Embed Size (px)

Citation preview

PETITIONER’S EXHIBIT 3

IURC CAUSE NO. 45032-S2 SETTLEMENT TESTIMONY OF BRIAN P. DAVEY

FILED JUNE 27, 2018

BRIAN P. DAVEY -1-

634100

SETTLEMENT TESTIMONY OF BRIAN P. DAVEY DIRECTOR, RATES AND REGULATORY STRATEGY, INDIANA,

DUKE ENERGY INDIANA, LLC CAUSE NO. 45032-S2 BEFORE THE

INDIANA UTILITY REGULATORY COMMISSION

I. INTRODUCTION 1

Q. PLEASE STATE YOUR NAME AND BUSINESS ADDRESS. 2

A. My name is Brian P. Davey, and my business address is 1000 East Main Street, 3

Plainfield, Indiana. 4

Q. BY WHOM ARE YOU EMPLOYED AND IN WHAT CAPACITY? 5

A. I am employed by Duke Energy Indiana LLC (“Duke Energy Indiana,” “Petitioner” or 6

“Company”) as Director, Rates and Regulatory Strategy, Indiana. 7

Q. ARE YOU THE SAME BRIAN DAVEY THAT PRESENTED DIRECT 8

TESTIMONY IN THIS PROCEEDING? 9

A. Yes, I am. 10

Q. WHAT IS THE PURPOSE OF YOUR SETTLEMENT TESTIMONY? 11

A. My testimony will present an overview of the Settlement Agreement entered into 12

between Duke Energy Indiana, the Indiana Office of Utility Consumer Counselor, the 13

Indiana Industrial Group and Nucor Steel-Indiana, a division of Nucor Corporation 14

(collectively, the “Settling Parties”) and attached to this testimony as Exhibit 3-A. 15

Mr. Stephen G. De May will explain how the substantive terms of the Settlement 16

help Duke Energy Indiana to preserve its credit quality for the benefit of its customers. 17

Mr. John Panizza will present an overview of the differences between protected and 18

unprotected excess accumulated deferred income taxes (“ADIT”) resulting from the 19

PETITIONER’S EXHIBIT 3

IURC CAUSE NO. 45032-S2 SETTLEMENT TESTIMONY OF BRIAN P. DAVEY

FILED JUNE 27, 2018

BRIAN P. DAVEY -2-

reduction in federal income tax rates from 35% to 21% under the 2017 Tax Cuts and Jobs 1

Act (“Tax Act”) and explain the agreed upon treatment of both. 2

II. SUBSTANTIVE TERMS OF THE SETTLEMENT AGREEMENT 3

Q. PLEASE PROVIDE AN OVERVIEW OF THE GENERAL AREAS ADDRESSED 4

BY THE SETTLEMENT AGREEMENT. 5

A. The Settlement Agreement addresses all issues in this proceeding (both Phase 1 and 6

Phase 2 issues), including the adjustment of base rates and riders, the regulatory liability 7

created by Commission Order dated January 3, 2018, as well as the time periods and 8

amounts of protected and unprotected ADIT to be returned to customers. 9

Q. WHEN WILL CUSTOMERS SEE THEIR BASE RATES AND TRACKERS 10

ADJUSTED AS A RESULT OF THE TAX ACT? 11

A. The Settling Parties agreed that the 21% corporate income tax rate would be included in 12

base rates and riders impacted by base rates no later than September 1, 2018. Under the 13

terms of the Settlement, the Company will submit a revised 30-day filing including 14

updated base rates and riders impacted by base rates such that the IURC could approve 15

the updated rates on or before September 1, 2018. 16

The Settling Parties agreed that Duke Energy Indiana’s trackers that are affected 17

by the tax rate change will include the 21% corporate income tax rate as they are filed 18

throughout 2018. Customers have already begun receiving the tax reduction in the 19

Company’s most impacted riders comprising approximately 91% of rider tax reduction 20

impacts, filed in the Environmental Compliance Cost Recovery (“ECR”) and Integrated 21

PETITIONER’S EXHIBIT 3

IURC CAUSE NO. 45032-S2 SETTLEMENT TESTIMONY OF BRIAN P. DAVEY

FILED JUNE 27, 2018

BRIAN P. DAVEY -3-

Coal Gasification Combined Cycle (“IGCC”) filings. These rider rates were updated to 1

include the lower 21% tax rate the first of March 2018 and late May 2018, respectively. 2

Q. HOW DOES THE SETTLEMENT AGREEMENT ADDRESS THE 3

REGULATORY LIABILITY CREATED BY COMMISSION ORDER FOR THE 4

IMPACTS OF THE CHANGE IN THE CORPORATE TAX RATE FROM THE 5

BEGINNING OF 2018? 6

A. On January 3, 2018, the Commission ordered all Indiana jurisdictional rate-regulated, 7

investor-owned utilities to immediately commence using regulatory accounting for all 8

calculated differences resulting from the Tax Act and what would have been recorded if 9

the Tax Act did not go into effect. Duke Energy Indiana has created a regulatory liability 10

for both the base rate and tracker impacts of the income tax reduction, which will 11

continue to accrue until such time as the rate change is incorporated in customer rates. 12

The Settling Parties agreed that for the base rate portion of the regulatory liability, 13

upon issuance of a final order in this Cause approving the Settlement Agreement, the 14

Company will make the necessary accounting entries to offset approximately $36 million 15

(prior to revenue requirement gross-up) of regulatory assets on Duke Energy Indiana’s 16

accounting books that are currently accruing carrying costs (IGCC Carbon Capture 17

Study, $26.3 million, and NOx AFUDC Continuation Environmental Plant – Retail After 18

Rate Case Cut-off, $9.8 million) with the regulatory liability associated with base rates as 19

of the effective date of the order.1 Any remainder between the regulatory liability 20

1 The amounts included above reflect the December 31, 2017 balances for the two referenced regulatory assets. Carrying costs will continue to accrue until the offset agreed to in the Settlement Agreement, increasing the balance subject to the offset, at which time the carrying costs will be discontinued.

PETITIONER’S EXHIBIT 3

IURC CAUSE NO. 45032-S2 SETTLEMENT TESTIMONY OF BRIAN P. DAVEY

FILED JUNE 27, 2018

BRIAN P. DAVEY -4-

associated with the over-collection of federal income tax through base rates and the 1

regulatory assets identified above shall be deferred, without carrying costs, until the 2

Company’s next general base rate case. 3

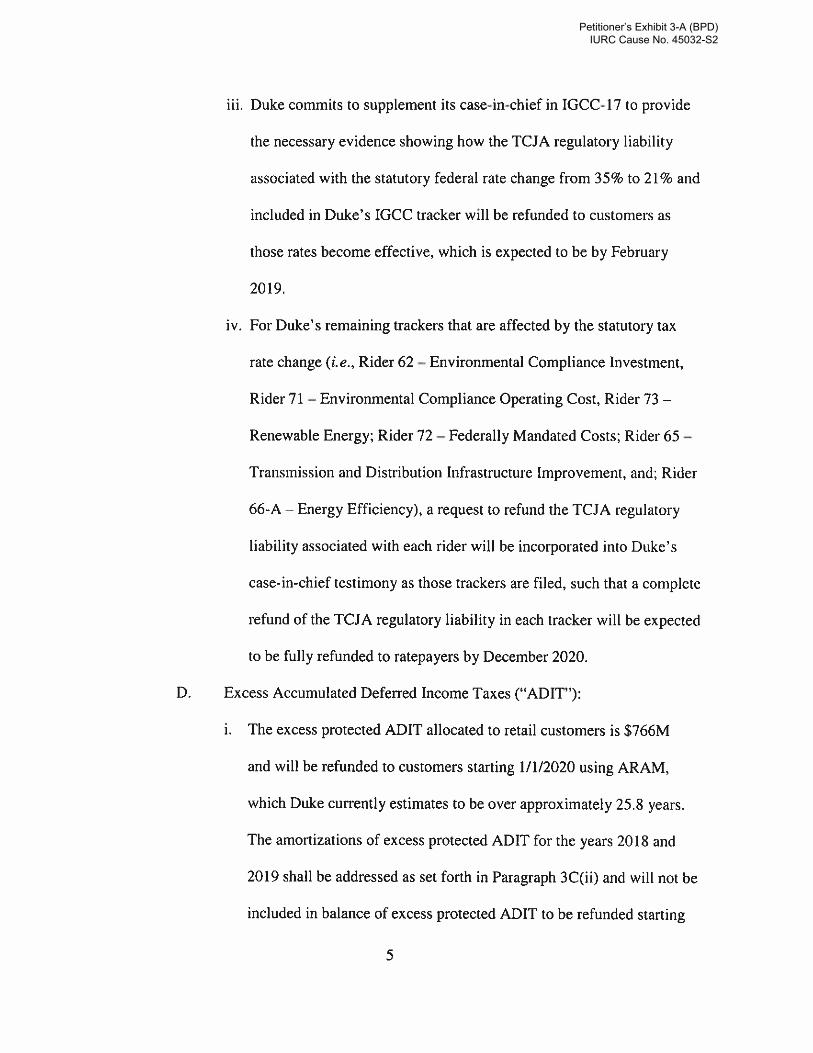

The Settlement Agreement provides that for the rider portion of the regulatory 4

liability, the Company commits to supplement its case-in-chief in IGCC-17 to provide the 5

necessary evidence showing how the regulatory liability associated with the statutory 6

federal rate change from 35% to 21% and included in IGCC tracker will be refunded to 7

customers as those rates become effective, which is expected to be by February 2019. 8

For the Company’s remaining trackers that are affected by the statutory tax rate 9

change (Rider 62 – Environmental Compliance Investment; Rider 71 – Environmental 10

Compliance Operating Cost; Rider 73 – Renewable Energy; Rider 72 – Federally 11

Mandated Costs; Rider 65 – Transmission and Distribution Infrastructure Improvement, 12

and; Rider 66-A – Energy Efficiency), the Settling Parties agreed that a request to refund 13

the regulatory liability associated with each rider will be incorporated into Duke Energy 14

Indiana’s case-in-chief testimony as those trackers are filed. As a result of this term, a 15

complete refund of the regulatory liability in each tracker is expected to be fully refunded 16

to customers by December 2020. 17

Q. HOW DO THE SETTLING PARTIES PROPOSE TO RETURN THE EXCESS 18

PROTECTED ADIT? 19

A. The Settling Parties propose to amortize the retail portion of excess protected ADIT, 20

which is $766 million over approximately 25.8 years as required under the normalization 21

rules and to commence refunding this amount on January 1, 2020. The amortization 22

PETITIONER’S EXHIBIT 3

IURC CAUSE NO. 45032-S2 SETTLEMENT TESTIMONY OF BRIAN P. DAVEY

FILED JUNE 27, 2018

BRIAN P. DAVEY -5-

amounts associated with 2018 and 2019 will be deferred in a regulatory liability to be 1

included in the next rate case. The testimony of Mr. John Panizza discusses excess ADIT 2

in more detail. 3

Q. HOW DO THE SETTLING PARTIES PROPOSE TO RETURN THE EXCESS 4

UNPROTECTED ADIT? 5

A. The Settling Parties agreed that the retail portion of excess unprotected ADIT, which is 6

$210 million, will be amortized and refunded to customers beginning with the final order 7

in this Cause over a 10-year period. For the first five years, the amortization amount 8

shall be $7 million annually. For the last five years, the amortization shall be $35 million 9

annually. To the extent an item that is classified as protected by IRS guidance is 10

subsequently reclassified due to a change in IRS guidance as unprotected or vice versa, 11

upon validation of any change by the Non-Duke Energy Settling Parties, the $35 million 12

annual amortization will continue until the remaining unprotected excess ADIT balance 13

is zero. 14

Q. WHAT IS THE MECHANISM FOR RETURNING THE EXCESS ADIT TO 15

CUSTOMERS? 16

A. The Settling Parties agreed that, until otherwise ordered by the Commission following a 17

general base rate case, Duke Energy Indiana will make a 30-day filing via the 18

Commission’s 30-day filing process using its existing Standard Contract Rider No. 67 – 19

Credits to Remove Annual Amortization of Cinergy Merger Costs, with certain agreed to 20

modifications, to implement the reduction in rates resulting from the amortization of the 21

excess protected and unprotected ADIT. 22

PETITIONER’S EXHIBIT 3

IURC CAUSE NO. 45032-S2 SETTLEMENT TESTIMONY OF BRIAN P. DAVEY

FILED JUNE 27, 2018

BRIAN P. DAVEY -6-

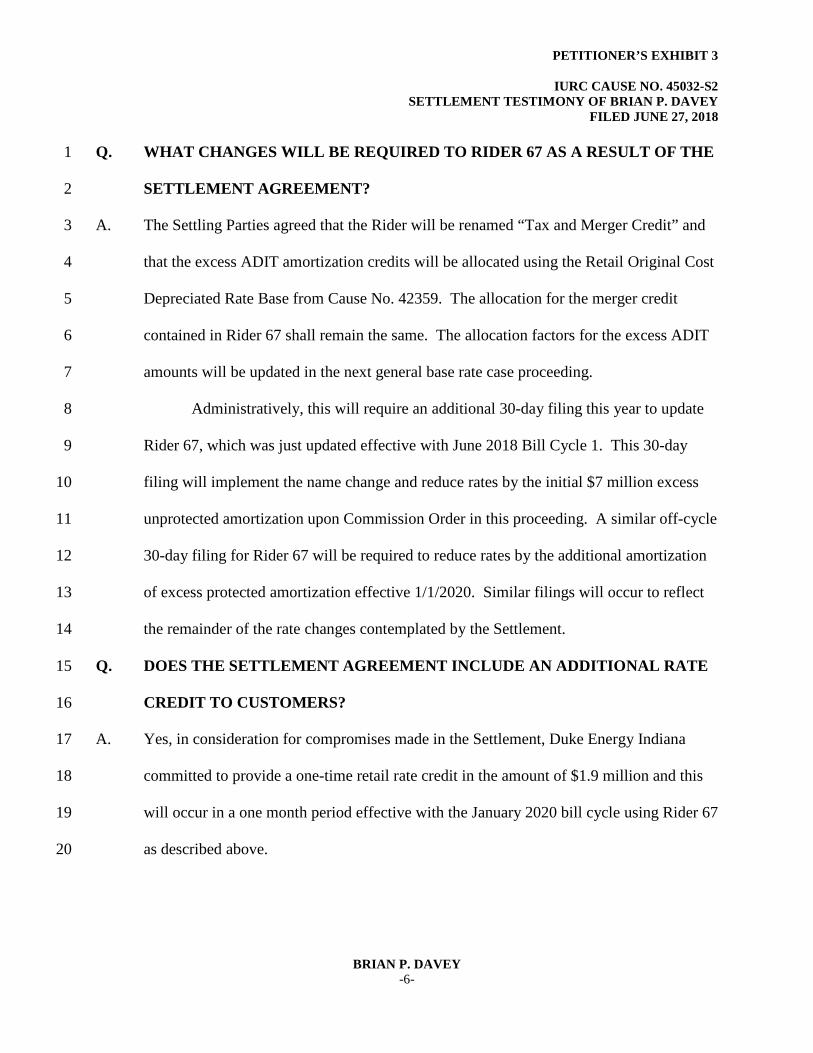

Q. WHAT CHANGES WILL BE REQUIRED TO RIDER 67 AS A RESULT OF THE 1

SETTLEMENT AGREEMENT? 2

A. The Settling Parties agreed that the Rider will be renamed “Tax and Merger Credit” and 3

that the excess ADIT amortization credits will be allocated using the Retail Original Cost 4

Depreciated Rate Base from Cause No. 42359. The allocation for the merger credit 5

contained in Rider 67 shall remain the same. The allocation factors for the excess ADIT 6

amounts will be updated in the next general base rate case proceeding. 7

Administratively, this will require an additional 30-day filing this year to update 8

Rider 67, which was just updated effective with June 2018 Bill Cycle 1. This 30-day 9

filing will implement the name change and reduce rates by the initial $7 million excess 10

unprotected amortization upon Commission Order in this proceeding. A similar off-cycle 11

30-day filing for Rider 67 will be required to reduce rates by the additional amortization 12

of excess protected amortization effective 1/1/2020. Similar filings will occur to reflect 13

the remainder of the rate changes contemplated by the Settlement. 14

Q. DOES THE SETTLEMENT AGREEMENT INCLUDE AN ADDITIONAL RATE 15

CREDIT TO CUSTOMERS? 16

A. Yes, in consideration for compromises made in the Settlement, Duke Energy Indiana 17

committed to provide a one-time retail rate credit in the amount of $1.9 million and this 18

will occur in a one month period effective with the January 2020 bill cycle using Rider 67 19

as described above. 20

PETITIONER’S EXHIBIT 3

IURC CAUSE NO. 45032-S2 SETTLEMENT TESTIMONY OF BRIAN P. DAVEY

FILED JUNE 27, 2018

BRIAN P. DAVEY -7-

III. TAX ACT SETTLEMENT AGREEMENT IMPACT TO CUSTOMERS 1

Q. PLEASE SUMMARIZE THE IMPACTS OF THE SETTLEMENT TO RETAIL 2

REVENUE. 3

A. Please see the following summary: 4

5

The first sub-total in the table reflects a 4.5% retail revenue decrease as of 6

October 2018 resulting from the benefits of the Tax Act. This assumes the Commission 7

approves the Settlement, rider updates, base rate adjustments and the rate update for the 8

excess unprotected ADIT amortization. 9

Estimated PercentageEstimated Annual Revenue of 2017

Description Effective Date Difference Retail Revenue(millions)

Riders (1) March-October 2018 ($50.9) (2.0%)

Base Rates September 2018 ($54.9) (2.2%)

Excess ADIT - Unprotected (2) September 2018 ($7.0) (0.3%)

Sub-total as of October 2018 ($112.8) (4.5%)

Excess ADIT - Protected January 2020 ($29.7) (1.1%)

Total as of January 2020 excluding $1.9 revenue credit for 2020 ($142.5) (5.6%)

Incremental Excess ADIT - Unprotected (2) September 2023 ($28.0) (1.1%)

Total for second five years ($170.5) (6.7%)

Total 2017 Retail Revenue $2,525.3

(1) As of June 2018, ($46.2) million or 90.8% is included in approved rider rates.(2) The Settlement includes two 5-year amortization periods: The first at $7 million/year and the second

at $35 million/year.

PETITIONER’S EXHIBIT 3

IURC CAUSE NO. 45032-S2 SETTLEMENT TESTIMONY OF BRIAN P. DAVEY

FILED JUNE 27, 2018

BRIAN P. DAVEY -8-

The first highlighted total reflects a cumulative total of 5.6% retail revenue 1

reduction as of January 2020 assuming the Commission approves the amortization of the 2

protected excess ADIT. 3

The second highlighted total reflects a cumulative total of 6.7% retail revenue 4

reduction for the second five years of the Settlement assuming the Commission approves 5

the increase in the amortization for the excess unprotected ADIT for the second five 6

years. 7

Additionally, 2020 will include a one-time revenue credit of $1.9 million, a retail 8

annual revenue reduction of 0.1%. 9

IV. THE SETTLEMENT IS IN THE PUBLIC INTEREST 10

Q. DO YOU BELIEVE THE SETTLEMENT AGREEMENT IS IN THE PUBLIC 11

INTEREST? 12

A. Yes. The Settlement Agreement balances the interest of customers and the Company. 13

Customers get the benefits of the lower federal income tax rates from the Tax Act in their 14

base rates no later than September 1, 2018 and for all impacted riders by the end of 15

October 2018 in a timely and administratively efficient way. Between base rates and the 16

riders, this accounts for a rate reduction of approximately $106 million annually. As to 17

excess ADIT, customers will start to see the return of the unprotected amount in 2018 18

upon approval of the Settlement Agreement by the Commission and will receive all of the 19

excess unprotected ADIT over 10 years. Under the Settlement, customers will 20

experience a slight delay in beginning to receive the excess protected ADIT to January 21

2020. The testimony of Mr. De May describes Duke Energy’s perspective on the credit 22

PETITIONER’S EXHIBIT 3

IURC CAUSE NO. 45032-S2 SETTLEMENT TESTIMONY OF BRIAN P. DAVEY

FILED JUNE 27, 2018

BRIAN P. DAVEY -9-

quality benefits of this term in the Settlement in more detail, including its impact on 1

ensuring access to capital at reasonable rates. 2

V. CONCLUSION 3

Q. ARE YOU FAMILIAR WITH PETITIONER’S EXHIBIT 3-A? 4

A. Yes. 5

Q. DOES THIS CONCLUDE YOUR TESTIMONY IN SUPPORT OF THE 6

SETTLEMENT AGREEMENT? 7

A. Yes, it does. 8

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

Petitioner’s Exhibit 3-A (BPD) IURC Cause No. 45032-S2

VERIFICATION

I hereby verify under the penalties of perjury that the foregoing representations are true to the best of my knowledge, infonnation and belief.

Signed: /l.AJM.fJ../)~ Brian P. Davey

Dated: _____.(p__,/i...=....J;__._7 __.{I ___ ! _

IURC 45032-S2