Embed Size (px)

Citation preview

ROLE OF CONSULTING AND CONTRACTING INDUSTRY IN ECONOMIC DEVELOPMENT OF TURKEY

www.isdb-am42.org

Presented by

Demir INOZUImmediate Past President of Association of Turkish Consulting Engineers and Architects (ATCEA)

Chairman of International Technical Consultancy Business Council of DEIK(Foreign Economic Relations Board)

TURKIYE

Turkish Construction Industry is the main driving force in the economic uplift and

development of Turkey. Construction Industry with its three main stakeholders;

• Contractors,

• Construction Materials Producers

• Technical Consultants;

plays an essential role in the socioeconomic development of Turkey.

Located at the crossroads of three continents; Europe, Asia and Africa; Turkey has

historical and strong political and economic relations in the region. Geographical

proximity of Turkey to the potential markets, provides a great advantage to the

global competitiveness of the Turkish construction industry abroad.

2

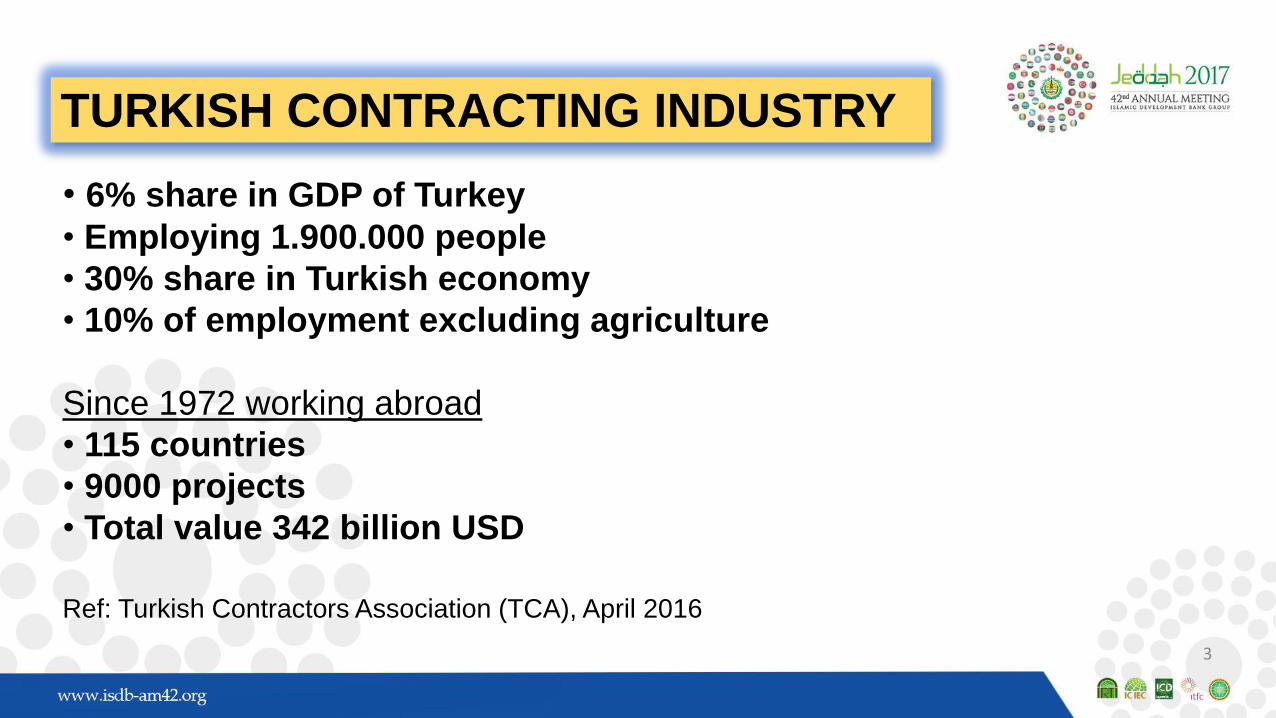

TURKISH CONTRACTING INDUSTRY

• 6% share in GDP of Turkey

• Employing 1.900.000 people

• 30% share in Turkish economy

• 10% of employment excluding agriculture

Since 1972 working abroad

• 115 countries

• 9000 projects

• Total value 342 billion USD

Ref: Turkish Contractors Association (TCA), April 2016

3

• According to rankings announced in 2016 by the leading international

industry magazine Engineering News Record (ENR), 40 Turkish contracting

companies ranked among "The World's Top 250 International Contractors“,

based upon 2015 data by overseas operations outside their home countries.

• Turkish contractors ranked second in number in the world after China for

the last 9 years.

• As of 2015, total amount of overseas projects undertaken by the 250

international contractors in the ENR list is 500 billion USD; and the share of

Turkish contractors is 22.8 billion USD (4.6 percent), ranking 9th in total

values of international contracts.

4

NUMBER OF TURKISH CONTRACTORS IN ENR “THE WORLD’S TOP 250 INTERNATIONAL CONTRACTORS LIST”

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

811

14

2022 23

3133

3133

3842 40

YEARS

5

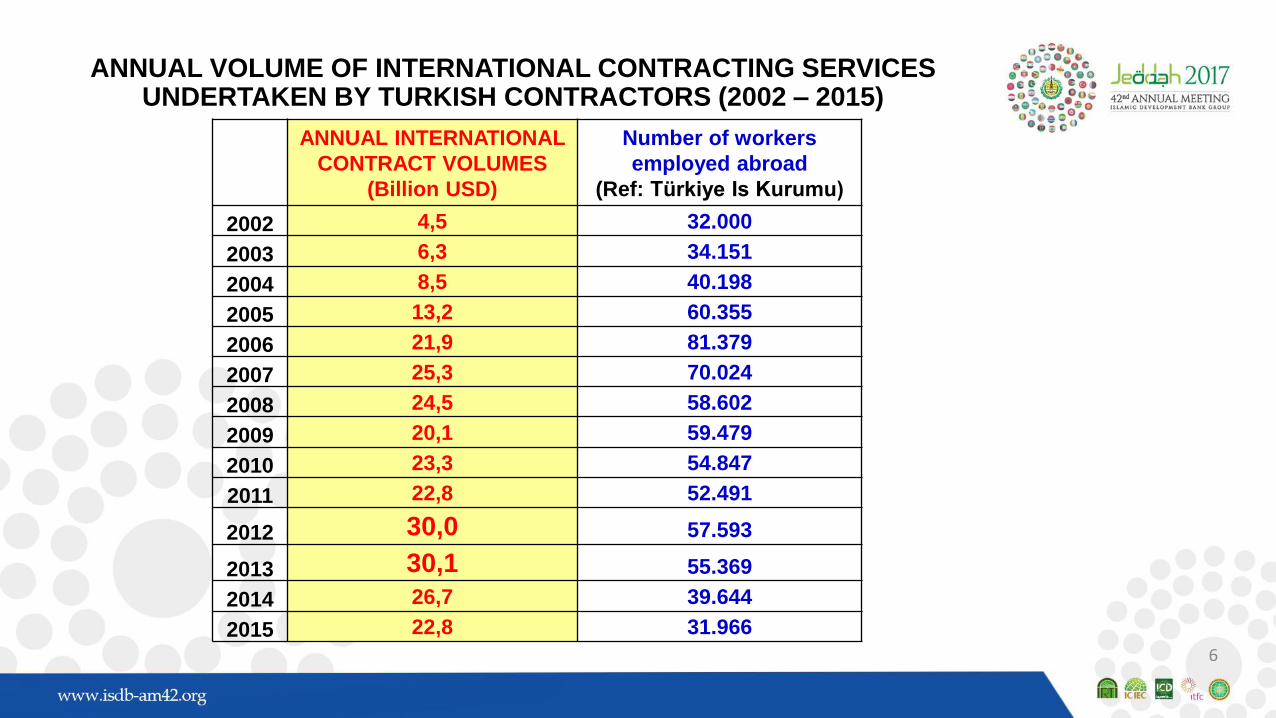

ANNUAL VOLUME OF INTERNATIONAL CONTRACTING SERVICES UNDERTAKEN BY TURKISH CONTRACTORS (2002 – 2015)

ANNUAL INTERNATIONAL

CONTRACT VOLUMES

(Billion USD)

Number of workers

employed abroad

(Ref: Türkiye Is Kurumu)

2002 4,5 32.000

2003 6,3 34.151

2004 8,5 40.198

2005 13,2 60.355

2006 21,9 81.379

2007 25,3 70.024

2008 24,5 58.602

2009 20,1 59.479

2010 23,3 54.847

2011 22,8 52.491

2012 30,0 57.593

2013 30,1 55.369

2014 26,7 39.644

2015 22,8 31.966

6

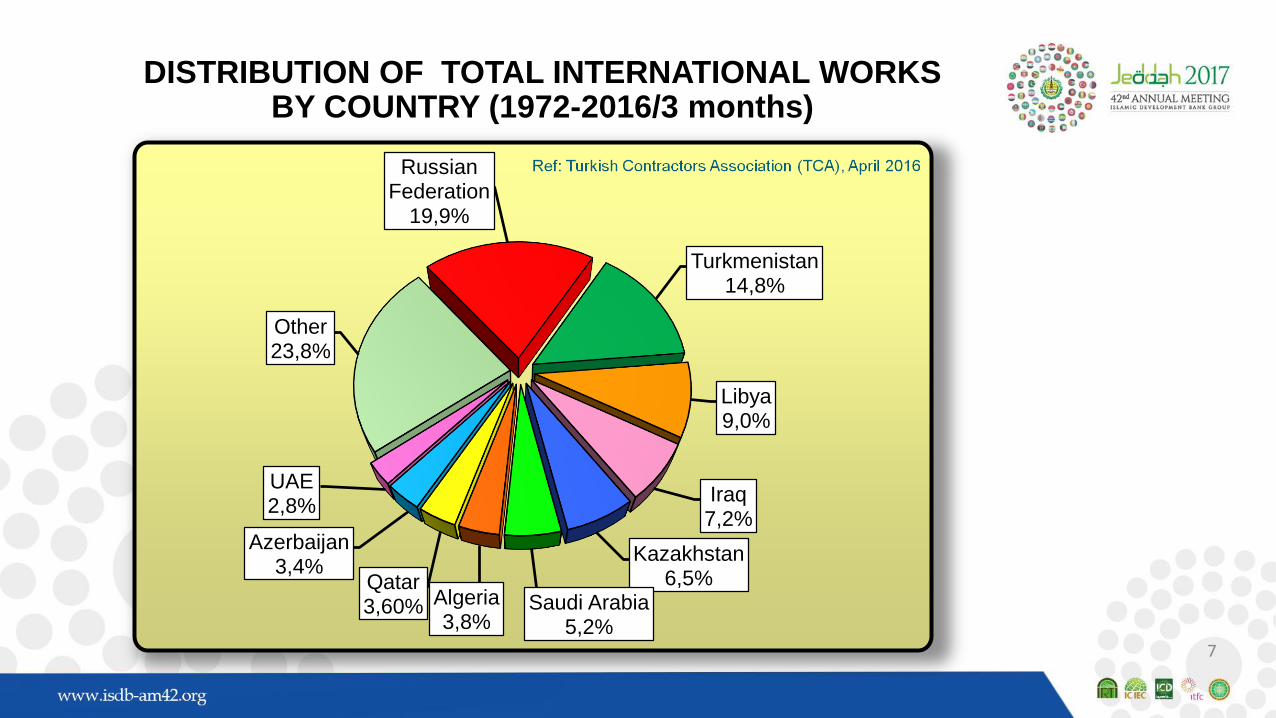

DISTRIBUTION OF TOTAL INTERNATIONAL WORKS BY COUNTRY (1972-2016/3 months)

Russian Federation

19,9%

Turkmenistan14,8%

Libya9,0%

Iraq7,2%

Kazakhstan6,5%

Saudi Arabia5,2%

Algeria3,8%

Qatar3,60%

Azerbaijan3,4%

UAE2,8%

Other 23,8%

7

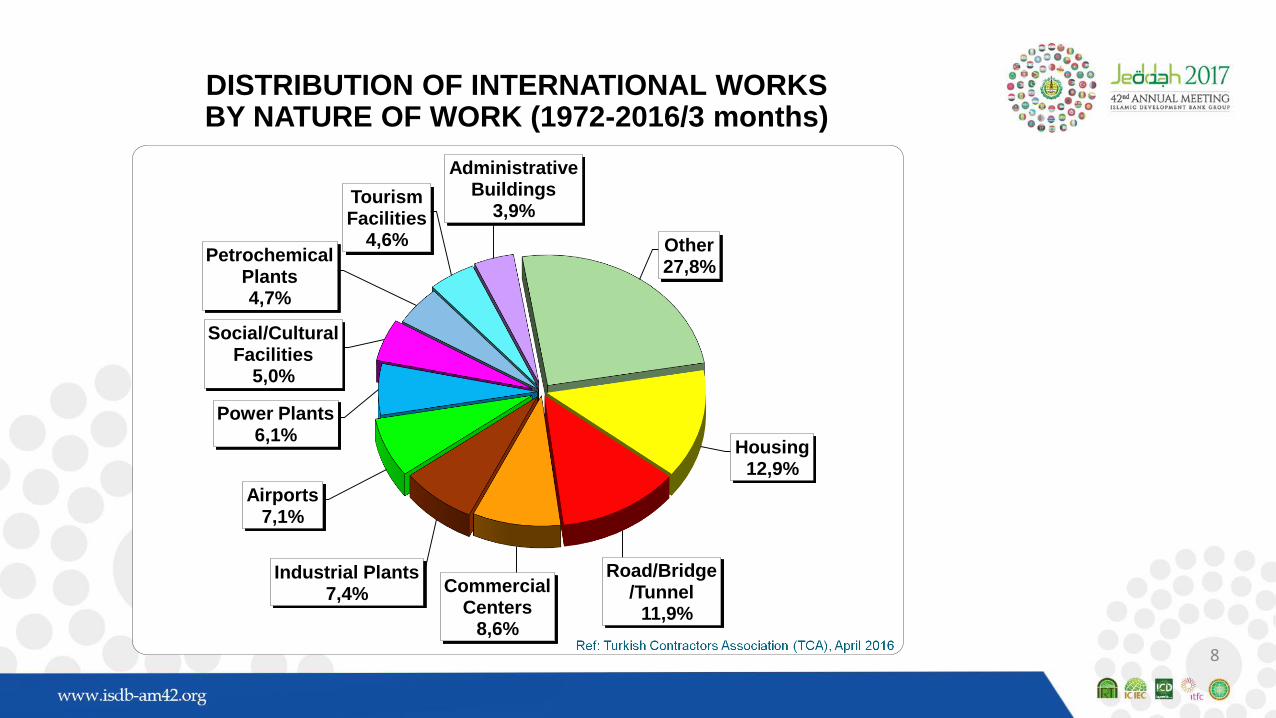

DISTRIBUTION OF INTERNATIONAL WORKS BY NATURE OF WORK (1972-2016/3 months)

Housing12,9%

Road/Bridge/Tunnel

11,9%

CommercialCenters

8,6%

Industrial Plants7,4%

Airports7,1%

Power Plants6,1%

Social/CulturalFacilities

5,0%

PetrochemicalPlants4,7%

TourismFacilities

4,6%

AdministrativeBuildings

3,9%

Other27,8%

8

Main advantages of Turkish Contractors:• high quality and cost effective services at international standards,

• experience and know-how, strong technical and technological

infrastructure,

• risk taking market policies, client satisfaction and skillful management.

•Turkish construction sector is contributing a lot to balance

the payments of Turkey arising from the foreign trade

deficit.

•Construction sector creates new employment areas andcontributes a lot to the employment.

9

YEAR

TOTAL

EMPLOYMENT

EXCLUDING

AGRICULTURE ( people )

EMPLOYMENT IN

CONSTRUCTION

SECTOR

( people )

%

EMPLOYMENT IN

CONSTRUCTION SECTOR

(excluding agriculture)

2005 15.553.000 1.171.000 7.53 %

2006 15.241.000 1.189.000 7.80 %

2007 15.588.000 1.224.000 7.85 %

2008 15.959.000 1.125.000 7.00 %

2009 16.324.000 1.297.000 7.94 %

2010 17.082.000 1.442.000 8.44 %

2011 18.079.000 1.512.000 8.36 %

2012 19.080.000 1.647.000 8.63 %

2013 19.755.000 1.753.000 8.87 %

2014 20.632.000 1.829.000 8.86 %

2015 21.127.000 1.916.000 9.06 %Ref: The Turkish Employers Association of Construction Industries, 2016

10

TURKISH CONSTRUCTION MATERIALS INDUSTRY

• Construction Materials Industry is one of the Turkey’s most competitive

industries in the international arena.

• Among the world’s top 12 producers

• Ranks in the top exporters of construction materials

• Total market size USD 61,5 billion

Domestic market size USD 44,5 billion

Export volume USD 17 billion

• Focus on sustainable development, energy efficiency, nanotechnology,

R&D investments and innovation.

11

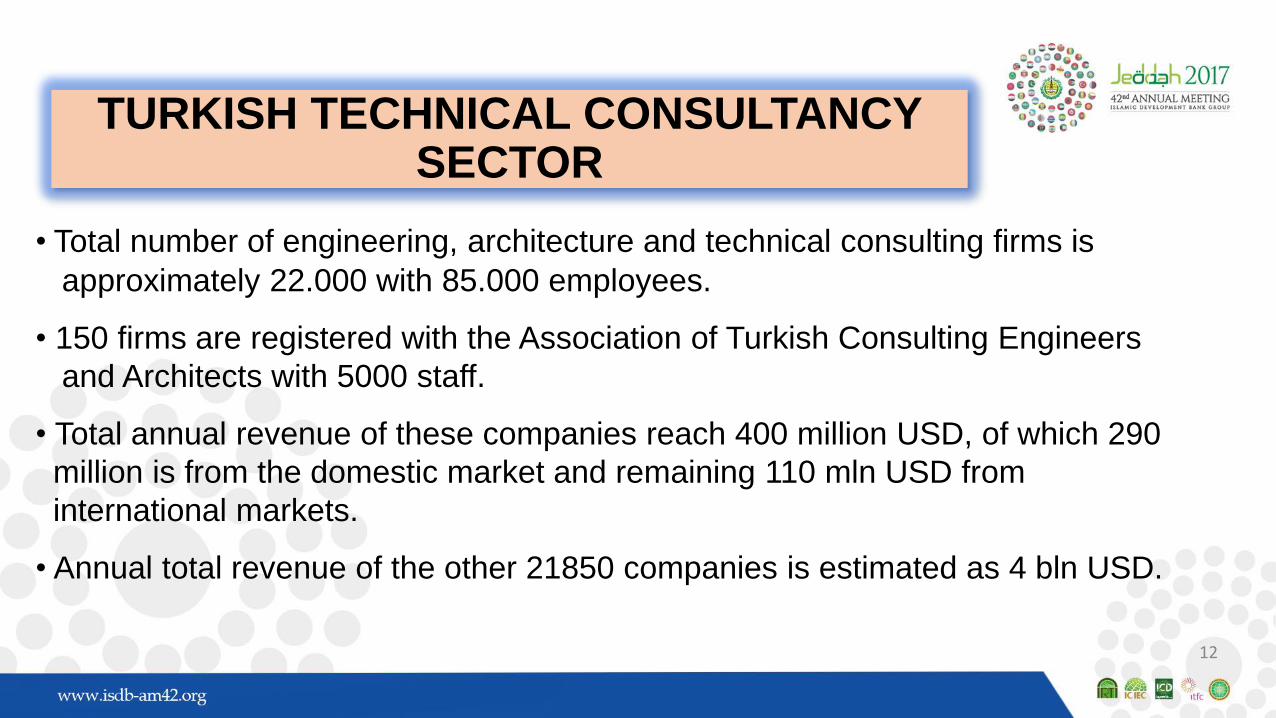

TURKISH TECHNICAL CONSULTANCY SECTOR

• Total number of engineering, architecture and technical consulting firms is

approximately 22.000 with 85.000 employees.

• 150 firms are registered with the Association of Turkish Consulting Engineers

and Architects with 5000 staff.

• Total annual revenue of these companies reach 400 million USD, of which 290

million is from the domestic market and remaining 110 mln USD from

international markets.

• Annual total revenue of the other 21850 companies is estimated as 4 bln USD.

12

• Turkish technical consultancy firms, with their diversified experience gained in

many challenging projects in Turkey and abroad, are also playing an important

role in the booming of Turkish construction industry.

• Some of the Turkish consulting engineering firms are also included in the

ENR Top 200 International Design Firms List since 2010.

• Involved in several projects in more than 40 countries by winning international

tenders financed by international financing institutions and through PPP and

EPC contracts.

• Sustainability, innovation, quality-time-cost control and risk management

are the first priority issues of Turkish consultancy sector.

13

DISTRIBUTION OF TOTAL ANNUAL REVENUES OF MEMBERS OF THE ASSOCIATION OF TURKISH CONSULTING ENGINEERS AND

ARCHITECTS - 2016

more than 20 mln $7,4%

10-20 mln $3,7%

5-10 mln $11,1%

3-5 mln$18,5%

less than 3 mln $59,3%

BY TOTAL VALUE

PUBLIC SECTOR

60,0%

PRIVATE SECTOR

25,0%ABROAD

15,0%

BY SOURCE

14

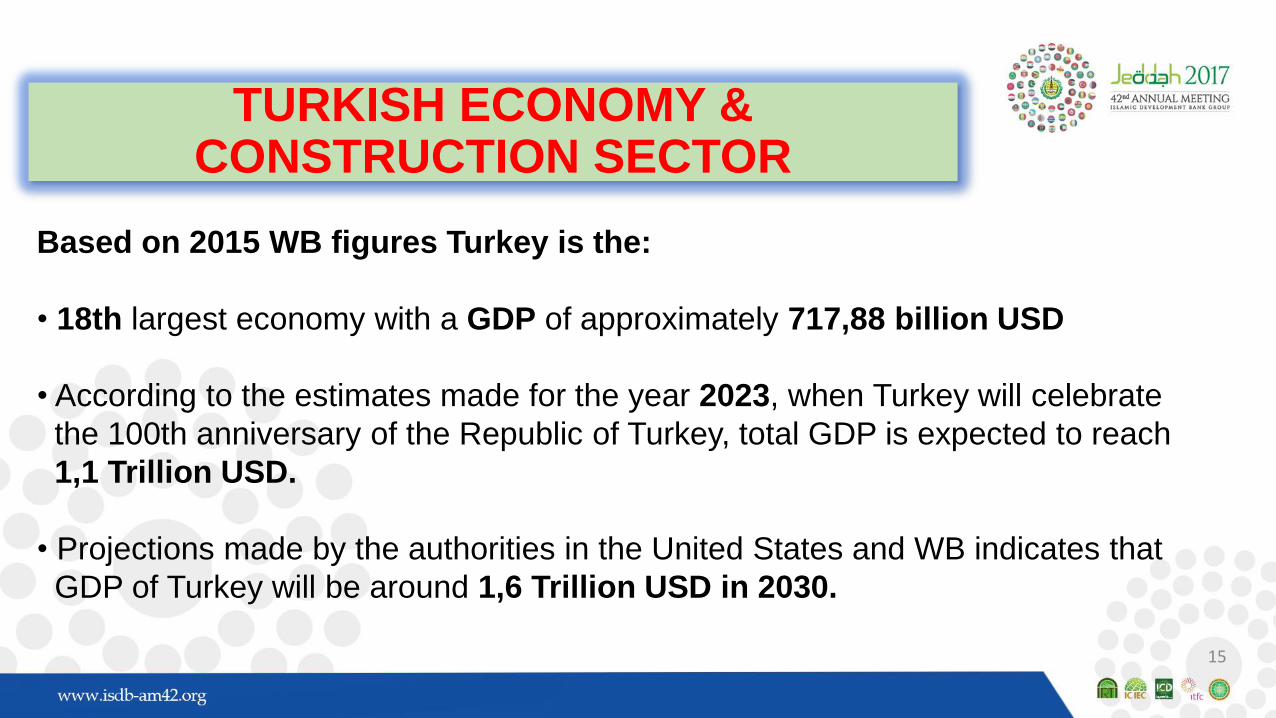

TURKISH ECONOMY & CONSTRUCTION SECTOR

Based on 2015 WB figures Turkey is the:

• 18th largest economy with a GDP of approximately 717,88 billion USD

• According to the estimates made for the year 2023, when Turkey will celebrate

the 100th anniversary of the Republic of Turkey, total GDP is expected to reach

1,1 Trillion USD.

• Projections made by the authorities in the United States and WB indicates that

GDP of Turkey will be around 1,6 Trillion USD in 2030.

15

Based on 2015 GDP figures Turkey is the

18th largest economy in the world (717,88 billion USD)(Ref: World Development Indicators, WB 31 Dec 2016)

Rank Country

GDP

trillion

USD

Rank Country

GDP

trillion

USD

1 United States 18,0 11 South Korea 1,4

2 China 11,0 12 Australia 1,3

3 Japan 4,1 13 Russia 1,3

4 Germany 3,4 14 Spain 1,2

5 United Kingdom 2,9 15 Mexico 1,1

6 France 2,4 16 Indonesia 0,862

7 India 2,1 17 Netherlands 0,752

8 Italy 1,8 18 TURKEY 0,718

9 Brazil 1,8 19 Switzerland 0,665

10 Canada 1,6 20 Saudi Arabia 0,64616

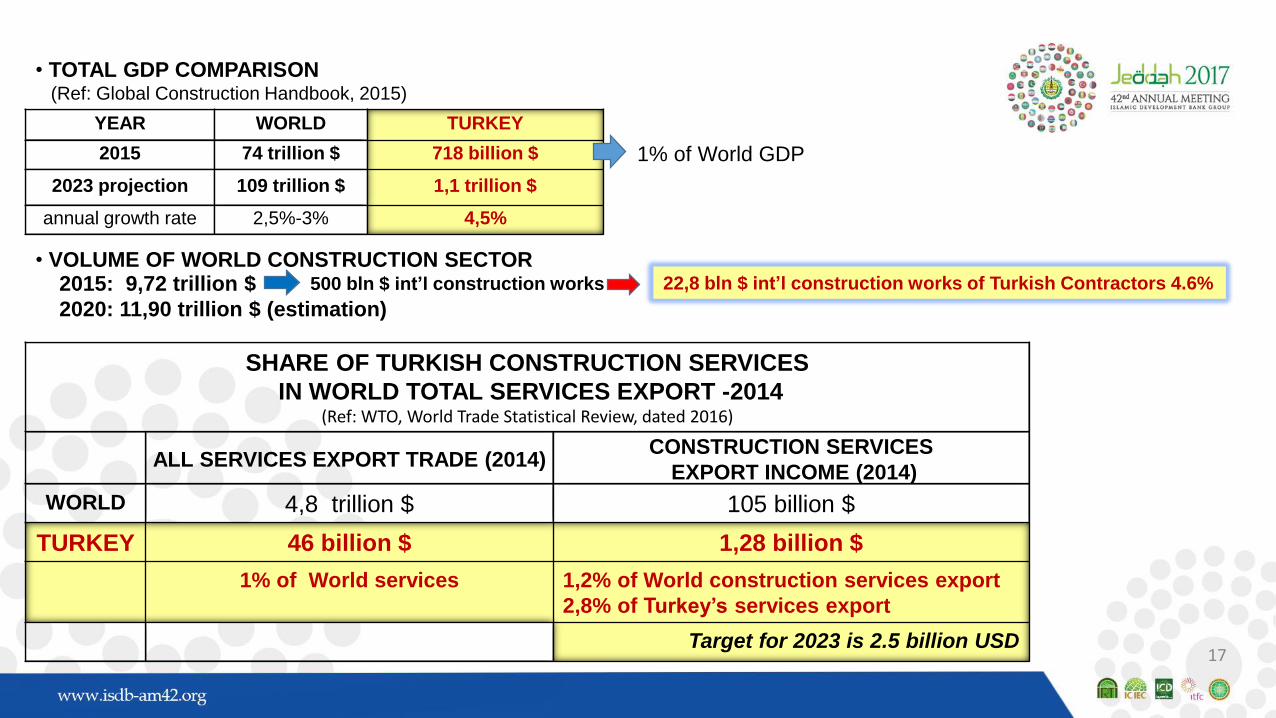

• TOTAL GDP COMPARISON(Ref: Global Construction Handbook, 2015)

• VOLUME OF WORLD CONSTRUCTION SECTOR2015: 9,72 trillion $

2020: 11,90 trillion $ (estimation)

YEAR WORLD TURKEY

2015 74 trillion $ 718 billion $

2023 projection 109 trillion $ 1,1 trillion $

annual growth rate 2,5%-3% 4,5%

1% of World GDP

SHARE OF TURKISH CONSTRUCTION SERVICES

IN WORLD TOTAL SERVICES EXPORT -2014(Ref: WTO, World Trade Statistical Review, dated 2016)

ALL SERVICES EXPORT TRADE (2014) CONSTRUCTION SERVICES

EXPORT INCOME (2014)

WORLD 4,8 trillion $ 105 billion $

TURKEY 46 billion $ 1,28 billion $

1% of World services 1,2% of World construction services export

2,8% of Turkey’s services export

Target for 2023 is 2.5 billion USD17

500 bln $ int’l construction works 22,8 bln $ int’l construction works of Turkish Contractors 4.6%

INTERACTION BETWEEN TURKISH CONSTRUCTION INDUSTRY AND TURKISH

ECONOMY

• Being the leader sector in Turkish economy, growth of construction sector

and growth rate of GDP are closely related. This relation and dependency

is clearly observed on these graphics:

• GDP Growth Rate

• Construction Sector GDP Growth Rate

• Share of Construction Sector GDP

18

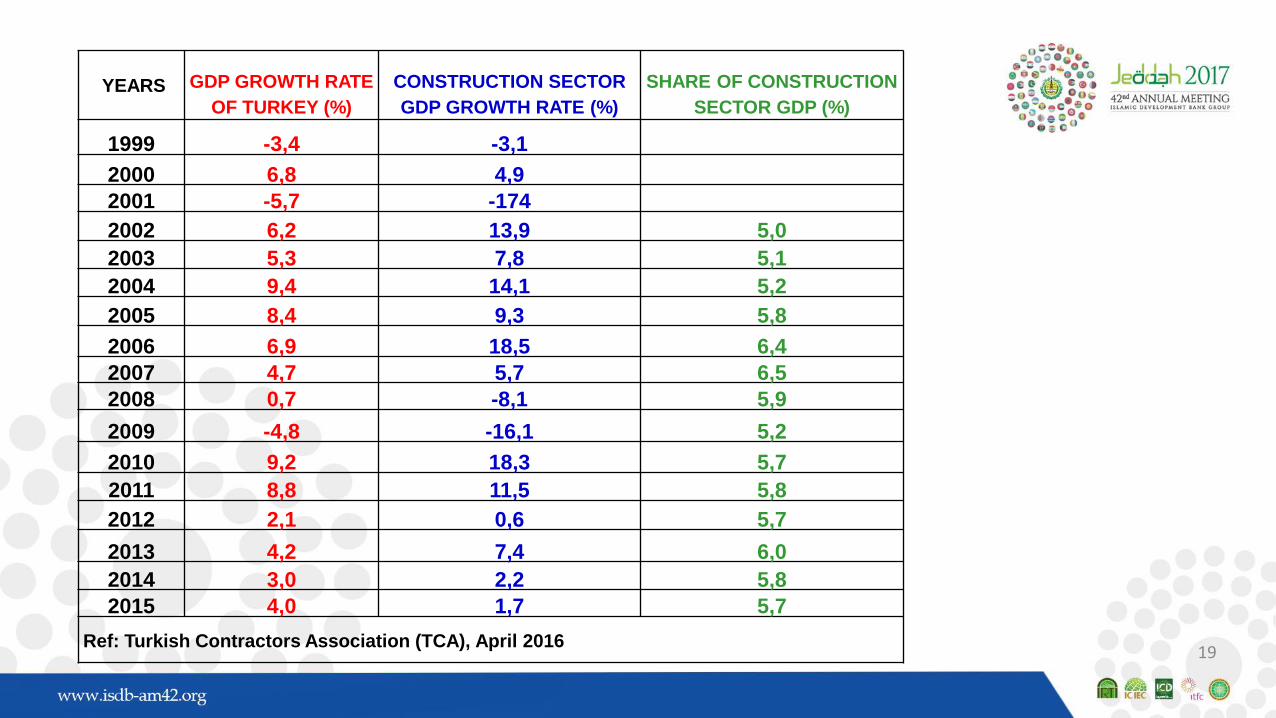

YEARS GDP GROWTH RATE

OF TURKEY (%)

CONSTRUCTION SECTOR

GDP GROWTH RATE (%)

SHARE OF CONSTRUCTION

SECTOR GDP (%)

1999 -3,4 -3,1

2000 6,8 4,9

2001 -5,7 -174

2002 6,2 13,9 5,0

2003 5,3 7,8 5,1

2004 9,4 14,1 5,2

2005 8,4 9,3 5,8

2006 6,9 18,5 6,4

2007 4,7 5,7 6,5

2008 0,7 -8,1 5,9

2009 -4,8 -16,1 5,2

2010 9,2 18,3 5,7

2011 8,8 11,5 5,8

2012 2,1 0,6 5,7

2013 4,2 7,4 6,0

2014 3,0 2,2 5,8

2015 4,0 1,7 5,7

Ref: Turkish Contractors Association (TCA), April 201619

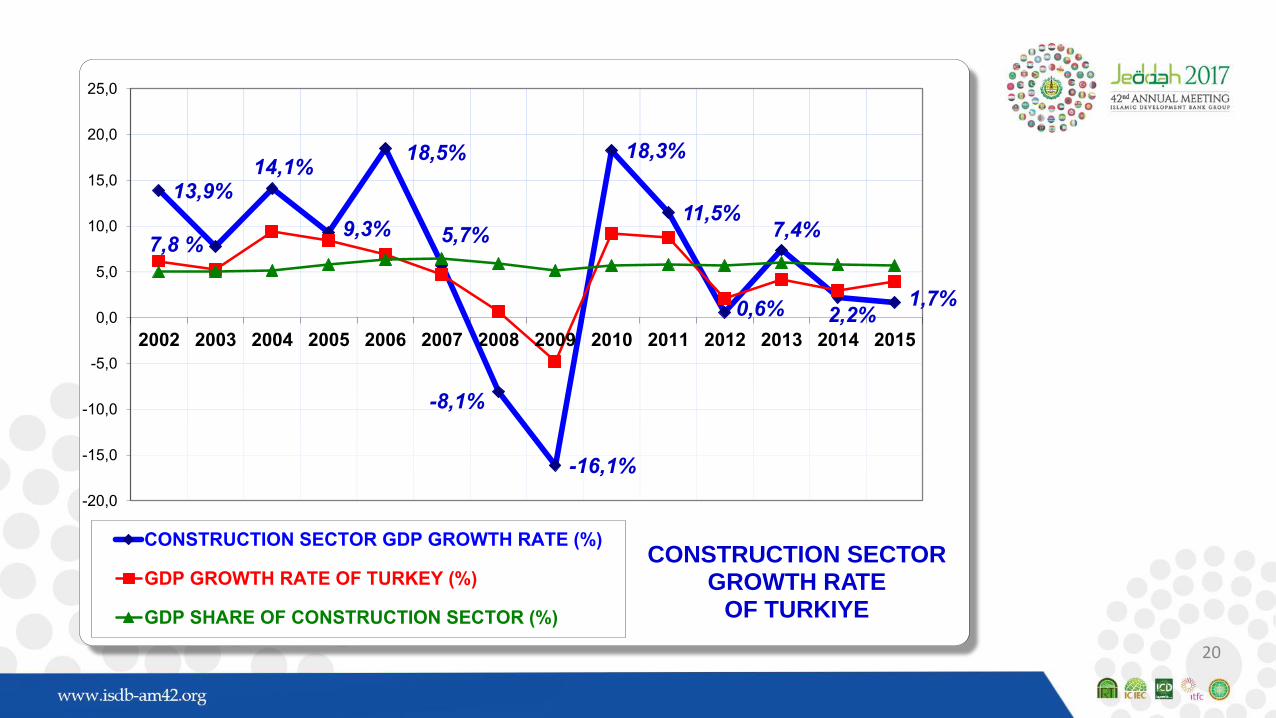

13,9%

7,8 %

14,1%

9,3%

18,5%

5,7%

-8,1%

-16,1%

18,3%

11,5%

0,6%

7,4%

2,2%1,7%

-20,0

-15,0

-10,0

-5,0

0,0

5,0

10,0

15,0

20,0

25,0

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

CONSTRUCTION SECTOR GROWTH RATE

OF TURKIYE

CONSTRUCTION SECTOR GDP GROWTH RATE (%)

GDP GROWTH RATE OF TURKEY (%)

GDP SHARE OF CONSTRUCTION SECTOR (%)

20

• 1999 and 2001 economic crises had a negative impact on the construction sector.

• After recovering, starting from 2002 the sector progressively grew until 2006,

• Then starting from 2007 economy entered into the recession period followed

by 2008 and 2009 crises, consequently construction sector shrunk 8,1% and

16,1% in these years respectively.

• Recovered quickly in 2010 in parallel with the start of large projects in Turkey

and grew by 18.3%; but after 2012 again the growth rate slowed down.

• Due to political uncertainities Turkish construction industry grew by 1.7% in 2015.

21

• Due to the general geo-political problems in the region and negative impacts of global

crises; economic development slowed down at certain periods, and growth of Turkish

construction sector was negatively affected during these periods.

• Due to its interrelations with the other sectors;

• On one hand the inputs used in the construction sector help

developing the production, manufacturing and transport sectors;

• on the other hand the demand for other buildings (housing, education tourism,

industrial buildings) increase the volume of construction activities.

• The power of construction sector for stimulating other sectors accelerates the growth of

Turkish economy.

22

• Construction sector has a potential for bringing foreign exchange and capital to Turkey

which supports Turkish economy during recession periods.

• It should be noted that because of the;

• diversification of markets and specialisations of the contractors,

• continuous demand from the domestic market for implementing

several grand challenging projects

• urban transformation program,

Turkish construction sector managed to overcome the difficult periods.23

Recently there are several ongoing and planned projects financed by

government as well as by local and foreign investors creating demand

for construction industry in domestic market :

With 7 PPP projects totalling USD 44,7 billion, corresponds 40 percent of global PPP investments

(including 3rd Istanbul Airport), Turkey is the global leader of Public Private Investments (2015 Global PPI

Update,WB)

Istanbul 3rd Airport (USD 35.6 bln) is under construction by PPP model.

Until 2023; 5700 km motorways will be constructed by BOT model, 6000 km long highways,

13.000 km railways will be constructed.

60 city hospitals (12 billion USD) will be constructed, most of them by PPP model.

Under the Urban Transformation Project 350 billion USD will be spent.

2 Nuclear power plants are planned to be constructed, total cost 45 bln$.

Trans Anatolian Natural Gas Pipeline is under construction.

Canakkale suspension bridge (3869 m long, the longest span 2023 m). will be constructed ( 3 billion $).

24

As for the international markets:

there are huge investment opportunities in Africa, especially in infrastructure, where the benefits are

expected to be very high. In particular, Sub-Saharan Africa and East Africa are forecast to be the fastest

growing regions in the world over the next five years.

Africa’s absolute and relative lack of infrastructure necessitates establishment of international and regional

cooperation and strategic partnerships. In this regard, African countries are among the main targets for

Turkish contractors, consulting engineers and architects for several ongoing and prospective PPP

and EPC contracts.

Eurasian, Middle East and North African countries are the key markets for the Turkish contractors, as

before. Recently Turkish contractors entered into the Colombia, Venezuela and Peru in South America.

25

CONCLUSION:Contribution of Turkish International Contracting and Technical Consulting ServicesIndustry together with the Construction Materials Industry to Turkish economy is veryimportant as it;• affects the foreign exchange input positively, • enhances economic growth,• contributes to the balance of payments, • increases the export volume, • increases the employment rate, • helps expanding construction machinery capacity of contractors,• contributes to transfer of technology and innovation, • improves quality of locally produced construction materials,• increases the power of competition of Turkey in the international markets.

26

Thank you

27