Embed Size (px)

Citation preview

Deliberazione n.7/2013 Certificazione bilancio ITU

SEZIONE DI CONTROLLO PER GLI AFFARI COMUNITARI ED INTERNAZIONALI

IL COLLEGIO PER L’ATTIVITA’ DI CONTROLLO SULL’ITU

Composto dai magistrati

Dott. Giuseppe COGLIANDRO Presidente

Dott. Giacinto DAMMICCO Consigliere

Dott. Michele COSENTINO Consigliere

Vista la nota del Presidente della Corte dei conti prot. 2559 del 15/06/2012 con

la quale si accetta di espletare il mandato di “External Auditor” assegnato dal Consiglio

dell’ITU (International Telecommunications Union) in data 11 ottobre 2011, per gli anni

dal 2012 al 2015 e comunicato dal Segretario Generale dell’I.T.U. con nota del

12/06/2012;

Vista l’ordinanza n. 4/2012 del 17 settembre 2012 con la quale è stato

costituito, nell’ambito della Sezione, un apposito Collegio per la citata attività di

revisione;

Visti i principi INTOSAI;

Visti i principi internazionali di Audit applicabili all’attività di certificazione dalle

Istituzioni Superiori di Controllo (International Standards of Supreme Audit Institutions –

ISSAI), richiamati dalla Dichiarazione di Lima;

Visti i principi internazionali di Audit (International Standards on Auditing - ISA)

emessi dall’International Auditing and Assurance Standards Board (IAASB), organo

dell’International Federation of Accountants (IFAC);

Visti i principi contabili internazionali per il settore pubblico (International Public

Sector Accounting Standards - IPSAS) che richiamano i principi contabili internazionali

(International accounting standards – IAS);

Viste le determinazioni assunte dall’apposito Collegio nella seduta del 13

maggio 2013 in merito alle risultanze dell’attività istruttoria concernente l’esame del

bilancio del’ITU chiuso al 31 dicembre 2012

Considerato concluso il relativo “financial audit”

DELIBERA

la certificazione - secondo i principi INTOSAI di legalità, regolarità e affidabilità - degli

atti contabili del bilancio dell’ITU chiuso al 31 dicembre 2012 “Annual Accounts

(Financial Statements) 2012” sulla base dell’allegata relazione riguardante: la

comparazione del budget con le relative entrate e uscite effettive (Statement of

comparison of budget and actual amounts); lo stato patrimoniale (Statement of

financial position); il conto economico (Statement of financial performance); il

rendiconto dei flussi di cassa (Cash-flow Statement) e relative note esplicative.

Roma 13 maggio 2013

IL PRESIDENTEF.to Giuseppe Cogliandro

F.to Consigliere Giacinto Dammicco (relatore)

F.to Consigliere Michele Cosentino

Depositata in Segreteria il 18 luglio 2013

Il DirigenteF.to Maria Teresa Macchione

REPORT OF EXTERNAL AUDITOR

INTERNATIONALTELECOMMUNICATION UNIONAudit of the financial statements for 2012

16.05.2013

Corte dei conti

2

Contents

INTRODUCTION ......................................................................................................................................4

AUDIT CERTIFICATE .................................................................................................................................6

STRUCTURE OF THE ACCOUNTING STATEMENTS...........................................................................8

STATEMENT OF FINANCIAL POSITION 2012........................................................................................8

Assets .............................................................................................................................................. 8

Current Assets................................................................................................................................. 9

Cash and cash equivalent ................................................................................................................ 9

Recommendation no. 1 ................................................................................................................. 10

Suggestion no. 1............................................................................................................................ 10

Recommendation no. 2 ................................................................................................................. 11

Investments ............................................................................................................................... 12

Suggestion no. 2............................................................................................................................ 12

Receivables ............................................................................................................................... 12

Other current receivables .......................................................................................................... 13

Inventories................................................................................................................................. 13

Non-current assets..................................................................................................................... 14

Property, plant and equipment .................................................................................................. 14

Recommendation no. 3 ................................................................................................................. 16

Recommendation no. 4 ................................................................................................................. 18

Intangible Assets ....................................................................................................................... 18

Liabilities .................................................................................................................................. 19

Current Liabilities ......................................................................................................................... 19

Suppliers and other creditors ........................................................................................................ 19

Deferred revenue .......................................................................................................................... 19

Provisions ..................................................................................................................................... 20

Suggestion no. 3............................................................................................................................ 20

Other current liabilities................................................................................................................. 20

Borrowings and financial debts ................................................................................................... 21

Non-current liabilities ................................................................................................................... 21

Employee benefits (long-term).................................................................................................... 21

Employee benefits: Repatriation grants ...................................................................................... 22

Recommendation no. 5 ................................................................................................................. 22

Employee benefits: ASHI ............................................................................................................ 22

Recommendation no. 6 ................................................................................................................. 24

Recommendation no. 7 ................................................................................................................. 25

Employee benefits: Pensions ....................................................................................................... 26

Net Assets ................................................................................................................................. 26

Recommendation no. 8 ................................................................................................................. 27

Suggestion no. 4............................................................................................................................ 29

3

Recommendation no. 9 ................................................................................................................. 29

STATEMENT OF FINANCIAL PERFORMANCE 2012 .................................................................30

Revenue and Expenses............................................................................................................. 30

Recommendation no. 10 ............................................................................................................... 31

STATEMENT OF CHANGES IN NET ASSETS FOR THE PERIOD WHICH CLOSED ON 31

DECEMBER 2012 ........................................................................................................................................31

COMPARISON OF BUDGETED AMOUNTS AND ACTUAL AMOUNTS FOR THE 2012

FINANCIAL PERIOD ....................................................................................................................................31

TABLE OF CASH FLOWS FOR THE PERIOD WHICH CLOSED ON 31 DECEMBER 2012

............................................................................................................................................................................32

STAFF SUPERANNUATION AND BENEVOLENT FUNDS.................................................. 32

Recommendation no. 11 ............................................................................................................... 33

UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP), ICT-DF, and TRUST FUNDS .....33

FOLLOW UP OF RECOMMENDATIONS OF OUR PREDECESSORS..............................................34

4

INTRODUCTION

The legal basis for the audit carried out by the External Auditors is given in the Financial

Regulations (2010 edition): Article 28 and Additional terms of reference.

The present report gives account to the Council of the results of our audits.

The audit considered the ITU Financial Operating Report at 31 December 2012 and the

budgetary accounts and their consistency.

The financial periods are governed by the Constitution and Convention of the

International Telecommunication Union, and by the ITU Financial Regulations and

Financial Rules in accordance with the International Public Sector Accounting Standards

(IPSAS).

We have carried out the audit of the accounts for the Financial Year 2012 based on

INTOSAI standards and, in particular, on IPSAS regime and in line with the additional

terms of reference forming an integral part of the Union's Financial Regulations.

We have planned the working activities according to our audit strategy to obtain a

reasonable assurance that the Financial Statements are free from material misstatement.

We have evaluated the accounting principles and related estimates made by Management

and we have assessed the adequacy of the presentation of information in the Financial

Statements.

Thus, we have obtained through the audit a sufficient basis for the opinion given below.

We have tested, on a sample basis, a number of transactions and relevant documentation

and we have obtained sufficient and reliable evidence in relation to the accounts and

disclosures in the Financial Statements.

During the audit all questions were clarified and discussed with the responsible officials.

The team had regular discussions with Mr Alassane Ba, Chief of ITU’s Financial

Resources Management Department, and with members of his staff or in other

departments, depending on the subject matter under consideration.

The result of the audit was communicated on 10th May 2013.

Pursuant to § 9 of the additional terms of reference governing external audit with regard

5

to comments by the Secretary-General for inclusion in this report, the Secretary-General

informed us through his colleagues during the final discussion on 15th May 2013 that his

comments would be sent to us. Those comments were received on 16 of May and have

been duly incorporated in this report.

We audited the ITU financial operating report on the audited accounts held by the

Organization relating to the financial results as at 31 December 2012, presented in

compliance with the Financial Regulations (2010 edition): Article 18, for the financial

year 2012.

A Letter of Representation referring to the Accounts for the Financial Year 2012, signed

by the Secretary-General and the Chief of the Financial Resources - Management

Department, was included in the Financial Statements and it is an integral part of the

audit documentation.

We audited also, according to Resolution 11 (Guadalajara 2010) resolves no. 6, the ITU

TELECOM World accounts for 2012 (Document C13/7, English language version).

Finally, we wish to express our appreciation for the courtesy shown by all the ITU

officials to whom we asked information and documents.

6

AUDIT CERTIFICATE

Independent Auditor’s Report

We have audited the financial statements at 31 December 2012 of the

International Telecommunication Union (ITU), comprising the Statement of

Financial Position, Financial Performance, the statement of changes in net

assets, the comparison of budgeted and actual amounts and the cash-flow

statement for the year ending on that date, as well as a summary of the

main accounting policies and other explanatory notes.

Responsibility of the ITU Secretary-General for the financial

statements

It is the responsibility of the Secretary-General to draw up and faithfully

present the financial statements in line with the requirements laid down in

the International Public Sector Accounting Standards (IPSAS) and in the ITU

Financial Regulations and Financial Rules. Furthermore, the General

Secretariat is responsible for designing, implementing and maintaining the

internal control system as it deems necessary to ensure the preparation and

fair presentation of financial statements that are free from material

misstatement, whether as a result of fraud or errors.

Responsibility of the auditor

It is our responsibility to express an opinion on ITU's financial statements

based on our audit. We conducted our audit in accordance with the

International Standards of Supreme Audit Institutions, published by

International Organization of Supreme Audit Institutions (INTOSAI). Those

standards require us to comply with ethical requirements, and to plan and

perform the audit in such a way as to obtain reasonable assurance that the

financial statements are free from material misstatement.

Audit involves performing procedures to gather evidence attesting about the

amounts and the data provided and disclosures in the financial statements.

The choice of procedures is left to the discretion of the auditor, including

assessment of the risk of material misstatement of the financial statements,

whether due to fraud or errors. In making those assessments, the auditor

considers internal control system in place in the entity for preparation and

fair presentation of the financial statements, in order to determine audit

7

procedures that are appropriate in the circumstances, but not with the aim

of expressing an opinion on the efficient functioning of the entity's internal

control system. Audit also includes assessment of the validity of the

accounting methods adopted and of whether the accounting estimates made

by the Secretary-General are reasonable, as well as appraisal of the overall

presentation of the financial statements.

We believe that the evidence obtained provides a sufficient and appropriate

basis for our opinion.

Emphasis of matter

The Statement of Financial Position shows a negative Net Asset (-227.7

MCHF) due to the impact of losses recognized directly in the Financial

Position of -335.2 MCHF mainly originated by provisions for actuarial liability

for the After Service Health Insurance (ASHI). Details of our analysis are

included in our report. Measures are being undertaken by the Management.

The Management has assured that it will monitor the effectiveness of these

measures.

Opinion

In our opinion, the financial statements present fairly, in all essential points,

the financial position of International Telecommunication Union as at 31

December 2012, and its financial performance, changes in net asset, cash

flows and the comparison of budget and actual amounts, in accordance with

IPSAS and the ITU Financial Regulations and Financial Rules.

In accordance with the additional terms of reference governing external

audit in Annex I to the ITU Financial Regulations and Financial Rules, we

have also issued a detailed report, dated 10 May 2013, on our audit of the

financial statements.

Rome, 13 May 2013

Giacinto DammiccoMember of Chamber of Audit forEuropean and International AffairsCorte dei conti of Italy

Giuseppe CogliandroPresident of Chamber of Audit forEuropean and International AffairsCorte dei conti of Italy

8

STRUCTURE OF THE ACCOUNTING STATEMENTS

1. The Financial Statements of ITU prepared and presented in compliance with IPSAS 1

included the following elements:

Statement of financial position – Balance sheet at 31 December 2012 with

comparative figures as at 31 December 2011 showing Assets (divided into Current

and Non-current assets), Liabilities (split into Current and Non-current liabilities)

and Net assets;

Statement of financial performance for the period which closed on 31 December 2012

with comparative figures as at 31 December 2011 showing the Surplus/Deficit for the

financial year;

A Statement of Changes in Net Assets for the period which closed on 31 December

2012, showing the value of the Net assets including the surplus or deficit for the

Financial Year including losses directly recorded in Net assets without being

transferred to the Statement of Financial Performance;

Comparison of budgeted amounts and actual amounts for the 2012 financial period;

Table of cash flows for the period closed on 31 December 2012, showing the inflow

and outflow of cash and cash equivalents, purposely regarding the operational,

investments and financing transactions and the treasury totals at the end of the

Financial Year;

Notes on the accounting statements providing information about accounting policies

and additional information necessary for a fair presentation.

STATEMENT OF FINANCIAL POSITION 2012

Assets

2. In 2012 Assets amounted to 360.3 MCHF and they decreased by 13.0 MCHF

(-3.5%) in comparison to the value recorded in 2011 (373.3 MCHF).

3. They consisted of Current assets, amounting to 243.0 MCHF, representing the

67.4% on Total Assets (same weight in 2011, 67.4%), and of Non-Current Assets,

equivalent to 117.3 MCHF, with 32,6% of weight on Total Assets (same weight in

2011, 32.6%).

9

Current Assets

4. Total current assets in 2012 amounted to 243.0 MCHF presenting a decrease of 8.5

MCHF (-3.4%) as compared to 2011 (251.5 MCHF). The decrease, in overall terms,

is broadly explained by the decrease in Investments (-32.7 MCHF), partially

reabsorbed with the increase in cash equivalent (+17.8 MCHF) and in Contributions

receivable (+7.9 MCHF). The basis for the evaluation of current assets is given in the

Accounting Principles (Note 3).

Cash and cash equivalent

5. The sub-heading "Cash and cash equivalent", totalling to 79.8 MCHF, increased of

17.8 MCHF (+28.7%) comparing to 62.0 MCHF in 2011, and it included cash in

hand and all the balances of ITU postal banks current account as at 31 December

2012. The mentioned above increase is mainly due to “Bank current accounts in

CHF” (+16.9 MCHF) which weight around 81% of the total sub-heading. A detailed

breakdown of Cash and cash equivalents is shown in the Note 6 of the Financial

Operating Report.

6. Under IPSAS 2, an indication is given in Note 6 to the financial statements of

liquidities held that are not available. In 2012 an amount of 12.3 MCHF is subject to

restrictions, comparing to 14.1 MCHF in 2011.

7. We asked all the banks having a business relation with ITU to confirm the current

accounts' balances as at 31 December 2012. we verified that the account’s balances

were properly recorded into the accounts. All variances detected have been explained

and justified. It is worthwhile mentioning that we have not received one direct

confirmation from one bank, the Busan Bank. We acknowledge that Management

made all the possible efforts to obtain it and, for the reconciliation, we have used the

bank’s statement received from ITU at year end.

Dual signatories should be required for amounts above CHF 5’000

8. Our audit of the banks’ confirmation revealed that, in some of the field offices, power

of signature (authorization in committing ITU in financial matters) is, in certain

circumstances, provided only to one person (often the Director of the field office),

meanwhile at ITU Headquarters, generally, operations with banks can be authorized

simultaneously only by two delegated people, “with no amount limit”, with the

exception of one bank’s confirmation which declared that one person has an

authorization to sign individually up to the maximum limit of CHF 5000. We did not

10

receive the list of authorized signatures for one bank.

Recommendation no. 1

9. Although we understood from Management about the feasibility of

implementing dual signatures in field offices, for example in a field office only a P

official could be present, we recommend Management to ensure dual signatories in

financial operations with banks for amounts above 5’000 CHF whenever possible, and,

in case the responsible officials on the field operates on an ITU’s bank account alone, he

should receive an ex-ante authorization from Management.

Comments by the Secretary-General:

These procedures are applied whenever possible. For Field offices where dual signature is

not possible due to specific constraints (legal constraints for some countries for bank

signatures), specific authorizations and monitoring will be applied.

Availability of financial reporting for field offices

Suggestion no. 1

10. It is worthwhile mentioning that all the banks account operational in field

offices are reconciled and supervised by ITU Management on a periodical base.

However, due to the fact that amounts are not inserted directly in the accounts by the

field officials, entry of all the movements in the IT accounting system (SAP) is

performed periodically at the level of Headquarters. Management is aware of this issue,

therefore we suggest to continue the efforts for implementing a suitable financial

reporting at level of field offices.

Comments by the Secretary-General:

I take note of this suggestion and inform you that a significant part of the identified issues

related to financial reporting will in principle be solved by training field offices relevant

employees.

Cash-in-hand at field offices: reconciliation of local currencies with amount recorded in

11

SAP not always possible

11. On 31 December 2012, the cash-in-hand kept by the ITU in CHF and foreign

currencies, amounted to 86 kCHF. We have performed, at year-end, a direct count of

cash-in-hand at the Headquarters and, remotely via videoconference, with two field

offices selected on a subjective sample basis.

12. Our audit revealed no discrepancies in the reconciliation between our counting and

the CHF amount recorded in SAP for the Headquarters and for one of the field

offices. However, for the other one, it was not possible to perform such

reconciliation, although the amount was minor.

13. Moreover, Internal Audit conducted an audit of ITU Regional Presence in 2012 of

three audit offices. This audit included controls on-the-spot of cash-in-hand managed

by these offices, but not at year-end. Internal Audit reported that not all the

movements in the petty cash registers were supported by adequate evidence and that

these registers were not kept up to date on a daily basis. In one case Internal Audit

found there was no petty cash register, however it was implemented at that time.

Recommendation no. 2

14. We consider the difference that we found due to reconciliation issue, as non-

material in terms of value. Nevertheless we recommend Management to strengthen

controls over the cash-in-hand, also having as a reference the recommendation made by

Internal Audit in its reports related to the ITU Regional Presence (see par. 13).

Comments by the Secretary-General:

Cash reconciliation is currently done on a monthly basis in field offices. Any counting

within a month will result in reconciliation issues due to this fact. Financial Resources

Management Department (FRMD) will ensure that a review of the current process is done

in 2013. Recent internal audit reports have already identified these issues as well as

internal control procedures to mitigate the related risks. Management has already agreed

with these recommendations and further action will be taken in 2013.

12

Investments

15. The sub-heading "Investments”, in 2012 amounted to 72.0 MCHF, decreased of 32.7

MCHF (-31.2%) comparing to 104.7 MCHF in 2011, and it included fixed-term with

maturity not over 9 months from the 31 December 2012. A detailed breakdown of

Investments by date of maturity is shown in the Note 7 of the Financial Operating

Report. An indication is given in the Note about restricted investments allocated to

extra-budgetary projects amounting to 31.1 MCHF in 2012, comparing to 38,4

MCHF in 2011.

Implementation of IPSAS 28, 29 and 30

16. Last year our predecessors, the SFAO, pointed out that “IPSAS 28-30 on financial

instruments will enter into force on 1 January 2013 and will necessitate the

preparation of comparative information in relation to 2012. The work involved

should not be underestimated and should ideally already have been begun by the

organization”.

Suggestion no. 2

17. Management assured us about its involvement in the implementation of IPSAS

28, 29 and 30 and we will follow-up the issue. Therefore, we suggest Management to

eventually reconsider the classification of “Investments” in non-current assets, and to

assess whether the investments will be held to maturity or not.

Comments by the Secretary-General:

I take note of this suggestion and confirm that this will be taken into account during the

implementation of IPSAS 28, 29 and 30 in 2013.

Receivables

18. Current receivables, whether for exchange or non-exchange transactions, represent a

net worth of around 82.4 MCHF in 2012 comparing to 76.3 MCHF in 2011. They

weighted around 34% on the total current assets comparing to around 30% in 2011.

13

They represent as stated in Note 8 of the Financial Operating Report the uncollected

revenue that Member States, Sector Members and associates have committed to pay

to ITU in respect of annual contributions, purchase of publications, satellite network

filings or other invoices issued by ITU.

19. Last year, our predecessors, the Swiss Federal Audit Office (SFAO), had corrections

made to the presentation and to the adjustment of certain provisions to ensure that the

criteria laid down in the IPSAS were fully respected. This year, all the invoices issued

from year 2011 backwards have been provisioned by the Management. We have

assessed the criteria used by the Management in 2012 for creating the provision for

losses on current receivables as correct. Furthermore, during our audit, we have also

verified the payments received in the first three months of year 2013, and our testing

revealed that a consistent amount has been paid.

20. Non-current receivables, also inserted and illustrated by the Management in Note 8,

whether for exchange or non-exchange transactions, resulted of a value of 15.2

MCHF (8.5 MCHF in 2011), are fully provisioned at 31 December 2011 in line with

the principles described in Note 3 to the financial statements. Additional explanations

are given under the Note 8 "Receivables".

Other current receivables

21. An amount of 7.9 MCHF (7.4 MCHF in 2011) is shown in the closing balance sheet

under other receivables. A detailed breakdown of “other receivables” is shown in the

Note 10 of the Financial Operating Report.

22. Last year, our predecessors, the SFAO noted that the amount owed by the Government

of the United States in connection with income tax was growing steadily since 2006,

the year in which last reimbursement was made. Therefore they recommended ITU to

ensure the reimbursement of these receivables “as quickly as possible”. During 2012

United States settled most of the income tax.

Inventories

23. In 2012, they were recorded at a net value of 0.7 MCHF with a decrease of 0.4 MCHF

compared to the 2011 net value of 1.1 MCHF. Inventories are related to publications,

souvenirs and supplies and they are detailed in Note 9 of the Financial Operating

14

Report.

24. We have carried out a physical stock checking at year end of a sample of items

randomly selected by us, not only related to publications and souvenirs but also in

relation to the items recorded fixed asset register (please refer to paragraph 45). No

major problems were identified, which may have an impact on the accounts at the

closing date (31.12.2012). We traced that all the tested items were properly recorded

into the Stores' accounts. The items we found as obsolete have been correctly

depreciated.

Non-current assets

25. Non-current assets as at 31 December 2012 totalled to 117.3 MCHF, recording a

reduction of 4.5 MCHF (-3.7%) as compared to 2011 figures (121.7 MCHF), mainly

due to the depreciation of the ITU buildings. The basis for the evaluation of Non-

current Assets is given in the Accounting Principles (Note 3).

26. The heading is composed by “Property, plant and equipment” (116,1 MCHF)

weighting 99.0% of the total non-current assets and by “intangible assets” (1.1

MCHF, 1.0% of weight). They are respectively illustrated in Note 11 and 12 of the

Financial Operating Report.

Property, plant and equipment

27. The heading showed a value of 116,1 MCHF, which is the net value at 31 December

2012 of the capitalised cost for the buildings (122.4 MCHF), machinery (3.3 MCHF),

furniture (1.6 MCHF), IT equipment (9.4 MCHF), and others assets (0.9 MCHF),

minus the related depreciation for each categories above listed (in total depreciation

amounted to 21.6 MCHF. They are illustrated in Note 11 of the Financial Operating

Report.

28. In the statement of the financial position, according to IPSAS 1, the recognition of

buildings as assets is required. This recognition is expressly related to the property of

them. For the initial recognition, IPSAS 17 indicates to refer to the costs of these

items or to a reliable fair value. Depreciation is charged systematically over the

asset’s useful life, and the depreciation method must reflect the pattern in which the

15

asset’s future economic benefits or service potential is expected to be consumed by

the entity. The residual value must be reviewed at least annually and shall equal the

amount the entity would receive currently if the asset were already of the age and

condition expected at the end of its useful life. Land and buildings are separable

assets and are accounted for separately, even when they are acquired together.

29. According to the ITU Financial Regulations, Annex II, the External Auditor has to

express whether “procedures satisfactory to the External Auditor have been applied to

the recording of all assets, liabilities, surpluses and deficits”.

30. In Note 3 of the Financial Operating Report “main accounting principles” sub

paragraph “property, plant and equipment” (p. 23/100) is stated that the initial

recognition of buildings was done at the “intrinsic value” “on the basis of the study

conducted by an external consultancy”, in order to define the IPSAS opening balance

sheet value. This was considered “historical cost”, and the depreciation was realized

referring to an “estimated useful life” that for the structure is of 100 years. Land, on

which ITU has a free “droit de superficies” was not considered in determining the

initial value of buildings.

31. In the Note 11 to the financial statements, the buildings recognized as non-current

assets were Tower, Varembé, Extension C and Cafeteria, and Montbrillant. Relating

to buildings, as already stated above, the net carrying amount varied from 115.3

MCHF at 1 January 2012 to 112.0 MCHF at 31 December 2012, due to an addition of

0.2 MCHF (the Popoff meeting room and the Museum), and the depreciation

recognized during the year of 3.5 MCHF.

32. The financing of the construction of a building for international organizations is

granted by the Swiss Confederation through FIPOI in the form of a loan on

favourable terms, i.e. a period of 50 years at an interest rate of 0%, while the land is

provided free of charge by the State of Geneva by mean of the “droit de superficie”.

The value of borrowings from FIPOI is illustrated in Note 15 of the 2012 financial

operating report.

“Droit de superficie”

33. ITU owns its buildings on the basis of a “droit de superficie”, defined as “une

servitude personelle (...) érigée en droit distinct et permanent” by which ITU has

“(…) le droit d’avoir ou de faire des constructions sur le fonds grevé”.

16

34. The original notarial act dated 22 December 1967 concerns the conclusion of a

contract for the establishment of the “droit de superficie” of a particle (nr. 5235) of

6123 square meters, belonging to the State of Geneva, in favour of the ITU. The right

is given free of charge (art. 3) and lasting until 31 December 2067. It consists of the

"right to have constructions and installations on the particle", with the statement that

they are "intended to accommodate the services of ITU". In 1999, the duration of the

“droit de superficie” was extended until 31 December 2079.

35. The “droit de superficie” is transferable, but in case of sale to an entity which do not

have a status similar to ITU’s one, the Republic and Canton of Geneva could exercise

a legal right of pre-emption.

36. The “droit de superficie” is renewable. At the end of its validity, and subject to non-

renewal, the buildings built on the particle would pass into the ownership of the

Republic and Canton of Geneva, with no other allowance than that concerning the

works of enlargement, alteration or renovation involving relevant complementary

interventions "not yet fully depreciated at the time of the extinction of law".

Recommendation no. 3

37. Considering that it is important and in ITU’s interest to extend the “droit de

superficie” granted to ITU by the State of Geneva since 1967, we recommend

Management to start, as soon as possible, the negotiations in this respect with the

competent Host Country Authorities.

Comments by the Secretary-General:

In January 2013, the Legal Adviser has already successfully contacted the Host Country

competent Authorities in order to initiate a negotiation process.

Depreciation should be in line with the duration of surface right

38. According to our analysis, we found that the depreciation of two buildings was

17

extended for a period not in line with the expiration of the surface right. We made a

recalculation of the potential impact on the Financial Statements of a new

depreciation value for the two buildings and we assessed it as not material.

39. Considering that, as stated in recommendation above (number 2, paragraph 14), a

new agreement on the “droit de superficie” should be negotiated, we agreed with the

Management to consider an adjustment in the accounts only in case the agreement

will not be reached.

Valuation of the Montbrillant building for the IPSAS opening balance sheet

40. We read in the Annual Activity Report of Secretary General for the year 2001 that

“The accounts relating to the Montbrillant building project were closed in 2001. Total

expenditure amounted to CHF 45.4 million, or CHF 1.6 million less than budgeted.

The project was financed by a loan, which will be repaid over a 50-year period

starting in 2002”.

41. The external consultancy in determining the “intrinsic value” of the Montbrillant, has

not taken into account, even as corroborative element, any of the actual costs incurred

in 2001, but has assessed the value according to the estimation used for all the other

building.

42. Considering that the construction of Montbrillant was realised only 9 years before the

external consultancy, we believe that actual construction costs could have been a

corroborative element or, even more, an important component of the estimation value

that ends in the determination of the “historical cost” (as defined in Note 3 of the

2012 financial operating report).

Renovation cost will need adequate resources

43. In the external consultancy (prepared in year 2010) it is also stated that for the

buildings were necessary investments for 35 MCHF over 10 years for major

renovation, of which the most conspicuous parts relate to the Tour (15 MCHF) and

Varembé (12 MCHF).

44. IPSAS 19 does not require to create a provision in case the date of the “obligation” is

uncertain, therefore the Management had a correct approach and it is compliant with

IPSAS. However, due to the relevant amount of the estimation for the major

renovation, we draw the Council’s attention that is important to start to consider costs

18

for renovation in the regular budget, in order not to have an unexpected impact in the

budget on the future years.

In case assets recorded in the register will not be found, a correction is needed

Recommendation no. 4

45. As also stated in the paragraph 24, we have performed a physical stock checking

of some fixed assets categories, such as a sample of items of furniture and IT equipment

and we have traced them into the accounts. We observed that the ITU responsible in

Facilities Management Division (HRMD Department) have not found some of the assets

during the physical stock checking at year end (around 0.73% of the acquisition value of

the assets concerned). We are aware that controls have detected part of these assets not

found at year end, however we recommend Management to continue its research and to

write-off the item that will not be found during 2013.

Comments by the Secretary-General:

I will instruct FRMD to coordinate with the Facilities Management Division to ensure the

continuation of efforts in 2013 and will clarify the existence and treatment of the items

not captured in the stock checking.

Intangible Assets

46. In 2012 Intangible Assets amounted to 1.1 MCHF and they increased by 0.1 MCHF

(+10%) in comparison to the value recorded in 2011 (1.0 MCHF).

47. Last year, our predecessor, the SFAO, highlighted that “(…) because the entry into

force on 1 April 2011 of IPSAS 31 on intangible assets, [this standard] will have to

be taken into account in the 2012 financial statements”. Moreover they added “this

standard, if correctly applied, will mean that IT projects are broken down into

different phases and only the design and implementation phases are to be

recognized”.

48. As stated by the Management in the related Note 12 in the financial operating report,

“following the first application of IPSAS 31, internal developments (…) have been

19

capitalized”. We have found no major issues and the consideration of SFAO in their

2011 Report “ITU has refrained for the time being from recording its own services in

this regard as assets. When IPSAS 31 enters into force on 1 April 2011, however, ITU

will have to change its approach in this regard for the 2012 annual accounts” can be

considered as closed (please refer to Annex 1).

Liabilities

49. In 2012 Liabilities amounted to 588.0 MCHF and they increased by 48.8 MCHF

(+9.0%) in comparison to the value recorded in 2011 (539.3 MCHF).

50. They consisted of Current liabilities, amounting to 144.9 MCHF, representing the

24.7% on Total Liabilities (weight in 2011, 27.1%), and of Non-Current Liabilities,

equivalent to 443.1 MCHF, with 75.3% of weight on Total Liabilities

(approximately same weight in 2011, 72.9%).

Current Liabilities

51. Total current liabilities in 2012 amounted to 144.9 MCHF presenting a decrease of

1.1 MCHF (-0.8%) as compared to 2011 (146.1 MCHF). The decrease, in overall

terms, is due to the effect, on one side, of the decrease of the heading “Suppliers and

other creditors” (-4.3 MCHF) and, on the other side, of the increase in the heading

“deferred revenue” (+3.5 MCHF). The basis for the evaluation of current liabilities

assets is given in the Accounting Principles (Note 3).

Suppliers and other creditors

52. An amount of 7.1 MCHF (11.4 MCHF in 2011) is shown in the closing balance sheet

under “Suppliers and other creditors”. A detailed breakdown is shown in the Note 13

of the Financial Operating Report.

Deferred revenue

53. The sub-heading "Deferred revenue”, in 2012 amounted to 132.2 MCHF, increased

of 3.5 MCHF (+2.7%) comparing to 128.8 MCHF in 2011. The majority of this

amount comes from contributions from the ITU membership (Member States, Sector

Members, Associates) for 2013 and from revenue for Satellite network Filing (SNF)

20

relates not yet finalized at the end of 2012. A detailed breakdown of deferred

revenues is shown in the Note 14 of the Financial Operating Report.

Provisions

54. The sub-heading "Provisions”, in 2012 amounted to 1.19 MCHF, increased of 0.2

MCHF (+2.0%) comparing to 1.17 MCHF in 2011. This heading included the

provision for litigations (0.72 MCHF) and provision for free satellite network filing

(0.47 MCHF).

Suggestion no. 3

55. We have revised the reports issued by the ITU legal advisor and we consider the

amount provisioned for possible loss in litigations substantially correct. Moreover, the

ITU legal advisor reported us that a litigation process has an average time of two years

and a half before its settling at ILO Tribunal. Therefore, according to the possible time

of settling, we suggest for the coming years to reclassify under non-current assets the

amount provisioned for litigation.

Comments by the Secretary-General:

I take note of this suggestion and confirm that this will be taken into account in 2013.

Other current liabilities

56. The sub-headings "Employee benefits” and “Other debts”, in 2012 amounted

respectively to 1.2 MCHF (0.7 MCHF in 2011) and to 1.8 MCHF (2.6 MCHF in

2011). A detailed description and breakdown is shown respectively in the Notes 16.1

and 18 of the Financial Operating Report.

57. In particular, short-term "Employee benefits”, recorded under “Current liabilities”,

are related to provision for overtime (0.4 MCHF in 2012) and to provision for

accrued leave (0.8 MCHF in 2012); provision for accrued leave related to long

term liabilities (9.2 MCHF in 2012) are recorded under Employee benefits. Our

checks have not revealed any major issue and the provisions are substantially

21

accurate.

Borrowings and financial debts

58. The amount related to ITU borrowed capital from FIPOI, for the construction and

renovation of some of its premises, is correctly recorded as short term (1.5 MCHF,

weighting 1.0% on total current liabilities), which corresponds to the instalment to be

repaid to FIPOI by ITU in 2013, and as long term (48.3 MCHF, weighting 10.9% on

total non-current liabilities). The amounts, also detailed in Note 15 of the Financial

Operating Report are also confirmed by the statement obtained from FIPOI.

59. Our predecessors, the SFAO, stated last year in its report that “These loans were

originally subject to interest. However, in 1996, the Federal Department of Foreign

Affairs of the Swiss Confederation ceased charging interest on these loans, and

henceforth only requires reimbursement of the principal according to a specified

repayment schedule”. Then SFAO, as required under IPSAS, requested ITU to

“include an indication in Note 3 to the financial statements of the value of the

interest relinquished by the creditor, which represented an in-kind contribution”.

Management has included in Note 3 the indication required by SFAO.

Non-current liabilities

60. Total non-current liabilities in 2012 amounted to 443.1 MCHF presenting an increase

of 49.9 MCHF (+12.7%) as compared to 2011 (393.2 MCHF). The increase, in overall

terms, is explained by the increase in employee benefits (+56.4 MCHF, +18,8%). The

basis for the evaluation of non-current liabilities is given in the Accounting Principles

(Note 3).

61. This heading comprised long-term debts (see paragraph “Borrowings”), third-party

funds, allocated or in process of allocation, liabilities against a capitalized fund

(SHIF) for the ITU Health Insurance Scheme and provisions covering obligations of

uncertain amount and timing mainly related to post-employment benefits.

Employee benefits (long-term)

62. The sub-heading "Employee benefits”, in 2012 amounted to 356.2 MCHF, increased

by 56.4 MCHF (+18.8%) comparing to 299.8 MCHF in 2011. It weighted 80.4% of

22

the total non-current assets and 60.6% of the total liabilities. This heading included the

actuarial liabilities for post–employment benefits under the ASHI plan (After Service

Health Insurance) (335.2 MCHF; in 2011 was 278.7 MCHF), provision for estimated

liabilities for the repatriation grant (11.7 MCHF; in 2011 was 11.8 MCHF) and

provision for accrued leave (9.2 MCHF; in 2011 was 9.2 MCHF). A detailed

description and breakdown of the employee benefit is shown in Notes 16.2 of the

Financial Operating Report.

Employee benefits: Repatriation grants

63. The provisions recognized at 31 December 2012 for repatriation grants amounted to

11.5 MCHF (11.8 MCHF in 2011) and is calculated according to the actuarial study

commissioned by the Management to CPA Conseil. The key assumptions used in 2012

are slightly different from the ones used by AON Hewitt for the calculation of the

ASHI post-employment benefits. Namely, CPA used as key assumptions, 2.0% as the

value of the discount rate (AON Hewitt used 2.24%), and 2.5% as salary increase

(AON Hewitt 3.58% for Professional and 3.48% for General categories of staff),

although differences might be justified.

Recommendation no. 5

64. However, this difference in key assumptions has not a significant impact on the

final calculation, in particular the lower discount rate utilized by CPA has an effect of

being more prudential in the final value, nevertheless, we recommend Management to

use similar key assumptions in all actuarial studies made where circumstances are

comparable, in particular regarding the discount rate used.

Comments by the Secretary-General:

I take note of this recommendation and will instruct FRMD to ensure the harmonization

of the chosen key assumptions in the actuarial studies when relevant in 2013.

Employee benefits: ASHI

65. In 2012, the provision for actuarial liabilities for the post-employment benefits,

namely ASHI (After Service Health Insurance plan) amounted to 335.2 MCHF

23

with an increase of over 56.5 MCHF (+20.2%) compared with 278.7 MCHF in

2011. This increase is due to the combined effect of changes in different key

actuarial assumptions, particularly the use of the new UN mortality table and the

discount rate (2.24% for 2012 and 2.50% for 2011). The calculation based on

actuarial assumptions was performed by an actuary, chosen by ILO (International

Labour Office).

Key actuarial and economic assumptions are consistent with previous year

66. The choice of actuarial assumptions is the sole responsibility of the organization. The

External Auditor checks their plausibility and if their consistency with IPSAS 25 and

with previous years and validates them.

67. The key assumptions have been reviewed by us and duly discussed with the

Management and with the Actuary and they are in line with economic trends and rates

and consistent with data available at ITU at the moment of our audit and we validated

them.

Provision for actuarial liabilities in the UN system are calculated differently

68. During the meeting of the Panel of External Auditors, held in New York in December

2012, we acted as facilitators on the IPSAS 25 “Employee benefits”. The outcome of

the discussion was that within the UN system it is not possible to have consistency in

any of the key assumptions used in relation to ASHI. This is explained by the different

characteristics of each Agency, such us, the number and composition of staff (salary

and career advancement, family allowances etc.), location (number of staff deployed in

field offices which effects illness and mortality).

69. Regarding the discount rate, an economic parameter, IPSAS 25 does not prescribe any

in particular. Our interpretation of IPSAS 25 is that the reference for the discount rate

in the public sector should be the 30-years Government Bonds rate. However, the UN

IPSAS Task Force recommended that the whole UN system uses as reference for the

discount rate, the AA Corporate Bonds yield curve.

70. As we stated above, IPSAS is not prescriptive on the issue and, in general, the discount

rate should reflect the trend in interest rates observed in the markets. Therefore from

this point of view the approach of the Management was correct not only because the

discount rate utilised reflected the trend observed in markets, but it was also consistent

24

with the UN system’s agreed approach.

71. Furthermore, it is worthwhile mentioning that within UN system, Agencies made

reference to different yield curves AA Corporate Bonds elaborated by different

operators (for instance, ITU and ILO used the Actuary’s curve). Therefore, as stated

earlier, the fact that provisions for actuarial liabilities are calculated on the basis of

mainly agency specific elements such as population, location and obligations toward

its staff, we draw the Council’s attention to the fact that is not possible to make a direct

comparison of the current situation of ITU actuarial liabilities with the liabilities of

other Agencies of the UN system.

Financial health is assured in the short-term, but remedial measures are necessary

72. ASHI provisions (335.2 MCHF) contributed considerably to the negative Net Assets

(-227.7 MCHF). We moreover reiterate our statement in the previous paragraphs

regarding the fact that it is not possible to directly compare the liabilities of ITU with

those of other Agencies. This also makes it difficult to undertake a direct comparative

analysis between the ITU underfunding and other UN Agencies.

73. Last year, our predecessors, the SFAO, wrote “while this situation in regard to the ITU

balance sheet is naturally a matter of concern, the Union's immediate, short-term

financial health is not directly affected”.

Recommendation no. 6

74. It is not possible to evaluate in this period when the UN financial health might be

compromised, therefore we recommend Management to be assisted by a full actuarial

review study in the coming years that it might produce answers, and possible solutions,

to this question.

Comments by the Secretary-General:

I take note of this recommendation and inform you that a process to perform a full

actuarial review and define different scenarios is in progress to evaluate corrective

measures for diminishing the unfunded ASHI obligation.

25

Principle of mutuality between ITU and ILO is not respected

75. Last years, our predecessors, the SFAO invited “the organization to clarify, as soon

as possible, the legal status of the health insurance. There seem to be widely

diverging opinions between ITU and ILO as to the applicable principle of

mutuality”.

76. Currently, SHIF maintains a separate accounting of contributions received and benefits

paid from ITU and ILO, it is only the performance of the assets that is divided pro-

quota. Contrary to ILO, ITU’s financial situation is unbalanced.

77. The ILO Treasurer and Financial Comptroller and HRM Director, in a letter dated 12

February 2012, drew the attention of ITU Management to its situation and suggested

that the two organizations discuss an eventual equalization process. He explained that

the difference in technical results is primarily attributable to two factors (i) the high

concentration of ITU insured in the Geneva area where healthcare cost are high” and

(ii) the higher ratio of ITU insured in the ‘retiree’ category as compared to the number

of insured in the ‘active’ category (0.61 for the ITU versus 0.44 for the ILO)”.

Discussions were initiated between the two organizations on the way forward.

78. Meanwhile the SHIF Management Committee proposed for, budgetary purposes, to

increase the base premia to 3.91 per cent in 2014, applicable to both originations.

However, the ILO Treasurer and Financial Comptroller informed ITU in a letter dated

5 December 2012, that ILO will include in its Programme and Budget Proposals for

2014-15, a provision for an increase in the base rate to 3.55 per cent, the rate necessary

for maintaining solvency for the ILO insured population only.

Recommendation no. 7

79. These statements confirmed that ILO will not accept the “principle of mutuality”

as defined by our predecessors, and therefore, we recommend Management to consider

alternatives to the SHIF, inside or outside the UN system.

Comments by the Secretary-General:

Since the beginning of 2013, ITU is in the process of studying alternatives to the SHIF.

26

SHIF audited by the Supreme Audit Institution of Canada: no major issues reported

80. It is worthwhile mentioning that SHIF Fund financial statements have been audited by

the Supreme Audit Institution of Canada. We had regular exchange of contacts and

information with them not only about the correctness of figures, but also about their

plausibility. We also discussed the audit methodology to apply to different key

assumptions used by ITU and ILO (in reference to the actuarial study). They did not

reported to us any major issue related to SHIF.

Employee benefits: Pensions (old Funds)

81. As also last year, an amount of 0.09 MCHF is recorded in the accounts at closure and it

relates to benefit obligations in the form of pensions payable to former staff members

under the Staff Superannuation and Benevolent Funds (see also related paragraph 107).

Net Assets

82. Net assets comprised allocated and unallocated own funds, the deficit for the financial

year and the effects of transition to IPSAS. In 2012, Net Assets resulted in a negative

value of -227.7 MCHF 2012, comparing to -166.0 MCHF in 2011 and to -94.3 in 2010.

83. This heading corresponded to the difference between liabilities and assets and it

included contributed capital, accumulated surpluses - or deficits -, the effects of

transition to IPSAS, reserves and ASHI related actuarial losses, as also shown in the

Statement of Changes in Net Assets1.

84. All the movements in Net assets are explained in different Tables and Notes of the

Financial Operating Report, in particular:

a) Table II “Statement of financial performance”, where is indicated the deficit for the

period.

b) Table III “Statement of changes in net assets” with the movements of allocated and

non-allocated own funds and IPSAS effects.

c) Table IV “Comparison of budgeted amounts and actual amounts”, where it is

indicated the “Loss on fund 1000 covered by withdrawal from Reserve Account”

and the “increase in fund 1010 Reserve”. In Table IV is not only listed the

“Comparison of budgeted amounts and actual amounts” but is also disclosed the

1 Refer to table III. Statement of changes in net asset for the period which closed on 31 December 2012.

27

accounting reconciliation between budget out-turns (actual amount) and amounts

recognized in the Financial Statements (in this regard, see also Note 33).

d) Note 3 “Main accounting principles” in the paragraph related to “recognition of

Funds”, in particular sub paragraph “Allocated own funds”, and in paragraph

related to “Reserve Account” (Reserve account is also described in Annex B1, in

particular paragraphs 45-47 of the Financial Operating Report).

e) Note 4 “Management of net assets and financial risks”, where are listed the

movements in the Reserve Account and the reconciliation between “own funds

allocated to the organization” –as in Table III- and the Reserve Account.

f) Note 19 “Allocated and unallocated funds”, for the part related to movements of

the allocated funds (at 31 December 2012, -101.8 MCHF).

Recommendation no. 8

85. Following the discussion at the Council of last year (on July 2013) about the

relation between Reserve Account and Net Assets, we noted that the Financial

Regulation was not in line with the accounting practice, therefore, Management

proposed to Council Working Group on Financial & Human Resources (CWG-FHR) an

amendment to the Financial Regulations. At the date of issuance of the Report the

amendments have not yet been approved. In case of approval, we recommend in the next

Financial Operating Report to adapt the current disclosure of Table I “Statement of

Financial position” and Table III “Statement of changes in net assets” (see paragraph

above), and relate notes, to the amended text of the Financial Regulations, providing a

detailed breakdown of all the component of the Net Assets.

Comments by the Secretary-General:

Pending the decision regarding the proposed modifications of ITU Financial Regulations

and Financial Rules during the Council 2013, I have instructed FRMD to consequently

adapt the presentation and disclosures related to Net Assets.

United Nations Joint Staff Pension Fund (UNJSPF) – liabilities have not been included

in the ITU's financial statements

86. Last year, our predecessors, the SFAO stated that “(…) no actuarial obligation has

been foreseen for what is the main retirement fund of the organization's employees”

28

and, furthermore, in order to comply with IPSAS 25, they stated that “the actuarial

obligation in respect of ITU staff pensions under UNJSPF should be reflected in the

balance sheet, insofar as the plan to which the organization subscribes is a ‘defined

benefit plan where the participating entities are under common control’ under IPSAS

25, on account of the following factors: a) organizations participating in the plan

share in the risk; b) UNJSPF Regulations in respect of share of future contributions;

c) organizational structure of UNJSPF (affiliated organizations).”

87. In relation to the 2011 Sessions of the Panel of External Auditors, SFAO reported

that “the Technical Group and the IPSAS Task Force agreed to state that there is no

need for the agencies to establish a provision for pension obligations” and they

concluded that it was nevertheless their duty as 2011 External Auditors of the ITU

accounts “to draw the Member States' attention to this type of potentially significant

risk, insofar as [we] believe that it is too soon for us to be able to form a broad

enough picture for a proper economic interpretation of IPSAS 25”.

88. SFAO concluded that “(…) since the situation is not only an ITU matter, [we]

consider that it is not necessary for the time being to express a reservation or make

any specific reference thereto in [the] audit opinion on the 2011 financial statements”

89. In December 2012 in the session of Technical Group of the Panel of External

Auditors, as facilitators of the discussion over IPSAS 25, we contributed a letter to

the UN Task Force on Accounting Standards (UNTFAS) on this matter. The

UNTFAS replied on 16 February 2013 that “in the event that the UNJSPF cannot

meet its pension obligations, the member organizations bear the liability for such

funding under Article 26 of the Regulations of the Pension Fund”.

90. Moreover, UNTFAS, declared that they were of the view “(…) that the UNJSPF has

neither the ability nor the plan to separate the obligation, plan assets and costs in the

future, and hence individual organizations will continue to treat the plan as if it were

a defined contribution plan in line with the requirements of IPSAS 25”.

91. In consideration of these statements above mentioned, we consider the position of the

Management on the issue in line with the UN guidance, however, in line wih the

SFAO position, considering the potential impact of such liabilities on the ITU’s

Financial Statements and on the Net Assets, we would like to draw the Council's

attention to this type of “potentially significant risk”, as also stated by our

predecessors.

29

Possibilities to offset Negative Net Assets

92. We observe that, ultimately, there are few “drivers” in order to offset negative Net

assets:

a) increase the level of Member States’ Contributions and voluntary contributions.

b) increase the level of Staff contributions to the SHIF (Staff Health Insurance Fund).

c) review of the benefits provided under the Staff Health plan for opportunities for cost

containment.

d) increase the level of internal savings, through a reduction of specific expenses.

e) increase the level of other revenues.

Suggestion no. 4

93. As remedial measures are necessary, these drivers have to be considered by the

Council: whereas the first driver is not within the Management’s remit, we suggest

Management to address the other drivers.

Comments by the Secretary-General:

I take note of this suggestion and this will be taken into account noting that some of

the drivers listed in the suggestion are sensitive and will need to be addressed at a

United Nations level to ensure a common approach of the issue.

Recommendation no. 9

94. We acknowledge the fact that Management is tackling some of the points,

for instance, there is the intention to increase the level of ITU contributions to SHIF

(3.91%) as proposed in the draft budget and we recommend constantly evaluating if

actions taken are indeed structural measures, aimed at decreasing the level of

underfunding.

30

Comments by the Secretary-General:

I take note of this recommendation and inform you that a process to perform a full

actuarial review and define different scenarios is in progress to evaluate corrective

measures for diminishing the unfunded ASHI obligation.

STATEMENT OF FINANCIAL PERFORMANCE 2012

95. This Statement showed the Organization's operating and financial revenue and

expenses classified, disclosed and presented on a consistent basis in order to

explain the year's net deficit or surplus. The result of the period resulted in a deficit

of 18.0 MCHF.

Revenue and Expenses

96. Total revenue amounted to 178.3 MCHF with a decrease of 12.7 MCHF (-6.6%),

as compared to 2011 (190.9 MCHF), chiefly owing to the decrease of i) the

contributions (-1.6 MCHF, -1.2%), which weighted 71.0% of the total revenue, in

particular the ones received from Member States (weighting 67.9% on total), ii) the

other operating revenues (-3.0 MCHF, -7,1%), in particular the decrease in extra-

budgetary revenue related to project support and iii) the finance revenue (-7.8

MCHF, -87.2%), mainly generated in unrealized exchange-rate gains, as also

reported in Note 22 of the Financial Operating Report.

97. Total expenses totalled 196.3 MCHF with a slight increase of 0.2 MCHF (+0.1%),

as compared to 2011 (196.1 MCHF). Employee expenses, which weighted the

75.6% of the total expenses, increased by 4.1% (+5.9) and the most important

subheading was “salaries and allowances” amounting to 104.6 MCHF, which

weighted 68.6% of total expenses.

98. A segmented report is given in the Note 32 of the 2012 Financial Statements. The

aim of such segmentation is to be able to assign expenses directly to the segments

concerned. The methodology also provides for a distribution of expenses and

revenues, primarily by fund and cost centre.

99. Considering Employee expenses, during our auditing, we observed that personnel

dossiers are mainly kept in a room in a paper copy and they are not digitalised.

Management reported to us that the implementation of an eventual software could

31

have a relevant cost.

Digitalisation of personnel dossiers

Recommendation no. 10

Recommendation no. 10

100. Although our analysis of the correspondence of the data inserted in the IT

System with personnel dossiers did not revealed any major issue, we recommend the

Management to start to evaluate the cost-effectiveness to digitalise personnel

dossiers, not only in order to prevent that an accidental event might bring to loose

fundamental data, but also to allow a direct interface of personnel dossiers with SAP

HR.

Comments by the Secretary-General:

I take note of this recommendation and inform you that HRMD is exploring this

possibility.

STATEMENT OF CHANGES IN NET ASSETS FOR THE PERIOD WHICHCLOSED ON 31 DECEMBER 2012

101.Table III “Statement of changes in net assets” represented the movements of

allocated and non-allocated own funds and IPSAS effects. Our comments on this

table are reported in paragraph 85.

COMPARISON OF BUDGETED AMOUNTS AND ACTUAL AMOUNTS FOR THE2012 FINANCIAL PERIOD

102.The table IV "Comparison of budgeted amounts and actual amounts for the 2012

financial period” is foreseen in compliance with IPSAS 24, which requires that a

comparison of budget amounts and actual amounts arising from execution of the

budget itself should be included in the Financial Statements. The Standard also

foresees the disclosure of the reasons concerning the material differences occurred

between budget and actual amounts.

103. In the Table IV there is also included the accounting reconciliation of the

32

differences between the budget out-turn (actual amounts) and the amounts

recognized in the accounting statement. Further details are provided in Note 33 of

the Financial Operating report and we also refer to the Secretary-General's

comments reflected in the financial operating report. The audits showed that

transfers of appropriations between Sectors were carried out in conformity with

Article 11 of the Financial Regulations.

TABLE OF CASH FLOWS FOR THE PERIOD CLOSED ON 31 DECEMBER

2012

104.The Table of cash flows identifies the sources of cash inflows, the items on which

cash was spent during the reporting period, and the cash balance as at the

reporting date.

105. In 2012 ITU reported a negative cash flows from operating activities (-13.0

MCHF) in comparison with 2011 when there was a surplus (+3.3 MCHF). Same

in 2012 and 2011 negative cash flow was reported also from finance activities

(-1.5 MCHF), due to the repayment of FIPOI loan. Net cash flows from

investment activities showed an increase from 10.9 MCHF in 2011 to 32.3 MCHF

in 2012, mainly due to the decrease in Investments (as also stated in paragraph

15).

106.The net result in cash and cash equivalents showed an increase of 17.8 MCHF in

2012 and an increase of 12.8 MCHF in 2011. We checked the underlying entries

by selecting samples from some accounts. The result was that all transactions

chosen were properly backed-up by supporting documentation. The Cash Flow

Statement is thus verified and confirmed.

STAFF SUPERANNUATION AND BENEVOLENT FUNDS

107. The Funds reported in Annex B2 of the Financial Operating report ITU Financial

Statement are three and are named “Reserve and Complement Fund” (with Total

Assets amounting to 6,3 MCHF), “Provident Fund” (with Total Assets amounting to

around 1,5 MCHF) and “Assistance fund” (with Total Assets amounting to around

0,2 MCHF). We have audited the three Funds and the underlying transactions

without identifying any error and/or misstatement.

33

108. For the “Reserve and Complement Fund” and for the “Provident Fund” in the

Liabilities, under the item “Employee benefits” are recorded two actuarial provisions

respectively of 54 kCHF and 36 kCHF, in line with an actuarial expertise performed

in the year 2010.

Recommendation no. 11

109. Last year our predecessors, the SFAO, declared that “it has not proved

necessary to conduct a new actuarial study. Given that the commitments in question

are relatively minor, the 2010 study is sufficient”. Therefore, in line with our

predecessors, and in view of the not relevant value of these provisions in comparison

with the value of the Assets, we recommend to have an actuarial review every 5 years.

Comments by the Secretary-General:

I take note of this recommendation and have instructed FRMD to conduct in 2015 a new

actuarial study for the old Pension Fund.

UNITED NATIONS DEVELOPMENT PROGRAMME (UNDP), ICT-DF, and

TRUST FUNDS

110.Rule 5 in Annex 2 of Financial Regulations provides that “a separate account for

each voluntary contribution or trust fund shall be opened in a special account of

the Union”.

111. In annex B3 of the Financial Operating Report, there are listed two projects

currently related to UNDP activity. Annex B4 of the Financial Operating Report

showed the Trust Fund projects. Part of them is financed by a withdrawal from

ICT-DF, authorized by a decision of the ICT-DF Steering Committee. Other

project are funded with specific contributions and regulated by agreements with

donors. In Annex B6, are listed projects related to ICT-DF.

112.Management will perform a review of the Annexes and tables in the coming years

and we will follow-up the whole re-drawing of the annexed tables.

34

FOLLOW UP OF RECOMMENDATIONS OF OUR PREDECESSORS

113.We have reviewed the External Auditors reports of the Swiss Federal Audit

Office for the period of time from 2008 to 2011 and the corresponding comments

by the Management. Annex 1 collects all the audit recommendations issued by

SFAO.

114.The recommendations that we will evaluate as “closed” in this Annex 1, will not

be enclosed again in next year’s Audit Report, unless they need an annual follow-

up.

115. In addition, Annex 1 also includes the comments received from ITU Management

at the time of the issuance of the corresponding Report and, when possible, the

latest status on actions taken by Management.

35

ANNEX 1

Recommendation raisedby Swiss Auditors

Comments received fromSecretary-General at the time of the

issuance of the report

Status asreported by ITU Management related

to Swiss Auditors’ report

Status on actions takenby Management as evaluated by Italian

Court of Audit

Rec. 12010

reiteratedin 2011

I recommend that ITU makes thenecessary corrections in regard tovaluation of inventories and adaptsits IT system accordingly, in order toensure correct valuation ofinventories in line with IPSAS.

A draft policy for the valuation of

inventories was submitted to the

External Auditor’s colleague in

November 2011. This policy

determined rules for the valuation of

inventories of publications with

depreciation calculated linearly. We

will conduct a study of the costs of

publications that will include staff

costs so as to demonstrate our

approach and have it validated by the

new External Auditors in 2012.

Inventories valuation policies are in

the process to be reviewed by our

new External Auditors.

No adjustment has been proposed bySFAO over the issue, so the rationalof the recommendation is not clear.We will perform an analysisaccordingly in the coming years.

36

Report Recommendation raisedby Swiss Auditors

Comments received fromSecretary-General at the time of the

issuance of the report

Status asreported by ITU Management related

to Swiss Auditors’ report

Status on actions takenby Management as evaluated by Italian

Court of Audit

Rec. 22008

Rec. 32009

Transactions carried out manuallyoutside the SAP environment aresources of error and dysfunction andgenerate additional tasks which may notbe reflected in the job descriptions of thestaff concerned. These tasks, conductedwithout any real backup, lead to delays.I once again invite ITU to move asquickly as possible to integrate the BCSproject management tool into the SAPsoftware.Accordingly, I invite ITU:– To make a decision on possibly

incorporating into the GrantManagement (GM) module allprojects that are not operationallyand financially closed, to enablecorrect calculation and distributionof interest on investments inconnection with projects.

– To define the main technicalcooperation processes and assigncorresponding responsibilities.

– To implement the necessary trainingmeasures for efficient use of thenew SAP environment in thetechnical cooperation area.

Comments by the Secretary-General:The two recommendations 1/2008 and2/2009 are closely linked. In 2011 theFinancial Resources ManagementDepartment, the TelecommunicationDevelopment Bureau (BDT) and theInformation Services Departmentconducted a study into whether it wouldbe necessary to introduce a secondaccounting system in USD, with thesupport of consultants. This studyconcluded that training in the GMmodule should be stepped up, so as tomake maximum use of the specificitiesof this module.Some progress has been made as regardsthe administrative management ofprojects. All projects on which there hasbeen no action for several years havebeen closed and any remaining fundsplaced in a suspense account (for thereimbursement of donors, use in otherprojects, etc.). Donors are contacted todecide the subsequent use of thesefunds.As regards the SAP GM system, a studyor gap analysis was conducted in 2011in order to determine the developmentrequirements that would allow for theoptimal and adapted use of the system.

SAP Grant Management (GM) was

implemented by ITU in January 2010

for the financial management of

technical cooperation projects. The

related financial processes have been

reviewed in 2011 and are in the

process of being optimized and the

users retrained.

Although we are not the owner ofthis recommendation, we confirm theon-going process of optimizing theimplementation of GrantManagement into SAP.

37

Reference Recommendation raisedby Swiss Auditors

Comments received fromSecretary-General at the time of the

issuance of the report

Status asreported by ITU Management related

to Swiss Auditors’ report

Status on actions takenby Management as evaluated by Italian

Court of Audit

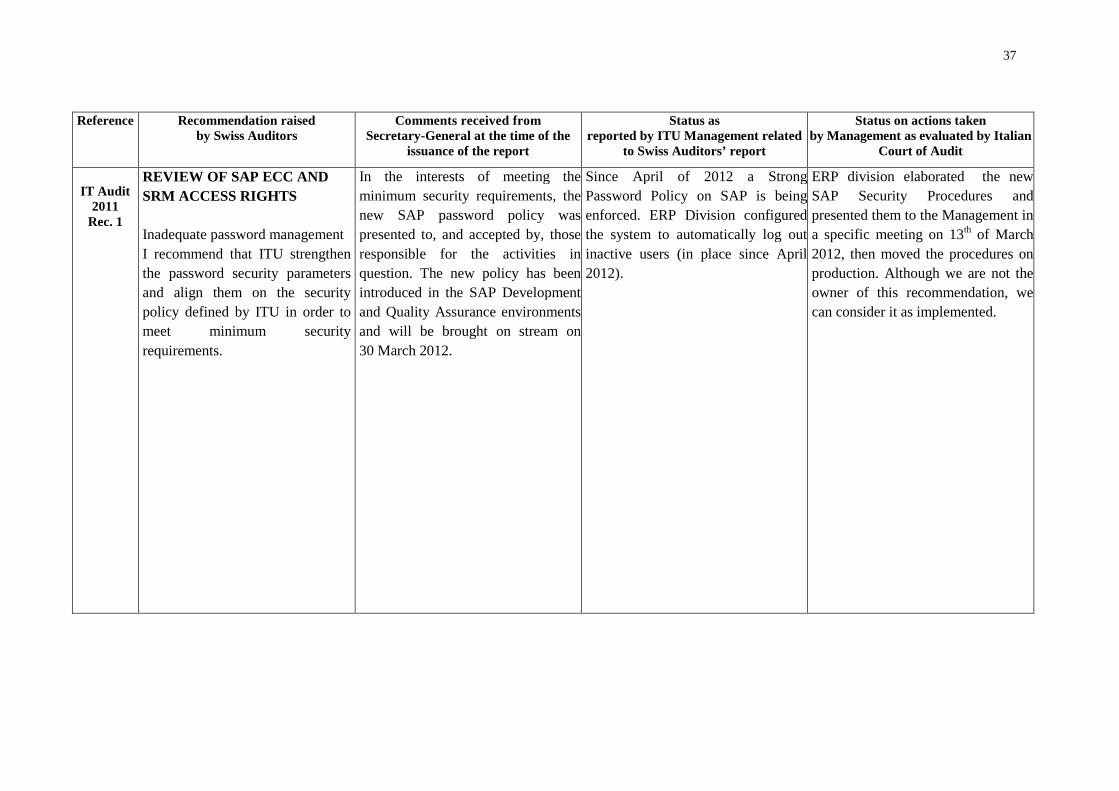

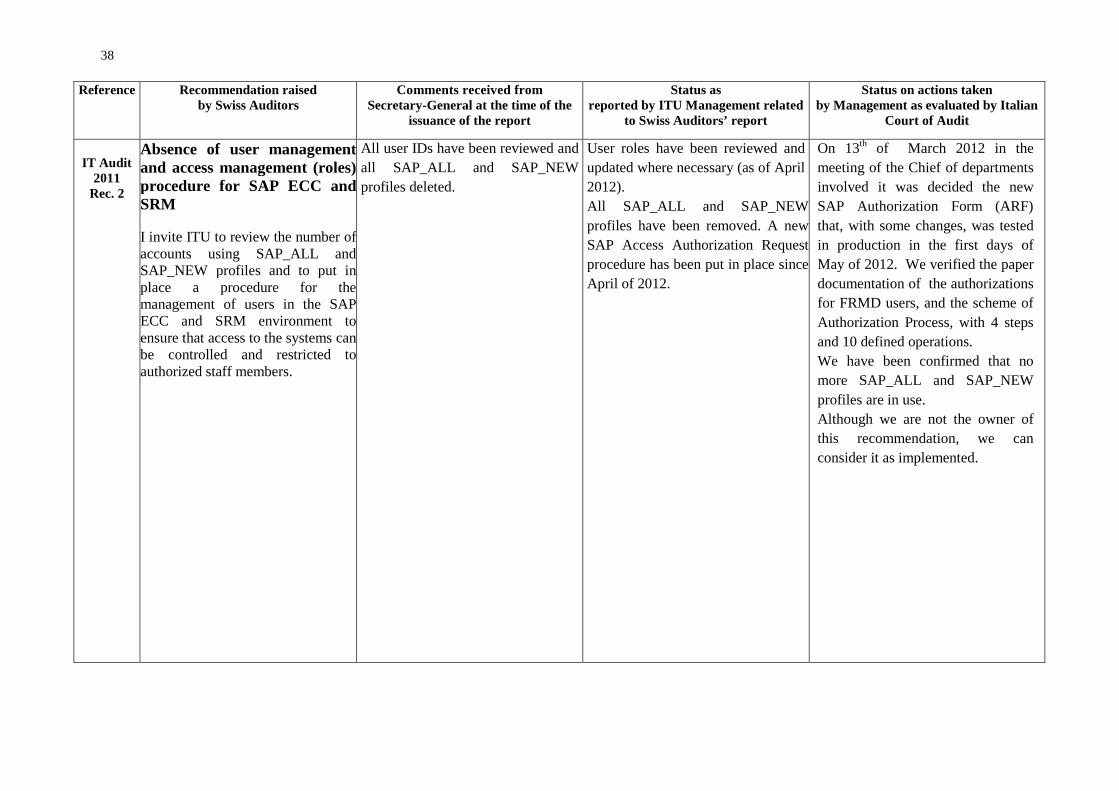

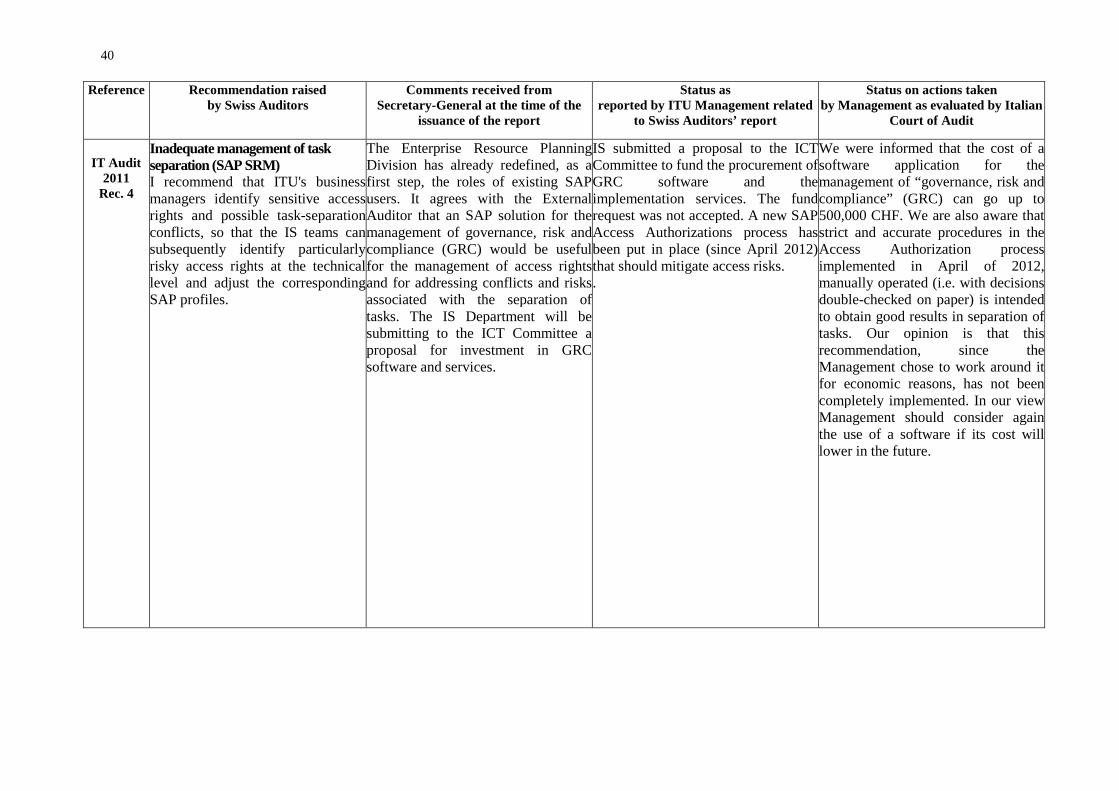

IT Audit2011

Rec. 1

REVIEW OF SAP ECC AND

SRM ACCESS RIGHTS

Inadequate password management

I recommend that ITU strengthen