Embed Size (px)

Citation preview

General Fund: Assets

Cash A200Cash in Time Deposits A201Petty Cash A210 Cash From Obligations A220Cash for Tax Anticipation Notes A221Cash for Revenue Anticipation Notes A222Cash With Fiscal Agent A223Cash, Special Reserves A230Cash in Time Deposits, Special Reserves A231Taxes Receivable, Current A250Taxes Receivable, Overdue A260Allowance for Uncollectible Taxes A342Accounts Receivable A380Allowance for Receivables A389Due From Other Funds A391Due From State and Federal A410Due From Other Governments A440 Inventory of Materials & Supplies (Optional) A445Investment in Securities A450Investment in Repurchase Agreements A451Investment in Securities, Special Reserves A452Investment in Repurchase Agreements, Special Reserves A453Mortgages Receivable A455Prepaid Expenditures A480

100 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

General Fund: Liabilities and Deferred Revenues

Accounts Payable A600Accrued Liabilities A601Tax Anticipation Notes Payable A620Revenue Anticipation Notes Payable A621Budget Notes Payable A622Bond Anticipation Notes Payable A626Bond Interest and Matured Bonds Payable A629Due To Other Funds A630Due To Other Governments A631Due To State Teachers’ Retirement System A632Due To Employees’ Retirement System A637Accrued Interest Payable A651Compensated Absences A687Overpayments A690Deferred Revenues A691Deferred Revenues - Planned Balance A692Deferred Revenues, Special Taxes, Suffolk Co. A693Deferred Tax Revenues (City) A694

ACCOUNT CODES 101

School District Account Codes

General Fund: Fund Balance

Workers’ Compensation Reserve A814Unemployment Insurance Reserve A815Reserve for Encumbrances A821Reserve for Retirement Contributions A827Reserve for Inventory of Materials/Supplies A845Reserve for Property Loss A861Reserve for Liability Claims A862Insurance Reserve A863Reserve for Tax Certiorari A864Reserve for Employee Benefi ts and Accrued Liabilities A867Reserve for Taxes Raised Outside Tax Limit (Cities Over 125,000) A874Capital Reserve A878Reserve for Repairs A882Mandatory Reserve A884Reserve for Tax Reduction A891Unreserved Appropriated Fund Balance (Next Year’s Budget) A910*Unappropriated Fund Balance A911*

* Reporting code only. Accounting entries will use code A909.

102 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

General Fund: Revenues

Local SourcesReal Property Taxes (Excludes STAR Revenue) A1001Appropriation of Planned Balance A1040Appropriation of Special Taxes (Suffolk Co) A1041Federal Payments in Lieu of Taxes A1080Other Payments in Lieu of Taxes A1081School Tax Relief Reimbursement A1085Interest and Penalties On Real Property Taxes A1090Tax On Consumer Utility Bills A1111Nonproperty Tax Distribution By Counties A1120

Gross Receipts Tax A1130Day School Tuition-Resident Nonveteran Postgrad Tuition (from Individuals)

A1310

Other Day School Tuition (from Individuals) A1311Continuing Education Tuition (from Individuals) A1315Summer School Tuition (from Individuals) A1320Textbook Charges (from Individuals) A1330Other Student Fee/Charges (from Individuals) A1335 Admissions (from Individuals) A1410Other Charges - Services (from individuals) A1489Data Processing for Other Districts and Governments A2228Day School Tuition - Other Districts in NYS A2230 Summer School Tuition - Other Districts in NYS A2232Services Provided for BOCES Other Than Transportation A2235Health Services for Other Districts A2280 Narcotic Control Service for Other Governments A2290Narcotic Control Service for BOCES A2291Transportation for Other Districts On Contract Buses A2304Transportation for Other Districts On District Owned or Operated Buses

A2304

Transportation for BOCES A2308Youth Services, Other Governments A2350Tuition from NYS for Native American Students who Reside on Reser-vations

A2389

Contractual Payments from NYS for Native American Student Trans-portation

A2389

Transportation Revenues for Non-resident Pre-K or DFY (Section 1709(25)(h) of Education Law)

A2389

Tuition - Districts in Other States A2395

ACCOUNT CODES 103

School District Account Codes

Other Misc Revenues – Districts in Other States A2395Interest and Earnings A2401Rental of Real Property, Individuals A2410Rental of Real Property, Other Governments A2412Rental of Real Property, BOCES A2413Rental of Equipment (Not Buses), Individuals A2414Rental of Equipment (Not Buses), Other Governments A2416Rental of Buses A2440Rental (Not Buses), Other (Specify) A2440Commissions A2450Forfeiture of Deposits A2620Sale of Scrap and Excess Materials A2650Minor Sales, Other (Specify) A2655Sale of Real Property A2660Sale of Equipment A2665Sale of Transportation Equipment A2666

Sale of Instructional Supplies A2670Insurance Recoveries -Transportation Related A2680Insurance Recoveries - Other A2680Self Insurance Recoveries A2683Other Compensation for Loss A2690Reimbursement of Medicare Part D Expenditures A2700Refund of Prior Years Expenses - BOCES Services Approved for Aid A2701Refund of Prior Years Expenses - Contracted Transportation (Including BOCES)

A2702

Refund of Prior Years Expenses - District Owned Transportation A2702Refund of Prior Years Expenses - Other-Not Transportation A2703Refund of Prior Years Expenses - Tuition for Spec Act District Ap-proved Private School Disabled

A2704

Gifts and Donations A2705Other Unclassifi ed Revenues A2770Refund of Transportation Contract Expense for Advertising on School Buses

A2770

Interfund Revenues A2801

State SourcesLoss of Public Utility Valuation A3017Real Property Tax Administration A3040

General Fund: Revenues

104 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Records Management A3060Rail Infrastructure Investment Act A3070Basic Formula Aid - General Aids (Excludes Excess Cost) (Section 3609a Education Law)

A3101

Basic Formula Aid - Excess Cost Aids Only (Excludes Charter Schools) (Section 3609b Education Law)

A3101

Basic Formula Aid - Excess Cost Aids for Charter Schools (Section 3609b Education Law)

A3101

Lottery Aid (Section 3609a Education Law) A3102BOCES Aid (Section 3609d Education Law) A3103Tuition for Students with Disabilities (Chapters 47, 66 and 721) A3104Transportation for Students with Disabilities in an ICF (Chapter 721) A3104

Sound Basic Education Aid A3106Textbook Aid (Including Textbook/Lottery Aid) A3260Special Aid for Small City School Districts A3261Computer Software Aid A3262Library A/V Loan Program Aid A3263Small Government Assistance A3265Other State Aid (Specify) A3289Youth Programs A3820Emergency Disaster Assistance (NYS Emergency Management Offi ce)

A3960

Federal SourcesFederally Affected Areas Operating Aid A4107Federally Affected Areas - Students with Disabilities A4108Other Federal Aid (Specify) A4289Medicaid Assistance-School Age-School Year Programs A4601Emergency Disaster Assistance (FEMA) A4960

Interfund Transfers and Proceeds of ObligationsInterfund Transfers (Other Than Debt Service) A5031Interfund Transfer for Debt Service A5050Term Bonds A5700Serial Bonds A5710Statutory Bonds A5720Bond Anticipation Notes A5730Capital Notes A5740Other Debt (Specify) A5789

General Fund: Revenues

ACCOUNT CODES 105

School District Account Codes

General SupportBoard of Education A1010.XXDistrict Clerk A1040.XXDistrict Meeting A1060.XXChief School Administrator A1240.XXBusiness Administration A1310.XXAuditing A1320.XXTreasurer A1325.XXTax Collector A1330.XXPurchasing A1345.XXFiscal Agent Fee A1380.4CLegal A1420.XXPersonnel A1430.XXRecords Management Offi cer A1460.XXPublic Information and Services A1480.XXOperation of Plant A1620.XXMaintenance of Plant A1621.XXCentral Storeroom A1660.XXCentral Printing and Mailing A1670.XXCentral Data Processing A1680.XXSpecial Items A1710.XXExcess Insurance A1722.4XUnallocated Insurance A1910.4CSchool Association Dues A1920.4CJudgment and Claims A1930.4CProperty Loss A1931.4CPurchase of Land/Right of Way A1940.4CAssessments on School Property A1950.4CRefund on Real Property Taxes A1964.4CBOCES Administrative Costs A1981.49BOCES Capital Expenses A1983.49Unclassifi ed A1989.4C

InstructionCurriculum Development and Supervision A2010.XXSupervision - Regular School A2020.XXSupervision - Special School A2040.XX

General Fund: Expenditures

106 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Research, Planning, and Evaluation A2060.XXInservice Training - Instruction A2070.XXTeaching - Regular School A2110.XXProgram for Students with Disabilities School Age - School Year A2250.XXOccupational Education (Grades 9-12) A2280.XXTeaching - Special Schools A2330.XXSchool Library and Audiovisual A2610.XXEducational Television A2620.XXComputer Assisted Instruction A2630.XXAttendance Regular School A2805.XXGuidance Regular School A2810.XXHealth Services Regular School A2815.XXPsychological Services Regular School A2820.XXSocial Work Services Regular School A2825.XXPupil Personnel Services Special Schools A2830.XXCo-Curricular Activities Regular School A2850.XXInterscholastic Athletics Regular School A2855.XX

TransportationDistrict Transportation Services A5510.XXGarage Building A5530.XXContract Transportation A5540.4CPublic Transportation A5550.4CTransportation from BOCES A5581.49

Community ServiceRecreation A7140.XXYouth Program A7310.XXCivic Activities A8060.XXCensus A8070.XX

Employee Benefi tsState Retirement A9010.8CTeachers’ Retirement A9020.8CSocial Security A9030.8CWorkers’ Compensation A9040.8CLife Insurance A9045.8CUnemployment Insurance A9050.8CDisability Insurance A9055.8CHospital, Medical and Dental Insurance A9060.8C

General Fund: Expenditures

ACCOUNT CODES 107

School District Account Codes

Union Welfare Benefi ts A9070.8COther, (Specify) A9089.8C

Debt ServiceTerm Bonds Principal - Public Library AL9700.6 Term Bonds Principal- School Construction A9701.6CTerm Bonds Principal - Bus Purchases A9702.6CTerm Bonds Principal- BOCES Construction A9703.6CTerm Bonds Principal - Other (Specify) A9700.6CSerial Bonds Principal- Public Library AL9710.6Serial Bonds Principal- School Construction A9711.6CSerial Bonds Principal- Bus Purchases A9712.6CSerial Bonds Principal- BOCES Construction A9713.6CSerial Bonds Principal- Real Property Tax Refund A9714.6CSerial Bonds Principal- Other (Specify) A9710.6CStatutory Bonds Principal - Public Library AL9720.6Statutory Bonds Principal - School Construction A9721.6CStatutory Bonds Principal - Bus Purchases A9722.6CStatutory Bonds Principal- BOCES Construction A9723.6CStatutory Bonds Principal- Real Property Tax Refund A9724.6CStatutory Bonds Principal - Other (Specify) A9720.6CBond Anticipation Notes Principal - Public Library AL9730.6Bond Anticipation Notes Principal- School Construction A9731.6CBond Anticipation Notes Principal - Bus Purchases A9732.6CBond Anticipation Notes Principal - BOCES Construction A9733.6CBond Anticipation Notes Principal - Other (Specify) A9730.6CCapital Notes Principal- Public Library AL9740.6Capital Notes Principal- School Construction A9741.6CCapital Notes Principal- Bus Purchases A9742.6CCapital Notes Principal- BOCES Construction A9743.6CCapital Notes Principal - Real Property Tax Refund A9744.6CCapital Notes Principal-Other (Specify) A9740.6CInstallment Purchase Debt Principal - Bus Purchases A9787.6CInstallment Purchase Debt Principal- State Aided Computer Hardware A9785.6CInstallment Purchase Debt Principal- Other (Specify) A9785.6COther Debt Principal (Specify) A9789.6CTerm Bonds Interest- Public Library AL9700.7

General Fund: Expenditures

108 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Term Bonds Interest- School Construction A9701.7CTerm Bonds Interest - Bus Purchases A9702.7CTerm Bonds Interest- BOCES Construction A9703.7CTerm Bonds Interest- Other (Specify) A9700.7CSerial Bonds Interest- Public Library AL9710.7Serial Bonds Interest- School Construction A9711.7CSerial Bonds Interest- Bus Purchases A9712.7CSerial Bonds Interest- BOCES Construction A9713.7CSerial Bonds Interest - Real Property Tax Refund A9714.7CSerial Bonds Interest - Other (Specify) A9710.7CStatutory Bonds Interest - Public Library AL9720.7Statutory Bonds Interest - School Construction A9721.7CStatutory Bonds Interest- Bus Purchases A9722.7CStatutory Bonds Interest- BOCES Construction A9723.7CStatutory Bonds Interest- Real Property Tax Refund A9724.7CStatutory Bonds Interest - Other (Specify) A9720.7CBond Anticipation Notes Interest - Public Library AL9730.7Bond Anticipation Notes Interest - School Construction A9731.7CBond Anticipation Notes Interest - Bus Purchases A9732.7CBond Anticipation Notes Interest- BOCES Construction A9733.7CBond Anticipation Notes Interest- Real Prop Tax Refund A9734.7CBond Anticipation Notes Interest- Other (Specify) A9730.7CCapital Notes Interest- Public Library AL9740.7Capital Notes Interest- School Construction A9741.7CCapital Notes Interest - Bus Purchases A9742.7CCapital Notes Interest- BOCES Construction A9743.7CCapital Notes Interest - Real Property Tax Refund A9744.7CCapital Notes Interest - Other (Specify) A9740.7CBudget Notes Interest A9750.7CTax Anticipation Notes Interest A9760.7CRevenue Anticipation Notes Interest A9770.7CInstallment Purchase Debt Interest- Bus Purchases A9787.7CInstallment Purchase Debt Interest- State Aided Computer Hardware A9785.7CInstallment Purchase Debt Interest- Other (Specify) A9785.7COther Debt Interest (Specify) A9789.7C

General Fund: Expenditures

ACCOUNT CODES 109

School District Account Codes

Interfund TransferTransfer To School Food Service Fund A9901.93Transfer To School Store Fund A9901.94Transfer To Special Aid Fund A9901.95Transfer To Debt Service Fund A9901.96Transfer To Capital Funds A9950.9C

General Fund: Expenditures

110 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Cash F200Cash in Time Deposits F201Accounts Receivable F380Due From Other Funds F391Due From State and Federal F410Prepaid Expenditures F480Other Assets (Specify) F489

Special Aid Fund: LiabilitiesAccounts Payable F600Accrued Liabilities F601Due To Other Funds F630Due To Other Governments F631Due To State Teachers’ Retirement System F632Due To Employees’ Retirement System F637Compensated Absences F687Other Liabilities (Specify) F689

Reserve for Encumbrances F821Unreserved Fund Balance - Appropriated F910*Unreserved Fund Balance - Unappropriated F911*

* Reporting code only. Accounting entries will use code F909.

Special Aid Fund: RevenuesReimbursement of Medicare Part D Expenditures F2700DOH-Chapter 428-Early Intervention Program F2770Section 4410 - 12 Month Preschool Programs F2770Other Local Revenues F2770Interfund Revenues F2801Employment Preparation Education Aid F3281Section 4408 - School Age July/August Program F3289Other State Aid F3289NCLB Title I Migrant Education F4110NCLB Title I Basic Grant F4126

Special Aid Fund: Assets

Special Aid Fund: Fund Balance

ACCOUNT CODES 111

School District Account Codes

NCLB Title V Innovative Program Strategies F4128NCLB Title IV Safe & Drug Free Schools F4129Individuals W/ Disabilities Education Act (IDEA) F4256Vocational Education F4277Other Federal Aid (Specify) F4289Medicaid Assistance F4601Workforce Investment Act F4791Interfund Transfers - Special Education (Section 4408 only) F5031Interfund Transfers F5031

Special Aid Fund: ExpendituresOperation of Plant F1620.XXMaintenance of Plant F1621.XXIndirect Cost (Undistributed) F1988.4CUnclassifi ed Expenditures (Specify) F1988.4CCurriculum Development and Supervision F2010.XXSupervision - Regular School F2020.XXSupervision - Special School F2040.XXResearch, Planning, and Evaluation F2060.XXInservice Training - Instruction F2070.XXTeaching - Regular School F2110.XXProgram for Students with Disabilities School Age - School Year F2250.XXProgram for Students with Disabilities - DOH - Chapter 428 - Early Intervention Program

F2251.XX

Program for Students with Disabilities - Preschool - 12 Month (Section 4410 Education Law)

F2252.XX

Program for Students with Disabilities School Age - July/August (Section 4408 Education Law)

F2253.XX

Teaching - Special Schools F2330.XXEmployment Preparation Education F2340.XXPre-Kindergarten Program (Do Not Include Students with Disabilities)

F2510.XX

School Library and Audiovisual F2610.XXEducational Television F2620.XXComputer Assisted Instruction F2630.XXAttendance Regular School F2805.XXGuidance Regular School F2810.XX

Special Aid Fund: Revenues

112 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Health Services Regular School F2815.XXPsychological Services Regular School F2820.XXSocial Work Services Regular School F2825.XXPupil Personnel Services Special Schools F2830.XXDistrict Transportation Services F5510.XXContract Transportation F5540.4CPublic Transportation F5540.4CTransportation Services from BOCES F5581.49.Workforce Investment Act F6293.XXWork Training F6320.XXWork Study F6322.XXCivic Activities F8060.XXTransfers to Other Funds F9901.9C

Special Aid Fund: Expenditures

ACCOUNT CODES 113

School District Account Codes

Cash C200Cash in Time Deposits C201Petty Cash C210Accounts Receivable C380Due From Other Funds C391Due From State and Federal C410Inventory of Materials & Supplies C445Surplus Food Inventory C446Purchased Food Inventory C446Other (Specify) C489

School Food Service Programs: LiabilitiesAccounts Payable C600Accrued Liabilities C601Due To Other Funds C630Due To Other Governments C631Due To Employees’ Retirement System C637

Compensated Absences C687Other (Specify) C689

School Food Service Programs: Fund BalanceReserve for Encumbrances C821Reserve for Inventory C845Unreserved Fund Balance - Appropriated C910*Unreserved Fund Balance - Unappropriated C911*

* Reporting code only. Accounting entries will use code C909.

School Food Service Programs: Assets

114 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

School Food Service Programs: RevenuesSale of Reimbursable Meals (Total) C1440Other Cafeteria Sales C1445Interest and Earnings C2401Sale of Equipment C2665Compensation for Loss C2690Reimbursement of Medicare Part D Expenditures C2700Refunds of Prior Years Expenditures C2701Gifts and Donations C2705Misc. Revenues from Local Sources (Specify) C2770State Reimbursement C3190Federal Reimbursement (Excl Surplus Food) C4190Federal Reimbursement - Surplus Food Only C4190Summer Food Service Program for Children C4192Transfer From General Fund C5031

School Food Service Programs: Expenditures

School Food Service C2860.XXState Retirement C9010.8CTeachers’ Retirement C9020.8CSocial Security C9030.8CWorkers’ Compensation C9040.8CLife Insurance C9045.8CUnemployment Insurance C9050.8CDisability Insurance C9055.8CHospital, Medical and Dental Insurance C9060.8CInterfund Transfers C9901.9C

ACCOUNT CODES 115

School District Account Codes

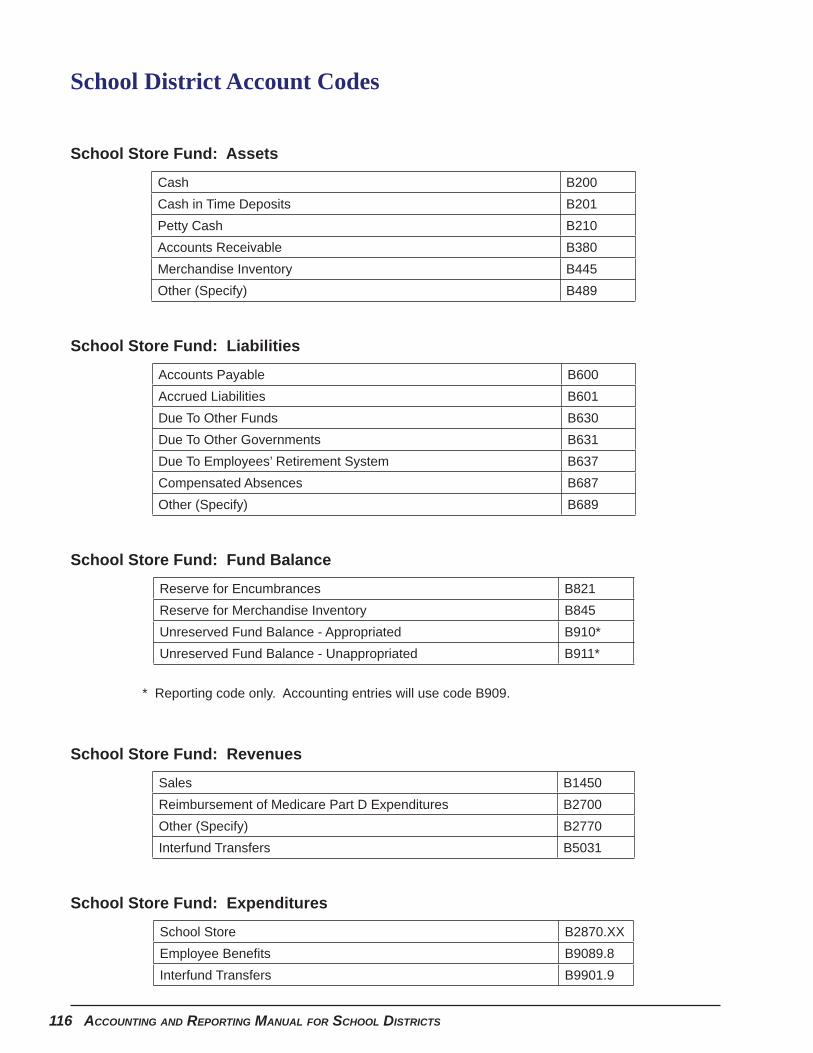

School Store Fund: Assets

Cash B200Cash in Time Deposits B201Petty Cash B210Accounts Receivable B380Merchandise Inventory B445Other (Specify) B489

School Store Fund: Liabilities

Accounts Payable B600Accrued Liabilities B601Due To Other Funds B630Due To Other Governments B631Due To Employees’ Retirement System B637 Compensated Absences B687Other (Specify) B689

School Store Fund: Fund Balance

Reserve for Encumbrances B821Reserve for Merchandise Inventory B845Unreserved Fund Balance - Appropriated B910*Unreserved Fund Balance - Unappropriated B911*

* Reporting code only. Accounting entries will use code B909.

School Store Fund: Revenues

Sales B1450Reimbursement of Medicare Part D Expenditures B2700Other (Specify) B2770Interfund Transfers B5031

School Store Fund: Expenditures

School Store B2870.XXEmployee Benefi ts B9089.8CInterfund Transfers B9901.9C

116 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Public Library Fund: Assets

Cash L200Cash in Time Deposits L201Petty Cash L210Accounts Receivable L380Due From Other Funds L391Investment in Securities L450Other (Specify) L489

Public Library Fund: Liabilities

Accounts Payable L600Accrued Liabilities L601Due To Employees’ Retirement System L637Compensated Absences L687Other (Specify) L689

Public Library Fund: Fund Balance

Reserve for Encumbrances L821Unreserved Fund Balance - Appropriated L910*Unreserved Fund Balance - Unappropriated L911*

* Reporting code only. Accounting entries will use code L909.

ACCOUNT CODES 117

School District Account Codes

Public Library Fund: Revenues

Real Property Taxes L1001Library Services for Free Assoc. Libraries L2080Library Charges L2082Library Services, Other Governments L2360Interest and Earnings L2401Rental of Real Property L2410Rental of Real Property, Other Governments L2412Commissions L2450Sales of Scrap and Excess Materials L2650Sales of Equipment L2665Sales of Instructional Supplies L2670Insurance Recoveries L2680Other Compensation for Loss L2690Reimbursement for Medicare Part D Expenditures L2700Refunds of Prior Years Expenditures L2701Gifts and Donations L2705Library System Grant L2760Unclassifi ed Revenues (Specify) L2770 State Aid for Libraries L3840Federal Aid for Libraries L4840Interfund Transfers L5031

Public Library Fund: Expenditures

Public Library L7410.XXState Retirement L9010.8CSocial Security L9030.8CWorkers’ Compensation L9040.8CLife Insurance L9045.8CHospital, Medical and Dental Insurance L9060.8COther (Specify) L9089.8CTransfers To Other Funds L9901.9CTransfer To Capital Projects Funds L9950.9C

118 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Cash V200Cash in Time Deposits V201Cash With Fiscal Agent V223Cash, Special Reserves V230Cash in Time Deposits, Special Reserves V231Accounts Receivable V380Due From Other Funds V391Deposits in State Sinking Fund V397Investment in Securities V450Investment in Repurchase Agreements V451Investment in Securities, Special Reserve Funds V452Investment in Repurchase Agreements, Special Reserve Funds V453Other (Specify) V489

Debt Service Fund: Liabilities

Term Bonds Payable V623Bond Interest and Matured Bonds Payable V629Due To Other Funds V630Accrued Interest Payable V651Other (Specify) V689

Debt Service Fund: Fund Balance

Mandatory Reserve V884Unreserved Fund Balance - Appropriated V910*Unreserved Fund Balance - Unappropriated V911*

* Reporting code only. Accounting entries will use code V909.

Debt Service Fund: Revenues

Interest and Earnings V2401Sale of Real Property V2660Premium on Obligations V2710Interfund Transfer From General Fund (A9901.96) V5031Interfund Transfers, Other (Specify) V5032Proceeds of Advanced Refunding Bonds V5791

Debt Service Fund: Assets

ACCOUNT CODES 119

School District Account Codes

Debt Service Fund: Expenditures

Fiscal Agent Fees V1380.4 Debt Service: PrincipalTerm Bonds - Public Library VL9700.6Term Bonds - School Construction V9701.6CTerm Bonds - Bus Purchases V9702.6CTerm Bonds - BOCES Construction V9703.6 Term Bonds - Other (Specify) V9700.6CSerial Bonds - Public Library VL9710.6Serial Bonds - School Construction V9711.6CSerial Bonds - Bus Purchases V9712.6CSerial Bonds - BOCES Construction V9713.6CSerial Bonds - Refund of Real Property Taxes V9714.6CSerial Bonds - Other (Specify) V9710.6CStatutory Bonds - Public Library VL9720.6Statutory Bonds - School Construction V9721.6CStatutory Bonds - Bus Purchases V9722.6CStatutory Bonds - BOCES Construction V9723.6CStatutory Bonds - Refund of Real Property Taxes V9724.6CStatutory Bonds - Other (Specify) V9720.6CBond Anticipation Notes - Public Library VL9730.6Bond Anticipation Notes - School Construction V9731.6CBond Anticipation Notes - Bus Purchases V9732.6CBond Anticipation Notes - BOCES Construction V9733.6CBond Anticipation Notes - Other (Specify) V9730.6CCapital Notes - Public Library VL9740.6Capital Notes - School Construction V9741.6CCapital Notes - Bus Purchases V9742.6CCapital Notes - BOCES Construction V9743.6CCapital Notes - Refund of Real Property Taxes V9744.6CCapital Notes - Other (Specify) V9740.6CInstallment Purchase Debt - Bus Purchases V9787.6CInstallment Purchase Debt - State Aided Computer Hardware V9785.6CInstallment Purchase Debt - Other (Specify) V9785.6COther Debt (Specify) V9789.6CTotal Principal V9798.6C

120 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Debt Service: Interest Term Bonds - Public Library VL9700.7Term Bonds - School Construction V9701.7CTerm Bonds - Bus Purchases V9702.7CTerm Bonds - BOCES Construction V9703.7CTerm Bonds - Other (Specify) V9700.7CSerial Bonds - Public Library VL9710.7Serial Bonds - School Construction V9711.7CSerial Bonds - Bus Purchases V9712.7CSerial Bonds - BOCES Construction V9713.7CSerial Bonds - Real Property Taxes V9714.7CSerial Bonds - Other (Specify) V9710.7CStatutory Bonds - Public Library VL9720.7Statutory Bonds - School Construction V9721.7CStatutory Bonds - Bus Purchases V9722.7CStatutory Bonds - BOCES Construction V9723.7CStatutory Bonds - Refund of Real Property Taxes V9724.7CStatutory Bonds - Other (Specify) V9720.7CBond Anticipation Notes - Public Library VL9730.7Bond Anticipation Notes - School Construction V9731.7CBond Anticipation Notes - Bus Purchases V9732.7CBond Anticipation Notes - BOCES Construction V9733.7CBond Anticipation Notes - Real Property Tax Refund V9734.7CBond Anticipation Notes - Other (Specify) V9730.7CCapital Notes - Public Library VL9740.7Capital Notes - School Construction V9741.7CCapital Notes - Bus Purchases V9742.7CCapital Notes - BOCES Construction V9743.7CCapital Notes - Refund of Real Property Tax V9744.7CCapital Notes - Other (Specify) V9740.7CInstallment Purchase Debt - Bus Purchases V9787.7CInstallment Purchase Debt - State Aided Computer Hardware V9785.7CInstallment Purchase Debt - Other (Specify) V9785.7C

Other Debt (Specify) V9789.7CTotal Interest V9798.7CInterfund Transfers V9901.9CPayment to Escrow Agent (Advanced Refunding Bonds) V9991.4C

Debt Service Fund: Expenditures

ACCOUNT CODES 121

School District Account Codes

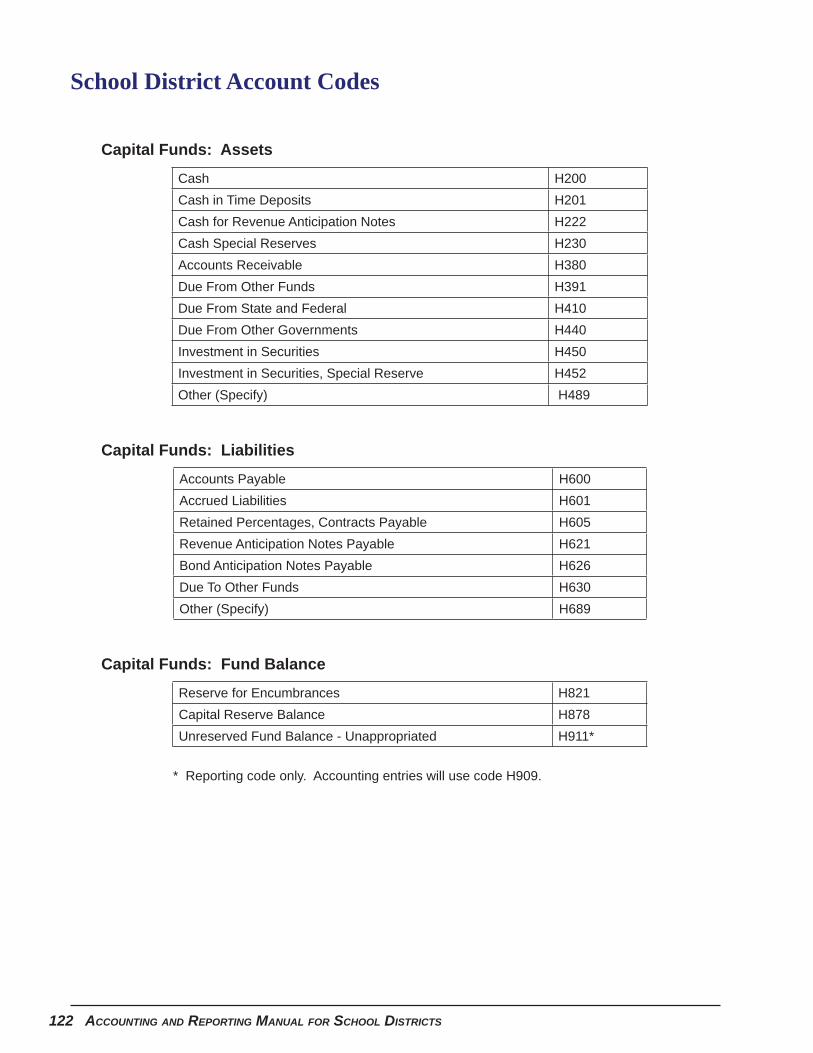

Capital Funds: Assets

Cash H200Cash in Time Deposits H201Cash for Revenue Anticipation Notes H222Cash Special Reserves H230Accounts Receivable H380Due From Other Funds H391Due From State and Federal H410Due From Other Governments H440Investment in Securities H450Investment in Securities, Special Reserve H452Other (Specify) H489

Capital Funds: Liabilities

Accounts Payable H600Accrued Liabilities H601Retained Percentages, Contracts Payable H605Revenue Anticipation Notes Payable H621Bond Anticipation Notes Payable H626Due To Other Funds H630Other (Specify) H689

Capital Funds: Fund Balance

Reserve for Encumbrances H821Capital Reserve Balance H878Unreserved Fund Balance - Unappropriated H911*

* Reporting code only. Accounting entries will use code H909.

122 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Capital Funds: Revenues

Interest and Earnings H2401Insurance Recoveries H2680Gifts and Donations H2705Other Miscellaneous (Specify) H2770 State Sources, RESCUE Aid H3297State Sources, Other (Specify) H3297Federal Sources, (Specify) H4297Interfund Transfer from General Fund H5031Interfund Transfers, Other (Specify) H5031Term Bonds H5700Serial Bonds H5710Statutory Installment Bond H5720Bond Anticipation Notes H5730Bond Anticipation Notes Redeemed from Appropriations H5731Capital Notes H5740Installment Purchase Debt H5785Other Debt H5789

Capital Funds: Expenditures

Buildings H1620.292General Construction (Incl HVAC, Plumbing, Electric, Site Imp, & Utility & Service)

H1620.293

Maintenance of Plant H1621.200Land H1940.291Regular School Furniture, Equipment, Textbooks H2110.200Superintendent of Construction or Clerk of Works H2110.201Contractual and Other (Incl Architecture, Legal, Engineering, and Insurance)

H2110.240

Interest H2110.270Buses H5510.210Transfers to General Fund H9901.9CCTransfers to Debt Service Fund H9901.96C

ACCOUNT CODES 123

School District Account Codes

Cash TA200Cash in Time Deposits TA201Accounts Receivable TA380Due from Other Funds TA391Investment in Securities TA450Investment in Repurchase Agreements TA451Securities and Mortgages TA455Accrued Interest On Securities Acquired TA456Personal Property TA457Real Property TA458Cash and Securities with Deferred Compensation Plan Pro-vider

TA460

Other (Specify) TA489

Agency Funds: Liabilities

Consolidated Payroll TA10Deferred Compensation TA17State Retirement TA18Disability Insurance TA19Group Insurance TA20New York State Income Tax TA21Federal Income Tax TA22Income Executions TA23Association and Union Dues TA24U.S. Savings Bonds TA25Social Security Tax TA26Teachers’ Retirement Loan TA27New York City Income Tax TA28Employee Annuities TA29Guaranty and Bid Deposits TA30Court Order Deposits TA36Student Deposits TA38Former District Monies TA70Due To Other Funds TA630Other Liabilities (Specify) TA85

Agency Funds: Assets

124 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Permanent Fund: Assets

Cash PN200Cash in Time Deposits PN201Cash, Special Reserves PN230Cash in Time Deposits, Special Reserves PN231Investment in Securities PN450Investment in Repurchase Agreements PN451Investment in Securities, Special Reserves PN452Investment in Repurchase Agreements, Special Reserves PN453Other (Specify) PN489

Permanent Fund: Liabilities

Accounts Payable PN600Other Liabilities PN688

Permanent Fund: Fund Balance

Appropriated Fund Balance PN910*Unappropriated Fund Balance PN911*

* Reporting code only. Accounting entries will use code PN909.

Permanent Fund: Revenues

Interest and Earnings PN2401Gifts and Donations PN2705Other (Specify) PN2770

Permanent Fund: Expenditures

Personal Services PN2989.1Contractual and Other PN2989.4

ACCOUNT CODES 125

School District Account Codes

Cash CM200Cash in Time Deposits CM201Cash, Special Reserves CM230Cash in Time Deposits, Special Reserves CM231Investment in Securities CM450Investment in Repurchase Agreements CM451Investment in Securities, Special Reserves CM452Investment in Repurchase Agreements, Special Reserves CM453Other (Specify) CM489

Miscellaneous Special Revenue Fund: Liabilities

Accounts Payable CM600Other Liabilities CM688

Miscellaneous Special Revenue Fund: Fund Balance

Appropriated Fund Balance CM910*Unappropriated Fund Balance CM911*

* Reporting code only. Accounting entries will use code CM909.

Miscellaneous Special Revenue Fund: Revenues

Interest and Earnings CM2401Gifts and Donations CM2705Other (Specify) CM2770

Miscellaneous Special Revenue Fund: Expenditures

Personal Services CM2989.1Contractual and Other CM2989.4

Miscellaneous Special Revenue Fund: Assets

126 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

School District Account Codes

Private Purpose Trust Fund: Assets

Cash TE200Cash in Time Deposits TE201Cash, Special Reserves TE230Cash in Time Deposits, Special Reserves TE231Investment in Securities TE450Investment in Repurchase Agreements TE451Investment in Securities, Special Reserves TE452Investment in Repurchase Agreements, Special Reserves TE453Other (Specify) TE489

Private Purpose Trust Fund: Liabilities

Accounts Payable TE600Other Liabilities TE688

Private Purpose Trust Fund: Net Assets

Restricted for Other Purposes TE923Non Restricted for Other Purposes TE924

Private Purpose Trust Fund: Revenues

Interest and Earnings TE2401Gifts and Donations TE2705Other (Specify) TE2770

Private Purpose Trust Fund: Expenditures

Personal Services TE2989.1Contractual and Other TE2989.4

ACCOUNT CODES 127

School District Account Codes

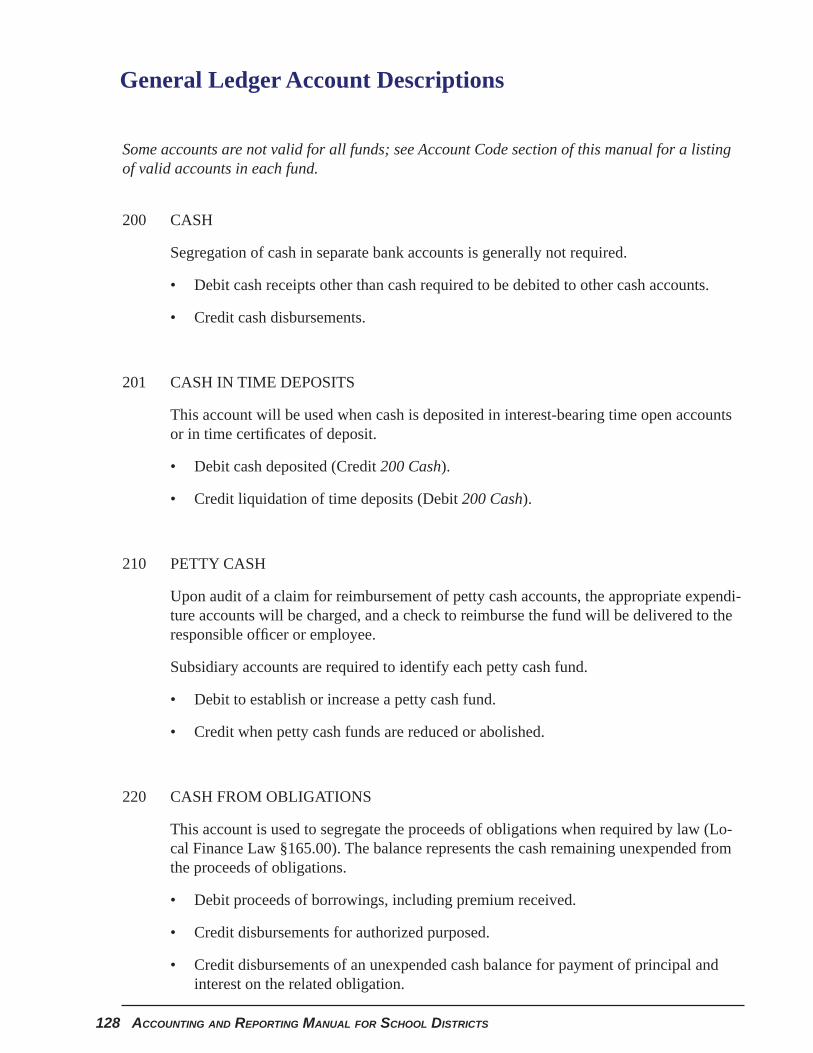

Some accounts are not valid for all funds; see Account Code section of this manual for a listing of valid accounts in each fund.

200 CASH

Segregation of cash in separate bank accounts is generally not required.

Debit cash receipts other than cash required to be debited to other cash accounts.

Credit cash disbursements.

201 CASH IN TIME DEPOSITS

This account will be used when cash is deposited in interest-bearing time open accounts or in time certifi cates of deposit.

Debit cash deposited (Credit 200 Cash).

Credit liquidation of time deposits (Debit 200 Cash).

210 PETTY CASH

Upon audit of a claim for reimbursement of petty cash accounts, the appropriate expendi-ture accounts will be charged, and a check to reimburse the fund will be delivered to the responsible offi cer or employee.

Subsidiary accounts are required to identify each petty cash fund.

Debit to establish or increase a petty cash fund.

Credit when petty cash funds are reduced or abolished.

220 CASH FROM OBLIGATIONS

This account is used to segregate the proceeds of obligations when required by law (Lo-cal Finance Law §165.00). The balance represents the cash remaining unexpended from the proceeds of obligations.

Debit proceeds of borrowings, including premium received.

Credit disbursements for authorized purposed.

Credit disbursements of an unexpended cash balance for payment of principal and interest on the related obligation.

•

•

•

•

•

•

•

•

•

128 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

General Ledger Account Descriptions

221 CASH FOR TAX ANTICIPATION NOTES

The balance in this account represents the amount set aside for the payment of tax antici-pation notes. A columnar analysis of the account should be maintained which will show separately the cash applicable to each year of tax levy concerned.

Debit collections of taxes when they must be set aside for payment of tax anticipation notes, pursuant to Local Finance Law §24.00.

Credit disbursements for redemption of notes within the limitation of the debit bal-ance of this account. Cash in this account will not be used for payment of interest on notes.

222 CASH FOR REVENUE ANTICIPATION NOTES

The balance represents the amount set aside for payment of revenue anticipation notes.

Debit collections of revenues when they must be set aside for redemption of notes, pursuant to Local Finance Law §25.00.

Credit disbursements for redemption of revenue anticipation notes within the limita-tion of the debit balance of this account. Cash in this account will not be used for payment of interest on notes.

223 CASH WITH FISCAL AGENT

The balance in this account represents amounts held by the fi scal agent for payment on principal and interest on outstanding obligations. The balance should agree with the bal-ance in 629 Bond Interest and Matured Bonds Payable, and should be reconciled with the bank account.

Debit deposits in banks acting as paying agents to pay bond principal and interest on due dates (Credit 629 Bond Interest and Matured Bonds Payable).

Credit upon notifi cation of payment by the fi scal agent.

•

•

•

•

•

•

GENERAL LEDGER ACCOUNT DESCRIPTIONSS 129

General Ledger Account Descriptions

230 CASH, SPECIAL RESERVES

This account is used to record cash transactions of special reserve funds. An analysis or a subsidiary account should be maintained to segregate the cash balance of each special reserve fund.

Debit cash receipts required to be deposited to reserve funds.

Credit purchase price of special reserve investments, including commissions.

Credit disbursements for authorized purposes (Debit 522 Expenditures - Subsidiary XXX).

231 CASH IN TIME DEPOSITS, SPECIAL RESERVES

This account will be used when reserve fund cash is deposited in interest-bearing time open accounts or in time certifi cates of deposit.

Debit cash deposited (Credit 230 Cash, Special Reserves).

Debit interest earned and remaining on deposit in time deposits (Credit 980 Revenues - Subsidiary XXX)

Credit liquidation of time deposits (Debit 230 Cash, Special Reserves).

250 TAXES RECEIVABLE, CURRENT

This account will be used to record the total real property taxes receivable. Collections and reductions will be posted to this account to enable the school district offi cials to read-ily determine the amount of unpaid taxes. Do not include interest received from collector or county treasurer.

Debit total real property taxes on the roll.

Credit amount of tax collections.

Credit reductions of taxes by the board of education, by the county legislature or by court order.

Credit amount received from the county treasurer for unpaid taxes returned (Non-city school districts only.)

Credit amount of taxes transferred to account 260 Taxes Receivable, Overdue when unpaid taxes are transmitted to the enforcement offi cer. (City school districts).

Credit amount of taxes on State lands not received by June 30 (Debit 260 Taxes Re-ceivable, Overdue).

•

•

•

•

•

•

•

•

•

•

•

•

130 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

General Ledger Account Descriptions

260 TAXES RECEIVABLE, OVERDUE

This account will be used by city school districts when the tax warrant has expired and the unpaid taxes have been turned over to the tax enforcement offi cer. It will also be used by any district where taxes on State lands are unpaid at June 30.

Subsidiary records shall be kept by the year of levy.

Debit amount of uncollected taxes transferred from account 250 Taxes Receivable, Current.

Debit amount of interest added to taxes returned to the proper enforcement offi cer (Credit 980 Revenues).

Credit amount of delinquent taxes received from the tax enforcement offi cer. Amounts received from the enforcement offi cer representing additional interest shall be credited to account 980 Revenues, 1090 Interest and Penalties on Real Property Taxes.

Credit upon receipt of payment of taxes on State lands.

Credit reduction of taxes by court order or by the board of education (Debit 342 Al-lowance for Uncollectible Taxes; only for city school districts).

342 ALLOWANCE FOR UNCOLLECTIBLE TAXES (Credit Account, City School District Only)

This account (credit balance) is used to provide an allowance for real property taxes deemed to be uncollectible. The account is deducted from 260 Taxes Receivable, Over-due on the balance sheet to arrive at the net amount of taxes receivable.

Credit amount of taxes which are estimated to be uncollectible (Debit 250 Taxes Re-ceivable, Current).

Debit reductions or cancellations of taxes.

380 ACCOUNTS RECEIVABLE

This is one of several general ledger accounts used to record amounts due the school dis-trict. A subsidiary record should be maintained for each debtor.

Debit amount receivable from individuals for tuition, claims for damages, etc. (Credit 980 Revenues; 389 Allowance for Receivables; or 691 Deferred Revenues).

•

•

•

•

•

•

•

•

GENERAL LEDGER ACCOUNT DESCRIPTIONSS 131

General Ledger Account Descriptions

Credit cancellations and adjustments authorized by the board of education (Debit 389 Allowance for Receivables; 980 Revenues; or 691 Deferred Revenues).

Credit collections of accounts receivable.

389 ALLOWANCE FOR RECEIVABLES (Credit Account)

This account (credit balance) is provided to record an estimate of accounts receivable which will never be collected.

Credit receivable estimated to be uncollectible at the time billed.

Debit cancellations or downward adjustment.

391 DUE FROM OTHER FUNDS

An analysis of this account will be maintained to show the amounts due from each fund. Subsidiary accounts shall be maintained by fund.

Debit charges to other funds.

Credit payments by other funds.

410 DUE FROM STATE AND FEDERAL

The debit balance will show the amount of aid or reimbursement receivable from the State or Federal government. Adjustments to this account should be supported by adjust-ment memoranda or correspondence from the agencies concerned.

Debit accrual of aid for reimbursement of expenditures.

Debit upward adjustments upon advice that aid or reimbursement was underclaimed.

Credit aid and reimbursements received which were previously accrued.

Credit rejections or deductions on claims upon advice that aid or reimbursement was overclaimed (Debit 980 Revenues)

•

•

•

•

•

•

•

•

•

•

132 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

General Ledger Account Descriptions

440 DUE FROM OTHER GOVERNMENTS

The balance will represent the amount due from other governments. Subsidiary accounts will be maintained.

Debit claims submitted to, or amounts due from, other governments for reimburse-ments of the cost of services or care.

Credit receipts from other governments in payment of claims.

445 INVENTORY

This account may be used to record bulk purchases. The balance represents the value of materials in inventory. The balance of this account should not exceed the balance of ac-count 845 Reserve for Inventory.

Debit cost of inventory purchased.

Debit cost of material returned to stock.

Debit overage when a physical count of inventory exceeds the book inventory (Credit 980 Revenues, Subsidiary 2770 (specify)).

Credit cost of items taken from stock (Debit 522 Expenditures).

Credit reduction of inventory when a physical count discloses that the book fi gure exceeds the actual stock on hand (Debit 522 Expenditures, Subsidiary 1989.4 Unclassifi ed).

450 INVESTMENT IN SECURITIES

This account will be used to record investments in securities, other than certifi cates of de-posit, special time deposits, repurchase agreements, and securities purchased from reserve funds.

The record of investments required by General Municipal Law, Section 10 will serve as the subsidiary for this account and other investment accounts.

Debit purchase price of securities, including commissions.

Credit purchase price upon sale, liquidation or maturity of the securities. Any excess over the purchase price will be credited to 980 Revenues - 2401 Interest and Earnings.

•

•

•

•

•

•

•

•

•

GENERAL LEDGER ACCOUNT DESCRIPTIONSS 133

General Ledger Account Descriptions

451 INVESTMENT IN REPURCHASE AGREEMENTS

This account will be used to record investments in repurchase agreements for all moneys other than those of special reserves.

Debit purchase price of securities.

Credit purchase price upon resale of the securities. Any excess over the purchase price will be credited to 980 Revenues - 2401 Interest and Earnings.

452 INVESTMENT IN SECURITIES, SPECIAL RESERVES

This account will be used to record investments of reserve moneys in securities other than certifi cates of deposit, special time deposits, and repurchase agreements.

Debit purchase price of securities, including commissions.

Credit purchase price upon sale, liquidation or maturity of the securities. Any excess over the purchase price will be credited to 980 Revenues - 2401 Interest and Earnings.

453 INVESTMENT IN REPURCHASE AGREEMENTS, SPECIAL RESERVES

This account will be used to record investment of special reserve moneys in repurchase agreements.

Debit purchase price of securities.

Credit purchase price upon resale of the securities. Any excess over the purchase price will be credited to 980 Revenues - 2401 Interest and Earnings.

480 PREPAID EXPENDITURES

This account may be used when items are purchased for the benefi t of future periods (i.e., insurance coverage, rent, etc.). Also use this account when purchase orders for books and supplies for the ensuing fi scal year are made in the spring and are delivered before the beginning of the ensuing fi scal year.

Debit expenditures made for items which will benefi t future periods.

Debit the amount of orders fi lled for the ensuing fi scal year (Credit 600 Accounts Payable).

Credit as expenditures are incurred (Debit 522 Expenditures).

•

•

•

•

•

•

•

•

•

134 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

General Ledger Account Descriptions

510 ESTIMATED REVENUES

This account is one of several budgetary accounts which will be used to record and sum-marize budgetary actions. It will not be used to record actual revenues. Details will be recorded in the subsidiary revenue ledger.

Debit aggregate of estimated revenues, including real property taxes.

Debit excess revenue appropriated to meet additional appropriations or increase existing appropriations.

Credit reduction in estimated revenues upon determination of the governing board that actual revenues will not equal estimated revenues. A corresponding reduction will be made in appropriations.

Credit to close (Debit 960 Appropriations).

511 APPROPRIATED RESERVES

This account will be used solely for budgetary entries. An analysis of the account should be maintained to segregate the amounts appropriated from each special reserve.

Debit special reserves appropriated in the adopted budget or in subsequent budget modifi cations (Credit 960 Appropriations).

Credit to close (Debit 960 Appropriations).

521 ENCUMBRANCES

Encumbrances are obligations in the form of purchase orders or contracts. A portion of the appropriation is reserved at the time orders are placed and contracts approved, and prior to the actual expenditure of funds.

The balance represents the total outstanding encumbrances; the details will be maintained in the subsidiary appropriation ledger. The balance before closing shall agree with the balance of 821 Reserve for Encumbrances.

Debit encumbrances outstanding at the end of the preceding fi scal year (Credit 909 Fund Balance).

Debit encumbrances placed (Credit 821 Reserve for Encumbrances).

Credit encumbrances liquidated upon payment of vouchers or cancellation of unneeded encumbrances (Debit 821 Reserve for Encumbrances).

Credit to close (Debit 909 Fund Balance).

•

•

•

•

•

•

•

•

•

•

GENERAL LEDGER ACCOUNT DESCRIPTIONSS 135

General Ledger Account Descriptions

522 EXPENDITURES

Details of this account shall be maintained in the subsidiary appropriation-expenditure ledger.

Debit amount of claims, vouchers and payrolls paid or accrued, include expenditures of special reserves.

Debit amount withheld from State aid representing the district’s contribution to the retirement system.

Debit at the end of the fi scal year with the amount of outstanding claims and the ac-crual of expenditures.

Debit when the County Vocational Education and Extention Board or BOCES re-ceives State aid which is used to reduce the charges for services to be paid by the district (Credit 980 Revenues).

Debit when BOCES settlement is accrued for defi cit (Credit 601 Accrued Liabilities).

Credit the amounts of voided checks of the current year for expenditures initially charged to this account.

Credit when BOCES settlement is accrued for surplus (Debit 440 Due from Other Governments).

Credit refunds of expenditures of the current year.

Credit closing entry to the appropriate fund balance account.

530 OBLIGATIONS AUTHORIZED

This account will be used solely for budgetary entries. The balance will represent the net amount of obligations authorized to fi nance appropriations of the current year.

Debit budget notes or other obligations authorized by the fi nance board (Credit 960 Appropriations).

Credit authorizations rescinded by the fi nance board (Debit 960 Appropriations).

Credit to close (Debit 960 Appropriations).

•

•

•

•

•

•

•

•

•

•

•

•

136 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

General Ledger Account Descriptions

599 APPROPRIATED FUND BALANCE

This is a budgetary account.

Debit estimated fund balance appropriated in the adopted budget or in the subsequent modifi cations (Credit 960 Appropriations).

Credit reduction by the governing body in the appropriation of fund balance when it is determined that the amount appropriated exceeds the actual amount available (Debit 960 Appropriations).

Credit to close (Debit 960 Appropriations).

600 ACCOUNTS PAYABLE

This account will be used to record liabilities due private persons, fi rms or corporations for goods or services received.

Credit the accrued claims, vouchers, judgments, court orders or other instruments of expenditures due person or fi rms for materials received or services performed (Debit 522 Expenditures).

Debit amounts liquidated.

601 ACCRUED LIABILITIES

This account will be used at the closes of the fi scal year to accrue the liability for ex-penditures chargeable to the current fi scal year but which are not due and payable until the following fi scal year. Expenditures for which vouchers or bills have been received should be credited to 600 Accounts Payable, 630 Due to Other Funds, or 631 Due to Other Governments according to the character of the vendor (i.e., commercial, interfund or other government).

Credit with the accrued (prorated amount chargeable to the current year) payrolls remaining unpaid at the end of the fi scal year.

Credit employer’s share of employees’ benefi ts chargeable to the current year.

Debit in the following year with amounts actually paid.

Debit liquidation of unneeded balances (Credit 980 Revenues - 2701 Refunds of Prior Years Expenditures)

•

•

•

•

•

•

•

•

•

GENERAL LEDGER ACCOUNT DESCRIPTIONSS 137

General Ledger Account Descriptions

620 TAX ANTICIPATION NOTES PAYABLE621 REVENUE ANTICIPATION NOTES PAYABLE

These accounts will be used to record the liability for outstanding notes. The note register maintained pursuant to Local Finance Law, §163.00 will serve as a detailed sub-sidiary record.

Credit principal amount of notes issued. Do not include accrued interest, if any, received as part of the proceeds of the notes.

Debit and credit renewals of notes.

Debit disbursements from 200 Cash, 221 Cash for Tax Anticipation Notes and/or 222 Cash for Revenue Anticipation Notes for redemption of notes.

622 BUDGET NOTES PAYABLE

This account will be used to record the liability for budget notes issued to fi nance unan-ticipated expenditures. A note register must be maintained. (Local Finance Law, §163.00)

Credit notes issued.

Debit and credit renewals of obligations.

Debit payments from 220 Cash From Obligations which represents the application of unexpended proceeds for redemption of the related obligations.

Debit payment from 200 Cash for the redemption of obligations.

626 BOND ANTICIPATION NOTES PAYABLE

This account will be used to record the liability for bond anticipation notes issued for operating expenditures (judgments and claims, defi cit fi nancing, etc.).

Credit proceeds of bond anticipation notes.

Debit principal payments on bond anticipation notes.

•

•

•

•

•

•

•

•

•

138 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

General Ledger Account Descriptions

629 BOND INTEREST AND MATURED BONDS PAYABLE

The balance of this account represents unpaid principal and interest on mature bonds. This account should agree with the balance in account 223 Cash With Fiscal Agent.

Credit amounts transferred to a paying agent.

Debit amounts paid by the paying agent as evidenced by cancelled bonds and notes or certifi cation from the paying agent.

630 DUE TO OTHER FUNDS

An analysis of this account will be maintained to identify the amount due to each fund.

Credit advances from other funds.

Debit payments to other funds for amounts previously advanced.

631 DUE TO OTHER GOVERNMENTS

This account is provided to record the liability to other units of governments. A subsid-iary record will be maintained to show the liability to each unit of government.

Credit amounts due to other units of government.

Debit with liquidation of liabilities.

632 DUE TO STATE TEACHERS’ RETIREMENT SYSTEM

This account refl ects the liability for amounts withheld from salaries as State Teachers’ Retirement Contributions and for the school district’s share of retirement.

Credit amount of teachers’ retirement contributions withheld from teachers’ salaries paid from the General Fund (Debit 522 Expenditures).

Credit amount of teachers’ retirement contributions withheld from teachers’ salaries paid from other funds. Such amounts shall be withdrawn from the funds when sala-ries are paid (Debit 200 Cash).

Credit the district’s share of teachers’ retirement contributions.

Debit amount withheld from State aid to satisfy the liability of the employees to the State Teachers’ Retirement System and the liability for the district’s share of accrued teachers’ retirement contributions.

•

•

•

•

•

•

•

•

•

•

GENERAL LEDGER ACCOUNT DESCRIPTIONSS 139

General Ledger Account Descriptions

637 DUE TO EMPLOYEES’ RETIREMENT SYSTEM

This account is provided to record the accrued liability to the New York State Employees’ Retirement System.

Credit with the amount accrued each year.

Debit payments to the retirement system.

651 ACCRUED INTEREST PAYABLE

Credit accrued interest received at the time of sale of obligations.

Debit with the balance at the time of the fi rst interest payment.

687 COMPENSATED ABSENCES

Credit for amounts for absences, such as vacation or sick leave, for which it is expect-ed employees will be paid.

Debit payments.

690 OVERPAYMENTS

Credit overpayments.

Debit refunds of overpayments.

691 DEFERRED REVENUE

The balance of this account represents amounts for which asset recognition criteria have been met, but which revenue recognition criteria have not been met.

Credit amounts which are not available in accordance with revenue recognition criteria.

Debit when amounts become available (Credit 980 Revenue).

•

•

•

•

•

•

•

•

•

•

140 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

General Ledger Account Descriptions

692 DEFERRED REVENUES - PLANNED BALANCE

This account will be used to segregate the amount in the current tax levy to meet the expenditures of the fi rst 120 days of the following school year as permitted by Education Law.

Credit with amount of taxes levied to provide funds to meet expenditures of the fi rst 120 days of operation of the year following that in which the taxes were levied (Debit 250 Taxes Receivable, Current)

Debit at the beginning of the succeeding year to appropriate money for use (Credit 980 Revenues - 1040 Appropriation of Planned Balance).

694 DEFERRED TAX REVENUES (City School Districts Only)

Credit taxes levied in excess of budgetary requirements (tax overlay).

Credit additional amounts when the deferral is deemed inadequate (Debit 980 Revenues - 1001 Real Property Taxes)

Debit at the close of the fi scal year with the amount deemed to be excessive. (Credit 980 Revenues - 1001 Real Property Taxes)

909 FUND BALANCE, UNRESERVED

This account refl ects the net result of operations.

Credit as a closing entry with the balance of 980 Revenues (less amounts closed to special reserves).

Credit at the beginning of the year with the amount of encumbrances outstanding at the end of the previous year (Debit 521 Encumbrances).

Debit as a closing entry with the amount of outstanding encumbrances (Credit 521 Encumbrances).

Debit as a closing entry with the balance of 522 Expenditures (less amounts closed to special reserves.

For reporting purposes, 909 Fund Balance, Unreserved will be broken down to:

910 Unreserved - Appropriated Fund Balance

911 Unreserved - Unappropriated Fund Balance

•

•

•

•

•

•

•

•

•

•

•

GENERAL LEDGER ACCOUNT DESCRIPTIONSS 141

General Ledger Account Descriptions

960 APPROPRIATIONS

This account is one of several budgetary accounts used to record and summarize all bud-getary actions of the governing board. It will not be used to record actual expenditures. The credit balance before closing will represent budgetary appropriations and modifi ca-tions.

Credit at the beginning of the year with the opening balance of 821 Reserve for En-cumbrances to provide the appropriation for outstanding encumbrances (Debit 599 Appropriated Fund Balance).

Credit with the aggregate of all appropriations in the adopted budget.

Credit supplemental appropriations (Debit 510 Estimated Revenues, 511 Appropriated Reserves or 599 Appropriated Fund Balance).

Credit appropriations fi nanced by obligations (Debit 530 Obligations Authorized).

Debit reductions of appropriations when the governing board determines that actual revenues will not equal estimated revenues (Credit 510 Estimated Revenues).

Debit with the closing entry to 510 Estimated Revenues, 511 Appropriated Reserves, 530 Obligations Authorized and 599 Appropriated Fund Balance).

962 BUDGETARY PROVISION FOR OTHER PURPOSES

This account is one of several budgetary accounts. It is used to record taxes levied for purposes other than current operations such as a repair reserve and taxes levied to redeem short-term notes.

Credit estimated amounts levied for other than current year appropriations, e.g., tax overlay, reserves, or short-term notes (Debit 510 Estimated Revenues).

Debit as a closing entry to 510 Estimated Revenues.

980 REVENUES

This account will be used to record revenues including revenues of special reserves. Detail accounts will be maintained in accordance with the chart of revenue accounts in a subsidiary revenue ledger.

Credit amount of cash receipts representing revenues.

Credit levy of real property taxes for budgetary appropriations and special reserves (Debit 250 Taxes Receivable, Current).

•

•

•

•

•

•

•

•

•

•

142 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

General Ledger Account Descriptions

Credit amount of interest added to taxes returned to the enforcement offi cer (Debit 260 Taxes Receivable, Overdue) (City School Districts only).

Credit amount withheld from State aid for teachers’ and districts’ contributions to Teachers’ Retirement System (Debit accounts 391 Due from Other Funds (their share), 522 Expenditures (district’s share), and 632 Due to State Teachers’ Retirement System (teachers’ share and district share of accrued)).

Credit revenues collected in advance (i.e., deferred revenues) and/or receivables which are now available to fi nance current appropriations. (Debit 691 Deferred Rev-enues, 692 Deferred Revenues Planned Balance, and 694 Deferred Revenues, Taxes).

Credit accrued revenues.

Debit corrections or refunds of revenues except taxes of prior years which are charged to 1964.4 Refund on Real Property Taxes.

Debit closing entry to 909 Fund Balance and to Special Reserves.

Accounting Reserves821 RESERVE FOR ENCUMBRANCES

The balance of this account represents the amount of outstanding encumbrances.

Credit encumbrances placed.

Debit encumbrances liquidated or cancelled.

845 RESERVE FOR INVENTORY

The purpose of this account is to limit the maximum investment in inventory and to re-strict that portion of fund balance which is not available for appropriation. The maximum investment in 445 Inventory should not exceed the balance in this account.

Credit amount provided to establish or increase a reserve for inventory purposes (Debit 909 Fund Balance, Unreserved).

Credit to record material year end values of inventories.

Debit when the reserve is to be reduced or eliminated.

•

•

•

•

•

•

•

•

•

•

•

GENERAL LEDGER ACCOUNT DESCRIPTIONSS 143

General Ledger Account Descriptions

Legal Reserves

814 WORKERS’ COMPENSATION RESERVE (GML §6-j)815 UNEMPLOYMENT INSURANCE RESERVE (GML §6-m)827 RESERVE FOR RETIREMENT CONTRIBUTIONS (GML §6-r)861 RESERVE FOR PROPERTY LOSS (EL §1709[8-c])862 RESERVE FOR LIABILITY CLAIMS (EL §1709[8-c])863 INSURANCE RESERVES (GML §6-n)864 RESERVE FOR TAX CERTIORARI (EL §3651[1-a])867 EMPLOYEE BENEFIT ACCRUED LIABILITY RESERVE (GML §6-p)878 CAPITAL RESERVE (EL §3651[1])882 REPAIR RESERVE (GML §6-d)884 MANDATORY RESERVE (GML §6-l)891 RESERVE FOR TAX REDUCTION (EL §§1604[36], 1709[37])

144 ACCOUNTING AND REPORTING MANUAL FOR SCHOOL DISTRICTS

General Ledger Account Descriptions

![legzoesemesztoszerviplenaris endoszkopia PR Belgy3 magyar 2018 eloadasok... · (qgrv]nysld 0huhy uljlg hqgrv]nys )oh[lelolv hqgrv]nys yhjv]iodv ilehu ylghrhqgrv]nys 0huhy hqgrv]nys](https://img.pdfslide.net/doc/110x75/5ebee793d71d7e03f54d9e3f/legzoesemesztoszerviplenaris-endoszkopia-pr-belgy3-magyar-2018-eloadasok-qgrvnysld.jpg)