Embed Size (px)

Citation preview

Swedish Savings Banks and Competition

A Panzar-Rosse model approach

Andreas Vigren

Student

Spring 2012

Master’s Thesis I, 15 ECTS

Supervisor, Thomas Aronsson

Abstract

In this paper the Swedish savings banks sector is analyzed between the years 2002 and

2010 using the Panzar-Rosse model. The model uses the reduced form revenue function

to capture a relation with the factor price elasticites. The narrow geographical area

for many savings banks along with local presence for many years creating awareness of

the bank may suggest that these banks could act as local monopolies. A comparison

is also made with commercial banks as well as savings banks of different sizes. Using

data for 49 savings banks and eight commercial banks the findings suggests monop-

olistic competition behaviour by savings banks and that commercial banks could be

characterized by monopoly. The results suggests that neither bank type, nor savings

banks of different sizes, can be confirmed acting competitively. The only exception is

medium sized savings banks. Thus, the conclusion is that the Swedish banking sector

is not competitive.

Keywords: Competition, Savings banks, Commercial banks, Panzar-Rosse model,

Swedish banking sector, Monopolistic competition, Perfect competition, Monopoly

Acknowledgements

First and foremost I would like to express my sincere thanks and gratitude to my

supervisor Thomas Aronsson for his guidance, support, comments and patience before

and throughout the writing process. Without his help this thesis would not have been

written.

A thanks also to all savings banks who provided data to the study. The Swedish postal

service has seen a large increase in revenues during this period.

Furthermore, I owe gratitude to Sherrill Shaffer for his time and help.

A special thanks is sent to the kind people in the front desk of the Swedish Companies

Registration Office (Bolagsverket) who not only provided help with computers, but

also fetched several cups of well needed coffee.

Audere Est Facere

Andreas Vigren

Contents

1 Introduction 5

1.1 The Swedish banking sector . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

1.2 Previous studies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

1.3 Purpose . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

1.4 Research question . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2 Theoretical Framework 11

2.1 The Panzar-Rosse model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.2 Empirical model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3 Empirical Framework 20

3.1 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

3.2 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

4 Results 25

5 Conclusion 29

References 32

Appendix A List of banks 34

Appendix B Econometric appendix 35

B.1 Correlation matrices and descriptive statistics . . . . . . . . . . . . . . . . . 35

B.2 Long-run equilibrium (ROA) test . . . . . . . . . . . . . . . . . . . . . . . . 37

B.3 Estimates including Nordea . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Appendix C Mathematical appendix 39

C.1 Monopolistic competition (section 2.1.2) . . . . . . . . . . . . . . . . . . . . 39

C.2 Perfect competition (section 2.1.3) . . . . . . . . . . . . . . . . . . . . . . . 40

1 Introduction

Today, banks are a crucial part of most people’s everyday life handling money, loans, debit

and credit cards and so on. One can argue that it is important with a well functioning

competition in a market that vital to society. Competition may, in this case, manifest itself

in terms of a wide selection of services and activities as well as in terms of prices for these

services. A lack of alternatives could, as in all other markets, make the market work more

inefficient. The Swedish banking sector is strongly dominated by four banks1 that together

hold about 80% of the total assets in the bank sector, a position that has been relatively

unchanged during the last decade (Swedish Bankers Association, 2011). The other 113

banks, both domestic and foreign, share the remaining 20%. This indicates that banks

may exhibit market power.

Schaeck et al. (2009) concludes that the greater the competition in a banking market,

the less is the risk of suffering a “systemic crisis”. This should speak in favor of having a

competitive banking market. In discussing if perfect competition is the market structure

that should be preferred, Cetorelli and Gambera (2001) note that a more competitive

market tends to increase the quantity of credit, while a a less competitive bank sector

instead would increase the quality of the loans (i.e. the borrowers). This is much in line

with what happened in Sweden during the late 1980’s after the deregulation of the credit

market. When the lending from banks rapidly increased, and the actors on the market

were fighting for customers, many bad loans were given leading to massive credit losses.

Sweden has a long tradition of a particular banking form called savings banks, reaching

back to 1820, which, in brief, has mainly focused on competing in the local districts’.

(Korberg, 2007) A more narrowed geographical business area for a bank could increase the

knowledge about the bank among the population, and also create sympathy, because of

its local presence. This is turn may give additional, and also more loyal, customers for

the bank, implying that the customers may, for example, be more reluctant to switching

banks or, because of loyalty feelings, not choosing other banks, creating entry barriers on

the local market (Nordic competition authorities, 2006). This raises questions about how

competitive this market really is. If customers are sticky (i.e. not behaving as in a perfect

competitive market) with respect to switching bank, the savings banks could be viewed as

local monopolies. Gischer and Stiele (2009) found that the savings banks in the German

market, and in particular the smaller ones, are characterized by less competition than the

1Swedbank, Handelsbanken, Nordea and SEB

5

commercial banks. More precisely, Gischer and Stiele found that the savings banks sector

is characterized by monopolistic competition. Another study, Sjoberg (2007), analyzed the

Swedish local banking market and found evidence of more competitive behavior among

commercial banks than among the savings banks.

This paper contributes to the empirical literature by investigating the structure of

the Swedish savings banks sector between the years 2002 and 2010. A comparison with

the commercial banks is also made which clarifies whether there could be differences in

competition depending on type of bank (i.e. savings bank or commercial bank).

The paper is organized as follows. The remainder of section 1 describes the Swedish

bank sector, and puts special emphasis on the history of the savings banks. There is also a

brief discussion of previous studies in this field, followed by the purpose of the paper along

with the research question. In section 2 the theoretical framework used for the empirical

analysis is presented. Section 3 specifies the data and model to be used in the analysis.

The result is presented in section 4 and conclusions in 5.

1.1 The Swedish banking sector

In the beginning of 2011 there were 114 banks doing business in the Swedish banking sector.

Of these, 19 were commercial banks, 29 foreign banks and 64 savings banks. Between the

years 2000 and 2011 the number of banks operating in Sweden decreased from 124 to 114.

The largest drop refers to the number of savings banks, which decreased from 79 in 2000

down to 50 in 2011.2 (Swedish Bankers Association, 2011) The overall decrease in the

number of banks as well as the dominance of the four largest banks could imply that the

competition has decreased during these years as the number of competitors has decreased.

1.1.1 The savings banks

Savings banks have a long tradition in the Swedish banking sector. The first savings bank

was founded in 1820 in Gothenburg and would become one of the hundreds of savings

banks established within the upcoming decades. In 1892, the first savings banks law was

established and included all of the 378 savings banks at that time. This law, and the

upcoming laws, pointed out some of the characteristics of savings banks’, for example, the

idea of promoting savings, local support and the absence of individual profits, which means

2The decrease is partly due to a conversion to commercial banks, done by 14 savings banks, but are alsodue to mergers to create larger units.

6

that the profits that were not reinvested in the savings bank were dispersed as dividends

to support the local district. The future laws also opened up, step by step, the possibilities

for the savings banks to manage lending and other banking activities apart from only the

savings business. These laws were established for the savings banks to be able to compete

with the larger commercial banks that did not face restrictions in which services to provide.

(Korberg, 2007)

During the forty years that passed, the number of savings banks substantially increased.

A decentralized business model meant there was little cooperation between the savings

banks, and many of them were dependent on commercial banks to, for example, supply

the savings banks with cash and, if needed, give credits to the savings banks. By the

establishment of Sparbankernas Bank in 1942, which was founded by several savings banks,

this dependence on the commercial banks was broken. Sparbankernas Bank acted similarly

to a central bank towards the savings banks, by helping them with the same things that

the commercial banks previously had done. The founded bank was a commercial bank,

but was fully owned by the participating savings banks across the whole country. In

1969, the savings banks law was changed so that the savings banks from then on could

compete on precisely the same conditions as the commercial banks because, until then,

they had been restricted in especially the lending business. During the next two decades,

several larger mergers amongst savings banks were made, leading in many cases to an

organization with more or less no coordination between the business units, because of the

large and geographically widespread units. This resulted in that the old rule of “the church

tower principle”3 was not applied as much as before. More and more, the smaller savings

banks felt the competition from the larger merged savings banks, as well as the commercial

banks, and formed the Savings Banks Association which made them a strong counterpart

to the larger banks. This association helped them to negotiate more favorable terms of

cooperation with other banks, which in turn helped them in their daily business. (Korberg,

2007)

The beginning of the 1990s turned out to be a turbulent time in the history of the

savings banks. Due to the credit deregulation in 1985, several savings banks had expanded

their lending dramatically, which lead to massive credit losses in the financial crisis that

struck Sweden in 1991. During the same year, an important change in the savings banks

law made it possible to convert savings banks to regular commercial banks, giving the

3This principle meant that the bank should not lend money to, or make other business arrangements,with customers living outside the sight from the districts church tower.

7

possibility to inject capital from outside sources. This possibility had been impossible for

the savings banks, which until then had only been able to rely on the previous profits

of the banks. The change made it possible for eleven savings banks to merge into one

commercial bank, resulting in the publicly listed Sparbanken Sverige AB. This new bank

was formally a public commercial bank, but was to a large extent owned by the savings

banks foundations4. A savings banks foundation are, and was, created when a savings

bank converted to become a commercial bank, and owned the shares in the newly created

commercial bank. The foundations have similar characteristics to the savings banks, which

means that the new commercial banks created by the new law still acted upon the values of

the savings banks. A similar merger as the one creating Sparbanken Sverige was made by

the Foreningsbanks’, creating Foreningsbanken AB, which until then had been a corporate

bank for the past 80 years. In 1997, Sparbanken Sverige and Foreningsbanken merged,

creating one of the largest banks in Sweden, Foreningssparbanken, which later changed its

name to Swedbank. (Korberg, 2007)

Today, the majority of the savings banks have a strong connection to Swedbank through

an intimate cooperation agreement where they share, for example, technological platforms

and possibilities for customers in the savings banks and Swedbank to use each other’s

branches for banking services. However, all savings banks that did not participate in the

merger to Sparbanken Sverige are, regardless of if it is a “pure” savings bank or a converted

commercial bank, still independent firms. A list of these banks are provided in appendix

A.

1.2 Previous studies

Today, a vast literature about the competition in the banking sector exists and is based

on different statistical methods. In this section, a selection of studies is discussed focusing

mainly on the Swedish banking sector, but also studies from Germany as the savings banks

have a strong position there.

Vesala (1995) uses the Panzar-Rosse model to investigate competition in the Finnish

banking sector. In brief, the Panzar-Rosse model tries to capture the relationship between

factor price elasticities and the reduced form revenue function at the firm level. This makes

it possible to test whether firms behave as monopolists, monopolistic competitors or in

accordance with perfect competition. A more thorough discussion of this model is provided

4Sparbanksstiftelserna

8

in section 2.1. Vesala conclude that the banks behave in a monopolistic competitive way,

which is a common result from the Panzar-Rosse model (see, for example, table 1)

Schaeck et al. (2009) also applied the Panzar-Rosse model, investigating the relationship

between competition in the banking sector and financial crises for 45 countries during the

years 1980 and 2005. The general findings were monopolistic competition, but the results

vary over countries. Schaeck et al. concludes that concentration cannot proxy competition,

probably due to that competition is a local issue and that the concentration measures do not

capture local competition as they often are conducted at national levels with aggregated

data. The authors estimates a H-statistic consistent with monopolistic competition in

Sweden, and a concentrate ratio of 0.98 based on the three largest banks.

Carbo et al. (2009) applied a number of different approaches to measure competition

in the bank sector in 14 European countries, including Sweden. The approaches used are

the net interest margin to total assets, Lerner Index, Ratio of bank net income to the

value of total assets, Panzar-Rosse model and also the Hirschman-Herfindahl index. The

findings were that the measures are only weakly positively related to each other, meaning

that they probably do not measure the same thing. However, any conclusions about the

Panzar-Rosse model and its fitness to similar methods are not drawn. The authors do,

however, conclude that amongst the four other measures the Lerner index and Returns on

assets are more preferred in measuring overall banking activity. In the study, the Swedish

banking sector was found to be a monopolistic competitive.

In analyzing the competition of the banking sector in the EU, Bikker and Haaf (2002)

found strong evidence for monopolistic competition in most markets, including Sweden,

when using the Panzar-Rosse methodology. Estimations were also conducted at small-

medium- and large bank sizes where the findings were that the degree of competition

declined with the size of the bank. However, this was not true in the Swedish market

where the medium-sized banks had the weakest competition measure.

Turning to the savings banks specifically there is a limited number of studies performed

in the Nordic countries. Sjoberg (2007) found that the Swedish savings banks do not act

in a perfectly competitive market, but not in a “Cournot conduct” either. Sjoberg also

concludes that the competition between savings banks was less than amongst commercial

banks.

In the German savings banks sector both Hempell (2002) and Gischer and Stiele (2009)

found evidence of monopolistic competition using the Panzar-Rosse approach. In their

analysis of the German savings bank Sparkassen the authors also found that smaller savings

9

Table 1: Summary of findings from previous studies

Author Country Time period Banks Method FindingSchaeck et al. (2009) Sweden1 1980-2005 Whole market P-R MCVesala (1995) Finland 1985-1992 Whole market P-R MCBikker and Haaf (2002) Sweden1 1988-1998 Whole market P-R MCBikker and Groeneveld (2000) Sweden1 1989-1996 Whole market P-R MCHempell (2002) Germany 1993-1998 Savings banks P-R MCGischer and Stiele (2009) Germany 1993-2002 Savings banks P-R MCCarbo et al. (2009) Sweden1 1995-2001 Whole market P-R MCSjoberg (2007) Sweden 1996-2002 Commercial BR Not PC2

Sjoberg (2007) Sweden 1996-2002 Savings banks BR Not PC2

MC=Monopolistic competition; PC=Perfect competition; P-R: Panzar-Rosse; BR=Bresnahanand Reiss entry model1 The paper provides results for more countries than just Sweden2 The competition amongst commercial banks are significantly higher than amongstsavings banks

banks had a lower degree of competition than the larger ones. They also conclude that

the economic problems facing the larger German banks seems not to be due to matters

of competition, but rather to “a more difficult market segment” such as financing large

corporate groups and trading with complex derivatives. Gischer and Stiele also find that

the less competitive savings banks market seems more profitable than the market facing

the larger actors.

The results from previous studies discussed in this section are summarized in table 1

1.3 Purpose

The main difference between this and the previous papers studying bank competitions is

the focus on savings banks. As far as the author is aware, no similar study has been

performed using the Panzar-Rosse model on savings banks specifically. In addition, there

are no previous studies analyzing the Swedish banking sector after 2007.

The purpose of this paper is to investigate if the Swedish savings banks are acting in

a perfectly competitive, monopolistic competitive, or monopoly market between the years

2002 and 2010. Furthermore, a comparison of the competition between the commercial

and savings banks in the same time period is made, as well as between savings banks of

different sizes.

10

1.4 Research question

Is the Swedish savings banks industry acting competitive, or is it rather characterized by

monopolistic competition or behaving as local monopolies? In addition, are there any

differences compared to the competition amongst commercial banks or savings banks of

different sizes?

2 Theoretical Framework

In measuring competition several methods are used in the literature, and the most fre-

quently used methods will be described below. A popular method is the Bresnahan-Lau

model. By defining demand- and supply functions for a product or market one can es-

timate, assuming that firms are not price takers, a markup (λ) from the price equation

(obtained from the supply function), where λ ∈ (0, 1). A value zero implies that the

market is characterized by perfect competition, whilst a value of one denotes a monopoly

market.(Bresnahan, 1982) (Lau, 1982) As the Bresnahan-Lau model requires data at the

market level, it is hard to apply the model on the banking market due to difficulties to

find appropriate explanatory variables in the demand and supply functions, especially the

price variable.

The Boone indicator has recently been applied (see e.g. van Leuvensteijn et al. (2010)

and van Leuvensteijn et al. (2011)). The model is built on the assumption that a more

efficient firm (firms with lower marginal cost) will be more competitive than a less effi-

cient one. Thus, by analyzing market shares and marginal costs, an indicator is obtained

measuring the degree of competition. The indicator has a more negative value (larger in

absolute terms) the more competitive a market is.

Another approach is typically referred to as the Panzar-Rosse model. Panzar and Rosse

(1987) developed a theoretical model which builds upon the elasticities of the firms income

with respect to factor prices, and that the competition could be tested from those. A

thorough explanation of this model is given in section 2.1. A major advantage of the

Panzar-Rosse model is that it does not require data on the market level, but instead uses

firm level data, which is easier to find. Also, it is possible to distinguish between more

forms of imperfect competition than just monopoly (compare with, e.g., the Bresnahan-Lau

model). Some disadvantages is that a banks annual reports might report data from more

than one market (e.g. other countries) which must be taken into consideration. Also, larger

11

banks most often make larger profits etc. which can cause problems in the estimation. A

solution to this is to divide the sample into different classes of size. In addition, since the

Panzar-Rosse model assumes that the sample is in long-run equilibrium the results from a

non-long-run equilibrium sample may cause spurious and unreliable results.5 Although the

Panzar-Rosse model has disadvantages, it will be used in this paper as it fits the banking

market well and are widely applied in academical literature.

2.1 The Panzar-Rosse model

John C. Panzar and James N. Rosse introduced a test for imperfect market structures,

which has been widely used when analyzing the competitiveness of different markets. In

brief, the model uses comparative statics from the firms reduced form revenue function, and

thereafter the sum of the factor price elasticities to determine the degree of competition.

(Panzar and Rosse, 1987) The model is based on the assumptions that the firms in the

sample are profit maximizing, that the sample must be in a long-run equilibrium, and

that the average cost curve is convex with respect to price and quantity. All of these

assumptions are assumed to be fulfilled. The presentation of the model given in section

2.1 mainly follows the articles of Panzar and Rosse (1977) and Panzar and Rosse (1987),

if nothing else is referenced. This theoretical framework will be the foundation of the

empirical model presented in section 2.2. The model will from now on also be referred to

as the PR-model.

2.1.1 The monopoly case

Consider a monopoly firm. If y is a vector of output variables affecting firm revenue, and z

a vector of q exogenous variables shifting the revenue function of the curve, the sole firms

revenue function can be described as

R = R(y, z) (2.1)

The firm’s cost is either directly, or indirectly, connected to y resulting in a cost function

C = C(y, w, t) (2.2)

5A test for long-run equilibrium is available through Shaffer (1982) and is presented in section 2.2.1

12

where w is a vector of factor prices and t a vector of variables shifting the firms cost

function. It is also possible for z and t to have common variables. Profits of the firm can

be expressed as

π = R− C = π(y, z, w, t) (2.3)

Define y0 = arg maxyπ(y, z, w, t) and y1 = arg maxyπ(y, z, (1 + h)w, t) where the scalar

h > 0. Also define R0 = R(y0, z) ≡ R∗(z, w, t) and R1 = R(y1, z) ≡ R∗[z, (1 + h)w, t],

where R∗ is the reduced form revenue function of the firm. By using equation (2.3) and that

the cost function is homogenous of degree one, the following is true by profit maximization

R1 − (1 + h)C(y1, w, t) > R0 − (1 + h)C(y0, w, t) (2.4)

and

R0 − C(y0, w, t) > R1 − C(y1, w, t) (2.5)

Multiplying (2.5) with (1 + h)

(1 + h)[R0 − C(y0, w, t)] > (1 + h)[R1 − C(y1, w, t)] (2.6)

and adding (2.6) to (2.4) gives

(1 + h)[R0 − C(y0, w, t)]− (1 + h)[R1 − C(y1, w, t)]

+R1 − (1 + h)C(y1, w, t)−R0 + (1 + h)C(y0, w, t) > 0

− h(R1 −R0) > 0 (2.7)

Dividing (2.7) with h2 gives

R1 −R0

h=R∗[z, (1 + h)w, t]−R∗(z, w, t)

h6 0 (2.8)

Equation (2.8) shows that an equiproportional cost increase results in a decrease in the rev-

enues of the firm. Assuming that the firms reduced form revenue functions is differentiable,

taking the limit of h and dividing with R∗

Ψ∗ ≡i∑

i=1

∂R∗

∂wi

wi

R∗ 6 0 (2.9)

13

which gives the sum of factor price elasticities of the reduced form revenue function. Equa-

tion (2.9) shows that the sum of these elasticities must be nonpositive in the case of a

monopoly firm.

2.1.2 Monopolistic competition

In the case of differentiated products across various firms, the monopolistic competition

case is a possible market imperfection. Panzar and Rosse argue, with a discussion about

the work by Chamberlin (1962) and the Chamberlin equilibrium, that

“Each firm, viewed in isolation, would, in both theories6, behave exactly as a monopoly would,

and its actions would satisfy all the conditions of profit maximization. Nevertheless it may be hoped

that by examining the effects of changes in exogenous variables the “hidden” forces of Chamberlin’s

“group equilibrium” condition may come into focus” - (Panzar and Rosse, 1987, p. 448-449)

The analysis is thus based on how the single acts in a long-run equilibrium, when prices and

number of firms active on the market have adjusted. A way to distinguish the monopolistic

competition case from perfect competition is desirable, and also possible to do by analyzing

the elasticity of factor prices derived later in this section. The monopolistic competition

concept used here could be called “The long-run monopolistic competition” or ‘Chamber-

linian Monopolistic Competition” and is a long-run equilibrium where the number of firms

is endogenous.

By using comparative statics and defining R(y, n, z) = yP (y, n, z), where n is the

number of firms , the monopolistic competition case is defined by equation (2.10) and

(2.11) and describes the long-run equilibrium values y∗ and n∗, treating the other variables

as exogenous.

Ry(y∗, n∗, z)− Cy(y∗, w, t) = 0 (2.10)

R(y∗, n∗, z)− C(y∗, w, t) = 0 (2.11)

In order to derive an expression for the factor price elasticities, using that R(y∗, n∗, z) =

R∗(z, w, t) from section 2.1.1 and the chain rule, differentiating (2.11) gives

∂R∗

∂wi= Cy

∂y∗

∂wi+∂C

∂wi= Cy

∂y∗

∂wi+ x∗i (2.12)

where x∗i is the optimal quantity of production factor i, following Shepard’s lemma. Multi-

6The pure monopoly and the pure competition (authors note)

14

plying by (wi/R∗) and summing over equation (2.12)

Ψ∗ =

i∑i=1

wi

R∗∂R∗

∂wi

=Cy

R∗

i∑i=1

wi∂y∗

∂wi+

C

R∗ (2.13)

Thus, an expression for the factor price elasticities is defined. ∂y∗/∂wi is obtained by

totally differentiating (2.10) and (2.11) with respect to y∗, n∗ and wi, and solving using

Cramer’s rule7∂y∗

∂wi=Rn(∂x∗i /∂y)−Rynx

∗i

D∗ (2.14)

where D∗ = (Ryy − Cyy)Rn > 0 from appendix C.1. Substituting (2.11) and (2.14) into

equation(2.13) gives

Ψ∗ =Cy[Rn

∑wi(∂x

∗i /∂y)−Ryn

∑wix

∗i ]

R∗D∗ + 1

As x∗i represents the cost minimizing input factor i, a change in this when the output level

(y) changes should equal marginal cost if multiplied with wi.

i∑i=1

wi(∂x∗i /∂y) =

∂C

∂y= Cy

From this, and using that∑i

i=1wix∗i = C, it follows that

Ψ∗ = 1 +Cy[RnCy −RynC]

R∗D∗

Again using (2.10) and (2.11)

Ψ∗ = 1 +Ry[RnRy −RRyn]

R∗D∗ (2.15)

By using the inverse demand function and the fact that R = Py, the bracketed term

7A complete derivation of the steps leading to equation 2.14 is provided in appendix C.1

15

(RnRy −RRyn) can be rewritten as

(Pyn + yPn)(P + yPy)− Py(Pn + ynPy + yPyn)

= y2PnPy − y2PPyn + P 2yn

The term P 2yn will disappear. The intuition is that a the change in n will not affect the

markets output, as the monopolistic equilibrium quantity is reached only with a specific

number of firms acting simultaneously in the long-run equilibrium. Entry of one more firm

must result in an exit of another, otherwise the long-run equilibrium will not hold. Hence,

output will not change, yn = 0 and the final equation reduces to

y2(PnPy − PPyn) = (RnRy −RRyn) (2.16)

Inserting (2.16) into (2.15) yields

Ψ∗ = 1 +Ry[y2(PnPy − PPyn)]

R∗D∗ (2.17)

An assumption made by Panzar and Rosse in deriving the monopolistic competition

outcome is that

“The elasticity of perceived demand facing the individual firm [...] is a nondecreasing function

of the number of (symmetric) rivals ” - (Panzar and Rosse, 1987, p. 450)

Writing the elasticity as e(y, n, z) ≡ −P/(y∂P/∂y), where P = P (y, n, z) and ∂P/∂y ≡Py < 0. We also say that ∂P/∂n ≡ Pn < 0. This leads to the fact that en > 0, which

implies that if there are entries into the market, and thereby more substitutes, the demand

facing the sole firm becomes more elastic and reduces the market power exhibited by that

firm (Vesala, 1995). en can be expressed as

en =PyPyn

(yPy)2− Pn

yPy

= −PnPy − PPyn

yP 2y

(2.18)

As en > 0, the numerator must be less than zero. Knowing this, its possible to sign Ψ.

When the term inside the parenthesis is less than zero and both R∗ and D∗ are larger than

16

zero the second term in equation (2.17) must be negative. This implies that

Ψ < 1 (2.19)

which states that if the factor prices are increased with one percent, there will not be an

equally large increase (or decrease) in the reduced form revenue.

2.1.3 Perfect competition

The conditions for perfect competition, price equal to marginal cost and zero profit, must

be fulfilled. These are written as

pc − Cy(yc, w, t) = 0 =⇒ pc = Cy(yc, w, t) (2.20)

pcyc − C(yc, w, t) = 0 =⇒ pcyc = Rc(w, t) = C(yc, w, t) (2.21)

where pc and yc is the equilibrium price and output, respectively, in the perfect competition

case, and Cythe firms marginal cost with respect to output. Equation (2.20) represents the

single firms first order profit maximizing condition, whilst equation (2.21) is the long-run

equilibrium condition. Using these two equations and totally differentiating with respect

to yc, pc and wi, and then solving by Cramer’s rule yields8

∂yc

∂wi=x∗i − yc(∂x∗i /∂yc)

ycCyy(2.22)

Using (2.21) and Shepard’s lemma, the derivative of Rc with respect to wi yields

∂Rc

∂wi= Cy

∂yc

∂wi+ x∗i

Multiplication by wi and summarize

i∑i=1

wi∂Rc

∂wi= Cy

i∑i=1

wi∂yc

∂wi+

i∑i=1

wix∗i (2.23)

8A complete derivation of the steps leading to equation 2.22 is provided in appendix C.2

17

Inserting (2.22), dividing with Rc and using (2.20) and (2.21) to simplify and rewrite the

expression in (2.23)

Ψc =i∑

i=1

∂Rc

∂wi

wi

Rc

=Cy

Rc

i∑i=1

(wix∗i − yc(∂x∗i /∂y)

ycCyy

)+

i∑i=1

wix∗i

R

=Cy

RcycCyy(C − ycCy) +

C

Rc

=P

RcycPy(pcyc − pcyc) +

Rc

Rc= 1 (2.24)

Thus, equation (2.24) shows that the sum of elasticities of the reduced form revenue func-

tion with respect to factor prices is equal to the one in the long-run partial equilibrium,

meaning that a proportional increase in factor prices leads to an equiproportional increase

in revenues in the long-run equilibrium.

2.1.4 The Ψ-statistic

From the previous sections Ψ is defined as∑i

i=1 [(∂R/∂wi)(wi/R)] which represents the

sum of elasticities of the reduced from revenue function. From now on this elasticity is

called the Ψ-statistic. Summing up the findings regarding Ψ obtained in sections 2.1.1 -

2.1.3 produces table 2 where the Ψ-statistic and its implications are presented. Earlier

studies often denote the measure as a H-statistic. However, this paper will follow the

original notation (Ψ) by Panzar and Rosse.

There are, however, four additional possible outcomes that were not derived above.

Perfectly collusive oligopoly outcome (oligopoly in a contestable market) which occurs at

Ψ 6 0 (Shaffer, 1983), conjectural variation oligopoly at Ψ > 0 (Panzar and Rosse, 1987) re-

spective natural monopoly and a “sales maximizing firm subject to a break-even constraint”

which both corresponds to Ψ = 1 (Shaffer, 1982). These outcomes are not analyzed further

as the Swedish banking sector, most likely, are not an oligopoly market, following from the

extensive control systems laid out by the government which should notice this type of un-

desirable behavior. A natural monopoly is neither likely as firms are able to stay in the

market and still make profits, which are not in line with this structural form.

One assumption necessary for Ψ ∈ (0, 1) is that the market operates in a long-run

18

Table 2: Outcomes of the Ψ-statistic

Type of market

Ψ = 1 Perfect competitionΨ < 1 Monopolistic competitionΨ 60 Monopoly

equilibrium (Panzar and Rosse, 1987) (Shaffer, 1982). If the firms are not in equilibrium,

adjustments in, for example, prices and quantities or entry and exit will most likely occur,

leading to effects not incorporated in the analysis and, thus, inaccurate estimates (Shaffer,

1982) (Vesala, 1995). A simple test for ensuring equilibrium is described in section 2.2.1.

2.2 Empirical model

The theoretical PR-model must be transformed into an empirical model in order to be

estimated. Following Bikker and Haaf (2002) the reduced form revenue function could be

written as a regression model as

lnR∗ = α+

m∑i=1

βi lnwi +

n∑l=1

δl ln cl (2.25)

where cl is a vector of n bank specific variables containing the variables z and t from the

revenue respective cost equations (2.1) and (2.2). This empirical version of the PR-model

can be used in estimating the elasticities of the factor prices, and therefore test whether

the firms behave as monopolists, monopolistic competitors or in accordance with perfect

competition. By taking the natural logarithm of each variable the parameter estimates can

be directly interpreted as elasticities. This imply that the Ψ-statistic is

Ψ =

m∑i=1

βi

There has been a discussion among the users of the PR-model whether the dependent

variable can (or should) be scaled, and also about including or not including a scaling

factor, such as total assets, in order to cope with heteroskedaticity (see, e.g., Vesala (1995)

and Bikker et al. (2011)). Bikker et al. argue that scaling a dependent variable by, for

example, total assets or including the scaling variable as an independent variable will yield

inaccurate estimations as the original derivations of Panzar and Rosse did not use scaling.

19

Scaling the dependent variable makes the revenue function become a price function, which

will not work in the estimations of the Ψ-statistic. (Bikker et al., 2011). In this study, the

dependent variable will not be scaled, nor will any separate scaling factor, such as total

assets, be included which is in line with the discussion of Bikker et al.

2.2.1 Test for long-run equilibrium

As was described in section 2.1.4, the sample used in estimating the Ψ-statistic needs to be

in a long-run equilibrium. A widely used method (see (Nathan and Neave, 1989), (Claessens

and Laeven, 2004) or (Gischer and Stiele, 2009)) is the one proposed by (Shaffer, 1982)

where an empirical test for equilibrium is conducted by replacing the dependent variable

with a variable representing rate of return. Shaffer writes

“If the risk level of a bank is unaffected by its input prices within the observed range of prices,

and if all banks in the sample compete in the same capital market, then equilibrium rates of return

should not be statistically correlated with input prices. If, however, the banks are in transition toward

a new equilibrium, then an increase (decrease) in factor prices would show up as a temporary decline

(increase) in the rate of return producing a negative correlation between factor prices and the rate

of return.” - (Shaffer, 1982, p. 230)

Thus, by using returns on assets (ROA) as the dependent variable, an approach adopted

by many other studies, if the ΨROA-statistic sums to zero, and a hypothesis test confirms

equality to zero, the sample is indeed in long-run equilibrium. The statistic is defined as

ΨROA =∑ ∂ROA

∂wi

wi

ROA

3 Empirical Framework

3.1 Data

The data is a strongly balanced panel data set collected from the annual reports of each

bank. The banks included in the sample are shown in appendix A. The time range is 2002 to

2010. The choice of time period is mainly due to that the Swedish Companies Registration

Office (SCRO)9 only keeps digital copies of the annual reports up to ten years, and the

reports for the year 2011 have not been published yet by the majority of banks. The data

is partly also available through Statistics Sweden (SCB), but because of the analysis of

9Bolagsverket

20

savings banks, which often tend to be small and do not report to SCB, this source does not

contain much of the data needed.10 The banks included in the data set are retail banks,

meaning that they offer regular bank services (e.g. mortgage lending and debit- and credit

cards) to the broad public. This is to make sure the market is fairly the same for all banks

in the sample and are therefore excluding niche banks.

The collected data mainly follows the international accounting standard IFRS. Nordea

and ICA Banken reports their results in euro for the whole time period respective since

2009. The yearly average exchange rate EUR/SEK for respective year is used to convert

the numbers into Swedish kronor, which is the currency used in the data set. All monetary

variables are expressed with their real values in 2012 by the consumer price index provided

by SCB.

3.1.1 Exclusion of banks

Unfortunately it is not possible to use data for all savings banks. The main reason is that

15 out of 64 savings banks are missing data due to missing records of annual reports in

the archives of the SCRO. Attempts to contact these banks and receive reports directly

from them have also been made without any success. A full list of which savings banks

not included is provided in appendix A. Although 15 savings banks are missing, it is a

fair assumption that the results of this paper will not be affected significantly and the

estimation process still be valid as there are 49 banks remaining.

In the estimation of competition within commercial banks there is also firms missing.

A list of banks is provided in appendix A. The majority of banks excluded are done so

because their main business area in Sweden are not retail banking but instead have a niche

towards, for example, investment banking or savings11.

The banks included are also acting mainly in the Swedish market, meaning that the

majority of their income originates from Swedish customers, which excludes for example

Danske Bank and DnB Nor which have their largest share of customers in Denmark and

Norway. A consequence of this is that one of the four largest banks acting at the Swedish

market, Nordea, is also excluded. The reason being that the income from the Swedish

market represents about 25% of their total income. Including Nordea could alter the

assumption of banks acting in the same market because of their large involvement in

10The same reasoning holds for other databases, such as Bankscope or OSIRIS11It is important to distinguish between savings banks (the bank type) and banks involved only or mainly

in savings business (for example Avanza Bank or Nordnet Bank)

21

other countries, and therefore also competition with other actors that the other banks in

the sample do not face. For completeness, estimations including Nordea is provided in

appendix B.3. The same reasoning could be applied on especially Swedbank and SEB due

to their activity in the Baltic countries, but also Handelsbanken and its involvement in the

British bank market. These three banks are, however, not excluded because their share of

income from the Swedish market is at least about 70% of their respective total income and

are therefore considered to compete mainly on the Swedish market. As the purpose of this

thesis mainly is to write about the competition of savings banks, the exclusion of Nordea

do not affect the savings banks result, nor the commercial bank results which is obvious

by comparing table 4 and 10.

3.2 Model

There are almost as many different variations of the Panzar-Rosse model as there are

articles. One common factor is, however, the dependent variable, corresponding to the

revenue, which most often is proxied by the total income (TI) of the bank or total interest

income (TII), both collected from the income statement in the annual reports. The reason

for using total income is that banks today have other business areas than just the ones

generating interest income, such as debit card and insurances, and that all of them should

be taken into account. A drawback of using total income is that, for example, losses in a

banks trading activity is included (as well as profits) lending to dramatically lower income

for several savings banks in 2008 and 2009, partly due to the massive drop in the Swedbank

share price. As the main business of banks is leading, using total interest income should also

make a good proxy for the revenue variable. For completeness, both dependent variables

(TI and TII) are regressed in different specifications.

The proxies for factor prices are the funding rate, cost of personnel and capital expen-

diture. These three factor price variables are widely applied when using the Panzar-Rosse

model (see, for example, Gischer and Stiele (2009) and Molyneux et al. (1996)), although

different calculation methods are used. Definitions of the variables are provided in table 3.

Funding rate is included as this is probably the single most important input factor for

the bank, being able to fund lending. The funding is made partly by deposits and also

other sources such as the central bank and a higher value implies that the bank’s cost of

borrowing are higher.

Personnel are a necessary cost for any firm, whether it works through many or few

22

branches. The bank employees could also be viewed as salesmen trying to improve the

income of the bank. The variable is scaled by the number of employees.

Other operating costs refer to all non-personnel costs a bank faces and proxy the phys-

ical cost of capital, and is scaled with total assets. This post includes, among other things,

marketing and IT expenses as well as rent.

Turning to the bank specific variables (cl in equation (2.25)), there is usually variables

included reflecting risk, funding mix, banking behavior and other control variables. In

order to measure risk, equity to total assets (EQ) is included. A higher equity ratio usually

means the bank is not taking as high risks as with a lower equity, and therefore may not

earn as much income. A higher equity, however, also implies that the bank needs not seek

as much external financing, leading to less interest costs. The sign of this coefficient is

therefore expected to be ambiguous.

Lending towards the public to total assets ratio reflects the banks portfolio composition

and business mix. A higher share of outstanding loans to the public (mainly consumers

and companies) should lead to increased interest revenues, as well as total revenues. The

sign is expected to be positive.

The number of branches operated by the bank is affecting the possibility to be close

to the customer and thereby offering local services and potential additional sales. Many

branches may, in short, lead to a closeness with the community and customers, which

could lead to a larger share of the customers in the area, and thereby also increasing

profits. Branches are, however, associated with higher costs not only for the personnel and

facilities, but also for security and handling cash. The sign of this coefficient is therefore

expected to be ambiguous.

The dependent variable used for determining whether the sample is in long-run equi-

librium is defined as the operating result divided by total assets, plus one to account for

negative operating results.

In addition, regressions will be conducted to analyze if there is any difference in com-

petitive behavior between small, medium sized and large savings banks. Findings from,

for instance, Gischer and Stiele (2009) suggest that smaller savings banks tend to behave

less competitive than larger ones. Thus, this is an interesting aspect to investigate also in

Sweden. The division between different sizes is based on the number of employees where

the 33 and 66 percentile has been used as limits for respective size. The 33 percentile

occurs at 25 employees, and the 66 percentile at 70.

The empirical models run in the regressions for bank i at time t are specified as

23

Table 3: Proxies for revenue- and cost variables

Variable Calculation

FP1 Funding rateInterest expenses

Total liabilities - (Equity + Reserves)

FP2 Personnel costPersonnel expenses

Number of employees

FP3 Other costsNon-personnel expenses

Total assets

EQ Attitude towards riskTotal equityTotal assets

CL Business mix by public loansLending towards the public

Total assets

BR Branches Number of branches

ROA Return on assets 1 +Operating result

Total assets

Specification 1:

lnTIi,t =α0,i + β1 lnFP1i,t + β2 lnFP2i,t + β3 lnFP3i,t

+ δ1 lnEQi,tδ2 lnCLi,t + δ3 lnBRi,t + εi,t(3.1)

Specification 2:

lnTIIi,t =α0,i + β1 lnFP1i,t + β2 lnFP2i,t + β3 lnFP3i,t

+ δ1 lnEQi,tδ2 lnCLi,t + δ3 lnBRi,t + εi,t(3.2)

Descriptive statistics and correlation matrices for all savings banks, commercial banks

and overall sample is provided in appendix B.1. All specifications are estimated using a

fixed effects estimator along with robust standard errors. The robust standard errors, and

the fact that the variables are scaled down and in logarithmic form, is a way of coping

with potential heteroskedasticity, which is common in panel data. Fixed effects are used

to account for bank specific characteristics that could influence the predictions, which are

not desirable. Instead the time specific effects are captured.

The fixed effects estimator needs individual bank’s error terms not to be correlated

24

with that of other banks, thus a Hausman test is conducted to every group to determines if

the fixed effects estimator is the appropriate one to use, or if the random effects estimator

should be used instead. All χ2-statistics produced from the Hausman test are significant

at 5%-level or less which confirms the use of the fixed effects estimator. In order to test

whether the obtained Ψ-statistics are statistically distinct from unity (perfect competition)

and/or zero (monopoly), Wald test’s is conducted. Thus, the hypothesis of these tests are

Ψ = 0 and Ψ = 1.

The test for long-run equilibrium is performed by regressing the model

lnROAi,t =α0,i + φ1 lnFP1i,t + φ2 lnFP2i,t + φ3 lnFP3i,t

+ δ1 lnEQi,tδ2 lnCLi,t + δ3 lnBRi,t + εi,t(3.3)

As specification 1 and 2 contain the same independent variables, only one equilibrium

specification is needed. A fixed effects estimation is done with robust standard errors also

for this model. As explained in section 2.2.1, the sum of factor price elasticities in equation

(3.3) should be zero for the models to be in long-run equilibrium, thus

ΨROA = φ1 + φ2 + φ3 = 0 (3.4)

4 Results

The estimation results from specification I and II are provided in table 4 on pages 26

and 27. Applying Wooldridge’s test for serial correlation12 in fixed effects panel data

sets no significant p-values was generated, meaning no serial correlation was found. The

correlation matrices in appendix B.1 show no sign of correlation between variables that

must be corrected for.

The long-run equilibrium test is provided in appendix B.2. All specification’s and

groups yield ΨROA estimates around zero, implying a long-run equilibrium bank sector.

By using a Wald test, the null hypothesis that ΨROA = 0 could not be rejected.

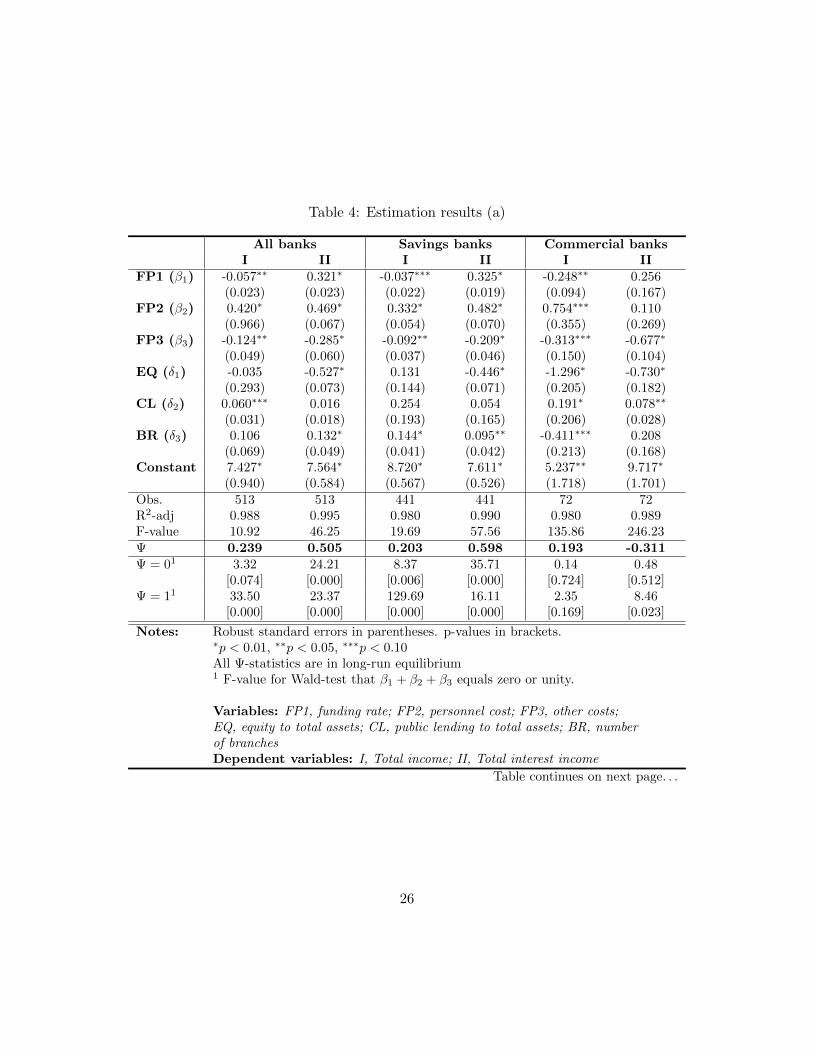

Turning to the main results from the estimations, the banks funding rate (β1) has a

significant effect in all cases, but one, and yields a slightly negative estimate using total

income as dependent variable, but positive if using total interest income. The p-values using

12see Drukker (2003)

25

Table 4: Estimation results (a)

All banks Savings banks Commercial banksI II I II I II

FP1 (β1) -0.057∗∗ 0.321∗ -0.037∗∗∗ 0.325∗ -0.248∗∗ 0.256(0.023) (0.023) (0.022) (0.019) (0.094) (0.167)

FP2 (β2) 0.420∗ 0.469∗ 0.332∗ 0.482∗ 0.754∗∗∗ 0.110(0.966) (0.067) (0.054) (0.070) (0.355) (0.269)

FP3 (β3) -0.124∗∗ -0.285∗ -0.092∗∗ -0.209∗ -0.313∗∗∗ -0.677∗

(0.049) (0.060) (0.037) (0.046) (0.150) (0.104)EQ (δ1) -0.035 -0.527∗ 0.131 -0.446∗ -1.296∗ -0.730∗

(0.293) (0.073) (0.144) (0.071) (0.205) (0.182)CL (δ2) 0.060∗∗∗ 0.016 0.254 0.054 0.191∗ 0.078∗∗

(0.031) (0.018) (0.193) (0.165) (0.206) (0.028)BR (δ3) 0.106 0.132∗ 0.144∗ 0.095∗∗ -0.411∗∗∗ 0.208

(0.069) (0.049) (0.041) (0.042) (0.213) (0.168)Constant 7.427∗ 7.564∗ 8.720∗ 7.611∗ 5.237∗∗ 9.717∗

(0.940) (0.584) (0.567) (0.526) (1.718) (1.701)Obs. 513 513 441 441 72 72R2-adj 0.988 0.995 0.980 0.990 0.980 0.989F-value 10.92 46.25 19.69 57.56 135.86 246.23Ψ 0.239 0.505 0.203 0.598 0.193 -0.311Ψ = 01 3.32 24.21 8.37 35.71 0.14 0.48

[0.074] [0.000] [0.006] [0.000] [0.724] [0.512]Ψ = 11 33.50 23.37 129.69 16.11 2.35 8.46

[0.000] [0.000] [0.000] [0.000] [0.169] [0.023]

Notes: Robust standard errors in parentheses. p-values in brackets.∗p < 0.01, ∗∗p < 0.05, ∗∗∗p < 0.10All Ψ-statistics are in long-run equilibrium1 F-value for Wald-test that β1 + β2 + β3 equals zero or unity.

Variables: FP1, funding rate; FP2, personnel cost; FP3, other costs;EQ, equity to total assets; CL, public lending to total assets; BR, numberof branchesDependent variables: I, Total income; II, Total interest income

Table continues on next page. . .

26

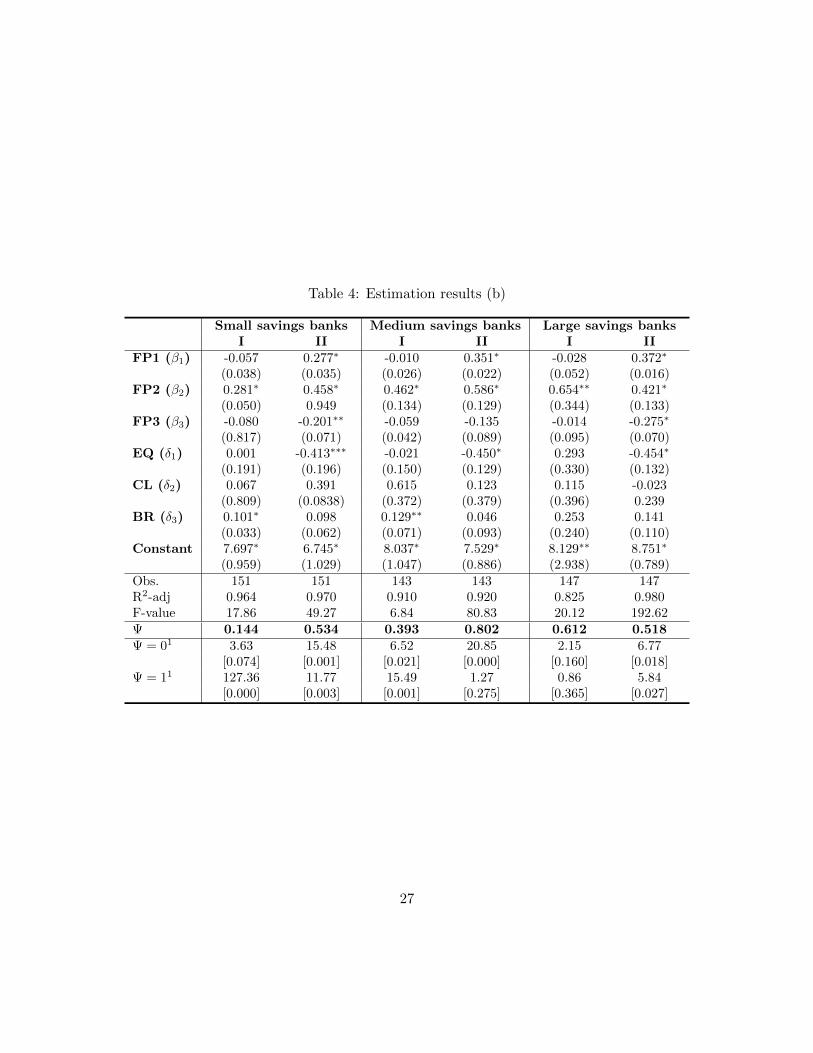

Table 4: Estimation results (b)

Small savings banks Medium savings banks Large savings banksI II I II I II

FP1 (β1) -0.057 0.277∗ -0.010 0.351∗ -0.028 0.372∗

(0.038) (0.035) (0.026) (0.022) (0.052) (0.016)FP2 (β2) 0.281∗ 0.458∗ 0.462∗ 0.586∗ 0.654∗∗ 0.421∗

(0.050) 0.949 (0.134) (0.129) (0.344) (0.133)FP3 (β3) -0.080 -0.201∗∗ -0.059 -0.135 -0.014 -0.275∗

(0.817) (0.071) (0.042) (0.089) (0.095) (0.070)EQ (δ1) 0.001 -0.413∗∗∗ -0.021 -0.450∗ 0.293 -0.454∗

(0.191) (0.196) (0.150) (0.129) (0.330) (0.132)CL (δ2) 0.067 0.391 0.615 0.123 0.115 -0.023

(0.809) (0.0838) (0.372) (0.379) (0.396) 0.239BR (δ3) 0.101∗ 0.098 0.129∗∗ 0.046 0.253 0.141

(0.033) (0.062) (0.071) (0.093) (0.240) (0.110)Constant 7.697∗ 6.745∗ 8.037∗ 7.529∗ 8.129∗∗ 8.751∗

(0.959) (1.029) (1.047) (0.886) (2.938) (0.789)Obs. 151 151 143 143 147 147R2-adj 0.964 0.970 0.910 0.920 0.825 0.980F-value 17.86 49.27 6.84 80.83 20.12 192.62Ψ 0.144 0.534 0.393 0.802 0.612 0.518Ψ = 01 3.63 15.48 6.52 20.85 2.15 6.77

[0.074] [0.001] [0.021] [0.000] [0.160] [0.018]Ψ = 11 127.36 11.77 15.49 1.27 0.86 5.84

[0.000] [0.003] [0.001] [0.275] [0.365] [0.027]

27

total income are above the 10%-level for all regressions run on different sizes. Increasing

the funding of the bank yields higher interest income, but lower total income.

The personnel costs (β2) have a positive effect in both specifications which is significant

mostly at the 1%-level. The personnel as factor price has a positive impact on the sales

of the bank, not only in yielding good interest income but also when it comes to other

business areas, proxied by the total income variable. This variable has the greatest impact

on Ψ and could therefore be regarded as the most important feature of the bank.

The estimated effects of other costs (β3) imply that increasing this post will yield lower

total- and interest income. Being significant mostly at the aggregated regressions (e.g.

including all banks of each type) it implies that increasing costs referring to, for example,

rents or marketing would decrease income.

Turning to the coefficients not associated with the Ψ-statistic there is fairly poor sig-

nificance for each of them depending on specification and group analyzed. The coefficient

taking risk into account (δ1) is in most cases negative or just slightly positive, while the

opposite is true for δ2. For to branches (δ3), an increased number of branches seems to

favor income of the bank as the coefficient is positive for all specifications and groups.

The estimated effects of factor price elasticities give Ψ-statistics that mostly are con-

sistent with monopolistic competition. The one exception is for commercial banks where

using total interest income as dependent variable yields a negative Ψ. Applying Wald test’s

on each statistic, in order to determine if the statistics are different from zero and/or unity,

confirms the conclusion of monopolistic competition for all banks, all savings banks and

small savings banks. This is also true using specification I for medium- and specification

II for large savings banks. Applying the Wald test on specification I for large savings

banks and commercial banks, neither hypothesis of Ψ = 0 or Ψ = 1 can be rejected im-

plying that the structure can not be statistically confirmed by the Ψ-statistic. Looking at

medium savings bank, the hypothesis of perfect competition can not be rejected. Turning

to specification II for commercial banks the unity Wald test can be rejected, but not the

monopoly hypothesis, which is consistent with the negative value of Ψ. Thus, commercial

banks could, using interest income as dependent variable, be characterized by monopoly

behavior.

In appendix B.3 estimates including the commercial bank Nordea is made. The results

show that the estimates of the Ψ-statistics does not differ very much from the ones obtained

by excluding the bank. The sign of the parameter estimates do not differ much (with

exception of the one corresponding to the BR variable, which changes sign), nor does the

28

level of significance for each coefficient.

One explanation of the low significance levels when estimating the model based on

data for the commercial banks, and savings banks of different sizes, are the small number

of observations. In the case of commercial banks a relaxation of the restriction only to

include retail banks could be made, which would increase the number of participating

banks a bit.

5 Conclusion

The purpose of this paper is to study the Swedish savings banks sector and determine if it

is characterized by perfect competition. Earlier studies suggest that the Swedish banking

sector as a whole is acting in a monopolistic competitive manner, and that this also holds

for the savings banks specifically. The analysis is made with the Panzar-Rosse model, which

has been widely applied amongst the academic literature when analyzing bank competition.

The panel data set, obtained from the annual reports of each bank, contains 49 savings

banks and 8 commercial banks. The time period stretches from year 2002 to 2010. Using

a fixed effects model with robust standard errors the estimation results, provided in table

4, are obtained. The dependent variables used are total income of the bank, and total

interest income.

The conclusion is that the Swedish savings banks acts in a monopolistic competitive

manner. The same result holds for the whole Swedish banking sector, whilst the commercial

banks appear to act as monopolists. Thus, there is no evidence of a perfectly competitive

behavior in the Swedish banking sector. The exception is medium sized savings banks

where the hypothesis of perfect competition cannot be rejected. The same is true for large

savings banks where neither this hypothesis, nor the one of monopoly, can be rejected. It

also appears as the savings banks are acting more competitive than the commercial banks.

Despite these results, the estimates for savings banks of different sizes should be inter-

preted carefully as few of the coefficients are statistically significant, and the sample sizes

are fairly small. The sample size argument is also applicable on the commercial banks,

but with the assumptions made to only include retail banks there is no more banks to

include. The over all test and test for all savings banks are, however, most often significant

at 10%-level, probably because they contain a larger sample. Relaxing the assumption of

retail banks will allow more banks to be analyzed, but also raise questions if the banks

are acting in the same market. Although Sweden has a large banking sector, four major

29

players hold the majority of the assets, all of which are commercial banks. This might

justify the low Ψ-statistic estimated for these banks. An interesting aspect of this would

be to analyze the four major banks specifically, as one might suspect that the monopolic

behavior can be tracked to them alone.

The findings of monopolistic competition in the whole banking sector are much in

line with previous studies performed on the Swedish banking sector. See, for example,

Bikker and Groeneveld (2000), Bikker and Haaf (2002) and Carbo et al. (2009) which all

find this with the Panzar-Rosse model, or Sjoberg (2007) who concludes that the local

banking market is not characterized by perfect competition. A comparison of the results

for savings banks with previous studies is not possible to do for the Swedish market as

the Panzar-Rosse model has not yet been applied on the Swedish savings banks sector

by other studies. However, studies performed in the German market are also concluding

monopolistic competition in the savings banks sector (see Gischer and Stiele (2009) and

Hempell (2002)). Hempell (2002) found that the savings banks are less competitive than

commercial banks, which is not the finding in this paper. Also, Gischer and Stiele (2009)

find that the Ψ-statistic is larger for larger savings banks when using total interest income

as dependent variable, which is not entirely the findings in this paper.

Year-to-year estimates for the Ψ-statistics would have been interesting in order to see

the development in competition for every year in the Swedish banking sector. Unfortunately

the number of observations corresponding to each year makes it hard to obtain significant

parameter estimates and valid models for these regressions, especially for the commercial

banks but also for the savings banks. At the same time it is hard to obtain data for more

banks, as the Swedish bank market is relatively small why another approach than the

Panzar-Rosse, or a restated econometric model, might be appropriate.

To summarize, the Swedish savings banks appear to act as monopolistic competitors to

one another, which means they exhibit some market power. They should also, according to

the theory of monopolistic competition, have heterogenous products, which seems plausible

as all banks offer similar products (e.g. loans, cards etc.), but differ in specifics such as

prices, contents or terms. Monopolistic competition also implies that customers are not as

sensitive to price changes as under a competitive market, which leads to higher prices. This,

and the potential monopoly situation among commercial banks, could set a foundation to

analyze the banks mortgage rates, and analyze if the market power exhibited by banks is

exploited to set too high rates. The local presence of savings banks might protect them

to some extent from the four large commercial banks that dominates the banking market

30

because of the possibly quite small local market. The large dependence on Internet and

phone banking does, however, allow commercial banks to act on markets that may not be

profitable to establish branches on. The market of local savings banks may extend for the

same reason, as their customers are not as dependent on single branches as before. Further

studies within the field of savings banks should try to determine if this effect exists, and

what implications it has on market structure. In the commercial bank sector, a further

investigation of potential monopoly power exhibited by the four major banks should be

studied.

31

References

Bikker, J. A. and J. M. Groeneveld (2000). Competition and concentration in the EUbanking industry. Kredit und Kapital 33 (1), 62.

Bikker, J. A. and K. Haaf (2002). Competition, concentration and their relationship:An empirical analysis of the banking industry. Journal of Banking & Finance 26 (11),2191–2214.

Bikker, J. A., S. Shaffer, and L. Spierdijk (2011). Assessing competition with the Panzar-Rosse model: The role of scale, costs, and equilibrium. Review of Economics and Statis-tics Accepted for publication.

Bresnahan, T. F. (1982). The oligopoly solution concept is identified. Economics Let-ters 10 (12), 87–92.

Carbo, S., D. Humphrey, J. Maudos, and P. Molyneux (2009). Cross-country comparisonsof competition and pricing power in european banking. Journal of International Moneyand Finance 28 (1), 115–134.

Cetorelli, N. and M. Gambera (2001). Banking market structure, financial dependenceand growth: International evidence from industry data. The Journal of Finance 56 (2),617–648.

Chamberlin, E. (1962). The theory of monopolistic competition: a re-orientation of thetheory of value. Harvard University Press.

Claessens, S. and L. Laeven (2004). What drives bank competition? some internationalevidence. Journal of Money, Credit and Banking 36 (3), 563–583.

Drukker, D. M. (2003). Testing for serial correlation in linear panel-data models. StataJournal 3 (2), 168–177.

Gischer, H. and M. Stiele (2009). Competition tests with a NonStructural model: the Pan-zarRosse method applied to germany’s savings banks. German Economic Review 10 (1),50–70.

Hempell, H. S. (2002). Testing for competition among german banks. Deutsche Bundes-bank .

Korberg, I. (2007). Bank sedan 1820: sparbankernas och Swedbanks historia. Spar-banksakademin.

Lau, L. J. (1982). On identifying the degree of competitiveness from industry price andoutput data. Economics Letters 10 (12), 93–99.

32

Molyneux, P., J. Thornton, and D. Michael Llyod-Williams (1996). Competition andmarket contestability in japanese commercial banking. Journal of Economics and Busi-ness 48 (1), 33–45.

Nathan, A. and E. H. Neave (1989). Competition and contestability in canada’s financialsystem: Empirical results. The Canadian Journal of Economics / Revue canadienned’Economique 22 (3), 576–594.

Nordic competition authorities (2006). Competition in nordic retail banking. Technicalreport.

Panzar, J. C. and J. N. Rosse (1977). Chamberlin versus robinson: An empirical test formonopoly rents. Bell Laboratories Economic Discussion Paper (92).

Panzar, J. C. and J. N. Rosse (1987). Testing for ”Monopoly” equilibrium. The Journalof Industrial Economics 35 (4), 443–456.

Schaeck, K., M. Cihak, and S. Wolfe (2009). Are competitive banking systems more stable?Journal of Money, Credit and Banking 41 (4), 711–734.

Shaffer, S. (1982). A non-structural test for competition in financial markets. Chicago, pp.225–243. Proceedings on the 14th Conference on Bank Structure & Competition;FederalReserve Bank of Chicago.

Shaffer, S. (1983). Non-structural measures of competition: Toward a synthesis of alterna-tives. Economics Letters 12 (34), 349–353.

Sjoberg, P. (2007). Essays on Performance and Growth in Swedish Banking. Ph. D. thesis,University of Gothenburg.

Swedish Bankers Association (2011). Bank- and finance statistics 2010. Technical report,Swedish Bankers Association.

van Leuvensteijn, M., J. A. Bikker, A. A. van Rixtel, and C. K. Sørensen (2010). Anew approach to measuring competition in the loan markets of the euro area. AppliedEconomics 43 (23), 3155–3167.

van Leuvensteijn, M., C. K. Sørensen, J. A. Bikker, and A. A. van Rixtel (2011). Im-pact of bank competition on the interest rate pass-through in the euro area. AppliedEconomics 45 (11), 1359–1380.

Vesala, J. (1995). Testing for Competition in Banking: Behavioral Evidence from Finland.Number 1 in Bank of Finland studies. Helsinki: Suomen pankki.

33

A List of banks

Table 5: Savings banks

Attmars Sparbank* Orusts Sparbank Sparbanken Oresund (C)Bergslagens Sparbank (C) Roslagens Sparbank Swedbank Sjuharad (C)Bjursas Sparbank Sala Sparbank Sodra Dalarnas Sparbank*Dalslands Sparbank Sparbanken i Karlshamn Sodra Hestra SparbankEkeby Sparbank* Sidensjo Sparbank Solvesborg-Mjallby SparbankFalkenbergs Sparbank Skurups Sparbank Sormlands SparbankFrenninge Sparbank* Snapphanebygdens Sparbank Tidaholms SparbankFryksdalens Sparbank Sparbanken 1826 Tjustbygdens Sparbank (C)Fars & Frosta Sparbank (C) Sparbanken Alingsas (C) Tjorns SparbankHalsinglands Sparbank Sparbanken Boken Ulricehamns SparbankHaradssparbanken Monsteras Sparbanken Eken* (C) Vadstena Sparbank*Hogsby Sparbank Sparbanken Gotland Valdemarsviks SparbankIvetofta Sparbank i Bromolla* Sparbanken Goinge* Varbergs Sparbank (C)Kinda-Ydre Sparbank Sparbanken i Enkoping* (C) Vimmerby Sparbank (C)Laholms Sparbank* Sparbanken Lidkoping (C) Virserums SparbankLekebergs Sparbank Sparbanken Nord Westra Wermlands SparbankLeksands Sparbank Sparbanken Rekarne (C) Alems Sparbank*Lonneberga-Tuna-Vena Sparbank* Sparbanken Skaraborg (C) Ase och Viste harads SparbankMarkaryds Sparbank Sparbanken Syd Atvidabergs Sparbank

Mjobacks Sparbank** Sparbanken Tanum Olands Bank (C)Norrbarke Sparbank* Sparbanken Tranemo*Nars Sparbank Sparbanken Vastra Malardalen∗ Data not available (14 banks) Total: 64 banks (49 used in analysis)∗∗ Chose not to participate (1 bank) (C)=Commercial savings bank

Table 6: Commercial banks

Handelsbanken SBABICA Banken SEBIKANO Bank SkandiabankenLansforsakringar Bank SwedbankNordea∗13

∗ Excluded (1 bank) Total: 9 banks

13For an explanation why Nordea is excluded, see section 3.1.1 on page 21

34

B Econometric appendix

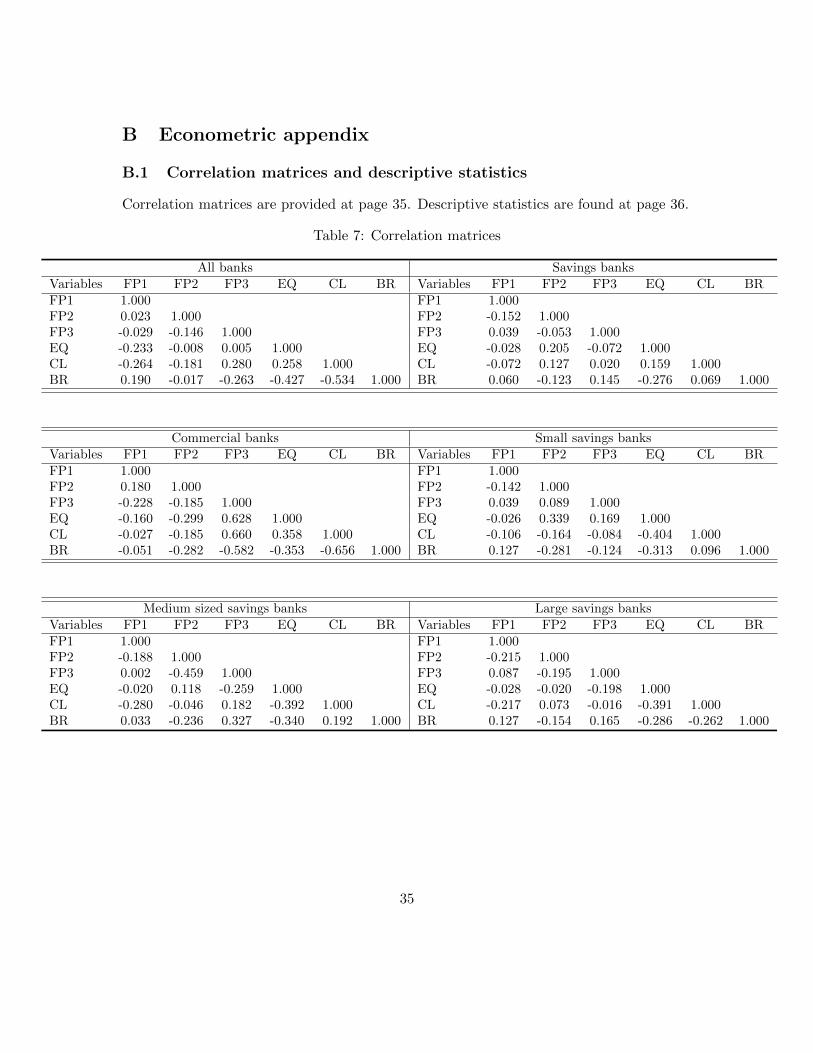

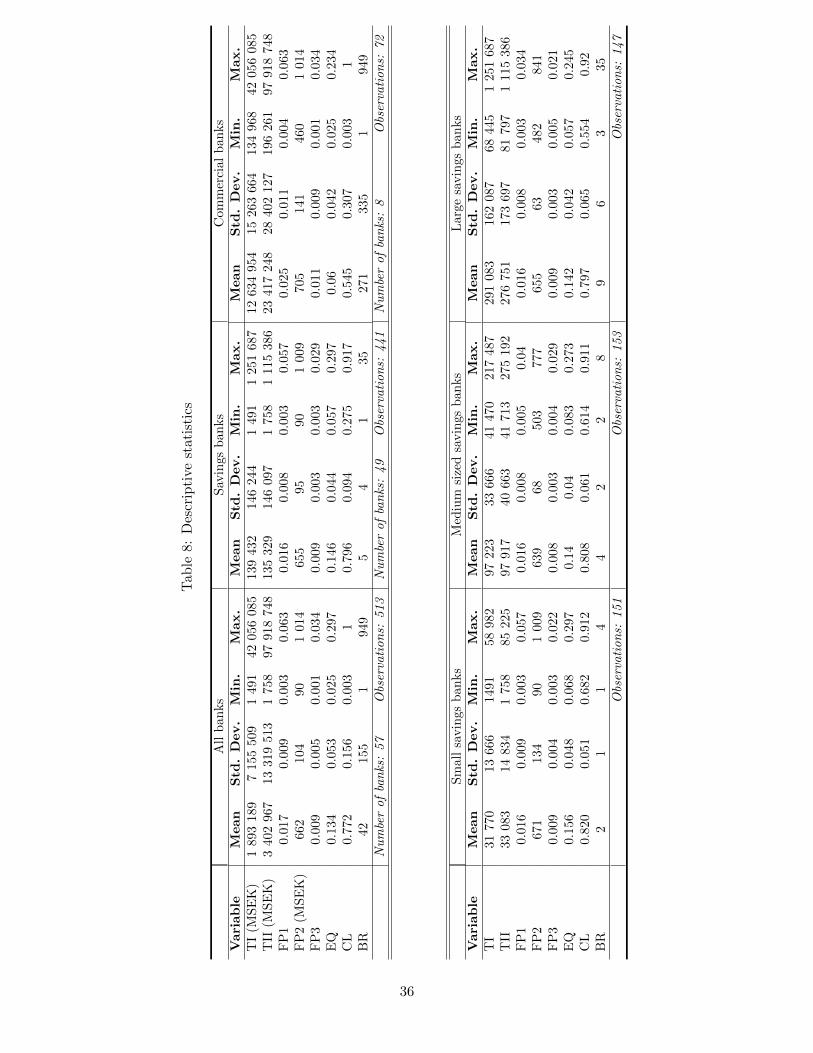

B.1 Correlation matrices and descriptive statistics

Correlation matrices are provided at page 35. Descriptive statistics are found at page 36.

Table 7: Correlation matrices

All banks Savings banksVariables FP1 FP2 FP3 EQ CL BR Variables FP1 FP2 FP3 EQ CL BRFP1 1.000 FP1 1.000FP2 0.023 1.000 FP2 -0.152 1.000FP3 -0.029 -0.146 1.000 FP3 0.039 -0.053 1.000EQ -0.233 -0.008 0.005 1.000 EQ -0.028 0.205 -0.072 1.000CL -0.264 -0.181 0.280 0.258 1.000 CL -0.072 0.127 0.020 0.159 1.000BR 0.190 -0.017 -0.263 -0.427 -0.534 1.000 BR 0.060 -0.123 0.145 -0.276 0.069 1.000

Commercial banks Small savings banksVariables FP1 FP2 FP3 EQ CL BR Variables FP1 FP2 FP3 EQ CL BRFP1 1.000 FP1 1.000FP2 0.180 1.000 FP2 -0.142 1.000FP3 -0.228 -0.185 1.000 FP3 0.039 0.089 1.000EQ -0.160 -0.299 0.628 1.000 EQ -0.026 0.339 0.169 1.000CL -0.027 -0.185 0.660 0.358 1.000 CL -0.106 -0.164 -0.084 -0.404 1.000BR -0.051 -0.282 -0.582 -0.353 -0.656 1.000 BR 0.127 -0.281 -0.124 -0.313 0.096 1.000

Medium sized savings banks Large savings banksVariables FP1 FP2 FP3 EQ CL BR Variables FP1 FP2 FP3 EQ CL BRFP1 1.000 FP1 1.000FP2 -0.188 1.000 FP2 -0.215 1.000FP3 0.002 -0.459 1.000 FP3 0.087 -0.195 1.000EQ -0.020 0.118 -0.259 1.000 EQ -0.028 -0.020 -0.198 1.000CL -0.280 -0.046 0.182 -0.392 1.000 CL -0.217 0.073 -0.016 -0.391 1.000BR 0.033 -0.236 0.327 -0.340 0.192 1.000 BR 0.127 -0.154 0.165 -0.286 -0.262 1.000

35

Tab

le8:

Des

crip

tive

stat

isti

cs

All

ban

ks

Sav

ings

ban

ks

Com

mer

cial

ban

ks

Vari

ab

leM

ean

Std

.D

ev.

Min

.M

ax.

Mean

Std

.D

ev.

Min

.M

ax.

Mean

Std

.D

ev.

Min

.M

ax.

TI

(MS

EK

)1

893

189

715

550

91

491

4205

608

5139

432

146

244

1491

125

1687

12

634

954

15

263

664

134

968

42

056

085

TII

(MS

EK

)3

402

967

1331

951

31

758

9791

874

8135

329

146

097

1758

111

5386

23

417

248

28

402

127

196

261

97

918

748

FP

10.

017

0.00

90.

003

0.06

30.0

16

0.0

08

0.0

03

0.057

0.0

25

0.0

11

0.0

04

0.0

63

FP

2(M

SE

K)

662

104

901

014

655

95

90

1009

705

141

460

1014

FP

30.

009

0.00

50.

001

0.03

40.0

09

0.0

03

0.0

03

0.029

0.0

11

0.0

09

0.0

01

0.0

34

EQ

0.13

40.

053

0.02

50.

297

0.1

46

0.0

44

0.0

57

0.297

0.0

60.0

42

0.0

25

0.2

34

CL

0.77

20.

156

0.00

31

0.7

96

0.0

94

0.2

75

0.917

0.5

45

0.3

07

0.0

03

1B

R42

155

194

95

41

35

271

335

1949

Nu

mbe

rof

ban

ks:

57

Obs

erva

tion

s:513

Nu

mbe

rof

ban

ks:

49

Obs

erva

tion

s:441

Nu

mbe

rof

ban

ks:

8O

bser

vati

on

s:72

Sm

all

savin

gsb

anks

Med

ium

size

dsa

vin

gs

ban

ks

Larg

esa

vin

gs

ban

ks

Vari

ab

leM

ean

Std

.D

ev.

Min

.M

ax.

Mean

Std

.D

ev.

Min

.M

ax.

Mean

Std

.D

ev.

Min

.M

ax.

TI

3177

013

666

1491

5898

297

223

33

666

41

470

217

487

291

083

162

087

68

445

1251

687

TII

3308

314

834

175

885

225

97

917

40

663

41

713

275

192

276

751

173

697

81

797

1115

386

FP

10.

016

0.00

90.

003

0.05

70.0

16

0.0

08

0.0

05

0.0

40.0

16

0.0

08

0.0

03

0.0

34

FP

267

113

490

100

9639

68

503

777

655

63

482

841

FP

30.

009

0.00

40.

003

0.02

20.0

08

0.0

03

0.0

04

0.029

0.0

09

0.0

03

0.0

05

0.0

21

EQ

0.15

60.

048

0.06

80.

297

0.1

40.0

40.0

83

0.2

73

0.1

42

0.0

42

0.0

57

0.2

45

CL

0.82

00.

051

0.68

20.

912

0.8

08

0.0

61

0.6

14

0.911

0.7

97

0.0

65

0.5

54

0.9

2B

R2

11

44

22

89

63

35

Obs

erva

tion

s:151

Obs

erva

tion

s:153

Obs

erva

tion

s:147

36

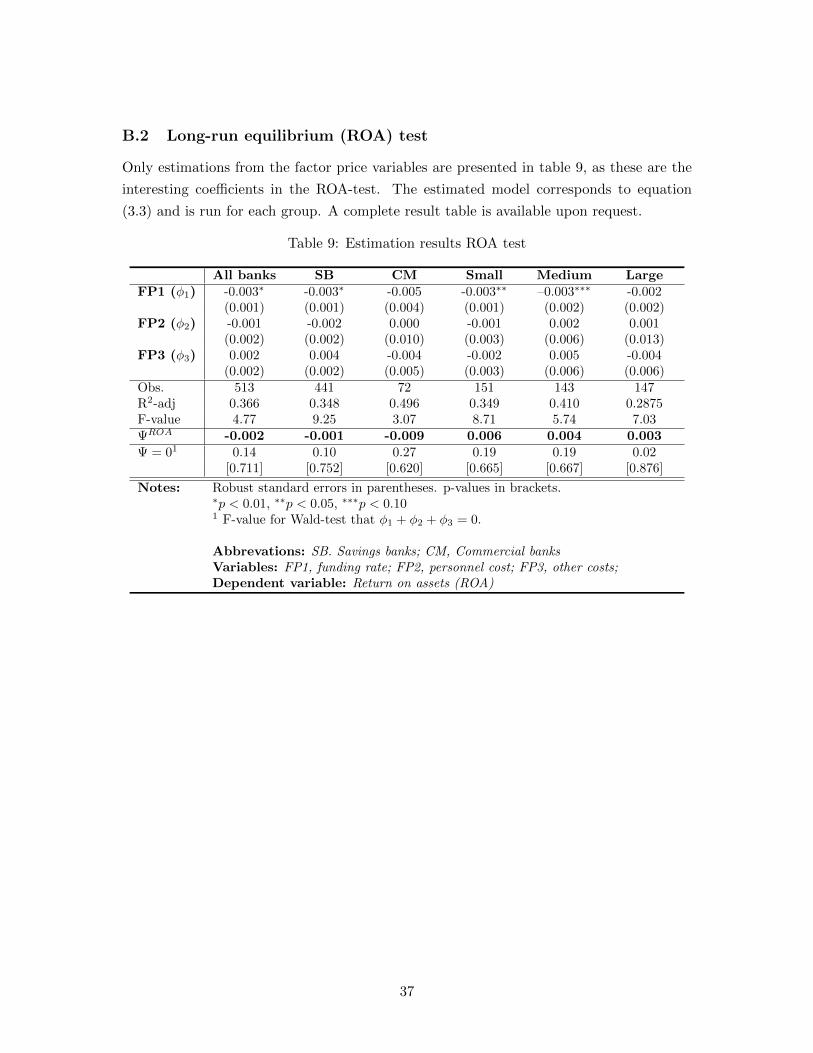

B.2 Long-run equilibrium (ROA) test

Only estimations from the factor price variables are presented in table 9, as these are the

interesting coefficients in the ROA-test. The estimated model corresponds to equation

(3.3) and is run for each group. A complete result table is available upon request.

Table 9: Estimation results ROA test

All banks SB CM Small Medium LargeFP1 (φ1) -0.003∗ -0.003∗ -0.005 -0.003∗∗ –0.003∗∗∗ -0.002

(0.001) (0.001) (0.004) (0.001) (0.002) (0.002)FP2 (φ2) -0.001 -0.002 0.000 -0.001 0.002 0.001

(0.002) (0.002) (0.010) (0.003) (0.006) (0.013)FP3 (φ3) 0.002 0.004 -0.004 -0.002 0.005 -0.004

(0.002) (0.002) (0.005) (0.003) (0.006) (0.006)Obs. 513 441 72 151 143 147R2-adj 0.366 0.348 0.496 0.349 0.410 0.2875F-value 4.77 9.25 3.07 8.71 5.74 7.03ΨROA -0.002 -0.001 -0.009 0.006 0.004 0.003Ψ = 01 0.14 0.10 0.27 0.19 0.19 0.02

[0.711] [0.752] [0.620] [0.665] [0.667] [0.876]

Notes: Robust standard errors in parentheses. p-values in brackets.∗p < 0.01, ∗∗p < 0.05, ∗∗∗p < 0.101 F-value for Wald-test that φ1 + φ2 + φ3 = 0.

Abbrevations: SB. Savings banks; CM, Commercial banksVariables: FP1, funding rate; FP2, personnel cost; FP3, other costs;Dependent variable: Return on assets (ROA)

37

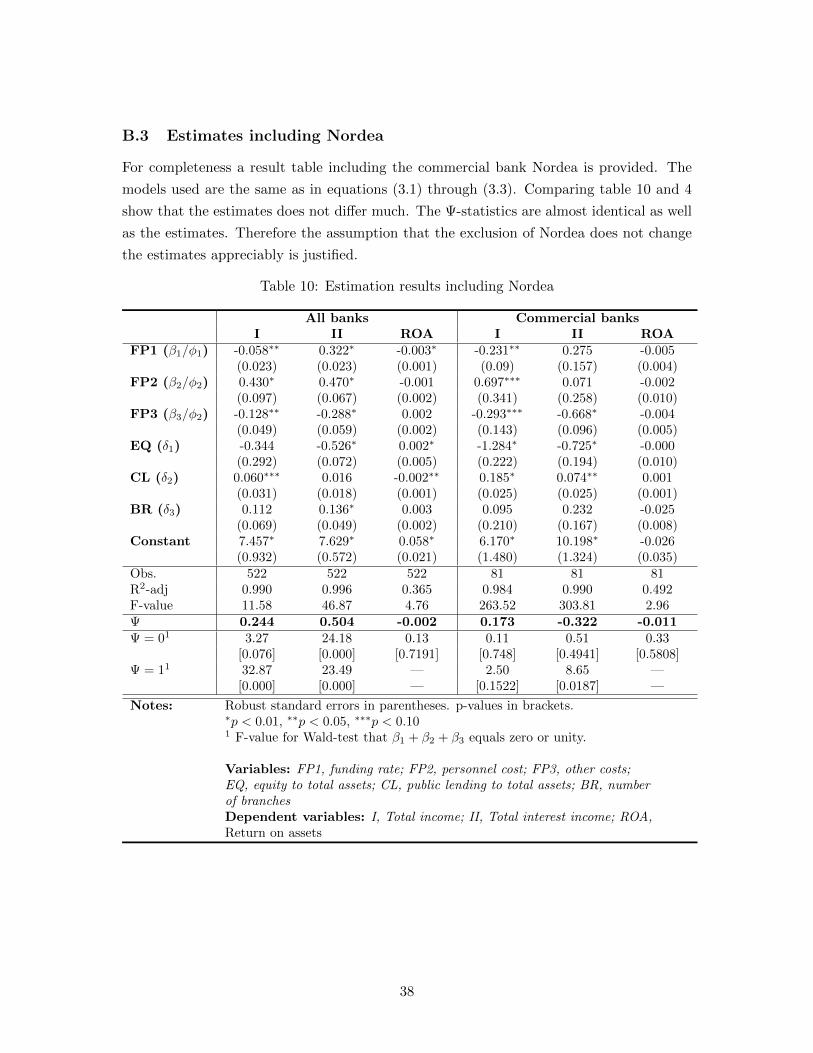

B.3 Estimates including Nordea

For completeness a result table including the commercial bank Nordea is provided. The

models used are the same as in equations (3.1) through (3.3). Comparing table 10 and 4

show that the estimates does not differ much. The Ψ-statistics are almost identical as well

as the estimates. Therefore the assumption that the exclusion of Nordea does not change

the estimates appreciably is justified.

Table 10: Estimation results including Nordea

All banks Commercial banksI II ROA I II ROA

FP1 (β1/φ1) -0.058∗∗ 0.322∗ -0.003∗ -0.231∗∗ 0.275 -0.005(0.023) (0.023) (0.001) (0.09) (0.157) (0.004)

FP2 (β2/φ2) 0.430∗ 0.470∗ -0.001 0.697∗∗∗ 0.071 -0.002(0.097) (0.067) (0.002) (0.341) (0.258) (0.010)

FP3 (β3/φ2) -0.128∗∗ -0.288∗ 0.002 -0.293∗∗∗ -0.668∗ -0.004(0.049) (0.059) (0.002) (0.143) (0.096) (0.005)

EQ (δ1) -0.344 -0.526∗ 0.002∗ -1.284∗ -0.725∗ -0.000(0.292) (0.072) (0.005) (0.222) (0.194) (0.010)

CL (δ2) 0.060∗∗∗ 0.016 -0.002∗∗ 0.185∗ 0.074∗∗ 0.001(0.031) (0.018) (0.001) (0.025) (0.025) (0.001)

BR (δ3) 0.112 0.136∗ 0.003 0.095 0.232 -0.025(0.069) (0.049) (0.002) (0.210) (0.167) (0.008)

Constant 7.457∗ 7.629∗ 0.058∗ 6.170∗ 10.198∗ -0.026(0.932) (0.572) (0.021) (1.480) (1.324) (0.035)