Embed Size (px)

Citation preview

.5733

2088HOV-1

O F F I C I A LJFJ!LE__COPV

DO NOT SEND(Xerox necessarycopies Irom IhKcopy and PLACE

BACK in FILE)

SABINE RIVER COMPACT ADMINISTRATION

FINANCIAL REPORT

AUGUST 31, 2008

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish clerk of court.

Release Date ill 14 hi

C O N T E N T S

Page

INDEPENDENT AUDITORS' REPORT 1 and 2

MANAGEMENT'S DISCUSSION AND ANALYSIS 3 and 4

FINANCIAL STATEMENTS

Basic financial statements:Government-wide financial statements -

Statements of net assets 5Statements of activities 6

Fund financial statements -Balance sheets - governmental fund 7Statements of revenues, expenditures

and changes in fund balance - governmental fund 8Budgetary comparison schedule 9

Notes to financial statements 10 and 11

REPORT ON INTERNAL CONTROL OVER FINANCIALREPORTING AND ON COMPLIANCE AND OTHERMATTERS BASED ON AN AUDIT OF FINANCIALSTATEMENTS PERFORMED IN ACCORDANCE WITHGOVERNMENT AUDITING STANDARDS 13 and 14

Schedule of findings and responses 15

Schedule of prior findings 16

BROUSSARD, POCHE, LEWIS & BREAUX, L.L.P.C E R T I F I E D P U B L I C A C C O U N T A N T S

4112 West CongressP.O. Box 61400Lafayette, Louisiana 70596-1400phone: (337) 988-4930fax: (337) 984-4574www.bplb.com

Other Offices:

Crowley, LA(337) 783-5693

Opelousas, LA(337) 942-5217

Abbeville, LA(337) 898-1497

New Iberia, LA(337) 364-4554

Church Point, LA(337) 684-2855

Frank A. Stagno, CPA*

Scott J. Broussard, CPA*

L. Charles Abshire, CPA*

P. John Blanchet, III, CPA*

Martha B. Wyatt, CPA*

Fayetta T. Dupre, CPA*

Mary A. Castille, CPA*

Joey L. Breaux, CPA*

Craig J. Viator, CPA*

Stacey E. Singleton, CPA*

John L. Istre, CPA*

Tricia D. Lyons, CPA*

Mary T. Miller, CPA*

Elizabeth J. Moreau, CPA*

Frank D. Bergeron, CPA*

Retired:

Sidney L, Broussard, CPA 1925-2005Leon K. Poche, CPA 1984

James H. Breaux, CPA 1987

Erma R. Walton, CPA 1988

George A. Lewis, CPA 1992

Geraldine J. Wimberley, CPA 1995

Lawrence A. Cramer, CPA 1999

Ralph Friend, CPA 2002

Donald W. Kelley, CPA 2005

George J. Trappey, III, CPA 2007

Terrel P. Dressel, CPA 2007

Herbert Lemoine II, CPA 2008

INDEPENDENT AUDITORS' REPORT

To the Board of CommissionersSabine River Compact AdministrationStates of Texas and Louisiana

We have audited the accompanying basic financial statements of theSabine River Compact Administration, a component unit of the Stateof Texas and State of Louisiana, as of and for the years endedAugust 31, 2008 and 2007. These financial statements are theresponsibility of the Administration's management. Ourresponsibility is to express an opinion on these financialstatements based on our audits.

We conducted our audits in accordance with auditing standardsgenerally accepted in the United States of America and thestandards applicable to financial audits contained in GovernmentAuditing Standards, issued by the Comptroller General of the UnitedStates. Those standards require that we plan and perform the auditto obtain reasonable assurance about whether the financialstatements are free of material misstatement. An audit includesexamining, on a test basis, evidence supporting the amounts anddisclosures in the financial statements. An audit also includesassessing the accounting principles used and significant estimatesmade by management, as well as evaluating the overall financialstatement presentation. We believe that our audits provide areasonable basis for our opinions.

In our opinion, the basic financial statements referred to abovepresent fairly, in all material respects, the financial position ofSabine River Compact Administration as of August 31, 2008 and 2007,and the changes in financial position for the years then ended inconformity with accounting principles generally accepted in theUnited States of America.

In accordance with Government Auditing Standards, we have alsoissued our report dated October 17, 2008, on our consideration ofthe Sabine River Compact Administration's internal control overfinancial reporting and our tests of its compliance with certainprovisions of laws, regulations, contracts and grant agreements andother matters. The purpose of that report is to describe the scope

* A Professional Accounting Corporation1 -

of our testing of internal control over financial reporting and compliance and theresults of that testing, and not to provide an opinion on the internal control overfinancial reporting or on compliance. That report is an integral part of an auditperformed in accordance with Government Auditing Standards and should be considered inassessing the results of our audit.

Management's discussion and analysis on pages 3 and 4 is not a required part of thebasic financial statements but is supplementary information required by accountingprinciples generally accepted in the United States of America. We have applied certainlimited procedures, which consisted principally of inquiries of management regardingthe methods of measurement and presentation of the required supplementary information.However, we did not audit the information and express no opinion on it.

Lafayette, LouisianaOctober 17, 2008

- 2 -

SABINE RIVER COMPACT ADMINISTRATION

MANAGEMENT'S DISCUSSION AND ANALYSIS

This section of the Sabine River Compact Administration (SRCA) annual financial reportpresents a discussion and analysis of SRCA's financial performance during the fiscalyears that ended August 31, 2008, 2007 and 2006. Please read this section inconjunction with SRCA's financial statements, which follow this section.

FINANCIAL HIGHLIGHTS

SRCA's net assets overall decreased from $33,888 to $32,358 or 4.5% from August 31,2005 to August 31, 2006, increased from $32,358 to $34,894 or 7.8% from August 31, 2006to August 31, 2007 and increased from $34,894 to $37,326 or 7.0% from August 31, 2007to August 31, 2008.

SRCA's intergovernmental revenues for the years ended August 31, 2008, 2007 and 2006were $72,375, $68,880 and $68,880, respectively. General governmental expenses were$70,186, $66,856 and $70,932 for the years ended August 31, 2008, 2007 and 2006,respectively.

OVERVIEW OF THE FINANCIAL STATEMENTS

The financial report consists of three parts: Management's Discussion and Analysis.(this section), the basic financial statements, and the notes to the financialstatements.

The basic financial statements present information for SRCA as a whole, in a formatdesigned to make the statements easier for the reader to understand. The statements inthis section include the statement of net assets and the statement of activities.

The statement of net assets presents the assets and liabilities. The differencebetween total assets and total liabilities is net assets and may provide a usefulindicator of whether the financial position of SRCA is improving or deteriorating.

The statement of activities presents information showing how SRCA's assets changed as aresult of current year operations. Regardless of when cash is affected, all changes innet assets are reported when the underlying transactions occur. As a result,transactions are recorded that will not affect cash until future periods.

The financial statements provide information about SRCA's overall financial status.The financial statements also include notes that explain some of the information in thefinancial statements and provide more detailed data.

SRCA's financial statements are prepared on an accrual basis in conformity withaccounting principles generally accepted in the United States of America (GAAP) asapplied to government units. Under this basis of accounting, revenues are recognizedin the period in which they are earned and expenses are recognized in the period inwhich they are incurred. All assets and liabilities associated with the operation ofSRCA are included in the statement of net assets.

- 3 -

FINANCIAL ANALYSIS

Net Assets

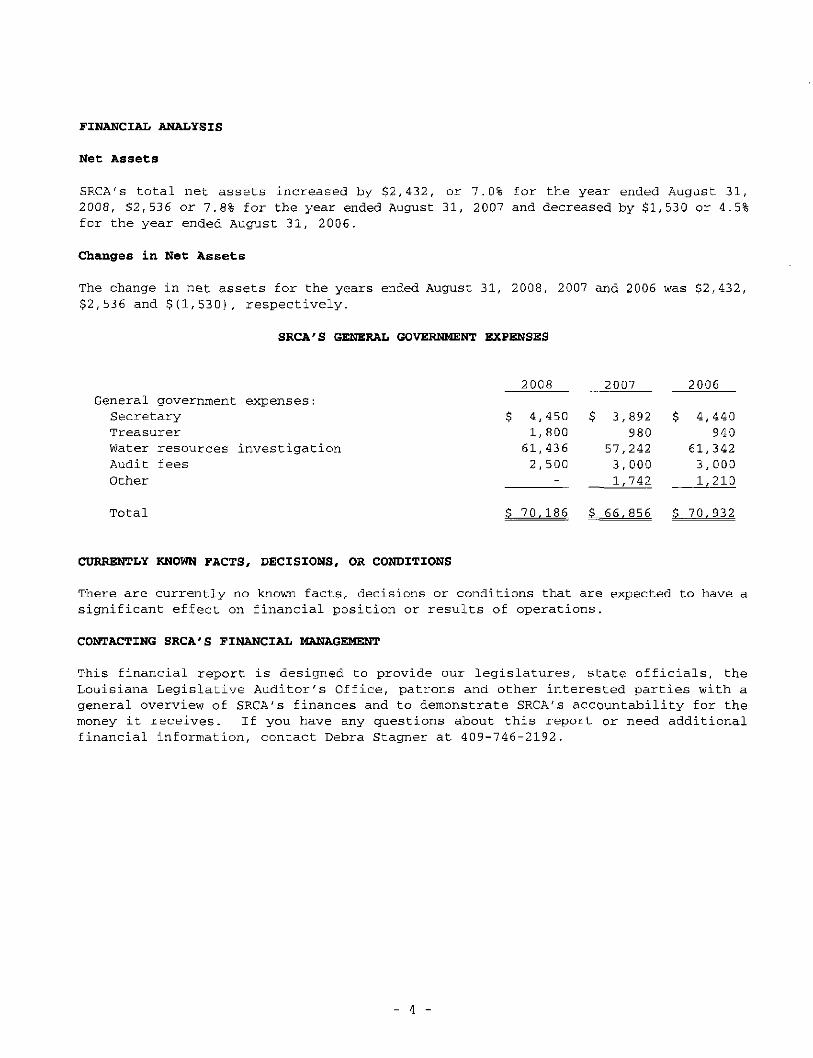

SRCA's total net assets increased by $2,432, or 7.0% for the year ended August 31,2008, $2,536 or 7.8% for the year ended August 31, 2007 and decreased by $1,530 or 4.5%for the year ended August 31, 2006.

Changes in Net Assets

The change in net assets for the years ended August 31, 2008, 2007 and 2006 was $2,432,$2,536 and $(1,530), respectively.

SRCA'S GENERAL GOVERNMENT EXPENSES

2008 2007 2006General government expenses:SecretaryTreasurerWater resources investigationAudit feesOther

Total

$ 4,1,

61,

2,

450800436500-

$ 3,

57,

3,1,

892980242000742

$ 4,

61,3,

1,

440940342000210

$ 70,186 $_ 66, 856 $ 70,932

CURRENTLY KNOWN FACTS, DECISIONS, OR CONDITIONS

There are currently no known facts, decisions or conditions that are expected to have asignificant effect on financial position or results of operations.

CONTACTING SRCA'S FINANCIAL MANAGEMENT

This financial report is designed to provide our legislatures, state officials, theLouisiana Legislative Auditor's Office, patrons and other interested parties with ageneral overview of SRCA's finances and to demonstrate SRCA's accountability for themoney it receives. If you have any questions about this report or need additionalfinancial information, contact Debra Stagner at 409-746-2192.

- 4 -

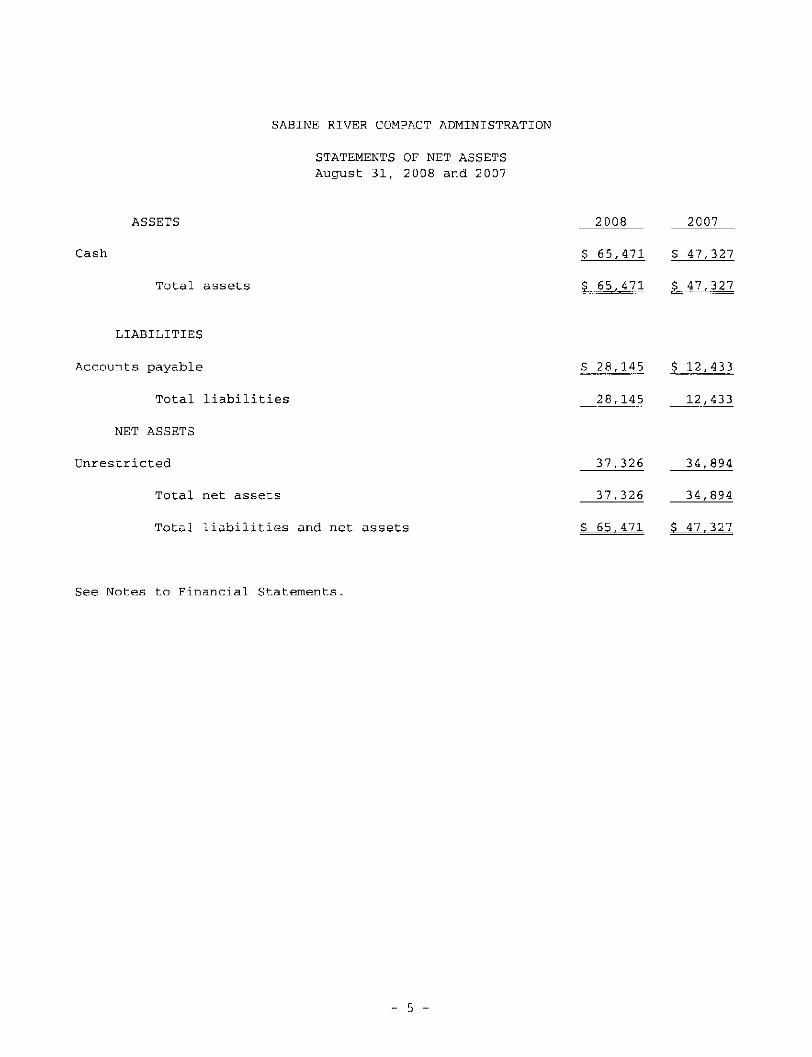

SABINE RIVER COMPACT ADMINISTRATION

STATEMENTS OF NET ASSETSAugust 31, 2008 and 2007

ASSETS

Cash

Total assets

LIABILITIES

Accounts payable

Total liabilities

NET ASSETS

Unrestricted

Total net assets

Total liabilities and net assets

2008

28,145

37,326

37,326

2007

$ 65,471 $ 47,327

$ 65,471 $ 47,327

S 28,145 $ 12,433

12,433

34,894

34,894

$ 65,471 $ 47.327

See Notes to Financial Statements.

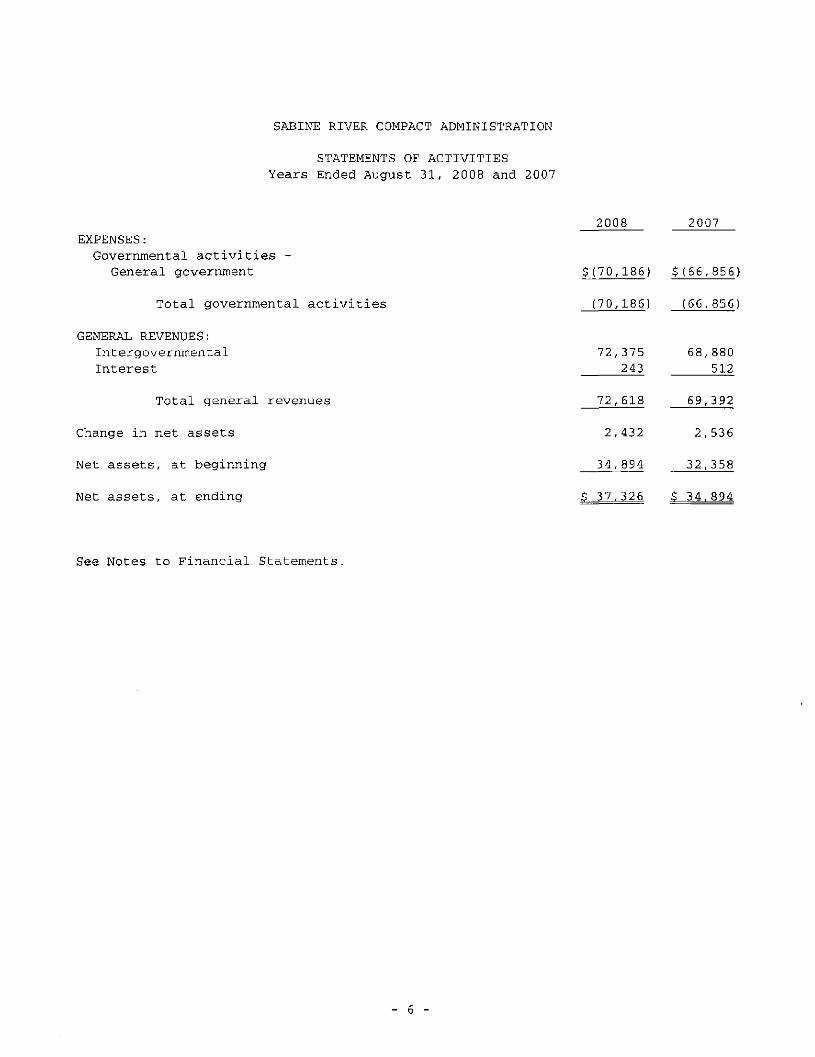

SABINE RIVER COMPACT ADMINISTRATION

STATEMENTS OF ACTIVITIESYears Ended August 31, 2008 and 2007

2008 2007EXPENSES:Governmental activities -

General government

Total governmental activities

GENERAL REVENUES:IntergovernmentalInterest

Total general revenues

Change in net assets

Net assets, at beginning

Net assets, at ending

$ (70,186) $(66,856)

[70,186) (66,856)

72,375243

72,618

2,432

34,894

68,880512

69,392

2, 536

32,358

$ 34,894

See Notes to Financial Statements.

- 6 -

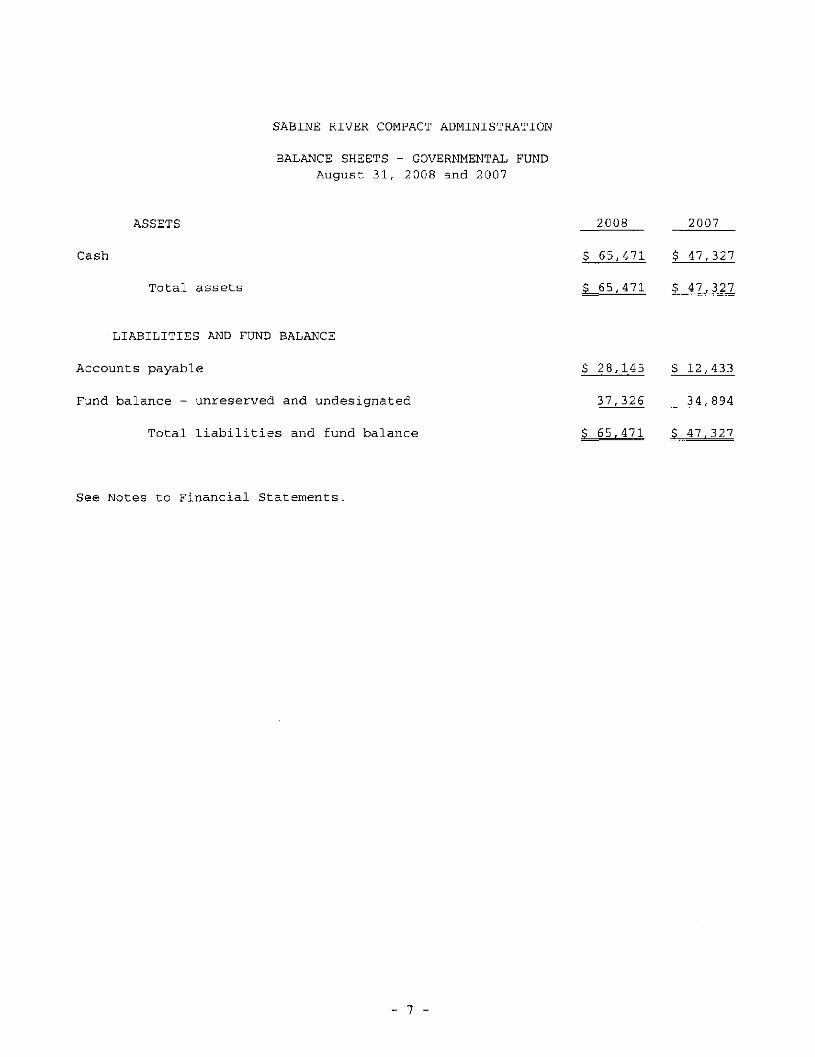

SABINE RIVER COMPACT ADMINISTRATION

BALANCE SHEETS - GOVERNMENTAL FUNDAugust 31, 2008 and 2007

Cash

ASSETS

Total assets

2008 2007

$ 65,471 $ 47,327

LIABILITIES AND FUND BALANCE

Accounts payable

Fund balance - unreserved and undesignated

Total liabilities and fund balance

$ 28,145 $ 12,433

37,326 34,894

See Notes to Financial Statements.

_ 7 _

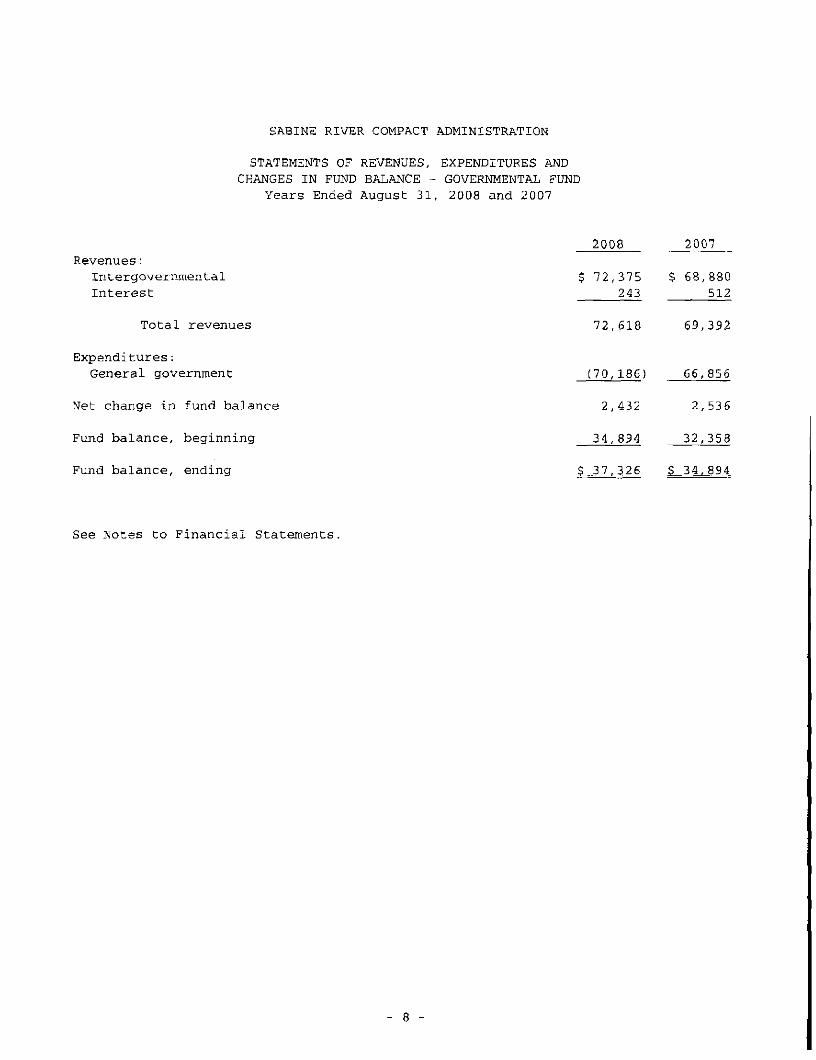

SABINE RIVER COMPACT ADMINISTRATION

STATEMENTS OF REVENUES, EXPENDITURES ANDCHANGES IN FUND BALANCE - GOVERNMENTAL FUND

Years Ended August 31, 2008 and 2007

2008 2007Revenues:

Intergovernmental $ 72,375 $ 68,880Interest 243 512

Total revenues 72,618 69,392

Expenditures:General government (70,186) 66,856

Net change in fund balance 2,432 2,536

Fund balance, beginning 34,894 32,358

Fund balance, ending $ 37,326

See Notes to Financial Statements.

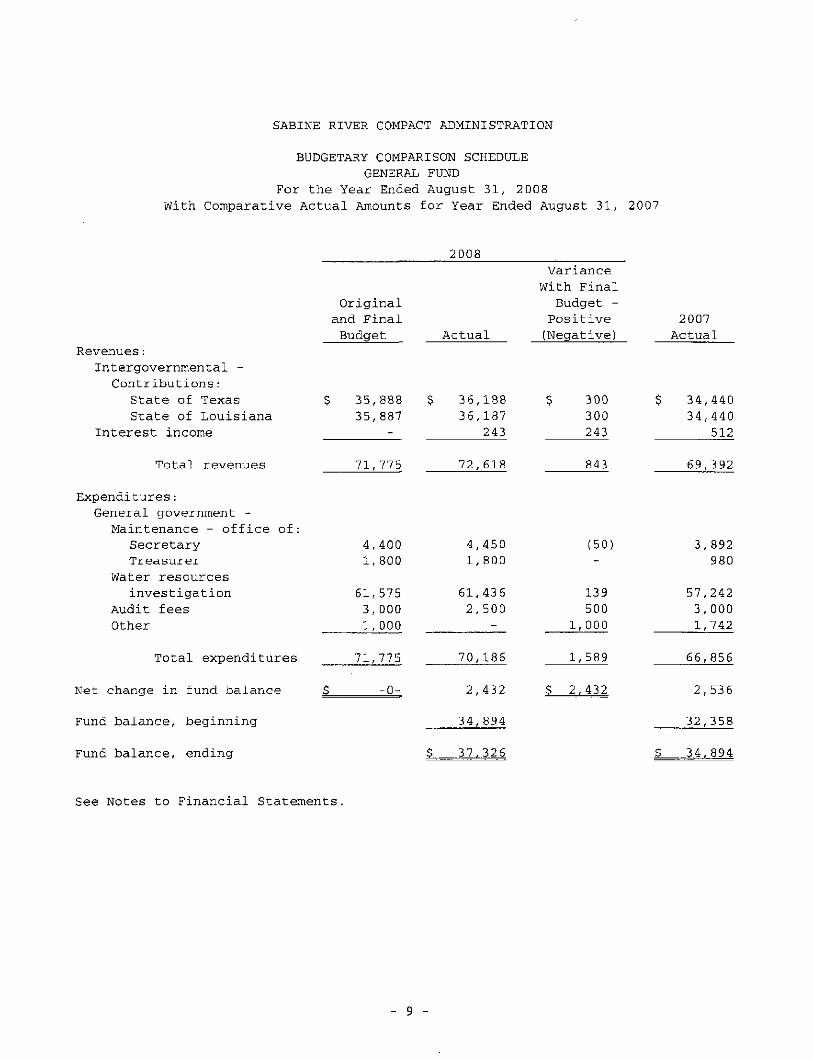

SABINE RIVER COMPACT ADMINISTRATION

BUDGETARY COMPARISON SCHEDULEGENERAL FUND

For the Year Ended August 31, 2008With Comparative Actual Amounts for Year Ended August 31, 2007

2008

Revenues:Intergovernmental -

Contributions:State of TexasState of Louisiana

Interest income

Total revenues

Expenditures:General government -

Maintenance - office of:SecretaryTreasurer

Water resourcesinvestigation

Audit feesOther

Total expenditures

Net change in fund balance

Fund balance, beginning

Fund balance, ending

Originaland FinalBudget Actual

$ 35,888 $35,887

-

71,775

4,4001,800

61,5753, 0001, 000

71,775

$ -0-

$

36,36,

72,

4,1,

61,2,

70,

2,

34,

37,

188187243

618

450800

436500-

186

432

894

326

VarianceWith Final

Budget -Positive(Negative)

$ 300300243

843

(50)-

139500

1,000

1, 589

$ 2,432

34,44034,440

512

69,392

3, 892980

5 7 , 2 4 2

3 , 0 0 0

1,742

66,856

2,536

32,358

34,894

See Notes to Financial Statements.

- 9 -

SABINE RIVER COMPACT ADMINISTRATION

NOTES TO FINANCIAL STATEMENTS

Note 1. Summary of Significant Accounting Policies

Basis of presentation:

The accompanying financial statements have been prepared in accordance withaccounting principles (GAAP) generally accepted in the United States ofAmerica as applied to government units. The Governmental AccountingStandards Board (GASB) is the accepted standard-setting body forestablishing governmental accounting principles and financial reportingstandards.

This financial report has been prepared in conformity with GASB StatementNo. 34, "Basic Financial Statements and Management's Discussion and Analysisfor State and Local Government," issued in June 1999.

Reporting entity:

The Sabine River Compact Administration, a component unit of the State ofTexas and State of Louisiana, is an entity formed by a compact entered intoby the State of Texas and the State of Louisiana on January 26, 1953, underauthority granted by an Act of the Congress of the United States approvedNovember 1, 1951, (Public Law No. 252, 82nd Congress, First Session). TheAct was amended on October 30, 1992 (Public Law No. 102-575 of the 102Congress). The objective of the Compact is to provide equitableapportionment of the waters of the Sabine River and its tributaries betweenthe two states. The operation is administered by an Inter-StateAdministrative Agency composed of two members appointed by the Governor ofTexas and two members appointed by the Governor of Louisiana; and onemember, as representative of the United States appointed by the Presidentof the United States, which member shall be ex-officio chairman of theAdministration without vote and shall not be a domiciliary of or residentin either state.

Measurement focus/basis of accounting:

Government-wide financial statements (GWFS):

The statement of net assets and the statement of activities displayinformation about the reporting government as a whole. These statementsinclude all the financial activities of the Administration.

The GWFS were prepared using the economic resources measurement focus andthe accrual basis of accounting. Revenues, expenses, gains, losses,assets and liabilities resulting from exchange or exchange-liketransactions are recognized when the exchange occurs (regardless of whencash is received or disbursed). Revenues, expenses, gains, losses,assets and liabilities resulting from nonexchange transactions arerecognized in accordance with the requirements of GASB Statement No. 33,"Accounting and Financial Reporting for Nonexchange Transactions."

- 10 -

NOTES TO FINANCIAL STATEMENTS

Fund financial statements:

Governmental funds are accounted for using a current financial resourcesmeasurement focus. With this measurement focus, only current assets andcurrent liabilities are generally included on the statement of netassets. The statement of activities reports on the sources (i.e.,revenues and other financing sources) and uses (i.e., expenditures andother financing uses) of current financial resources. This approachdiffers from the manner in which the governmental activities of the GWFSare prepared; however, there are no differences between the GWFS and thefund financial statements as of and for the year ended August 31, 2008.

Fund financial statements report detailed information about theAdministration. The focus of governmental fund financial statements ison major funds rather than reporting funds by type. The Administrationhas only one fund, the General Fund, which by definition is always amajor fund.

Governmental funds use the modified accrual basis of accounting. Underthe modified accrual basis of accounting, revenues are recognized whensusceptible to accrual (i.e., when they become both measurable andavailable). Measurable means the amount of the transaction can bedetermined and available means collectible within the current period orsoon enough thereafter to pay liabilities of the current period.Expenditures are recorded when the related fund liability is incurred.

The two major sources of revenues are intergovernmental and interest. Bothof these are susceptible to accrual.

Budgets:

Budgets are adopted on a basis consistent with accounting principlesgenerally accepted in the United States of America. An annual appropriatedbudget is adopted for the General Fund. The budget is prepared by theSabine River Compact Administration management for formal approval by theBoard of Commissioners. Any amendments to the original budget are approvedby the Board of Commissioners. Budgeted amounts presented are asoriginally adopted and as amended. Because the Administration did notamend its budget during the fiscal year, the amounts presented as originaland final are the same.

Cash:

Cash consists of amounts in interest bearing deposit accounts.

Note 2. Deposits

The bank balance of deposits was $65,471 and $47,327 at August 31, 2008 and2007, respectively, which was entirely covered by federal depositoryinsurance. Accordingly, the Administration did not have any custodial creditrisk at August 31, 2008 and 2007.

- 11 -

This page intentionally left blank.

- 12 -

BRQUSSARD, PQCHE, LEWIS & BREAUX, L.L.P.C E R T I F I E D P U B L I C A C C O U N T A N T S

4112 West CongressP.O. Box 61400Lafayette, Louisiana 70596-1400phone: (337) 988-4930fax: (337) 984-4574www.bplb.com

Other Offices:

Crowley, LA(337) 783-5693

Opelousas, LA(337) 942-5217

Abbeville, LA(337) 898-1497

New Iberia, LA(337) 364-4554

Church Point, LA(337) 684-2855

Frank A. Stagno, CPA*

Scott J. Broussard, CPA*

L. Charles Abshire, CPA*

P. John Blanchet, III, CPA*

Martha B. Wyatt, CPA*

Fayetta T. Dupre, CPA*

Mary A. Castille, CPA*

Joey L. Breaux, CPA*

Craig J. Viator, CPA*

Stacey E. Singleton, CPA*

John L. Istre, CPA*

Tricia D. Lyons, CPA*

Mary T. Miller, CPA*

Elizabeth J. Moreau, CPA*

Frank D. Bergeron, CPA*

Retired:

Sidney L. Broussard, CPA 1925-2005Leon K. Poche, CPA 1984

James H. Breaux, CPA 1987

Erma R. Walton, CPA 1988

George A. Lewis, CPA 1992

Geraldine J. Wimberley, CPA 1995

Lawrence A. Cramer, CPA 1999

Ralph Friend, CPA 2002

Donald W. Kelley, CPA 2005

George J. Trappey, III, CPA 2007

Terrel P. Dressel, CPA 2007

Herbert Lemoine II, CPA 2008

REPORT ON INTERNAL CONTROL OVER FINANCIALREPORTING AND ON COMPLIANCE AND OTHER MATTERS BASEDON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED INACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

To the Board of CoinmissionersSabine River Compact AdministrationState of Texas and Louisiana

We have audited the basic financial statements of the Sabine RiverCompact Administration, a component unit of the State of Texas andState of Louisiana, as of and for the year ended August 31, 2008,and have issued our report thereon dated October 17, 2008. Weconducted our audit in accordance with auditing standards generallyaccepted in the United States of America and the standardsapplicable to financial audits contained in Government AuditingStandards, issued by the Comptroller General of the United States.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered theAdministration's internal control over financial reporting as abasis for designing our auditing procedures for the purpose ofexpressing our opinions on the financial statements, taut not forthe purpose of expressing an opinion on the effectiveness of theAdministration's internal control over financial reporting.Accordingly, we do not express an opinion on the effectiveness ofthe Administration's internal control over financial reporting.

A control deficiency exists when the design or operation of acontrol does not allow management or employees, in the normalcourse of performing their assigned functions, to prevent or detectmisstatements on a timely basis. A significant deficiency is acontrol deficiency, or combination of control deficiencies, thatadversely affects the Administration's ability to initiate,authorize, record, process, or report financial data reliably inaccordance with generally accepted accounting principles such thatthere is more than a remote likelihood that a misstatement of theAdministration's financial statements that is more thaninconsequential will not be prevented or detected by theAdministration's internal control.

A Professional Accounting Corporation

- 13 -

A material weakness is a significant deficiency, or combination of significantdeficiencies, that results in more than a remote likelihood that a materialmisstatement of the financial statements will not be prevented or detected by theAdministration's internal control.

Our consideration of the internal control over financial reporting was for the limitedpurpose described in the first paragraph of this section and would not necessarilyidentify all deficiencies in the internal control that might be significantdeficiencies or material weaknesses. We did not identify any deficiencies in internalcontrol over financial reporting that we consider to be material weaknesses, as definedabove.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Administration's financialstatements are free of material misstatement, we performed tests of its compliance withcertain provisions of laws, regulations, contracts and grant agreements, noncompliancewith which could have a direct and material effect on the determination of financialstatement amounts. However, providing an opinion on compliance with those provisionswas not an objective of our audit and, accordingly, we do not express such an opinion.The results of our tests disclosed no instances of noncompliance or other matters thatare required to be reported under Government Auditing Standards.

This report is intended solely for the information of management. However, this reportis a matter of public record and its distribution is not limited.

Lafayette, LouisianaOctober 17, 2008

- 14 -

SABINE RIVER COMPACT ADMINISTRATION

SCHEDULE OF FINDINGS AND RESPONSESYear Ended August 31, 2008

We have audited the basic financial statements of Sabine River Compact Administrationas of and for the year ended August 31, 2008, and have issued our report thereon datedOctober 17, 2008. We conducted our audit in accordance with auditing standardsgenerally accepted in the United States of America and the standards applicable tofinancial audits contained in Government Auditing Standards, issued by the ComptrollerGeneral of the United States. Our audit of the basic financial statements as ofAugust 31, 2008 resulted in an unqualified opinion.

Section I - Summary of Auditors' Reports

A. Report on Internal Control and Compliance Material to the Financial Statements

Internal ControlMaterial Weaknesses Yes X NoSignificant Deficiencies Yes X None Reported

ComplianceCompliance Material to Financial Statements Yes X No

Section II - Financial Statement Findings

No matters were reported.

- 15 -

SABINE RIVER COMPACT ADMINISTRATION

SCHEDULE OF PRIOR FINDINGSFor the Year Ended August 31, 2008

Section I. Internal Control and Compliance Material to the Financial Statements

None reported.

Section II. Internal Control and Compliance Material to Federal Awards

Not applicable.

Section III. Management Letter

The prior year's report did not include a management letter.

- 16 -