Embed Size (px)

Citation preview

Session 72 PD, Organizational Barriers to Product Innovation

Moderator:

Kelly J. Rabin, FSA, MAAA

Presenters: Jay M. Jaffe, FSA, MAAA

Steve Leigh Philip R. Murphy, FLMI, MBA

THE PERSONAL SIDE OF ORGANIZATIONAL BARRIERS TO PRODUCT INNOVATION

Jay M. Jaffe, FSA, MAAAActuarial Enterprises, Ltd.

Chicago, IL [email protected]

312-397-0099SOA, May 17, 2016, Nashville, TN

Session #72

1SOA, 5/17/66, Session #72

DISCUSSION AREAS

• Invention v. Innovation• Types of innovation projects• Personal r/t organizational barriers to

product innovation• Common to all areas: Actuarial related

innovation projects

2SOA, 5/17/66, Session #72

INVENTION V. INNOVATION

• Invention:– Involves working on something really new– Maybe more of a legal concept

• Patenting• Proprietary information

• Innovation: making the invention actually work

3SOA, 5/17/66, Session #72

THE INVENTION/INNOVATIONTIMELINE

“ . . . our lives improve not at the moment of invention but when society

creates the conditions to allow new ideas to become integrated into our

daily lives.”(Davidson, NY Times Magazine, 2/21/16, p. 18)

4SOA, 5/17/66, Session #72

ACTUARIES AND INNOVATION/INVENTION

• Actuaries mainly involved with innovation• Example: Rx data in underwriting was an

innovation r/t an invention for most of us– Invention: creating the Rx analytic system– Innovation: actuaries, underwriters, agents and

applicants

5SOA, 5/17/66, Session #72

MIT Sloan Management Review.

Cognitive Technologies: The Next Step Up for Data and Analytics

6SOA, 5/17/66, Session #72

5 INNOVATION GOALS

1. Eliminate tedious work2. Reduce labor costs3. Utilize the explosion of available data4. Make more accurate decisions5. Embrace powerful new technologies

7SOA, 5/17/66, Session #72

WE MAKE IT REDDER

WE DON’T MAKE THE DRESS

8SOA, 5/17/66, Session #72

9SOA, 5/17/66, Session #72

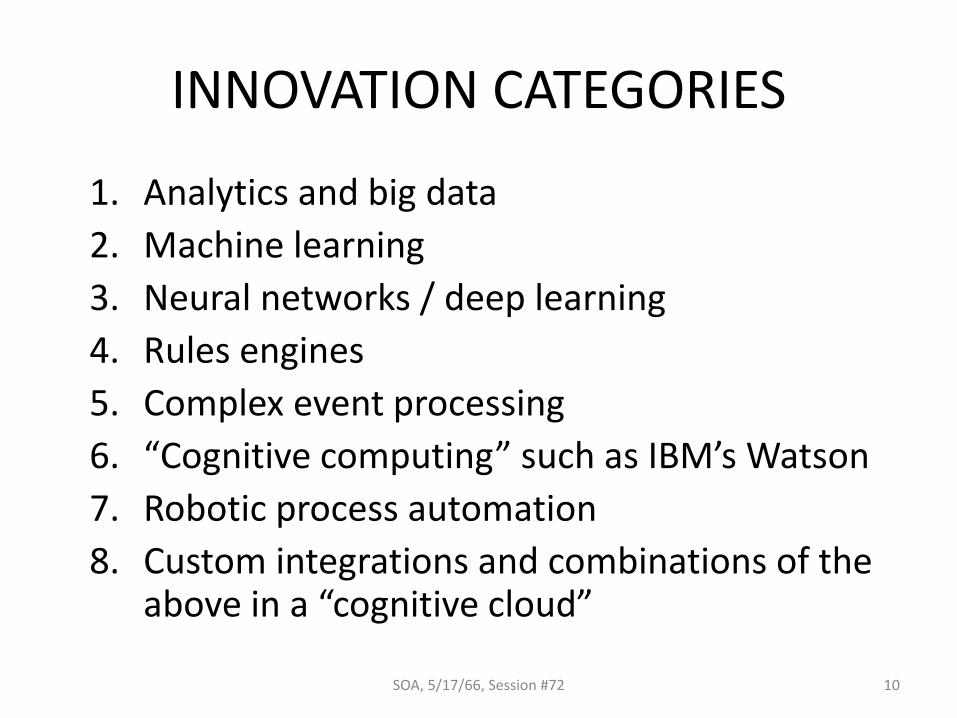

INNOVATION CATEGORIES

1. Analytics and big data2. Machine learning3. Neural networks / deep learning4. Rules engines5. Complex event processing6. “Cognitive computing” such as IBM’s Watson7. Robotic process automation8. Custom integrations and combinations of the

above in a “cognitive cloud”

10SOA, 5/17/66, Session #72

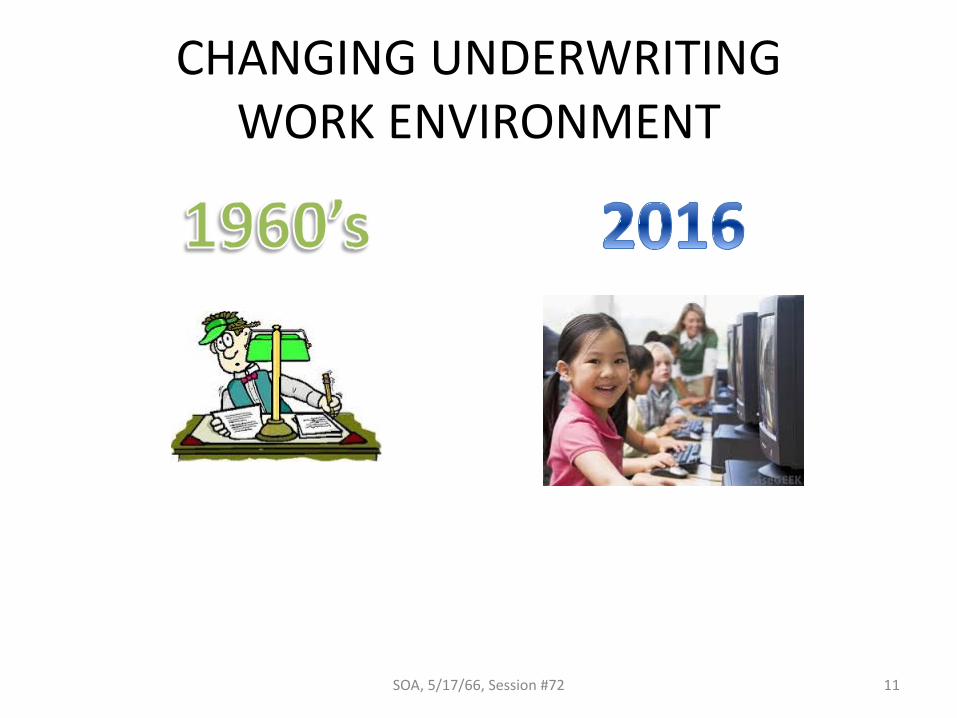

CHANGING UNDERWRITING WORK ENVIRONMENT

11SOA, 5/17/66, Session #72

IMPORTANCE OF HUMANS TO INNOVATION --- THE 5 STEPS

• Step In• Step Up• Step Aside• Step Narrowly• Step Forward

12SOA, 5/17/66, Session #72

IMPORTANCE OF HUMANS TO INNOVATION --- STEP #1

STEP INMaster the details of the

system to know when it needs modification

13SOA, 5/17/66, Session #72

IMPORTANCE OF HUMANS TO INNOVATION --- STEP #2

STEP UPTake a big picture view and

help make the decisions about automating new areas

14SOA, 5/17/66, Session #72

IMPORTANCE OF HUMANS TO INNOVATION --- STEP #3

STEP ASIDEFocus on areas where humans still do the work better than

new technologies

15SOA, 5/17/66, Session #72

IMPORTANCE OF HUMANS TO INNOVATION --- STEP #4

STEP NARROWLYWork in areas that are too

narrow to be worth automating

16SOA, 5/17/66, Session #72

IMPORTANCE OF HUMANS TO INNOVATION --- STEP #5

STEP FORWARDRemember, humans build

the new systems

17SOA, 5/17/66, Session #72

IMPORTANCE OF HUMANS TO INNOVATION --- THE 5 STEPS

• Step In• Step Up• Step Aside• Step Narrowly• Step Forward

18SOA, 5/17/66, Session #72

BECOMING A BETTER INNOVATOR

• Think HOW TO• Become TIME SENSITIVE• TAKE RISK• Remember the BASF PERSPECTIVE• Become a LICENSED AGENT• READ, READ, READ• Attend NON-ACTUARIAL MEETINGS• VOLUNTEER

19SOA, 5/17/66, Session #72

20SOA, 5/17/66, Session #72

21SOA, 5/17/66, Session #72

© 2016 NEOS and Milliman

Organizational Barriers to Product Innovation

Steve Leigh, NEOS LLCKelly Rabin, Milliman

May 2016

© 2016 NEOS and Milliman

“We know what is needed to become product leaders, but the way is blocked.”

1

• Modern, flexible technology

• Strong, clear decision-making with clear roles

and responsibilities

• Clear focus on the customer and target market

• Collection and leveraging of innovative ideas

• Skilled use of data

• Broad IT and operational capabilities

• Dedicated resources for priority tasks

• Understanding of regulatory and pricing

constraints

Requirements for successful innovation:

© 2016 NEOS and Milliman

Three categories on the product innovation spectrum.

2

Traditional – Not a product innovator (but may be innovative in the way they sell, service, or engage with consumers).

True Innovator – Invent new products and assemble new products in new ways.

Fast Follower – Wait for others to prove new product ideas are viable and in demand, then develop similar products.

How do we move from the left to the right?

© 2016 NEOS and Milliman

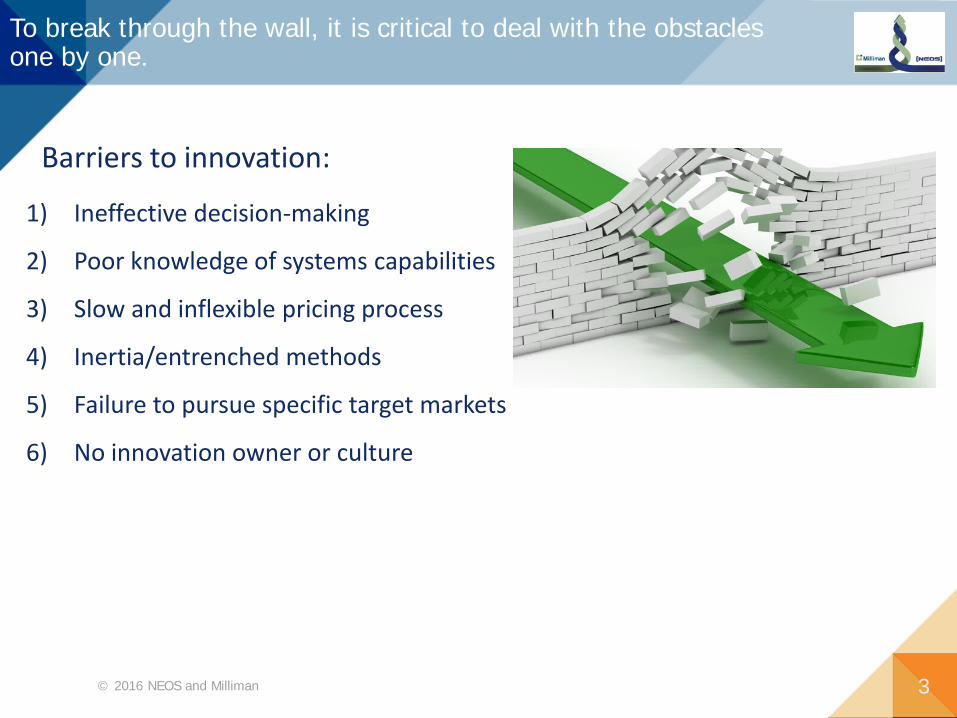

To break through the wall, it is critical to deal with the obstacles one by one.

3

Barriers to innovation:

1) Ineffective decision-making

2) Poor knowledge of systems capabilities

3) Slow and inflexible pricing process

4) Inertia/entrenched methods

5) Failure to pursue specific target markets

6) No innovation owner or culture

© 2016 NEOS and Milliman 4

Barrier #1:Ineffective decision-making

© 2016 NEOS and Milliman

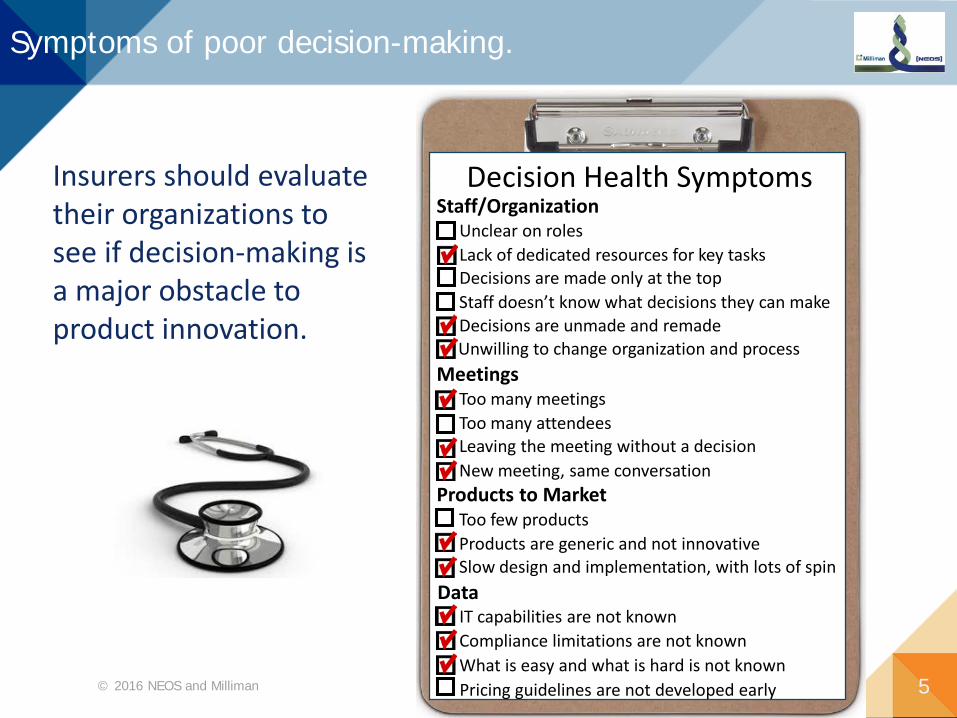

Symptoms of poor decision-making.

5

Decision Health Symptoms

MeetingsToo many meetingsToo many attendeesLeaving the meeting without a decision

Products to MarketToo few productsProducts are generic and not innovativeSlow design and implementation, with lots of spin

Staff/OrganizationUnclear on rolesLack of dedicated resources for key tasksDecisions are made only at the top

DataIT capabilities are not knownCompliance limitations are not knownWhat is easy and what is hard is not known

New meeting, same conversation

Staff doesn’t know what decisions they can makeDecisions are unmade and remadeUnwilling to change organization and process

Pricing guidelines are not developed early

Insurers should evaluate their organizations to see if decision-making is a major obstacle to product innovation.

© 2016 NEOS and Milliman

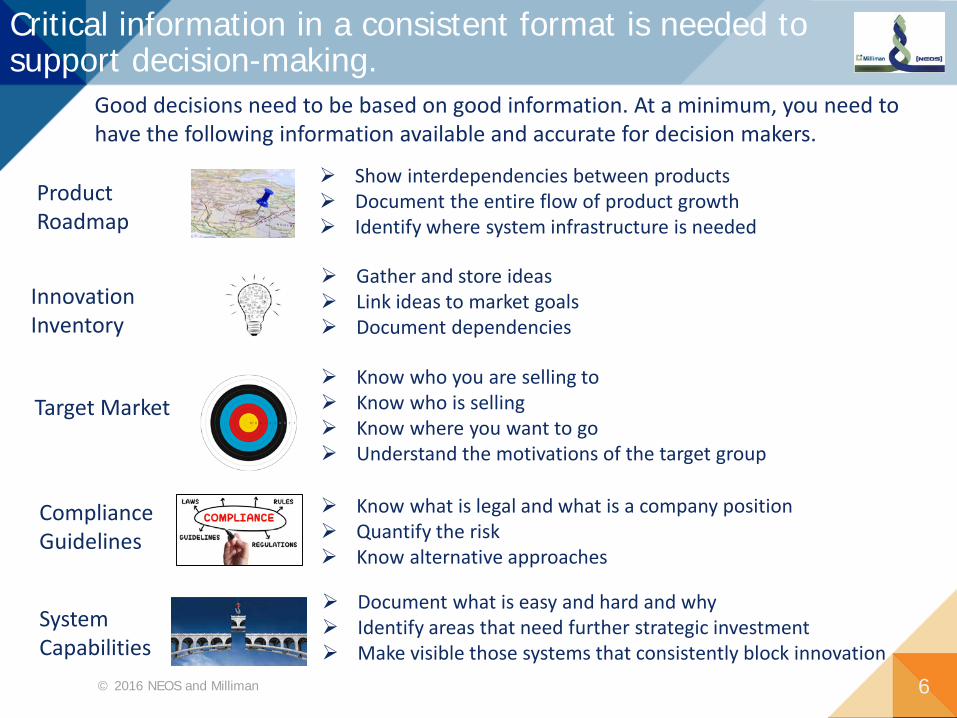

Critical information in a consistent format is needed to support decision-making.

6

Show interdependencies between products Document the entire flow of product growth Identify where system infrastructure is needed

Product Roadmap

Innovation Inventory

Good decisions need to be based on good information. At a minimum, you need to have the following information available and accurate for decision makers.

Compliance Guidelines

Target Market

Know what is legal and what is a company position Quantify the risk Know alternative approaches

System Capabilities

Document what is easy and hard and why Identify areas that need further strategic investment Make visible those systems that consistently block innovation

Gather and store ideas Link ideas to market goals Document dependencies

Know who you are selling to Know who is selling Know where you want to go Understand the motivations of the target group

© 2016 NEOS and Milliman

Breaking the barriers to facilitate good decision-making.

7

Strategies:• Provide the right amount of critical information at the right time for each decision.• Meeting agendas must identify what decisions are scheduled to be made and roles for

attendees. • Create a safe environment for decision-makers that fosters risk-taking.• Document the why and share all decisions.• Build a framework for information collection and maintenance.

Objective: Make decisions quickly and accurately.

Decisions are rarely changed and changes are well justified.

Decisions are fact-based. Excellent documentation around

decisions so that everyone is on the same page.

© 2016 NEOS and Milliman 8

Barrier #2:Poor knowledge of systems

capabilities

© 2016 NEOS and Milliman

Symptoms of poor systems knowledge.

9

Systems knowledge is an obstacle if: There is a lack of understanding of who

has the right information.

It is not clear where systems are inflexible.

The same question(s) are asked multiple

times with “different answers” given.

Time delays, cost overruns, and surprises

around new products are typical.

There seems to be no single source of the

truth.

© 2016 NEOS and Milliman

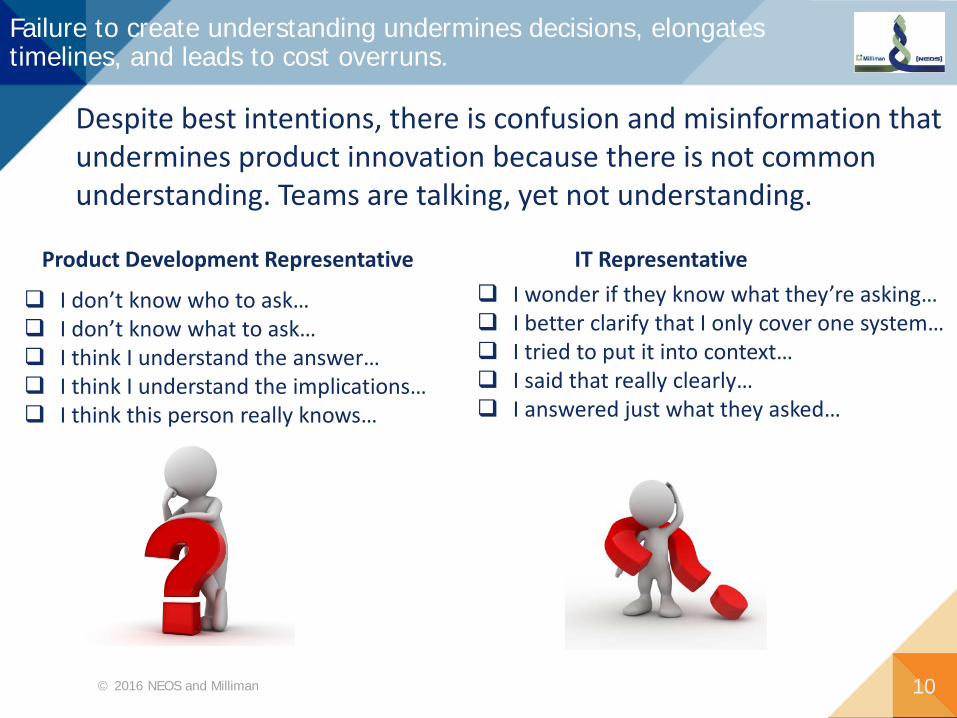

Failure to create understanding undermines decisions, elongates timelines, and leads to cost overruns.

10

I don’t know who to ask… I don’t know what to ask… I think I understand the answer… I think I understand the implications… I think this person really knows…

Product Development Representative IT Representative I wonder if they know what they’re asking… I better clarify that I only cover one system… I tried to put it into context… I said that really clearly… I answered just what they asked…

Despite best intentions, there is confusion and misinformation that undermines product innovation because there is not common understanding. Teams are talking, yet not understanding.

© 2016 NEOS and Milliman

Strategies to facilitate good system knowledge.

11

Strategies:• Document capabilities against business functions and product characteristics.• Maintain capabilities over time for new products and product ideas.• Document where systems are flexible and adaptable, and where they are not.• Have system capabilities well documented, so that what is easy, difficult or

impossible with new products can be known up front.• Separate system features into those that are strategic and those that are tactical.

Objective: To capture and maintain IT capability data to eliminate rework, confusion, and spin in product development.

Create a comprehensive capability assessment across the entire platform.

Identify areas for strategic investment. Identify those areas that are likely to be

problematic and delay implementation.

© 2016 NEOS and Milliman 12

Barrier #3:Slow and inflexible pricing

process

© 2016 NEOS and Milliman

Symptoms of poor pricing flexibility.

13

The pricing process is an obstacle if:

Assumptions must be fully baked and blown out

before any pricing can occur.

Rates are not benchmarked against market

conditions.

The process is not dynamic and iterative.

The focus is solely on risk aversion.

Innovative products that are not yet to scale must

meet the same pricing hurdles as industrialized

products.

Pricing actuaries are siloed and dictate product

development outcomes, vs. being collaborative

members of a team.

© 2016 NEOS and Milliman

Strategies to facilitate pricing that supports innovation.

14

Objective: Price incrementally to avoid putting significant time and cost into pricing the full product when only price validation is needed.

Determine minimum viability prior to investing substantial resources across the entire organization.

Established expected profitability to support development of a business case.

Build an iterative, interactive pricing capability.

Strategies:• Create a stripped-down model office (a few cells) for which distribution has

provided indicative premiums.• Develop rough, ballpark assumptions.• Use modeling tools that allow you to tweak product design easily.• Share results early and often to facilitate decision-making.• Strive to have actuaries be treated as team members vs. barriers.

© 2016 NEOS and Milliman 15

Barrier #4:Inertia/entrenched methods

© 2016 NEOS and Milliman

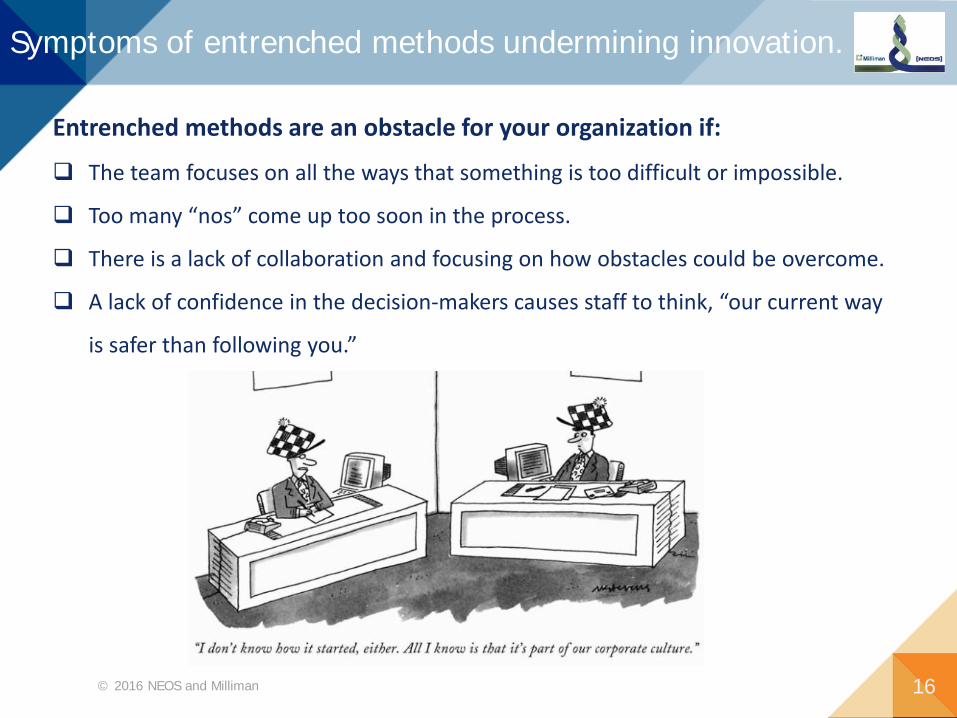

Symptoms of entrenched methods undermining innovation.

16

Entrenched methods are an obstacle for your organization if:

The team focuses on all the ways that something is too difficult or impossible.

Too many “nos” come up too soon in the process.

There is a lack of collaboration and focusing on how obstacles could be overcome.

A lack of confidence in the decision-makers causes staff to think, “our current way

is safer than following you.”

© 2016 NEOS and Milliman

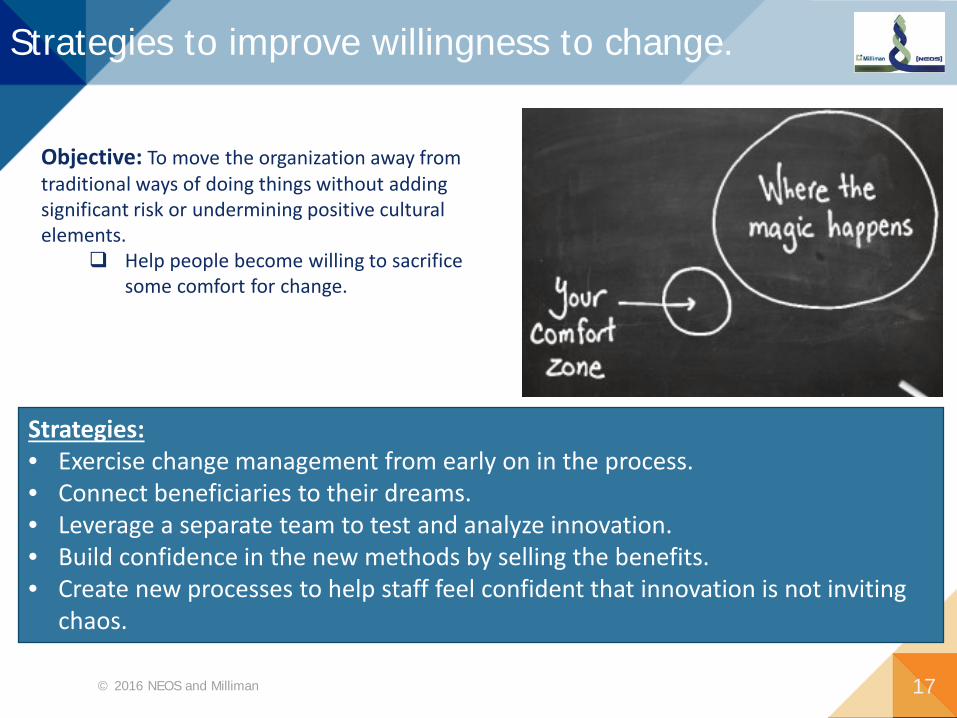

Strategies to improve willingness to change.

17

Strategies:• Exercise change management from early on in the process.• Connect beneficiaries to their dreams.• Leverage a separate team to test and analyze innovation.• Build confidence in the new methods by selling the benefits.• Create new processes to help staff feel confident that innovation is not inviting

chaos.

Objective: To move the organization away from traditional ways of doing things without adding significant risk or undermining positive cultural elements.

Help people become willing to sacrifice some comfort for change.

© 2016 NEOS and Milliman 18

Barrier #5:Failure to pursue specific target

markets

© 2016 NEOS and Milliman

Symptoms of not knowing the target market and sticking to it.

19

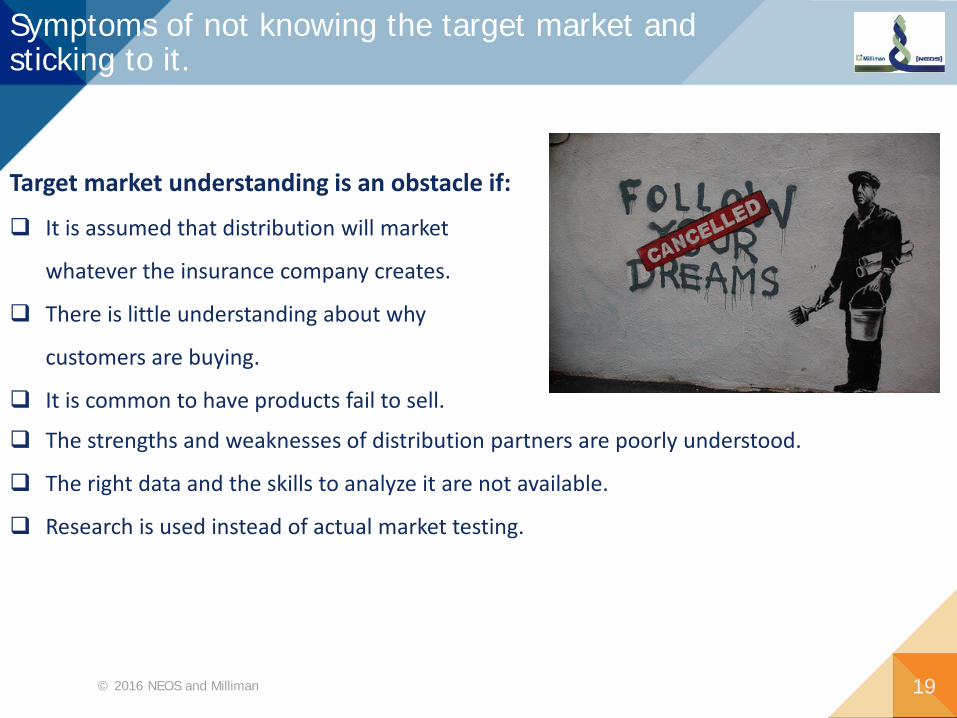

Target market understanding is an obstacle if:

It is assumed that distribution will market

whatever the insurance company creates.

There is little understanding about why

customers are buying.

It is common to have products fail to sell.

The strengths and weaknesses of distribution partners are poorly understood.

The right data and the skills to analyze it are not available.

Research is used instead of actual market testing.

© 2016 NEOS and Milliman

Strategies to facilitate clear direction based on specific target market objectives.

20

Strategies:• Develop skills to access and analyze data to understand why customers buy.• Develop skills to access and analyze data to understand distribution behavior.• Create products that are known to drive sales to identified market segments.• Market test products for specific segments and evaluate the data.• Do your own segment analysis instead of relying solely on the success of

competitors.• Make sure there is alignment between distribution partners and defined

markets.

Objective: To use defined market segments to guide product innovation.

Define market segments aligned to distribution.

Understand the segment. Allow knowledge of the segment to shape

new product innovation.

© 2016 NEOS and Milliman 21

Barrier #6:No innovation owner or culture

© 2016 NEOS and Milliman

Symptoms of no single innovation owner.

22

Failure to designate a single innovation owner is an obstacle if:

Innovative ideas are only generated from top leaders.

Innovations are either not linked or poorly linked to specific market objectives.

There is a fear of Google, Amazon, and others entering the life insurance

market, but little to no action.

You are unprepared for innovation in the following areas: organizational

structure, customer service, new business, underwriting, and other areas of

the company.

There are no viable plans to reach increasing numbers of under- and uninsured

consumers.

© 2016 NEOS and Milliman

Strategies to facilitate an innovation owner.

23

Strategies:• Create a process to vet new innovation ideas and reward idea generators.• Establish outside sources for innovative ideas.• Create innovation inventory to capture and maintain innovative ideas.• Link innovation ideas to sales objectives, service improvements, customer

demands or other business value.• Test before broad deployment: design a test plan, define success, perform test,

and analyze the results.

Objective: Develop a single owner for product innovation that will drive new ideas, competitive analysis, and the innovation process.

Keep innovation tied to the target market, service, or other business objective.

Leverage ideas from internal, external, and non-industry sources.

© 2016 NEOS and Milliman 24

Where do we go from here?

© 2016 NEOS and Milliman

Recommendations for success.

25

Work with your internal IT group to help you identify what is easy, difficult, and/or a strategic investment.

Document reasons behind the decisions you make.

Align product innovation to markets you are trying to reach.

Define a repeatable product development process.

Create a plan that will help you separate strategic IT investments from tactical investments in your infrastructure.

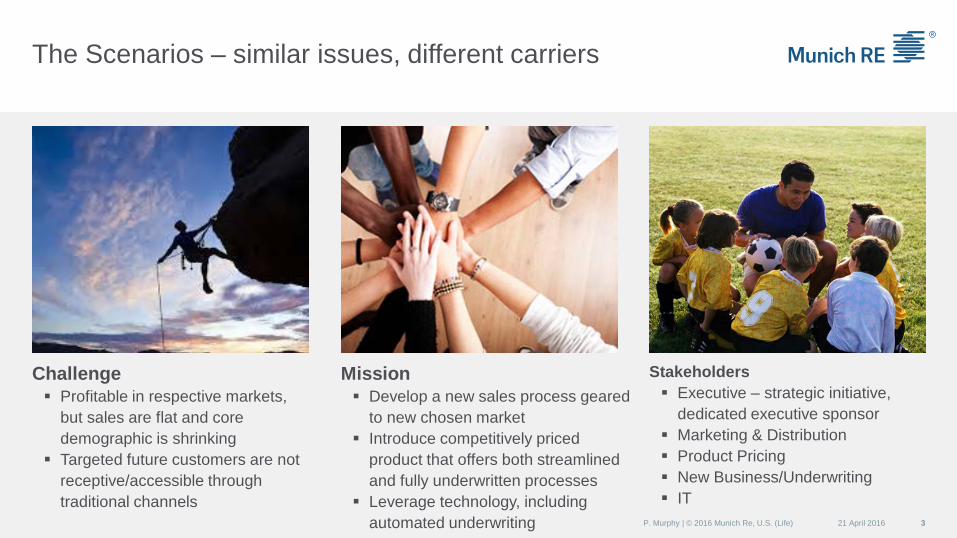

Obstacles to product innovation alignment and stakeholders2016 Life and Annuity Symposium

Philip R. MurphyMay 16, 2016

Quelle: Verwendung unter Lizenz von Shutterstock.com

Goals

Reinforce key considerations Underscore non-actuarial perspectives Share lessons learned

21 April 20162

Challenge Profitable in respective markets,

but sales are flat and core demographic is shrinking

Targeted future customers are not receptive/accessible through traditional channels

Mission Develop a new sales process geared

to new chosen market Introduce competitively priced

product that offers both streamlined and fully underwritten processes

Leverage technology, including automated underwriting

Stakeholders Executive – strategic initiative,

dedicated executive sponsor Marketing & Distribution Product Pricing New Business/Underwriting IT

The Scenarios – similar issues, different carriers

21 April 2016 3P. Murphy | © 2016 Munich Re, U.S. (Life)

Brokerage market

Strong brand recognition

Product chosen for new market - Term

Similarities

21 April 2016 4P. Murphy | © 2016 Munich Re, U.S. (Life)

Brokerage market

Strong brand recognition

Product chosen for new market - Term

Newly chosen target markets –degree of separation from core business

Current core product emphasis –term versus perm

Existing distribution versus access to new “non-life” distribution

Differences

21 April 2016 5P. Murphy | © 2016 Munich Re, U.S. (Life)

Brokerage market

Strong brand recognition

Product chosen for new market - Term

Outcome and status

21 April 2016 6P. Murphy | © 2016 Munich Re, U.S. (Life)

Launched late

Three years in production inaugural product selling very well

Very low sales of second perm product

Reconsidering next product, but focused on updating current program - product limits, distribution, applicant experience, looking for specialty plays

Expanding underwriting platform across entire business

Launched on time

Just under one year into product and selling “fair” (adoption rates are low)

Working to increase straight through processing rates

Company A Company B

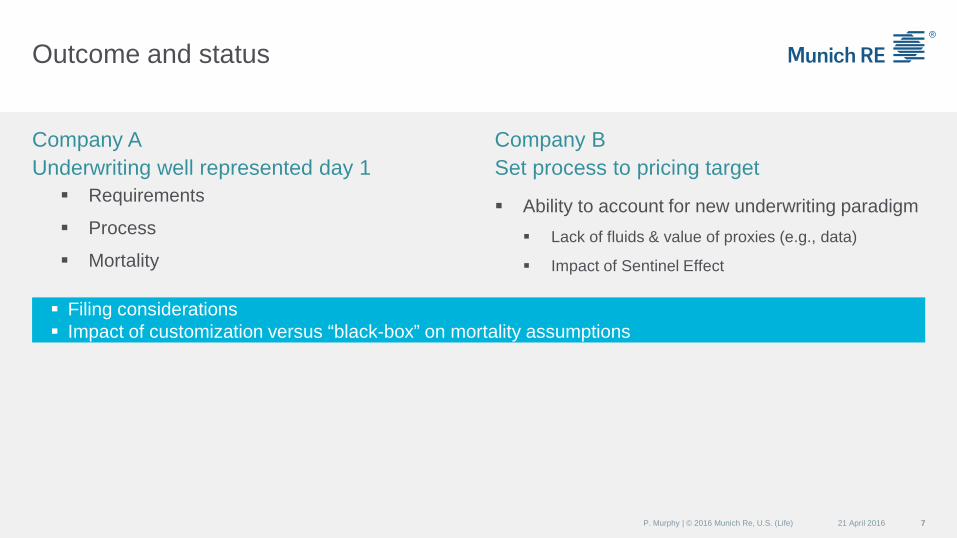

Outcome and status

21 April 2016 7P. Murphy | © 2016 Munich Re, U.S. (Life)

Requirements

Process

Mortality

Ability to account for new underwriting paradigm Lack of fluids & value of proxies (e.g., data)

Impact of Sentinel Effect

Company AUnderwriting well represented day 1

Company BSet process to pricing target

Filing considerations Impact of customization versus “black-box” on mortality assumptions

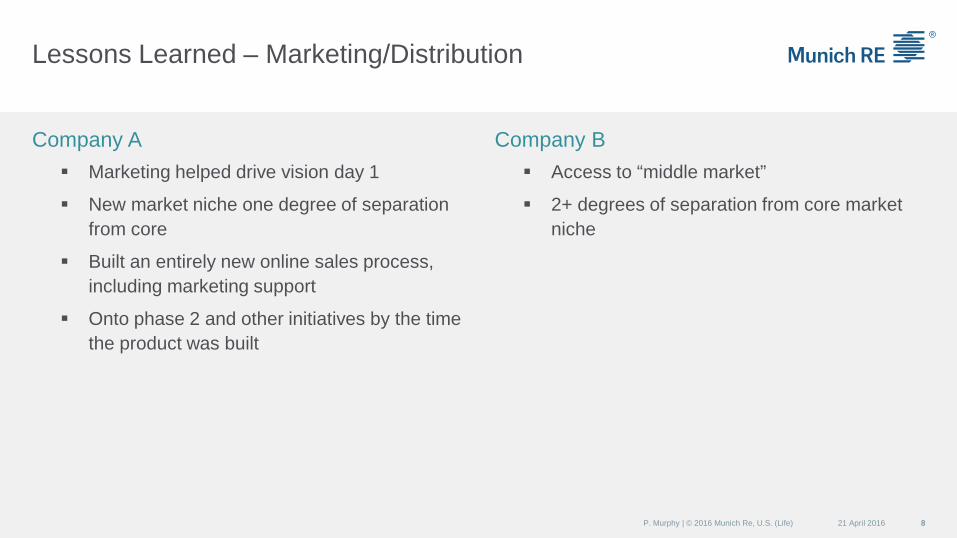

Lessons Learned – Marketing/Distribution

21 April 2016 8P. Murphy | © 2016 Munich Re, U.S. (Life)

Marketing helped drive vision day 1

New market niche one degree of separation from core

Built an entirely new online sales process, including marketing support

Onto phase 2 and other initiatives by the time the product was built

Access to “middle market”

2+ degrees of separation from core market niche

Company A Company B

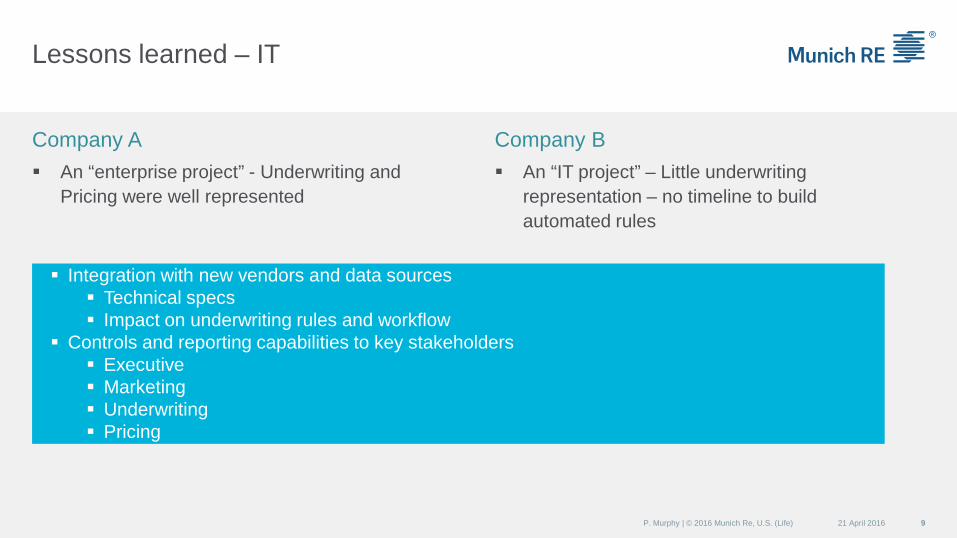

Lessons learned – IT

21 April 2016 9P. Murphy | © 2016 Munich Re, U.S. (Life)

An “enterprise project” - Underwriting and Pricing were well represented

An “IT project” – Little underwriting representation – no timeline to build automated rules

Company A Company B

Integration with new vendors and data sources Technical specs Impact on underwriting rules and workflow

Controls and reporting capabilities to key stakeholders Executive Marketing Underwriting Pricing

Organizational readiness Executive sponsorship & regular connection go

project manager (no misinterpretation)

Enterprise/strategic buy-in

Deadlines can’t be set in a vacuum

Account for consumer experience and rules development

Lessons learned – Project Management

21 April 2016 10P. Murphy | © 2016 Munich Re, U.S. (Life)

Conclusions – increasing chances for success Ensure strategic initiative and executive sponsorship Strategic vision versus reaction to competition

Don’t stray too far - leverage core competencies

Marketing - design, advise, apprise Upfront development

Back-end reporting and accountability (sales and mortality)

Full-time, multi-discipline project team, no silos, run by the business Project Management

Pricing

Underwriting

IT

Commit to post-launch refinements STP rates and rules enhancements

Sales & agent behavior

New underwriting tools and pricing adjustment 21 April 2016 11P. Murphy | © 2016 Munich Re, U.S. (Life)