Embed Size (px)

Citation preview

Rice value chains in SE Asia

Andrew W. Shepherd FAO Consultant

Solo, Indonesia, September 2016

My presentation

1. What do we mean by “value chains”?

2. Traditional rice value chains in SE Asian countries

3. Scope for developing modern value chains for rice

What do we mean by “value chains”

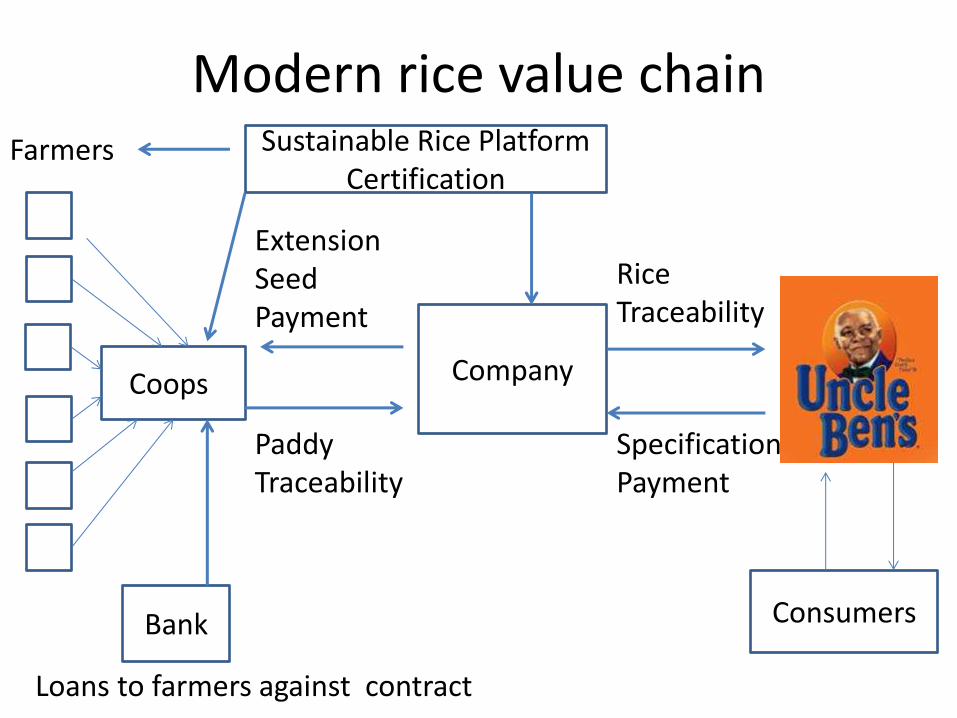

The modern value chain

Value chains involve identifying the needs of consumers and carrying out activities necessary to ensure that those needs are met, through coordinated linkages that add value at all stages of the chain.

Modern rice value chain

Coopss Company

Extension Seed Payment

Paddy Traceability

Bank

Loans to farmers against contract

Farmers Sustainable Rice Platform Certification

Specification Payment

Rice Traceability

Consumers

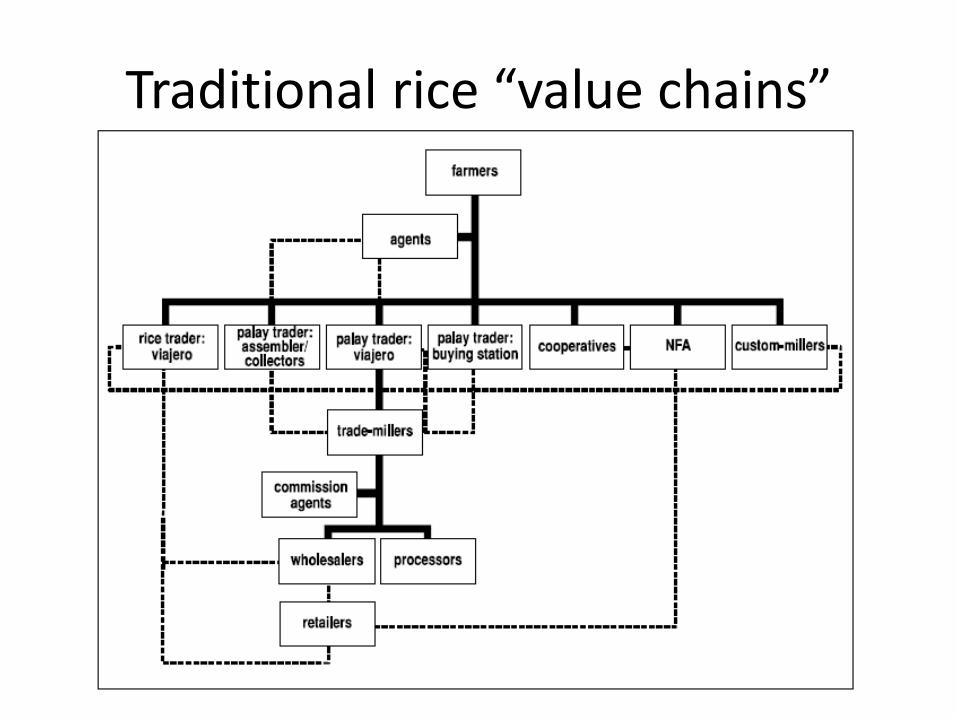

The traditional value chain

Value chains are basically the production-marketing system for a commodity in a country (e.g. the Indonesian rice value chain)

Traditional rice “value chains”

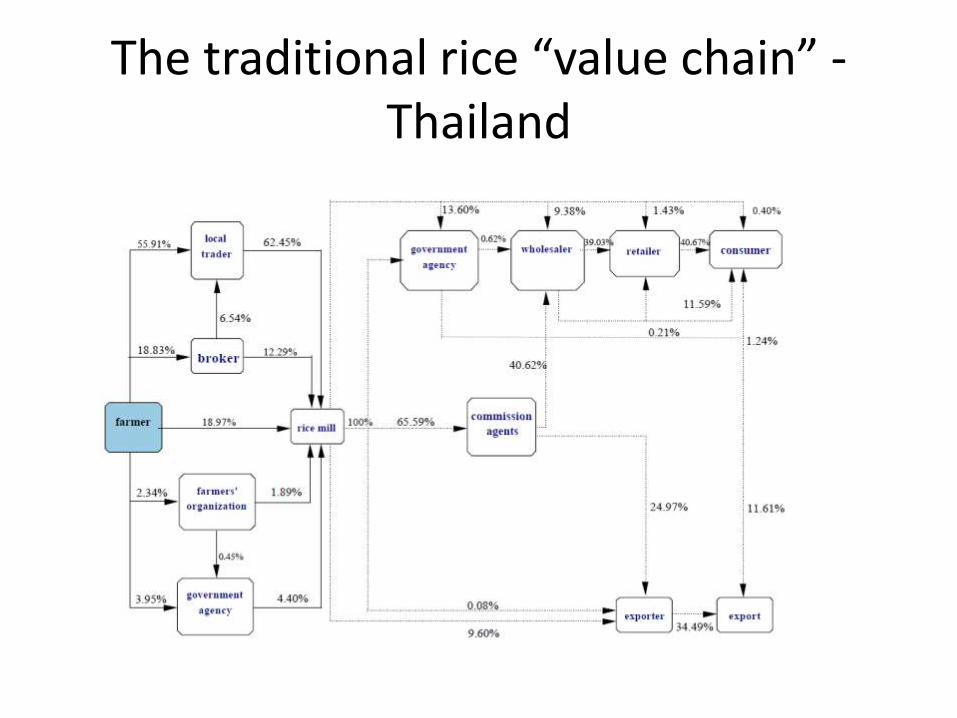

The traditional rice “value chain” - Thailand

Whichever definition you use

• and chains need to be economically, environmentally and socially sustainable

Traditional rice “value chains” in SE Asia

Cambodia • Four different production systems depending on the

area. Southern zones can produce three IRRI crops a year

• Average farm area 2ha. Adaptation to modern production systems has been slow but heavy use of pesticides, particularly on IRRI varieties

• Traditional non-aromatic varieties very important for local consumption

• Domestically, farmers sell wet and dried paddy to traders/ collectors and mills.

• Rapid increase in harvest mechanization in last decade, reflecting labour shortages and market opportunities

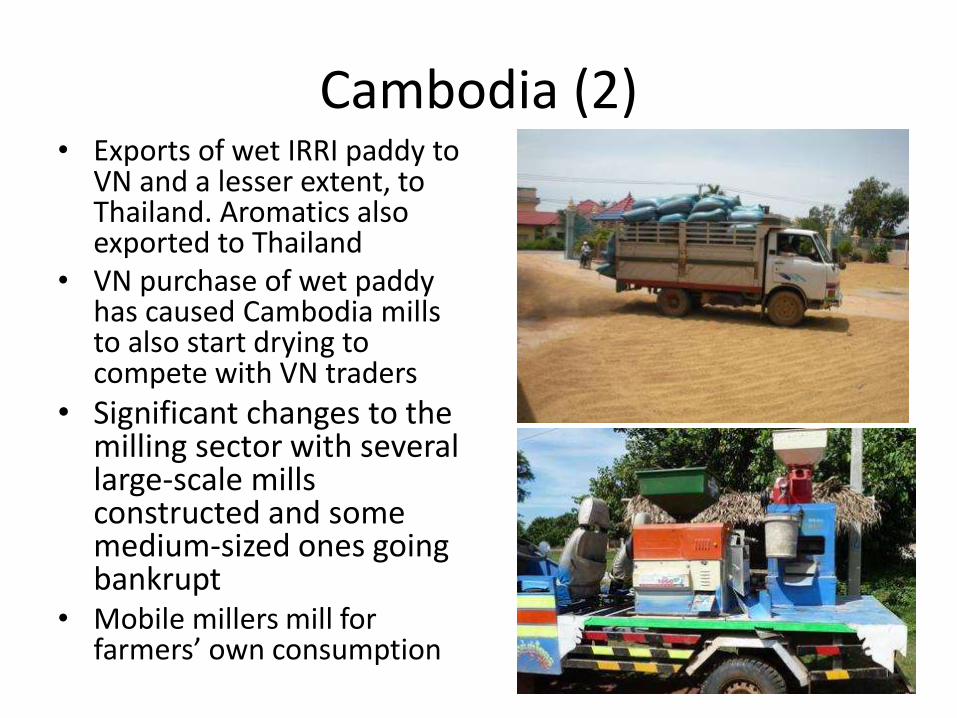

Cambodia (2) • Exports of wet IRRI paddy to

VN and a lesser extent, to Thailand. Aromatics also exported to Thailand

• VN purchase of wet paddy has caused Cambodia mills to also start drying to compete with VN traders

• Significant changes to the milling sector with several large-scale mills constructed and some medium-sized ones going bankrupt

• Mobile millers mill for farmers’ own consumption

Indonesia

• Two harvests (Feb-May 60%; Oct. onwards 40%)

• Rice harvesting, post-harvest and milling are complex and vary across the country

• Threshing equipment usually rented but delays between harvest and threshing cause quality and quantity losses, as does poor drying

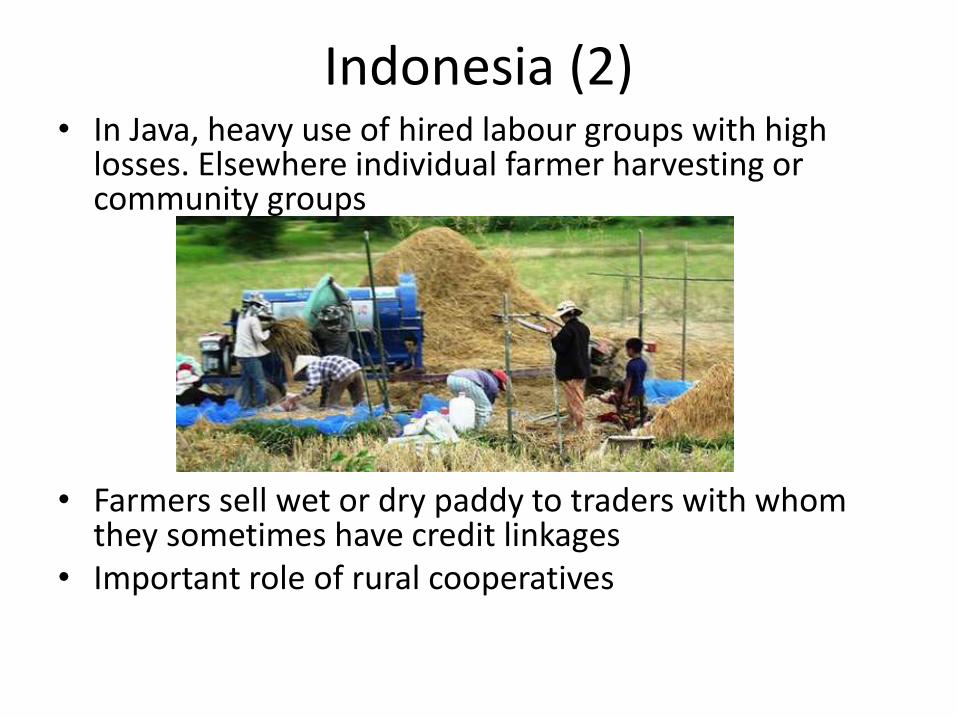

Indonesia (2) • In Java, heavy use of hired labour groups with high

losses. Elsewhere individual farmer harvesting or community groups

• Farmers sell wet or dry paddy to traders with whom they sometimes have credit linkages

• Important role of rural cooperatives

Indonesia (3)

• Some modern, high-quality mills mainly supplying supermarkets but most are antiquated, with low conversion rates.

• Around 110,000 mills. Surplus capacity. Some smaller mills just remove the bran and sell on to larger mills

Laos

• Insufficient returns to labour for small farmers and number of rice farmers declining

• Ageing farm population

• At same time, yields are increasing, mainly through wet season lowland production

• Improved seed availability required

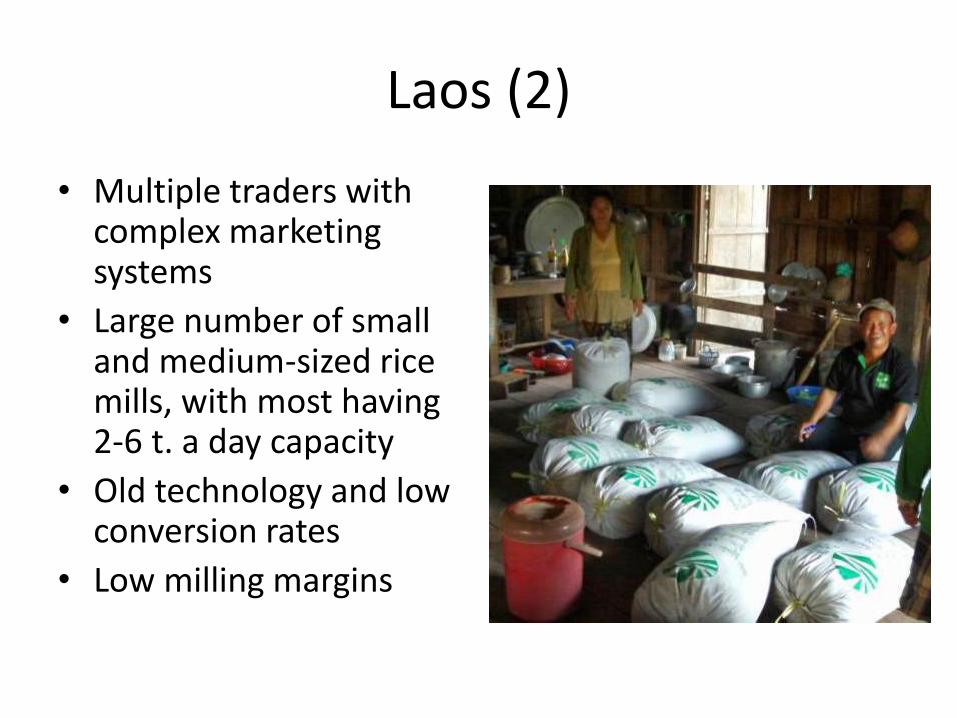

Laos (2)

• Multiple traders with complex marketing systems

• Large number of small and medium-sized rice mills, with most having 2-6 t. a day capacity

• Old technology and low conversion rates

• Low milling margins

Laos (3)

• No resources to upgrade existing mills but some investment in new, larger mills

• Trade restrictions within country and for export (e.g. wet paddy to VN or China) but likely to be significant informal trade of paddy to neighbouring countries and some imports of rice

• Quality issues for sale on formal export markets

Myanmar

• Following marketing liberalization and abolition of government marketing agency Myanmar again has (small) export surplus

• Farm size 2-3ha on average. HYV and traditional. Inadequate seed availability

• 80% production wet season, other 20% in irrigated areas.

• Farmers often have other work, but employ labour when needed. Obtaining finance a common problem.

• Government provides seasonal loan but insufficient • Possibility of warehouse receipt finance being

actively investigated

Myanmar (2)

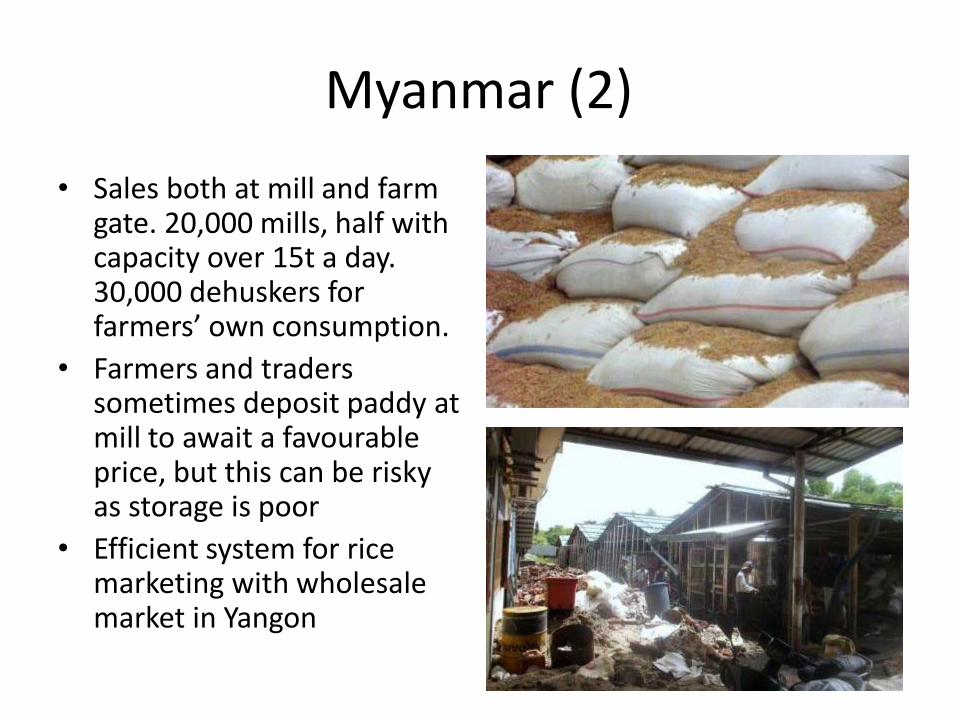

• Sales both at mill and farm gate. 20,000 mills, half with capacity over 15t a day. 30,000 dehuskers for farmers’ own consumption.

• Farmers and traders sometimes deposit paddy at mill to await a favourable price, but this can be risky as storage is poor

• Efficient system for rice marketing with wholesale market in Yangon

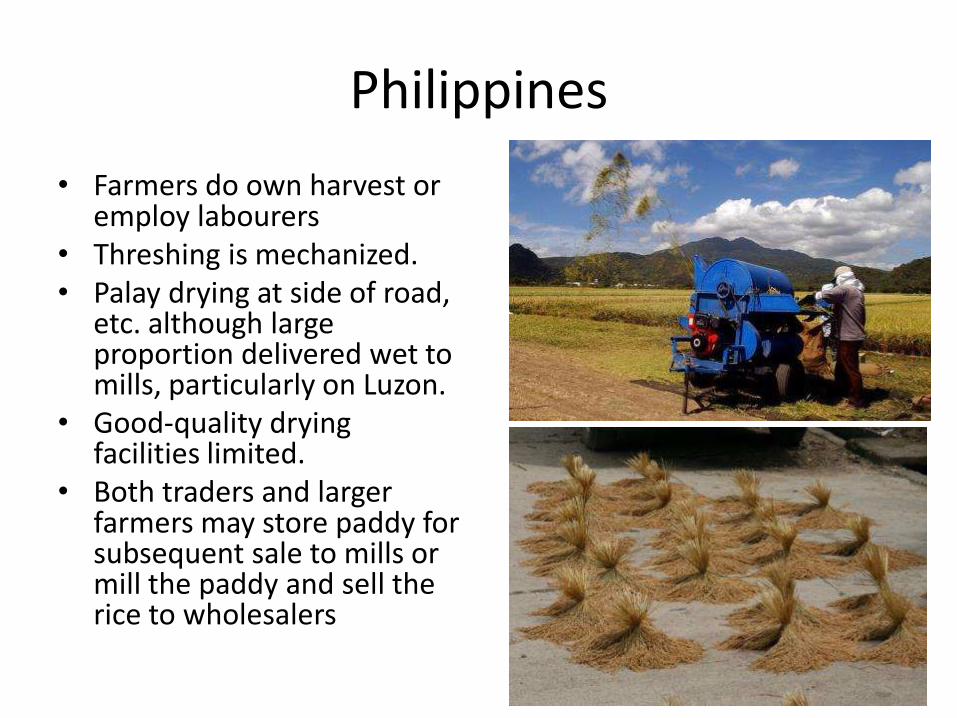

Philippines

• Farmers do own harvest or employ labourers

• Threshing is mechanized. • Palay drying at side of road,

etc. although large proportion delivered wet to mills, particularly on Luzon.

• Good-quality drying facilities limited.

• Both traders and larger farmers may store paddy for subsequent sale to mills or mill the paddy and sell the rice to wholesalers

Philippines (2)

• Palay for farmers’ own consumption milled at small huller mills known as “kikisan”

• Financing a major constraint. Farmers can receive production loans from traders as result of long-term farmer-trader relationships.

• Market dictated by price and does not reward good post-harvest handling. Rice sold with highest proportion of brokens in the region.

Philippines (3)

• Around 10,000 mills but most not of good standard.

• Government continues to target self-sufficiency although rising production costs, rapidly growing population, production difficulties and antiquated milling equipment make this difficult.

• NFA has intervened in the market both as a buyer of palay and as an importer of rice. The Agency is highly indebted and its activities criticised for disrupting the market.

Thailand • Farmers sell directly to

traders or to mills at assembly markets. Around 1000 mills.

• Poorest 50% buy more rice than they produce.

• Very few facilities for farmers to mill own paddy

• Millers sell to exporters or domestic rice traders, who may carry out further polishing, cleaning and broken separation

Thailand (2)

• Exports usually account for 40-50% of production.

• Retailing most advanced in region. Rice increasingly sold branded, with 5% brokens

• Limited contract farming

• Biggest problems faced as result of abuse of the Paddy Pledging Scheme

Vietnam

• Main production systems: Mekong Delta; Red River Delta and northern uplands

• Liberalized market and switch to individual rather than collective production from 1981 moved VN from deficit to major exporter

• Farm size remains very small and rice quality remains low with use of farmer-retained seed common

• Production of specific varieties relatively rare

• High-yielding varieties with fertilizer give 3-4 crops a year

Vietnam (2)

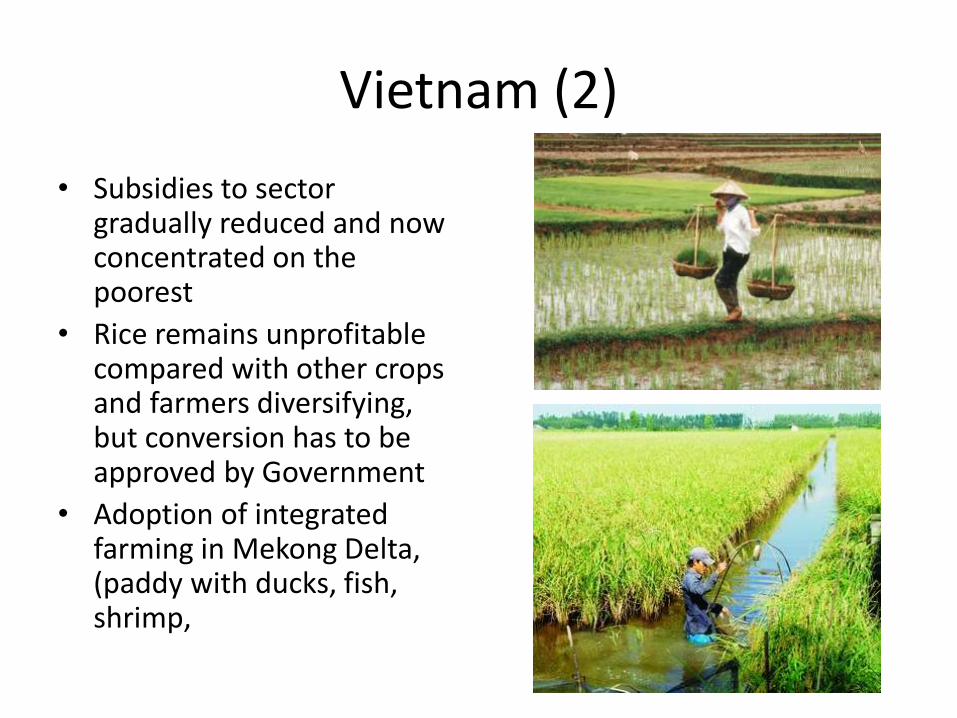

• Subsidies to sector gradually reduced and now concentrated on the poorest

• Rice remains unprofitable compared with other crops and farmers diversifying, but conversion has to be approved by Government

• Adoption of integrated farming in Mekong Delta, (paddy with ducks, fish, shrimp,

Vietnam (3)

• Significant yield increases as a result of policy reform and IRRI varieties

• Land consolidation has permitted mechanization but constrained by lack of finance. Harvesters owned by mills, richer farmers (who rent them out) and coops

• Farmers sell through collectors and directly to mills. Close relationship between traders and farmers and credit arrangements sometimes involved

• Dehusking (to produce brown rice) and polishing (to the white rice stage) often done by different companies.. One estimate: 300,000 dehuskers and 30,000 milling plants

Vietnam (4)

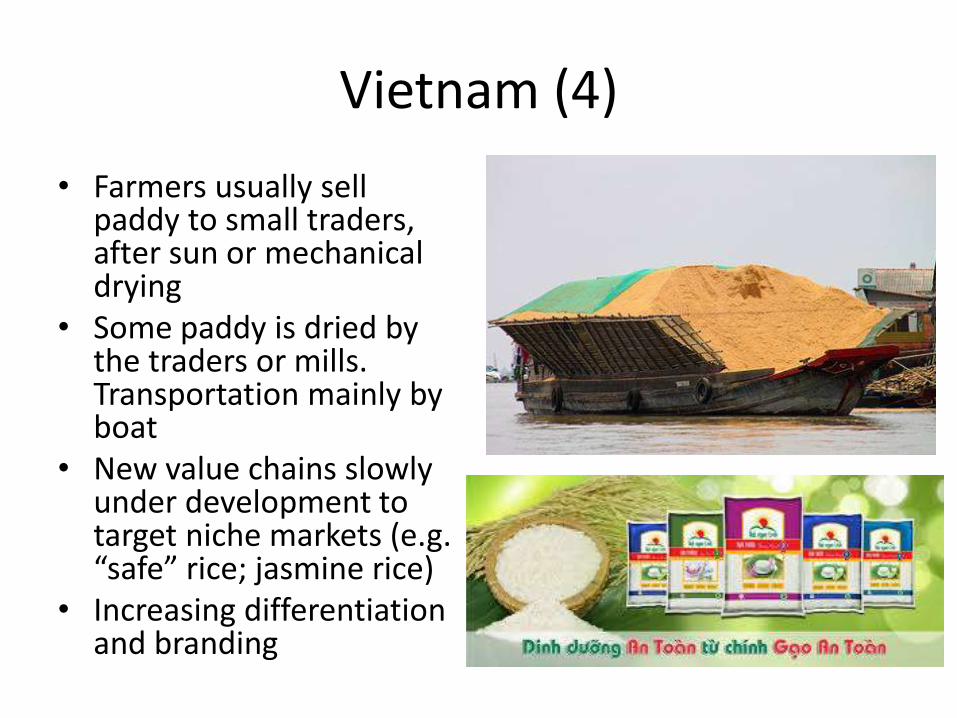

• Farmers usually sell paddy to small traders, after sun or mechanical drying

• Some paddy is dried by the traders or mills. Transportation mainly by boat

• New value chains slowly under development to target niche markets (e.g. “safe” rice; jasmine rice)

• Increasing differentiation and branding

Summary of main issues relating to traditional value chains

• Small size of individual farms, unimproved seeds, farming systems fairly slow to change, low yields and poor returns; ageing farmers

• Poor post-harvest handling (harvesting, threshing, drying)

• Small and inefficient mills with relatively little new investment in most countries

• Suspicion of intermediaries, including often by donor organizations

• Farmers are consumers too!

• Government involvement in value chains (everywhere)

• Obsession with self-sufficiency (Indonesia; Malaysia; Philippines)

• BUT!

– Evidence of dynamic response where opportunity presents itself

Some conclusions re traditional chains

• Difficulties are experienced throughout the value chain. This argues for a “whole chain” approach to upgrading

• There is little point in improving production techniques if post-harvest handling, milling and storage are not also considered

• Mills and traders are increasingly concerned with product quality. They should be seen as agents of change

• Development agencies need to work more with traders and millers and not see them as the “evil middlemen”.

The scope for developing modern value chains for rice

All modern value chains are driven by consumer trends

• urbanization

• growth of supermarkets

• women’s employment (urban and rural)

• smaller families

• refrigerators and cars

• demand for processed, semi-processed and ready-to-eat products

• globalization

• increased awareness of quality and safety

Modern value chains involving contract

farming can benefit farmers

… – credit access is enhanced (in-kind or via banks)

– inputs can be more easily obtained (less uncertainty regarding availability, timing, quality)

– services and technological assistance are also sometimes available (mechanization, transportation, extension)

– production and management skills of groups enhanced

– market outlet is more secure, promoting a reliable revenue stream and income stabilization

– for perishable produce, production planned to only meet demand reduces losses

Possible risks for farmers

– firms might renege on contractual terms:

• of particular concern for long-term crops (e.g. oil palm) or other products where there is “asset specificity”

– firms may fail to deliver inputs on time

– loss of flexibility and possible increase in risk

– inability to benefit from high prices

Not all farmers are suitable for

contracts

Despite efforts to develop “inclusive” value chains, farmers must have capacity to meet market requirements in terms of:

• agronomic suitability, climate, pests and diseases

• location, input supply and infrastructure

• assets and access to finance (e.g. to pay labourers)

• capacity to meet market requirements

• land area

• social structure and education levels

• a certain willingness to take risk

Obligations of farmers

• To follow recommended production practices

and schedules

• To utilise inputs supplied under the contract for

intended purposes

• To sell all products produced under contract to

the company unless otherwise permitted

• To repay loans

• Not to deliver to the company produce not

produced under the contract

Gender and other social problems

• social structures and gender relations might be disrupted

– land used by women for food crops is allocated by men for contract production

– contracts in man’s name, men attend training courses but women do the work

– payment to men, who spend the money unwisely

– social obligations (e.g. funerals and religious observations) can conflict with contractual obligations

– contracting farmers may encounter jealousy from those without contracts

Developing modern value chains for rice through contracts could permit

• Introduction of new varieties to an area

• Strict technical supervision

• Closer collaboration between farmers and buyers

• Certification

• Traceability

• Approved input supply

• Farmer organization

• Finance support for mechanization

However, this requires TRUST!

Developing mutual trust in value chains

• Transparency – maximizing communication (e.g.

through exchange visits)

• Clear transparency in grading and pricing

• Timely delivery of inputs and price transparency

• Timely payments

• Arbitration procedures

43

Developing mutual trust in value

chains (2)

• Working through groups or

through farmer leaders

• “On-the-ground” presence of

extension workers

• Planning for possible

problems right from the

beginning

• Contract flexibility

• Contract language that is

easily understood

44

“Modern” value chains in the rice sector in Asia are not easy to find

• Possible reasons: – Rice is mainly a “commodity” that can be traded without

meeting exacting quality requirements

– For standard types of rice there are multiple buyers so market guarantees provided by contracts are not required

– With many buyers, side-selling (pole vaulting) is easy

– Farmers find quality standards difficult to meet

• However, there are a few examples of modern rice chains and the number is likely to increase

• Alternative models also emerging, particularly marketing contracts

Enhancing Milled Rice Production in Lao PDR (EMRIP)

• Project provided training to mills and mills received support for improvements

• Millers organized and paid for extension to farmer groups with intention of buying high- quality paddy from farmer.

• Main lessons: – Flexible pricing arrangements were preferred – Farmers needed to be sure of alternative outlets – Side selling an issue unless strong relationships are

built – Rules and regulations achieve little

Lao Arrowny Corporation - Laos

• joint venture between Lao and Japanese investors in Vientiane province

• koshihikari rice was marketed as “bio-organic” rice as some fertilizers permitted

• 2004 study concluded that contract farming had been beneficial to farmers involved

• no in-house processing capacity and high transport costs to have paddy processed in Thailand for export to Japan.

• 2009 flooding in Laos made production difficult and farmers unable to repay credit

• political turmoil in Thailand increased milling problems

Rice seed production for PT Pertani Indonesia

• smallholders provided with free foundation seed and extension advice

• must deliver at least 75% of production to PT Pertani and remaining 25% only for own use

• four extension visits per farmer.

• 15% of crop rejected on visual inspection prior to harvest but could be sold for consumption purposes

• company does drying of paddy

• price paid about 50% of market price but accepted by farmers given other benefits provided by the company

SL Agritech, Philippines

• Company has contract farming arrangements for hybrid seed. Claims to be largest hybrid seed company in Asia

• Also does contract growing for its brand, “Dona Maria Premium Quality Rice”, with hybrid seeds provided on credit

• Expansion planned in Visayas and Mindanao to meet needs of rapidly growing urban areas.

• Yields of over 14t per hectare have been achieved

AKR Cambodia

• Contracted with farmers to grow aromatic variety

• At one time 87,000 participating farmers, working through farmer associations.

• Company provide seed, with farmers supplying mill with the same quantity of paddy at harvest

• Associations monitor production progress and providing technical advice.

• Tendency for farmers to move out of the contract as they became more experienced

AMRU Cambodia

• Around 2,000 farmers to produce organic rice, increasing to 10,000

• Supported by French-funded project

• Contracts implemented through agricultural cooperatives

• Contract development and negotiation involves MAFF

• No financial support or input supply to farmers

• Company provides technical support and training, transport for the paddy, and bags, which are marked to ensure identification of the producer.

Elsewhere • Thailand. Production of “Japanese rice”

– Several mills involved, using variety of contractual terms and conditions

– Seed shortage a problem – Mill liquidity also a problem

• Myanmar. Rice Leading Companies (RLCs) – Provide inputs on credit as well as technical support – Aim to improve quality and link with exporters – Liquidity has been a problem

• Vietnam. e.g. An Giang Plant Protection Joint Stock Company (AGPPS) – Input supply, private extension service, storage to await price

rises – An Giang’s model has encouraged replication by other

companies