Embed Size (px)

Citation preview

Serving Asia and the Middle East since 1990

oc

t-de

c 2015 V

oL 25 N

o.4

AN

AS

IA PA

cIFIc

eN

eR

GY

BU

SIN

eS

S P

UB

LIcA

tIo

NH

Yd

Ro

cA

RB

oN

AS

IA

http://www.safan.com oct-dec 2015 McI (P) 217/07/2014 • PPS 1064/10/2013 (025508) • ISSN 0217-1112 • Published by AP energy Business Publications Pte Ltd 19 Kim Keat Road, #04-06 Fu tsu Building, Singapore 328804. Printed by KHL Printing co Pte Ltd

PV GAS – Sustainable Development .... pg 8Asian Outlook .... pg 18Instrument Asset Management .... pg 34

Gas Fuelled Progress

Clock Spring205x275aug.indd 1 8/27/10 11:30 AM

Learn more about the art and science of sampling at Sabin Metal, one of many Elements Of Success we’ve provided to catalyst users around the world for over six decades.

www.sabinmetal.com

Elements of Success

Precious metal refining with response and responsibility

SabinElementsOfSuccessAd-HE.indd 1 2/22/15 1:30 PM

An Asia Pacific Energy Publication

Hydrocarbon Asia is published four times a year by AP ENERGY BUSINESS PUBLICATIONS PTE LTD

19 Kim Keat Road #04 - 06 Fu Tsu Building

Singapore 328804Tel : (65) 6222 3422 Fax: (65) 6222 5587

Website: http: //www.safan.com

Now in its 25th year, Hydrocarbon Asia is a technical & business publication covering the oil and gas processing and petrochemical

industry, and all downstream activities, including oil marketing, trading,

terminalling, transportation and financing.

The Publisher reserves the right to accept or reject all editorial or advertising material,

and assumes no responsibility for the return of unsolicited artwork or manuscripts.

All rights reserved. Reproduction of the magazine, in whole or in part, is prohibited without the prior

written consent, not unreasonably withheld, of the Publisher. Reprints of articles appearing in previous

issues of the magazine can be had on request, subject to a minimum quantity.

The views expressed in this journal are not necessarily those of the Publisher and while every

attempt will be made to ensure the accuracy and authenticity of information appearing in

the magazine, the Publisher accepts no liability for damages caused by misinterpretation

of information, expressed or implied, within the pages of the magazine. All correspondence regarding edito-rial, editorial contributions or editorial content should

be directed to the Editor.

The magazine is available at an annual subscription rate of US$110. Please refer to the subscription

form or contact the subscription department for further details at Fax: (65) 6222 5587.

Printed in Singapore by KHL Printing Co Pte Ltd

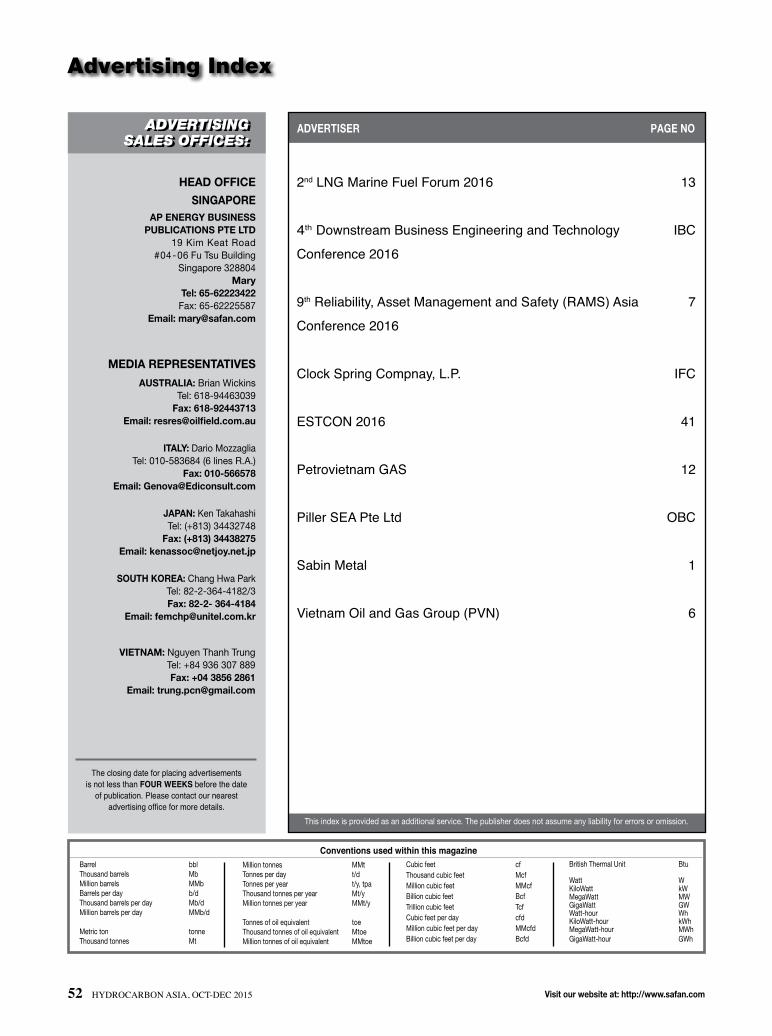

2 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

6RepoRtsInternational Oil and Gas Companies Attend Petrovietnam Conference & Exhibition

PV GAS Concentrates Efforts for Sound and Sustainable Development After 40 years of establishment and development, the Vietnam National Oil and Gas Group has grown into a leading economic group in Vietnam, contributing to the assurance of national energy security. As a leading member of PetroVietnam, PetroVietnam Gas Joint Stock Corporation (PV GAS) orientated strategies are devel-oping the gas industry into a leading economic engine, gradually stepping into the world market, securing a high ranking in the ASIAN gas industry, and becoming one of the strongest gas brands in ASIA in 2025. Mr. Duong Manh Son, Member of the Board of Directors, President and CEO of PV GAS has provided Hydrocarbon Asia his views on this issue!

PV GAS and potential for co-operation in LNG import projects

LNG a Boon for AustraliaThis regional report focuses on Australia, the largest energy entity in the Pacific Rim. Despite refinery closures in the last few years, Australia is gas rich and a leading LNG exporter.

Asian Refining & Marketing 2016 Outlook Moody's says that the Asian refining and marketing outlook remains stable and low oil prices and easing capacity overhang will keep margins healthy. Industry’s EBITDA will grow by around 1%-3% through 2016, driven by healthy petroleum product demand and stable refining margins.

Driving Up Profitable Downstream DollarsThe article highlights that being able to quickly analyse and produce different scenarios delivers swift results. By opening the gateway to a world of new opportunities, refineries are better equipped to explore even more ways to optimise their planning, grow the business and boost profit.

Transforming the Safety Culture Saudi Aramco Base Oil Company-Luberef decided to commit on a November day at the end of 2011 to improve the company’s safety performance which had plateaued. This article is a case study of Luberef plant.

22

18

14

24

8

12

HYDROCARBON ASIA, OCt-DeC 2015 3

We also publish

oct-dec 2015 VoL.25 No.4

RegulaR Focus

Editorial 4

Calendar of Events 50

Advertisers Index 52

Notice to our Readers

While maintaining the printed circulation, we also present the magazine on-line... free access to viewers. Please use the Website to apply for a complimentary copy. Executives / Professionals in the petrochemical, process, energy and related Industries, if they are eligible, will receive Hydrocarbon Asia 'free'.

Notice to our Advertisers

Please do continue to send us your News and your Events for promotion. We will have them on the Web within hours of receiving them. Please remember to include your own Website address.

Official Publication for : Reliability, Asset Management & Safety

(RAMS) Conference • Pressure Vessel and Heat Exchange Engineering

Technology Asia Convention • Corrosion Management in Refineries and

Process Plants • FLNG Technology and Unconventional Gas Asia Summit

• Deepwater Technology and Offshore Support Vessel Asia C&E • Onshore Technology Asia C&E

• Jack Up and Semi Submersible Technology Asia Summit • Corrosion

Management, Welding and Composites Technology Asia Convention

Quality Management Training is KeyThe American Petroleum Institute spoke with Paulette San-galang, Deputy General Manager of Operations at Haward Technology Middle East, API-U training provider, to discuss the importance of API Spec Q1 and Spec Q2 training and why companies have an increasing interest in understand-ing quality management excellence.

The Downstream Grapevine

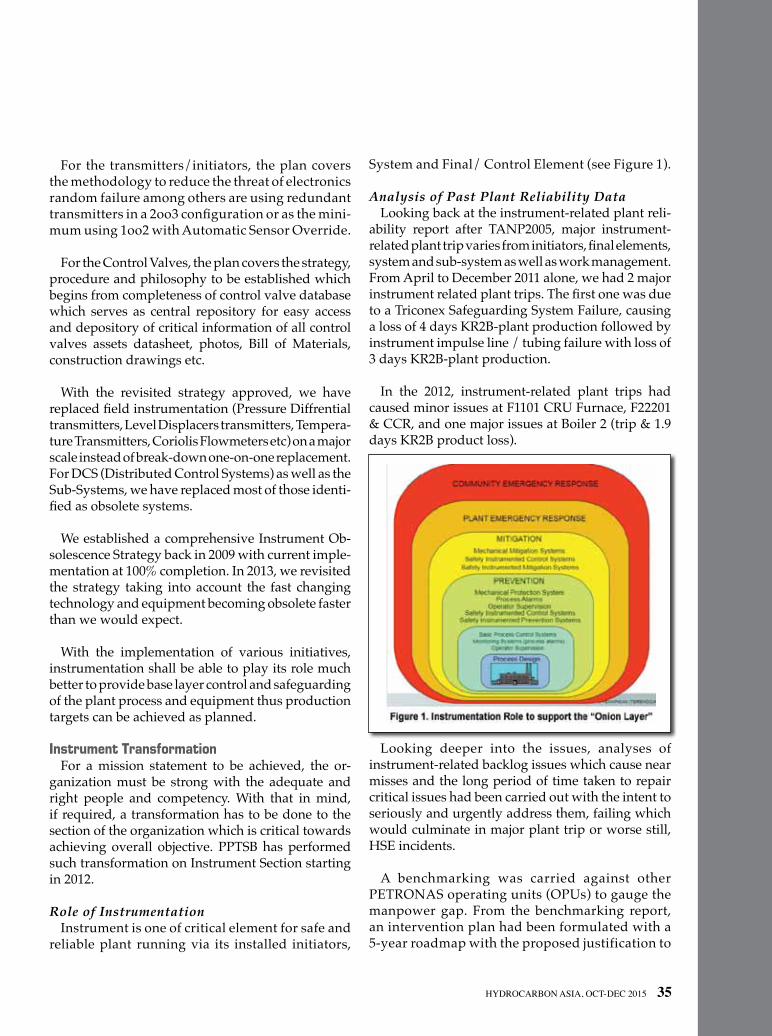

tecHNologYTowards Instrument Asset Management Excellence: PP(T)SB Yesterday, Today and TomorrowReliability of Instrumentation in PPTSB (Petronas Penapisan Terengganu Sdn Bhd), a refinery situated on the East Coast of Peninsular Malaysia is critical. A Five-Year Road-map was drawn out to provide a clear planning, scheduling and prioritisation of initiatives to provide plant instrumentation.

DNV GL Combines Tools to Aid Operational Performance in Rotating EquipmentMany pieces of rotating equipment are operating below optimum capacity, affecting production costs, revenues and resulting in unexpected down time. DNV GL has been working together with operators to help unlock the potential of their existing rotating equipment.

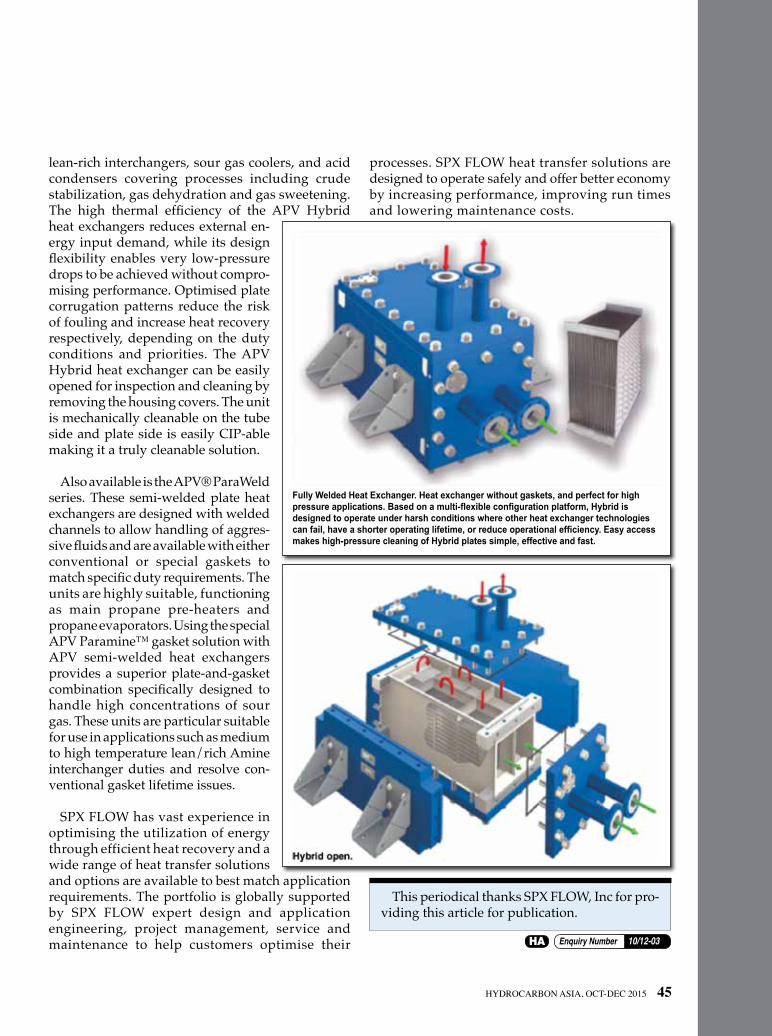

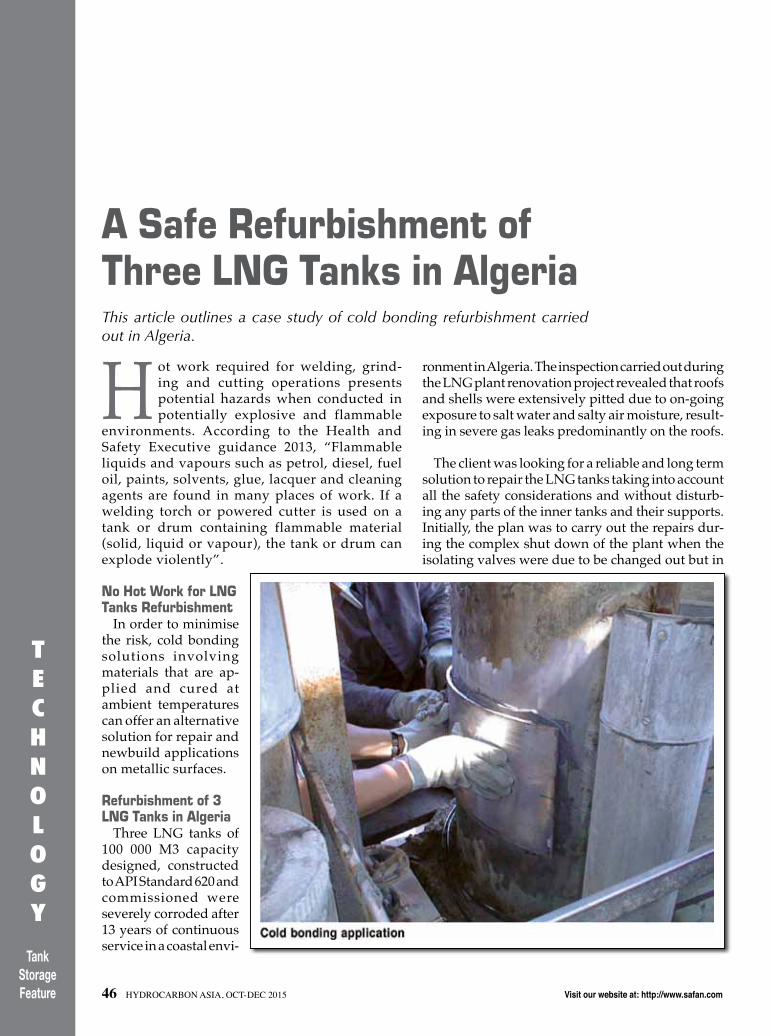

APV® Heat Exchangers Designed to Lower Energy Costs in Oil and Gas ApplicationsEnergy consumption and runtime are key parameters affecting production costs in several sectors. Minimizing energy consumption through more efficient process heat recovery is critical to profitability in the face of increasing energy costs. Improving process performance and avoiding unscheduled stoppages can increase runtime. Both deliver immediate and significant cost savings that translate directly to the bottom line.

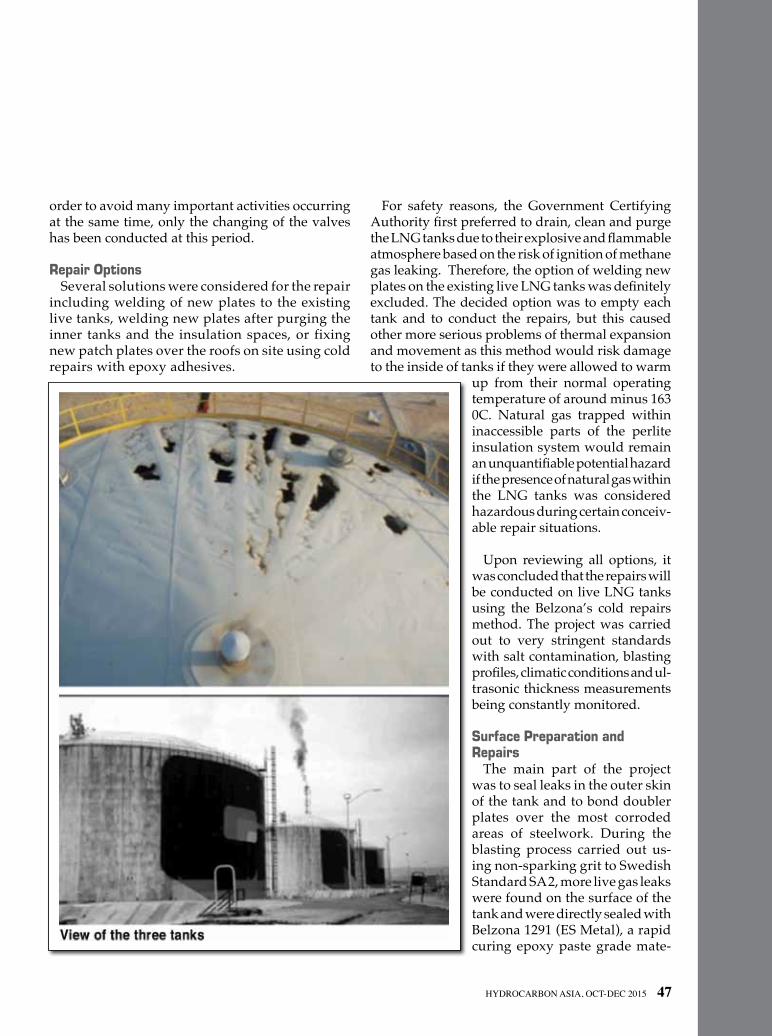

A Safe Refurbishment of Three LNG Tanks in Algeria This article outlines a case study of cold bonding refurbishment carried out in Algeria.

28

34

46

30

42

44

4 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

Publisher/Executive Editor Eddie Raj

Group Editor Vishnu PillaiTel: 6222 3422 ext: 209email: [email protected]

Advertising Co-ordinatorMary Tel: 6222 3422 ext: 206 email: [email protected]

Subscription/Cirulation JaquilynTel: 6222 3422 ext: 201 email: [email protected]

Conference Co-ordinator Zaman Tel: 6222 3422 ext: 204email: [email protected]

Graphic ArtistChua Ai HwaTel: 6222 3422 ext: 211email: [email protected]

Technical consulTanTs

HArry VAn DiJK Business Development Manager Shell Global Solutions - Singapore

ediTorial advisory Board

Dr. FErEiDun FESHArAKiPresident FACT Inc.

EnriCo SiSmonDoManaging Director - SingaporeMUSE Stancil

TAn CHEE HonGRegional ManagerCustomer SalesUniversal Oil Products Asia Pacific Pte Ltd

PAuL KEnnEDyVice PresidentOperationsKBC Advanced Technology Pte Ltd

DAViD TurnErVice President Business DevelopmentKBC Advanced Technology Pte Ltd

Tony AnDErSon Senior Consultant

D. P. miSrAPresidentIndian Institute of Chemical Engineers & MemberBoard of Governors of Engineering Council of India

DAViD onG Managing Director Excel Marco Industrial Systems Pte Ltd

corresPondenTs

Australia/PnGBrian Wickins

Dhaka, BangladeshGhazi Mahmud lqbal

Beijing, ChinaLi PeizhongWang Yong

Delhi, indiaSiddharth Raghavan

new ZealandWarner Saville

PakistanDr Salman Saif Ghouri

Editorial Desk

HA

When Not If….

The downstream sector is really a curious animal. In most, if not all other industries, a decrease in the price of raw materials would be

cause for celebration. However, in the downstream sector of the oil and gas in-dustry, this does not seem to be the case even though leaders in the downstream sector, together with most analysts, ac-knowledge and even promote the fact that lower feedstock costs would trans-late to higher margins. The main reason for this is the fact that most of the major downstream players are upstream play-ers too. Ergo, the downturn in the up-stream sector has cast a pall on its down-stream counterparts.

One of the bigwigs in the refining sector of a regional NOC recently com-mented that the constant drop in the oil price has led him to have sleep-less nights, as oil shares and company shares are part of his remuneration and thus the slide has resulted in the shrink-age of the monetary value of his assets. This puts him in a conundrum where as a downstream proponent, he should be happy as feedstock prices fall but from a personal standpoint, so has his finan-cial portfolio. This is a microcosm of the downstream sector’s dilemma.

Another factor prompting this curi-ous behaviour is that oil prices have a rather direct relationship with the glo-bal economy. When oil prices are up the global economy seems to be on a high; conversely, when oil prices be-gin to fall the global economy starts to flounder. There certainly are rea-sons for this co-relationship between the oil and gas industry and the glo-bal economy (which I am not qualified to assess). Similar the demand for re-fined products is linked to the global economy, though that relationship is rather more straightforward – a boom-ing economy means a greater demand for energy (refined products), and a

depressed economy means a reduced demand for energy.

It also takes time for the industry to react to market conditions. During high demand more facilities are added, whether it be new refineries or capac-ity increments, and these end up being under-utilised during downturns. Such is the current situation. The slowdown of China’s industrial growth has been a major factor, though by no means the only one, as have been economic fluctua-tions in Europe. Development in Asian countries, especially India and some Southeast Asian countries, have helped to ensure a healthy demand remains; however, despite refinery closures in the Pacific region (Australia), there is still a rather prominent margin of over-capaci-ty. On a positive note, the region will be ready when the upturn comes around.

Notice that I said when and not if. If future plans are anything to go by then I am not alone in this thinking. An increase in refining capacity is in the pipeline for a number of countries such as India, Vi-etnam, Thailand, Malaysia and Indone-sia. Considering the costs involved we can be sure that the decision to go ahead with these plans must be well thought out. Despite the limitations of the sector I am positive of the turnaround.

As is the norm, please allow me to take this opportunity, on behalf of all the staff at AP Energy (publishers of Hydrocar-bon Asia), to wish our readers Merry Christmas and Happy New Year. May 2016 be a less arduous year than this. As we look to the future and expansion, Hydrocarbon Asia will be helmed by a new editor next year. I believe he will re-ceive the same support and interest his predecessors had. We look forward to engaging you once again in the upcom-ing year.

Group Editor

6 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

CompanyFocus

REPORT

International Oil and Gas Companies Attend Petrovietnam Conference & Exhibition

Vietnam National Oil and Gas Group’s Conference and Exhibition 2015 with the theme “Petrovietnam - 40

years of integration and develop-ment” is an international event to mark significant milestones through four decades of development - its emergence and contribution to Vietnam’s economy in general as well as to Vietnam’s oil and gas industry in particular.

The event has attracted more than 500 delegates from 80 Vietnamese and international oil and gas companies to take part in. They include 15 key Petrovietnam’s subsidiaries and 59 organisations and companies from Southeast Asia, Europe, the USA and Australia. Among them, the biggest international oil and gas players operating on the Vietnam continental shelf played an important role in the success of the event.

The US oil and gas giant Exxon-Mobil - one of the leading petroleum companies outstanding for its activi-ties in deepwater. Its commercial gas discovery at Ca Voi Xanh field is the largest of its kind ever found in the country with the reserves of strategic significance. The project will in the future be a national scale complex project , which covers from upstream sector to gas pipeline construction and includes two potential gas thermal plants with a combined capacity of 6,000 to 6,500 megawatts. This project is likely to make the United States one of the top

four foreign investors in Vietnam along with Japan, South Korea and the Russia.

Murphy Oil may have seen at the depth of 1.000 - 2.500m of Vietnam East sea. Vietnam is a great potential market with a long-term expansion strategy. Besides, Mexico Gulf is desirable region for Petrovietnam and Murphy Oil cooperation.

Talisman Energy Inc. (Canada) has been exploring and producing oil and gas in Vietnam since 2001 and invested more than USD 3 billion so far on different projects in the country. Currently, Talisman Energy and its partners are supplying around 20% demands of gas for thermal power plants in Vietnam. Even though Repsol S.A has recently replaced Talis-man Energy but Asia and Vietnam is continue to be its potential market for strategic investment. The discover oil fields are Song Doc, Cai Nuoc, Hai Su Trang and Ca Rong Do.

The Russian Federation players are Petrovietnam strategic traditional

partners and have an important contribution to the Vietnam oil and gas industry in the long history. Together with 35-year partner - Zarubezhneft, Rosneft and Gazprom are accounting for increasingly significant role in oil and gas explora-tion and production activities on the Vietnam continental shelf.

Gazprom with its deep sea active operation found commercial oil at Bao Vang, Bao Trang, Bao Den fields, gas production at Hai Thach and Moc Tinh fields should be considered as the steps towards Gazprom penetra-tion into Vietnam Gas industry.

Taking over TNK-BP in 2013 Ros-neft became main gas supplier in Vietnam, operator of Nam Con Son Gas biggest Pipeline. 2015 marks Rosneft 300 million boe production.

Petronas is a long-term partner of Petrovietnam in Southeast Asia with mutual projects in Vietnam, overlap-ping areas and Malaysia, in both upstream and downstream activities as well as other commercial activities.

The operation areas include Song Hong, Cuu Long, Malay - Tho Chu basins, Ruby, To-paz, Pearl, Diamond, Thang Long, Dong Do, 46-Cai Nuoc and Thai Binh, Ham Rong, Gau Chua and Ca Cho.

Over the past half of century, foreign oil and gas contractors have played an important role in Vietnam oil and gas industry de-velopment and society contribution.

In theSpotlight

HA

H.E Prime Minister of Vietnam Nguyen Tan Dung and H.E Prime Minister of Malaysia Najib Rajak witnessed the signing of MOU between Petrovietnam and Petronas on August 7th 2015 in Malaysia.Photo: PVJ

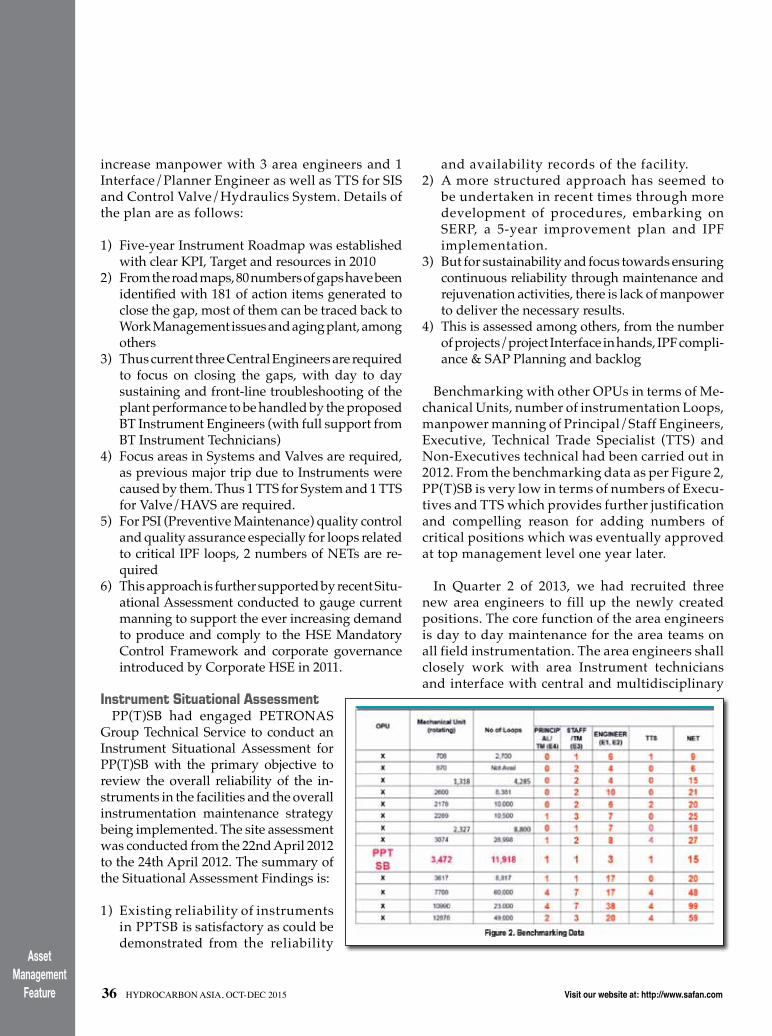

TECHNICAL COMMITTEE:• Kamarul Ariffin Bin Tajul A’mar, Head Centralized Services, PETRONAS

Chemical Group Berhad• Mohd Azmi Mohd Noor, Advisor, Technical Integrity & Process Safety, HSE

Division, Exploration & Production Business, PETRONAS• Grant Vidrine, Regional VP, HSSE & Operational Assurance, Talisman Energy• Michael Costello, Technical Service Manager, Joint Venture & Affiliates,

Chevron International Pte Ltd• Phil Slowther, IMCA, Fugro Group• Dr Krishna M Bala, Director EHS, Hess Asia Pacific• David MacLaren, Technical Advisor, RAMS ASIA

PATRON

Datuk Ir. Kamarudin ZakariaHead, Group Technical Solutions

PETRONAS

The Patrons & Technical Committee Members of the 9th Reliability, Asset Management & Safety Asia Conference (RAMS Asia) cordially invite you to submit your abstract for technical presentations with the theme, “Enhancing Asset Management and Reliability with Futuristic Concepts”.

The event will highlight issues related to maintaining reliable and safe operations while optimizing productivity. The event, seeks to be the premier platform for knowledge and experience sharing in the areas of reliability, asset management and safety at the operational level.

TOPICS: QHSE, Process Safety Management and Reliability, Asset Integrity including RBI, RCM and SIL, En-hanced Safety Practices for Operations as well as installing a platform for Safety Managers, Engineers and Practitioners involved in the UPSTREAM, MIDSTREAM and DOWNSTREAM of gas power sectors.

The recent trend in the oil and gas industries has demanded we examine our usual concepts of Asset Management to search for better ways to care for aging equipment and reduced demand from our existing assets.

Abstracts on relevant topics not included above will also be taken into consideration by the programme committee. The abstract should not exceed 400 words. Abstracts should be submitted by 15 January 2016.

In line with the conference theme and objective, the program committee is careful in selecting the topics and invite speakers to present papers on their own experience and case studies to share with the conference participants. Papers of purely marketing / commercial nature will not be considered. All final papers must be written in MS WORD, to facilitate publication of selected papers in our Energy Publications. PowerPoint used for presentation will not be considered for publication.

The technical committee is in the process of selecting and inviting the industry experts for the appropriate panel sessions and presentations.

Organized by:

Call For Papers

For abstract submission, delegate registration and please contact: [email protected] / [email protected] or call us at +65 6222 3422

9th ReliAbility, ASSet MAnAgeMent & SAfety ASiA ConfeRenCe (RAMS ASiA)Theme: Enhancing Asset Management and Reliability with Futuristic Concepts

25-26 April 2016 • Kuala Lumpur, Malaysia

Abstract Submission Notification of Acceptance Final Paper Submission 15 January 2016 30 January 2016 25 March 2016

Supported by:

In theSpotlight 8 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

PV GAS Concentrates Efforts for Sound and Sustainable Development

Q: After 25 years of establisment and development, PV GAS is now a premier supplier of gas and gas products in Vietnam, contributing to the national e n e r g y s e c u r i t y a n d s u s t a i n a b l e d e v e l o p m e n t o f t h e Vi e t n a m g a s industry. Can you tell us what you consider to be, the most important l a n d m a r k s i n t h e d e v e l o p m e n t o f PV GAS?

Mr. Duong Manh Son: PV GAS was established on September 20th, 1990 with the main goals of gathering, importing, transporting, storing, processing, dis-tributing and trading in gas and its products. Since it brought ashore the first gas flows in 1995, PV GAS has supplied more than 98 billion cubic metres of dry gas, 9.8 million tons of liquefied petro-leum gas (LPG) and nearly 1.6 million tons of condensate. With safe, continu-

RepoRt

ous management and operation, i ts gas collecting, transporting, storing, processing and distributing systems from Cuu Long, Nam Con Son and PM3-Ca Mau basins annually provide gas to produce 35 percent of the country’s elec-tricity, 70 percent of fertilisers and over 70 percent of liquefied petroleum gas for domestic civil and industrial users. PV GAS has built a system of modern facilities for the gas industry with 4 gas pipeline systems: Cuu Long basin - Dinh Co, Nam Con Son 1 - Nam Con Son 2 (Phase 1), PM3 - Ca Mau, and Ham Rong - Thai Binh.

In April 1995, f irst gas f low from Bach Ho field was brought to land with a capacity of 1 million m3 of gas/day to supply Ba Ria Power Plant. This he lped to reduce huge s ta te budget expenditures in foreign currency to

After 40 years of establishment and development, the Vietnam National Oil and Gas Group has grown into a leading economic group in Vietnam, contributing to the assurance of national energy security. As a leading member of PetroVietnam, PetroVietnam Gas Joint Stock Corporation (PV GAS) orientated strategies are developing the gas industry into a leading economic engine, gradually stepping into the world market, securing a high ranking in the ASIAN gas industry, and becoming one of the strongest gas brands in ASIA in 2025. Mr. Duong Manh Son, Member of the Board of Directors, President and CEO of PV GAS has provided Hydrocarbon Asia his views on this issue!

In theSpotlight

HYDROCARBON ASIA, OCt-DeC 2015 9

import diesel oil as a traditional fuel for power plants. With the completion of offshore gas compression plat-forms and an onshore gas pipeline system, PV GAS increased gradually the pipeline capacity up to 3 million m3 of gas/day in 1997, and over 5 million m3 of gas/day in 2002 to transport addi-tional gas sources from other fields of Cuu Long basin.

By the end of 1998, Dinh Co Gas Processing Plant and Thi Vai Terminal came in to operat ion and began to supply LPG and condensate for the Vietnam market for the first time. This marked a great significance in terms o f t e c h n i c a l , e c o n o m i c a n d s o c i a l developments.

In December 2002, the first gas flow from Nam Con Son basin was brought to land and transported to consumers, increasing significantly the gas outputs of PV GAS supplies. After that, the Nam Con Son basin gas system has received additional gas supply from other fields and become the highest capacity gas system with a capacity of over 8 billion m3 of gas per year. Nam Con Son basin gas system and Cuu Long basin gas system have created an important gas system infrastructure for the key economic triangle of Ho Chi Minh City - Dong Nai - Ba Ria Vung Tau in the Southeast.

On 11 May 2007, first gas flow from PM3 field was brought to land to supply p o w e r a n d f e r t i l i z e r p l a n t s i n C a Mau. PM3-46 Cai Nuoc Gas pipeline system with a capacity of 2 billion m3 of gas/year, has contributed to the e c o n o m i c d e v e l o p m e n t o f C a M a u

Province and Mekong River Delta.

In August 2015 , PV GAS put the Ham Rong - Thai Binh gas ultilisation system into operation with a 25km off-shore and onshore gas pipelines and design capacity of 500 million m3 of gas/year, initiating the development of gas consumption in the Northern Vietnam in the coming years.

PV GAS has gradually expanded and completed gas system constructions, o p e r a t e d T h i Va i R e f r i g e r a t e d L P G Storage - the most modern LPG tank system of Vietnam currently; expanded CNG production capacity to provide for markets being far from Gas pipeline networks. Conducting the investment preparat ion and implementat ion o f large-scale projects such as: Block B - O Mon Pipel ine Pro ject , Nam Con Son Pipeline 2, Gas Processing Plants Ca Mau and Nam Con Son 2, Gas Gathering Pipelines - Su Tu Trang field, Thi Vai LNG Import Storage Terminal, Son My LNG Import Storage Terminal, Thai Binh - Ham Rong Gas Project.

Q: What are the future goals of PV GAS?

Mr. Duong Manh Son: To develop PV Gas to have an im age of strength, safety, quality, effectiveness, modernity, cover-ing a complete scope of the whole chain such as: Gas gathering, transporting, processing, storing, trading, services, export and import; to focus on boosting investment in the infrastructure of the gas industry nat ionwide .

To achieve growth rate of revenue: be-tween 18 - 20% per year, of which: Revenue

In theSpotlight 10 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

from gas is 61%, from gas products 17% and from services 22%.

Q: Can you tell us, to deal with the challenges in the coming period, how does Vietnamese gas industry have to innovate technology?

Mr. Duong Manh Son: In the near future, the Vietnam gas industry will face challenges related to the decline in domestic gas production while demand is continuing to rise. This requires long-term solutions, application of modern technologies to supplement gas supply sources, expand markets, improve gas usage, efficiency, increase profits and business sustainability.

To supplement the gas supply, we need to research and implement meas-ures to diversify gas supplies, first of all is to implement importation of LNG drast ical ly. Also , we need to boost research of technological applications and put in the production gas sources having high contents of inert gas, im-purit ies or small/marginal/offshore fields; non-traditional sources of CBM gas, coalif ication gas. This is also a general trend to develop new gas sup-ply sources in countries which have features like Vietnam, which we are interested in implementing.

In addition to supply gas for power production in order to ensure energy security, PetroVietnam/PV GAS will thoroughly advocated enhanced re-covery of valuable products from gas processing plants (such as ethane, propane, butane, condensate); from a certain amount of gas for processing, producing products with high added

value, serving industry development in Vietnam such as ammonia, methanol, plastics PE, PP, PVC, PS, etc.

Wi t h a l e a d i n g e c o n o m i c ro l e i n Vietnam, PetroVietnam/PV GAS will take the lead in applying new modern tech-nology, saving energy and protecting the environment. Currently, over 80% of natural gas is provided to produce electricity, with the new generation of gas power plants (combined cycle), raising the efficiency of energy usage by ~ 50%. However this number is still quite modest.

To improve this problem, PetroVietnam/PV GAS are interested in research and technology applications combined power generation and using up thermal waste for different purposes in order to rise the thermal efficiency of the plants by 70 - 80%. In addition, studies of CO2 recovery from emissions from power plants, supplying gas for transportation to help protect the environment are also focused area.

Q: What main motivation of technol-ogy in the last 5 years has created the breakthrough development of the Vietnam gas industry?

M r. D u o n g M a n h S o n : To a c h i e v e these outstanding achievements in the past 5 years, the application of science - technology really became the main d r i v i n g f o rc e f o r t h e d e v e l o p m e n t o f t h e g a s i n d u s t r y. P V G A S h a s successfully applied technical solutions, modern technologies to manage, op-erate, maintain and protect existing gas constructions such as monitoring and control systems, DCS, SCADA,

HYDROCARBON ASIA, OCt-DeC 2015 11

ROV, smart spindle launch, satellite navigation system, the method of anti-corrosion, pipeline protection, man-agement of materials and equipment and O&M Maximo. The Corporation has developed the processes, plans, equipped with facilities and modern technical equipment allowing allow-ing us to overcome the problems re la ted to gas pro jec ts quick ly and effectively, ensuring continuous and sa fe gas supply.

F o r t h e i m p l e m e n t a t i o n o f n e w projects, PV GAS has always taken a proactive approach, researching and selecting new innovative and efficient technologies, that are consistent with Vietnam's conditions, to ensure that the projects will achieve the best re-sults, especially those related to tech-nology for storage, distribution and usage of LNG - the new fuel source in Vietnam.

Furthermore, the workforce of PV G A S i s c o n s t a n t l y t r y i n g t o l e a r n , gain experience, master the technol-ogy, promote innovation in operating systems and gas projects, successful-ly contributing to many innovations, production rationalization measures to improve the operation of the gas projects, improving labor productiv-ity, operating capacity of gas systems and increasing gas product recovery with high economic value.

Q: What message does PV GAS want to convey to the regional and global gas industries?

Mr. Duong Manh Son: International integration is an inevitable trend. Par-

ticularly in taking into account this context, Vietnam is integrating deeply into the global economy through the signing of new trade agreements. As the flagship unit of the gas industry in Vietnam, PV GAS has also identi-fied as one of the development goals the need to be actively involved in the international market.

In recent years, PV GAS has been ac-tively participating in the international gas industry market, being a reliable customer/partner of large gas groups across the wor ld , such as Gazprom (Russia), Adnoc (UAE), Astomos (Ja-pan). Nam Con Son Gas Pipeline Com-pany is being operated successfully and effectively by joint business be-tween PV GAS, Rosneft and Perenco; LPG import activities from the Middle East and other countries in the region are featured examples of successful cooperation of PV GAS with foreign partners.

In the future, PV GAS will focus on building relationships at many levels of cooperation with international part-ners to implement investment projects as well as in production and business activities, based on equal cooperation, mutual benefit and the strengths of each party, to develop stably and sus-tainably. PV GAS is striving to move up to the top 4 companies based on annual gas business production in the ASEAN region by 2025, and named in the list of major gas companies of Asia.

HA

12 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

CompanyFocus

REPORT

PV GAS and potential for co-operation in LNG import projects

P etroVietnam Gas Joint S t o c k C o r p o r a t i o n (PV GAS) is seeking partners to invest in

a high-priori ty l iquefied natural gas (LNG) import p r o j e c t s . T h e p r o j e c t i s o f n a t i o n a l i m p o r t a n c e a s Vi e t n a m ' s e n e r g y r e -quirement is expected to grow beyond the capacity of current supply over the next 10 years.

Gas shortage in the South of Vietnam is forecasted to be 1 billion m3 in 2020 and increase to over 5 billion m3 in 2025. LNG will play an im-portant and profitable part in meeting that demand.

The LNG import project offers an unique opportunity f o r i n v e s t o r s w h o h a v e strong financial capabilities, competency in long term LNG supply and experience in developing gas markets to get involved at the beginning of Vietnam's LNG industry development.

PV GAS has been ap-pointed by its parent com-pany, Vietnam Oil and Gas Group (PVN), to develop two projects - Thi Vai LNG

receiving and regasification terminal, and Son My LNG receiving and regasification terminal.

The Thi Vai LNG terminal in Ba Ria Vung Tau, southern province of Vietnam, is the first, and the smaller, of the two terminals. It will have a capacity of 1 million tons per year and is scheduled to be completed by 2020. Thi Vai has completed its Front End Engineering Design (FEED) bid and is ready for the next stage. The project aims to supply LNG to industrial customers and independent power plants.

The larger Son My LNG i m p o r t t e r m i n a l w i l l b e located in Binh Thuan, and is expected be operating by 2020 to 2022 with initial capacity of 3 .6 mi l l ion tons per year to supply to power plants in the Son My area. PV GAS is working on the feasibil-ity study of the project. The total investment for the Son My project is estimated to be more than USD1.3 billion. The terminal’s capacity is p l a n n e d t o u p g r a d e t o 6 million tons per year and 10 million tons per year af-

ter 2025 to supply gas to power plants, industrial cus-tomers and other customers in the South Central and the South of Vietnam.

PV GAS is the sole and larg-est gas entity in Vietnam hav-ing extensive experience and expertise in the gas value chain. It is among the top 10 corporate income taxpayers of Vietnam. Vietnam is one of the fastest-growing Asian economies in recent years and is still in its golden period of economic growth.

Low labour costs, alongside an increasingly skilled and educated workforce, mean manufacturing is booming in Vietnam, leading to rising demand for industrial power. At the same time, growing domestic energy consumption is underpinned by rising living standards.

PV GAS’s objectives are to develop a strong, safe, high quality, effective and modern gas industry with a holistic operating range in all stages from gathering, transporting, s t o r i n g , p ro c e s s i n g a n d d i s t r i b u t i n g g a s a n d g a s products.

CompanyFocus

HA

LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Fo-rum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Ma-rine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Fo-rum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Ma-rine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Fo-rum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Ma-rine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Fo-rum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG

Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG

Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG LNG Ma-rine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Fo-rum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2015 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine Fuel Forum 2015 LNG Marine Fuel Forum 2016 LNG

Marine Fuel Forum 2016 LNG Marine Fuel Forum 2016 LNG Marine

• PolicyandStrategy• PricingandConsumptionForecasts• AnOil&GasCompanyView• TheInvestmentFramework• ALegalPerspective• ABankingPerspective• Certification• Environment&Safety

• ApplicationsandEconomics• ProductionandDistributionTrends• LNGFueledOffshoreVesselDesignandEquipment• OperationalEconomics• PracticalExperience• LNG–HandlingandDistribution• LNGBunkering• LNGTechnology

PetroMin,Hydrocarbon Asia,theleadingmagazinesintheOil&GasindustryinAsia,areorganizingthe2nd LNG Marine Fuel Forum,whichwillbeheldinSingaporeon10-11May2016.

TheTechnicalCommitteehasselectedtheTHEME:“ASIAN LNG - Forging Ahead in the Marine Industry”.

“ The MPA is working on various fronts to develop LNG bunkering in the Port of Singapore…and also launched the S12million funding for players seeking to build vessels capable of using LNG as a marine fuel. A technical committee formed under Spring Singapore’s National Standardization Program is in place to develop standard procedures and technical operations for LNG bunkering operations. To ensure overall development of LNG bunkering across the globe, the MPA has also signed MOUs with the Ports of Antwerp, Zeebrugge and Rotterdam and will be looking into the harmonization of LNG bunkering procedures. ”

Dr. Parry OeiDirector Port Services and Chief Hydrographer, Maritime Port Authority of Singapore (MPA)

CONFereNCe CHAIrMAN AND TeCHNICAL COMMITTeeWong Toon Suan,MDofONEBLUE;ExecutiveAdvi-sorofILO,NationalUniversitySingapore;ConferenceChairmanelsie Tang,ConsultantofDNVGLMaritimeAdvisory(Singapore)rolv Stokkmo,ManagingDirectorofGasPartners

Denis Welch,ChairmanofOneWorldMaritimePteLtd;IMCARegionalDirectorAsiaPacificTesch Alexander,DirectorofSalesMarine&Offshore,MTUAsiaAbul Bashar Md Masum reza, Asst.PrincipalRe-searchEngineer,KeppelOffshore&MarineTechnologyCentre(KOMTech)

CONFereNCe TOPICS

The technical committee invites you to present papers in this conference. The conference will be an excellent platform for the authors and speakers to address a highly sophisticated and experienced audience.

Theabstract,whichshouldnotexceed400words,shouldbesenttousviaemail.Thecommitteememberswillreviewthewrittenpaperstoensurethatthecontentisinlinewiththeobjectiveoftheconference.Pleasenotethatpapersofapurely marketing / commercial nature will not be considered.

Forthebenefitoftheindustry,selectedpaperswillbepublishedinHydrocarbon Asia MagazineorPetroMin(inprint)andwillalsobepresentedonthewebsite.

Forabstractsubmissionandfurtherinformationpleaseemail:[email protected] / [email protected]

Organised by:

LNG Marine Fuel Forum 2016Theme: AsiAn LnG - Forging Ahead in the Marine industry 10 - 11 May 2016 • Singapore

CALL FOR PAPERs

AbstractSubmissionDeadline15 January 2016 FinalPaperSubmissionDeadline15 March 2016

14 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

Regional Feature

REPORT

LNG a Boon for Australia

Australia is rich in com-modities, including fos-sil fuel and uranium reserves. It is one of

the few countries belonging to the Organization for Economic Cooperation and Development (OECD) that is a significant net energy exporter, sending nearly 70% of its total energy produc-tion (excluding energy imports) overseas, according to data from Australia's Bureau of Resource and Energy Economics (BREE).

The majority of revenue in the Petroleum Refining and Petroleum Fuel Manufacturing industry is

generated by four major oil refiners that process crude oil into a range of fuels and secondary products for downstream markets. The purchase of crude oil by major players dominates the industry's cost structure. This input cost, in conjunction with exchange rate movements, contributes to significant revenue volatility as movements in the world price are passed on to domestic markets in little over a week.

Australia is a net importer of both crude oil and oil products because its consumption of both energy sources exceeds overall

production. In 2013, net crude oil imports were 253,000 bbl/d, and net product imports were 325,000 bbl/d, according to the Australia's Bureau of Statistics data. The country's northern and northwestern regions rely on oil product imports resulting from the lack of sufficient regional refining capacity, while the eastern side imports crude oil for its refineries and domestic markets. Singapore supplies about 47% of Australia's oil product imports, with the most of the remainder coming from refiners in Japan and South Korea. Most crude oil imports are from

Regional Feature

This regional report focuses on Australia, the largest energy entity in the Pacific Rim. Despite refinery closures in the last few years, Australia is gas rich and a leading LNG exporter.

The industry is in a decline phase of its life cycle. Several refineries have closed in the past five years causing produc-tion volumes to decline significantly as the indus-try’s production sites fail to keep pace with newer and larger facilities in the Asia-Pacific region. Some major players have chosen to renew their refineries supplying Australia in neighbouring countries, converting older, domestic plant to fuel import termi-nals. The lower production costs and technological ef-ficiencies of international refineries have resulted in the industry’s declining market share.

HYDROCARBON ASIA, OCt-DeC 2015 15

Malaysia, United Arab Emirates, and Indonesia, which altogether produced about 48% of the total imports in 2013. Another 20% of crude oil imports comes from West Africa, as Nigeria, Congo, and Gabon have increasingly supplied crude oil to Australia in recent years.

According to FGE, Australia had 6 major refineries at the beginning of 2014, with a total crude oil re-fining capacity of 634,000 bbl/d operated by BP, ExxonMobil, Shell, and Caltex Australia. Scheduled refinery closures will reduce this capacity to 414,000 bbl/d by the end of 2015. Crude oil feedstock for these refineries comes from domestic oil produced in the Bass Strait offshore of southeastern Australia and from the coun-try's crude oil imports. Refining throughput meets an estimated 56% of domestic demand, accord-ing to FGE. As refining capacity diminishes in Australia, this share will also decline as petroleum product imports increase.

Australia's refining margins have tightened, and the major refiners are taking financial losses as a result of increasing refinery competition within Asia, Austral-ia's escalating labour and operating costs, stricter environmental standards on fuels, and higher prices of imported crude oil. Aus-tralia's refineries are small and dated compared to the larger and more com-plex refineries being built within Asia.

These unfavourable eco-nomics have pressured operators to close several facilities and convert some of them to oil product im-port terminals. ExxonMo-bil closed its 80,000 bbl/d Adelaide refinery in 2003.

Shell also shut down the 85,000 bbl/d Clyde refinery, located near Sydney, in late 2012, which had contributed to Australia becoming Asia's top diesel importer. Planned closures include Caltex's 125,000 bbl/d-Kurnell refinery located near Sydney by the end of 2014 and BP's Bulwer Island facility by mid-2015. Shell announced the sale of its 105,000 bbl/d-Geelong refinery to oil trading company Vitol in 2014, leaving the fate of this refinery uncertain. Overall, these refinery closures represent about half of the capacity in operation a decade ago, and these closures will likely lead to increases in the country's petroleum product imports, particularly for diesel, gasoline, and jet fuel.

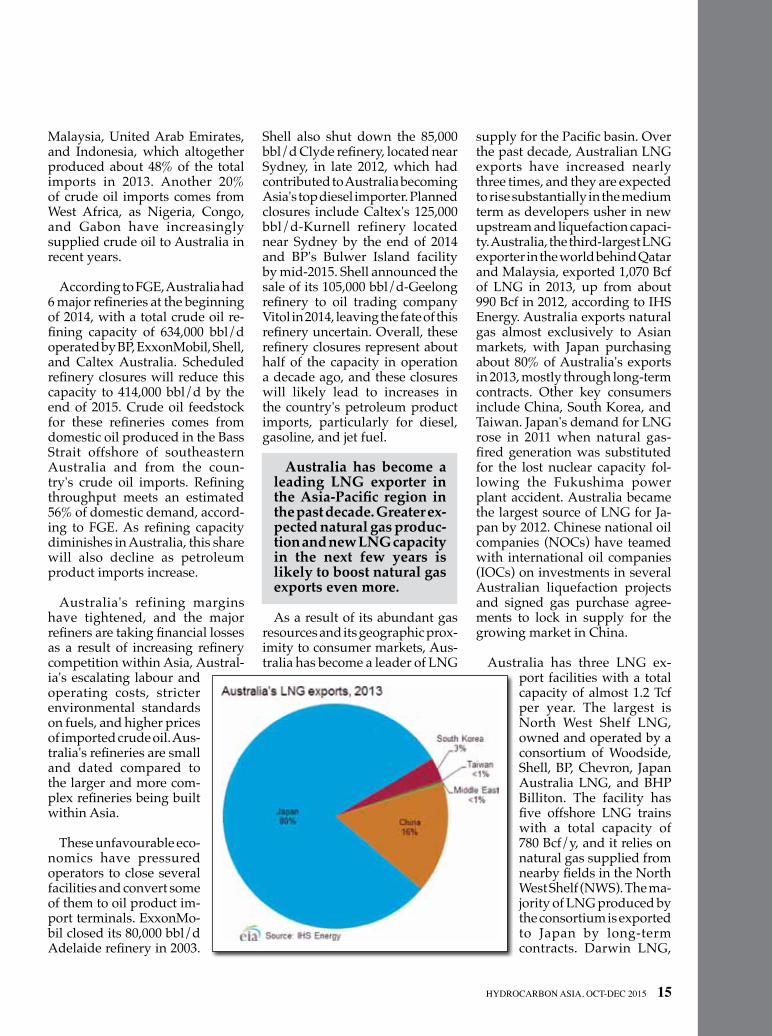

Australia has become a leading LNG exporter in the Asia-Pacific region in the past decade. Greater ex-pected natural gas produc-tion and new LNG capacity in the next few years is likely to boost natural gas exports even more.

As a result of its abundant gas resources and its geographic prox-imity to consumer markets, Aus-tralia has become a leader of LNG

supply for the Pacific basin. Over the past decade, Australian LNG exports have increased nearly three times, and they are expected to rise substantially in the medium term as developers usher in new upstream and liquefaction capaci-ty. Australia, the third-largest LNG exporter in the world behind Qatar and Malaysia, exported 1,070 Bcf of LNG in 2013, up from about 990 Bcf in 2012, according to IHS Energy. Australia exports natural gas almost exclusively to Asian markets, with Japan purchasing about 80% of Australia's exports in 2013, mostly through long-term contracts. Other key consumers include China, South Korea, and Taiwan. Japan's demand for LNG rose in 2011 when natural gas-fired generation was substituted for the lost nuclear capacity fol-lowing the Fukushima power plant accident. Australia became the largest source of LNG for Ja-pan by 2012. Chinese national oil companies (NOCs) have teamed with international oil companies (IOCs) on investments in several Australian liquefaction projects and signed gas purchase agree-ments to lock in supply for the growing market in China.

Australia has three LNG ex-port facilities with a total capacity of almost 1.2 Tcf per year. The largest is North West Shelf LNG, owned and operated by a consortium of Woodside, Shell, BP, Chevron, Japan Australia LNG, and BHP Billiton. The facility has five offshore LNG trains with a total capacity of 780 Bcf/y, and it relies on natural gas supplied from nearby fields in the North West Shelf (NWS). The ma-jority of LNG produced by the consortium is exported to Japan by long-term contracts. Darwin LNG,

16 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

Regional Feature

operated by the consortium of ConocoPhillips, Santos, Eni, IN-PEX, Tokyo Gas, and Tokyo Elec-tric (TEPCO) is Australia's second facility. It has one production train with capacity of 170 Bcf/y and exports LNG under contracts to Tokyo Gas and Tokyo Electric. Darwin, located on Australia's northern coast, is supplied with natural gas from the Bayu-Undan field in the Timor Sea. Pluto LNG is Australia's most recent terminal to come online in 2012. Located in the Northwest region, Pluto LNG has a capacity of more than 200 Bcf/y. Woodside is discussing ex-pansion plans for Pluto LNG, but difficulties procuring additional gas reserves nearby and rising project costs pose challenges to the expansion moving forward.

As new LNG facilities and ex-pansions of existing facilities come online within the next decade, Australia's LNG export capacity is set to expand substantially. Most of the liquefaction projects are located in the coastal or offshore northwestern Australia and in the northeastern Queensland region. Some projects such as Ichthys are designed to produce associated condensates and LPG. Currently, there are 7 projects under con-struction with a total capacity of 3 Tcf/y, 3 in Queensland and 4 in the basins of the northwest coast and offshore. These projects are sched-uled to commence operations by 2017. Other projects are waiting on regulatory approval or final invest-ment decisions, although these projects are facing competition and delays because of escalating costs and potential overcapacity for the amount of available natural gas supply. Australia currently has more than $190 billion worth of LNG projects under construc-tion, and the country is on target to overtake Qatar as the world's largest LNG exporter by 2020, ac-cording to industry sources.

Australia Existing and Planned Export Liquefac-tion Terminals

CBM-to-LNG projects have become feasible with the sizeable amount of gas reserves associated with the coal production. Queens-land Curtis LNG could become the world's first LNG project of this kind, with two neighboring projects under construction and two other projects waiting on final investment decisions. Even though many companies are lev-eraging the vast CBM resources in Queensland to convert the fuel to LNG, CBM projects pose unique challenges to production. There are typically more hurdles for environmental approval. Also, CBM wells produce much less than traditional gas wells and ramp up to peak production over

a much longer period, according to PFC Energy.

Australia's burgeoning LNG industry faces acute capital cost escalation requiring much larger investments for new greenfield projects and has delayed or can-celled some proposed projects. According to FGE and IHS Energy, cost increases are attributed to a number of factors such as labor shortages and resultant high wag-es, high material costs and changes in engineering requirements, ap-preciation of the Australian dollar to the U.S. dollar between 2009 and 2013, greater environmental hur-dles because of stricter regulations, land rights issues, and the remote locations of some projects. Several projects have experienced notable cost inflation such as Ichthys, Gor-

HYDROCARBON ASIA, OCt-DeC 2015 17

gon, Wheatstone, Gladstone, and Queensland Curtis. Pluto LNG also incurred budget overruns by 30% from its original financial investment decision (FID) in 2007. Ichthys LNG, sanctioned in 2012, is currently the world's most ex-pensive liquefaction project on a per unit basis, and Chevron's Gorgon LNG project cited cost increases of 46% in U.S. dollar terms since the project's final investment decision, from $37 billion to $54 billion.

Some of the economic and re-source constraints have caused several equity partners to pri-oritize and reduce their project portfolio stakes and even exit some projects. Also, some neigh-boring projects face competition with each other for contracted

gas supply and limited natural gas production especially in the eastern part of Australia. In Aus-tralia's high-cost environment, international companies are begin-ning to target their investments towards projects in more advanced stages and could shift focus to the expansion of existing facilities or projects currently under construc-tion versus new projects in the planning phase. In 2014, Shell sold its 6.4% stake in the Wheatstone LNG project to partner, KUFPEC, a Kuwaiti company and decided to delay project development for Arrow LNG. As less expensive natural gas from Russia, the United States, and Africa is brought on-line and exported, Australia faces global LNG supply competition for projects that are not currently under construction.

To reduce project costs and to liquefy gas from fields that are far from shore, companies are turning to the floating liquefied natural gas (FLNG) terminal design, which is less expensive than the cost of an onshore plant. Prelude LNG, located in the Browse Basin off the northwest coast, is slated to become the world's first FLNG terminal by 2017 by using a new technology developed by Shell. Woodside decided to convert Browse LNG from a land-based terminal to a floating terminal in 2013 to reduce the massive project costs. Gaz de France and Santos cancelled the Bonaparte LNG project in 2014. Despite the FLNG design of Bonaparte LNG, the companies determined that the rates of return on investment were too low based on the project's ris-ing costs and small gas resource base. Natural gas from the fields may be able to feed other more advanced LNG projects or piped to the domestic market.

ReferencesAAP NewsfeedABC.netAPA Group (APA)Asia PulseAustralian Bureau of Resources and Energy Economics (BREE)Australian Bureau of Statistics (ABS)Australian Petroleum Produc-tion and Exploration Association Ltd. (APPEA)Energy Intelligence FinanceFACTS Global EnergyIBIS WorldIHS EnergyNewsbase Asian OilPFC EnergyPlatt's Oilgram NewsReutersRigzone NewsSantosThe AustralianU.S. Energy Information Ad-ministration HA

Plans for $700m Gladstone Oil Refinery Revealed

Plans are being drawn up to build Australia's first major oil refinery in 50 years in central Queensland. The United States based Eagle Ford Oil and Gas Corpora-tion and Australia's Casper Energy will jointly develop the $700 million project near Gladstone.

Initially the refinery would produce 43,500 barrels a day, turning crude oil into high quality diesel and premium gasoline. The companies said it will help produce a secure fuel industry for Australia and price competitiveness.

In 2014 about 60 per cent of all liquid fuels consumed in Australia were imported, the companies said in statement.

"In the very near future Australia is expected to

have only four of an origi-nal eight oil refineries with a combined capacity of only 490,000 barrels per day versus demand of over 1.25 million barrels per day," the companies said. "Diversity in crude processing capabil-ity reduces the likelihood of exposure to risk of supply in-terruptions due to economic and political volatility in world markets."

Gladstone Mayor Gail Sellers said the refinery would buoy the town's em-ployment as the construc-tion of liquefied natural gas plants on Curtis Island wound down.

The project could create 1,000 construction jobs and 300 operational positions.

"This is an amazing project and just what Gladstone needs, another little boost for us," she said.

18 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

IndustryOverview

Asian Refining & Marketing 2016 Outlook

The report proposes that the 2016 Asian refining and marketing outlook will be stable. This is because low

oil prices and easing capacity over-hang will keep margins healthy.

EBITDA - Earnings Before Interest, Taxes, Depreciation and Amortization'

EBITDA is an indicator of a company's financial per-formance which is calculated in the following manner:

EBITDA = Revenue - Expenses (excluding tax, interest, depreciation and amortization).

EBITDA is essentially net income with interest, taxes, depreciation, and amortiza-tion added back to it, and can be used to analyze and com-pare profitability between companies and industries because it eliminates the effects of financing and ac-counting decisions.

The report has divided the sec-tor’s outlook into three categories – negative, stable and positive. A negative industry outlook indi-cates our view that fundamental business conditions will worsen. A positive outlook indicates that we expect fundamental business conditions to improve. A stable industry outlook indicates that conditions are not expected to change significantly. Since indus-try outlooks represent our for-ward looking view on conditions that factor into ratings, a negative (positive) outlook indicates that negative (positive) rating actions are more likely on average.

Proposed OutlooksA modest EBITDA growth and

easing capacity overhang support a stable outlook.

NegativeThe following are the factors

that could change the sector’s outlook to negative:

• Net refining capacity addi-tions in Asia materially out-pace demand growth, leading

us to project a 10% or more decline in industry EBITDA.

• Contraction in refined prod-uct demand from China and India.

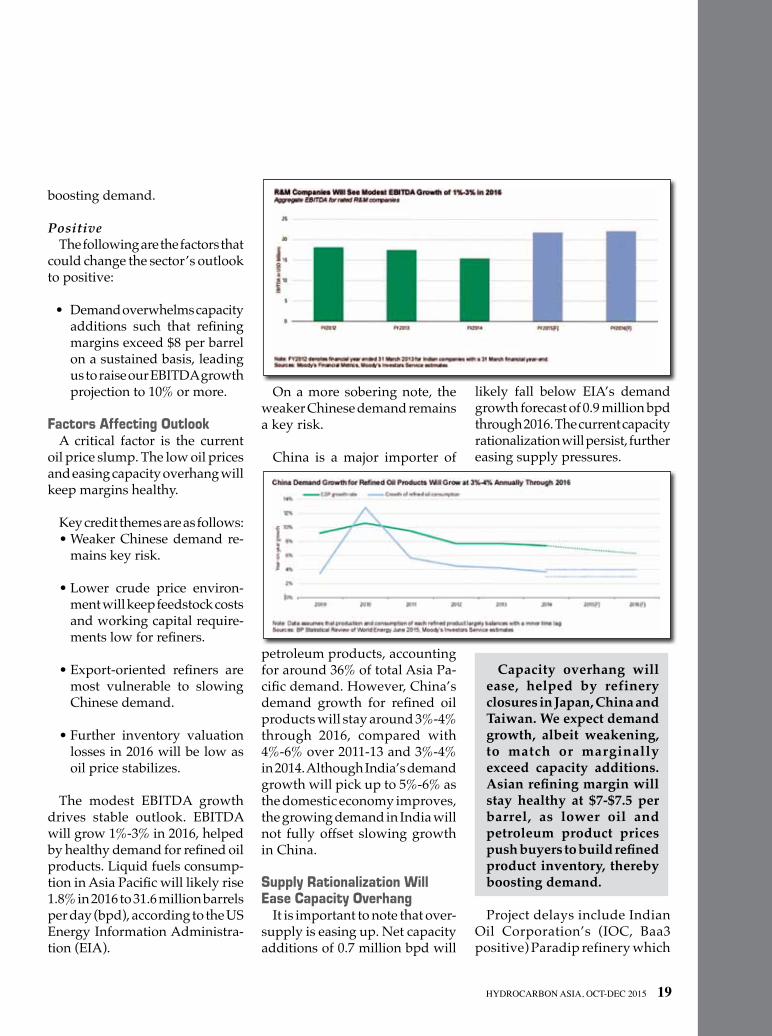

StableThe industry’s EBITDA will

grow by around 1%-3%through 2016, driven by healthy petroleum product demand and stable refin-ing margins.

The following are the factors that could maintain the stability of the sector’s outlook:

• Capacity overhang will ease, helped by refinery closures in Japan, China and Taiwan. We expect demand growth, albeit weakening, to match or marginally exceed capacity additions.

• Asian refining margin will stay healthy at $7-$7.5 per bar-rel, as lower oil and petroleum product

prices push buyers to build re-fined product inventory, thereby

REPORT

IndustryOverview

Moody's says that the Asian refining and marketing outlook remains stable and low oil prices and easing capacity overhang will keep margins healthy. Industry’s EBITDA will grow by around 1%-3% through 2016, driven by healthy petro-leum product demand and stable refining margins. This article is an adaptation of Moody’s latest presentation “Refining & Marketing –Asia: 2016 Outlook –Modest EBITDA Growth and Easing Capacity Overhang Support Stable Outlook”.

HYDROCARBON ASIA, OCt-DeC 2015 19

boosting demand.

PositiveThe following are the factors that

could change the sector’s outlook to positive:

• Demand overwhelms capacity additions such that refining margins exceed $8 per barrel on a sustained basis, leading us to raise our EBITDA growth projection to 10% or more.

Factors Affecting OutlookA critical factor is the current

oil price slump. The low oil prices and easing capacity overhang will keep margins healthy.

Key credit themes are as follows:• Weaker Chinese demand re-

mains key risk.

• Lower crude price environ-ment will keep feedstock costs and working capital require-ments low for refiners.

• Export-oriented refiners are most vulnerable to slowing Chinese demand.

• Further inventory valuation losses in 2016 will be low as oil price stabilizes.

The modest EBITDA growth drives stable outlook. EBITDA will grow 1%-3% in 2016, helped by healthy demand for refined oil products. Liquid fuels consump-tion in Asia Pacific will likely rise 1.8% in 2016 to 31.6 million barrels per day (bpd), according to the US Energy Information Administra-tion (EIA).

On a more sobering note, the weaker Chinese demand remains a key risk.

China is a major importer of

petroleum products, accounting for around 36% of total Asia Pa-cific demand. However, China’s demand growth for refined oil products will stay around 3%-4% through 2016, compared with 4%-6% over 2011-13 and 3%-4% in 2014. Although India’s demand growth will pick up to 5%-6% as the domestic economy improves, the growing demand in India will not fully offset slowing growth in China.

Supply Rationalization Will Ease Capacity Overhang

It is important to note that over-supply is easing up. Net capacity additions of 0.7 million bpd will

likely fall below EIA’s demand growth forecast of 0.9 million bpd through 2016. The current capacity rationalization will persist, further easing supply pressures.

Capacity overhang will ease, helped by refinery closures in Japan, China and Taiwan. We expect demand growth, albeit weakening, to match or marginally exceed capacity additions. Asian refining margin will stay healthy at $7-$7.5 per barrel, as lower oil and petroleum product prices push buyers to build refined product inventory, thereby boosting demand.

Project delays include Indian Oil Corporation’s (IOC, Baa3 positive) Paradip refinery which

20 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.com

IndustryOverview

was scheduled to commence production in 2012 but is now likely to come on-stream in late 2015.

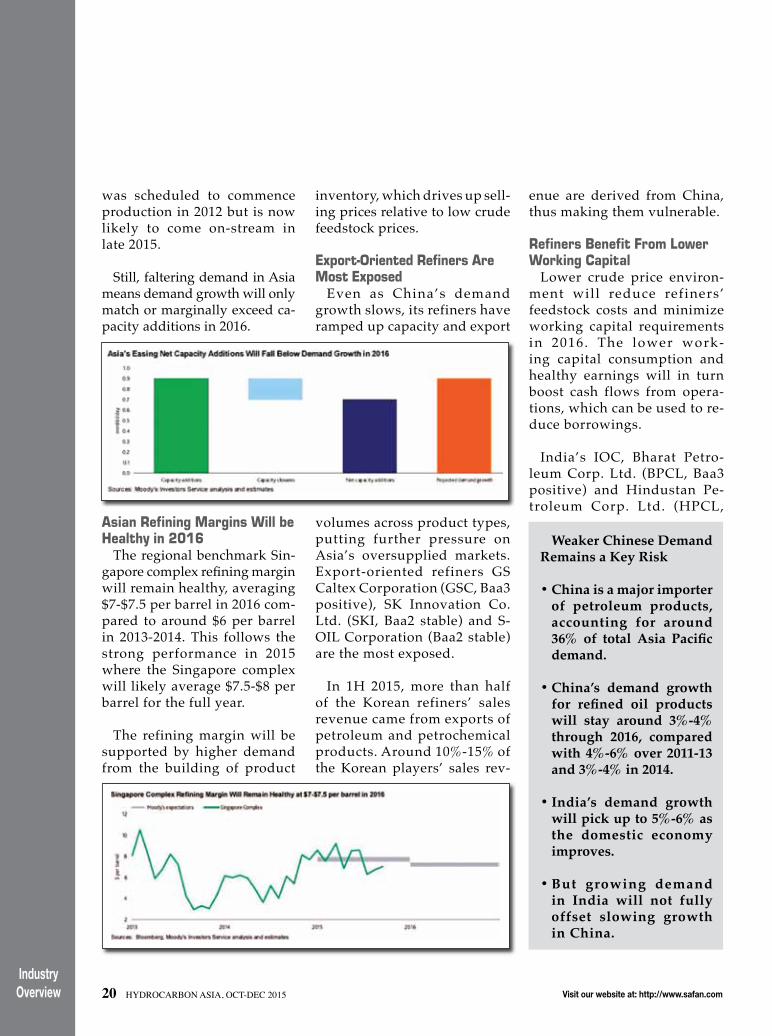

Still, faltering demand in Asia means demand growth will only match or marginally exceed ca-pacity additions in 2016.

Asian Refining Margins Will be Healthy in 2016

The regional benchmark Sin-gapore complex refining margin will remain healthy, averaging $7-$7.5 per barrel in 2016 com-pared to around $6 per barrel in 2013-2014. This follows the strong performance in 2015 where the Singapore complex will likely average $7.5-$8 per barrel for the full year.

The refining margin will be supported by higher demand from the building of product

inventory, which drives up sell-ing prices relative to low crude feedstock prices.

Export-Oriented Refiners Are Most Exposed

Even as China’s demand growth slows, its refiners have ramped up capacity and export

volumes across product types, putting further pressure on Asia’s oversupplied markets. Export-oriented refiners GS Caltex Corporation (GSC, Baa3 positive), SK Innovation Co. Ltd. (SKI, Baa2 stable) and S-OIL Corporation (Baa2 stable) are the most exposed.

In 1H 2015, more than half of the Korean refiners’ sales revenue came from exports of petroleum and petrochemical products. Around 10%-15% of the Korean players’ sales rev-

enue are derived from China, thus making them vulnerable.

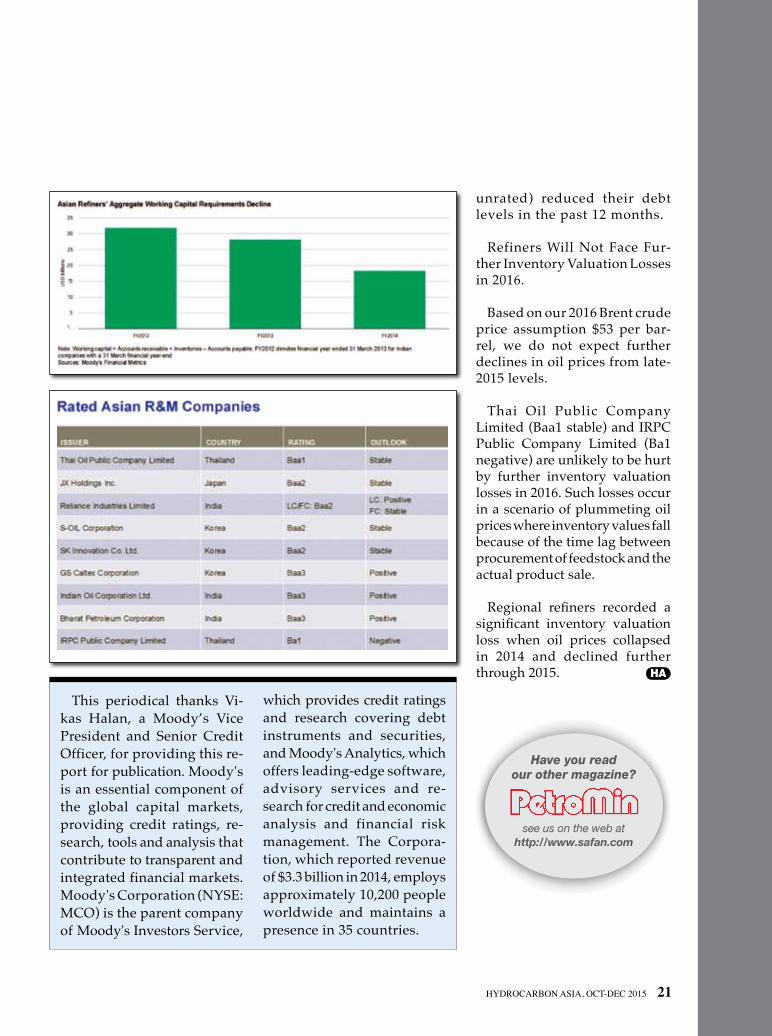

Refiners Benefit From Lower Working Capital

Lower crude price environ-ment will reduce refiners’ feedstock costs and minimize working capital requirements in 2016. The lower work-ing capital consumption and healthy earnings will in turn boost cash flows from opera-tions, which can be used to re-duce borrowings.

India’s IOC, Bharat Petro-leum Corp. Ltd. (BPCL, Baa3 positive) and Hindustan Pe-troleum Corp. Ltd. (HPCL,

Weaker Chinese Demand Remains a Key Risk

• China is a major importer of petroleum products, accounting for around 36% of total Asia Pacific demand.

• China’s demand growth for refined oil products will stay around 3%-4% through 2016, compared with 4%-6% over 2011-13 and 3%-4% in 2014.

• India’s demand growth will pick up to 5%-6% as the domestic economy improves.

• But growing demand in India will not fully offset slowing growth in China.

HYDROCARBON ASIA, OCt-DeC 2015 21

HA

Have you readour other magazine?

see us on the web athttp://www.safan.com

unrated) reduced their debt levels in the past 12 months.

Refiners Will Not Face Fur-ther Inventory Valuation Losses in 2016.

Based on our 2016 Brent crude price assumption $53 per bar-rel, we do not expect further declines in oil prices from late-2015 levels.

Thai Oil Public Company Limited (Baa1 stable) and IRPC Public Company Limited (Ba1 negative) are unlikely to be hurt by further inventory valuation losses in 2016. Such losses occur in a scenario of plummeting oil prices where inventory values fall because of the time lag between procurement of feedstock and the actual product sale.

Regional refiners recorded a significant inventory valuation loss when oil prices collapsed in 2014 and declined further through 2015.

This periodical thanks Vi-kas Halan, a Moody’s Vice President and Senior Credit Officer, for providing this re-port for publication. Moody's is an essential component of the global capital markets, providing credit ratings, re-search, tools and analysis that contribute to transparent and integrated financial markets. Moody's Corporation (NYSE: MCO) is the parent company of Moody's Investors Service,

which provides credit ratings and research covering debt instruments and securities, and Moody's Analytics, which offers leading-edge software, advisory services and re-search for credit and economic analysis and financial risk management. The Corpora-tion, which reported revenue of $3.3 billion in 2014, employs approximately 10,200 people worldwide and maintains a presence in 35 countries.

22 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.comBottomline

Driving Up Profitable Downstream Dollars

Advanced planning soft-ware delivers greater profit -capitalising on potential downstream

dollars is essential to remain competitive in the energy in-dustry. Shifting demand pat-terns caused by volatile crude prices and new crude oi l sources can greatly affect the profitability of a refinery. Therefore, planners must adapt quickly to navigate the fluctu-ating economic storm. The use of advanced and innovative planning software can make the difference to easily identify more robust planning solutions for a true global optimum.

The mismatch between sup-ply and demand, however, has led to a global glut of oil. On the supply side, turmoil in the Middle East has not stifled production. There has been no reduction in output from places like Saudi Arabia or other Gulf states. The strong growth of US tight oil in shale gas feedstock is increasingly moving westward to the east. Demand on the other hand in areas like Europe is reduced

due to weak economic activity and the move to renewables. The global spare refining capacity is already above its low in recent years, which indicates that there will be a long period where refineries are being forced to reduce plant capacity, whilst they are struggling to be operationally efficient. The trend for energy demand growth in China and India continues, but the long-term future is uncertain.

Securing every possible dol-lar available downstream can be achieved by implementing advanced planning software, which provides the answer to the burning day-to day plan-ning questions, such as “which c ru d e s t o b u y ? ” “ W h i c h products to make?” “How to capitalise on new crudes and feedstock on the market?” “How to effectively manage a complex crude slate with limited storage?” Innovative software helps to make the right decisions, increase ac-curacy in yield predictions and reduce model maintenance for optimal refinery planning.

Making Good Crude Purchase Decisions

Determining which crudes will be most profitable to run and anticipating product demand requires the best planning tools to make quicker and more profitable decisions. Reacting to discrepancies between the plan and schedule is also vital to fully exploit profitable deci-sions in the supply chain and also be able to capitalise on newly available feedstocks like global shale plays.

The challenge is that with new crudes and feedstocks on the market, what is the most effec-tive way to manage a complex crude slate with limited storage capacity? Which crudes will yield the most profitable prod-ucts? With options comes com-plexity and decisions become much more difficult. For exam-ple, process units can be run in different ways to make different products. As the price of crude changes, those refineries famil-iar with running “dirty” crudes might change their operations now that the lighter, sweeter crudes are less expensive. Spot

REPORT

Bottomline

The article highlights that being able to quickly analyse and produce different scenarios delivers swift results. By opening the gateway to a world of new opportunities, refineries are better equipped to explore even more ways to optimise their planning, grow the business and boost profit.

HYDROCARBON ASIA, OCt-DeC 2015 23

crude opportunities too could become available that the refin-ery might consider purchasing. Therefore, the planner has to be agile enough to determine if the crude is suitable and how to change the plan to accommodate the new feedstock.

Exploiting Feedstock Flexibility With powerful planning

tools, planners can run more scenarios faster, gain more time for analysis and respond quickly to traders by making more robust decisions in a dy-namic environment. This will achieve a realistic and optimal target and achieve accurate planning that increases profit.

For years planners have used model-based planning systems, such as Aspen PIMS™ to help make more optimal decisions - the tool of choice used to plan 75% of the world’s refineries. However, historically it was challenging to find the elusive “global optimum” that spans across a large number of refin-ery operating conditions and different crudes types. Many times “local optima” are en-countered, which are sometimes difficult to identify. With Aspen PIMS-AO (Advanced Optimisa-tion), planners can now quickly determine a global optimum that leads to improved profit-ability of refineries.

In essence, there are three

key benefits to using advanced planning tools compared to standard applications:

• Performance: run more scenarios faster than ever

• Stability: reduce crudes logistics complexity by determining minimum number of crudes to run using the Feedstock Basket Reduction tool

• Optimum: easily determine the global optimum for the best possible solution

Companies have successfully reduced their run times from 30 hours to 90 minutes with Aspen PIMS-AO, which makes an enormous difference to reach-ing the decision point earlier in the process. Additional time can be spent to further analyse results and different scenarios. On a separate point, case com-parison runs have been known to reduce from 30 hours to only 18 minutes.

“By reducing our crude slate from seven crudes to five we made 15 - 20 cents more per barrel.”

– Multinational Oil & Gas Company

By using newly developed collaborative tools, this sophis-ticated software system enables planners to deliver optimal plans faster and more easily. They can visualise and evaluate multiple scenarios along with plant data to make better and more profitable decisions. It

HA

Have you readour other magazine?

see us on the web athttp://www.safan.com

de-mystifies the plan by provid-ing clearly displayed data with an easy-to-use interface on a common platform available to all key stakeholders.

Capitalising On the Downstream Dollars

Getting an edge in the energy industry is essential in today’s market. The opportunity to capitalise on the downstream dollars is achievable with advanced planning software. Being able to quickly analyse and produce different scenarios delivers swift results. By open-ing the gateway to a world of new opportunities, refineries are better equipped to explore even more ways to optimise their planning, grow the busi-ness and boost profit.

This periodical thanks Nirmala Arifin, Director of Business Consulting and Allison McNulty, Pe-troleum Supply Chain Manager, AspenTech, for providing this article for publication.

24 HYDROCARBON ASIA, OCt-DeC 2015 Visit our website at: http://www.safan.comSafety

Transforming the Safety Culture

Change requires believers; people who are willing to deviate from the well-trodden path to carve a

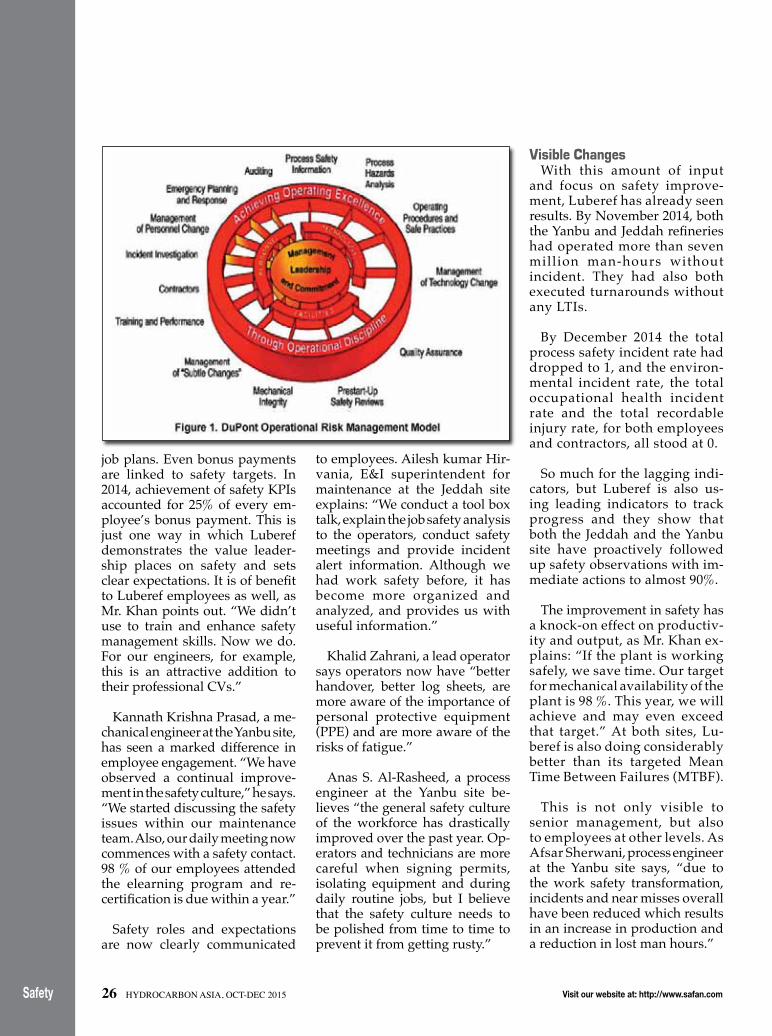

new one. But that takes courage, effort, time and dedication. All of which Saudi Aramco Base Oil Company-Luberef decided to commit on a November day at the end of 2011 to improve the com-pany’s safety performance which had plateaued. In discussion with DuPont Sustainable Solutions (DSS) the company embarked on a journey to unlock its potential for an improved safety management system and best in class perform-ance compliance.

Luberef is the only base oil producer in the Kingdom of Saudi Arabia, supplying compa-nies such as Shell, Mobil, Caltex, Fuchs and Petromin Corporation. Founded in 1978, it now operates as a joint venture between Saudi Aramco and Jadwa Industrial In-vestment. It also exports the high quality base oil manufactured at its two refineries in Jeddah and Yanbu to more than 15 countries around the world. It is a fast grow-ing company, with significantly expanded production capacity at its Yanbu site planned to come online in 2016.

No More STOP-START SafetyIn anticipation of this planned

expansion, the question of how to bring about safety change became

critical in 2011. In 2003, Luberef had already tried to implement a safety management system by itself without help from others, but only achieved limited suc-cess. As Samir Khan, who was safety and security manager at the time and is now corporate risk coordinator and project manager for the safety culture transformation project, explains: “One could say that safety used to be ‘policed’. That was the culture in which Luberef had grown up. Safety was a discipline issue and considered to be the sole responsibility of the safety department. It was very hard to make people realize that safety is everyone’s responsibility.”

In describing the past work safety culture, Saad Saud Bukhari, a maintenance field foreman says, “We used to look for a solution after an incident had happened. The root cause was always hu-man error. The culture was one of attaching blame.”

Hussam Al-Johani, inspection engineer, says the result was that “people were afraid to report any unsafe conditions. They would by-pass procedures or safety require-ments in order to save time. People would only follow the safety rules in front of officials. For example, they would wear the safety belt only when they reached the main gate of the refinery.”

Abduhllah Banakhr, specialist mechanic, is equally forthright: “Hundreds of changes were implemented without proper review and without documen-tation. Near misses were not re-ported.” Initiatives would start and stop in isolation with no clear link between them. There was consequently only limited safety awareness at Luberef. Mr. Ibrahim Al-Faqeeh, vice-president manufacturing says: “The drivers of the safety effort did not really believe in it and consequently did not push it. As a result, the safety system was never adopted from the ground up. When I looked at incidents, I could see a link, but there was no proper system in place to make that link visible to everyone. That is why we ended up having repetitive incidents.”

All that came to a stop in 2011, when Luberef ’s president real-ized safety had to be tackled in an over-arching process with help from outside. As Luberef President and CEO Dr. Hasan Alzahrani says: “Safety is one of our core corporate values and an integral part of our strategic objective. As such we look at safety as a way of not only doing business, but rather as a way of life, because we want to be safe at work, at home and on the road. Our major challenge was not creating a safety management

REPORT

Safety

Saudi Aramco Base Oil Company-Luberef decided to commit on a November day at the end of 2011 to improve the company’s safety performance which had plateaued. This article is a case study of Luberef plant.

HYDROCARBON ASIA, OCt-DeC 2015 25

system or policy or procedures. Although these are imperatives for any successful safety pro-gram, our challenge was to estab-lish the mind-set, behaviors and culture needed to achieve and maintain safe actions and condi-tions. That is why we embarked on a journey to transform our safety culture. Our aim is to be a leading company for the sake of our people, properties, commu-nity and shareholders.” Luberef had worked with DuPont in 1994 on very successful manager and supervisor training. The decision was taken to call DuPont back in to study Luberef ’s culture and develop a systematic approach to safety management.

Integrated ApproachMr. Al-Faqeeh says: “Back in

2011, I was refinery manager at our Yanbu site. I really liked the comprehensiveness of the DuPont approach. It tackles all aspects of operational risk management in an integrated fashion from mechanical integrity to risk as-sessment, from management of change to contractor safety and more. I looked at their approach to safety and thought ‘This is what is missing. It has the potential to not only improve safety, but the whole manufacturing process.’’