Embed Size (px)

Citation preview

Sovereign spreads in the euro area. Which Prospects for a Eurobond?

Carlo A. Favero, A. Missale

QFIN Colloquia

April 2011

The Relevant Stylized Facts

Assess the degree of integration in the European government bond market by examining the behavior of interest rate differentials.

Examine the potential for a larger European market to better compete with the US market, by considering the liquidity premium on German relative to US bonds.

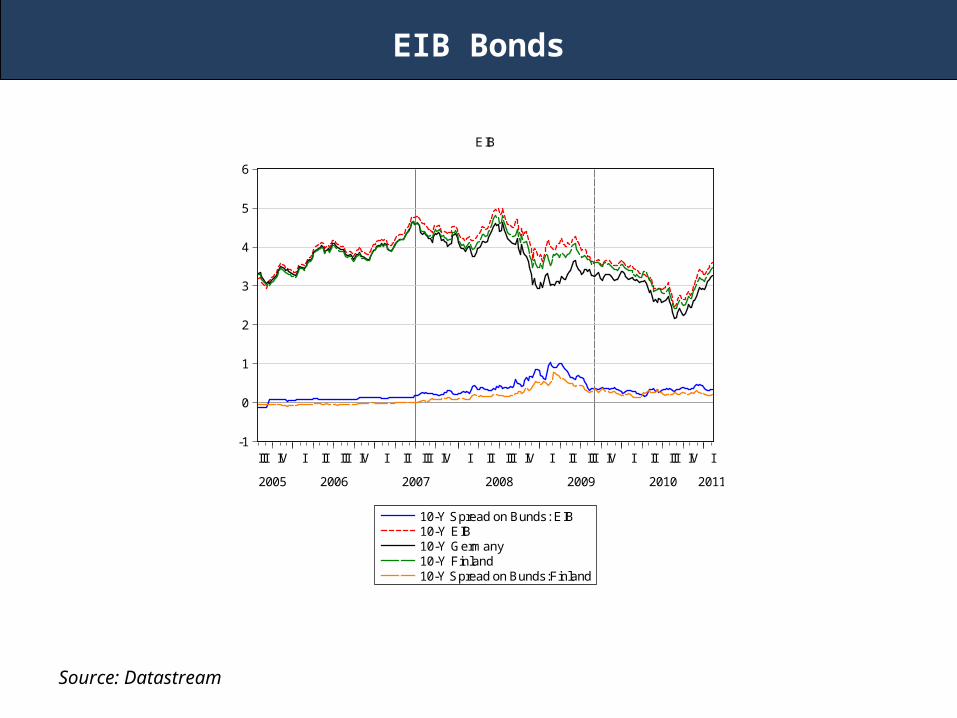

Look at the interest rate on bonds issued by the European Investment Bank (EIB) to evaluate the performance of a bond issued by an EU Institution.

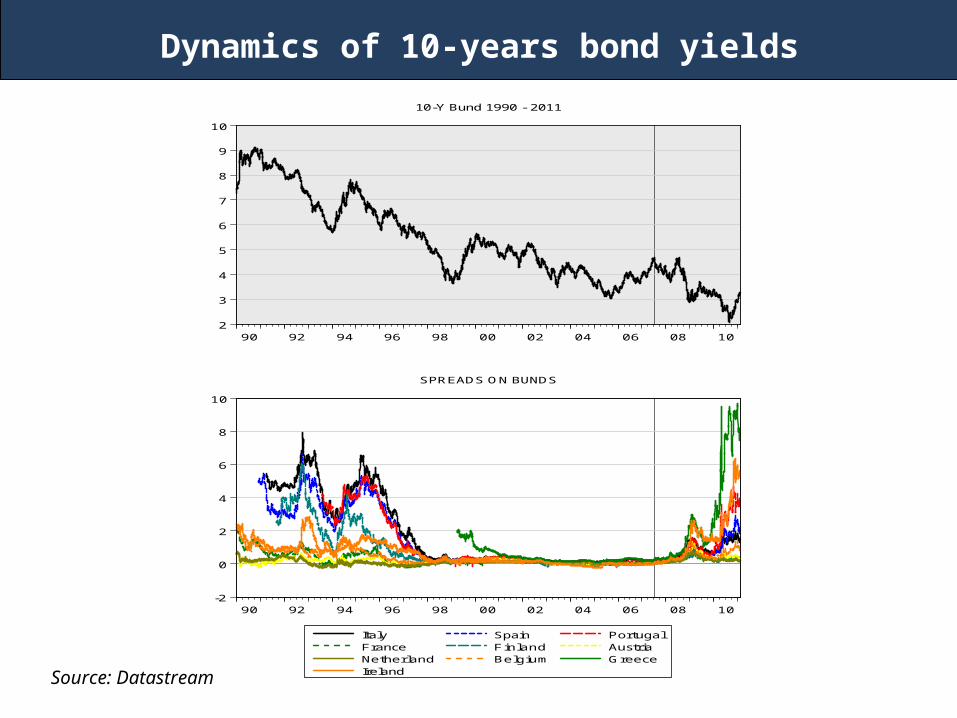

Dynamics of 10-years bond yields

Source: Datastream

2

3

4

5

6

7

8

9

10

90 92 94 96 98 00 02 04 06 08 10

10-Y Bund 1990 - 2011

-2

0

2

4

6

8

10

90 92 94 96 98 00 02 04 06 08 10

Italy Spain PortugalFrance Finland AustriaNetherland Belgium GreeceIreland

SPREADS ON BUNDS

Spread of 10-years government bond yields vs Bund

After only one year from the introduction of the European Monetary Union (EMU) in 1998 the market for fixed-income government securities was taking the form of an almost perfectly integrated market

The spreads between high yield Member States (Portugal, Italy, Spain) moved from the high peak of 300 basis points in the pre-EMU to less than 30 basis points of post-EURO

The differentials among different national bonds remained low, although not negligible, for almost ten years

With the burst of the subprime financial and the euro debt crisis the differential become sizable

Credit and Liquidity Risks and Expectations of Exchange Rate Depreciation

Interest rates of government bonds (same maturity and currency) may differ because of different credit and liquidity risks and expectations of exchange rate depreciation

Credit risk depends on the probability that an issuer may not honour its obligations (default risk premia). This is related to fiscal fundamentals of each country (deficit and debt) and to GDP growth rates, but also to external factors (global risks, “flight to quality” effects)

Liquidity risk depends on the total amount of volumes traded in the market, transaction costs and market efficiency

Expectations of exchange rate depreciation were the main components of spreads in the pre-euro era. They have disappeared in the first decade of the second millenium and they are currently dominated by Credit risk concerns

Spread of 10-years government bond yields vs Bund

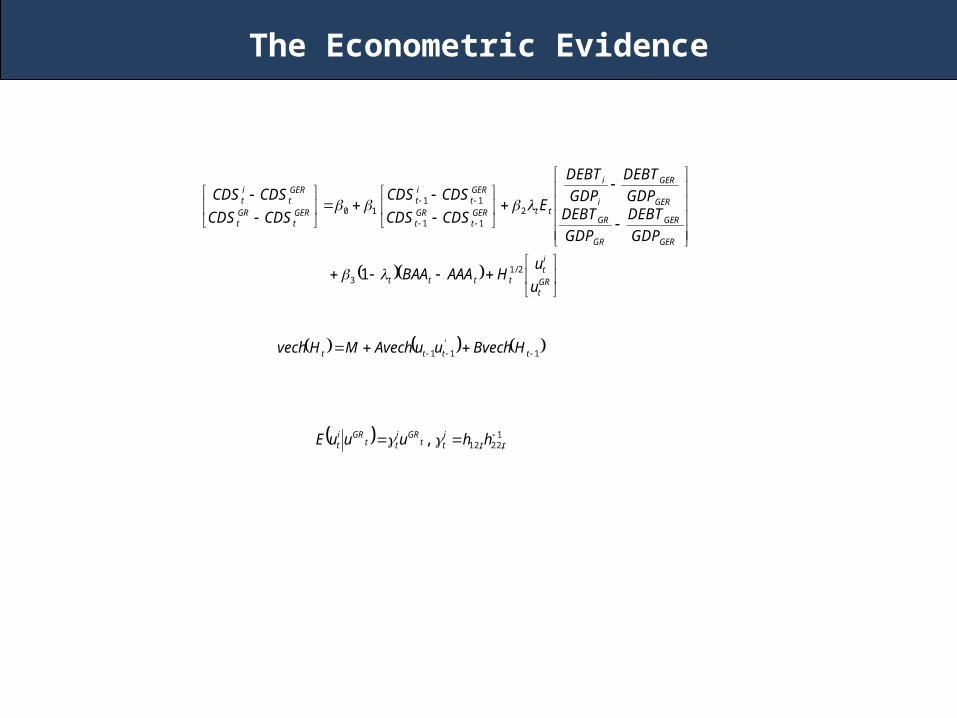

It is possible to identify the credit risk premium form the liquidity premium by using the Credit Default Swaps (CDS) as a proxy of the credit risk premium

The difference between a CDS on a MS bond and the CDS on the German Bund (the same maturity) is a measure of the credit risk premium of the State relative to Germany

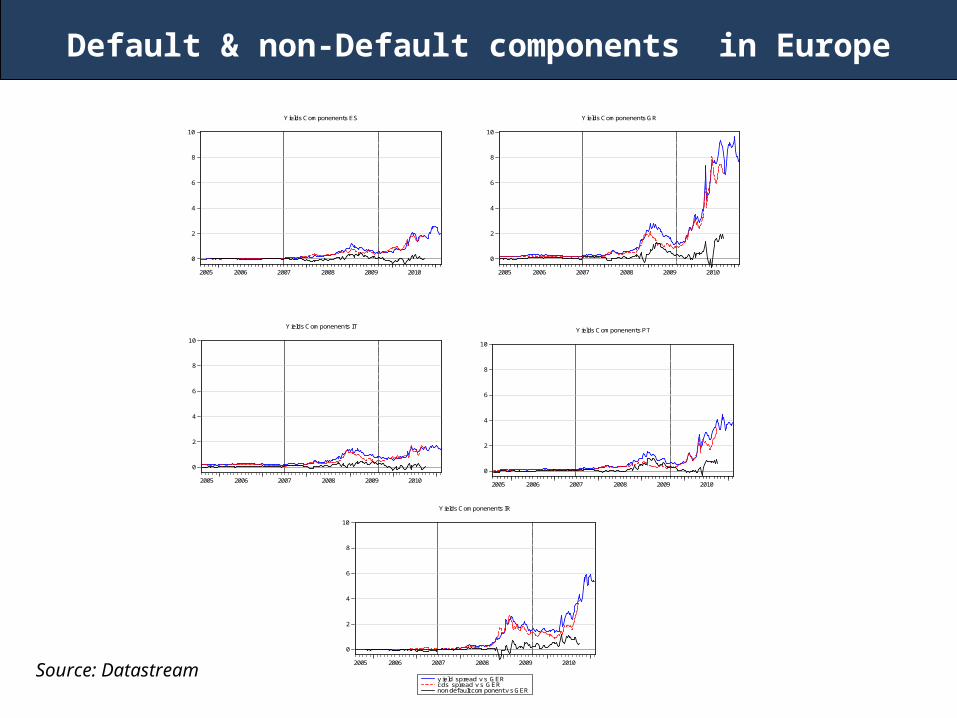

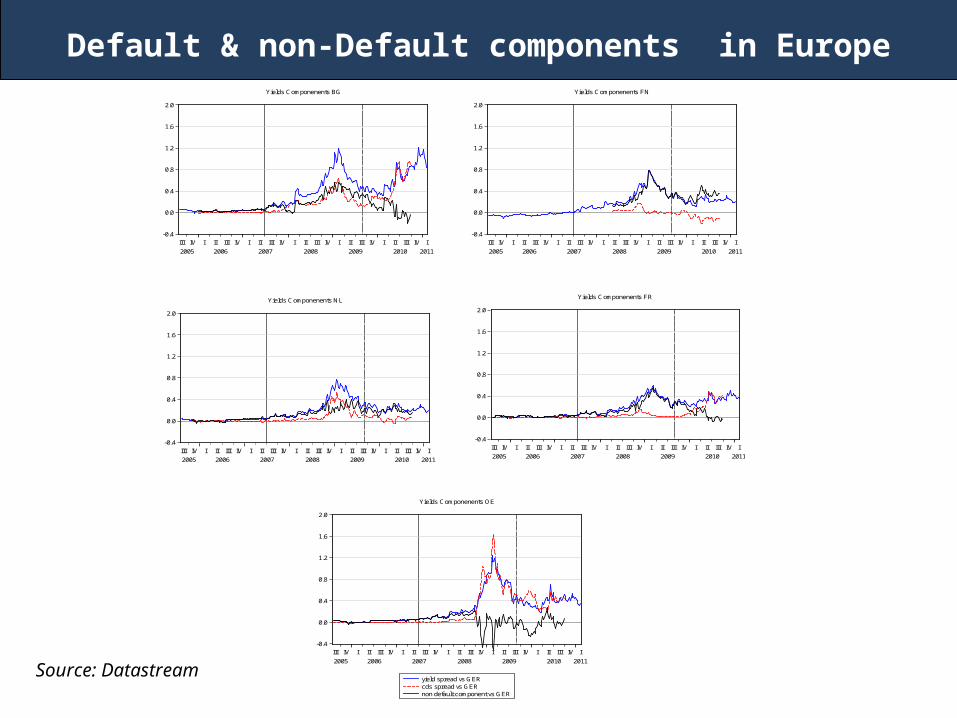

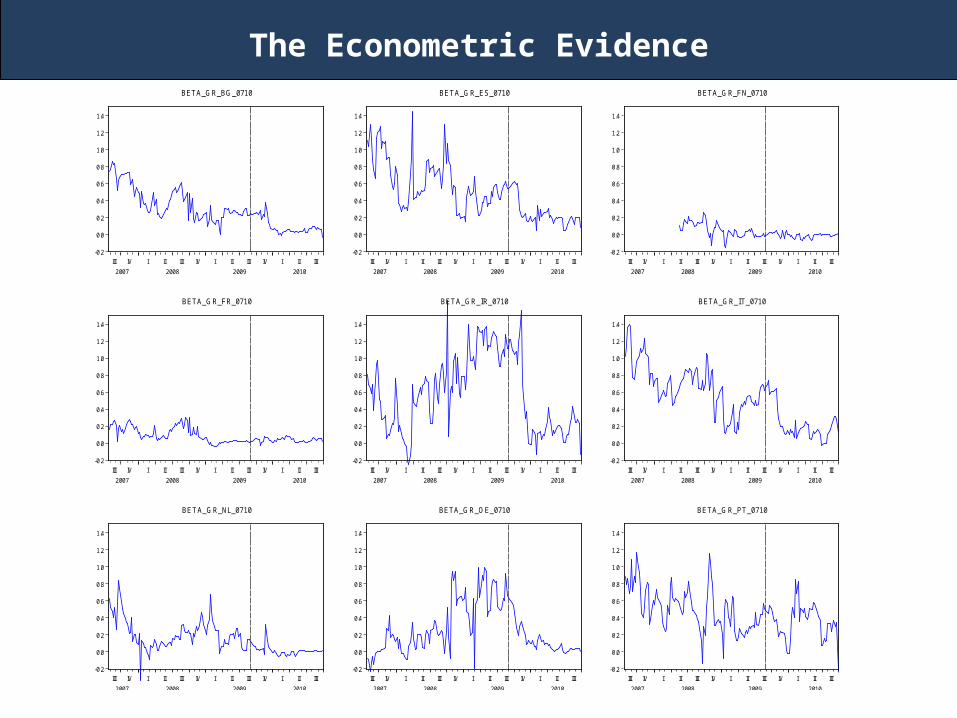

The Evidence from the data tells us that There is a clear tendency of all spreads on Bunds in the euro-area to co-move but, importantly, the nature of the comovement is not constant over time The non-default component of the interest-rate spread is very small for all Member States with only few exceptions: Finland, France and, perhaps, the Netherlands. in a global crisis the liquidity premium rises to determine a positive comovement between the Finnish spread and all other euro-area spreads.

For all countries non-default components are much more likely to reflect liquidity risk rather than expectations of depreciation of the exchange rates.

Default & non-Default components in Europe

Source: Datastream

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010

Yields Componenents ES

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010

Yields Componenents GR

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010

y ield spread v s GERcds spread v s GERnon default component v s GER

Yields Componenents IR

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010

Yields Componenents IT

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010

Yields Componenents PT

Default & non-Default components in Europe

Source: Datastream

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

III IV I II III IV I II III IV I II III IV I II III IV I II III IV I

2005 2006 2007 2008 2009 2010 2011

Yields Componenents BG

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

III IV I II III IV I II III IV I II III IV I II III IV I II III IV I

2005 2006 2007 2008 2009 2010 2011

Yields Componenents FN

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

III IV I II III IV I II III IV I II III IV I II III IV I II III IV I

2005 2006 2007 2008 2009 2010 2011

Yields Componenents FR

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

III IV I II III IV I II III IV I II III IV I II III IV I II III IV I

2005 2006 2007 2008 2009 2010 2011

Yields Componenents NL

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

III IV I II III IV I II III IV I II III IV I II III IV I II III IV I

2005 2006 2007 2008 2009 2010 2011

yield spread vs GERcds spread vs GERnon default component vs GER

Yields Componenents OE

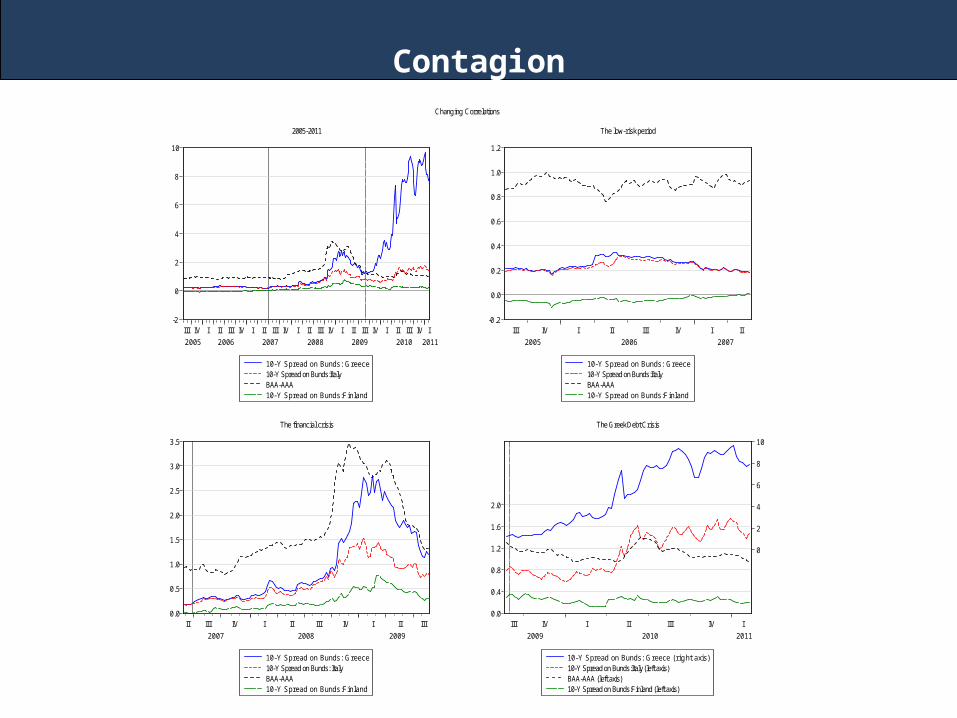

Contagion

-2

0

2

4

6

8

10

III IV I II III IV I II III IV I II III IV I II III IV I II III IV I

2005 2006 2007 2008 2009 2010 2011

10-Y Spread on Bunds: Greece10-Y Spread on Bunds:ItalyBAA-AAA10-Y Spread on Bunds:Finland

2005-2011

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

III IV I II III IV I II

2005 2006 2007

10-Y Spread on Bunds: Greece10-Y Spread on Bunds:ItalyBAA-AAA10-Y Spread on Bunds:Finland

The low-risk period

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

II III IV I II III IV I II III

2007 2008 2009

10-Y Spread on Bunds: Greece10-Y Spread on Bunds: ItalyBAA-AAA10-Y Spread on Bunds:Finland

The financial crisis

0.0

0.4

0.8

1.2

1.6

2.0

0

2

4

6

8

10

III IV I II III IV I

2009 2010 2011

10-Y Spread on Bunds: Greece ( r ight axis)10-Y Spread on Bunds:Italy (left axis)BAA-AAA (left axis)10-Y Spread on Bunds:Finland (left axis)

The Greek Debt Crisis

Changing Correlations

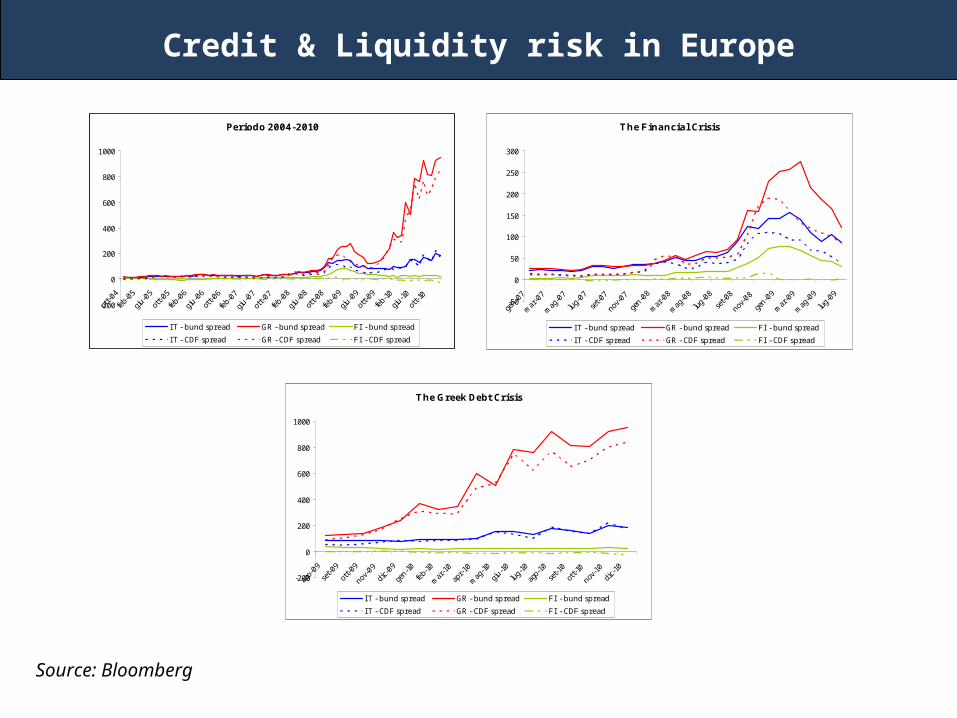

Credit & Liquidity risk in Europe

Periodo 2004-2010

-200

0

200

400

600

800

1000

ott-0

4

feb-

05

giu-0

5

ott-0

5

feb-

06

giu-0

6

ott-0

6

feb-

07

giu-0

7

ott-0

7

feb-

08

giu-0

8

ott-0

8

feb-

09

giu-0

9

ott-0

9

feb-

10

giu-10

ott-1

0

IT - bund spread GR - bund spread FI - bund spread

IT - CDF spread GR - CDF spread FI - CDF spread

Source: Bloomberg

The Financial Crisis

-50

0

50

100

150

200

250

300

gen-

07

mar

-07

mag

-07

lug-

07

set-0

7

nov-07

gen-

08

mar

-08

mag

-08

lug-

08

set-0

8

nov-08

gen-

09

mar

-09

mag

-09

lug-

09

IT - bund spread GR - bund spread FI - bund spread

IT - CDF spread GR - CDF spread FI - CDF spread

The Greek Debt Crisis

-200

0

200

400

600

800

1000

ago-

09

set-0

9

ott-0

9

nov-09

dic-09

gen-

10

feb-

10

mar

-10

apr-1

0

mag

-10

giu-10

lug-

10

ago-

10

set-1

0

ott-1

0

nov-10

dic-10

IT - bund spread GR - bund spread FI - bund spread

IT - CDF spread GR - CDF spread FI - CDF spread

The Econometric Evidence

GRt

it

tttt

GER

GER

GR

GR

GER

GER

i

i

ttGERt

GRt

GERt

it

GERt

GRt

GERt

it

u

uHAAABAA

GDP

DEBT

GDP

DEBTGDP

DEBT

GDP

DEBT

ECDSCDS

CDSCDS

CDSCDS

CDSCDS

2/13

2

11

1110

1

1'

11 tttt HBvechuuAvechMHvech

1,22,12, tt

itt

GRitt

GRit hhuuuE

The Econometric Evidence

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

III IV I II III IV I II III IV I II III

2007 2008 2009 2010

BETA_GR_BG_0710

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

III IV I II III IV I II III IV I II III

2007 2008 2009 2010

BETA_GR_ES_0710

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

III IV I II III IV I II III IV I II III

2007 2008 2009 2010

BETA_GR_FN_0710

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

III IV I II III IV I II III IV I II III

2007 2008 2009 2010

BETA_GR_FR_0710

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

III IV I II III IV I II III IV I II III

2007 2008 2009 2010

BETA_GR_IR_0710

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

III IV I II III IV I II III IV I II III

2007 2008 2009 2010

BETA_GR_IT_0710

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

III IV I II III IV I II III IV I II III

2007 2008 2009 2010

BETA_GR_NL_0710

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

III IV I II III IV I II III IV I II III

2007 2008 2009 2010

BETA_GR_OE_0710

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

III IV I II III IV I II III IV I II III

2007 2008 2009 2010

BETA_GR_PT_0710

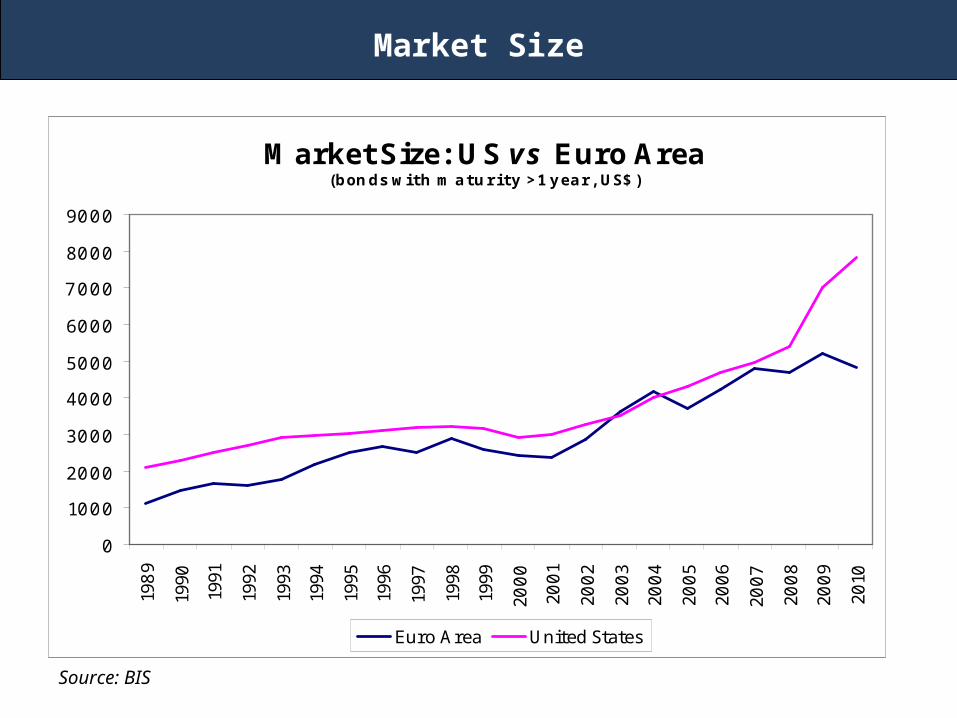

Market Size

Market Size: US vs Euro Area (bonds with maturity >1 year, US$)

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Euro Area United States

Source: BIS

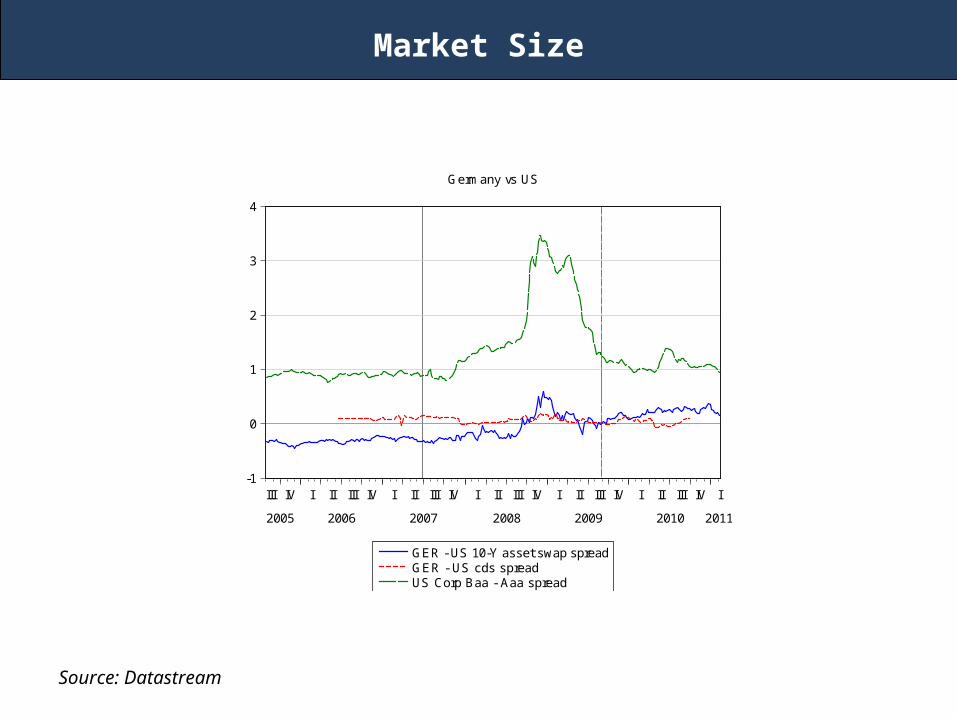

Market Size

Source: Datastream

-1

0

1

2

3

4

III IV I II III IV I II III IV I II III IV I II III IV I II III IV I

2005 2006 2007 2008 2009 2010 2011

GER - US 10-Y asset swap spreadGER - US cds spreadUS Corp Baa - Aaa spread

Germany vs US

EIB Bonds

Source: Datastream

-1

0

1

2

3

4

5

6

III IV I II III IV I II III IV I II III IV I II III IV I II III IV I

2005 2006 2007 2008 2009 2010 2011

10-Y Spread on Bunds: EIB10-Y EIB10-Y Germany10-Y Finland10-Y Spread on Bunds:Finland

EIB

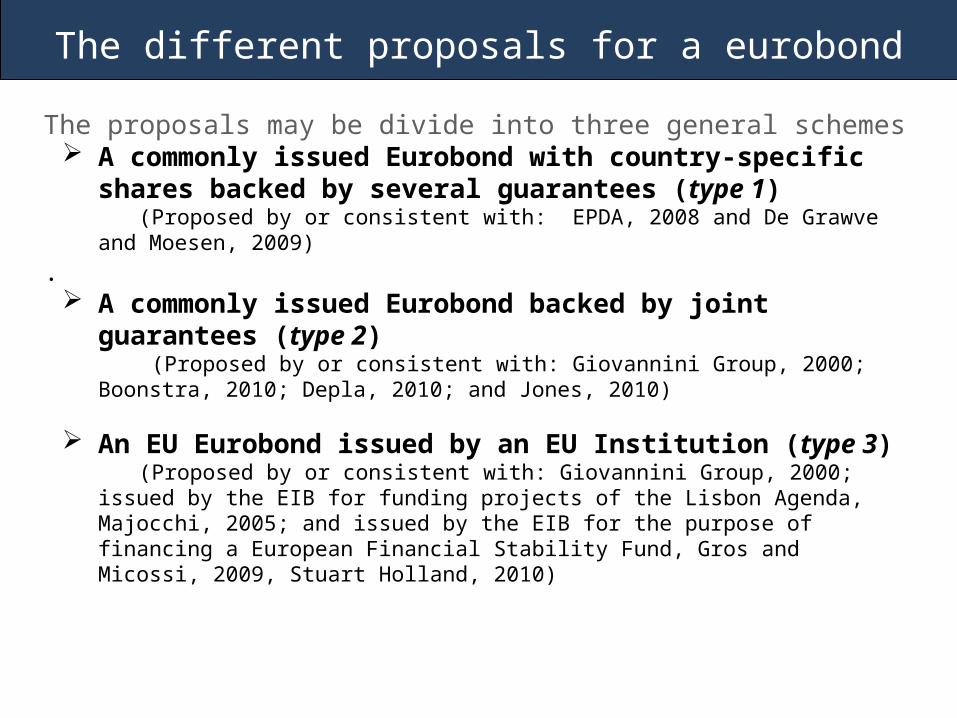

The different proposals for a eurobond

The proposals may be divide into three general schemes A commonly issued Eurobond with country-specific

shares backed by several guarantees (type 1) (Proposed by or consistent with: EPDA, 2008 and De Grawve and

Moesen, 2009). A commonly issued Eurobond backed by joint

guarantees (type 2) (Proposed by or consistent with: Giovannini Group, 2000; Boonstra,

2010; Depla, 2010; and Jones, 2010)

An EU Eurobond issued by an EU Institution (type 3) (Proposed by or consistent with: Giovannini Group, 2000; issued by the

EIB for funding projects of the Lisbon Agenda, Majocchi, 2005; and issued by the EIB for the purpose of financing a European Financial Stability Fund, Gros and Micossi, 2009, Stuart Holland, 2010)

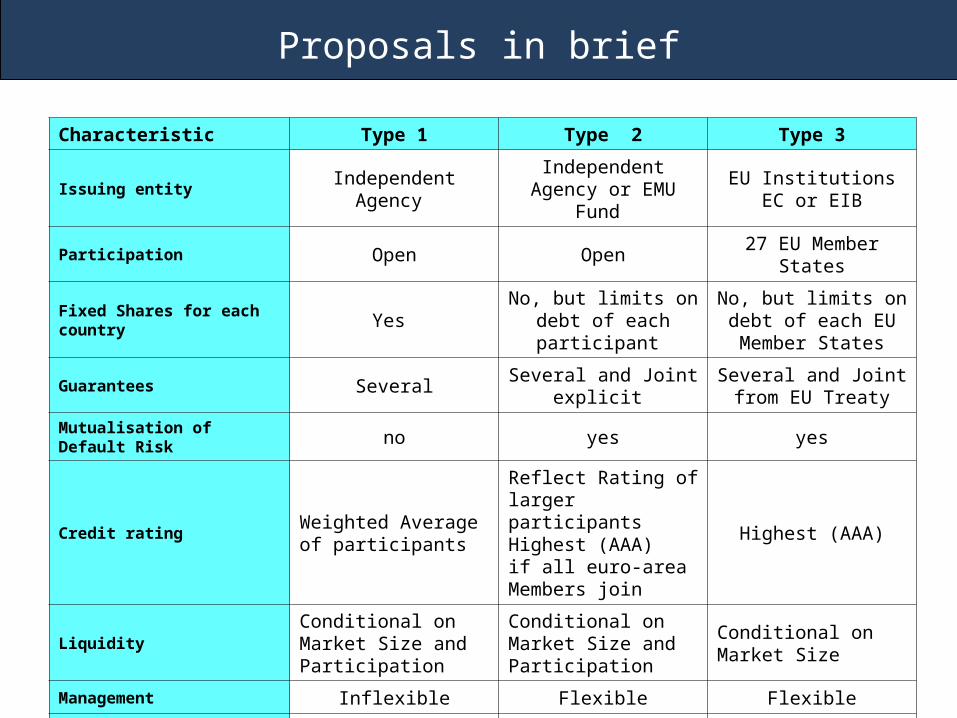

Proposals in brief

Characteristic Type 1 Type 2 Type 3

Issuing entity Independent Agency Independent Agency or

EMU Fund EU Institutions EC or

EIB

Participation Open Open 27 EU Member States

Fixed Shares for each country Yes No, but limits on debt of

each participant No, but limits on debt of each EU Member States

Guarantees SeveralSeveral and Joint

explicit Several and Joint from

EU Treaty

Mutualisation of Default Risk no yes yes

Credit rating Weighted Average of participants

Reflect Rating oflarger participantsHighest (AAA)if all euro-areaMembers join

Highest (AAA)

LiquidityConditional onMarket Size andParticipation

Conditional onMarket Size andParticipation

Conditional onMarket Size

Management Inflexible Flexible Flexible

Legal obstacles NoneChange in TFEUArt.125 No-Bailout

Change in TFEU

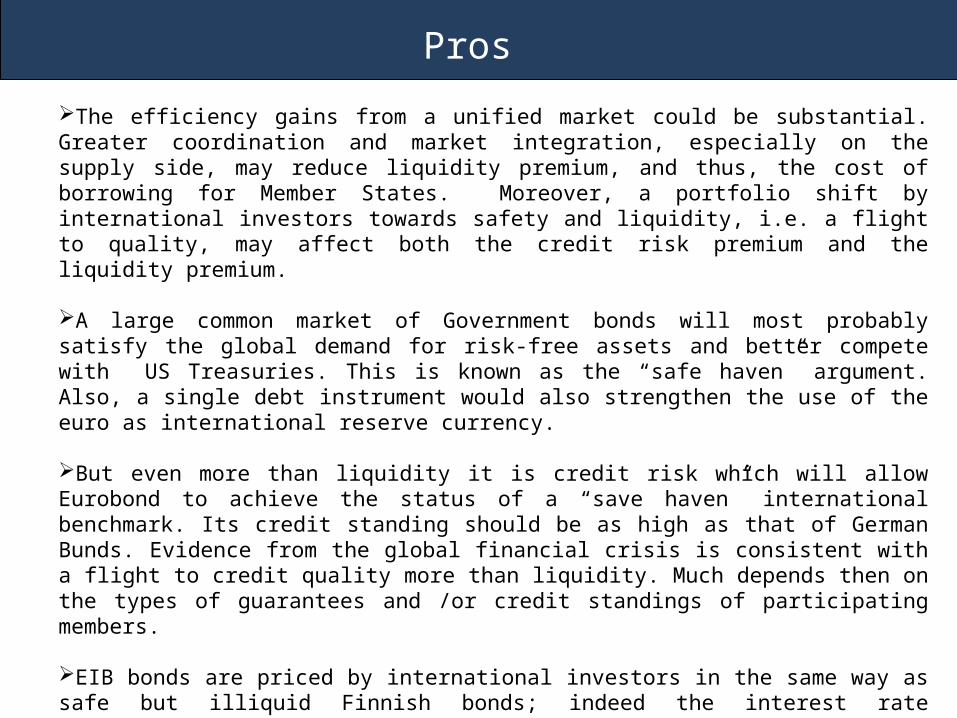

Pros

The efficiency gains from a unified market could be substantial. Greater coordination and market integration, especially on the supply side, may reduce liquidity premium, and thus, the cost of borrowing for Member States. Moreover, a portfolio shift by international investors towards safety and liquidity, i.e. a flight to quality, may affect both the credit risk premium and the liquidity premium.

A large common market of Government bonds will most probably satisfy the global demand for risk-free assets and better compete with US Treasuries. This is known as the “safe haven” argument. Also, a single debt instrument would also strengthen the use of the euro as international reserve currency.

But even more than liquidity it is credit risk which will allow Eurobond to achieve the status of a “save haven” international benchmark. Its credit standing should be as high as that of German Bunds. Evidence from the global financial crisis is consistent with a flight to credit quality more than liquidity. Much depends then on the types of guarantees and /or credit standings of participating members.

EIB bonds are priced by international investors in the same way as safe but illiquid Finnish bonds; indeed the interest rate differential between the two bonds is practically zero. This suggests that a Eurobond issued by an EU institution (and probably all euro-area MS) would be perceived as the highest credit quality and could reach the “safe haven” status if its market size approached that of US Treasuries.

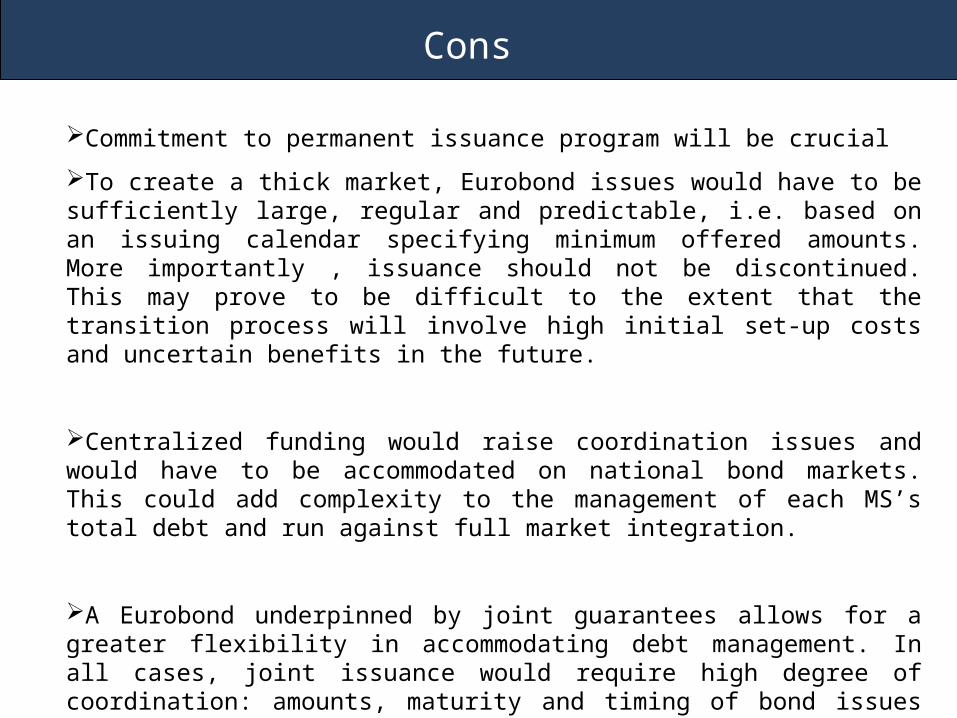

Cons

Commitment to permanent issuance program will be crucial

To create a thick market, Eurobond issues would have to be sufficiently large, regular and predictable, i.e. based on an issuing calendar specifying minimum offered amounts. More importantly , issuance should not be discontinued. This may prove to be difficult to the extent that the transition process will involve high initial set-up costs and uncertain benefits in the future.

Centralized funding would raise coordination issues and would have to be accommodated on national bond markets. This could add complexity to the management of each MS’s total debt and run against full market integration.

A Eurobond underpinned by joint guarantees allows for a greater flexibility in accommodating debt management. In all cases, joint issuance would require high degree of coordination: amounts, maturity and timing of bond issues would have to be decided by the issuing entity in close operation with MS.

Cons

The most forceful argument against a common European bond is that it undermines fiscal discipline by removing incentives for sound budgetary policies. At worst, it could create a moral hazard problem in that a Member State may be tempted to free ride on other Members’ legal obligations to assume its debt in case of default. In particular, a common Eurobond prevents financial markets from exerting their disciplinary effects through higher interest rates and undermines the no bailout clause that prohibits a Member State to be liable for or assume the debt obligations of another government. Then, with lower costs ofdefault and deficit financing, Member States would be encouraged to run lax fiscal policies and take up more debt. This would weaken the credibility of the euro-zone as an area of stability and fiscal soundness.

In the end the problem of moral hazard created by the mutualisation of risks would always emerge, as it is inherent in any insurance contract. The important question to ask is whether a common Eurobond can reduce exposure to crisis transmission and whether this benefit can compensate for the risk of moral hazard.