Embed Size (px)

Citation preview

Journal of Business and Economics, ISSN 2155-7950, USA February 2014, Volume 5, No. 2, pp. 142-161 Academic Star Publishing Company, 2014 http://www.academicstar.us

142

Small and Medium Enterprises Landscape in Egypt:

New Facts from a New Dataset*

Hala El-Said, Mahmoud Al-Said, Chahir Zaki

(Faculty of Economics and Political Science, Cairo University, Cairo, Egypt)

Abstract: Small and medium sized enterprises (SMEs) have usually been perceived as a dynamic force for

sustained economic growth and job creation in developing countries. In Egypt, despite banking reforms that have

been launched in 2004, the ability of SMEs to more easily access suitable and sufficient means of finance has

always been considered a major obstacle facing many SMEs. For this reason, and in order to be able to extend the

financial services provided to this segment and increase the benefits of the banking reform, the Central Bank of

Egypt launched in December 2008 an initiative, as an integral part of the Second Phase of the Banking Sector

Reform Program (2008-2011), to enhance SMEs access to finance and banking services. In this paper, we present

a descriptive analysis of the SMEs landscape in Egypt relying on this extensive census. The main findings of the

census show that there is a high concentration of SMEs at different levels. First, the geographical distribution of

SMEs is significantly skewed since almost half of them are concentrated in three governorates Sharkeya, Cairo

and Gharbeya. Second, they are chiefly operating in two economic activities, namely manufacturing and trade.

Third, a very few firms are exporting. Finally, financial services seem to be under-utilized by SMEs as only 50

percent are dealing with banks and benefiting from an improved access to finance.

Key words: SMEs; access to finance; Egypt

JEL codes: D2, G21, P42

1. Introduction

Micro, small and medium sized enterprises (SMEs) have usually been perceived as a dynamic force for

sustained economic growth and job creation in developing countries. From a social viewpoint, SMEs secure

livelihood for a large and ever expanding segment of the population. In Egypt, there are around 2.5 Million SMEs

representing 75% of the total employed workforce and 99% of non-agricultural private sector establishments.

Despite their importance, they are still facing several problems, in particular access to finance which a typical

challenge in developing countries. In fact, 70% of non-OECD countries report SME financing gap compared to 30%

in OECD ones. Therefore, reducing this SMEs financing gap in low-income countries should increase the

* An empirical version of this paper entitled “Access to Finance and Financial Problems of SMEs: Evidence from Egypt” in the International Journal of Entrepreneurship and Small Business, Vol. 20, No. 3, pp. 286-309.

Hala El Said, Professor of Economics and Dean of the Faculty of Economics and Political Science, Cairo University; research areas: financial sector, privatization and economic reform. E-mail: [email protected].

Mahmoud Al-Said, Associate Professor of Statistics, Cairo University; research areas: statistics and quality control. E-mail: [email protected].

Chahir Zaki, Assistant Professor of Economics, Cairo University; research areas: international trade, modeling and macroeconomics. E-mail: [email protected].

Small and Medium Enterprises Landscape in Egypt: New Facts from a New Dataset

143

incentive of SMEs creation and consequently improve economic growth and increase job creation. In addition,

improving the access to finance of SMEs is significantly important in promoting entrepreneurship and innovation.

In Egypt, despite banking reforms that have been launched in 2004, the ability of SMEs to more easily access

suitable and sufficient means of finance has always been considered a major obstacle facing many SMEs (Egyptian

Banking Institute, 2009). It is worthy to mention that, from a supply point of view, the majority of banks are

becoming more risk averse towards SMEs, especially due to a wide spread notion that financing SMEs is risky and

that serving them requires high transaction costs which makes them less profitable than larger companies (El Said

et al., 2013).

For this reason, and in order to be able to extend the financial services provided to this segment and increase

the benefits of the banking reform, establishing a database for SMEs to serve bankers as well as policy makers

seems to be an important priority. Hence, the Central Bank of Egypt launched in December 2008 an initiative, as

an integral part of the Second Phase of the Banking Sector Reform Program (2008-2011), to enhance SMEs access

to finance and banking services. In this respect, and due to the importance of the availability of timely and

accurate information, the Central Bank of Egypt (CBE) and the Egyptian Banking Institute (EBI) commissioned

the Central Agency for Public Mobilization and Statistics (CAPMAS) to conduct an SME nation-wide census,

fully focusing on value added formal economic activities on a full census basis. The Center of Surveys and

Statistical Applications (CSSA) at the Faculty of Economics and Political Science, Cairo University undertook the

project on- site quality control. This survey includes quantitative and qualitative characteristics of each company

or unit. This includes identifying the number of employees, legal status, economic activity, level of exports, sales

turnover, invested capital and the problems facing each company in dealing with banks, etc.

The descriptive analysis of this paper is largely inspired from a companion paper (El-Said et al., 2013) in

which we conduct an empirical analysis of the determinants of access to finance of SMEs in Egypt. Yet, the

contribution of this paper is that it provides a much more detailed descriptive analysis at several fronts: access to

finance, exports, regional location, economic sectors and factors of production. The main findings of the census

show that there is a high concentration of SMEs at different levels. First, the geographical distribution of SMEs is

significantly skewed since almost half of them are concentrated in three governorates (Sharkeya, Cairo &

Gharbeya). Second, they are chiefly operating in two economic activities, namely manufacturing and trade. Third,

a very few firms are exporting. Finally, financial services seem to be under-utilized by those firms as only 50

percent are dealing with banks and benefiting from an improved access to finance. It is worthy to mention that

those financial services are also concentrated in the same governorates and the same economic activities that have

been mentioned above.

The paper is organized as follows: Section 2 presents some stylized facts regarding the banking sector reform

in Egypt. Section 3 shows the questionnaire design. Section 4 presents a landscape of SMEs characteristics using

the firm-level data that have been collected. Section 5 focuses on SMEs and their access to finance. Finally,

section 6 concludes and presents some policy implications.

2. Banking Reform in Egypt

The Central Bank of Egypt in 2004 adopted a reform program that aims at building solid infrastructure and

more efficient and sound banking sector. Although the global financial crisis led to many negative repercussions

on several world economies, the Egyptian banking sector weathered the negative repercussions due to the

Small and Medium Enterprises Landscape in Egypt: New Facts from a New Dataset

144

successful reform program that have launched in 2004. Indeed, as it was mentioned by the World Bank (2009)

“the Egyptian financial sector is the most far reaching, substantive and comprehensive drive toward financial

sector strengthening so far in Egypt-and indeed in any other country of the Middle East and North Africa region”.

This reform has been implemented in two phases. The first phase had three main pillars: first, strengthening

the legal, regulatory and supervisory framework; second, consolidating the banking sector and increasing private

participation within banking assets and finally the financial, operational and institutional restructuring of

public-sector banks. Those reforms led to a robust, solid and well capitalized banks (see Table 1), as banks

decreased from 57 to 39; assets increased by 88% to reach EGP 1.1 billion in 2008 up from EGP 0.57 billion in

2003; total deposits increased by 85% over the same period; capital adequacy ratio increased from 12.2% to reach

15.1% and total net worth increased by more than 100% from EGP 32 billion to EGP 75 billion.

Table 1 Banking Aggregates before and after 2004 Reform

LE million (as at June) 2003 2008 % change

Total Assets 577,938 1,083,311 + 87.7%

Total Deposits 403,144 747,199 + 85,3%

Loans & Discounts 284,722 401,425 + 41.2%

Capital & Reserves 29,960 53,436 +82.7%

Source: Central Bank of Egypt.

The second phase of the banking sector reform program that started in 2009 aims at deepening the Egyptian

banking sector and enhancing its efficiency and competitiveness through enhancing Access to Financial Services,

continuing the strengthening of the regulatory and supervisory framework through the implementation of Basel

II/III and enhancing the implementation of Corporate Governance rules and regulations. Those reforms increased

the loans-deposits ratio reaching 54%, average loans-GDP ratio reaching 49.4% and average deposits-GDP ratio

reaching 90%. Those figures are much higher than the world average in 2008.

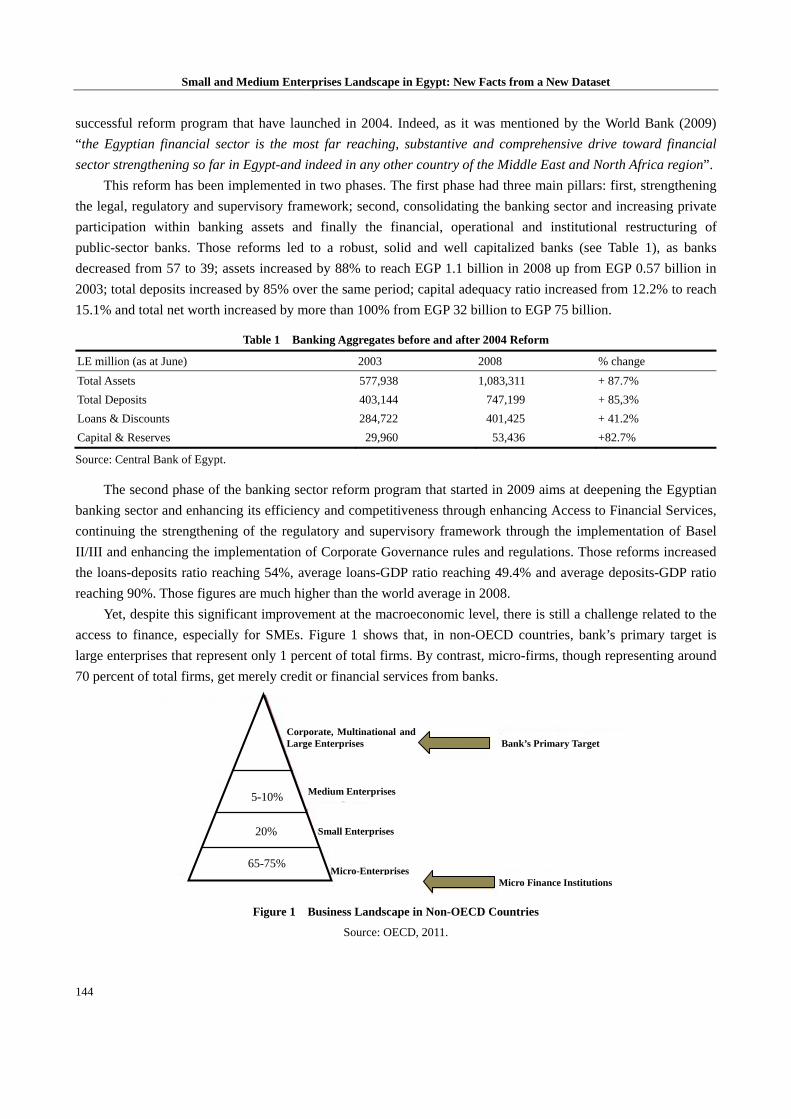

Yet, despite this significant improvement at the macroeconomic level, there is still a challenge related to the

access to finance, especially for SMEs. Figure 1 shows that, in non-OECD countries, bank’s primary target is

large enterprises that represent only 1 percent of total firms. By contrast, micro-firms, though representing around

70 percent of total firms, get merely credit or financial services from banks.

Figure 1 Business Landscape in Non-OECD Countries

Source: OECD, 2011.

Micro-Enterprises

Small Enterprises

1%

5-10%

20%

65-75%

Corporate, Multinational andLarge Enterprises Bank’s Primary Target

Medium Enterprises

Micro Finance Institutions

Small and Medium Enterprises Landscape in Egypt: New Facts from a New Dataset

145

For this reason, and in order to be able to extend the financial services provided to this segment and increase

the benefits of the banking reform, establishing a database for SMEs to serve bankers as well as policy makers

seems to be an important priority. Hence, as it was mentioned before, the Central Bank of Egypt launched in

December 2008 an initiative, as an integral part of the Second Phase of the Banking Sector Reform Program

(2008-2011), to enhance SMEs access to finance and banking services. The next section provides more details

about this census.

3. Questionnaire Design

3.1 Structure

The questionnaire includes four main categories of questions.

First, it contains some general information regarding the legal status of the firm (whether it is a partnership, a

limited liability firm, branch of a foreign firm, sole proprietorship, etc.). In addition, since only formal firms are

taken into account, the interviewee should mention the number and the date of his industrial and commercial

registration.

Second, it includes some information related to the firm endowments, such as the number of workers (less

than 20; from 20 to 34; from 35 to 50 and more than 51) and the value of the capital.

Third, the questionnaire is categorizing firms according to the sales turnover which is the variable banks

consider the most while giving loans. In addition, this section includes some questions showing whether the firm

exports or not, the destination of exports (Arab countries, African countries, other) and the share of exports to total

sales (less than 25%, from 25 to 50% and more than 50%).

Fourth, the questionnaire contains a final module on access to finance by asking the interviewee:

whether she/he deals with banks or not,

whether she/he benefits from some banking facilities or not,

whether she/he faces problems with banks or not and if yes, she has to determine the type of the problems

(high interests, commissions and administrative expenses; banks ask for a lot of collaterals; procedures are lengthy

and complicated; banks ask for a lot of documents; others)

3.2 Scope

The census covers all SMEs in Egypt, identified here as every company or economic activity:

That is formally registered: therefore we exclude informal firms which represent almost 20 percent in Egypt

That employs five employees or more.

That has a significant economic value added: thus activities of limited economic value added have been

excluded, namely Barber shops, beauty salons and kiosks were excluded from the survey.

In other words, three filters have been taken into account in order to include only registered firms with more

than 5 employees and having a significant value-added. Based on these criteria, the census ended-up by including

around 36,492 firms.

3.3 Methodology

First, it is worth to mention that the framework used is that developed by the Central Agency for Public

Mobilization and Statistics (CAPMAS) in 2006 adding new establishments and excluding activities of limited

economic value added. Second, the primary data was obtained through conducting face to face interviews with

SMEs, using a well-structured questionnaire designed jointly by Central Bank of Egypt (CBE)/Egyptian Banking

Small and Medium Enterprises Landscape in Egypt: New Facts from a New Dataset

146

Institute (EBI) committee in consultation with an experienced statistician to measure both quantitative and

qualitative factors. The census was done through seven phases to guarantee the quality of the collected data

Pre-testing the questionnaire: A pretest of the questionnaire was conducted to a sample of SMEs in “El

Qualiobia” governorate whereby some modifications and repositioning of sequence of questions was made

according to the pretest results.

Training of CAPMAS researchers: Extensive training sessions were conducted to all CAPMAS field

researchers to ensure their understanding of the questionnaire and the approach in conducting the interviews. The

training was conducted jointly by CAPMAS and the Center of Surveys and Statistical Applications (CSSA) at the

Faculty of Economics and Political Science under the supervision of CBE and EBI.

Pilot: After collecting the data of the pilot (that was conducted in “El-Sharkia” governorate in April 2010) the

data collected was analyzed, verified and validated, accordingly, some activities of limited economic value added

were excluded throughout the survey.

Collecting the data: Data was collected through face-to-face interviews conducted by CAPMAS researches

using the developed questionnaire.

Quality control: Two different quality control teams were assigned to ensure the validity and accuracy of the

data collection process

On-site QC: Undertaken by the (CSSA) that was responsible for monitoring and controlling the process of

data collection in the field on a daily basis.

Off-site QC: Undertaken by a joint team from CBE and EBI responsible for verification and quality

controlling the data entry process with random checks.

4. Landscape of SMEs in Egypt

4.1 Legal Form

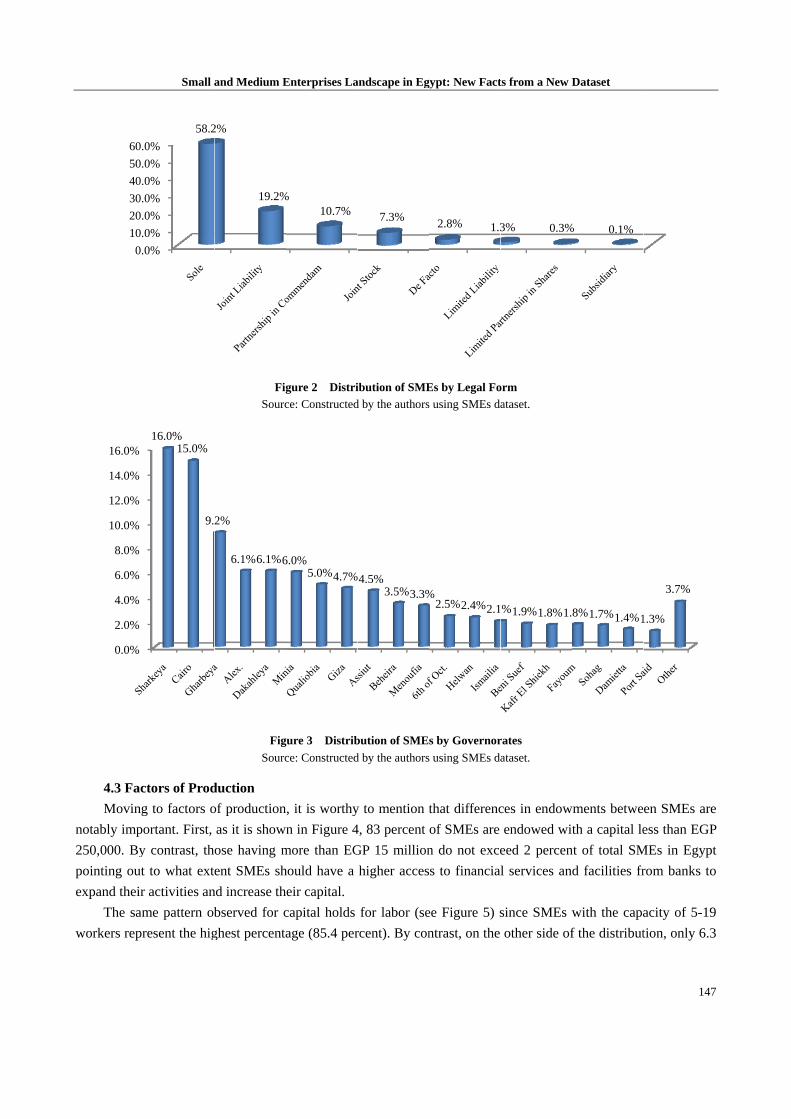

Figure 2 shows the distribution of SMEs according to the legal form. SMEs adopt chiefly a

sole-proprietorship (that represents almost 60 percent of total firms) given the fact that it is the easiest to be

created. Those firms are owned and run by one individual and in which there is no legal distinction between the

owner and the business. The owner receives all profits (subject to taxation specific to the business) and has

unlimited responsibility for all losses and debts. Its advantages are related to the fact that entrepreneurs have the

ability to limit risk to investors. Sole proprietorships also have the least government rules and regulations affecting

it which fosters their creation by entrepreneurs. The remaining 40 percent are distributed among joint liability,

partnership in commendams, joint stock, de facto, limited liability, limited partnership in shares and subsidiaries.

4.2 Geographical Location

It is worthy to note that SMEs are highly skewed at the geographical level since almost half of them is

concentrated in the three governorates of Sharkeya, Cairo and Gharbeya (see Figure 3). This may be explained by

higher externalities coming from other firms which are located in large governorates that are located in urban

regions. Similarly, access to road and to transportation of goods positively and significantly affects firms’

productivity as they allow firms to better produce and market their products or services to a wider scope of clients.

Finally, since other governorates have not a significant share of SMEs, more attention should be attribute to them

in order to improve their infrastructure and therefore to allow firms to be established there.

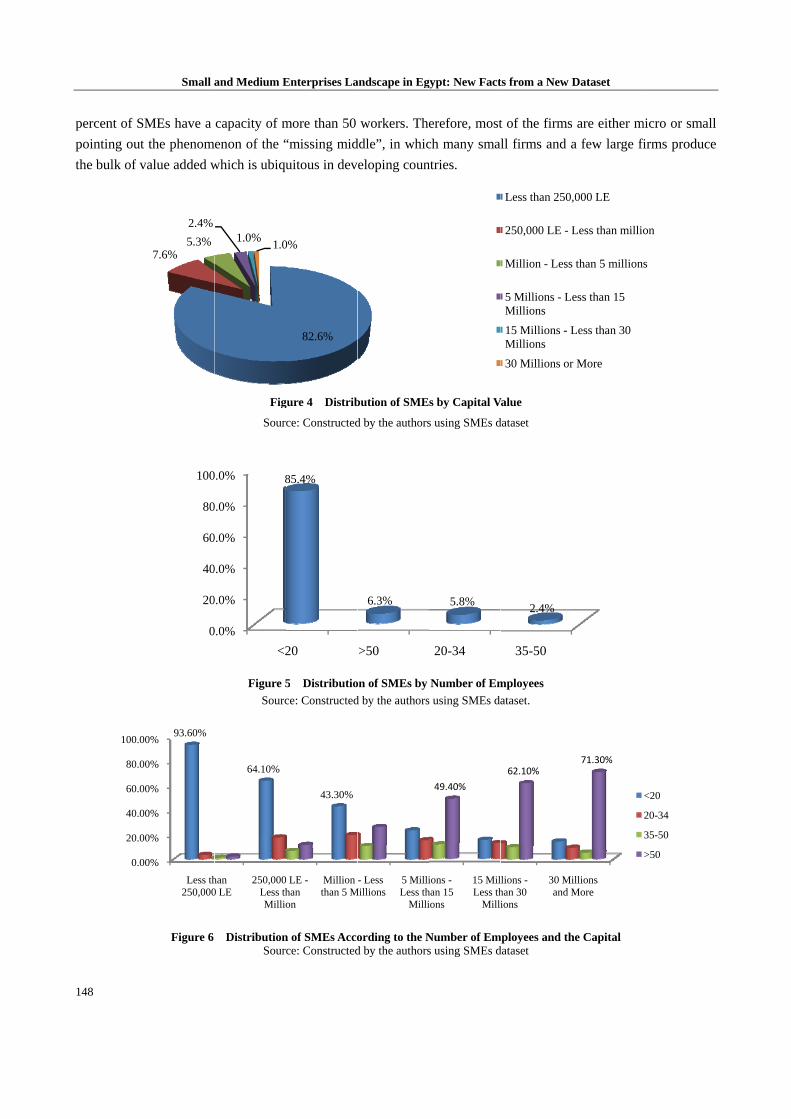

4.3 Fac

Moving

notably imp

250,000. By

pointing out

expand their

The sam

workers repr

0.

10.

20.

30.

40.

50.

60.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Small a

ctors of Prod

g to factors o

ortant. First,

y contrast, th

t to what ext

r activities an

me pattern ob

resent the hig

.0%

.0%

.0%

.0%

.0%

.0%

.0%

58.2

16.0%15.0%

9.

and Medium E

Fig

Sourc

Fig

Sourc

duction

of production

as it is show

ose having m

ent SMEs sh

nd increase th

bserved for c

ghest percenta

2%

19.2%

2%

6.1%6.1%6

Enterprises La

gure 2 Distri

ce: Constructed

gure 3 Distrib

ce: Constructed

n, it is worthy

n in Figure 4

more than EG

hould have a

eir capital.

capital holds

age (85.4 per

%10.7%

6.0%5.0%4.7%

andscape in Eg

ibution of SME

d by the authors

bution of SME

d by the authors

y to mention t

4, 83 percent

GP 15 million

higher acces

for labor (se

rcent). By con

7.3%

%4.5%3.5%3.3%

gypt: New Fact

Es by Legal Fo

s using SMEs da

s by Governor

s using SMEs da

that differenc

of SMEs are

n do not exce

s to financia

ee Figure 5) s

ntrast, on the

2.8% 1.3

%2.5%2.4%2.1

ts from a New D

orm

ataset.

rates

ataset.

ces in endow

endowed wi

eed 2 percen

l services an

since SMEs w

other side of

3% 0.3%

%1.9%1.8%1.

Dataset

wments betwe

th a capital le

nt of total SM

d facilities fr

with the capa

f the distribut

% 0.1%

8%1.7%1.4%1

147

en SMEs are

ess than EGP

MEs in Egypt

rom banks to

acity of 5-19

tion, only 6.3

1.3%

3.7%

7

e

P

t

o

9

3

148

percent of S

pointing out

the bulk of v

0.0

20.0

40.0

60.0

80.0

100.0

Small a

SMEs have a

t the phenom

value added w

Figure 6

7.6%5.3%

2.4%

0

20

40

60

80

100

00%

00%

00%

00%

00%

00%

Less th250,000

93.60%

and Medium E

capacity of m

menon of the “

which is ubiqu

Fig

Sour

Figure 5

Sourc

DistributionSour

1.0%1.0

0.0%

0.0%

0.0%

0.0%

0.0%

0.0%

<2

8

han 0 LE

250,000Less thMillio

64.10%

Enterprises La

more than 50

“missing mid

uitous in dev

gure 4 Distrib

ce: Constructed

5 Distributio

ce: Constructed

n of SMEs Accoce: Constructed

82.6%

0%

20

85.4%

0 LE -han on

Million than 5 M

43.30%

andscape in Eg

workers. The

ddle”, in whic

eloping coun

bution of SME

d by the authors

on of SMEs by

d by the authors

ording to the Nd by the authors

>50

6.3%

- Less Millions

5 MilliLess th

Milli

gypt: New Fact

erefore, most

ch many sma

ntries.

s by Capital V

s using SMEs d

Number of Em

s using SMEs da

Number of Ems using SMEs d

20-34

5.8%

ions -han 15 ions

15 MilLess th

Milli

49.40%

ts from a New D

t of the firms

ll firms and a

Value

dataset

mployees

ataset.

mployees and thdataset

Less than 250

250,000 LE - L

Million - Less

5 Millions - LMillions

15 Millions - LMillions

30 Millions or

35-50

2.4%

llions -han 30 ions

30 Miand M

62.10%

Dataset

s are either m

a few large fi

he Capital

,000 LE

Less than millio

s than 5 million

ess than 15

Less than 30

r More

illions More

71.30%

micro or small

firms produce

on

s

<20

20-34

35-50

>50

l

e

Figure

conclude tha

the coefficie

especially m

there are som

Table 2

Activities

Agriculture

Manufacturing

Trade

Food & Bever

Health

Construction &

Other

Source: Const

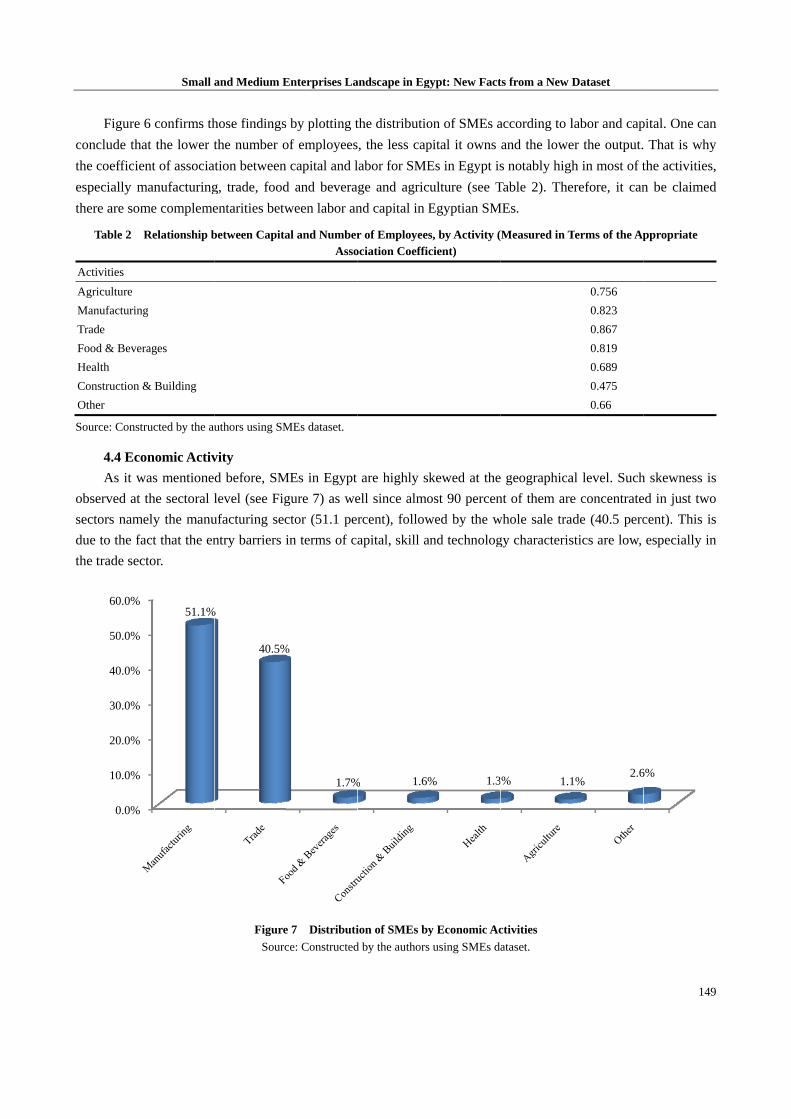

4.4 Eco

As it w

observed at

sectors nam

due to the fa

the trade sec

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Small a

6 confirms th

at the lower t

ent of associa

manufacturing

me compleme

Relationship b

g

rages

& Building

tructed by the au

onomic Activ

was mentione

the sectoral l

ely the manu

act that the en

ctor.

51.1%

and Medium E

hose findings

the number o

ation between

g, trade, food

entarities betw

between Capita

uthors using SM

vity

d before, SM

level (see Fig

ufacturing sec

ntry barriers i

Figure

Sourc

%

40.5%

Enterprises La

s by plotting t

of employees

n capital and l

d and bevera

ween labor an

al and NumberAsso

MEs dataset.

MEs in Egypt

gure 7) as we

ctor (51.1 per

in terms of ca

e 7 Distributi

ce: Constructed

%

1.7%

andscape in Eg

the distributio

s, the less cap

labor for SME

ge and agric

nd capital in E

r of Employeesociation Coeffic

are highly sk

ell since almo

rcent), follow

apital, skill a

ion of SMEs by

d by the authors

% 1.6%

gypt: New Fact

on of SMEs a

pital it owns

Es in Egypt is

ulture (see T

Egyptian SM

s, by Activity (cient)

kewed at the

ost 90 percen

wed by the w

and technolog

y Economic Ac

s using SMEs da

% 1.3

ts from a New D

according to l

and the lowe

s notably high

Table 2). The

MEs.

(Measured in T

e geographica

nt of them are

whole sale tra

gy characteris

ctivities

ataset.

% 1.1

Dataset

labor and cap

er the output.

h in most of t

erefore, it can

Terms of the Ap

0.756

0.823

0.867

0.819

0.689

0.475

0.66

al level. Such

e concentrate

ade (40.5 perc

stics are low,

1%2.6

149

pital. One can

That is why

the activities,

n be claimed

ppropriate

h skewness is

ed in just two

cent). This is

especially in

6%

9

n

y

,

d

s

o

s

n

150

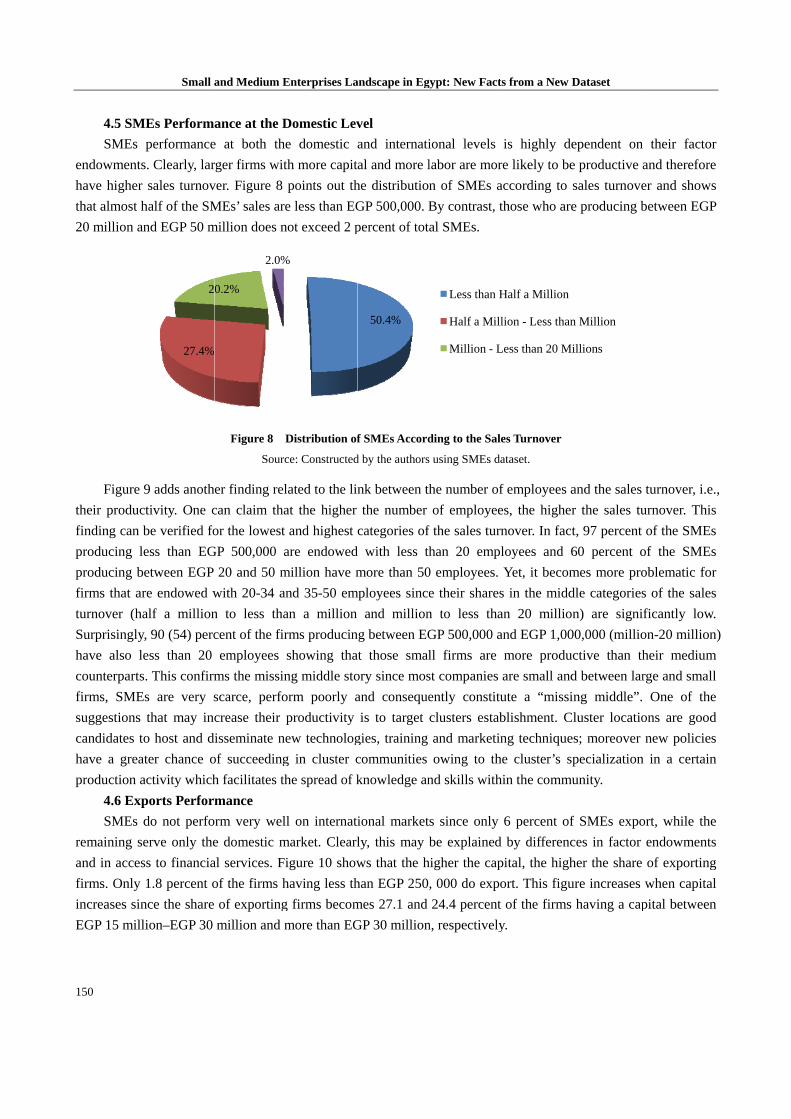

4.5 SM

SMEs

endowments

have higher

that almost h

20 million a

Figure

their produc

finding can b

producing l

producing b

firms that ar

turnover (ha

Surprisingly

have also l

counterparts

firms, SME

suggestions

candidates t

have a grea

production a

4.6 Exp

SMEs

remaining s

and in acces

firms. Only

increases sin

EGP 15 mill

Small a

MEs Perform

performance

s. Clearly, lar

sales turnov

half of the SM

and EGP 50 m

9 adds anoth

ctivity. One c

be verified fo

ess than EG

between EGP

re endowed w

alf a million

y, 90 (54) perc

ess than 20

s. This confirm

Es are very s

that may inc

o host and d

ater chance o

activity which

ports Perfor

do not perfo

erve only the

ss to financia

1.8 percent o

nce the share

lion–EGP 30

27.4%

2

and Medium E

ance at the D

e at both the

rger firms wit

ver. Figure 8

MEs’ sales are

million does n

Figure 8 D

Sourc

er finding rel

can claim tha

or the lowest

GP 500,000 a

20 and 50 m

with 20-34 an

n to less tha

cent of the fir

employees

ms the missin

scarce, perfo

crease their p

isseminate ne

of succeeding

h facilitates th

mance

rm very wel

e domestic m

al services. Fi

of the firms h

of exporting

million and m

0.2%

2.0%

Enterprises La

Domestic Lev

e domestic

th more capit

points out th

e less than EG

not exceed 2 p

Distribution of

ce: Constructed

lated to the lin

at the higher

and highest

are endowed

million have m

nd 35-50 em

an a million

rms producin

showing tha

ng middle sto

orm poorly a

productivity

ew technolog

g in cluster c

he spread of k

l on internati

market. Clearl

igure 10 show

having less th

g firms becom

more than EG

%

andscape in Eg

vel

and internati

al and more l

he distributio

GP 500,000. B

percent of tot

f SMEs Accord

d by the authors

nk between th

the number

categories of

d with less th

more than 50

mployees since

and million

ng between EG

at those smal

ory since mos

and conseque

is to target

gies, training

communities

knowledge an

ional market

ly, this may

ws that the h

han EGP 250

mes 27.1 and

GP 30 million

50.4%

gypt: New Fact

ional levels

labor are mor

n of SMEs a

By contrast, t

al SMEs.

ding to the Sal

s using SMEs da

he number of

of employee

f the sales tur

han 20 emp

0 employees.

e their shares

n to less tha

GP 500,000 a

ll firms are

st companies

ently constitu

clusters estab

and marketin

owing to th

nd skills with

s since only

be explained

higher the cap

, 000 do expo

24.4 percent

n, respectively

Less than H

Half a Mill

Million - L

ts from a New D

is highly de

re likely to be

according to

those who are

es Turnover

ataset.

f employees a

es, the higher

rnover. In fact

loyees and 6

Yet, it becom

s in the midd

an 20 millio

and EGP 1,00

more produ

are small and

ute a “missi

blishment. C

ng technique

he cluster’s s

hin the commu

6 percent of

d by differenc

pital, the high

ort. This figu

t of the firms

y.

Half a Million

lion - Less than

Less than 20 M

Dataset

ependent on

e productive a

sales turnove

e producing b

and the sales

r the sales tu

t, 97 percent

60 percent o

mes more pro

dle categories

n) are signi

00,000 (millio

uctive than th

d between lar

ing middle”.

Cluster locatio

es; moreover

pecialization

unity.

f SMEs expo

ces in factor

her the share

ure increases

having a cap

n Million

illions

their factor

and therefore

er and shows

between EGP

turnover, i.e.

urnover. This

of the SMEs

of the SMEs

oblematic for

s of the sales

ficantly low.

on-20 million

heir medium

rge and small

One of the

ons are good

new policies

n in a certain

ort, while the

endowments

of exporting

when capital

pital between

r

e

s

P

.,

s

s

s

r

s

.

n)

m

l

e

d

s

n

e

s

g

l

n

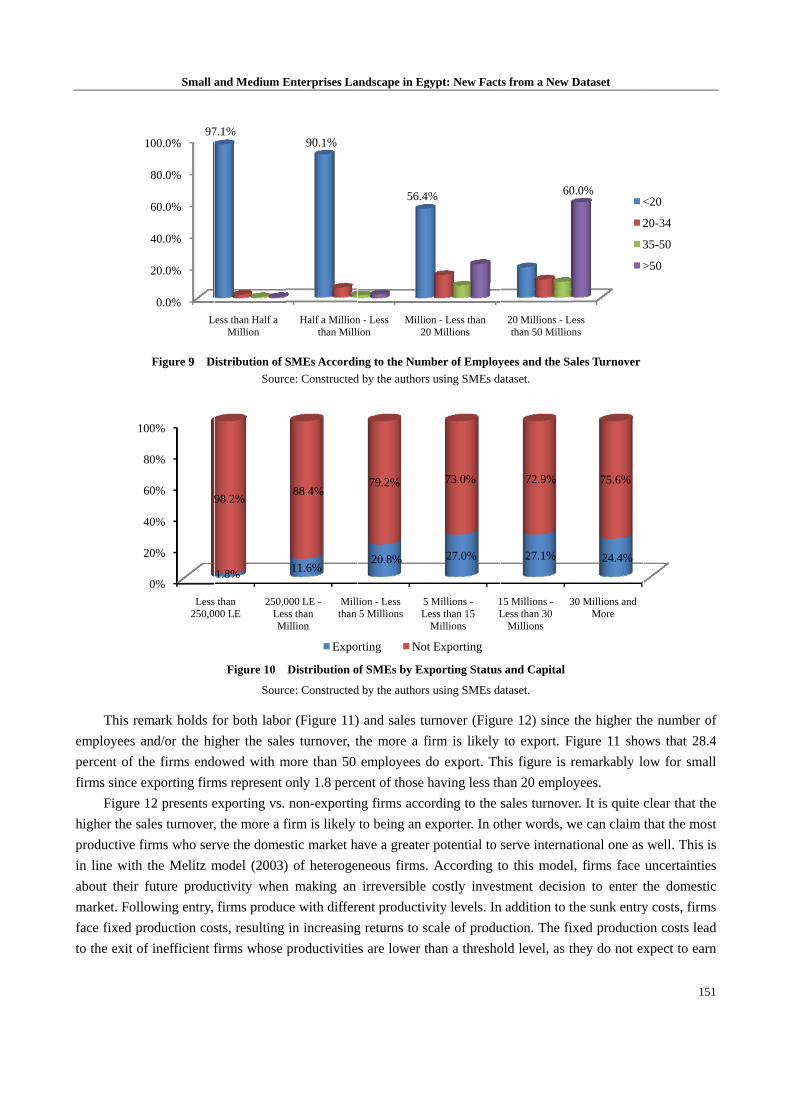

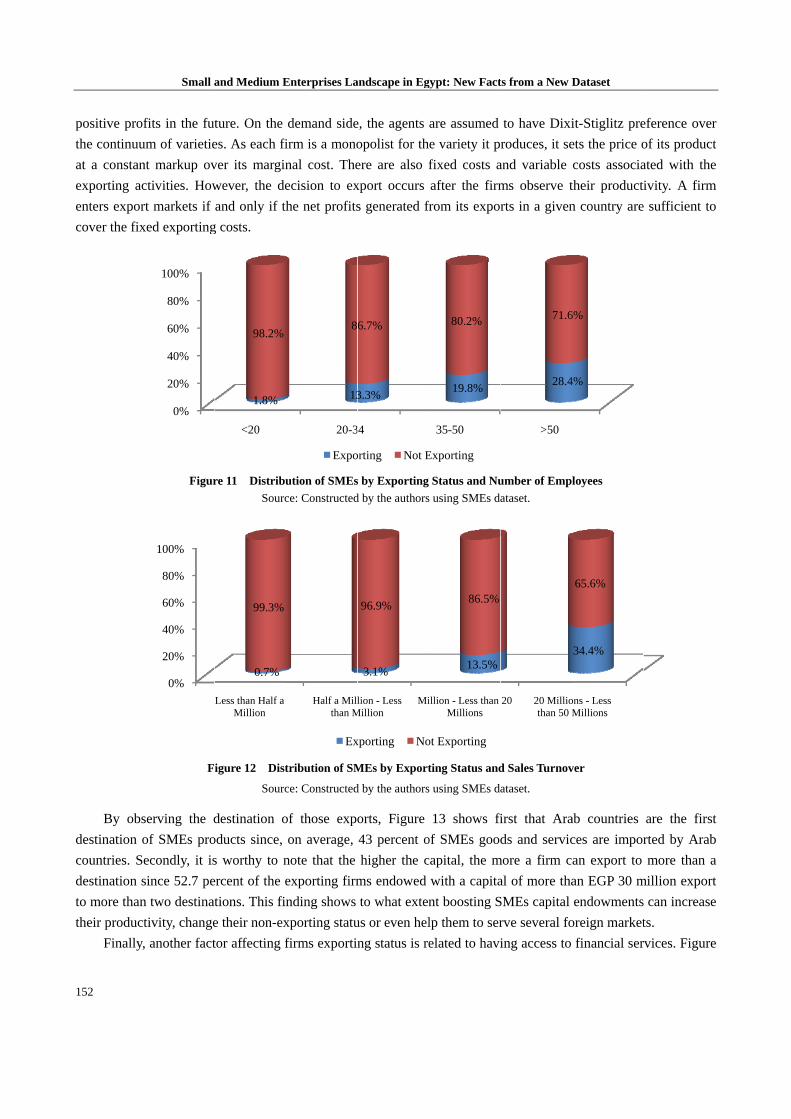

This re

employees a

percent of th

firms since e

Figure

higher the sa

productive f

in line with

about their

market. Foll

face fixed pr

to the exit o

1

Small a

Figure 9 D

emark holds f

and/or the hi

he firms end

exporting firm

12 presents e

ales turnover,

firms who ser

the Melitz m

future produ

lowing entry,

roduction cos

of inefficient f

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

L

97

0%

20%

40%

60%

80%

00%

Less250,0

9

and Medium E

istribution of S

Sourc

Figure 10

Sourc

for both labo

gher the sale

dowed with m

ms represent o

exporting vs.

, the more a f

rve the domes

model (2003)

uctivity when

firms produc

sts, resulting

firms whose

Less than Half a Million

7.1%

s than 00 LE

250,0LesM

1.8%

98.2%

Enterprises La

SMEs Accordi

ce: Constructed

Distribution o

ce: Constructed

r (Figure 11)

es turnover, t

more than 50

only 1.8 perc

non-exportin

firm is likely

stic market h

) of heteroge

n making an

ce with differ

in increasing

productivitie

Half a Millionthan Milli

90.1%

000 LE -ss than

Million

Millthan

11.6%

88.4%

Expo

andscape in Eg

ing to the Num

d by the authors

of SMEs by Ex

d by the authors

) and sales tu

the more a fi

employees d

cent of those h

ng firms acco

to being an e

have a greater

eneous firms.

irreversible

rent productiv

g returns to sc

s are lower th

n - Less ion

Millio20

56.4%

lion - Less 5 Millions

5 Le

20.8%

79.2%

orting Not

gypt: New Fact

mber of Employ

s using SMEs da

porting Status

s using SMEs da

urnover (Figu

firm is likely

do export. Th

having less th

ording to the

exporter. In ot

r potential to

According t

costly inves

vity levels. In

cale of produ

han a thresho

on - Less than 0 Millions

%

Millions -ess than 15 Millions

1L

27.0%

73.0%

t Exporting

ts from a New D

yees and the Sa

ataset.

s and Capital

ataset.

ure 12) since

to export. F

his figure is r

han 20 emplo

sales turnove

ther words, w

serve interna

to this model

stment decisi

n addition to t

uction. The fi

old level, as t

20 Millions - Lthan 50 Million

60

15 Millions -Less than 30

Millions

3

27.1%

72.9%

Dataset

ales Turnover

the higher th

Figure 11 sho

remarkably lo

oyees.

er. It is quite

we can claim

ational one as

l, firms face

on to enter t

the sunk entry

ixed producti

they do not ex

ess ns

0.0%<

2

3

>

30 Millions and More

24.4%

75.6%

151

he number of

ows that 28.4

ow for small

clear that the

that the most

well. This is

uncertainties

the domestic

y costs, firms

on costs lead

xpect to earn

<20

20-34

35-50

>50

f

4

l

e

t

s

s

c

s

d

n

152

positive pro

the continuu

at a constan

exporting ac

enters expor

cover the fix

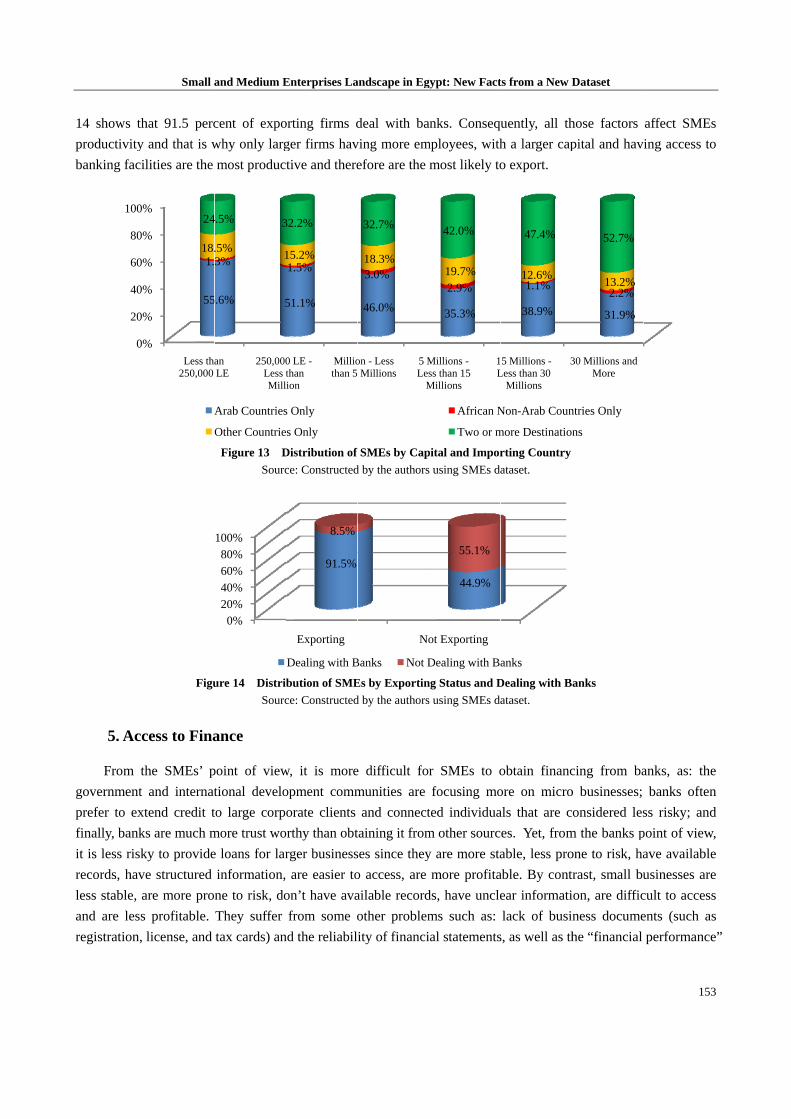

By obs

destination o

countries. S

destination s

to more than

their produc

Finally,

Small a

fits in the fut

um of varietie

nt markup ov

ctivities. How

rt markets if

xed exporting

Figur

F

serving the d

of SMEs pro

econdly, it is

since 52.7 pe

n two destinat

tivity, change

, another fact

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

and Medium E

ture. On the

es. As each fi

ver its margin

wever, the de

and only if th

g costs.

re 11 Distribu

Sourc

igure 12 Dist

Sourc

destination o

oducts since,

s worthy to n

ercent of the e

tions. This fin

e their non-ex

tor affecting f

<20

1.8%

98.2%

Less than Half a Million

0.7%

99.3%

Enterprises La

demand side

irm is a mono

nal cost. The

ecision to ex

he net profits

ution of SMEs

ce: Constructed

tribution of SM

ce: Constructed

of those expo

on average,

note that the

exporting firm

nding shows

xporting statu

firms exportin

20-3

13

8

Expo

Half a Millthan M

Ex

andscape in Eg

e, the agents

opolist for th

ere are also f

xport occurs

s generated fr

s by Exporting

d by the authors

MEs by Export

d by the authors

orts, Figure

43 percent o

higher the c

ms endowed

to what exten

us or even hel

ng status is re

4

3.3%

6.7%

orting Not E

lion - Less Million

Mi

3.1%

96.9%

xporting No

gypt: New Fact

are assumed

e variety it p

fixed costs a

after the firm

from its expor

Status and Nu

s using SMEs da

ting Status and

s using SMEs da

13 shows fi

of SMEs good

capital, the m

with a capita

nt boosting S

lp them to ser

elated to havi

35-50

19.8%

80.2%

Exporting

illion - Less than Millions

13.5%

86.5%

ot Exporting

ts from a New D

to have Dixi

roduces, it se

and variable

ms observe t

rts in a given

umber of Emp

ataset.

d Sales Turnov

ataset.

first that Ara

ds and servic

more a firm c

al of more tha

SMEs capital

rve several fo

ing access to

>50

28.4

71.6

20 20 Milliothan 50 M

Dataset

it-Stiglitz pre

ets the price o

costs associa

their product

n country are

loyees

ver

ab countries

ces are impor

an export to

an EGP 30 m

endowments

oreign market

financial ser

4%

6%

ons - Less Millions

34.4%

65.6%

eference over

of its product

ated with the

ivity. A firm

e sufficient to

are the first

rted by Arab

more than a

million export

s can increase

ts.

rvices. Figure

r

t

e

m

o

t

b

a

t

e

e

14 shows th

productivity

banking faci

5. Acc

From t

government

prefer to ex

finally, bank

it is less risk

records, hav

less stable, a

and are less

registration,

0%

20%

40%

60%

80%

100%

Small a

hat 91.5 perc

y and that is w

ilities are the

Figu

cess to Fina

the SMEs’ p

and internat

xtend credit t

ks are much m

ky to provide

ve structured

are more pro

s profitable.

license, and

%

%

%

%

%

%

Less tha250,000

55

1.18.

24

A

and Medium E

cent of expo

why only larg

most produc

Figure 13 D

Sourc

ure 14 Distri

Sourc

ance

point of view

tional develo

to large corp

more trust wo

e loans for lar

information,

ne to risk, do

They suffer

tax cards) an

an LE

250,000Less tMill

.6% 5

3%.5%

1

4.5% 3

Arab Countries

Other Countrie

0%20%

40%

60%

80%

100%

Enterprises La

orting firms d

ger firms hav

tive and there

Distribution of

ce: Constructed

bution of SME

ce: Constructed

w, it is more

opment comm

orate clients

orthy than obt

rger business

are easier to

on’t have ava

from some o

nd the reliabil

0 LE -than ion

Milliothan 5

51.1%

1.5%15.2%

32.2%

s Only

es Only

Exporting

91.5%

8.5%

Dealing with B

andscape in Eg

deal with ba

ving more em

efore are the

f SMEs by Cap

d by the authors

Es by Exportin

d by the authors

e difficult fo

munities are

and connect

taining it from

ses since they

o access, are

ailable record

other problem

ity of financi

on - Less Millions

5 MLes

M

46.0%

3.0%18.3%

32.7%

No

Banks Not D

gypt: New Fact

anks. Consequ

mployees, with

most likely to

pital and Impor

s using SMEs da

ng Status and D

s using SMEs da

r SMEs to o

focusing mo

ted individua

m other sourc

y are more sta

more profita

ds, have uncle

ms such as:

ial statements

Millions -ss than 15 Millions

1L

35.3%

2.9%19.7%

42.0%

African N

Two or m

ot Exporting

44.9%

55.1%

Dealing with B

ts from a New D

uently, all th

h a larger cap

o export.

rting Country

ataset.

Dealing with B

ataset.

obtain financ

ore on micro

als that are c

es. Yet, from

able, less pro

able. By cont

ear informati

lack of busi

s, as well as th

5 Millions -Less than 30

Millions

3

38.9%

1.1%12.6%

47.4%

Non-Arab Coun

more Destinatio

anks

Dataset

hose factors

pital and hav

anks

cing from ba

o businesses;

onsidered les

m the banks p

one to risk, ha

trast, small bu

ion, are diffic

ness docume

he “financial

30 Millions and More

31.9%

2.2%13.2%

52.7%

ntries Only

ns

153

affect SMEs

ing access to

anks, as: the

banks often

ss risky; and

point of view,

ave available

usinesses are

cult to access

ents (such as

performance

3

s

o

e

n

d

,

e

e

s

s

e”

154

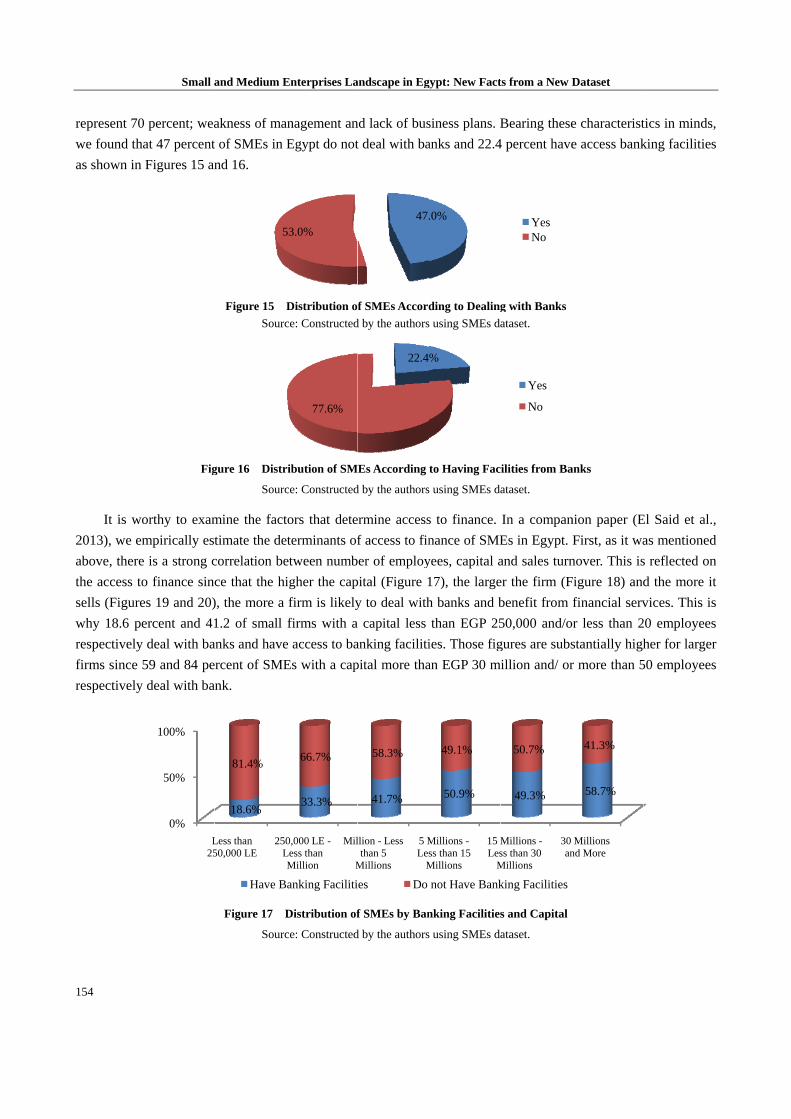

represent 70

we found th

as shown in

It is wo

2013), we em

above, there

the access to

sells (Figure

why 18.6 pe

respectively

firms since 5

respectively

Small a

0 percent; wea

at 47 percent

Figures 15 an

Fig

orthy to exam

mpirically est

e is a strong c

o finance sin

es 19 and 20)

ercent and 41

deal with ba

59 and 84 pe

deal with ba

0%

50%

100%

L25

and Medium E

akness of ma

t of SMEs in

nd 16.

Figure 15

Sourc

gure 16 Distr

Sourc

mine the fact

timate the de

correlation be

ce that the hi

), the more a

1.2 of small

anks and have

ercent of SME

ank.

Figure 17 D

Sourc

5

Less than 50,000 LE

250L

18.6%

81.4%

Have B

Enterprises La

anagement an

Egypt do not

Distribution o

ce: Constructed

ribution of SM

ce: Constructed

tors that dete

eterminants of

etween numb

igher the cap

firm is likely

firms with a

e access to ba

Es with a cap

Distribution of

ce: Constructed

53.0%

77.6%

0,000 LE -Less than Million

Mil

M

33.3%

66.7%

Banking Faciliti

andscape in Eg

nd lack of bus

t deal with ba

f SMEs Accord

d by the authors

MEs According

d by the authors

ermine access

f access to fin

ber of employ

pital (Figure 1

y to deal with

a capital less

anking faciliti

pital more tha

f SMEs by Ban

d by the authors

47.

22.4

llion - Less than 5

Millions

5 MLes

M

41.7%

58.3%

ies Do

gypt: New Fact

siness plans. B

anks and 22.4

ding to Dealing

s using SMEs da

to Having Fac

s using SMEs da

s to finance.

nance of SME

yees, capital a

17), the large

h banks and b

than EGP 25

ies. Those fig

an EGP 30 m

nking Facilities

s using SMEs da

.0%

%

Millions -ss than 15 Millions

15 MLes

M

50.9%

49.1%

not Have Bank

ts from a New D

Bearing these

4 percent have

g with Banks

ataset.

cilities from Ba

ataset.

In a compan

Es in Egypt.

and sales turn

er the firm (F

benefit from

50,000 and/o

gures are subs

million and/ or

s and Capital

ataset.

YesNo

Yes

No

Millions -ss than 30 Millions

30 an

49.3%

50.7%

king Facilities

Dataset

e characterist

e access bank

anks

nion paper (E

First, as it wa

nover. This is

Figure 18) and

financial serv

or less than 2

stantially high

r more than 5

Millions nd More

58.7%

41.3%

tics in minds,

king facilities

El Said et al.,

as mentioned

s reflected on

d the more it

vices. This is

20 employees

her for larger

50 employees

,

s

,

d

n

t

s

s

r

s

Small a

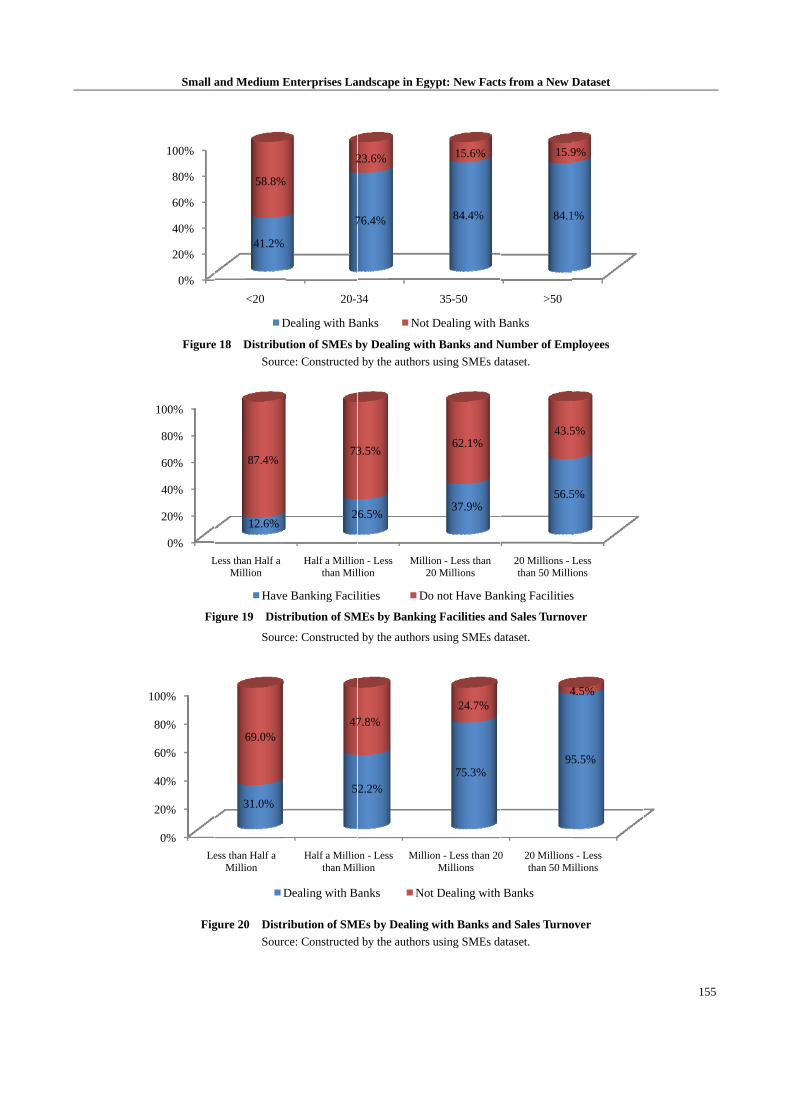

Figure

Fi

Fig

0%

20%

40%

60%

80%

100%

0%

20%

40%

60%

80%

100%

L

0%

20%

40%

60%

80%

100%

Le

and Medium E

e 18 Distribut

Sourc

igure 19 Dist

Sourc

gure 20 Distr

Sourc

<20

41.2%

58.8%

D

Less than Half a Million

12.6%

87.4%

Have

ess than Half a Million

31.0%

69.0%

D

Enterprises La

tion of SMEs b

ce: Constructed

ribution of SM

ce: Constructed

ribution of SM

ce: Constructed

20-3

7

2

Dealing with Ba

Half a Milliothan Mil

2

73

e Banking Facil

Half a Milliothan Mil

5

47

Dealing with B

andscape in Eg

by Dealing wit

d by the authors

MEs by Bankin

d by the authors

MEs by Dealing

d by the authors

34

76.4%

23.6%

anks Not

on - Less llion

Milli2

6.5%

3.5%

lities Do

on - Less llion

Milli

2.2%

7.8%

anks No

gypt: New Fact

h Banks and N

s using SMEs da

ng Facilities an

s using SMEs da

with Banks an

s using SMEs da

35-50

84.4%

15.6%

t Dealing with B

ion - Less than 20 Millions

37.9%

62.1%

o not Have Ban

ion - Less than 20Millions

75.3%

24.7%

ot Dealing with

ts from a New D

Number of Em

ataset.

d Sales Turnov

ataset.

nd Sales Turno

ataset.

>50

84.1

15.9

Banks

20 Millions -than 50 Milli

56.5

43.5

nking Facilities

0 20 Millionsthan 50 Mi

95

4

Banks

Dataset

ployees

ver

over

1%

9%

Less ions

5%

5%

s

s - Less illions

5.5%

4.5%

155

5

156

Numero

likely to hav

countries as

SMEs in non

Africa, this

financially c

bank standp

high interest

SMEs opera

not have leg

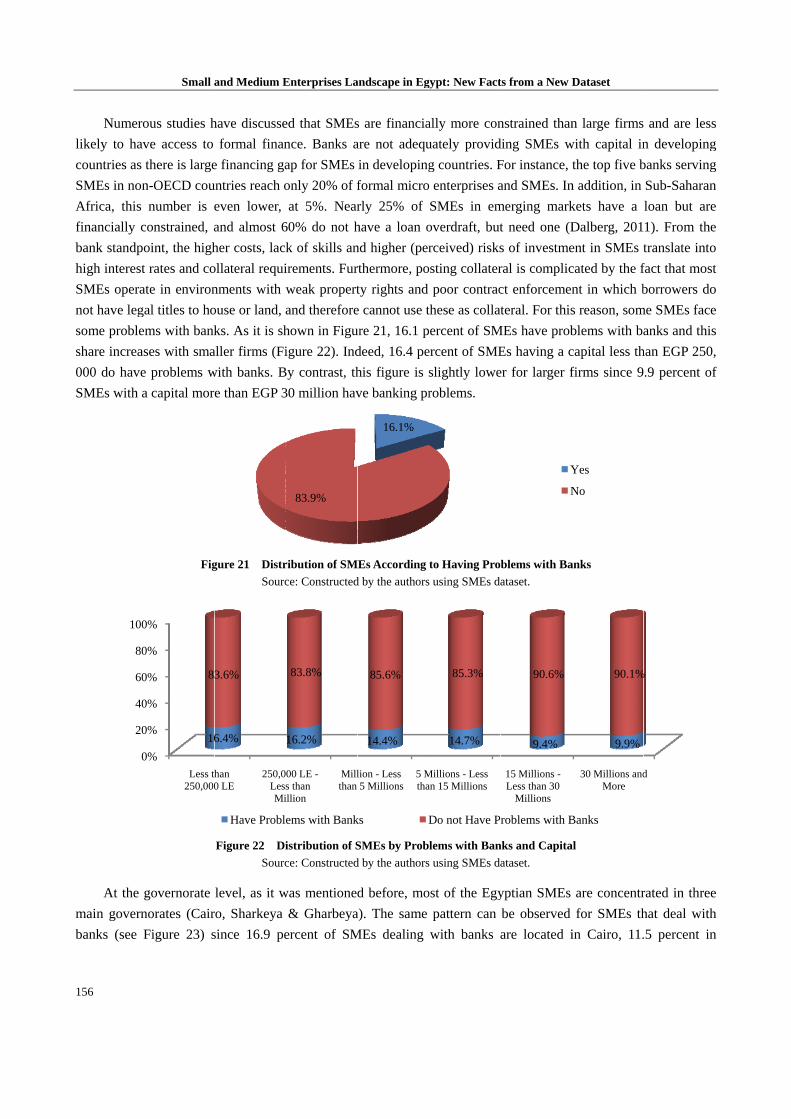

some proble

share increa

000 do have

SMEs with a

At the

main govern

banks (see

0

20

40

60

80

100

Small a

ous studies h

ve access to

there is large

n-OECD cou

number is e

constrained, a

oint, the high

t rates and co

ate in environ

gal titles to ho

ems with bank

ases with sma

e problems w

a capital mor

Fig

governorate

norates (Cair

Figure 23) s

0%

0%

0%

0%

0%

0%

Less th250,000

16

8

and Medium E

have discusse

formal finan

e financing ga

untries reach o

even lower,

and almost 6

her costs, lack

ollateral requi

nments with w

ouse or land, a

ks. As it is sh

aller firms (Fi

with banks. B

e than EGP 3

gure 21 Distr

Sourc

Figure 22 Di

Sourc

level, as it w

ro, Sharkeya

since 16.9 pe

han 0 LE

250,0LessMi

6.4%

3.6%

Have Proble

Enterprises La

ed that SMEs

nce. Banks a

ap for SMEs

only 20% of f

at 5%. Near

60% do not h

k of skills an

irements. Fur

weak propert

and therefore

hown in Figu

igure 22). Ind

By contrast, th

30 million hav

ribution of SM

ce: Constructed

istribution of S

ce: Constructed

was mentioned

& Gharbeya

ercent of SM

83.9%

00 LE -s than illion

Millthan

16.2%

83.8%

ems with Bank

andscape in Eg

s are financia

are not adequ

in developing

formal micro

rly 25% of

have a loan o

nd higher (per

rthermore, po

ty rights and

e cannot use t

ure 21, 16.1 p

deed, 16.4 pe

his figure is s

ve banking pr

MEs According

d by the authors

SMEs by Prob

d by the authors

d before, mo

a). The same

MEs dealing

16.1%

lion - Less 5 Millions

5 Mtha

14.4%

85.6%

ks D

gypt: New Fact

ally more con

uately provid

g countries. F

o enterprises a

SMEs in em

overdraft, but

rceived) risks

osting collater

poor contrac

these as collat

percent of SM

ercent of SME

slightly lowe

roblems.

to Having Pro

s using SMEs da

lems with Ban

s using SMEs da

ost of the Egy

pattern can

with banks a

Millions - Less an 15 Millions

14.7%

85.3%

Do not Have P

ts from a New D

nstrained than

ding SMEs w

For instance,

and SMEs. In

merging mark

t need one (D

s of investme

ral is complic

ct enforcemen

teral. For this

MEs have prob

Es having a c

er for larger f

blems with Ba

ataset.

nks and Capita

ataset.

yptian SMEs

be observed

are located i

Y

N

15 Millions -Less than 30

Millions

9.4%

90.6%

roblems with B

Dataset

n large firms

with capital in

the top five b

n addition, in

kets have a

Dalberg, 201

ent in SMEs t

cated by the f

nt in which b

s reason, som

blems with ba

capital less th

firms since 9

anks

al

are concentr

for SMEs th

in Cairo, 11.

Yes

No

30 Millions andMore

9.9%

90.1%

Banks

and are less

n developing

banks serving

Sub-Saharan

loan but are

1). From the

translate into

fact that most

borrowers do

me SMEs face

anks and this

han EGP 250,

.9 percent of

rated in three

hat deal with

.5 percent in

d

%

s

g

g

n

e

e

o

t

o

e

s

,

f

e

h

n

Small and Medium Enterprises Landscape in Egypt: New Facts from a New Dataset

157

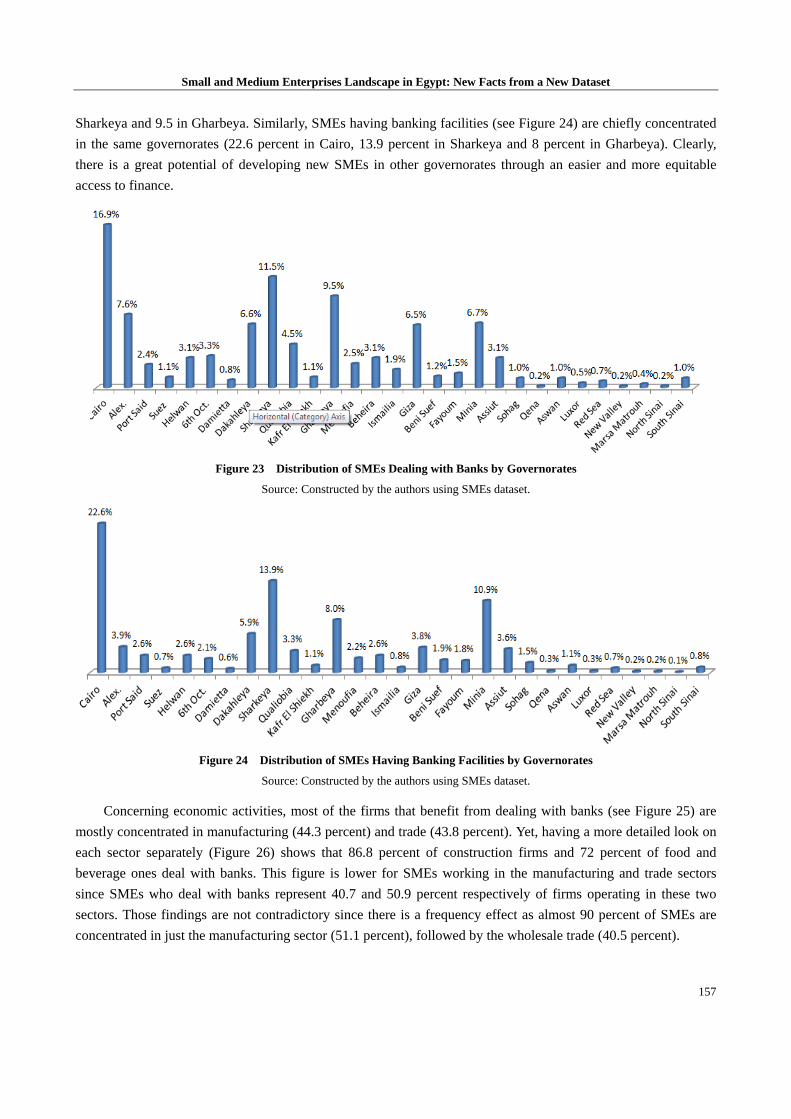

Sharkeya and 9.5 in Gharbeya. Similarly, SMEs having banking facilities (see Figure 24) are chiefly concentrated

in the same governorates (22.6 percent in Cairo, 13.9 percent in Sharkeya and 8 percent in Gharbeya). Clearly,

there is a great potential of developing new SMEs in other governorates through an easier and more equitable

access to finance.

Figure 23 Distribution of SMEs Dealing with Banks by Governorates

Source: Constructed by the authors using SMEs dataset.

Figure 24 Distribution of SMEs Having Banking Facilities by Governorates

Source: Constructed by the authors using SMEs dataset.

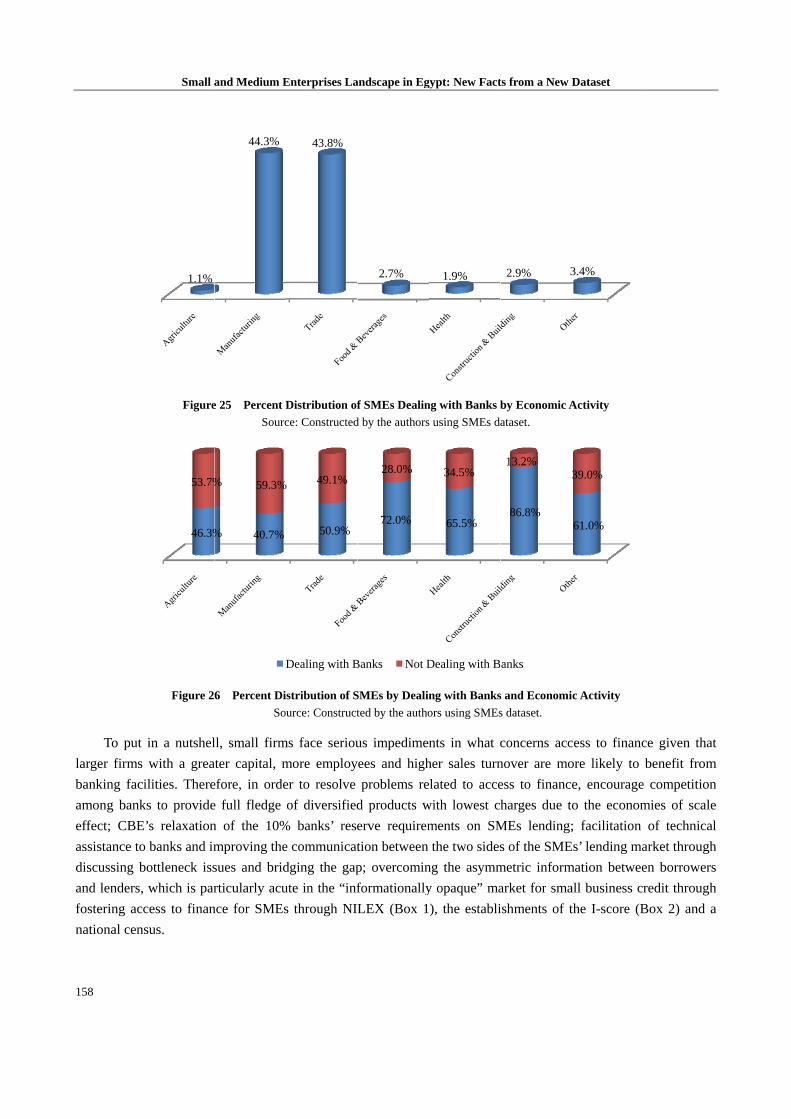

Concerning economic activities, most of the firms that benefit from dealing with banks (see Figure 25) are

mostly concentrated in manufacturing (44.3 percent) and trade (43.8 percent). Yet, having a more detailed look on

each sector separately (Figure 26) shows that 86.8 percent of construction firms and 72 percent of food and

beverage ones deal with banks. This figure is lower for SMEs working in the manufacturing and trade sectors

since SMEs who deal with banks represent 40.7 and 50.9 percent respectively of firms operating in these two

sectors. Those findings are not contradictory since there is a frequency effect as almost 90 percent of SMEs are

concentrated in just the manufacturing sector (51.1 percent), followed by the wholesale trade (40.5 percent).

158

To put

larger firms

banking fac

among bank

effect; CBE

assistance to

discussing b

and lenders,

fostering ac

national cen

Small a

Figure

Figure 2

in a nutshel

with a grea

ilities. There

ks to provide

E’s relaxation

o banks and im

bottleneck iss

, which is par

cess to finan

nsus.

1.1%

46.3%

53.7%

and Medium E

e 25 Percent D

Sourc

6 Percent Di

So

ll, small firm

ater capital, m

efore, in orde

e full fledge

n of the 10%

mproving the

sues and brid

rticularly acu

nce for SMEs

44.3%

% 40.7%

% 59.3%

D

Enterprises La

Distribution of

ce: Constructed

istribution of S

urce: Construct

ms face seriou

more employ

er to resolve

of diversified

% banks’ rese

e communicat

dging the gap

ute in the “inf

s through NI

43.8%

50.9%

% 49.1%

Dealing with B

andscape in Eg

f SMEs Dealin

d by the authors

SMEs by Dealin

ted by the autho

us impedimen

yees and high

problems re

d products w

erve requirem

tion between

p; overcomin

formationally

LEX (Box 1

2.7%

72.0%

28.0%

Banks Not D

gypt: New Fact

ng with Banks b

s using SMEs da

ng with Banks

ors using SMEs

nts in what c

her sales turn

elated to acce

with lowest ch

ments on SM

the two sides

ng the asymm

y opaque” ma

), the establi

1.9%

65.5%

34.5%

Dealing with B

ts from a New D

by Economic A

ataset.

s and Economi

s dataset.

concerns acc

nover are mo

ess to finance

harges due to

MEs lending;

s of the SME

metric inform

arket for sma

ishments of t

2.9% 3

86.8%

13.2%

anks

Dataset

Activity

ic Activity

cess to financ

ore likely to

e, encourage

o the econom

; facilitation

Es’ lending ma

mation betwee

all business cr

the I-score (B

3.4%

61.0%

39.0%

ce given that

benefit from

e competition

mies of scale

of technical

arket through

en borrowers

redit through

Box 2) and a

t

m

n

e

l

h

s

h

a

Small and Medium Enterprises Landscape in Egypt: New Facts from a New Dataset

159

Box 2: Egyptian Credit Bureau “I-Score” The Egyptian Credit Bureau “I-Score” maintains a database of credit information for SMEs and consumers. The first credit bureau in Egypt, which demonstrates how a private credit bureau can be set up in a relatively short time when all stakeholder interests are aligned and the project has backing of the authorities. The Credit Bureau has been established under the name of the Egyptian Credit Bureau “Estealam”. The first general assembly meeting was held on September 5th, 2005. 25 banks in addition to the Social Fund for Development contributed in the company, with an issued capital of 30 million Egyptian pounds distributed to seven million and five hundred thousand shares, the value of each share of four pounds (all the shares in cash). The founders and subscribers have paid the 25% of the nominal value of the shares upon subscription and completed the paid up capital in February 2007. The purpose of the company is to provide information services and credit classification. It includes work in the following areas:

Gathering all information about customers, whether associated with credit companies and financial institutions, retailers and credit provided by banks or other views from all available sources of information.

Creating certified official records of that information with the company, analyzing the data and classifying it.

Creating indicators of credit quality for debtors whether individuals or institutions, making it possible for them to form a sound credit history.

Providing financial advice and practical solutions, all of the specialized counseling to individuals or institutions who want to improve the level of credit ratings, or those who want to improve the financial instrument or who want to build a credit history on a sound basis to start by a specific institution (with the exception of legal advice).

The sale of information services and products associated service and other new services to all beneficiaries in Egypt and in a manner that does not conflict with the provisions of secret bank accounts.

Carrying out the work of the agency in the field of information and credit classification of enterprises or companies linked to their work with the company subject to the provisions of laws, regulations and decisions applicable licensing condition for the exercise of such activities.

Impact of I-Score:

I-Score led the process of the creation of the borrower data bank with Unique ID (GT 5.7 Million).

Significant increase in number of credit facilities/loans data base size (GT 14.3 Million).

Catalyst for banks/lenders to improve their data quality, revision of internal lending policies/procedures leading to new avenues to grow credit/improved profitability and advanced skill sets.

Contribution to increased awareness among lenders on data quality in acquisition and management.

Catalyst for active credit growth with prudence and confidence by providing a unified and robust borrower database across the lending community

For more information, please check www.i-score.com.eg

Box 1: NILEX NILEX is the Egyptian Exchange’ market for growing medium and small companies, which offers an appropriate, secure, yet flexible regulatory framework, for both companies and investors, together with a streamlined admission process. It supports the capital raising activities of small and mid cap developing companies. Its advantage is not only limited to providing finance, but companies can access to long term capital for the expansion of their businesses. It supports promising sectors in the economy which suffers from finance obstacles; and it also provides opportunity for investors to diversify their portfolios by investing in high growth companies. NILEX Benefits can be summarized in the following:

Unlimited Long-term Finance

Cheap Financing cost

Relaxed Rules & Regulation

Dedicated Funds to ensure liquidity

Full Government Support

Lower Listing Fees (0.5 per thousand of the capital)

Local & Foreign investors’ Interest For more information, please check: www.nilex.egyptse.com/ar/

Small and Medium Enterprises Landscape in Egypt: New Facts from a New Dataset

160

6. Conclusion and Policy Implications

Small and medium sized enterprises (SMEs) have usually been perceived as a dynamic force for sustained

economic growth and job creation in developing countries. In Egypt, despite banking reforms that have been

launched in 2004, the ability of SMEs to more easily access suitable and sufficient means of finance has always

been considered a major obstacle facing many SMEs. For this reason, and in order to be able to extend the

financial services provided to this segment and increase the benefits of the banking reform, the Central Bank of

Egypt launched in December 2008 an initiative, as an integral part of the Second Phase of the Banking Sector

Reform Program (2008-2011), to enhance SMEs access to finance and banking services. In this paper, we present

a descriptive analysis of the SMEs landscape in Egypt relying on this extensive census. The main findings of the

census show that there is a high concentration of SMEs at different levels. First, the geographical distribution of

SMEs is significantly skewed since almost half of them are concentrated in three governorates (Cairo, Sharqiya &

Gharbeya). Second, they are chiefly operating in two economic activities, namely manufacturing and trade. Third,

a very few firms are exporting. Finally, financial services seem to be under-utilized by SMEs as only 50 percent

are dealing with banks and benefiting from an improved access to finance.

From a policy implication standpoint, there is a need for strategic economic reforms to bring Egypt’s

economic condition into vitality and promote investment, especially for SMEs through:

Improvements in the legislative infrastructure, several rules and regulations associated with bankruptcy,

creditor capacity to take fast possession of collateral in case of default. In addition, there is an urgent need to

speed up the process of establishing collateral registries which should aim at building electronic registers and

streamlining registration process.

Encouraging banks to build on their expertise in matchmaking their clients in different stages of value chain

(linkages)

A need for updating financial method for financial reporting (e.g., standardized template)

Changing the Mindset

Enhancing Entrepreneurship Education

It is worth to mention that this last point is crucial to improve SME performance in Egypt. Indeed, the role of

entrepreneurship has become increasingly apparent in economic and social development. Economically,

entrepreneurship stimulates markets. The formation of new business leads to job creation and has a multiplying

effect on the economy. Socially, entrepreneurship empowers citizens, generates innovation and changes mindsets.

These changes have the potential to integrate developing countries into the global economy. Thus,

entrepreneurship is described as a potential driver to support the economic growth, since it is important for

productivity, innovation and employment. Accordingly, it has been a policy goal of many developed countries to

develop a culture of entrepreneurial thinking. This can be done through providing appropriate enabling

environment via integrating entrepreneurship into education systems, learning process, technical assistance,

legislation and integration among all stakeholders.

Access to finance of small and medium enterprises is extremely important in promoting entrepreneurship and

innovation as well improving the state of the national economy in Egypt. Accordingly helping those who decide to

start their small enterprise in acquiring necessary entrepreneurial and managerial competencies is essential in

order to ensure their success. Being aware of the importance of entrepreneurship development, EBI SME unit is

Small and Medium Enterprises Landscape in Egypt: New Facts from a New Dataset

161

providing several training packages for Small and medium business owners who need to enhance their

understanding of dealing with and satisfying the requirements of banks.

References:

Central Bank of Egypt (2010). “Banking Reform in Egypt”, mimeo. Cinar E. M., Evcimen G. and Kaytaz M. (1987). “A case study on the growth potential of small scale manufacturing enterprises in

Bursa, Turkey”, METU Studies in Development, Vol. 24, No. 2, pp. 123-146. Cinar E. M., Evcimen G. and Kaytaz M. (1988). “The present day status of small scale industries (Sanatkar) in Bursa, Turkey”,

International Journal of Middle Eastern Studies, Vol. 20, pp. 287-301. Doing Business (2011). “Making a difference for entrepreneurs”, IFC and the World Bank, Washington D.C. Egyptian Banking Institute (2010). “A facilitating access to finance for SMEs”, mimeo, February. El-Hamidi F. and C. Baslevent (2010). “The gendered aspects of MSEs in MENA: Evidence from Egypt and Turkey”, Economic

Research Forum (ERF) Working Paper No. 535. El-Gamal M. A., El-Megharbel N. and Inanoglu H. (2001). “Beyond credit: A taxonomy of SMEs and financing methods for Arab

countries”, ECES Working Paper Series No. 57, Egypt, The Egyptian Center for Economic Studies (ECES), May. El-Hamidi F. (2011). “How do women entrepreneurs perform? Empirical evidence from Egypt”, Economic Research Forum (ERF)

Working Paper No. 621. El-Kabbani R. N. and Kalhoefer C. (2011). “Financing resources for Egyptian small and medium enterprises”, Working Papers 28,

The German University in Cairo, Faculty of Management Technology. El-Mahdi A. (2006). “The changing economic environment and the development of the micro and small enterprises in Egypt 2006”,

Economic Research Forum (ERF) Working Paper No. 0706. El-Said H., Al Said M. and Zaki C. (2013). “Access to Finance and Financial Problems of SMEs: Evidence from Egypt”

International Journal of Small Business and Entrepreneurship, Vol. 20, No. 3, pp. 286-309. El-Said H. (2006). “Access to finance: Forms of financing for SMEs in Egypt”, Centranl Bank of Egypt and the Egyptian Banking

Institute, mimeo. Erzan R. and Filiztekin A. (2005). “Does size matter in growth, productivity, employment, and vulnerability/flexibility in Turkish

manufacturing?”, Turkish Studies, Vol. 6, No. 1, pp. 113-126. Evcimen G., Kaytaz M. and Cinar E. M. (1991). “Subcontracting, growth and capital accumulation in small-scale firms in the textile

industry in Turkey”, The Journal of Development Studies, Vol. 28, No. 1, pp. 130-149. Hamdouch B. et al. (2004). “Dynamisme de la Micro et Petite Entreprise au Maroc”, ERF Research Report Series No. 0419. OECD (2011). “Entrepreneurship at a glance 2011”, OECD Publishing, available online at:

http://dx.doi.org/10.1787/9789264097711-en. Semsa Ozar (2004). “Micro and small enterprises in Turkey: Uneasy development”, Research Report Series No. 0420. The World Bank (2010). “Access to finance and economic growth in Egypt”, led by Sahar Nasr, Washington D.C..