Embed Size (px)

Citation preview

SCANIA 1999ANNUAL REPORT

In 1897 came the first Swedish-made automobile with a com-bustion engine.

In 1909, only five trucks weremade. Of these, the one shownabove is the oldest preserved Scania truck.

During the 1920s, Scania-Vabis began making buses. In 1923, it produced 20.

In 1925, an entirely newtruck chassis and a newtype of engine with an integral gearbox were introduced.

In the 1930s, the “BulldogBus” arrived. Developed froma Leyland Tiger design, it waspath-breaking owing to itssimple design and efficientuse of space and weight.

In 1949, Scania took a significant stepforward by unveiling its new 40- and60-series trucks, featuring a direct-injection diesel engine that con-sumed 20–25 percent less fuel. Itwas soon called the 400,000 km engine, a tribute to its great durability.

In 1958, Scania began building the 75 series, its most long-lived model series.The model remained in production until1980, when Scania introduced morecomfortable, stronger, heavier truckswith largely the same appearance.

Scania through the decadesScania was founded in 1891. Since then, the companyhas manufactured and delivered nearly one milliontrucks, buses and bus chassis.

Scania is one of the world’s leading manufacturersof heavy trucks and buses as well as industrial and marine engines. With 25,800 employees and produc-tion units in Europe and Latin America, Scania is oneof the most profitable manufacturers in its industry.During 1999, sales reached SEK 47.1 billion. Incomeafter financial items was SEK 4.5 billion. Scania prod-ucts are sold in some 100 markets and about 95 per-cent of Scania vehicles are sold outside Sweden.

In 1945, at the end of the war, a“unitary” bus range was ready for production.The various busmodels, built according to thesame principles, were suitable forcity, intercity and tourist coachservice.

During the 1980s, the 2- and 3-seriesemerged, a range of models based onthe modular philosophy that Scania hadworked with for years.The 3-series wasnamed Truck of the Year in 1989.

During the 1990s, Scania expanded innew markets for trucks and buses incentral and eastern Europe.

City bus in Gdansk, Poland. Up to 85 percent of the components in a bus chassis are common with a truck chassis in the 4-series.

Tourist coach in South Korea.

Scania industrial and marine engines operate under tough conditions in generators and boatsworldwide.

Scania’s prototype of a concept vehicle for the 2010sshows the potential for reducing heavy truck trafficby boosting per-vehicle capacity by 50 percent com-pared to today’s trucks.

In the autumn of 1995, Scania unveiled the 4-series,which was very well received in the market.The 4-series was named Truck of the Year in 1996.The 4-series, which was the result of the most extensive development effort in Scania’s history,offers very high adaptability to customer needs.Among other things, it has greatly improved Scania’s competitiveness in the construction truck segment.

2

CONTENTS

Important events in 1999 and 2000 2

Highlights 3

Statement of the President and CEO 4

Statement of the Chairman 6

Scania share data 8

Mission and strategy 10

Scania’s identity and behaviour 11

Scania during the 1990s 14

Review of operations 16

Vehicles 16

Service-related products 28

Customer financing 30

Our employees 32

Scania and the environment 34

Financial review 38

Consolidated income statement 42

Consolidated balance sheet 43

Consolidated statement of cash flows 44

Parent Company financial statements 45

Accounting principles 46

Notes to the consolidated financial statements 48

Financial information in accordance with U.S. GAAP 56

Proposed distribution of earnings 57

Auditors’ report 58

Value-added 59

Quarterly data, financial ratios, definitions 60

Multi-year statistical review 62

Board of Directors 64

Group Management 66

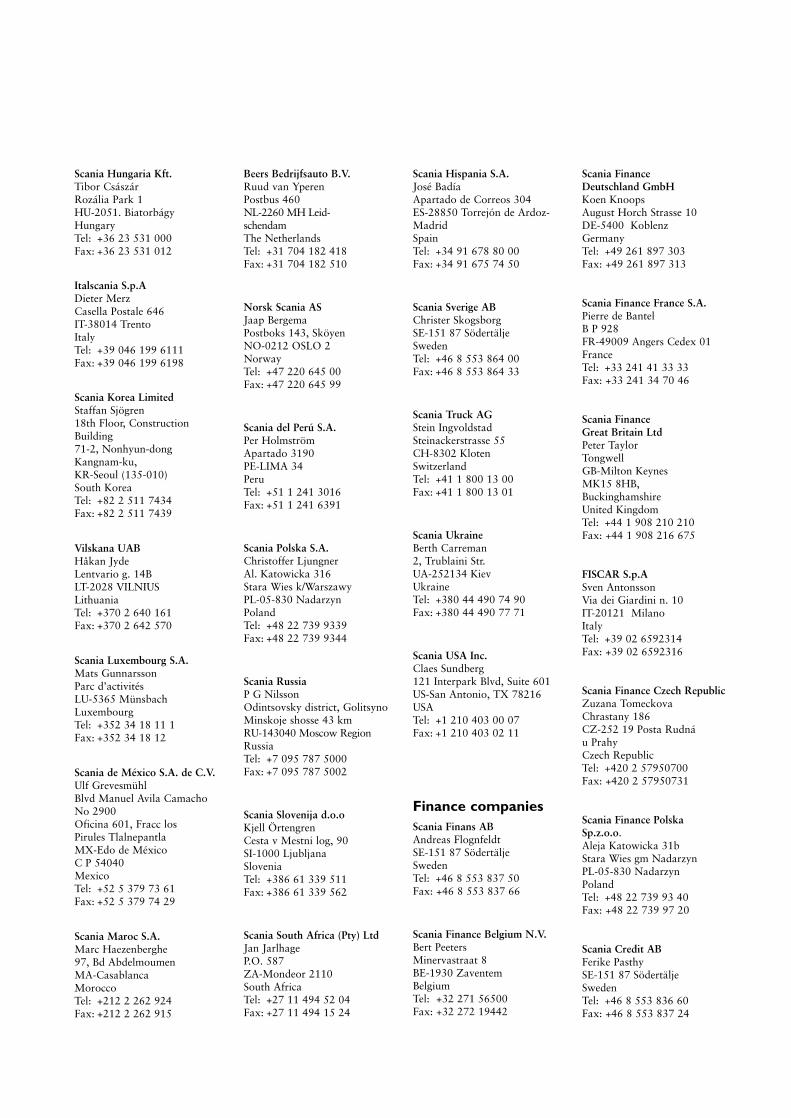

Addresses 68

The Report of the Directors encompasses pages 2–57.

Swedish corporate identity number:Scania AB (publ)556184-8564

IMPORTANT EVENTS1999January: • Scania and American engine manufacturer Cummins started

a jointly owned company to produce advanced fuel injectionsystems.

• Distribution of trucks in the South Korean market resumed, viathe newly established wholly-owned subsidiary Scania Korea Ltd.

• Scania acquired its truck distributor in the Italian market, Ital-scandia Autocarri S.p.A.

• Volvo announced it had bought shares equivalent to 13.5 percentof the voting power and 12.9 percent of share capital in Scania.

March: • A new cutting-edge vehicle electronics company, Scania Info-

tronics AB, was established in partnership with the researchcompany Mecel AB.

April: • All Scania facilities in Sweden received ISO 14001 environ-

mental management accreditation.• Volvo gradually enlarged its shareholding in Scania. By the

end of April, it held 21.5 percent of the votes and 20.3 percentof the capital.

July:

• Scania acquired its distributor in the Norwegian market, NorskScania AS.

• Scania decided to invest in a new finishing paintshop and cabassembly facility in Oskarshamn, Sweden.

August: • Volvo signed an agreement with Investor to acquire all of In-

vestor’s shares in Scania. At the same time, Volvo announced apublic offer for the other Scania shares outstanding.

September: • Scania’s new concept truck for the 2010s was unveiled at a

road safety seminar in Brussels.

October: • Scania acquired the remaining 50 percent of its Finnish distrib-

utor, Oy Scan-Auto Ab.• Scania’s frame component production unit in Luleå, Sweden

was reorganised into an autonomous limited company, Ferru-form AB.

November: • Mecel and Scania Infotronics unveiled the first WAP browser

for a truck environment.

• Scania signed an agreement to sell 340 intercity buses to SouthAfrica.

2000March: • The European Commission decided not to approve Volvo’s

proposed acquisition of Scania. Volvo withdrew its offer toScania’s shareholders.

• Investor announces an agreement with Volkswagen AG on thesale of 34.0 percent of voting rights and 18.7 percent of capitalin Scania.

3

HIGHLIGHTS

0

10,000

20,000

30,000

40,000

50,000

1998 19991997

SEK m.

Sales 1997 1998 1999

Sales, units

Trucks 42,392 45,553 46,651

Buses 4,584 4,117 3,763

Total 46,976 49,670 50,414

Sales, SEK m.

Scania products 35,087 39,675 41,728

Svenska Volkswagen products 4,632 5,637 5,382

Total 39,719 45,312 47,110

Operating income, SEK m.

Scania products 2,789 3,342 4,795

Svenska Volkswagen products 258 250 250

Total 3,047 3,592 5,045

Operating margin, %

Scania products 7.9 8.4 11.5

Svenska Volkswagen products 5.6 4.4 4.6

Total 7.7 7.9 10.7

Income after financial items, SEK m. 2,751 3,214 4,500

Net income, SEK m. 1,943 2,250 3,146

Earnings per share, SEK 9.70 11.25 15.75

Earnings per share accordingto U.S. GAAP, SEK 11.10 11.20 16.40

Operating cash flows excludingcustomer finance operations, SEK m. –55 1,797 476

Return, %

on shareholders’ equity 20.2 20.7 25.1

on capital employed1 16.2 17.4 21.4

Net debt/equity ratio1 0.69 0.55 0.61

Equity/assets ratio, % 27.0 26.5 26.0

Capital expenditures for property, plant and equipment, SEK m. 2,566 2,026 1,876

Research and development expenses, SEK m. 1,248 1,168 1,267

Number of employees at year-end 23,763 23,537 25,814

1 With customer finance operations reported according to the equity method.1997 1998 1999

%

Operating margin

0

2

4

6

8

10

0

1,000

2,000

3,000

4,000

1997 1998 1999

SEK m.

Operating income

5,000

4

A number of circumstances contributedto the fine growth in earnings. One was avery strong western European market.But the main explanation is that the com-pany has now completed the changeoverto new product ranges and its transitionto a partly new production system.

Bolstering the distribution networkIn recent years, European haulage compa-nies have increasingly demanded vehiclesthat carry maintenance, repair and financ-ing packages for a period of four to fiveyears. The trend towards focusing on their

STATEMENT OF THE PRESIDENT AND CEO

Leif Östling

Scania had a very good year in 1999. Sales volume rosesomewhat and earnings jumped by 40 percent.The op-erating margin on Scania products, at 11.5 percent, isback at a traditionally high Scania level.

actual transport operations and outsourc-ing other activities has become clearerand clearer.

This trend began in the late 1980s inGreat Britain and the Benelux countriesbut is also becoming more common in other countries. It will become even morepronounced in the future, both in Europeand elsewhere.

In light of this, we have systematicallystrengthened and expanded our distribu-tion and service organisation in all west-ern European markets over the past fiveyears. During 1999, Scania acquired itsdistributors in Italy, Norway and Finland.

We are also continuing to expand ourdistributor organisations in the importantgrowth markets of central and easternEurope, despite temporarily weak demand

5

Broader product conceptDelivering the best total solutions in themarket is the key to achieving Scania’sgrowth targets. During 1999, efforts tofurther refine Scania’s service, maintenanceand finance packages thus continued.

Investments in Scania-specific electron-ic and information systems intensified. Asone step in this effort, Scania Infotro-nics AB, a cutting-edge company in infor-mation technology (IT) based vehicle electronics, was established. Scania iscommitted to assuming a leading role intransforming IT developments into prac-tical vehicle applications that benefit ourcustomers.

Continued strong demandDuring 1999, demand for heavy trucks inwestern Europe was larger than most ob-servers had expected. The EU is showinggood economic growth, and there is prob-ably still a large need to replace the ve-hicles sold during the previous demandpeak around 1990. Another reinforcingfactor is environmentally related demand,due to new regulations as well as the factthat customers see it as a competitive ad-vantage to have the best environmentallyadapted vehicles.

Markets in Asia were weak during1999, but there was some recovery dur-ing the second half. In the long term, theregion offers major potential to Scania,and we are continuing to strengthen ourdistribution and service network there.

Latin America had a difficult year.Early in 1999, Brazil devalued its currency,driving demand throughout the regiondown to a very low level. We have imple-mented vigorous action programmes toadapt our cost level to the prevailing de-mand. Given these actions, in our judge-ment we will achieve at least break-evenduring 2000.

This year is certain to be exciting.Western European markets seem to becontinuing at a high level. Central andeastern Europe are bouncing back, as arethe markets of Asia. I also see certainsigns that Latin America will be able torecover from the current low demand.

Focus on qualityDespite the prevailing uncertainty duringthe past 14 months, in my judgement Scania has not suffered any serious harmin the short term. We are working at fullspeed to develop new products. Scania’sproduction system will be further stream-lined by a number of development pro-grammes. The distribution and service organisation will continue to undergochanges in response to customer demandfor fast, high-quality service. All workwill focus on quality – in the development,production and distribution/servicing ofour products.

I would like to close by thanking allour employees for their solid dedication,outstanding contributions and very fineearnings performance during the tumul-tuous year we have now completed.

Leif ÖstlingPresident and CEO

6

The European truck market remained vigorous during 1999. Despite continuedvery weak demand in important Scaniamarkets – South America, eastern Europeand South East Asia – and mounting pricecompetition, Scania increased its earnings.

In January 1999, when Scania an-nounced its preliminary results for 1998,we issued a forecast stating that operatingincome would improve by about SEK 1.5billion during 1999. I am now pleased tonote that this was achieved.

Highest profitability in the industryWith an operating margin of 11.5 per-cent, Scania has again shown the highestprofitability in its industry. The operatingmargin of Scania’s European operationswas 13 percent, which must be describedas very strong.

This is the result of Scania’s invest-ments over the past several years in anew, attractive range of vehicles, service-related products and customer financing,as well as a largely new and more efficientproduction system.

Focus on ownershipVolvo’s purchase in January 1999 of ashareholding in Scania, and Volvo’s ex-press desire to purchase all shares, accen-tuated the issue of Scania’s future andownership structure.

STATEMENT OF THE CHAIRMAN

Anders Scharp

For Scania, 1999 was a year of upheaval.The issue ofthe company’s future ownership structure was in focusand we were forced to work in uncertainty regardingour future ownership. Meanwhile Scania showed itsstrength in the form of earnings at a historically highScania level.

We are convinced that Scania has verygood potential to remain an independentplayer in the heavy vehicle market. Scaniais one of the world’s five largest makes of both heavy trucks and buses. The com-pany has successfully implemented itsproduct renewal and production change-over and thus stands well equipped forthe future.

In August, Volvo agreed to purchaseInvestor’s shareholding in Scania and announced a public offer for all sharesoutstanding in Scania.

The Competition Directorate of theEuropean Union then carried out its ex-amination of Volvo’s acquisition – fromSeptember 1999 to March 2000. The European Commission’s decision on 14March signified a rejection of Volvo’sproposed acquisition of Scania. As a re-sult, Volvo withdrew its offer to the share-holders of Scania.

A strong ScaniaDespite the uncertainty of the past year,Scania has continued to show strength.The unique Scania spirit has enabled ouremployees to focus successfully on theirrespective assignments without being dis-tracted by everything that has been hap-pening on the ownership issue. Scania’svery strong 1999 earnings consolidated its leading global position in the industry.

Late in March 2000, it was announcedthat Volkswagen had agreed with Investorto acquire 34 percent of the voting power and18.7 percent of the share capital in Scania.

7

The intention is that Scania, in accor-dance with statements in conjunction tothe deal between Volkswagen and Investor,continues to be a listed company and willalso continue to follow Swedish practiceregarding obligations towards share-holders, corporate governance, auditingand disclosure.

In closing, I would like to express thegratitude of the Board to the managementand all employees of Scania for their finecontributions during a year of turbulencebut of very good results for our company.

Anders ScharpChairman

8

SCANIA SHARE DATA

Since 1 April 1996, both types of Scaniashares – Series A and Series B – have beenquoted on what is now called the OMStockholm Stock Exchange (SSE) and onthe New York Stock Exchange (NYSE).In Stockholm, both A shares and B sharesare quoted on the SSE’s A list. A roundlot consists of 100 shares. Since 1 January2000, the B share is no longer included in the Swedish OMX Index. On theNYSE, Scania shares are traded in theform of American Depositary Receipts(ADRs), consisting of 10 shares. Citibankis the depositary bank. Scania shares arealso traded on the London Stock ExchangeAutomated Quotations system for non-UK equities (SEAQ International).

Share prices and tradingB shares – the more heavily traded of Scania’s two series – rose by 104 percentduring 1999. During the same period, theindex of Swedish engineering companies

rose by 117 percent and the SSE GeneralIndex by 66 percent. At year-end, B shareswere quoted at a market value of SEK306.50 apiece. This was equivalent to amarket capitalisation of SEK 61,100 m.The highest closing price for B shares during the year was SEK 312.50 apieceon 27 August. The lowest, SEK 157.50,was paid on 4 January.

The beta coefficient shows the fluctua-tions of a specific share in relation to anentire stock exchange. According to cal-culations by the OM Stockholm StockExchange, the beta coefficient of Scania Bshares was 1.04 at the end of 1999. Thismeans that on average, Scania shares fluc-tuated 4 percent more than the Exchangeon average. The explanatory value forScania shares was 0.55, which means the55 percent of share price changes can beexplained by overall changes on the SSE.

On average, about 1,082,000 shareschanged hands each trading day in Stock-holm, for a turnover rate of 137 (86) per-cent, compared to 94 (76) percent on theSSE as a whole. The heavy trading is ex-plained by Volvo’s purchases of Scaniashares during the year as well as other heavy trading due to changes in owner-ship structure.

Scania’s share capital is distributed among 100 millionA shares and 100 million B shares. Each A share rep-resents one vote and each B share one tenth of a vote.Otherwise there are no differences between these typesof shares.The nominal (par) value per share is SEK 10.

B shares

Affärsvärlden General Index

(c) SIX

4/96

5/96

6/96

7/96

8/96

9/96

10/9

611

/96

12/9

61/

972/

973/

974/

975/

976/

977/

978/

979/

9710

/97

11/9

712

/97

1/98

2/98

3/98

4/98

5/98

6/98

7/98

8/98

9/98

10/9

811

/98

12/9

81/

992/

993/

994/

995/

996/

997/

998/

99 9/99

10/9

911

/99

12/9

91/

002/

00

Share price, OM Stockholm Stock Exchange, Scania B shares

Trading volumein thousands(incl. after-market)

6,50013,00019,50026,00032,50039,00045,50052,000 58,50065,000

100

150

200

250

300

350

400

450500550600650

9

In NewYork, an average of about 1,100Scania ADRs were traded per day, downby about 400 from the year before. Atyear-end there were 86,000 ADRs out-standing, compared to 77,000 at the be-ginning of 1999.

Ownership structureOn 15 January 1999, AB Volvo acquired13.5 percent of the voting power and 12.9percent of the share capital in Scania. Volvo gradually increased its stake, hold-ing 21.5 percent of the votes and 20.3 percent of the capital at the end of April.On 6 August 1999, Volvo signed an agree-ment to purchase Investor AB’s shareholdingin Scania, equivalent to 49.3 percent of thevotes and 27.8 percent of the capital. Atthe same time, it presented a conditionalpublic offer for the remaining shares out-standing. After a decision by the EuropeanCommission not to approve the proposedacquisition, on 14 March 2000, Volvowithdrew its offer. On 27 March 2000, Investor agreed with Volkswagen AG tosell 34.0 percent of the voting power and18.7 percent of share capital in Scania. On 29 February 2000, Volvo’s holdingamounted to 30.8 percent of the votes and46.9 percent of the capital. Apart from Volvoand Investor, SPP remained as a major share-holder on 29 February, with 3.1 percent ofthe capital and 4.6 percent of the votes.

On 29 February 2000, the number ofshareholders in Scania was about 43,000,an increase of 4,000 since the beginning of 1999.

Scania on the InternetScania’s website includes informationabout the company and provides a wayto contact Scania’s Investor Relations de-partment. The address is www.scania.com

Per share data

SEK (unless otherwise stated) 1999 1998 1997

Earnings 15.75 11.25 9.70

Shareholders’ equity 67.75 59.30 51.80

Dividend (1999 proposed) 7.00 6.50 5.50

Market prices, B-shares(closing price)

Highest for the year 312.50 230.00 240.00Lowest for the year 157.50 132.50 166.50Year-end 306.50 150.00 179.00

Price/earnings ratio, B-shares 19.5 13.3 18.5

Dividend payout ratio, % 44.4 57.8 56.6

Dividend yield, % (B-shares) 1 2.3 4.3 3.1

Annual turnover rate, % 136 86 60

Number of shareholders 43,0002 39,0003 45,000

Average daily number of shares traded 1999:

– OM Stockholm Stock Exchange A 232,000B 850,000

Total 1,082,000

– New York Stock Exchange A-ADRs 575B-ADRs 543

Total 1,1181 Dividend divided by the market price of a

B share at year-end.2 As of 29 February 2000.3 As of 29 January 1999.

Ownership structure29 February 2000

% of % ofNumber of shares shareholders shares

1– 500 91.1 2.7501– 2,000 6.9 1.52,001– 10,000 1.4 1.310,001– 50,000 0.3 1.650,001–100,000 0.1 1.1

> 100,000 0.2 91.8

Total 100.0 100.0

The ten largest shareholders29 February 2000

% of voting % ofpower shares

Investor 49.3 27.8Volvo 30.8 46.0SPP 4.6 3.1Svenska Handelsbanken (SHB) sphere 1.5 0.9Nordbanken mutual funds 1.1 1.1SEB sphere 0.9 1.2Wallenberg sphere 0.8 3.9AMF Pension 0.5 0.6Hagströmer-Qviberg sphere 0.3 0.2SHB mutual funds 0.3 0.3Total 90.1 85.1

10

MISSION AND STRATEGY

Mission statementScania’s mission is to supply its customers with vehicles and servicesrelated to the transport of goods and passengers by road. By focusingon customer needs, Scania shall create value-added for the customerand grow with sustained profitability. Scania thereby generates share-holder value.

Scania’s industrial operations specialise in developing and manufac-turing vehicles, which shall lead the market in terms of performance,life-cycle cost, quality and environmental characteristics.

Scania’s commercial operations, which include distributors, dealersand service points, shall supply customers with optimal equipment andaftersales support, thereby providing maximum operating time at mini-mum cost over the service life of their vehicles.

Strategy• Focus on heavy transport vehicles:

Scania’s operations concentrate on heavy transport vehicles. In maturemarkets, demand for heavy trucks andbuses increases with GDP growth. Indeveloping countries, it also increasesas infrastructure expands.

Heavy vehicles are specialised prod-ucts that are used as working tools.Scania’s trucks, buses and industrialand marine engines have an establishedreputation as quality products, both interms of performance and price.

• Modular product system and globalproduction system:Buyers of heavy transport vehicles de-mand customer-specific solutions. Themore closely a vehicle is adapted to itstransport task, the more economically itwill operate.

Scania’s modular system is based onthe use of common components in anumber of different specifications. Thiscreates customer benefit by making itpossible to specify vehicles individually.It also leads to improved quality, sim-

plified parts management and a higherdegree of service.

The modular system limits the totalnumber of components in Scania’s prod-uct range. It thereby allows consider-ably longer production runs for thesecomponents than a conventional prod-uct system. Scania’s global productrange, featuring standardised compo-nents and global quality standards, makesit possible to use the same process technology at all Scania facilities.

• Complete range of vehicles, servicesand financing:Offering the best package solutions in the market is the key to achievingScania’s growth targets. Scania’s cus-tomers demand round-the-clock access to their vehicles. This presupposes rapidaccess to service and repairs. In addi-tion to its vehicle development work,Scania is continuously improving itsdistribution and service network.

Scania is working actively to expandits range of services and financing in order to achieve more rapid profitabilitygrowth.

• Focus on growth markets:Scania’s main markets – Europe, LatinAmerica and Asia – have good potentialfor long-term growth.

A borderless Europe of growingeconomies is offering major opportuni-ties to manufacturers that have a well-developed distribution and service net-work.

In Latin America, an increasing shareof both goods and passenger traffic uti-lises heavy vehicles. The demand for ve-hicles, services and financing is increasing.

Asia is a long-term growth market.As the infrastructure improves, a stream-lining of the transport sector will becomepossible.

11

Scania’s identityScania has a strong corporate culture thathas laid the groundwork for the company’ssuccess. Scania’s identity is shaped bothby its products – vehicles, services andcustomer financing – and by the valuesand behaviour of the company.

Scania’s product identityThe Scania brand name has a strong iden-tity, and Scania’s products stand for pres-tige and high performance. The promisesmade by this brand name must constantlybe fulfilled in the company’s encounterswith its customers.

Only high performance and qualitycan satisfy customers’ expectations ofScania. Scania offers prestige products inwhich customers must feel total confidence.These products must also help their own-ers and drivers to feel proud of their choiceof professional working tools.

Behaviour/way of workingThe principles that have governed thecompany’s past work have laid the ground-work for Scania’s public image and success.In modernised form, these principles mustalso characterise its future efforts.

Forward-looking integrityClose and lasting relationships with de-manding customers have laid the ground-work for Scania’s development of productsand services. Scania has based its work onthe customer’s business and has peeked around the corner. By thinking independ-ently, Scania has developed forward-lookingtransport solutions that are competitivethroughout the life cycle of its products.

Scania takes responsibility for a holis-tic approach to customer transport solu-tions by expanding its service offeringand adapting it to a customer’s overallbusiness.

SCANIA’S IDENTITY AND BEHAVIOUR

Scania offers prestigeproducts in whichcustomers must feeltotal confidence.These productsmust also help theirowners and driversto feel proud oftheir choice of pro-fessional workingtools.

Systematised simplicityModularisation is one cornerstone in thedevelopment of Scania’s products and services, making it possible to combinespecialised, customer-adapted solutionswith the economies of long productionruns. It also ensures quality, simple partsmanagement and a high level of service.

Scania uses advanced technology butavoids fads and unnecessary complexity.Its technical solutions must generate value

12

by providing robust and reliable productsas well as simple, comprehensible, demand-controlled work flows.

Coordinated independenceScania takes advantage of economies ofscale, striving for uniformity that willcontribute to higher quality, productivityand flexibility. Otherwise general guide-lines are responsible for the necessarycoordination.

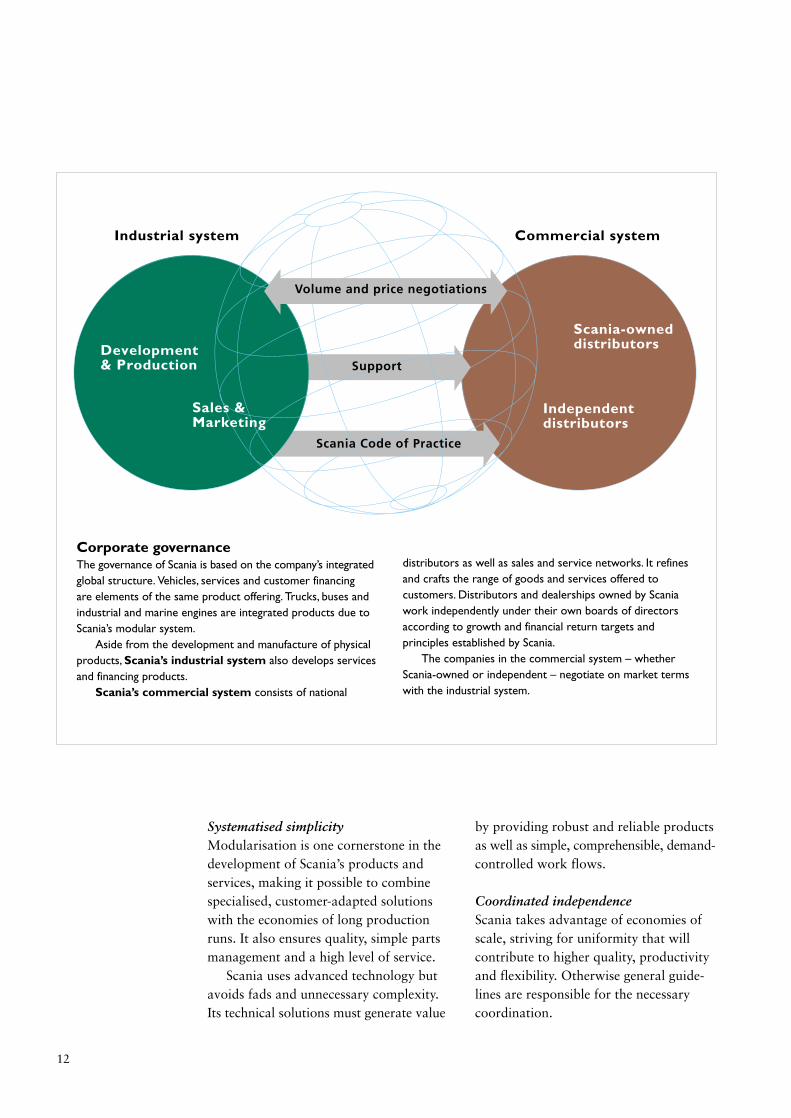

Corporate governanceThe governance of Scania is based on the company’s integratedglobal structure. Vehicles, services and customer financing are elements of the same product offering. Trucks, buses andindustrial and marine engines are integrated products due toScania’s modular system.

Aside from the development and manufacture of physicalproducts, Scania’s industrial system also develops servicesand financing products.

Scania’s commercial system consists of national

distributors as well as sales and service networks. It refines and crafts the range of goods and services offered tocustomers. Distributors and dealerships owned by Scaniawork independently under their own boards of directorsaccording to growth and financial return targets andprinciples established by Scania.

The companies in the commercial system – whetherScania-owned or independent – negotiate on market termswith the industrial system.

Industrial system Commercial system

Development & Production

Scania-owneddistributors

Sales & Marketing

Independent distributors

Volume and price negotiations

Support

Scania Code of Practice

13

Within the limits of existing rules andguidelines, Scania managers independent-ly develop the operations they manage.They set targets for their operations andrely on the willingness and ability of em-ployees to take responsibility for resultsand development.

Continuous improvementScania has a tradition of working econo-mically with limited resources. Every ac-

tivity must create value-added for its re-cipients and every cost must be related to a corresponding benefit.

In Scania’s day-to-day work, the qualityand efficiency of a unit’s own efforts mustbe systematically compared to the bestpractices in each field. Continuous im-provement efforts generate higher valueand lower the consumption of resources.

Scania’s V8-engine iswidely used for de-manding transporttasks.

Scania’s sales of heavy vehicles rose fromjust above 30,000 to approximately 50,000during the 1990s. This expansion is theresult of deliberate investments in higherproduction capacity. Scania has capturedmarket share in both western Europe andthe growth markets of Latin America,central and eastern Europe and Asia. Dur-ing the 1990s, growth in the service sec-tor was even higher than for vehicles.

Scania’s owners1991: Investor bought Saab-Scania, de-listing it from the stock market.

1994: Scania again became an indepen-dent company when Saab-Scania was de-merged into two separate companies.

1996: Scania gained a listing on theStockholm Stock Exchange and – as thefirst Swedish company – on the NewYork Stock Exchange.

1999: Scania’s main owner, Investor, signed an agreement to sell all its shares to Volvo, which made a public offer for the remaining shares in Scania.

14

2000: The European Commission decidednot to approve Volvo’s proposed acquisi-tion of Scania. Volvo withdrew its offerto Scania’s shareholders.

Investor signed an agreement withVolkswagen AG on the sale of 34.0 per-cent of voting rights and 18.7 percent ofcapital in Scania.

Evolution into a global player1989: Scania’s new management, headedby Leif Östling, established as its objec-tives that Scania would increase sales volume and work in an even more inte-grated way, in order to preserve the bestprofitability in its industry.

1990: Scania began the split into an industrial system (development, manu-facturing and marketing) and a commer-cial system (Scania-owned and independ-ent distributors). The aim was to create aclearer structure in the Group and greaterfocus on growth and profitability.

1991: Scania introduced a new produc-tion system adapted to its plans for a glo-bal production structure. It began to con-centrate European component productionto fewer units, a process that continuedthroughout the 1990s. Scania began toinvest in future capacity.

SCANIA DURING THE 1990s

During the 1990s, Scania was affected by the deregula-tion of transport markets in Europe.The growing use of heavy vehicles in both the industrialised world anddeveloping countries also played a major role in thecompany’s development.

The new corporate symbol, designed whenScania again became an independent com-pany, has ties to historical Scania symbols.

The new assembly plantin Angers, France, wascompleted and fully op-erative when demandtook off in 1994.

15

1992: Scania built a new assembly plantin Angers, France, as a consequence of itsdecision to increase capacity.

1995: Scania introduced the 4-series. The4-series took Scania’s modular philosophy astep further, reducing the number of com-ponents while increasing the integrationbetween trucks, buses and industrial andmarine engines. The restructuring of op-erations into an industrial and a commer-cial system began in Latin America.

1995/1996: The changeover in the Euro-pean production system took place anddeliveries of 4-series vehicles began.

1997: Scania created a global productionstructure. After the changeover in Latin

America, it became the first heavy vehiclemanufacturer with a global product range.In other words, Scania manufactures anddelivers products with interchangeablecomponents and the same quality andperformance in all markets where thecompany is active.

Late 1990s: During the second half of the1990s, Scania intensified its forward inte-gration by acquiring several of its distrib-utors, especially in European markets.

The company expanded and strength-ened its service organisation in Europeand in other markets, by improving em-ployee expertise and establishing commonstandards. In this way, Scania guaranteesits customers a high level of vehicle avail-ability.

The 4-series, unveiledin 1995, has consoli-dated Scania’s positionas a leading truck andbus make.

In 1996 Scania becamea listed company, quotedon the Stockholm StockExchange and, as thefirst Swedish company,on the New York StockExchange.

The market in EuropeTrucks in western EuropeThe western European market for heavytrucks remained strong during the year. Atotal of 236,000 heavy trucks were regis-tered during 1999, compared to 207,000during 1998. This represented a 14 per-cent increase. The number of trucks regis-tered in 1997 was 170,000.

Of the largest markets in western Europe, Germany, France, Italy and Spainshowed the most vigorous growth, whilethe trend in Great Britain and the Nether-lands was weaker in comparison. One ofScania’s expressed goals is to prioritise alarger presence in the German, Frenchand Italian truck markets.

Scania’s share of the western Europe-an market for heavy trucks was 14.9 per-cent (15.2). The downturn in market sharewas due in large part to comparativelyweaker volume increases in the marketswhere Scania has a stronger position. Anadditional factor was a shortage of capac-ity among distributors and bodybuildersdue to high volume.

Scania’s order bookings for heavytrucks in the western European marketrose by 9 percent to 36,200 (33,300), and the number of trucks sold rose by 10 percent to 36,100 (32,700).

Despite the increase in demand, pricelevels did not rise and competition re-mained vigorous. Depressed new truckprices, combined with shorter trade-in cycles, also created pressure on prices for used trucks.

Mercedes-Benz and Volvo are thecompetitors Scania encounters in virtuallyevery market. Mercedes-Benz’ share ofthe western European heavy truck marketamounted to 20.9 percent (20.5). Volvo’sshare was 14.9 percent (15.1).

In the German market, the number ofheavy trucks registered rose by 17 per-cent. Scania increased its market share to9.5 percent (8.9) and consolidated its po-sition as the leading importer of heavytrucks.

The number of trucks registered in theBritish market during 1999 amounted to31,300, somewhat higher than the 1998

16

REVIEW OF OPERATIONS

VEHICLES

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

97 98 9990 91 92 93 94 95 96

Units

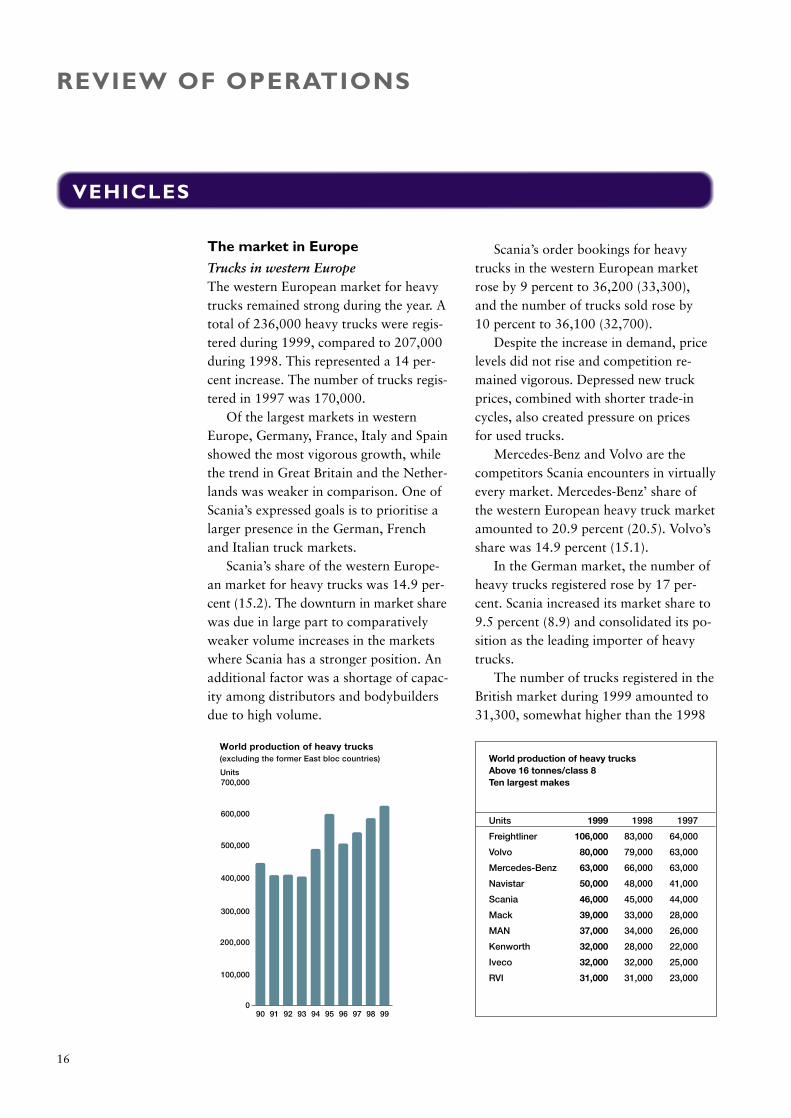

World production of heavy trucks(excluding the former East bloc countries) World production of heavy trucks

Above 16 tonnes/class 8Ten largest makes

Units 1999 1998 1997

Freightliner 106,000 83,000 64,000

Volvo 80,000 79,000 63,000

Mercedes-Benz 63,000 66,000 63,000

Navistar 50,000 48,000 41,000

Scania 46,000 45,000 44,000

Mack 39,000 33,000 28,000

MAN 37,000 34,000 26,000

Kenworth 32,000 28,000 22,000

Iveco 32,000 32,000 25,000

RVI 31,000 31,000 23,000

17

level. Scania’s market share amounted to18.1 percent (18.8).

In the French market, rapid growthcontinued and the peak achieved in 1998was exceeded. Scania’s share of the mar-ket rose to 10.7 percent (9.4).

The Italian market was characterisedby the continued impact of deregula-tion, and sales increased sharply. Scania’s market share rose to 12.8 percent (12.5).Early in 1999, Scania acquired its Italiandistributor as part of its expansion in Italy.During October, it also acquired the Italianfinance company Fiscar S.p.A.

In the Netherlands the total number ofregistrations decreased somewhat, follow-ing strong growth in the preceding year.Scania’s share of the market decreased to19.4 percent (22.7).

The demand in the Nordic market waslargely unchanged during the year. Scaniastrengthened its market position, primarilyin Sweden. Its total market share in theNordic countries amounted to 35.5 per-cent (34.9).

Market shares, heavy trucks in western Europe

5

10

15

20

25

30

VolvoScania

RVI

Mercedes

MAN Iveco

DAF

%

89 90 91 92 93 94 95 96 97 98 99

0

50,000

100,000

150,000

200,000

250,000

90 91 92 93 94 95 96 97 98 99

Units

Registrations, heavy trucksin western Europe

With the 4-series,Scania has strength-ened its position inthe construction segment.

Trucks in central and eastern EuropeThe downturn in the markets of centraland eastern Europe that began during thesecond half of 1998 continued during1999. The recession, caused by Russia’seconomic slump, led to lower volume andsharp price reductions, especially for inter-national transport services. This resultedin diminished buying power among hauli-ers, which in turn decreased the room fornew truck sales.

The number of newly registered heavytrucks of western European origin de-creased by 30 percent to 11,600 (16,600).During the year, Scania delivered about1,600 trucks (2,200), down more than 25percent. However, Scania noted increaseddemand during the latter part of the year.

Despite temporarily difficult marketconditions, Scania views the region as animportant growth market. During the

year, efforts to strengthen the distributionand service network continued, with newfacilities being added in most countries inthe region.

Gradually improved transport volumeplus a general improvement in the credit-worthiness of hauliers indicate a strongermarket ahead.

Buses in EuropeThe total market for heavy buses in west-ern Europe remained at the same level asduring 1998. The number of bus registra-tions rose somewhat to 21,800 (21,000).

The markets in Austria, Sweden andGreat Britain grew the most during the year.

The deregulation of city and intercitybus services in western Europe continued.This improves the opportunities for Scaniato enter markets, such as Germany, Franceand Italy, previously dominated by do-mestic makes.

Scania’s transition to the new genera-tion of buses, which are manufactured ac-cording to the same modular concept astrucks, was fully implemented.

Scania has decided to establish twocentral distribution units for its bus salesin 15 European markets, independent ofthe truck distribution organisation. This

“A dense network of service points

with professional mechanics and the

availability of vehicle service essentialy

round the clock is very important to

our business. Our customers are de-

pendent on punctual deliveries.”

Hans Adam Schanz,

Managing Director and owner of Spedition Schanz,

Ober-Ramstadt, Frankfurt, Germany.

18

0

5,000

10,000

15,000

20,000

25,000

90 91 92 93 94 95 96 97 98 99

Units

Registrations of heavy busesin western Europe

0

20,000

10,000

30,000

50,000

40,000

60,000

70,000

90 91 92 93 94 95 96 97 98 99

80,000

Units

World production of heavy buses(excluding the former East bloc countries)

new structure enables an increased focuson sales and services of buses. The needsof bus companies that operate across na-tional boundaries can also be better satis-fied. The two units, Scania Bus Europe andScania Bus Nordic, will have a resourcecentre in Belgium and one in Sweden.

Scania’s bus sales grew more than thetotal market. This was due, among otherthings, to a broader product range as wellas more efficient production of buses andbus chassis.

Sales in Europe rose by 9 percent to2,000 buses and bus chassis (1,840) andmarket share rose to 8.3 percent (7.6).

Scania’s order bookings in Europe to-talled 1,700 buses and bus chassis(1,840), a decrease of 8 percent.

Spain was again Scania’s foremost busmarket in Europe, with 560 Scania busesregistered (370). Last year’s downturn inmarket share, due to delivery problems,was recouped and surpassed.

Scania’s share of the Nordic marketstrengthened substantially to 28.7 percent(24.4), due to large sales volume, espe-cially of city buses.

Industrial and marine enginesTotal deliveries of industrial and marineengines showed good growth. Scania’soverall sales amounted to 3,280 engines

(2,840), of which 70 percent industrialengines and 30 percent marine engines. Onecontributing reason behind the increasewas strong demand for generator sets.

The 12-litre engine for industrial useshowed continued sales successes duringthe year.

In Europe, the number of engines soldincreased to 2,080 (1,910).

19

Scania engines are used in the prestigesegment of pleasure craft.

The OmniCity is Scania’s new city bus.It is available eitherwith a body by Scaniaor as a chassis (N94)on which independentbodywork companiesbuild a customised superstructure.

The market in Latin AmericaTrucksThe Latin American markets showedweakness during 1999. Scania’s sales fellby 17 percent to 6,300 trucks (7,600).Order bookings decreased by 25 percentto 6,100 trucks (8,100).

During the year, the Latin Americanplants had full delivery capacity after theproduction changeover to the 4-series,which could nevertheless not be utiliseddue to limited demand.

“Salt is a good business, but global

competition is tough and the margins

are shrinking.To lower our transport

costs, we use new Scania trucks.”

Brothers Carlos, Francisco and Benedito

de Lima, owners of Sal Maranata in Mossoró,

Rio Grande do Norte, Brazil.

The Brazilian economy performed weakly during the year, and GDP grewinsignificantly. Even though the currencyfell by nearly 60 percent against the USdollar, trade balance problems persisted.Financing costs for hauliers remainedhigh, although interest rates improved to-ward year-end.

The Brazilian market for heavy trucksdecreased by 15 percent to 13,500 vehi-cles, compared to 15,800 vehicles in1998.

The market was characterised by ex-tremely tough competition, among otherthings due to the sharp depreciation inthe currency as well as the entry of Ivecoand Navistar in the heavy truck market.Scania’s market share amounted to 31.7percent (33.4).

The market trend in Argentina wasweak during the year. GDP declined byabout 3 percent in 1999 and the country’strade balance and central governmentbudget showed a weak trend. Despite gov-ernment subsidies to buyers of domesti-cally made vehicles, heavy truck registra-tions decreased by 25 percent andamounted to 4,200.

Scania consolidated its position as themarket leader in Argentina, increasing itsmarket share to 32.5 percent (28.6).

The Mexican truck market grew by 12percent to 14,800 during 1999. Scania’ssales in Mexico are comparatively low,

Sales of Scania trucks in Latin America

0

2,000

4,000

6,000

8,000

10,000

999796959493929190 98

Units

20

0% 20% 40% 60% 80% 100%

Argentina

Brazil

Scania Iveco Mercedes Ford Others

Scania Mercedes Volvo Ford Others

Market shares in Argentina and Brazil

21

but there are long-term prospects forgood market growth. During the year,Scania established four wholly-owneddistributors.

BusesThe demand for buses in Latin Americawas weak. Scania’s deliveries of bus chas-sis totalled 1,200 (1,700), a decrease of29 percent.

In the Brazilian bus market, demandwas very weak. The total market shrankby 40 percent, from 13,400 to 8,100 ve-hicles. Scania’s deliveries decreased byabout 40 percent to 700 bus chassis

(1,200) and its market share was un-changed at 9.0 percent. Scania’s positionin the intercity and long-distance segmentstrengthened.

In Argentina, Scania increased its mar-ket share to 14.9 percent (7.0) in a weaktotal market. Scania dominates the long-distance bus segment, but also had somesuccess in the city bus segment.

Sales in other Latin American marketsdeclined.

Industrial and marine enginesDeliveries of industrial and marine en-gines in Latin America rose to 740 units(700), due to higher demand for dieselengine-driven generators during the latterpart of the year.

Paolo Silveira,Managing Director, City Rio Project.

Sales of Scania buses in Latin America

0

500

1,000

1,500

2,000

2,500

3,000

98 999796959493929190

Units

“With new low-floor buses from Scania, we have given Rio de Janeiro’s tourists the chance to seeone of the world’s most beautiful cities in a morepleasant and convenient way.”

During 1999, Scania’sbreakthrough into thecity bus segment inBuenos Aires, Argen-tina, continued.

22

Markets in Asia, Africa and AustraliaTrucksDemand for heavy trucks was weak inmost of Scania’s other markets during1999. Scania’s order bookings decreasedto 2,600 vehicles, compared to 2,800 dur-ing 1998. In most Asian markets, pricesremained depressed due to weak demand,both for new and second-hand trucks.Asian markets, in particular, were still af-fected by the aggressive marketing andpricing of Japanese truck manufacturers.

Towards the end of 1999, however, animprovement was discernible in most ma-cro-economic indicators, and inventoriesof new trucks in most markets had fallensharply since the beginning of the year.

Sales in Asia rose by 5 percent to1,480 vehicles (1,410) and decreased inother markets to 1,300 vehicles (1,600).

In East Asia, Taiwan and Hong Kongaccounted for the heaviest demand forScania products. Strong competition, es-

pecially from Japanese manufacturers, ledto falling price levels, however, as well aslower market shares for European makes.The South Korean market remainedweak. During the year, Scania inaugurat-ed a new superstructure factory in Koreaand further expanded the distribution andservice network under its own auspices.

Demand varied between the variousmarkets in the Middle East. In Iraq, Scaniadelivered vehicles to the United Nations“Oil for Food” project, as part of the easingof sanctions approved by the UN. TheTurkish market remained weak. Scania’sdeliveries to the Israeli market increasedsharply.

The market in Australia was character-ised by new sales tax rules, which contrib-uted to a wait-and-see attitude by haul-iers on new investments in trucks. Earlyin the year, a new Scania facility was in-augurated in Melbourne.

Demand in North Africa remainedgood, and Scania became the market

Timber transportwork in Ngome,South Africa, a rapidly growingmarket for Scania.

23

leader in Morocco. The South African mar-ket was weak, but showed signs of recov-ery by year-end. Scania increased its mar-ket share to 12.1 percent (7.9) during 1999.

BusesThe demand for heavy buses varied be-tween markets. Total sales amounted to520 bus chassis (580).

Taiwan and Australia were importantbus markets for Scania during 1999. InTaiwan, sales rose during the year after aperiod of weak demand.

Demand in Australia remained strong,and during 1999 Scania received an orderfor up to 120 gaspowered buses fromBrisbane.

Demand was also strong in Morocco

and Egypt. Scania made a breakthroughin the city bus market in Morocco, re-ceiving an order for 70 buses from Marr-akesh. A new service facility was also built in Morocco.

In South Africa, Scania signed agree-ments to sell 340 buses for intercity ser-vice. This is the company’s largest-everbus deal in southern Africa.

Industrial and marine enginesDeliveries of industrial and marine enginesto markets in Asia, Africa and Australiarose to 380 units (170). This change waslargely explained by the recovery of themarket in Saudi Arabia. In addition, mar-ket conditions improved somewhat in theAsian region.

Tourist coaches areScania’s largest bussegment. For the mostpart, Scania deliverschassis to which localbodywork manufac-turers add superstruc-tures, as here in NewZealand.

The pay level in Sweden rose by about5 percent, compared to about 3 percentin the Netherlands and France, calculatedin local currency. Of all production em-ployees in Europe, 75 percent are in Swe-den, 19 percent in the Netherlands and 4percent in France.

Material costs per truck produced, ex-pressed in local currency and with an un-changed specification level, declined byabout 4 percent during the year as a re-sult of component redesign and lowerpurchasing costs. Due to a changed mar-ket mix and a higher specification level,total material costs per truck increased.

Warranty costs for trucks at the factorylevel decreased, but remained at a some-what higher level than for the previousproduct range. Delivery assurance wasvery high during the year.

Depreciation was largely unchangedfrom 1998. The capital expenditure levelcontinued to fall, amounting to SEK 780 m.

Steps toward greater specialisationand production coordination continued,in response to demands for greater effi-

Production in EuropeThe pace of production remained highduring the year, as a result of strong de-mand for heavy trucks in western Europe.In all, European operations produced42,300 vehicles (41,700), of which 39,800trucks (38,900) and 2,500 buses (2,800).

Productivity, measured on a rolling12-month basis as the number of vehiclesmanufactured divided by hours worked,rose by 3 percent.

The workforce was largely unchangedduring the year. A significant proportion of Scania’s production personnel are em-ployed on time-limited contracts. This increases Scania’s ability to respond tofluctuating demand in a cost-effective,flexible way.

One important production-related goalhas been to increase volume flexibility infinal assembly. In the existing productionsystem, today it is possible within onemonth to change production volume by±10 percent in relation to the approved bas-ic production rate and change the basicrate by ±15 percent within three months.

24

Scania is a global manufacturer

Södertälje Head Office, research anddevelopment, component and enginemanufacture, truck assembly.

Falun Axle manufacture.

Silkeborg Bus assembly.

San Luís Potosí Truck andbus assembly.

Tucumán Gearbox and axle manu- facture, truck assembly.

São Paulo Engine and cab manufacture,truck and bus assembly.

Angers Truck assembly.

Zwolle/Meppel Engine and cab manufacture, truck assembly.

Katrineholm Bus and bus chassis de-velopment and manufacture.

Sibbhult Gearbox manufacture.

Slupsk Truck and bus assembly.

Luleå (Ferruform AB) Manufacture ofside and crossmembers as well as rearaxle housings.

Oskarshamn Cab manufacture.

Mexico

Sweden

Sweden

Poland

Denmark

The Netherlands

France

Argentina

Brazil

25

ciency. During the year, Scania decided on a gradual transfer of remaining cabproduction in Meppel, the Netherlands,to Oskarshamn, Sweden. The transfer ofengine and axle assembly from Zwolle,the Netherlands to Södertälje and Falun,Sweden, respectively, continued. In Octo-ber, the frame, crossmember and rear axle housing production unit in Luleå,Sweden, was turned into a limited com-pany under the name Ferruform AB. Thiscompany will compete in the market andbe able to have other customers besidesScania. In addition, the production unitfor special-purpose vehicles in Laxå, Sweden, was sold to its management.

In truck assembly, projects aimed atdeveloping standardised working meth-ods for all of Scania’s assembly plantscontinued. During 1999, among otherthings these projects focused on increasingthe proportion of trucks that go directlyfrom the assembly line to the customer, aswell as on reducing inventory costs. In ad-dition, Scania continued its streamliningof final assembly in order to achieve evenhigher delivery assurance and quality.

Production in Latin AmericaDue to the weakness of Latin Americanmarkets, the pace of production was low.

During the year, 7,200 vehicles (8,400)were produced, of which 6,000 trucks(6,700) and 1,200 buses (1,700).

An extensive action programme wasimplemented in order to adapt the costsituation to the prevailing demand andreduce manufacturing cost per vehicle.This included a continued reduction inthe workforce. During 1998–1999, thenumber of production employees declinedby nearly 23 percent.

The changeover to the 4-series at bothtruck and bus production units was com-pleted by the beginning of 1999, makingpossible a substantial improvement inproductivity.

Other elements of the programme area sharp decrease in indirect costs, inven-tory reductions and a slower pace of in-vestments.

Domestic component content in ve-hicles was increased, among other thingsto offset the effects of the Brazilian currencydevaluation. In addition, deliveries fromLatin American production units to othermarkets increased. This included the de-livery of 150 complete trucks from Brazilto western Europe.

In Mexico, Scania began assembly ofbus chassis.

Axle manufacturing inthe European produc-tion system has beenconcentrated at Scania’splant in Falun, Sweden.

Research and developmentScania’s research and development expensesduring 1999 rose to SEK 1,267 m. (1,168).R&D operations are concentrated at theScania Technical Centre in Södertälje,Sweden.

Scania’s review of its product develop-ment process, which has been under wayfor three years, entered its final phase in1999. The main purpose of the projecthas been to standardise working methodsand introduce a multidisciplinary approachto the pursuit of product development.The result is increased opportunities tosatisfy the needs of customers for cutting-edge products in a shorter time, throughoptimal utilisation of development re-sources. By year-end, 85 percent of currentprojects were being run according to thenew product development model, com-pared to 20 percent at the beginning ofthe year.

During 1999, Scania started a newproject aimed at making further develop-ment and customer-adaptation of the 4-series more efficient.

In September, Scania unveiled a proto-type concept vehicle for the decade begin-ning in 2010. This concept shows the po-tential for reducing heavy truck traffic byincreasing the capacity of each vehicle by50 percent compared to the trucks of to-day. The concept vehicle features advancedaerodynamics and other forward-lookingsolutions representing substantial environ-mental improvements due to enhanced fuelconsumption and safety improvements dueto reduced stopping distances, for example.

During 1999, there were intensifiedinvestments in Scania-specific electronicand information systems. Scania’s focuson service and maintenance is behind size-able development work on analytic anddiagnostic tools. The purpose of thesetools is to inform drivers and hauliers con-

ProcurementThe programme that Scania began during1997 to streamline its procurement op-erations was largely completed during theyear. This has included reorganising theinternal purchasing process and optimis-ing supplier structure. Regular activitiesto streamline Scania’s procurement workwill continue, however.

The goal of the restructuring pro-gramme has been to lower the long-termcosts of materials, components and com-ponent systems. Scania is working togetherwith its suppliers to lower its costs andcreate room to improve profitability forboth parties. The ambition is to allowsuppliers to assume greater responsibilityfor the components or systems that theydeliver and to concentrate Scania’s ownproduct development work on areas unique to Scania’s products and brandname. Suppliers should preferably be ableto furnish Scania’s production units withlocally manufactured components.

A total of 13 different product groups– including steel and pipes, wiring, forgedcomponents and lighting – have beenidentified and are or will be subject to areview. One example is Scania’s collabo-ration with a Finnish cable supplier,which will be responsible for delivery ofwiring to all Scania assembly plants world-wide and take an active part in productdevelopment.

Since the programme started, the num-ber of sub-contractors has been morethan halved.

During 1999, the Procurement and Industrial Development unit also workedwith an IT project aimed at integrationbetween the control systems at Scania’sproduction plants and those of the mostimportant sub-contractors. A commonnetwork is expected to go into operationduring 2000.

26

engines is focusing on additional improve-ments in environmental characteristicsand performance, in preparation for futureenvironmental standards. During 1999,Scania launched a broad range of low-emission engines for distribution and con-struction vehicles as well as for long haul-age. All engines fulfil the new Euro 3standard, which will be legally requiredfor new vehicles from 2001 onward. Scaniaalso unveiled a gas-powered engine thatcomplements its range of engines for al-ternative fuels.

During 1999, Scania introduced thesecond generation of electronically con-trolled disc brake systems, which allowautomatic adjustment of braking powerbetween the various truck axles and be-tween the tractor unit and the trailer. Thisachieves more uniform and safer brakingfor the entire vehicle and a longer servicelife for brake components.

tinuously and in good time of a vehicle’smaintenance and repair needs. This allowsmore efficient servicing procedures and ahigh degree of utilisation. Unplanned stop-pages can be avoided and service inputcan take place along the ordinary route of the vehicle.

As one element in this effort, in March1999 Scania established Scania Infotro-nics AB, a cutting-edge company in vehi-cle electronics. This company, operated inpartnership with Mecel AB, will designIT-based systems and functions where theycan create genuine customer benefit. Im-proved operating economy and logisticsas well as reduced environmental impactand greater road safety are prioritised de-velopment areas. Scania Infotronics alsostarted collaboration with the Ericsson tele-communications group to develop Internet-based solutions for the transport sector.

The task of further refining Scania’s

27

Scania’s conceptvehicle for the2010s shows thepotential for in-creased transportcapacity for heavytrucks in futuretraffic.

vehicles more intensively. This creates agreater need for service, despite the im-proved quality of the vehicles. Meanwhilehauliers are focusing to a greater extenton their core business, logistics.

The service-related market is morehighly developed in Europe than in Scania’sother markets. Owing to economic growth,deregulation of transport markets and theemergence of international transportcompanies, other markets are moving inthe same direction as European ones interms of customer and market structure.This also increases the demand for services.

Expanding the range of servicesDuring 1999, Scania continued to expandits range of services. The development ofnew services is strategically important toScania and takes place at Group level in

Greater demand for servicesThe service-related market continued togrow in importance as a proportion ofScania’s operations. Scania’s sales of serviceand parts rose 8 percent during the yearto SEK 6,945 m. (6,419). Service andmaintenance contract sales continued toincrease, especially in the most maturemarkets in Europe.

The deregulated, increasingly integrat-ed transport market in Europe is leadingto tougher competition among transportcompanies. These companies are demand-ing service packages that provide variousdegrees of total responsibility for the ve-hicle, financing, service and maintenance.

One importance reason for the expan-sion of the service-related market is theongoing change in customer structure.Major international operators are utilising

28

SERVICE-RELATED PRODUCTS

Scania is at the fore-front of developmentwork in fleet manage-ment, which aims atmore efficient utilisa-tion of customers’ vehicle fleets.

29

collaboration with local markets. Servicesare packaged by marketing companies tofit specific customer needs.

Scania’s service offering has shown verygood growth. An average of 25 percent ofnew truck sales in Europe include a serviceand maintenance and/or financing package.

As one element in its strategy of satis-fying the customer’s total transport needs,Scania initiated its Dealer OperatingStandards (DOS) project. The purpose ofthe project is to create a high common level of knowledge, quality and productivi-ty in Scania’s European service and distrib-ution network. The project includes 18markets, 1,000 local distributors and15,000 people. For example, it encom-passes uniform working methods andelapsed times for specified tasks. Custom-ers must receive the same high level ofservice from Scania no matter where theyare. During 1999, the project continuedand some fifty local distributors wereDOS certified. The target is to have eval-uated most dealerships according to DOSstandards by mid-2000.

One of Scania’s priority service areasis fleet management, which aims at makingcustomer utilisation of vehicle fleets moreefficient. During 1999, Scania launchedan innovative, flexible interface that ena-

bles existing fleet management systems inthe market to retrieve and process infor-mation from a Scania vehicle’s computernetwork, such as its fuel consumption.

In the future, an expanded range ofservices available via Internet and webtechnology will increase the availabilityof services for drivers on the road.

To assure customers the availability oftheir vehicle, for some years Scania hasoffered Scania Assistance. This service ena-bles customers to get help round the clock,every day of the year, in their own language.By means of regional call centres in a num-ber of locations around Europe, the Scaniaorganisation’s overall efforts are efficientlycoordinated in case of unplanned stoppages.

During the 1990s, Scania developed abusiness concept in which it assumes re-sponsibility for the customer’s access totransport capacity. Scania owns the ve-hicle and makes it available according tothe requirements of the transport assign-ment. Scania thus sells financing, mainte-nance and repairs as well as other servicessuch as administration and insurance.

Scania is successfully engaged in thetruck rental business. Used vehicles in itsinventory are also used for short-termrentals, thereby yielding revenues to Scaniawhile enabling the customer to handle peaks in transport demand.

Expanded organisationThe expansion of Scania’s sales and ser-vice organisation continued during 1999.In addition to acquiring its distributors inItaly, Norway, Finland and Latvia, Scaniainaugurated a new distribution and ser-vice unit in Poland, for example. Totalnet capital expenditures (acquisitions andnew facilities) in the European marketingorganisation amounted to SEK 1,600 m.during 1999.

Scania also expanded its independentdistribution and service network.

Scania Assistanceenables customers tominimise downtimeand get help roundthe clock, all yearround.

30

Lending volume continued to increase during 1999. This volume growth resultedfrom continued strong demand for Scania’sproducts and integrated financing services,combined with expansion in operationsduring 1999 due to acquisition of the Italian finance company.

Year-end 1999 financing volume amounted to SEK 15,300 m. (12,300). In unit terms, during the year 8,560 newtrucks, 220 new buses and 2,010 usedScania vehicles were financed.

Of the total loan portfolio, 40 percentconsisted of operating leases and 21 per-cent financial leases. The remaining 39percent represented loan financing. Thenumber of contracts in the portfolio atyear-end totalled about 33,000 (27,700).

The income of customer finance oper-ations totalled SEK 140 m. (91). This wasequivalent to an operating income of 1.01percent of the portfolio and represents asubstantial improvement from 0.89 per-cent in 1998.

The improved profit margin was main-ly due to a decline in overhead from 1.11percent to 0.94 percent of the portfolio.This was the result of economies of scaledue to increased lending volume.

The effect of credit losses on earningswas SEK –57 m (–44). Actual credit lossesduring 1999 amounted to SEK 53 m. (14).

The increase in actual credit losses du-ring 1999 was largely a direct consequence

of the write-offs for possible losses in eas-tern Europe during the year. At year-end,the total reserve for possible credit lossesamounted to SEK 212 m.

Total year-end receivables outstandingin central and eastern Europe (excludingPoland and the Czech Republic) was SEK560 m., of which 12 percent consisted ofreserved funds. Total reserved fundsamounted to 1.4 percent (1.7) of totallending volume.

Given its increased customer financeexposure, Scania must devote efforts tocontinuous credit evaluations and moni-toring of financed contracts. Scania’s totalcommitments are monitored at Group leveland risks are limited by establishing ceilingson exposure per country and customer.During 1999, Scania continued to strength-en its resources for credit evaluation.

During the year, human resource devel-opment efforts intensified. There werecontinuous exchanges of personnel, bothbetween finance companies and betweendifferent disciplines in Scania finance op-erations.

EuropeIn Europe, customer financing mainly takesplace through nine Scania-owned financecompanies that cover Great Britain, France,Germany, Italy, Belgium, Poland, the CzechRepublic and the Nordic region plus thecountries in central and eastern Europe.

In those markets where Scania pursuesfinance company operations, the propor-tion of trucks financed via its own financecompanies averaged 33 percent (36).

Scania’s strategy for its customer fi-nance operations is to work in local mar-kets around Europe, and thus close tocustomers. Working in an integrated way

CUSTOMER FINANCING

Customer financing provides an important contributionto Scania’s earnings and growth, both as a form of mar-keting and sales support for the company’s productsand owing to the profitability of the actual financingoperations. It also creates industrial synergies by in-creasing the sales of service-related products for thevehicles provided with financing contracts.

31

together with distributors results in localknow-how and proximity to the customer,which is a prerequisite for the decentralisedcredit management process that is applied.This system also creates opportunities fora high degree of customer adaptation andcustomer-oriented product development.

To a great extent, customer financingunder Scania’s own auspices is a prerequi-site for sales in central and eastern Europe.

Latin AmericaScania offers financing in Latin Americaprimarily on the basis of collaborationwith international lenders. Finance opera-tions under Scania’s own auspices grewduring 1999 but do not yet represent alarge enough volume to be separately re-ported.

0

3,000

6,000

9,000

12,000

15,000

SEK m.

9998979695

Total assets, finance companies

18,000

In the Brazilian market, Scania alsooffers a customer-financed savings pro-gramme, in which customers are organisedinto consortia. Through regular savingsin consortia, the customer is guaranteedthe allocation of a vehicle within a certainpredetermined period. During 1999, 42percent of sales in Brazil occurred viasuch financing. This form of financingstabilises vehicle sales during recessions.

Other marketsDuring the year, customer finance opera-tions under Scania’s own auspices wereestablished in South Korea. In 2000,continued expansion is planned, both viaan increased range of financial servicesand through efforts in new markets.

100

0

200

300

400

500

600

700

800

900

1,000

95 96 97 98 99

SEK m. Revenues

Revenues/Operating income,finance companies

Operating income

Scania offers the customer a package solution in which financing is often animportant component.

32

OUR EMPLOYEES

Trust – a prerequisite for“coordinated independence”Scania’s future success will depend on having skilled, motivated, responsible em-ployees who all pull in the same direction.

Coordinated independence is a guid-ing principle at Scania. Overall principlesand rules are drafted by all departments.This will enable the company to take ad-vantage of quality, productivity and flexi-bility in an effective way. Meanwhile it isimportant to delegate responsibility andauthority far down in the organisation.Scania relies on its employees to be will-ing and able to take responsibility for re-sults and growth.

Scania managers must motivateand develop other employeesNew conditions in the world around Scania are putting heavier demands onboth managers and other employees.Smoothly functioning leadership focusedon motivating, developing and rewardingScania’s employees is critical if Scania is

to remain competitive. This is why con-tinuous management development is needed.

Management development occurs in anumber of different ways at Scania. Projectwork, training and mobility of employeesbetween different operations and units areexamples of steps to improve the leadershipskills of executives and other managers.

During 1999, Scania invested heavilyin management training. A new internalprogramme in this field was developedand introduced. The focus of the pro-gramme is that personal leadership is based on self-awareness, communication,stress management and group develop-ment. During the year, about 250 man-agers and executives participated in va-rious activities in this programme, calledthe “basic management developmentblock”. In 1999, the programme was im-plemented in Swedish. The ambition is to internationalise it during 2000.

The Scania Marketing Academy is anacademically accredited training pro-gramme developed and implemented incollaboration with the Stockholm Schoolof Economics among others. Its purposeis to strengthen the business skills of Sca-nia’s marketing organisation, develop theleadership talents of individuals and en-hance Scania’s corporate culture. Twenty-five future and established managers in keypositions received certificates of comple-tion from the Scania Marketing Academyduring 1999.

Continuous human resource development is essential ifScania is to remain a competitive and profitable com-pany in the future.To make this possible, Scania mustoffer an attractive and effective workplace for demand-ing people.

Managers at Scania must motivate,develop and reward other employees.

33

In addition to the above-mentionedmanagement development activities, whichare initiated and coordinated at Group level,a large number of development activitiesoperate locally in different units.

Encouraging employees totake greater responsibilityScania’s employees are encouraged toseek new, future-oriented solutions totasks, take responsibility and make deci-sions on their own. Human resource de-velopment is supported by a number ofmethods, among them job enrichment,job rotation, training, project work andproject management.

The Scania Professional programmetrains employees from the distribution organisation in marketing, parts manage-ment and workshop services. This pro-gramme includes courses on Dealer Op-erating Standards (DOS) and in Scania’sservice offering. During 1999, 180 peoplewere trained at Scania Professional.

The internal Personnel Exchange Pro-gramme (PEP), in which employees workin another country within the Scania or-ganisation for up to one year, is an exam-ple of a programme designed to increasemobility between different operations andcountries. The scale of the programme in-creased during the year.

In 1999, employees at Scania partici-pated in an average of 14 days of trainingactivities. Internal mobility during theyear was about 15 percent.

Recruitment for continuedleadershipRecruitment is an essential element ofScania’s growth strategy and of its ambi-tion to be a technical development leaderin its product areas. During the year, Sca-nia continued its collaboration with edu-cational institutions in various countriesin research and development, recruitment

and trainee work. The industrial researchprogramme enables graduate engineers tocombine jobs at Scania with research atthe doctoral level.

Since 1941, Scania has operated atechnical upper secondary school next toits facility in Södertälje, Sweden. Scania-affiliated industrial schools are also foundin the Netherlands and Brazil.

Employee surveys:a key management toolDuring 1999, Scania conducted employeesurveys among employees of its develop-ment and procurement departments andelsewhere. These surveys covered suchmatters as working conditions, personaljob situation, job assignments and termsof employment.

Those employees who were involvedin newly started projects stated that theywere strongly positive to their job situa-tion. In areas where there is room for im-provement, processes of change havebeen started.

Bonus systems that motivateAs a result of the introduction of flexibleworking hours in 1996, there are variousearnings-based bonus systems at Scania.The amounts paid depend on predeter-mined delivery assurance and productivitytargets. In Sweden, funds are transferredto a foundation in which employees holda share. The foundation owned at year-end 0.3 percent of Scania’s shares.

Scania pays varying forms of earnings-based bonuses in different countries. InSweden and France, they measure deliveryassurance and productivity. In Latin America, they measure production, absen-teeism, market leadership, establishmentof teamwork and improvement efforts.

Number of employees(right-hand scale)

Number of vehicles produced (left-hand scale)

98 999796959493929190

Number of vehicles produced and employees, Latin American operations

0

1,000

2,000

3,000

4,000

5,000

0

5,000

10,000

15,000

Vehicles Employees

0

10,000

20,000

30,000

40,000

98 999796959493929190

Number of production employees (right-hand scale)

Number of vehicles produced (left-hand scale)

Number of vehicles produced andproduction employees, European operations

0

3,000

6,000

9,000

12,000

15,000

Vehicles Employees

34

SCANIA AND THE ENVIRONMENT

Environmental strategyEnvironmental work is integrated intoScania’s operations in the same way asquality, training and economic issues, forexample. The Scania Environmental Board,Environmental Committee and local envi-ronmental coordinators have advisoryand supportive roles throughout the Scaniaorganisation. The Environmental Board isthe highest decision-making body in its field and deals with issues of strategic im-portance to Scania. These then becomepart of Group decisions, regardless ofwhether they concern marketing, produc-tion or communications issues.

Management systemsScania’s entire industrial system works un-der an environmental management systemthat is certified according to ISO 14001international standards. Efforts have alsobegun to integrate the distribution sys-tem, in compliance with both ISO 9002

quality management and ISO 14001 en-vironmental management standards.

Reporting Since 1996, Scania has worked with Group-wide environmental objectives and tar-gets. During 1999, on the basis of Scania’senvironmental targets, environmental andfinancial managers have drafted commondefinitions and reporting procedures toimprove the reporting of environmentaleconomics. The first step was to focus oncosts and revenues in manufacturing op-erations. This work will continue, alsoembracing clearer definitions of environ-mentally related investments and R&D,as well as how large a proportion of totalsales can be related to products with thehighest level of environmental performance.

Research and developmentMost of a vehicle’s environmental impactoccurs during its service life. This is whyScania’s development and design work isdevoted to functional characteristics thatresult in improved fuel consumption andreduced exhaust emissions. More efficientengines and a reduction of weight as wellas rolling and air resistance are factors ofgreat importance to the final outcome.Aside from this, there is obviously room

Scania’s environmental work is an important element ofthe Scania brand name.Taking environmental aspectsinto account in day-to-day work is a natural task for everyemployee.The aim is to reduce the environmental im-pact of the company’s products throughout their life cycle:from development via manufacture, operation to finaldismantling.

By making it possi-ble to build largercombinations withbetter cargo capaci-ty, the total numberof vehicles on theroads can be re-duced by one third.

35

for environmental improvements throughcareful choice of materials and improve-ments in production processes.

Alternative fuelsThe main area of Scania’s developmentwork on alternative-fuel vehicles is buses,where there is already clear and stable demand today. The focus is primarily on ethanol and gaseous fuels.

One sixth of the city buses sold during1999 were powered by alternative fuels.This was equivalent to about 0.5 percentof Scania’s total sales.