Embed Size (px)

DESCRIPTION

In this issue:- Regional Currency Outlook and Property Investments – Which Overseas Markets - Singapore Property News This Week- Resale Property Transactions (March 12 – March 15)

Citation preview

ContributeDo you have articles and insights and articles that you’d like to share with thousands of readers interested in the Singapore property market? Send them to us at [email protected], and if they’re good enough, we’ll publish them here, on our blog and even on Yahoo! News.

AdvertiseWant to get your brand, product, service or property listing out to thousands of Singapore property investors at a very reasonable cost? Head over to www.propwise.sg/advertise/ to find out more.

CONTENTS

p2 Regional Currency Outlook and Property

Investments – Which Overseas Markets

Look Attractive?

p10 Singapore Property News This Week

p14 Resale Property Transactions

(March 12 – March 15)

Welcome to the 253th edition of the Singapore Property Weekly.

Hope you like it!

Mr. Propwise

FROM THE

EDITOR

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 2Back to Contents

By Paul Ho (guest contributor)

An overseas property investment consists oftwo components – the property investmentand the currency investment. If you invest ina property that increases in value by 20%over a period of three years, but the currencydepreciates by 30% over the same period,

you will be realizing a loss if you liquidate.

Usually, Singapore-based investors willcompare the local currency in the country ofinvestment against either the SingaporeDollar (SGD) or the US Dollar (USD).Mostoften the base currency is SGD, simplybecause that is the currency that the

Regional Currency Outlook and Property Investments –Which Overseas Markets Look Attractive?

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 3Back to Contents

Singapore-based investor earns, and is mostfamiliar with.

Interest rate trends in major economies

The US economy is recovering, withunemployment at five percent (as of Nov2015) and an Interest Rate (IR) of 0.25%. On16 Dec 2015, the Federal Reserve increasedthe overnight target rate from 0.25 percent to0.5 percent. Inflation in the US is currently stillunder one percent, below the FederalReserve’s target of 1.5 to 2 percent.

Although the US recovery seems tentative, itis nonetheless an economic recovery. It ispossible there will be a few rate hikes in 2016as the target overnight Federal Reserve fundsrate at 0.5% is still low.

However, other major economies such as theEuropean Union, China and Japan areslowing down. The EU’s growth rate is less

than two percent, China is struggling tomaintain seven percent growth, and Japan’s

growth hovers around one to two percent.

The EU’s interest rate is close to zeropercent, Japan’s is at zero, while Chinadropped its benchmark yearly interest rate to4.35 percent.

Just to put things into perspective, the world’s

major economies are:

The European Union – at around 18 trillion USD

USA – Number 2 – at around 17 trillionUSD

China – Number 3 – at around 10 trillionUSD

Japan – Number 4 – at around 4.6 trillionUSD

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 4Back to Contents

The world economy is around US$77 trilliondollars. The top 4 economies make uproughly US$49.6 trillion dollars or about 65percent of the world’s economy and would bea good enough representative.

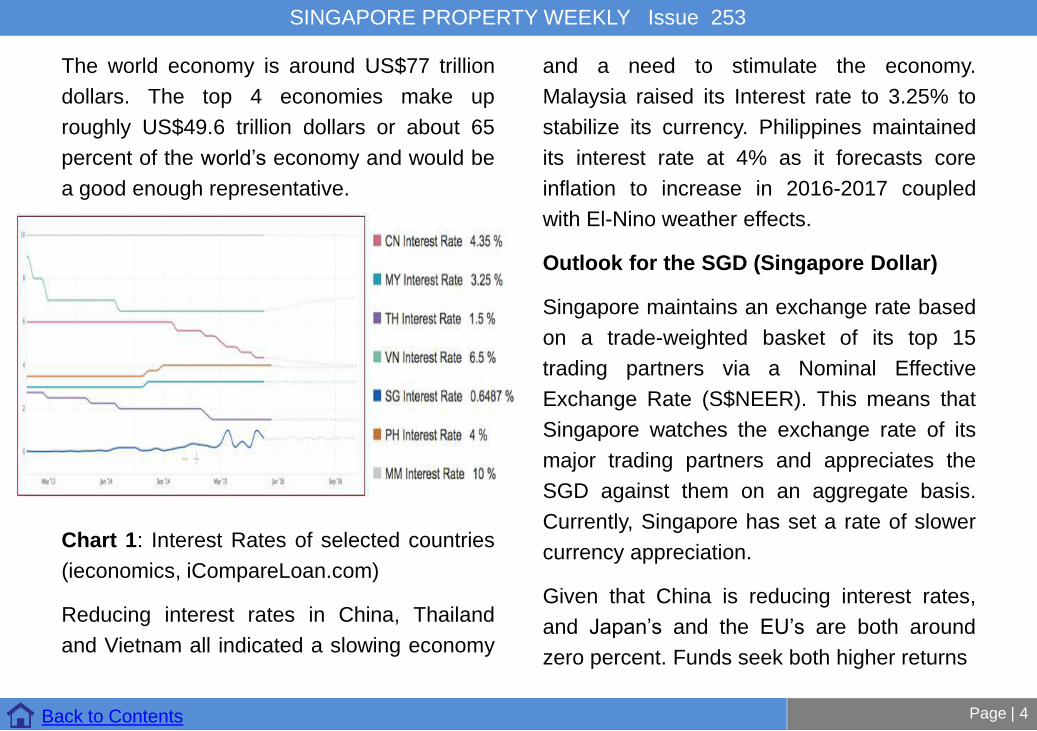

Chart 1: Interest Rates of selected countries(ieconomics, iCompareLoan.com)

Reducing interest rates in China, Thailandand Vietnam all indicated a slowing economy

and a need to stimulate the economy.Malaysia raised its Interest rate to 3.25% tostabilize its currency. Philippines maintainedits interest rate at 4% as it forecasts coreinflation to increase in 2016-2017 coupledwith El-Nino weather effects.

Outlook for the SGD (Singapore Dollar)

Singapore maintains an exchange rate basedon a trade-weighted basket of its top 15trading partners via a Nominal EffectiveExchange Rate (S$NEER). This means that

Singapore watches the exchange rate of itsmajor trading partners and appreciates theSGD against them on an aggregate basis.Currently, Singapore has set a rate of slowercurrency appreciation.

Given that China is reducing interest rates,and Japan’s and the EU’s are both aroundzero percent. Funds seek both higher returns

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 5Back to Contents

as well as an appreciating currency such asthe USD. And an appreciating currencytypically coincides with improving economicoutlook or fundamentals. Singapore’s

economy is slowing down – the Dec 2015Purchasing Manager Index (PMI) at 49.5%,indicating forecasted economic contraction.Hence, the SGD may find itself having toappreciate.

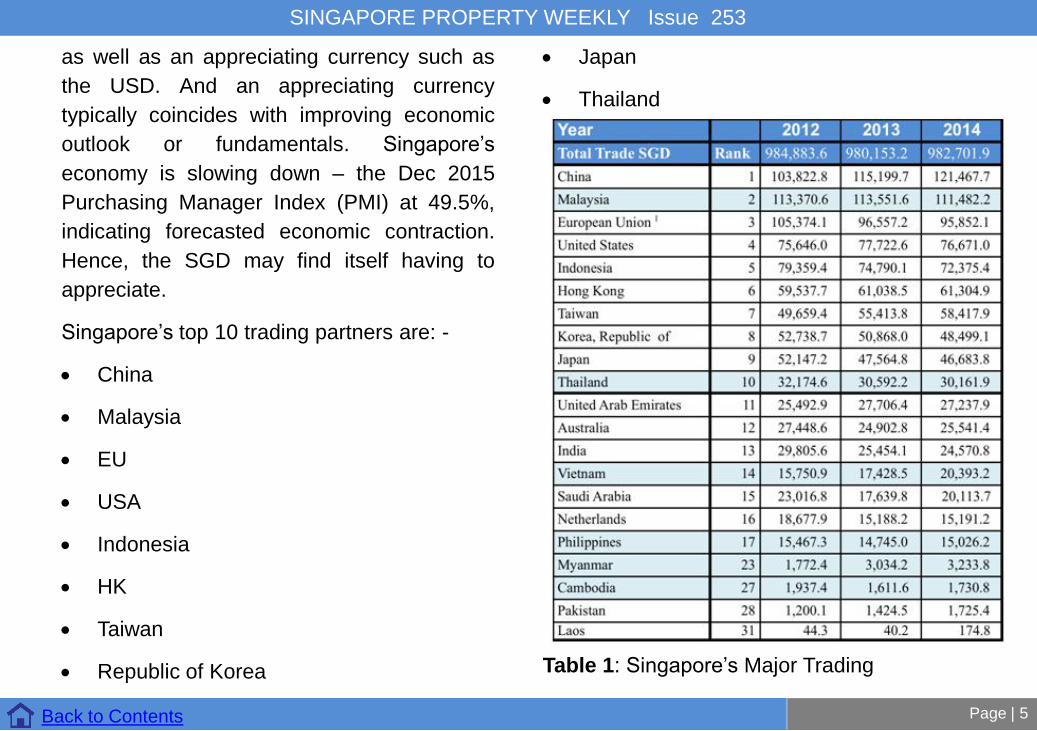

Singapore’s top 10 trading partners are: -

China

Malaysia

EU

USA

Indonesia

HK

Taiwan

Republic of Korea

Japan

Thailand

Table 1: Singapore’s Major Trading

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 6Back to Contents

Partners (IE Singapore, Singstats Nov 2015,iCompareLoan.com, in SGD)

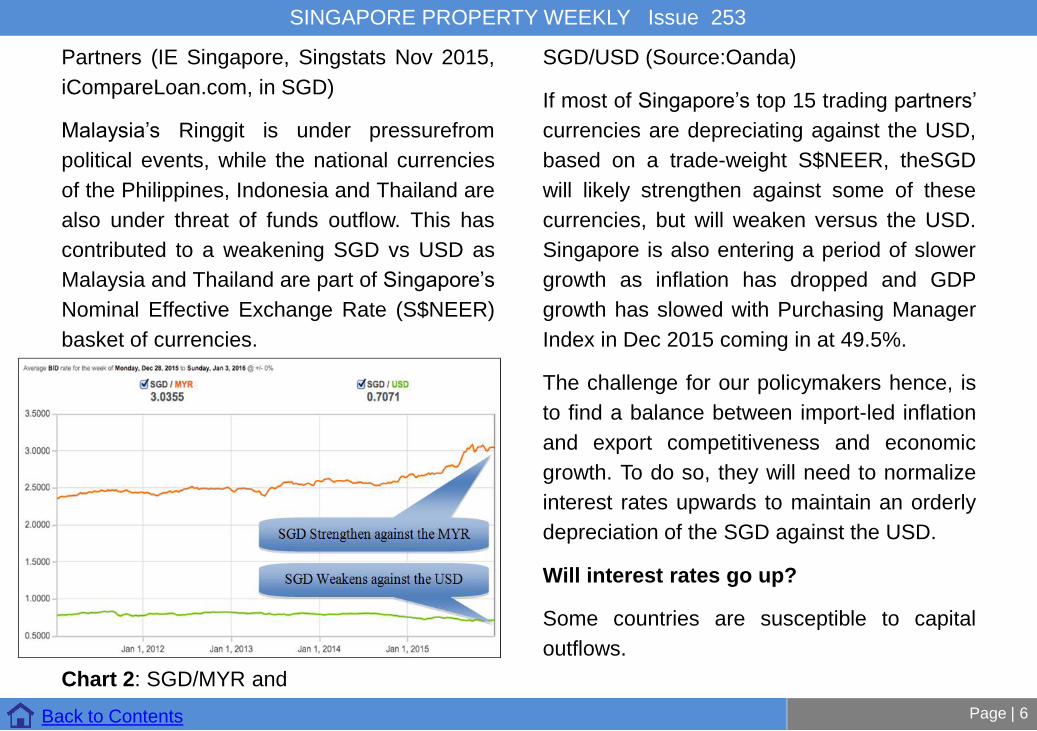

Malaysia’s Ringgit is under pressurefrompolitical events, while the national currenciesof the Philippines, Indonesia and Thailand arealso under threat of funds outflow. This hascontributed to a weakening SGD vs USD asMalaysia and Thailand are part of Singapore’sNominal Effective Exchange Rate (S$NEER)basket of currencies.

Chart 2: SGD/MYR and

SGD/USD (Source:Oanda)

If most of Singapore’s top 15 trading partners’

currencies are depreciating against the USD,based on a trade-weight S$NEER, theSGDwill likely strengthen against some of thesecurrencies, but will weaken versus the USD.Singapore is also entering a period of slowergrowth as inflation has dropped and GDPgrowth has slowed with Purchasing ManagerIndex in Dec 2015 coming in at 49.5%.

The challenge for our policymakers hence, isto find a balance between import-led inflationand export competitiveness and economicgrowth. To do so, they will need to normalizeinterest rates upwards to maintain an orderlydepreciation of the SGD against the USD.

Will interest rates go up?

Some countries are susceptible to capitaloutflows.

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 7Back to Contents

They will hence need to raise interest rates toslow the depreciation of their currency despitea slowing economy. This could lead toprolonged economic problems and corporatebankruptcies, which could in turn affectproperty prices.

Therefore, any property investor in the regionwill need to take a 5 to 10 years’ view of thisinvestment, as the US economic recoveryusually runs for 3 to 4 years.

Why do currencies come under threat?

Currencies usually come under threat when anumber of factors become present. Generally,they are: -

Low Foreign Reserves

Pegged exchange rate

High Debt

High sovereign debt denominated inforeign currencies

High household debt to GDP ratio

High corporate debt

High Budget Deficit

Trade Deficit

Slowing GDP growth

Inflated Asset prices

Stock markets

Property prices

Low Interest rates

Unstable political situation and socialtension

Countries with low foreign reserves, high foreign debt and a high budget deficit are most at risk of a weak currency.

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 8Back to Contents

A weakening economy with many of theabove attributes will suffer an extra blow fromcapital outflows when it needs it most.

An untimely exodus of funds from the countrywill weaken the currency causing interestrates to rise at a time when the economy canill afford it and cause a rapid deterioration ofits financial position.

High asset prices, such as an inflated stockmarket or property market would besusceptible to speculative attacks and

magnify the crisis.

Where are the bright spots?

Under-developed countries such asCambodia, Laos and Myanmar did notreceive a lot of capital inflow and hence arenot susceptible to capital outflow.

Cambodia, Laos and Myanmar are potential

high risk and high returns areas to put yourmoney. Nonetheless, their fiscal positions arepoor. The opening up of the economies ofCambodia and Myanmar are gooddevelopments.

Philippines is fast growing with a youngpopulation, but debt levels are high andexports are weak, although this is mitigatedby stable and strong remittances fromOverseas Foreign workers. I’d rate thismarket as Neutral to Positive.

Thailand’s economy is slowing down and mayenter a period of recession, but it has one ofthe best infrastructure for tourism, far aheadof the Philippines, Vietnam, Cambodia, Laosand Myanmar. Thailand has about US$100billion in reserves and a floating currency,hence it is unlikely to suffer from massivecurrency depreciation unless riots occur. I’d

rate this market as Neutral.

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 9Back to Contents

Malaysia does have good infrastructure, butits currency has already taken a beating andits political stability is in question. Malaysianonetheless is still competitive and runs atrade surplus. Despite its huge debt, Malaysiaalso has ample reserves and has raised itsinterest rates to mitigate currencydepreciation. I’d rate this market as Neutralwith selective buy potential due to its weakcurrency.

Vietnam is highly trade dependent and it haslow foreign reserves. It runs a huge budget

deficit, has huge debt coupled with risingcorporate Non-Performing Loans. I’d rate thismarket as Negative, i.e.stay away for a while.

SINGAPORE PROPERTY WEEKLY Issue 253

Singapore Property This Week

Page | 10Back to Contents

Residential

Global House Price Index up by 3% in2015

According to Knight Frank’s Global HousePrice Index, prices have increased by 3% in2015. Market experts believe that the lowinterest rate had influenced buyer’s

sentiments. Of the 55 countries accounted for

in the price index, 43 markets saw prices rise.This is up from the 10 countries recorded inthe aftermath of the Lehman’s collapse in2008. Based on the price index, Ukraine andGreece were the weakest housing marketslast year with price falls of 12% and 5%respectively. While the rate of quarterly pricedeclines of non-landed private homes have

moderated in Q4 2015 after 9 consecutivequarters of decline, Singapore is still one ofthe weakest performers, said Knight Frank’sAlice Tan. According to Knight Frank, pricesof Singapore’s non-landed private homes arelikely to decrease by 0.2% to 0.5% for Q1 thisyear.

(Source: Business Times)

Authorities believe it is premature to liftcooling measures

In his Budget Speech, Heng Swee Keat,Minister for Finance, said that it is too early tolift cooling measures given current marketconditions and price levels. Since the peak in2013, private home prices have fallen by8.4%.

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 11Back to Contents

Tay Huey Ying from JLL echoed thegovernment’s stance and said that anyinterference at this juncture would bepremature. Cushman & Wakefield’s ChristineLi added that if cooling measures are liftedprematurely, buyers may rush into the marketand property prices which are led by demandwill surge. Li also added that tweaking theadditional buyer’s stamp duty (ABSD) wouldnot serve the interest of the masses as theABSD helps to keep property prices low.Instead, changes to the ABSD will benefit

property developers, Singaporeans who canafford a second property, permanentresidents and foreigners.

(Source: Business Times)

Developers optimistic about selling outbefore ABSD deadlines

Despite the looming deadlines, developers

are optimistic that they will be able to sell outbefore the respective additional buyer’s

stamp duty (ABSD) deadlines. Not only so,developers have said that they would notneed to resort to massive price cuts in orderto meet the deadline. SingLand’s boutiqueproject, Mon Jervois and Pollen & Bleu, aswell as Alex Residences will be liable for theABSD of 10% with interest if there are anyunsold units by February, June andDecember 2017 respectively. As of Februarythis year, there are 61 unsold units at Mon

Jervois, 94 units at Pollen & Bleu and 13 unitsat Alex Residences. Another developer, CityDevelopment is also confident of clearing allits units at Jewel@Buangkok, Bartley Ridgeand The Venue Residences before theirdeadlines due to their prime location.According to the Business Times, developersmay set up a subsidiary or fund to buy the

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 12Back to Contents

unsold units if the loss in a stack sale to aninstitutional fund is more than developer’s

cost of paying an ABSD of 15% on thepurchase of unsold units. Thus, developersneed not resort to massive price cuts. Notonly so, the location and design of thedevelopment may also affect developer’s

ability to sell of the project.

(Source: Business Times)

Commercial

Q1 property investment sales set to fall tonear 7-year low

Investment sales of property or big tickettransactions of at least $10 million areexpected to fall to about $2 billion in Q1, saidSavills Singapore. This would be less thanhalf the $5 billion for Q4 last year and thelowest quarterly level since Q2 2009.According to Savills, it is expected that therewill also be a fall in Q1’s investments this year

from the $3.6 billion invested in Q1 2015.Steven Ming from Savills said that the sharpquarter-on-quarter fall will likely to be due to alack of big deals in the commercial propertysegment. Galven Tan from CBRE said thatinvestors are cautious in completing officetransactions as they anticipate that there willbe an increase in demand for office rental.Nonetheless Ming said that due to the declinein global interest rates, interest in commercialproperty deals may still pick up. On theresidential front, investment of sales haveincreased 12.9% to $1.5 billion in 1 Jan to 22March this year over Q4 2015. Not only so,the top bids by developers for threeresidential sites at state tenders in Q1 wereabove market expectations. This reflectsdevelopers’ optimism for 2017 when theprojects are expected to be marketed, addedSavills.

(Source: Business Times)

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 13Back to Contents

CaptiaLand enters co-working spacearena

In partnership with Collective Works,CapitaLand will turn the entire 12th floor atCapital Tower into co-working space thatspans about 22,000 sq ft. The space isexpected to house up to 250 companies.Collective Works, which is a co-workingspace operator, will manage the space.Grade-A office rents in Tanjong Pagar areestimated to range from $8 to $8.50 psf permonth. The average rent of remaining leasesexpiring at Capital Tower disclosed by the

CapitaLand Commercial Trust was $9.15 psfper month in Q4 last year. Wen Khai Mengfrom CapitaLand said that the co-workingspace is likely to appeal to fast-growingbusinesses, entrepreneurs and freelancerswho are seeking to rent fully functional, fitted-out office spaces under flexible lease terms.

(Source: Business Times)

SINGAPORE PROPERTY WEEKLY Issue 253

Page | 14Back to Contents

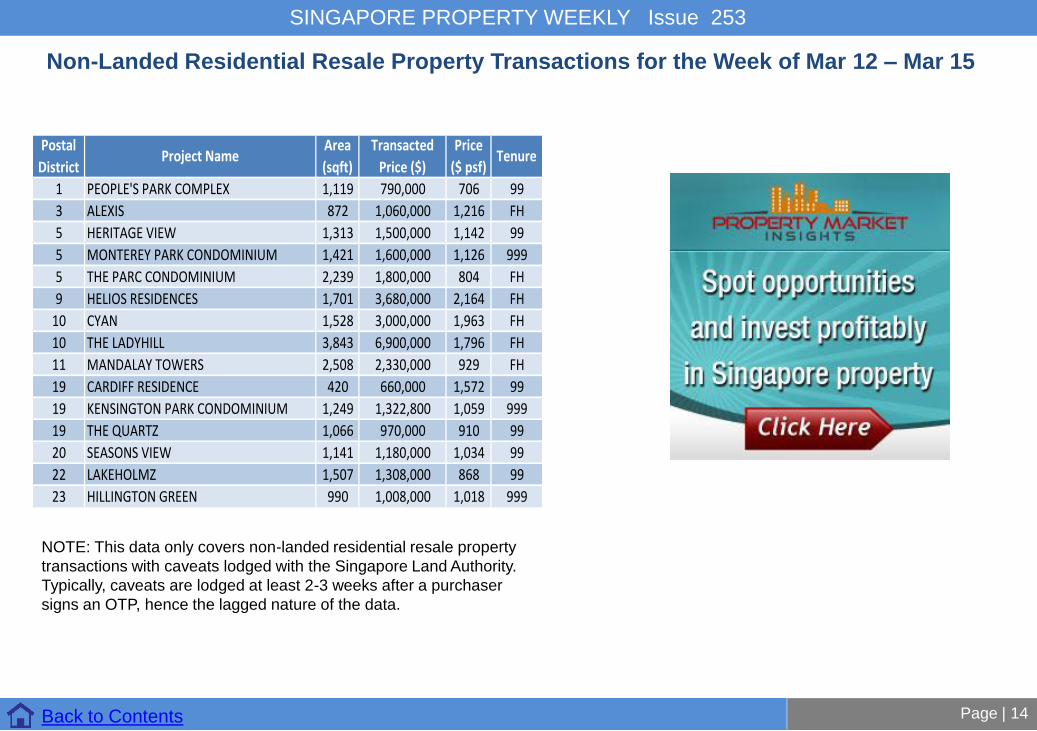

Non-Landed Residential Resale Property Transactions for the Week of Mar 12 – Mar 15

Postal

DistrictProject Name

Area

(sqft)

Transacted

Price ($)

Price

($ psf)Tenure

1 PEOPLE'S PARK COMPLEX 1,119 790,000 706 99

3 ALEXIS 872 1,060,000 1,216 FH

5 HERITAGE VIEW 1,313 1,500,000 1,142 99

5 MONTEREY PARK CONDOMINIUM 1,421 1,600,000 1,126 999

5 THE PARC CONDOMINIUM 2,239 1,800,000 804 FH

9 HELIOS RESIDENCES 1,701 3,680,000 2,164 FH

10 CYAN 1,528 3,000,000 1,963 FH

10 THE LADYHILL 3,843 6,900,000 1,796 FH

11 MANDALAY TOWERS 2,508 2,330,000 929 FH

19 CARDIFF RESIDENCE 420 660,000 1,572 99

19 KENSINGTON PARK CONDOMINIUM 1,249 1,322,800 1,059 999

19 THE QUARTZ 1,066 970,000 910 99

20 SEASONS VIEW 1,141 1,180,000 1,034 99

22 LAKEHOLMZ 1,507 1,308,000 868 99

23 HILLINGTON GREEN 990 1,008,000 1,018 999

NOTE: This data only covers non-landed residential resale property transactions with caveats lodged with the Singapore Land Authority. Typically, caveats are lodged at least 2-3 weeks after a purchaser signs an OTP, hence the lagged nature of the data.