Embed Size (px)

Citation preview

• INDUSTRY & BUSINESS

Rubber Business at Crossroads Temporary over-capacity has developed in synthetic rubber, but the long-range picture is excellent

C O P O L Y M E R EXPANSIONS started in 1955 and 1956 by the four major rubber companies have doubled synthetic rubber capacity and have produced a temporary surplus of capacity in the industry. Production of all types of synthetic through July had run 3.6''r less than in 1956, but consumption had improved by about 6C4 and was holding at the monthly average of 80,000 tons. As for SBR rubber, production has equaled 70,000 tons monthly. Yet, the Big Four rubber companies alone can boast almost this SBR copolymer capacity. This gives some indication of the size of the over-capacity problem.

Independent producers, such as United Carbon, Phillips, and Shell, are finding competition keen, since they have no assured outlets for more than a small fraction of plant capacity. However, Copolymer Corp. and American Synthetic can place the bulk of their output with their rubber-consuming parent companies. The independents have expanded plant capacity only modestly for the most part, as compared with 70% or larger plant increase for the Big Four. Sales of the independents are down slightly. One independent estimates that present industry capacity will not be needed before I960.

• Litchfield's Latest. In a new issue of "Notes on America's Rubber Industry," P. W. Litchfield, Goodyear's chairman of the board, pleads for a faster build up of synthetic rubber capacity abroad rather than at home. His argument rests on the present lack of balance in synthetic vs. natural rubber consumption in the U. S. (with a ratio of 63 to 37) compared to the rest of the world (ratio of 20 to 8 0 ) . The argument for accelerating synthetic rubber plant construction abroad stems from the fact that there will be little, if any, increase in the world supply of natural rubber, while rubber demand will continue to increase. Litchfield

offers two reasons: New plants of trees will yield no rubber for seven years, while critical needs will begin in two years; new, large scale investments in plantations are just not in the cards in view of political and economic disturbances in major rubber-growing areas. By raising the percentage of synthetic in total rubber consumed abroad to 32 in 1960 and 4 1 in 1965, Litchfield hopes we can "free up the

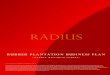

Process Industries trends SYNTHETIC RUBBER Consumption Thousands of Long Tons

50 ^ ^ * * H A I A J I , • Λ *

^ \ \ / / \ :

<s .

k / ν \ Λ /79.0 , ' V/Aug.

j Ι ι ι ι t * ι t ι t * ι < t t ι * ι « t ι t t t 1 \ 1956 1 9 5 7

NATURAL RUBBER Consumpt ion Thousands of Long Tons

;Ay*rvte

! RECLAIMED RUBBER

j Thousand of Long Tons

,

^ * N "

1 *

7Λ '̂ 1 °ι ν » , ! . - . t ' i ' I'T-"*'" t »" ι .r v;:r * t t » * . ι j 1956 1 9 5 7

impending squeeze in natural rubber supply."

• Enter Technology. The missing factor in Litchfield's equation is obviously technology. Possibilities of stretching the fixed available supply of natural rubber range from further improvements in synthetics (enabling them to extend usage beyond the 63 to 37 ratio) to synthetic production of natural rubber. Even though cis-polyisoprene will probably be an expensive material, production plans are now being made. The search for pentane streams which can be dehydro-genated to isoprene is under way. Another approach, taken mainly by Phillips, involves use of polybutadiene as an extender in natural rubber; blending up to equal parts of each doubles the natural rubber supply, but differing properties of polybutadiene isomers have created problems.

Also not to be crossed off as yet is continuing work on Butyl rubber which has certain desirable properties, such as good ozone resistance.

• Butadiene Boom. Although the copolymer end of the rubber business is having its private recession, butadiene operations are still coining money. One independent operator, Petro-Tex, claims to be selling nearly full capacity, variously put at 160,000 to 200,000 tons a year. Odessa Butadiene and Texas Butadiene & Chemical have placed a total of 150,000 tons of capacity on stream within the past few months, but TBC, using one of its alternate processing routes, is mainly making alkylate for aviation gas rather than butadiene. Butadiene producers, including captive operators, are beginning a campaign to increase nonrubber outlets.

• Tire Prospects. At the moment, there appears to be a slight deterioration in the tire business. An unusually high rate of replacement tire shipments in the first quarter placed a damper on business in following quarters. The sustained high rate of new car production, of course, helped new equipment sales, which ran 23 million units through the first eight months, or 12r/r higher than last year. Manufacturers' tire inventories are above last year and are probably on the high side, but were reduced from 16 million units in July to 15.3 million in August, according to reports of the Rubber Manufacturers Association. The outlook for 1958 is promising, as most 1955 cars (with almost 8 million produced) will need replacement tires.

3 0 C & E N N O V . I I , 1 9 5 7