Embed Size (px)

Citation preview

Company Presentation

1

Contents

General information

- RWE Trading as an operating companywithin the RWE Group

- RWE Trading is RWE’s interface with the market- The trading floor as the central

information platform for wholesale market issues- RWE’s power sales portfolio- Best in class – our history and our future- RWE Trading – key figures (I)- RWE Trading – key figures (II)- RWE Trading – organisation

Power trading- Facts and figures for RWE Trading

Gas trading- Cooperation between RWE Trading and

RWE Gas Midstream

Oil trading

Coal trading- RWE Trading’s role in the world of

coal trading- Main drivers of the coal trading

market and the respective challenges for RWE’s coal trading business

Emissions trading

Our risk management- Commodity Risk Governance

Structure- Risk philosophy- Backup

16

1819

20

21

2324

2526

2

34

56789

1011

1315

Page Page

2

RWE Trading as an operating company within the RWE Group

RWE AG (Group Centre)

Upstream (Production)

Electricitygeneration

Gas and oilproduction

Supraregionaland regional electricity and gas networks

Gas Midstream(commercial optimisation of procurement, transport, storage)

Continental Europe

UK

RWEPower

RWEDea

RWEGas Midstream

RWETrading

Energy trading Electricity and gas supply

RWEEnergy

RWEnpower

RWEPower

RWEGas Midstream

RWEEnergy

RWEnpower

RWESystems

RWEDea

RWETrading

RWEnpower

3

RWE Trading is RWE‘s interface with theenergy wholesale markets

RWE Trading implements the market-defined benchmarks for the RWE Group’s generation and supply activities.RWE traders not only deal with commodities such as power, gas, coal and oil, they also actively trade physical and financial derivatives as well as environmental certificates.The asset the based commodity positions of RWE Group are sold to or bought from RWE Trading at wholesale market prices. We consolidate these positions through proprietary trading. This hedging helps us to manage the risks of having very large open positions in each of the physical commodity markets.This business model unites the natural focus on obtaining the best potential value from the RWE Group’s physical assets with the benefits of financial (proprietary) trading.

* STPM = Short-term position management

RWE Energy/ npower

STPM*

RWE Power/ RWE npower

RWE Trading

Retail customers/industrial customers

Market

buy/sell

Trading customers

sell

buy sell

Proprietary trading

4

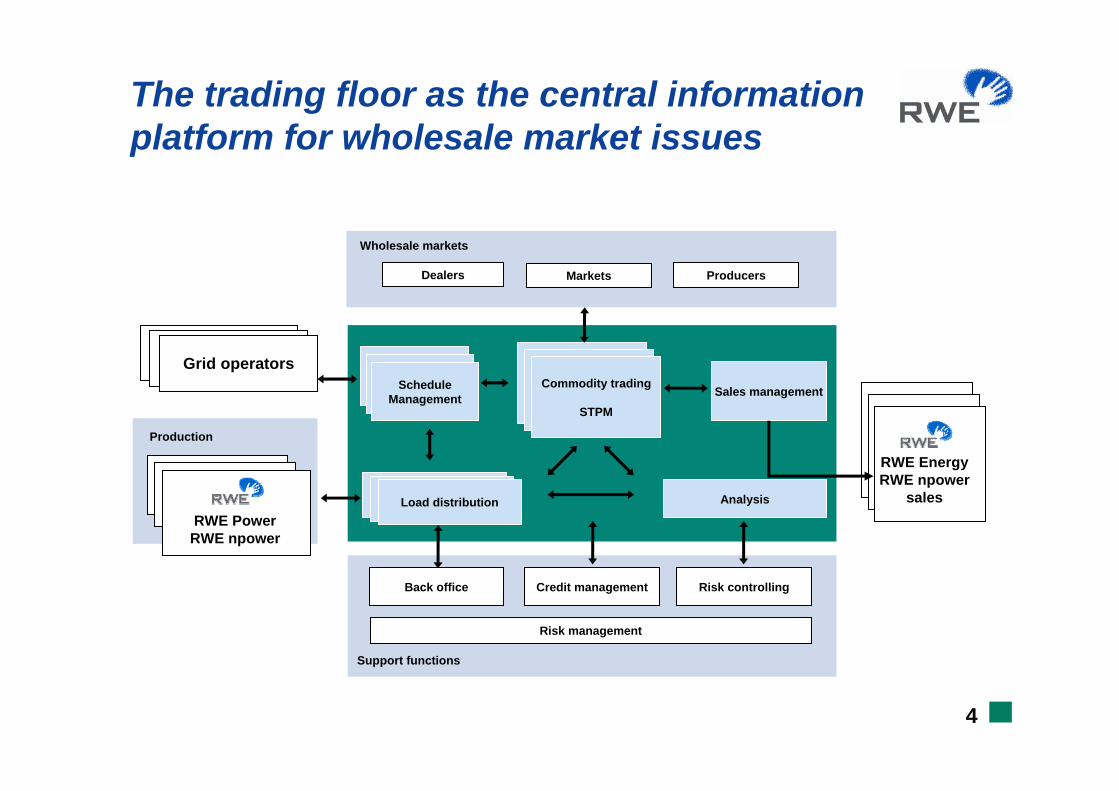

The trading floor as the central information platform for wholesale market issues

Sales management

Analysis

Risk management

Dealers Markets Producers

Commodity trading

STPM

Load distribution

Risk controlling

Grid operatorsSchedule

Management

Wholesale markets

Production

Support functions

RWE PowerRWE npower

RWE EnergyRWE npower

sales

Credit managementBack office

5

RWE’s power sales portfolio

The wholesale markets set the benchmark

RWE places its trust in the liquidity and reliability of the wholesale markets and sells a large part of its production directly into this pan-European market.

Of the 164.3 TWh produced by its own power plants in 2006, the RWE Groupsold 92.8 TWh on the wholesale markets and 71.5 TWh through sales organisations.

Salesorganisations

43.5%

Wholesale markets56.5%

71.5 TWh

92.8 TWh

6

Best in class – our history and our future

We contribute to the commercial success of the RWE Group by applying our combined knowledge and skills in the best interests of the Group’s assets.We continue to expand our proprietary trading activities based on fundamental analysis of the drivers of supply and demand, and therefore prices.

We continue to be a driver of liquidity in the power, gas, coal, oil and CO2 markets.

We continue to be the preferred long-term partner for sustainable success in European energy markets, capable of delivering innovative energy commodity risk management solutions.

2000 2002 2003

Joint short-term trading and asset dispatch

function –STPM*2005 ff.1898 1998

Purely speculative

trading

Best practiceblueprint for risk control

Providerof market

information/ route to the wholesale markets

Integratedwholesale risk pool

and portfolio manager

* Short-term position management

Hugo Stinnes

7

RWE Trading – key figures (I)

RWE Trading is one of the largest and most important European energy commodity traders.With a workforce of over 500 employees, RWE Trading operates trading floors in Essen, Swindon and London, as well as representative and agency offices across Europe.RWE Trading is active on leading international exchanges. Besides our activities in Europe, RWE Trading actively trades on the NYMEX and the global commodity markets.Oil: USA, Europe, Asia, Middle EastCoal: ARA, Newcastle, Richards Bay RWE Trading currently forms the backbone of the European OTC power and gas trading business.

RWE Trading in Europe

Oslo

Essen

Amsterdam

Paris

Madrid

Leipzig

London

SwindonWarsaw

Trading floor

Representative/agency office

Traded markets

Energy exchange

PragueKosice

Graz

Brussels

Ljubljana Bucharest

8

RWE Trading – key figures (II)

RWE Trading employees at year end**

* Figures for 2004 incorporate Innogy’s trading and assetmanagement team after RWE takeover.

**Year-end figures for RWE Trading GmbH, including apprentices.

Management accounts of RWE Trading 2006

Performance gross margin € 875.3 m

Performance EBITDA € 690.3 mRisk capital € 438.8 mRORAC 98.2 %

Since 2005, RWE Trading profits have been reported externally, together with the figures from the RWE Power generation business, to reflect a higher degree of integration with the asset business of the RWE Group.RWE Trading measures its performance on a pure mark-to-market basis, whereas RWE discloses these results following the legal structure and according to the applicant rules of IAS/IFRIC.

0

100

200

300

400

500

600

2002 2003 2004 2005 2006

192

176

483*

504 53

4

9

RWE Trading – organisation

Finance & Reporting (Global)

Project Controlling & Valuation

Back Office, IT & Business Change Management (Global)

Integration & Organisation

Managing Director and Chief Commercial Officer (CCO)

Dr Peter Kreuzberg

Managing Director and Chief Financial Officer (CFO)

Dr Bernhard Günther

Chief Executive Officer and Member of the Group Business CommitteePeter Terium

Power Trading (Continental Europe)Short-Term Position Management (Continental Europe)Power Trading (UK)Short-Term Position Management (UK)Gas Trading (all Europe)Global Commodities TradingGlobal Commodities Marketing & LogisticsCarbon TradingAnalysis for Global & Pan-European CommoditiesStructure & Valuation (Global)

Lobbying and Regulations (Global)

Legal & Communications (Global)

Strategy Application & Asset Interface (Global)

Risk (Global)

Human Resources (Global)

Power trading

11

RWE Trading – facts and figures

Our power trading volumes have seen consistent growth in recent years. This is just one indication of RWE Trading’s successful market approach. The slight decline in 2006 was due to politically influenced market distortions in France and Spain.

Where we trade powerRWE Trading: power trading volumes

TWh

Trend

Power trading CE and power trading UK

799

1,05

5

1,31

6

1,31

5

1,25

0

0

200

400

600

800

1,000

1,200

1,400

2002 2003 2004 2005 2006

12

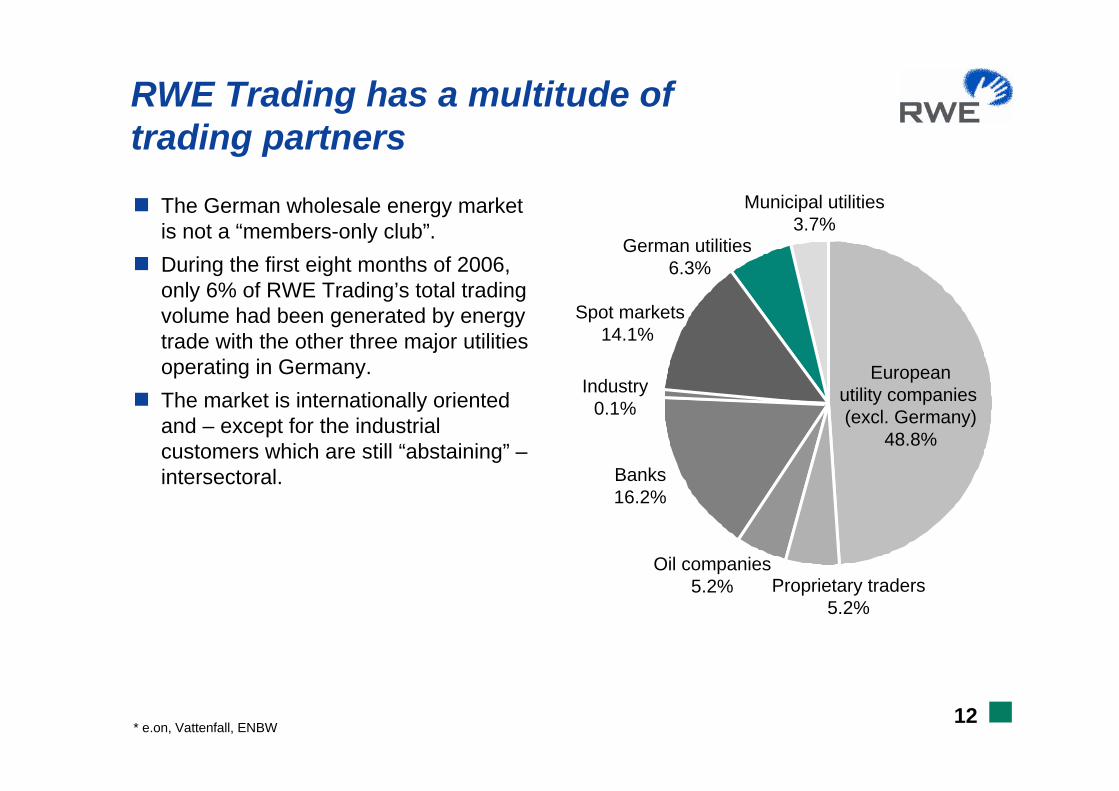

RWE Trading has a multitude of trading partners

The German wholesale energy market is not a “members-only club”. During the first eight months of 2006, only 6% of RWE Trading’s total trading volume had been generated by energy trade with the other three major utilities operating in Germany.The market is internationally oriented and – except for the industrial customers which are still “abstaining” –intersectoral.

* e.on, Vattenfall, ENBW

Proprietary traders5.2%

Oil companies5.2%

Industry0.1%

Municipal utilities3.7%

German utilities 6.3%

Banks16.2%

Europeanutility companies (excl. Germany)

48.8%

Spot markets14.1%

Gas trading

14

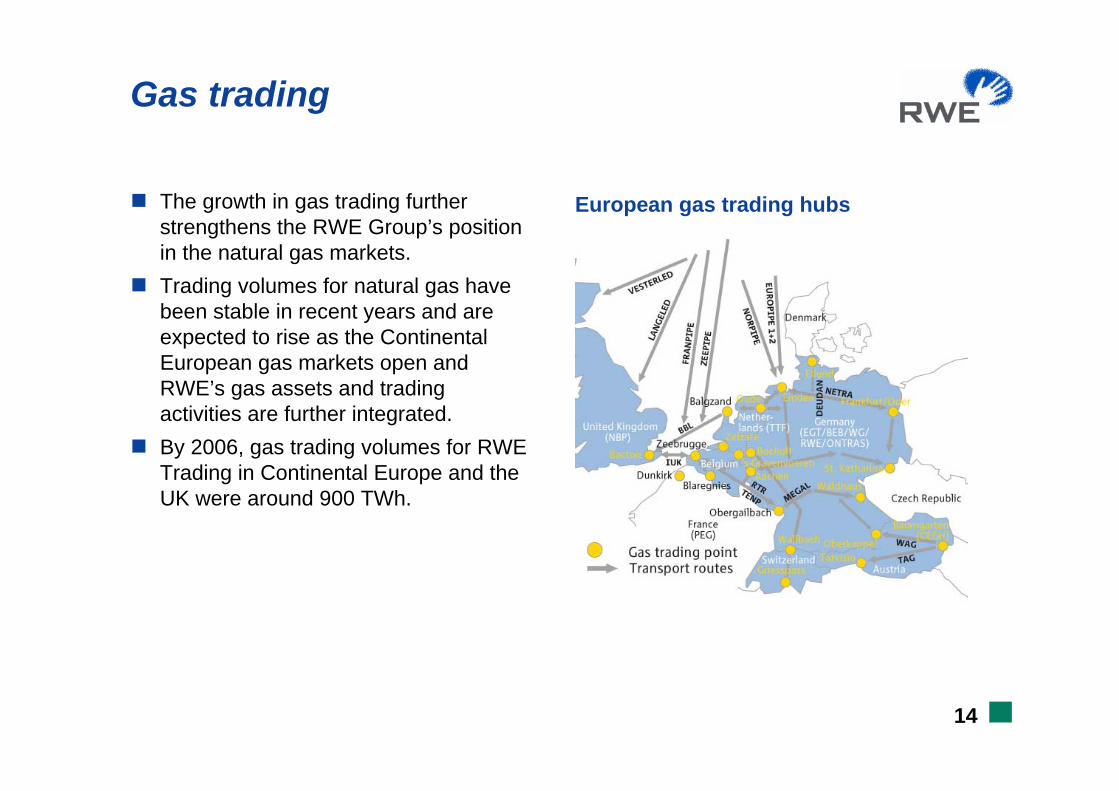

Gas trading

The growth in gas trading further strengthens the RWE Group’s position in the natural gas markets.Trading volumes for natural gas have been stable in recent years and are expected to rise as the Continental European gas markets open andRWE’s gas assets and tradingactivities are further integrated. By 2006, gas trading volumes for RWE Trading in Continental Europe and the UK were around 900 TWh.

European gas trading hubs

15

Cooperation between RWE Tradingand RWE Gas Midstream

RWE Gas Midstream will further strengthen RWE Group’s competitiveness in the increasingly liberalised European gas market. RWE Gas Midstream bundles the non-regulated areas of the RWE Group’s gas business (purchase, transportand storage capacity rights).RWE Trading and RWE Gas Midstream cooperate closely with each other in the gas business. RWE Trading will continue to be an active trader at liquid gas trading points. This business is being integrated by RWE Gas Midstream as part of the commercial optimisation of the entire gas portfolio of the RWE Group, ranging from short-to long-term procurement and supply commitments.

Oil trading

17

Oil trading

RWE Trading’s business model for oil covers global physical commodities and derivatives trading as well as risk management.Group-wide synergies include:– Marketing of RWE Dea equity crude (among others North Sea, Dubai, Egypt)– Risk management and hedging of RWE Dea’s physical upstream position– Procurement of fuel oil for RWE power plants– Global derivative expertise for hedging strategies of oil-indexed fuels (e.g. gas)RWE Trading carries out spread transactions between oil products and locations based on price differentials.

Coal trading

19

RWE Trading’s role in the world of coal trading

As a significant player in the international physical coal and freight trading markets, RWE Trading offers a range of products, from basic supply and trading deals to advanced integrated risk management and marketing solutions.The value of these activities is enhanced by our active involvement in coal and freight financial derivatives.RWE Trading is the RWE Group’s interface with the international coal trading market:– Physical: >20 million tonnes of coal are

burnt (directly/indirectly) per year, including an increasing amount of coal from abroad

– Derivatives: >100 million tonnes of derivatives per year

20

Main drivers of coal trading market and the challenges for RWE’s coal trading business

Rising demand from China and India and the renaissance of coal-fired power generation in Europe.Significant increases in ocean freight rates and coal export prices.Larger trade flows and higher price volatility, creating a vibrant market with a very strong international orientation.Thanks to extensive market knowledge and its team of dedicated experts, RWE Trading is well positioned to manage the risks presented by a changing market and to offer made-to-measure supply solutions to our customers.We source from and supply to a number of different countries and suppliers globally, including long-term basis contracts.We will also play an active role as a market maker for new and attractive products.

Emissions trading

22

Emissions trading

Optimisation of power, gas and other fuel positions via emissions trading is a necessary part of European energy markets.The European Trading System (ETS) combines market forces with politically imposed caps on emissions. RWE Trading has been a successful participant from the very beginning and is a leading contributor to the rapid development of this market. We are ready to meet the complex challenges of the ETS market, by handling day-to-day fluctuations, and by having the tools and experience to hedge long-term risks. For example, we actively support the further development of trading master agreements.The ETS will continue to be an important futures market. Although there is a high degree of volatility in daily trading, there is a also strong long-term element. The CO2 market provides decision makers with valuable input when it comes to planning long-term investments in generation assets/power plants.

Our risk management

24

Commodity risk governance structure

RWE Group Center

RWE AG Executive Board Group Risk Management

RWE Energy RWE Power RWE Trading RWE npower

Portfolio management

Risk control Risk control Risk control Risk control

Short-term position management (UK)

Short-term position management (continent)

Asset management Trading desks

Asset interface

Portfolio management

Asset management

RWE Gas Midstream

Risk control

Portfolio management

Market Committee

New Product Team

Risk Committee

Asset BookCommitteeGas & Oil

Asset BookCommitteeContinent

Asset BookCommittee

UK

CarbonWorking Group

Group Business Committee

Market Assessment Team

25

Risk philosophy

The Chairman of the Board is the chief risk controller.Professional risk management forms the basis of our successful energy trading business.Our strict risk management philosophy is implemented through the following structures and measures:– Best-in-class processes for trading, risk controlling and

back office/operations based on banking industry standards– Integrated management of all trading activities, and independent

evaluation and supervision of market and credit risks using aninter-organisational state-of-the-art trading and risk management system

– Organisational separation of front office and support and control functions (dual control principle)

– Transactions on the basis of international master agreements (ISDA, EFET, etc.)

Backup

27

Contents of Backup

Power trading- RWE Trading = the Group’s wholesale risk

pool and portfolio manager in Germany, Continental Europe …

- … and the UK- Major fundamental factors influencing

power prices on the wholesale market- Forward price development in Europe- Power trading volumes in Continental

Europe: increasing liquidity- Wholesale markets work: development of

trading volumes in Germany as of 2002

Coal trading- Coal prices (US$/t)- Coal prices and freight prices (US$/t)

Emissions trading- Environmental trading- Environmental trading

Price development (EUA 06)- Environmental trading

Price development (EUA 07)- Environmental trading

Price development (EUA 08)

2831

3233

3540

41

Page

474849

505152

53

54

Page

Power trading

29

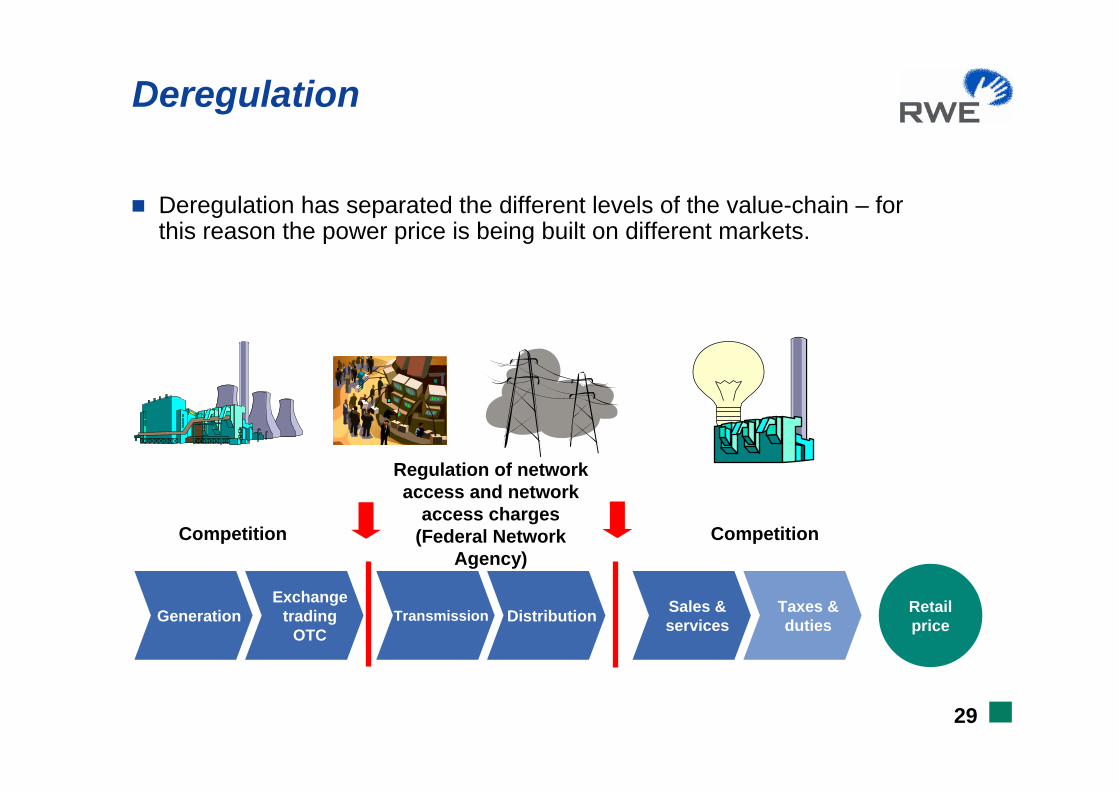

Deregulation

Competition Competition

Regulation of network access and network

access charges (Federal Network

Agency)

RetailpriceGeneration

Exchangetrading

OTCTransmission Distribution Sales &

servicesTaxes &duties

Deregulation has separated the different levels of the value-chain – for this reason the power price is being built on different markets.

30

The power wholesale market

Forwards/ options/

structured products

Settlement: physical and

financial

Physical

Futures/ options

Settlement: mainly

financialPhysical

Trading

Wholesale market

OTC market(e-OTC Germany 2006: 1,680 TWh)

Spot market Futures market

Exchange(EEX 2006: 1,133 TWh)

Spot market(EEX 2006: 88.7 TWh)

Future market(EEX 2006: 1,044 TWh)

OTCclearing

EEX 2006: 642 TWh

31

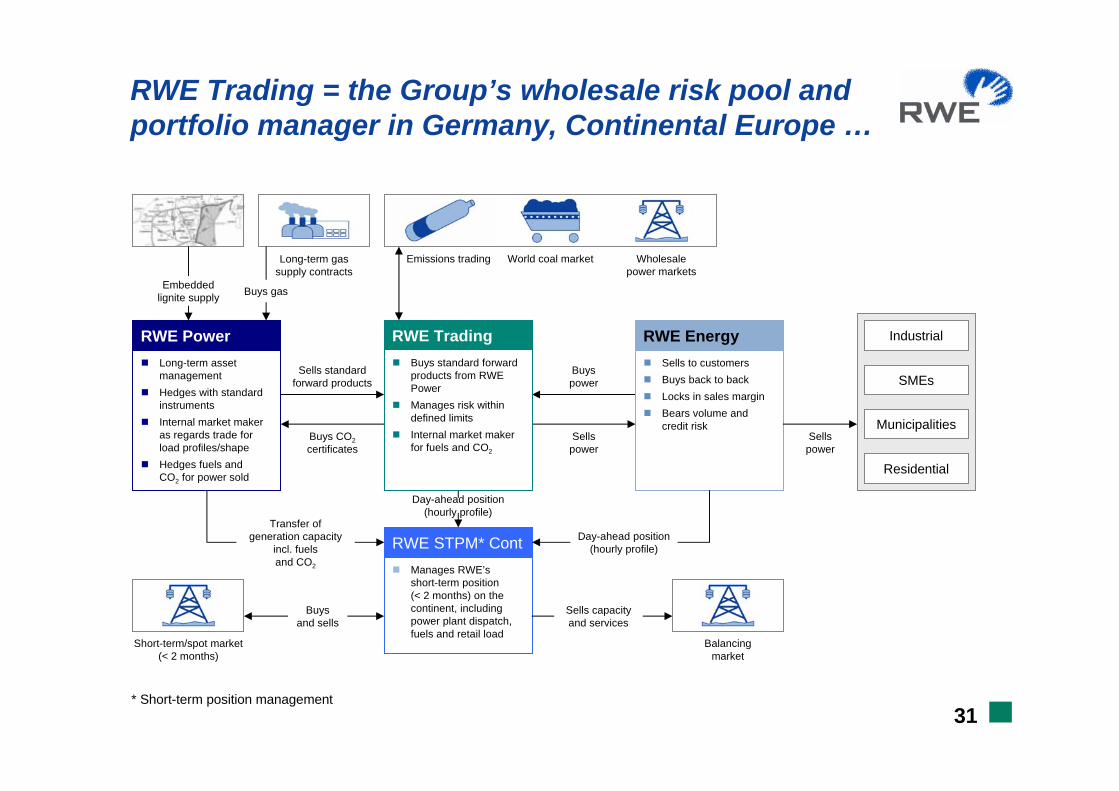

RWE Trading = the Group’s wholesale risk pool and portfolio manager in Germany, Continental Europe …

Sells standardforward products

Buys CO2certificates

Buyspower

Sellspower

RWE EnergySells to customersBuys back to backLocks in sales marginBears volume andcredit risk

Industrial

SMEs

Municipalities

Residential

Sellspower

RWE STPM* ContManages RWE’sshort-term position(< 2 months) on the continent, including power plant dispatch, fuels and retail load

Day-ahead position(hourly profile)

Day-ahead position(hourly profile)

Transfer of generation capacity

incl. fuelsand CO2

Sells capacityand services

Buysand sells

Short-term/spot market(< 2 months)

Balancingmarket

RWE PowerLong-term asset managementHedges with standard instrumentsInternal market maker as regards trade forload profiles/shapeHedges fuels andCO2 for power sold

Long-term gassupply contracts

Embeddedlignite supply Buys gas

RWE TradingBuys standard forward products from RWE PowerManages risk within defined limitsInternal market maker for fuels and CO2

Emissions trading World coal market Wholesalepower markets

* Short-term position management

32

… and the UK

RWE npower Generation

Long-term asset managementHedges CO2 for capability not yet transferred to Trading

Buyspower

Sellspower

RWE npower Retail

Sells to customersBuys back to backLocks in sales marginBears volume andcredit risk

Industrial

SMEs

Residential

Sellspower

RWE STPM* UK

When an option is exercised, STPM* manages generation capability until production (< 1 week)Manages optionality of plants (dispatch including fuels) andretail load

Option exercise

Loadprofile

Sells capacityand services

Buysand sells

Spot market(< 1 week)

Balancingmarket

RWE TradingBuys capabilityfrom RWE npowerManages the spread option within defined limitsInternal marketmaker for power,fuels and CO2

Emissions trading World coal market Wholesale gas market

Buysand sells

Wholesalepower market

Transfer ofcapabilityincl. CO2

Buys CO2certificates

* Short-term position management

33

Major fundamental factors influencing power prices on the wholesale market

Power price

Rainfall CO2 price Gas price Oil price Coal price Uranium price

RevisionsThermic power plant

Technicalfailures

Power plants/ networks

school holidays

WindturbinesWind

Temperature

Public holidays

Illumination

Brightness

Climatisation/ electric heating

Time of dayCloudsLong-term influences:• Changes on basis of

market changes• Political decisions• Capacity changes

Storage and riverpower plant

Futures markets reflect traders’ expectations in terms of future

fundamental influence factors

34

“Marginal power plant” principle: decisive for price formation on the wholesale market

The daily demand on the EEX is countered by a multitude of offers for electricity from different generation sources. Each power plant type (nuclear, gas, coal, etc.) has marginal costs for its utilisation.

Marginal costs are mainly determined by “variable costs” for fuels (incl. CO2) and operating resources - costs that are incurred during power plant operation and have to be earned as a minimum.

Starting with the most favourable offer, power plants are successively called up on the EEX until demand is met.

The offer price of the last power plant needed to meet this demand (“marginal power plant”) determines the market price for all other power plants.

The power price thus results from the intersection of supply and demand. That is why in case of high demand prices will rather be determined by power plants with relatively high marginal costs whereas in case of low demand they will rather be determined by lower marginal cost power plants.

€/MWh

Power supply in MW (graded by offer prices)

Offer price

Market price

Power demand

K2 K3 K4 K5

Full costs

K1

variable costs + capital costs

Short-term variable costs per power plant type (fuel + operating resources) + CO2

35

Forward price development in Europe

Marked price increase throughout Europe in 2005 and 2006. Since mid-2006, stable price level for Germany at around € 55/MWh.

25

30

35

40

45

50

55

60

65

70

01.0

1.05

01.0

3.05

01.0

5.05

01.0

7.05

01.0

9.05

01.1

1.05

01.0

1.06

01.0

3.06

01.0

5.06

01.0

7.06

01.0

9.06

01.1

1.06

01.0

1.07

01.0

3.07

01.0

5.07

01.0

7.07

€/M

Wh

DeutschlandFrankreichNiederlandeSkandinavien

Germany

Netherlands

France

Scandinavia

36

Price increase for 2008 since 2005

Germany shows the lowest price increase by European comparison at 48%.

90%

100%

110%

120%

130%

140%

150%

160%

170%

180%

190%

01.0

1.05

01.0

3.05

01.0

5.05

01.0

7.05

01.0

9.05

01.1

1.05

01.0

1.06

01.0

3.06

01.0

5.06

01.0

7.06

01.0

9.06

01.1

1.06

01.0

1.07

01.0

3.07

01.0

5.07

01.0

7.07

€/M

Wh

DeutschlandFrankreichNiederlandeSkandinavien

Germany

Netherlands

France

Scandinavia

37

Spot market volume at important european markets 2003 - 2007

02468

1012141618202224262830

Jan

03

Apr

03

Jul 0

3

Okt

03

Jan

04

Apr

04

Jul 0

4

Okt

04

Jan

05

Apr

05

Jul 0

5

Okt

05

Jan

06

Apr

06

Jul 0

6

Okt

06

Jan

07

Apr

07

Jul 0

7

Month

TWh

EEXEXAAPowernextAPXNordpool

38

Futures market volume at important europeanmarkets 2003 - 2007

0

10

20

30

40

50

60

70

80

90

100

110

120Ja

n 03

Apr 0

3

Jul 0

3

Okt

03

Jan

04

Apr 0

4

Jul 0

4

Okt

04

Jan

05

Apr 0

5

Jul 0

5

Okt

05

Jan

06

Apr 0

6

Jul 0

6

Okt

06

Jan

07

Apr 0

7

Jul 0

7

.

Month

TWh

EEX

Powernext

Endex

Nordpool

39

EEX market volume 2004 - 2007

0

20

40

60

80

100

120

140

160

Jan 04

Apr 04

Jul 0

4

Okt 04

Jan 05

Apr 05

Jul 0

5Okt

05

Jan 06

Apr 06

Jul 0

6Okt

06

Jan 07

Apr 07

Jul 0

7

Month

Volu

me

(TW

h)

EEX ClearingEEX FuturesEEX Spot

40

Power trading volumes in Continental Europe: increasing liquidity*

2002 2003 2004 2005 20061,000,000,000

2,000,000,000

3,000,000,000

4,000,000,000

5,000,000,000

6,000,000,000

2001

Scandinavia

Netherlands OTC

Netherlands

France OTC

France

Germany OTC

Germany

Spain

* In bn kWh; measurable trading volume at exchanges and via electronic broker platforms OTC

41

Wholesale markets work: development of trading volumes in Germany as of 2002

2002 2003 2004 2005 20060

500

1.000

1.500

2.000

2.500

Source: EEX, RWE Trading data, 2006e = “estimate”/based on data available up to October 2006.

Since deregulation there has been a continual increase in the volumes traded on the German wholesale market.

Note: this graph is based on measurable trading volumes and does not include bilateral “voice OTC” trading. Market analysts estimate the total trading volume including non-measurable, anonymous OTC trading to be around double the volumes shown here.

3.000

e-OTC Forwards

Clearing

Futures

Spot

TWh

42

European network effectively limits the market position of individual producersRelevant production for Germany is 192 GW.

Conclusion of the “

EU sector inquiry regarding networking*:

“Pivotal Supplier Index (PSI) for Germany is small”

Share of the“big four”:

43%

30% Cross-border

capacities(58 GW)

17%Others (33 GW)

10%Inst. windpower plants(20 GW)

17%RWE

(32 GW)

12%e.on

(23 GW)

7%EnBW

(13 GW)

7%Vattenfall(13 GW)

0.0%UK

0.0%DE

0.0%NL

8.2%E

97.2%BE

100.0 %F

* Sources: EU Sector Inquiry 2005/2006, study by London Economics and Global Energy Decisions

43

Europe’s power market is connected

Price level often higher than in GermanyPrice level often lower than in Germany

Northern EuropeStrongly dependent on hydropower and thus largely influenced by other fundamental factors than other European regionsPresently “normal” water levels

Southern EuropeIncreased use of air conditioning and electric heatingFailing hydropower productionGenerally increasing demand due to economic development

Eastern EuropePartly subsidised cheaper electricityNo open wholesale marketsCO2 not as fungible as in open energy markets

Rising exports are a sign of healthy competition: electric power, too, tries to find the highest available price. If a trader can sell electricity at a higher price in a neighbouring European country than at home, he will try to use this opportunity. Different production structures and different fundamental influences result in growing cross-border trading (but not necessarily in growing physical electricity flows)

44

Power wholesale markets and market deregulation -status quo regarding cross-border network capacities

Germany already complies with all requirements for cross-border network capacities.

Compliant

Compliant with most requirements

Non-compliant

Long-term agreements are available (no publicly accessible information)

Status: April 2006

45

Four core statements by RWE Trading on power wholesale markets

Functioning wholesale markets are the prerequisite for competition and the ensuing economic benefits for the European industry.The European wholesale market for power has shown a very positive development: just look at the growth rate for traded volumes or the increasing number of market participants.RWE Trading is one of the leading market participants in Europe and plays an active part in shaping the wholesale markets.Markets require a framework and regulation, but overregulation stifles trust in the markets! Regulation should always focus on promoting competition.

46

European power markets showing outstanding development

More than sufficient liquidity in the core markets

Diversified and numerous market participants

Convergence of power prices in Europe

Price peaks are also a European phenomenon

Market position of individual producers effectively limited in the European market

Coal trading

48

Coal prices (US$/t)

20

40

60

80

100

120Ja

n 03

Mar

03

May

03

Jul 0

3

Sep

03

Nov

03

Jan

04

Mar

04

May

04

Jul 0

4

Sep

04

Nov

04

Jan

05

Mar

05

May

05

Jul 0

5

Sep

05

Nov

05

Jan

06

Mar

06

May

06

Jul 0

6

Sep

06

Nov

06

Jan

07

Mar

07

May

07

Jul 0

7

Sep

07

Nov

07

Monat

Prei

s in

$/t

API#2 API#4

Pric

e in

US$

Month

API#2 API#4

49

Coal prices and freight prices (US$/t)Pr

ice

in U

S$/t

5

10

15

20

25

30

35

40

45Ja

n 03

Apr

03

Jul 0

3

Oct

03

Jan

04

Apr

04

Jul 0

4

Oct

04

Jan

05

Apr

05

Jul 0

5

Oct

05

Jan

06

Apr

06

Jul 0

6

Oct

06

Jan

07

Apr

07

Jul 0

7

Oct

07

C4 ausschließlich Frachtrate (API#2 - API#4)Month

C4 Implied freight

Emissions trading

51

CO2 emissions trading

The CO2 market is characterised by fast-growing liquidity

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

160.000

180.000

Jan 0

4Apr

04Ju

l 04

Okt 04

Jan 0

5Apr

05Ju

l 05

Okt 05

Jan 0

6Apr

06Ju

l 06

Okt 06

Jan 0

7Apr

07Ju

l 07

Okt 07

Han

dels

volu

men

[100

0 EU

A]

Trad

edvo

lum

esin

1,0

00 E

UA

52

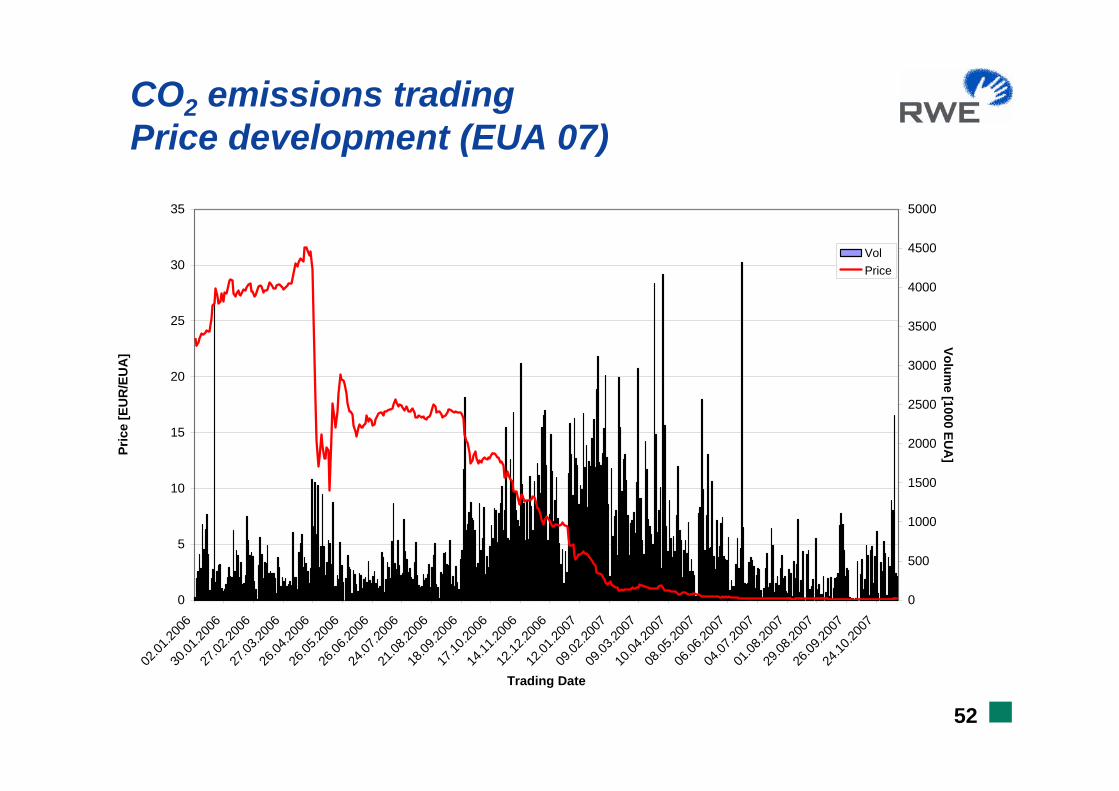

CO2 emissions trading Price development (EUA 07)

0

5

10

15

20

25

30

35

02.01

.2006

30.01

.2006

27.02

.2006

27.03

.2006

26.04

.2006

26.05

.2006

26.06

.2006

24.07

.2006

21.08

.2006

18.09

.2006

17.10

.2006

14.11

.2006

12.12

.2006

12.01

.2007

09.02

.2007

09.03

.2007

10.04

.2007

08.05

.2007

06.06

.2007

04.07

.2007

01.08

.2007

29.08

.2007

26.09

.2007

24.10

.2007

Trading Date

Pric

e [E

UR

/EU

A]

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Volume [1000 EU

A]

VolPrice

53

CO2 emissions trading Price Development (EUA 08)

0

5

10

15

20

25

30

35

02.01

.2006

30.01

.2006

27.02

.2006

27.03

.2006

26.04

.2006

26.05

.2006

26.06

.2006

24.07

.2006

21.08

.2006

18.09

.2006

17.10

.2006

14.11

.2006

12.12

.2006

12.01

.2007

09.02

.2007

09.03

.2007

10.04

.2007

08.05

.2007

06.06

.2007

Trading Date

Pric

e [E

UR

/EU

A]

0

2000

4000

6000

8000

10000

12000Volum

e [1000 EUA

]

VolPrice