Embed Size (px)

Citation preview

September 20, 2017

IPO Review

ICICI Securities Ltd | Retail Equity Research

Incorporated in 2009, Prataap Snacks is an Indore, Madhya Pradesh,

based Indian food company, which sells its products under brand name

Yellow Diamond. It is among the top six players in the | 22000 crore

Indian organised snacks market with a 4% market share. The company

sells its products under three categories – a) extruded snacks b) chips and

c) namkeen. In FY17, these aforesaid categories contributed 63.0%,

23.9% and 12.2% to revenue, respectively. As of June 30, 2017, the

company has a distribution network of 218 super stockists across India

and ~3,500 distributors. It owns three manufacturing facilities, one in

Indore, Madhya Pradesh and the other two in Guwahati, Assam. Prataap

reported revenue CAGR of 27.3%, in FY13-17. The company aims to raise

~| 482 crore through a fresh issue (21.5 lakh shares) and offer for sale of

shares (30.1 lakh shares) at a price band of | 930-938 per share.

Investment Rationales

Diversified product portfolio and market share gain

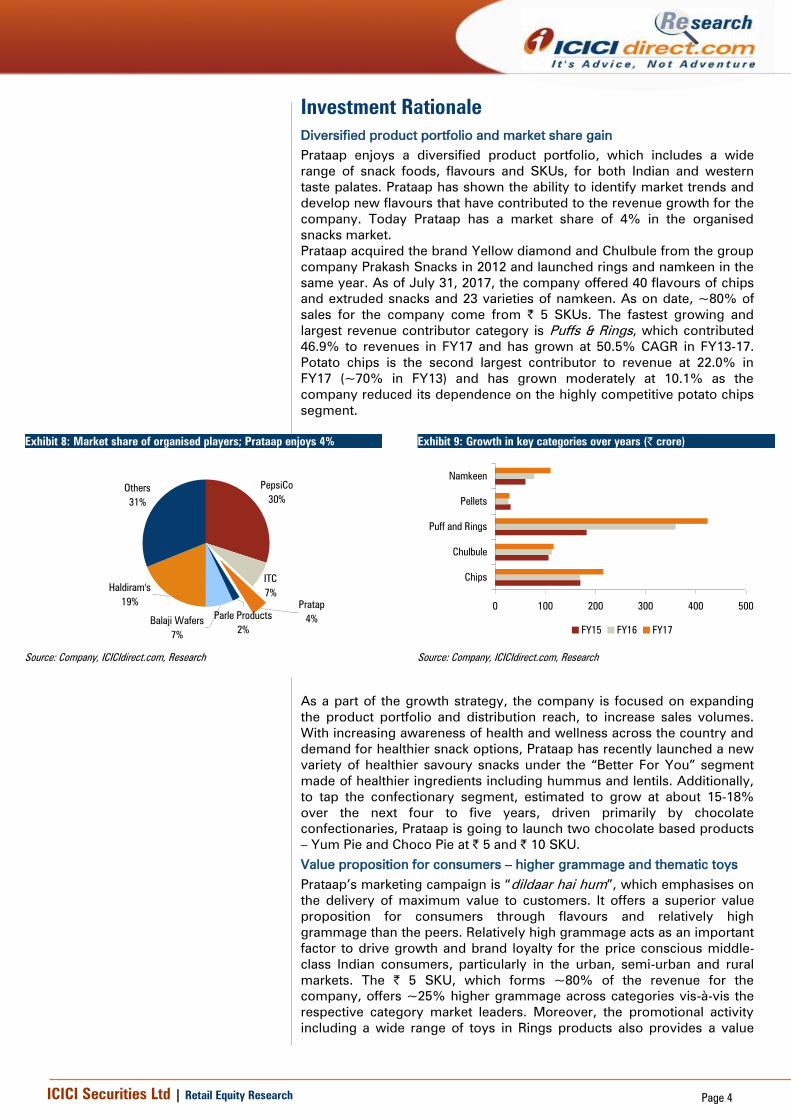

Prataap enjoys a diversified product portfolio, which includes a wide

range of snack foods, flavours and SKUs, for both Indian and western

taste palates. At present, Prataap has a market share of 4% in the

organised snacks market. The fastest growing and largest revenue

contributor category is Puffs & Rings, which contributed 46.9% to

revenues in FY17 and has grown at 50.5% CAGR in FY13-17. Potato chips

is the second largest contributor to revenue at 22.0% in FY17 (~70% in

FY13) and has grown moderately at 10.1% as the company reduced its

dependence on the highly competitive potato chips segment.

Value proposition for consumers – higher grammage, thematic toys

Prataap’s marketing campaign “dildaar hai hum” emphasises on the

delivery of maximum value to customers. It offers a superior value

proposition for consumers through flavours and relatively high

grammage vs. peers along with a wide range of toys in rings products.

Relatively high grammage acts as an important factor to drive growth and

brand loyalty for the price conscious middle-class Indian consumers. The

| 5 SKU, which forms ~80% of revenue for the company, offers ~25%

higher grammage across categories compared to the market leaders.

Risks

1. Any fluctuation in prices or the supply of raw materials (70.4% of net

sales in FY17) may adversely affect the operating margin of the

company. It does not have any long term contract with suppliers

2. Inability to maintain the competitive position, failure to develop,

launch and market new products due to a change in consumer

preferences may dampen the company’s future prospect

3. The company is basing its future growth on the new capacity it

intends to build with net proceeds of the IPO. Any delay of inability to

expand as per plan may impact the growth outlook for the company

Attractively valued at 2.4x Mcap/sales – recommend SUBSCRIBE

At the higher end of the IPO price band of | 938, the stock is valued at

2.4x FY17 MCap/sales (post issue). DFM Foods, which is present in a

similar business, is trading at 4.1x MCap/sales. We believe Prataap

Snacks is attractively placed compared to its peers at 2.4x MCap/sales.

With expansion plans in place, initiative to penetrate the weaker markets

and strengthening of brand image & recall through | 40 crore investment

over coming three years, the company would be able to post sustainable

operating margin and also record better earnings going forward.

Prataap Snacks

Price band | 930-938

Rating matrix

Rating : Subscribe

Issue Details

Issue Details

Issue Opens 22-Sep-17

Issue closes 26-Sep-17

Issue size (| crore) 480-482

Fresh Issue (| crore) 200.0

Offer for sale (| crore) 281.9

Price Band (|) 930-938

No. of shares for offer (crore) 0.5

QIB (%) 50.0

Non-Institutional (%) 15.0

Retail (%) 35.0

Objects of issue

Objects of the issue (| crore)

Repayment/pre-payment, in full or part, of certain borrowings 13.0 Funding capital expenditure requirements in relation to

expansion and modernisation

at certain of our existing manufacturing facilities 67.0 Investment in our Subsidiary, Pure N Sure, for

repayment/pre-payment of certain borrowings availed by

our Subsidiary 29.4

Marketing and brand building activities 40.0

General corporate purpose 50.7

Total 200.0

Shareholding Pattern

Pre-Issue* Post Issue

Promoter & promoter group 92.7 73.4

Public & others 7.3 26.6

*Including pre IPO placement of 5.3 lakh shares to Malabar India

Fund and Malabar Value Fund

Financial Summary

FY13 FY14 FY15 FY16 FY17

Net Sales 344.5 446.8 560.6 757.9 905.5

EBITDA 28.3 21.4 35.6 57.2 42.4

EBITDA margin (%) 8.2 4.8 6.4 7.6 4.7

Net profit 14.9 5.4 10.9 33.2 9.9

Diluted EPS (post issue) 6.3 2.3 4.6 14.1 4.2

Valuation Summary (at | 938; Post issue)

FY13 FY14 FY15 FY16 FY17

P/E 147.9 409.0 202.5 66.3 222.4

Mcap / Sales 6.4 4.9 3.9 2.9 2.4

EV / EBITDA 77.9 103.7 62.5 39.2 53.2

Research Analyst

Sanjay Manyal

sanjay,[email protected]

Tejashwini Kumari

Page 2 ICICI Securities Ltd | Retail Equity Research

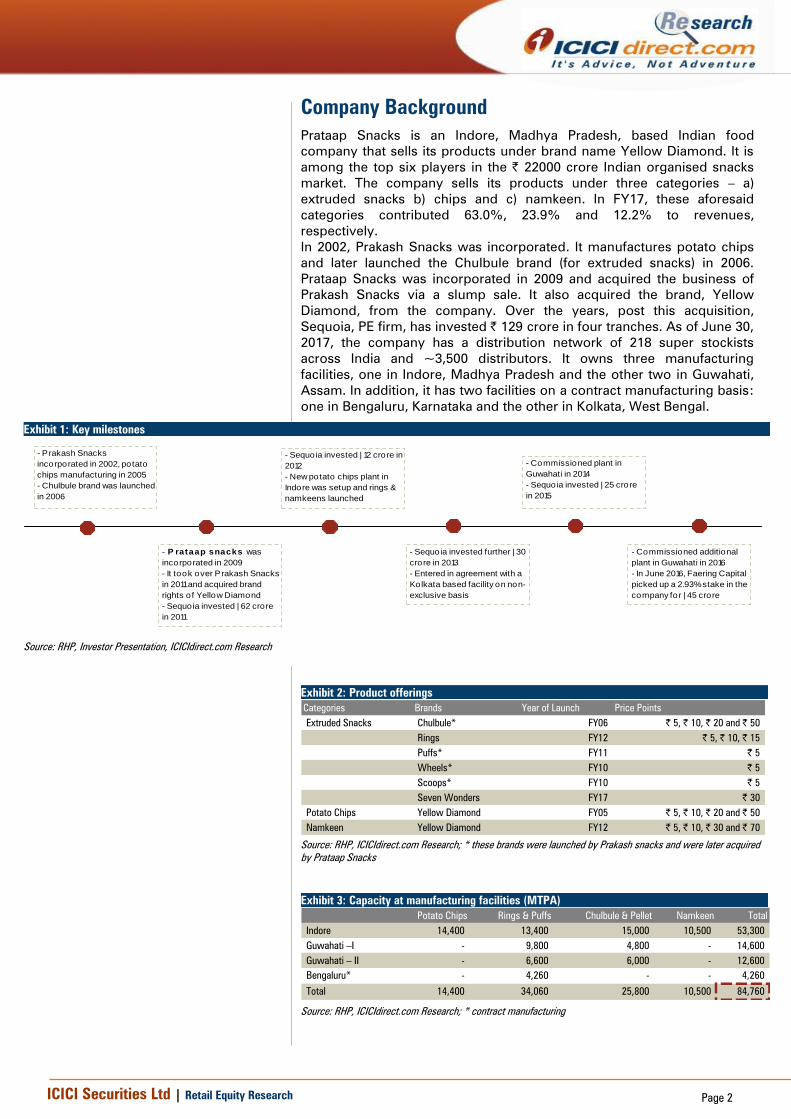

Company Background

Prataap Snacks is an Indore, Madhya Pradesh, based Indian food

company that sells its products under brand name Yellow Diamond. It is

among the top six players in the | 22000 crore Indian organised snacks

market. The company sells its products under three categories – a)

extruded snacks b) chips and c) namkeen. In FY17, these aforesaid

categories contributed 63.0%, 23.9% and 12.2% to revenues,

respectively.

In 2002, Prakash Snacks was incorporated. It manufactures potato chips

and later launched the Chulbule brand (for extruded snacks) in 2006.

Prataap Snacks was incorporated in 2009 and acquired the business of

Prakash Snacks via a slump sale. It also acquired the brand, Yellow

Diamond, from the company. Over the years, post this acquisition,

Sequoia, PE firm, has invested | 129 crore in four tranches. As of June 30,

2017, the company has a distribution network of 218 super stockists

across India and ~3,500 distributors. It owns three manufacturing

facilities, one in Indore, Madhya Pradesh and the other two in Guwahati,

Assam. In addition, it has two facilities on a contract manufacturing basis:

one in Bengaluru, Karnataka and the other in Kolkata, West Bengal.

Exhibit 1: Key milestones

Source: RHP, Investor Presentation, ICICIdirect.com Research

Exhibit 2: Product offerings

Categories Brands Year of Launch Price Points

Extruded Snacks Chulbule* FY06 | 5, | 10, | 20 and | 50

Rings FY12 | 5, | 10, | 15

Puffs* FY11 | 5

Wheels* FY10 | 5

Scoops* FY10 | 5

Seven Wonders FY17 | 30

Potato Chips Yellow Diamond FY05 | 5, | 10, | 20 and | 50

Namkeen Yellow Diamond FY12 | 5, | 10, | 30 and | 70

Source: RHP, ICICIdirect.com Research; * these brands were launched by Prakash snacks and were later acquired

by Prataap Snacks

Exhibit 3: Capacity at manufacturing facilities (MTPA)

Potato Chips Rings & Puffs Chulbule & Pellet Namkeen Total

Indore 14,400 13,400 15,000 10,500 53,300

Guwahati –I - 9,800 4,800 - 14,600

Guwahati – II - 6,600 6,000 - 12,600

Bengaluru* - 4,260 - - 4,260

Total 14,400 34,060 25,800 10,500 84,760

Source: RHP, ICICIdirect.com Research; * contract manufacturing

- Prakash Snacks

incorporated in 2002, potato

chips manufacturing in 2005

- Chulbule brand was launched

in 2006

- P rataap snacks was

incorporated in 2009

- It took over Prakash Snacks

in 2011 and acquired brand

rights of Yellow Diamond

- Sequoia invested | 62 crore

in 2011

- Sequoia invested | 12 crore in

2012

- New potato chips plant in

Indore was setup and rings &

namkeens launched

- Sequoia invested further | 30

crore in 2013

- Entered in agreement with a

Kolkata based facility on non-

exclusive basis

- Commissioned plant in

Guwahati in 2014

- Sequoia invested | 25 crore

in 2015

- Commissioned additional

plant in Guwahati in 2016

- In June 2016, Faering Capital

picked up a 2.93% stake in the

company for | 45 crore

Page 3 ICICI Securities Ltd | Retail Equity Research

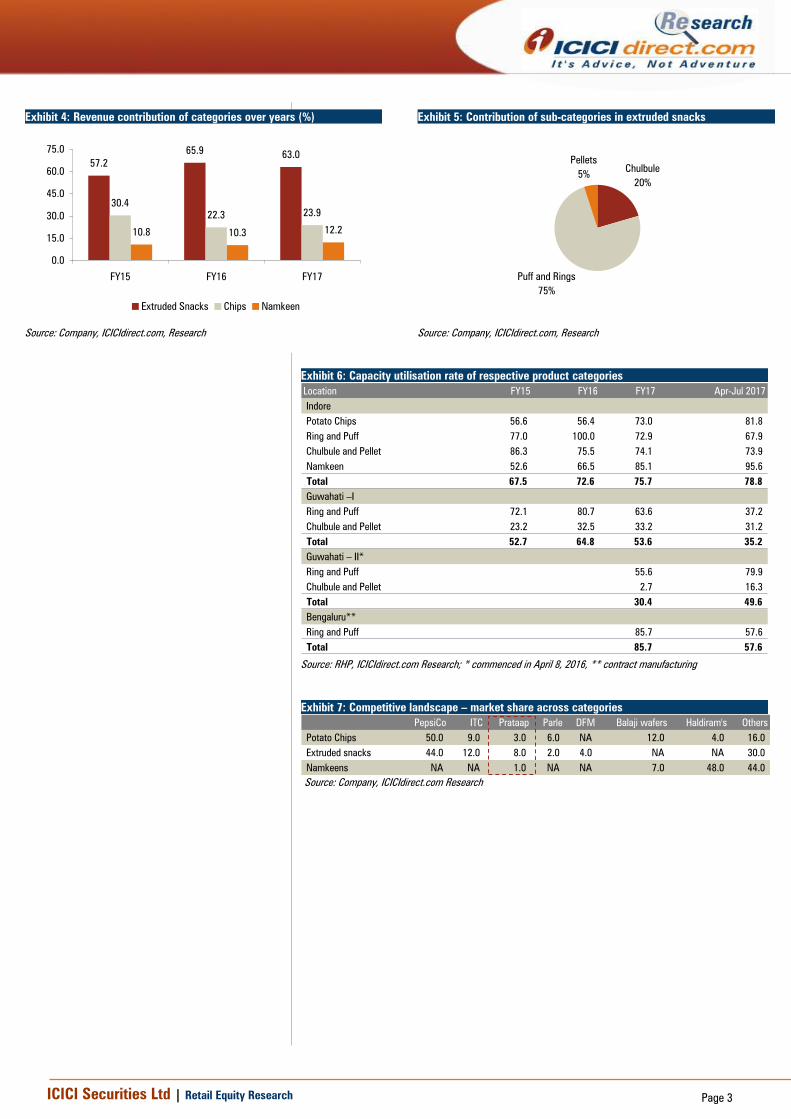

Exhibit 4: Revenue contribution of categories over years (%)

57.2

65.963.0

30.4

22.3 23.9

10.8 10.3 12.2

0.0

15.0

30.0

45.0

60.0

75.0

FY15 FY16 FY17

Extruded Snacks Chips Namkeen

Source: Company, ICICIdirect.com, Research

Exhibit 5: Contribution of sub-categories in extruded snacks

Chulbule

20%

Puff and Rings

75%

Pellets

5%

Source: Company, ICICIdirect.com, Research

Exhibit 6: Capacity utilisation rate of respective product categories

Location FY15 FY16 FY17 Apr-Jul 2017

Indore

Potato Chips 56.6 56.4 73.0 81.8

Ring and Puff 77.0 100.0 72.9 67.9

Chulbule and Pellet 86.3 75.5 74.1 73.9

Namkeen 52.6 66.5 85.1 95.6

Total 67.5 72.6 75.7 78.8

Guwahati –I

Ring and Puff 72.1 80.7 63.6 37.2

Chulbule and Pellet 23.2 32.5 33.2 31.2

Total 52.7 64.8 53.6 35.2

Guwahati – II*

Ring and Puff 55.6 79.9

Chulbule and Pellet 2.7 16.3

Total 30.4 49.6

Bengaluru**

Ring and Puff 85.7 57.6

Total 85.7 57.6

Source: RHP, ICICIdirect.com Research; * commenced in April 8, 2016, ** contract manufacturing

Exhibit 7: Competitive landscape – market share across categories

PepsiCo ITC Prataap Parle DFM Balaji wafers Haldiram's Others

Potato Chips 50.0 9.0 3.0 6.0 NA 12.0 4.0 16.0

Extruded snacks 44.0 12.0 8.0 2.0 4.0 NA NA 30.0

Namkeens NA NA 1.0 NA NA 7.0 48.0 44.0

Source: Company, ICICIdirect.com Research

Page 4 ICICI Securities Ltd | Retail Equity Research

Investment Rationale

Diversified product portfolio and market share gain

Prataap enjoys a diversified product portfolio, which includes a wide

range of snack foods, flavours and SKUs, for both Indian and western

taste palates. Prataap has shown the ability to identify market trends and

develop new flavours that have contributed to the revenue growth for the

company. Today Prataap has a market share of 4% in the organised

snacks market.

Prataap acquired the brand Yellow diamond and Chulbule from the group

company Prakash Snacks in 2012 and launched rings and namkeen in the

same year. As of July 31, 2017, the company offered 40 flavours of chips

and extruded snacks and 23 varieties of namkeen. As on date, ~80% of

sales for the company come from | 5 SKUs. The fastest growing and

largest revenue contributor category is Puffs & Rings, which contributed

46.9% to revenues in FY17 and has grown at 50.5% CAGR in FY13-17.

Potato chips is the second largest contributor to revenue at 22.0% in

FY17 (~70% in FY13) and has grown moderately at 10.1% as the

company reduced its dependence on the highly competitive potato chips

segment.

Exhibit 8: Market share of organised players; Prataap enjoys 4%

Others

31%

Haldiram's

19%

Balaji Wafers

7%

Parle Products

2%

Pratap

4%

ITC

7%

PepsiCo

30%

Source: Company, ICICIdirect.com, Research

Exhibit 9: Growth in key categories over years (| crore)

0 100 200 300 400 500

Chips

Chulbule

Puff and Rings

Pellets

Namkeen

FY15 FY16 FY17

Source: Company, ICICIdirect.com, Research

As a part of the growth strategy, the company is focused on expanding

the product portfolio and distribution reach, to increase sales volumes.

With increasing awareness of health and wellness across the country and

demand for healthier snack options, Prataap has recently launched a new

variety of healthier savoury snacks under the “Better For You” segment

made of healthier ingredients including hummus and lentils. Additionally,

to tap the confectionary segment, estimated to grow at about 15-18%

over the next four to five years, driven primarily by chocolate

confectionaries, Prataap is going to launch two chocolate based products

– Yum Pie and Choco Pie at | 5 and | 10 SKU.

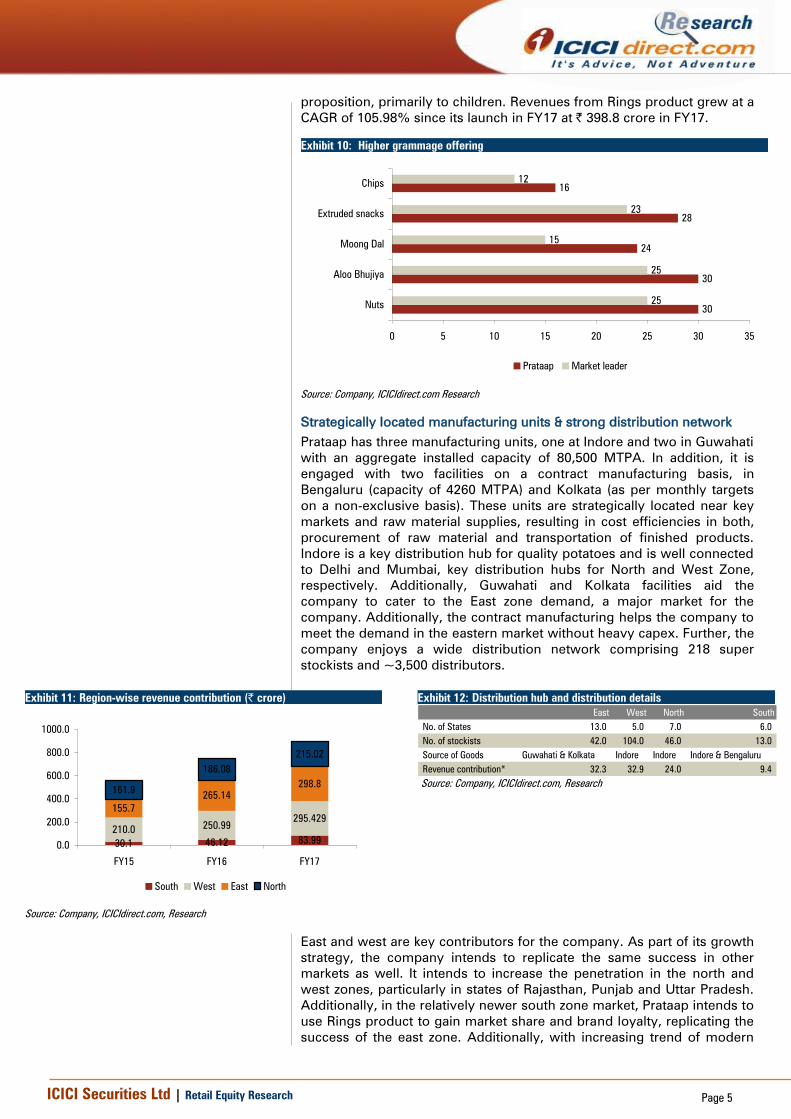

Value proposition for consumers – higher grammage and thematic toys

Prataap’s marketing campaign is “dildaar hai hum”, which emphasises on

the delivery of maximum value to customers. It offers a superior value

proposition for consumers through flavours and relatively high

grammage than the peers. Relatively high grammage acts as an important

factor to drive growth and brand loyalty for the price conscious middle-

class Indian consumers, particularly in the urban, semi-urban and rural

markets. The | 5 SKU, which forms ~80% of the revenue for the

company, offers ~25% higher grammage across categories vis-à-vis the

respective category market leaders. Moreover, the promotional activity

including a wide range of toys in Rings products also provides a value

Page 5 ICICI Securities Ltd | Retail Equity Research

proposition, primarily to children. Revenues from Rings product grew at a

CAGR of 105.98% since its launch in FY17 at | 398.8 crore in FY17.

Exhibit 10: Higher grammage offering

30

30

24

28

16

25

25

15

23

12

0 5 10 15 20 25 30 35

Nuts

Aloo Bhujiya

Moong Dal

Extruded snacks

Chips

Prataap Market leader

Source: Company, ICICIdirect.com Research

Strategically located manufacturing units & strong distribution network

Prataap has three manufacturing units, one at Indore and two in Guwahati

with an aggregate installed capacity of 80,500 MTPA. In addition, it is

engaged with two facilities on a contract manufacturing basis, in

Bengaluru (capacity of 4260 MTPA) and Kolkata (as per monthly targets

on a non-exclusive basis). These units are strategically located near key

markets and raw material supplies, resulting in cost efficiencies in both,

procurement of raw material and transportation of finished products.

Indore is a key distribution hub for quality potatoes and is well connected

to Delhi and Mumbai, key distribution hubs for North and West Zone,

respectively. Additionally, Guwahati and Kolkata facilities aid the

company to cater to the East zone demand, a major market for the

company. Additionally, the contract manufacturing helps the company to

meet the demand in the eastern market without heavy capex. Further, the

company enjoys a wide distribution network comprising 218 super

stockists and ~3,500 distributors.

Exhibit 11: Region-wise revenue contribution (| crore)

30.1 46.12 83.99

210.0250.99

295.429

155.7

265.14

298.8161.9

186.08

215.02

0.0

200.0

400.0

600.0

800.0

1000.0

FY15 FY16 FY17

South West East North

Source: Company, ICICIdirect.com, Research

Exhibit 12: Distribution hub and distribution details

East West North South

No. of States 13.0 5.0 7.0 6.0

No. of stockists 42.0 104.0 46.0 13.0

Source of Goods Guwahati & Kolkata Indore Indore Indore & Bengaluru

Revenue contribution* 32.3 32.9 24.0 9.4

Source: Company, ICICIdirect.com, Research

East and west are key contributors for the company. As part of its growth

strategy, the company intends to replicate the same success in other

markets as well. It intends to increase the penetration in the north and

west zones, particularly in states of Rajasthan, Punjab and Uttar Pradesh.

Additionally, in the relatively newer south zone market, Prataap intends to

use Rings product to gain market share and brand loyalty, replicating the

success of the east zone. Additionally, with increasing trend of modern

Page 6 ICICI Securities Ltd | Retail Equity Research

retail, the company is planning to enter this category to increase brand

visibility as well as push its premium and higher priced SKUs.

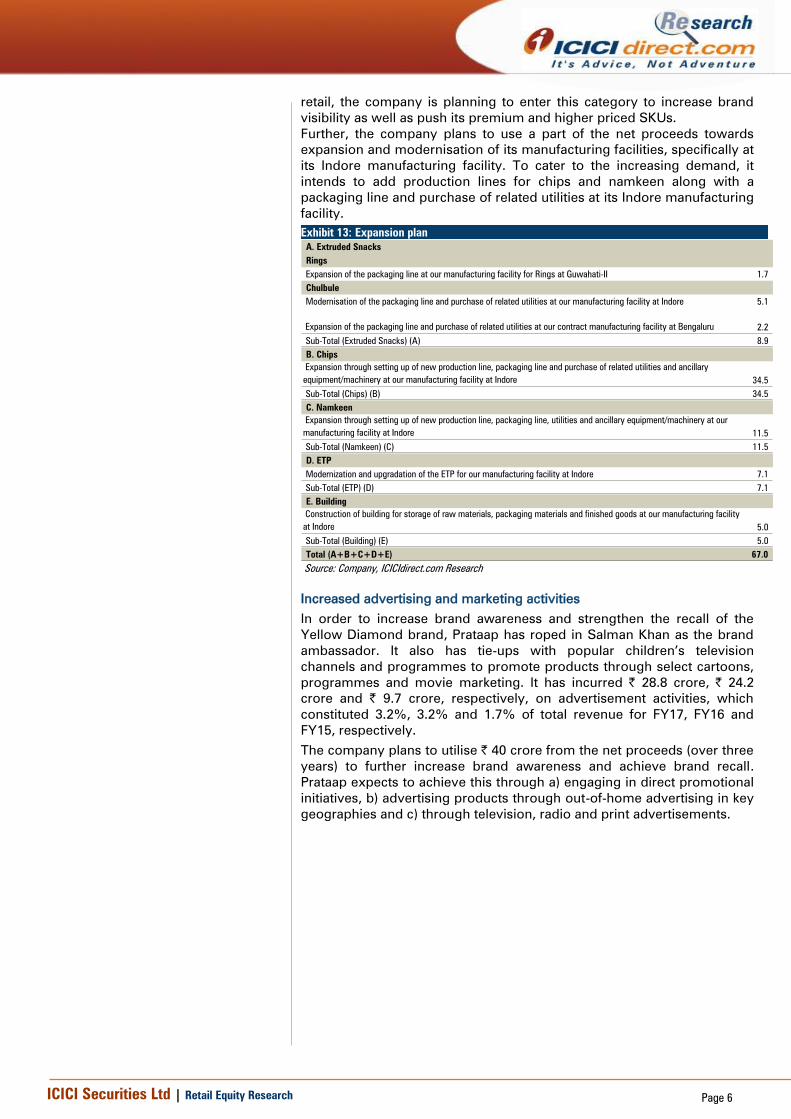

Further, the company plans to use a part of the net proceeds towards

expansion and modernisation of its manufacturing facilities, specifically at

its Indore manufacturing facility. To cater to the increasing demand, it

intends to add production lines for chips and namkeen along with a

packaging line and purchase of related utilities at its Indore manufacturing

facility.

Exhibit 13: Expansion plan

A. Extruded Snacks

Rings

Expansion of the packaging line at our manufacturing facility for Rings at Guwahati-II 1.7

Chulbule

Modernisation of the packaging line and purchase of related utilities at our manufacturing facility at Indore 5.1

Expansion of the packaging line and purchase of related utilities at our contract manufacturing facility at Bengaluru 2.2

Sub-Total (Extruded Snacks) (A) 8.9

B. Chips

Expansion through setting up of new production line, packaging line and purchase of related utilities and ancillary

equipment/machinery at our manufacturing facility at Indore 34.5

Sub-Total (Chips) (B) 34.5

C. Namkeen

Expansion through setting up of new production line, packaging line, utilities and ancillary equipment/machinery at our

manufacturing facility at Indore 11.5

Sub-Total (Namkeen) (C) 11.5

D. ETP

Modernization and upgradation of the ETP for our manufacturing facility at Indore 7.1

Sub-Total (ETP) (D) 7.1

E. Building

Construction of building for storage of raw materials, packaging materials and finished goods at our manufacturing facility

at Indore 5.0

Sub-Total (Building) (E) 5.0

Total (A+B+C+D+E) 67.0

Source: Company, ICICIdirect.com Research

Increased advertising and marketing activities

In order to increase brand awareness and strengthen the recall of the

Yellow Diamond brand, Prataap has roped in Salman Khan as the brand

ambassador. It also has tie-ups with popular children’s television

channels and programmes to promote products through select cartoons,

programmes and movie marketing. It has incurred | 28.8 crore, | 24.2

crore and | 9.7 crore, respectively, on advertisement activities, which

constituted 3.2%, 3.2% and 1.7% of total revenue for FY17, FY16 and

FY15, respectively.

The company plans to utilise | 40 crore from the net proceeds (over three

years) to further increase brand awareness and achieve brand recall.

Prataap expects to achieve this through a) engaging in direct promotional

initiatives, b) advertising products through out-of-home advertising in key

geographies and c) through television, radio and print advertisements.

Page 7 ICICI Securities Ltd | Retail Equity Research

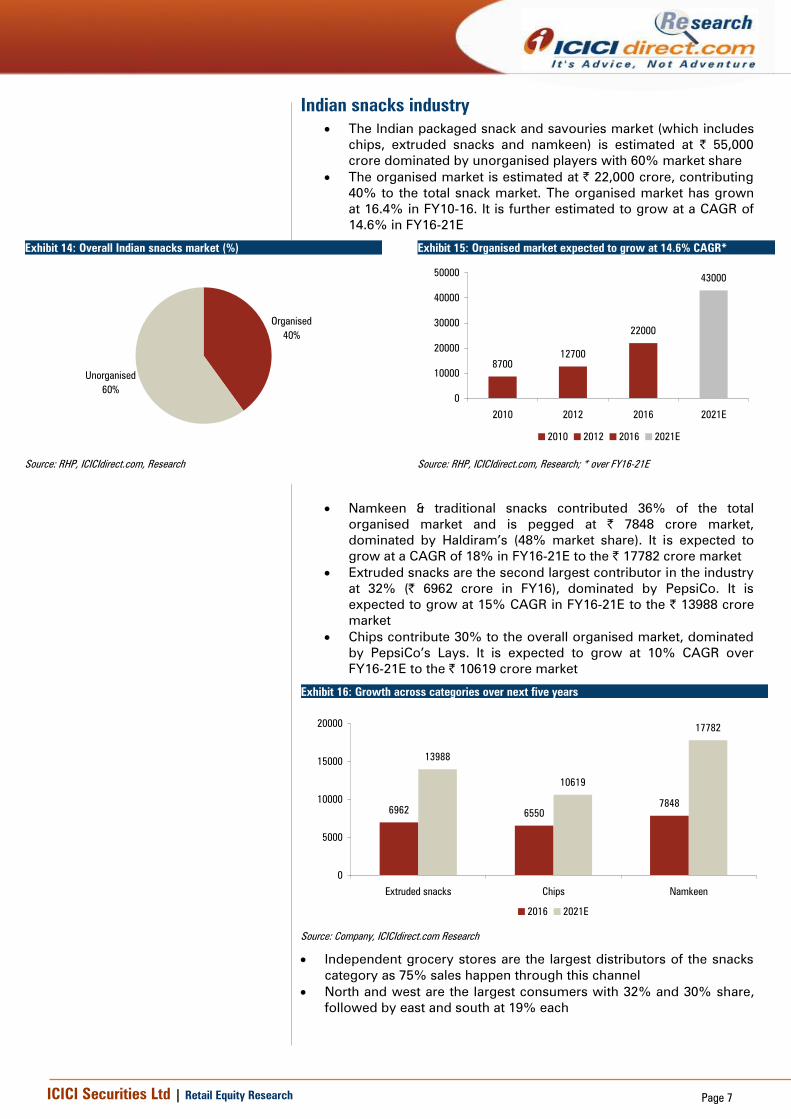

Indian snacks industry

The Indian packaged snack and savouries market (which includes

chips, extruded snacks and namkeen) is estimated at | 55,000

crore dominated by unorganised players with 60% market share

The organised market is estimated at | 22,000 crore, contributing

40% to the total snack market. The organised market has grown

at 16.4% in FY10-16. It is further estimated to grow at a CAGR of

14.6% in FY16-21E

Exhibit 14: Overall Indian snacks market (%)

Unorganised

60%

Organised

40%

Source: RHP, ICICIdirect.com, Research

Exhibit 15: Organised market expected to grow at 14.6% CAGR*

8700

12700

22000

43000

0

10000

20000

30000

40000

50000

2010 2012 2016 2021E

2010 2012 2016 2021E

Source: RHP, ICICIdirect.com, Research; * over FY16-21E

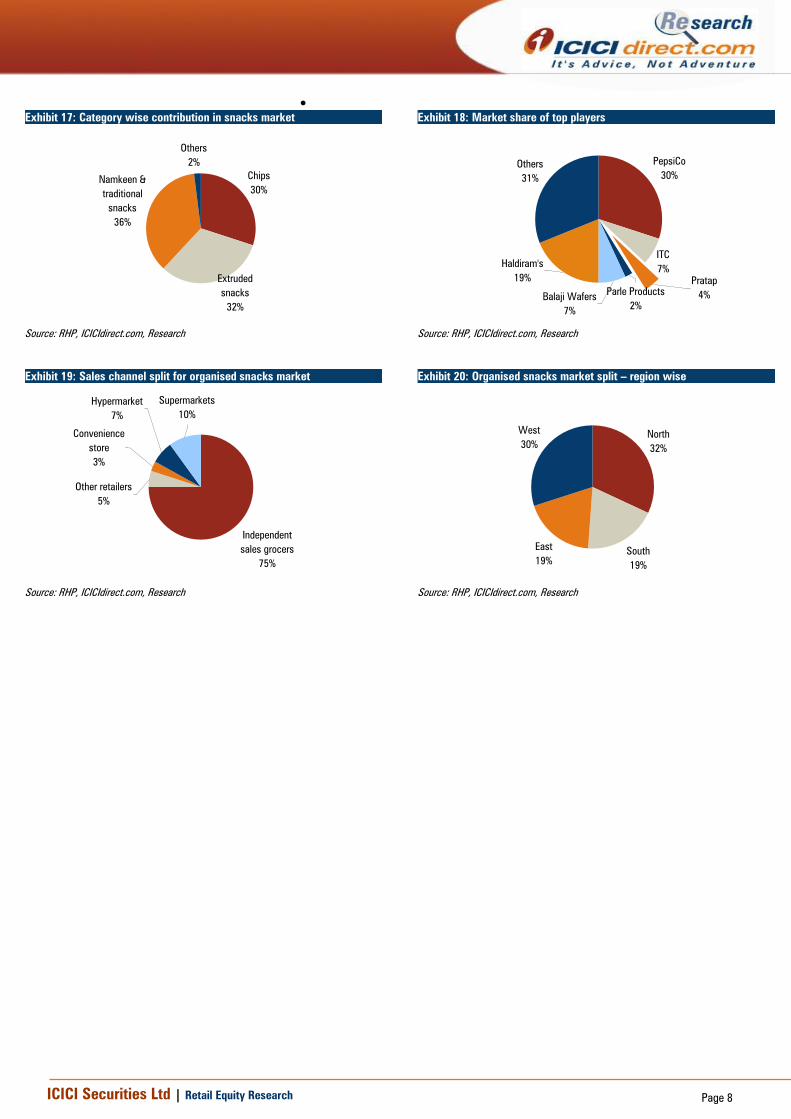

Namkeen & traditional snacks contributed 36% of the total

organised market and is pegged at | 7848 crore market,

dominated by Haldiram’s (48% market share). It is expected to

grow at a CAGR of 18% in FY16-21E to the | 17782 crore market

Extruded snacks are the second largest contributor in the industry

at 32% (| 6962 crore in FY16), dominated by PepsiCo. It is

expected to grow at 15% CAGR in FY16-21E to the | 13988 crore

market

Chips contribute 30% to the overall organised market, dominated

by PepsiCo’s Lays. It is expected to grow at 10% CAGR over

FY16-21E to the | 10619 crore market

Exhibit 16: Growth across categories over next five years

69626550

7848

13988

10619

17782

0

5000

10000

15000

20000

Extruded snacks Chips Namkeen

2016 2021E

Source: Company, ICICIdirect.com Research

Independent grocery stores are the largest distributors of the snacks

category as 75% sales happen through this channel

North and west are the largest consumers with 32% and 30% share,

followed by east and south at 19% each

Page 8 ICICI Securities Ltd | Retail Equity Research

Exhibit 17: Category wise contribution in snacks market

Others

2%

Namkeen &

traditional

snacks

36%

Extruded

snacks

32%

Chips

30%

Source: RHP, ICICIdirect.com, Research

Exhibit 18: Market share of top players

Others

31%

Haldiram's

19%

Balaji Wafers

7%

Parle Products

2%

Pratap

4%

ITC

7%

PepsiCo

30%

Source: RHP, ICICIdirect.com, Research

Exhibit 19: Sales channel split for organised snacks market

Supermarkets

10%

Hypermarket

7%

Convenience

store

3%

Other retailers

5%

Independent

sales grocers

75%

Source: RHP, ICICIdirect.com, Research

Exhibit 20: Organised snacks market split – region wise

West

30%

East

19%

South

19%

North

32%

Source: RHP, ICICIdirect.com, Research

Page 9 ICICI Securities Ltd | Retail Equity Research

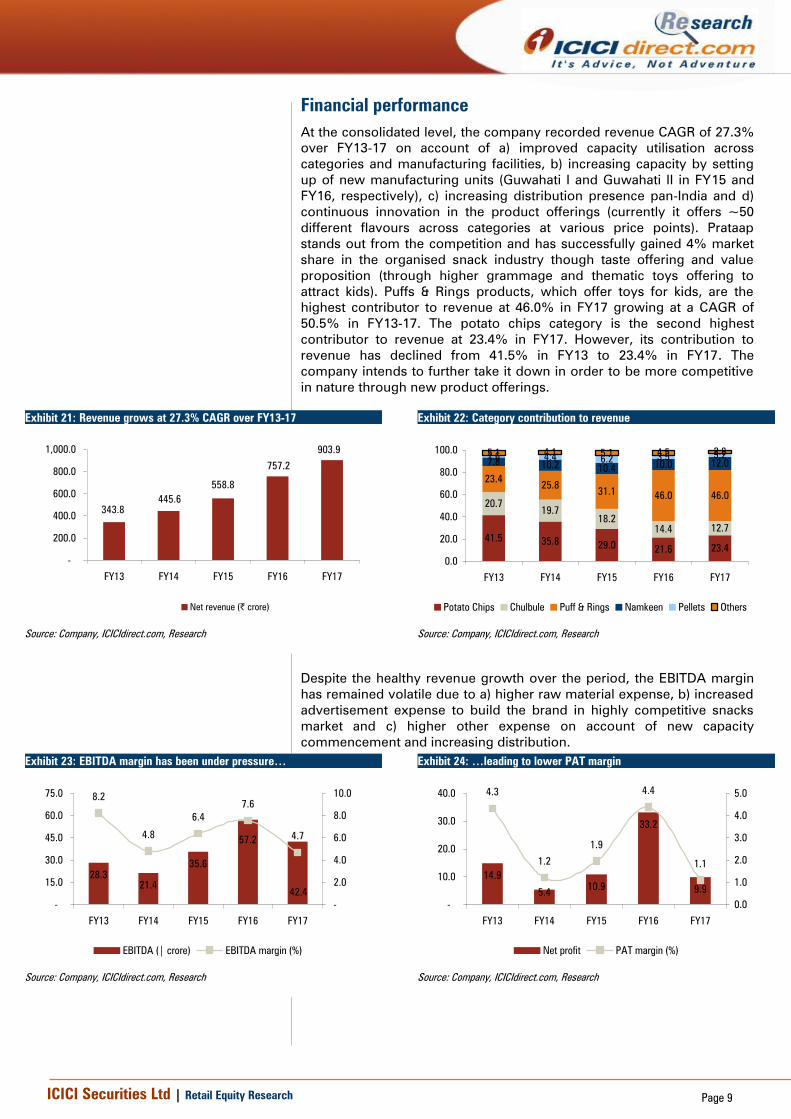

Financial performance

At the consolidated level, the company recorded revenue CAGR of 27.3%

over FY13-17 on account of a) improved capacity utilisation across

categories and manufacturing facilities, b) increasing capacity by setting

up of new manufacturing units (Guwahati I and Guwahati II in FY15 and

FY16, respectively), c) increasing distribution presence pan-India and d)

continuous innovation in the product offerings (currently it offers ~50

different flavours across categories at various price points). Prataap

stands out from the competition and has successfully gained 4% market

share in the organised snack industry though taste offering and value

proposition (through higher grammage and thematic toys offering to

attract kids). Puffs & Rings products, which offer toys for kids, are the

highest contributor to revenue at 46.0% in FY17 growing at a CAGR of

50.5% in FY13-17. The potato chips category is the second highest

contributor to revenue at 23.4% in FY17. However, its contribution to

revenue has declined from 41.5% in FY13 to 23.4% in FY17. The

company intends to further take it down in order to be more competitive

in nature through new product offerings.

Exhibit 21: Revenue grows at 27.3% CAGR over FY13-17

343.8

445.6

558.8

757.2

903.9

-

200.0

400.0

600.0

800.0

1,000.0

FY13 FY14 FY15 FY16 FY17

Net revenue (| crore)

Source: Company, ICICIdirect.com, Research

Exhibit 22: Category contribution to revenue

41.535.8

29.021.6 23.4

20.719.7

18.2

14.4 12.7

23.425.8

31.146.0 46.0

7.810.2

10.410.0 12.0

1.6 4.4 6.2 3.5 3.25.1 4.1 5.1 4.5 2.9

0.0

20.0

40.0

60.0

80.0

100.0

FY13 FY14 FY15 FY16 FY17

Potato Chips Chulbule Puff & Rings Namkeen Pellets Others

Source: Company, ICICIdirect.com, Research

Despite the healthy revenue growth over the period, the EBITDA margin

has remained volatile due to a) higher raw material expense, b) increased

advertisement expense to build the brand in highly competitive snacks

market and c) higher other expense on account of new capacity

commencement and increasing distribution.

Exhibit 23: EBITDA margin has been under pressure…

28.3

21.4

35.6

57.2

42.4

8.2

4.8

6.4

7.6

4.7

-

15.0

30.0

45.0

60.0

75.0

FY13 FY14 FY15 FY16 FY17

-

2.0

4.0

6.0

8.0

10.0

EBITDA (| crore) EBITDA margin (%)

Source: Company, ICICIdirect.com, Research

Exhibit 24: …leading to lower PAT margin

14.9

5.410.9

33.2

9.9

4.3

1.2

1.9

4.4

1.1

-

10.0

20.0

30.0

40.0

FY13 FY14 FY15 FY16 FY17

0.0

1.0

2.0

3.0

4.0

5.0

Net profit PAT margin (%)

Source: Company, ICICIdirect.com, Research

Page 10 ICICI Securities Ltd | Retail Equity Research

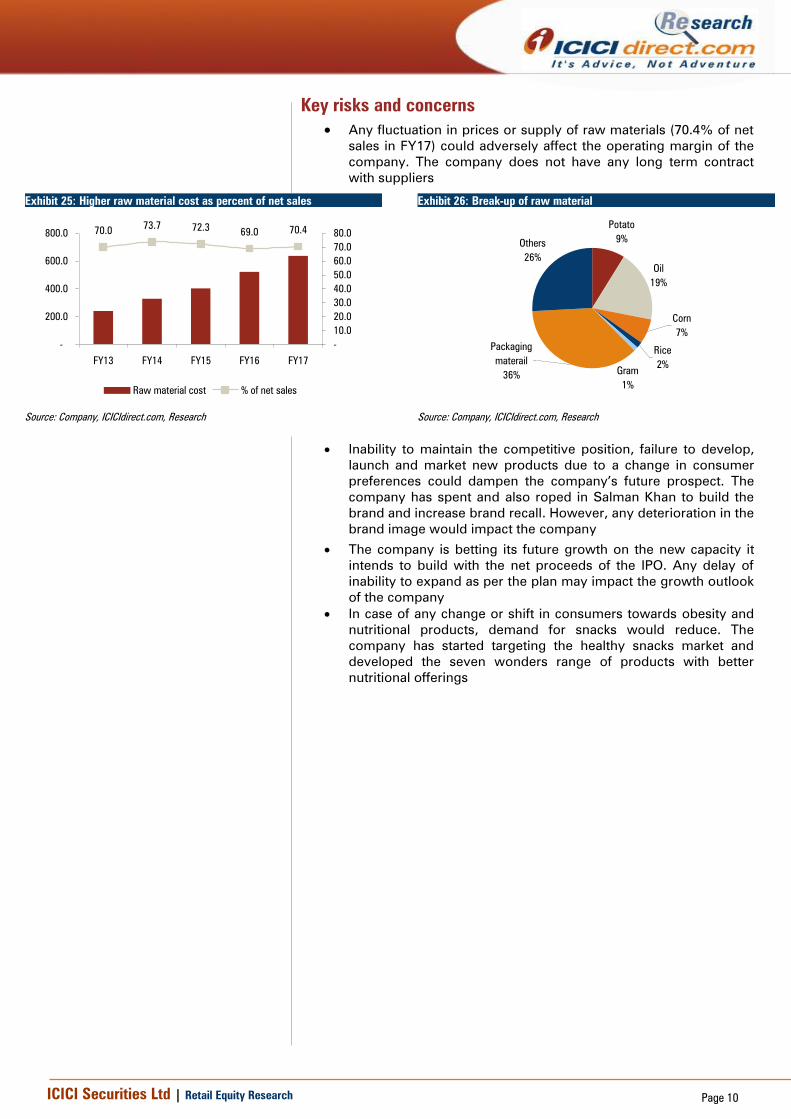

Key risks and concerns

Any fluctuation in prices or supply of raw materials (70.4% of net

sales in FY17) could adversely affect the operating margin of the

company. The company does not have any long term contract

with suppliers

Exhibit 25: Higher raw material cost as percent of net sales

70.073.7 72.3

69.0 70.4

-

200.0

400.0

600.0

800.0

FY13 FY14 FY15 FY16 FY17

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Raw material cost % of net sales

Source: Company, ICICIdirect.com, Research

Exhibit 26: Break-up of raw material

Others

26%

Packaging

materail

36%Gram

1%

Rice

2%

Corn

7%

Oil

19%

Potato

9%

Source: Company, ICICIdirect.com, Research

Inability to maintain the competitive position, failure to develop,

launch and market new products due to a change in consumer

preferences could dampen the company’s future prospect. The

company has spent and also roped in Salman Khan to build the

brand and increase brand recall. However, any deterioration in the

brand image would impact the company

The company is betting its future growth on the new capacity it

intends to build with the net proceeds of the IPO. Any delay of

inability to expand as per the plan may impact the growth outlook

of the company

In case of any change or shift in consumers towards obesity and

nutritional products, demand for snacks would reduce. The

company has started targeting the healthy snacks market and

developed the seven wonders range of products with better

nutritional offerings

Page 11 ICICI Securities Ltd | Retail Equity Research

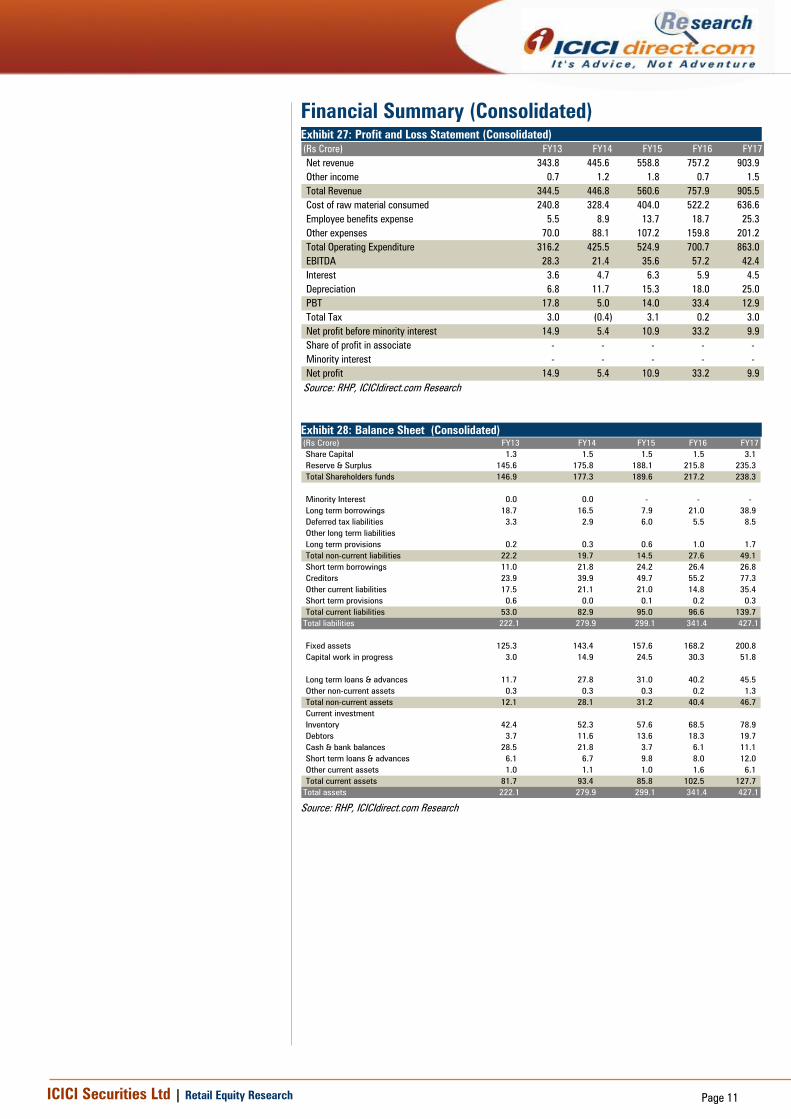

Financial Summary (Consolidated)

Exhibit 27: Profit and Loss Statement (Consolidated)

(Rs Crore) FY13 FY14 FY15 FY16 FY17

Net revenue 343.8 445.6 558.8 757.2 903.9

Other income 0.7 1.2 1.8 0.7 1.5

Total Revenue 344.5 446.8 560.6 757.9 905.5

Cost of raw material consumed 240.8 328.4 404.0 522.2 636.6

Employee benefits expense 5.5 8.9 13.7 18.7 25.3

Other expenses 70.0 88.1 107.2 159.8 201.2

Total Operating Expenditure 316.2 425.5 524.9 700.7 863.0

EBITDA 28.3 21.4 35.6 57.2 42.4

Interest 3.6 4.7 6.3 5.9 4.5

Depreciation 6.8 11.7 15.3 18.0 25.0

PBT 17.8 5.0 14.0 33.4 12.9

Total Tax 3.0 (0.4) 3.1 0.2 3.0

Net profit before minority interest 14.9 5.4 10.9 33.2 9.9

Share of profit in associate - - - - -

Minority interest - - - - -

Net profit 14.9 5.4 10.9 33.2 9.9

Source: RHP, ICICIdirect.com Research

Exhibit 28: Balance Sheet (Consolidated)

(Rs Crore) FY13 FY14 FY15 FY16 FY17

Share Capital 1.3 1.5 1.5 1.5 3.1

Reserve & Surplus 145.6 175.8 188.1 215.8 235.3

Total Shareholders funds 146.9 177.3 189.6 217.2 238.3

Minority Interest 0.0 0.0 - - -

Long term borrowings 18.7 16.5 7.9 21.0 38.9

Deferred tax liabilities 3.3 2.9 6.0 5.5 8.5

Other long term liabilities

Long term provisions 0.2 0.3 0.6 1.0 1.7

Total non-current liabilities 22.2 19.7 14.5 27.6 49.1

Short term borrowings 11.0 21.8 24.2 26.4 26.8

Creditors 23.9 39.9 49.7 55.2 77.3

Other current liabilities 17.5 21.1 21.0 14.8 35.4

Short term provisions 0.6 0.0 0.1 0.2 0.3

Total current liabilities 53.0 82.9 95.0 96.6 139.7

Total liabilities 222.1 279.9 299.1 341.4 427.1

Fixed assets 125.3 143.4 157.6 168.2 200.8

Capital work in progress 3.0 14.9 24.5 30.3 51.8

Long term loans & advances 11.7 27.8 31.0 40.2 45.5

Other non-current assets 0.3 0.3 0.3 0.2 1.3

Total non-current assets 12.1 28.1 31.2 40.4 46.7

Current investment

Inventory 42.4 52.3 57.6 68.5 78.9

Debtors 3.7 11.6 13.6 18.3 19.7

Cash & bank balances 28.5 21.8 3.7 6.1 11.1

Short term loans & advances 6.1 6.7 9.8 8.0 12.0

Other current assets 1.0 1.1 1.0 1.6 6.1

Total current assets 81.7 93.4 85.8 102.5 127.7

Total assets 222.1 279.9 299.1 341.4 427.1

Source: RHP, ICICIdirect.com Research

Page 12 ICICI Securities Ltd | Retail Equity Research

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

Page 13 ICICI Securities Ltd | Retail Equity Research

ANALYST CERTIFICATION

We /I, Sanjay Manyal, MBA (Finance) and Tejashwini Kumari, MBA (Finance) Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this

research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific

recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Sanjay Manyal, MBA (Finance) and Tejashwini Kumari, MBA (Finance) Research Analysts of this report have not received any compensation from the companies mentioned in the report

in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Sanjay Manyal, MBA (Finance) and Tejashwini Kumari, MBA (Finance) Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction