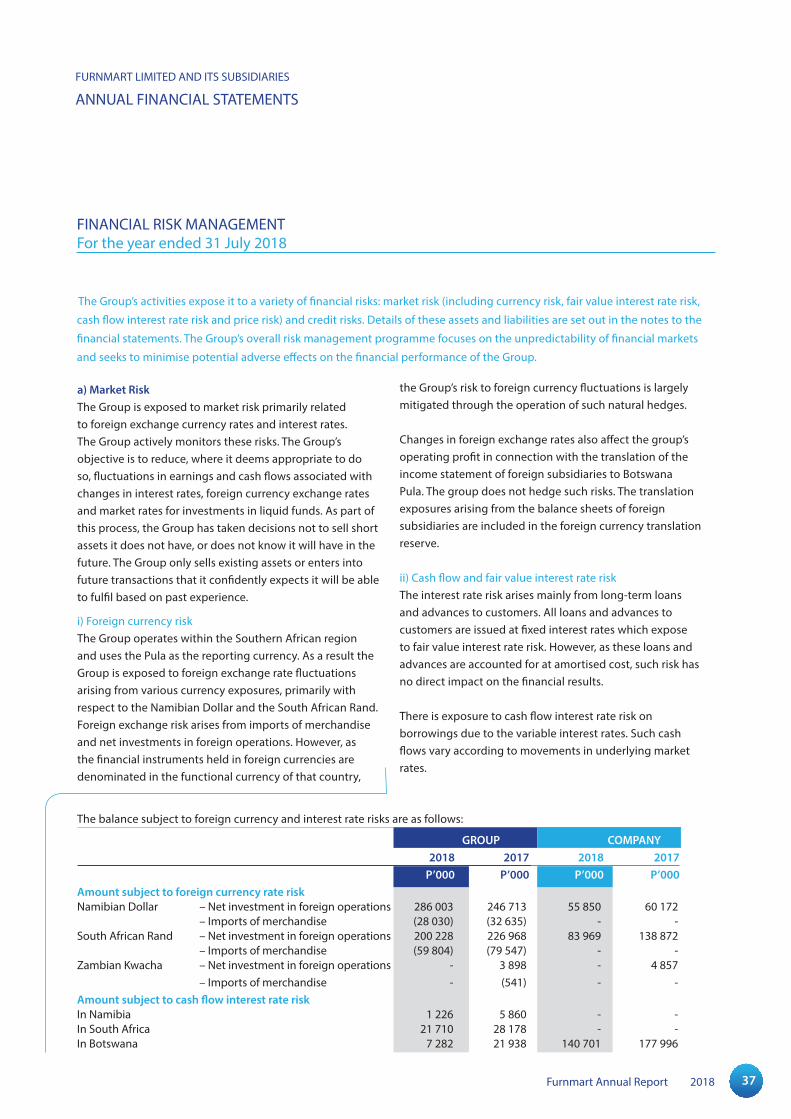

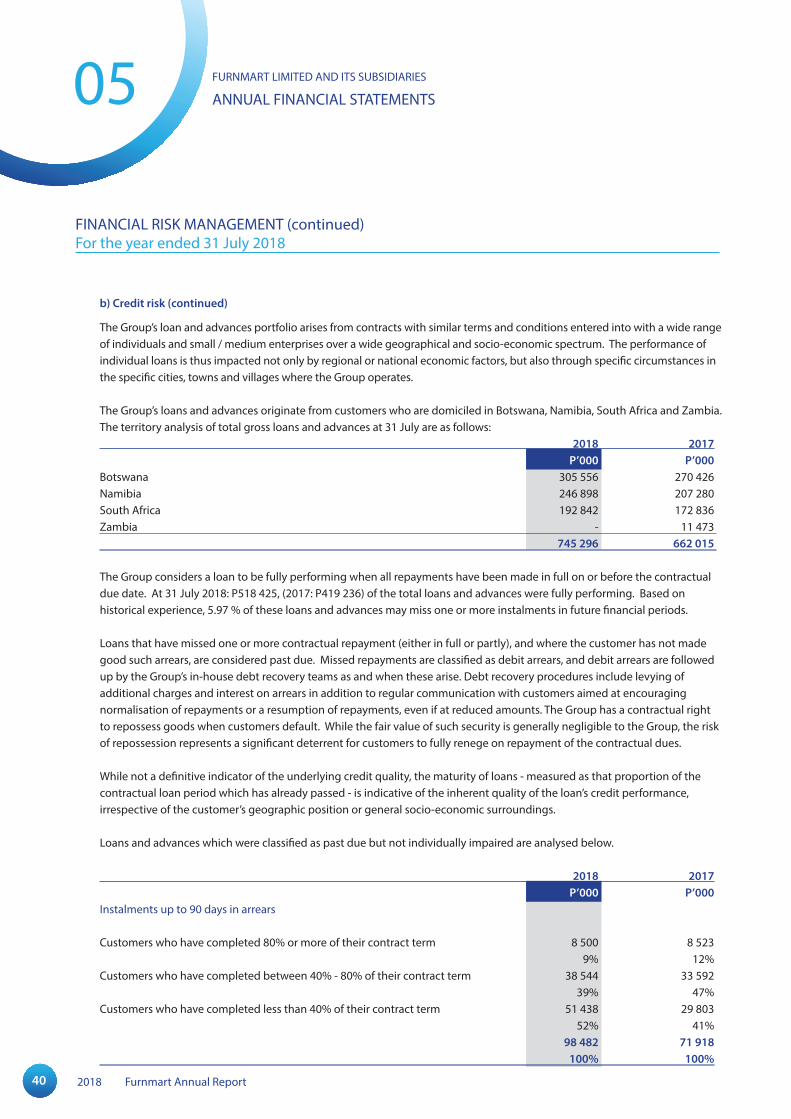

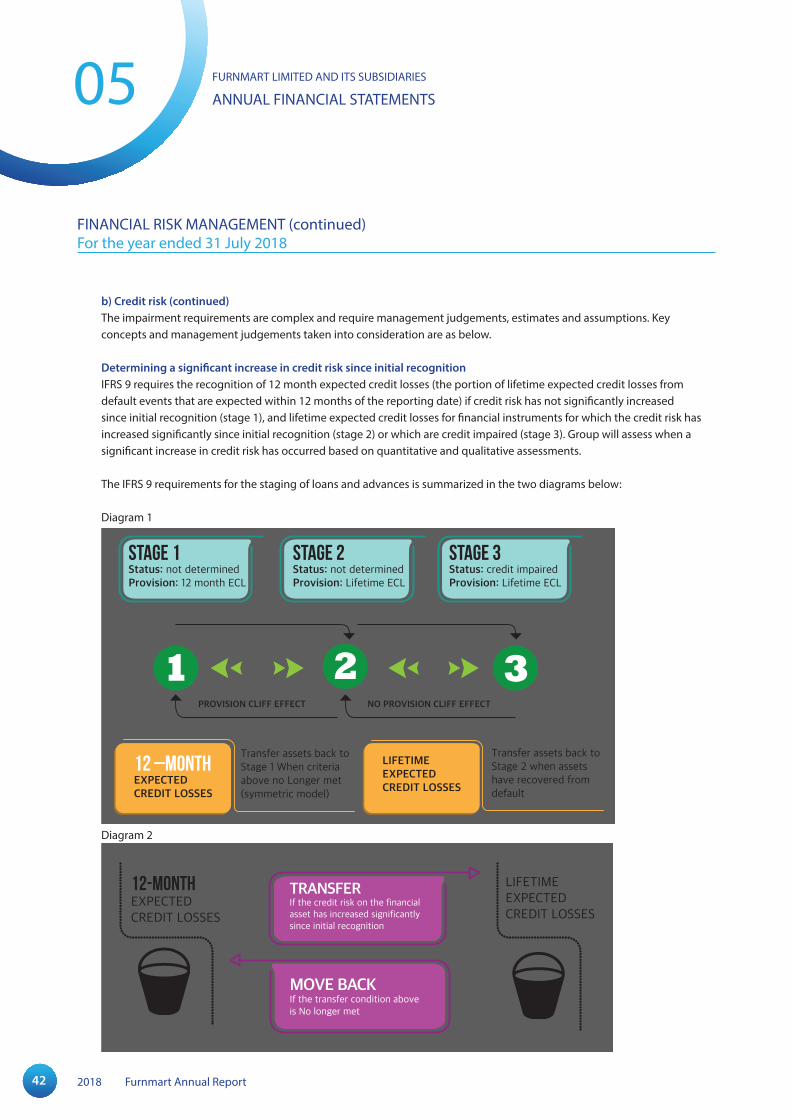

37-46 FINANCIAL RISK MANAGEMENT

47-63 NOTES TO THE ANNUAL FINANCIAL STATEMENTS

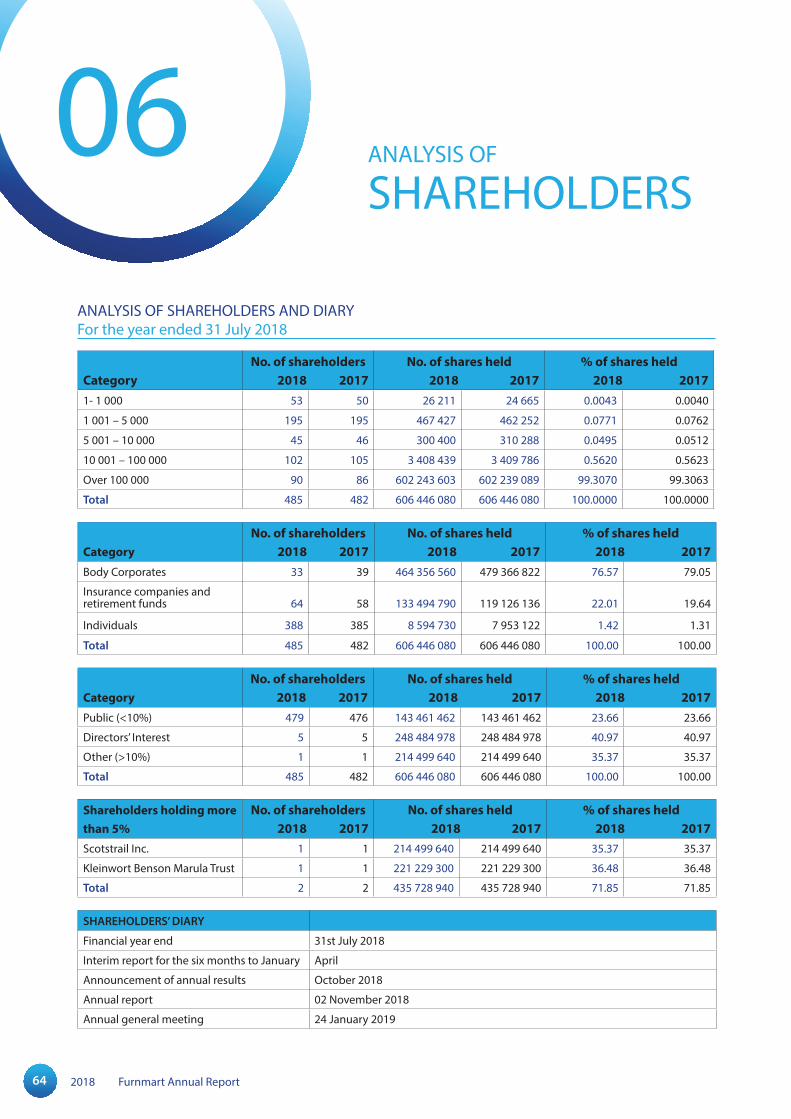

CHAPTER 06 64 SHAREHOLDERS’ ANALYSIS AND DIARY

CHAPTER 07 65 SHARE STATISTICS

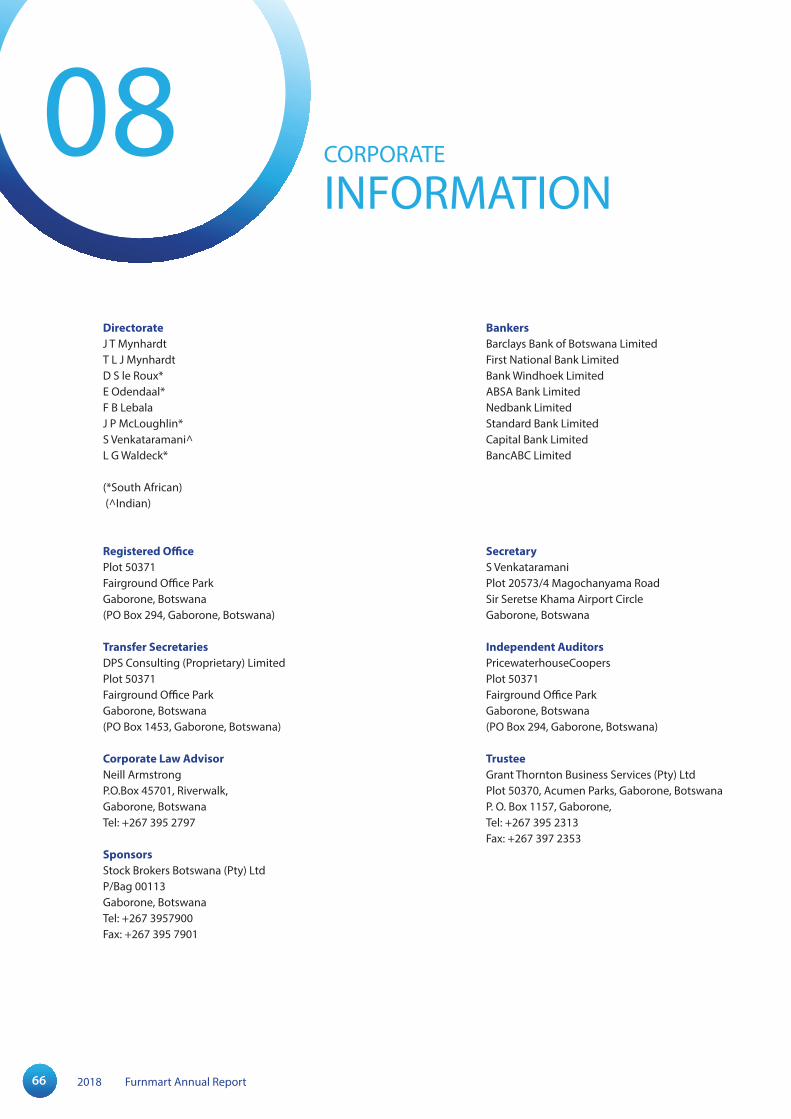

CHAPTER 08 66 CORPORATE INFORMATION

CHAPTER 09 67 NOTICE OF THE ANNUAL GENERAL MEETING

CHAPTER 10 LOOSE PROXY FORM

4 2017 Furnmart Annual Report

5Furnmart Annual Report 2018 5Furnmart Annual Report 2018

GROUP PROFILE

Furnmart Limited retails domestic furniture and

electrical appliances through its network of stores

in Botswana, South Africa and Namibia. It aims

at the majority of households in its market and

concentrates on cultivating relationships with its

customers through its ‘value for money’ and ‘smart

credit’ policies. Furnmart Limited is listed on the

Botswana Stock Exchange.

MISSION STATEMENT • Wearedeterminedtobethemarketleaderinretailing‘value

for money’ furniture and electrical appliances

• Wewillachievethisby:

» offering service excellence to all our partners, customers,

staff, suppliers and shareholders;

» valuing our people and helping them to become the best;

» constantly adapting to market needs and opportunities;

and

» working as a team and encouraging the free flow of

information and ideas.

WHOWEARE

01

6 2018 Furnmart Annual Report

John Tobias MynhardtChairman [B. Comm (UCT)]

After completing his Bachelor of Commerce degree at the University of Cape Town in

1968, John Mynhardt started work in the family trading store in Francistown. He has

remained involved in the Botswana retail industry ever since. During this time he has

developed extensive business interests in Botswana and he remains actively involved

as chairman of all the companies in the Cash Bazaar Holdings Group as well as and

including Furnmart Limited and the companies in the group’s Tourism and Hospitality

division. During his career he has served as a member of the Francistown Town

Council, the Boards of the Botswana Housing Corporation and First National Bank of

Botswana. He is currently a member of the University of Botswana Council.

Tobias Louis John Mynhardt Deputy Chairman [B.Comm (Hons-UCT) MSc Econ(LSE)]

Tobias Mynhardt is the Deputy Chairman of the CBH Group which has investments

in a number of industries including property, retail, tourism, hospitality, building

manufacturing and supplies and financial services. He has assumed responsibility for

various CBH Group divisions since being appointed a director in 2003. Mr Mynhardt

assisted with the listing of Furnmart in 1998 and joined the management team in

2006. He was appointed Deputy Managing Director of Furnmart in 2007 and was

Managing Director from 2009 until his appointment as Deputy Chairman in 2016.

Mr Mynhardt led the 2011 listing of New African Properties Limited and has been

Managing Director of this associated company since. Mr Mynhardt’s early career

encompassed a broad exposure to the investment industry through an investment

advisory and fund of hedge funds firm in London, following the completion of

his Masters in Economics from the London School of Economics. In 2016 he was

appointed to the board of Barclays Bank of Botswana Limited as a Non Executive

Director.

DanielServaasleRoux:ManagingDirector[B.Com (Hons- UJ) (Financial Management), M.Com (Business Management), ACMA]

Serniel le Roux has more than 22 years’ experience in the furniture retail industry

and joined the Furnmart Group in 2011. His experience includes statutory reporting,

financial accounting, management accounting, treasury, micro-lending and general

management. Serniel has extensive knowledge of Southern African furniture retail

markets. He was appointed as Managing Director in July 2016.

BRIEF PROFILE OF

DIRECTORS

7Furnmart Annual Report 2018

Fact Badzile LebalaNon Executive Director

Fact Lebala left the Botswana Police Force after 28 years’

of service with the rank of Superintendent of Police and

was awarded the Police Medal for Long Service and Good

Conduct. During this career he was Commanding Officer for

all the major Police Districts in Botswana and was attached

to Scotland Yard in London for nine months. He has retired

from the CBH group after serving as a director in the group

for over 28 years. He continues to be a board member in

Furnmart Limited.

Leonard Godfrey WaldeckIndependent, Non Executive Director [Dip.Acc]

Len Waldeck has a Diploma in Accounting from Rhodes

University (PE) & served his articles with Starling, Treasure,

Blake and Company in Port Elizabeth. He has more than

23 years of experience in the furniture retail industry in

credit, finance and retail operations. He has served in

several different capacities, such as Financial Director,

Group Credit Director & Joint Managing Director, with the

Beares, McCarthy Retail, Relyant & Ellerines Groups until his

retirement in 2007. He is also a member of the Institute of

Directors, South Africa.

Jerome Patrick McLoughlinIndependent, Non Executive Director [B.Com, Dip Acc (Natal), CA(SA)]

Jerome McLoughlin is a qualified Chartered Accountant

and completed articles with Deloitte (Durban). He started

a career in public audit practice and currently serves as a

director of a firm of registered auditors known as Hodkinson

Inc. He also serves as a non-executive director to companies

and as trustee on a number of trusts. He has substantial

experience in an advisory capacity and in property

investment.

Subbarao VenkataramaniNon Executive Director [B.Com, ACA, ACS]

Subbarao Venkataramani qualified as a Chartered

Accountant in 1978. He has more than 39 years of

experience in financial management, treasury and

accounting as head of finance in various listed companies.

He joined Furnmart in May, 1998 as Group Financial

Manager. He became Chief Financial Officer of Furnmart

Group in 2007. He was fully involved in the implementation

of Argility Furniture Retail operations and information

systems and involved in the issue and listing of rights shares

and bonds. He was appointed as the Finance Director on

15 August 2011 and he continued till 12 July 2016 when he

relinquished his position as head of finance. He continues

to be a board member in Furnmart Limited and is currently

responsible for secretarial and compliance matters. He is also

overseeing the microlending activities of CBH Group.

Eric OdendaalDirector Operations

Eric Odendaal joined Furnmart in August 1997 as Group

Operations Manager. He has overseen the expansion of the

business in Botswana and RSA and is fully involved in the

opening of Home Corp Stores in both these countries. He

has more than 40 years of experience in the furniture retail

industry. He is responsible for the day to day operations

of Furnmart and Home Corp stores in Botswana and South

Africa.

8 2018 Furnmart Annual Report

02 MANAGEMENT

REPORT

OVERVIEW

Trading was strong in this first half of the financial year

but considerably weaker since the half year. Of concern, in

general, is that this weakening trend has continued into the

new financial year.

This was the first full financial year subsequent to closing

the Group’s Zambian operations. The main reason for the

improvement in Group results stemmed from the elimination

of the material losses that the Group previously incurred in

Zambia. All activities in the Zambian operations, including

the collection of the debtor’s book, have been shut down.

Management’s continued focus on productivity and gross

profit margins has contributed to the improvement in profits

too.

The Group’s store base grew steadily during the last 12

months. Limited opportunities exist for expansion in

Botswana and Namibia. The subdued economic climate in

Namibia is continuing longer than anticipated. The Group

will adopt a cautious approach to expansion in South Africa

given pending regulatory changes.

TRADING AND FINANCIAL PERFORMANCE

The Group has finally returned to double digit return on

investment after a few years of single digit returns. The

12 months to July 2018 has seen an improvement in the

Group’s results but mainly due to the closure of our Zambian

operations.

The Group experienced a marked downturn in trading since

early 2018. As a result, the second half of the year was much

less buoyant than the first six months.

Revenue of P1.25 billion for the year ended July 2018, was

P72.0m (6.1%) higher than the prior year. On a comparable

basis, revenue increased by 11.3%, as the prior year included

revenue from some of the non-performing business units

that were closed.

Gross profit margins increased compared to last year, but the

prior year comparable figures included the low margin sales

of the non-performing operations, whilst closing them down.

Operating income of P185.8m was P55.6m (42.7%) higher

than last year. This improvement in operating income is the

result of the closing down of some of the Group’s non-

performing business units; as well as increased revenue and

gross profit margins. Growth in operating expenses was kept

at levels below inflation on a comparable basis.

Total debtors’ costs have increased by 55.6% during the

period under review. The increase is as a result of the growth

in the debtors’ book and slowdown in Namibia and South

Africa. The impairment provision, management believes, is at

a satisfactory level.

The Pula strengthened marginally against the Rand during

the financial year. As a result, the Group realised an exchange

loss of P1.4m compared to an exchange gain of P10.6m in

the prior year. However, subsequent to year-end the Pula has

strengthened considerably against the Rand. The volatility

and weakness of the Rand bring uncertainty and risk to the

Group’s earnings.

Profit after tax of P107.9m is P43.4m (67.2%) higher than the

previous year.

Cash generated from operations has declined by P26.8m

mainly due to an increase in credit sales, resulting in the

growth of the Group’s debtor’s book.

9Furnmart Annual Report 2018

STORE FOOTPRINT

The Group opened nine new Furnmart stores during the

period under review and is now trading out of 129 stores

in three countries. Store growth during the period under

review came from all three countries where the Group

trades. Total number of stores is weighted slightly towards

Botswana but the portfolio is increasingly more balanced

geographically.

OUTLOOK

Trading during the first couple of months of the new

financial year has been sluggish. Namibia in particular

is finding trading conditions difficult and achieving real

sales growth remains a challenge. The Namibian economy

has contracted on the back of the Government’s austerity

measures.

The Group’s remaining non-performing stores will continue

to attract further focus from management in an attempt

to turn them around. In addition, management will put

emphasis on the respective business models and specifically

on sales growth, gross margin maintenance, expense

control, productivity and debtor’s management.

The impact of the draft National Credit Amendment Bill

in South Africa, which proposes that all or part of the

debt under certain qualifying credit agreements can be

extinguished, is likely to have far reaching consequences

for credit providers. This amendment bill is of great concern

as most of the Group’s South African customers fall in the

income bracket that this legislation is targeting.

The furniture retail market in Botswana and Namibia

remains overtraded and imminent sweeping regulatory

changes, in these markets, may present future headwinds.

Given the concerns as highlighted above, the Group’s

strategy is to be cautious with new store openings,

particularly in South Africa.

10 2018 Furnmart Annual Report

03NATURE OF BUSINESS

Furnmart Limited retails domestic furniture and electrical appliances through its network

of stores in Botswana, Namibia and South Africa. The merchandise mix at mass-market

Furnmart stores is aimed at the middle to lower income market, thus covering the majority

of the population. The Group’s HomeCorp super stores, located in Gaborone, Windhoek,

Swakopmund, Boksburg and Kempton Park are aimed at the middle to higher income

market. Furnmart Limited strives to establish lasting relationships with its customers

through its ‘value for money’ and ‘smart credit’ policies.

SHARE CAPITAL

Theissuedsharecapitalofthecompanyis606446080(2017:606446080)shares.

DIVIDEND

A gross interim dividend of 3.44 thebe per share was paid to the shareholders who were

registered as at 11 May 2018. A gross final dividend of 2.49 thebe per share has been

proposed to be paid to the shareholders registered in the books of the company as at

16 November 2018.

Dividends are subject to withholding tax in accordance with the Botswana Income Tax Act.

SUBSIDIARY COMPANIES

The Group’s shareholdings in the issued share capital of the subsidiary companies are as

follows:

Company Countryheld

Percentage Nature ofbusiness

Furn Mart (Proprietary) Limited Namibia 100% Furniture retail

Xtreme Discounters (Proprietary) Limited South Africa 100% Furniture retail

Furniture Mart (Proprietary) Limited Botswana 100% Furniture retail

Furnmart (Proprietary) Limited South Africa 100% Distribution and shared services

DIRECTORS

REPORT

The Directors have

pleasure in submitting

their report for the

financial year ended

31 July 2018.

11Furnmart Annual Report 2018

DIRECTORS’ INTERESTS The aggregate number of shares directly held by the directors was 1 127 685 at 31 July 2018 and 1 027 685 at 31 July 2017. Directors indirectly held 26 159 080 shares at 31 July 2018 and 26 159 080 shares at 31 July 2017.

DIRECTORS’ REMUNERATIONThe independent directors are paid for meetings attended and these fees amountedtoP353656(2017:P359250)fortheyear.Otherdirectorsincludingthose on contract to the Group from Cash Bazaar Holdings (Pty) Ltd, a related company,earnedremunerationofP7417657(2017:P6561158)fromtheGroup.

COMPANY SECRETARYThe Company Secretary is S. Venkataramani.

APPROVAL OF FINANCIAL STATEMENTSThe Directors of Furnmart Limited are responsible for the preparation, integrity and objectivity of the financial statements and other information contained in this annual report, which has been prepared in accordance with International Financial Reporting Standards and in the manner required by Botswana Companies Act (2003) and the Group’s policies and procedures.

The directors are also responsible for the Company and its subsidiaries’ systems of internal financial control. Nothing has come to the attention of the directors to indicate that any material breakdown in the functioning of these controls, procedures and systems has occurred during the year under review.

The directors have reviewed the Group’s financial projections for the year ending 31 July 2019 and are satisfied that the company and its subsidiaries have adequate resources in place to continue in operation for the foreseeable future. The financial statements have therefore been prepared on the going concern basis.

The Board of Directors approved the annual financial statements presented on pages 19 to 63 on 25 October 2018.

EVENTS AFTER THE REPORTING PERIODSubsequent to the year end the Board took to a decision to seek a delisting of the Company’s shares from quotation and trade on the BSE. The notice of the Extraordinary General Meeting in this regard is set out in the announcement released on 31 October 2018 and a circular will be dispatched to shareholders on 3 November 2018. As a result of this, and subject to shareholder approval, the Company will make an offer to shareholders to repurchase shares from shareholders who wish to exit the Company (the “Offer”). The company has adequate facilities in place to meet the maximum consideration that could be payable as a result of the Offer.

On behalf of the Board

D S le Roux T L J Mynhardt Managing Director Deputy Chairman

DIRECTORSThe following directors served on the Board duringtheyear:J T Mynhardt (Chairman)T L J Mynhardt (Deputy Chairman) D S le Roux* (Managing Director) E Odendaal*F B LebalaJ P McLoughlin* S Venkataramani^ L G Waldeck*

* South African, ^Indian

As per article 53 and 55 of the Articles of Association of the company, the following directors will retire at the forthcoming annual general meeting and, being eligible, offerthemselvesforre-election:

D S le RouxJ P McLoughlin S Venkataramani

12 2018 Furnmart Annual Report

04In accordance with international developments, the Group is committed to the underlying principles as set out in the King III Report on corporate governance.

BOARD OF DIRECTORSThe day-to-day operations of the Group is vested in the executive management, while the Group Executive Management Committee and Board meet periodically to review and decide on strategy, risk, compliance and corporate affairs.

The Board meets at least three times per annum. While the Board strives to have full attendance at meetings, the quorum is any four directors and board papers are distributed timeously to enable members to be properly briefed prior to meetings. Directors who are unable to attend a meeting receive the relevant documents and are able to communicate with the Chairman and Company executives on any issue.

FINANCIAL CONTROLSInternal controls and systems are in place in the Group and are designed to provide reasonable assurance as to the integrity and reliability of the financial statements. These controls are regularly reviewed by the Board and management.

RISK, AUDIT AND COMPLIANCE COMMITTEEThe Group has a Risk, Audit and Compliance Committee which reports to the Board of Directors on the effectiveness of internal controls and management control systems. The committee ensures the effective assessment of all significant risks affecting the achievement of the missions and objectives of the Group. The committee also monitors compliance with BSE Listing requirements, adherence to International Financial Reporting Standards, corporate governance, Companies Act, adequacy of debtors’ impairment and other applicable legislation.

The Risk, Audit and Compliance Committee chaired by an independent Director meets at least twice a year and includes experts with sufficient financial literacy so as to enable the effectiveness of the Board sub-committee. The Chief Finance Officer, IT Executive and the external auditors attend the meeting by invitation.

The Committee met thrice during the year.

CODE OF ETHICSAll employees of the Group are required to maintain high ethical standards, ensuring that the Group conducts its business in a proper and professional manner.

D S le Roux T L J Mynhardt Managing Director Deputy Chairman

CORPORATE

GOVERNANCE

13Furnmart Annual Report 2018 13

PricewaterhouseCoopers, Plot 50371, Fairground Office Park, Gaborone, P O Box 294, Gaborone, Botswana T: (267) 395 2011, F: (267) 397 3901, www.pwc.com/bw Country Senior Partner: B D Phirie Partners: R Binedell, A S Edirisinghe, L Mahesan, R van Schalkwyk, S K K Wijesena

Independent auditor’s report To the Shareholders of Furnmart Limited

Report on the audit of the consolidated and separate financial statements Our opinion In our opinion, the consolidated and separate financial statements give a true and fair view of the consolidated and separate financial position of Furnmart Limited (the “Company”) and its subsidiaries (together the “Group”) as at 31 July 2018, and its consolidated and separate financial performance and its consolidated and separate cash flows for the year then ended in accordance with International Financial Reporting Standards (“IFRS”).

What we have audited

Furnmart Limited’s consolidated and separate financial statements set out on pages 19 to 63 comprise:

● the consolidated and separate statements of financial position as at 31 July 2018;

● the consolidated and separate statements of comprehensive income for the year then ended;

● the consolidated and separate statements of changes in equity for the year then ended;

● the consolidated and separate statements of cash flows for the year then ended; and

● the notes to the financial statements, which include a summary of significant accounting policies.

Basis for opinion We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the consolidated and separate financial statements section of our report.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Independence We are independent of the Group in accordance with the Botswana Institute of Chartered Accountants’ Code of Ethics (the “BICA Code”) and the ethical requirements that are relevant to our audit of financial statements in Botswana. We have fulfilled our other ethical responsibilities in accordance with these requirements and the BICA Code. The BICA Code is consistent with the International Ethics Standards Board for Accountants’ Code of Ethics for Professional Accountants (Parts A and B).

14 2018 Furnmart Annual Report

2 of 7

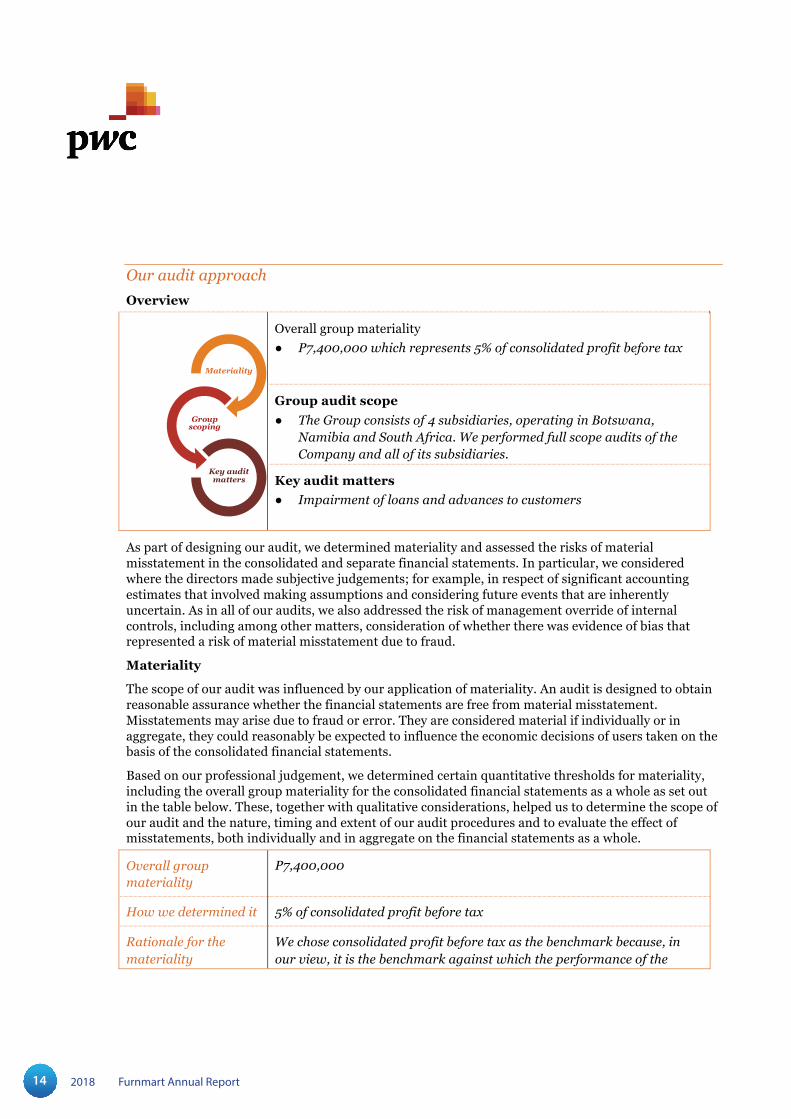

Our audit approach Overview

Overall group materiality ● P7,400,000 which represents 5% of consolidated profit before tax

Group audit scope ● The Group consists of 4 subsidiaries, operating in Botswana,

Namibia and South Africa. We performed full scope audits of the Company and all of its subsidiaries.

Key audit matters ● Impairment of loans and advances to customers

As part of designing our audit, we determined materiality and assessed the risks of material misstatement in the consolidated and separate financial statements. In particular, we considered where the directors made subjective judgements; for example, in respect of significant accounting estimates that involved making assumptions and considering future events that are inherently uncertain. As in all of our audits, we also addressed the risk of management override of internal controls, including among other matters, consideration of whether there was evidence of bias that represented a risk of material misstatement due to fraud.

Materiality

The scope of our audit was influenced by our application of materiality. An audit is designed to obtain reasonable assurance whether the financial statements are free from material misstatement. Misstatements may arise due to fraud or error. They are considered material if individually or in aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of the consolidated financial statements.

Based on our professional judgement, we determined certain quantitative thresholds for materiality, including the overall group materiality for the consolidated financial statements as a whole as set out in the table below. These, together with qualitative considerations, helped us to determine the scope of our audit and the nature, timing and extent of our audit procedures and to evaluate the effect of misstatements, both individually and in aggregate on the financial statements as a whole.

Overall group materiality

P7,400,000

How we determined it 5% of consolidated profit before tax

Rationale for the materiality

We chose consolidated profit before tax as the benchmark because, in our view, it is the benchmark against which the performance of the

Materiality

Group scoping

Key audit matters

15Furnmart Annual Report 2018

3 of 7

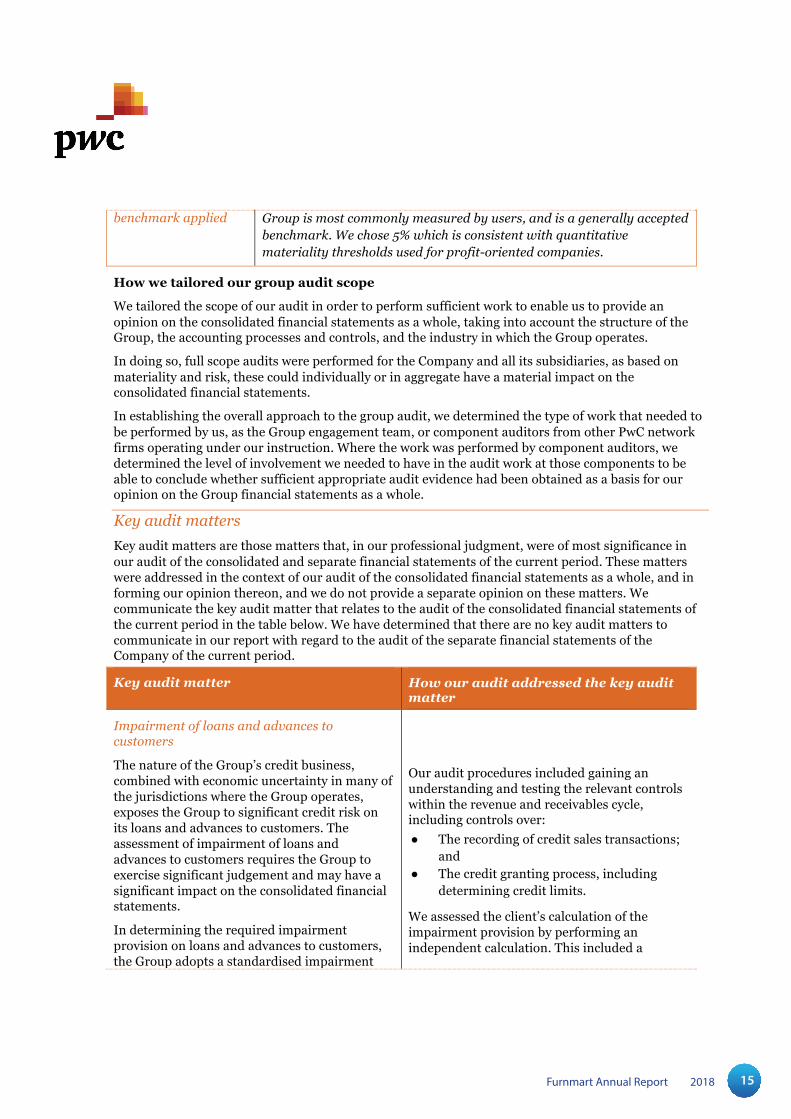

benchmark applied Group is most commonly measured by users, and is a generally accepted benchmark. We chose 5% which is consistent with quantitative materiality thresholds used for profit-oriented companies.

How we tailored our group audit scope

We tailored the scope of our audit in order to perform sufficient work to enable us to provide an opinion on the consolidated financial statements as a whole, taking into account the structure of the Group, the accounting processes and controls, and the industry in which the Group operates.

In doing so, full scope audits were performed for the Company and all its subsidiaries, as based on materiality and risk, these could individually or in aggregate have a material impact on the consolidated financial statements.

In establishing the overall approach to the group audit, we determined the type of work that needed to be performed by us, as the Group engagement team, or component auditors from other PwC network firms operating under our instruction. Where the work was performed by component auditors, we determined the level of involvement we needed to have in the audit work at those components to be able to conclude whether sufficient appropriate audit evidence had been obtained as a basis for our opinion on the Group financial statements as a whole.

Key audit matters Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated and separate financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. We communicate the key audit matter that relates to the audit of the consolidated financial statements of the current period in the table below. We have determined that there are no key audit matters to communicate in our report with regard to the audit of the separate financial statements of the Company of the current period.

Key audit matter How our audit addressed the key audit matter

Impairment of loans and advances to customers

The nature of the Group’s credit business, combined with economic uncertainty in many of the jurisdictions where the Group operates, exposes the Group to significant credit risk on its loans and advances to customers. The assessment of impairment of loans and advances to customers requires the Group to exercise significant judgement and may have a significant impact on the consolidated financial statements.

In determining the required impairment provision on loans and advances to customers, the Group adopts a standardised impairment

Our audit procedures included gaining an understanding and testing the relevant controls within the revenue and receivables cycle, including controls over: ● The recording of credit sales transactions;

and ● The credit granting process, including

determining credit limits.

We assessed the client’s calculation of the impairment provision by performing an independent calculation. This included a

16 2018 Furnmart Annual Report

4 of 7

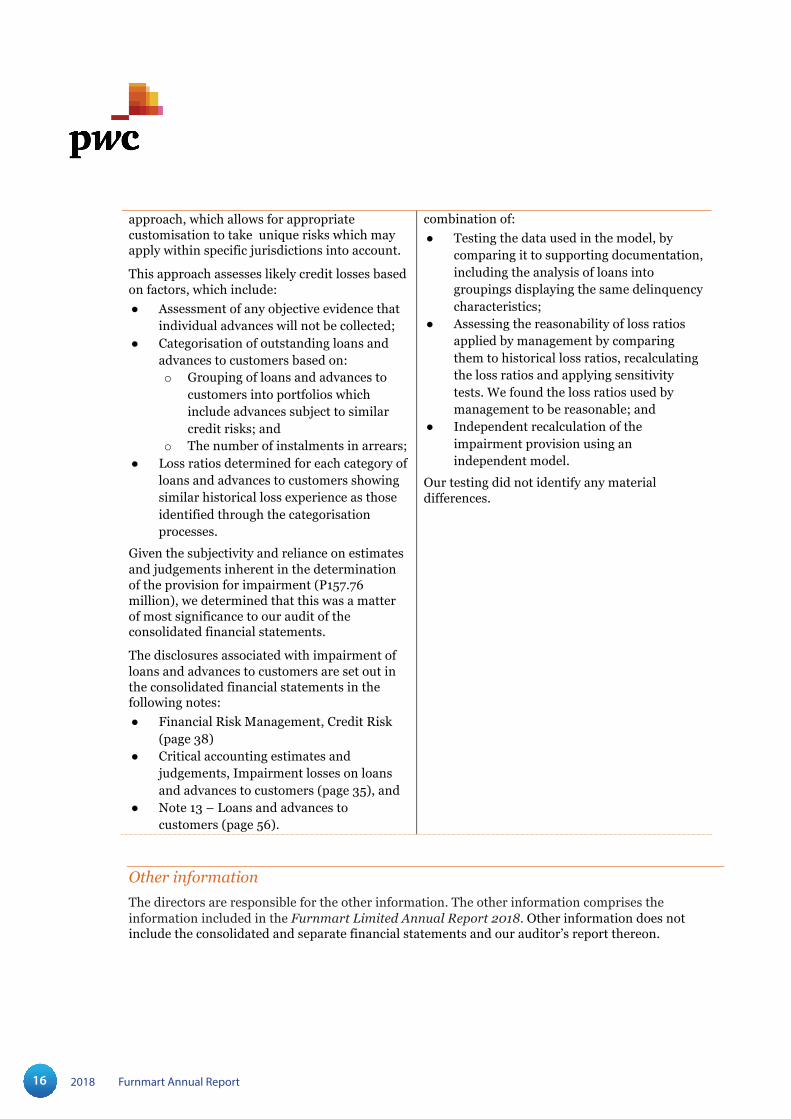

approach, which allows for appropriate customisation to take unique risks which may apply within specific jurisdictions into account.

This approach assesses likely credit losses based on factors, which include: ● Assessment of any objective evidence that

individual advances will not be collected; ● Categorisation of outstanding loans and

advances to customers based on: o Grouping of loans and advances to

customers into portfolios which include advances subject to similar credit risks; and

o The number of instalments in arrears; ● Loss ratios determined for each category of

loans and advances to customers showing similar historical loss experience as those identified through the categorisation processes.

Given the subjectivity and reliance on estimates and judgements inherent in the determination of the provision for impairment (P157.76 million), we determined that this was a matter of most significance to our audit of the consolidated financial statements.

The disclosures associated with impairment of loans and advances to customers are set out in the consolidated financial statements in the following notes: ● Financial Risk Management, Credit Risk

(page 38) ● Critical accounting estimates and

judgements, Impairment losses on loans and advances to customers (page 35), and

● Note 13 – Loans and advances to customers (page 56).

combination of: ● Testing the data used in the model, by

comparing it to supporting documentation, including the analysis of loans into groupings displaying the same delinquency characteristics;

● Assessing the reasonability of loss ratios applied by management by comparing them to historical loss ratios, recalculating the loss ratios and applying sensitivity tests. We found the loss ratios used by management to be reasonable; and

● Independent recalculation of the impairment provision using an independent model.

Our testing did not identify any material differences.

Other information The directors are responsible for the other information. The other information comprises the information included in the Furnmart Limited Annual Report 2018. Other information does not include the consolidated and separate financial statements and our auditor’s report thereon.

17Furnmart Annual Report 2018

5 of 7

Our opinion on the consolidated and separate financial statements does not cover the other information and we do not express an audit opinion or any form of assurance conclusion thereon.

In connection with our audit of the consolidated and separate financial statements, our responsibility is to read the other information identified above and, in doing so, consider whether the other information is materially inconsistent with the consolidated and separate financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated.

If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of the directors for the consolidated and separate financial statements The directors are responsible for the preparation of the consolidated and separate financial statements that give a true and fair view in accordance with International Financial Reporting Standards, and for such internal control as the directors determine is necessary to enable the preparation of consolidated and separate financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated and separate financial statements, the directors are responsible for assessing the Group and the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the Group and/or the Company or to cease operations, or have no realistic alternative but to do so.

Auditor’s responsibilities for the audit of the consolidated and separate financial statements Our objectives are to obtain reasonable assurance about whether the consolidated and separate financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated and separate financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgement and maintain professional scepticism throughout the audit. We also:

● Identify and assess the risks of material misstatement of the consolidated and separate financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

● Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Group’s and the Company’s internal control.

18 2018 Furnmart Annual Report

6 of 7

● Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the directors.

● Conclude on the appropriateness of the directors’ use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Group’s and the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the consolidated and separate financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Group and / or Company to cease to continue as a going concern.

● Evaluate the overall presentation, structure and content of the consolidated and separate financial statements, including the disclosures, and whether the consolidated and separate financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

● Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with the directors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide the directors with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with the directors, we determine those matters that were of most significance in the audit of the consolidated and separate financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

Individual practicing member: Lalithkumar Mahesan Gaborone Registration number: 20030046 31 October 2018

19Furnmart Annual Report 2018

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS

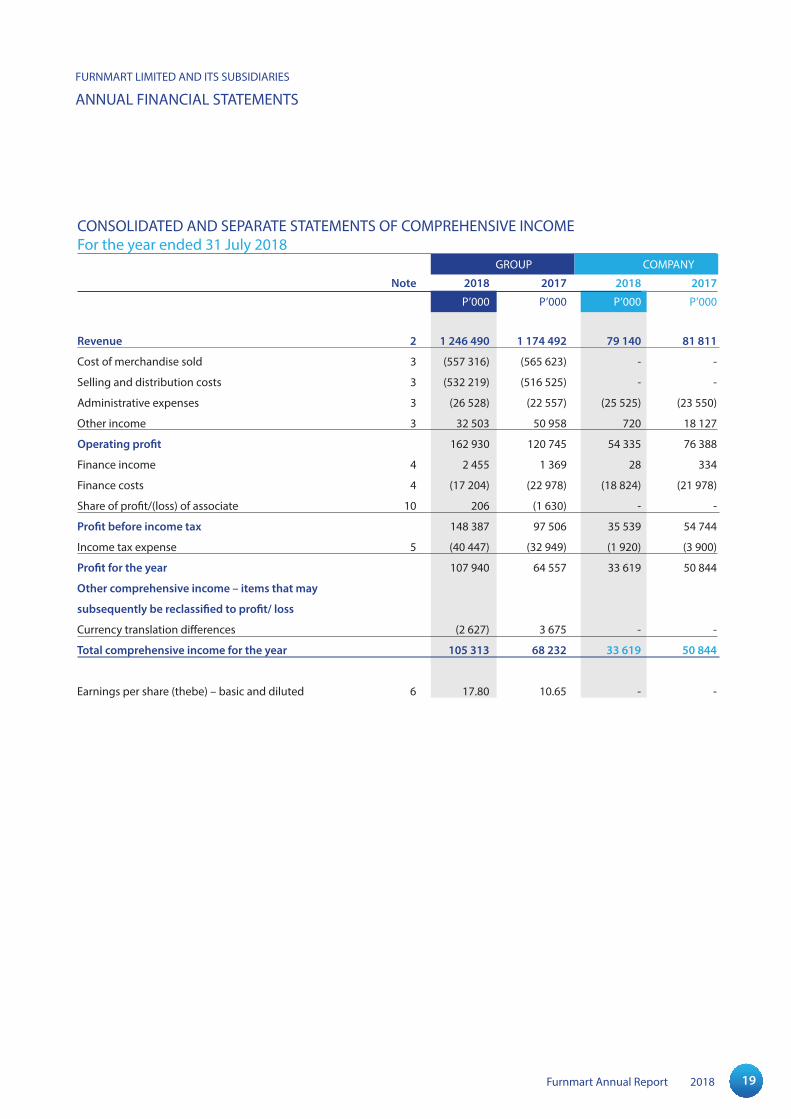

CONSOLIDATED AND SEPARATE STATEMENTS OF COMPREHENSIVE INCOMEFor the year ended 31 July 2018 GROUP COMPANY

Note 2018 2017 2018 2017

P’000 P’000 P’000 P’000

Revenue 2 1 246 490 1 174 492 79 140 81 811

Cost of merchandise sold 3 (557 316) (565 623) - -

Selling and distribution costs 3 (532 219) (516 525) - -

Administrative expenses 3 (26 528) (22 557) (25 525) (23 550)

Other income 3 32 503 50 958 720 18 127

Operating profit 162 930 120 745 54 335 76 388

Finance income 4 2 455 1 369 28 334

Finance costs 4 (17 204) (22 978) (18 824) (21 978)

Share of profit/(loss) of associate 10 206 (1 630) - -

Profit before income tax 148 387 97 506 35 539 54 744

Income tax expense 5 (40 447) (32 949) (1 920) (3 900)

Profit for the year 107 940 64 557 33 619 50 844

Other comprehensive income – items that may

subsequently be reclassified to profit/ loss

Currency translation differences (2 627) 3 675 - -

Total comprehensive income for the year 105 313 68 232 33 619 50 844

Earnings per share (thebe) – basic and diluted 6 17.80 10.65 - -

20 2018 Furnmart Annual Report

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS05

CONSOLIDATED AND SEPARATE STATEMENTS OF FINANCIAL POSITIONAt 31 July 2018 GROUP COMPANY

Note 2018 2017 2018 2017

P’000 P’000 P’000 P’000

ASSETS

Non-current assets

Property plant and equipment 8 79 137 71 539 1 768 1 671

Intangible assets 8 5 643 4 398 5 643 4 398

Investment in associate 10 725 1 599 - -

Other financial assets 11 59 683 67 189 - -

Investment in subsidiaries 10 - - 290 628 291 200

Deferred income tax 9 7 613 1 718 4 084 340

152 801 146 443 302 123 297 609

Current assets

Inventories 12 191 272 195 099 - -

Loans and advances to customers 13 587 538 517 399 - -

Receivables and prepayments 14 18 741 23 419 158 156 200 774

Income tax receivable 26 14 261 17 426 8 212 10 771

Cash and cash equivalents 15 133 121 136 049 15 110 4 894

944 933 889 392 181 478 216,439

Total assets 1 097 734 1 035 835 483 601 514 048

EQUITY AND LIABILITIES

Capital and reserves

Stated capital 16 198 899 198 899 198 899 198 899

Other reserves (25 258) (22 631) - -

Retained earnings 602 439 529 006 9 399 10 287

Total equity 776 080 705 274 208 298 209 186

Non-current liabilities Borrowings 17 164 997 180 402 150 000 157 122

Deferred income tax 9 25 329 21 989 - -

190 326 202 391 150 000 157 122

Current liabilities

Borrowings 17 15 293 26 148 7 282 14 816

Trade and other payables 18 83 681 73 170 116 067 130 594

Income tax payable 26 10 103 12 045 - -

Accruals 19 22 251 16 807 1 954 2 330

131 328 128 170 125 303 147 740

Total liabilities 321 654 330 561 275 303 304 862

Total equity and liabilities 1 097 734 1 035 835 483 601 514 048

21Furnmart Annual Report 2018

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS

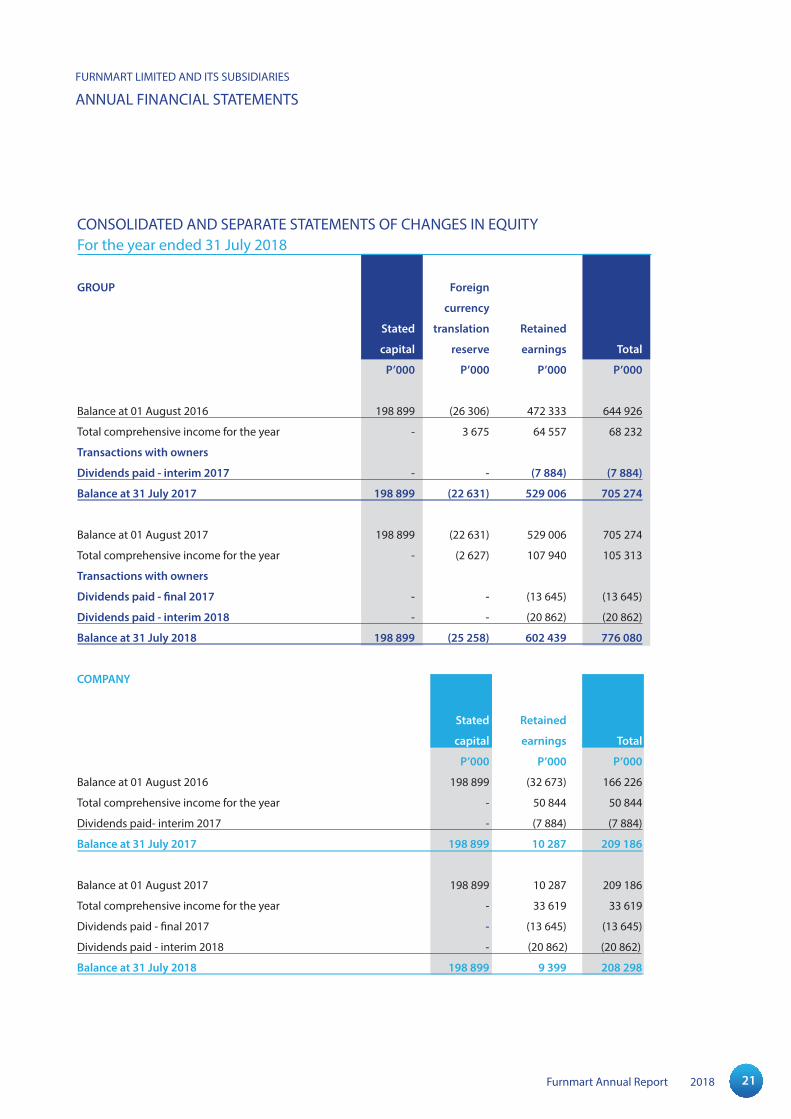

CONSOLIDATED AND SEPARATE STATEMENTS OF CHANGES IN EQUITYFor the year ended 31 July 2018

GROUP Foreign

currency

Stated translation Retained

capital reserve earnings Total

P’000 P’000 P’000 P’000

Balance at 01 August 2016 198 899 (26 306) 472 333 644 926

Total comprehensive income for the year - 3 675 64 557 68 232

Transactions with owners

Dividends paid - interim 2017 - - (7 884) (7 884)

Balance at 31 July 2017 198 899 (22 631) 529 006 705 274

Balance at 01 August 2017 198 899 (22 631) 529 006 705 274

Total comprehensive income for the year - (2 627) 107 940 105 313

Transactions with owners

Dividends paid - final 2017 - - (13 645) (13 645)

Dividends paid - interim 2018 - - (20 862) (20 862)

Balance at 31 July 2018 198 899 (25 258) 602 439 776 080

COMPANY

Stated Retained

capital earnings Total

P’000 P’000 P’000

Balance at 01 August 2016 198 899 (32 673) 166 226

Total comprehensive income for the year - 50 844 50 844

Dividends paid- interim 2017 - (7 884) (7 884)

Balance at 31 July 2017 198 899 10 287 209 186

Balance at 01 August 2017 198 899 10 287 209 186

Total comprehensive income for the year - 33 619 33 619

Dividends paid - final 2017 - (13 645) (13 645)

Dividends paid - interim 2018 - (20 862) (20 862)

Balance at 31 July 2018 198 899 9 399 208 298

22 2018 Furnmart Annual Report

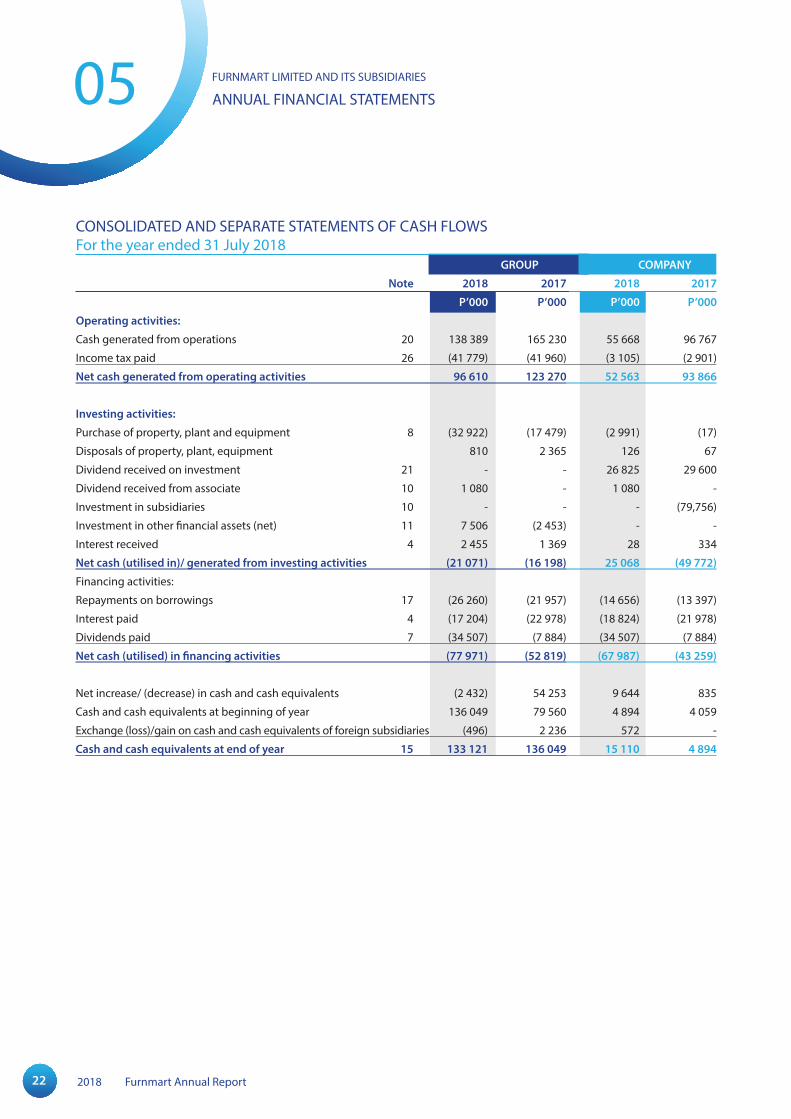

CONSOLIDATED AND SEPARATE STATEMENTS OF CASH FLOWSFor the year ended 31 July 2018 GROUP COMPANY

Note 2018 2017 2018 2017

P’000 P’000 P’000 P’000

Operating activities:

Cash generated from operations 20 138 389 165 230 55 668 96 767

Income tax paid 26 (41 779) (41 960) (3 105) (2 901)

Net cash generated from operating activities 96 610 123 270 52 563 93 866

Investing activities:

Purchase of property, plant and equipment 8 (32 922) (17 479) (2 991) (17)

Disposals of property, plant, equipment 810 2 365 126 67

Dividend received on investment 21 - - 26 825 29 600

Dividend received from associate 10 1 080 - 1 080 -

Investment in subsidiaries 10 - - - (79,756)

Investment in other financial assets (net) 11 7 506 (2 453) - -

Interest received 4 2 455 1 369 28 334

Net cash (utilised in)/ generated from investing activities (21 071) (16 198) 25 068 (49 772)

Financingactivities:

Repayments on borrowings 17 (26 260) (21 957) (14 656) (13 397)

Interest paid 4 (17 204) (22 978) (18 824) (21 978)

Dividends paid 7 (34 507) (7 884) (34 507) (7 884)

Net cash (utilised) in financing activities (77 971) (52 819) (67 987) (43 259)

Net increase/ (decrease) in cash and cash equivalents (2 432) 54 253 9 644 835

Cash and cash equivalents at beginning of year 136 049 79 560 4 894 4 059

Exchange (loss)/gain on cash and cash equivalents of foreign subsidiaries (496) 2 236 572 -

Cash and cash equivalents at end of year 15 133 121 136 049 15 110 4 894

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS05

23Furnmart Annual Report 2018

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) and the requirements of the Botswana Companies Act (2003). The financial statements are prepared under the historical cost convention, as modified by the valuation of certain financial assets and financial liabilities at fair value through profit and loss.

The preparation of financial statements in conformity with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the Group’s accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the Group’s financial statements are disclosed in the “Critical accounting estimates and judgements” section of the financial statements.

Estimates and judgments are continually evaluated based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

New standards, amendments and interpretations issued, relevant to the Group, but not yet effective and not early adopted.There were no new standards or amendments to existing standards that become effective for the first time during the year, that are relevant or had material impact to the operations of the group.

Standards issued but not yet effective at year endA number of new standards and amendments to standards are issued but not yet effective for period ended 31 July 2018. Those which may be relevant to the Group are set out below. The Group do not plan to

adopt these standards early. These will be adopted in the period that they become mandatory.

IFRS 9 Financial InstrumentsIFRS 9, published in July 2015, replaces the existing guidanceinIAS39:FinancialInstruments:Recognitionand Measurement. IFRS 9 includes revised guidance on the classification and measurement of financial instruments, including a new expected credit loss model for calculating impairment on financial assets, and the new general hedge accounting requirements. It also carries forward the guidance on recognition and de recognition of financial instruments from IAS 39. In addition, IFRS 9 will include changes in the measurement bases of the Group’s financial assets to amortised cost, fair value through other comprehensive income or fair value through profit or loss. Even though these measurement categories are similar to IAS 39, the criteria for classification into these categories are significantly different. IFRS 9 is effective for annual reporting periods beginning on or after 1 January 2018, with early adoption permitted. IFRS 9 introduces a revised impairment model which will require entities to recognise expected credit losses based on unbiased forward - looking information. This replaces the existing IAS 39 incurred loss model which only recognises impairment if there is objective evidence that a loss has already been incurred and would measure the loss at the most probable outcome. The IFRS 9 impairment model will be applicable to all financial assets at amortised cost, lease receivables, debt financial assets at fair value through other comprehensive income, loan commitments and financial guarantee contracts.The measurement of expected credit loss will involve increased complexity and judgement including estimation of probabilities of default, loss given default, a

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIESFor the year ended 31 July 2018

The principal accounting policies applied in the preparation of these financial statements are set out below. These policies have been consistently applied to all the years presented, and are unchanged from those applied in previous periods, unless noted otherwise.

These financial statements have been approved by the board of directors on 25 October 2018.

1. BASIS OF PREPARATION

24 2018 Furnmart Annual Report

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)For the year ended 31 July 2018

range of unbiased future economic scenarios, estimation of expected lives and estimation of exposures at default and assessing significant increases in credit risk.

IFRS 15 Revenue from Contracts with CustomersIFRS 15 establishes a comprehensive framework for revenue recognition. The model features a contract-based five-step analysis of transactions to determine whether, how much and when revenue is recognised. It replaces existing revenue recognition guidance, including IAS 18 Revenue, IAS 11 Construction Contracts and IFRIC 13 Customer Loyalty Programmes. IFRS 15 is effective for annual reporting periods beginning on or after 1 January 2018, with early adoption permitted. The Group is currently in the process of performing a more detailed assessment of the impact of this standard on the Group and the outcome of it is yet to be quantified.

IFRS 16 LeasesIASB and FASB decided that lessees should be required to recognise assets and liabilities arising from all leases (with limited exceptions) on the balance sheet. The model reflects that, at the start of a lease, the lessee obtains the right to use an asset for a period of time and has an obligation to pay for that right. A lessee measures lease liabilities at the present value of future lease payments. A lessee measures lease assets, initially at the same amount as lease liabilities, and also includes costs directly related to entering into the lease. Lease assets are amortised in a similar way to other assets such as property, plant and equipment. This approach will result in a more faithful representation of a lessee’s assets and liabilities and, together with enhanced disclosures, will provide greater transparency of a lessee’s financial leverage and capital

employed. IFRS 16 is effective for annual reporting periods beginning on or after 1 January 2019 and the Group is in the process of assessing the potential impact to the financial statements.

Other standards/amendmentsThe following new or amended standards are not expected to have a significant impact of the Group’s consolidatedfinancialstatements:

• Sharebasedpayments,accountingoncertainshare based transactions

(Amendments to IFRS 2 – effective 1 January 2018).• Revenuefromcontractswithcustomers

(Amendments to IFRS 15 – effective 1 January 2018).

• Foreigncurrencytransactionsandadvanceconsideration (IFRIC 22 – effective 1 January 2018).

• ConsolidatedFinancialStatements(IFRS10–effective date postponed initially 1 January 2016).

• Uncertaintyoverincometaxtreatments(IFRIC23–effective 1 January 2019)

Management is currently assessing the impact of the application of these standards on the company’s financial results.

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS05

25Furnmart Annual Report 2018

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS

All Group companies have a 31 July year end and apply uniform accounting policies for like transactions.

All intercompany transactions and balances between Group entities are eliminated. The company carries its investment in subsidiaries in its seperate financial statement at cost less any accumulated impairment.

AssociatesAssociates are entities over which the Group has significant influence but not control, generally accompanying a shareholding of between 20% and 50% of the voting rights.

Investments in associates are accounted for using the equity method of accounting and are initially recognised at cost. The Group’s investment in associates includes goodwill identified on acquisition, net of any accumulated impairment loss.

The Group’s financial statements include the following associatewhosefinancialyearalsoendson31July:

Company Country %Nature of business 2018 2017

United Impex (Pty) Ltd

Botswana 25% Financial Services(Dormant)

25% 25%

The Group’s share of its associates’ post-acquisition profits or losses and its share of post-acquisition movements in reserves are recognised in the Statement of Comprehensive Income. When the Group’s share of losses in an associate equals or exceeds its interest in the associate, the Group does not recognise any further losses, unless it has incurred obligations, issued guarantees or made payments on behalf of the associate.

Gains and losses arising from dilution of investments in associates are recognised in the Statement of Comprehensive Income when such dilutionary transactions become effective.

2 CONSOLIDATION

SubsidiariesSubsidiaries are all entities (including structured entities) over which the group has control. The group controls an entity when the group is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity. Subsidiaries are fully consolidated from the date on which control is transferred to the group. They are deconsolidated from the date that control ceases.

3 CELL CAPTIVE ARRANGEMENTS

The Group has entered into cell captive arrangements for purposes of managing and administering its customer protection programmes in Namibia and South Africa. These programmes offer customer credit insurance in the event of death or certain other life changing events prior to full settlement of outstanding balances.

The cell captive arrangements do not qualify as subsidiaries as they do not exist as separate entities from the underwriter. In one of these, the Group has no recapitalisation obligation and there is no ‘insurance contract’ as there is no transfer of risk and the arrangement is more akin to a profit sharing arrangement. On the other, the group has a recapitalisation obligation in the event the cell captive became insolvent. The group

continually assesses the cell captive status and where warranted a provision is recognised.

In both these instances, the group is the beneficiary. On this basis, where the cell captive is financially sound and has surplus cash the Group recognises its right to receive cash as a financial asset.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)For the year ended 31 July 2018

26 2018 Furnmart Annual Report

Group

The Group recognises revenue when the amount of revenue can be reliably measured, it is probable that future economic benefits will flow to the entity and when specific criteria have been met for each of the Group’s activities as described below.

a) Sale of merchandiseRevenue from the sale of merchandise is recognised upon transfer to the customer of the significant risks and rewards of ownership. In the case of cash sales, this is generally when cash is received, an invoice is raised and delivery of the goods has taken place. In the case of credit sales, this is generally when a credit sale agreement is concluded, an invoice is raised and delivery of the goods has taken place (related delivery charges are also recognised on this basis).

b) Ancillary charges on credit salesOther revenue flowing from the credit sale of merchandise comprises of the following significant components.• Financeincome:Onatimeproportionbasisthat

takes into account the effective yield over the loan life cycle on the principal amount outstanding;

• Customerprotectionplanincome:Thesearerecognised on a straight-line basis over the debt repayment period of the invoiced amount;

• FMClubmembershipfees:Ontheaccrualbasisascharged every month;

• Debtfollow-upcharges:Uponcustomerfallinginto arrears and on additional follow-up services being rendered. Customer protection plan income, FM Club membership fees and finance income are classified as financing income. Debt follow up charges and delivery charges are included as ancillary services.

Company

Interest incomeOn the accrual basis, taking into account the effective interest yield on underlying balances. When a loan and receivable is impaired, the company reduce the carrying amount to its recoverable amount, being the estimated future cash flows discounted at the original effective interest rate of the instrument, and continues unwinding discount interest income.

Dividend Income

Dividend income is recognised when the right to receive payment is established. Administration FeeAdministration fee represents sale of managerial and infrastructure services to Group companies. Revenue from sale of services is recognised in the period in which the services are rendered.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)For the year ended 31 July 2018

5 REVENUE RECOGNITION

The Group operates a chain of retail outlets for selling furniture and other household appliances. Revenue for the Group comprises of the fair value of the consideration received or receivable for the sale of goods and finance and other income earned on credit granted in the ordinary course of the Group’s activities. Revenue is shown net of value-added tax, returns, rebates and discounts and after eliminating sales within the Group.

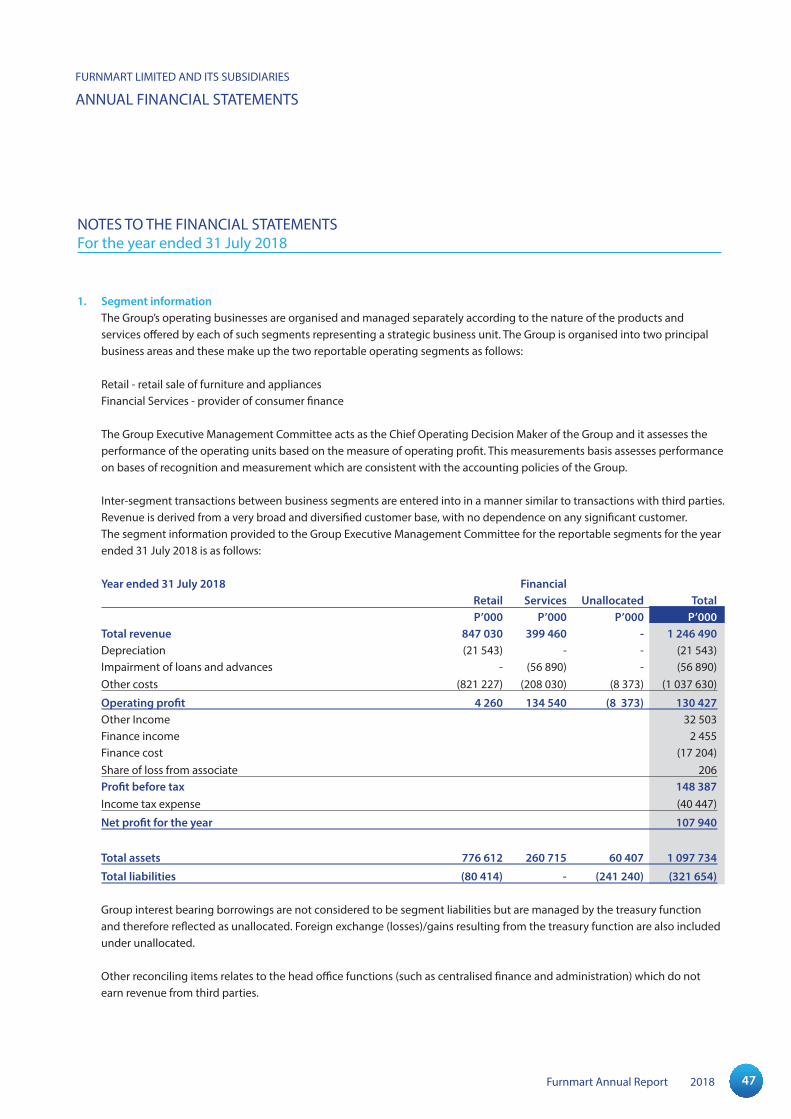

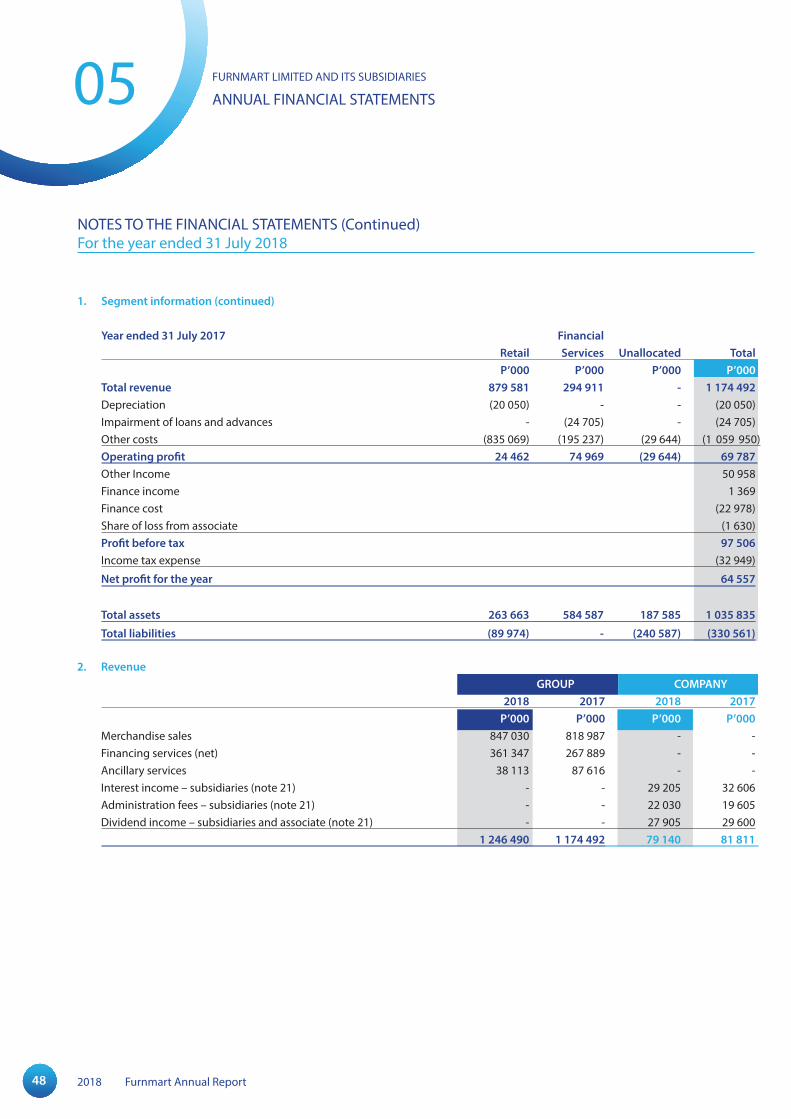

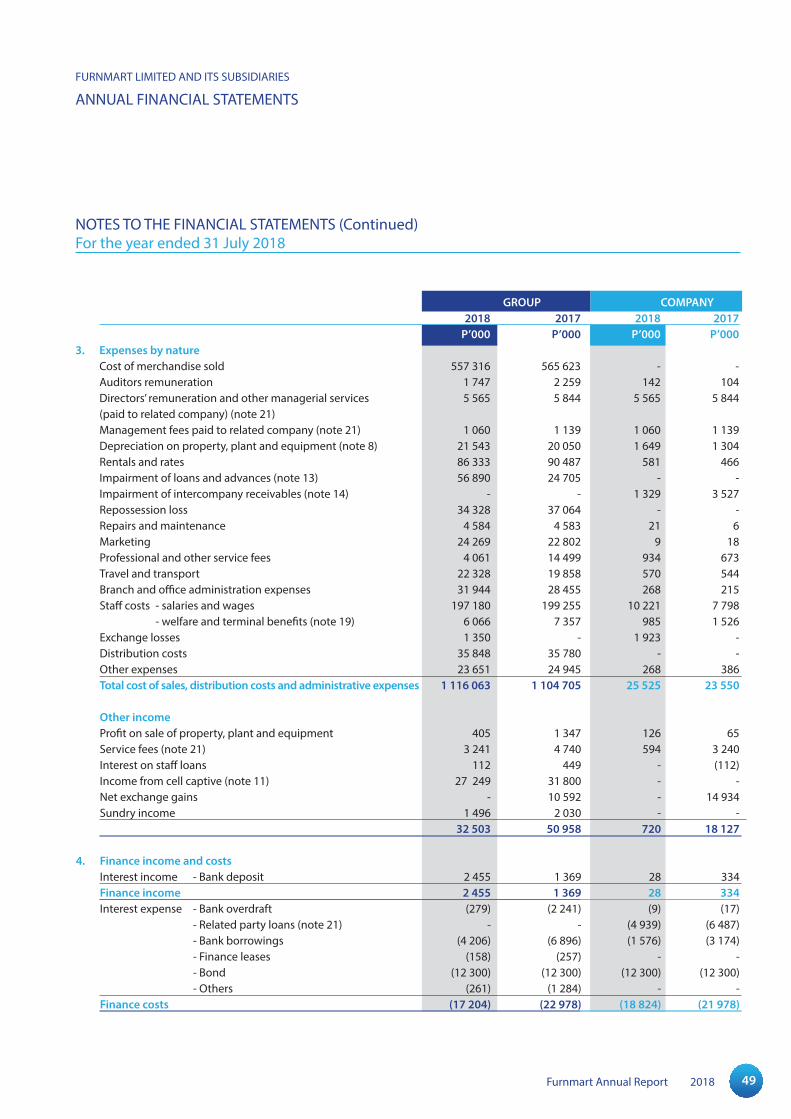

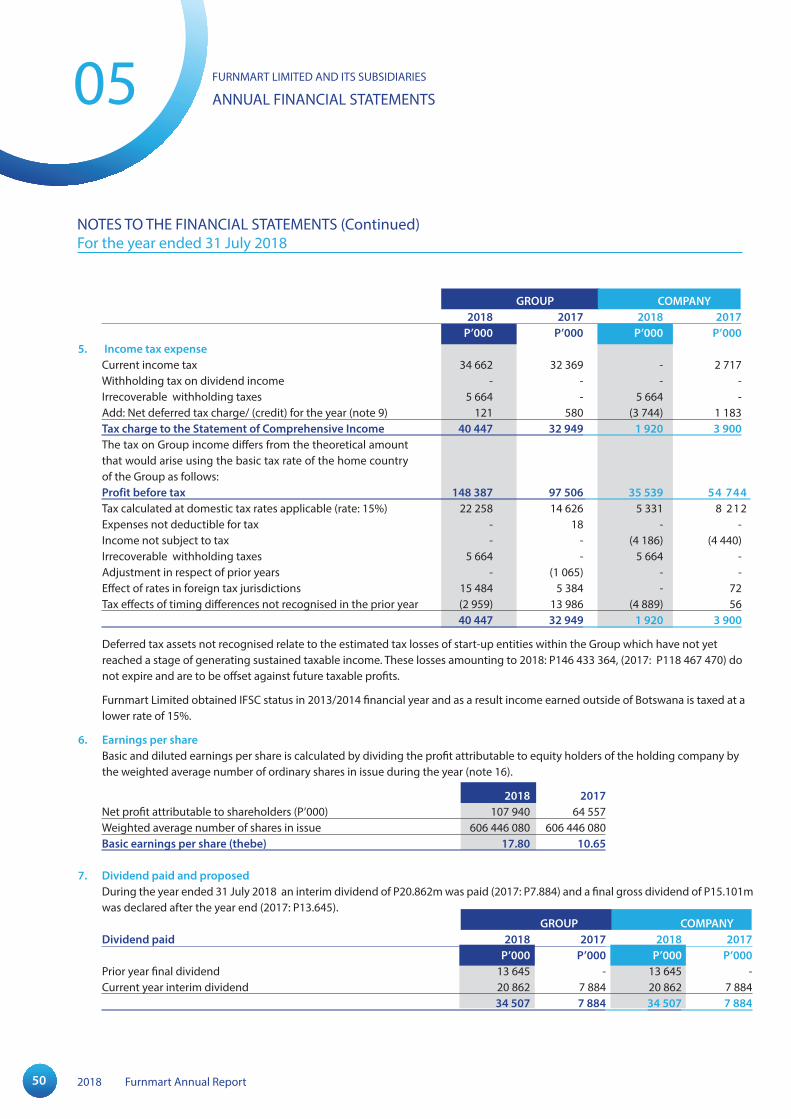

4 SEGMENT REPORTING

Operating segments are reported in a manner consistent with the internal reporting provided to the Group Executive Management Committee. The Group Executive Management Committee is responsible for allocating resources and assessing performance of the operating segments and is considered the Chief Operating Decision Maker as defined in IFRS 8.

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS05

27Furnmart Annual Report 2018

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS

Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted or substantively enacted at the Statement of Financial Position date, and any adjustment to tax payable in respect of previous years.

Income tax payable on profits, based on the applicable tax law, is recognised as an expense in the period in which profits arise.

Deferred tax is provided using the liability method, providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for current tax purposes. Deferred tax is not recognised for the followingtemporarydifferences:theinitialrecognitionof goodwill, the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit, and differences relating to investments in subsidiaries to the extent that they probably will not reverse in the

foreseeable future. Deferred tax is measured at the tax rates that are expected to be applied to the temporary differences when they reverse, based on the laws that have been enacted or substantively by the reporting date.

The principal temporary differences arise from differing tax depreciation rates on property, plant and equipment. A deferred tax is provided on temporary differences arising from investments in subsidiaries and associates, except where the timing of the reversal of the temporary difference is controlled by the Group and it is probable that the difference will not reverse in the foreseeable future.

A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the asset can be utilised. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that related tax benefit will be realised.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)For the year ended 31 July 2018

6 CURRENT AND DEFERRED INCOME TAX

Income tax expense comprises current and deferred tax. Income tax expense is recognised in the Statement of Comprehensive Income except to the extent that it relates to items recognise directly in equity, in which case it is recognised in equity.

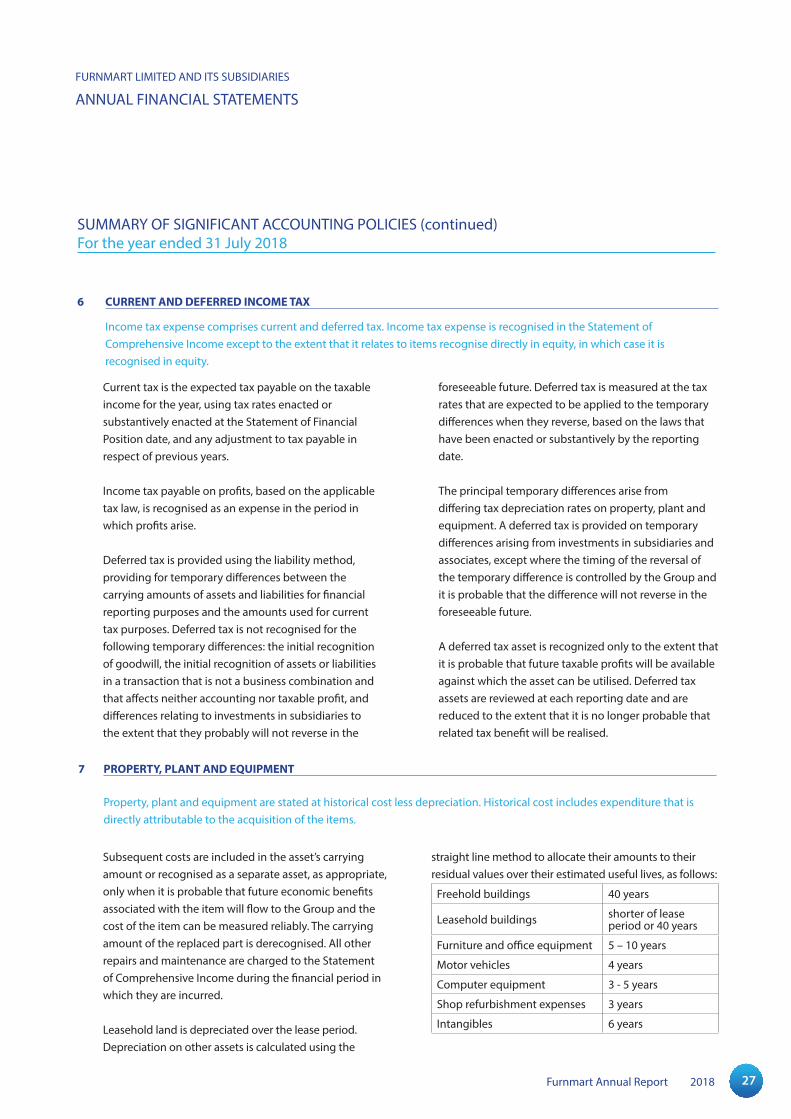

7 PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment are stated at historical cost less depreciation. Historical cost includes expenditure that is directly attributable to the acquisition of the items.

Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the Group and the cost of the item can be measured reliably. The carrying amount of the replaced part is derecognised. All other repairs and maintenance are charged to the Statement of Comprehensive Income during the financial period in which they are incurred.

Leasehold land is depreciated over the lease period. Depreciation on other assets is calculated using the

straight line method to allocate their amounts to their residualvaluesovertheirestimatedusefullives,asfollows:

Freehold buildings 40 years

Leasehold buildings shorter of lease period or 40 years

Furniture and office equipment 5 – 10 years

Motor vehicles 4 years

Computer equipment 3 - 5 years

Shop refurbishment expenses 3 years

Intangibles 6 years

28 2018 Furnmart Annual Report

(a) Financial assets at fair value through profit or lossFinancial assets at fair value through profit or loss are financial assets held for trading. A financial asset is classified in this category if acquired principally for the purpose of selling in the short term. Derivatives are also categorised as held for trading unless they are designated as hedges. Assets in this category are classified as current assets if expected to be settled within 12 months, otherwise they are classified as non-current.

(b) Loans and receivablesLoans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are included in current assets. The group’s loans and receivables comprise ‘trade and other receivables’ and ‘cash and cash equivalents’ in the balance sheet.

(c) Available-for-sale financial assetsAvailable-for-sale financial assets are non-derivatives that are either designated in this category or not classified in any of the other categories. They are included in non-current assets unless the investment matures or management intends to dispose of it within 12 months of the end of the reporting period.

(d) Held to maturity investments Held to maturity investments are non-derivative financial assets with fixed or determinable payments that an entity intents and is able to hold to maturity and

that do not meet the definition of loans and receivables and are not designated on initial recognition as asset at fair value through profit or loss or as available for sale.

Recognition and measurementRegular purchases and sales of financial assets are recognised on the trade-date – the date on which the group commits to purchase or sell the asset. Investments are initially recognised at fair value plus transaction costs for all financial assets not carried at fair value through profit or loss. Financial assets carried at fair value through profit or loss is initially recognised at fair value, and transaction costs are expensed in the income statement. Financial assets are derecognised when the rights to receive cash flows from the investments have expired or have been transferred and the group has transferred substantially all risks and rewards of ownership. Available-for-sale financial assets and financial assets at fair value through profit or loss are subsequently carried at fair value. Loans and receivables are subsequently carried at amortised cost using the effective interest method.

Gains or losses arising from changes in the fair value of the ‘financial assets at fair value through profit or loss’ category are presented in the income statement within ‘Other (losses)/gains – net’ in the period in which they arise. Dividend income from financial assets at fair value through profit or loss is recognised in the income statement as part of other income when the group’s right to receive payments is established.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)For the year ended 31 July 2018

8 FINANCIAL INSTRUMENTS

ClassificationTheGroupclassifiesitsfinancialassetsinthefollowingcategories:atfairvaluethroughprofitorloss,loansandreceivables,available for sale and held to maturity investments. The classification depends on the purpose for which the financial assets were acquired. Management determines the classification of its financial assets at initial recognition.

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at the end of each reporting period.

Where the carrying amount of an asset is greater than its estimated recoverable amount, it is written down to

its recoverable amount. Gains and losses on disposal of property, plant and equipment are determined by reference to their carrying amount and are taken to the Statement of Comprehensive Income in the period of disposal.

7 PROPERTY, PLANT AND EQUIPMENT (CONTINUED)

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS05

29Furnmart Annual Report 2018

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS

Changes in the fair value of monetary and non-monetary securities classified as available for sale are recognised in other comprehensive income. When securities classified as available for sale are sold or impaired, the accumulated fair value adjustments recognised in equity are included in the income statement as ‘Gains and losses from investment securities’. Interest on available-for-sale securities calculated using the effective interest method is recognised in the income statement as part of finance income. Dividends on available-for-sale equity instruments are recognised in the income statement as part of other income when the group’s right to receive payments is established.

Offsetting financial instrumentsFinancial assets and liabilities are offset and the net amount reported in the balance sheet when there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis or realise the asset and settle the liability simultaneously. The legally enforceable right must not be contingent on future events and must be enforceable in the normal course of business and in the event of default, insolvency or bankruptcy of the company or the counterparty.

Impairment of financial assets(a) Assets carried at amortised costThe group assesses at the end of each reporting period whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is impaired and impairment losses are incurred only if there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (a ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated.

Evidence of impairment may include indications that the debtors or a group of debtors is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other financial reorganisation, and where observable data indicate that there is a measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults.

(b) Loans and receivables For loans and receivables category, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset’s original effective interest rate. The carrying amount of the asset is reduced and the amount of the loss is recognised in the consolidated income statement. If a loan or held-to-maturity investment has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract. As a practical expedient, the group may measure impairment on the basis of an instrument’s fair value using an observable market price.If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognised (such as an improvement in the debtor’s credit rating), the reversal of the previously recognised impairment loss is recognised in the consolidated income statement.

(c) Assets classified as available for saleThe group assesses at the end of each reporting period whether there is objective evidence that a financial asset or a group of financial assets is impaired.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)For the year ended 31 July 2018

8 FINANCIAL INSTRUMENTS (CONTINUED)

30 2018 Furnmart Annual Report

a) Finance leasesLeases of property, plant and equipment, where the Group assumes substantially all the benefits and risks of ownership are classified as finance leases. Finance leases are capitalised at the estimated present value of the underlying lease payments. Each lease payment is allocated between the liability and finance charges so as to achieve a constant rate on the finance balance outstanding. The interest element of the finance charge is charged to the Statement of Comprehensive Income over the lease period. Property, plant and equipment, acquired under finance leases, are depreciated over the useful lives of the assets.

b) Operating leases - as a lessorLease arrangements in which a significant portion of the risks and rewards of ownership are retained by the

lessor are classified as operating leases. Rental receipts under operating leases (net of any incentives provided to the lessee) are recognised in the Statement of Comprehensive Income on a straight-line basis over the period of the lease.

c) Operating leases - as a lesseeLease arrangements in which a significant portion of the risks and rewards of ownership are retained by the lessor are classified as operating leases. Payments made under operating leases (net of any incentives received from the lessor) are charged to the Statement of Comprehensive Income on a straight-line basis over the period of the lease.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)For the year ended 31 July 2018

9 IMPAIRMENT OF NON-FINANCIAL ASSETS

Property, plant and equipment and other non-current assets with finite useful lives are reviewed for impairment losses whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for the amount by which the carrying amount of the assets exceeds its recoverable amount which is the higher of an asset’s fair value less cost to sell and value in use. For the purposes

of assessing impairment, assets are grouped at the lowest level for which there is separately identifiable cash flows (cash generating units). Non-financial assets that suffered impairment are reviewed annually for possible reversal of the impairment.

Assets that have infinite useful life are not subject to amortisation and are tested annually for impairment.

10 ACCOUNTING FOR LEASES

11 COMPUTER SOFTWARE DEVELOPMENT COSTS

Costs associated with maintaining computer software programmes are recognised as an expense as incurred. Development Costs that are directly attributed to the design and testing of identifiable and unique software products controlled by the Group are recognised as intangibleassetswhenthefollowingcriteriaaremet:

• itistechnicallyfeasibletocompletethesoftwareproduct so that it will be available for use;

• managementintendstocompletethesoftwareproduct and use or sell;

• thereisanabilitytouseorsellthesoftwareproduct;• itcanbedemonstratedhowthesoftwareproduct

will generate probable future economic benefits;

• adequatetechnical,financialandotherresourcesto complete the development and to use or sell the software product are available; and

• theexpenditureattributabletothesoftwareproductduring its development can be reliably measured.

Directly attributable costs that are capitalised as part of the software product include the software development employee costs and an appropriate portion of relevant overheads.

Other development expenditures that do not meet this criteria are recognised as an expense as incurred.

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS05

31Furnmart Annual Report 2018

FURNMART LIMITED AND ITS SUBSIDIARIES

ANNUAL FINANCIAL STATEMENTS

All loans and advances are recognised when an underlying credit agreement has been signed and the Group has supplied the related goods to the borrower.

An allowance for loan impairment is established if there is objective evidence that the Group will not be able to collect all amounts due according to the original contractual terms of loans. The amount of the provision is the difference between the carrying amount and the recoverable amount estimated.

The loan impairment provision also cover losses where there is objective evidence that incurred losses are present in components of the loan portfolio at the

Statement of Financial Position date. These have been estimated based upon historical pattern of losses in each component, reflecting the current economic climate in which the borrower operates. When a loan is uncollectible, it is written off against the related provision for impairments; subsequent recoveries are credited to the provision for loans losses in the Statement of Comprehensive Income.

If the amount of the impairment subsequently decreases due to an event occurring after the write down, the release of the provision is credited as a reduction of the provision for loan impairment.

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)For the year ended 31 July 2018

12 INVENTORIES

Inventories are stated at the lower of cost and estimated net realisable value. Cost is determined by the first in first out (FIFO) method. Net realisable value is the estimated selling price in the ordinary course of business, less applicable selling expenses.

13 LOANS AND ADVANCES TO CUSTOMERS

Loans originated by the Group by providing money directly or indirectly to the borrower are categorised as loans and advances to customers and are carried at amortised cost, which is defined as the fair value of the cash consideration given to originate those loans as is determined by reference to market prices at origination date.

14 OTHER RECEIVABLES

Other receivables arise in the normal course of business and are stated at amortised cost or realisable value.

15 CASH AND CASH EQUIVALENTS

Cash and cash equivalent includes cash in hand, deposits held at call with banks, other short term highly liquid investments with original maturities of three months or less and bank overdrafts. Cash and cash equivalents are measured at amortised cost using the effective interest rate method.

16 STATED CAPITAL

Ordinary share capital is recognised at the fair value of the consideration received.

Dividends on ordinary shares are recorded in the Group’s financial statements in the period in which they are paid or approved by the Group’s shareholders, whichever is earlier.

32 2018 Furnmart Annual Report

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)For the year ended 31 July 2018

17 PROVISIONS

Provisions are recognised when the Group has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources will be required to settle the obligation and a reliable estimate of the amount can be made. Where the Group expects a provision to be reimbursed, for example under an insurance contract, the reimbursement is recognised as a separate asset but only when the reimbursement is virtually certain.

18 BORROWINGS

Borrowings are recognised initially at fair value, net of transaction costs. In subsequent periods, borrowings are stated at amortised cost using the effective yield method; any difference between proceeds (net of transaction costs) and the redemption value is recognised in the Statement of Comprehensive Income over the period of the borrowings.

Borrowings are classified as current liabilities unless the Group has an unconditional right to defer settlement of the liability for at least 12 months after the Statement of Financial Position date.

Functional and presentation currency

Items included in the financial statements of each of the Group’s entities are measured using the currency of the primary economic environment in which the entity operates (“the functional currency”). The financial statements are presented in Botswana Pula, which is the holding company’s functional and presentation currency.

Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in the statement of other comprehensive income.

Group companies

The results and financial position of all the Group entities (none of which has the currency of a hyperinflationary economy) that have a functional currency different from the presentation currency are translated into the presentationcurrencyasfollows:

• assetsandliabilitiesforeachStatementofFinancialPosition presented are translated at the closing rate

at the date of that Statement of Financial Position;• incomeandexpensesforeachstatementofother

comprehensive income are translated at average exchange rates (unless this average is not a reasonable approximation of the cumulative effect of the rates prevailing on the transaction dates, in which case income and expenses are translated at the rate on the date of the transaction) and;

• allresultingexchangedifferencesarerecognisedinthe statement of other comprehensive income and as a separate component of equity.

On consolidation, exchange differences arising from the translation of the net investment in foreign operations are recognised in the statement of other comprehensive income.

When a foreign entity is sold, exchange differences that were recorded in equity are recognised in the Statement of Comprehensive Income as part of the gain or loss on sale.

Goodwill and fair value adjustments arising on the acquisition of a foreign entity are treated as assets and liabilities of the foreign operation and translated at the closing rate.

19 FOREIGN CURRENCY TRANSLATION