Embed Size (px)

Citation preview

Shekha& Mufti Chartered Accountants

SALES TAX MEMORANDUM

Sindh & Punjab Finance Bills 2015

Shekha & Mufti is an independent member firm of Moore Stephens

International Limited, members in principal cities throughout the world.

Shekha & Mufti Chartered Accountants

2 Sales Tax Memorandum 2015

Preface

This Tax Memorandum summarizes crucial changes proposed through Sindh & Punjab Finance Bills 2015 regarding changes in Sindh Sales Tax on Services Act, 2011 and Punjab Sales Tax on Services Act, 2012, respectively. All changes through the Sindh & Punjab Finance Bills 2015 are effective from 01 July 2015. This Tax Memorandum contains the comments, which represent our interpretation of the legislation. We, therefore, recommend that while considering their application to any particular case, reference be made to the specific wordings of the relevant statute(s). The memorandum can also be accessed on our website www.shekhamufti.com

June 15, 2015

Shekha & Mufti Chartered Accountants

3 Sales Tax Memorandum 2015

SINDH SALES TAX ON SERVICES ACT, 2011

Overview

Reduction in general sales tax rate from 15% to 14%; Rate of tax on telecommunication decreased from 18% from 19.5%

16 New Taxable Services are brought into tax net

Increase in sales tax rates to 6% from 5% on reduced rate services

Powers of SRB Officers Enhanced

Concept of Minimum Tax Liability introduced

Penal provisions made stringent. Banks to pay upto 200% tax if it fails to attach defaulter’s bank accounts

Right of appeal granted against suspension of registration

Payment of impugned tax made compulsory before filing an appeal

Shekha & Mufti Chartered Accountants

4 Sales Tax Memorandum 2015

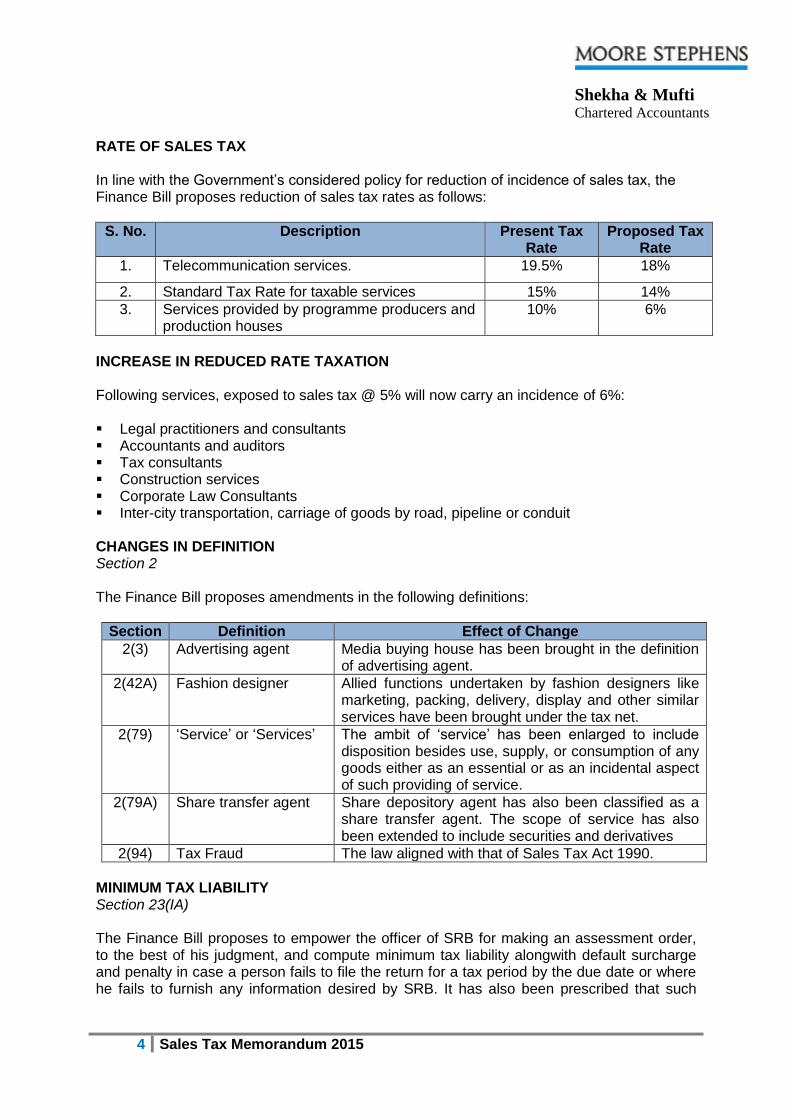

RATE OF SALES TAX In line with the Government’s considered policy for reduction of incidence of sales tax, the Finance Bill proposes reduction of sales tax rates as follows:

S. No. Description Present Tax Rate

Proposed Tax Rate

1. Telecommunication services. 19.5% 18%

2. Standard Tax Rate for taxable services 15% 14%

3. Services provided by programme producers and production houses

10% 6%

INCREASE IN REDUCED RATE TAXATION Following services, exposed to sales tax @ 5% will now carry an incidence of 6%: Legal practitioners and consultants Accountants and auditors Tax consultants Construction services Corporate Law Consultants Inter-city transportation, carriage of goods by road, pipeline or conduit CHANGES IN DEFINITION Section 2 The Finance Bill proposes amendments in the following definitions:

Section Definition Effect of Change

2(3) Advertising agent Media buying house has been brought in the definition of advertising agent.

2(42A) Fashion designer Allied functions undertaken by fashion designers like marketing, packing, delivery, display and other similar services have been brought under the tax net.

2(79) ‘Service’ or ‘Services’ The ambit of ‘service’ has been enlarged to include disposition besides use, supply, or consumption of any goods either as an essential or as an incidental aspect of such providing of service.

2(79A) Share transfer agent Share depository agent has also been classified as a share transfer agent. The scope of service has also been extended to include securities and derivatives

2(94) Tax Fraud The law aligned with that of Sales Tax Act 1990.

MINIMUM TAX LIABILITY Section 23(IA) The Finance Bill proposes to empower the officer of SRB for making an assessment order, to the best of his judgment, and compute minimum tax liability alongwith default surcharge and penalty in case a person fails to file the return for a tax period by the due date or where he fails to furnish any information desired by SRB. It has also been prescribed that such

Shekha & Mufti Chartered Accountants

5 Sales Tax Memorandum 2015

minimum tax liability shall not be the final and the taxpayer shall be liable to discharge his actual liability after the conclusion of audit, special audit or forensic audit. The proposed amendment is in line with Section 11(6) of Sales Tax Act 1990. COMMISSIONER’S POWER FOR REVIEWING ITS SUBORDINATE’S ORDER Section 23(6) Sindh Finance Bill proposes to withdraw Commissioner’s power for reviewing / amending orders passed by his subordinates, even where appeal was pending before the appellate fora. However, subject to certain conditions, Commissioner SRB can still revise orders passed under Section 55 of SSTSA. SUSPENSION OF REGISTRATION Section 25 Extended powers have been proposed for SRB officers for suspending the registration of

registered person. Currently, such powers only rests with SRB.

AUDIT BY SPECIAL AUDIT PANELS Section 29 In line with Federal Finance Bill 2015, necessary amendments have been introduced for carrying out joint forensic audit with FBR or other provincial authorities. OFFENCES AND PENALTIES

Section 43 Significant amendments have been proposed in penalty provisions thereby enhancing

the monetary limits thereof or reducing the beneficial timelines already existed in Section 43.

A specific penalty has been prescribed where the taxpayer denies or obstructs the entry

or access of the officer of the SRB posted to his business premises. In order to strengthen and protect recoveries from taxpayers’ bank accounts, a penalty of

Rs. 100,000 or 200% tax sought to be recovered from taxpayers (whichever is higher) has been proposed to be levied upon the bank if such bank fails to attach or delays in attaching the bank account of such taxpayer. Further, the manager or the officer incharge of such bank shall also be liable to conviction by a Special Judge, to imprisonment which may extend to one year or with fine or with both.

We understand such penal provision is quite harsh and would put undue pressures on the bankers for effecting the recovery of impugned demands without fulfilling their legal homework otherwise necessary before the recovery may be effected from taxpayers’ bank accounts.

Shekha & Mufti Chartered Accountants

6 Sales Tax Memorandum 2015

POWER TO ARREST AND PROSECUTE Section 49 Bill proposes amendment to empower Assistant Commissioner SRB to exercise the captioned powers. Before this amendment, Commissioner SRB was empowered to exercise such a discretion. PROVISION OF INFORMATION AND DOCUMENTS Section 52 By virtue of the amendment, SRB Officers would be entitled to call any information from the taxpayers whether or not such information was relating to SSTSA or otherwise. Presently, officer of SRB can call only that information relating to record maintained under the SSTSA. Presently, SRB can call information which relates to formulation, administering or implementing of policy. Such conditionalties have been removed from the statute. Hence, SRB has also been empowered to call for any information without any objective criteria. POSTING OF AN OFFICER OF THE SRB TO BUSINESS PREMISES Section 54(3) Necessary amendments have been made in Section 54(3) to align it with Section 40B of

Sales Tax Act 1990.

APPEAL AGAINST SRB’S ORDER REGARDING SUSPENSION OF REGISTRATION Section 57 The Finance Bill proposes granting right of appeal to taxpayer before Commissioner (Appeals) in case where his registration was suspended under Section 25(5) of SSTSA. In terms of Section 25(5), SRB may, interalia, institute proceedings against the person accused of noncompliance or cancel his registration after 60 days of suspension of registration. REFERENCE TO THE HIGH COURT Section 63 The Assistant Commissioner SRB has been empowered to file reference before High Court. Currently, an officer not below the rank of a Deputy Commissioner can exercise such an authority.

DEPOSIT OF SALES TAX DEMAND WHILE APPEAL IS PENDING Section 64 The Finance Bill proposes payment of 100% of impugned tax by the taxpayer before filing an appeal before the appellate fora. This condition is likely to cause immense burden upon taxpayers who would have to pay the entire tax demand unfront before preferring the appeal.

Shekha & Mufti Chartered Accountants

7 Sales Tax Memorandum 2015

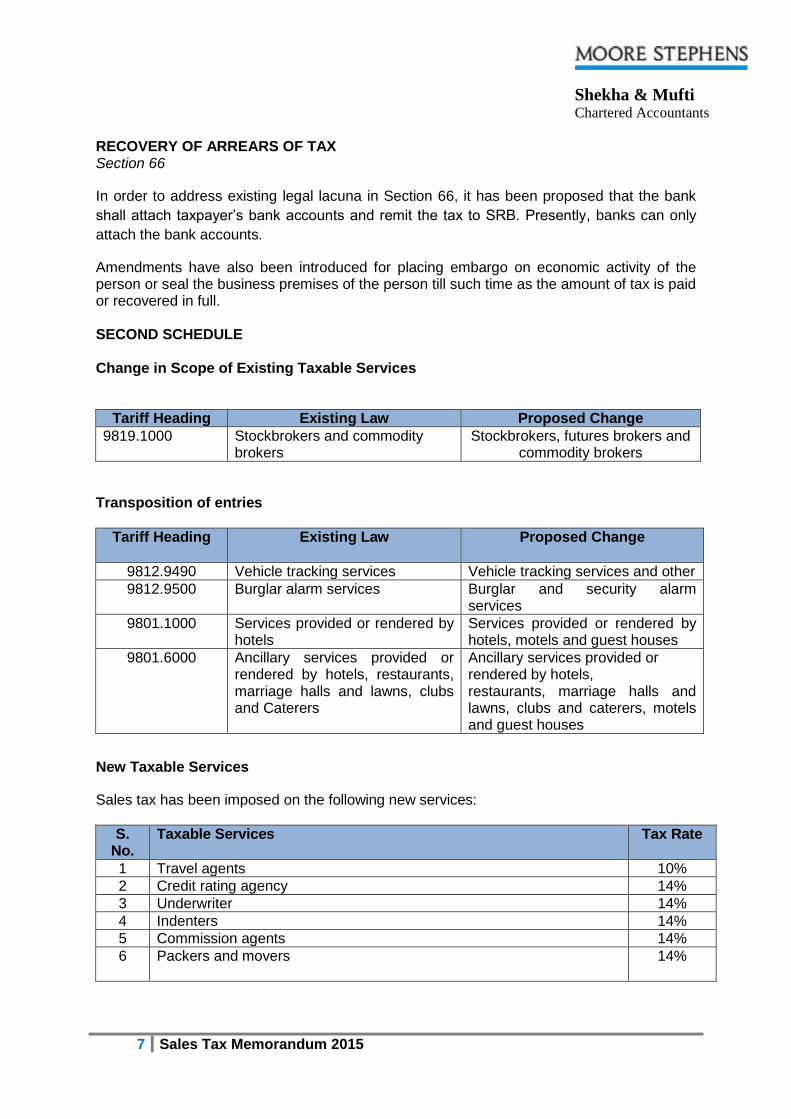

RECOVERY OF ARREARS OF TAX Section 66

In order to address existing legal lacuna in Section 66, it has been proposed that the bank

shall attach taxpayer’s bank accounts and remit the tax to SRB. Presently, banks can only

attach the bank accounts.

Amendments have also been introduced for placing embargo on economic activity of the person or seal the business premises of the person till such time as the amount of tax is paid or recovered in full. SECOND SCHEDULE Change in Scope of Existing Taxable Services

Tariff Heading Existing Law Proposed Change

9819.1000 Stockbrokers and commodity brokers

Stockbrokers, futures brokers and commodity brokers

Transposition of entries

Tariff Heading Existing Law Proposed Change

9812.9490 Vehicle tracking services Vehicle tracking services and other

9812.9500 Burglar alarm services Burglar and security alarm services

9801.1000

Services provided or rendered by hotels

Services provided or rendered by hotels, motels and guest houses

9801.6000

Ancillary services provided or rendered by hotels, restaurants, marriage halls and lawns, clubs and Caterers

Ancillary services provided or rendered by hotels, restaurants, marriage halls and lawns, clubs and caterers, motels and guest houses

New Taxable Services

Sales tax has been imposed on the following new services:

S. No.

Taxable Services Tax Rate

1 Travel agents 10%

2 Credit rating agency 14%

3 Underwriter 14%

4 Indenters 14%

5 Commission agents 14%

6 Packers and movers

14%

Shekha & Mufti Chartered Accountants

8 Sales Tax Memorandum 2015

S. No.

Taxable Services Tax Rate

7 Renting of immovable property services By virtue of such levy, renting, letting, sub-letting, leasing, sub-leasing, licensing or similar other arrangements of immovable property for commercial usage such as factories, offices including government offices or public offices, warehouses, laboratories, educational institutions, shops, showrooms, retail outlets, multiple-use buildings, etc. will be taxed. In case of a single composite rental agreement for both commercial and residential accommodation, the entire property under the agreement shall be treated as commercial property and taxed accordingly. Immovable property shall comprise of building and part of a building and the land or space appurtenant thereto; land or space incidental to the use of such building or part of a building; common or shared areas and facilities relating to the property rented; vacant land or space given on lease or license for construction or temporary structure to be used at a later stage for furtherance of business or commerce; and plant, machinery, equipment, furniture, fixture or fitting installed in or provided in or attached to the immovable property. We understand taxing rental as service will require serious deliberations regarding the exact classification of ‘rent’. Such a levy will also have far reaching consequences and impact upon a vast number of businesses operating on rented properties.

6% *

8 Services provided or rendered by laboratories other than the services relating to pathological, radiological or diagnostic tests of patients.

14%

9 Auctioneers 10% *

10 Dredging or desilting services 10% *

11 Ready mix concrete services Concrete Mix Blocks are also taxable under Sales Tax Act 1990

14% or 6% *

12 Intellectual property services 10% *

13 Erection, commissioning and installation services 14%

14 Technical inspection and certification services, including quality control certification services and ISO certifications

14%

15 Valuation services, including competency and eligibility testing services 14%

16 Utility bills collection by banks, financial institutions, NBFCs and NADRA Technologies Ltd (NTL).

14%

* Input Tax not adjustable against reduced rate services

Shekha & Mufti Chartered Accountants

9 Sales Tax Memorandum 2015

PUNJAB SALES TAX ON SERVICES ACT, 2012

Overview

10 new services brought under the tax net

Concept of forensic audit introduced

Time Limit for record maintenance prescribed

Prize schemes for general public

Rewards scheme for whistleblowers

Increase in penalties relating to non-compliance of provisions relating to compulsory registration and provision of information

Some statutory exemption threshold in case of services which have traditionally remained out of tax net and are still reluctant to pay Punjab sales tax on Services.

Shekha & Mufti Chartered Accountants

10 Sales Tax Memorandum 2015

NEW DEFINITION Section 2 The Bill proposes to insert the following new definitions in the Act:

Proposed Section

Proposed Definition

42A "taxpayer" means any person who, in the course of an economic activity, provides taxable services for consideration

2(26A) “non-banking financial institution” includes a company licensed by the Securities and Exchange Commission of Pakistan to carry out any one or more of the following forms of business: (i) investment finance services; (ii) leasing; (iii) housing finance services; (iv) venture capital investment; (v) discounting services; (vi) investment advisory services; (vii) asset management services; and (viii) any other form of business which the Federal Government may, from time to time, by notification in the official Gazette specify. The proposed definition is already defined under Rule 67 of Punjab Sales Tax on Services (Definitions) Rules, 2012.

SCOPE OF TAXABLE SERVICES Section 3(6) The Finance Bill proposes insertion of a new sub-section which gives legal status to all services as taxable services, whether existent or to be notified by Punjab Revenue Authority [PRA] in future. Through this amendment, PRA will be empowered to bring any service into tax net by way of rules and circular. It, thus, appears that services defined in Punjab Sales Tax on Services (Definitions) Rules, 2012, which are otherwise not listed in Second Schedule of PSTSA seem to have attained status of taxable services by virtue of said amendment.

RETENTION & PRODUCTION OF RECORDS / DOCUMENTS Section 32(1) In line with Section 24 of Sales Tax Act 1990, period for retention of records has been enhanced from five years to six years.

Shekha & Mufti Chartered Accountants

11 Sales Tax Memorandum 2015

SPECIAL AUDIT Section 34 In line with the proposed amendments introduced in Federal Finance Bill 2015, the concept of joint forensic audit or special audit has been introduced which may be conducted by PRA in collaboration with FBR, other provincial authorities, Chartered Accountants & Cost and Management Accountant, etc. OBLIGATION TO PRODUCE DOCUMENTS Section 57(2) & (3) Section 57(2) has been amended to enhance powers of PRA officers for calling information for the purpose of conducting audit or enquiry or investigation or otherwise under PSTSA. In addition to PRA, its Officers have also been empowered to obtain information for purposes of formulation of policy or administering or implementing PSTSA and the rules. Currently, only PRA is authorized to obtain such information. PRIZE SCHEMES TO PROMOTE TAX CULTURE Section 88 In line of Federal Finance Bill 2015, the Bill proposes introduction of a new provision to incentivize general public to make purchases from registered persons against proper sales tax invoices. WHISTLE BLOWER Section 89 A new concept of whistleblower has been introduced to align PSTSA with that of other fiscal laws. Through this scheme, the PRA will give rewards to any such person who would disclose to the competent authority any information pertaining to concealment or evasion of sales via fraud, which would result in detection of tax fraud, tax collection or misconduct carried out by any person or authority. However, the claim of reward would not be entertained in the following conditions: information provided is of no value; the Board already had the information; the information is publicly available; does not lead to collection of tax In order to place a check and balance over the information furnished by whistle blowers, a penalty of Rs.100,000 has been proposed, in case when whistleblower has provided false, misleading or frivolous information. This is a welcoming move which will ensure that only creditable information is passed onto PRA.

Shekha & Mufti Chartered Accountants

12 Sales Tax Memorandum 2015

SECOND SCHEDULE New Taxable Services Following new services have been brought into the tax net:

S. No.

Taxable Services Tariff Heading

Rate

47 Services in relation to transport of goods other than water, through pipeline, conduit or any other medium (other than inland carriage of goods by road otherwise taxable or chargeable to tax as such). Such services are already covered under S. No. 4 of Second Schedule to PSTSA.

Respective Headings

16%

48 Services provided by persons for inter-city carriage of goods by rail or road. EXCLUDING: Services provided by an individual owner of a vehicle for carriage of goods.

98.04, 9804.2000, 9804.9000 and respective headings

16%

49 Visa processing services including advisory or consultancy services for foreign education or for migration, visa application filing, services provided by document collection centres and subsequent assistance in visa processing (including all ancillary services).

Respective headings

16%

50 Services in relation to supply of tangible goods including machinery, equipment and appliances for use, without transferring right of possession and effective control of such machinery, equipment and appliances.

Respective headings

16%

51 Public relation services including communication services and services provided by public relations or media management businesses, communication specialists, media researchers, and services provided by opinion poll agencies.

9819.9200 and respective headings

16%

52 Services provided by accountants (including practicing chartered or cost accountants), auditors, actuaries, tax consultants (by whatever name called), practicing company secretaries, receivers, liquidators, auctioneers and corporate law consultants, whether individual or otherwise.

9815.2000 9815.3000 9850.0000 9851.0000 9855.0000 and respective headings

16%

Shekha & Mufti Chartered Accountants

13 Sales Tax Memorandum 2015

S. No.

Taxable Services Tariff Heading

Rate

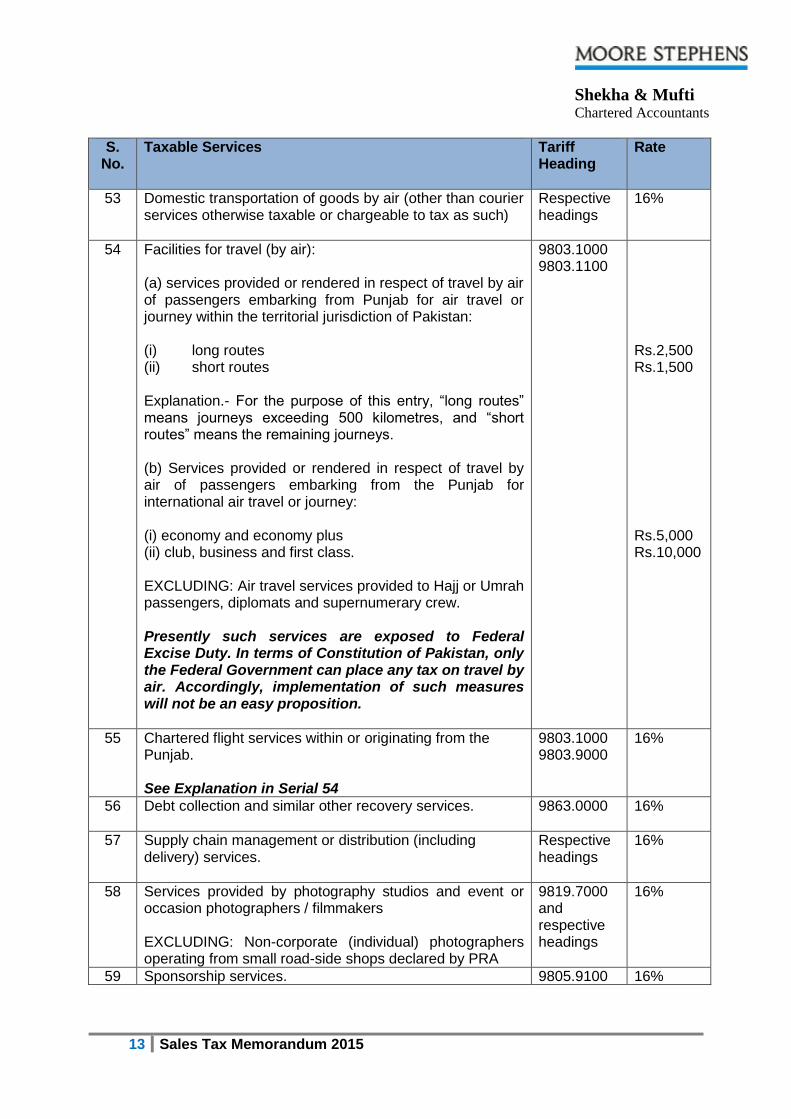

53 Domestic transportation of goods by air (other than courier services otherwise taxable or chargeable to tax as such)

Respective headings

16%

54 Facilities for travel (by air): (a) services provided or rendered in respect of travel by air of passengers embarking from Punjab for air travel or journey within the territorial jurisdiction of Pakistan: (i) long routes (ii) short routes Explanation.- For the purpose of this entry, “long routes” means journeys exceeding 500 kilometres, and “short routes” means the remaining journeys.

(b) Services provided or rendered in respect of travel by air of passengers embarking from the Punjab for international air travel or journey: (i) economy and economy plus (ii) club, business and first class. EXCLUDING: Air travel services provided to Hajj or Umrah passengers, diplomats and supernumerary crew. Presently such services are exposed to Federal Excise Duty. In terms of Constitution of Pakistan, only the Federal Government can place any tax on travel by air. Accordingly, implementation of such measures will not be an easy proposition.

9803.1000 9803.1100

Rs.2,500 Rs.1,500 Rs.5,000 Rs.10,000

55 Chartered flight services within or originating from the Punjab. See Explanation in Serial 54

9803.1000 9803.9000

16%

56 Debt collection and similar other recovery services.

9863.0000 16%

57 Supply chain management or distribution (including delivery) services.

Respective headings

16%

58 Services provided by photography studios and event or occasion photographers / filmmakers EXCLUDING: Non-corporate (individual) photographers operating from small road-side shops declared by PRA

9819.7000 and respective headings

16%

59 Sponsorship services. 9805.9100 16%

Shekha & Mufti Chartered Accountants

14 Sales Tax Memorandum 2015

CHANGE IN SCOPE OF EXISTING TAXABLE SERVICES

Services Amendments / Modifications

Services provided by hotels, “motels, guest houses, marriage halls and lawns (by whatever name called) including pandal and shamiana services”, clubs including race clubs and caterers.

Ancillary services rendered by caterer such as floral or other decoration, furnishing of space whether or not involving rental of equipment and accessories has been brought into tax net.

Advertisement on television and radio, excluding advertisements financed out of funds provided by a Government.

Exemption of sales tax has been restricted to advertisements financed out by Government of Punjab under foreign grant in aid.

Courier services Express cargo or logistic services are proposed to be brought under tax net in addition to other services

Franchise Service Licensing services such as software licensing fee, etc. are proposed to be brought under tax net

Construction services Following exemptions are proposed to be withdrawn:

Threshold of Rs.50 million per annum for

construction projects

Construction of industrial zones, Other organizations exempt from income

tax. Currently, blanket tax exemption is available on residential projects meant for the purpose of construction. However, proposed amendment places conditions for such tax exemptions.

Services provided by property developers. Builders are proposed to be brought under tax net besides property developers.

Services provided for personal care

Additional personal care services are proposed to be brought under tax net. However, parlour, salon or clinic without air-conditioning will remain exempt.

Shekha & Mufti Chartered Accountants

15 Sales Tax Memorandum 2015

Services Amendments / Modifications

I.T. services

Variety of information technology services are proposed to be brought under tax net.

Services provided by other consultants Human resource and personnel development services, exhibition or convention services, event management services (whole range and variety of their services regardless of separate or individual classification thereof), valuation services evaluation services (including competency and eligibility testing services), certification, verification and equivalence services, market research services, marketing or sales services (including marketing agencies and on line marketing or sales services), surveyors services, training or coaching services (other than general education services) and credit rating services have been brought under the tax net.

Services provided by a registrar to an issue, etc.

Investor account services, trustee or custodial services, share registrar services and their allied or connected services have been added in the list of taxable services.

Services provided by fashion designers Ambit of fashion designer’s services has been enhanced.

Services provided by architects, town planners.

Landscapers and landscape designers are proposed to be included under tax net.

Services provided in respect of rent-a-car

Through such amendment, scope of renting services has been enhanced to all sort of vehicles including cars.

Services provided by laboratories

Exemption of sales tax on pathological or diagnostic labs has been restricted for medical treatment only.

Shekha & Mufti Chartered Accountants

16 Sales Tax Memorandum 2015

CHANGE IN RATE OF EXISTING TAXABLE SERVICES

Taxable Services Existing Rate Proposed Rate

Freight forwarding agents. Rs. 400 per bill of lading

Rs.1,000 per bill of lading

EXEMPTION

The Punjab Finance Minister announced withdrawal of tax on internet services in her budget speech in the Punjab Assembly. Earlier, tax on internet was imposed vide PRA Notification No. SO(TAX)1-1/2014-15(Vol-1) dated 28 May 2015.

Shekha & Mufti Chartered Accountants

17 Sales Tax Memorandum 2015

Principal Office C-253, P.E.C.H.S., Block 6 Off Shahrah-e-Faisal Karachi. Pakistan

P + 92 21 3 4374811-15 F + 92 21 34544766 [email protected] Branch Office

Office No. 4, 3rd Floor Rehman Plaza Queens Road, Off The Mall Lahore. Pakistan P + 92 42 3 6298231-3 F + 92 42 3 6298234 [email protected]