Embed Size (px)

Citation preview

INDUSTRY SYNOPSIS

SIC 6037 – State and Federal Savings Institutions

TABLE OF CONTENTS 1. SCOPE OF SYNOPSIS

A. Industry Definition Page 3 B. Contextual Overview Page 5

2. INDUSTRY OVERVIEW

A. Number of Establishments and Companies Page 7 B. Size and Type of Production by- Size Page 7 C. Concentration and Major Service Providers Page 12 D. Stability of the Industry Page 13 E. Geographic Dispersion Page 15 F. Sample Information Page 15 G. Value of Shipments Per Employee Information Page 15

3. PRODUCT INFORMATION

A. Service Delivery Process Page 16 B. Major Service Lines and Value of Receipts Page 16 C. Price Determining Characteristics Page 16 D. Custom Services Page 17 E. Seasonality Page 18 F. Service Substitution Page 18

4. MARKET AND TRANSACTION INFORMATION

A. Interplant and Intraindustry Payments Page 18 B. Price Behavior Page 18 C. Unit of Measure D. Types of Prices Page 19 E. Types of Buyers Page 22 F. Discounts Page 23 G. Additional Charges Page 24 H. Size of Purchase Page 24 I. Contracts Page 25 J. Other Variables Affecting Prices Page 25

5. INDUSTRY INFORMATION AND RELATIONS

A. Industry Relations Page 25 B. Currently Available Price Data Page 26

1

C. Litigation and Other Cooperation Problems Page 26 D. Service Identification Problems Page 26 E. Checklist Clarifications Page 27 F. Industry Specific Questions and Procedures Page 27 G. Presurvey and Pretest Contacts Page 33

6. PUBLICATION GOALS Page 34

2

1. SCOPE OF SYNOPSIS

A. INDUSTRY DEFINITION

Savings Institutions, Federally Chartered (SIC 6035) and Savings Institutions, Not Federally Chartered (SIC 6036) are being collected together as SIC 6037 Savings Institutions. Under the 1987 SIC definition, Savings Institutions can be defined as financial intermediaries that primarily engage in accepting time deposits, making mortgage and real estate loans, and investing in high-grade securities. Savings Institutions, Federally Chartered operate under a federal charter, while Savings Institutions, Not Federally Chartered operate under a state charter. SIC 603 SAVINGS INSTITUTIONS SIC 6035 Savings Institutions, Federally Chartered Federal savings and loan associations Savings banks, Federal Savings and loan associations, federally chartered

SIC 6036 Savings Institutions, Not Federally Chartered Savings and loans associations, not federally chartered Savings banks, State: not federally chartered The 1997 North American Industrial Classification System has the same definition as the 1987 Standard Industrial Classification manual, but it does not contrast federally and state-chartered institutions.

Output The primary output of savings institutions (SIC 6037) is financial intermediation. That is, savings institutions—also known as thrifts—function to gather and allocate funds in the economy. Financial intermediaries such as thrifts transform financial claims in ways that make them more attractive to the ultimate investor. Thrifts purchase direct claims (IOUs) with one set of characteristics (e.g., term to maturity) from a deficit spending unit (DSU) and transform them into indirect claims (IOUs) with a different set of characteristics, which they then sell to a surplus spending unit (SSU). This transformation process is called intermediation. Therefore, households (SSUs) deposit excess cash balances in deposit accounts of a thrift, which in turn makes loans to households and businesses (DSUs). Output/Financial Intermediation Services Indirectly Measured (FISM) Banks are able to provide services for which they do not charge explicitly by paying or charging different rates of interest to borrowers and lenders. They pay lower rates of interest than would otherwise be the case to those who lend them money and charge higher rates of interest to those who borrow from them. The resulting net revenues of interest are used to defray their expenses and provide an operating surplus. This scheme of interest rates avoids the need to charge their customers individually for services provided and leads to the pattern of interest rates observed in practice. Therefore, these unpriced services are referred to as financial intermediation services indirectly measured. Interest is only indirectly relevant to measuring unpriced services.

3

Due to FISIM there is difficulty in allocating the interest earned on loans between the two outputs, loans and deposits. Deposits, besides being inputs (since without deposits banks could not make loans), are also considered outputs since they provide surplus spending units (depositors) services such as record-keeping, safekeeping, and insurance. Therefore, a reference rate methodology is used to allocate the interest between loans and deposits. The reference rate to be used represents the pure cost of borrowing funds- that is, a rate from which the risk premium has been eliminated to the greatest extent possible and which does not include any intermediation services. Reference rates and how they will be used to price the output of the industry will be explained in detail in Price Determining Characteristics, Checklist Clarifications and Industry Specific Questions and Procedures sections of this synopsis. SIC 6037 consists of the following banking services:

Loans Residential Real Estate (Residential mortgages) Nonresidential Real Estate Commercial and Industrial Loans (except real estate) Consumer Loans Deposits Demand Savings Time Deposits Fee Based Services: Loan Servicing Fees Service Charges on Deposit Accounts Other Fees and Commissions Industry Exclusions

SIC 602 Commercial Banks --Institutions that engage in accepting deposits from the public for commercial, consumer, and mortgage loans, and US government securities and municipal bonds. SIC 6021 National Commercial Banks Commercial banks, National National Trust companies (accepting deposits) SIC 6022 State Commercial banks Commercial Banks, State Trust companies (accepting deposits) SIC 606 Credit Unions

4

--Cooperative thrift and loan associations (accepting deposits) organized for a particular group, such as union members, employees of a particular firm, and so forth. -- SIC 6061 Credit Unions, Federally Chartered -- SIC 6062 Credit Unions, Not Federally Charted SIC 608 Foreign Banking Branches and Agencies of Foreign Banks SIC 6081 Branches and Agencies of Foreign Banks --Establishments operating as branches or agencies of foreign banks that specialize in commercial loans, especially in trade finance. --Agencies of foreign banks --Branches of foreign banks SIC 6082 Foreign Trade and International Banking Institutions --Establishments of foreign trade companies operating in the United States under Federal or State charter for the purpose of aiding or financing foreign trade. Also included in this industry are Federal and State chartered banking institutions that only participate in banking outside of the United States. --Agreement Corporations

--Edge Act Corporations The following non-depository SICs should not be confused with SIC 6037. SIC 6111 Federal and Federally Sponsored Credit Agencies --Establishments of the Federal Government and federally sponsored credit agencies primarily engaged in guaranteeing, insuring, or making loans. SIC 6141 Personal Credit Institutions --Establishments primarily engaged in providing loans to individuals. SIC 6162 Mortgage Bankers and Loan Correspondents --Establishments primarily engaged in originating mortgage loans, selling mortgage loans to permanent investors, and servicing these loans. They may also provide real estate construction loans. SIC 6163 Loan Brokers --Establishments primarily engaged in arranging loans for others and operate mostly on a commission or fee basis.

B. CONTEXTUAL OVERVIEW

According to Standard and Poor’s, the thrift industry is the nation’s fourth-largest group of financial institutions in terms of assets, after commercial banks, mutual funds, and insurance companies. As of January 30, 1998, there are 1,179 savings and loan associations, and 549 savings banks in the United States. In that same year S&Ls held total assets of approximately $787 billion, compared to $258 billion held by savings banks. Savings institutions thus total about $1 trillion dollars in total assets.

5

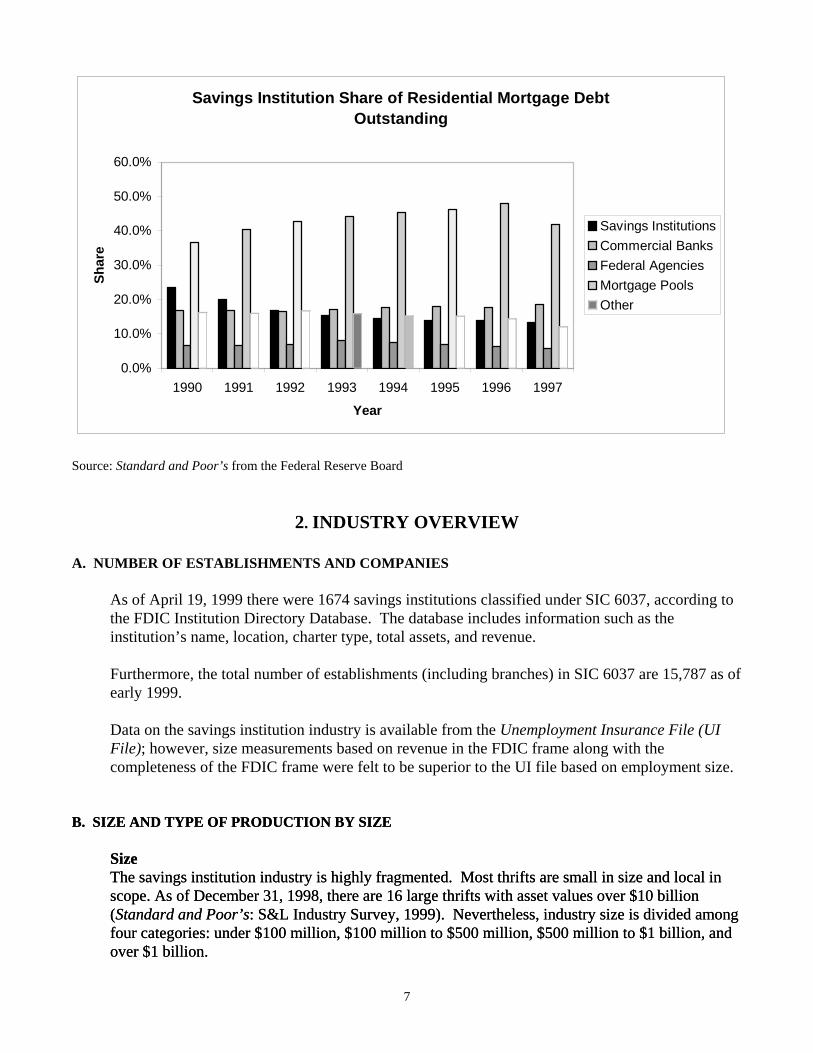

Historically, savings institutions were created to serve the banking needs of consumers who needed to borrow or deposit small amounts of money. Commercial banks did not meet the needs for long-term credit because their main focus was on short-term, primarily self-liquidating, commercial loans. Therefore, savings institutions targeted the needs of savers who had small amounts of funds to deposit and wanted to earn a respectable rate of interest on their deposits, while also providing long-term credit such as home mortgages. Today, all thrifts depend on savings and other types of deposits that appeal to thrifty consumers (Kidwell et al, 529). However, the thrift industry has faced significant changes since their beginnings in the early 1800s, and especially since the savings and loan crisis of the early 1980s. Mergers and acquisitions (M&As) continue to shrink the number of institutions, and severely troubled thrifts have closed altogether due to market share erosion by commercial banks and credit unions, a disappearing deposit base, and interest rate risk. According to Barbara Spain of Hoover’s Online, savings institutions numbered 3,600 in 1987. Today, about 1,693 thrifts exist. The numbers have dwindled because of insolvency or huge mergers and acquisitions (M&As), such as Washington Mutual and HF Ahmanson. This acquisition in 1998 created the largest savings institution in the nation, with assets of $158.5 billion. (Standard and Poor’s: S&L Industry Survey, 1999). Although M&As affect the size and efficiency of the savings industry, the bread and butter of savings institutions is its ability to profitably hold a deposit base (public savings deposit--often called shares--and time and checkable deposits). Savings institutions use these funds to offer loans and services. S&Ls, for example, can pay customers 3% to 5% interest on savings deposits (liabilities), and in turn charge 8% to 12% on home mortgage loans (assets). This spread (assets minus liabilities) can give a sizable profit for savings institutions. However, during the past decade and a half, the savings institutions’ deposit base has significantly decreased. Investors and the general population have invested their disposable income into money market mutual funds and individual retirement accounts (IRAs) instead of the traditional savings and checking accounts. According to Frederic Mishkin, Professor of Economics at Columbia University, “In 1977, money market mutual funds had assets under $4 billion. Currently they hold around $900 billion. The general public has become more sophisticated and knowledgeable in investments, and thus seeks higher yields than passbook savings.”(Mishkin, 285) Therefore, savings institutions and banks now struggle to compete for depository public funds: they have begun offering higher rates for liabilities while charging lower rates on assets. As a result, savings institutions have gained smaller spreads. Furthermore, as an example of increased pressure on competition and profitability, the following table and graph demonstrate the savings institutions’ share of mortgage debt outstanding between 1990 and 1997. In 1990, savings institutions held 23.6% of residential mortgage outstanding. Due to M&As, a disappearing deposit base and financial innovation, ten years later the savings institutions’ share of residential mortgages dropped over ten percentage points to 13.3%, while commercial banks’ share increased from 16.8% to 18.6% during the same period.

6

Savings Institution Share of Residential Mortgage Debt Outstanding

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

1990 1991 1992 1993 1994 1995 1996 1997

Year

Shar

e

Savings InstitutionsCommercial BanksFederal AgenciesMortgage PoolsOther

Source: Standard and Poor’s from the Federal Reserve Board

2. INDUSTRY OVERVIEW

A. NUMBER OF ESTABLISHMENTS AND COMPANIES

As of April 19, 1999 there were 1674 savings institutions classified under SIC 6037, according to the FDIC Institution Directory Database. The database includes information such as the institution’s name, location, charter type, total assets, and revenue. Furthermore, the total number of establishments (including branches) in SIC 6037 are 15,787 as of early 1999. Data on the savings institution industry is available from the Unemployment Insurance File (UI File); however, size measurements based on revenue in the FDIC frame along with the completeness of the FDIC frame were felt to be superior to the UI file based on employment size.

B. SIZE AND TYPE OF PRODUCTION BY SIZE B. SIZE AND TYPE OF PRODUCTION BY SIZE

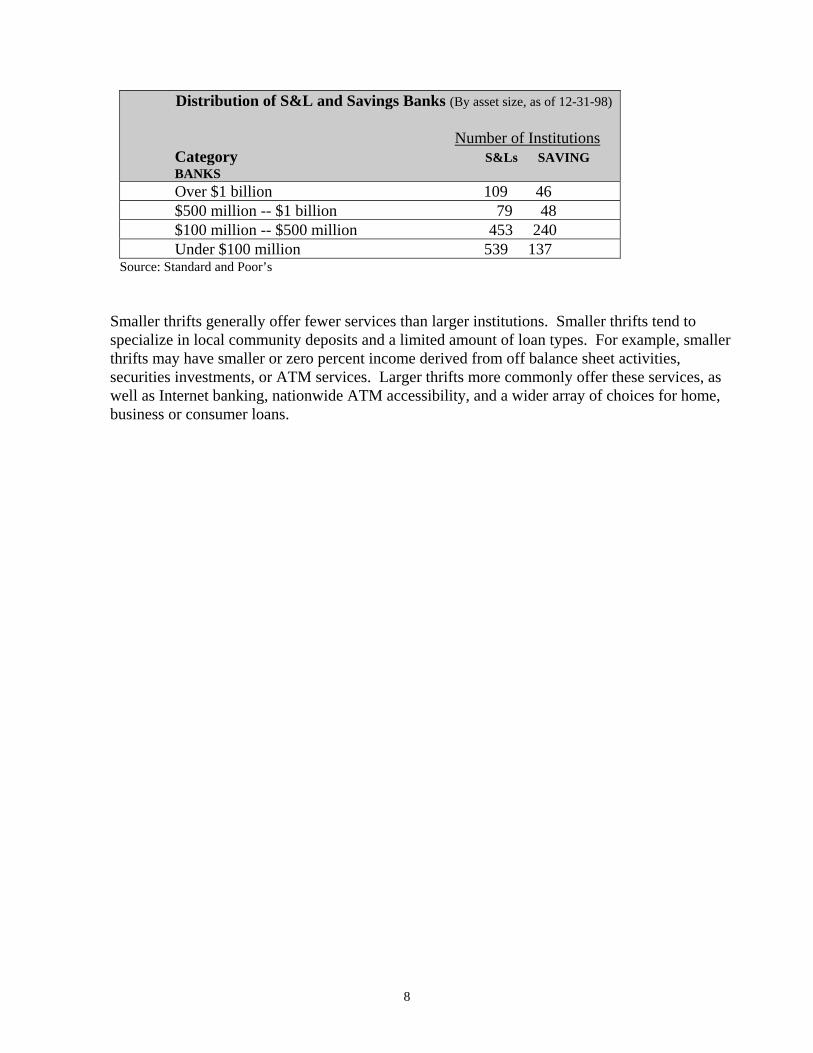

Size Size The savings institution industry is highly fragmented. Most thrifts are small in size and local in scope. As of December 31, 1998, there are 16 large thrifts with asset values over $10 billion (Standard and Poor’s: S&L Industry Survey, 1999). Nevertheless, industry size is divided among four categories: under $100 million, $100 million to $500 million, $500 million to $1 billion, and over $1 billion.

The savings institution industry is highly fragmented. Most thrifts are small in size and local in scope. As of December 31, 1998, there are 16 large thrifts with asset values over $10 billion (Standard and Poor’s: S&L Industry Survey, 1999). Nevertheless, industry size is divided among four categories: under $100 million, $100 million to $500 million, $500 million to $1 billion, and over $1 billion.

7

Distribution of S&L and Savings Banks (By asset size, as of 12-31-98)

Number of Institutions Category S&Ls SAVING BANKS Over $1 billion 109 46 $500 million -- $1 billion 79 48 $100 million -- $500 million 453 240 Under $100 million 539 137

Source: Standard and Poor’s

Smaller thrifts generally offer fewer services than larger institutions. Smaller thrifts tend to specialize in local community deposits and a limited amount of loan types. For example, smaller thrifts may have smaller or zero percent income derived from off balance sheet activities, securities investments, or ATM services. Larger thrifts more commonly offer these services, as well as Internet banking, nationwide ATM accessibility, and a wider array of choices for home, business or consumer loans.

8

C. CONCENTRATION AND MAJOR SERVICE PROVIDERS

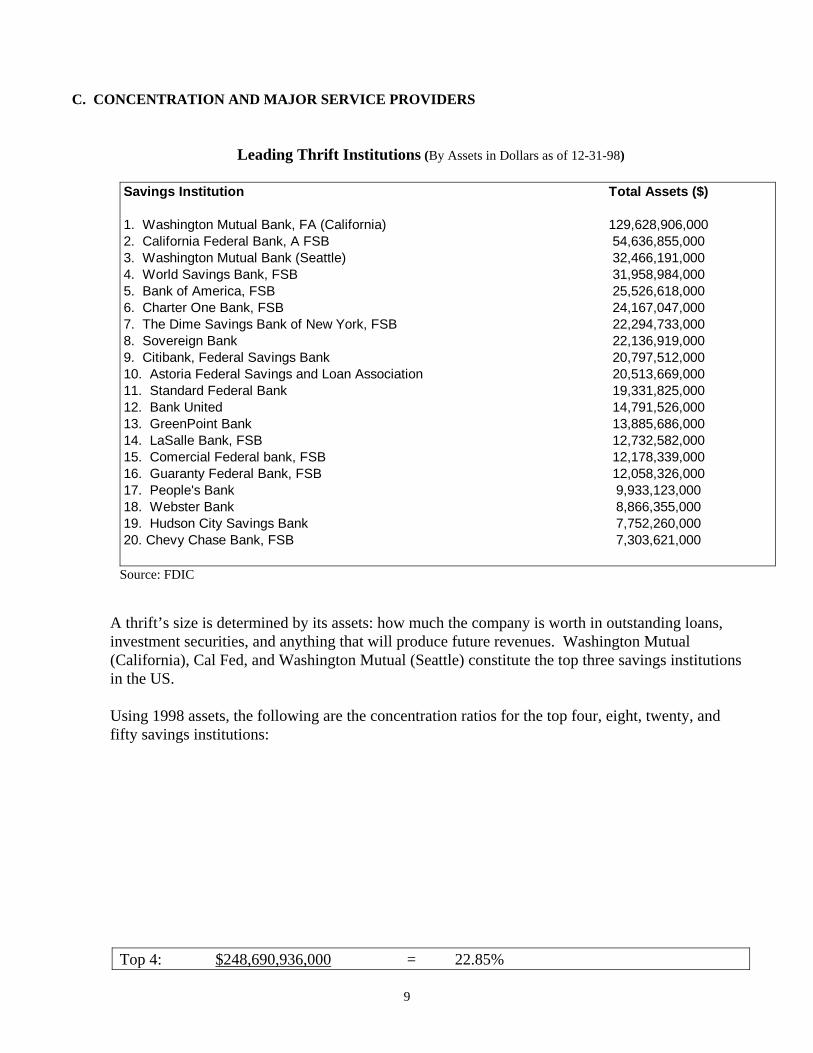

Leading Thrift Institutions (By Assets in Dollars as of 12-31-98) Savings Institution Total Assets ($)

1. Washington Mutual Bank, FA (California) 129,628,906,0002. California Federal Bank, A FSB 54,636,855,0003. Washington Mutual Bank (Seattle) 32,466,191,0004. World Savings Bank, FSB 31,958,984,0005. Bank of America, FSB 25,526,618,0006. Charter One Bank, FSB 24,167,047,0007. The Dime Savings Bank of New York, FSB 22,294,733,0008. Sovereign Bank 22,136,919,0009. Citibank, Federal Savings Bank 20,797,512,00010. Astoria Federal Savings and Loan Association 20,513,669,00011. Standard Federal Bank 19,331,825,00012. Bank United 14,791,526,00013. GreenPoint Bank 13,885,686,00014. LaSalle Bank, FSB 12,732,582,00015. Comercial Federal bank, FSB 12,178,339,00016. Guaranty Federal Bank, FSB 12,058,326,00017. People's Bank 9,933,123,00018. Webster Bank 8,866,355,00019. Hudson City Savings Bank 7,752,260,00020. Chevy Chase Bank, FSB 7,303,621,000

Source: FDIC

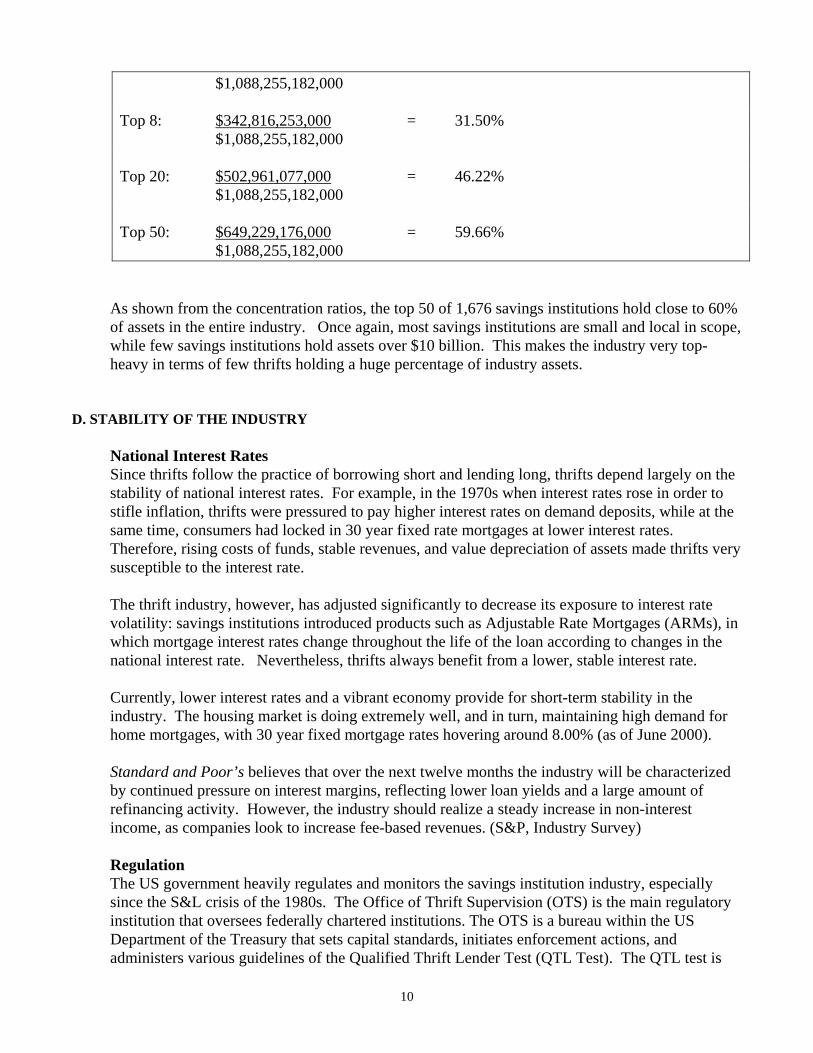

A thrift’s size is determined by its assets: how much the company is worth in outstanding loans, investment securities, and anything that will produce future revenues. Washington Mutual (California), Cal Fed, and Washington Mutual (Seattle) constitute the top three savings institutions in the US. Using 1998 assets, the following are the concentration ratios for the top four, eight, twenty, and fifty savings institutions:

Top 4: $248,690,936,000 = 22.85%

9

$1,088,255,182,000 Top 8: $342,816,253,000 = 31.50% $1,088,255,182,000 Top 20: $502,961,077,000 = 46.22% $1,088,255,182,000 Top 50: $649,229,176,000 = 59.66% $1,088,255,182,000

As shown from the concentration ratios, the top 50 of 1,676 savings institutions hold close to 60% of assets in the entire industry. Once again, most savings institutions are small and local in scope, while few savings institutions hold assets over $10 billion. This makes the industry very top-heavy in terms of few thrifts holding a huge percentage of industry assets.

D. STABILITY OF THE INDUSTRY National Interest Rates Since thrifts follow the practice of borrowing short and lending long, thrifts depend largely on the stability of national interest rates. For example, in the 1970s when interest rates rose in order to stifle inflation, thrifts were pressured to pay higher interest rates on demand deposits, while at the same time, consumers had locked in 30 year fixed rate mortgages at lower interest rates. Therefore, rising costs of funds, stable revenues, and value depreciation of assets made thrifts very susceptible to the interest rate. The thrift industry, however, has adjusted significantly to decrease its exposure to interest rate volatility: savings institutions introduced products such as Adjustable Rate Mortgages (ARMs), in which mortgage interest rates change throughout the life of the loan according to changes in the national interest rate. Nevertheless, thrifts always benefit from a lower, stable interest rate. Currently, lower interest rates and a vibrant economy provide for short-term stability in the industry. The housing market is doing extremely well, and in turn, maintaining high demand for home mortgages, with 30 year fixed mortgage rates hovering around 8.00% (as of June 2000). Standard and Poor’s believes that over the next twelve months the industry will be characterized by continued pressure on interest margins, reflecting lower loan yields and a large amount of refinancing activity. However, the industry should realize a steady increase in non-interest income, as companies look to increase fee-based revenues. (S&P, Industry Survey) Regulation The US government heavily regulates and monitors the savings institution industry, especially since the S&L crisis of the 1980s. The Office of Thrift Supervision (OTS) is the main regulatory institution that oversees federally chartered institutions. The OTS is a bureau within the US Department of the Treasury that sets capital standards, initiates enforcement actions, and administers various guidelines of the Qualified Thrift Lender Test (QTL Test). The QTL test is

10

designed to ensure that a savings institution maintain 65% of their assets in housing-related investments, on a monthly basis, for nine out of twelve months. (S&P) State savings institutions could either choose to be regulated by the OTS or by state bank commissioners. State banks not regulated by the OTS tend to be more commercial bank-like, since they have more lenient regulations in the services they can provide.

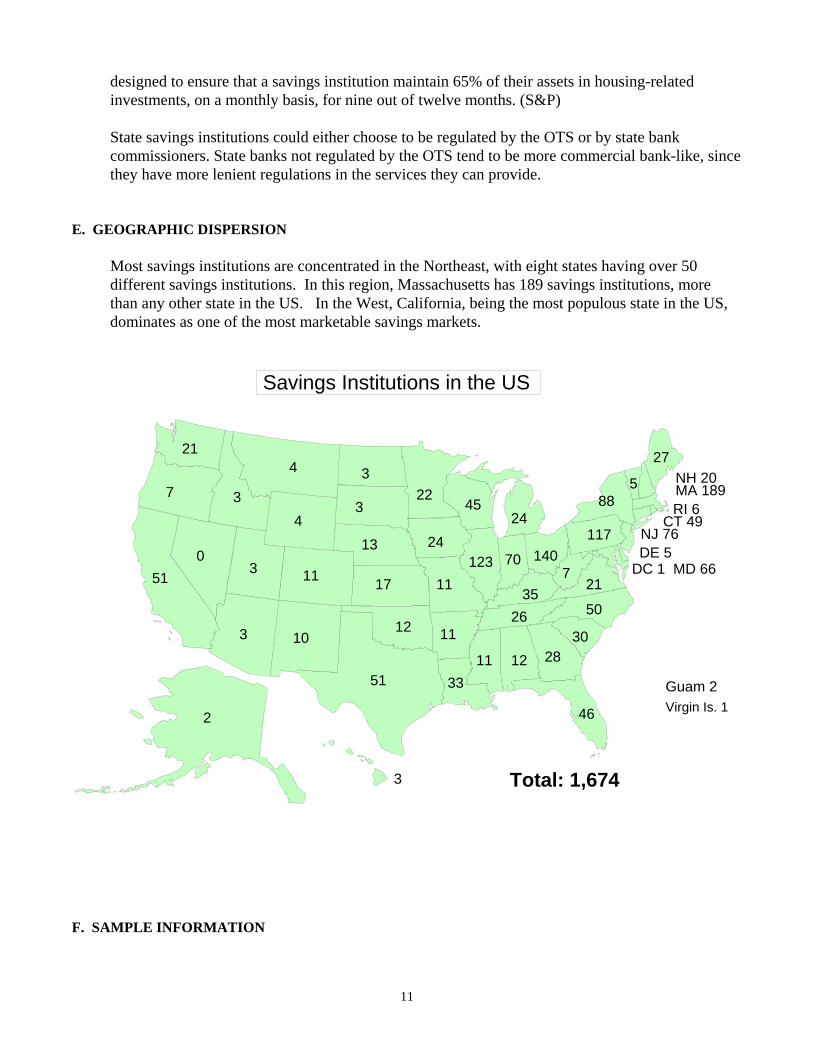

E. GEOGRAPHIC DISPERSION

Most savings institutions are concentrated in the Northeast, with eight states having over 50 different savings institutions. In this region, Massachusetts has 189 savings institutions, more than any other state in the US. In the West, California, being the most populous state in the US, dominates as one of the most marketable savings markets.

0

51

DC 1 MD 66DE 5NJ 76

CT 49RI 6

NH 20MA 189

Virgin Is. 1Guam 2

2

3

21

7

51

3

3

3

4

4

11

1012

17

13

3

322

24

11

11

33

5

27

88

11724

45

123 70 140

2635

721

50

3011 12 28

46

Total: 1,674

Savings Institutions in the US

F. SAMPLE INFORMATION

11

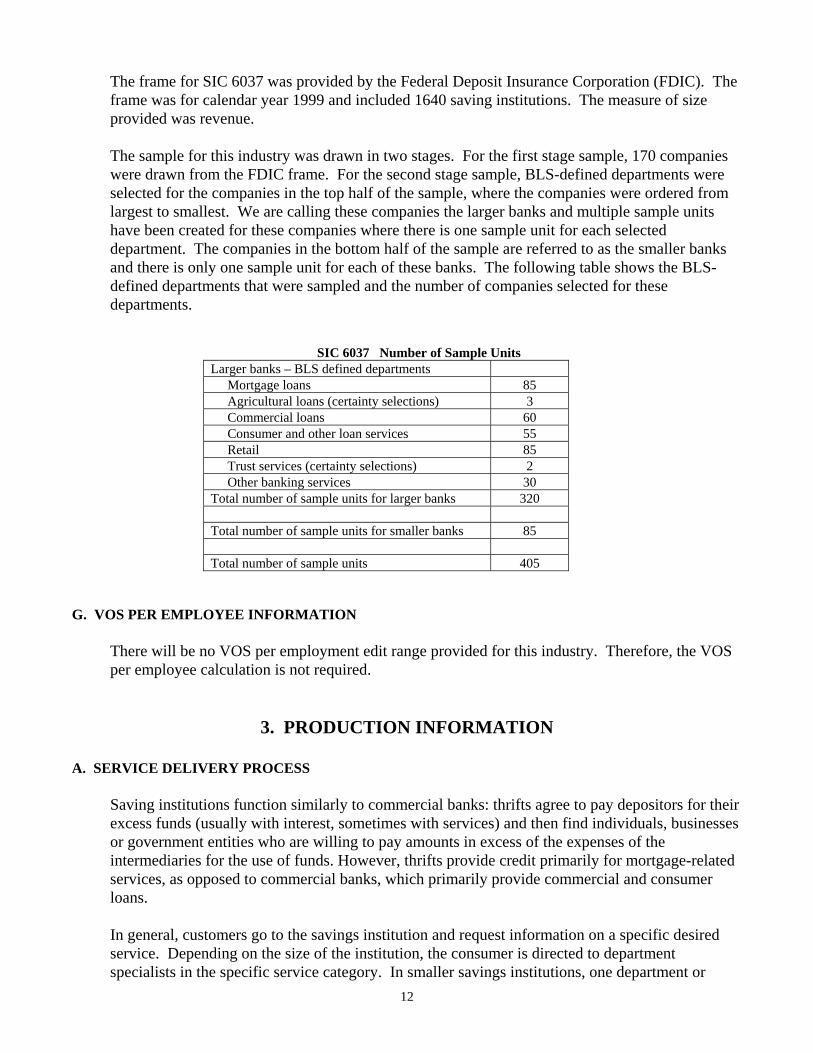

The frame for SIC 6037 was provided by the Federal Deposit Insurance Corporation (FDIC). The frame was for calendar year 1999 and included 1640 saving institutions. The measure of size provided was revenue. The sample for this industry was drawn in two stages. For the first stage sample, 170 companies were drawn from the FDIC frame. For the second stage sample, BLS-defined departments were selected for the companies in the top half of the sample, where the companies were ordered from largest to smallest. We are calling these companies the larger banks and multiple sample units have been created for these companies where there is one sample unit for each selected department. The companies in the bottom half of the sample are referred to as the smaller banks and there is only one sample unit for each of these banks. The following table shows the BLS-defined departments that were sampled and the number of companies selected for these departments.

SIC 6037 Number of Sample Units Larger banks – BLS defined departments Mortgage loans 85 Agricultural loans (certainty selections) 3 Commercial loans 60 Consumer and other loan services 55 Retail 85 Trust services (certainty selections) 2 Other banking services 30 Total number of sample units for larger banks 320 Total number of sample units for smaller banks 85 Total number of sample units 405

G. VOS PER EMPLOYEE INFORMATION

There will be no VOS per employment edit range provided for this industry. Therefore, the VOS per employee calculation is not required.

3. PRODUCTION INFORMATION

A. SERVICE DELIVERY PROCESS Saving institutions function similarly to commercial banks: thrifts agree to pay depositors for their excess funds (usually with interest, sometimes with services) and then find individuals, businesses or government entities who are willing to pay amounts in excess of the expenses of the intermediaries for the use of funds. However, thrifts provide credit primarily for mortgage-related services, as opposed to commercial banks, which primarily provide commercial and consumer loans. In general, customers go to the savings institution and request information on a specific desired service. Depending on the size of the institution, the consumer is directed to department specialists in the specific service category. In smaller savings institutions, one department or

12

branch may handle most services. If a customer seeks a loan, the customer fills out an application form which will detail his or her credit history, he or she pays an application fee (if applicable), and upon approval, receives thrift loan services at certain prices or interest rates. If the customer seeks retail-banking services, the customer speaks with a retail-banking representative to open an account. Customers may also seek to buy securities, commodities, or insurance. Thrifts offer these products only through their affiliates. Affiliates may include thrift holding companies, subsidiaries, or independent service companies. These services are currently out of scope for SIC 603. There are several methods thrifts earn revenue from fostering affiliate business. Affiliates may either A) pay the thrift under conditions of contract for business referral; B) make monthly lease payments for office space on thrift premises; or C) pay thrifts by method of dividend earnings. However, fees and commissions earned from insurance and commodity sales, as a percentage of revenue, is very small compared to other service lines--approximately less than one percent of total industry assets in 1992. (Census Sources of Revenue, 1992) With the advent of information technology, thrifts have begun to offer services and loans over the Internet. Current news articles have reported an increase in web-based mortgage loan applications and online banking. This trend should continue long-term, and should become a viable new service for savings institutions.

B. MAJOR SERVICE LINES AND VALUE OF RECEIPTS

Type of Production According to the Bureau of the Census, savings institutions derive revenue from: Interest income: residential real estate loans, nonresidential real estate loans, commercial and industrial loans (except real estate), credit cards, overdraft credit and related plans, other loans to individuals, lease financing receivables, new and used auto loans, home equity loans, and miscellaneous revenue. This revenue captures the earnings for own-loan servicing. See Loan Servicing. Loan Servicing: This type of loan servicing is different from the revenue earned when thrifts receive income from servicing their own loans. When thrifts pool loans together and sell them to third parties, thrifts may choose to continue to service the loans, such as handling loan payments, correspondence, and other services, while the third party collects interest payments. Loan origination fees: Residential real estate loans, nonresidential real estate loans, and other loans. Other fees and commissions: Loan (and line of credit) servicing fees collected after placement; underwriting fee income; commissions and fees from securities and commodities sales; commissions and fees from insurance sales; other fees and commissions (including ATM charges, etc.); service charges on deposit accounts; income from fiduciary (trust) activities; leasing revenue (except from finance and capital leases); and other revenue.

13

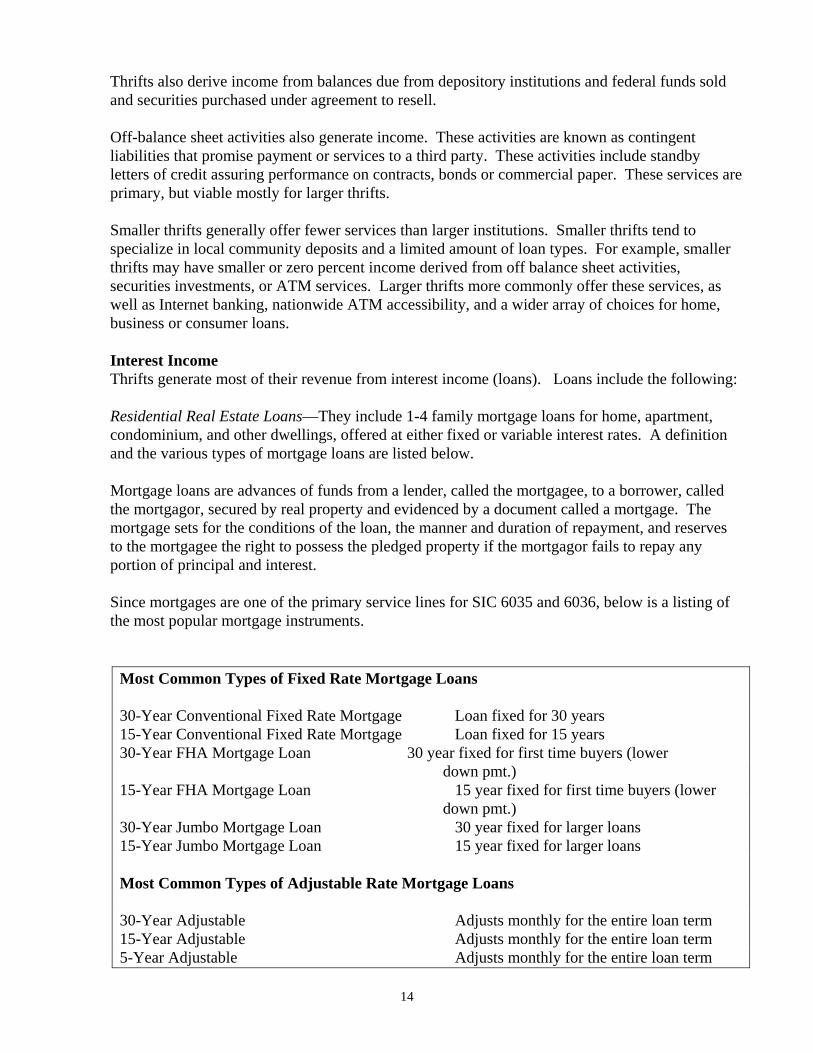

Thrifts also derive income from balances due from depository institutions and federal funds sold and securities purchased under agreement to resell. Off-balance sheet activities also generate income. These activities are known as contingent liabilities that promise payment or services to a third party. These activities include standby letters of credit assuring performance on contracts, bonds or commercial paper. These services are primary, but viable mostly for larger thrifts. Smaller thrifts generally offer fewer services than larger institutions. Smaller thrifts tend to specialize in local community deposits and a limited amount of loan types. For example, smaller thrifts may have smaller or zero percent income derived from off balance sheet activities, securities investments, or ATM services. Larger thrifts more commonly offer these services, as well as Internet banking, nationwide ATM accessibility, and a wider array of choices for home, business or consumer loans. Interest Income Thrifts generate most of their revenue from interest income (loans). Loans include the following:

Residential Real Estate Loans—They include 1-4 family mortgage loans for home, apartment, condominium, and other dwellings, offered at either fixed or variable interest rates. A definition and the various types of mortgage loans are listed below. Mortgage loans are advances of funds from a lender, called the mortgagee, to a borrower, called the mortgagor, secured by real property and evidenced by a document called a mortgage. The mortgage sets for the conditions of the loan, the manner and duration of repayment, and reserves to the mortgagee the right to possess the pledged property if the mortgagor fails to repay any portion of principal and interest. Since mortgages are one of the primary service lines for SIC 6035 and 6036, below is a listing of the most popular mortgage instruments.

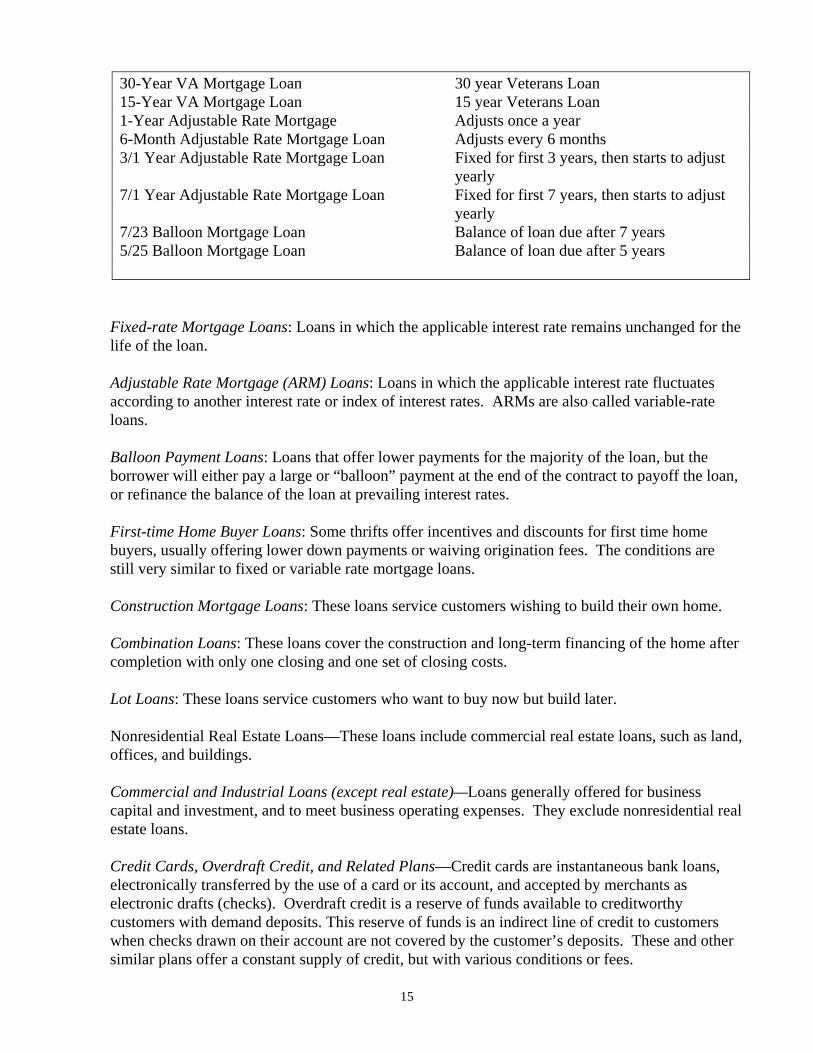

Most Common Types of Fixed Rate Mortgage Loans 30-Year Conventional Fixed Rate Mortgage Loan fixed for 30 years 15-Year Conventional Fixed Rate Mortgage Loan fixed for 15 years 30-Year FHA Mortgage Loan 30 year fixed for first time buyers (lower down pmt.) 15-Year FHA Mortgage Loan 15 year fixed for first time buyers (lower down pmt.) 30-Year Jumbo Mortgage Loan 30 year fixed for larger loans 15-Year Jumbo Mortgage Loan 15 year fixed for larger loans Most Common Types of Adjustable Rate Mortgage Loans 30-Year Adjustable Adjusts monthly for the entire loan term 15-Year Adjustable Adjusts monthly for the entire loan term 5-Year Adjustable Adjusts monthly for the entire loan term

14

30-Year VA Mortgage Loan 30 year Veterans Loan 15-Year VA Mortgage Loan 15 year Veterans Loan 1-Year Adjustable Rate Mortgage Adjusts once a year 6-Month Adjustable Rate Mortgage Loan Adjusts every 6 months 3/1 Year Adjustable Rate Mortgage Loan Fixed for first 3 years, then starts to adjust yearly 7/1 Year Adjustable Rate Mortgage Loan Fixed for first 7 years, then starts to adjust yearly 7/23 Balloon Mortgage Loan Balance of loan due after 7 years 5/25 Balloon Mortgage Loan Balance of loan due after 5 years

Fixed-rate Mortgage Loans: Loans in which the applicable interest rate remains unchanged for the life of the loan. Adjustable Rate Mortgage (ARM) Loans: Loans in which the applicable interest rate fluctuates according to another interest rate or index of interest rates. ARMs are also called variable-rate loans. Balloon Payment Loans: Loans that offer lower payments for the majority of the loan, but the borrower will either pay a large or “balloon” payment at the end of the contract to payoff the loan, or refinance the balance of the loan at prevailing interest rates. First-time Home Buyer Loans: Some thrifts offer incentives and discounts for first time home buyers, usually offering lower down payments or waiving origination fees. The conditions are still very similar to fixed or variable rate mortgage loans. Construction Mortgage Loans: These loans service customers wishing to build their own home. Combination Loans: These loans cover the construction and long-term financing of the home after completion with only one closing and one set of closing costs. Lot Loans: These loans service customers who want to buy now but build later. Nonresidential Real Estate Loans—These loans include commercial real estate loans, such as land, offices, and buildings. Commercial and Industrial Loans (except real estate)—Loans generally offered for business capital and investment, and to meet business operating expenses. They exclude nonresidential real estate loans. Credit Cards, Overdraft Credit, and Related Plans—Credit cards are instantaneous bank loans, electronically transferred by the use of a card or its account, and accepted by merchants as electronic drafts (checks). Overdraft credit is a reserve of funds available to creditworthy customers with demand deposits. This reserve of funds is an indirect line of credit to customers when checks drawn on their account are not covered by the customer’s deposits. These and other similar plans offer a constant supply of credit, but with various conditions or fees.

15

Other Loans to Individuals—College loans and other personal borrowings, secured or unsecured, fall under this category. These loans may include the following: personal loans, such as passbook and certificate loans (loans that are secured by savings accounts and certificates of deposits), collateral loans, and installment loans-- such as home improvements or repairs, education, travel, emergencies, and any worthwhile purpose. New and Used Auto Loans—Auto loans are offered to individuals or companies for the purchasing or financing of vehicles. Home Equity Loans-- Home equity loans are loans given to consumers for multiple purposes, such as debt consolidation and home improvements, and are backed by the equity or value of the home. Home equity loans can also be a source of revolving lines of credit.

Fee based services Loan Origination Fees: Thrifts receive revenue from originating and administering the loan process. Revenue from this service originates from residential real estate loans, non-residential real estate loans, and other loans. Closing costs such as discount points, title insurance, escrow fees, attorney fees, recording fees, appraisal fees, notary fees, and so forth, are included in this fee based services category. Interest income is excluded. Other Fees and Commissions: This category includes loan and line of service fees collected after placement, underwriting fee income, commissions and fees from securities and commodity sales, commissions and fees from insurance sales, other fees and commissions and miscellaneous fee revenue. Retail Banking Fees: Service charges on deposit accounts, such as checking account maintenance fees, overdraft fees, and ATM charges. Miscellaneous services rendered in this industry include, broker-dealer services, transfer agent services, accounting/administrative services, and insurance brokerage services. As part of a bundle, fee-based loan service charges attach to loan contracts. For example, when a customer purchases a mortgage, the customer must also pay closing costs, origination fees, and loan service fees. Deposit Accounts The principal source of funds for most thrifts is deposit accounts -demand, savings, and time deposits. Individuals may now choose from among a number of deposit products, including the traditional demand deposit account on which the law prohibits payment of interest; regular savings account on which interest is paid but withdrawals are sometimes limited; Negotiable Order of Withdrawal (NOW) accounts or other negotiable withdrawal accounts upon which interest is paid and checks are drawn; various kinds of time or certificate accounts which bear interest and which mature at a specific time and on which, until maturity, withdrawals are limited or require the customer to forfeit a penalty; and Individual Retirement Account (IRA) or Keogh accounts which are designed for individual retirement purposes .

16

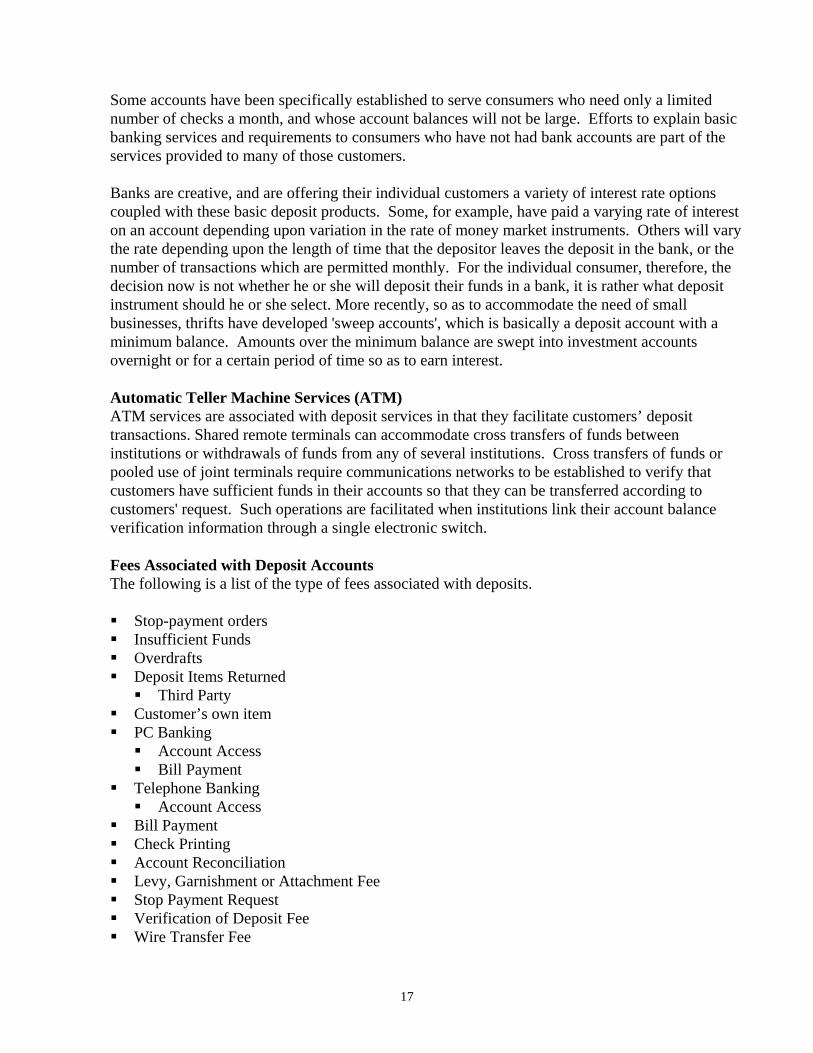

Some accounts have been specifically established to serve consumers who need only a limited number of checks a month, and whose account balances will not be large. Efforts to explain basic banking services and requirements to consumers who have not had bank accounts are part of the services provided to many of those customers. Banks are creative, and are offering their individual customers a variety of interest rate options coupled with these basic deposit products. Some, for example, have paid a varying rate of interest on an account depending upon variation in the rate of money market instruments. Others will vary the rate depending upon the length of time that the depositor leaves the deposit in the bank, or the number of transactions which are permitted monthly. For the individual consumer, therefore, the decision now is not whether he or she will deposit their funds in a bank, it is rather what deposit instrument should he or she select. More recently, so as to accommodate the need of small businesses, thrifts have developed 'sweep accounts', which is basically a deposit account with a minimum balance. Amounts over the minimum balance are swept into investment accounts overnight or for a certain period of time so as to earn interest. Automatic Teller Machine Services (ATM) ATM services are associated with deposit services in that they facilitate customers’ deposit transactions. Shared remote terminals can accommodate cross transfers of funds between institutions or withdrawals of funds from any of several institutions. Cross transfers of funds or pooled use of joint terminals require communications networks to be established to verify that customers have sufficient funds in their accounts so that they can be transferred according to customers' request. Such operations are facilitated when institutions link their account balance verification information through a single electronic switch. Fees Associated with Deposit Accounts The following is a list of the type of fees associated with deposits.

Stop-payment orders Insufficient Funds Overdrafts Deposit Items Returned

Third Party Customer’s own item PC Banking

Account Access Bill Payment

Telephone Banking Account Access

Bill Payment Check Printing Account Reconciliation Levy, Garnishment or Attachment Fee Stop Payment Request Verification of Deposit Fee Wire Transfer Fee

17

Automated Teller Machines Fees Annual Fees Card Fees Fees for Customer Transactions On Us

Withdrawal Fee Deposit Fee Balance Inquiry Fee

Fees for Customer Transactions on Others Withdrawal Fee Deposit Fee Balance Inquiry Fee

Surcharge ATM Postage Stamp Postage Fee ATM Statement Fee

C. PRICE DETERMINING CHARACTERISTICS

Loans Mortgage Loans, Nonresidential Real Estate Loans, Commercial and Industrial Loans (except real estate), and Consumer Loans: Type of loan (mortgage, commercial, consumer). Type of loan is price determining mainly

because of the collateral backing the loans or their inherent risk to the bank. For example, a residential mortgage loan is backed by the property as collateral, while some consumer loans, such as student loans, may not be backed by collateral.

Determined interest rate (i.e. 8.0%, 9.5%) Type of interest rate (variable or fixed) Maturity (length of loan amortization) Credit history of the borrower (by tier ranking) Payments (fixed, variable, periodic, on demand) Collateral Loan to value ratio

Loan Origination Fees Type of loan Types of fees and closing costs (discount points, title insurance, escrow fees, attorney fees,

recording fees, appraisal fees, notary fees, and so forth) Other Loan Fees and Commissions Type of Loan Fee (fees collected after closing mortgage loans, consumer loans, and

commercial loans) Type of service (commissions and fees from security sales, commodity sales, insurance sales,

etc.) Deposit Account Service Charges Checking, Money Market Deposit Accounts, Sweep Accounts

18

Type of Account (checking, NOW, MMDA) Minimum Balance Interest rate (if applicable) Fees (if applicable)

Savings and Money Market Savings Accounts Liquidity (measured by time and access to funds) Maturity Interest rate Minimum balance Fees (if applicable)

D. CUSTOM SERVICE

Most products in the thrift industry are standardized, but the pricing of the products vary by customer. For example, Bank A offers 30-year fixed mortgage rate loans at all of their branches. However, the actual mortgage interest rate may be 9.0% for an individual with poor credit history while an individual with excellent credit purchasing a home in Des Moines, Iowa may be offered the same loan product at 7.5% APR from the same bank. The reader should note that the standardization of loan products serves a vital function for savings institutions: it facilitates the sale of loans to secondary agencies, which pool similar mortgages and market them as securities. Therefore, even though pricing may vary by customer, each customer falls into a credit risk bracket, which is usually assigned a pricing range. In turn, this standardizes loans among credit risk levels and types of loans. Standardization is more pronounced for thrift liabilities. Primarily, rates and terms distinguish savings accounts. (Standard and Poor’s)

E. SEASONALITY

Thrift industry services are not seasonal. F. SERVICE SUBSTITUTION

There will be instances where thrift branches may close and clients withdraw the assets from an account. In these cases, similar services and clients with similar accounts will be used as substitutes for the previous bank product or service.

4. MARKET AND TRANSACTION INFORMATION

A. INTERPLANT AND INTRAINDUSTRY PAYMENTS

Thrifts participate in interplant and intraindustry sales. Thrifts offer the following interplant and intraindustry services.

19

Mortgage-backed Securities Sales and Mortgage Pools—Many wholesale thrifts engage in the business of selling mortgage backed securities, which could be sold to other thrifts. They can also be sold to commercial banks, as well as commercial businesses and individuals. Thrifts may pool all of their originated loans and sell them as a package in the secondary market or among other thrifts. For a wholesale thrift, mortgage backed securities represent more than 40% of total assets. Correspondent Banking: Some small thrifts hold deposits in larger thrifts (also commercial banks and holding banks) for a variety of services, including check collection and clearance, foreign exchange transactions, and help with securities purchases. Officers and principal shareholders go to larger thrifts and maintain one or more correspondent accounts. The accounts in aggregate usually exceed an average daily balance during the reporting calendar year of $100,000 or 0.5 percent of the officer’s or principal shareholder’s bank’s total deposits (Office of Thrift Supervision, 12/23/96 Thrift Bulletin).

B. PRICE BEHAVIOR

Price behavior of thrifts’ primary service, mortgage lending, has always been dependent on national interest rates and the thrifts’ costs of funds. The two most important interest rates for the thrift industry are the six- month Treasury Bill (T-bill) and the 30 year fixed mortgage interest rate (Federal Home Loan Mortgage Corporation money rate). The six-month T-bill rate is important because it is a proxy for deposit costs; the average term for a certificate of deposit (CD) is about six months. The 30-year fixed rate mortgage figure indicates the yield a given institution might receive on its new loans. (Standard and Poor’s) Since the industry’s practice is to borrow short and lend long, thrifts have very little opportunity to change interest rates on fixed rate loans once loan contracts are signed. Adjustable rate mortgages do offer variable mortgage interest rates in line with movements of national interest rates, but they also stipulate an interest rate ceiling. The prices of checking and savings accounts, however, are more volatile. Not only does the national interest rate affect the costs for the bank, market competition also greatly influences the cost of thrifts to service the customer.

C. UNIT OF MEASURE The unit of measure is either going to be per transaction for pricing fee based services or per portfolio per month for pricing deposits and loans. For deposit and loan services, individual account data is not acceptable. But rather, the pricing will be for groups of loans or deposits with homogeneous characteristics. The records of the bank or bank department will determine the level of each portfolio. The data for the portfolio being priced must be on a per month basis. The reporter may have to make some conversions to get the data to a per month basis.

D. TYPES OF PRICES

REFERENCE RATE

20

A reference rate is used in calculating in order to allocate earned income on loans between loans and implicit services on deposits The reference rate to be used represents the pure cost of borrowing funds- that is, a rate from which the risk premium has been eliminated to the greatest extent possible and which does not include any intermediation services. This rate is calculated by the Washington office TYPE OF PRICES FOR DEPOSITS “Interest less fees” All deposits will be priced at the portfolio level on a monthly basis. The following formula will be used to determine the deposit price:

{Reference Rate - Interest payments - Earned deposit fees } * $1,000 Average deposit balance The reference rate will be calculated by the Washington Office. A dummy value is preprinted on the checklist because it is a different value every quarter and will be updated during collected data review in the WO. The respondent is to provide total interest payments made for the selected deposit portfolio for the calendar month, deposit fees earned for the month, and the average deposit balance for the month. The average deposit balance is to be calculated by dividing the sum of the ending daily balances for the calendar month by the number of days in the month. A worksheet to assist in this calculation is provided in the checklist. LOANS “Interest income plus fees” All loans will be priced at the portfolio level on a monthly basis. The following formula will be used to determine the loan price:

{Earned interest income + Fees - Reference Rate } * $1,000 Average loan balance The reference rate will be calculated by the Washington Office. A dummy value is preprinted on the checklist because it is a different value every quarter and will be updated during collected data review in the WO. The respondent is to provide total earned interest income for the selected loan portfolio for the calendar month, fees earned for the month, and the average loan balance for the month. The average deposit balance is to be calculated by dividing the sum of the ending daily balances for the calendar month by the number of days in the month.

21

A worksheet to assist in this calculation is provided in the checklist.

NOTE: The Annual Percentage Rate (APR) incorporates loan origination and loan servicing fees that are associated with real estate, commercial, industrial, and home equity loans. Thus, for all real estate, commercial, industrial, and home equity loans, the loan yield (effective interest rate) will be used in the estimation of the loan price. NOTE: If the bank does not separate loan servicing fees for loans that they do not hold from those fees earned on loans they do hold, they should be included as part of the fee component of this price. If fees for loans not held can be separated, price these services on fee basis as described below. TYPE OF PRICE FOR ALL OTHER SERVICES “Fee” The remaining services are price on a fee basis. Loan Servicing for loans not held (if separate records) : Banks can pool loans together and sell them to third parties. Banks may choose to continue to service the loans, such as handling loan payments, correspondence, and other services, while the third party collects interest payments. For this service, collect the percentage charged to third parties for loan servicing. When banks service their own loans, this income is captured in their interest earnings. Trust Operations: The fees that banks charge for trust operations are usually determined by a percent of the market value of the assets in custody at the banks. For example, a mutual fund may place in custody assets valuing $1,000,000, and the bank may charge .05% to safeguard the assets. Therefore, the bank's fee is $1,000,000 times .05% or $5,000. Standby Letter of Credit: The fee for this service is based on a flat fee. The flat fee is determined in a contractual agreement between the bank and its customer. The price is calcalated as a percentage of the value of the assets. Cash management services: The service can be provided on a flat fee or cost per item basis.

E. TYPES OF BUYERS

Retail Retail buyers usually seek services such as mortgage and consumer loans, checking and savings accounts, and credit cards. Retail services are available to any individual, company, government entity, or other financial intermediary. Retail buyers are the most important buyers, since thrift business relies mainly on retail deposits and the selling of mortgage loans. Wholesale

22

Wholesale buyers include institutions that buy intraindustry and interplant services, mainly mortgage backed securities sold in the secondary market. Mortgage backed securities represent approximately 40% of total assets for the industry. Commercial Commercial buyers have access to retail, commercial, and wholesale services. Commercial buyers include businesses seeking real estate and non-real estate commercial loans, commercial checking accounts, and other services helpful to the running of business operations. Commercial buyers may also seek correspondent banking services. Commercial buyers, however, constitute a small percentage of thrift business. Government Government entities may seek thrift services, such as savings accounts, selling and buying of treasury bills, or purchases of mortgage backed securities. Thrifts generate very little business from government buyers.

F. DISCOUNTS

Loans The amount of down payment may serve to directly benefit the borrower with discounted interest rates on loans. Upon discretion of the lender, the larger the down payment, the lower the interest rates the lender can offer. This is true since the lender reduces his or her loan-loss risk because the borrower has established equity on the loan. For example, if a borrower seeks to purchase a $10,000 car, but offers to place a $5,000 down payment, (thus seeking to borrow $5,000), the lender can offer lower interest rates on the loan due to the established equity on the collateral (the car). The opposite holds true. In order to entice customers further, thrifts may require lower down payments or even zero percent down payments on loans, but usually require higher interest rates. The Federal Housing Administration (FHA) and the Department of Veteran’s Affairs VA mortgage loans usually offer this discount. Therefore, down payments or loan to value ratios shall be used as constants to compare loan prices. Other types of discounts may include introductory loan rates in order to draw a borrower to borrow long term. Introductory rates are usually very low, but after a specified short term, interest rates increase to market or above market rates. Lastly, discounts may also be offered to certain groups of people, such as low-income families and United States veterans and their spouses, or customers that hold other accounts in the thrift. Loan origination fees In order to increase interest revenue, thrifts may waive certain fees or charge fewer points on loans. This type of discount occurs frequently due to the competitiveness of the industry. Other fees and commissions Current figures indicate that thrifts have significantly increased non-interest income due to these types of service fees. Thrifts are usually reluctant to waive or discount these fees and commissions, but it does occur.

23

Service charges on deposit accounts Discounts occur frequently in thrift deposit accounts, especially for those customers who hold loans and other thrift income-generating accounts. Thrifts also typically reduce or waive checking monthly maintenance fees for customers who agree to maintain a minimum balance on the deposit accounts. Certain groups such as students, senior citizens, and high-volume commercial accounts also benefit from deposit account discounts.

NOTE: The pricing formula for deposits and loans captures all discounts.

G. ADDITIONAL CHARGES

Loans As previously mentioned, loans always attach loans service fees, such as loan origination fees, attorney and appraisal fees, credit history research, and other administrative fees. Some loan service fees are added to the list price of loans (quoted interest rates) to establish the Annual Percentage Rate (APR), sometime referred as the true price of the loan to the consumer. Points (loan discount points) are also an additional charge added to the price of loans. Points are measured as one percent of the amount of the loan, and are defined as prepaid interest on a mortgage that is usually paid at the time of closing. One point on an $80,000 mortgage is $800, or 1 percent of $80,000. Most lenders offer mortgages with several combinations of points and interest rates; generally, the lower the interest rate, the more points the borrower will pay at settlement. Other fees and commissions Most of the fees in this category are independent of additional charges. Other fees that fall in this category are additional charges for separate services. Service charges on deposit accounts The fees described and included in this category are self-explanatory on how they may apply as additional charges. The following is a list of the most common fees: overdraft fees, ATM fees, check printing fees, transaction fees (per item processed), interest on overdraft protection, bounced check fees, and various other customized styles and fee arrangements. NOTE: The pricing formula for deposits and loans captures all discounts.

H. SIZE OF PURCHASE

For service lines in the thrift industry, such as deposit accounts, sometimes there is no minimum purchase or balance required. However, some thrifts may require some sort of account restrictions. A savings account can be opened with very minimal dollar amounts, i.e. 5 dollars, at certain banks.

Loans usually require a minimum down payment. For most mortgages, the minimum down payment is usually 20% of the loan, unless they are FHA and VA loans that offer as incentives lower down payments, which typically call for 10% down or less.

24

Mortgage backed securities do have several minimum amount requirements. For example, the Federal Home Loan Mortgage Company (FHLMC or Freddie Mac) requires a minimum investment of $100,000 per participation certificate. The Government National Mortgage Association (GNMA) issues securities at $25,000 denominations with $5,000 increments. Other mortgage-backed securities follow similar restrictions.

I. CONTRACTS

Loans are contracts in which money is lent at interest. The borrower agrees to make payment(s)--including interest--in a timely manner, as specified under contract. A thrift’s primary “contract” is the mortgage loan.

J. OTHER VARIABLES AFFECTING PRICE

Currently there are no other known variables that affect price.

5. INDUSTRY INFORMATION AND RELATIONS

A. INDUSTRY RELATIONS

America’s Community Bankers 900 19th St. NW, Ste. 400 Washington, DC 20006 (202) 857-3100 Contact: Kit Harahan, Manager, Information Resources Members include savings and loan associations, savings banks, cooperative banks, and state and local savings and loan association leagues in all US states and territories. American Bankers Association 1120 Connecticut Avenue, NW Washington, DC 20036 (202) 663-5350 Contact: Dr. Robert Strand and Dr. Keith Leggett Office of Thrift Supervision 1700 G. Street, NW Washington, DC 20552 (202) 906-6000

American Council of State Savings Supervisors PO BOX 34175 Washington, DC 20043-4175 (202) 371-0666 Members include state savings and loans supervisors and are appointed by the governor of each state.

25

B. CURRENTLY AVAILABLE PRICE DATA

There is no comprehensive listing of price data for all the service lines in the savings institution industry. There are to some degree published data on mortgage rates. They can be accessed over the Internet for most thrifts, but thrifts only quote their annual percentage rates and not the quoted interest rate. Deposit prices are very accessible for most thrifts on the Internet or by phone. Thrift Reports provide financial information; however, their function is to state the operations, services, and soundness of the banks. They do not break down the necessary information for a PPI calculation. Bysis Corporation: The Bysis corporation provides pricing data for all commercial banks and thrifts, which include annual percentage rates on loans and deposits. This is for current daily rates not including products in the portfolio of the institution. It should be kept in mind that the sources mentioned above do not provide the necessary price information for pricing thrift services because of methodological requirements. The following lists the major advantages that a PPI SIC 603 price index would have over the above data sources on thrift services:

Index measures spreads, such as value added and liquidity at the producer level. The above

data sources only provide consumer prices. Index measures price movements at the wholesale level on a monthly basis. No other resource

does this. Other sources do not provide price data for all deposits in a bank portfolio—only currently

offered services, excluding previously contracted services that continually are sold. Index is for all revenue generating services including those initiated in past periods for which

institutions continue to receive revenue. This contrasts with other sources that have pricing data only on services currently initiated.

C. LITIGATION AND OTHER COOPERATION PROBLEMS

There is no known litigation at this time. Moreover, at this time there appears to be no anti-trust actions taken against this industry. However, because of heavy government regulation and overseeing, bankers may be hesitant to provide prices to a government entity since banks may fear anti-trust issues. But, if the BLS seeks trade association endorsement, cooperation among thrifts is expected to greatly improve. A point worth noting is that pricing problems may arise from future deregulation of the industry. Since the early 1980s, deregulation has changed the thrift industry dramatically. In 1980, in order to help struggling thrifts compete more efficiently against banks, congress passed the Depository Institutions Deregulation and Monetary Control Act (DIDMCA) which allowed thrifts to offer other bank-like services such as negotiable order of withdrawal accounts (NOWs), which are essentially interest-bearing checking accounts. In 1982, the Garn-St. Germain Act gave thrifts

26

investment powers to expand their holdings of corporate bonds and corporate equities. The act also allowed thrifts to convert from mutual to stock institutions, thus increasing their net worth. In 1989, the FIRRE Act allowed commercial banks to freely acquire thrifts across state borders while setting stringent capital standards for thrifts. Lastly, the Reigle-Neil Interstate Banking Act of 1994 permits commercial banks to have interstate branches nationwide, thus greatly increasing competition against thrifts. More significantly, Congress approved landmark legislation in November 1999 that repealed the Glass-Steagall Act of 1933. The Glass-Steagall Act of 1933 separated bankers and brokers in order to reduce the potential conflicts of interest that were thought to have contributed to the speculative stock frenzy before the Depression. (Source: New York Times)This new legislation will transform the financial industry dramatically. Commercial banks, thrifts, securities houses, and insurers will find it easier and cheaper to enter in each other’s businesses. Therefore, we will see thrifts offer one-stop shopping for financial services, such as the selling of insurance or mutual fund management.

D. SERVICE IDENTIFICATION PROBLEMS

It is anticipated that services in the banking sector will continuously be changing, especially as Internet banking and electronic commerce become more popular. Several banking services are considered investment activities by the PPI, and therefore, will not be collected. These services include trading in Federal Funds, derivatives, repurchase agreements, and loan brokerage.

E. CHECKLIST CLARIFICATIONS

A6037A DEPOSIT SERVICES Type of Deposit Service (group 01) –For code 020 (other deposit service), describe any deposit service that is not specified in the checklist, or any portfolio which crosses two or more ISDWS categories (e.g. a portfolio that includes both time deposits and demand deposits). Service Identification (group 2) – For codes 001- 002, specify the name or identification of the portfolio of deposit service, such as 1-year retail CD bucket, if applicable. Type of Checking Account (group 3) – Only complete the group if the selected portfolio is further defined. If the portfolio includes more than one type of account, it is unnecessary to indicate all types included. Type of Deposit Fees (group 5)—Record up to 5 of the top fees that are included as revenue for the deposit service portfolio, even though the portfolio may actually include more than 5. Should the respondent wish to see more than 5, then specify all applicable fees. Deposit Characteristics (group 6) – For code 001 Number of Accounts, record an estimate of the number of accounts included in the selected portfolio. This number does not have to be exact.

27

For code 002 Average number of transactions per loan, record an estimate of the average number of transactions for each deposit included in the portfolio. This number does not have to be exact. A6037B LOAN AND LEASING SERVICES Type of Service (Group 1) – Code 013 (other loan services) refers to boat loans, passbook loans, installment loans, student loans and overdraft protection loans. Also select this code if the loan service includes portfolios that cross two or more ISWDS categories (e.g. a portfolio that includes both residential and non-residential real estate loans). Service Identification (group 2) – For codes 001- 002, specify the name or identification of the portfolio of loans or leases, such as “All Real Estate Loans”, if applicable. Type of Loan (group 4) - If the portfolio has both fixed and adjustable rate loans, specify this in this code 003 Other Type of Loan.. Term of Loan (group 5) – For code 001, express the portfolio in terms of months or years, whichever the bank prefers. Fees Required by Lender (group 13) This group is NOT limited to 5 fees like deposits. Indicate all fees that apply. Loan Characteristics (group 16) – For code 001, record an estimate of the number of loan accounts in the portfolio. This number does not have to be exact. For code 002, record an estimate of the average number of transactions incurred for each loan in the selected portfolio (e.g. one late payment fee). This number does not have to be exact. A6037C TRUST SERVICES Rate of Return Excluding fees and distributions (group 5) - For code 001, indicate the return earned on the selected trust. This rate should not reflect changes due to new money being added to and removed from the trust account. For code 002, indicate if the bank calculates this rate monthly or quarterly.

F. INDUSTRY SPECIFIC QUESTIONS AND PROCEDURES

Related SICS SIC 6023 Commercial Banking and SIC 6037 Savings Institutions are related SICs. Sample Unit Identification The sample unit is the bank's headquarters. It may be the case that a sample unit operates both as the bank's headquarters as well as the bank's branch. This may be the case for small rural banks.

28

There will also be instances where the bank's holding company may be located in the same building as the bank's headquarters. If this is the case, pay particularly close attention to the name of the contact person. The sample is divided into two tiers: small banks and large banks. (1) Small Banks The sample unit is the bank's headquarters. It may be the case that a sample unit operates both as the bank's headquarters as well as the bank's branch. This may be the case for small rural banks. There will also be instances where the bank's holding company may be located in the same building as the bank's headquarters. If this is the case, pay particularly close attention to the name of the contact person. The “small” banks are sampled as the “whole” bank. That is, all output of the banks is to be given a chance of selection. The sample unit is identified by its unique certificate number that is provided on the facesheet. The absence of a secondary name on the facesheet will indicate that the sample unit is a small bank. In this case, the most appropriate contact is the cashier or CFO. Either of these bank officials can identify the single person who can provide the data for the sample unit. This person should be the best “match” for the sample unit. If a single person cannot provide all data for the sample unit, subsample to a single person/record center based on rank or equal probability. (2) Large Banks The “large” banks are sampled by department. Keep in mind that these are BLS-created departments. That is they may not match the actual department structure of the sample unit. There are seven department designations: 1. Mortgage Loans: ISDWS #1-3 2. Agricultural Loans: ISDWS #4 3. Commercial Loans: ISDWS #5 4. Consumer and Other Loan Serivces: ISDWS #6-8 5. Retail: ISDWS #9-11 6. Trust services: ISDWS #12 7. Other banking services: ISDWS #13 The retail department refers to “deposits.” Only the output of the sampled department (defined by the ISDWS categories included) is eligible for selection. Again, the sampled bank can be identified by its unique certificate number. The most appropriate contact is the head of the department. Facesheet Procedures 1) Leave all S&R information blank in the collection system.

29

2) The measure of size indicated on the facesheet is revenue rather than employment. Leave “RU revenue” blank in the collection system.

3) There are no counties provided on the facesheet. Therefore, it is unnecessary to obtain this information.

4) No VOS per employee edit range is provided for this industry. Therefore, the VOS per employee calculation in not required.

Contact person

For small banks (not sampled by department), the most appropriate contact for obtaining data is the cashier. For large banks (sampled by department), it is the head of each department. Other Receipts Services such as insurance, investment advice and brokerage services should be collected as other receipts. It is unlikely that you will encounter these services. They are provided by a separate subsidiary of the bank as required by law. If these services are provided by a department and comprise 5% or more of the bank’s revenue, give them a chance of selection. Use the checklists for the Investment Advice, Stockbrokers and Dealers, and Insurance.

Special Disaggregation Procedures Disaggregation procedures for small banks All small banks have been assigned 8 items: Loans 4 items (2 items must be residential real estate) Deposits 3 items Other banking services

1 item

Other receipts Assign 1 add’l item if 5% or more of revenue If the bank does not provide other banking services, assign that quote to deposits (collecting 4 deposit quotes). The most appropriate contact is the cashier. If the cashier cannot provide the data, then find out if there is one person who can. If one person cannot provide the data for all services, subsample to a single person/department head using the assigned quotes as a size measure. All output within the subsampled department should be given a chance of selection.

Disaggregation procedures for large banks

30

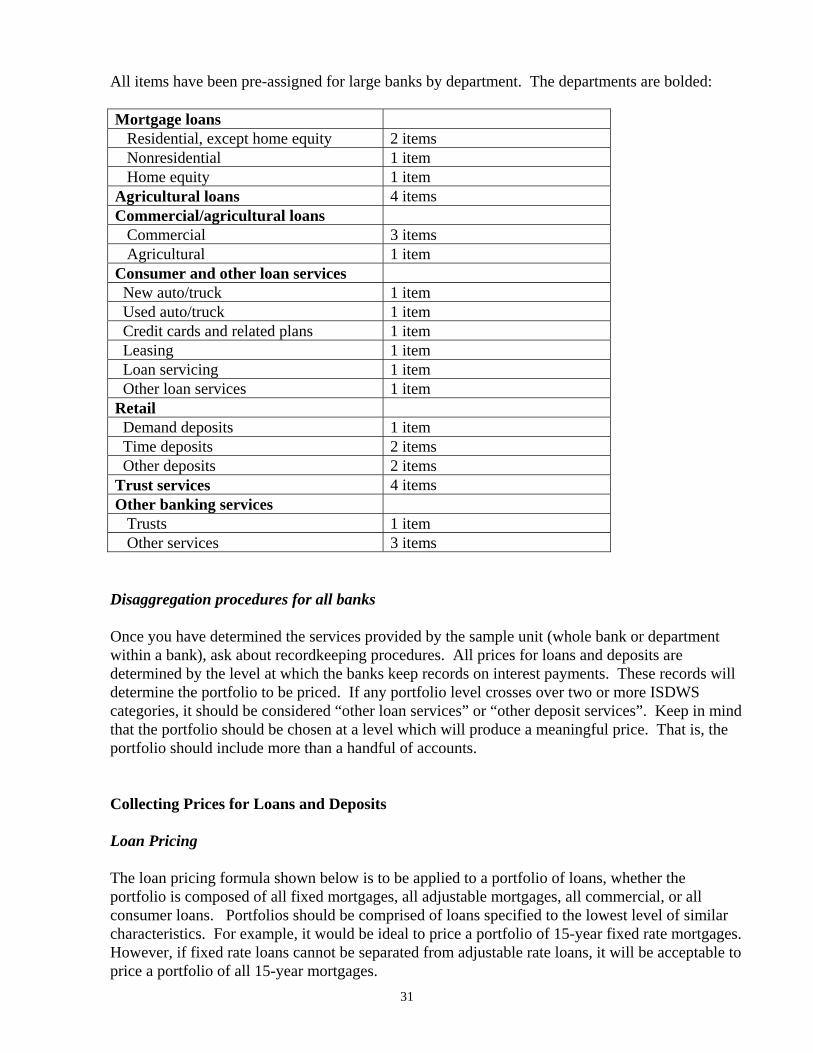

All items have been pre-assigned for large banks by department. The departments are bolded: Mortgage loans Residential, except home equity 2 items Nonresidential 1 item Home equity 1 item Agricultural loans 4 items Commercial/agricultural loans Commercial 3 items Agricultural 1 item Consumer and other loan services New auto/truck 1 item Used auto/truck 1 item Credit cards and related plans 1 item Leasing 1 item Loan servicing 1 item Other loan services 1 item Retail Demand deposits 1 item Time deposits 2 items Other deposits 2 items Trust services 4 items Other banking services Trusts 1 item Other services 3 items

Disaggregation procedures for all banks Once you have determined the services provided by the sample unit (whole bank or department within a bank), ask about recordkeeping procedures. All prices for loans and deposits are determined by the level at which the banks keep records on interest payments. These records will determine the portfolio to be priced. If any portfolio level crosses over two or more ISDWS categories, it should be considered “other loan services” or “other deposit services”. Keep in mind that the portfolio should be chosen at a level which will produce a meaningful price. That is, the portfolio should include more than a handful of accounts. Collecting Prices for Loans and Deposits Loan Pricing The loan pricing formula shown below is to be applied to a portfolio of loans, whether the portfolio is composed of all fixed mortgages, all adjustable mortgages, all commercial, or all consumer loans. Portfolios should be comprised of loans specified to the lowest level of similar characteristics. For example, it would be ideal to price a portfolio of 15-year fixed rate mortgages. However, if fixed rate loans cannot be separated from adjustable rate loans, it will be acceptable to price a portfolio of all 15-year mortgages.

31

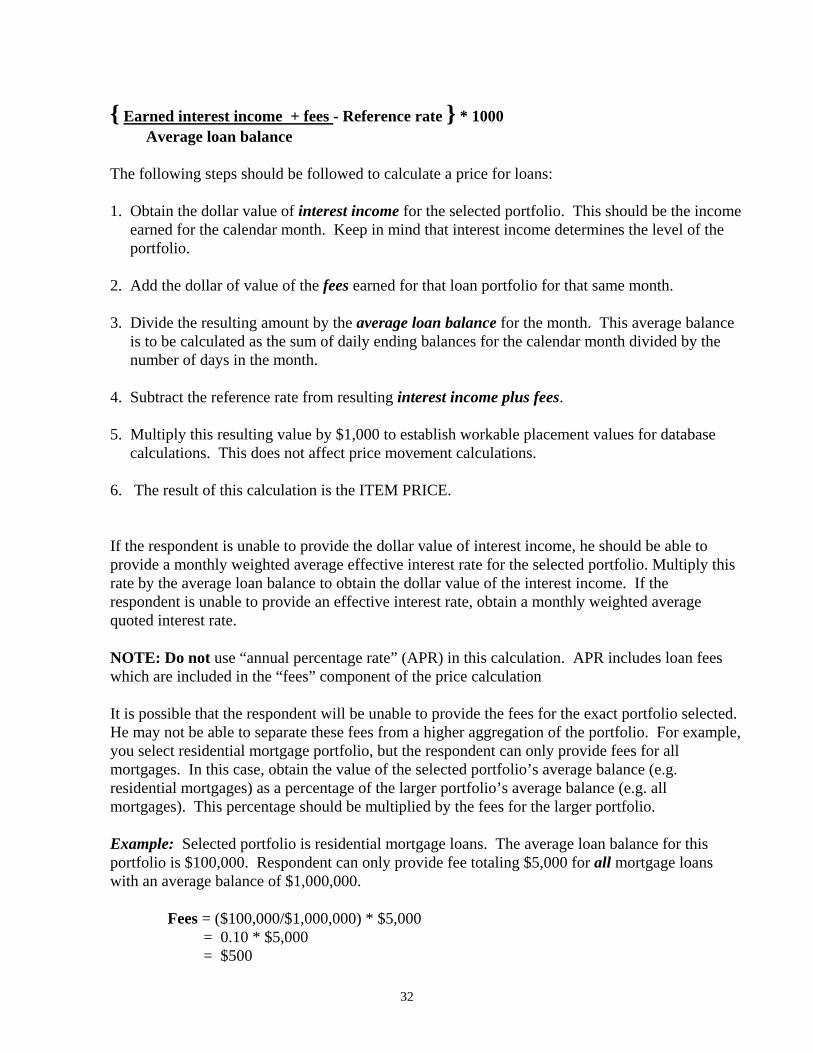

{ Earned interest income + fees - Reference rate } * 1000 Average loan balance The following steps should be followed to calculate a price for loans: 1. Obtain the dollar value of interest income for the selected portfolio. This should be the income earned for the calendar month. Keep in mind that interest income determines the level of the portfolio. 2. Add the dollar of value of the fees earned for that loan portfolio for that same month. 3. Divide the resulting amount by the average loan balance for the month. This average balance is to be calculated as the sum of daily ending balances for the calendar month divided by the number of days in the month. 4. Subtract the reference rate from resulting interest income plus fees. 5. Multiply this resulting value by $1,000 to establish workable placement values for database calculations. This does not affect price movement calculations. 6. The result of this calculation is the ITEM PRICE. If the respondent is unable to provide the dollar value of interest income, he should be able to provide a monthly weighted average effective interest rate for the selected portfolio. Multiply this rate by the average loan balance to obtain the dollar value of the interest income. If the respondent is unable to provide an effective interest rate, obtain a monthly weighted average quoted interest rate. NOTE: Do not use “annual percentage rate” (APR) in this calculation. APR includes loan fees which are included in the “fees” component of the price calculation It is possible that the respondent will be unable to provide the fees for the exact portfolio selected. He may not be able to separate these fees from a higher aggregation of the portfolio. For example, you select residential mortgage portfolio, but the respondent can only provide fees for all mortgages. In this case, obtain the value of the selected portfolio’s average balance (e.g. residential mortgages) as a percentage of the larger portfolio’s average balance (e.g. all mortgages). This percentage should be multiplied by the fees for the larger portfolio. Example: Selected portfolio is residential mortgage loans. The average loan balance for this portfolio is $100,000. Respondent can only provide fee totaling $5,000 for all mortgage loans with an average balance of $1,000,000. Fees = ($100,000/$1,000,000) * $5,000 = 0.10 * $5,000

= $500

32

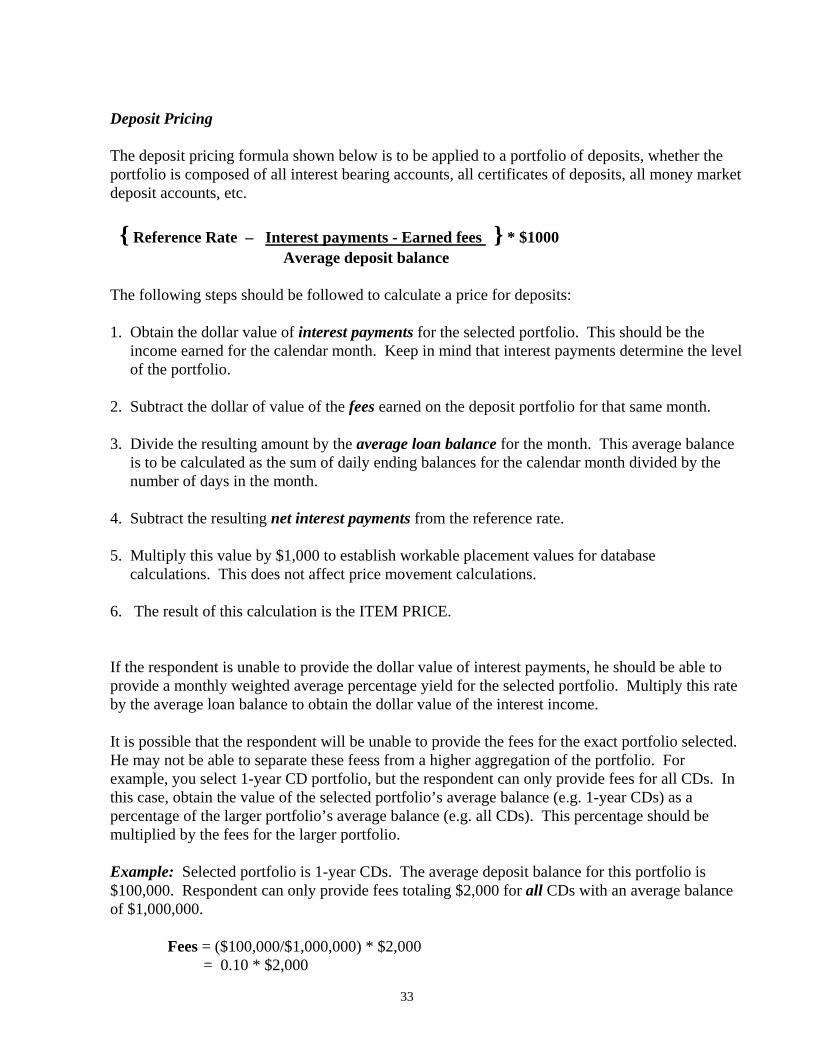

Deposit Pricing The deposit pricing formula shown below is to be applied to a portfolio of deposits, whether the portfolio is composed of all interest bearing accounts, all certificates of deposits, all money market deposit accounts, etc. { Reference Rate – Interest payments - Earned fees } * $1000 Average deposit balance

The following steps should be followed to calculate a price for deposits: 1. Obtain the dollar value of interest payments for the selected portfolio. This should be the income earned for the calendar month. Keep in mind that interest payments determine the level of the portfolio. 2. Subtract the dollar of value of the fees earned on the deposit portfolio for that same month. 3. Divide the resulting amount by the average loan balance for the month. This average balance is to be calculated as the sum of daily ending balances for the calendar month divided by the number of days in the month. 4. Subtract the resulting net interest payments from the reference rate. 5. Multiply this value by $1,000 to establish workable placement values for database calculations. This does not affect price movement calculations. 6. The result of this calculation is the ITEM PRICE. If the respondent is unable to provide the dollar value of interest payments, he should be able to provide a monthly weighted average percentage yield for the selected portfolio. Multiply this rate by the average loan balance to obtain the dollar value of the interest income. It is possible that the respondent will be unable to provide the fees for the exact portfolio selected. He may not be able to separate these feess from a higher aggregation of the portfolio. For example, you select 1-year CD portfolio, but the respondent can only provide fees for all CDs. In this case, obtain the value of the selected portfolio’s average balance (e.g. 1-year CDs) as a percentage of the larger portfolio’s average balance (e.g. all CDs). This percentage should be multiplied by the fees for the larger portfolio. Example: Selected portfolio is 1-year CDs. The average deposit balance for this portfolio is $100,000. Respondent can only provide fees totaling $2,000 for all CDs with an average balance of $1,000,000. Fees = ($100,000/$1,000,000) * $2,000 = 0.10 * $2,000

33

= $200 Completing the Worksheets for Deposits and Loans There are four worksheets provided for deposit and loan services. Only ONE worksheet is to completed as described below. Option 1: Complete this worksheet if respondent can provide the dollar value of interest payments/income and the fees for the selected portfolio. Option 2: Complete this worksheet if the respondent can only provide the interest rate necessary to calculate the interest payment/income AND can only provide fees for a more highly aggregated portfolio. Option 3: Complete this worksheet if the respondent can provide the dollar value of interest payments/income, BUT he can only provide fees for a more highly aggregated portfolio. Option 4: Complete this worksheet if the respondent can only provide the interest rate necessary to calculate the interest payment/income BUT he can provide fees for the selected portfolio. Procedures for Repricing Respondents will be asked to reprice on a monthly basis. All fee components should be updated as they change. The reference rate will be updated periodically by the Washington Office and will be provided on the repricing form. The Washington Office will also “escalate” certain dollar values on an annual basis to account for the time value of money. For loans and deposits, it is the $1000 multiplier that will be escalated. For all other services, the value upon which the price is based will be adjusted.

G. PRE-SURVEY CONTACTS

Presurvey Contacts GreenPoint Bank 1981 Marcus Ave. Lake Success, NY 11042-1038 Phone: 203 965-1980 Stephen Morfeld, Vice President Telebank 1111 N. Highland Street Arlington, VA 22201-2807 Phone: 703 247-3705 Aileen Pugh, Vice President, CFO

34

Chevy Chase FSB 8401 Connecticut Ave. Chevy Chase, MD 20815 Phone: 301 986-7427 Rich Handloff, Vice President, Senior Product Manager Pretest Contacts Dennis L. Parente, President Foxboro Federal Savings One Central Street Foxboro, MA 02035 (508) 543-5321 Dennis L. Parente, President Middlesex Federal Savings, FA One College Avenue Somerville, MA 02144 (617) 66-4700 Joseph Smalarz, President Peoples Federal Savings Bank 435 Market Street Brighton, MA 02135 (617) 254-0707 Charles L. Gaffney, Operations Officer & Assistant Vice President Colonial FSB 15 Beach Street Quincy, MA 02170 First Indiana Bank First Indiana Plaza 135 North Pennsylvania Street Indianapolis, IN 46024 (317) 269-1346 David L. Gray, Senior Vice President Lincoln Federal Savings Bank Andy LoCascio, Financial Analyst 1121 East Main St. PO Box 510 Plainfield, IN 46168 (317) 839-6539 John M. Baer, CFO

35

36

Landmark Savings Bank 54 Monument Circle Indianapolis, IN 46204 (317) 633-0900 Larry Delpha, CFO Union Federal Savings Bank of Indianapolis 45 North Pennsylvania Street Indianapolis, IN 46204 (317) 269-4834 Mr. Dana Dillard, CFO

6. PUBLICATION GOALS

6037 Savings institutions 6037P Primary services 60371 Loan services 6037101 Residential real estate loans, except home equity 6037102 Nonresidential real estate loans 6037103 Home equity loans 6037104 Agricultural loans, except real estate 6037105 Commercial and industrial loans, except real estate 6037106 New and used auto and truck loans 6037107 Credit cards, overdraft credit, and related plans 6037108 Other loan services 60372 Deposit services 6037201 Demand deposits 6037202 Time deposits 6037203 Other deposit services 60373 Other banking services 6037SM Other receipts