Embed Size (px)

Citation preview

361australiancommodities • vol. 12 no. 2 • june quarter 2005

r u s s i a n o i l a n d g a s

RUSSIAN OIL AND GASimpacts on global supplies to 2020Marina Kim

• In the past few years the Russian Federa-tion has become an important player in world energy markets. Since 2000 it has been ag-gressively increasing oil output to become the world’s largest crude oil producer and the second largest oil exporter. The Russian Federation has the seventh largest proven oil reserves in the world. It is also the world’s leading producer and exporter of natural gas and is expected to maintain its dominant posi-tion in the longer term, backed by abundant reserves.

• The Russian Federation’s energy supplies have major implications for world energy supply security, particularly while the Middle East remains an area of heightened political uncertainty and investment risk. Major Asia Pacifi c energy importers, in particular, are al-ready competing for Russian oil and gas in their pursuit of supply diversifi cation.

Economic overviewAfter the disintegration of the Soviet Union in 1991, the Russian Federation went through a per-iod of deep economic recession. By 1999 the feder-ation’s economy had largely recovered, enabling the start of robust economic growth, further stimu-lated by the expansion of natural resource exports in response to strong world demand. Since 1999 the Russian Federation has recorded its sixth successive year of economic growth (table 1), refl ecting robust domestic consumer spending, and growth in investments and exports.

Economic growth in the Russian Federation is projected to slow to about 4 per cent a year to the end of the current decade and then to average 3.4 per cent a year during the 2010s (IEA 2004a). This is less optimistic than the Russian Government’s projections of the average rate of economic growth of 5–6 per cent a year over the period 2005–08, which is, nonetheless, a slow-down from the average growth rate of 6.8 per cent a year over the period 2000–04.

The projected future deceleration of economic growth results primarily from assumptions about falling world energy prices, in particular oil prices, and export infrastructure constraints. The higher bound of the economic growth projec-tions represents gains from the diversifi cation of the Russian economy away from energy and other commodity exports and from further insti-tutional reforms (MEDT 2005a).

The projected slowdown in economic devel-opment in the medium to long term can also be attributed to the assumed slowing of growth in industrial production, as the share of service activities in the economy increases, and the expected aging and contraction of the Russian population, leading to a decline in the workforce and productive potential (IEA 2004a).

Oil and gas in the Russian economyOil and gas is a major sector of the Russian eco-nomy that plays a key role in providing state bud-get revenues and maintaining positive balance of payments. The sector accounted for 27 per cent of gross domestic product (MEDT 2005b) • Marina Kim • +61 2 6272 2238 • [email protected]

r u s s i a n o i l a n d g a s

362 australiancommodities • vol. 12 no. 2 • june quarter 2005

1 Ru

ssia

’s oi

l fi e

lds

and

pipe

lines

M

ap fr

om W

orld

Ene

rgy

Out

look

200

4, s

uppl

ied

by c

ourte

sy o

f the

Inte

rnat

iona

l Ene

rgy

Age

ncy,

OEC

D, P

aris

r u s s i a n o i l a n d g a s

363australiancommodities • vol. 12 no. 2 • june quarter 2005

and 54 per cent of total exports in 2003 (IMF 2004a). The oil and gas sector is often referred to as the locomotive of the Russian economy because of its signifi cant contribution to the growth in industrial output after the fi nancial crisis of 1998.

Diversifi cation of the Russian economy is likely to reduce the oil and gas sector’s share of gross domestic product, as other economic sectors grow. Further expansion of the sector may also be hindered by insuffi cient explora-tion for natural resources, export infrastructure constraints, and lack of new product develop-ment, such as liquefi ed natural gas (LNG) and petroleum products. Nonetheless, maintaining a rapid rate of economic growth remains depen-dent on strong exports of natural resources, mainly hydrocarbons and metals.

The Russian Government’s target of doubling average GDP per person by 2010 (within a decade of the election of President Putin in 2000) is also likely to provide an additional stimulus to maintain a high level of energy exports at least in the short to medium term.

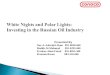

Oil reserves At the end of 2003 the Russian Federation had the seventh largest proven oil reserves in the world and the largest among non-OPEC producers (BP 2004). Various sources estimate Russian proven oil reserves at 60–69 billion barrels (IEA 2004a), equivalent to around a quarter of Saudi Arabian proven oil reserves, the largest in the world. Russian reserves are expected to last for 22 years based on current production (BP 2004).

When probable reserves, which have a smal-ler probability of being produced profi tably,

are included, the estimate rises to 116 billion barrels, with West Siberia accounting for about 74 per cent and the rest split among Volga–Urals/Precaspian, Timan–Pechora, East Siberia and the Far East regions (IEA 2004a; map 1).

Possible reserves, which are in addition to the abovementioned 116 billion barrels and which are likely to be even less profi table for production, are estimated at approximately 30 billion barrels, while undiscovered resources are estimated at 90 billion barrels. Although still dominant, West Siberia’s share in the location of possible reserves and undiscovered resources is expected to decline, while East Siberia’s share is expected to increase signifi cantly. These possible reserves and undiscovered resources are not expected to come into production until the second decade of the century. The potential impact of their devel-opment on Russia’s production profi le is highly uncertain and heavily dependent on the capacity to convert them to proven plus probable reserves and on the rate of development (Lambert and Woollen 2004).

Oil production In 1987 the Russian Federation (excludes former Soviet republics) produced 11.5 million barrels of oil a day, the highest oil production in one country in the history of the oil industry (MIE 2004). Oil production then declined sharply, partly as a result of depressed domestic and inter-national demand, reaching its lowest level in the second half of the 1990s (table 2). Since 2000, oil output, driven mainly by private oil compa-nies (box 1), has risen substantially in response to higher world oil prices and growing external oil demand (IET 2001, 2004, 2005; fi gure A).

1 Key economic indicators Russian Federation

1997 1998 1999 2000 2001 2002 2003 2004Gross domestic product (nominal) – in national currency billion roubles 2 343 2 630 4 823 7 306 8 944 10 834 13 285 16 543 – in US dollars US$b 405 271 196 260 307 346 433 572Growth in real GDP % 1.4 –5.3 6.4 10.0 5.1 4.7 7.3 7.1Population million 147.3 146.9 146.3 145.6 144.8 144.1 143.4 naEnergy consumption Mtoe a 596.8 582.9 604.2 615.2 622.7 619.0 na na

a Million tonnes of oil equivalent. na Not available. Sources: IMF (a,b); IEA (2003); World Bank (2004); IET (2005).

r u s s i a n o i l a n d g a s

364 australiancommodities • vol. 12 no. 2 • june quarter 2005

World oil prices have been relatively high since 1999, driving increases in investments and oil output in the Russian Federation. By 2004, Russian oil production was 50 per cent above its 1999 level. A new oil price spike in 2004 and 2005 has caused signifi cant uncer-tainty about future world oil price dynamics. However, it is expected that the high prices reached in 2004 and 2005 will not be sustained. By 2010, real oil prices are forecast to decline from their present high levels (IEA 2004a; Burg, Haine and Maurer 2005) and reach levels similar to those at the beginning of the current decade — levels that were nonetheless suffi -cient to drive the recent expansion in Russian oil production (table 3). After 2010, world oil prices are projected to increase gradually in real terms (IEA 2004a).

Russian oil production is projected to continue to grow to 2020, although at a slower rate than over the period 1999–2003. The projected easing in world oil prices from their recent highs, along with the rapid expansion

that has already occurred since 1999 is expected to dampen growth in upstream investment and production capacity in the medium term. Addi-tional downward pressure will be exerted by the current tax system in the oil sector in the Russian Federation (box 2).

2 Production, consumption and exports of crude oil and products, and natural gas Russian Federation

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Oil mbd mbd mbd mbd mbd mbd mbd mbd mbd mbd mbd mbd mbd

Production 8.02 7.11 6.38 6.16 6.05 6.14 6.09 6.12 6.49 6.99 7.62 8.46 9.21 aExports of crude oil and products b 3.63 3.41 3.56 3.40 3.67 3.77 3.83 3.84 4.14 4.63 5.28 6.06 6.74 a – to non-CIS c 1.84 2.31 2.63 2.80 3.22 3.37 3.40 3.40 3.73 4.12 4.57 5.24 5.85 a – to CIS 1.80 1.10 0.93 0.59 0.45 0.38 0.44 0.44 0.41 0.51 0.71 0.81 0.89 aDomestic consumption 4.65 3.95 3.04 3.02 2.64 2.65 2.51 2.42 2.47 2.47 2.48 2.61 2.63 a

US$/bbl US$/bbl US$/bbl US$/bbl US$/bbl US$/bbl US$/bbl US$/bbl US$/bbl US$/bbl US$/bbl US$/bbl US$/bbl

Real world oil price d 21.48 18.47 17.61 18.48 21.49 19.67 12.64 18.24 27.50 22.16 22.02 24.66 30.43

Gas bcm bcm bcm bcm bcm bcm bcm bcm bcm bcm bcm bcm bcm

Production 641.0 618.4 607.2 595.4 601.1 571.1 591.0 590.7 584.2 581.5 594.5 620.3 634.0 aExports 194.4 174.4 184.3 192.2 198.5 200.9 200.6 205.4 193.8 180.9 185.5 189.3 200.8 a – to non-CIS 87.9 95.9 109.3 121.9 128.0 120.9 125.0 131.1 133.8 131.9 134.2 142.0 144.4 a – to CIS 106.5 78.5 75.0 70.3 70.5 80.0 75.6 74.3 60.0 48.9 51.3 47.3 56.4 aDomestic consumption 453.6 450.0 426.9 407.1 407.2 374.7 393.4 389.4 394.5 404.7 416.2 439.8 442.0 a

a Estimates. b Totals may not add up as a result of rounding. c Commonwealth of Independent States (CIS) refers to Azerbaijan, Armenia, Belarus, Georgia, Kazakhstan, Kyrgyzstan, Moldova, Russian Federation, Tajikistan, Turkmenistan, Uzbekistan and Ukraine. d Real trade weighted crude oil prices (in constant 2000 US$). mbd = million barrels a day; bbl = barrels; bcm = billion cubic metres.Sources: IET (2001, 2004, 2005); ABARE’s estimates based on US Energy Information Administration data.

Crude oil and refined products industry

19981992 1994 1996 2000 2002 2004

mbd

2

4

8

6

A

CIS export

Domestic consumption

Non-CIS export

Production

Russian Federation

r u s s i a n o i l a n d g a s

365australiancommodities • vol. 12 no. 2 • june quarter 2005

The oil sector in the Russian Federation currently comprises eleven vertically integrated oil compa-nies that produce more than 90 per cent of Russia’s crude oil (table below). There are also a number of project operators under production sharing agree-ments and about 150 small scale oil producers. However, their share in total Russian crude oil output has been steadily declining as a result of less favorable business conditions than for oil majors. The state retains major shares in Rosneft and Gazprom, while other companies have been gradually privatised since the start of the 1990s.

At the end of 2004, the oil sector went through signifi cant restructuring after Yukos’s main producing asset, Yuganskneftegaz, was sold at auction. Yuganskneftegaz, with a production capacity of 1 million barrels of oil a day, became part of the state owned Rosneft, which brings the share of state owned companies in total oil produc-tion to 18.6 per cent.

The gas sector is dominated by Gazprom, the largest gas producing company in the world. Gazprom holds licences to fi elds containing more than 55 per cent of Russia’s proven gas reserves, provides about 20 per cent of state budget revenues, produces 86 per cent of Russia’s gas and supplies it to generate around 50 per cent of electricity in the Russian Federation (OECD 2004). The

company owns and operates a national network of high-pressure interregional gas pipelines and has a monopoly over Russian gas exports to non-CIS countries.

Oil companies and independent gas producers account for about 14 per cent of total indigenous gas production, almost a quarter of which is fl ared. This is largely attributed to unprofi table gas processing and sales conditions for these producers compared to Gazprom. In most cases, these other producers will have to sell gas to Gazprom, or Gazprom has to provide pipeline access to deliver gas to non-Gazprom buyers. Nonetheless, in the government’s Energy Strategy it is expected that the share of non-Gazprom gas in production will reach 20 per cent by 2020 (Government of the Russian Federation 2003). While one of the poten-tial sources of non-Gazprom gas is imports from neighboring central Asian countries, it is highly uncertain whether these supplies will occur as planned. The limited throughput capacity of the pipeline linking central Asian gas reserves with Gazprom’s network, together with the associ-ated political issues, raise serious concerns about stability of supplies. If so, the only way to ramp up supplies of non-Gazprom gas would be to improve pipeline access and gas sales conditions for inde-pendent producers and oil companies.

Box 1: Corporate structure of the Russian oil and gas sector

Corporate structure of oil and gas production in the Russian Federation, end of 2004

Share in Share in Oil production total output Gas production total output

mbd % bcm %

Russian Federation 9.21 100.0 633.95 100.0Lukoil 1.69 18.3 5.02 0.8Rosneft + Yuganskneftegaz 1.47 16.0 10.80 1.7TNK–BP 1.41 15.3 8.00 1.3Surgutneftegaz 1.20 13.0 14.31 2.3Sibneft 0.68 7.4 1.95 0.3Yukos – Yuganskneftegaz 0.68 7.4 2.01 0.3Tatneft 0.50 5.5 0.74 0.1Slavneft 0.44 4.8 0.92 0.1Bashneft 0.24 2.6 0.36 0.1Gazprom 0.24 2.6 544.42 85.9RussNeft 0.13 1.4 0.77 0.1Other producers 0.52 5.6 44.65 7.0

mbd = million barrels a day; bcm = billion cubic metres. Source: IET (2005).

r u s s i a n o i l a n d g a s

366 australiancommodities • vol. 12 no. 2 • june quarter 2005

Oil production in the Russian Federation is projected to reach 10.4 million barrels a day in 2010 and 10.7 million barrels a day in 2020 (IEA 2004a; table 4). If, contrary to current expecta-tions, high world oil prices were to be sustained for a long period, there would be a greater like-

lihood of more rapid expansion in Russian oil output.

These IEA projections are more optimistic than those of the Russian Government in the Energy Strategy of the Russian Federation for the Period up to 2020 (the Energy Strategy), the main offi cial document that sets out priori-ties and goals for Russian energy sector devel-opment for the period to 2020. However, in the past, both offi cial and private projections have consistently underestimated the scale of Russian oil production. Importantly, the Energy Strategy was developed before the strong rise in world oil prices in 2004 and 2005 in response to a combi-nation of sound underlying market fundamen-tals and signifi cant concerns about the security of global oil supply (Burg et al. 2005). These factors have driven Russian oil production and exports to the 2010 levels earlier than projected in the Strategy.

Gas reservesThe Russian Federation is extremely well en-dowed with natural gas reserves. At the end of 2003, Russia’s proven gas reserves amounted to 47 trillion cubic metres, the largest share of total proven gas reserves in the world (26.7 per cent). These are expected to last for more than eighty years at the current rate of production. The country also has an estimated 33 trillion cubic metres of undiscovered gas resources (IEA 2004a).

Three quarters of Russia’s gas reserves and a similar share of current production are located in West Siberia, mostly in the Nadym–Pur–Taz region, followed by the European part of the Russian Federation (to the west of the Ural Mountains), East Siberia and the Far East (IEA 2004a; map 2).

In 2002, 80 per cent of gas was produced at fi elds with declining production (Government of the Russian Federation 2003), which means that signifi cant new capacity will need to come on stream over the next two decades to maintain current rates of production. The Energy Strategy projects that West Siberia will remain the main gas producing region until 2020, although its share in total gas production will decline.

3 Average world real oil pricesIn 2000 US dollars

2001 2003 2010 z 2020 z

US$/bbl US$/bbl US$/bbl US$/bbl

ABARE a 22 25 21 naIEA b na 27 22 26

a Trade weighted crude oil prices. b IEA crude oil import prices. z Projections.Sources: IEA (2004a); Burg et al. (2005) (projections reported in constant 2005 US$ have been converted to constant 2000 US$).

In 2002, a new tax on minerals production (equivalent to a royalty) was introduced as part of tax reform in the oil sector. It replaced a number of earlier oil production related taxes and deductions and simplifi ed the overall tax system. The reform has established the maximum rate of oil export tax, depending on the world oil price. Under the new regime, if the world price for crude Russian Urals oil rose by US$1 above US$25 a barrel, the state budget received 68.5 cents of the extra dollar through the tax on minerals production, export duty and profi t tax.

The tax regime in the oil sector underwent additional signifi cant changes in 2004, leading to an increased tax burden on the sector, partic-ularly on oil exports. The new, more progres-sive, scale of taxation is aimed at withdrawing extra profi t from oil exporters when world oil prices are high. Under the most recent scale, deductions in favor of the state budget rose above 70 cents of an extra dollar if world prices for Russian Urals oil exceed US$25 a barrel. Some sources estimate these deductions at 90 per cent of extra profi t. Sources: IET (2003a); IEA (2005).

Box 2: Tax regime in the oil sector in the Russian Federation

r u s s i a n o i l a n d g a s

367australiancommodities • vol. 12 no. 2 • june quarter 2005

The development of gas fi elds in East Siberia, the Far East, the European part of the Russian Federation (including the Arctic Sea shelf) and Yamal Peninsula are expected to become a priority in the next decade (Government of the Russian Federation 2003). The rate of devel-opment of new gas fi elds will be signifi cantly affected by the ability to raise the required amount of investments (as discussed later).

Gas production Over the period 1992–2004, the Russian Federa-tion remained the world’s largest gas producer, accounting for more than a fi fth of world gas production (IEA 2004b). As with oil, gas production declined after the disintegration of the Soviet Union. However, the reductions were not as great as those for oil (IET 2001; 2004; 2005; fi gure B). Gas output fell to its lowest level of 571 billion cubic metres in 1997 before rising to 634 billion cubic metres in 2004 (table 2). Unlike oil, changes in gas production have been driven mainly by domestic consumption, with low regulated domestic gas prices favoring the uptake of gas against other fuels.

Gas output is expected to expand further in the period to 2020, backed by abundant gas reserves. It is projected to reach 655 billion cubic metres in 2010 and 801 billion cubic metres in 2020 (table 4). Most of the incremental gas produc-tion is likely to be consumed domestically, as the country continues to rely heavily on gas as a primary energy source and the main fuel for heat

and power generation (IEA 2004a). The less optimistic projections of future gas output in the Energy Strategy can be attributed to concerns over declining output from the major producing fi elds in West Siberia and the limited capacity to incur signifi cant investments required to main-tain and further boost gas production.

Investment in the oil and gas sectorInvestment in oil exploration and production has increased in the Russian Federation since the start of the current decade (table 5). Between 2000 and 2003, oil sector investments made up around 35 per cent of total industry invest-ments in the Russian Federation (OECD 2004) and led to marked acceleration in oil produc-tion and exports. The robust growth in oil output

4 Projected growth of oil and gas production and exports to 2020Russian Federation

2004 2010 2020

IEA Energy Strategy IEA Energy Strategy

Oil mbd mbd mbd mbd mbd

Production 9.2 10.4 8.9–9.8 10.7 9.0 – 10.4Exports of crude oil and products 6.7 7.3 6.1–6.8 7.0 6.1–7.0

Gas bcm bcm bcm bcm bcm

Production 634 655 555–665 801 680–730Exports 201 182 a 250–265 249 a 275–280

a Net exports. mbd = million barrels a day; bcm = billion cubic metres.Sources: IEA (2004a); Government of the Russian Federation (2003); IET (2005).

Natural gas industry

19981992 1994 1996 2000 2002 2004

bcm

100

300

200

500

600

400

Russian FederationB

CIS export

Domestic consumption

Non-CIS export

Production

r u s s i a n o i l a n d g a s

368 australiancommodities • vol. 12 no. 2 • june quarter 2005

2 Ru

ssia

’s ga

s re

serv

es a

nd in

fras

truc

ture

M

ap fr

om W

orld

Ene

rgy

Out

look

200

4, s

uppl

ied

by c

ourte

sy o

f the

Inte

rnat

iona

l Ene

rgy

Age

ncy,

OEC

D, P

aris

r u s s i a n o i l a n d g a s

369australiancommodities • vol. 12 no. 2 • june quarter 2005

occurred partly as a result of bringing under-utilised or idle standing facilities into produc-tion, and there is still potential for greater and more effi cient utilisation of existing facilities. However, in the longer term it will be necessary to increase capital investment in new projects to sustain high rates of production.

The size of investment in natural gas explo-ration and production is largely determined by Gazprom, the dominant player in the domestic gas market (box 1). The company needs to make signifi cant investments if it is to maintain current levels of gas production in the medium to long term, as production from mature gas fi elds declines and infrastructure degrades.

The development cost of new large gas fi elds, all of which are located in the harsh Arctic zone, is estimated at US$35–40 billion, excluding necessary gas infrastructure (OECD 2004). Esti-mated reserves of the new gas fi elds are signifi -cant. For example, Yamal Peninsula reserves are estimated at 5.8 trillion cubic metres of gas (Government of the Russian Federation 2003). The high cost of development and lack of new infrastructure may be one of the reasons why Gazprom prefers investing in new smaller fi elds in the vicinity of working giant fi elds in West Siberia to be able to use the existing pipeline system (IEA 2004a).

Another issue is that the low regulated domestic gas prices make it practically impos-sible to raise the required capital for invest-ment, as three quarters of Gazprom’s gas is used domestically.

The total level of capital investment in the Russian Federation, amounting to around 18 per cent of GDP, is still considered low relative to other fast developing economies in eastern Europe and Asia, and relative to the average level of investment in OECD countries of about 22 per cent (table 6).

Concerns over exploration rates for natural resourcesThe Russian Government views insuffi cient exploration of natural resources and a growing share of oil and gas fi elds that are costly to explore and less attractive for investment as a threat to national energy and economic security (Government of the Russian Federation 2003). For example, after an increase of 33 per cent over 2000 and 2001, exploration oil drilling fell by 40 per cent in 2002 and by a further 11 per cent and 18 per cent in 2003 and 2004 respec-

5 Investment in oil exploration and production Russian Federation

Investment Change from 1998

US$m %

1998 2 795 1001999 1 821 682000 4 143 1482001 6 018 2152002 4 679 1672003 a 4 690 168

a January–October. Source: OECD (2004).

6 Capital investment to GDP ratio in selected countries

1995 1996 1997 1998 1999 2000 2001 2002

% % % % % % % %

Russian Federation 21.1 20.0 18.3 16.2 14.4 16.9 18.9 17.9OECD 21.0 21.7 22.3 22.8 22.5 22.5 22.0 21.0Japan 27.7 28.3 27.9 26.8 26.2 26.2 25.6 24.1United States 18.2 18.7 19.1 19.8 20.3 20.5 19.7 18.6Hungary 20.0 21.4 22.2 23.6 23.9 24.1 23.6 22.3Poland 18.6 20.7 23.5 25.1 25.5 23.9 20.9 19.1Korea, Rep. of 36.7 36.8 35.1 29.8 27.8 28.4 27.0 26.8China 40.7 33.8 33.4 35.7 36.4 36.8 38.8 42.2

Source: OECD (2004).

r u s s i a n o i l a n d g a s

370 australiancommodities • vol. 12 no. 2 • june quarter 2005

tively. Similarly, the number of new oil wells put into operation grew by 85 per cent over 2000 and 2001 before falling by 22 per cent in 2002, 5 per cent in 2003 and 1 per cent in 2004 (IET 2003b, 2004, 2005).

The Ministry of Natural Resources has devel-oped a long term program for the development of natural resources for the period 2005–20. It calls for total investment of almost US$90 billion in exploration over fi fteen years, with US$9 billion from the budget and the rest from the mine oper-ators. The 2005 budget provides only US$277 million for natural resources exploration, which needs to be raised to US$756 million a year by 2020 (MNR 2005). It is uncertain whether the government will be able to signifi cantly increase the exploration budget and whether this initia-tive will stimulate increased investment from private investors.

High world oil prices and the current tax system are the most commonly cited reasons for declining investment in oil exploration (IEA 2004a; Mironov and Berezinskaya 2004; Tutushkin, Levinsky and Bushueva 2004). When oil prices are high, companies concentrate on production and exports rather than building up reserves. The current tax regime and macroeconomic conditions also seem to favor short term projects and increased production from working fi elds.

At present, companies do not have the right of fi rst refusal on reserves that they discover. That is, they do not have preference above others to obtain the right to extract the oil they have found. This is an additional disincentive to exploration. Another potential reason for the current decline in exploration activity is that Russian oil companies view their reserves to production ratio as relatively high and therefore do not see the need for making large investments in exploration.

Domestic consumptionRussia’s economic recession at the start of the 1990s resulted in a sharp contraction in domestic primary energy consumption. After reaching a trough of 583 Mtoe in 1998, domestic primary energy consumption in the Russian Federation

started to rise slowly in response to the strong economic recovery and reached 619 Mtoe in 2002 (table 7). While this was considerably less than in 1992, the Russian Federation remained the third largest energy consumer in the world after the United States and China (IEA 2003).

During the period 1992–2002, the share of oil in the primary fuel mix declined from 29 to 21 per cent as a result of reduced industrial consumption and lower use of fuel oil in power generation. However, the share of natural gas rose from 47 per cent in 1992 to over 52 per cent in 2002, maintaining its dominance in both the primary fuel mix and heat and power generation (IEA 2004a).

Total primary energy consumption in the Russian Federation is projected to grow by 1.7 per cent a year until the end of the current decade and then by 1.2 per cent a year in the 2010s as economic growth slows. By 2020 the share of oil in the primary fuel mix is expected to be main-tained at 21 per cent, while the share of gas is projected to increase to 54 per cent as a result of the higher uptake of gas in power generation and the underlying growth in demand for electricity (IEA 2004a; table 7).

In contrast, the Energy Strategy projects a decrease in the share of natural gas in the fuel mix to below 50 per cent by 2020, and increases in the shares of coal, oil, nuclear and hydropower (Government of the Russian Federation 2003). The government’s desire to reduce the share of natural gas in the primary fuel mix refl ects concerns over excessive dependence on gas, which is viewed as an energy security risk.

Oil exportsExternal demand for Russian crude oil has been steadily recovering after the downturn at the start of the 1990s (fi gure A). Some of the factors responsible for the earlier decline included the loss of subsidised former Soviet buyers, the depletion of large oil fi elds as a result of overpro-duction during Soviet times, and the reorganisa-tion of the oil sector (EIA 2005).

Exports of crude oil and refi ned products from the Russian Federation have almost doubled from the historical low of 3.4 million

r u s s i a n o i l a n d g a s

371australiancommodities • vol. 12 no. 2 • june quarter 2005

barrels a day in 1995 to 6.7 million barrels a day in 2004, making the country the second largest oil exporter in the world (table 8).

Non-CIS countries (countries other than for-mer members of the Soviet Union including Latvia, Lithuania and Estonia) accounted for most of the increase in exports, with their share growing from 51 per cent in 1992 to 87 per cent in 2004 (table 2).

As well as exports increasing in absolute terms, the proportion of total oil production exported has also increased markedly. The proportion of exports in the form of crude oil and refi ned prod-ucts in total oil production has grown steadily, from 51 per cent in 1995 to more than 71 per cent in 2004 (IET 2001, 2005). Exports were the main driver of oil sector growth over this

period compared with relatively low domestic oil demand.

Exports of crude oil and refi ned products are projected to grow further to 7.3 million barrels a day in 2010 and then to decline slightly to 7.0 million barrels a day in 2020 (table 4). Growth in domestic consumption, projected to be slower than growth in production in the fi rst decade, will outstrip the pace of production in the second decade, leaving reduced domestic supply of oil available for export (IEA 2004a).

Gas exportsThe volume and share of gas exports in total gas production have remained relatively unchanged since the start of the 1990s. Being sensitive to the

8 Top ten world exporters of oil and natural gas, 2003

Rank Oil exporters Oil exports a Natural gas exporters Gas exports b

mbd bcm

1 Saudi Arabia 8.3 Russian Federation 189.32 Russian Federation 5.8 Canada 102.23 Norway 3.0 Norway 71.04 Iran 2.5 Algeria 63.65 Venezuela 2.3 Netherlands 48.36 United Arab Emirates 2.3 Turkmenistan 42.87 Kuwait 2.0 Indonesia 41.48 Nigeria 1.9 Austria 26.69 Mexico 1.8 Malaysia 24.610 Libya 1.3 United States 19.6

World 45.8 World 783.5

a Net exports. b Exports include pipeline gas and LNG. mbd = million barrels a day. bcm = billion cubic metres.Sources: EIA (2004); BP (2004); IEA (2004c); IET (2005).

7 Total domestic primary energy consumption, Russian Federation

1992 2002 2010 2020

Mtoe % Mtoe % Mtoe % Mtoe %

Coal 132 17.0 107 17.2 118 16.7 125 15.6Oil 221 28.5 128 20.7 149 21.0 171 21.3Gas 364 46.9 326 52.6 371 52.4 433 54.0Nuclear 32 4.1 37 6.0 45 6.4 47 5.9Hydro 15 1.9 14 2.3 16 2.3 17 2.1Other 12 1.6 7 1.1 9 1.3 10 1.2

Total 776 100.0 619 100.0 708 100.0 802 100.0

Mtoe = million tonnes of oil equivalent. Source: IEA (2004a).

r u s s i a n o i l a n d g a s

372 australiancommodities • vol. 12 no. 2 • june quarter 2005

level of domestic gas consumption, exports were sustained over the period 1992–2004 (fi gure B), at around 30 per cent of total gas production. However, the main focus of export supplies has switched to non-CIS countries, whose share grew from 45 per cent of total gas exports in 1992 to a high of 72 per cent in 2004 (table 2).

Net gas exports are projected to increase further to 249 billion cubic metres in 2020, maintaining their share at 31 per cent of total gas production (IEA 2004a). In contrast, the Energy Strategy projects higher export supplies of gas, with the share of exports reaching 38–40 per cent of total gas production in 2020. Larger amounts of gas are expected to become available for export as a result of a projected decline in the share of gas in the primary fuel mix, accentuating the coun-try’s position as the world’s leading exporter of natural gas (table 8). Increased export earnings could also help fi nance investments in the devel-opment of gas reserves (IEA 2002).

Export markets At present more than 90 per cent of Russian oil exports are destined for Europe, including CIS countries (EIA 2005; fi gure C). However, supplies of Russian oil to Europe are unlikely to expand signifi cantly over the next ten to fi fteen years. This refl ects the partial redirection in oil exports to other markets, such as the Asia Pacifi c in order to take advantage of oil price differential and the European market’s preference for higher quality Middle Eastern oil.

By 2020, the share of oil exports destined for Europe is projected to decline to 60 per cent (MIE 2004), while the share going to the Asia Pacifi c region is projected to reach 30 per cent from about 3 per cent in 2003.

Europe and the CIS are also the main markets for Russian gas exports (table 9). Currently, Russian gas provides almost a quarter of OECD Europe’s total gas needs (IEA 2004a), with gas supplied mainly on the basis of long term contracts (up to 25 years) on ‘take or pay’ condi-tions. Sales volumes under existing contracts amount to 2 trillion cubic metres of natural gas (Gazprom 2004a). Although European gas demand is expected to remain the primary driver

of Russian gas exports until 2020, the share of gas exports to the Asia Pacifi c region is expected to reach 15 per cent by 2020 from nil at present (Government of the Russian Federation 2003).

The Russian Federation has long been exploring ways to export oil and gas to the Asia Pacifi c, where China, Japan and Korea are the primary markets. This intent is strongly backed by reciprocal interest from large energy importers in the region, who seek to diversify their supply sources outside the Middle East and ensure regional energy security.

9 Top ten recipients of Russian natural gas exports, 2003 a

Rank Country Imports

bcm

1 Germany 37.32 Italy 19.43 Belarus 19.04 Turkey 12.65 Hungary 11.06 France 10.67 Poland 7.28 Czech Republic 7.09 Romania 5.810 Finland 5.0

Total of above countries 134.9

Total all markets 189.3

a Data are provisional for the OECD and are estimates for the non-OECD countries. bcm = billion cubic metres.Source: IEA (2004b).

Crude oil export destinations, 2003

2010 155%

JapanChinaTurkey

United StatesOther western Europe

GreeceSpain

ScandinaviaNetherlands

FrancePoland

ItalyOther central Europe

Germany

Other

CISC

r u s s i a n o i l a n d g a s

373australiancommodities • vol. 12 no. 2 • june quarter 2005

The IEA has recently urged China, Japan and Korea to work together with the Russian Federa-tion to develop Siberian oil and gas resources, as these are projected to become a major source of energy supplies to Asia (Hardy 2004). A major deal for supply of Siberian oil to the Asia Pacifi c region has recently been fi nalised by Rosneft, the new owner of Yuganskneftegaz, with expected exports of approximately 1 million barrels of oil to China until 2010, via railroad.

The Sakhalin Island projects have resulted in a major development of oil and gas resources in the Russian Far East. Sakhalin-1 and Sakhalin-2 have been implemented by a consortium of Russian and foreign companies on the basis of production sharing agreements which are discussed later. The planned Sakhalin-3 oil and gas project is very large and incorporates three smaller projects that are comparable with Sakhalin-1 and Sakhalin-2. Sakhalin-4 and Sakhalin-5 are also in the pre-paratory stages. The combined output of these projects will signifi cantly exceed projected local and regional energy needs, with large volumes becoming available for export to neighboring countries and elsewhere.

North America is another important pros-pective market for Russian oil and gas. The promotion of oil and gas exports to the United States is the focus of US–Russian energy cooperation (White House 2005). However, the initiatives underlying this energy cooperation so far seem to lack signifi cant support from the parties involved. Additional factors associated with slow progress in this export direction are the geographic remoteness of the market, and the United States being a large regional gas producer itself. However, recent shortages in supply of natural gas in the region, followed by a signifi cant price hike, could stimulate progress on gas projects for exports to north America.

Development of oil and gas export infrastructure

The Russian Federation has an extensive system of oil and gas pipelines, refl ecting the inland location of major oil and gas reserves. More than 80 per cent of Russian oil was exported

via pipelines in 2003, either cross-border or to sea terminals (OECD 2004). Higher oil prices in recent years have made rail and barge trans-port viable economic alternatives despite their higher costs relative to that of pipelines. The gas pipeline system, the longest in the world (over 150 000 kilometres), also serves as the main transport mode for delivering Russian gas to external markets.

With oil production and exports increasing, limited oil transport capacity has emerged as one of the key constraints to further export expan-sion. Declining demand from eastern Europe and CIS countries has resulted in oil exports being redirected to other international markets, mainly western and northern Europe. Major bottlenecks are occurring at the ports and in the pipelines supplying those markets, especially on the Black Sea.

Development of oil export pipeline infrastruc-ture has been identifi ed as one of the priority tasks of the Russian Government, with the Baltic Pipeline System, East Siberia – Pacifi c Ocean and West Siberia – Barents Sea routes being of key importance (table 10).

Exports to EuropeRussian crude oil fl ows to Europe through the Druzhba pipeline system and via Russian oil ports on the Baltic and Black Seas (map 1). The Druzhba pipeline with a capacity of 1.3 million barrels a day, was built in Soviet times and remains the main artery for Russian crude oil exports to eastern Europe. The Latvian Baltic port of Ventspils was the main outlet for Russian crude oil destined for northern European markets until Transneft, the state operator of the national oil pipeline system, built its own Baltic terminal at Primorsk, on the Gulf of Finland, as part of its Baltic Pipeline System (BPS) in late 2001. The recently approved expansion of BPS capacity to 1.2 million barrels a day is one of Transneft’s major projects and is expected to be completed by late 2005 – early 2006.

The Russian Black Sea ports of Novoros-siysk and Tuapse, as well as the Ukrainian port of Odessa, are used to reach western European markets (IEA 2002). Black Sea ports are running at full capacity, and there is little additional

r u s s i a n o i l a n d g a s

374 australiancommodities • vol. 12 no. 2 • june quarter 2005

throughput potential. Congestion is also occur-ring because of bad weather conditions and bottlenecks on the Turkish Straits.

Two major proposals were developed to bypass the Turkish Straits — building an oil pipeline across the Turkish territory to the Aegean coast (Trans-Frakian Kiyiköy–Ibrikhaba route) or building one through Bulgaria and Greece (Burgas–Alexandrupolis route). Neither project has made much progress since they were proposed several years ago (Transneft 2004; Krutikhin 2005), perhaps because of the poten-tial decline in the attractiveness of the European market for Russian oil supplies in the medium to long term.

Russia’s natural gas exporting strategy to Europe is based on new large scale projects, offshore resources development in the north and the Yamal Peninsula projects. These undertak-ings may require investments of tens of billions of dollars, and their realisation is likely to depend on favorable prices for natural gas and large markets being secured to allow investment funds to be mobilised.

In the medium term, however, rising compe-tition and liberalisation of European energy markets do not provide suffi cient guarantees that these projects will be implemented. Moreover, it is likely that European importers of natural gas will be interested in diversifi cation of supplies to enhance energy security, thus reducing dependence on Russian imports, provided that

greater security of alternative gas supplies can be ensured.

Exports to Asia Pacifi c marketsOne of the major proposed projects for supplying Russian oil to the Asia Pacifi c region is the construction of a 1.6 million barrels a day pipe-line from East Siberia ending near the Russian Pacifi c port of Nakhodka, enabling shipments to Japan, Korea, China and the United States (map 1). The pipeline’s construction faces several major diffi culties, including high pipeline construction costs, technical complexity of the project, the need for costly greenfi eld oil developments in West and East Siberia, and the possibility of the pipeline’s underutilisation. In late 2004 the Russian Government commissioned a feasibility study of the project, with the results expected in mid-2005.

The major potential sources of Russian gas for Asia are East Siberia and the Far East, which together are scheduled to produce up to 50 billion cubic metres of natural gas a year by 2010, and up to 110 billion cubic metres by 2020 (Government of the Russian Federation 2003). A large scale project for supplying Russian gas to the Asia Pacifi c region involves building a pipeline from East Siberia to Dalian and Beijing in China, with an undersea branch to Korea (map 2). However, the export prospects of the project seem some-what unclear at present, as Gazprom, the coordi-nator of Russian gas exports to the Asia Pacifi c

10 Major existing and proposed oil pipelines and sea terminal capacities for export and transit of oil from the Russian Federation to non-CIS destinations

2003 2005 2010 2015 2020

mbd mbd mbd mbd mbdTransport systemBaltic Pipeline System (BPS) – sea port of Primorsk 0.60 1.20 1.20 1.20 1.20Other north western sea ports 0.12 0.30 0.30 0.30 0.30Druzhba pipeline 1.27 1.33 1.33 1.33 1.33Transneft a pipeline system – Black Sea ports 1.26 1.26 1.26 1.26 1.26Caspian Pipeline Consortium (CPC) b 0.4 0.56 1.4 1.4 1.4East Siberia (Taishet) – Pacifi c Ocean 0.6 1 1.6West Siberia – Timan-Pechora – Barents Sea 1 1.6

Total 3.64 4.65 6.09 7.49 8.69

a Monopoly state operator of the Russian trunk pipeline system. b CPC connects Kazakhstan’s Tengiz oil fi eld with the sea terminal near Russian port of Novorossiysk. mbd = million barrels a day.Source: MIE (2004).

r u s s i a n o i l a n d g a s

375australiancommodities • vol. 12 no. 2 • june quarter 2005

region, appears to prioritise Sakhalin Island proj-ects over East Siberian gas developments.

The Sakhalin Island projects are renowned for their gas export initiatives; however, there are also plans for oil production and exports. While

Japan is the proposed destination for Sakhalin-1 gas, recent reports suggest that the fi nal destina-tion of Sakhalin-1 gas is not decided yet, with northern China being mentioned as one of the potential buyers. The limited national gas pipe-

East Siberia – Pacifi c Ocean oil pipelineThe proposal for an oil pipeline from Taishet in East Siberia to the Pacifi c Ocean was developed in accordance with the Energy Strategy and based on the long term forecasts of oil production and consumption in the Russian Federation and future demand from Asia Pacifi c markets. Oil is to be supplied from the West and East Siberian fi elds. The Russian Government’s decision in late 2004 to commission a feasibility study for the East Siberia–Pacifi c Ocean route has ended the decade long rivalry between China and Japan for the pipeline’s destination, practically supporting Japan’s option. However, a potential branch to China’s Daqing, favored by China, has not been fully dismissed yet. If built, the Taishet–Nakhodka pipeline would be one of the longest in the world (4130 kilometres), over harsh terrain. The state monopoly over oil pipelines eliminates private capital participation in the project, which is estimated at US$11–16 billion, and leaves the burden of raising the required funds solely in Transneft. The costs of bringing on additional capacity from greenfi eld developments in West and East Siberia are likely to be consider-ably higher than for existing brownfi eld projects in West Siberia (IEA 2004a), leaving aside the possi-bility of underutilisation of the expensive pipeline. The proposed high transport tariff could also place restrictions on export volumes.

Irkutsk gas projectThe project to supply natural gas to China and Korea via a pipeline from the Kovykta gas fi eld near Irkutsk in East Siberia was proposed by RUSIA Petroleum with British–Russian TNK–BP as its major shareholder. Explored reserves of the Kovykta fi eld are deemed suffi cient to produce more than 30 billion cubic metres of natural gas a year for over thirty years (RUSIA Petroleum 2004). However, Gazprom, which was appointed by the Russian Government as a coordinator of gas

developments in East Siberia and the Far East and gas exports to the Asia Pacifi c region, is report-edly prioritising Sakhalin projects over Irkutsk gas developments. There are still a lot of issues, which need to be resolved before the project can proceed. Project implementation is likely to prog-ress at a faster rate once Gazprom and TNK–BP reach an agreement on Gazprom’s participation in the project.

Sakhalin Island oil and gas projectsTotal recoverable reserves of the Sakhalin-1 project area are estimated at 2.3 billion barrels of oil and 485 billion cubic metres of natural gas. The Sakhalin-1 project is expected to produce approxi-mately 0.25 million barrels of export quality oil a day by the second half of the current decade (Sakhalin-1 2005). For gas exports, the Sakhalin-1 project consortium plans to build a pipeline with a design capacity of 8 billion cubic metres a year, which could run to Japanese Hokkaido Island with an extension to the Niigata or Tokyo area. The recoverable reserves of the Sakhalin-2 main project fi elds are estimated at 1 billion barrels of oil and more then 500 billion cubic metres of gas. The Sakhalin-2 project currently produces about 0.07 million barrels of oil a day during the summer season, but is expected to produce oil all year round from 2006 (Sakhalin Energy 2004). The project consortium has recently signed long term agreements with Japanese and Korean utility companies for the supply of almost 5 million tonnes of LNG a year (7 billion cubic metres), with the fi rst contracts to start in 2007. The project consortium has also fi nalised a contract to supply 1.6 million tonnes of LNG a year (2.2 billion cubic metres) over twenty years to the Energia Costa Azul future terminal in Mexico on the west coast of north America. This deal brings the total volume of natural gas committed from the Sakhalin-2 project to 7 million tonnes a year (10 billion cubic metres).

Box 3: Major export projects targeting the Asia Pacifi c region

r u s s i a n o i l a n d g a s

376 australiancommodities • vol. 12 no. 2 • june quarter 2005

line network in Japan and competition from the East–West pipeline in China create barriers to the imports of Russian pipeline gas. The predomi-nant reliance of prospective gas buyers, such as Japan and Korea, on LNG also forces Russian gas producers to seek alternatives to pipeline supplies, such as LNG.

The Sakhalin-2 project consortium is building the fi rst Russian LNG plant in Prigorodnoye on the south of Sakhalin, which is scheduled to reach its design capacity of 9.6 million tonnes of LNG a year in 2008. Sakhalin-2 has already signed long term agreements for supply of LNG to Asia Pacifi c and north American markets (box 3).

Exports to north AmericaA major proposal for oil exports to north America involves constructing a pipeline with a design capacity of 1.6 million barrels of oil a day from West Siberia to the Murmansk port on Barents Sea, or building a new port at Indiga on the Barents Sea as an alternative pipeline desti-nation (map 1). The north American project faces a number of counterarguments including potentially insuffi cient reserves of light crude oil preferred by the north American market, lack of support from the United States, and more importantly the need to compete with the higher quality oil supplies from the Middle East (Vain-shtock 2004), which could result in less favor-able prices for Russian oil exports.

Although north America is considered the main market for the West Siberia – Barents Sea route, it could potentially become a more cost competitive way of shipping Russian crude oil to closer European markets. This, however, may make it a potential competitor with the Baltic Pipeline System, Transneft’s current priority, partly explaining its willingness to put off the project until later in the decade.

North American gas projects envisage LNG supplies either from the port of Murmansk on the Barents Sea or from an LNG terminal on the Gulf of Finland near St Petersburg (box 4). Before the start of direct exports from the Barents Sea, Gazprom plans to swap its pipeline gas exports to Europe with LNG to be shipped to the United States, with shipments potentially starting as early as this year (Platts 2004). The

north American export projects appear to receive less priority compared with the Asia Pacifi c proj-ects, perhaps as a result of lack of support from the parties involved.

ConclusionsSince the end of the 1990s the importance of the Russian Federation as a major world oil and gas supplier has increased. It is currently the world’s largest gas exporter and the second largest oil exporter. Oil and gas supplies are backed by abundant indigenous reserves.

The potential for future supplies of oil and gas to the international market is signifi cant. Oil production is expected to continue to grow, although at a slower rate than over the past few

A potential gas supplier for the north American market is the Shtokmanovskoye fi eld in the Barents Sea shelf, capable of producing up to 60 billion cubic metres of gas a year, with the full period of development being fi fty years (Rosneft 2004). The project envisages construc-tion of an offshore production platform, an LNG plant and an export terminal near the ice-free port of Murmansk on the Kola Peninsula. Gazprom, the sole owner of the Shtokmanovs-koye fi eld, plans to decide on an international project partner(s) this year, followed by supply deals later in 2005 and 2006 (Platts 2004). Start of production is currently scheduled for 2010, with the United States a primary destination for LNG supplies.

Another potential option to expand LNG supplies to north America is building an LNG terminal in the Gulf of Finland near St Petersburg. Gazprom and PetroCanada signed a memorandum of understanding to look at the feasibility of constructing an LNG plant in the Leningrad region and the possibility of LNG supplies to a terminal in Canada by 2009 (Gazprom 2004b). The Canadian terminal could provide Gazprom faster access to the US market given the slow pace of approval of new LNG import terminals in the United States.

Box 4: LNG projects for the east coast of north America

r u s s i a n o i l a n d g a s

377australiancommodities • vol. 12 no. 2 • june quarter 2005

years, and to exceed 10 million barrels of oil a day by 2020. Oil exports are projected to expand from 6.7 million barrels of oil a day in 2004 to approximately 7.3 million barrels a day by 2010, before declining slightly to 7.0 million barrels of oil a day by 2020. These projections are based on the expectation that the recent spike in oil prices will be temporary. If, however, a sustained period of high prices were to eventuate, higher future Russian oil production and exports could be expected.

Natural gas production and exports could reach 801 and 249 billion cubic metres a year by 2020 up from 634 and 201 billion cubic metres respectively in 2004. The ability to reduce the dominant share of natural gas in the domestic primary fuel mix (currently over 50 per cent) could free up more gas for export.

The key barriers to future expansion of export supplies include the signifi cant levels of investment required in oil and gas exploration and production, the need to stabilise the busi-ness climate and improve the tax regime, and the ability to expand export infrastructure and diversify export markets. Implementation of these conditions could stimulate Russian energy supplies to exceed the projected levels.

At present, Europe remains the largest external market for Russian oil and gas. However, the competitiveness of European energy markets and aspirations for regional diversifi cation of supplies may reduce the future attractiveness of the European market for Russian oil and gas exporters.

The Asia Pacifi c and north American regions are promising new markets for Russian oil and gas. Advancing these export directions requires building new lengthy and costly pipelines; signifi cant greenfi eld investments in the unde-veloped oil and gas resources in East Siberia, the Far East, and the Arctic Sea shelf; the devel-opment of new products, including LNG; and strong commitment from the parties involved. The ability to successfully resolve these chal-lenges and address the earlier mentioned barriers will determine whether the Russian Federation can become a truly global supplier of oil and gas and a new stabilising force in the world energy market.

References

BP 2004, BP Statistical Review of World Energy 2004, BP, London.

Burg, G., Haine, I. and Maurer, A. 2005, ‘Energy outlook to 2010’, Australian Commodities, vol. 12, no. 1, March quarter, pp. 90–102.

EIA (Energy Information Administration) 2004, Top Petroleum Net Exporters, 2003, US De-partment of Energy, Washington DC, August

(www.eia.doe.gov/emeu/security/topexp.html).—— 2005, Russia Country Analysis Brief, US

Department of Energy, Washington DC, Feb- ruary (www.eia.doe.gov/emeu/cabs/russia.html).Gazprom 2004a, Gas supplies to non-CIS coun-

tries (in Russian), reference source, Moscow, 17 June (www.gazprom.ru/articles/ru/articles/article12545.shtml).

—— 2004b, Gazprom and Petro-Canada signed a memorandum on mutual understanding, press release, 12 October (www.gazprom.com/eng/news/2004/10/14194.shtml).

Government of the Russian Federation 2003, Energy Strategy of the Russian Federation for the Period up to 2020, Ministry of Energy, Moscow.

Hardy, A. 2004, East Asians fi ghting over pea-nuts says IEA, EnergyReview.Net, Asper-mont Limited, Perth, 19 November.

IEA (International Energy Agency) 2002, Russia Energy Survey 2002, OECD/IEA, Paris.

—— 2003, Energy Balances of Non-OECD Countries, OECD/IEA, Paris.

—— 2004a, World Energy Outlook, OECD/IEA, Paris.

—— 2004b, Natural Gas Information, 2004 Edition, OECD/IEA, Paris.

—— 2004c, Key World Energy Statistics, OECD/IEA, Paris.

—— 2005, Oil Market Report, OECD/IEA, Paris, 11 April.

IET (Institute for the Economy in Transition) 2001, Russian Economy in 2000: Trends and Perspectives, Issue 22, Moscow.

—— 2003a, Tax Reform in Russia: Issues and Solutions, vol. 2, Moscow.

—— 2003b, Russian Economy in 2002: Trends and Perspectives, Issue 24, Moscow.

r u s s i a n o i l a n d g a s

378 australiancommodities • vol. 12 no. 2 • june quarter 2005

—— 2004, Russian Economy in 2003: Trends and Perspectives, Issue 25, Moscow.

—— 2005, Russian Economy in 2004: Trends and Perspectives, Issue 26, Moscow.

IMF (International Monetary Fund) 2004a, Rus-sian Federation: Statistical Appendix, IMF Country Report No. 04/315, Washington DC.

—— 2004b, World Economic Outlook Database, Washington DC, September 2004 (www.imf.org/external/pubs/pubs/ft/weo/2004/02/data/dbginim.cfm).

Krutikhin, M. 2005, ‘Balkan route: the oil industry formulates conditions of Burgas-Alexandrupolis pipeline construction’ (in Russian), RusEnergy, Moscow, 3 March.

Lambert, T. and Woollen, I. 2004, ‘View of 12 million b/d Russian output by 2010 places focus on export limits’, Oil and Gas Journal Online, PennWell, Tulsa, Oklahoma, 26 July.

MEDT (Ministry of Economic Development and Trade of the Russian Federation) 2005a, Scenarios of the Social and Economic Develop-ment and Main Indicators of the Consolidated Financial Statement of the Russian Federation for 2006 and for the Period to 2008, Moscow, April (www.economy.gov.ru).

—— 2005b, Program for Social and Economic Development of the Russian Federation for the Mid-term Outlook (2005-2008), Draft revised and submitted to the Government of the Rus-sian Federation on 5 February, Moscow.

MIE (Ministry of Industry and Energy) 2004, Speech of the Minister of Industry and Energy of the Russian Federation Viktor Khristenko at the IV annual Russian Oil and Gas Week, press release, Moscow, 26 October (www.mte.gov.ru/fi les/2166/2287.Doklad_VNNG.pdf).

Mironov, V. and Berezinskaya, O. 2004, Natural rent: oil industry freezes (in Russian), Vedo-mosti, # 214 (1254), Business News Media, Moscow, 22 November.

MNR (Ministry of Natural Resources of the Russian Federation) 2005, Minister of Natural Resources of the Russian Federation Yuri Trutnev made a speech on the actions taken

for replacement, preservation and economic utilisation of the natural resources and devel-opment of mineral-raw base in the Russian Federation, Moscow, 11 February (www.mnr.gov.ru/part/?act=print&id=82&pid=11.

OECD (Organisation for Economic Coopera- tion and Development) 2004, OECD Economic Survey of the Russian Federation 2004, OECD, Paris.

Platts 2004, ‘Gazprom Sakhalin door ‘opens’’, International Gas Report, Issue 509, New York, 8 October.

Rosneft 2004, Shtokmanovskoe gas-and-condensate fi eld, Moscow (www.rosneft.ru/english/projects/stockmanovskoye.html).

RUSIA Petroleum 2004, Kovykta Project – Mar-kets, Irkutsk, Russia (www.rusiap.ru/kovykta/market.html).

Sakhalin-1 2005, Project Information – Overview, Yuzhno – Sakhalinsk, Russia (www.sakhalin1.ru).

Sakhalin Energy 2004, Project Overview, Yuzhno – Sakhalinsk, Russia (www.sakhalinenergy.ru).

Transneft 2004, Trans-Frakian oil pipeline is under development, Moscow, 28 May (www.transneft.ru/Projects/Defaultasp?LANG=EN).

Tutushkin, A., Levinsky R. and Bushueva, Y. 2004, Not the time for exploration (in Rus-sian), Vedomosti, # 209 (1249), Business News Media, Moscow, 15 November.

Vainshtock S. 2004, Speech of the Transneft’s President S.M. Vainshtock at the presentation of the Centre for Strategic Research’s report ‘About potential development trends of the infrastructure for transportation of Russian oil’, Press release, Moscow, 12 November (www.transneft.ru/press/Default.asp?LANG=RU&ATYPE=9&ID=7006).

White House 2005, Joint Statement by President Bush and President Putin on US–Russian Energy Cooperation, Washington DC, 24 February (www.whitehouse.gov/news/releases/2005/02/20050224-6.html).

World Bank 2004, World Development Indica-tors database, Washington DC, August.